interim consolidated ancial statements...

81

int erim consolidated fin ancial statements March 31, 2000 and 1999 The information of the Financial Statements are available in English, Portuguese and Spanish at our site: http://www.itau.com.br/ri Banco Itaú S.A.

Transcript of interim consolidated ancial statements...

�

interimconsolidated

financialstatementsMarch 31, 2000and 1999

The information of the FinancialStatements are available in English,Portuguese and Spanish at our site:

http://www.itau.com.br/ri

Banco Itaú S.A.

1

Banco Itaú S.A. – Management Report

To our stockholders:

We hereby submit the Management Report and financial statements of Banco Itaú S.A.and its subsidiaries for the 1st quarter of the year 2000. The presentation of this reportcomplies with the regulations of the Central Bank of Brazil and the Comissão de ValoresMobiliários (the Brazilian Securities and Exchange Commission).

RESULTS AND MARKET CAPITALIZATION

Banco Itaú's consolidated net income totaled R$ 365 million in the quarter, representingannualized 26.1 % return on equity. In comparison with recurring net income for the sameperiod in 1999 (R$ 226 million), a 61.7 % increase was recorded.

It is important to point out that in 2000/first quarter Banco Itaú ran up foreign exchangelosses of R$ 69 million, accounted for in the operating income as resulting from currencydevaluation in Reais of permanent investments abroad. The opposite situation hadoccurred in 1999/first quarter, when the Bank obtained an extraordinary net income of R$535 million from such investments, due to the Brazilian monetary authorities' decision tomodify the foreign exchange policy. As a result, the total net income in that period came toR$ 761 million.

Consolidated net income per batch of one thousand shares of Banco Itaú's capital stocktotaled R$ 3.10, while book value was R$ 51.97. Banco Itaú paid shareholders the amountof R$ 139 million in the form of interest on stockholders’ equity.

At the end of the quarter, the Bank's preferred stock was quoted at R$ 155.00 per batch ofone thousand shares. As a result, Itaú's market capitalization came to R$ 16,566 million,the highest among all of the Latin American banks.

STOCKHOLDERS' EQUITY

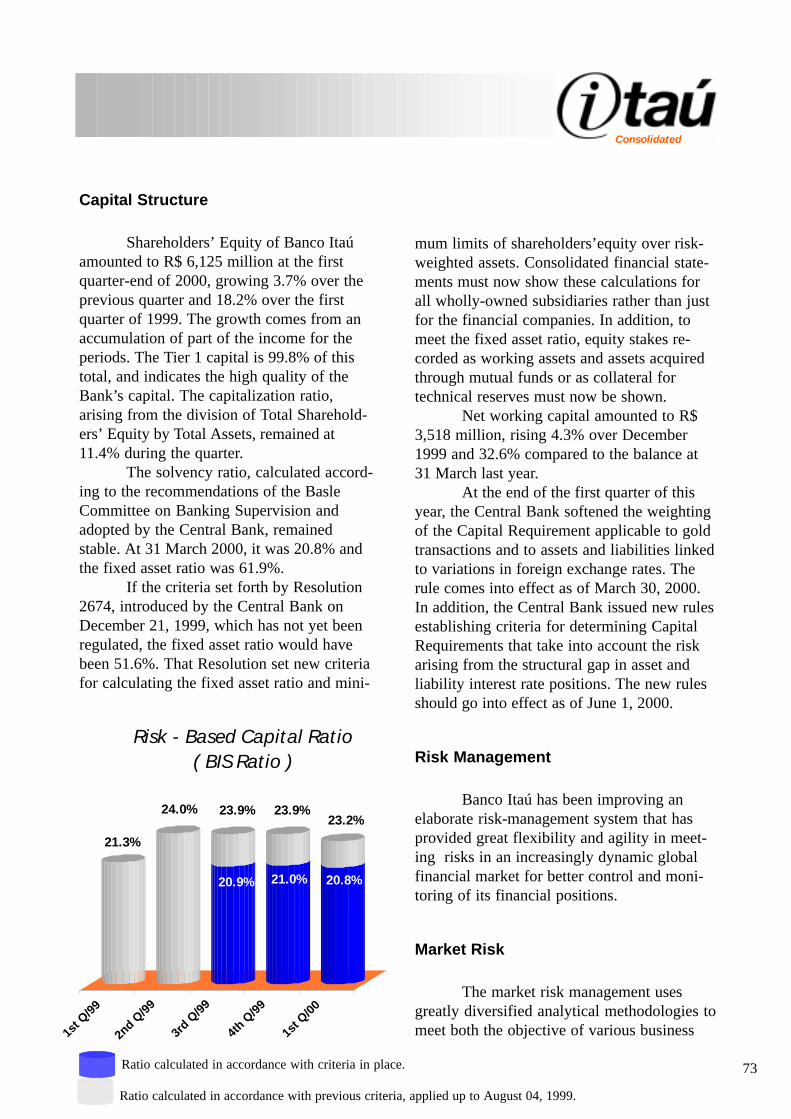

Consolidated stockholders' equity totaled R$ 6,125 million at the end of the period, an 18.2% increase over March 1999. Own working capital, totaling R$ 3,518 million and the 20.8% risk-based capital ratio attest to Itaú's sound financial structure.

Banco Itaú's fixed-asset ratio corresponded to 61.9 %, at the end of the period, well belowthe maximum 80% allowed by the Central Bank of Brazil. Had the new criteria set forth inthe Central Bank's Resolution 2,674 been adopted — such Resolution has not yet beenofficially approved —, basically allowing the inclusion of stock investments registered inthe bank's own portfolio or through investment funds, and the use of consolidated resultsof subsidiaries, then the index would have corresponded to 51.7 %. As for theconsolidated results of the financial companies, the index would have corresponded to67.1 %.

2

FUNDING AND RESOURCES UNDER MANAGEMENT

Banco Itaú's own free resources added to those raised or managed amounted to aconsolidated R$ 77,366 million at the end of the quarter. This figure is 12.7 % higher thanthe one recorded for March 1999. Of this amount, R$ 34,135 million corresponds toinvestment funds and other resources under management, which in turn increased by 32.4%.

Banco Itaú and Banco Matrix entered into a partnership for the co-management of 48funds hitherto managed by Matrix, in Brazil and abroad, the assets of which amount to R$1,800 million. Itaú assumed the direct management of these funds with the objective ofsupplementing, diversifying and broadening its derivatives fund portfolio, withoutincreasing the operating costs. The related value has not been consolidated into Itaú'sfigures yet because there are still bureaucratic procedures to be complied with.Banco Itaú, through its Grand Cayman branch, carried out two Eurobond placements onthe international market in the year 2000. The last such issue was on April 13, andamounted to US$ 150 million, maturing in one year, with an 8.0 % coupon/ year. Theissue was launched at a discount, representing a final yield of 8.08 % a year for investors,corresponding to 166 basic points above one-year Treasuries. Ever since the Asian crisis,this was the lowest cost registered for a foreign funding transaction for such maturity term.

ASSETS AND LOANS

Itaú's consolidated assets at the end of the quarter amounted to R$ 54,094 million.

The consolidated portfolio of loans, leasing operations, advances, guarantees, and creditgranting operations amounted to R$ 20,241 million, an 11.5 % increase in comparison withMarch 1999. The portfolio totaled R$ 28,668 million, when investments in securities issuedby companies, including financial ones, were added to the former amount, correspondingto a 20.1 % increase over March 1999.

The total value of securities issued by the National Treasury or the Central Bankcorresponded to R$ 9,738 million at the end of the quarter, confirming the Bank's highliquidity level.

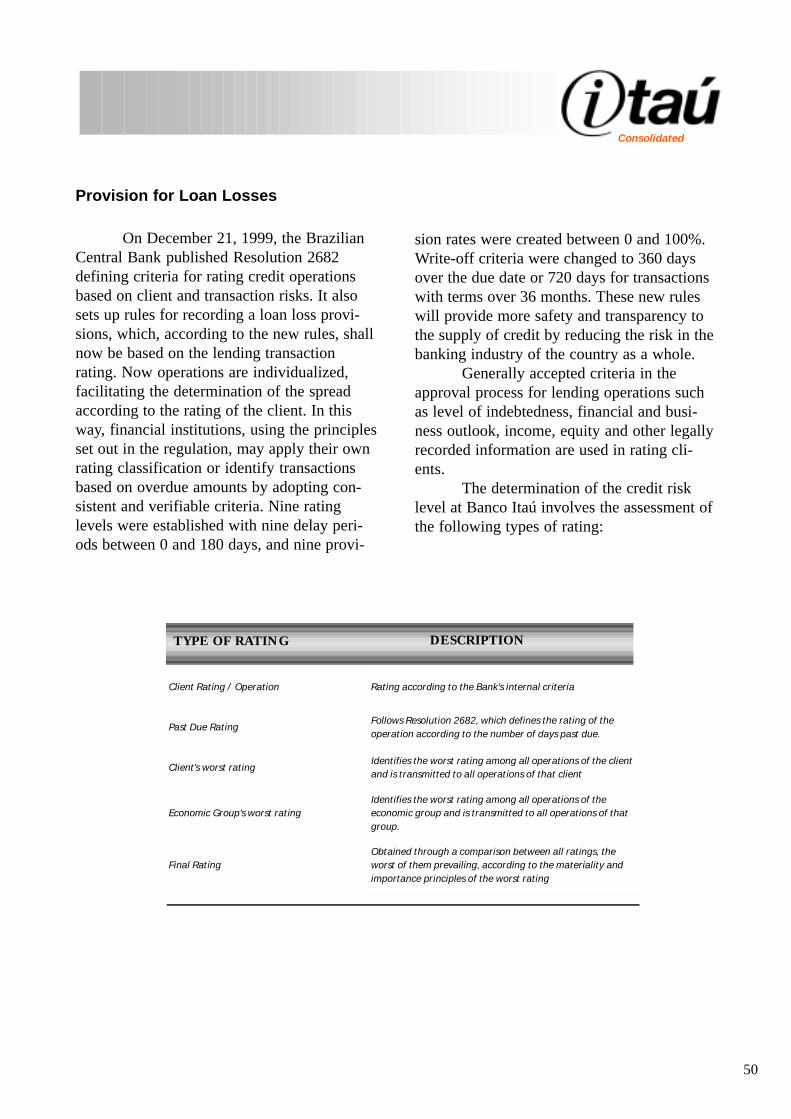

CREDIT RISK POLICY

According to the Central Bank's Resolution 2,682, Banco Itaú started to classify credit risksbased on assessments of customers and operations. The object was to make provisionfor credit losses. On the balance sheet, the provision in excess, above the minimumrequired amount, was R$ 625 million. On the income statement, provision for credit losses,net of credit recoveries, had an impact of R$ 61 million on the quarter's result, dropping byR$ 168 million, when compared with the same period in 1999.

The current credit process, coupled with the more stable macroeconomic scenariopredicted for this year, will permit the expansion of the credit portfolios, while maintainingthe same liquidity level.

3

INTERNET

New sites, focusing on specific needs and segments were made available this quarter, inline with Itaú's investments in the Internet for the benefit of the bank's clients. The newsites are: (1) Small-sized Companies, which provides products and services for thisimportant segment of the economy; (2) Itaú Investnet Personnalité, which provides ItaúPersonnalité clients with access to information, simulations and the management of theirinvestments; and (3) Investor Relations, which facilitates the obtaining of the bank'scorporate data by its shareholders and institutional investors.

In addition to the ongoing improvement of the Bank's other sites and of Itaú BanklineInternet, Itaú's customers have two new services at their disposal: Itaú i-Mail and Itaú i-Cellbank, through which they can get their current and savings account balances andstatements by e-mail and mobile phone. Itaú is actively and continuously analyzingpartnership alternatives in the Internet business.

HUMAN RESOURCES

Banco Itaú and its subsidiary companies employed 39,072 people at the end of thequarter. Payroll (fixed and variable remuneration), plus social charges and benefits,totaled R$ 517 million. The Bank’s employee benefits accounted for R$ 38 million of thisamount. The Plano de Aposentadoria Complementar (Supplementary Retirement Plan),offered by Fundação Itaubanco, deserves to be mentioned. These figures indicate monthlyaverage wages and social charges of R$ 4,000 per employee in the quarter.

AUDIT COMMITTEE

After the Internal Control Committee was set up as a statutory body, in 1999, BancoItaú S.A's General and Extraordinary Shareholders' Meeting, held on April 24, decidedto set up the Statutory Audit Committee. This decision was in line with themanagement, transparency and corporate governance process. The following peoplewere elected as full members of the Statutory Audit Committee:

! Gustavo Jorge Laboissiere Loyola (Graduate Degree in Economics from theUniversity of Brasília, Master's and Doctorate Degree in Economics from FundaçãoGetúlio Vargas, former president of the Central Bank of Brazil.);

! Iran Siqueira Lima (Economist and accountant, Ph.D. Degree in comptrolling andaccounting from the University of São Paulo, former director of the Central Bank ofBrazil); and

! Alberto Sozin Furuguem (Economist, former director of the Central Bank of Brazil).

The three new members are highly qualified professionals, with renowned expertise onthe financial market.

4

The Statutory Audit Committee will be installed and the members will take office assoon as the Central Bank of Brazil approves the decisions of the General ShareholdersMeeting.

ANNOUNCEMENT

It is with great regret that we record the death of Olavo Franco Bueno Júnior, Senior VicePresident and Member of the Board of Directors of Banco Itaú, who passed away on April1, 2000. Mr. Bueno's professional career with the Itaú Group spanned a period of morethan 30 years. During the time he worked for the Bank, he was able to show his uniqueprofessional talents and dedication in all the positions he held or on missions that he wasasked to undertake. In the last five years, he successfully modernized and restructured theFinancial Area, adapting it to today's complex financial world and, once again, remindingus of his outstanding qualities.

We also regret to announce the death of Professor Américo Oswaldo Campíglia, acolleague who was Chief Executive Officer of “Itaucred” from 1952 to 1988 and a Memberof the Bank's Advisory Board since 1988.

We regret the inestimable loss of our tireless companions with whom we spent years offruitful cooperation.

ACKNOWLEDGEMENTS

We would like to thank our shareholders for their indispensable trust and support for theon-going growth achieved by Itaú. We would also like to acknowledge the work of ouremployees and collaborators and thank them for their efforts, which have allowed the Bankto obtain impressive results, and constantly improve its products and services. Our specialthanks go to our customers for their trust and loyalty, which we have always made a pointof rewarding by offering high quality and conveniently differentiated services that meettheir financial servicing requirements.

(Approved at the Meeting of the Board of Directors on May 8, 2000)

5

2000 1999

Current and long term assets 51.091.878 51.661.597 Cash and cash equivalents 1.496.118 2.003.007 Interbank funds applied 4.013.295 8.039.317

Money market 2.256.735 5.488.083 Interbank deposits 1.756.560 2.556.694 Valuation Allowance - (5.460)

Securities 15.830.564 13.693.154 Own portfolio 14.070.863 12.678.137 Subject to repurchase commitments 1.988.046 1.106.796 Subject to forward commitments:

Open contracts and premiums 11.284 77.401 Subject to External Funding 228.578 - Deposited with the Central Bank 324.473 608.788 Privatization certificates 95.894 2 Valuation allowance (888.574) (777.970)

Interbank accounts 6.367.653 6.658.072 Pending settlements 2.225.729 3.057.280 Compulsory deposits:

Central Bank deposits 4.078.068 3.535.248 National Housing System 63.527 63.773

Interbank repasses - 338 Correspondents 329 1.433

Interbranch accounts 3.333 1.342 Third party funds in transit 1.569 882 Own funds in transit 1.764 460

Loan operations 13.890.694 12.673.272 Loans:

Public sector 619.170 185.457 Private sector 14.503.757 13.741.084 (Allowance for loan losses) (1.232.233) (1.253.269)

Leasing operations 554.328 397.575 Lease receivables:

Public sector - 1.859 Private sector 588.574 450.600 (Allowance for lease losses) (34.246) (54.884)

Other receivables 8.550.802 7.735.309 Foreign exchange portfolio 3.117.351 2.703.583 Income receivable 468.685 525.961 Securities clearing accounts 632.754 571.495 Specific Credits 3.518 5.531 Other 4.349.403 3.953.823 (Allowance for losses) (20.909) (25.084)

Other assets 385.091 460.549 Short-term investments 3.993 2.875 Assets received in settlement of debt 323.112 233.498 (Valuation allowance) (151.725) (68.087) Prepaid expenses 209.711 292.263

Permanent assets 3.001.663 2.883.366 Investments 594.054 477.559

Subsidiaries and affiliates: Domestic 173.903 125.444 Foreign 142.443 87.651

Other investments 282.436 273.117 (Allowance for losses) (4.728) (8.653)

Fixed assets 2.225.649 2.288.344 Property for own use 2.473.296 2.504.034 Other fixed assets for own use 1.676.843 1.516.090 Accumulated depreciation (1.924.490) (1.731.780)

Deferred expenses 181.960 117.463 Goodwill to be amortized 2.120 865 Deferred installation expenses 317.617 215.528 Accumulated amortization (137.777) (98.930)

Total assets 54.093.541 54.544.963

See the accompanying notes to the financial statements.

Assets

6

Liabilities 2000 1999

Current and long term liabilities 45.527.219 47.144.466 Deposits 22.131.021 21.526.852

Demand deposits 4.163.950 3.373.226 Savings accounts 14.674.345 15.108.061 Interbank deposits 16.696 300.986 Time deposits 3.276.030 2.744.579

Money market repurchase commitments 4.289.307 3.599.380 Own portfolio 2.425.951 1.923.910 Third party portfolio 1.863.356 1.675.470

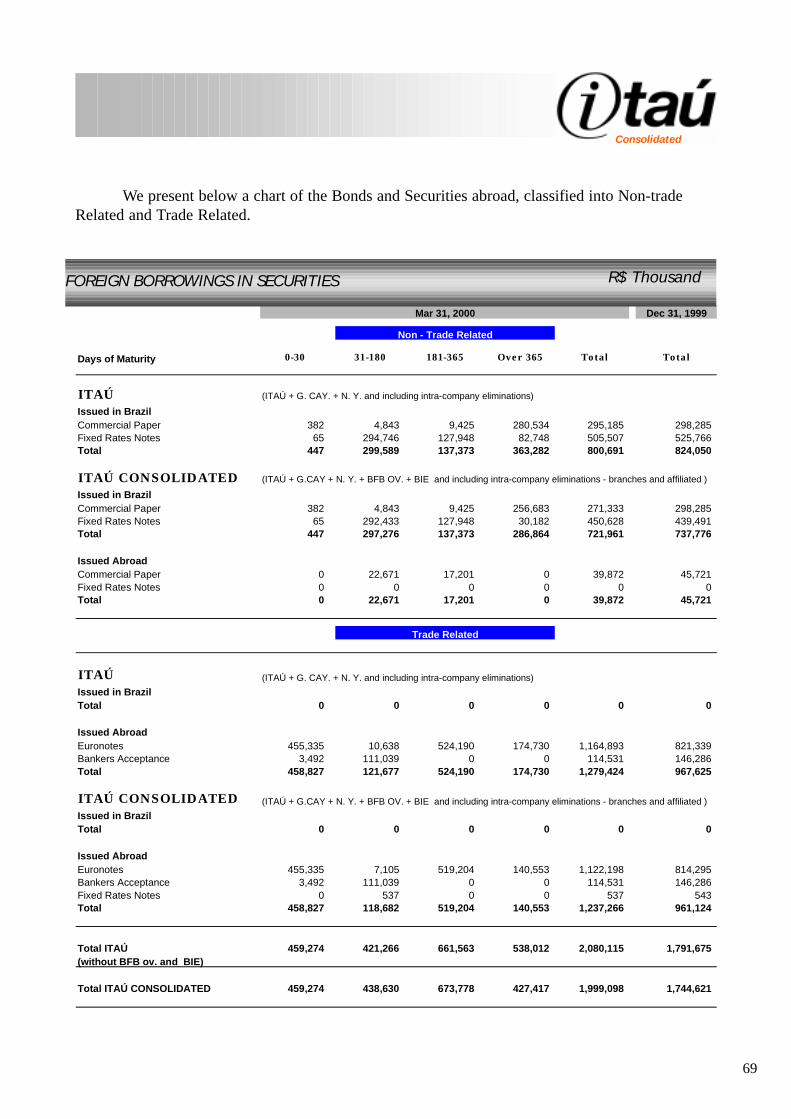

Acceptances and debentures 3.139.584 4.957.250 Debentures 1.140.486 3.228.321 Foreign Borrowings in Securities 1.999.098 1.728.929

Interbank accounts 2.170.674 2.862.944 Pending settlements 2.064.035 2.755.188 Interbank on-lending 1.026 28.092 Correspondents 105.613 79.664

Interbranch accounts 332.899 388.861 Third party funds in transit 321.753 366.045 Own funds in transit 11.146 22.816

Borrowing 3.570.308 4.449.505 Borrowings from domestic - Other institutions 460.748 224.301 Foreign currency trade finance borrowings 3.109.560 4.225.204

On-lending borrowings from public institutions 1.899.840 1.450.451 Federal Development Bank (BNDES) 1.226.497 599.597 CEF 1 1 Federal Capital Goods Financing Agency (FINAME) 672.535 849.919 Other institutions 807 934

Foreign currency on-lending borrowings 161 - Foreign currency on-lending borrowings 161 -

Other liabilities 7.993.425 7.909.223 Collection of taxes and contributions 456.771 964.757 Foreign exchange portfolio 1.989.092 1.243.042 Corporate and statutory contributions 174.200 230.326 Taxes and social security contributions 817.239 857.208 Due in connection with securities dealing 503.904 875.036 Technical provision of insurance, pension plans and capitalization operations - Vinculated 331.980 250.652 Financial and development funds 98 104 Others 3.720.141 3.488.098

Technical provision of insurance, pension plans and capitalization operations - Not vinculated 1.904.201 1.750.178

Deferred income 142.581 113.699 Deferred income 142.581 113.699

Minority interest in consolidated subsidiaries 394.722 354.708

Stockholders' equity 6.124.818 5.181.912 Capital:

Domestic 1.975.208 1.603.721 Foreign 524.792 396.279

Capital reserves 264.394 415.770 Revaluation reserves 12.434 15.461 Retained income 3.458.703 2.852.647 (Treasury shares) (110.713) (101.966)

Total liabilities 54.093.541 54.544.963

7

2000 1999

Income from financial operations 1.964.933 3.388.469

Loans 901.801 1.400.369 Leases 144.630 166.485 Securities portfolio 862.624 1.709.370 Trade finance and foreign exchange portfolio 7.351 22.981 Compulsory deposits 48.527 89.264

Expenses of financial operations (938.717) (2.474.163)

Deposits, money market and interbank funds (588.277) (1.548.320) Borrowings and on-lending (81.721) (520.798) Leases (115.967) (105.824) Provision for loan losses (152.752) (299.221)

Net income from financial operations 1.026.216 914.306

Other operating income (expenses) (486.285) (475.687)

Banking service fees 801.635 696.519 Capitalization, insurance and pension plans premiums 465.884 456.090 Expenses in constituting technical provisions of insurance, (103.480) (83.789) capitalization and pension plan operations Insurance claims (181.952) (235.913) Selling expenses - Insurance (50.260) (57.863) Pension plan benefits expense (41.796) (28.361) Salaries and employee benefits (516.626) (474.968) Other administrative expenses (639.026) (574.900) Tax expenses (141.141) (154.898) Equity share in income of subsidiaries and affiliates (53.074) 31.931 Other operating income 99.786 184.543 Other operating expenses (126.235) (234.078)

Operating income 539.931 438.619

Non operating income 9.884 (2.523)

Income before income tax and social contribution and profit sharing 549.815 436.096

Income tax and social contribution Due on operations for the years (162.055) (299.993) Deferred related to temporary additions 3.864 169.926

Extraordinary results - 534.683

Profit sharing (28.531) (22.547)

E Employees (23.150) (19.298) D Directors - Statutories (5.381) (3.249)

Minority interest 2.182 (57.565)

Net income 365.275 760.600

Number of outstanding shares 117.844.337.341 117.803.569.740 (*)Net income per thousand shares - R$ 3,10 6,46Stockholders' equity per thousand shares - R$ 51,97 43,99

(*) Number of shares adjusted for better comparability due to the split performed in 1999

See the accompanying notes to the financial statements.

8

Three-month periods ended March 31, 2000 and 1999

(In thousands of reais)

1 Presentation of the financial statements

The consolidated financial statements of Banco Itaú S.A. and its subsidiaries (ITAÚCONSOLIDATED) have been prepared in accordance with accounting practices derived fromthe Brazilian Corporation Law and instructions issued by the Brazilian Securities and ExchangeCommission (CVM) and the Central Bank of Brazil (BACEN), which include the use ofestimates necessary to calculate accounting provisions.

2 Consolidated companies

The consolidated financial statements include Banco Itaú S.A. (ITAÚ) and its direct and indirectsubsidiaries, including those listed below:

Participation %

Financial institutions 03/31/2000 03/31/1999

Banco Banerj S.A. and subsidiaries 99.99 99.99Banco Bemge S.A. and subsidiaries 99.85 99.85Banco del Buen Ayre S.A. (a) - 99.49Banco Francês e Brasileiro S.A. 100.00 100.00Banco Itaú Buen Ayre S.A. (b) 99.99 100.00Banco Itaú Europa Luxembourg S.A. and subsidiaries (c) 24.57 24.60Banco Itaú Europa, S.A. and subsidiaries (c) 24.59 24.62BFB Leasing S.A. Arrendamento Mercantil 99.99 99.99Cia. Itauleasing de Arrendamento Mercantil 99.99 99.99Itaú Banco de Investimento S.A. 99.99 99.99Itau Bank, Ltd. 100.00 100.00Itauvest Banco de Investimento S.A. and subsidiaries (d) 100.00 53.75Itaú Corretora de Valores S.A. 99.99 99.99Intrag Distribuidora de Títulos e Valores Mobiliários Ltda. (e) 99.99 -

9

Non-financial institutions

Afinco Ltda. and subsidiaries 99.88 99.99Armazéns Gerais Itaú Ltda. 99.78 99.78Credicard S.A. Administradora de Cartões de Crédito andsubsidiaries (f) 33.28 33.33Redecard S.A. (f) 31.89 32.02Itaú Capitalização S.A. and subsidiaries 99.85 99.99Itaucard Administradora de Cartões de Crédito e Imobiliária Ltda. 99.85 99.99Itaú Gráfica Ltda. 99.85 99.99Itaú Previdência e Seguros S.A. 99.85 99.99Itaú Rent Administração e Participações S.A. 99.85 99.99Itaú Seguros S.A. and subsidiaries 95.83 95.98Itaúsa Export S.A. and subsidiaries (c) 27.98 28.03

(a) The investment was incorporated by Banco Itaú Argentina S.A. on October 5, 1999.(b) New name of Banco Itaú Argentina S.A., after incorporation of Banco del Buen Ayre S.A.(c) Subsidiaries included in the consolidation, with the authorization of the Brazilian Securites and

Exchange Comission (CVM) to better present the business of the Group. Subsidiaries controlled byItaúsa - Investimentos Itaú S.A. (ITAÚSA).

(d) New name of Itaú Bankers Trust Banco de Investimento S.A. - IBT which since September 10, 1999 isfully controlled by ITAÚ.

(e) The investment was acquired from ITAUSA on August 31, 1999.(f) The investments are proportionally included in the consolidation financial statements.

3 Summary of significant accounting practices

a. Basis of consolidation

All material intercompany profits, transactions and balances have been eliminated onconsolidation.

10

b. Securities

Securities are recorded at the lower of price-level restated cost and adjusted by a provision toreflect its market value.

c. Interbank funds applied, loan operations, traded receivable discounted, financingremunerated deposits, money market repurchase commitments and otherreceivables and payables

Transactions subject to monetary correction or foreign exchange rates are recorded at presentvalue calculated “pro rata die” based on the variation of the contractual index. Real estateloans are adjusted to present value based on the discounted cash flow of future installments.Transactions with predetermined remuneration rates are recorded at their redemption value,adjusted for any unearned income/expenses.

d. Allowance for loan losses

The balance of the allowance for loan losses was constituted based on an analysis of creditrisk in the loan portfolio in amounts considered sufficient to cover possible losses.

e. Fixed assets

Fixed assets are stated at cost of acquisition or construction less accumulated depreciation,monetarily corrected at December 31, 1995. For insurance, pension plan and capitalizationsubsidiaries, fixed assets are adjusted to market value, through revaluations supported byappraisal reports. Depreciation and amortization are recorded using the straight line method,based on monetarily corrected cost over the useful lives of depreciable assets at thefollowing annual rates:

%Buildings used in operations 4Installations, furnishings, equipment and Security and communications systems 10 to 25EDP systems 20 to 50

11

f. Deferred expenses

Deferred organization and expansion expenses represent improvements in third partyproperties and are amortized linearly amortized over the respectively rental periods, andacquisition and development of logistic, which are amortized on a straight-line basis in fiveyears.

g. Income tax, social contribution, PIS and COFINS

The provisions were calculated utilizing the appropriate calculation base consideringpertinent legislation for each tax at the rates shown below:

03/31/2000 03/31/1999

Income tax 15.00% 15.00%Additional income tax 10.00% 10.00%Social contribution 8.00% 8.00%Additional social contribution 1.00% (*) -PIS 0.65% 0.65%COFINS 3.00% 3.00%

(*) Effective until December 31, 2002. Since February 1, 2000, the additional was decreased from 4% to 1%.

Amounts subject to litigation have been fully provided.

(In thousands of reais)

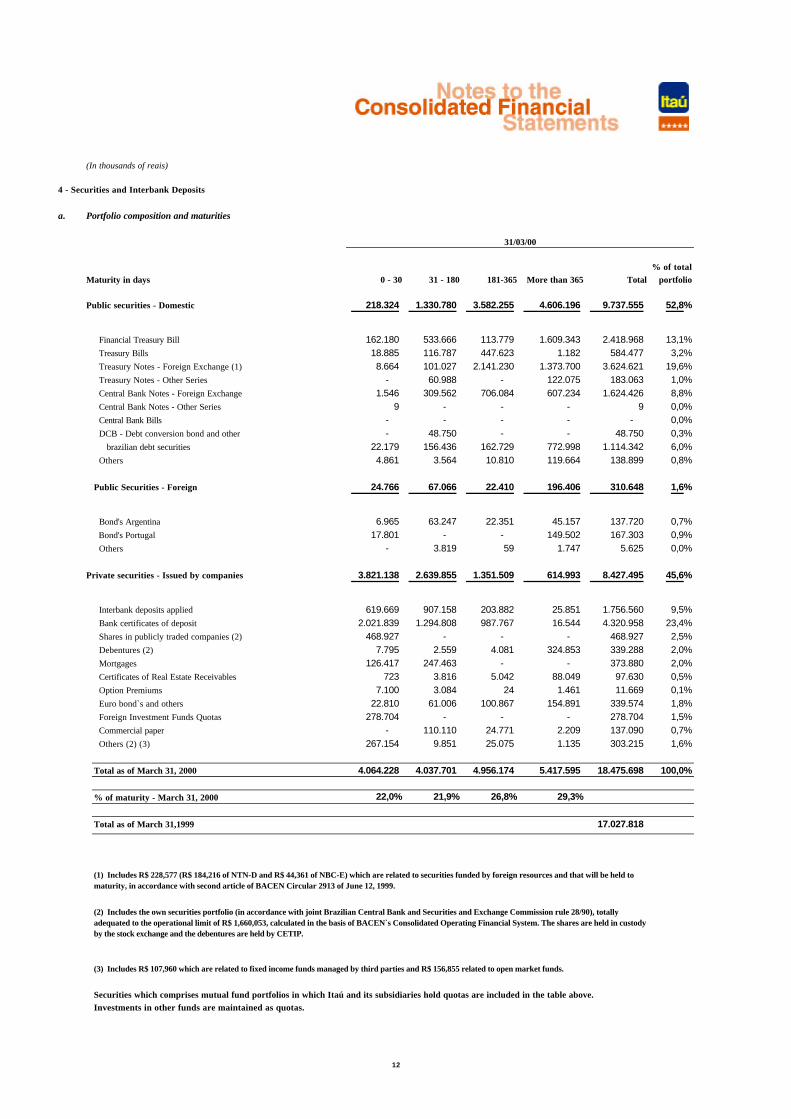

4 - Securities and Interbank Deposits

a. Portfolio composition and maturities

% of totalMaturity in days 0 - 30 31 - 180 181-365 More than 365 Total portfolio

Public securities - Domestic 218.324 1.330.780 3.582.255 4.606.196 9.737.555 52,8%

Financial Treasury Bill 162.180 533.666 113.779 1.609.343 2.418.968 13,1% Treasury Bills 18.885 116.787 447.623 1.182 584.477 3,2% Treasury Notes - Foreign Exchange (1) 8.664 101.027 2.141.230 1.373.700 3.624.621 19,6% Treasury Notes - Other Series - 60.988 - 122.075 183.063 1,0% Central Bank Notes - Foreign Exchange 1.546 309.562 706.084 607.234 1.624.426 8,8% Central Bank Notes - Other Series 9 - - - 9 0,0% Central Bank Bills - - - - - 0,0% DCB - Debt conversion bond and other - 48.750 - - 48.750 0,3% brazilian debt securities 22.179 156.436 162.729 772.998 1.114.342 6,0% Others 4.861 3.564 10.810 119.664 138.899 0,8%

ForeignPublic Securities - Foreign 24.766 67.066 22.410 196.406 310.648 1,6%

Bond's Argentina 6.965 63.247 22.351 45.157 137.720 0,7% Bond's Portugal 17.801 - - 149.502 167.303 0,9% Others - 3.819 59 1.747 5.625 0,0%

Private securities - Issued by companies 3.821.138 2.639.855 1.351.509 614.993 8.427.495 45,6%

Interbank deposits applied 619.669 907.158 203.882 25.851 1.756.560 9,5% Bank certificates of deposit 2.021.839 1.294.808 987.767 16.544 4.320.958 23,4% Shares in publicly traded companies (2) 468.927 - - - 468.927 2,5% Debentures (2) 7.795 2.559 4.081 324.853 339.288 2,0% Mortgages 126.417 247.463 - - 373.880 2,0% Certificates of Real Estate Receivables 723 3.816 5.042 88.049 97.630 0,5% Option Premiums 7.100 3.084 24 1.461 11.669 0,1% Euro bond`s and others 22.810 61.006 100.867 154.891 339.574 1,8% Foreign Investment Funds Quotas 278.704 - - - 278.704 1,5% Commercial paper - 110.110 24.771 2.209 137.090 0,7% Others (2) (3) 267.154 9.851 25.075 1.135 303.215 1,6%

Total as of March 31, 2000 4.064.228 4.037.701 4.956.174 5.417.595 18.475.698 100,0%

% of maturity - March 31, 2000 22,0% 21,9% 26,8% 29,3%

Total as of March 31,1999 17.027.818

Securities which comprises mutual fund portfolios in which Itaú and its subsidiaries hold quotas are included in the table above. Investments in other funds are maintained as quotas.

31/03/00

(2) Includes the own securities portfolio (in accordance with joint Brazilian Central Bank and Securities and Exchange Commission rule 28/90), totally adequated to the operational limit of R$ 1,660,053, calculated in the basis of BACEN`s Consolidated Operating Financial System. The shares are held in custody by the stock exchange and the debentures are held by CETIP.

(1) Includes R$ 228,577 (R$ 184,216 of NTN-D and R$ 44,361 of NBC-E) which are related to securities funded by foreign resources and that will be held to maturity, in accordance with second article of BACEN Circular 2913 of June 12, 1999.

(3) Includes R$ 107,960 which are related to fixed income funds managed by third parties and R$ 156,855 related to open market funds.

12

13

b. Changes in the valuation allowance for securities

Balances as of December 31, 1998 271,526Provisions 128,190Write-offs: (126,173)• Reversals (21,477)• Losses for sales ( 104,696)

Balances as of March 31, 1999 273,543Additional provision (*) 509,887

Balances as of March 31, 1999 with the additional provision 783,430

Balances as of December 31, 1999 156,401Write-offs: ( 13,727)! Reversals ( 11,695)! Losses for sales ( 2,032)

Balances as of March 31, 2000 142,674Additional provision (*) 745,900

Balances as of December 31, 2000 with the additional provision 888,574

(*) Additional provisions were constituted to cover the risk of future price fluctuations.

c. Summary

03/31/2000 03/31/1999

Securities and interbank deposits 18,475,698 17,027,818Valuation allowance ( 888,574) ( 783,430)

Net book value 17,587,124 16,244,388

14

5 Loan and leasing portfolio

a. Summary

03/31/2000 03/31/1999

Loan and leasing operations 15,711,501 14,379,000Other receivables (1) 168,491 153,879Advances on exchange contracts (2) 1,512,988 1,314,184

Total 17,392,980 15,847,063

Endorsements and sureties (3) 2,847,560 2,302,048

Total with endorsements and sureties 20,240,540 18,149,111

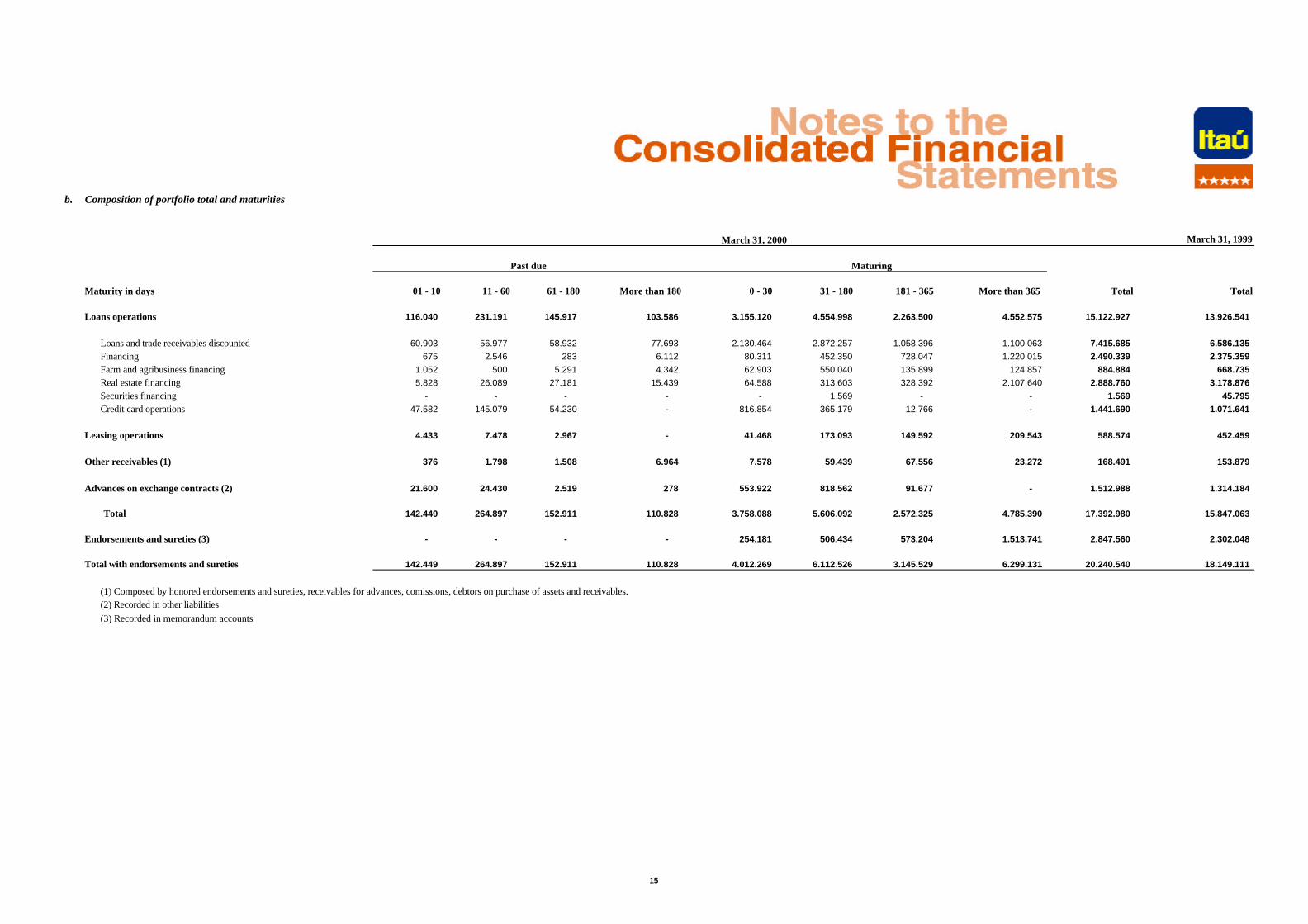

(1) Composed by honored endorsements and sureties, receivable for advances, comissions, debtors on purchase of assets and receivables.

(2) Advances on exchange contracts are recorded in other liabilities.

(3) Endorsements and sureties are recorded in memorandum accounts.

b. Composition of portfolio total and maturities

March 31, 1999

Maturity in days 01 - 10 11 - 60 61 - 180 More than 180 0 - 30 31 - 180 181 - 365 More than 365 Total Total

Loans operations 116.040 231.191 145.917 103.586 3.155.120 4.554.998 2.263.500 4.552.575 15.122.927 13.926.541

Loans and trade receivables discounted 60.903 56.977 58.932 77.693 2.130.464 2.872.257 1.058.396 1.100.063 7.415.685 6.586.135 Financing 675 2.546 283 6.112 80.311 452.350 728.047 1.220.015 2.490.339 2.375.359 Farm and agribusiness financing 1.052 500 5.291 4.342 62.903 550.040 135.899 124.857 884.884 668.735 Real estate financing 5.828 26.089 27.181 15.439 64.588 313.603 328.392 2.107.640 2.888.760 3.178.876 Securities financing - - - - - 1.569 - - 1.569 45.795 Credit card operations 47.582 145.079 54.230 - 816.854 365.179 12.766 - 1.441.690 1.071.641

Leasing operations 4.433 7.478 2.967 - 41.468 173.093 149.592 209.543 588.574 452.459

Other receivables (1) 376 1.798 1.508 6.964 7.578 59.439 67.556 23.272 168.491 153.879

Advances on exchange contracts (2) 21.600 24.430 2.519 278 553.922 818.562 91.677 - 1.512.988 1.314.184

Total 142.449 264.897 152.911 110.828 3.758.088 5.606.092 2.572.325 4.785.390 17.392.980 15.847.063

Endorsements and sureties (3) - - - - 254.181 506.434 573.204 1.513.741 2.847.560 2.302.048

Total with endorsements and sureties 142.449 264.897 152.911 110.828 4.012.269 6.112.526 3.145.529 6.299.131 20.240.540 18.149.111

(1) Composed by honored endorsements and sureties, receivables for advances, comissions, debtors on purchase of assets and receivables.(2) Recorded in other liabilities

(3) Recorded in memorandum accounts

Past due Maturing

March 31, 2000

15

16

c. Concentration of credit (*)

Risk % of Total

Largest debtor 695,469 3.420 largest debtors 4,128,400 20.450 largest debtors 6,398,700 31.6100 largest debtors 8,279,648 40.9

(*) Balances include endorsements and sureties.

17

d. Composition of thecredit portfolio by business sector

March 31, 2000

Public sector 695,926

Industry 695,926

Chemicals and petrochemicals 695,469

Others 457

Private sector 19,544,614

Industry 6,140,868

Steel, mettallurgy and heavy industry 1,426,117

Chemicals and petrochemicals 936,232

Food and beverages 1,064,531

Paper and pulp 506,973

Light and heavy vehicles 451,800

Electrical and electronics 426,728

Textiles and clothing 198,754

Autoparts and accessories 121,314

Fertilizers, insecticides, and crop protection 217,747

Pharmaceuticals 98,998

Others 691,674

Commerce 995,777

Services 3,703.855

Financial 1,076,628

Energy, telecommunications, and others 1,453,256

Other 1,173,971

Housing 2,888,760

Individuals 2,487,811

Businesses 400,949

Primary sector 945,932

Farming and livestock 400,353

Mining 545,579

Other - individuals 4,457,372

Credit cards 1,441,690

Other 3,015,682

Other - Businesses 412,050

Total 20,240,540

e. Allowance for loan losses

On December 21, 1999, BACEN introduced new criterion for the classification of creditrights from credit operations and leases through Resolution 2,682 including theestablishment of provisions for loans losses and disclosures of information relating to the

18

portfolio in the notes to the financial statements, these measures have to be applied afterMarch 2000.

The new criteria introduced by this Resolution includes:

• Financial institutions are required to classify loan operations by level of risk, based onconsistent and verifiable criteria.

• Non-accrual loans and overdue loan operations are no longer presented separately in thebalance sheet. The balances at March 31, 1999 have been reclassified for purposes ofcomparison.

• A provision has to be made, once the loans has been provided, based on a periodicanalysis of the quality of the client/loan and not just in the event of default as requiredby the Regulations in force until February 29, 2000.

• Write-offs can only be made 360 days after the due date of the credit or 720 days foroperations that mature after a period of 36 months.

19

Although BACEN Resolution 2697 of February 24, 2000 permits financial institutions to begradually introduced to the criteria of BACEN Resolution 2682, ITAÚ CONSOLIDATED financial statements at March 31, 2000 reflect these criteria, already.

BACEN Circular 2974 of February 24, 2000 provided that the adjustments from thedifference from providing for operations contracted to December 31, 1999, from applyingcriteria established under BACEN Resolutions 2682 and 2697 have to be recorded inretained earnings. The adoption of new criteria by ITAÚ CONSOLIDATED has not resultedin any adjustments to be made in retained earnings.

I - Changes in the allowance for loan losses

Balances as of December 31, 1999 1,253,371

Provisions for the period 152,752Write-offs made up to February 29, 2000 (118,735)

Balances as of March 31, 2000 1,287,388

Specific provision (1) 321,599Generic provision (2) 341,162Excess provision 624,627

(1) For operations for which installments are overdue more than 14 days, with renegotiationmade, or under the responsibility of companies in the process of debt rehabilitation orbankruptcy.

(2) For operations not covered by the previous item, but due to the classification of the client orthe operation.

The balance of the provision at March 31, 2000 was equivalent to 7.4% of the loan portfolio.

20

II - Provision for loan losses by risks level

Risk levelsCredit

portfolioMinimum provision

requiredExcess

provisionExisting

provision

Specific Generic AA 4,906,983 - - A 6,021,657 - 30,104 B 3,506,932 2,284 32,786 C 1,530,268 7,819 38,086 D 723,475 11,686 60,660 E 90,347 26,295 809 F 298,218 40,976 108,132 G 39,920 26,034 1,910 H 275,180 206,505 68,675

Total 17,392,980 321,599 341,162 624,627 1,287,388

III – Main Accounts Comparative, as of March 31, 2000, related to the criteria ofResolutions n° 1748/90 and 2682/99.

Creditportfolio

Non-accrual and

overdueloans (*)

Minimum provisionrequired

Existingprovision (*)

Excessprovision

Specific Generic

Prior situation (Res. 1748) 17,121,513 271,467 271,467 - 1,287,388 1,015,921 Effects of new criteria adoption 271,467 (271,467) 50,132 341,162 - (391,294) Present situation (Res. 2682) 17,392,980 - 321,599 341,162 1,287,388 624,627

(*) Without including the effects of write-offs made on March 2000, amounting to R$ 38,321,which were not made in the accelerated way (61 days after recorded as non-accrual loan) asrequired by Resolution n° 2682/99.

21

f. Credit recoveries offset against the provision for loan losses

Three-month period ended March 31, 1999 70,264

• Renegotiations 24,482

• Receipts 45,782

Three-month period ended March 31, 2000 92,141

• Renegotiations 31,685

• Receipts 60,456

On March 31, 2000, the balances of renegotiated credits amounted to R$ 308.479 (R$ 241.253 inMarch 31, 1999).

6 Investments - Composition

03/31/2000 03/31/1999

Investments in subsidiaries and affiliates:

Domestic 173,903 125,444

Duraflora S.A. (1) 32,259 32,053

Union Carbide do Brasil S.A. (2) 36,082 30,558

AGF Brasil Seguros S.A. 77,196 44,321

Serasa 27,104 17,055

Others 1,262 1,457

Foreign 142,443 87,651

· BPI - SGPS S.A. (BPI) 142,443 87,651

Other investments: 282,436 273,117

Tax incentive investments 217,978 204,398

Equity securities 17,977 16,003

Shares and quotas 26,419 31,030

Others 20,062 21,686(1) Investments arising from tax incentives(2) Investment resulting from the usage of privatization currencies

22

7 Foreign exchange operations

03/31/2000 03/31/1999

Assets - Other receivables 3,117,351 2,703,583

Exchange purchases pending settlement 2,300,321 2,113,081Foreign currency bills exchange and term documents 20,484 19,918Exchange sale rights 1,140,461 710,529(-) Local currency advances received (371,706) (184,728)Income receivable on advances granted 27,791 44,783

Liabilities - Other liabilities 1,989,092 1,243,042

Exchange sales pending settlement 1,138,468 696,269Exchange purchases obligations 2,349,244 1,851,551(-) Advances on exchange contract (1,512,988) (1,314,184)Others 14,368 9,406

Memorandum accountsImport credits outstanding 23,803 39,398

23

8 Income and social contribution taxes

a. Income tax and social contribution due on operations for the period are shown below:

03/31/2000 03/31/1999

Net income before income tax and social contribution 549,815 436,096

Taxes payable (income tax and social contribution ) at rates of 25% e 9% (8%in 1999) respectively (*) (186,937) (143,912)

Increases/Decreases in income tax and socialcontribution payable as the result of:

Permanent (inclusions)/exclusions 44,645 (46,720)

Equity share in income of subsidiaries and affiliates 18,045 10,537

Non-deductible expenses and provisions (20,248) (129,837)

Interest on capital 46,848 72,580

Temporary (inclusions)/exclusions (8,348) (97,111)

Allowance for loan losses 19,084 93,561

Labor provisions, tax contingencies and other expenses (27,432) (190,672)

Other adjustments (11,415) (12,250)

Income tax of foreign branches and subsidiaries (11,415) (12,250)

Income tax and social contribution from operations of the year (162,055) (299,993)

Withholding tax on distribution of interest on capital (20,793) (33,053)

Total income tax and social contribution (182,848) (333,046)

(*) Effective until December 31, 2002. Since February 1, 2000, the additionalwas decreased from 4% to 1%

24

b. The composition of accounting adjustments, which refer to temporary additions to deferredincome and social contribution taxes is shown below:

03/31/2000 03/31/1999

Deferred income tax and socialcontribution related to temporary additions 3,864 169,926

Tax credits Constitution over temporary inclusions/exclusions 3,508 97,111 Constitution over tax loss carry 10,537 83,087 Reversal over initial balance of tax loss carry/write-off and others (10,181) (10,272)

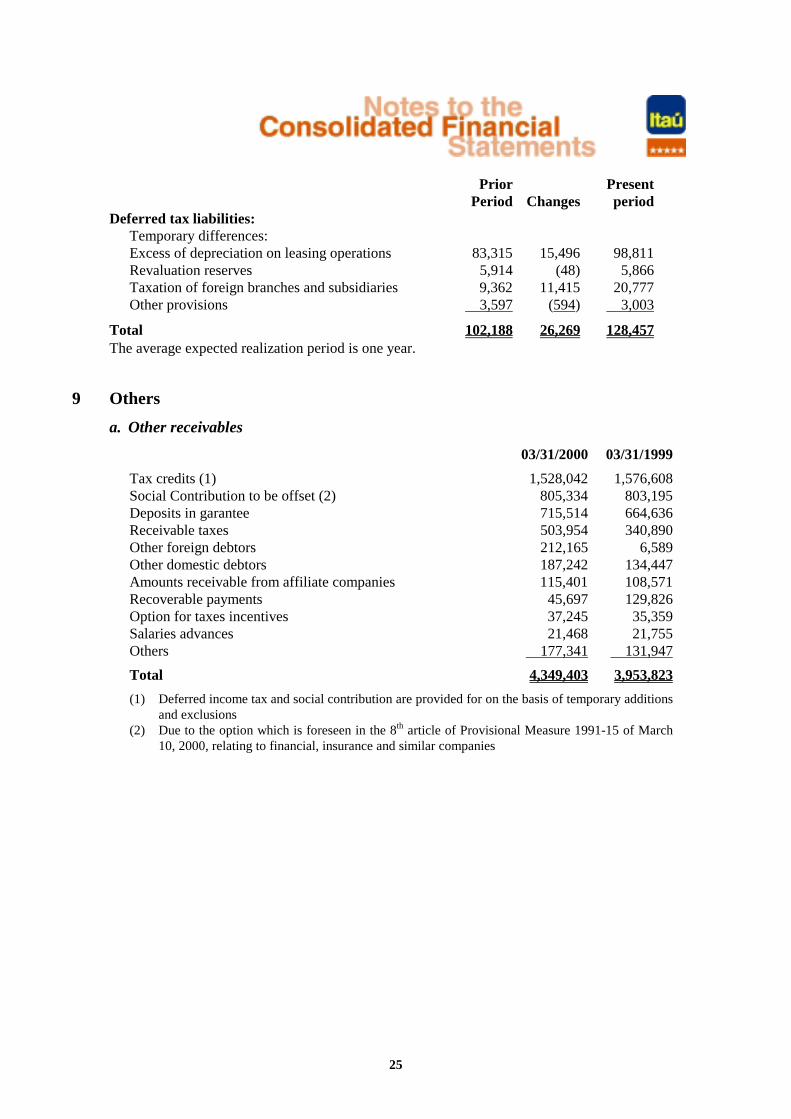

c. The balances of tax credits and deferred tax liabilities (income tax and social contribution)as of March 31, 2000 were comprised as follows:

PriorPeriod Changes

Presentperiod

Tax credits:Temporary differences:

Provision for loan losses 544,335 ( 26,379) 517,956Valuations allowance Securities/Interbank Deposits 159,785 20,956 180,741Provisions for interest on capital 116,048 4,590 120,638Provision for tax contingencies 87,131 5,185 92,316Provision for labor contingencies 95,658 8,879 104,537Provision for civil contingencies 35,273 7,686 42,959Real Estate allowances 51,315 (1,025) 50,290Tax losses 201,802 ( 1,582) 200,220Other 237,700 19,315 218,385

Total 1,529,047 ( 1,005) 1,528,042

25

PriorPeriod Changes

Presentperiod

Deferred tax liabilities:Temporary differences:Excess of depreciation on leasing operations 83,315 15,496 98,811Revaluation reserves 5,914 (48) 5,866Taxation of foreign branches and subsidiaries 9,362 11,415 20,777Other provisions 3,597 (594) 3,003

Total 102,188 26,269 128,457The average expected realization period is one year.

9 Others

a. Other receivables

03/31/2000 03/31/1999

Tax credits (1) 1,528,042 1,576,608Social Contribution to be offset (2) 805,334 803,195Deposits in garantee 715,514 664,636Receivable taxes 503,954 340,890Other foreign debtors 212,165 6,589Other domestic debtors 187,242 134,447Amounts receivable from affiliate companies 115,401 108,571Recoverable payments 45,697 129,826Option for taxes incentives 37,245 35,359Salaries advances 21,468 21,755Others 177,341 131,947

Total 4,349,403 3,953,823

(1) Deferred income tax and social contribution are provided for on the basis of temporary additionsand exclusions

(2) Due to the option which is foreseen in the 8th article of Provisional Measure 1991-15 of March10, 2000, relating to financial, insurance and similar companies

26

b. Other liabilities

03/31/2000 03/31/1999

Credit card companies 1,069,260 793,330Provision for contingent liabilities 1,024,589 943,049Provision for labour liabilities 454,892 236,227Other foreign creditors 270,166 218,368Salaries and employee benefits 196,554 255,583Liabilities for official agreement insurance 70,281 121,732Insurance companies 58,210 65,227Provision for payments 43,934 72,944Values to be paid - Affiliate companies 39,837 5,504Others 492,418 776,134

Total 3,720,141 3,488,098

c. Other operating income

03/31/2000 03/31/1999

Income from insurance operations 30,847 21,482Recovery of charges and expenses 11,663 15,035Equity share of subsidiaries and affiliates not originatedfrom earnings 8,118 34,131Reversal of Operational Provisions 5,761 40,115Monetary variation of assets 4,934 1,334Revenues related to real estate loans 1,178 2,485Others 37,285 69,961

Total 99,786 184,543

27

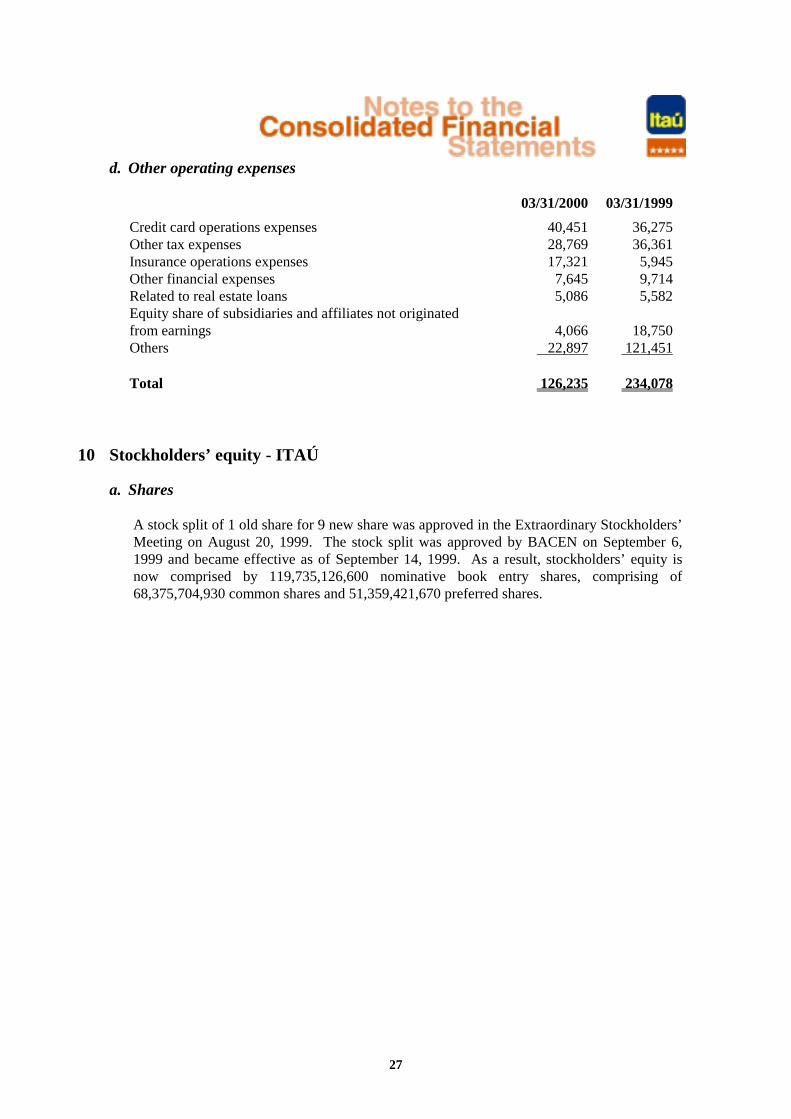

d. Other operating expenses

03/31/2000 03/31/1999

Credit card operations expenses 40,451 36,275Other tax expenses 28,769 36,361Insurance operations expenses 17,321 5,945Other financial expenses 7,645 9,714Related to real estate loans 5,086 5,582Equity share of subsidiaries and affiliates not originatedfrom earnings 4,066 18,750Others 22,897 121,451

Total 126,235 234,078

10 Stockholders’ equity - ITAÚ

a. Shares

A stock split of 1 old share for 9 new share was approved in the Extraordinary Stockholders’Meeting on August 20, 1999. The stock split was approved by BACEN on September 6,1999 and became effective as of September 14, 1999. As a result, stockholders’ equity isnow comprised by 119,735,126,600 nominative book entry shares, comprising of68,375,704,930 common shares and 51,359,421,670 preferred shares.

28

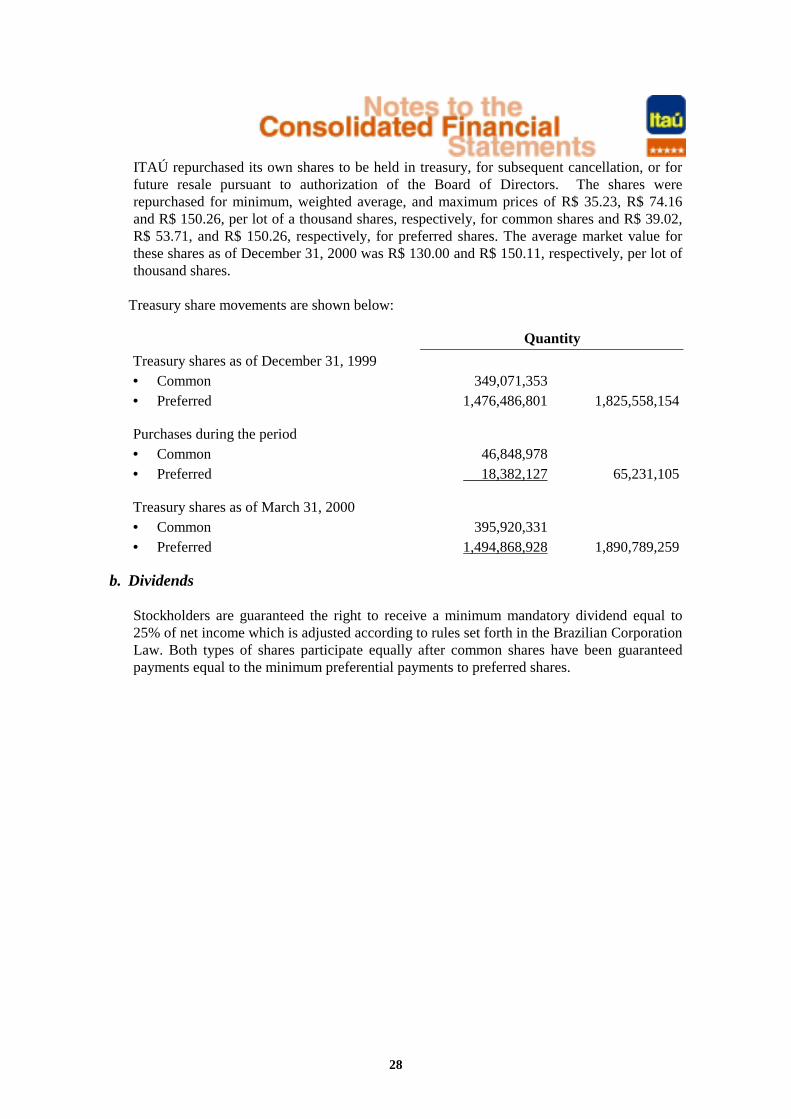

ITAÚ repurchased its own shares to be held in treasury, for subsequent cancellation, or forfuture resale pursuant to authorization of the Board of Directors. The shares wererepurchased for minimum, weighted average, and maximum prices of R$ 35.23, R$ 74.16and R$ 150.26, per lot of a thousand shares, respectively, for common shares and R$ 39.02,R$ 53.71, and R$ 150.26, respectively, for preferred shares. The average market value forthese shares as of December 31, 2000 was R$ 130.00 and R$ 150.11, respectively, per lot ofthousand shares.

Treasury share movements are shown below:

Quantity

Treasury shares as of December 31, 1999• Common 349,071,353• Preferred 1,476,486,801 1,825,558,154

Purchases during the period• Common 46,848,978• Preferred 18,382,127 65,231,105

Treasury shares as of March 31, 2000• Common 395,920,331• Preferred 1,494,868,928 1,890,789,259

b. Dividends

Stockholders are guaranteed the right to receive a minimum mandatory dividend equal to25% of net income which is adjusted according to rules set forth in the Brazilian CorporationLaw. Both types of shares participate equally after common shares have been guaranteedpayments equal to the minimum preferential payments to preferred shares.

29

In 1997, the system of monthly advances against the minimum mandatory dividend wassubstituted by a monthly advance against the payment of interest on capital. As of June 1,1999, the amount of the advance was raised to R$ 0.75 (seventy-five cents) per thousandshare lot. Due to 900% share split, deliberated on the Extraordinary Stockholder’s Generalmeeting of August 20, 1999, the antecipation changed to R$ 0.075 per thousand share lot.

11 Related parties

Transactions between related parties were entered into for amounts and terms in accordance withnormal market practices and terms as well as under reciprocal conditions. Transactions withconsolidated companies consolidated were eliminated from the consolidated financialstatements. Other operations with companies not included in the consolidation were immaterial.

12 Financial instruments

a. Derivatives

In relation to transactions involving derivatives, ITAÚ has sough to meet the principal needsof its Corporate customers to manage market risks, resulting mainly, from fluctuations in theinterest and exchange rates, an has developed an internal control systems to monitor theserisks in an appropriate manner.

ITAÚ’s policy is to minimize market risks resulting from derivative operations. As such, theBank avoids taking positions which are subject to fluctuations due to market factors and onlyemploys instruments that permit risk control, which is the responsibility of an independentarea within ITAÚ.

30

Most derivative contracts negotiated with customers are swap and future operations, whichare all registered at the BM&F or CETIP, and involve pre-fixed rates, interbank depositsrates, exchange variations or price indices. BM&F futures contracts involving interbankrates, and U.S. dollars are principally used to hedge financing operation offered to customerswith maturities or in currencies which are mismatched with the resources used to fund theseoperations.

The notional values for these financial instruments are recorded in memorandum accounts,and the adjustments/premiums are recorded in balance sheet accounts.

31

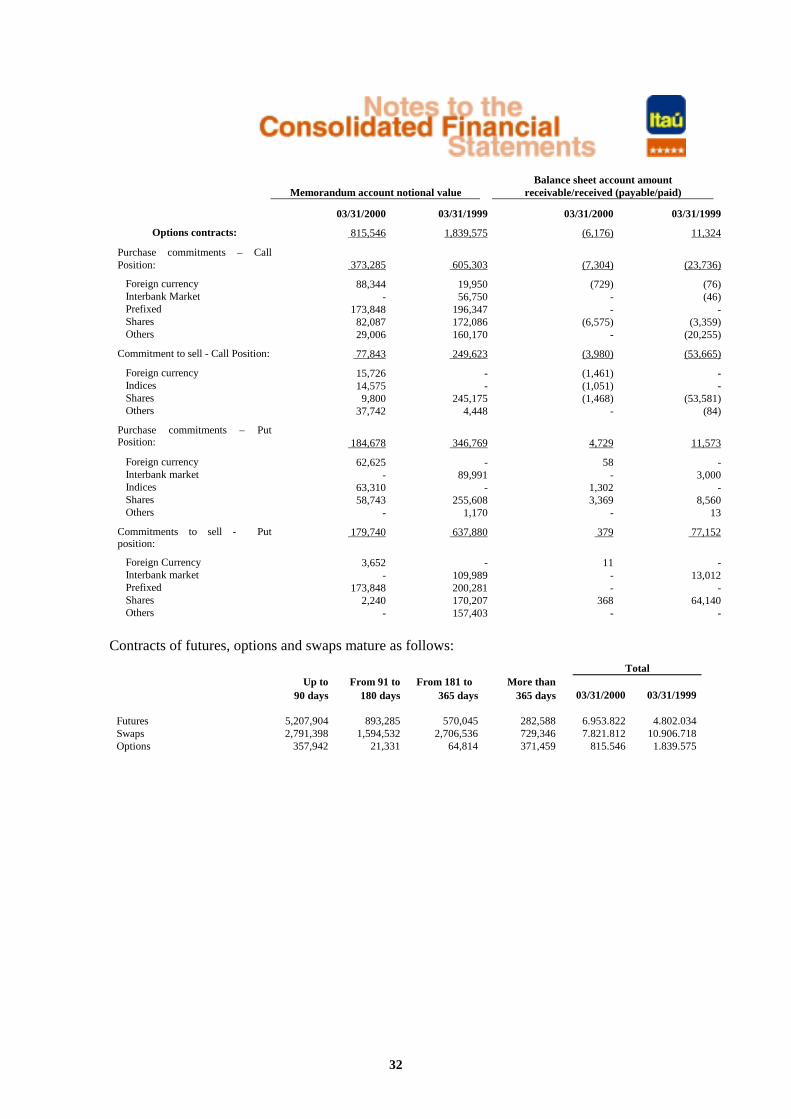

The amounts related to positions in future, swap and options operations were as follows:

Memorandum account notional valueBalance sheet account amount

receivable/received (payable/paid)

03/31/2000 03/31/1999 03/31/2000 03/31/1999

Future contracts 6,953,822 4,802,034 12,567 13,125

Purchase commitments: 3,421,765 2,026,491 (2,737) (4,723) Foreign currency 456,075 322,864 (1,133) (3,840) Interbank market 2,716,909 - (18) - Indices 243,474 1,702,382 (1,562) (865) Others 5,307 1,245 (24) (18)

Commitments to sell: 3,532,057 2,775,543 15,304 17,848

Foreign currency 1,658,012 1,151,325 7,070 2,535 Interbank market 581,549 - 79 - Indices 1,040,893 1,623,686 5,640 15,306 Shares 246,432 - 2,480 - Others 5,171 532 35 7

Swap contracts 124,684 (150,690)

Assets position: 8,014,411 11,192,120 192,599 285,402

Foreign currency 597,718 442,436 623 70,457 Interbank market 3,435,029 4,053,259 98,745 150,525 Prefixed 3,550,918 5,695,526 68,466 48,073 Indices 32,454 25,863 - - Others 398,292 975,036 24,765 16,347

Liability position: 7,889,727 11,342,810 (67,915) (436,092)

Foreign currency 2,279,858 2,474,745 (4,272) (242,301) Interbank market 3,682,302 5,893,421 (27,271) (183,769) Prefixed 1,513,485 2,067,691 (27,532) (7,421) Indices 193,680 66,155 (8,135) (1,684) Others 220,402 840,798 (705) (917)

32

Memorandum account notional valueBalance sheet account amount

receivable/received (payable/paid)

03/31/2000 03/31/1999 03/31/2000 03/31/1999

Options contracts: 815,546 1,839,575 (6,176) 11,324

Purchase commitments – CallPosition: 373,285 605,303 (7,304) (23,736)

Foreign currency 88,344 19,950 (729) (76) Interbank Market - 56,750 - (46) Prefixed 173,848 196,347 - - Shares 82,087 172,086 (6,575) (3,359) Others 29,006 160,170 - (20,255)

Commitment to sell - Call Position: 77,843 249,623 (3,980) (53,665)

Foreign currency 15,726 - (1,461) - Indices 14,575 - (1,051) - Shares 9,800 245,175 (1,468) (53,581) Others 37,742 4,448 - (84)

Purchase commitments – PutPosition: 184,678 346,769 4,729 11,573

Foreign currency 62,625 - 58 - Interbank market - 89,991 - 3,000 Indices 63,310 - 1,302 - Shares 58,743 255,608 3,369 8,560 Others - 1,170 - 13

Commitments to sell - Putposition:

179,740 637,880 379 77,152

Foreign Currency 3,652 - 11 - Interbank market - 109,989 - 13,012 Prefixed 173,848 200,281 - - Shares 2,240 170,207 368 64,140 Others - 157,403 - -

Contracts of futures, options and swaps mature as follows:

TotalUp to From 91 to From 181 to More than

90 days 180 days 365 days 365 days 03/31/2000 03/31/1999

Futures 5,207,904 893,285 570,045 282,588 6.953.822 4.802.034Swaps 2,791,398 1,594,532 2,706,536 729,346 7.821.812 10.906.718Options 357,942 21,331 64,814 371,459 815.546 1.839.575

33

b. Market value

The financial statements were prepared based on the assumption of normal continuity in theoperations of ITAÚ and its subsidiaries.

The recorded values of each financial instrument whether included or not in the balancesheet, when compared with the values that might be obtained in an active market, or in theabsence of such markets, using the net present value of adjusted discounted future cash flowsbased on the prevailing market interest rate, are close to the corresponding market value, orits value is not available, except for the amounts included:

Recorded value Market valueUnrealized

Gain / (Loss)

03/31/2000 03/31/1999 03/31/2000 03/31/1999 03/31/2000 03/31/199

9

Interbank deposits: 1,756,560 2,551,234 1,778,179 2,565,289 21,619 14.055

Securities and derivatives: 15,950,382 13,554,154 16,899,964 14,082,599 949,582 528,445

Securities – BACEN’s Circular2,913/99 228,577 - 232,853 - 4,276 -- NTN - D 184,216 - 188,492 - 4,276 -- NBC - E 44,361 - 44,361 - - -Other securities 15,601,987 13,693,153 16,508,566 14,270,013 906,579 576,860Derivatives-differential receivable/payable 119,818 (138,999) 158,545 (187,414) 38,727 ( 48,415)

Loan operations 13,895,649 12,641,204 13,913,562 12,635,615 17,913 ( 5,589)

Participation in BPI 142,443 87,651 455,043 414,734 312,600 327,083

Other investments 277,708 264,463 279,940 264,346 2,232 ( 117)

Time and interbank deposits and Debentures 6,432,400 8,013,951 6,291,073 7,768,372 141,327 245,579

Treasury shares 110,713 101,966 275,864 162,396 165,151 60,430

Total Unrealized Gain / (Loss) 1,610,424 1.169.886

(*) Includes unrealized gains (losses) relating to minority interests amounting to R$ 148,934,(R$ 246,546 at March 31, 1999).

34

To obtain the market values for these Financial Instruments, the following criteria were adopted:

• Interbank deposits, certificates of bank deposit and mortgage securities, the latter twoincluded in “Securities” were determined on the basis of their nominal values, monetarilycorrected to maturity and discounted to present value using interest futures market rates, 367-day swap market rates for pre-fixed securities, and fixed interest securities market rates forpost-fixed securities published in the Gazeta Mercantil on April 3, 2000;

• Public securities, included in “Securities” were determined on the basis of actual tradesregistered with BACEN/DICEL/SELIC (Special System for Settlement and Custody), inaccordance with lists held by ANDIMA (the National Association of Open MarketInstitutions);

• Investment fund quotas included in “Securities” were determined on the basis of net valueper quota on the balance sheet date;

• Publicly traded shares when included in “Securities” were valued using the average pricequota of the last trading day of the month if available, or on the basis of the most recentquotations for the companies’ shares published in the daily bulletin of each Stock Exchange;

• Loans with maturities of over 90 days were calculated on the basis of their net present value,determined by means of future cash flows discounted using market interest rates on thebalance sheet date, when available; the effects of hedges (swap contracts) are also taken intoaccount;

• Other investments and equity shares in foreign subsidiaries and affiliates are determined onthe basis of stock market quotations, book value per share and auction quotation;

• Time and interbank deposits and debentures, when available, were calculated on the basis oftheir present value, determined by means of future cash flows discounted using interestfutures market rates, 367-day swap market for pre-fixed securities, and fixed incomesecurities market rates for post-fixed securities published in the Gazeta Mercantil on April 3,2000; the effects of hedges (swap contracts) are also taken into account.

35

• Derivatives related to swaps contracted to hedge other assets and liabilities are determinedon the basis of reference values for each parameter set forth in the contracts (both parties),monetarily corrected through maturity and discounted to present value using interest futuresmarket rates, according to the characteristics of each contract.

• Treasury shares are valued according to the average quotation available on the last tradingday of the month, or if this is not available, according to the most recent quotation on priortrading days, published in the daily bulletin of each Stock Exchange.

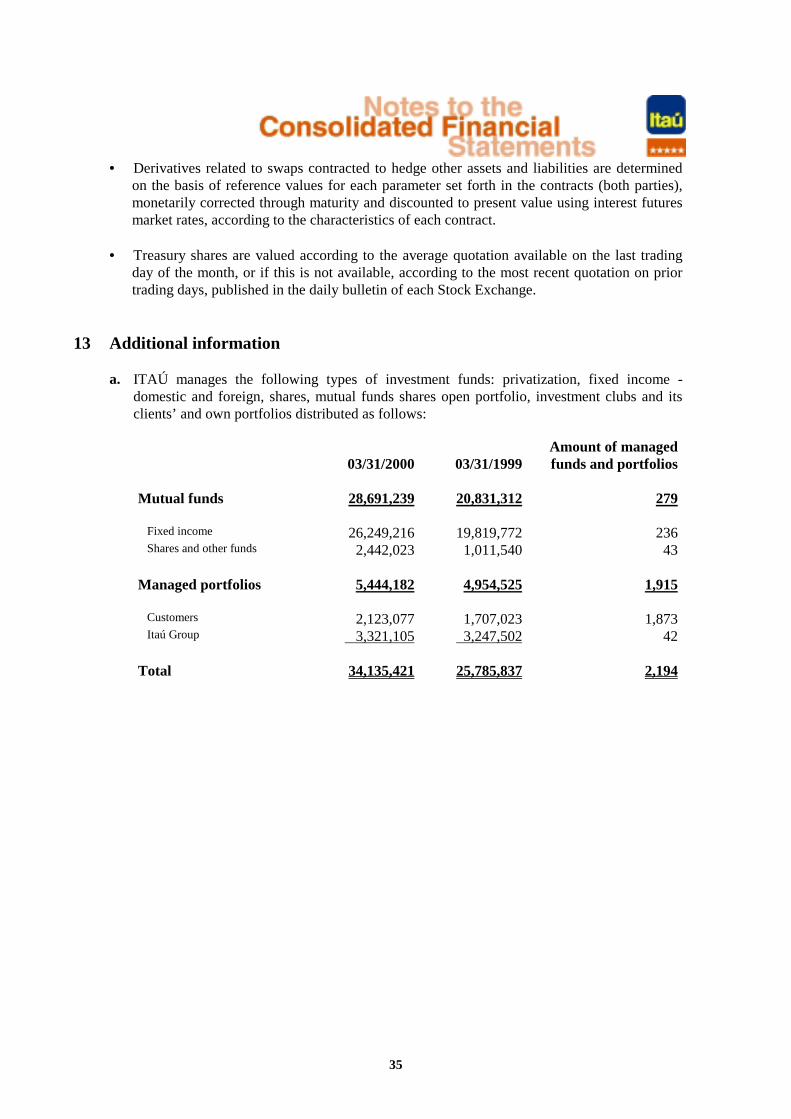

13 Additional information

a. ITAÚ manages the following types of investment funds: privatization, fixed income -domestic and foreign, shares, mutual funds shares open portfolio, investment clubs and itsclients’ and own portfolios distributed as follows:

03/31/2000 03/31/1999Amount of managedfunds and portfolios

Mutual funds 28,691,239 20,831,312 279

Fixed income 26,249,216 19,819,772 236 Shares and other funds 2,442,023 1,011,540 43

Managed portfolios 5,444,182 4,954,525 1,915

Customers 2,123,077 1,707,023 1,873 Itaú Group 3,321,105 3,247,502 42

Total 34,135,421 25,785,837 2,194

36

b. The balances vinculated to foreign currency were:

In thousand of reais

03/31/2000 03/31/1999

Foreign investments 2,625,548 2,260,673Net value of assets and liabilities indexed in foreigncurrency including derivatives 13,846 331,352

Net foreign exchange position 2,639,394 2,592,025

c. ITAÚ and its subsidiaries sponsor complementary pension plans managed by FundaçãoItaubanco and Fundação Bemge de Seguridade Social - FASBEMGE (closed private pensionfunds), for the purpose of granting lifetime income (in the case of FASBEMGE also for thepurpose of death benefits) to complement the retirement pension paid by social security.The contributions amounted to R$ 14.854 (R$ 9.145 in March 31, 1999). The actuarialliabilities are calculated in accordance with the actuarial models established in the plans’Technical Notes, which call for compound capitalization and defined benefits, and are fullycovered by the technical provisions for expired and unexpired risks. The contribution rateincreases in accordance with the participant’s salary.

d. ITAÚ has established an Employee Stock Options Plan to provide an incentive forexecutives to focus on the future success of Itaú over the medium and long terms timehorizons. As of March 31, 2000 ITAÚ has granted 3.021.800.000 preferred shares. Thesestock options may be exercised as follows: 282,000,000 as of January 1, 1998, 597,000,000shares as of January 1, 1999, 533,000,000 shares as of January 1, 2002 and 578,500,000shares as of January 1, 2003 and 498,100,000 shares as of January 1, 2004 and 533,200,000shares as of January 1, 2005. Up to March 31, 2000, 835,952,060 shares have beenexercised.

e. During the first quarter of 2000, R$ 380,123 (R$ 798,318 in March 31, 1999) were collectedand provisioned in ITAÚ CONSOLIDATED related to taxes and contributions of income,revenues and salaries. Moreover, taxes on financial intermediation were collected fromclients in the amount of R$ 762,582 (R$ 513,557 in March 31, 1999) in ITAÚCONSOLIDATED.

37

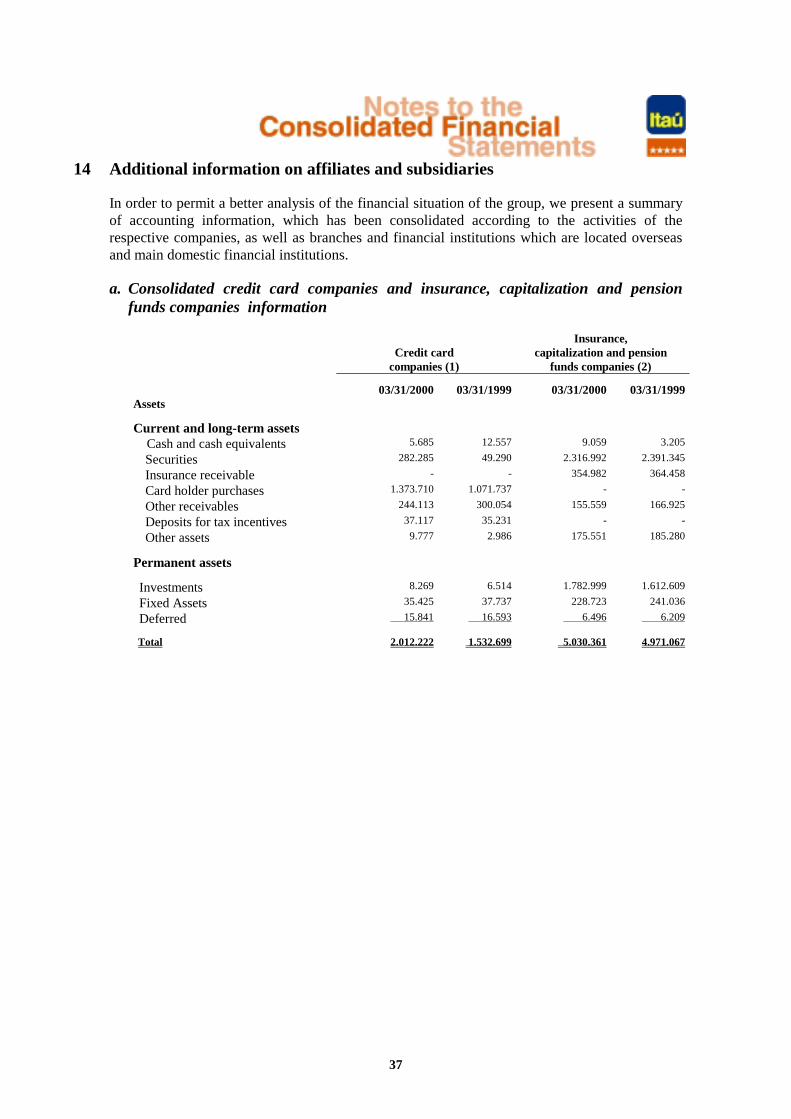

14 Additional information on affiliates and subsidiaries

In order to permit a better analysis of the financial situation of the group, we present a summaryof accounting information, which has been consolidated according to the activities of therespective companies, as well as branches and financial institutions which are located overseasand main domestic financial institutions.

a. Consolidated credit card companies and insurance, capitalization and pensionfunds companies information

Insurance,Credit card capitalization and pension

companies (1) funds companies (2)

03/31/2000 03/31/1999 03/31/2000 03/31/1999Assets

Current and long-term assets Cash and cash equivalents 5.685 12.557 9.059 3.205

Securities 282.285 49.290 2.316.992 2.391.345

Insurance receivable - - 354.982 364.458

Card holder purchases 1.373.710 1.071.737 - -

Other receivables 244.113 300.054 155.559 166.925

Deposits for tax incentives 37.117 35.231 - -

Other assets 9.777 2.986 175.551 185.280

Permanent assets

Investments 8.269 6.514 1.782.999 1.612.609

Fixed Assets 35.425 37.737 228.723 241.036

Deferred 15.841 16.593 6.496 6.209

Total 2.012.222 1.532.699 5.030.361 4.971.067

38

Liabilities

Current and long-term liabilities

Technical provisions - Vinculated - - 332.158 250.652

Insurance operations payable - - 68.233 46.576

Borrowings 124.782 159.234 - -

Taxes and social security contributions 33.623 28.191 117.938 213.596

Payable amounts - Stores 737.764 500.492 - -

Banking Financing - Card holders 536.297 481.459 - -

Credit Card - Annuity revenues 82.398 75.682 - -

Other liabilities 157.856 141.161 106.703 179.463

Technical provisions - Not vinculated - - 1.904.201 1.750.178

Minority interest in consolidated subsidiaries - - 1.199 17.283

Stockholders’ equityCapital and reserves 267.346 102.765 2.438.934 2.289.507

Income for the period 72.156 43.715 60.995 223.812

Total 2.012.222 1.532.699 5.030.361 4.971.067

(1) Includes Banerjcard Administradora de Cartões de Crédito Ltda., BFB Administradorade Cartões de Crédito e Serviços Ltda., Itaucard Administradora de Cartões de Crédito eImobilária Ltda., Bemge Administradora de Cartões de Crédito Ltda. and proportionally,Credicard Comercial e Importadora Ltda., Credicard S.A. Administradora de Cartões deCrédito, and Redecard S.A.

(2) Includes Banerj Seguros S.A., Itaú Capitalização S.A., Itaú Previdência e Seguros S.A.and Itaú Seguros S.A., Bemge Seguradora S.A. and Investprev Seguros e PrevidênciaS.A. (proportionally consolidated) - Companies regulated by the Insurance CompanyRegulatory Agency (SUSEP).

(In thousands of reais)

b. Foreign branches/financial institutions

Banco Itaú Europa S.A. consolidated (3)

Banco Itaú Europa Luxembourg S.A. Consolidated (4) Itau Bank, Ltd. Other Non- Financial (5) Foreign Consolidated (6)

03/31/2000 03/31/1999 03/31/2000 03/31/1999 03/31/2000 03/31/1999 03/31/2000 03/31/1999 03/31/2000 03/31/1999 03/31/2000 03/31/1999 03/31/2000 03/31/1999 03/31/2000 03/31/1999Assets

Current and long-term assets:Cash and cash equivalents 19,435 9,932 179,515 233,224 13,734 7,356 13,106 1 488 5,580 2,057 8,883 2,975 1,508 229,766 266,276 Interbank funds applied 57,073 795,206 87,622 234,832 650,018 748,335 - 59,865 - 328,497 55 19,317 - 148,934 794,768 1,931,239 Money market 57,073 125,634 87,622 51,660 - - - 52,881 - 108,567 - - - - 144,695 230,175 Interbank deposits - 669,572 - 183,172 650,018 748,335 - 6,984 - 219,930 55 19,317 - 148,934 650,073 1,701,064 Securities 3,543,271 1,266,956 256,041 164,017 496,624 342,750 161,306 - 580,957 363,297 50,228 16,778 87,650 24,532 4,934,735 2,126,137 - Brazil 1,900,115 1,150,613 118,321 - 70,355 36,995 5,332 - 407,903 177,591 39,389 16,757 28,602 24,190 2,570,017 1,406,146 - Federal government 806,953 365,783 - - - 14,615 - - 214,398 167,807 - - 2,641 - 1,023,992 548,205 - Financial institutions 1,093,162 784,830 118,321 - 70,355 22,380 5,332 - 193,505 9,784 39,389 16,757 25,961 24,190 1,546,025 857,941 - Others 1,643,156 116,343 137,720 164,017 426,269 305,755 155,974 - 173,054 185,706 10,839 21 59,048 342 2,364,718 719,991 Interbank and interbranch accounts - 5 1,741 - - - - - - - 886 - - - 2,627 5 Loans and leasing 2,019,146 2,062,112 597,892 608,167 857,655 500,808 50,460 51,829 188,842 252,913 21,867 - 1,554 14,720 3,709,947 3,471,667 Foreign trading loans 1,090,854 2,060,286 82,087 - 532,084 497,863 216 1,363 181,955 126,742 - - 540 13,721 1,887,736 2,875,130 Others 928,292 1,826 515,805 608,167 325,571 2,945 50,244 50,466 6,887 126,171 21,867 - 1,014 999 1,822,211 596,537 Prepaid expenses 25,853 2,652 2,351 1,533 315 30,377 118 220 356 - - - 47 240 28,677 34,940 Other assets 106,460 64,519 73,582 21,184 11,729 2,705 3,804 45 54,312 18,457 - - 401,116 356,435 642,767 463,346

Permanent assets:Investments - - 175 172 51 - 1,625 - - - - 874 735,764 407,781 144,006 88,526 Fixed Assets 805 961 116,841 118,478 3,834 4,341 648 711 78 91 111 70 523 396 122,840 125,044 Deferred 151 309 13,726 17,776 355 - 322 417 31 21 15 17 151 - 14,864 18,540

Total 5,772,194 4,202,652 1,329,486 1,399,383 2,034,315 1,636,672 231,389 113,088 825,064 968,856 75,219 45,939 1,229,780 954,546 10,624,997 8,525,720

LiabilitiesCurrent and long-term liabilities

Deposits 407,931 67,994 860,076 800,421 1,570,129 13,607 186,146 88,541 152,415 163,549 20,556 - 22,815 - 3,085,454 998,484 Demand deposits 14,881 6,093 106,990 94,860 1,674 811 93,035 53,950 38,421 35 1,942 - - - 217,200 155,505 Savings deposits - - 301,210 283,036 - - - - - - - - - - 301,210 283,036 Interbank deposits - - - 43,262 - - - - - - - - - - - 43,262 Times deposits 393,050 61,901 451,876 379,263 1,568,455 12,796 93,111 34,591 113,994 163,514 18,614 - 22,815 - 2,567,044 516,681 Money market 647,322 393,862 - - 4,833 1,398,418 - - 259,511 253,532 2,835 - - 27,885 914,501 1,766,683 Acceptances and debentures 1,279,424 918,858 - - 39,872 - - - - - - - 537 7,208 1,277,138 926,066 Borrowings 1,898,218 1,509,904 83,216 99,570 3,692 - - - 43,871 92,522 - - 124,117 17,388 2,128,011 1,701,044 Other liabilities 183,053 159,745 128,604 191,233 110,791 31,705 7,070 2,722 31 127,954 14 1,430 103,125 143,248 477,899 816,345

Deferred income 39,211 9,520 - - 542 - - - 5,589 10,061 - - 1,630 845 46,783 20,426

Minority Interest in consolidated subsdiaries - - - - - - 1 - - - - - - - 69,663 35,999

Stockholders’ equity Capital and reserves 1,307,746 1,117,428 271,795 313,914 299,442 188,678 36,191 21,201 352,755 313,471 50,742 43,686 958,198 737,918 2,596,743 2,214,197 Income for the period 9,289 25,341 (14,205) (5,755) 5,014 4,264 1,981 624 10,892 7,767 1,072 823 19,358 20,054 28,805 46,476

Total 5,772,194 4,202,652 1,329,486 1,399,383 2,034,315 1,636,672 231,389 113,088 825,064 968,856 75,219 45,939 1,229,780 954,546 10,624,997 8,525,720

(1) Includes Grand Cayman and New York Branches(2) New name of Banco Itaú Argentina S.A., after incorporation of Banco del Buen Ayre S.A.(3) Banco Itaú Europa, S.A., BIE - Bank & Trust, Ltd., Itaú Europa, SGPS, S.A.(4) Banco Itaú Europa Luxembourg S.A., BIE - Fund Management Company, S.A., BIEL Holding AG

(6) The foreign consolidated information are presented net of the elimination.

Foreign branches (1) Banco Itaú Buen Ayre S.A. (2)IFE - Banco do Estado Minas

Gerais S.A. (Uruguay)

(5) Afinco - Americas Madeira, SGPS Ltda., Banctec Informática S.A., BFB Overseas Inc., BFB Overseas Cayman, Ltd., Externalizacion Global S.A., Inversora del Buen Ayre S.A., Itaú Europa, SGPS, S.A., Itaú Sociedad Gerente de Fondos Comunes de Inversion S.A., Itaúsa Portugal - SGPS, S.A., ITH Zux Cayman Company Ltd., Itaú Leasing de Chile Ltda., Zux Cayman Company Ltd., Zux SGPS, S.A., BIEL Holding AG, IPI Ita[usa Portugal Invest. Ltda.

39

40

c. Main financial institutions in the country

BANERJ (1) BEMGE (2)

03/31/2000 03/31/1999 03/31/2000 03/31/1999AssetsCurrent and long-term assets Cash and cash equivalents 234,451 240,191 50,196 35,151

Interbank funds applied 2,069,656 2,420,665 796,761 4,142,038

Securities 481,186 584,394 4,453,125 1,965,949

Interbank accounts 431,934 492,275 149,792 167,831

Interbranch accounts 1,758 - 23 460

Loan and leasing operations 825,829 433,802 2,316,290 127,774

Other receivables 294,519 210,424 1,959,305 626,682

Other assets 7,275 20,253 184,183 8,127

Permanent assets Investments 8,899 9,278 309,331 7,900

Fixed assets 145,661 131,268 859,335 71,611

Deferred expenses 131,309 137,923 93,731 5,370

Total 4,632,477 4,680,473 11,172,072 7,158,893

LiabilitiesCurrent and long-term liabilities Deposits 2,765,124 3,621,109 3,376,347 1,396,834

Money market repurchase commitments 510,148 1,879 127,603 67,083

Acceptance and endorsements - - 484,324 -

Interbank accounts 136,957 56,642 38,318 84,453

Interbranch accounts 5,106 10,210 1,107 3,358

Borrowings 95,573 24,164 223,119 13,032

On-lending borrowings from public Institutions 808 935 2,748 9,244

Technical provisions for insurance operations – Vinculated - 19,865 331,980 8,906

Other liabilities 406,020 443,543 2,398,200 4,070,481

41

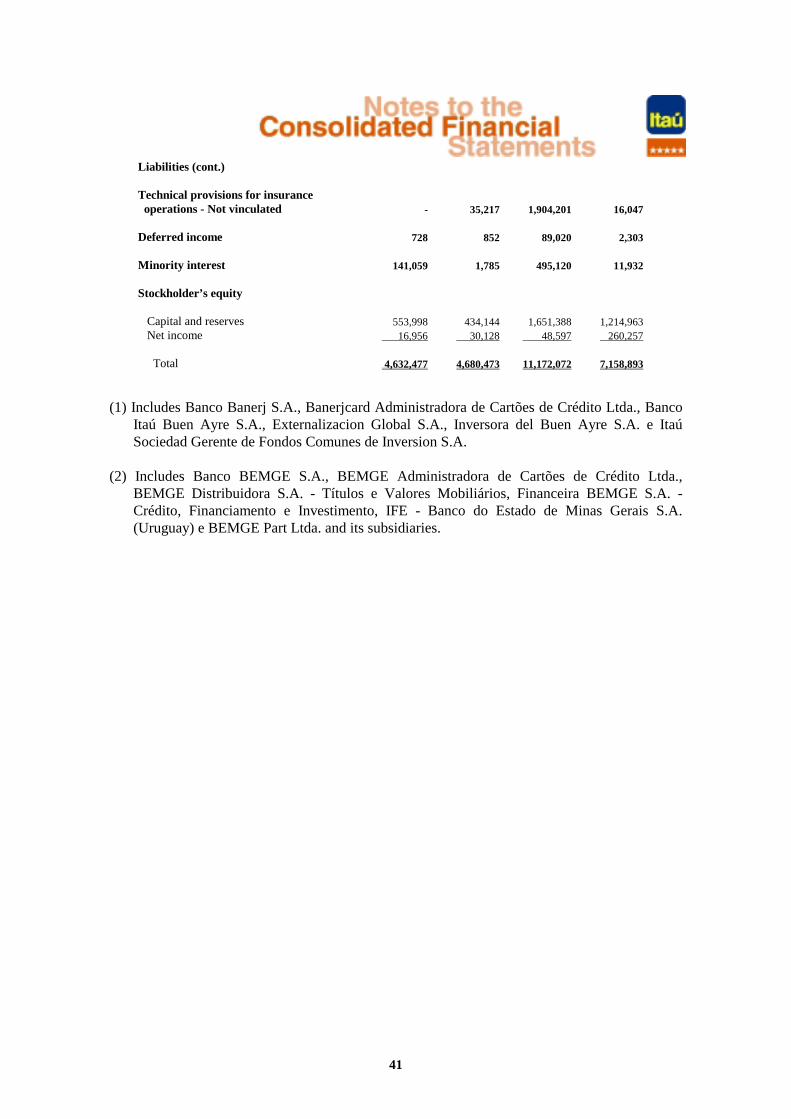

Liabilities (cont.)

Technical provisions for insurance operations - Not vinculated - 35,217 1,904,201 16,047

Deferred income 728 852 89,020 2,303

Minority interest 141,059 1,785 495,120 11,932

Stockholder’s equity

Capital and reserves 553,998 434,144 1,651,388 1,214,963 Net income 16,956 30,128 48,597 260,257

Total 4,632,477 4,680,473 11,172,072 7,158,893

(1) Includes Banco Banerj S.A., Banerjcard Administradora de Cartões de Crédito Ltda., BancoItaú Buen Ayre S.A., Externalizacion Global S.A., Inversora del Buen Ayre S.A. e ItaúSociedad Gerente de Fondos Comunes de Inversion S.A.

(2) Includes Banco BEMGE S.A., BEMGE Administradora de Cartões de Crédito Ltda.,BEMGE Distribuidora S.A. - Títulos e Valores Mobiliários, Financeira BEMGE S.A. -Crédito, Financiamento e Investimento, IFE - Banco do Estado de Minas Gerais S.A.(Uruguay) e BEMGE Part Ltda. and its subsidiaries.

42

The Administrative Council and StockholdersBanco Itaú S.A.São Paulo -SP

We have performed a special review of the interim consolidated report of Banco Itaú S.A. andits subsidiaries for the three-month period ended March 31, 2000, comprising the consolidatedbalance sheet, the consolidated statement of income, the performance report and relevantdisclosures, which were prepared in accordance with the accounting practices derived fromBrazilian Corporation Law.

Our review was performed in conformity with the specific norms establish by the BrazilianInstitute of Accountants (IBRACON), jointly with the Federal Accounting Council, andconsisted principally of: (a) inquiries and discussions with management responsible for theaccounting, financial and operational areas of the Bank and its subsidiaries, regarding theprincipal criteria adopted in the preparation of the interim reports; and; (b) review ofinformation and subsequent events that have or may have a relevant effect on the financialsituation and the operations of Banco Itaú S.A. and its subsidiaries.

On the basis of our review we are not aware of any significant modifications that should bemade to the aforementioned interim consolidated report for it to be in conformity withaccounting practices derived from Brazilian Corporation Law, applied in accordance with rulesof the Brazilian Securities Commission specifically applicable to the preparation of interimreports.

May 8, 2000

KPMG Auditores IndependentesCRC 2SP014428/O-6

José Marcelo Bessan Alberto Spilborghs NetoAccountant CRC 1SP129705/O-0 Accountant CRC1SP167455/O-0

Banco Itaú S.A.Consolidated

Management ‘s Discussion & AnalysisFirst Quarter of 2000

20002000

44

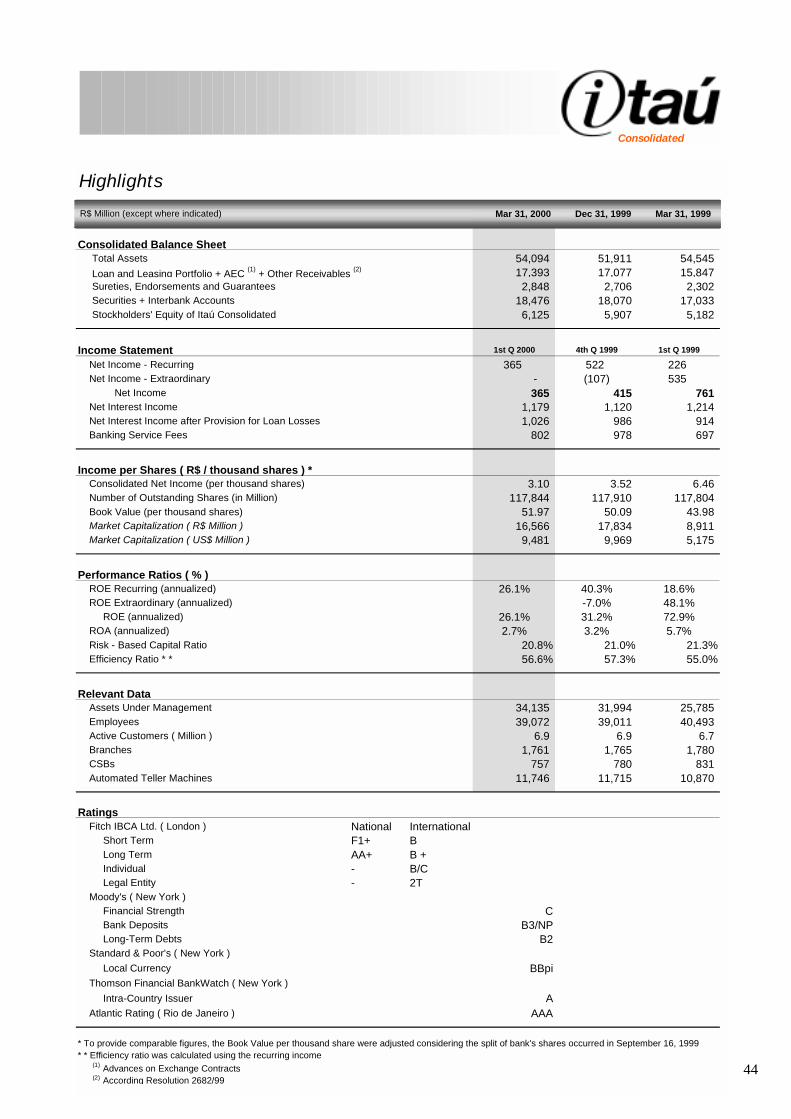

Consolidated

Highlights

Consolidated Balance Sheet Total Assets 54,094 51,911 54,545 Loan and Leasing Portfolio + AEC

(1) + Other Receivables

(2) 17,393 17,077 15,847 Sureties, Endorsements and Guarantees 2,848 2,706 2,302 Securities + Interbank Accounts 18,476 18,070 17,033 Stockholders' Equity of Itaú Consolidated 6,125 5,907 5,182

Income Statement 1st Q 2000 4th Q 1999 1st Q 1999

Net Income - Recurring 365 522 226 Net Income - Extraordinary - (107) 535

Net Income 365 415 761 Net Interest Income 1,179 1,120 1,214 Net Interest Income after Provision for Loan Losses 1,026 986 914 Banking Service Fees 802 978 697

Income per Shares ( R$ / thousand shares ) * Consolidated Net Income (per thousand shares) 3.10 3.52 6.46 Number of Outstanding Shares (in Million) 117,844 117,910 117,804 Book Value (per thousand shares) 51.97 50.09 43.98 Market Capitalization ( R$ Million ) 16,566 17,834 8,911 Market Capitalization ( US$ Million ) 9,481 9,969 5,175

Performance Ratios ( % ) ROE Recurring (annualized) 26.1% 40.3% 18.6% ROE Extraordinary (annualized) -7.0% 48.1%

ROE (annualized) 26.1% 31.2% 72.9% ROA (annualized) 2.7% 3.2% 5.7% Risk - Based Capital Ratio 20.8% 21.0% 21.3% Efficiency Ratio * * 56.6% 57.3% 55.0%

Relevant Data Assets Under Management 34,135 31,994 25,785 Employees 39,072 39,011 40,493 Active Customers ( Million ) 6.9 6.9 6.7 Branches 1,761 1,765 1,780 CSBs 757 780 831 Automated Teller Machines 11,746 11,715 10,870

R$ Million (except where indicated)

Ratings Fitch IBCA Ltd. ( London ) National International

Short Term F1+ BLong Term AA+ B +Individual - B/CLegal Entity - 2T

Moody's ( New York )Financial Strength CBank Deposits B3/NPLong-Term Debts B2

Standard & Poor's ( New York )

Local Currency BBpi Thomson Financial BankWatch ( New York )

Intra-Country Issuer A Atlantic Rating ( Rio de Janeiro ) AAA

* To provide comparable figures, the Book Value per thousand share were adjusted considering the split of bank's shares occurred in September 16, 1999* * Efficiency ratio was calculated using the recurring income

(1) Advances on Exchange Contracts(2) According Resolution 2682/99

Mar 31, 2000 Dec 31, 1999 Mar 31, 1999

45

Consolidated

1.7%

4.0%

2.4%3.3%

-0.6%

4.1%

-0.8%

2.7%

1st Q1999

2nd Q1999

3rd Q1999

4th Q1999

1st Q2000

ROA (% )

3.2%2.7

5.7%

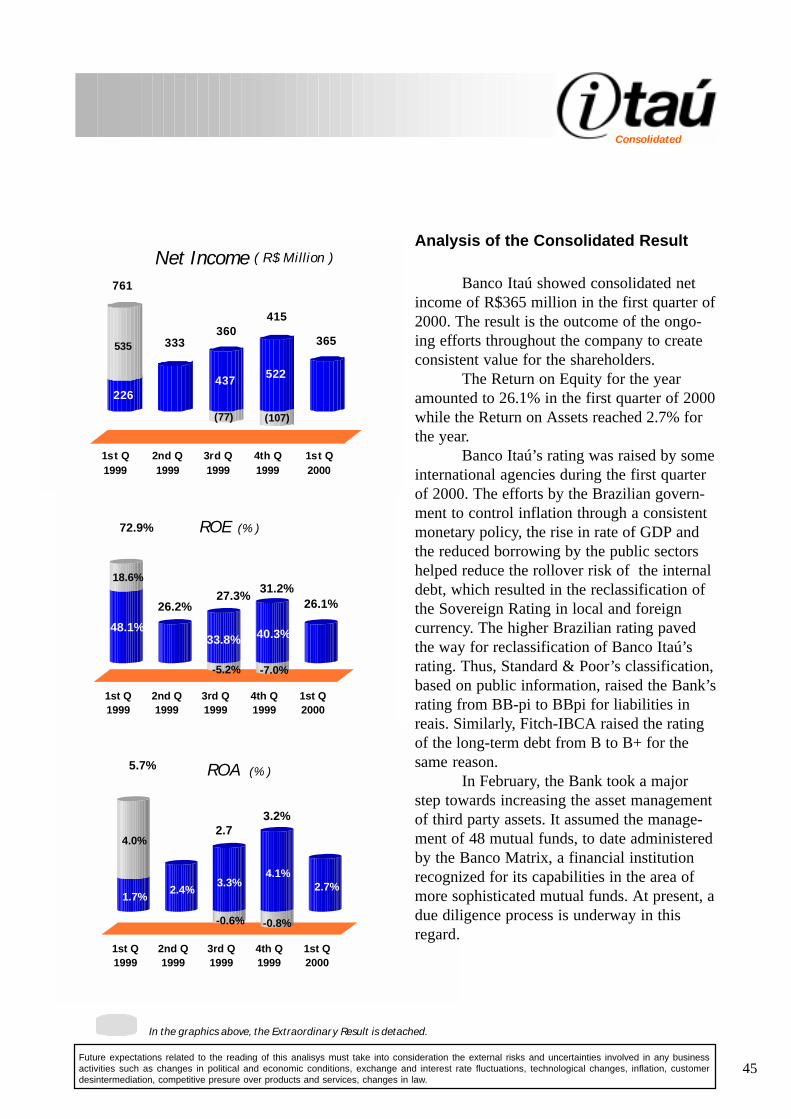

In the graphics above, the Extraordinary Result is detached.

226

535 333

437

(77)

522

(107)

365

1st Q1999

2nd Q1999

3rd Q1999

4th Q1999

1st Q2000

Net Income ( R$ Million )

415360

761

Future expectations related to the reading of this analisys must take into consideration the external risks and uncertainties involved in any businessactivities such as changes in political and economic conditions, exchange and interest rate fluctuations, technological changes, inflation, customerdesintermediation, competitive presure over products and services, changes in law.

Analysis of the Consolidated Result

Banco Itaú showed consolidated netincome of R$365 million in the first quarter of2000. The result is the outcome of the ongo-ing efforts throughout the company to createconsistent value for the shareholders.

The Return on Equity for the yearamounted to 26.1% in the first quarter of 2000while the Return on Assets reached 2.7% forthe year.

Banco Itaú’s rating was raised by someinternational agencies during the first quarterof 2000. The efforts by the Brazilian govern-ment to control inflation through a consistentmonetary policy, the rise in rate of GDP andthe reduced borrowing by the public sectorshelped reduce the rollover risk of the internaldebt, which resulted in the reclassification ofthe Sovereign Rating in local and foreigncurrency. The higher Brazilian rating pavedthe way for reclassification of Banco Itaú’srating. Thus, Standard & Poor’s classification,based on public information, raised the Bank’srating from BB-pi to BBpi for liabilities inreais. Similarly, Fitch-IBCA raised the ratingof the long-term debt from B to B+ for thesame reason.

In February, the Bank took a majorstep towards increasing the asset managementof third party assets. It assumed the manage-ment of 48 mutual funds, to date administeredby the Banco Matrix, a financial institutionrecognized for its capabilities in the area ofmore sophisticated mutual funds. At present, adue diligence process is underway in thisregard.

48.1%

18.6%

26.2%

33.8%

-5.2%

40.3%

-7.0%

26.1%

1st Q1999

2nd Q1999

3rd Q1999

4th Q1999

1st Q2000

ROE (% )

31.2%27.3%

72.9%

46

Consolidated

Stock Market Performance

Banco Itaú preferred shares weretrading at the end of the first quarter of 2000 atR$155.00 per lot of 1,000 shares, remainingsteady during the period. Market capitaliza-tion, which also takes into account the valueof ordinary shares, amounted to R$16,566

million, a decrease of 7.1% from December1999. Consolidated net income per thousandshares amounted to R$3.10 for the quarter.Share value per thousand reached R$51.97,rising 3.75% over the share value at December1999.

Market Capitalization, Stockholders’ Equity andConsolidated Net Income (1)

6,1255,9075,8015,5635,182

16,56617,834

11,1099,9148,911226

333 360415

365

02,000

4,0006,000

8,000

10,00012,000

14,00016,000

18,00020,000

1Q99 2Q99 3Q99 4Q99 1Q000

100

200

300

400

500

600

700

800Consolidated Stockholders' Equity

Market Capitalization

Consolidated Net Income

R$ Million

(1) Net Income of Quarter; Stockholders’ Equity and Market Capitalization as of period ended.

761

Ext

raor

dina

ry R

esul

t (2)

(2) In the first quarter of 1999, the Banco Itaú has Extraordinary Result of R$ 535 million, related to the valorization ofpermanent Bank investments abroad.

Cons

olid

ated

Net

Inco

me

Mar

ket C

apita

lizat

ion,

Sto

ckho

lder

s’ E

quity

Collor Plan

Real Plan

Mexican Crisis

Asian Crisis

Russian Crisis

Preferred Shares AppreciationEvolution of US$ 100 Invested in March 31, 1990

The Reinvestiment of Dividends received in Banco itaú was not taken into consideration US$

90 91 92 93 94 95 96 97 98 99 00

Real Devaluation

US$100

0

4,000

8,000

12,000

16,000

20,000

Annual Appreciation ( in US$ ):10 YEARS (Average) 66.94 %5 YEARS (Average) 35.41 %12 MONTHS (Average) 81.78 %2000 2.55 %

Average Annual Appreciation of 66.94% in the last 10 years

US$ 16,884

47

Consolidated

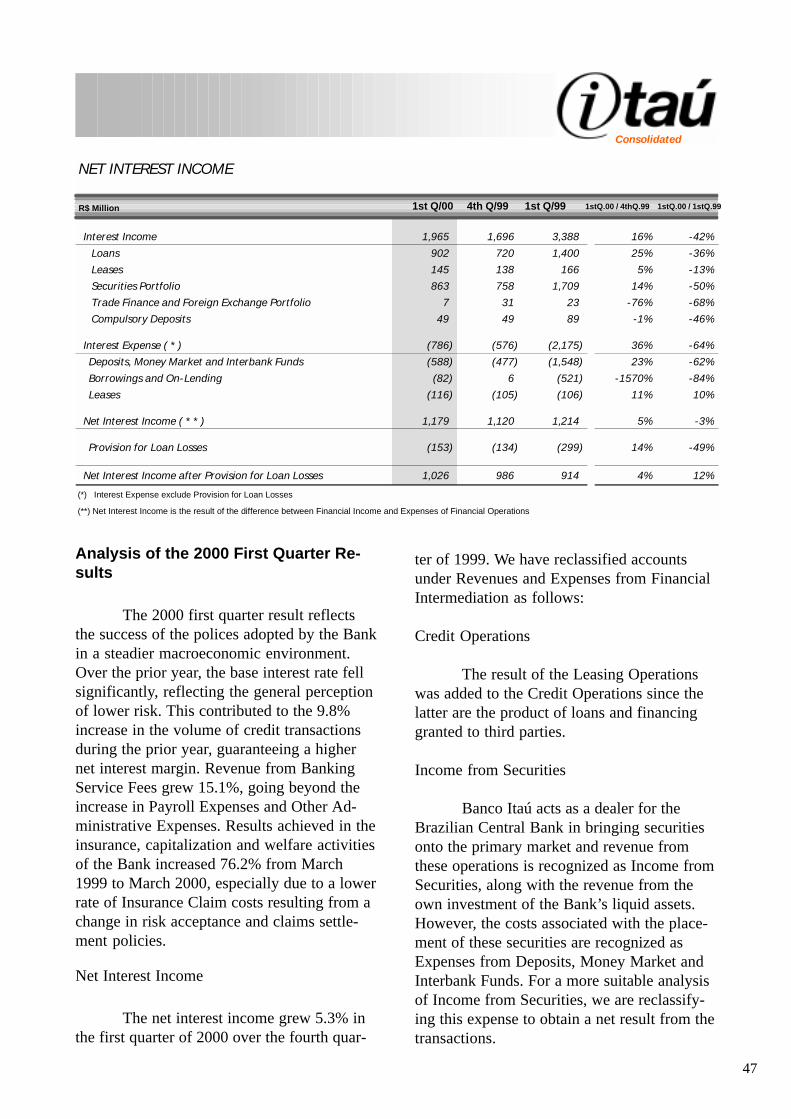

Analysis of the 2000 First Quarter Re-sults

The 2000 first quarter result reflectsthe success of the polices adopted by the Bankin a steadier macroeconomic environment.Over the prior year, the base interest rate fellsignificantly, reflecting the general perceptionof lower risk. This contributed to the 9.8%increase in the volume of credit transactionsduring the prior year, guaranteeing a highernet interest margin. Revenue from BankingService Fees grew 15.1%, going beyond theincrease in Payroll Expenses and Other Ad-ministrative Expenses. Results achieved in theinsurance, capitalization and welfare activitiesof the Bank increased 76.2% from March1999 to March 2000, especially due to a lowerrate of Insurance Claim costs resulting from achange in risk acceptance and claims settle-ment policies.

Net Interest Income

The net interest income grew 5.3% inthe first quarter of 2000 over the fourth quar-

ter of 1999. We have reclassified accountsunder Revenues and Expenses from FinancialIntermediation as follows:

Credit Operations

The result of the Leasing Operationswas added to the Credit Operations since thelatter are the product of loans and financinggranted to third parties.

Income from Securities

Banco Itaú acts as a dealer for theBrazilian Central Bank in bringing securitiesonto the primary market and revenue fromthese operations is recognized as Income fromSecurities, along with the revenue from theown investment of the Bank’s liquid assets.However, the costs associated with the place-ment of these securities are recognized asExpenses from Deposits, Money Market andInterbank Funds. For a more suitable analysisof Income from Securities, we are reclassify-ing this expense to obtain a net result from thetransactions.

NET INTEREST INCOME

Interest Income 1,965 1,696 3,388 16% -42% Loans 902 720 1,400 25% -36% Leases 145 138 166 5% -13% Securities Portfolio 863 758 1,709 14% -50% Trade Finance and Foreign Exchange Portfolio 7 31 23 -76% -68% Compulsory Deposits 49 49 89 -1% -46%

Interest Expense ( * ) (786) (576) (2,175) 36% -64% Deposits, Money Market and Interbank Funds (588) (477) (1,548) 23% -62% Borrowings and On-Lending (82) 6 (521) -1570% -84% Leases (116) (105) (106) 11% 10%

Net Interest Income ( * * ) 1,179 1,120 1,214 5% -3%

Provision for Loan Losses (153) (134) (299) 14% -49%

Net Interest Income after Provision for Loan Losses 1,026 986 914 4% 12%

(*) Interest Expense exclude Provision for Loan Losses

(**) Net Interest Income is the result of the difference between Financial Income and Expenses of Financial Operations

R$ Million 1st Q/00 4th Q/99 1st Q/99 1stQ.00 / 4thQ.99 1stQ.00 / 1stQ.99

48

Consolidated

REALLOCATED NET INTEREST INCOME

Loans 902 720 1,400 25% -36%Leases 29 34 61 -15% -53%

Total of Loans 930 753 1,461 24% -36%Securities Portfolio 863 758 1,709 14% -50%Repurchase Commitments Expenses (163) (43) (331) 277% -51%

Total of Securities Portfolio 699 715 1,379 -2% -49%Trade Finance and Foreign Exchange Portfolio 7 31 23 -76% -68%

Total of Trade Finance and Foreign Exchange Portfolio 7 31 23 -76% -68%Adjusted Expenses of Deposits, Money Market and Interbank Funds (425) (434) (1,218) -2% -65%Compulsory Deposits 49 49 89 -1% -46%Borrowings and On-Lending (82) 6 (521) -1570% -84%

Total of Funding Expenses (458) (380) (1,649) 21% -72%

Net Interest Income 1,179 1,120 1,214 5% -3%

R$ Million 1stQ.00 / 4thQ.99 1stQ.00 / 1stQ.99 1st Q/00 4th Q/99 1st Q/99

Income from Foreign Exchange

This item was not reclassified.

Borrowings, Deposits, Money Market andInterbank Funds

The expenses with Borrowings, De-posits, Money Market and Interbank FundsOperations were added to the expenses of onBorrowings, Assignment and Pass-ThroughOperations. We have subtracted the Expenses

from Repurchase Agreements from Borrow-ings, Deposits, Money Market and InterbankFunds Operations as described under theIncome from Securities item.

Considering that part of the depositsmust by law be deposited with the CentralBank and that they have the same financialcosts as the funds to which they relate, wehave deducted the revenue with MandatoryApplications from the total of the Expensesfrom Borrowings, Deposits, Money Marketand Interbank Funds. Therefore, we have thefollowing considerations: