Institutional Presentation - 2019 · 2019-11-18 · Institutional Presentation - 2019. ... STS MHC...

38

Institutional Presentation - 2019

Transcript of Institutional Presentation - 2019 · 2019-11-18 · Institutional Presentation - 2019. ... STS MHC...

Institutional Presentation - 2019

Content

World Port Container Throughput

Macroeconomic Context

Container Ports in Brazil

Port of Santos

About Santos Brasil

Tecon Santos

Tecon Imbituba

Tecon Vila do Conde

TEV – Vehicle Terminal

Logistics

Investments & Financial Highlights

Corporate Governance

ESG 2

03

04

06

07

09

12

18

23

28

29

31

36

37

9,365

10,530

10,698

10,732

11,857

12,284

13,259

13,860

13,951

14,965

17,065

19,448

20,770

21,281

21,904

24,719

27,427

33,600

51,425

213,720

Largest countries in container handling World port container throughput in 2017 -> 752 million TEU

Source: ANTAQ, CEPAL and United Nations Conference about Trading and Development - UNCTAD 3

China

USA

Singapore

South Korea

Malaysia

Japan

United Arab

Emirates

Hong Kong

Germany

Spain

Taiwan

Netherlands

Indonesia

India

Vietnam

Belgium

Thailand

Italy

United Kingdom

Brazil

Brazil: world’s 20th largest container throughput in 2017 (‘000 TEU)

Rank Port Country Volume (TEU) 1 Colón Panama 4,324,478

2 Santos Brazil 4,122,243

3 Manzanillo Mexico 3,078,505

4 Cartagena Colombia 2,862,787

5 Panamá Pacífico Panama 2,520,587

6 El Calao Peru 2,340,657

7 Guayaquil Equador 2,064,281

8 Kingston Jamaica 1,833,053

9 Buenos Aires Argentina 1,797,955

10 San Antonio Chile 1,660,832

11 San Juan Puerto Rico 1,405,348

12 Buenaventura Colombia 1,369,139

13 Caucedo Dominican Republic 1,331,907

14 Lázaro Cardenas Mexico 1,314,798

15 Limón-Monin Costa Rica 1,187,140

16 Veracruz Mexico 1,176,253

17 Freeport Bahamas 1,050,140

18 Itajaí Brazil 1,045,813

19 Valparaíso Chile 903,296

20 Altamira Mexico 820,092

Port of Santos: Latin America’s 2nd largest container throughput in 2018

3,5

4,0 4,2

4,6 4,6 4,54,3 4,6

5,0

3,33,9

4,1

4,44,7 4,7 4,5 4,7

5,0

1,761,67

1,962,17

2,36

3,39 3,453,20

3,68

2010 2011 2012 2013 2014 2015 2016 2017 2018

Imported Containers (MM TEU) Exported Containers (MM TEU) Exchange Rate

6,8

7,9 8,49,2

10,0 9,9 9,610,2

10,97.5%

4.0%

1.9% 3.0%

0.5%

-3.5% -3.5%

1.0% 1.1%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Brazil (MM TEU) GDP

GDP X Brazil Container Throughput Exchange Rate X Long Haul Cntrs

4

Macroeconomic indicators

Source: IBGE, ANTAQ and IPEADATA

Containers volume: resiliency amidst economy slowdown

0%

2%

4%

6%

8%

10%

12%

14%

16%

IPCA (12 months) Selic (12 months)

*** 0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

-30%

-20%

-10%

0%

10%

20%

jan-10 nov-10 set-11 jul-12 mai-13 mar-14 jan-15 nov-15 set-16 jul-17 mai-18

Industrial Activity - %YoY (L) Monthly Selic (R)

Inflation x Interest Rate Industrial Activity x Interest Rate

2,73,0

3,23,4

3,7 3,83,6

3,9

4,17.5%

4.0%

1.9%

3.0%

0.5%

-3.5% -3.5%

1.0% 1.1%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Port of Santos (MM TEU) GDP

63 71 71 78 80 79 77 82 8429 29 27 26 28 31 31 34 3468 70 71 66 72 67 66 75 74

462487 501 515 534 577 570

613 631

2010 2011 2012 2013 2014 2015 2016 2017 2018

Containerized Cargo General Cargo Liquid and Gaseous Bulk Solid Bulk

622 657 671 684 714 754 743 805 823

5 6 7 9 10 10 11 12 134 5 5 5 5 5 6 5 7

100 105 110 111 116 118 117 118 122

1821 17 17

17 16 17 2119

2010 2011 2012 2013 2014 2015 2016 2017 2018

Containerized Cargo General Cargo Liquid and Gaseous Bulk Solid Bulk

127 136 139 142 148 149 150 157 161

Brazil Cabotage Cargo Breakdown (MM Ton) Brazil Long-Haul Cargo Breakdown (MM Ton)

1,1 1,31,8

2,1 2,3 2,3 2,32,5

2,8

5,6

6,5 6,46,9 7,0 6,8

6,56,8

7,2

2010 2011 2012 2013 2014 2015 2016 2017 2018

Cabotage Long Haul

Brazil GDP X Port of Santos Container Throughput (MM TEU)

5

Port sector in Brazil Resiliency amidst economy slowdown

Source: ANTAQ

Brazil Container Throughput (MM TEU)

Port sector in Brazil South and Southeast ports are the largest in volume

Source: ANTAQ and IBGE 6

4.122

327

366

210

1.112

766

737

634

85

455

310

360

154

3.854

281

283

195

1.108

725

744

592

50

461

301

284

117

Santos

Rio de Janeiro

Itaguai / Sepetiba

Vitoria

Itajaí / Navegantes

Paranaguá

Rio Grande

Itapoá / S. F. do Sul

Imbituba

Suape

Salvador

Pecém / Fortaleza

Vila do Conde

2018 2017

Container throughput - main Brazilian ports (‘000TEU) North Northeast Southeast South

% Population 9% 28% 42% 14%

% GDP 6% 15% 53% 17%

% Volume (TEU) 7% 12% 46% 35%

12

Port of Santos ‘Must-call port’ in South America

7

Largest Port in South America

> 25% of Brazilian Trade Balance

Hinterland covers 55% of Brazil’s GDP

Connected to Brazil’s main roads and railways

~90% of São Paulo’s industrial base is located

less than 200 kilometers from the Port of Santos

Libra

Rodrimar

Ecoporto

BTP

DPW Santos

799 775 801 1,048

1,224 1,560

1,883

2,268 2,446 2,533

2,685

2,252

2,722 2,984 3,104

3,448 3,656 3,780

3,565 3,854

4,122

9M19

248

302

346 350 436 612

746

1,008 1,159 1,253 1,270

1,044

1,355 1,487

1,733 1,811

1,380 1,314 1,426

1,316 1,446

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Port of Santos Tecon Santos

3,061

BTP 39,2%

Santos Brasil40,3%

DP World Santos 16,0%

Libra 3,9%

Others 0,6%

8 Source: CODESP and Santos Brasil

Port of Santos Tecon Santos’ market-share recovery: 40.3% in 9M19 vs. 35.4% in FY18

2018 x 2017

- Port of Santos: +4.0% (+7.0% in TEU)

- Tecon Santos: +7.8% (+9.5% in TEU)

Market share – 9M19 Container throughput (TEU x 1,000)

CAGR 1998 – 2018

- Port of Santos: 8.5%

- Tecon Santos: 9.2%

Container throughput (TEU x 1,000)

About Santos Brasil History

1997

Santos Brasil is

founded, and Tecon

Santos is acquired in

an auction under a

25-year leasing period

Initial Public

Offering

2006

2007

Mesquita, now

Santos Brasil

Logística,

is acquired

2008

Tecon

Imbituba

and Tecon

Vila do Conde

are acquired

2009

The Santos Vehicle

Terminal - TEV is

acquired under a lease 2013

Tecon Santos

operates the vessel

with the highest cargo

capacity ever to call

at the Port of Santos

Tecon Santos

renews its lease

for additional

25 years

2015

2016

Migration to the

B3 Novo Mercado

2017

Tecon Vila do

Conde renews its

lease for additional

15 years

2018

Tecon Santos reaches a

new productivity record

of 243.58 MPH

(Moves per Hour)

9

About Santos Brasil

Publicly-traded company, listed in B3’s Novo Mercado segment

Five terminals on the Brazilian coast

- Three container terminals

- One vehicle terminal

- One general cargo terminal

Container throughput: 1.68 million TEU (twenty-foot equivalent

unit) in 2018

Port-to-Door full logistics solution (Santos Brasil Logística)

17% of the Brazilian container throughput in 2018*

* Source : ANTAQ

TECON

IMBITUBA

DISTRIBUTION

CENTER (SÃO BERNARDO

DO CAMPO)

TECON

SANTOS

TECON VILA

DO CONDE

TEV

BONDED LOGISTICS

CENTERS (SANTOS AND GUARUJÁ)

TCG IMBITUBA (GENERAL CARGO TERMINAL)

Highlights

10

Container terminal operation The container cycle in a import operation (reverse for exports)

11

1 Ship arrives at the

Port 2 Ship-to-Shore (STS) or

Mobile Harbor Cranes

(MHC)

3 Trucks 4 Reach Stackers 6 Port Warehouse/ De-

Consolidation

5b Reefer Containers

5a Regular Containers

7 Customs 8 Road 9 Logistics Unit 10 Importer

Containers are transported by

ships, which dock at the

terminal’s quayline

Cranes unload the containers

from the ships, positioning

them in trucks and/or terminal

tractors

After the container is placed

on the truck's bed, it is taken

to the (reefer or dry) backyard

RTGs are used to lift the

containers from flat-bed trucks

and to position them in the

stockpiles at the yard.

Containers are stored before

collected by the client

Reefer containers are

positioned in a reefer yard.

Connections and

functionalities are regularly

monitored (i.e. temperature)

Regular containers are taken to the

common yard, where they are positioned

according to the order

in which they will most likely be moved into

trucks to leave the terminal

Cargo of dry

containers is partially

unstuffed (fee is

charged over the

importer)

After the container is placed in

the yard or warehouse,

customs have the green light

to make any required

inspection or to clear the

cargo

The containers transportation

is made by truck, train (Tecon

Santos) or barge (Tecon Vila

do Conde)

Containers can be transported

by road to freight processing

units in the region

TECON

SANTOS

7

Tecon Santos Best solution for containers in South America

13

Geographic Footprint

Market Share 2018

RS

SC

PR

SP

MG

GO

MT

AC

AM

RR

RO BA

PI

MA PA

AP

TO

CE RN

PE AL

SE

MS

RJ

ES

DF

PB

SC

Rio +

Itaguaí

Southeastern

Ports

Tecon

Santos

SP

SP

MG

RJ

ES

Vitória

Growth capacity: CAPEX plan of c.R$1.5 billion, already started

Lease contract renewed until 2047

Equipment 100% GPS-controlled

Connected to Brazil’s main roads and railways

4 internal railway tracks

35.4% 35.6%

15.6%12.6%

0.8%

Tecon Santos BTP DP World Santos Libra Others

7

Tecon Santos Infrastructure and other information

14

Security

Scanner (non-invasive

inspection)

Surveillance cameras

Restricted access

General data

Depth: 13.5m

Quayline extension: 980m +

310m (TEV)

Area: 596,000 m2

Annual capacity: 2,000,000

TEU

Allows

Post-

Panamax

vessels

to dock

at the

Port

Equipment #

Ship-to-Shore

MHC

Reach Stackers

RTG

13¹

1

18

46

STS MHC Reach Stacker RTG

(1) There are currently 11 STS cranes in operation. In 2018, 2 cranes were acquired, expected to be delivered in 2020.

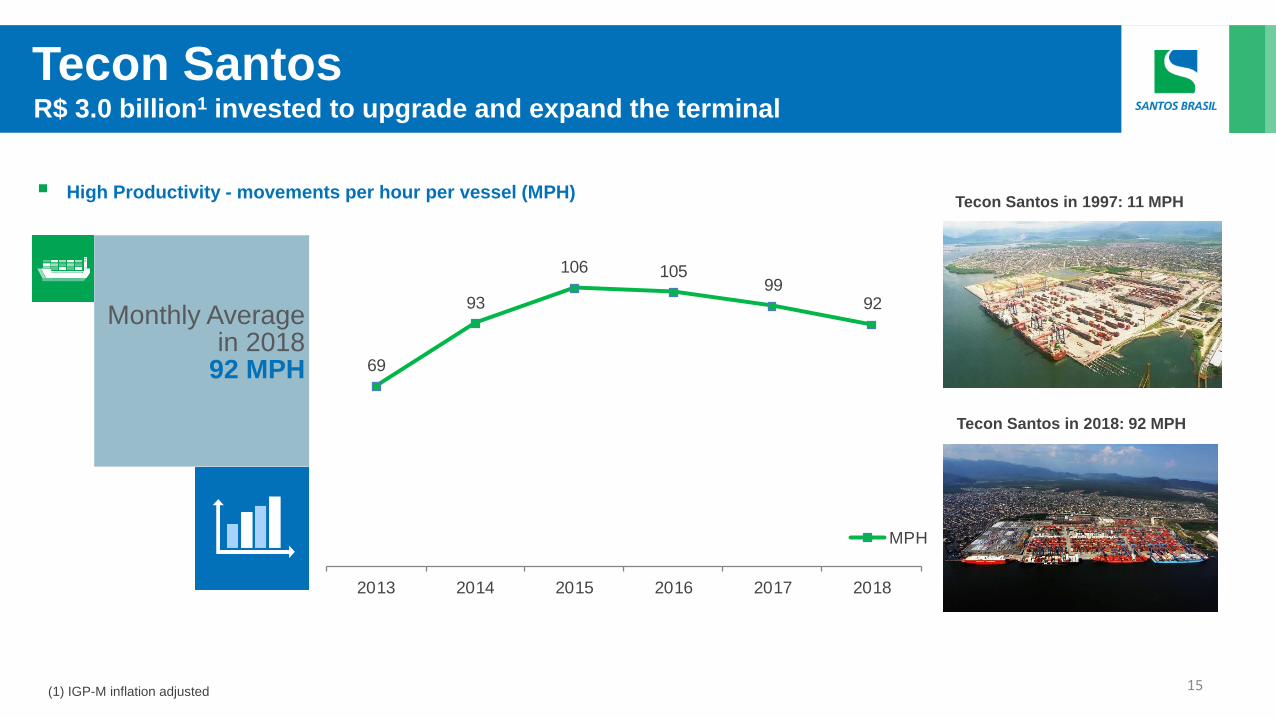

R$ 3.0 billion1 invested to upgrade and expand the terminal

High Productivity - movements per hour per vessel (MPH)

Tecon Santos

15 (1) IGP-M inflation adjusted

Tecon Santos in 1997: 11 MPH

Tecon Santos in 2018: 92 MPH

69

93

106 10599

92

2013 2014 2015 2016 2017 2018

MPH

Monthly Average in 2018

92 MPH

Automation

Focus on efficiency

New Capacity

2,400,000 TEU

Estimated CapEx

R$ 1.5 billion

Investments contracted (FY18)

c.R$ 100M

NEW LAYOUT

Investment cycle in progress: cutting-edge technology, modern layout

Tecon Santos

Quay extension

16

Tecon Santos Phases of the project

Phase 1

Berths extension

and modernization

to attend ships with

366 meters length

Phase 2

Backyard capacity

expansion

Improvement of the

road-rail access

Phase 3

Automation:

increasing capacity

and cost reduction

17

Inserir imagem aqui,

preenchendo o espaço por

completo.

Tecon Imbituba

TECON

IMBITUBA

18

14.5m draft: port terminal ready to receive Super-Post-Panamax

vessels of 366 meters length

Close to Santa Catarina and Rio Grande do Sul industrial zones

25-year lease contract (starting in 2008), with a renewal option

for additional 25 years

Beneficiary of adjacent infrastructure projects: widening of BR-

101 federal highway and the construction of Coastal Railway

(“Ferrovia Translitorânea”)

Favorable meteorological conditions and 24-hour access

Tecon Imbituba hosts 2 terminal types: Container and General

Cargo

One-stop shop: ship, DEPOT and container freight station (CFS)

operations

7

Tecon Imbituba Strategic Location at Southern Region, with developed logistical access

19

Geographic Footprint

Market Share 2018

RS

SC

PR

SP

MG

GO

MT

AC

AM

RR

RO BA

PI

MA PA

AP

TO

CE RN

PE AL

SE

MS

RJ

ES

DF

PB

RS

SC

PR

Tecon Rio Grande

Itapoá

TCP

Southern

Ports

APM & Portonave

Imbituba

Hinterland

3.3%

28.7% 28.7%

24.7%

14.6%

Tecon Imbituba Tecon Rio Grande Portonave

Porto Itapoá Porto Itajaí

7

Tecon Imbituba Infrastructure and other information

20

Security

Scanner (non-invasive

inspection)

Surveillance cameras

Restricted access

General data

Depth: 15.0m

Quayline extension: 660m

Area: 207,000m2

Annual Capacity: 450,000 TEU

Equipment #

Ship-to-Shore

MHC

Reach Stackers

2

2

8

STS MHC Reach Stacker

Allows

Super-

Post-

Panamax

vessels

to dock

at the

Port

TECON VILA DO CONDE

PARANAGUÁ

765,785 TEU*

Tecon Imbituba Potential for volume increase

21

ITAPOÁ / SÃO FRANCISCO DO SUL

634,197 TEU*

ITAJAÍ / NAVEGANTES

1,111,938 TEU*

RIO GRANDE

736,967 TEU*

Container Terminal

Imbituba Hinterland

Pork And Poultry Production

Rio Grande do Sul Industrial Zone

IMBITUBA

84,885 TEU*

* Source: Volume in 2018 (ANTAQ)

(1) Brazilian Association of Animal Protein 2018 Annual Report; (2) InvestRS – Rio Grande do Sul State

Nearby Agricultural

Area

The states of Rio Grande do Sul and Santa

Catarina together accounted for 40.5% of

Brazilian chicken and 69.7% of pork exports

in 2017(1)

With Premium

Logistics Premium transportation logistics with 2 main

roads and railways under construction

Nearby Industrial

Cluster

Rio Grande do Sul holds the largest

concentration of biodiesel, tobacco,

automation, agricultural & road machinery,

wine, trailers & car bodies, and leather &

footwear producers / manufacturers in

Brazil(2)

Tecon Imbituba and its peer terminals (Itajaí/Navegantes and Rio

Grande) are equidistant from the industrial zones and the

consumption centers in the Southern region

R$ 965 million(1) invested since 2008

Improving Productivity - movements per hour per vessel (MPH)

Tecon Imbituba

22 (1) IGP-M inflation adjusted. Includes investments in Imbituba General Cargo terminal

Montlhy Average in 2018

60 MPH

TECON

VILA DO

CONDE

23

Located in the North region of Brazil, with no physical constraints

to receive long haul vessels

Dominant container terminal in Pará state, well connected to other

Brazilian ports via cabotage

Connected to all continents, directly, through Caribbean hub ports

and Panama Canal

Offers container stuffing and unstuffing services, as well as

refrigerated warehousing

Capacity expanded in 2018: investments in new equipment and

infrastructure modernization

Lease contract recently renewed for an additional 15-year period

(by 2033)

Important commodities export hub in the region (e.g. timber, frozen

meat, pepper, agricultural products, metals, minerals and fruits)

7

Tecon Vila do Conde Located in the delta of Amazon River

24

Market Share 2018

Geographic Footprint

RS

SC

PR

SP

MG

GO

MT

AC

AM

RR

RO BA

PI

MA PA

AP

TO

CE RN

PE AL

SE

MS

RJ

ES

DF

PB

Northern

Ports

PA

PI

MA

AP

CE

Vila do Conde

Belém Itaqui

Fortaleza

(Pecém)

2539 45

6578

103

1614

15

2013 2014 2015 2016 2017 2018

Vila do Conde¹ Belém²

# ‘000 containers

(1) Santos Brasil; (2) ANTAQ;

7

Tecon Vila do Conde Infrastructure and other information

25

Security

Scanner (non-invasive

inspection)

Surveillance cameras

Restricted access

General data

Depth: 13.5m

Quayline extension: 254m

Area: 86,615 m2

Annual Capacity: 217,000 TEU

Allows

Post-

Panamax

vessels

to dock

at the

Port

Equipment #

MHC

Reach Stackers

3

11

MHC Reach Stacker

TECON VILA DO CONDE

Vila do Conde x BELÉM

Main Cargo: Wood

Vila do Conde x MACAPÁ - AP

Main Cargos: Chemical Products

Vila do Conde x SANTARÉM X ITAITUBA

Main Cargo: Wood

Vila do Conde x MUNGUBA

Main Cargoes: Kaolin and Cellulose

Vila do Conde x CAMETÁ

Main Cargo: Palm Oil

Vila do Conde x TUCURUÍ

Main Cargo: Silicon

Vila do Conde x MANAUS - AM

Main Cargos: Spare Parts and

Chemical Products

Vila do Conde x ALTAMIRA

Main Cargo: Machinery

Tecon Vila do Conde North Region: inland waterway cargo transportation

26

VILA DO

CONDE

7 27

Tecon Vila do Conde Recent upgrade and capacity expansion to 217,000 TEU annual capacity

Neighbor to Tecon Santos

Handling of different types of cargo: trains, dismantled industrial

plants, power transformers, dismantled machinery, large sculptures

etc

Annual capacity: 300,000 vehicles

- Static capacity: 10,000 vehicles

- FY18 throughput: 241,291 vehicles

- Total area: 164,000 m²

- Quayline extension: 310 meters

TEV - Vehicle Terminal Largest vehicle terminal in Brazil

28

29

Taylor-made logistics services, integrating maritime transportation to exporters’ and importers’ supply chain

Potential to increase customers’ competitiveness: eg. “K10” logistics operation for BASF

Synergies between integrated logistics and port operations

Infrastructure:

- Distribution Center in São Bernardo do Campo (105,000m²)

- CLIA Guarujá (bonded warehouse - 52,900m²)

- CLIA Santos (bonded warehouse - 64,755m²)

- Truck fleet (130 vehicles)

Logistics Vertical integration

Port terminals and Logistics

Main clients

30

31

Investments R$ 5 billion(1) in 22 years

M&A

1997 – Tecon Santos bidding

2006 – Santos Brasil IPO

2007 – Santos Brasil Logística acquisition

2008 – Tecon Imbituba bidding & Tecon Vila do Conde acquisition

2009 – Vehicles terminal bidding

CAPEX

2004/2006 – Tecon Santos first expansion

2008/2010 – Tecon Santos second expansion

2008/2011 – Tecon Imbituba expansion

274

95

190 220

86 5 12 10 48 28

61 91

112 97

127

297 197

124

184

98 85

28 27 15 7

72

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

M&A CAPEX

(1) IGP-M inflation adjusted

147

87 84 107

78 80

15.2%

10.5% 10.2% 11.6% 11.2% 10.8%

2015 2016 2017 2018 9M18 9M19

(23) (28)

(5)

3

(1)

5

-2.4% -3.4%

-0.6%

0.3%

-0.1% -0.7%

2015 2016 2017 2018 9M18 9M19

965 829 824

922 700 742

2015 2016 2017 2018 9M18 9M19

Port Terminals (quay)

39%

Port Terminals (warehousing)

30%

Logistics26%

Vehicle terminal5%

36

EBITDA and EBITDA Mg. Financial Highlights

32 (1) Does not consider intracompany eliminations;

(2) Pro-forma EBITDA adds leasing and rent expenses;

Net Revenue (R$M)

Pro Forma EBITDA² (R$M) and EBITDA margin (%)

Net Revenue Breakdown (3Q19)

Net Income (R$M) and Net margin (%)

82% 88% 97%

78% 90% 89%

18% 12% 3% 22%

10% 11%

2015 2016 2017 2018 3Q18 3Q19

Local Currency Foreign currency

168

122 108

75 55

74

2015 2016 2017 2018 9M18 9M19

340

233 233 227 209

461

59%

29% 26%

43% 52%

76%

2015 2016 2017 2018 3Q18 3Q19

108

40

(38) (27)

(39)

(3)

0.73x

0.46x

-0.45x -0.25x

-0.37x

-0.03x

2015 2016 2017 2018 3Q18 3Q19

EBITDA and EBITDA Mg. Debt Leverage and Cash Flow

33

S&P – Corporate rating in national scale: brAAA

(1) Last-twelve-month pro-forma EBITDA;

Gross Debt (R$M) and Long Term Debt (%)

Operating Cash Flow (R$M) Net Debt (R$M) and Net Debt / pro-forma EBITDA¹

Gross Debt – Currency Breakdown

464

112

27 18

305

Cash & Equivalents Short Term 2020 2021 2022+

411

50

Local Currency Foreign currency

36

EBITDA and EBITDA Mg. Debt highlights and financial ratios

34

Net cash of R$ 3.3 million at 09/30/2019

Debt Currency Outstanding (R$M) %

NCE BRL 103.2 22.4%

Finimp USD/EUR 15.7 3.4%

Finame BRL 2.3 0.5%

Debentures BRL 295.3 64.1%

CCE BRL 10.3 2.2%

CCE USD 34.0 7.4%

Total 460.9 100.0%

Financial indicators – 3Q19

Debt leverage -0.03x net debt / pro-forma EBITDA LTM

Coverage ratio 1.0 pro-forma EBITDA LTM / interest expenses LTM

Current ratio 2.1 current assets / current liabilities

Quick ratio 2.1 (current assets - inventories) / current liabilities

Cash ratio 1.6 cash & equivalents / current liabilities

Debt Amortization (R$M)

Gross Debt - currency breakdown

51% 52%

82%

42%

99% 97%

31%45%

16%

16%

1% 3%9%38%

8% 3% 1% 3%

28 2715 7

7287

2014 2015 2016 2017 2018 9M19

Port Terminals Logistics Corporate TEV Total (R$M)

1831

85

187205

194

70

4 2 3

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Dividends and Interest on Equity distribution (R$M)

CapEx and Dividends R$ million

Capital Expenditures (R$M)

100% Tag Along for all minority shareholders

One Share, One Vote (no shareholders agreement)

Board of directors: 7 members formed by shareholders

Permanent Fiscal Board

Management:

- Stock Options, Performance Shares and Matching for key executives;

- Compensation program for managers and employees: EBITDA and EVA oriented;

- Individual performance plans = clear and targets;

- Progression, promotion and compensation based on meritocracy;

THE BANK OF NEW YORK ADR

DEPARTMENT29,7%

PW237 Participações

22,3%

Dynamo6,2%

Multi STS Participações

5,8%

Richard Klien2,6%

Others32,7%

Management0,4%

Treasury0,3%

38

Corporate Governance “Novo Mercado” listing on B3 – STBP3

36 Total of 669,798,378 voting shares

(1) Includes the participation of the fund ‘RK Exclusivo FIA’

Shareholding Structure (Oct/19)

Sustainability Report¹ compliant with GRI Standard since 2011;

19.2% reduction in CO2 emission per TEU handled in our

terminals;

‘ZeroAcidente’ (Zero Accident) campaign, in 2019: dissemination

of risk and accident prevention culture;

42 37

(1) Acesse o site: Santos Brasil - Sustentabilidade

R$ 26 million invested in training over the last 6 years;

‘Formare Aprendiz’ program: 251 youngsters graduated since

2009; 86 have been hired;

Revision of all compliance policies and codes in 2019: launch

of the New Code of Conduct;

The Best Company in Corporate Governance

in the infrastructure sector – Época magazine

360 yearbook 7th edition.

Awarded as an Outstanding Company in the

Solid Waste Management category – Exame

magazine Sustainability Guide 2018 edition.

Awards 2014 2015 2016 2017 2018

CO2 Emission

CO2 Emission (tons) 30,435 30,337 31,437 31,556 32,297

Port Operation (kgCO2e/TEU¹) 17.32 15.49 15.32 14.85 13.99

Bonded Warehouses (kgCO2e/TEU) 26.57 27.21 19.81 27.61 25.03

Truck Transportation (kgCO2e/TEU) 1.03 0.97 1.01 1.02 1.02

Distribution Center (kgCO2e/TEU) 0.99 1.30 0.63 0.53 0.41

Water

Water consuption (m³) 82,611 69,858 84,817 110,041 82,724

Employees (Own + Fixed third party) 48,645 50,274 48,539 43,587 41,139

Water consumption (m³) per capita 1.70 1.39 1.75 2.52 2.01

Residues

Non-recyclable (tons) 117 119 723 594 627

Recyclable (tons) 395 156 1,454 1,646 1,552

Total residues (tons) 512 275 2,176 2,239 2,179

1. Twenty-Foot Equivalent Unit – unit related to a twenty-foot length container;

Environmental, Social and Governance

45

IR contact, Web and Social Medias

SantosBrasil

santosbrasil_

santosbrasiloficial

santos-brasil

+55 (11) 3279-3279