Integrated Reporting: The Brave New World · integrated reporting to ensure the survival of this...

19

29/11/2016 1 Integrated Reporting: The Brave New World By Professor Brendan O’Connell, School of Accounting, RMIT University President, ICMA Australia [email protected] 1 Presentation Structure • Introduction to IR and what it is • Examples of IR in Practice • Potential Benefits of IR • Potential Issues with IR • Management Accounting Implications of IR • Frontiers of IR: Extending to the Balanced Scorecard Approach • Frontiers of IR: 5-Star Reporting Index 2

Transcript of Integrated Reporting: The Brave New World · integrated reporting to ensure the survival of this...

29/11/2016

1

Integrated

Reporting: The

Brave New WorldBy

Professor Brendan O’Connell, School of

Accounting, RMIT University

President, ICMA Australia

Presentation Structure

• Introduction to IR and what it is

• Examples of IR in Practice

• Potential Benefits of IR

• Potential Issues with IR

• Management Accounting Implications of IR

• Frontiers of IR: Extending to the Balanced

Scorecard Approach

• Frontiers of IR: 5-Star Reporting Index

2

29/11/2016

2

Introduction

• Integrated reporting [IR] is the latest reporting

innovation, emerging in 2010 with the formation of the

International Integrated Reporting Council (IIRC).

• The IIRC developed the International /IRS Framework to

“to establish Guiding Principles and Content Elements

that govern the overall content of an integrated report”.

• Not the next generation of sustainability reporting but as

an attempt to promote “a more cohesive and efficient

approach to corporate reporting that draws on different

reporting strands” (IIRC, 2013, p. 2). 3

What is Integrated Reporting

• IR brings together material

information about an

organization’s strategy,

governance, performance and

prospects,

• in a way that reflects the

commercial, social and

environmental context within

which it operates.

4

29/11/2016

3

IR Explained

• “integrated reporting combines the most

material elements of information currently

reported in separate reporting strands. . . in a

coherent whole, and

• importantly shows the connectivity between

them and explains how they affect the ability of

an organization to create and sustain value in the

short, medium and long term” (IIRC, 2011, p. 6).

5

Continued• It states that it seeks to achieve a reporting framework

that: ‘reflects the use of and effect on all the resources

and relationships or ‘‘capitals’’ (human, natural and

social, as well as financial, manufactured and intellectual)

on which the organization and society depend for

prosperity; and

• It reflects and communicates the interdependence

between the success of the organization and the value it

creates for investors, employees, customers and, more

broadly, society’ (IIRC, 2011, p. 5).

• Next slide some examples of each type of capital as

adopted from Flower (2015: 3). 6

29/11/2016

4

Type of Capital Internal to Firm External to Firm

Financial Cash, Debts -

Manufactured Factories, machines Public roads,

Schools

Human Employees -

Intellectual Patents, systems -

Natural Livestock,

commodities

Flora and fauna

Social Brands, reputation Cohesive society,

stable government

Types of Capital

7

IR Idea• A firm’s integrated report should indicate how the firm,

through its activities, has created value, as measured by the

increase less the decrease in the value of these six capitals.

• Thus the IIRC’s concept of ‘capitals’ covers not only the

firm’s capital in the conventional sense, but also the capital

of society, for example the environment.

• Hence many of the capitals included in the integrated

report are not owned by the firm.

8

29/11/2016

5

Continued• Value created by an organization over time manifests itself in

increases, decreases or transformations of the capitals caused by

the organization’s business activities and outputs.

• That value has two aspects – Value created:

• For the Organization Itself, which enables financial returns to

the providers of financial capital;

• For Others (i.e. stakeholders and society at large) - this happens

through a wide range of activities, interactions and

relationships. . .

• for example, the effects of the organization’s business activities

on customer satisfaction, suppliers’ willingness to trade with the

organization. . .

• When these interactions, activities and relationships are

material to the organization’s ability to create value for itself,

they are included in the integrated report’.

9

Externalities• ‘This includes taking account of the extent

to which effects on the capitals have been externalized (i.e. the costs and other effects on capitals that are not owned by the organization). . .

• Externalities may ultimately increase or decrease value created for the organization;

• therefore providers of financial capital need information about material externalities to assess their effects and to allocate capital accordingly’ (IIRC, 2013a, paragraphs 2.6–2.8).

• These paragraphs make clear that the IIRCconsiders that the integrated report should cover ‘value to others’ only to the extent that this is ‘material to the organization’s ability to create value for itself’.

10

29/11/2016

6

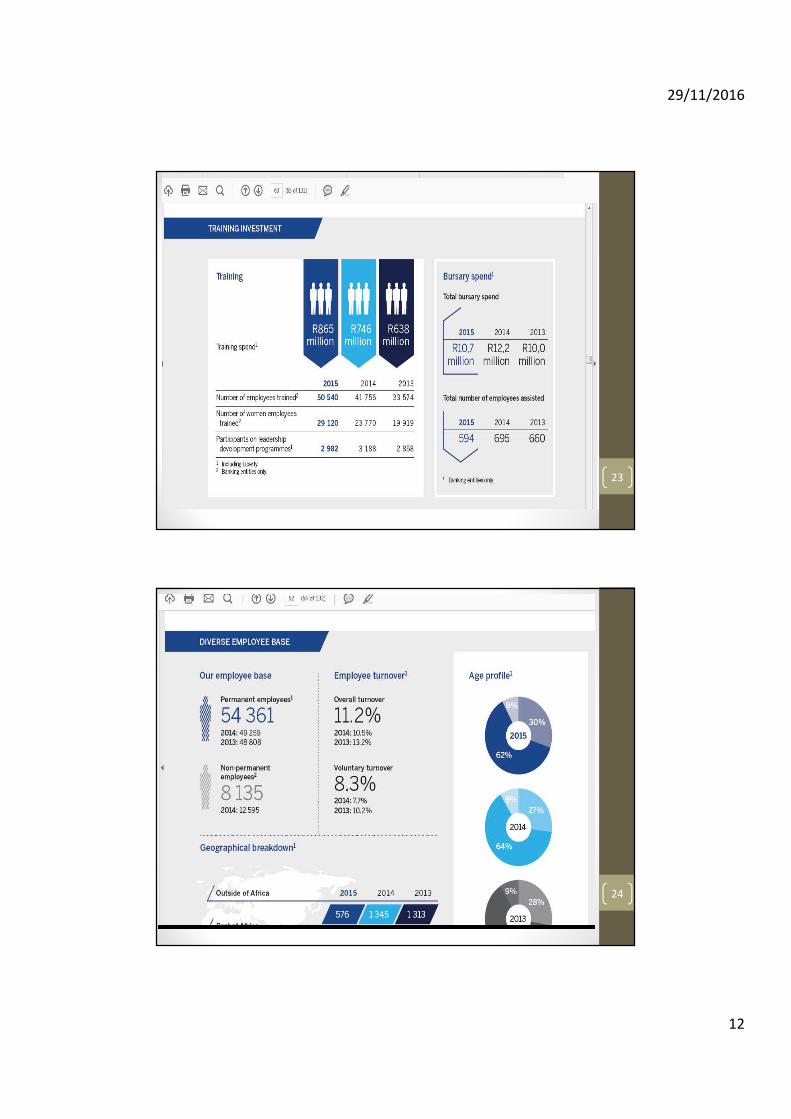

Examples of IR

• The first example is taken from the Annual

Report 2015/16 of People’s Leasing and Finance

PLC.

• This Report is held out to be an exemplar of IR

by:

• http://examples.integratedreporting.org/organis

ation/260

• The second example is taken from the 2015

Annual Report of Standard Bank Group (Sth.

African bank – IR is mandatory there). 11

12

29/11/2016

7

13

14

29/11/2016

8

15

16

29/11/2016

9

17

18

29/11/2016

10

19

20

29/11/2016

11

21

22

29/11/2016

12

23

24

29/11/2016

13

Potential Benefits of IR• It may provide forward-looking information.

• it may demonstrate how organisations create and sustain value

• it may reduce reputational risk and enables companies to make

better financial and non-financial decisions

• it may break down operational and reporting silos in

organisations

• It may lead to improved systems and processes

• It may help drive organisational change towards more

sustainable outcomes

• It may help improve resource allocation decision making.

25

Potential Issues with IR• Criticised for its focus on financial capital providers to

the detriment of the information demands and needs of

other key stakeholders.

• It is targeted at large, publicly listed companies,

excluding small to medium-sized organisations, and

those in the government and non-government sectors.

• In regards to the six capitals, the “subjective” concepts

of stock and flow of capitals create difficulties for

organisations “to explain some of their capitals beyond

insubstantial narratives” (Cheng et al., 2014, p. 98). 26

29/11/2016

14

Potential Issues with IR (Cont.)• Question about the assurance aspects of integrated

reporting and whether the International /IRS Framework

provides suitable criteria and appropriate subject matter for

reports to be assured.

• Questionable whether, in the absence of assurance,

organisational stakeholders will be interested enough in

integrated reporting to ensure the survival of this new

corporate reporting form and therefore whether the “mass

implementation of integrated reporting is likely to

eventuate” (Burritt, 2012, p. 391).

27

Management Accounting

Implications of IR• Despite its potential to enhance management

decision-making as outlined earlier, there is little

evidence to date that this has occurred in practice.

• Stubbs and Higgins (2014) using interviews with

organisations in varying stages of implementing IR

found that there was no evidence that IR was

challenging the underlying DNA of the organisation.

• There was no evidence that integrated reporting

initiatives led to changes in the intangible elements

of the organisations (core beliefs, values, norms or

mission/ purpose). 28

29/11/2016

15

Management Accounting

Implications of IR• Nor was there evidence that a shift to integrated reporting reflects

a people centred and environment-centred organisation with a

focus on stewardship of all capitals.

• However, there was some evidence of cross-functional teams and

broadening out of constituencies involved in the reporting

process.

• Haji and Hossain (2016) in a study of South African companies’ IR

found that there was no improvement in the underlying substance

of organisational reports even though the terminology of IR had

been adopted by firms.

• Enhancing corporate reputation and organisational legitimacy

seem to be the main motivators for IR at present rather than using

it as a key tool for reform or management decision-making (Haji

and Hossain 2016).

29

Financial PerspectiveGoals Measures

“How efficient is our deployment of resources ?”

Internal Business PerspectiveGoals Measures

Customer PerspectiveGoals Measures

“How do customers see us?”

Innovation and

Learning PerspectiveGoals Measures

Direction

Strategic

Direction

“How can we continue to improve and add value?”

“What must we excel at?”

• The Balanced Scorecard is a conceptual framework for translating an organisation's vision into a set of performance indicators distributed among four perspectives.

• An Integrated Reporting Balanced Scorecard will enable management to have a vision of the strategic implications of implementing integrated reporting in their organisations.

Frontiers of IR: A Potential Way Forward -

Extending the Balanced Scorecard Concept

29/11/2016

16

Financial

Goals & Measures

Intellectual

Goals & Measures

Manufactured

Goals & Measures

Natural

Goals & Measures

Integrated

Social

Goals & Measures

Human

Goals & Measures

Balanced Integrated Reporting

31

Measures of “Hard Capital”

Measures of “Soft Capital”

Measuring the Impact of

Integrated Reporting• IIRC requires a firm to report on the effect on its activities on

society and on the environment only to the extent that there is a

material impact on its own operations.

• However, there is no one number to indicate/ summarise the net-

change in value within each of these six capitals, as many of the

‘pillars’ that makes up a particular capital cannot be added (apples

& oranges problem).

• Firms have to use “subjective” concepts of stock and flow of

capitals – this create difficulties for organisations “to explain some

of their capitals beyond insubstantial narratives”.

• An early attempt to obtain a single-number to rate the various

strands of corporate reporting will now be looked at.32

29/11/2016

17

• As demonstrated IR Reports do not result in one number

(financial or otherwise) that can encapsulate the value created

by all the” capitals”.

• What was required, therefore, was an approach to truly

integrate and evaluate the initiatives taken in the multiple-areas

of economic, environmental, social, governance and

empowerment (which must ultimately form the totality of an

organisation’s value enhancing initiatives) and obtain one-

number.

• As initiatives in these multiple areas are reported by public

companies, the 5-STAR Reporting IndexTM was developed and

prescribes a process and metrics for a holistic approach to

value-based reporting.

• This approach, developed by the ICMA sponsored Institute for

the Advancement of Corporate Reporting and Assurance

(IACRA), combines the reporting in the above 5-areas into one-

number for the ranking of all publicly listed companies.

Another Potential Way Forward

33

5-STAR Reporting approach is to collect and classify the information

presented in annual reports, corporate web-pages and other publicly

available information in the 5-Reporting areas of Economic,

Environmental, Social, Governance and Empowerment along the lines

of a control framework as follows:

• Primary Stakeholder Expectations

• Objectives

• Strategies

• Implementation

• Results

34

The 5-Star Reporting Index

29/11/2016

18

• The objective of the 5-Star approach is to rate the quality and comprehensiveness (and therefore the understandability) of publicly available information to multiple stakeholders.

• This was done using the following approach:

• Step 1 : Content Analysis of Publicly Available Information

• Step 2: Judge Ratings of Content (Rating between 0-5 of the Reporting on each criterion (strand) of the Control Framework)

• Step 3: Development of Criterion Weights

• The ICMA conducted 16 research symposiums in 12 countries (343 respondents) to determine stakeholder perceptions regarding the weights to be used.

• E.g. Actual Implementation was given a higher weight than just stating a strategy that required future action).

• Step 4: Multiply the Content analysis judge rated scores with the

Criterion Weights to obtain a Group score for each Reporting area (i.e. Rate x Weight)

• Step 5: Add the Group scores in each Reporting area to obtain a 5-Star

score for the company (e.g. Max score 25 = 5-Stars)

35

The 5-Star Approach

5-STAR RATING: AUSTRALIAN COMPANY ANALYSIS

COMPANY ANALYSIS

Company

Economic

Reporting

Rating

Environme

ntal

Reporting

Rating

Social

Report

ing

Rating

Corpor

ate

Gover

nance

Rating

Empo

werm

ent

Report

ing

Rating

Overall

Rating

Star

Rating

AGL ENERGY LIMITED (AGK) 3.32 2.52 3.30 2.90 0.00 12.04 ***

ANSELL LIMITED (ANN) 3.64 2.76 3.48 3.25 0.00 13.13 ***

ASCIANO GROUP (AIO) 3.64 3.42 3.36 1.80 0.00 12.22 ***

ASX LIMITED (ASX) 3.64 1.08 1.20 2.85 0.00 8.77 **

AUSTRALIAN WORLDWIDE EXPLORATION LIMITED (AWE) 2.36 1.62 0.72 2.30 0.00 7.00 **

BENDIGO AND ADELAIDE BANK LIMITED (BEN) 2.80 1.62 3.30 3.80 0.12 11.64 ***

BILLABONG INTERNATIONAL LIMITED (BBG) 3.08 2.46 2.04 3.30 0.00 10.88 ***

BORAL LIMITED (BLD) 2.64 2.94 2.58 4.15 0.20 12.51 ***

BRAMBLES LIMITED (BXB) 4.00 2.40 6.00 4.50 0.68 17.58 ****

CENTENNIAL COAL COMPANY LIMITED (CEY) 2.68 1.56 0.60 1.55 0.00 6.39 **

CFS RETAIL PROPERTY TRUST (CFX) 3.16 4.98 1.02 4.25 0.00 13.41 ***

COCHLEAR LIMITED (COH) 3.24 0.96 2.46 4.30 0.20 11.16 ***

COMPUTERSHARE LIMITED (CPU) 3.80 2.58 3.12 4.30 0.20 14.00 ***

CONNECTEAST GROUP (CEU) 3.04 3.00 3.36 4.00 0.00 13.4 ***

CONSOLIDATED MEDIA HOLDINGS LIMITED (CMJ) 2.92 0.24 0.96 4.15 0.00 8.27 **

CROWN LIMITED (CWN) 2.72 4.62 3.84 4.75 0.68 16.61 ****

FAIRFAX MEDIA LIMITED (FXJ) 3.40 2.46 2.52 3.95 0.20 12.53 ***

FOSTER’S GROUP LIMITED (FGL) 2.56 2.16 0.96 3.55 0.36 9.59 **

GOODMAN FIELDER LIMITED (GFF) 3.40 1.14 0.00 1.95 0.20 6.69 **

HARVEY NORMAN HOLDINGS LIMITED (HVN) 3.00 0.60 0.00 4.00 0.20 7.80 **

ING OFFICE FUND (IOF) 2.56 3.78 0.00 4.40 0.20 10.94 ***

INSURANCE AUSTRALIA GROUP LIMITED (IAG) 3.36 4.20 3.78 4.20 0.20 15.74 ****

JAMES HARDIE INDUSTRIES N.V. (JHX) 4.00 3.24 4.74 3.95 0.40 16.33 ****

JB HI-FI LIMITED (JBH) 3.40 3.60 2.82 5.00 0.00 14.82 ***

Recent Australian

Results

29/11/2016

19

5 Steps to a Better Ranking

1. Higher weighting for voluntary disclosure of

environmental, social, governance and empowerment

data.

2. Higher weighting for implementing activities.

3. Providing quantitative measures to show progress and

results is highly rated.

4. Good and bad news disclosures treated equally

(disclosure is what matters).

5. Providing separate discussions for each of the “bottom

lines” makes for greater transparency and easier

analysis. 37

SourcesAdams, C.A. (2015). “The International Integrated Reporting Council: A call to action”, Critical

Perspectives on Accounting, 27: 23-28.

Brown, J., & Dillard, J. (2014). “Integrated reporting: On the need for broadening out and

opening up”, Accounting, Auditing & Accountability Journal, 27(7): 1120-1156.

de Villiers, C., Rinaldi, L., & Unerman, J. (2014). “Integrated reporting: Insights, gaps and an

agenda for future research”, Accounting, Auditing & Accountability Journal, 27(7): 1042-1067.

Flower, J. (2015). “The International Integrated Reporting Council: A story of failure”, Critical

Perspectives on Accounting, 27: 1-17.

Haji, A., & Hossain, D. M. (2016).” Exploring the implications of integrated reporting on

organisational reporting practice”, Qualitative Research in Accounting and Management,

13(4): 415-444.

IIRC (2011). Towards Integrated Reporting, Communicating value in the 21st Century. 2011.

Available on the IIRC’s web-site, www.theiirc.org/wp-content/uploads/ 2011/09/IR-

Discussion-Paper-2011_single.pdf.

IIRC (2013). The International /IRS Framework, The International Integrated Reporting Council,

London.

People’s Leasing and Finance PLC. Annual Report 2015-16. Accessed on 14 November 2016

from: http://examples.integratedreporting.org/organisation/260

Ratnatunga, J. & Jones, S. (2012). “A methodology to rank the quality and comprehensiveness

of sustainability information provided in publicly listed company reports; in Jones, S. (Editor)

“Issues in Sustainability Accounting, Assurance and Reporting’, Emerald, pp. 225-266

Stubbs, W., & Higgins, C. (2014). “Integrated reporting and internal mechanisms of change”,

Accounting, Auditing & Accountability Journal, 27(7), 1068-1089.

38