Intermediate Financial Accounting I Inventories: Additional Valuation Issues.

47

Intermediate Financial Accounting I Inventories: Additional Valuation Issues

-

Upload

layla-salisbury -

Category

Documents

-

view

253 -

download

2

Transcript of Intermediate Financial Accounting I Inventories: Additional Valuation Issues.

Intermediate Financial Accounting I

Inventories: Additional Valuation Issues

Inventories: Additional Issues 2

Objectives of this Chapter

I. Introduce Inventory estimation methods: the gross profit method and the retail inventory method.

II. Determine ending inventory cost by applying the gross profit method.

III. Determine ending inventory cost by applying the retail inventory method.

Inventories: Additional Issues 3

Objectives of this Chapter (contd.)

IV. Compare the gross profit method and the retail inventory method.

V. Explain dollar-value LIFO retail method.

VI. Discuss accounting issues related to purchase commitments.

Inventories: Additional Issues 4

I. Estimating Inventory: Gross Profit Method and Retail Inventory Method

Reasons: For some companies, inventory information is needed between accounting periods . Companies cannot afford to do physical inventory count every quarter.

Thus, either the gross profit method or the retail inventory method can be used to estimate value of ending inventory for interim reports.

Inventories: Additional Issues 5

Estimating Inventory: Gross Profit Method and Retail Inventory Method (contd.)

No physical count of inventory is needed for either method. The value of inventory is based on estimation.

Neither method is acceptable for annual financial reporting purposes.

Inventories: Additional Issues 6

Estimating Inventory: Gross Profit Method and Retail Inventory Method (contd.)

Both methods are acceptable for interim reporting.

The insurance adjusters may use the gross profit method to estimate the loss of inventory in case of fire or flood.

Inventories: Additional Issues 7

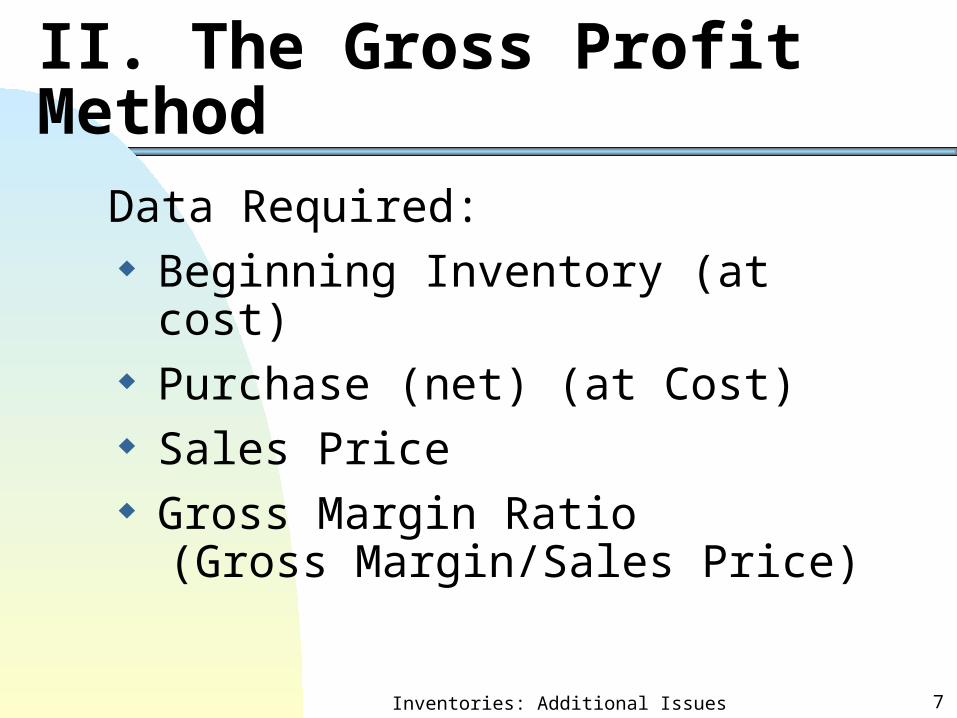

II. The Gross Profit Method

Data Required: Beginning Inventory (at cost) Purchase (net) (at Cost) Sales Price Gross Margin Ratio

(Gross Margin/Sales Price)

Inventories: Additional Issues 8

Gross Profit Method

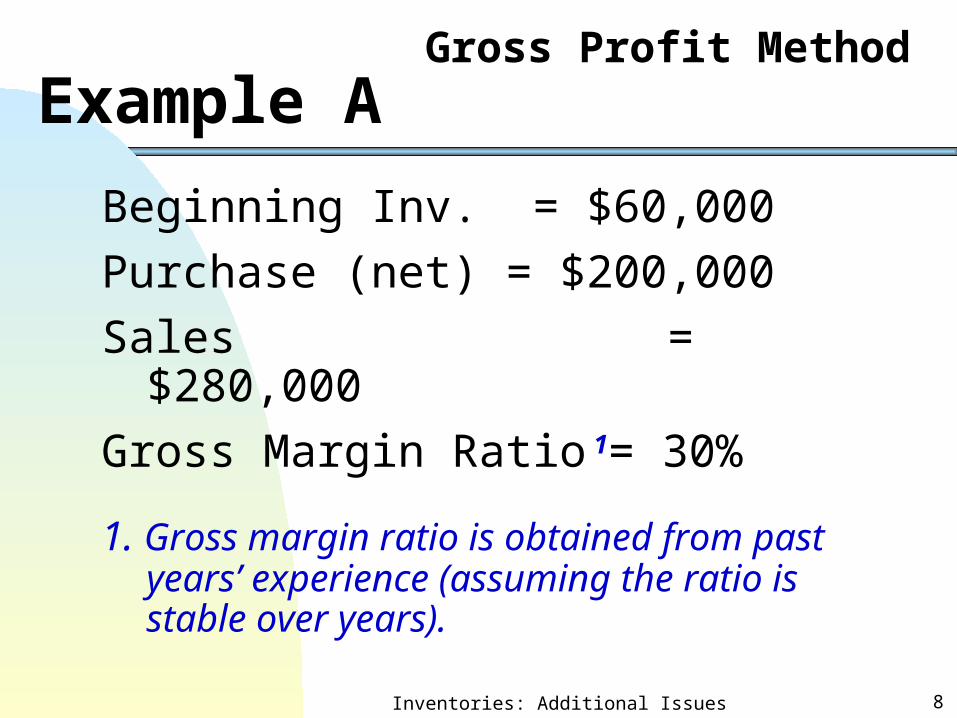

Example A

Beginning Inv. = $60,000

Purchase (net) = $200,000

Sales = $280,000

Gross Margin Ratio 1= 30%

1. Gross margin ratio is obtained from past years’ experience (assuming the ratio is stable over years).

Inventories: Additional Issues 9

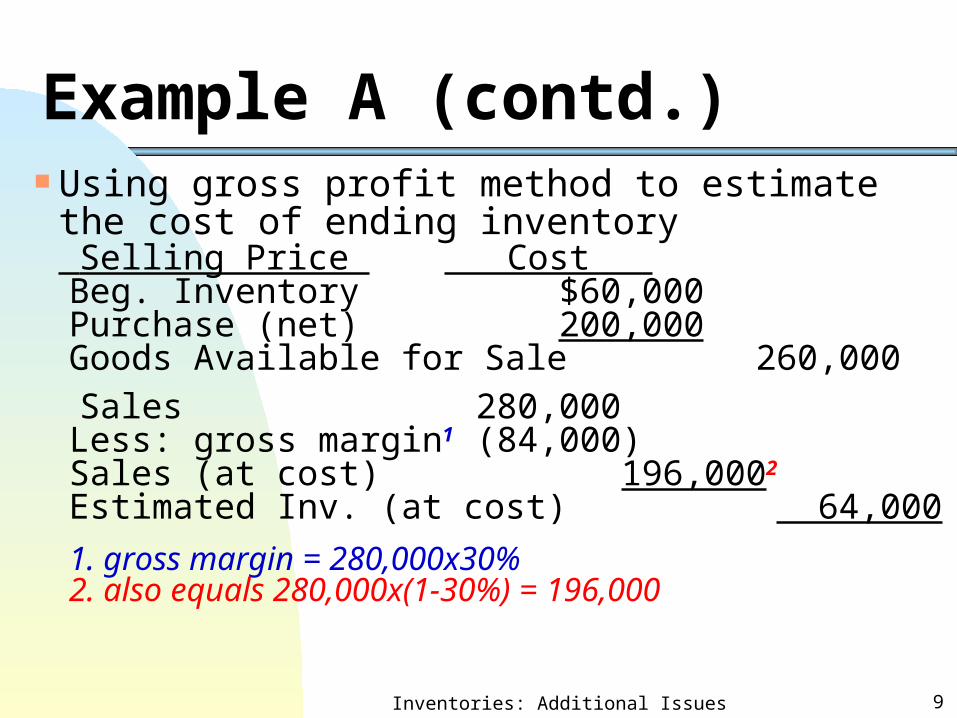

Example A (contd.) Using gross profit method to estimate the cost of

ending inventory Selling Price Cost Beg. Inventory $60,000Purchase (net) 200,000Goods Available for Sale 260,000

Sales 280,000Less: gross margin1 (84,000) Sales (at cost) 196,0002Estimated Inv. (at cost) 64,000

1. gross margin = 280,000x30%2. also equals 280,000x(1-30%) = 196,000

Inventories: Additional Issues 10

Gross Profit Method

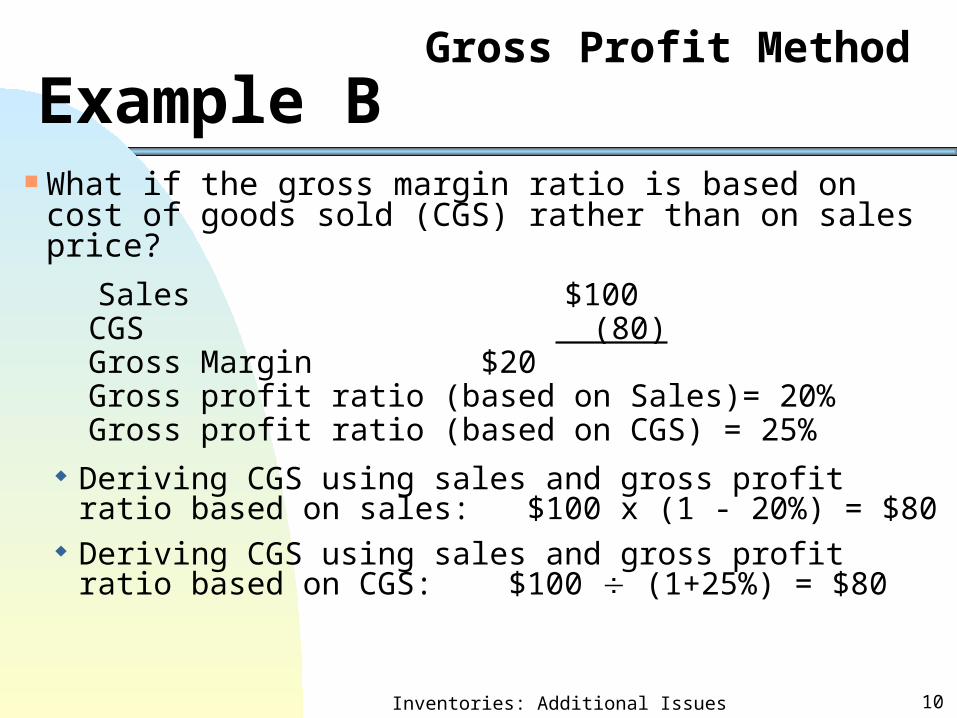

Example B What if the gross margin ratio is based on cost of

goods sold (CGS) rather than on sales price?

Sales $100CGS (80)Gross Margin $20Gross profit ratio (based on Sales)= 20%Gross profit ratio (based on CGS) = 25%

Deriving CGS using sales and gross profit ratio based on sales: $100 x (1 - 20%) = $80

Deriving CGS using sales and gross profit ratio based on CGS: $100 (1+25%) = $80

Inventories: Additional Issues 11

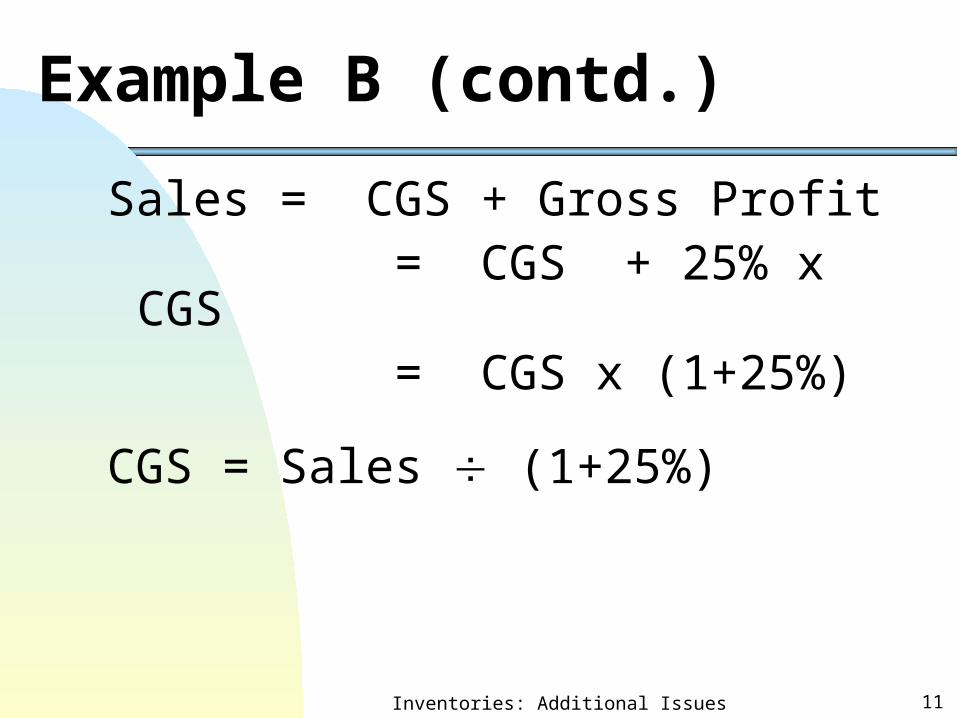

Example B (contd.)

Sales = CGS + Gross Profit = CGS + 25% x CGS = CGS x (1+25%)

CGS = Sales (1+25%)

Inventories: Additional Issues 12

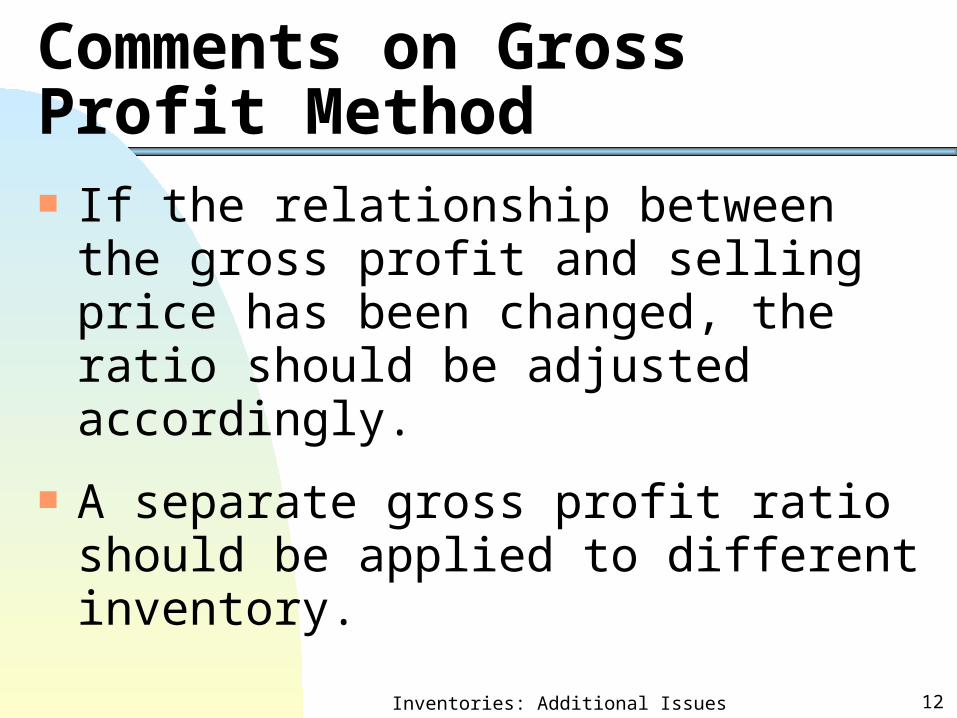

Comments on Gross Profit Method

If the relationship between the gross profit and selling price has been changed, the ratio should be adjusted accordingly.

A separate gross profit ratio should be applied to different inventory.

Inventories: Additional Issues 13

Market

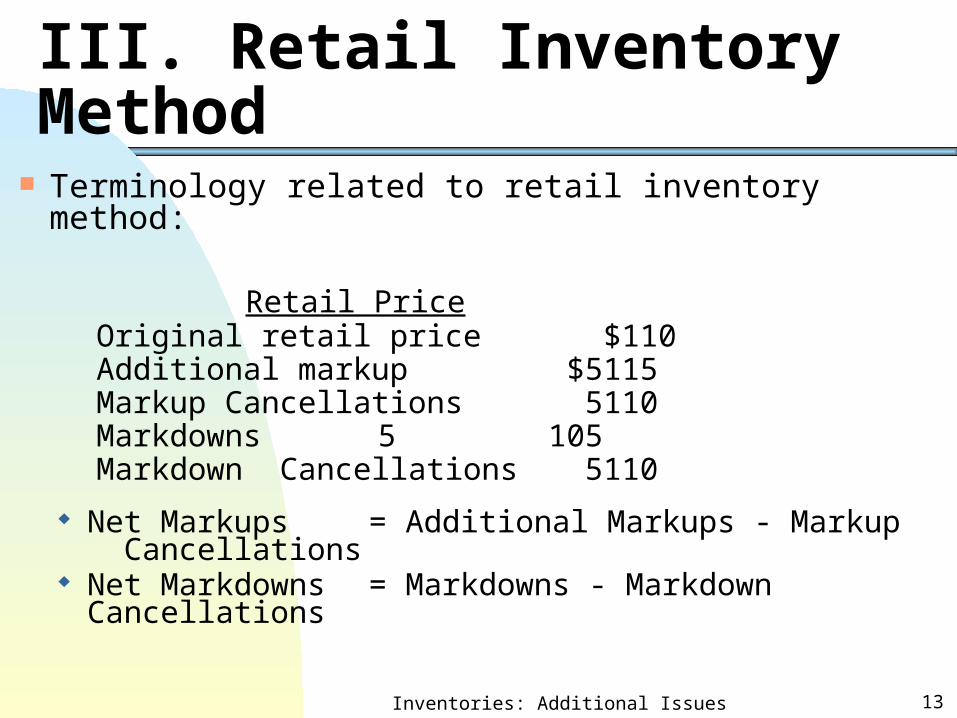

III. Retail Inventory Method Terminology related to retail inventory method:

Retail PriceOriginal retail price $110Additional markup $5 115Markup Cancellations 5 110Markdowns 5 105Markdown Cancellations 5 110

Net Markups = Additional Markups - Markup Cancellations

Net Markdowns = Markdowns - Markdown Cancellations

Inventories: Additional Issues 14

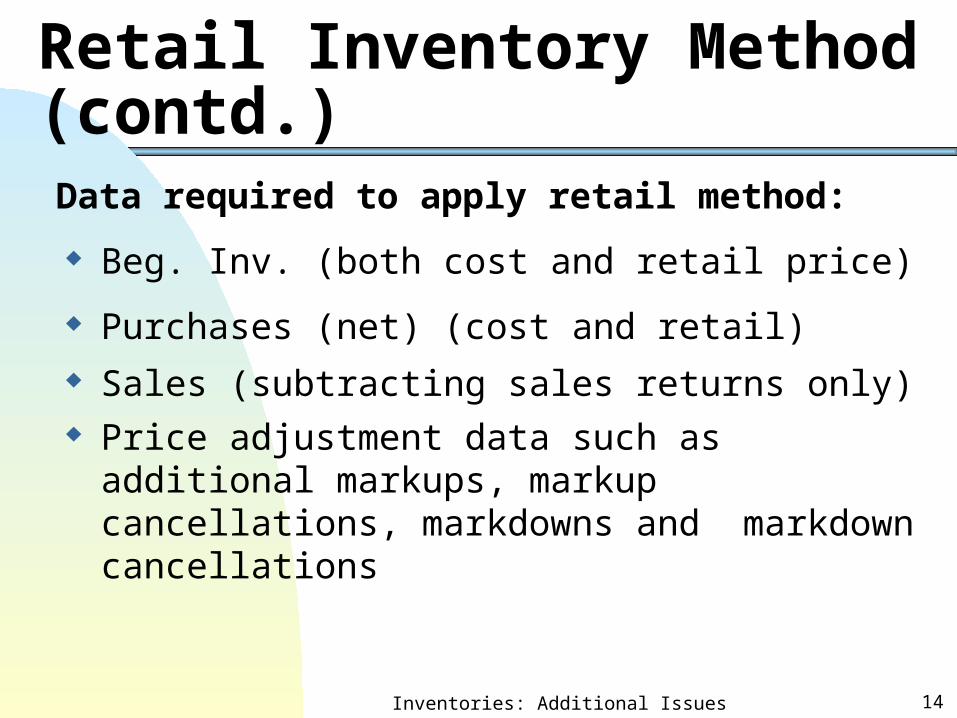

Retail Inventory Method (contd.)

Data required to apply retail method:

Beg. Inv. (both cost and retail price)

Purchases (net) (cost and retail) Sales (subtracting sales returns only) Price adjustment data such as additional

markups, markup cancellations, markdowns and markdown cancellations

Inventories: Additional Issues 15

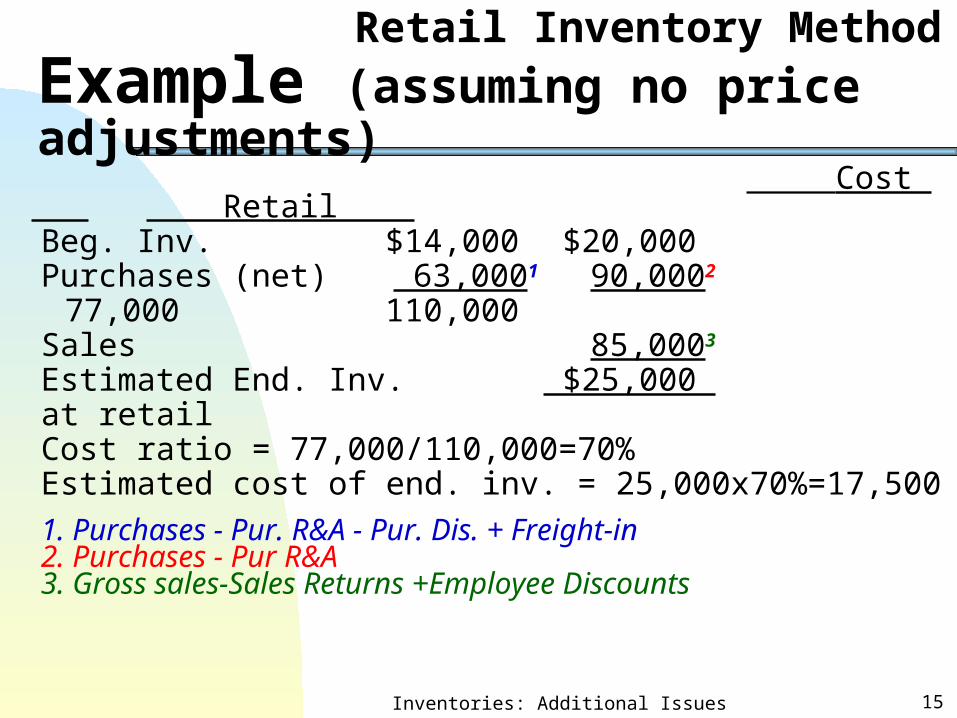

Retail Inventory Method

Example (assuming no price adjustments) Cost Retail Beg. Inv. $14,000 $20,000 Purchases (net) 63,0001 90,0002

77,000 110,000 Sales 85,0003Estimated End. Inv. $25,000 at retailCost ratio = 77,000/110,000=70%Estimated cost of end. inv. = 25,000x70%=17,500

1. Purchases - Pur. R&A - Pur. Dis. + Freight-in2. Purchases - Pur R&A3. Gross sales-Sales Returns +Employee Discounts

Inventories: Additional Issues 16

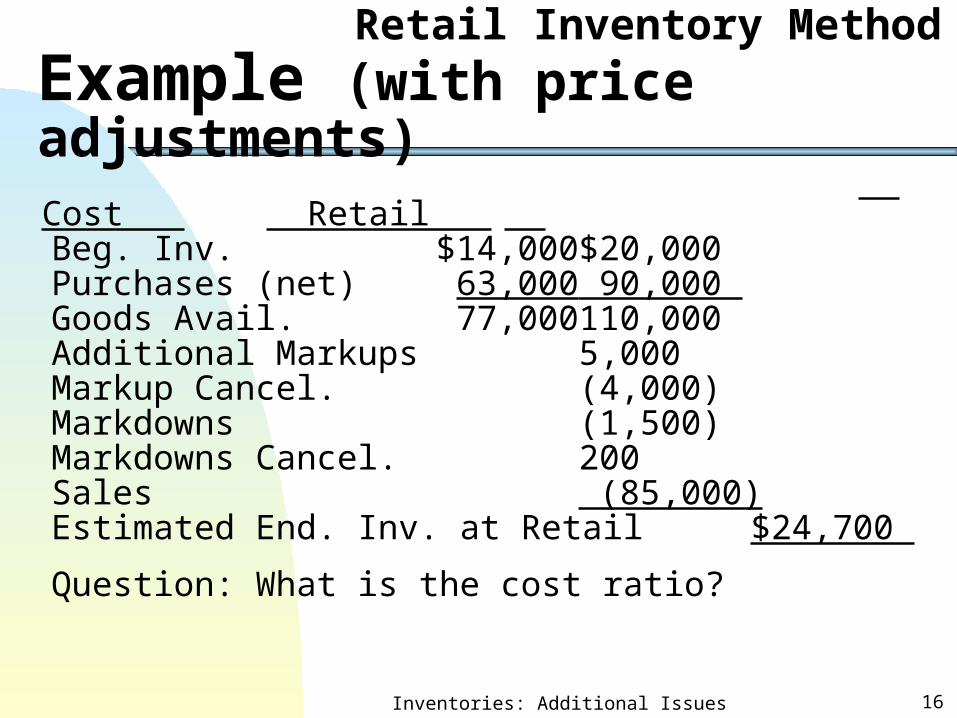

Retail Inventory Method

Example (with price adjustments) Cost Retail Beg. Inv. $14,000 $20,000 Purchases (net) 63,000 90,000 Goods Avail. 77,000 110,000 Additional Markups 5,000 Markup Cancel. (4,000)Markdowns (1,500)Markdowns Cancel. 200 Sales (85,000)Estimated End. Inv. at Retail $24,700

Question: What is the cost ratio?

Inventories: Additional Issues 17

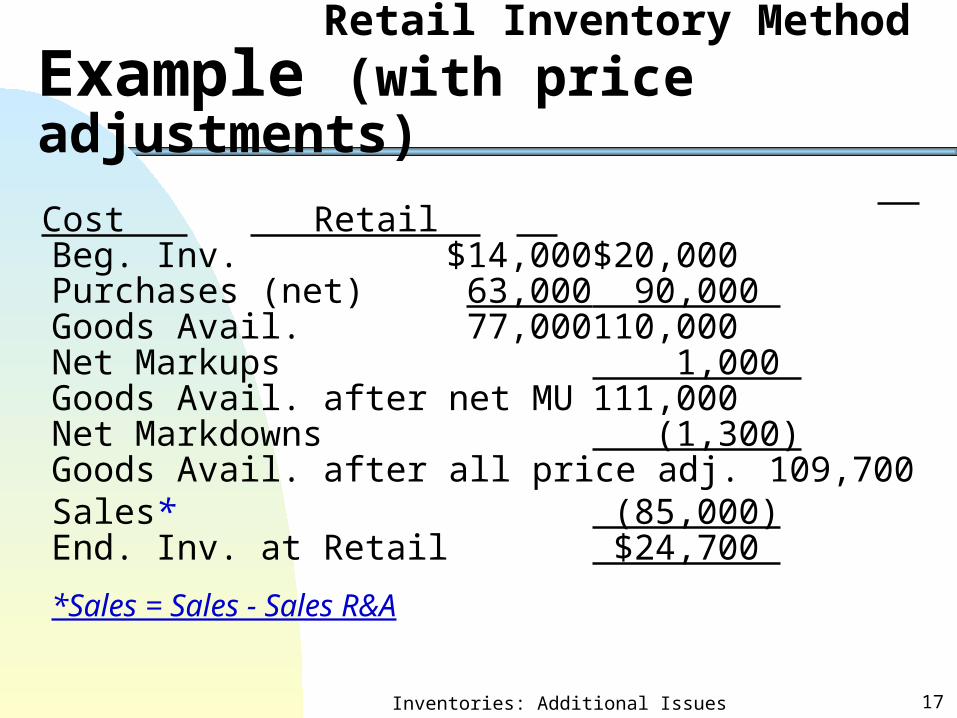

Retail Inventory Method

Example (with price adjustments)

Cost Retail Beg. Inv. $14,000 $20,000 Purchases (net) 63,000 90,000 Goods Avail. 77,000 110,000 Net Markups 1,000 Goods Avail. after net MU 111,000 Net Markdowns (1,300)Goods Avail. after all price adj. 109,700 Sales* (85,000)End. Inv. at Retail $24,700

*Sales = Sales - Sales R&A

Inventories: Additional Issues 18

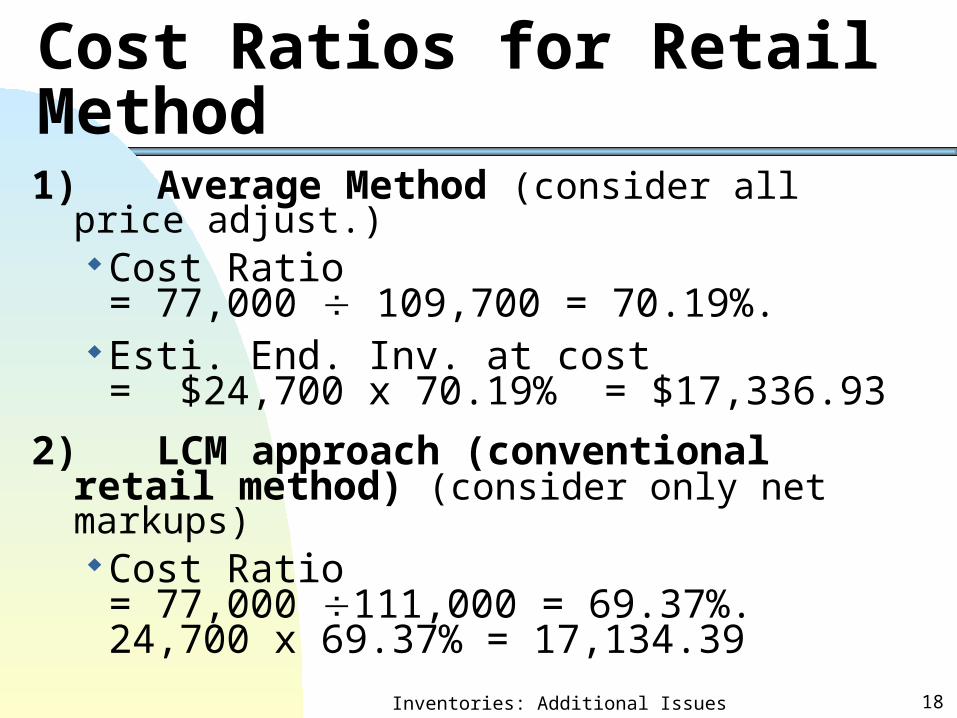

Cost Ratios for Retail Method

1) Average Method (consider all price adjust.) Cost Ratio = 77,000 109,700 = 70.19%.

Esti. End. Inv. at cost = $24,700 x 70.19% = $17,336.93

2) LCM approach (conventional retail method) (consider only net markups) Cost Ratio= 77,000 111,000 = 69.37%.24,700 x 69.37% = 17,134.39

Inventories: Additional Issues 19

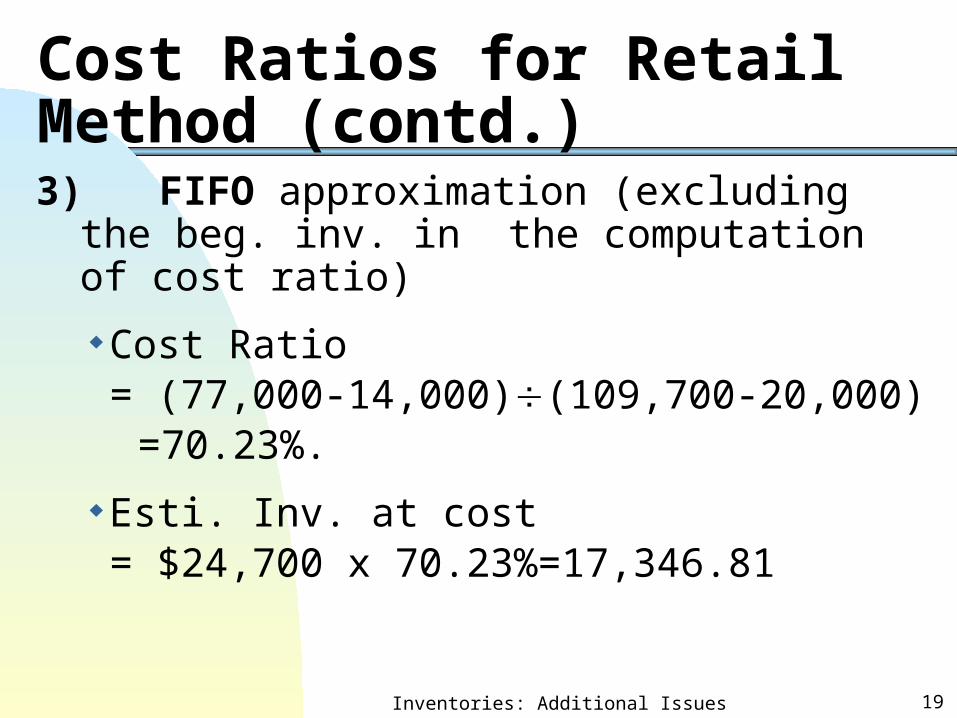

Cost Ratios for Retail Method (contd.)

3) FIFO approximation (excluding the beg. inv. in the computation of cost ratio)

Cost Ratio= (77,000-14,000)(109,700-20,000)

=70.23%.

Esti. Inv. at cost = $24,700 x 70.23%=17,346.81

Inventories: Additional Issues 20

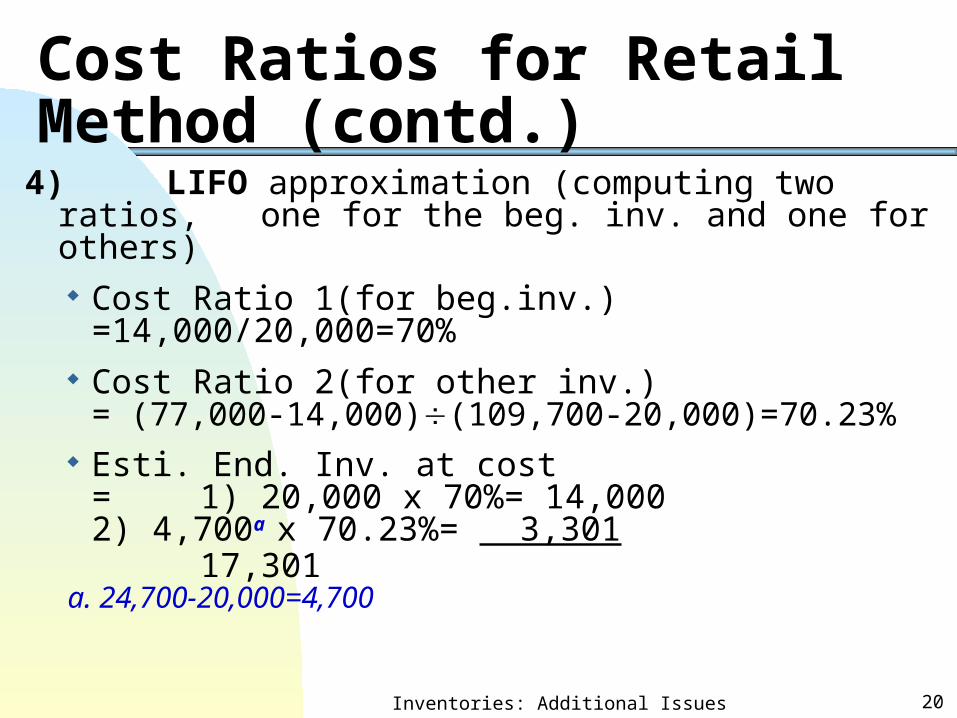

Cost Ratios for Retail Method (contd.)4)LIFO approximation (computing two ratios, one for

the beg. inv. and one for others) Cost Ratio 1(for beg.inv.)

=14,000/20,000=70% Cost Ratio 2(for other inv.)

= (77,000-14,000)(109,700-20,000)=70.23% Esti. End. Inv. at cost

= 1) 20,000 x 70% = 14,0002) 4,700a x 70.23% = 3,301

17,301a. 24,700-20,000=4,700

Inventories: Additional Issues 21

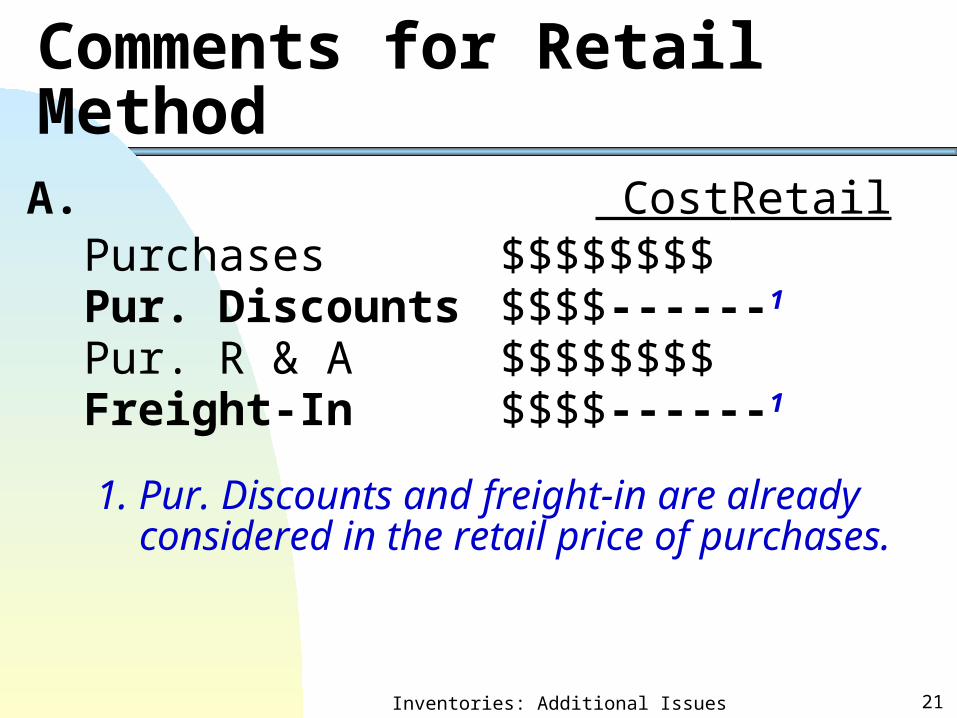

Comments for Retail Method

A. Cost RetailPurchases $$$$ $$$$Pur. Discounts $$$$ ------1

Pur. R & A $$$$ $$$$Freight-In $$$$ ------1

1. Pur. Discounts and freight-in are already considered in the retail price of purchases.

Inventories: Additional Issues 22

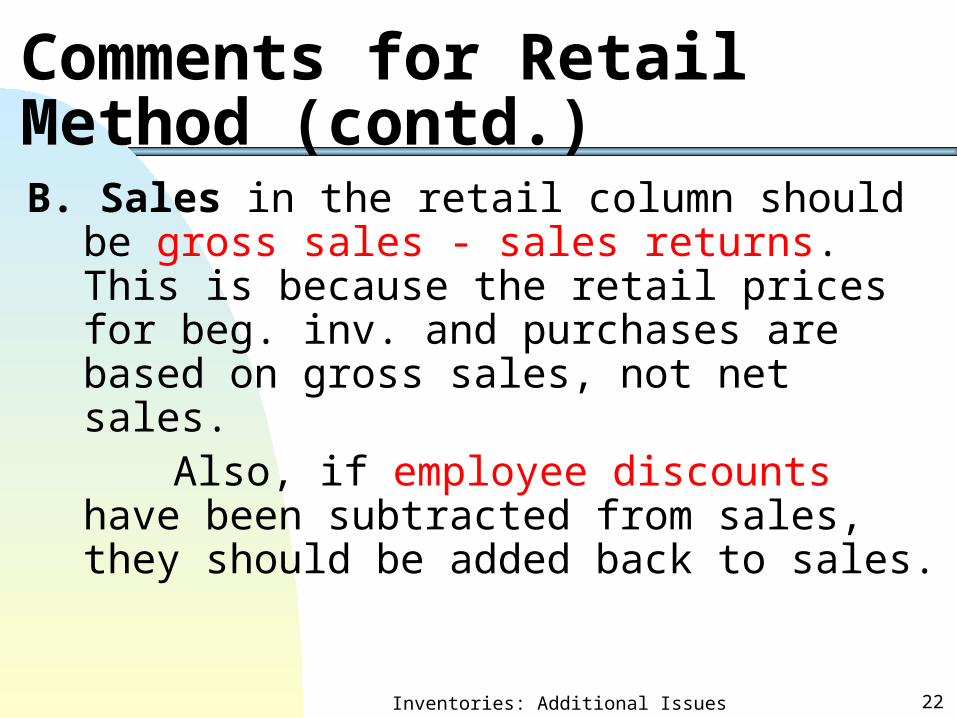

Comments for Retail Method (contd.)

B. Sales in the retail column should be gross sales - sales returns. This is because the retail prices for beg. inv. and purchases are based on gross sales, not net sales.

Also, if employee discounts have been subtracted from sales, they should be added back to sales.

Inventories: Additional Issues 23

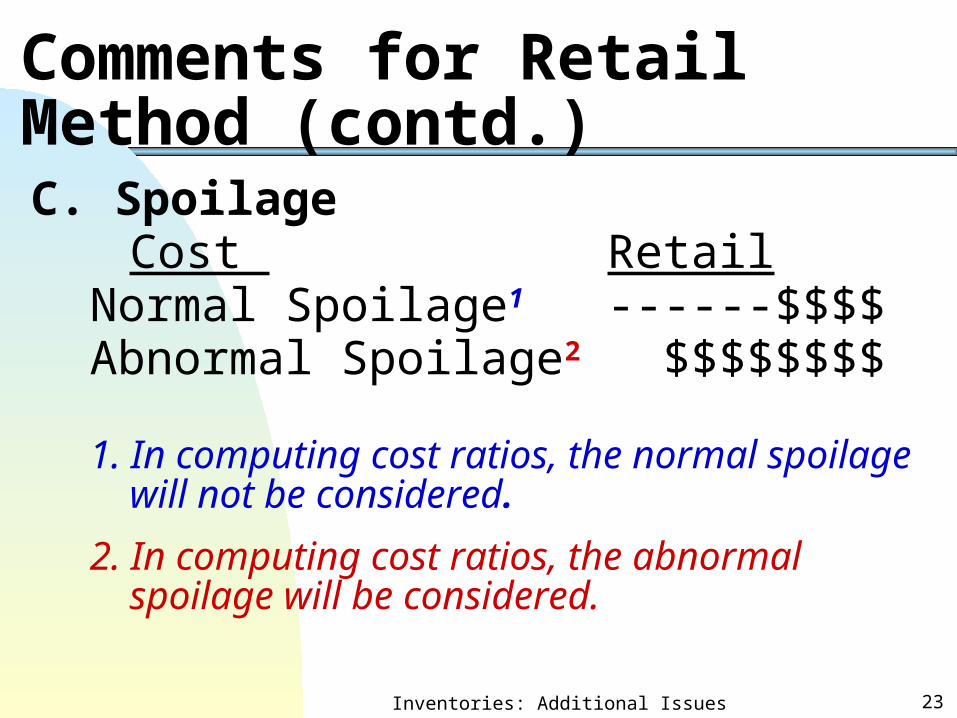

Comments for Retail Method (contd.)

C. SpoilageCost Retail

Normal Spoilage1 ------ $$$$Abnormal Spoilage2 $$$$ $$$$

1. In computing cost ratios, the normal spoilage will not be considered.

2. In computing cost ratios, the abnormal spoilage will be considered.

Inventories: Additional Issues 24

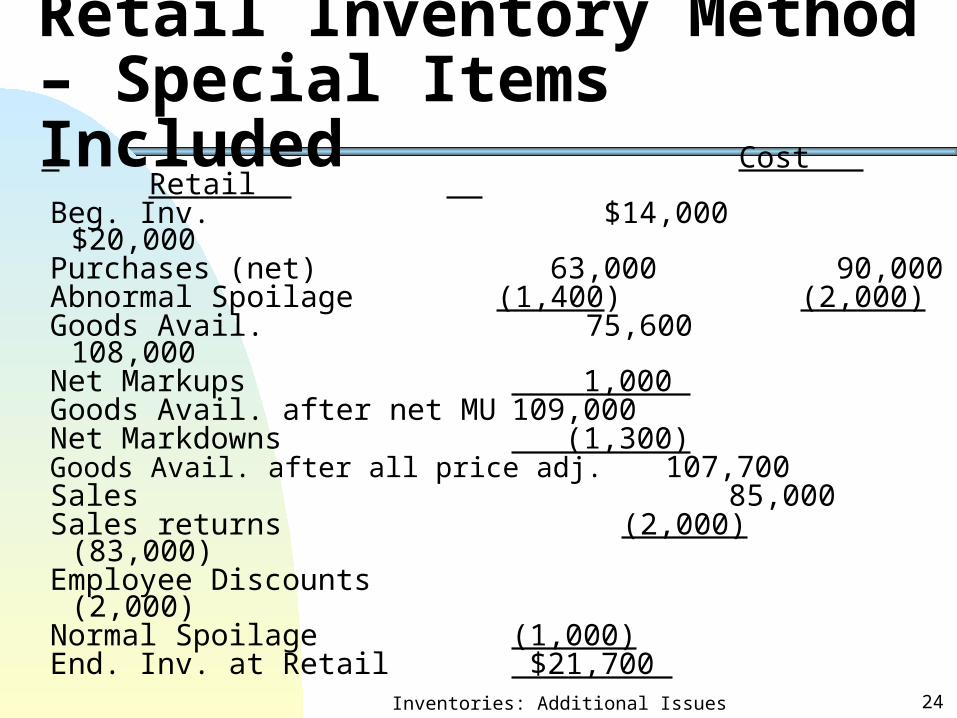

Retail Inventory Method – Special Items Included Cost Retail Beg. Inv. $14,000 $20,000 Purchases (net) 63,000 90,000 Abnormal Spoilage (1,400) (2,000) Goods Avail. 75,600 108,000 Net Markups 1,000 Goods Avail. after net MU 109,000 Net Markdowns (1,300)Goods Avail. after all price adj. 107,700 Sales 85,000 Sales returns (2,000) (83,000)Employee Discounts (2,000)Normal Spoilage (1,000)End. Inv. at Retail $21,700

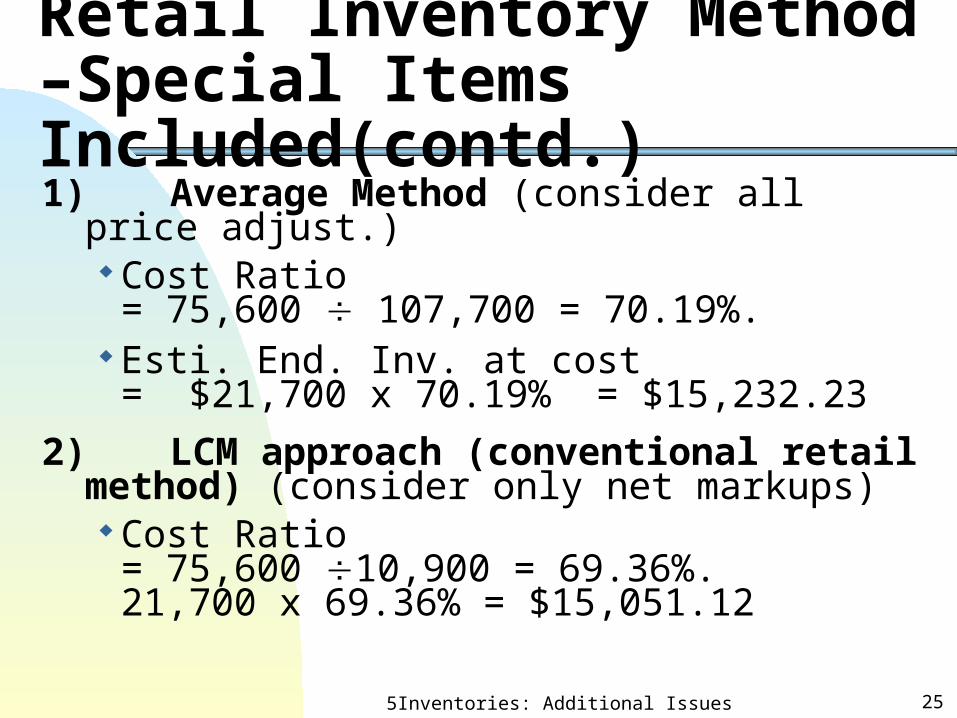

Retail Inventory Method –Special Items Included(contd.)1) Average Method (consider all price adjust.)

Cost Ratio = 75,600 107,700 = 70.19%.

Esti. End. Inv. at cost = $21,700 x 70.19% = $15,232.23

2) LCM approach (conventional retail method) (consider only net markups) Cost Ratio

= 75,600 10,900 = 69.36%.21,700 x 69.36% = $15,051.12

5Inventories: Additional Issues 25

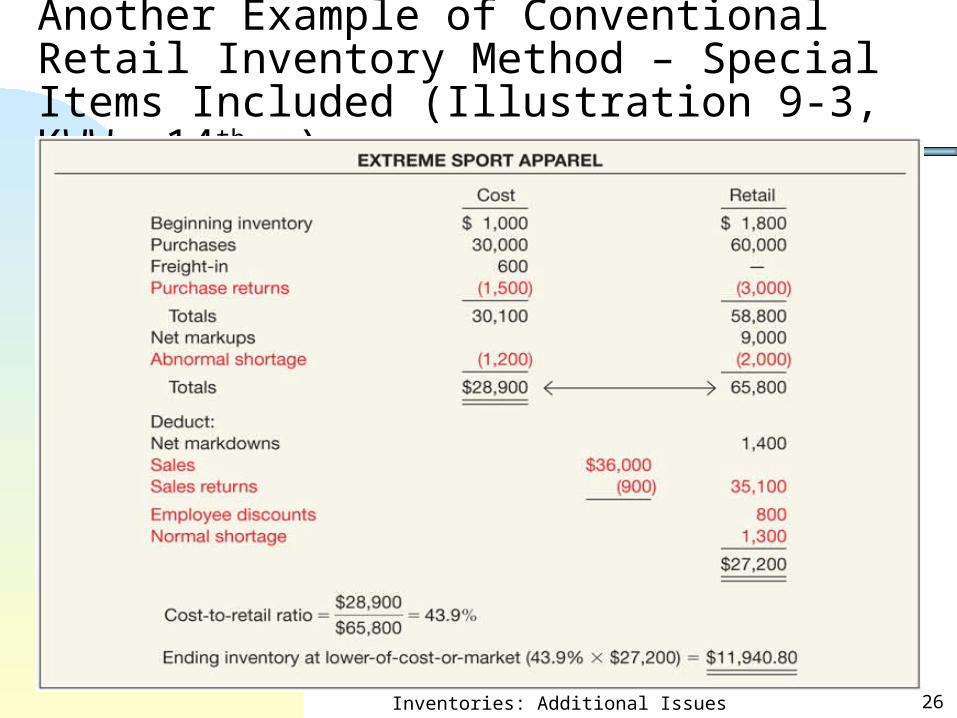

Another Example of Conventional Retail Inventory Method – Special Items Included (Illustration 9-3, KWW, 14 th e)

Inventories: Additional Issues 26

Inventories: Additional Issues 27

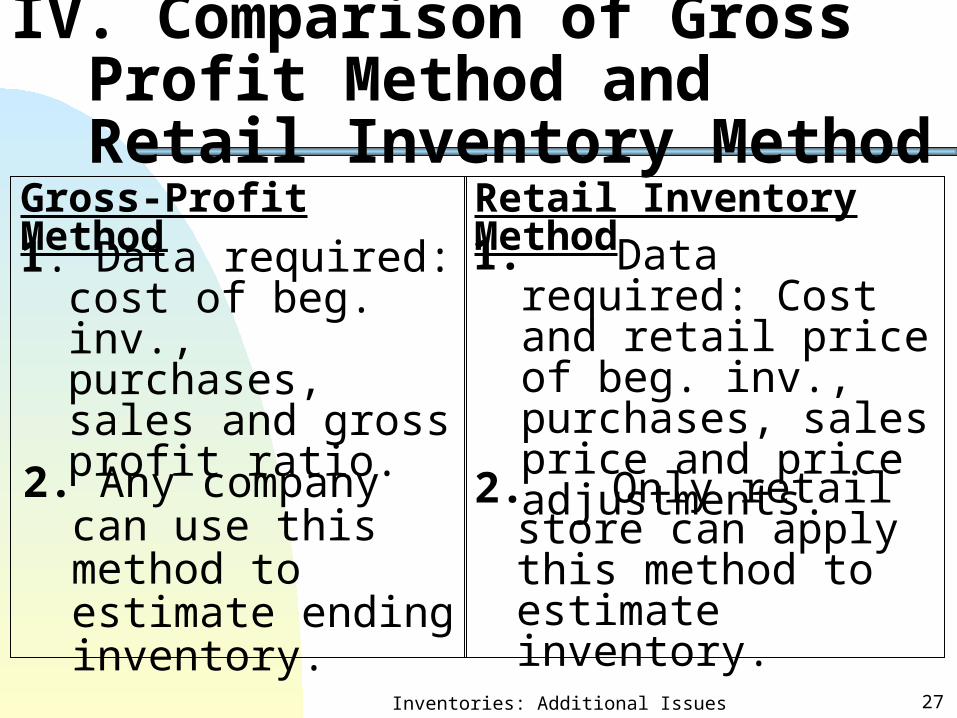

IV. Comparison of Gross Profit Method and Retail Inventory Method

Gross-Profit Method Retail Inventory Method

1. Data required: cost of beg. inv., purchases, sales and gross profit ratio.

2. Any company can use this method to estimate ending inventory.

1. Data required: Cost and retail price of beg. inv., purchases, sales price and price adjustments.

2. Only retail store can apply this method to estimate inventory.

Inventories: Additional Issues 28

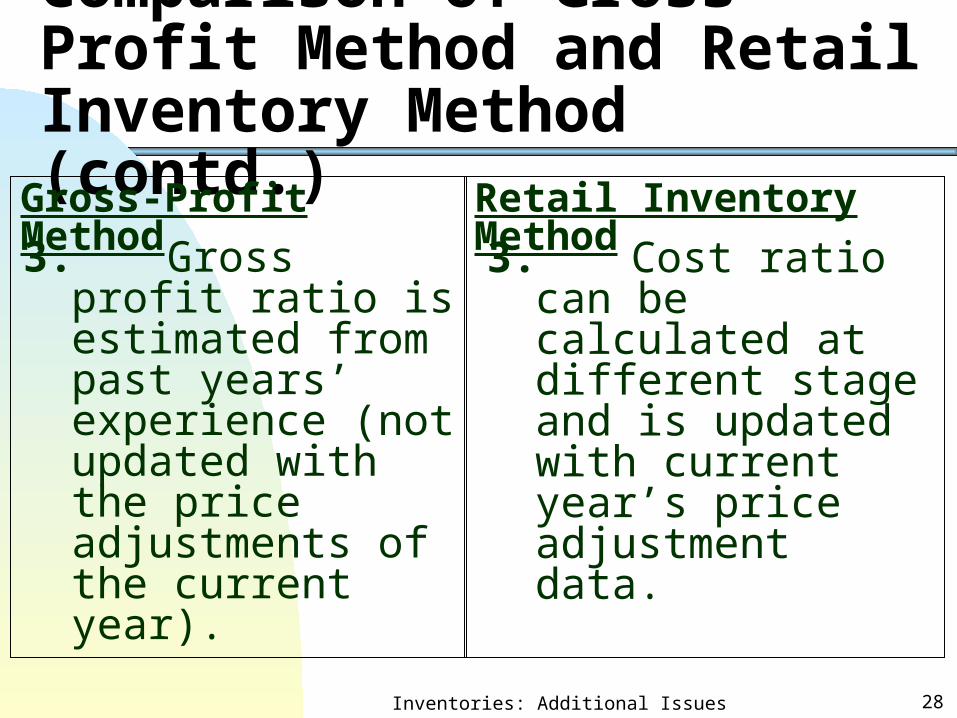

Comparison of Gross Profit Method and Retail Inventory Method (contd.)

Gross-Profit Method Retail Inventory Method

3. Gross profit ratio is estimated from past years’ experience (not updated with the price adjustments of the current year).

3. Cost ratio can be calculated at different stage and is updated with current year’s price adjustment data.

Inventories: Additional Issues 29

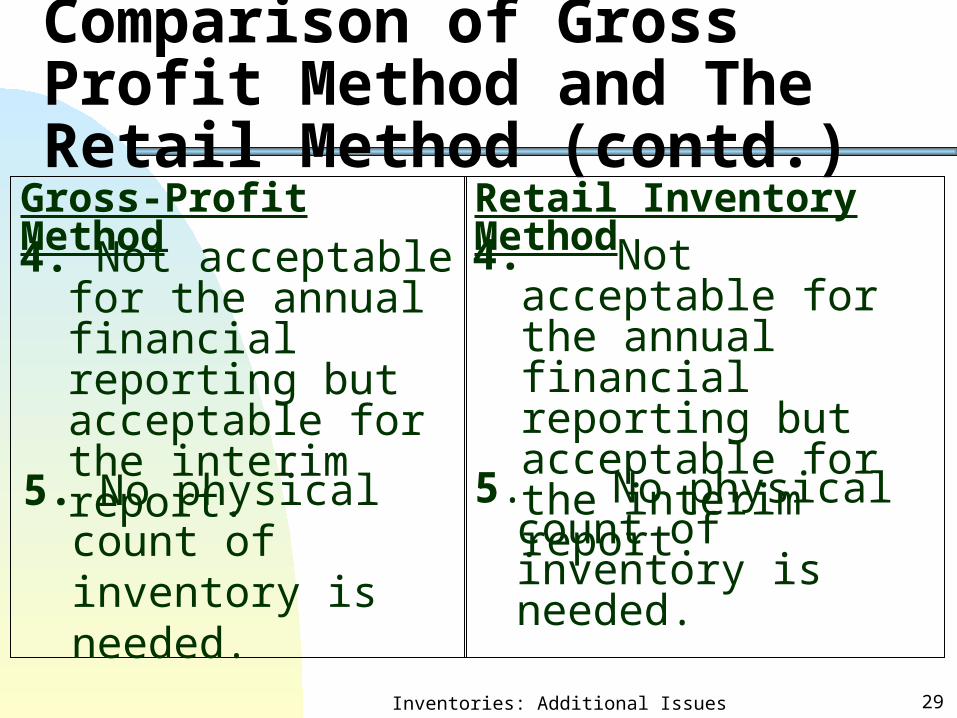

Comparison of Gross Profit Method and The Retail Method (contd.)

Gross-Profit Method Retail Inventory Method

4. Not acceptable for the annual financial reporting but acceptable for the interim report.

5. No physical count of inventory is needed.

4. Not acceptable for the annual financial reporting but acceptable for the interim report.

5. No physical count of inventory is needed.

Inventories: Additional Issues 30

V. Dollar-Value LIFO Retail Method

Applying retail method to estimate cost of ending inventory and also considering price index when prices are fluctuating.

Inventories: Additional Issues 31

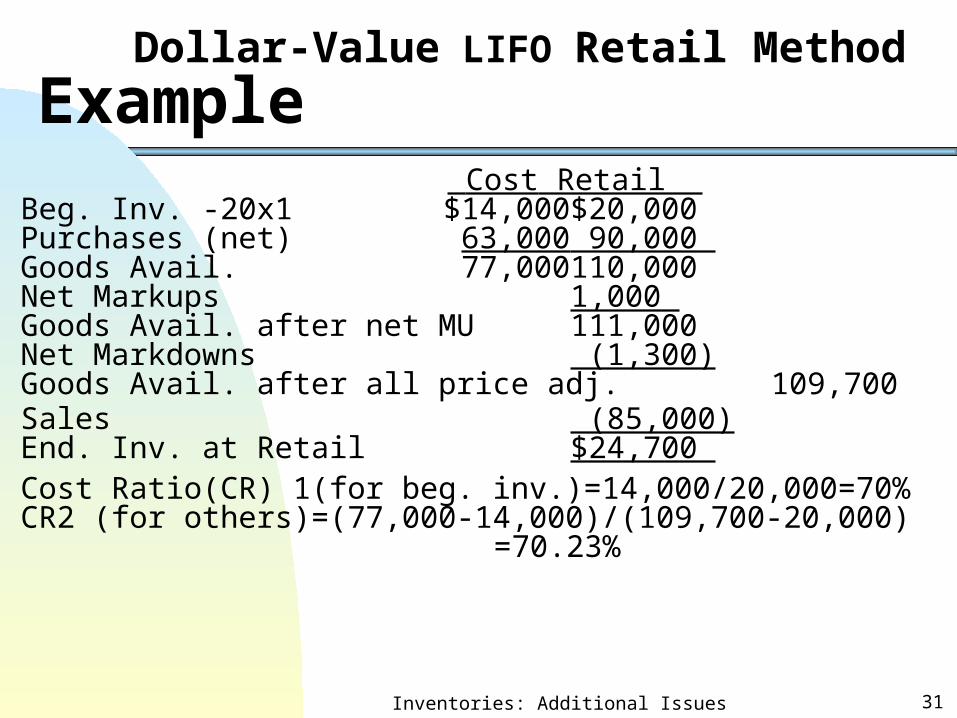

Dollar-Value LIFO Retail Method

Example Cost Retail

Beg. Inv. -20x1 $14,000 $20,000 Purchases (net) 63,000 90,000 Goods Avail. 77,000 110,000 Net Markups 1,000 Goods Avail. after net MU 111,000 Net Markdowns (1,300)Goods Avail. after all price adj. 109,700 Sales (85,000)End. Inv. at Retail $24,700 Cost Ratio(CR) 1(for beg. inv.)=14,000/20,000=70%CR2 (for others)=(77,000-14,000)/(109,700-20,000) =70.23%

Inventories: Additional Issues 32

Dollar-Value LIFO Retail Method

Example (contd.) Assuming the price indices of 20x0 and

20x1 are 100% and 112%, respectively.

Procedures of applying Dollar-Value LIFO concept to Retail method (LIFO approximation):

Inventories: Additional Issues 33

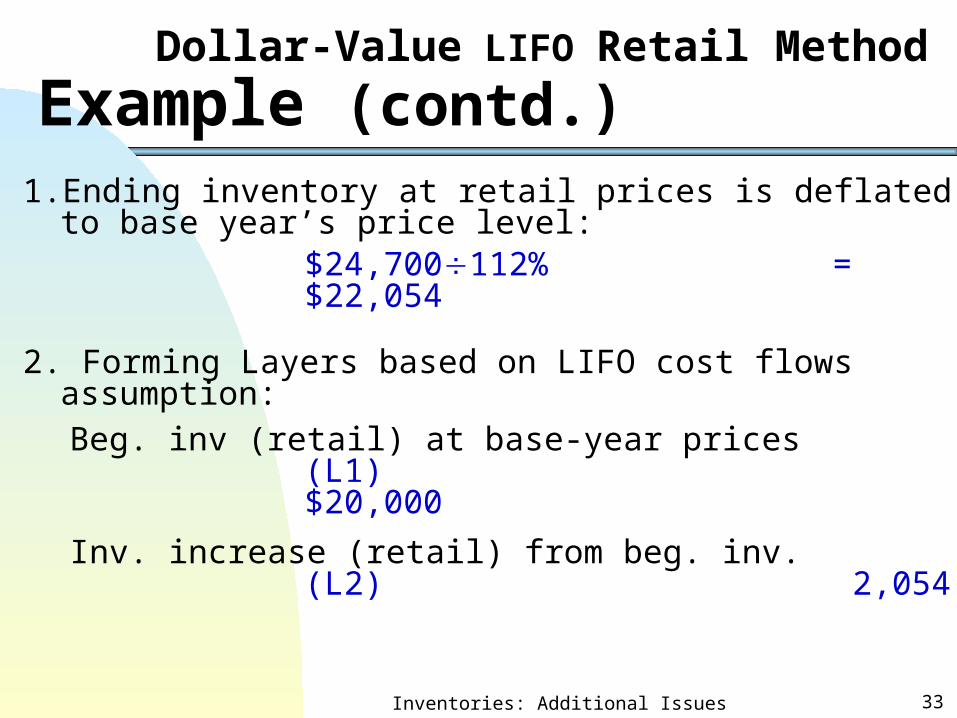

Dollar-Value LIFO Retail Method

Example (contd.)1. Ending inventory at retail prices is deflated to base

year’s price level:$24,700112% =

$22,054

2. Forming Layers based on LIFO cost flows assumption:

Beg. inv (retail) at base-year prices(L1)

$20,000

Inv. increase (retail) from beg. inv. (L2)

2,054

Inventories: Additional Issues 34

Dollar-Value LIFO Retail Method

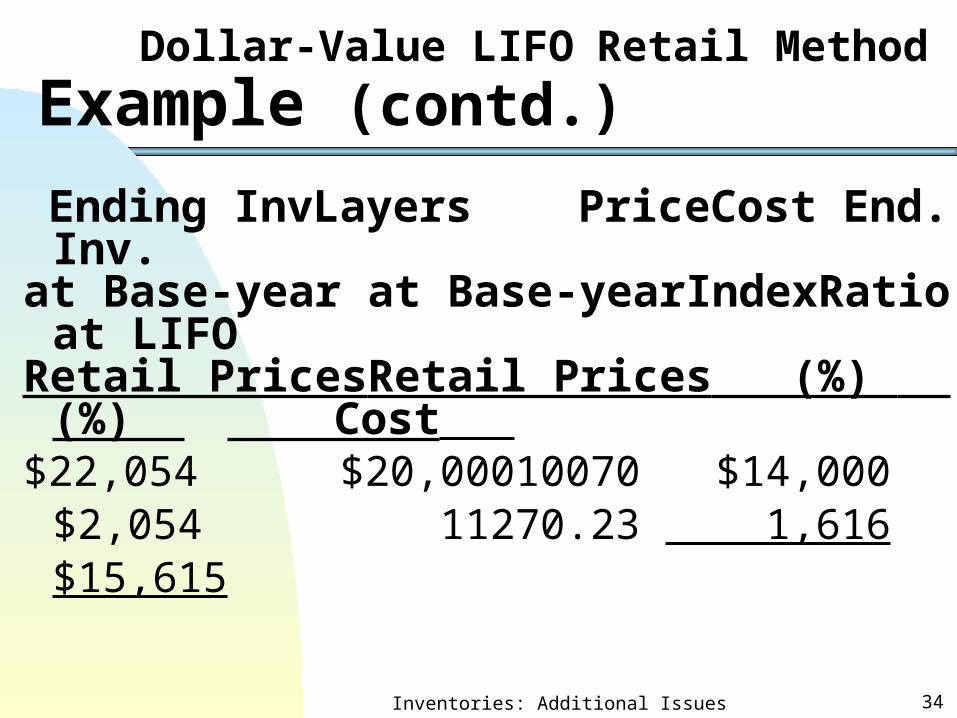

Example (contd.)

Ending Inv Layers Price Cost End. Inv.at Base-year at Base-year Index Ratio at LIFO Retail Prices Retail Prices (%) (%) Cost

$22,054 $20,000 100 70 $14,000$2,054 112 70.23 1,616

$15,615

Inventories: Additional Issues 35

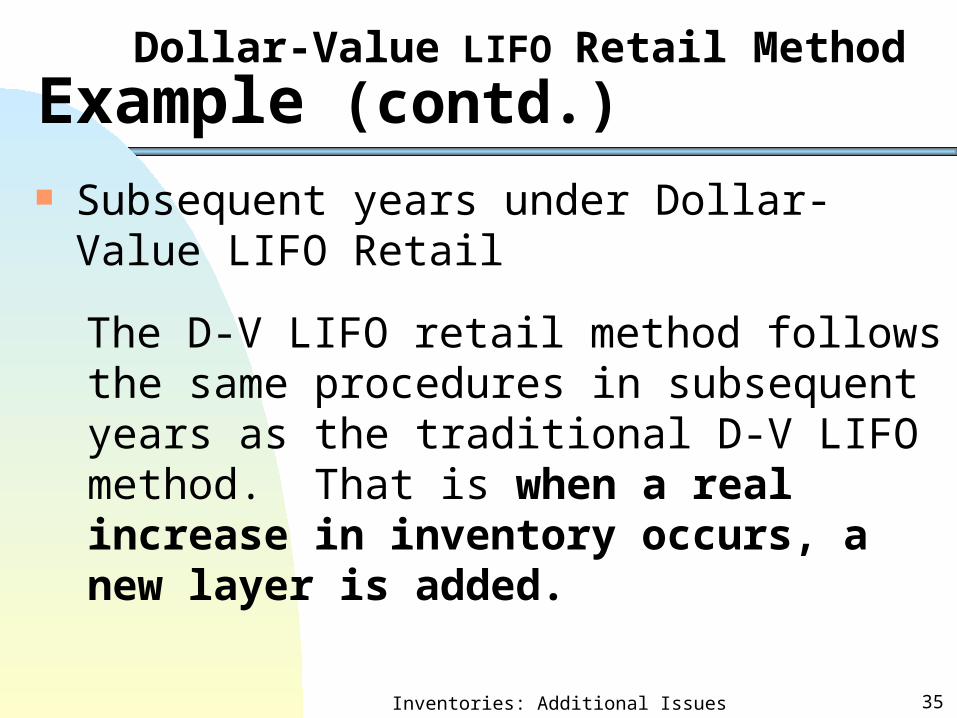

Dollar-Value LIFO Retail Method

Example (contd.) Subsequent years under Dollar-Value

LIFO Retail

The D-V LIFO retail method follows the same procedures in subsequent years as the traditional D-V LIFO method. That is when a real increase in inventory occurs, a new layer is added.

Inventories: Additional Issues 36

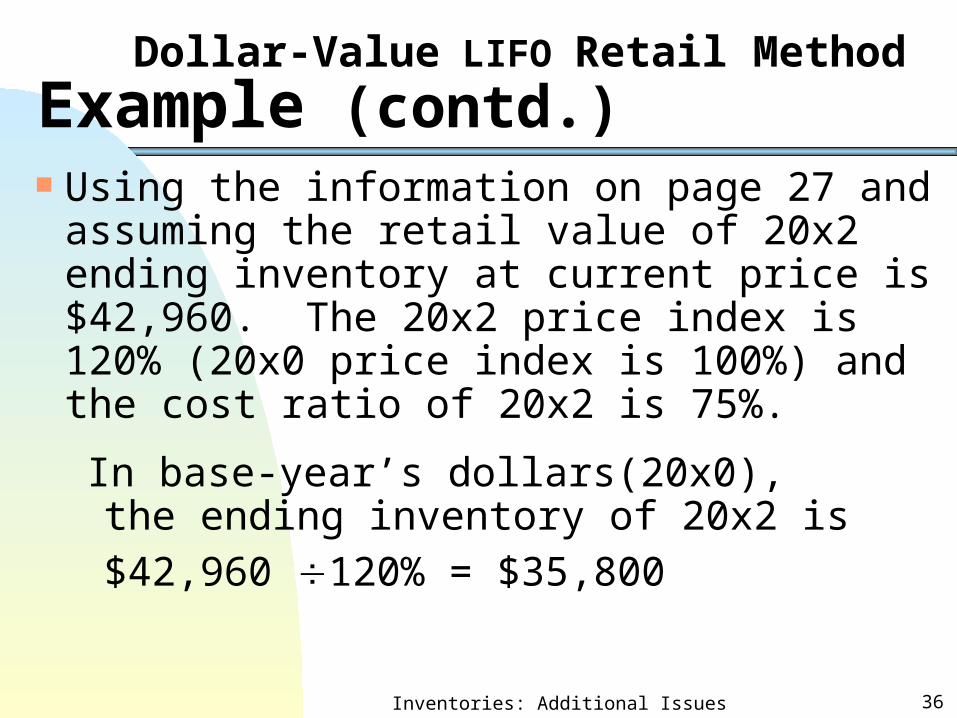

Dollar-Value LIFO Retail Method

Example (contd.) Using the information on page 27 and

assuming the retail value of 20x2 ending inventory at current price is $42,960. The 20x2 price index is 120% (20x0 price index is 100%) and the cost ratio of 20x2 is 75%.

In base-year’s dollars(20x0), the ending inventory of 20x2 is $42,960 120% = $35,800

Inventories: Additional Issues 37

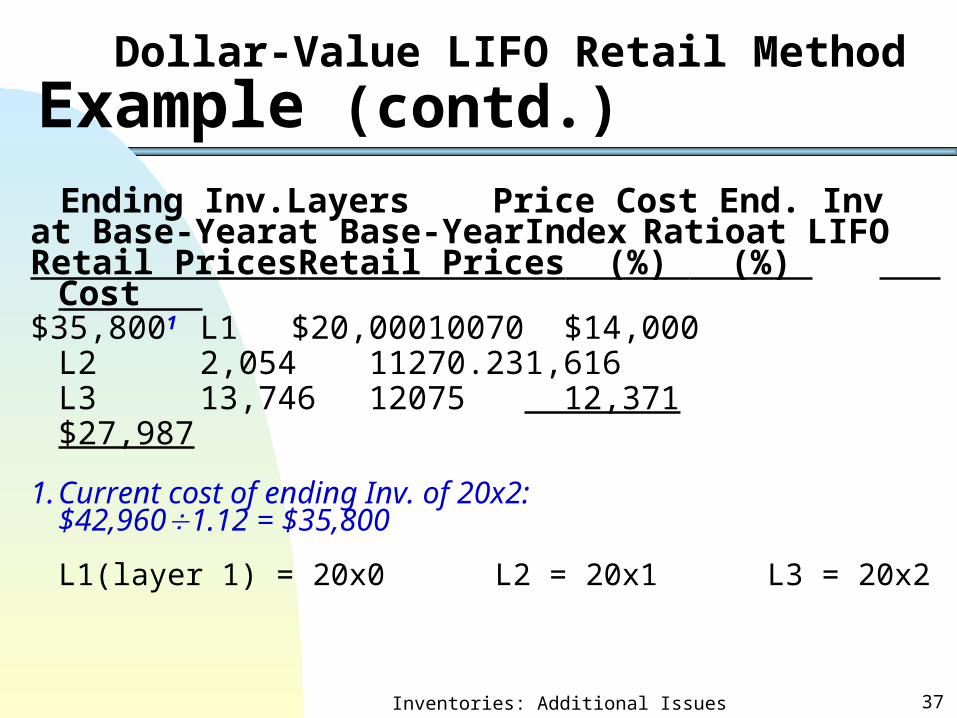

Dollar-Value LIFO Retail Method

Example (contd.)

Ending Inv. Layers Price Cost End. Inv at Base-Year at Base-Year Index Ratio at LIFO Retail PricesRetail Prices (%) (%) Cost $35,8001 L1 $20,000 100 70 $14,000

L2 2,054 112 70.23 1,616L3 13,746 120 75 12,371

$27,987

1.Current cost of ending Inv. of 20x2: $42,9601.12 = $35,800

L1(layer 1) = 20x0 L2 = 20x1 L3 = 20x2

Inventories: Additional Issues 38

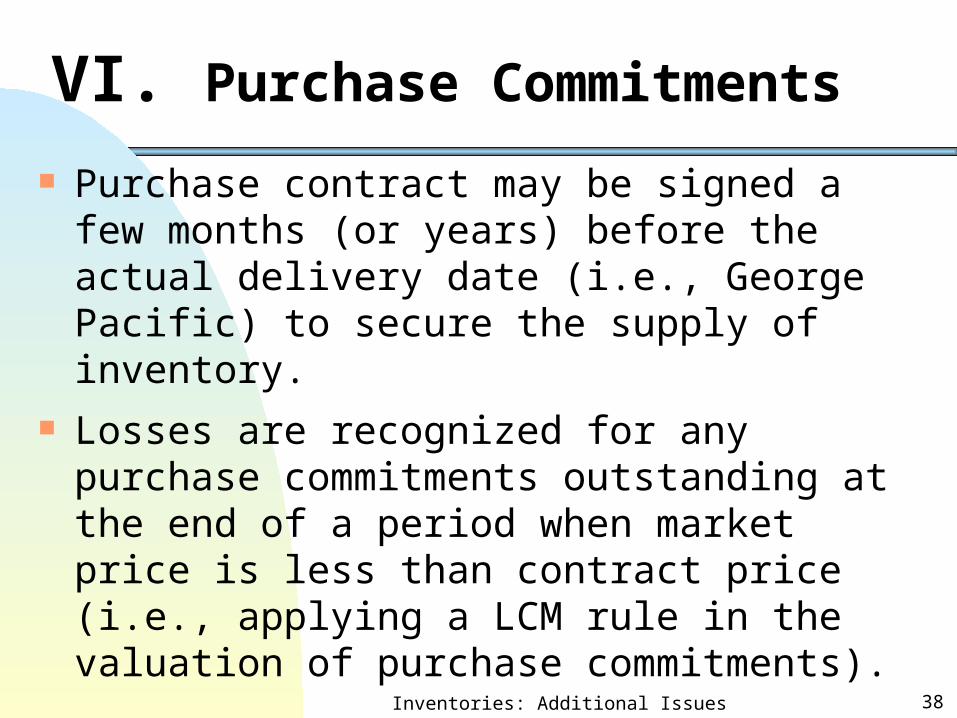

VI. Purchase Commitments

Purchase contract may be signed a few months (or years) before the actual delivery date (i.e., George Pacific) to secure the supply of inventory.

Losses are recognized for any purchase commitments outstanding at the end of a period when market price is less than contract price (i.e., applying a LCM rule in the valuation of purchase commitments).

Inventories: Additional Issues 39

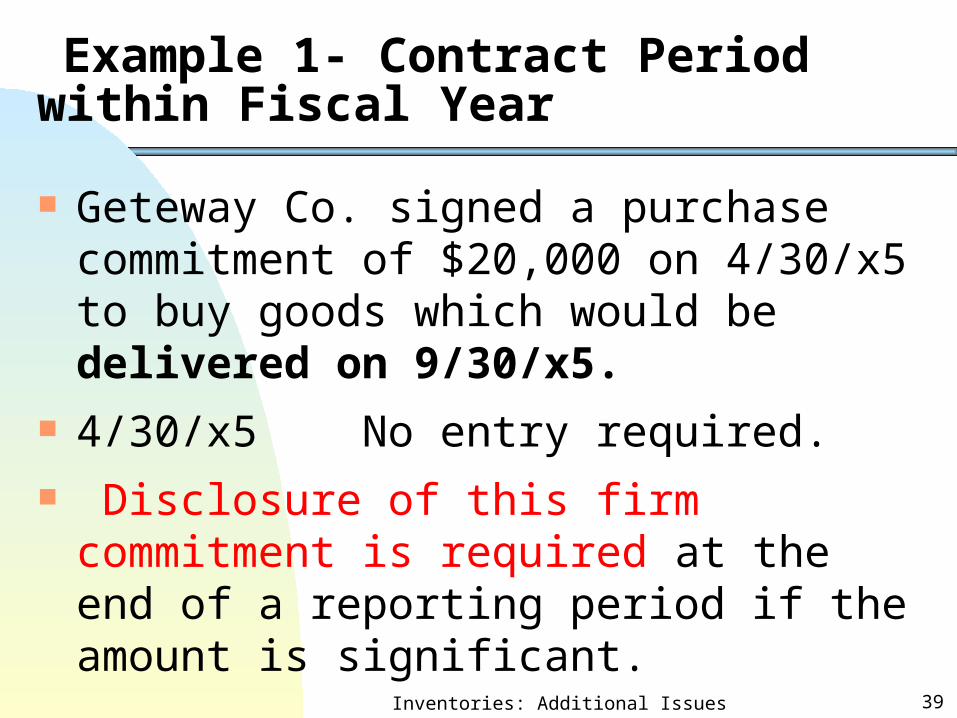

Example 1- Contract Period within Fiscal Year

Geteway Co. signed a purchase commitment of $20,000 on 4/30/x5 to buy goods which would be delivered on 9/30/x5.

4/30/x5 No entry required. Disclosure of this firm commitment is

required at the end of a reporting period if the amount is significant.

Inventories: Additional Issues 40

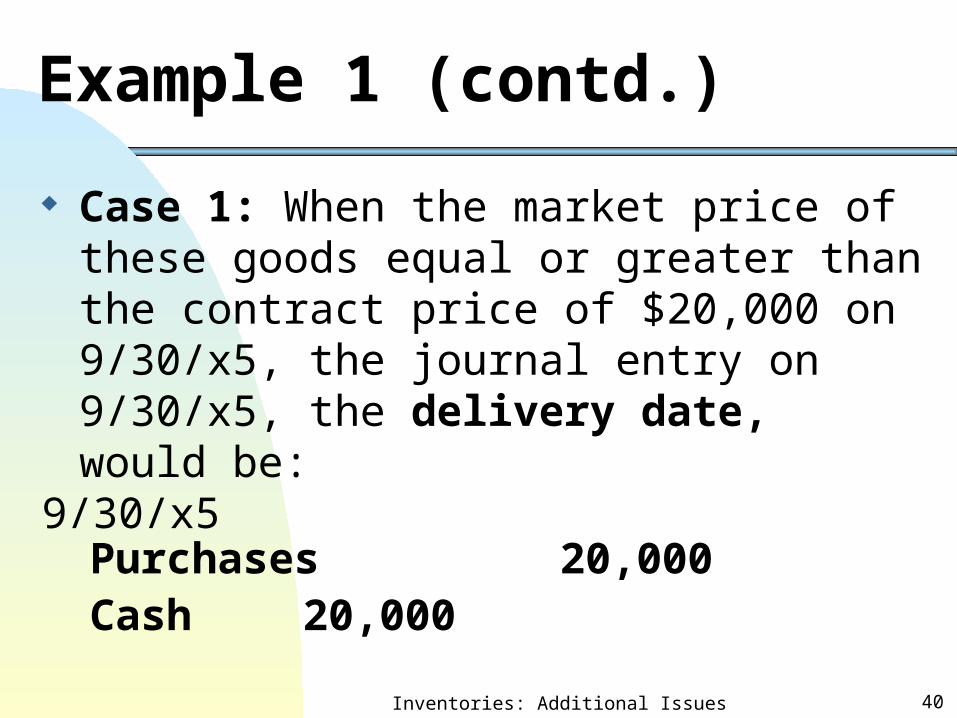

Example 1 (contd.)

Case 1: When the market price of these goods equal or greater than the contract price of $20,000 on 9/30/x5, the journal entry on 9/30/x5, the delivery date, would be:

9/30/x5Purchases 20,000

Cash 20,000

Inventories: Additional Issues 41

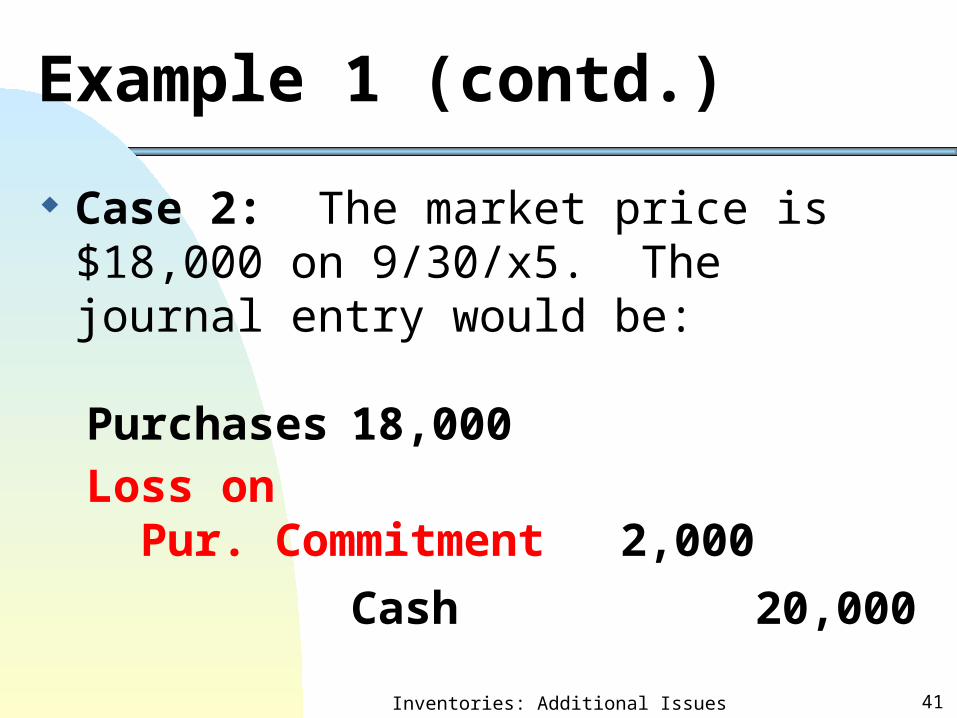

Example 1 (contd.)

Case 2: The market price is $18,000 on 9/30/x5. The journal entry would be:

Purchases 18,000Loss on Pur. Commitment 2,000

Cash 20,000

Inventories: Additional Issues 42

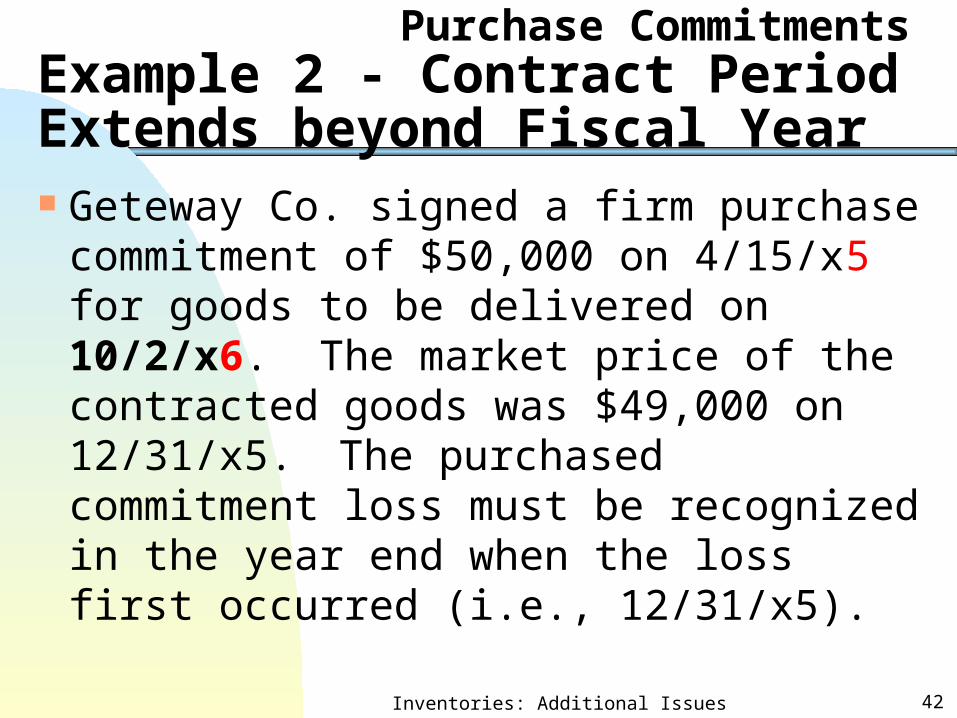

Purchase CommitmentsExample 2 - Contract Period Extends beyond Fiscal Year Geteway Co. signed a firm purchase

commitment of $50,000 on 4/15/x5 for goods to be delivered on 10/2/x6. The market price of the contracted goods was $49,000 on 12/31/x5. The purchased commitment loss must be recognized in the year end when the loss first occurred (i.e., 12/31/x5).

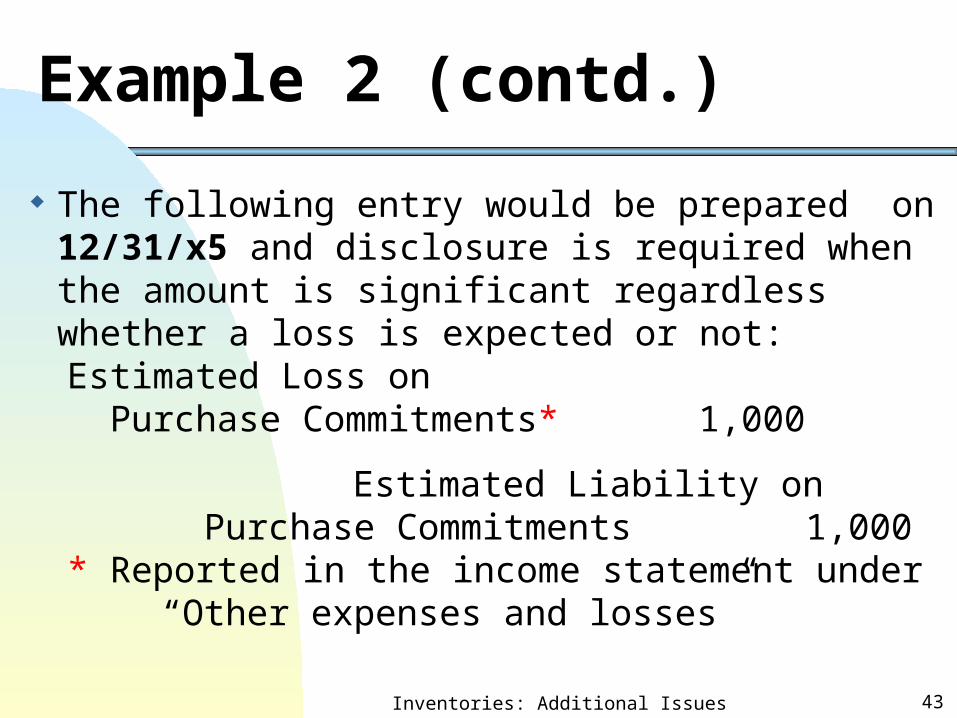

Inventories: Additional Issues 43

Example 2 (contd.)

The following entry would be prepared on 12/31/x5 and disclosure is required when the amount is significant regardless whether a loss is expected or not:Estimated Loss on Purchase Commitments* 1,000

Estimated Liability on Purchase Commitments 1,000

* Reported in the income statement under “Other expenses and losses”

Inventories: Additional Issues 44

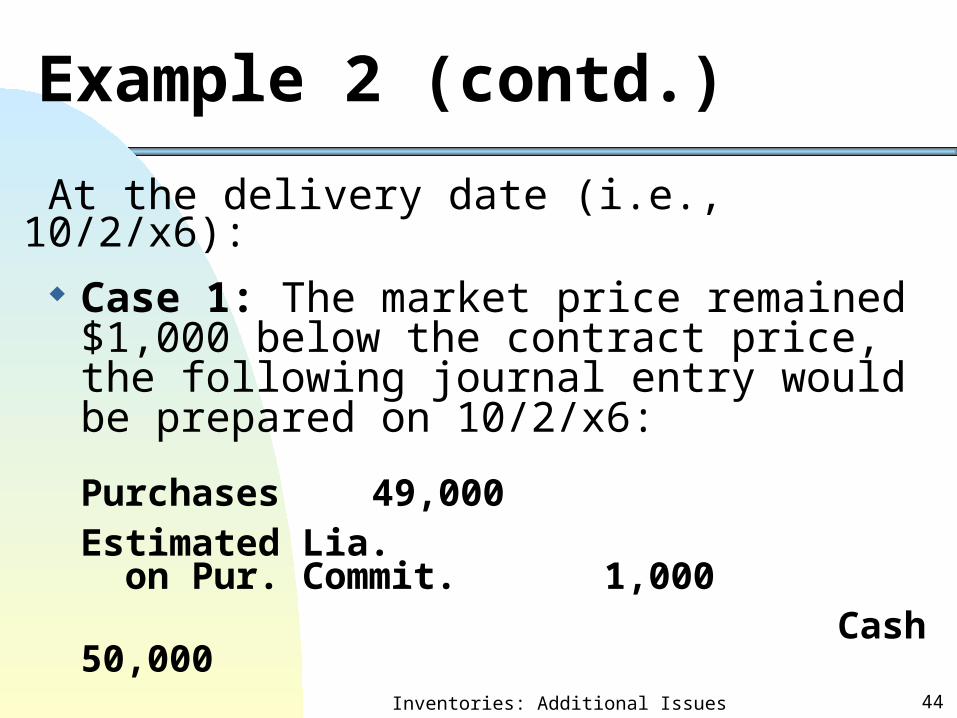

Example 2 (contd.)

At the delivery date (i.e., 10/2/x6): Case 1: The market price remained

$1,000 below the contract price, the following journal entry would be prepared on 10/2/x6:

Purchases 49,000Estimated Lia. on Pur. Commit. 1,000

Cash50,000

Inventories: Additional Issues 45

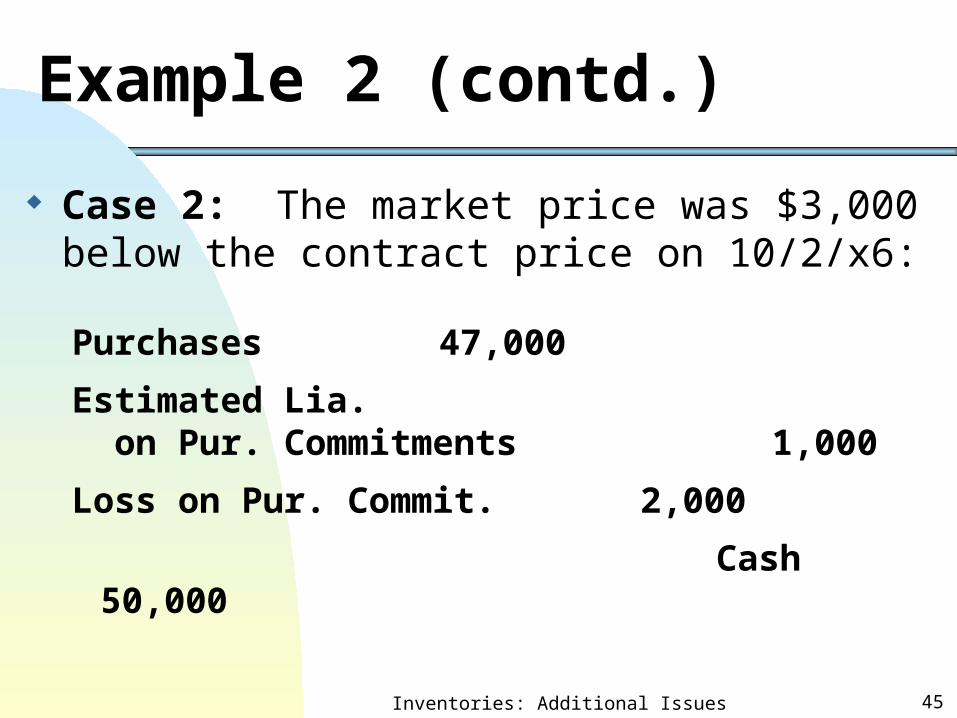

Example 2 (contd.)

Case 2: The market price was $3,000 below the contract price on 10/2/x6:

Purchases 47,000

Estimated Lia. on Pur. Commitments 1,000

Loss on Pur. Commit.2,000

Cash 50,000

Inventories: Additional Issues 46

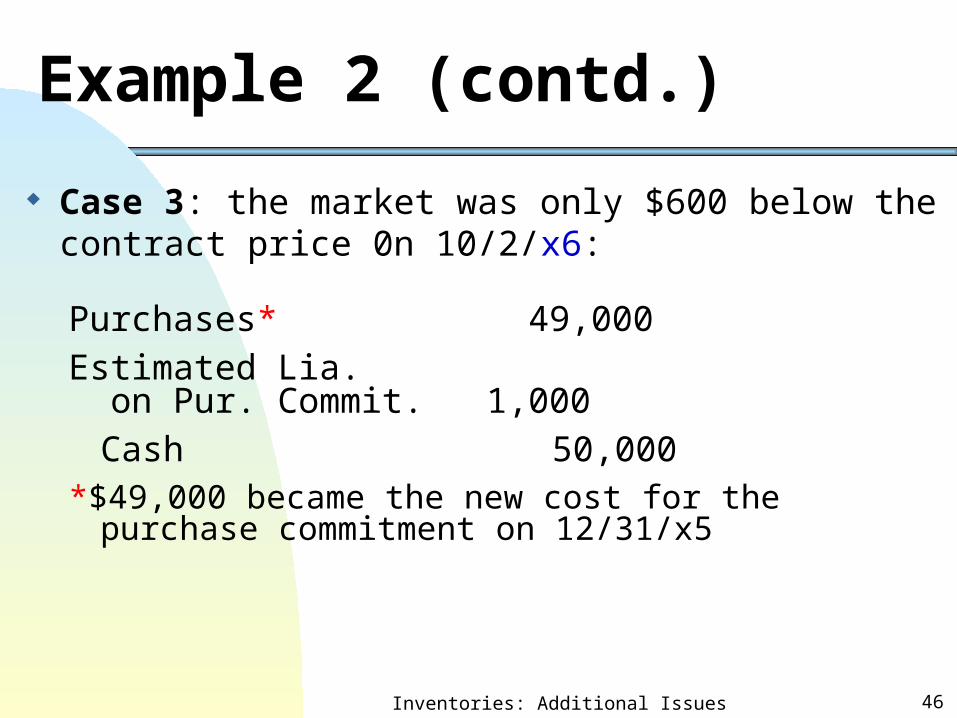

Example 2 (contd.)

Case 3: the market was only $600 below the contract price 0n 10/2/x6:

Purchases* 49,000

Estimated Lia. on Pur. Commit. 1,000

Cash 50,000*$49,000 became the new cost for the purchase

commitment on 12/31/x5

Hedging of Purchase Commitments with Future Sales Contracts In order to offset the potential future

loss on purchase commitments, a firm can enter a future sales contract at the same quantity of inventory purchased in a purchase commitment.

Inventories: Additional Issues 47