Intermediate Financial Accounting Study Notes

23

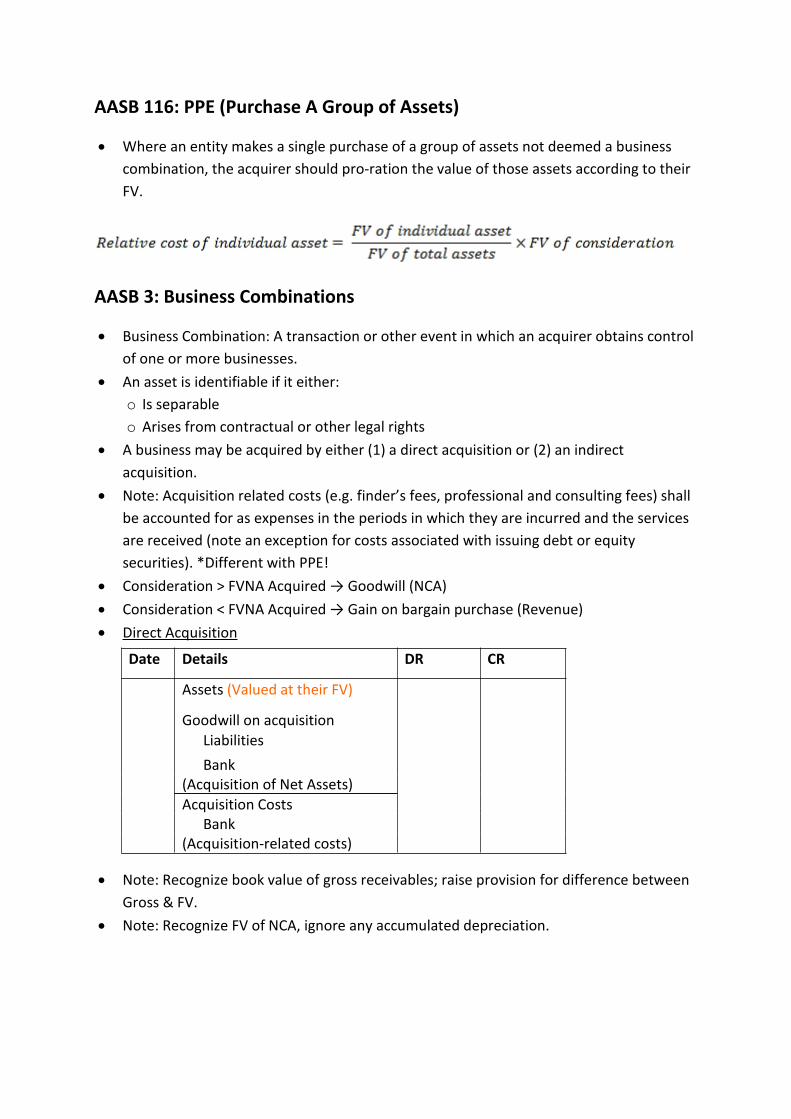

AASB 116: PPE (Purchase A Group of Assets) Where an entity makes a single purchase of a group of assets not deemed a business combination, the acquirer should pro-ration the value of those assets according to their FV. AASB 3: Business Combinations Business Combination: A transaction or other event in which an acquirer obtains control of one or more businesses. An asset is identifiable if it either: o Is separable o Arises from contractual or other legal rights A business may be acquired by either (1) a direct acquisition or (2) an indirect acquisition. Note: Acquisition related costs (e.g. finder’s fees, professional and consulting fees) shall be accounted for as expenses in the periods in which they are incurred and the services are received (note an exception for costs associated with issuing debt or equity securities). *Different with PPE! Consideration > FVNA Acquired → Goodwill (NCA) Consideration < FVNA Acquired → Gain on bargain purchase (Revenue) Direct Acquisition Note: Recognize book value of gross receivables; raise provision for difference between Gross & FV. Note: Recognize FV of NCA, ignore any accumulated depreciation. Date Details DR CR Assets (Valued at their FV) Goodwill on acquisition Liabilities Bank (Acquisition of Net Assets) Acquisition Costs Bank (Acquisition-related costs)

-

Upload

sayting-toon -

Category

Documents

-

view

238 -

download

4

Transcript of Intermediate Financial Accounting Study Notes

AASB 116: PPE (Purchase A Group of Assets)

Where an entity makes a single purchase of a group of assets not deemed a businesscombination, the acquirer should pro-ration the value of those assets according to theirFV.

AASB 3: Business Combinations

Business Combination: A transaction or other event in which an acquirer obtains controlof one or more businesses.

An asset is identifiable if it either:o Is separableo Arises from contractual or other legal rights

A business may be acquired by either (1) a direct acquisition or (2) an indirectacquisition.

Note: Acquisition related costs (e.g. finder’s fees, professional and consulting fees) shallbe accounted for as expenses in the periods in which they are incurred and the servicesare received (note an exception for costs associated with issuing debt or equitysecurities). *Different with PPE!

Consideration > FVNA Acquired → Goodwill (NCA) Consideration < FVNA Acquired → Gain on bargain purchase (Revenue) Direct Acquisition

Note: Recognize book value of gross receivables; raise provision for difference betweenGross & FV.

Note: Recognize FV of NCA, ignore any accumulated depreciation.

Date Details DR CR

Assets (Valued at their FV)

Goodwill on acquisitionLiabilitiesBank

(Acquisition of Net Assets)Acquisition Costs

Bank(Acquisition-related costs)

↑by 240

↑ by 40

↑ by 200

Indirect Acquisition

AASB 116: PPE (Measurement after Recognition)

Cost Model

Depreciation applied based on cost Subject to impairment test under AASB 136

Revaluation Model Revaluation > CA → Incremental Revaluation < CA → Decremental When an item of PPE is revalued, any accumulated depreciation at the date of

revaluation is treated in one of the following ways: (1) The gross method; (2) The netmethod.

Subject to impairment test under AASB 136

Accounting for the Increment (FV>CA) The Net Method

Gain on revaluation (Other comprehensive income)

The Gross Method

Date Details DR CR

Investment in Y LtdBank

(Acquisition of shares in Y Ltd)

Date Details DR CR

Accumulated DepreciationAsset (e.g. Equipment)

(Depreciation write back)Asset (e.g. Equipment)

Revaluation surplus(Incremental revaluation)

OLD NEW

Gross Amount 1200 1440

Acc Depreciation 200 240

Carrying Amount 1000 1200[1] Ratio of 1.2 to 1

[2] 1200*1.2

[3] 1440-1200

↓by 240

↓ by 40

↓ by 200

Gain on revaluation (Other comprehensive income)

Accounting for the Decrement (FV<CA) In line with PRUDENCE, recognise losses as soon as anticipated, recognise gains when

realized. The Net Method

**or Loss on Evaluation (P&L)

The Gross Method

Revaluation expense (P&L)

Date Details DR CR

Asset (e.g. Equipment) 240Accumulated Depreciation 40Revaluation surplus 200

(Incremental revaluation)

Date Details DR CR

Accumulated DepreciationAsset (e.g. Equipment)

(Depreciation write back)Revaluation expense **

Asset (e.g. Equipment)(Decremental revaluation)

OLD NEW

Gross Amount 1200 960

Acc Depreciation 200 160

Carrying Amount 1000 800

Date Details DR CR

Revaluation expense 200Accumulated Depreciation 40

Asset (e.g. Equipment) 240(Decremental revaluation)

[1] Ratio of 0.8 to 1

[2] 1200*0.8

[3] 960-800

↑by 640

↑ by 240

↑ by 400

Accounting for the Increment (FV>CA) After a Prior Revaluation Downwards If an asset’s CA is increased as a result of a revaluation, the increase shall be credited

directly to equity under the heading of revaluation surplus. However, the increase shallbe recognized in P&L to the extent that it reverses a revaluation decrease of the sameasset previously recognized in P&L.

E.g.Equipment 1600

Acc Depreciation 600

Carrying Amount 1000

FV=1400Prior revaluation downwards=100

The Net Method

** or Gain on Revaluation (P&L)

The Gross Method

Date Details DR CR

Accumulated Depreciation 600

Equipment 600(Depreciation write back)Equipment 400

Revaluation revenue** 100Revaluation surplus 300

(Incremental revaluation)

OLD NEW

Gross Amount 1600 2240

Acc Depreciation 600 840

Carrying Amount 1000 1400

Date Details DR CR

Asset (e.g. Equipment) 640Accumulated Depreciation 240Revaluation revenue 100Revaluation surplus 300

(Incremental revaluation)

[1] Ratio of 1.4 to 1

[2] 1600*1.4

[3] 2240-1400

↓by 640

↓ by 240

↓ by 400

Accounting for the Decrement (FV<CA) After a Prior Revaluation Upwards If an asset’s CA is decreased as a result of a revaluation, the decrease shall be

recognized in P&L. However, the decrease shall be recognized in other comprehensiveincome to the extent that any credit balance existing in the revaluation surplus inrespect of that asset. The decrease recognized in the other comprehensive incomereduces the amount accumulated in equity under the heading of revaluation surplus.

E.g.Equipment 1600

Acc Depreciation 600

Carrying Amount 1000

FV=600Prior revaluation upwards=100

The Net Method

The Gross Method

Date Details DR CRAccumulated Depreciation 600

Equipment 600(Depreciation write back)Revaluation surplus 100Revaluation expense 300

Equipment 400(Decremental revaluation)

OLD NEW

Gross Amount 1600 960

Acc Depreciation 600 360

Carrying Amount 1000 600

Date Details DR CR

Revaluation surplus 100Revaluation expense 300Accumulated Depreciation 240

Equipment 640(Decremental revaluation)

[1] Ratio of 0.6 to 1

[2] 1600*0.6

[3] 960-600

AASB 116: PPE (Derecognition of a Revalued Asset) Example 1: Land with CA of $400 is sold for $650

CA=$400; Proceeds=$650 → Profit on sale=$250 Example 2: Land was purchased for $400, revalued by $100

CA=$500; Proceeds=$650 → Profit on sale=$150 But $100 previously recognized as an unrealized gain (which has now been realized),

so GJ entry:DR Revaluation surplus 100

CR Retained earnings 100

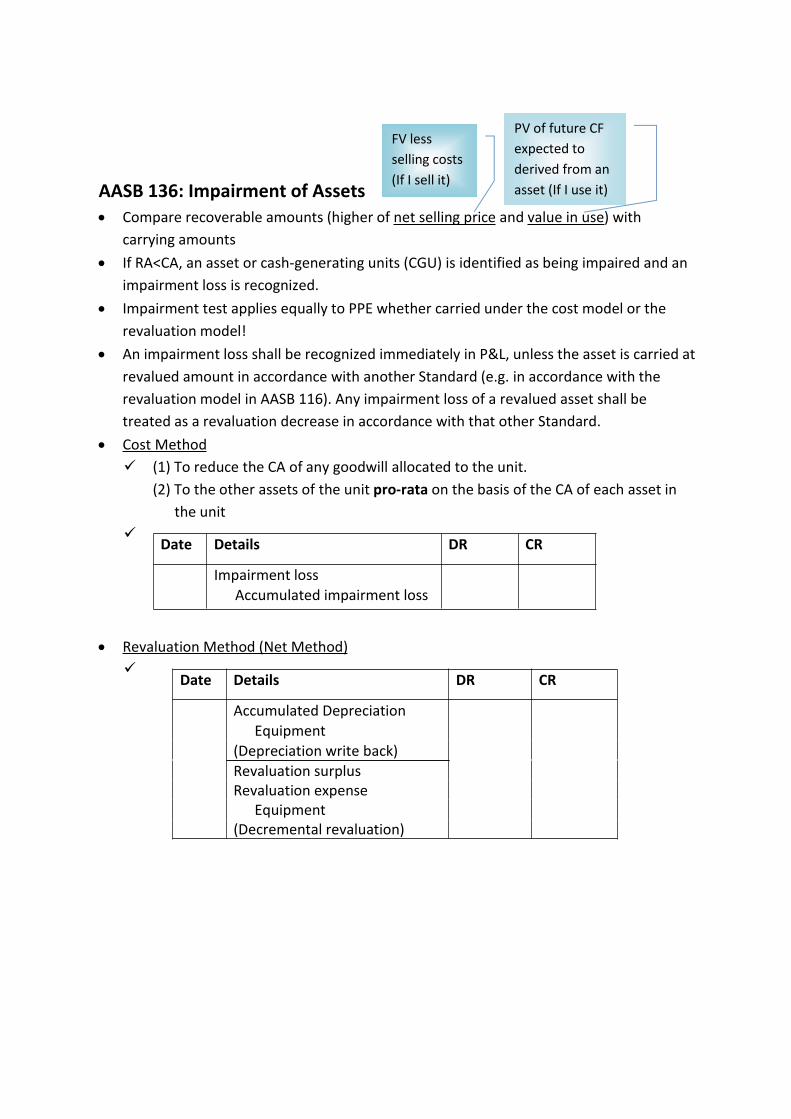

AASB 136: Impairment of Assets Compare recoverable amounts (higher of net selling price and value in use) with

carrying amounts If RA<CA, an asset or cash-generating units (CGU) is identified as being impaired and an

impairment loss is recognized. Impairment test applies equally to PPE whether carried under the cost model or the

revaluation model! An impairment loss shall be recognized immediately in P&L, unless the asset is carried at

revalued amount in accordance with another Standard (e.g. in accordance with therevaluation model in AASB 116). Any impairment loss of a revalued asset shall betreated as a revaluation decrease in accordance with that other Standard.

Cost Method (1) To reduce the CA of any goodwill allocated to the unit.

(2) To the other assets of the unit pro-rata on the basis of the CA of each asset inthe unit

Revaluation Method (Net Method)

Date Details DR CR

Impairment lossAccumulated impairment loss

Date Details DR CR

Accumulated DepreciationEquipment

(Depreciation write back)Revaluation surplusRevaluation expense

Equipment(Decremental revaluation)

FV lessselling costs(If I sell it)

PV of future CFexpected toderived from anasset (If I use it)

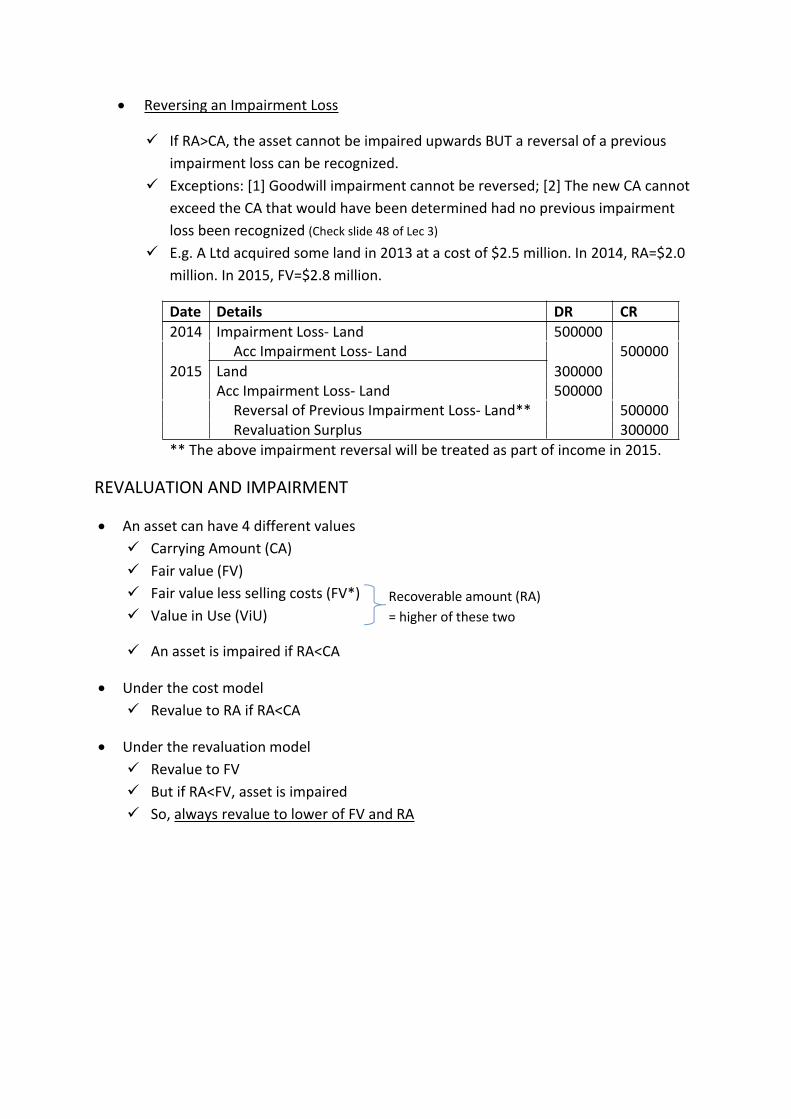

Reversing an Impairment Loss

If RA>CA, the asset cannot be impaired upwards BUT a reversal of a previousimpairment loss can be recognized.

Exceptions: [1] Goodwill impairment cannot be reversed; [2] The new CA cannotexceed the CA that would have been determined had no previous impairmentloss been recognized (Check slide 48 of Lec 3)

E.g. A Ltd acquired some land in 2013 at a cost of $2.5 million. In 2014, RA=$2.0million. In 2015, FV=$2.8 million.

Date Details DR CR2014 Impairment Loss- Land 500000

Acc Impairment Loss- Land 5000002015 Land 300000

Acc Impairment Loss- Land 500000Reversal of Previous Impairment Loss- Land** 500000Revaluation Surplus 300000

** The above impairment reversal will be treated as part of income in 2015.

REVALUATION AND IMPAIRMENT

An asset can have 4 different values Carrying Amount (CA) Fair value (FV) Fair value less selling costs (FV*) Value in Use (ViU)

An asset is impaired if RA<CA

Under the cost model Revalue to RA if RA<CA

Under the revaluation model Revalue to FV But if RA<FV, asset is impaired So, always revalue to lower of FV and RA

Recoverable amount (RA)= higher of these two

AASB 112: Income Taxes

Tax liability= Taxable income * corporate tax rate (30%)

PERMANENT DIFFERENCE Income that is never assessable (e.g. some capital gains, royalty) Expenses that are never deductible (e.g. entertainment, goodwill impairment) Tax incentives

TEMPORARY DIFFERENCE Income Tax Assessment Act →substantiation rules (i.e. items are assessable/

deductible in the period when invoice is generated/received or when the associatedCF occurs)

GAAP → accrual accounting (recognize revenue and expenses when earned/ incurred) ∴Timing difference between recognition → reconcile/ offset over time

Deductible temporary differences Taxable temporary differencesResults in amounts that are deductible fromaccounting profit in determining taxableprofit of future periods when the CA of theasset is recovered or the CA of the liability issettled.

Results in taxable amounts (added toaccounting profit) in determining taxableprofit of future periods when the CA of theasset is recovered or the CA of the liability issettled.

E.g. Accrued expenses/ Provisions; Unearnedrevenue; LCR write down

E.g. Prepaid expenses; Accrued revenue

Deductible TD give rise to Deferred TaxAssets (DTAs) i.e. DTA = Deductible TD x 30%

Taxable TD give rise to Deferred TaxLiabilities (DTLs) i.e. DTL = Taxable TD x 30%

Deductible TD arises when: CA of an asset in BS < Tax base CA of a liability > Tax base

Taxable TD arises when: CA of an asset in BS > Tax base

CA > Tax base CA < Tax baseAssets DTL DTALiabilities DTA DTL (Not in IFA!!!)

Not the same asaccounting profit!!

REVALUATION OF NCA Asset revaluation represents an unrealized gain (or loss) that is not assessable (or

deductible) at the time of the revaluation. Revaluation ↑→ CA of asset> tax base → DTL Revaluation ↓→ CA of asset< tax base → DTA

Date Details DR CR

Asset 10Revaluation surplus 10

(Adj for upward revaluation)Revaluation surplus 3

DTL 3(Adj for DTL)

Accounting for Foreign Currency Transactions

AASB 121: The Effects of Changes in Foreign Exchange Rates

Problems arise when the spot rate is different to the invoice date spot rate!→ Exchange differences arising on settlement of monetary items (e.g. Receivables orpayables) shall be recognised in P&L (as gains or losses).

Credit Purchase of InventoryDate Details DR CR

InventoryForeign currency payable

(Credit purchase of inventory)Foreign Exchange Loss

Foreign currency payable(Adj for foreign exchange loss)

ORForeign currency payable

Foreign Exchange Gain(Adj for foreign exchange gain)Foreign currency payable

Bank(Settlement of account payable)

Credit Sale of Inventory

Credit Purchase of Qualifying Asset (AASB 121 Qualifying Assets): FC gains or losses relating to loans relating to loans or other payables associated with

qualifying assets are capitalized to the asset (same treatment as interest costs) Can only capitalize to the extent that the asset’s CA does not exceed its RA! (Or the

asset will be impaired after the capitalization of interest or exchange currencydifference)

Date Details DR CR

Foreign currency receivableSale

COGSInventory

(Credit sale of inventory)Foreign Exchange Loss

Foreign currency receivable(Adj for foreign exchange loss)

ORForeign currency receivable

Foreign Exchange Gain(Adj for foreign exchange gain)Bank

Foreign currency receivable(Settlement of account payable)

Date Details DR CR

NCAForeign currency payable

(Credit purchase of NCA)NCA

Foreign currency payable(Adj for foreign exchange loss)

ORForeign currency payable

NCA(Adj for foreign exchange gain)Foreign currency payable

Bank(Settlement of account payable)

HEDGED TRANSACTION[1] Hedging a Purchase To create certainty + anticipate depreciation of AUD A contract to hedge a purchase gives rise to: (i) a FIXED forward contract payable, and;

(ii) a VARIABLE forward contract receivable The payable from the underlying transaction will vary with spot rates (which will be

offset as...) the forward contract receivable and, therefore, the FV of the contract,varies with the forward rates

[2]

Date Details DR CR

InceptionDate

No entry – FV of contract=zero

TransactionDate

Hedging ReserveForward contract

(Change in FV of forward contract)Loss on Fwd K (Or Asset)

Hedging Reserve(Transfer of reserve to P&L)InventoryForeign currency payable

(Credit purchase of inventory)SettlementDate

Foreign Exchange LossForeign currency payable

(Adj for foreign exchange loss)

Forward ContractGain on Fwd K

(Change in FV of forward contract)Foreign currency payableForward ContractBank

(Settlement of account payable)

If Loss on Fwd K //FV of Fwd K ↓

Underlying Transaction

If Gain on Fwd K //FV of Fwd K ↑

Underlying Transaction

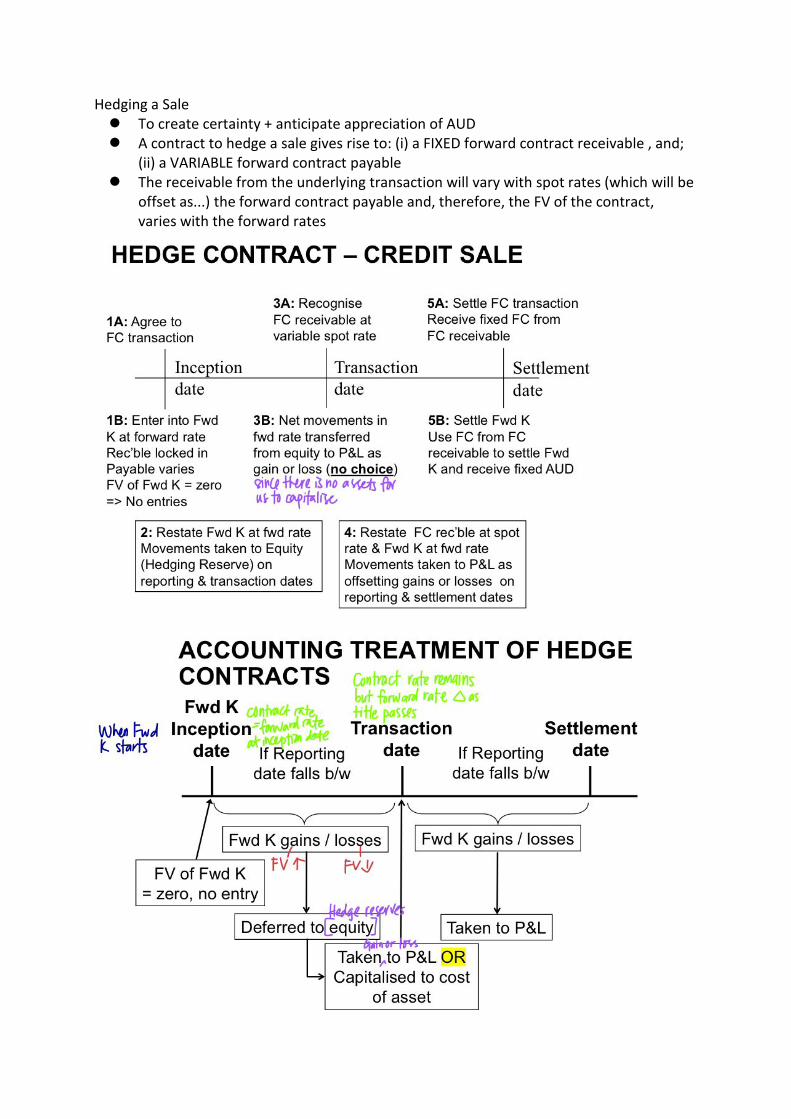

Hedging a Sale To create certainty + anticipate appreciation of AUD A contract to hedge a sale gives rise to: (i) a FIXED forward contract receivable , and;

(ii) a VARIABLE forward contract payable The receivable from the underlying transaction will vary with spot rates (which will be

offset as...) the forward contract payable and, therefore, the FV of the contract,varies with the forward rates

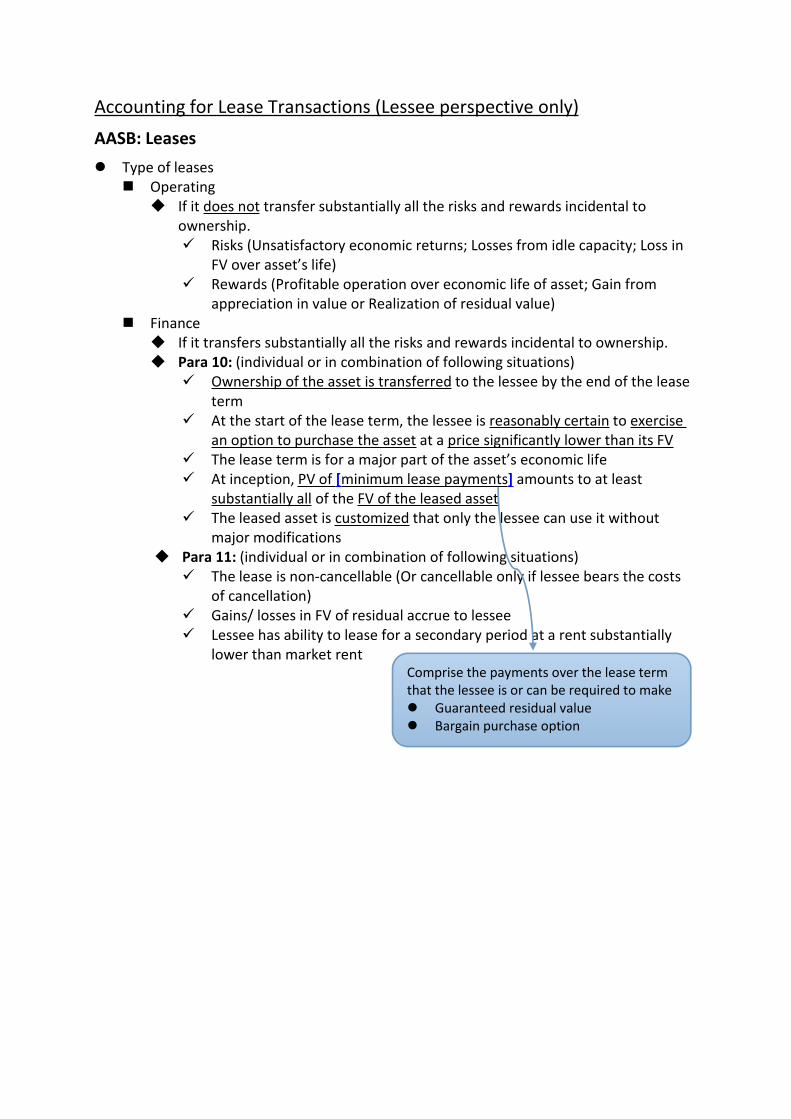

Accounting for Lease Transactions (Lessee perspective only)AASB: Leases Type of leases

Operating If it does not transfer substantially all the risks and rewards incidental to

ownership. Risks (Unsatisfactory economic returns; Losses from idle capacity; Loss in

FV over asset’s life) Rewards (Profitable operation over economic life of asset; Gain from

appreciation in value or Realization of residual value) Finance

If it transfers substantially all the risks and rewards incidental to ownership. Para 10: (individual or in combination of following situations)

Ownership of the asset is transferred to the lessee by the end of the leaseterm

At the start of the lease term, the lessee is reasonably certain to exercisean option to purchase the asset at a price significantly lower than its FV

The lease term is for a major part of the asset’s economic life At inception, PV of [minimum lease payments] amounts to at least

substantially all of the FV of the leased asset The leased asset is customized that only the lessee can use it without

major modifications Para 11: (individual or in combination of following situations)

The lease is non-cancellable (Or cancellable only if lessee bears the costsof cancellation)

Gains/ losses in FV of residual accrue to lessee Lessee has ability to lease for a secondary period at a rent substantially

lower than market rentComprise the payments over the lease termthat the lessee is or can be required to make Guaranteed residual value Bargain purchase option

Lessee Accounting for Operating Leases

OR

Lessee has possession and all benefits of ownership without recognition of anyasset or liability, hence “off balance sheet finance”!

Lessee Accounting for Finance LeasesInitial Recognition Record a lease asset and a lease liability at the lower of:

FV of the leased property, and PV of the minimum lease payments

Note: It would not be unusual for these to be equal! Initial direct costs (e.g. Legal costs) can be separately capitalized to the costs of the

asset BUT NOT TO THE LIABILITY (CR to bank or payables)

Subsequent Recognition Apportion the lease payments between the interest and principal [Slide 22]

If the lease payments include “executory costs: (e.g. Insurance, maintenance),then these are isolated and recorded separately as expenses.

Depreciation of the lease asset Depends on the reasonable certainty of acquisition at the end of lease term

Date Details DR CR

Lease expenseBank

Date Details DR CR

Prepaid leaseBank

Lease expensePrepaid lease

Intention to purchase No intention to purchaseDepreciation/Amortizationmethod

Consistent with policyused for other assets inthat class

Straight-line

Depreciationperiod

Useful life Shorter of lease term anduseful life

Residual value Estimated residual value(at end of useful life)

Guaranteed residual value(at end of lease term)

As each periodic payment is made

When lump sum payment is made

At each reporting date

Date Details DR CRLease asset

Lease liability(Commencement of finance lease)Lease liability

Bank(1st Lease payment)Lease interest expenseLease liability

Bank(2nd lease payment)Depreciation of lease asset

Acc Depreciation of lease asset(Adj for depreciation)

Journal entries at commencement

Journal entries at end of year 1

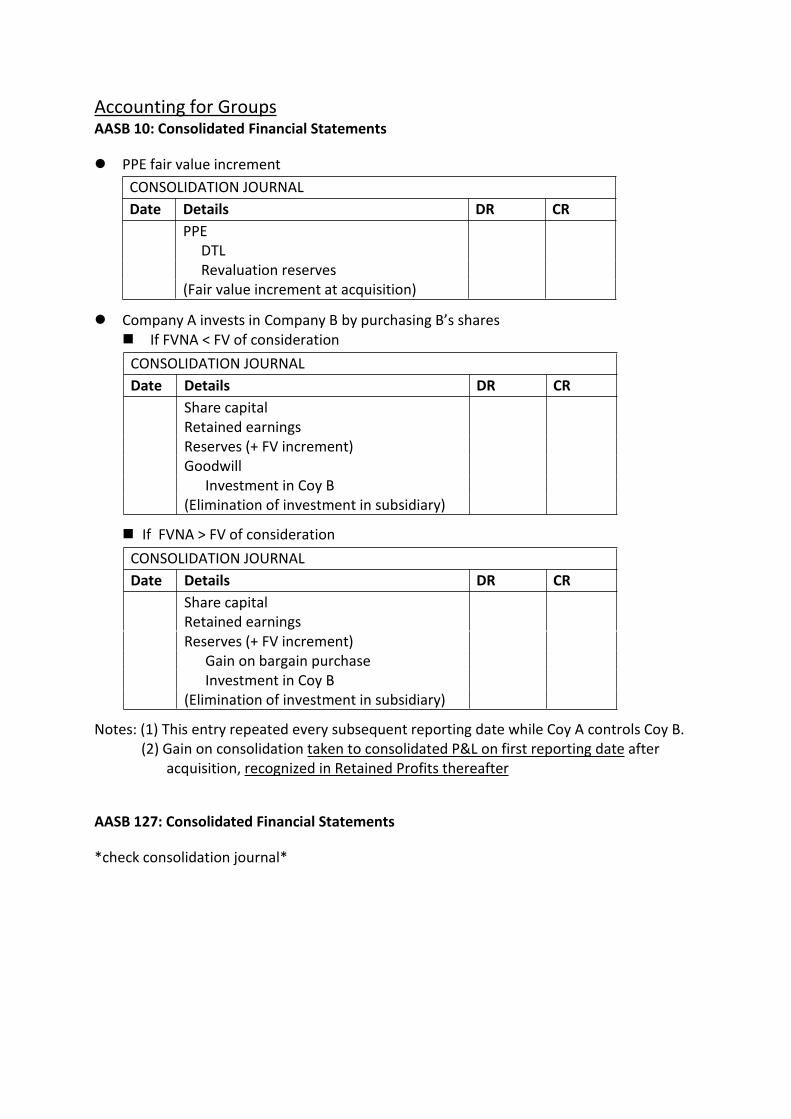

Accounting for GroupsAASB 10: Consolidated Financial Statements

PPE fair value increment

Company A invests in Company B by purchasing B’s shares If FVNA < FV of consideration

If FVNA > FV of consideration

Notes: (1) This entry repeated every subsequent reporting date while Coy A controls Coy B.(2) Gain on consolidation taken to consolidated P&L on first reporting date after

acquisition, recognized in Retained Profits thereafter

AASB 127: Consolidated Financial Statements

*check consolidation journal*

CONSOLIDATION JOURNALDate Details DR CR

PPEDTLRevaluation reserves

(Fair value increment at acquisition)

CONSOLIDATION JOURNALDate Details DR CR

Share capitalRetained earningsReserves (+ FV increment)Goodwill

Investment in Coy B(Elimination of investment in subsidiary)

CONSOLIDATION JOURNALDate Details DR CR

Share capitalRetained earningsReserves (+ FV increment)

Gain on bargain purchaseInvestment in Coy B

(Elimination of investment in subsidiary)

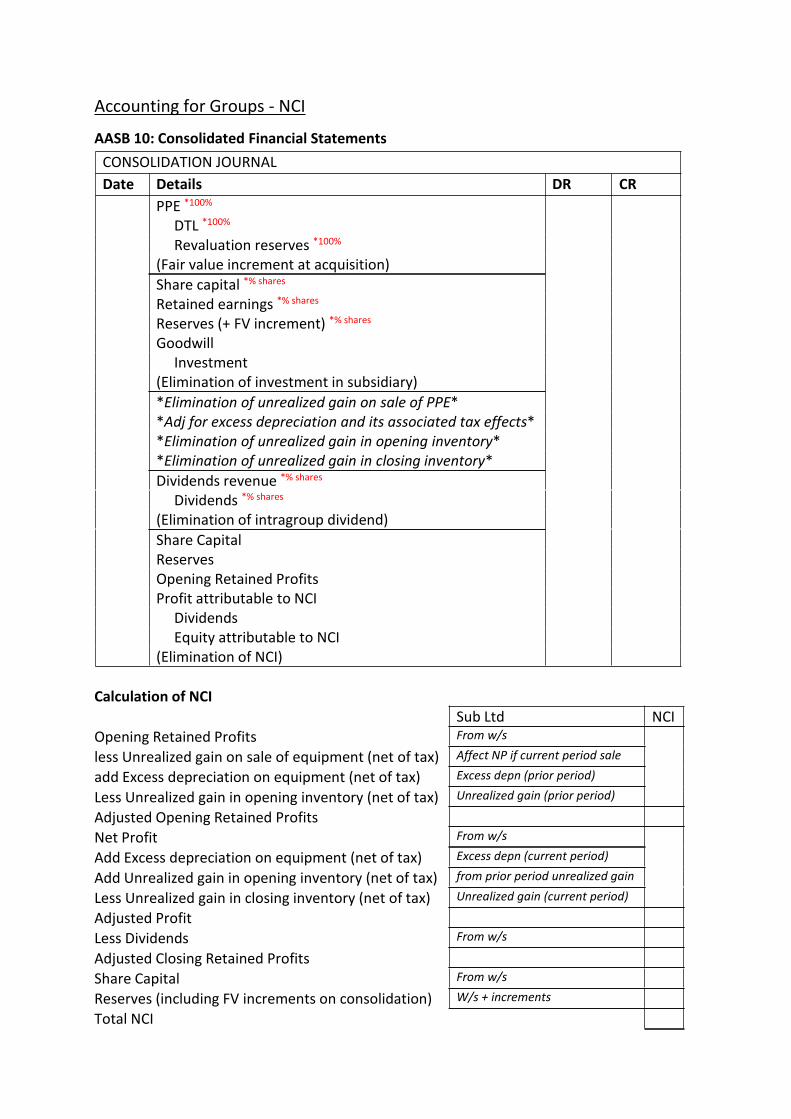

Accounting for Groups - NCI

AASB 10: Consolidated Financial Statements

Calculation of NCISub Ltd NCI

Opening Retained Profits From w/s

less Unrealized gain on sale of equipment (net of tax) Affect NP if current period sale

add Excess depreciation on equipment (net of tax) Excess depn (prior period)

Less Unrealized gain in opening inventory (net of tax) Unrealized gain (prior period)

Adjusted Opening Retained ProfitsNet Profit From w/s

Add Excess depreciation on equipment (net of tax) Excess depn (current period)

Add Unrealized gain in opening inventory (net of tax) from prior period unrealized gain

Less Unrealized gain in closing inventory (net of tax) Unrealized gain (current period)

Adjusted ProfitLess Dividends From w/s

Adjusted Closing Retained ProfitsShare Capital From w/s

Reserves (including FV increments on consolidation) W/s + increments

Total NCI

CONSOLIDATION JOURNALDate Details DR CR

PPE *100%

DTL *100%

Revaluation reserves *100%(Fair value increment at acquisition)Share capital *% shares

Retained earnings *% shares

Reserves (+ FV increment) *% shares

GoodwillInvestment

(Elimination of investment in subsidiary)*Elimination of unrealized gain on sale of PPE**Adj for excess depreciation and its associated tax effects**Elimination of unrealized gain in opening inventory**Elimination of unrealized gain in closing inventory*Dividends revenue *% shares

Dividends *% shares

(Elimination of intragroup dividend)Share CapitalReservesOpening Retained ProfitsProfit attributable to NCIDividendsEquity attributable to NCI

(Elimination of NCI)

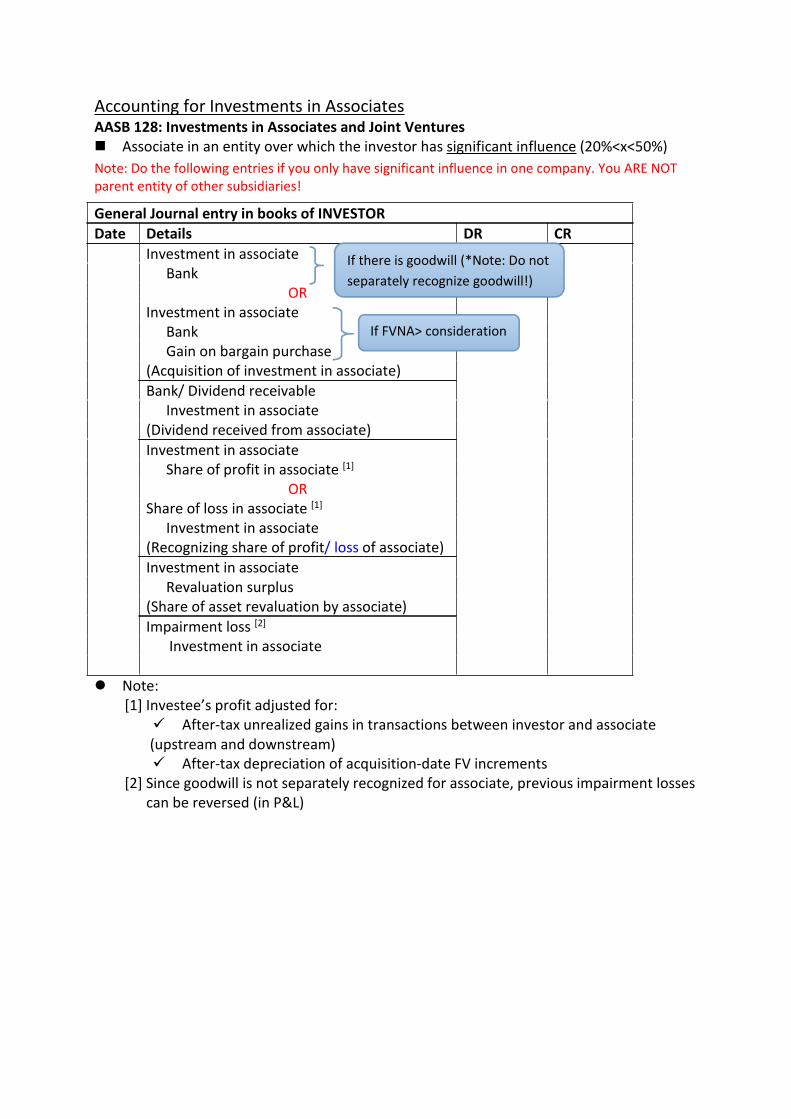

Accounting for Investments in AssociatesAASB 128: Investments in Associates and Joint Ventures Associate in an entity over which the investor has significant influence (20%<x<50%)Note: Do the following entries if you only have significant influence in one company. You ARE NOTparent entity of other subsidiaries!

General Journal entry in books of INVESTORDate Details DR CR

Investment in associateBank

ORInvestment in associate

BankGain on bargain purchase

(Acquisition of investment in associate)Bank/ Dividend receivable

Investment in associate(Dividend received from associate)Investment in associate

Share of profit in associate [1]

ORShare of loss in associate [1]

Investment in associate(Recognizing share of profit/ loss of associate)Investment in associate

Revaluation surplus(Share of asset revaluation by associate)Impairment loss [2]

Investment in associate

Note:[1] Investee’s profit adjusted for:

After-tax unrealized gains in transactions between investor and associate(upstream and downstream) After-tax depreciation of acquisition-date FV increments

[2] Since goodwill is not separately recognized for associate, previous impairment lossescan be reversed (in P&L)

If there is goodwill (*Note: Do notseparately recognize goodwill!)

If FVNA> consideration

Do the following entries if you have significant influence in one entity + you are parent entity ofother subsidiaries!Need to convert the investment to the equity method upon consolidation!

Equity Method when Investor is a Parent Entity

General Journal entry in books of Parent LtdDate Details DR CRT=0 Investment in associate

Bank(Acquisition of investment in associate)Bank/ Dividend receivableDividends Revenue

(Dividend received from associate)

Consolidation Journal entry in books of Parent LtdDate Details DR CRT=0 Investment in associate

Dividends RevenueShare of profit

(Adj to recognize investment in associateunder equity method)

General Journal entry in books of Parent LtdDate Details DR CRT=1 Bank/ Dividend receivable

Dividends Revenue(Dividend received from associate)

Consolidation Journal entry in books of Parent LtdDate Details DR CRT=1 Investment in associate

Dividends RevenueOpening Retained ProfitShare of profitRevaluation Surplus

(Adj to recognize investment in associateunder equity method)

AASB 121: Foreign Currency Translation If the presentation currency differs from the entity’s functional currency, it translates its

results and financial position into the presentation currency.

Rules of ThumbRevenue & Expenses Average rateDividends declared Spot rate on date of declarationAssets & Liabilities Closing rate at reporting dateEquity accounts at acquisition Spot rate at date of acquisitionPost-acquisition movements in share capital& reserves

Spot rate on date of recognition

Post acquisition movements in retainedprofits

Profit at average rate each period lessdividends at spot rate