INTERIM REPORT JANUARY-MARCH 2015 - Saab …¥kan Buskhe President and CEO 24 April 2015 INTERIM...

19

Håkan Buskhe President and CEO 24 April 2015 INTERIM REPORT JANUARY-MARCH 2015 Magnus Örnberg EVP and CFO SAAB NAVIGATING THE NORDICS

Transcript of INTERIM REPORT JANUARY-MARCH 2015 - Saab …¥kan Buskhe President and CEO 24 April 2015 INTERIM...

Håkan Buskhe President and CEO

24 April 2015

INTERIM REPORT JANUARY-MARCH 2015

Magnus Örnberg EVP and CFO

SAAB NAVIGATING THE NORDICS

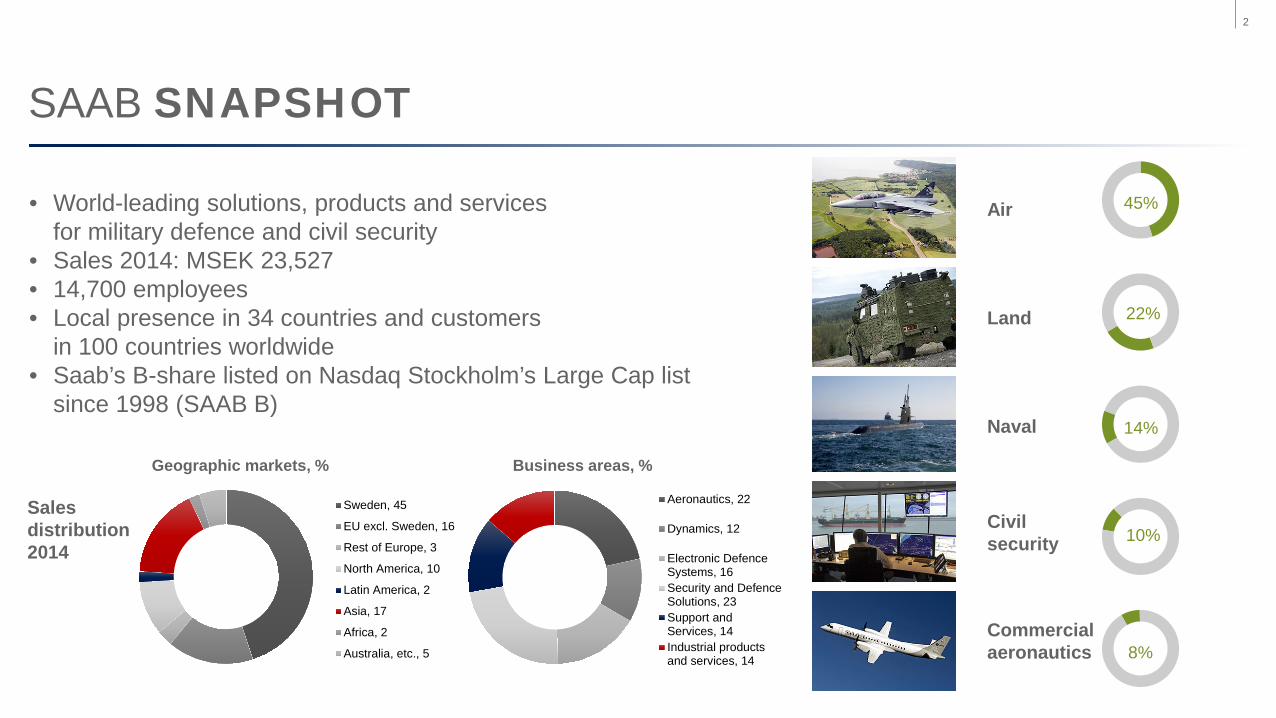

SAAB SNAPSHOT

• World-leading solutions, products and services for military defence and civil security

• Sales 2014: MSEK 23,527 • 14,700 employees • Local presence in 34 countries and customers

in 100 countries worldwide • Saab’s B-share listed on Nasdaq Stockholm’s Large Cap list

since 1998 (SAAB B)

Sales distribution 2014

Sweden, 45

EU excl. Sweden, 16

Rest of Europe, 3

North America, 10

Latin America, 2

Asia, 17

Africa, 2

Australia, etc., 5

Geographic markets, % Business areas, %

Aeronautics, 22

Dynamics, 12

Electronic DefenceSystems, 16Security and DefenceSolutions, 23Support andServices, 14Industrial productsand services, 14

Air

Land

Naval

Civil security

Commercial aeronautics

10%

8%

45%

22%

14%

2

AT THE FOREFRONT OF CHANGE

1941 First B17 delivered

1979 First RBS 15 ordered

1990 First laser simulator BT 46

1961 Viggen introduced

1955 Draken first flight

2002 First contract NLAW

1993 First Gripen delivered

2005 Neuron contract

2006 Saab 2000 A&EW

2008 First flight Gripen Demo

2014 Carl-Gustaf M4 launch

2011 RBS 70 NG launch

3

1990 Saab Automobile independent company

1937 Saab founded

2000 Celsius acquired

2005 Grintek acquired

2007 SeaEye Marine acquired

2012 HITT acquired

2014 TKMS Kockums acquired

1894 Alfred Nobel acquires Bofors

1646 Bofors founded

1948 First Carl-Gustaf order

1998 StriC in operation

1950- Development of fighter radar

1970- Development of Giraffe radar family

1980- Development of Arthur

1990- Sea Giraffe AMB launched

2006 Ericsson Microwave Systems acquired

1987 Celsius

1989 Kockums AB

1999 HDW

2005 ThyssenKrupp

1679 Örlogsvarvet Karlskrona

1840 Kockums Malmö

1977 Svenska Varv

SAAB’S BROAD OFFERING

4

SAAB – ORGANISATION

AERONAUTICS DYNAMICS ELECTRONIC DEFENCE SYSTEMS

SECURITY AND DEFENCE SOLUTIONS

SUPPORT AND SERVICES

INDUSTRIAL PRODUCTS AND SERVICES

BUSINESS AREAS MARKET AREAS

Nordic & Baltic

Latin America

Europe, Middle East

& Africa

Asia Pacific

North America

CEO

GROUP FUNCTIONS

5

GLOBAL DEFENCE MATERIEL MARKET

North America 36%

Latin America 3%

Nordic & Baltic 1%

EMEA3) 27%

Russia1) 4%

China1) 12%

APAC2) 17%

1.0%

2.2%

1.5%

3.0%

1.5%

6.0%

2.7% X%

X%

Share of global defence procurement market, 2016-2020 (constant USD)

Compound annual growth rate, 2016-2020 (constant USD) Source: IHS Group, December 2014

1)Defence market not approached by Saab 2)Excl. China 3)Excl. Russia

6

2015 STARTED ACCORDING TO PLAN

• Order bookings on a good level

• Defence market remains challenging

• Swedish Government announced intention to acquire two A26 submarines

• T-X development according to plan

• Successful deployment of Remote Tower at Örnsköldsvik airport in Sweden

• Contract with Brazil on weapon acquisition for Gripen NG

7

FINANCIAL KEY DATA

MSEK

Jan-Mar

2015 Jan-Mar

2014 Change Full year

2014

Order bookings 4,800 4,078 18% 22,602

Order backlog 59,811 58,608 2% 60,128

Sales 5,389 5,280 2% 23,527

Operating income 210 270 -22% 1,659

Operating margin 3.9% 5.1% 7.1%

Net income 90 176 -49% 1,168

Free cash flow -941 -316 -1,094

8

ORDER BACKLOG

Order backlog duration, SEK bn 31 Mar 2015 31 Dec 2014 31 Mar 2014 2015: 15.1 2015: 17.8 2014: 15.4 2016: 11.1 2016: 10.2 2015: 10.7 2017: 6.2 2017: 5.7 2016: 7.8 2018: 4.6 2018: 5.6 2017: 5.1 After 2018: 22.8 After 2018: 20.8 After 2017: 19.6 Total: 59.8 Total: 60.1 Total: 58.6

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 Q1'15

MSE

K

Order backlog development

60%

40%

Order backlog distribution

SwedenRoW

9

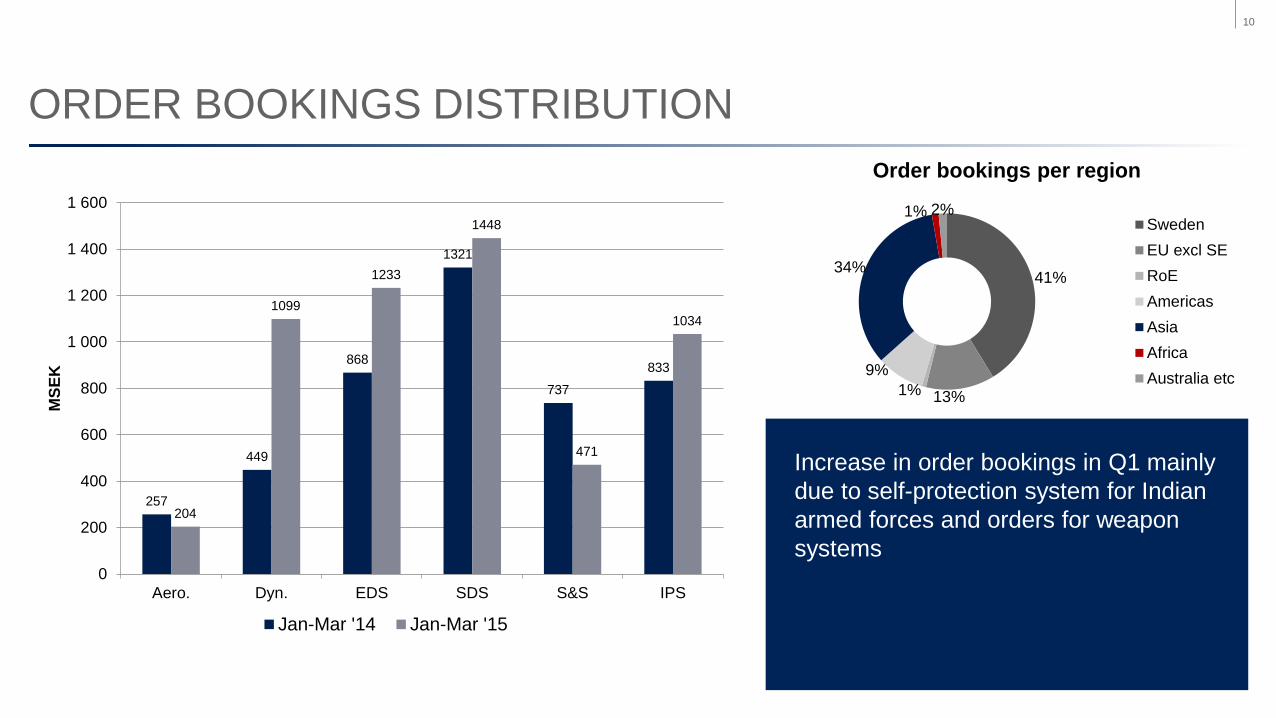

ORDER BOOKINGS DISTRIBUTION

Increase in order bookings in Q1 mainly due to self-protection system for Indian armed forces and orders for weapon systems

257

449

868

1321

737

833

204

1099

1233

1448

471

1034

0

200

400

600

800

1 000

1 200

1 400

1 600

Aero. Dyn. EDS SDS S&S IPS

MSE

K

Jan-Mar '14 Jan-Mar '15

41%

13% 1% 9%

34%

1% 2%

Order bookings per region

SwedenEU excl SERoEAmericasAsiaAfricaAustralia etc

10

SALES 1 328

716

852

1 156

839 787

1 098

628

875

1 292

929 866

0

200

400

600

800

1 000

1 200

1 400

Aero. Dyn. EDS SDS S&S IPS

MSE

K

Jan-Mar '14 Jan-Mar '15

49%

17%

2%

10%

2%

16% 2% 4%

Sales per region Sweden

EU excl SE

RoE

North America

Latin America

Asia

Africa

Australia etc

Aeronautics decrease due to transition from development to production

Increase in SDS mainly related to underwater business

S&S good pace in small and mid-sized projects

11

OPERATING INCOME

107

28

-25

-12

87

12

54

-28

29

64

83

34

-40

-20

0

20

40

60

80

100

120

Aero. Dyn. EDS SDS S&S IPS

MSE

K

Jan-Mar '14 Jan-Mar '15

8.1% 4.9% 3.9% -4.5% -2.9% 3.3% -1.0% 5.0% 10.4% 8.9% 1.5% 3.9%

12

CASH FLOW

Jan-Mar 2015 MSEK Cash flow from operating activities before changes in working capital

340

Change in working capital -920 Investing activities -225 Operational cash flow -805

Tax and other financial items -133 Acquisitions and sale of subsidiaries

-3

Free cash flow -941

-1200

-1000

-800

-600

-400

-200

0

200

400

600

Cash flow from

operating activities before

changes in working capital

Change in working capital

Investing activities

Tax and other

financial item

Acq. and sale of

subsidiaries

13

STRATEGY FOR INNOVATIVE SOLUTIONS

• Come closer to customers in key markets

• Develop innovative solutions in priority product areas with good potential

• Continue to improve efficiency

• Continuously develop leaders and employees while continuing to build a culture that encourages performance, engagement and diversity

14

1995 2000 2005 2010 2015 2020+ 1990

HUNGARIAN AIR FORCE Leased 12 Gripen C and 2 Gripen D

SOUTH AFRICAN AIR FORCE Purchased 17 Gripen C and 9 Gripen D

SWEDISH AIR FORCE Purchased 105 Gripen A and 13 Gripen B

Purchased 75 Gripen C and 25 Gripen D

Purchased 60 Gripen E

Thai Air Force Purchased 8 Gripen C and 4 Gripen D

UK Empire Test Pilot School Leased 1 Gripen D

Czech Republic Air Force Leased 12 Gripen C and 2 Gripen D

Brazilian Air Force Purchased 28 Gripen NG and 8 Gripen F

Slovakian Air Force Selected Gripen

GRIPEN’S WORLDWIDE CUSTOMERS

15 COMPANY RESTRICTED | NOT EXPORT CONTROLLED | NOT CLASSIFIED

© Saab

FINANCIAL GOALS Sales

Average organic sales growth of 5% per year over a business cycle. In 2014, organic sales declined by -3% (-2).

Operating margin

Average operating margin (EBIT) of at least 10% per year over a business cycle. In 2014, the operating margin (EBIT) was 7.1% (5.7).

Equity/assets ratio

The equity/assets ratio will exceed 30%. At year-end 2014, the equity/assets ratio was 38.5% (44.0).

Dividend

The long-term dividend goal is to distribute 20–40% of net income to the shareholders over a business cycle.

0

5

10

15

20

25

'10 '11 '12 '13 '14

SE

K b

n

0%

10%

20%

30%

40%

50%

'10 '11 '12 '13 '140%2%4%6%8%

10%12%14%

'10 '11 '12 '13 '140

1

2

3

4

5

'10 '11 '12 '13 '14

SE

K

16

PROFITABLE GROWTH

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013 2014 2015

SEK

bn

Order backlog development

Incl. order for Gripen to Brazil

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014

SEK

bn

Sales

17

OUTLOOK STATEMENT 2015

• In 2015, we estimate sales to increase more than Saab’s long-term goal: annual organic sales growth of 5 per cent.

• The operating margin 2015 excluding material non-recurring items is expected to be in line with the operating margin in 2014. In 2015, increased internally funded research and development efforts within Aeronautics will have a negative impact on the operating margin.

18