Intermediate correction imminent? - Sanjiv Chainani

1

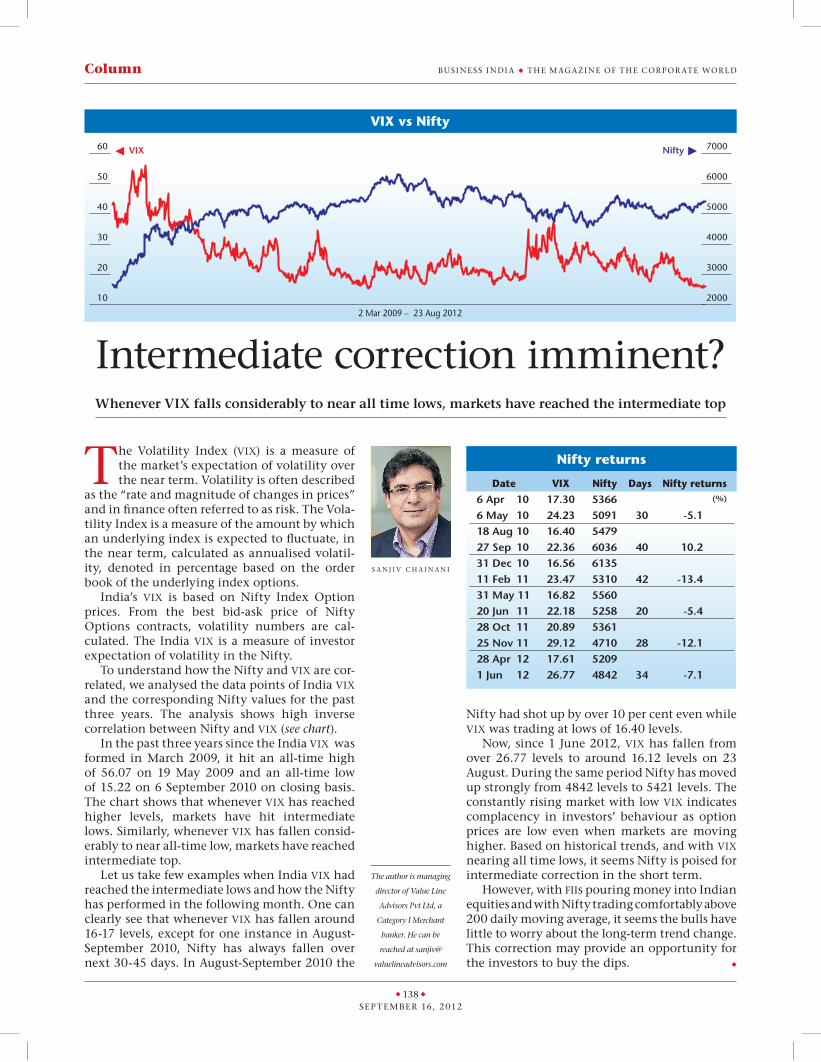

u 138 u SEPTEMBER 16, 2012 BUSINESS INDIA u THE MAGAZINE OF THE CORPORATE WORLD Column Intermediate correction imminent? Whenever VIX falls considerably to near all time lows, markets have reached the intermediate top T he Volatility Index (VIX) is a measure of the market’s expectation of volatility over the near term. Volatility is often described as the “rate and magnitude of changes in prices” and in finance often referred to as risk. The Vola- tility Index is a measure of the amount by which an underlying index is expected to fluctuate, in the near term, calculated as annualised volatil- ity, denoted in percentage based on the order book of the underlying index options. India’s VIX is based on Nifty Index Option prices. From the best bid-ask price of Nifty Options contracts, volatility numbers are cal- culated. The India VIX is a measure of investor expectation of volatility in the Nifty. To understand how the Nifty and VIX are cor- related, we analysed the data points of India VIX and the corresponding Nifty values for the past three years. The analysis shows high inverse correlation between Nifty and VIX (see chart). In the past three years since the India VIX was formed in March 2009, it hit an all-time high of 56.07 on 19 May 2009 and an all-time low of 15.22 on 6 September 2010 on closing basis. The chart shows that whenever VIX has reached higher levels, markets have hit intermediate lows. Similarly, whenever VIX has fallen consid- erably to near all-time low, markets have reached intermediate top. Let us take few examples when India VIX had reached the intermediate lows and how the Nifty has performed in the following month. One can clearly see that whenever VIX has fallen around 16-17 levels, except for one instance in August- September 2010, Nifty has always fallen over next 30-45 days. In August-September 2010 the Nifty had shot up by over 10 per cent even while VIX was trading at lows of 16.40 levels. Now, since 1 June 2012, VIX has fallen from over 26.77 levels to around 16.12 levels on 23 August. During the same period Nifty has moved up strongly from 4842 levels to 5421 levels. The constantly rising market with low VIX indicates complacency in investors’ behaviour as option prices are low even when markets are moving higher. Based on historical trends, and with VIX nearing all time lows, it seems Nifty is poised for intermediate correction in the short term. However, with FIIs pouring money into Indian equities and with Nifty trading comfortably above 200 daily moving average, it seems the bulls have little to worry about the long-term trend change. This correction may provide an opportunity for the investors to buy the dips. u The author is managing director of Value Line Advisors Pvt Ltd, a Category I Merchant banker. He can be reached at sanjiv@ valuelineadvisors.com SANJIV CHAINANI VIX vs Nifty 2 Mar 2009 – 23 Aug 2012 10 20 30 40 50 60 2000 3000 4000 5000 6000 7000 VIX Nifty Nifty returns Date VIX Nifty Days Nifty returns 6 Apr 10 17.30 5366 6 May 10 24.23 5091 30 -5.1 18 Aug 10 16.40 5479 27 Sep 10 22.36 6036 40 10.2 31 Dec 10 16.56 6135 11 Feb 11 23.47 5310 42 -13.4 31 May 11 16.82 5560 20 Jun 11 22.18 5258 20 -5.4 28 Oct 11 20.89 5361 25 Nov 11 29.12 4710 28 -12.1 28 Apr 12 17.61 5209 1 Jun 12 26.77 4842 34 -7.1 (%)

-

Upload

sanjiv-chainani -

Category

Economy & Finance

-

view

105 -

download

1

Transcript of Intermediate correction imminent? - Sanjiv Chainani

u 138 u

Sep tember 16, 2012

buSi n e SS i n di a u the m aga zi n e of the cor por ate wor ldColumn

intermediate correction imminent?Whenever VIX falls considerably to near all time lows, markets have reached the intermediate top

the Volatility index (vix) is a measure of the market’s expectation of volatility over the near term. Volatility is often described

as the “rate and magnitude of changes in prices” and in finance often referred to as risk. the Vola-tility index is a measure of the amount by which an underlying index is expected to fluctuate, in the near term, calculated as annualised volatil-ity, denoted in percentage based on the order book of the underlying index options.

india’s vix is based on nifty index option prices. from the best bid-ask price of nifty options contracts, volatility numbers are cal-culated. the india vix is a measure of investor expectation of volatility in the nifty.

to understand how the nifty and vix are cor-related, we analysed the data points of india vix and the corresponding nifty values for the past three years. the analysis shows high inverse correlation between nifty and vix (see chart).

in the past three years since the india vix was formed in march 2009, it hit an all-time high of 56.07 on 19 may 2009 and an all-time low of 15.22 on 6 September 2010 on closing basis. the chart shows that whenever vix has reached higher levels, markets have hit intermediate lows. Similarly, whenever vix has fallen consid-erably to near all-time low, markets have reached intermediate top.

let us take few examples when india vix had reached the intermediate lows and how the nifty has performed in the following month. one can clearly see that whenever vix has fallen around 16-17 levels, except for one instance in august-September 2010, nifty has always fallen over next 30-45 days. in august-September 2010 the

nifty had shot up by over 10 per cent even while vix was trading at lows of 16.40 levels.

now, since 1 June 2012, vix has fallen from over 26.77 levels to around 16.12 levels on 23 august. during the same period nifty has moved up strongly from 4842 levels to 5421 levels. the constantly rising market with low vix indicates complacency in investors’ behaviour as option prices are low even when markets are moving higher. based on historical trends, and with vix nearing all time lows, it seems nifty is poised for intermediate correction in the short term.

however, with fiis pouring money into indian equities and with nifty trading comfortably above 200 daily moving average, it seems the bulls have little to worry about the long-term trend change. this correction may provide an opportunity for the investors to buy the dips. u

The author is managing

director of Value Line

Advisors Pvt Ltd, a

Category I Merchant

banker. He can be

reached at sanjiv@

valuelineadvisors.com

S a n J i V c h a i n a n i

VIX vs Nifty

2 Mar 2009 – 23 Aug 2012

10

20

30

40

50

60

2000

3000

4000

5000

6000

7000VIX Nifty

Nifty returns

Date VIX Nifty Days Nifty returns6 Apr 10 17.30 53666 May 10 24.23 5091 30 -5.118 Aug 10 16.40 547927 Sep 10 22.36 6036 40 10.231 Dec 10 16.56 613511 Feb 11 23.47 5310 42 -13.431 May 11 16.82 556020 Jun 11 22.18 5258 20 -5.428 Oct 11 20.89 536125 Nov 11 29.12 4710 28 -12.128 Apr 12 17.61 52091 Jun 12 26.77 4842 34 -7.1

(%)