Insurance Law 2

48

Insurance Code of the Philippines PD No. 1460, as amended July 26, 2012

-

Upload

melissa-mozo-abansi -

Category

Documents

-

view

216 -

download

0

Transcript of Insurance Law 2

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 1/48

Insurance Code of the Philippines

PD No. 1460, as amended

July 26, 2012

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 2/48

Insurance…

• A contract of insurance is an agreementwhereby one undertakes for a

consideration to indemnify another againstloss, damage or liability arising from anunknown or contingent event. (Section 2)

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 3/48

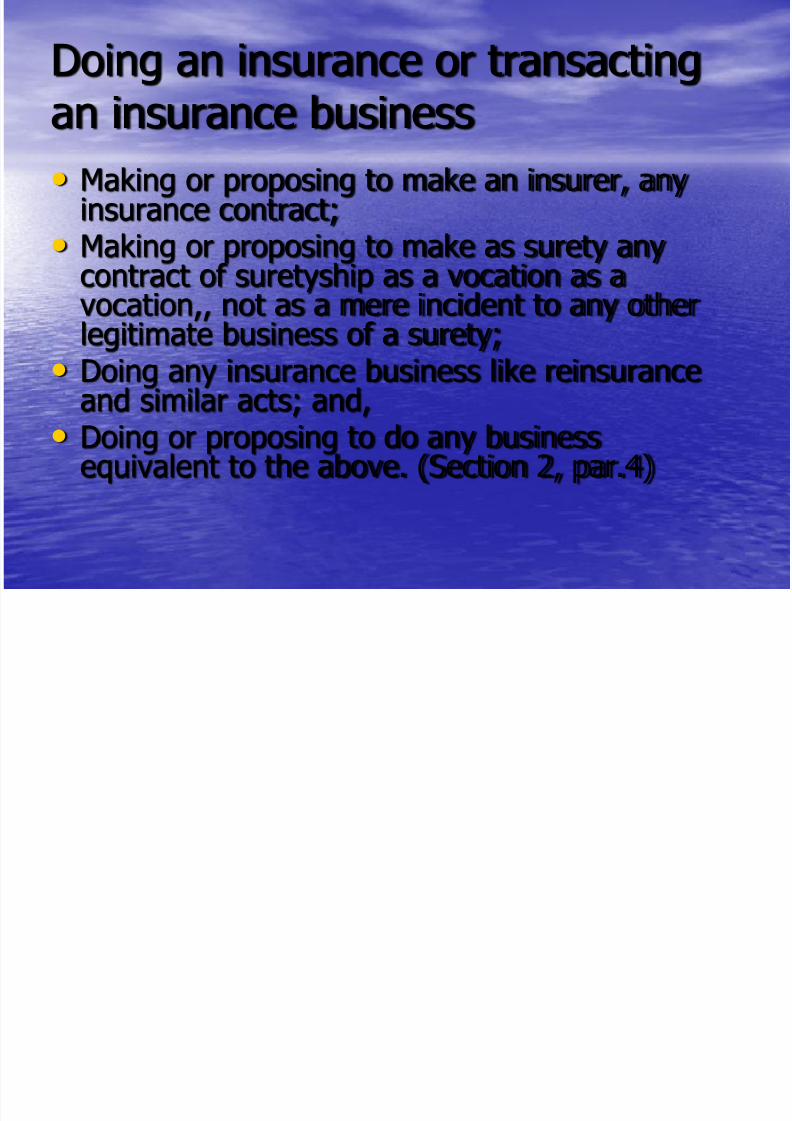

Doing an insurance or transactingan insurance business

• Making or proposing to make an insurer, anyinsurance contract;

• Making or proposing to make as surety any

contract of suretyship as a vocation as avocation,, not as a mere incident to any otherlegitimate business of a surety;

• Doing any insurance business like reinsurance

and similar acts; and,• Doing or proposing to do any businessequivalent to the above. (Section 2, par.4)

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 4/48

Characteristics…

• Insurance as a risk distributing device

– By paying a pre-determined amount into a

general fund out of which payment will bemade for an economic loss of a defined type,each member contributes to a small degreetoward compensation for losses suffered by

any member of the group

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 5/48

Characteristics…

• Contract of adhesion or fine print rule – In case of doubt, the contract shall be

interpreted strictly against the insurer andliberally in favor of the insured

• Aleatory – The obligation of the insurer to pay the

proceeds of the insurance arises only uponthe happening of an event which is uncertainor which is to occur at an indeterminate time

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 6/48

Characteristics…

• Commutative

– The amount paid by the insured is deemed theequivalent of the protection given by the insuredbased on the insurance contract

• Contract of indemnity

– The insured who has insurable interest over a

property is only entitled to recover the amount of actual loss sustained and the burden is upon him toestablish the amount of such loss

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 7/48

Characteristics….

• Applicable only to property insurance, exceptcreditor insuring the life of his debtor;

• Life insurance is not a contract of indemnity.There is no overinsurance in life insurance

• There is overinsurance only in propertyinsurance and if this is present, the insurer isonly liable up to the extent of the loss.

• Insurance contracts are not wagering contracts.(Section 4)

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 8/48

Characteristics…

• Uberrimae fides contract

– The contract of insurance is one of perfect good faithnot for the insured alone, but equally so for theinsurer, in fact, it is more so for the latter since itsdominant bargaining position carried with it stricterresponsibility.

• Personal contract

– The law presumes that the insured considered thepersonal qualifications of the insured in approving theinsurance application.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 9/48

Elements of insurance

• Existence of an insurable interest

• Risk of loss

• Assumption of risks

• Scheme to distribute losses; and,

• Payment of premiums

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 10/48

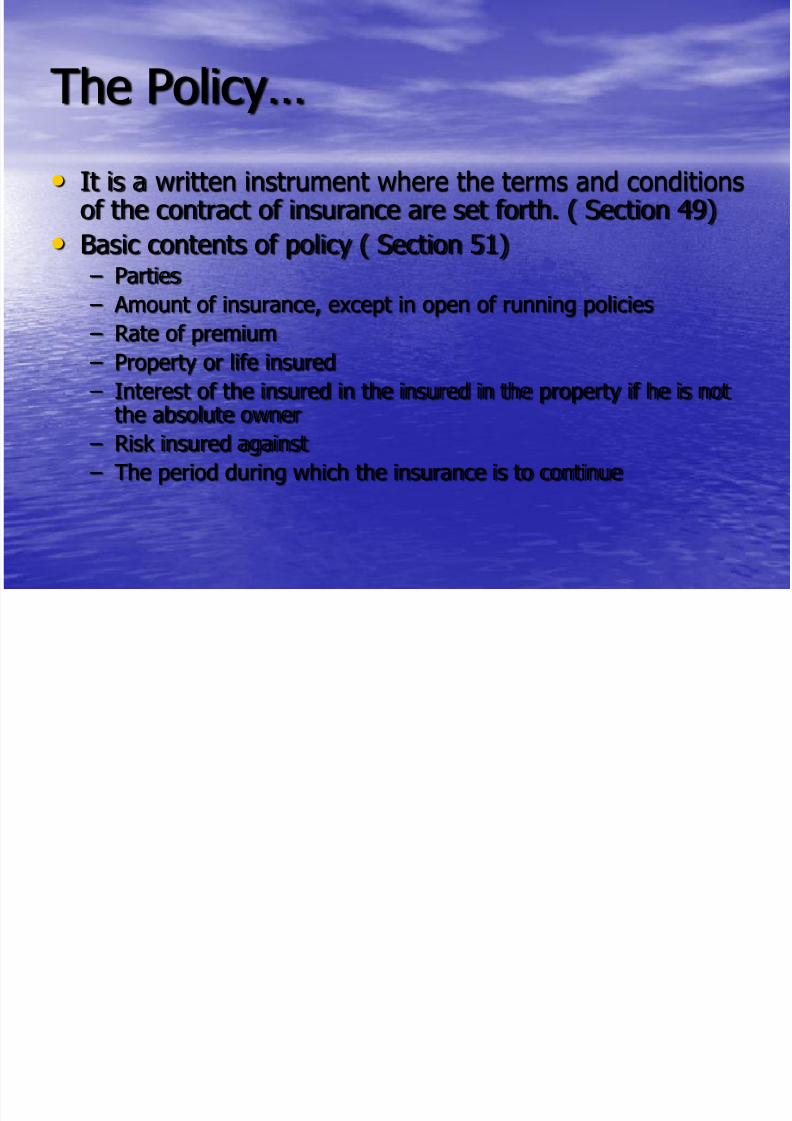

The Policy…

• It is a written instrument where the terms and conditionsof the contract of insurance are set forth. ( Section 49)

• Basic contents of policy ( Section 51)

– Parties – Amount of insurance, except in open of running policies

– Rate of premium

– Property or life insured

– Interest of the insured in the insured in the property if he is not

the absolute owner – Risk insured against

– The period during which the insurance is to continue

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 11/48

The Policy…

• Rider

– An attachment to an insurance policy that

modifies the conditions of the policy byexpanding or restricting its benefits orexcluding certain conditions from thecoverage

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 12/48

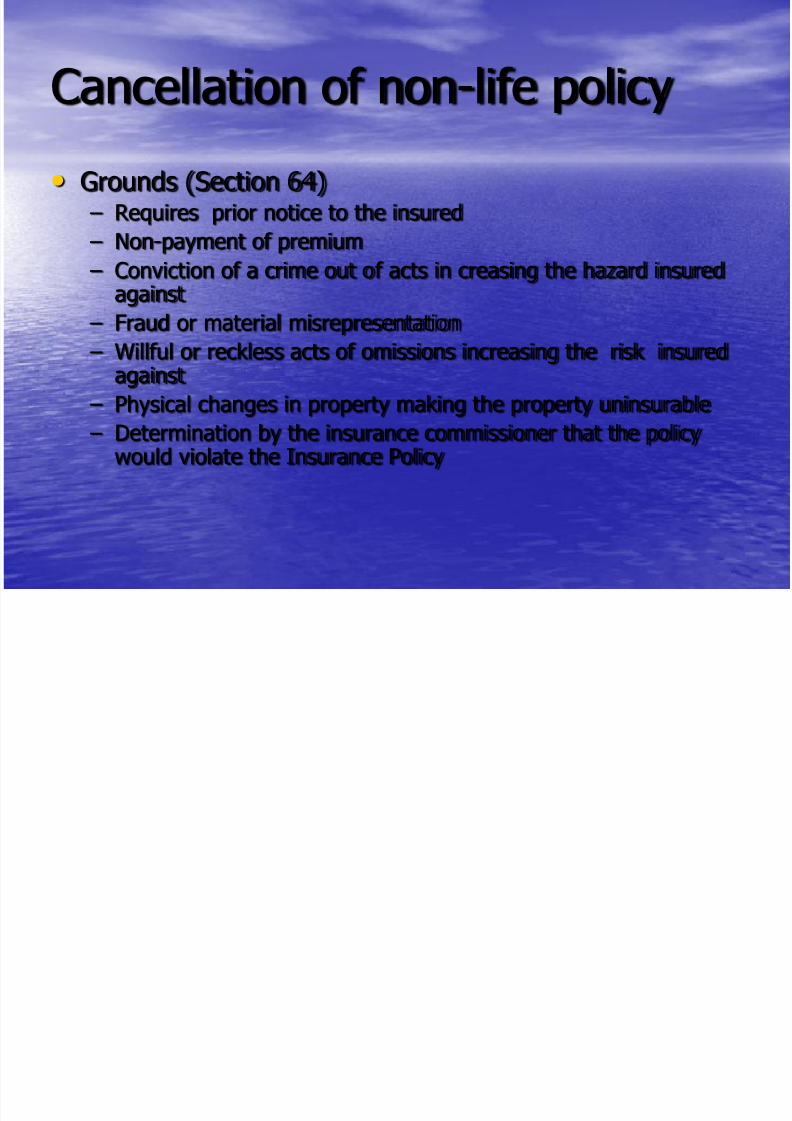

Cancellation of non-life policy

• Grounds (Section 64) – Requires prior notice to the insured

– Non-payment of premium

– Conviction of a crime out of acts in creasing the hazard insuredagainst

– Fraud or material misrepresentation

– Willful or reckless acts of omissions increasing the risk insuredagainst

– Physical changes in property making the property uninsurable – Determination by the insurance commissioner that the policywould violate the Insurance Policy

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 13/48

Requisites for cancellation(Section 65)

• Prior notice of cancellation to insured

• Notice must be based on the occurrence aftereffective date of the policy or one or more of thegrounds mentioned;

• Notice must be in writing, mailed or delivered tothe insured at the address shown in the policy;and,

• Notice must state the grounds relied uponprovided in Section 64 of ICP.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 14/48

Kinds of Policies

• Open policy- value of the thing insured is notagreed upon, but left to be ascertained at thetime of loss (Section 60)

• Valued policy-definite valuation is agreed byboth parties and written on the face of the policy• Running policy- contemplates successive

insurances and which provides that the subject

of the policy may from time to time be defined.(Section 62)• Life insurance policies are always valued

policies.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 15/48

Types of Insurance Contracts

• Life insurance

– Individual life- insurance on human live and insuranceappertaining thereto or connected therewith ( Section179)

– Group life- a blanket policy covering a number of individuals. Its most common form is an insurancethat provides life or health insurance coverage for the

employees of a single employer.

– Industrial life

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 16/48

Types…

• Non-life insurance

– Marine

– Fire – Casualty

• Contracts of suretyship

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 17/48

Parties to Insurance Contract

• Insurer

– The person who undertakes to indemnify

another – May be individuals, partnership, associations

or corporations

– Insurance corporation

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 18/48

Parties…

• Insured-the person with capacity tocontract and having an insurable interest

in the life or property of the insured• Beneficiary- person designated to received

proceeds of policy when the risk attaches

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 19/48

Designation of the beneficiary

• When one insures his own life, he maydesignate any person as beneficiary;

• If the person who will insure the life of anotherpayable to himself, he must have insurableinterest on the life of the person he is insuring;

• In property insurance, the beneficiary must haveinsurable interest in the property

• The designation is revocable unless providedotherwise.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 20/48

Insurable Interest

• Life Insurance

• Every person has an insurable interest in the life andhealth:

– Of himself, of his spouse and of his children; – Of any person on whom he depends wholly or in part for

education or support or in whom he has pecuniary interest

– Of any person under a legal obligation to him for the payment of money or respecting property or services, of which death mightdelay or prevent the performance

– Of any person upon whose life any estate or interest vested inhim depends

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 21/48

Insurable interest…

• Insurable interest in property is anyinterest therein, or liability in respect

thereof and it may consist in an existinginterest, an inchoate interest founded onan existing interest or any expectancy

coupled with an existing interest

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 22/48

Insurable interest…

• A person has an insurable interest in theproperty if he derives pecuniary benefit or

advantage from its preservation or wouldsuffer pecuniary loss, damage or prejudiceby its destruction whether he has or has

no title in or lien upon or possession of theproperty.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 23/48

Insurable interest in propertyvs insurable interest in life

Limited to the actual value of the interest thereon

Unlimited save in lifeinsurance effected by acreditor on the life of his

debtorExists at the time the policytakes effect and at the timeof loss

Exists at the time the policytakes effect but need not bepresent at the time of loss

No need for legal basis There must be legal basis

Need for insurable interest of the beneficiary

Not necessary if the insurerinsured himself

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 24/48

Risks insured against

• May be any contingency or unknown event thehappening of which will damnify a person havinginsurable interest or will create liability against

him. Even fortuitous events may be insuredagainst.• General Rule: A future event is the only event

that can be covered by an insurance contact.

•Exception: A event may be covered by a marineinsurance- if the loss of the vessel in the pastcould not have been known by ordinary meansof communication.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 25/48

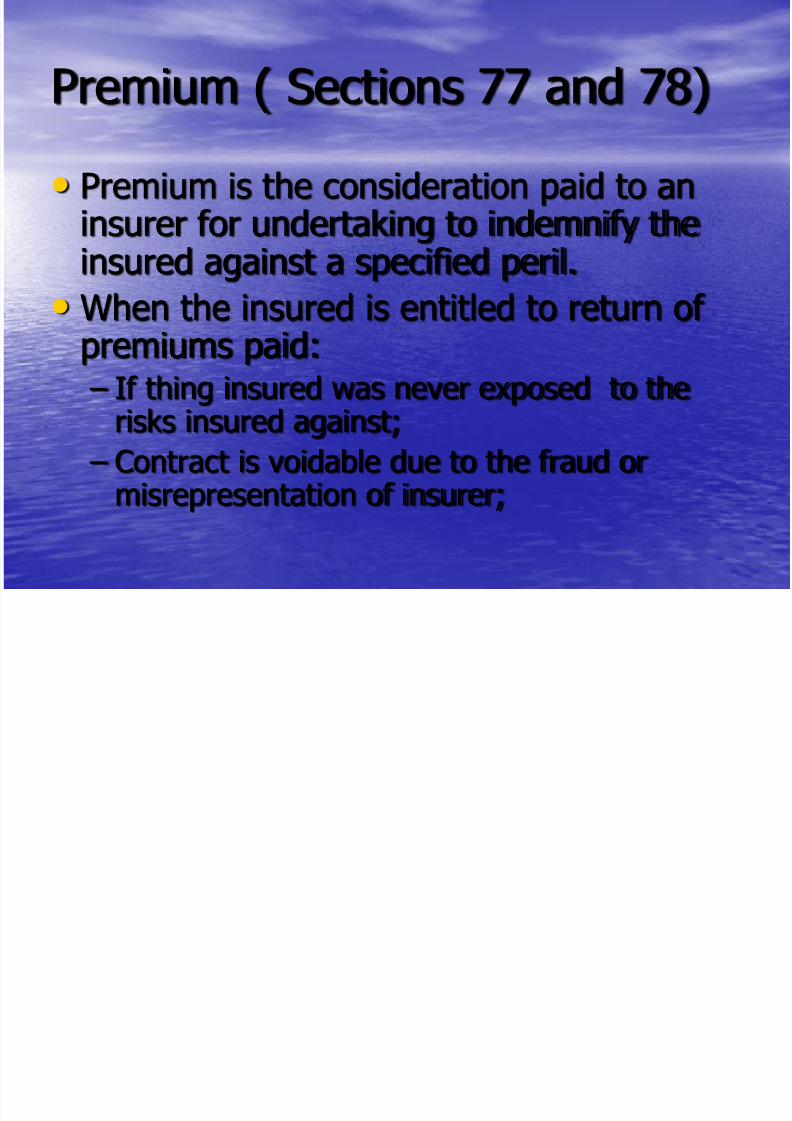

Premium ( Sections 77 and 78)

• Premium is the consideration paid to aninsurer for undertaking to indemnify the

insured against a specified peril.• When the insured is entitled to return of premiums paid: – If thing insured was never exposed to the

risks insured against; – Contract is voidable due to the fraud or

misrepresentation of insurer;

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 26/48

Return of premiums…

• Insurer never incurred liability;• When the insurance is for a definite period and

the insured surrenders his policy before the

termination thereof;• Contract is voidable because of the existence of

facts of which the insured was ignorant withouthis fault;

• When there is over-insurance;• When rescission is granted due t the insurer’sbreach of contract.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 27/48

Devices for ascertaining andcontrolling risk and loss

• Concealment- a neglect to communicate thatwhich a party knows and ought to communicate( Section 26)

• Representation- factual statements made by theinsured at the time of or prior to the issuance of the policy to give information to the insurer and

otherwise induce him to enter into the insurancepolicy

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 28/48

Devices…

• Warranties- statements or promise by theinsured set forth in the policy itself orincorporated in it by proper reference. The same

may be expressed, implied, affirmative orpromissory

• Condition- the insurer must also protect himself against fraudulent claims of loss and this he

attempts to do by inserting in the policy variousconditions which take the form of conditionsprecedent.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 29/48

Incontestability Clause

• After a policy of life insurance made payable onthe death of the insured shall have been in forceduring the lifetime of the insured for a period of two years from the date of its issuance or of itslast reinstatement, the insurer cannot prove thatthe policy is void ab initio or is rescindable by

reason of the fraudulent concealment ormisrepresentation of the insured or his agent.(Section 48)

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 30/48

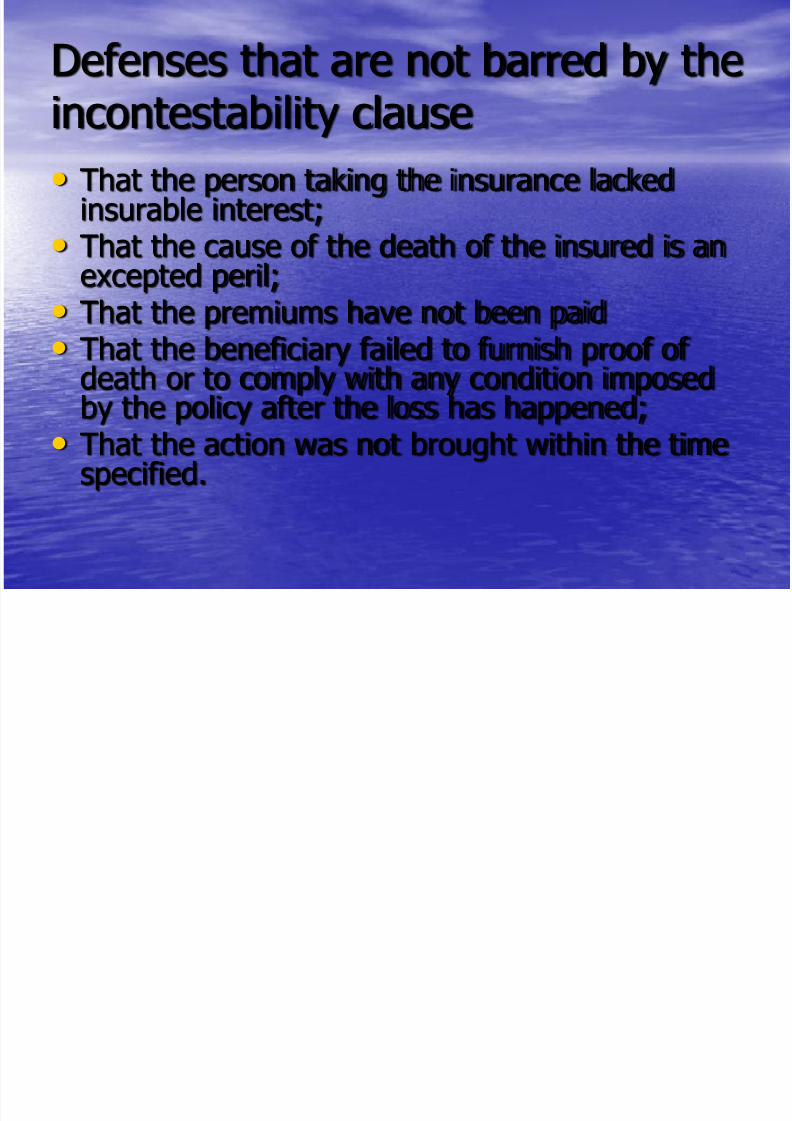

Defenses that are not barred by theincontestability clause

• That the person taking the insurance lackedinsurable interest;

• That the cause of the death of the insured is an

excepted peril;• That the premiums have not been paid• That the beneficiary failed to furnish proof of

death or to comply with any condition imposed

by the policy after the loss has happened;• That the action was not brought within the timespecified.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 31/48

Double insurance

• The person insured is the same;

• There are two or more insurers insuring

separately;• The subject matter is the same;

• The interest insured is also the same;

• The risk or peril insured against is likewisethe same

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 32/48

Double insurance vs. reinsurance

Involves the same interest Insurance of differentinterest

Insurer remains in such

capacity

Insurer becomes an insured

in relation to the reinsurer

Insured in the 1st contract isa party in the secondcontract

Original insured has nointerest in reinsurancecontract

Subject of insurance isproperty

Subject of insurance is theoriginal insurer’s risk

Insured has to give hisconsent

Consent of original insured isnot necessary

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 33/48

Liabilities…

• The insurer is liable if: – Loss the proximate cause of which is the peril

insured against;

– Loss the immediate cause of which is the perilinsured against except where the proximatecause is an excepted peril;

– Loss through negligence of the insured; – Loss caused by efforts to rescue the thing

from peril insured against

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 34/48

Liabilities…

• The insurer is not liable:

– Loss by insured’s willful act or gross

negligence; – Loss due to connivance of the insured; and,

– Loss where the expected peril is theproximate cause.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 35/48

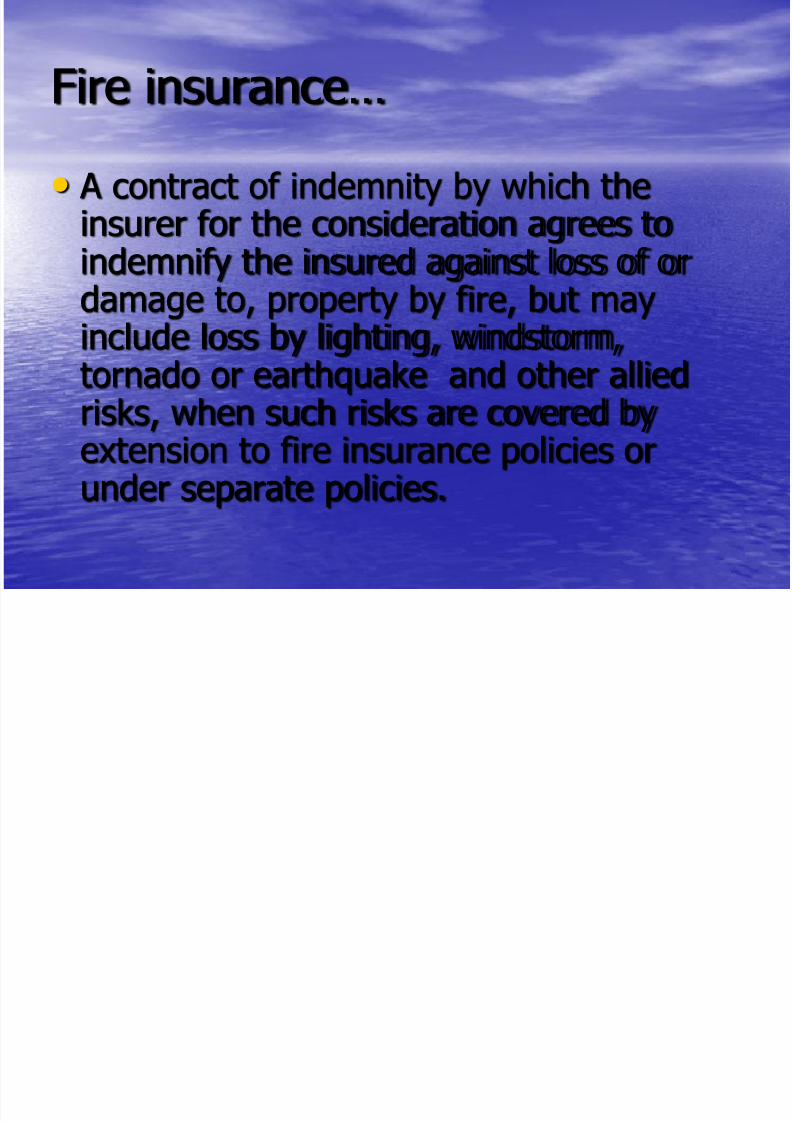

Fire insurance…

• A contract of indemnity by which theinsurer for the consideration agrees toindemnify the insured against loss of ordamage to, property by fire, but mayinclude loss by lighting, windstorm,tornado or earthquake and other allied

risks, when such risks are covered byextension to fire insurance policies orunder separate policies.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 36/48

Casualty insurance

• An insurance covering loss or liabilityarising from accident of mishap, excluding

those falling under other types of insurance as fire or marine;

• Third Party Liability-

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 37/48

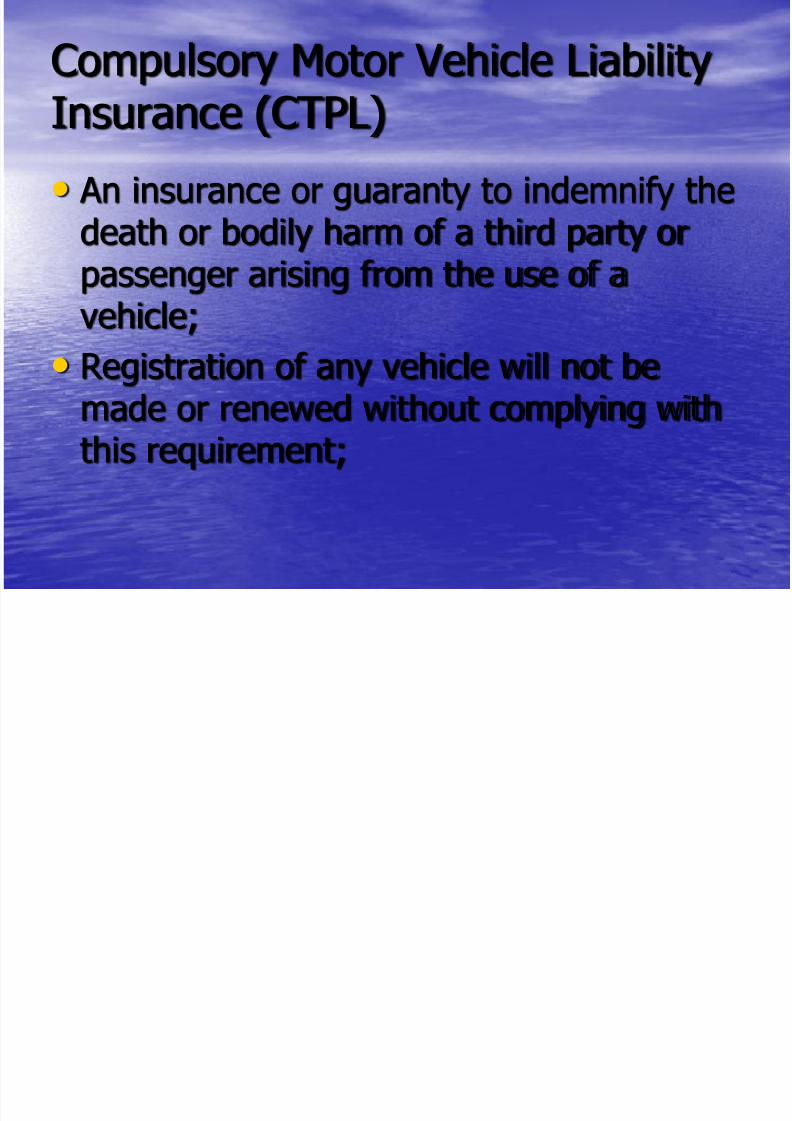

Compulsory Motor Vehicle LiabilityInsurance (CTPL)

• An insurance or guaranty to indemnify thedeath or bodily harm of a third party or

passenger arising from the use of avehicle;

• Registration of any vehicle will not be

made or renewed without complying withthis requirement;

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 38/48

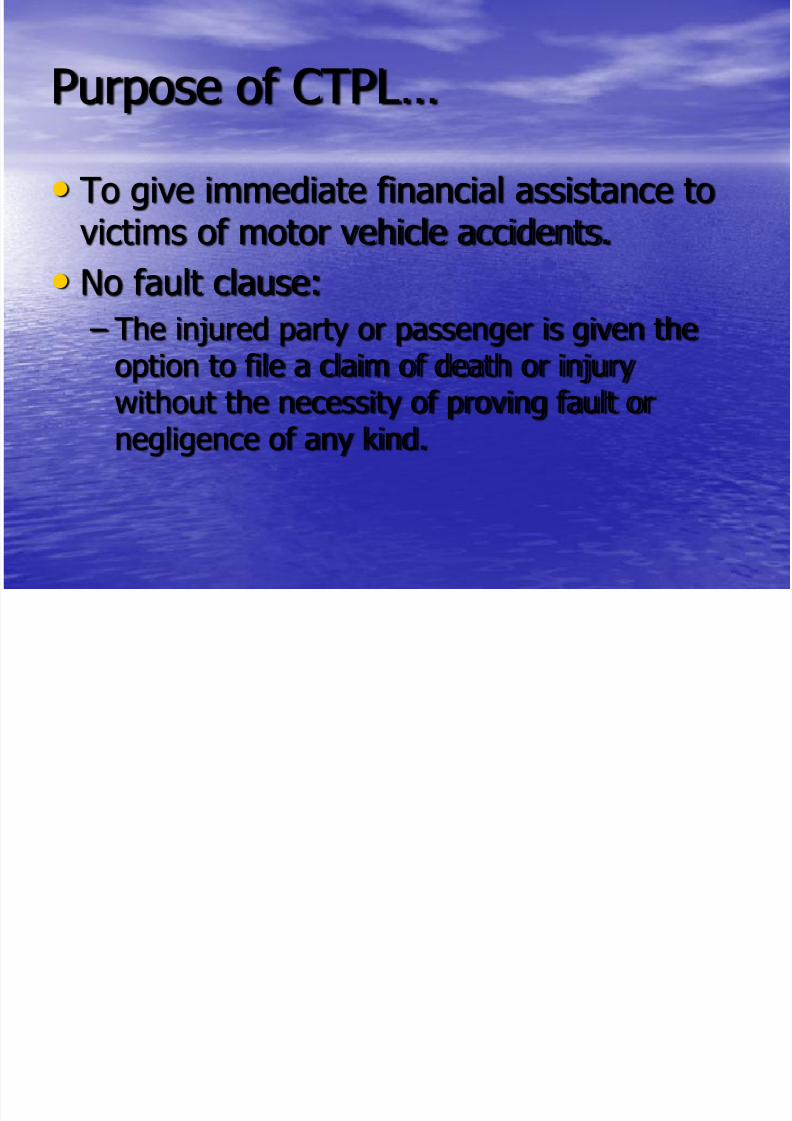

Purpose of CTPL…

• To give immediate financial assistance tovictims of motor vehicle accidents.

• No fault clause: – The injured party or passenger is given the

option to file a claim of death or injurywithout the necessity of proving fault ornegligence of any kind.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 39/48

No fault clause…conditions

• The total indemnity in respect of any personshall not exceed five thousand pesos;

• The following proof of loss, when submitted

under oath, shall be sufficient evidence tosubstantiate the claim: – Police report of accident;

– Death certificate and evidence sufficient to establish

the proper payee; – Medical report and evidence of medical or hospital

disbursement in respect of which refund is claimed.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 40/48

Other rules concerningmotor vehicles…

• Authorized driver clause- a stipulation in a motorvehicle insurance which provides that the driver,other than the insured owner, must be dulylicensed to drive the motor vehicle otherwise theinsurer is excused from liability.

• Theft clause- if there is such a provision and the

vehicle was unlawfully taken, the insurer is liableunder the theft clause.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 41/48

The Insolvency Law (Act No. 1956)

• Purposes:

– To effect equitable distribution of the

insolvent’s property among his creditors; – To discharge the debtor from his liabilities so

that he can start afresh with the property setapart to him as exempt.

Suspension of Payment

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 42/48

Suspension of Paymentvs. Insolvency

The debtor has sufficient propertybut he foresees the impossibilityof meeting his debts as they falldue

The debtor does not havesufficient property to pay his debts

The purpose is to suspend ordelay the payment of debts.

The purpose is to discharge thedebtor from paying certain debts

The amount of indebtedness is

not affected

Some of the creditors may receive

less than their credits

The number of creditors isimmaterial

In case of involuntary insolvency,three or more creditors are

required

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 43/48

Voluntary insolvencyvs. involuntary insolvencyOne creditor is sufficient Three or more creditors are

required

Filed by the debtor Filed by three or more

qualified creditors

No need for commissions of acts of insolvency

Debtors must havecommitted one or more actsof insolvency

Amount of indebtednessmust exceed one thousandpesos

Indebtedness must not beless than one thousand

Bond is not required Petition must be

accompanied by bond

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 44/48

Effects of filing petition forsuspension of payments

• No disposition in any manner of his propertymay be made by the Petitioner except insofar asconcerns the ordinary operations of commerce

or if industry in which he engaged;• No payments may be made by the petitionerexcept in the ordinary course of his business orindustry; and,

• Upon request to court, all pending executionsagainst the debtor shall be suspended exceptexecution against property especiallymortgaged.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 45/48

Effects of adjudication of insolvency

• Forbid the payment to the debtor of anydebt due to him and the delivery to him of

any property belonging to him;• Forbid the transfer of any property to him;

• Stay of all pending civil proceedings

against the insolvent.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 46/48

Discharge…

• The insolvent debtor is released from:

– All his debts and liabilities set forth in the

schedule; and, – All debts, liabilities or claims which were or

might have been proved against the estate ininsolvency.

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 47/48

Discharge…

• Only natural persons may ask fordischarge;

• Corporations cannot ask for discharge

7/29/2019 Insurance Law 2

http://slidepdf.com/reader/full/insurance-law-2 48/48

The following are not discharged:

• Taxes or assessment due to the Nationalor local government;

• Debt created by fraud or embezzlement;• Debts created by defalcation by public

officer or while acting in fiduciary

capacity;• Claims of secured creditors.