Institutional Equities Two-wheeler Sector - Nirmal Bang wheeler sector- 26 May 2015.pdf · wheeler...

48

Please refer to the disclaimer towards the end of the document. Institutional Equities Re-initiating Coverage Slow But Steady Two-wheeler stock prices on a YTD basis have underperformed Nifty by 6%-18% as volume growth decelerated after the festive season last year. Adding to it, unseasonal rains in CY15 adversely impacted crop output, leading to weak rural demand. The outlook for the next two quarters looks challenging because of: 1) Crop damage, and 2) High base of 1HFY15. We believe that strong pent-up demand and rising market penetration in rural areas will drive a secular ~9% volume CAGR over the next five years. Valuation of two-wheeler companies like Hero MotoCorp and Bajaj Auto having return ratios in the range of 30%-40% are trading inexpensively at 14x-16x FY17E earnings, restricting downside risk. We have re-initiated coverage on two-wheeler companies with Buy rating on Hero MotoCorp, Accumulate rating on Bajaj Auto and Sell rating on TVS Motor Company. Two-wheeler industry eyeing economic recovery and pent-up demand: Domestic two-wheeler industry posted a CAGR of 8% over FY11-FY15, largely led by scooterisation trend, whereby scooter sales registered a robust 21% CAGR over the period while motorcycle sales witnessed a muted 4% CAGR over the same period. Given the replacement cycle age of five to six years for motorcycles, we believe that strong pent-up demand could come through in FY17/FY18 for motorcycles. Adding to it, demand recovery on the back of improvement in the economy and a normal monsoon will drive domestic two-wheeler growth .It should be noted that motorcycle sales posted a healthy 11% CAGR over FY10-FY12, when the economy picked up. Rural market penetration will continue to drive growth for two-wheelers: Two- wheeler sales growth over the next four-five years will largely come from increased rural market penetration which, as per rating agency Crisil, currently stands at 39% of addressable rural households. It is estimated that by 2020 ~40mn rural households will enter the addressable two-wheeler market. The existing household two-wheeler penetration in India in the addressable income segment (i.e. income of over Rs90,000 per annum) is estimated at around 52% in 2014-15, which is likely to increase to 63% by 2019-20 , largely led by the sharp rise in rural market penetration from 39% to 50%. Two-wheeler industry outperformed car industry in the past: Generally, given the lower market penetration in cars and higher penetration in two-wheelers, the market has a bias towards cars over two-wheelers with the belief that car industry’s growth will outperform that of two-wheelers, However, it is worth noting that two wheeler industry, on a consistent basis in the last few years, has outperformed the car industry in good as well as bad times. Given the low expectations of growth from two-wheeler industry over FY16/FY17, there are higher prospects of this industry’s growth springing a surprise in FY17, just like in 1HFY15 when the car industry reported a muted growth of 4% and the two-wheeler industry reported a strong growth of 16%. Valuations: Valuation of two-wheeler companies like Hero MotoCorp and Bajaj Auto having return ratios in the range of 30%-40% are trading inexpensively at 14x-16x FY17E earnings, restricting downside risk. We have re-initiated coverage on two- wheeler companies with Buy rating on Hero MotoCorp, Accumulate rating on Bajaj Auto and Sell rating on TVS Motor Company. View: Neutral Gaurant Dadwal [email protected] +91-22-3926 8145 One-Year Indexed Performance 70 80 90 100 110 120 130 140 150 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15 S&P BSE India Auto IDX NSE CNX NIFTY INDEX Source: Bloomberg (Rsmn) Market capitalisation CMP Target (%) Up/ EPS (Rs) P/E (x) RoE (%) Companies Rating (Rsbn) (US$bn) (Rs) Price (Rs) (Down) FY15 FY16E FY17E FY15 FY16E FY17E FY15 FY16E FY17E Hero MotoCorp Buy 519.2 8.2 2,588 2,981 15 127.2 150.7 186.3 20.3 17.2 13.9 41.8 41.5 42.2 Bajaj Auto Acc. 666.4 12.6 2,302 2,401 4 109.0 123.4 140.7 21.1 18.6 16.3 31.1 30.9 30.2 TVS Motor Sell 109.2 1.7 230 193 (16) 7.3 10.2 12.9 31.4 22.5 17.9 22.7 26.7 27.7 Source: Bloomberg, Nirmal Bang Institutional Equities Research 26 May 2015 Two-wheeler Sector

-

Upload

truongdien -

Category

Documents

-

view

214 -

download

2

Transcript of Institutional Equities Two-wheeler Sector - Nirmal Bang wheeler sector- 26 May 2015.pdf · wheeler...

Please refer to the disclaimer towards the end of the document.

Institutional Equities

Re-

initi

atin

g C

over

age

Slow But Steady Two-wheeler stock prices on a YTD basis have underperformed Nifty by 6%-18% as volume growth decelerated after the festive season last year. Adding to it, unseasonal rains in CY15 adversely impacted crop output, leading to weak rural demand. The outlook for the next two quarters looks challenging because of: 1) Crop damage, and 2) High base of 1HFY15. We believe that strong pent-up demand and rising market penetration in rural areas will drive a secular ~9% volume CAGR over the next five years. Valuation of two-wheeler companies like Hero MotoCorp and Bajaj Auto having return ratios in the range of 30%-40% are trading inexpensively at 14x-16x FY17E earnings, restricting downside risk. We have re-initiated coverage on two-wheeler companies with Buy rating on Hero MotoCorp, Accumulate rating on Bajaj Auto and Sell rating on TVS Motor Company.

Two-wheeler industry eyeing economic recovery and pent-up demand: Domestic two-wheeler industry posted a CAGR of 8% over FY11-FY15, largely led by scooterisation trend, whereby scooter sales registered a robust 21% CAGR over the period while motorcycle sales witnessed a muted 4% CAGR over the same period. Given the replacement cycle age of five to six years for motorcycles, we believe that strong pent-up demand could come through in FY17/FY18 for motorcycles. Adding to it, demand recovery on the back of improvement in the economy and a normal monsoon will drive domestic two-wheeler growth .It should be noted that motorcycle sales posted a healthy 11% CAGR over FY10-FY12, when the economy picked up.

Rural market penetration will continue to drive growth for two-wheelers: Two-wheeler sales growth over the next four-five years will largely come from increased rural market penetration which, as per rating agency Crisil, currently stands at 39% of addressable rural households. It is estimated that by 2020 ~40mn rural households will enter the addressable two-wheeler market. The existing household two-wheeler penetration in India in the addressable income segment (i.e. income of over Rs90,000 per annum) is estimated at around 52% in 2014-15, which is likely to increase to 63% by 2019-20 , largely led by the sharp rise in rural market penetration from 39% to 50%. Two-wheeler industry outperformed car industry in the past: Generally, given the lower market penetration in cars and higher penetration in two-wheelers, the market has a bias towards cars over two-wheelers with the belief that car industry’s growth will outperform that of two-wheelers, However, it is worth noting that two wheeler industry, on a consistent basis in the last few years, has outperformed the car industry in good as well as bad times. Given the low expectations of growth from two-wheeler industry over FY16/FY17, there are higher prospects of this industry’s growth springing a surprise in FY17, just like in 1HFY15 when the car industry reported a muted growth of 4% and the two-wheeler industry reported a strong growth of 16%.

Valuations: Valuation of two-wheeler companies like Hero MotoCorp and Bajaj Auto having return ratios in the range of 30%-40% are trading inexpensively at 14x-16x FY17E earnings, restricting downside risk. We have re-initiated coverage on two-wheeler companies with Buy rating on Hero MotoCorp, Accumulate rating on Bajaj Auto and Sell rating on TVS Motor Company.

View: Neutral

Gaurant Dadwal [email protected] +91-22-3926 8145

One-Year Indexed Performance

70

80

90

100

110

120

130

140

150

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

S&P BSE India Auto IDX NSE CNX NIFTY INDEX

Source: Bloomberg

(Rsmn) Market capitalisation CMP Target (%) Up/ EPS (Rs) P/E (x) RoE (%)

Companies Rating (Rsbn) (US$bn) (Rs) Price (Rs) (Down) FY15 FY16E FY17E FY15 FY16E FY17E FY15 FY16E FY17E

Hero MotoCorp Buy 519.2 8.2 2,588 2,981 15 127.2 150.7 186.3 20.3 17.2 13.9 41.8 41.5 42.2

Bajaj Auto Acc. 666.4 12.6 2,302 2,401 4 109.0 123.4 140.7 21.1 18.6 16.3 31.1 30.9 30.2

TVS Motor Sell 109.2 1.7 230 193 (16) 7.3 10.2 12.9 31.4 22.5 17.9 22.7 26.7 27.7

Source: Bloomberg, Nirmal Bang Institutional Equities Research

26 May 2015

Two-wheeler Sector

Institutional Equities

2 Automobile Sector

Table of Content

Our coverage universe …………………………………….…………………………………..……………………...03 Investment rationale …………………………………….…………………………………………..……….………...06 Two-wheeler industry eyeing economic recovery and pent-up demand…………………………..……...……….07 Scooterisation trend………….……………………………………………………………………………..…….…….08 Established players lost market share, largely to HMSI……..………………………………………………………10 Hero MotoCorp retains market share in motorcycles in FY15………………..……………………...…..……..….12 New launches in premium motorcycle and scooter segments ……….………………………..…………………..14 OEMs adding capacity in anticipation of better FY17/FY18……….……………..…………………………….…..15 OEMs expand dealer network……….……………..…………………………………………………………………..16

Companies

Bajaj Auto……………………………………………………………………….……………....….….….…..19

Hero MotoCorp……………………………………………...…………………….…………..……..….……29

TVS Motor………………………………………………………………………………………………..……39

Institutional Equities

3 Automobile Sector

Our Coverage Universe

Bajaj Auto

BAL underperformed benchmark index Nifty on a YTD basis by 6%. The underperformance was largely because of steep market share loss in the domestic motorcycle segment and weak export demand. Going forward, we expect a PAT CAGR of 10% over FY15-FY17 because we see improvement in volume growth and profitability in FY16/FY17. Post 4QFY15 results, the stock has run up sharply, trading at 16.3x one-year forward earnings. We have valued BAL at 16x FY17E EPS of Rs141+ Rs151/share for stake in KTM and assigned Accumulate rating to it with a target price of Rs2,401.

Exhibit 1: Bajaj Auto’s one-year forward P/E band

0

500

1,000

1,500

2,000

2,500

3,000 A

ug

-08

De

c-0

8

Ap

r-0

9

Au

g-0

9

De

c-0

9

Ap

r-1

0

Au

g-1

0

De

c-1

0

Ap

r-1

1

Au

g-1

1

De

c-1

1

Ap

r-1

2

Au

g-1

2

De

c-1

2

Ap

r-1

3

Au

g-1

3

De

c-1

3

Ma

y-1

4

Au

g-1

4

De

c-1

4

Ma

y-1

5

(Rs)

Price 14 16 18 20

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 2: Bajaj Auto’s relative performance to Nifty

80

90

100

110

120

130

140

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

Bajaj Auto NSE CNX NIFTY INDEX

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 3: Our estimates are broadly in line with consensus estimates

NBIE estimates Bloomberg estimates Deviation (%)

(Rsmn) FY16E FY17E FY16E FY17E FY16E FY17E

Net sales 232,275 260,036 241,985 274,968 (4.0) (5.4)

EBITDA 46,105 52,583 47,649 54,347 (3.2) (3.2)

EBITDA margin (%) 19.4 19.7 19.7 19.8 (0.3) (0.0)

PAT 35,701 40,701 36,690 41,930 (2.7) (2.9)

EPS (Rs) 123 141 127 145 (3.2) (3.2)

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

4 Automobile Sector

Hero MotoCorp

We like Hero MotoCorp as the company could surprise positively on low expectations. Further, we believe the market share loss in the motorcycle segment over FY10-FY14 bottomed out with the company gaining a 110bps market share in motorcycles in FY15. Margins could expand by a realistic 175bps in FY17E over FY15 and could surprise positively if demand picks up by the end of FY16. Successful launch of scooters and also penetration in key export markets of Nigeria and Latin America in FY16 remains the joker in the pack. On realistic low estimates, the stock currently trades at 13.9x FY17E earnings of Rs186.3. We have assigned Buy rating to the stock with a target price of Rs2,981, up 15% from the current market price.

Exhibit 4: Hero MotoCorp’s one-year forward P/E ratio

-

500

1,000

1,500

2,000

2,500

3,000

3,500 M

ay-

05

No

v-0

5

Ma

y-0

6

No

v-0

6

Ma

y-0

7

No

v-0

7

Ma

y-0

8

No

v-0

8

Ma

y-0

9

No

v-0

9

Ma

y-1

0

No

v-1

0

Ma

y-1

1

No

v-1

1

Ma

y-1

2

No

v-1

2

Ma

y-1

3

No

v-1

3

Ma

y-1

4

No

v-1

4

Ma

y-1

5

(Rs)

Price 14 16 18 20

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 5: Hero MotoCorp’s performance versus BSE Nifty

80

90

100

110

120

130

140

150

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

Hero MotoCorp NSE CNX NIFTY INDEX

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 6: Our earnings estimates for FY17 are 7% above consensus estimates

NBIE estimates Bloomberg estimates Deviation (%)

(Rsmn) FY16E FY17E FY16E FY17E FY16E FY17E

Net sales 294,560 335,967 299,590 338,780 (1.7) (0.8)

EBITDA 39,531 49,000 40,720 47,640 (2.9) 2.9

EBITDA margin (%) 13.4 14.6 13.59 14.06 (0.2) 0.5

PAT 30,102 37,210 30,000 34,870 0.3 6.7

EPS (Rs) 150.7 186.3 149.9 174.1 0.6 7.0

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

5 Automobile Sector

TVS Motor

TVS Motor has been one of the best performing stocks in last one year with a 84% outperformance against benchmark Nifty. After a solid FY15, full of successful new vehicle launches and a robust 22% volume growth, we have factored in 10%/14% volume growth for FY16E/FY17E, respectively, and margin expansion of 100bps/60bps to 7.1%/7.6%, respectively, for the same period. The stock trades expensively at 23x/18x FY16E/FY17E earnings, i.e. at a premium to its historical average and compared to peers like Hero MotoCorp and Bajaj Auto. We have valued TVS Motor at 15x FY17E earnings, at a discount to Bajaj Auto and Hero MotoCorp’s multiple of 16x and assigned Sell rating to the stock with a target price of Rs193, down 16% from the current market price. We believe a re-rating is possible only after the company starts reporting better-than-expected EBITDA margin, which we believe is unlikely in the near term despite strong volume growth expectations.

Exhibit 7: TVS Motor’s one-year forward P/E

(100)

(50)

0

50

100

150

200

250

300

350

Ma

y-0

5

No

v-0

5

Ma

y-0

6

No

v-0

6

Ma

y-0

7

No

v-0

7

Ma

y-0

8

No

v-0

8

Ma

y-0

9

No

v-0

9

Ma

y-1

0

No

v-1

0

Ma

y-1

1

No

v-1

1

Ma

y-1

2

No

v-1

2

Ma

y-1

3

No

v-1

3

Ma

y-1

4

No

v-1

4

Ma

y-1

5

(Rs)

Price 15 20 25 30

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 8: TVS Motor stock’s performance versus Nifty

50

70

90

110

130

150

170

190

210

230

250

270

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

TVS Motor Company NSE CNX NIFTY INDEX

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 9: Our earnings estimates are significantly below consensus estimates

NBIE estimates Bloomberg estimates Deviation (%)

(Rsmn) FY16E FY17E FY16E FY17E FY16E FY17E

Net sales 114,867 134,071 120,860 143,380 (5.0) (6.5)

EBITDA 8,075 10,229 8,780 11,730 (8.0) (12.8)

EBITDA margin (%) 7.0 7.6 7.26 8.18 (0.2) (0.6)

PAT 4,849 6,113 5,220 7,350 (7.1) (16.8)

EPS (Rs) 10.2 12.9 10.97 15.4 (7.0) (16.4)

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

6 Automobile Sector

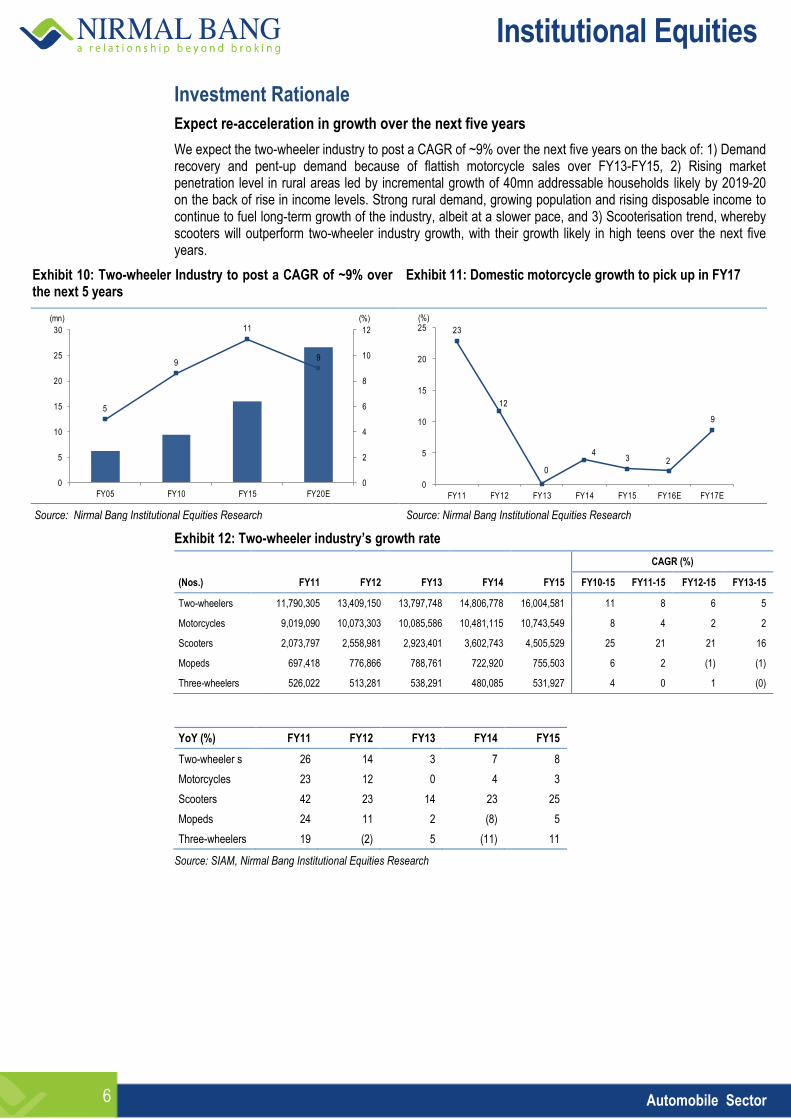

Investment Rationale

Expect re-acceleration in growth over the next five years

We expect the two-wheeler industry to post a CAGR of ~9% over the next five years on the back of: 1) Demand recovery and pent-up demand because of flattish motorcycle sales over FY13-FY15, 2) Rising market penetration level in rural areas led by incremental growth of 40mn addressable households likely by 2019-20 on the back of rise in income levels. Strong rural demand, growing population and rising disposable income to continue to fuel long-term growth of the industry, albeit at a slower pace, and 3) Scooterisation trend, whereby scooters will outperform two-wheeler industry growth, with their growth likely in high teens over the next five years.

Exhibit 10: Two-wheeler Industry to post a CAGR of ~9% over the next 5 years

Exhibit 11: Domestic motorcycle growth to pick up in FY17

5

9

11

9

0

2

4

6

8

10

12

0

5

10

15

20

25

30

FY05 FY10 FY15 FY20E

(mn) (%)

23

12

0

4 3 2

9

0

5

10

15

20

25

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(%)

Source: Nirmal Bang Institutional Equities Research Source: Nirmal Bang Institutional Equities Research

Exhibit 12: Two-wheeler industry’s growth rate

CAGR (%)

(Nos.)

FY11 FY12 FY13 FY14 FY15 FY10-15 FY11-15 FY12-15 FY13-15

Two-wheelers

11,790,305 13,409,150 13,797,748 14,806,778 16,004,581 11 8 6 5

Motorcycles

9,019,090 10,073,303 10,085,586 10,481,115 10,743,549 8 4 2 2

Scooters

2,073,797 2,558,981 2,923,401 3,602,743 4,505,529 25 21 21 16

Mopeds

697,418 776,866 788,761 722,920 755,503 6 2 (1) (1)

Three-wheelers

526,022 513,281 538,291 480,085 531,927 4 0 1 (0)

YoY (%) FY11 FY12 FY13 FY14 FY15

Two-wheeler s 26 14 3 7 8

Motorcycles 23 12 0 4 3

Scooters 42 23 14 23 25

Mopeds 24 11 2 (8) 5

Three-wheelers 19 (2) 5 (11) 11

Source: SIAM, Nirmal Bang Institutional Equities Research

Institutional Equities

7 Automobile Sector

Two-wheeler industry eyeing economic recovery and pent-up demand

Domestic two-wheeler industry posted a CAGR of 8% over FY11-FY15, largely led by scooterisation trend, whereby scooters witnessed a robust 21% CAGR while motorcycle sales reported a muted 4% CAGR over the same period. Given the replacement cycle age of five-six years for motorcycles, we believe that strong pent-up demand may be visible over FY17/FY18 for motorcycles, driving domestic two-wheeler growth, as motorcycle sales constitute 67% of domestic two-wheeler industry’s sales. It should be noted that motorcycle sales posted a healthy 11% CAGR over FY10-FY12, when the economy picked up. In the long– run, we expect the two-wheeler industry to report a CAGR of 8%-9% over next 5 years.

Exhibit 13: Domestic two-wheeler sales Exhibit 14: Scooters posted a robust 21% CAGR over the past five years

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

(Nos)

(2)

3

12 9

27

42

25

14

23 25

17 13

(12)

1

26 23

12

0 4 3

(20)

(10)

0

10

20

30

40

50

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

(%)

Source: SIAM, Nirmal Bang Institutional Equities Research Source: SIAM, Nirmal Bang Institutional Equities Research

Exhibit 15 : Domestic motorcycle sales remain flat Exhibit 16: Robust scooter sales

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

(Nos)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

(Nos)

Source: SIAM, Nirmal Bang Institutional Equities Research Source: SIAM, Nirmal Bang Institutional Equities Research

Rural market penetration to drive two-wheeler industry’s growth in coming years

Currently, India is the second-largest two-wheeler market in the world, with a two-wheeler population of ~ 76mn. Asia accounts for over 80% of overall global two-wheeler sales led by China, India, Indonesia and Vietnam. It should be noted that India remains one of the lowest penetrated markets among others in Asia, largely because of the rural-urban divide, where rural market penetration remained low at ~39% versus 67% in case of urban market in 2015E. According to Crisil, the existing household two-wheeler penetration in the country in the addressable income segment (i.e. income of over Rs90,000 per annum) is estimated at around 52%/42% in 2014-15E, which is likely to increase to 63% by 2019-20E, largely led by rural market penetration rising sharply from 39% to 50%.

Institutional Equities

8 Automobile Sector

Exhibit 17: Two-wheeler penetration in India Exhibit 18: Rural addressable households to increase by ~40mn in five years

49

67

90

29

39

50

39

52

63

0

10

20

30

40

50

60

70

80

90

100

2009-10 2014-15E 2019-20

Urban Rural All India

(%)

161173

183

73

103

142

0

20

40

60

80

100

120

140

160

180

200

2009-10 2014-15E 2019-20

Rural total Households (mn) Addressable Households (mn)

(mn)

Source: Crisil Source: Crisil

Scooterisation trend

Two-wheeler industry’s growth in the past few years has come on the back of robust sales as scooter is the preferred second alternative two-wheeler in a family because of ease and comfort in using it. Scooter contribution has almost doubled from 16% of domestic two-wheeler sales to 28% of sales in FY15. We expect scooters to continue to grow in double-digits for the next few years and drive growth for companies going forward. From our coverage universe, we expect Hero MotoCorp and TVS Motor’s scooter sales to grow 16%/10% and 21%/15% in FY16E/FY17E, respectively.

Exhibit 19: Rising share of scooters in two-wheeler sales

78 77 75 73 71 67

6 6 6 6 55

16 17 19 21 24 28

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Motorcycle Moped Scooter Source: SIAM, Nirmal Bang Institutional Equities Research

Exhibit 20: Most OEMs witness increase in the share of scooter mix

Motorcycle mix Scooter mix

(%) FY14 FY15 bps change FY14 FY15 bps change

Hero 89 88 (41) 11 12 41

HMSI 47 41 (521) 53 59 521

TVS Motor 33 32 (100) 26 32 641

Bajaj 100 100 - - - -

Yamaha India 63 62 (185) 37 38 185

Suzuki 17 19 248 83 81 (248)

Mahindra 77 72 (476) 23 28 476

Two Wheeler Industry 71 67 (366) 24 28 382

Source: SIAM, Nirmal Bang Institutional Equities Research

Institutional Equities

9 Automobile Sector

Two-wheelers have outperformed car industry in the past

Generally, given the lower market penetration in cars and higher penetration in two-wheelers, the market has a bias towards cars over two-wheelers with the belief that car industry’s growth will outperform that of two-wheelers. However, it is worth noting that two wheeler industry, on a consistent basis in the last few years, has outperformed the car industry in good as well as bad times. Given the low expectations of growth from two-wheeler industry over FY16/FY17, there are higher prospects of this industry’s growth springing a surprise in FY17, just like in 1HFY15 when the car industry reported a muted growth of 4% and the two-wheeler industry reported a strong growth of 16%. A stronger correlation is also visible in car sales versus motorcycle sales, which makes us believe that two-wheelers should witness growth in FY17/FY18 if the economy picks up over the next two years.

It is only in recent months that car sales outperformed two-wheeler sales and that too because of: 1) Weak motorcycle sales on account of subdued rural demand 2) Fall in crude oil prices resulting in demand revival for petrol cars, 3) Improved sentiment in urban areas, and 4) Market leader in cars, Maruti Suuzki India, doing well because of new vehicle launches and revival in petrol car demand.

It should be noted that the car industry in FY15 grew solely because of Maruti Suzuki India’s strong performance, with the company reporting a domestic 11% YoY volume growth in FY15.

Exhibit 21: Domestic two-wheeler have outgrown passenger vehicle growth rate

Exhibit 22: Monthly trend also paints a similar picture, but two-wheelers underperformed in recent months because of rural market weakness

(10)

(5)

0

5

10

15

20

25

30

35

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Total passenger vehicles Total Two wheelers

(%)

(15)

(10)

(5)

0

5

10

15

20

25

Ap

r-1

3

Ma

y-1

3

Jun

-13

Jul-1

3

Au

g-1

3

Se

p-1

3

Oct

-13

No

v-1

3

De

c-1

3

Jan

-14

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-1

4

Au

g-1

4

Se

p-1

4

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Fe

b-1

5

Ma

r-1

5

Motorcycle Industry growth rate PV Industry growth rate

(%)

Source: SIAM, Nirmal Bang Institutional Equities Research Source: SIAM, Nirmal Bang Institutional Equities Research

Exhibit 23: Recent underperformance largely because of weak motorcycle sales.

Exhibit 24: Two-wheeler industry’s growth surprised positively in 1HFY15 , writing off higher market penetration assumption

(15)

(10)

(5)

0

5

10

15

20

25

30

Ap

r-1

3

Ma

y-1

3

Jun

-13

Jul-1

3

Au

g-1

3

Se

p-1

3

Oct

-13

No

v-1

3

De

c-1

3

Jan

-14

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-1

4

Au

g-1

4

Se

p-1

4

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Fe

b-1

5

Ma

r-1

5

2W Industry growth rate PV Industry growth rate

(%)

(10)

(5)

0

5

10

15

20

25

30

Ap

r-1

3

Ma

y-1

3

Jun

-13

Jul-1

3

Au

g-1

3

Se

p-1

3

Oct

-13

No

v-1

3

De

c-1

3

Jan

-14

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-1

4

Au

g-1

4

Se

p-1

4

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Fe

b-1

5

Ma

r-1

5(%)

Source: SIAM, Nirmal Bang Institutional Equities Research Source: SIAM, Nirmal Bang Institutional Equities Research

Institutional Equities

10 Automobile Sector

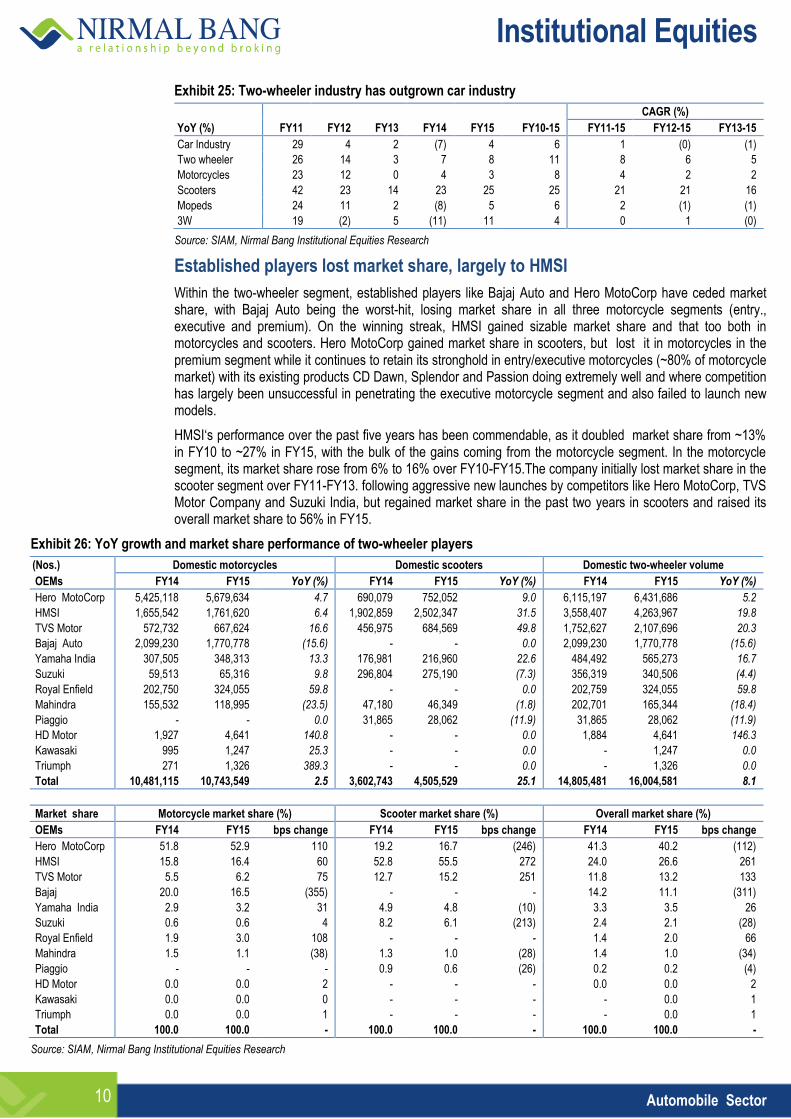

Exhibit 25: Two-wheeler industry has outgrown car industry

CAGR (%)

YoY (%) FY11 FY12 FY13 FY14 FY15 FY10-15 FY11-15 FY12-15 FY13-15

Car Industry 29 4 2 (7) 4 6 1 (0) (1)

Two wheeler 26 14 3 7 8 11 8 6 5

Motorcycles 23 12 0 4 3 8 4 2 2

Scooters 42 23 14 23 25 25 21 21 16

Mopeds 24 11 2 (8) 5 6 2 (1) (1)

3W 19 (2) 5 (11) 11 4 0 1 (0)

Source: SIAM, Nirmal Bang Institutional Equities Research

Established players lost market share, largely to HMSI

Within the two-wheeler segment, established players like Bajaj Auto and Hero MotoCorp have ceded market share, with Bajaj Auto being the worst-hit, losing market share in all three motorcycle segments (entry., executive and premium). On the winning streak, HMSI gained sizable market share and that too both in motorcycles and scooters. Hero MotoCorp gained market share in scooters, but lost it in motorcycles in the premium segment while it continues to retain its stronghold in entry/executive motorcycles (~80% of motorcycle market) with its existing products CD Dawn, Splendor and Passion doing extremely well and where competition has largely been unsuccessful in penetrating the executive motorcycle segment and also failed to launch new models.

HMSI‘s performance over the past five years has been commendable, as it doubled market share from ~13% in FY10 to ~27% in FY15, with the bulk of the gains coming from the motorcycle segment. In the motorcycle segment, its market share rose from 6% to 16% over FY10-FY15.The company initially lost market share in the scooter segment over FY11-FY13. following aggressive new launches by competitors like Hero MotoCorp, TVS Motor Company and Suzuki India, but regained market share in the past two years in scooters and raised its overall market share to 56% in FY15.

Exhibit 26: YoY growth and market share performance of two-wheeler players

(Nos.) Domestic motorcycles Domestic scooters Domestic two-wheeler volume

OEMs FY14 FY15 YoY (%) FY14 FY15 YoY (%) FY14 FY15 YoY (%)

Hero MotoCorp 5,425,118 5,679,634 4.7 690,079 752,052 9.0 6,115,197 6,431,686 5.2

HMSI 1,655,542 1,761,620 6.4 1,902,859 2,502,347 31.5 3,558,407 4,263,967 19.8

TVS Motor 572,732 667,624 16.6 456,975 684,569 49.8 1,752,627 2,107,696 20.3

Bajaj Auto 2,099,230 1,770,778 (15.6) - - 0.0 2,099,230 1,770,778 (15.6)

Yamaha India 307,505 348,313 13.3 176,981 216,960 22.6 484,492 565,273 16.7

Suzuki 59,513 65,316 9.8 296,804 275,190 (7.3) 356,319 340,506 (4.4)

Royal Enfield 202,750 324,055 59.8 - - 0.0 202,759 324,055 59.8

Mahindra 155,532 118,995 (23.5) 47,180 46,349 (1.8) 202,701 165,344 (18.4)

Piaggio - - 0.0 31,865 28,062 (11.9) 31,865 28,062 (11.9)

HD Motor 1,927 4,641 140.8 - - 0.0 1,884 4,641 146.3

Kawasaki 995 1,247 25.3 - - 0.0 - 1,247 0.0

Triumph 271 1,326 389.3 - - 0.0 - 1,326 0.0

Total 10,481,115 10,743,549 2.5 3,602,743 4,505,529 25.1 14,805,481 16,004,581 8.1

Market share Motorcycle market share (%) Scooter market share (%) Overall market share (%)

OEMs FY14 FY15 bps change FY14 FY15 bps change FY14 FY15 bps change

Hero MotoCorp 51.8 52.9 110 19.2 16.7 (246) 41.3 40.2 (112)

HMSI 15.8 16.4 60 52.8 55.5 272 24.0 26.6 261

TVS Motor 5.5 6.2 75 12.7 15.2 251 11.8 13.2 133

Bajaj 20.0 16.5 (355) - - - 14.2 11.1 (311)

Yamaha India 2.9 3.2 31 4.9 4.8 (10) 3.3 3.5 26

Suzuki 0.6 0.6 4 8.2 6.1 (213) 2.4 2.1 (28)

Royal Enfield 1.9 3.0 108 - - - 1.4 2.0 66

Mahindra 1.5 1.1 (38) 1.3 1.0 (28) 1.4 1.0 (34)

Piaggio - - - 0.9 0.6 (26) 0.2 0.2 (4)

HD Motor 0.0 0.0 2 - - - 0.0 0.0 2

Kawasaki 0.0 0.0 0 - - - - 0.0 1

Triumph 0.0 0.0 1 - - - - 0.0 1

Total 100.0 100.0 - 100.0 100.0 - 100.0 100.0 -

Source: SIAM, Nirmal Bang Institutional Equities Research

Institutional Equities

11 Automobile Sector

Exhibit 27: Two-wheeler industry’s market share movement: Bajaj Auto cedes maximum market share

17 19 20 19 18 14 11

49 48 45 45 4341

40

14 13 13 15 19 24 27

15 14 15 14 13 12 13

5 6 7 7 8 9 9

0

10

20

30

40

50

60

70

80

90

100

FY09 FY10 FY11 FY12 FY13 FY14 FY15

Bajaj Auto Hero Motocorp HMSI TVS Motor Company Others

(%)

Source: SIAM, Nirmal Bang Institutional Equities Research

HMSI continues to gain market share in scooters

HMSI has ruled the domestic scooter space since a long time and continues to do so. What is even more commendable is that despite the rise in competitive intensity, the company steadily gained market share from FY11. In FY15 too, the company gained a 272bps market share. Scooters now contribute ~ 59% to HMSI’s two-wheeler volume versus 53% in FY14.

Exhibit 28: Market share trend in scooters – HMSI continues to gain market share

57

51

42

48 4953

56

1314 17 16

19 1917

0

10

20

30

40

50

60

FY09 FY10 FY11 FY12 FY13 FY14 FY15

HMSI TVS Motor Hero MotoCorp Suzuki India

(%)

Source: SIAM, Nirmal Bang Institutional Equities Research

Exhibit 29: Monthly scooter market share (%)

Domestic scooter market share FY14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 FY15

HMSI 52.8 51.7 53.0 51.5 58.0 59.0 55.0 52.0 56.1 55.7 56.4 56.3 60.4 55.5

TVS Motor 12.7 13.5 14.6 17.0 15.4 17.4 15.5 17.5 15.9 13.8 13.8 14.8 13.2 15.2

Hero MotoCorp 19.2 19.1 17.9 18.3 14.2 12.7 15.3 15.5 16.2 19.9 19.0 18.2 14.8 16.7

Suzuki motorcycle 8.2 7.0 7.4 6.3 6.3 4.4 7.5 7.1 6.1 4.8 5.9 5.4 5.1 6.1

Mahindra two-wheelers 1.3 0.9 0.7 0.6 0.5 0.5 0.7 1.6 1.1 1.1 1.4 1.4 1.7 1.0

Piaggio 0.9 0.7 0.6 0.7 0.5 0.7 0.6 0.8 0.6 0.5 0.6 0.6 0.6 0.6

Yamaha India 4.9 7.2 5.8 5.6 5.0 5.4 5.4 5.5 4.0 4.2 2.8 3.3 4.1 4.8

Source: SIAM, Nirmal Bang Institutional Equities Research

Institutional Equities

12 Automobile Sector

Hero MotoCorp retains market share in motorcycles in FY15

In the two-wheeler segment, developing successful brand remains a key challenge as witnessed in the various new launches by OEMs (original equipment manufacturers) in the two-wheeler space, but only a few succeeded and most of them, over the recent years, failed to come out with successful brands. Hero MotoCorp, after the split with Honda, weathered the competition successfully on the back of strong Splendor and Passion brands which dominate the entry/executive segments of the motorcycle market with a strong 65% share. We think it’s commendable that Splendor and Passion have held their feet strong on the ground despite aggressive launches by competitors like Bajaj Auto, TVS Motor, HMSI, Suzuki and Yamaha India, but only a handful of them tasted success while the rest either disappeared or come down to low single-digits, including Bajaj’ Auto’s Discover family.

Exhibit 30: Market share trend – motorcycles

60 5855 56

53 52 53

2224

27 25 2420

16

6 6 7 812

16 16

0

10

20

30

40

50

60

FY09 FY10 FY11 FY12 FY13 FY14 FY15

Hero MotoCorp Bajaj Auto HMSI TVS Motor

(%)

Source: SIAM, Nirmal Bang Institutional Equities Research

Exhibit 31: Monthly market share - motorcycles

(%) FY14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 FY15

Hero MotoCorp 51.8 54.4 53.4 53.8 54.0 53.7 48.6 48.7 53.7 55.4 54.0 52.7 53.7 52.9

Bajaj Auto 20.0 18.3 17.9 16.9 14.6 15.1 18.9 20.3 15.0 13.7 14.8 15.0 15.7 16.5

HMSI 15.8 14.4 15.5 16.3 17.2 16.8 17.0 16.1 16.0 15.6 17.2 18.0 16.9 16.4

TVS Motor 5.5 5.7 6.2 5.9 5.9 6.4 7.3 6.7 6.6 6.0 6.0 6.0 5.5 6.2

Yamaha India 2.9 3.0 2.7 2.6 3.7 3.6 3.4 3.3 3.4 3.7 3.2 3.3 2.9 3.2

Suzuki Motorcycles 0.6 0.4 0.4 0.3 0.2 0.4 0.9 0.8 0.9 0.8 0.8 0.8 0.8 0.6

Royal Enfield 1.9 2.5 2.5 2.8 3.1 2.9 2.6 2.5 3.2 3.6 3.2 3.8 3.8 3.0

Source: SIAM, Nirmal Bang Institutional Equities Research

Institutional Equities

13 Automobile Sector

Exhibit 32: Entry, executive and premium market share - monthly

Economy (%) FY14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 FY15 YoY

bps change

Bajaj Auto (Boxer, CT, Platina, Discover) 17.2 15.0 15.5 14.0 10.9 9.4 13.6 13.8 9.7 9.6 9.7 11.1 12.6 12.1 (508)

Hero MotoCorp (CD Dawn, CD Deluxe, Splendor, Passion) 66.2 71.1 69.0 69.6 71.7 71.4 64.5 64.6 71.1 74.6 72.9 73.0 71.4 70.2 402

Honda Motorcycle (CB Twister, Dream Yuga) 8.7 6.0 6.6 7.7 8.9 10.7 11.1 11.3 10.6 8.5 10.2 9.0 9.4 9.2 49

Yamaha India Motor (Crux, YBR 110) 0.6 0.5 0.5 0.4 0.5 0.5 0.4 0.5 0.4 0.4 0.5 0.4 0.4 0.5 (14)

TVS Motor (MAX, Victor GX, Jive, Max 4r, Star City, Sport) 5.0 5.2 6.3 6.0 6.1 6.5 8.3 7.3 6.5 5.1 5.7 5.9 5.3 6.2 126

Mahindra 2W (Pantero) 2.3 2.1 2.2 2.2 2.0 1.6 2.1 2.3 1.6 1.7 1.1 0.6 0.9 1.7 (55)

Executive

Bajaj Auto Ltd (Boxer, Platina, Discover, KTM) 13.9 13.1 10.4 7.6 6.1 5.2 4.5 6.0 4.1 4.1 3.7 3.7 3.3 6.4 (754)

Hero MotoCorp Ltd (Super Splendor, Glamour, Ignitor) 39.5 41.4 42.3 41.7 43.4 34.4 47.8 40.6 41.6 41.4 37.6 37.7 42.6 41.4 189

Honda Motorcycle & Scooter India (Pvt) Ltd (CB Shine, CBF Stunner/Fi) 38.4 39.6 42.2 46.3 46.9 54.7 41.7 47.6 50.5 52.6 56.0 55.8 51.8 47.8 939

Yamaha India Motor Pvt Ltd (SS 125, Enticer, YD125) 0.7 0.5 0.5 0.5 0.8 1.0 0.6 1.3 0.5 0.6 0.9 0.9 0.7 0.7 (3)

Suzuki Motorcycle India Pvt Ltd (Hayate, Slingshot) 2.8 1.8 1.7 1.7 0.8 0.9 2.6 2.4 1.1 0.7 0.9 1.5 1.5 1.5 (132)

TVS Motor Company Ltd (Victor GLX, Flame, Star City 125, Phoenix) 4.5 3.6 2.8 2.2 2.0 3.7 2.9 2.1 2.2 0.7 0.9 0.4 0.1 2.1 (241)

Premium

Bajaj Auto (Boxer, Discover, Pulsar) 40.9 37.9 37.9 42.8 38.4 49.3 53.8 58.6 55.2 46.8 50.4 47.5 48.6 47.6 663

Hero MotoCorpd (Achiever, Hunk, CBZ X-Treme, Impulse) 9.7 16.0 14.5 13.8 13.4 6.3 3.8 3.5 3.8 2.6 4.0 8.0 8.0 8.1 (164)

Honda Motorcycle & Scooter India (CB Unicorn, CB Unicorn Dazzler, CBR 150R)

26.7 24.1 27.0 22.6 21.0 16.0 20.7 16.8 11.0 18.1 20.3 17.1 17.2 19.5 (715)

Yamaha India Motor (FZ, Fazer, SZ, R15) 22.3 21.9 20.4 20.7 27.1 26.4 21.6 21.1 29.9 32.5 25.3 27.3 26.2 24.6 226

Suzuki Motorcycle India (GS150R) 0.4 0.1 0.2 0.2 0.1 2.0 0.0 0.1 0.0 0.0 0.0 0.0 0.0 0.3 (10)

Source: SIAM, Nirmal Bang Institutional Equities Research

Exhibit 33: Vehicle launches which failed in entry and executive motorcycle segments

Exhibit 34: Model launches which failed in premium motorcycle segment in the past few years

Bajaj Auto Wind 125

XCD 125

XCD 135

Discover 150

Boxer 150

Yamaha India G5

Gladiator

Alba

YBR 125 SS

YD 125

Freedom110

TVS Motor MAX 100 R

Centra

Victor 125

Flame

Jive

TVS Phoenix

Suzuki Heat

Zeus

Sling Shot

M&M Stallio

Pantero

Centuro

Hero MotoCorp Karizma

Impulse

Yamaha India R1

Fazer

VMAX

SZ

FZ1

Source: Nirmal Bang Institutional Equities Research Source: Nirmal Bang Institutional Equities Research

Institutional Equities

14 Automobile Sector

New launches in premium motorcycle and scooter segments

Given the ongoing rural slowdown, most of the two-wheeler OEMs have postponed their new motorcycle launches planned in 2HFY16 and are now banking on new scooter launches and premium motorcycles whose demand remains strong as they are largely preferred in urban and semi- urban areas. Most OEMs have planned new premium motorcycle launches as this segment is growing versus overall market size of the industry and also because demand for these motorcycles is less impacted by weakness in rural areas. OEMs are also banking on scooters in 1HFY15 because despite strong growth in the past few years the demand continues to remain strong. To cite an instance, Hero MotoCorp postponed its motorcycle launches in 2HFY16 and will instead launch two scooter models in 1HFY16. Also, it should be noted that competitive intensity has eased in entry segment motorcycles with no new launch planned by existing players in the near future.

Exhibit 35: Upcoming scooter launches

Scooters

OEM Model

Hero MotoCorp

Dare

Dash

ZIR

Honda Motorcycle and Scooters India PCX125

Yamaha India Motorcycles Ray 125

D'elight

Vespa Fly 125

946

Source: Nirmal Bang Institutional Equities Research

Exhibit 36: Upcoming motorcycle launches – largely in premium category

Bajaj Auto

Pulsar 150 NS

Pulsar 400 SS

Pulsar 160 NS

Pulsar 400 CS

RS400

180NS

200NS FI

Hero MotoCorp

Impulse 250

HX250R

RNT

Hastur

Honda Motorcycle and Scooters India

CBR 650F

CBR300R

CB500F

CBR500R

CB500X

Suzuki Motorcycle Gladius 650

Yamaha India Motorcycles YZF R25

YZF-R3

Mahindra & Mahindra Mojo 300

KTM

390 Adventure

1190 Adventure

1050 Adventure

TVS Motor Apache

TVS Victor

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

15 Automobile Sector

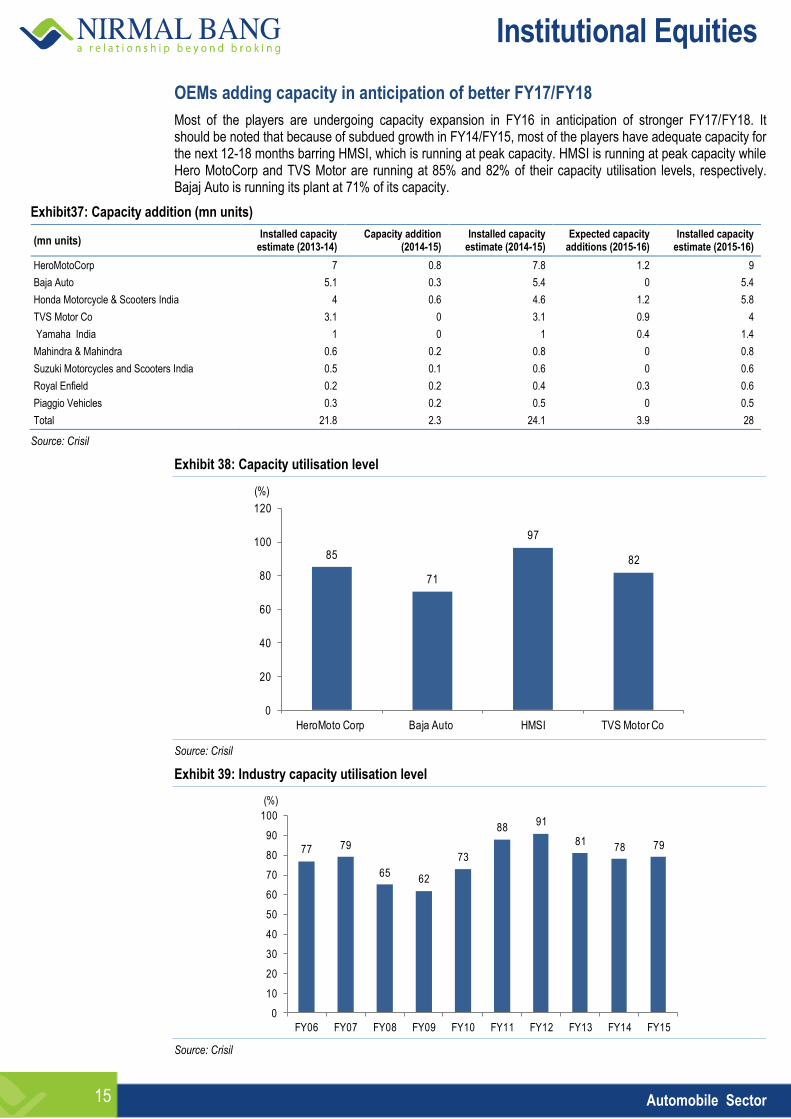

OEMs adding capacity in anticipation of better FY17/FY18

Most of the players are undergoing capacity expansion in FY16 in anticipation of stronger FY17/FY18. It should be noted that because of subdued growth in FY14/FY15, most of the players have adequate capacity for the next 12-18 months barring HMSI, which is running at peak capacity. HMSI is running at peak capacity while Hero MotoCorp and TVS Motor are running at 85% and 82% of their capacity utilisation levels, respectively. Bajaj Auto is running its plant at 71% of its capacity.

Exhibit37: Capacity addition (mn units)

(mn units) Installed capacity

estimate (2013-14) Capacity addition

(2014-15) Installed capacity

estimate (2014-15) Expected capacity

additions (2015-16) Installed capacity

estimate (2015-16)

HeroMotoCorp 7 0.8 7.8 1.2 9

Baja Auto 5.1 0.3 5.4 0 5.4

Honda Motorcycle & Scooters India 4 0.6 4.6 1.2 5.8

TVS Motor Co 3.1 0 3.1 0.9 4

Yamaha India 1 0 1 0.4 1.4

Mahindra & Mahindra 0.6 0.2 0.8 0 0.8

Suzuki Motorcycles and Scooters India 0.5 0.1 0.6 0 0.6

Royal Enfield 0.2 0.2 0.4 0.3 0.6

Piaggio Vehicles 0.3 0.2 0.5 0 0.5

Total 21.8 2.3 24.1 3.9 28

Source: Crisil

Exhibit 38: Capacity utilisation level

85

71

97

82

0

20

40

60

80

100

120

HeroMoto Corp Baja Auto HMSI TVS Motor Co

(%)

Source: Crisil

Exhibit 39: Industry capacity utilisation level

77 79

6562

73

8891

8178 79

0

10

20

30

40

50

60

70

80

90

100

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

(%)

Source: Crisil

Institutional Equities

16 Automobile Sector

OEMs expand dealer network

Given the lower penetration in rural areas, OEMs expanded their capacities in rural and semi–urban areas. Most of the players who witnessed increase in the dealer base have tried their fortune in scooter segment which has witnessed robust growth in the past few years on the back of scooterisation trend in urban and semi-urban areas. Also, OEMs have aggressively launched new products in entry and executive motorcycle segments, and ramped up their network in smaller towns and villages which offer more room for growth compared to urban areas. Hero MotoCorp’s dealer base has witnessed a low single-digit growth in dealer base over the past three years, but the company penetrated deeper into rural areas by adding more touch-points than dealers. To cite an example, Hero MotoCorp’s touch-points in FY12 stood at ~3,700 which the company almost doubled to more than 6,000 in FY15.

Exhibit 40: Major expansion of dealer base of most companies

FY12 FY15

Players Dealers (nos) Dealers (nos) % Change

Bajaj Auto 600 675 13

Hero Honda 700 800 14

TVS Motor 650 900 38

Mahindra & Mahindra 370 500 35

Honda Motorcycle & Scooters 400 768 92

Suzuki Motorcyles India 200 330 65

Yamaha India 450 410 (9)

Source: Crisil, Nirmal Bang Institutional Equities Research

Institutional Equities

17 Automobile Sector

CCoommppaannyy SSeeccttiioonn

Institutional Equities

18 Automobile Sector

This page has been intentionally left blank

Please refer to the disclaimer towards the end of the document.

Institutional Equities

Reuters: BAJA.BO; Bloomberg: BJAUT IN

Bajaj Auto

Re-

initi

atin

g C

over

age

Valuation Factors In Positives

We re-initiate coverage on Bajaj Auto (BAL) with Accumulate rating and a one- year target price of Rs2,390. After declining 6% YTD, the stock has moved up sharply by 15% in the past one month on the back of pick-up in exports and improved domestic market share with the launch of CT 100 motorcycle. We expect market share gains for BAL in the motorcycle segment in FY16 on the back of successful launch of CT 100, which is expected to offset falling Discover sales. As regards exports, we believe the company will post a 10% growth in FY16E because headwinds such as political instability in some countries and currency devaluations have somewhat eased. We have valued Bajaj Auto at 16x FY17E EPS of Rs141 + Rs151/share for stake in KTM and assigned Accumulate rating to it with a target price of Rs 2,401.

Volume to grow for the first time in three years: BAL reported volume decline of 3%/9%/2% in FY13/FY14/FY15, respectively, and lost a 680bps market share to competitors over FY13-FY15 as new vehicles launched struggled. With the introduction of CT 100 and Platina (electric start), domestic motorcycle volume gained momentum, while export outlook improved with headwinds easing. We expect BAL to report 8%/11% YoY growth in volume for FY16/FY17, respectively. We expect domestic market growth of 6% and export market growth of 10% in FY16.

Market share losses bottom out: Recent launches of CT 100 and Platina (electric start) gained strong momentum in the past couple of months, with BAL’s market share improving from ~15% in 4QFY15 to 18.2% as of end-April 2015. Ramp-up in volume of CT 100 and Platina (electric start) helped the company to offset the sharp decline in Discover volume, where its recent monthly run-rate had slipped below 30,000 units per month versus 57,000 units in 1HFY15 and 82,000 units in FY14. We believe the market share losses for BAL since FY13 have bottomed out at 15% in 4QFY15 and expect the company to regain market share of ~17% in FY16.

Exports in recovery mode: Exports in 4QFY15 fell sharply by 11% YoY and 27% QoQ on economic/political factors and devaluation of currencies impacting demand. With currency headwinds easing and general elections concluded in Nigeria and Sri Lanka, export demand witnessed a healthy improvement in April 2015. BAL is targeting 10%-11% volume growth in exports in FY16, while in 1QFY16 it is looking at ~ 0.48mn units versus 0.35mn units in 4QFY15 with the order book expected to remain healthy in May and June 2015.We have factored in a 10% export volume growth in FY16E.

Earnings to post a 10% CAGR over FY15-FY17E: Despite a worsening mix of higher contribution of entry segment motorcycles and weak exports, BAL reported adjusted margin of ~ 19% for 4QFY15. Margins for FY15 stood at 19%, which continues to remain miles ahead of competitors Hero MotoCorp (~13%), TVS Motor (~6.5%) and HMSI (~10%-11%). We expect the margins to improve marginally to 19.4% and 19.7% in FY16/FY17, respectively, from 19% in FY15 and earnings CAGR of 10% over FY15-FY17 driven by a 8% volume growth and marginal EBITDA margin improvement. We have valued BAL at 16x FY17E EPS of Rs 141 + Rs151/share for stake in KTM and assigned Accumulate rating to it with a target price of Rs2,401.

ACCUMULATE

Sector: Automobile

CMP: Rs2,302

Target Price: Rs2,401

Upside: 4%

Gaurant Dadwal [email protected] +91-22-3926 8145

Key Data

Current Shares O/S (mn) 289.4

Mkt Cap (Rsbn/US$bn) 666.1/12.6

52 Wk H / L (Rs) 2,695/1,913

Daily Vol. (3M NSE Avg.) 507,994

Share Holding (%) 2QFY15 3QFY15 4QFY15

Promoter 50.0 50.0 49.2

FII 17.7 18.8 17.0

DII 8.0 18.8 17.0

Others 24.3 24.2 25.1

One-Year Indexed Stock Performance

80

90

100

110

120

130

140

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

Bajaj Auto NSE CNX NIFTY INDEX

Price Performance (%)

1 M 6 M 1 Yr

Bajaj Auto 15.2 (12.9) 16.5

Nifty Index 0.8 (1.1) 13.6

Source: Bloomberg

Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E

Revenues 194,890 197,176 211,039 232,275 260,036 YoY (%) 2.4 0.8 7.3 10.1 11.9 EBITDA 36,381 41,057 41,166 46,105 52,583 EBITDA (%) 18.2 20.4 19.0 19.4 19.7 Adj. PAT 30,436 32,420 31,540 35,701 40,701 YoY (%) 1.3 6.6 (13.2) 26.9 14.0 FDEPS (Rs) 105.2 112.0 109.0 123.4 140.7 RoE (%) 43.7 37.0 31.1 30.9 30.2

RoCE (%) 46.9 42.8 36.5 36.1 35.7

P/E (x) 21.9 20.5 21.1 18.6 16.3 EV/EBITDA 17.4 15.5 14.6 12.7 10.7

EV/sales 3.2 3.2 2.8 2.5 2.1

Source: Company, Nirmal Bang Institutional Equities Research

26 May 2015

Institutional Equities

20 Bajaj Auto

We assign Accumulate rating to BAL with a target price of Rs2,401

BAL underperformed benchmark index Nifty on a YTD basis by 6%. The underperformance was largely because of steep market share loss in the domestic motorcycle segment and weak export demand. Going forward, we expect a PAT CAGR of 10% over FY15-FY17 because we see improvement in volume growth and profitability in FY16/FY17. Post 4QFY15 results, the stock has run up sharply, trading at 16.3x one-year forward earnings. We have valued BAL at 16x FY17E EPS of Rs141+ Rs151/share for stake in KTM and assigned Accumulate rating to it with a target price of Rs2,401.

Exhibit 1: Bajaj Auto’s relative performance to Nifty Exhibit 2: One-year forward P/E band

80

90

100

110

120

130

140

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

Bajaj Auto NSE CNX NIFTY INDEX

0

500

1,000

1,500

2,000

2,500

3,000

Au

g-0

8

De

c-0

8

Ap

r-0

9

Au

g-0

9

De

c-0

9

Ap

r-1

0

Au

g-1

0

De

c-1

0

Ap

r-1

1

Au

g-1

1

De

c-1

1

Ap

r-1

2

Au

g-1

2

De

c-1

2

Ap

r-1

3

Au

g-1

3

De

c-1

3

Ma

y-1

4

Au

g-1

4

De

c-1

4

Ma

y-1

5

(Rs)

Price 14 16 18 20 Source: Bloomberg, Nirmal Bang Institutional Equities Research Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 3: Our estimates are broadly in line with consensus estimates

NBIE estimates Bloomberg estimates Deviation (%)

(Rsmn) FY16E FY17E FY16E FY17E FY16E FY17E

Net sales 232,275 260,036 241,985 274,968 4.2 5.7

EBITDA 46,105 52,583 47,649 54,347 3.3 3.4

EBITDA margin (%) 19.4 19.7 19.7 19.8 (31.1) (1.9)

PAT 35,701 40,701 36,690 41,930 2.8 3.0

EPS (Rs) 123 141 127 145 3.3 3.3

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Institutional Equities

21 Bajaj Auto

Investment Rationale

Volume to grow for the first time in three years

BAL reported volume decline of 3%/9%/2% in FY13/FY14/FY15, respectively, and lost a 680bps market share to competitors over FY13-FY15 as new vehicles launched struggled. With the introduction of CT 100 and Platina (electric start), domestic motorcycle volume gained momentum, while export outlook improved with headwinds easing. We expect BAL to report 8%/11% YoY growth in volume for FY16/FY17, respectively. We expect domestic market growth of 6% and export market growth of 10% in FY16.

Exhibit 4: New launches to drive improvement in volumes Exhibit 5: After three years of weak volumes , growth to pick up in FY16

3,400,000

3,600,000

3,800,000

4,000,000

4,200,000

4,400,000

4,600,000

4,800,000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(Nos.)

34

14

(3)

(9)

(2)

8 11

(15)

(10)

(5)

-

5

10

15

20

25

30

35

40

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(%)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 6: Two-wheeler volume to witness sharp improvement Exhibit 7: Exports to continue growth momentum

3,000,000

3,100,000

3,200,000

3,300,000

3,400,000

3,500,000

3,600,000

3,700,000

3,800,000

3,900,000

4,000,000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(Nos.)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(Nos.)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 8: Volume estimates

(Units) FY12 FY13 FY14 FY15 FY16E FY17E

Domestic 3,834,405 3,757,094 3,422,403 3,292,084 3,532,754 3,867,436

2-wheeler 2,566,757 2,463,863 2,099,230 1,770,778 1,859,317 2,026,655

3-wheeler 1,267,648 1,293,231 1,323,173 1,521,306 1,673,437 1,840,780

Exports 507,317 477,213 447,618 519,117 580,503 679,358

2-wheeler 195,141 223,287 186,856 234,345 264,406 315,846

3-wheeler 312,176 253,926 260,762 284,772 316,097 363,511

Total 4,341,722 4,234,307 3,870,021 3,811,201 4,113,256 4,546,793

YoY Growth (%)

Domestic 13.2 (2.0) (8.9) (3.8) 7.3 9.5

2-wheeler 6.3 (4.0) (14.8) (15.6) 5.0 9.0

3-wheeler 30.4 2.0 2.3 15.0 10.0 10.0

Exports 17.3 (5.9) (6.2) 16.0 11.8 17.0

2-wheeler (3.0) 14.4 (16.3) 25.4 12.8 19.5

3-wheeler 35.1 (18.7) 2.7 9.2 11.0 15.0

Total 13.7 (2.5) (8.6) (1.5) 7.9 10.5

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

22 Bajaj Auto

Market share losses bottom out

Recent launches of CT 100 and Platina (electric start) gained strong momentum in the past couple of months, with BAL’s market share improving from ~15% in 4QFY15 to 18.2% as of end-April 2015. Ramp-up in volume of CT 100 and Platina (electric start) helped the company to offset the sharp decline in Discover volume, where its recent monthly run-rate had slipped below 30,000 units per month versus 57,000 units in 1HFY15 and 82,000 units in FY14. We believe the market share losses for BAL since FY13 have bottomed out at 15% in 4QFY15 and expect the company to regain market share of ~17% in FY16.

Exhibit 9: Two-wheeler industry’s market share movement- Bajaj Auto sheds maximum market share

Exhibit 10: Market share trend – motorcycles

17 19 20 19 18 14 11

49 48 45 45 4341

40

14 13 13 15 19 24 27

15 14 15 14 13 12 13

5 6 7 7 8 9 9

0

10

20

30

40

50

60

70

80

90

100

FY09 FY10 FY11 FY12 FY13 FY14 FY15

Bajaj Auto Hero Motocorp HMSI TVS Motor Company Others

(%)

60 5855 56

53 52 53

2224

27 25 2420

16

6 6 7 812

16 16

0

10

20

30

40

50

60

FY09 FY10 FY11 FY12 FY13 FY14 FY15

Hero MotoCorp Bajaj Auto HMSI TVS Motor

(%)

Source: SIAM, Nirmal Bang Institutional Equities Research Source: SIAM, Nirmal Bang Institutional Equities Research

Focus on premium and economy segments

BAL revisited its strategy after Discover sales failed to gain market share in the executive segment. The company now plans to focus entirely on economy and premium segments, which account for ~40% of the motorcycle industry. The company dominated the premium segment with a market-leading share in excess of 30% on the back of Pulsar model, while in entry segment the launch of Platina and CT100 increased its market share to 33% and 40% in March 2015 and April 2015, respectively, versus FY15 average of 23%. In premium segment, BAL recently launched Pulsar variants RS200/AS200/AS150 and plans to launch more variants to strengthen its position in premium segment motorcycles. BAL is targeting a market share of 23%-24% by the end of 4QFY16, as it expects to gain market share in economy and premium motorcycles.

Exhibit 11: Monthly motorcycle market share – Bajaj Auto Exhibit 12: Bajaj Auto’s market share in entry, executive, premium segments – continuous market share loss in executive segment

23

21

18

17

18 19 19 18 18

17

15 15

19

20

15

14

15 15 16

18

10

12

14

16

18

20

22

24

Se

p 2

01

3

Oct

20

13

No

v 2

01

3

De

c 2

01

3

Jan

20

14

Fe

b 2

01

4

Ma

r 20

14

Ap

r 20

14

Ma

y 2

01

4

Jun

20

14

Jul 2

01

4

Au

g 2

01

4

Se

p 2

01

4

Oct

20

14

No

v 2

01

4

De

c 2

01

4

Jan

20

15

Fe

b 2

01

5

Ma

r 20

15

Ap

r 20

15

(%)

0

5

10

15

20

25

30

35

40

45

Se

p 2

01

3

Oct

20

13

No

v 2

01

3

De

c 2

01

3

Jan

20

14

Fe

b 2

01

4

Ma

r 20

14

Ap

r 20

14

Ma

y 2

01

4

Jun

20

14

Jul 2

01

4

Au

g 2

01

4

Se

p 2

01

4

Oct

20

14

No

v 2

01

4

De

c 2

01

4

Jan

20

15

Fe

b 2

01

5

Ma

r 20

15

Ap

r 20

15

Entry Executive Premium

(%)

Source: Crisil, Nirmal Bang Institutional Equities Research Source: Crisil, Nirmal Bang Institutional Equities Research

Institutional Equities

23 Bajaj Auto

Exhibit 13: Model-wise monthly sales

(Nos.) Sep

2013 Oct

2013 Nov

2013 Dec

2013 Jan

2014 Feb

2014 Mar

2014 Apr

2014 May 2014

Jun 2014

Jul 2014

Aug 2014

Sep 2014

Oct 2014

Nov 2014

Dec 2014

Jan 2015

Feb 2015

Mar 2015

Apr 2015

CT 100 - - - - - - - - - - - - - - - -

6,845 29,189 53,440

Pulsar 69,023 64,169 43,252 30,803 47,738 44,439 49,971 53,605 56,420 52,875 46,035 50,814 71,396 70,810 48,397 38,446 52,966 43,954 48,156 51,296

Platina 100/125 40,985 49,199 34,734 26,269 39,345 36,131 42,955 48,563 57,023 47,750 31,413 31,599 53,200 55,766 31,427 28,948 35,571 35,076 29,252 27,224

Discover 100cc 58,060 82,423 65,899 60,965 59,977 59,720 40,344 36,653 38,215 29,553 25,085 25,350 37,301 35,894 22,903 19,918 20,912 13,698 12,415 15,326

Discover 125cc 28,558 25,290 14,040 14,964 17,005 11,982 31,878 23,702 20,133 12,914 17,291 24,236 38,160 34,614 19,446 14,495 13,709 10,807 9,382 8,067

Eliminator/Avenger 4,612 5,491 3,263 1,984 2,996 2,850 3,617 3,136 3,331 3,585 3,536 3,964 5,257 4,754 3,362 2,910 4,136 3,315 3,561 3,284

Source: Crisil, Nirmal Bang Institutional Equities Research

Exports in recovery mode

Exports in 4QFY15 fell sharply by 11% YoY and 27% QoQ as economic/political factors and devaluation of currencies impacted demand. With currencies stabilising and general elections concluded in Nigeria and Sri Lanka, export demand witnessed a healthy improvement in April 2015 .BAL is targeting 10%-11% volume growth in exports in FY16, while in 1QFY16 it is looking at ~ 0.48mn units versus 0.35mn units in 4QFY15 as the order book is likely to remain healthy in May and June 2015. We have factored in a 10% export volume growth in FY16E.

After elections in March 2015, motorcycle demand revived in Nigeria with the monthly run-rate stabilising at 30,000-35,000 units per month versus a low of 15,000 units per month in 4QFY15 and a high of ~48,000 units per month in 3QFY15. In Egypt and Latin America also, the company witnessed a pick-up in demand from 1QFY16.

Exhibit 14: Quarterly exports fell sharply in 4QFY15 because of multiple headwinds

Exhibit 15: Headwinds have eased , export volume to grow in FY16/FY17

0

100,000

200,000

300,000

400,000

500,000

600,000

1Q

FY

12

2Q

FY

12

3Q

FY

12

4Q

FY

12

1Q

FY

13

2Q

FY

13

3Q

FY

13

4Q

FY

13

1Q

FY

14

2Q

FY

14

3Q

FY

14

4Q

FY

14

1Q

FY

15

2Q

FY

15

3Q

FY

15

4Q

FY

15

(Nos.)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(Nos.)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

24 Bajaj Auto

Exports have strong potential for growth

BAL currently exports its products to 48 countries (Asia, Middle East , Africa and Latin America), which have a combined market size of 5.65mn units and plans to enter another 28 countries (developed markets) in two years which have a combined market size of 2.75mn units. It is noteworthy that BAL has a leadership position in 85% of the markets it exports to, largely in Africa and Latin America. Exports offer significant room to grow from the current level because two-wheeler penetration in Africa and Latin America is still much less compared to Asia and Middle East markets. Further, penetration into developed markets over a span of two-five years with high-end motorcycles offers strong revenue growth potential.

Exhibit 16: Motorcycle penetration in African and Latin American markets remains low

0

10

20

30

40

50

60

70

80

90

Africa Asia and Middle East Latin America

(Motorcycle Penetration /1,000)

Source: Company

Exhibit 17: Bajaj Auto’s share in two-wheelers in key export markets Exhibit18: Bajaj Auto’s market share in three-wheelers

Bajaj Auto’s market share - country-wise estimates for FY15 Ranking in

country

South Asia and Middle East

Sri Lanka 80% 1

Bangladesh 54% 1

Nepal 40% 1

Egypt 28% 1

Iran 28% 2

ASEAN Philippines 30% 1

Africa

Uganda 88% 1

South Sudan 58% 1

Ethiopia 49% 1

Nigeria 42% 1

Congo 33% 1

Kenya 25% 1

Angola 29% 1

Tanzania 16% 2

Latin America

Colombia 44% 1

Guatemala 34% 1

Nicaragua 46% 1

Honduras 18% 2

Peru 19% 2

Bajaj Auto’s market share – country-wise estimates for FY15

Ranking in country

South Asia and Middle East

Sri Lanka 91% 1

Bangladesh 98% 1

Egypt 98% 1

Africa

Sudan 97% 1

Nigeria 52% 1

Ethiopia 51% 1

Latin America

Mexico 92% 1

Central America 82% 1

Peru 83% 1

Colombia 64% 1

Source: Company Source: Company

Institutional Equities

25 Bajaj Auto

Margins to remain stable in the range of 19%-20%

Despite a worsening mix of higher contribution of entry segment motorcycles and weak exports, BAL reported adjusted margins of ~19% for 4QFY15. Margins for FY15 at 19% continues to remain miles ahead of competitors Hero MotoCorp (~13%), TVS Motor (~6.5%) and HMSI (~10%-11%). We expect margins to improve marginally to 19.4%/19.7% in FY16/FY17, respectively, from 19.0% in FY15 because of: 1) Better operating leverage following volume growth, and 2) Weak realisation in INR terms in FY16 (management guidance of US dollar realisation of Rs63.5 ) to offset the negative impact of rising contribution of entry segment motorcycles.

Exhibit 19: Margins adversely impacted in 4QFY15 because of one-offs

Exhibit 20: Expect improvement in EBITDA margin over the next two years

17.9 18.4 18.7 17.6

18.5

21.9 22.1

18.9 17.6

18.9

21.7

17.7

0

5

10

15

20

25

1Q

FY

12

2Q

FY

12

3Q

FY

12

4Q

FY

12

1Q

FY

13

2Q

FY

13

3Q

FY

13

4Q

FY

13

1Q

FY

14

2Q

FY

14

3Q

FY

14

4Q

FY

14

(%)

19

19

18

20

19

19

20

17.0

17.5

18.0

18.5

19.0

19.5

20.0

20.5

21.0

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(%)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 21: Quarterly volume fell sharply in 4QFY15 Exhibit 22: Gross margin continues to improve despite tough

environment in domestic and export markets

600,000

700,000

800,000

900,000

1,000,000

1,100,000

1,200,000

1Q

FY

12

2Q

FY

12

3Q

FY

12

4Q

FY

12

1Q

FY

13

2Q

FY

13

3Q

FY

13

4Q

FY

13

1Q

FY

14

2Q

FY

14

3Q

FY

14

4Q

FY

14

1Q

FY

15

2Q

FY

15

3Q

FY

15

4Q

FY

15

(Nos.)

2627

29 29

26 26 2627

29

31

29 2928

2930

31

22

24

26

28

30

32

34

36

1Q

FY

12

2Q

FY

12

3Q

FY

12

4Q

FY

12

1Q

FY

13

2Q

FY

13

3Q

FY

13

4Q

FY

13

1Q

FY

14

2Q

FY

14

3Q

FY

14

4Q

FY

14

1Q

FY

15

2Q

FY

15

3Q

FY

15

4Q

FY

15

(%)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 23: Quarterly realisation trend – Sharp improvement because of a richer product mix and weak INR/USD rate

Exhibit 24: EBITDA/vehicle declines in 4QFY15

(4)

(2)

-

2

4

6

8

10

12

25,000

30,000

35,000

40,000

45,000

50,000

55,000

1Q

FY

12

2Q

FY

12

3Q

FY

12

4Q

FY

12

1Q

FY

13

2Q

FY

13

3Q

FY

13

4Q

FY

13

1Q

FY

14

2Q

FY

14

3Q

FY

14

4Q

FY

14

1Q

FY

15

2Q

FY

15

3Q

FY

15

4Q

FY

15

Realisation YoY

(Rs) (%)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1Q

FY

12

2Q

FY

12

3Q

FY

12

4Q

FY

12

1Q

FY

13

2Q

FY

13

3Q

FY

13

4Q

FY

13

1Q

FY

14

2Q

FY

14

3Q

FY

14

4Q

FY

14

1Q

FY

15

2Q

FY

15

3Q

FY

15

4Q

FY

15

(Rs)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

26 Bajaj Auto

Financials

Earnings CAGR of 10% likely over FY15-FY17E

After three years of weak sales, BAL is likely to report improvement in volume, which is expected to rise 8%/11% in FY16/FY17, respectively. We expect margins to improve marginally by 70bps over FY15-FY17, purely because of better operating leverage, while on the earnings front we expect the company to report a 10% CAGR over FY15-FY17E.

Exhibit 25: Net sales trend Exhibit 26: PAT trend

0

50,000

100,000

150,000

200,000

250,000

300,000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(Rsmn)

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(Rsmn)

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

Key Risks

Valuation

BAL underperformed benchmark index Nifty on a YTD basis by 6%. The underperformance was largely because of steep market share loss in the domestic motorcycle segment and weak export demand. Going forward, we expect a PAT CAGR of 10% over FY15-FY17 because we see improvement in volume growth and profitability in FY16/FY17. Post 4QFY15 results, the stock has run up sharply, trading at 16.3x one-year forward earnings. We have valued BAL at 16x FY17E EPS of Rs141+ Rs151/share for stake in KTM and assigned Accumulate rating to it with a target price of Rs2,401.

Exhibit 27: Investment in KTM

KTM

CMP (in euros) 120

Market cap (in euros) 1,300

Market cap (Rsmn) 90,986

Bajaj Auto’s 47.99% 43,664

Invested value 43,664

Invested value/ share 151

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

27 Bajaj Auto

Financials (standalone)

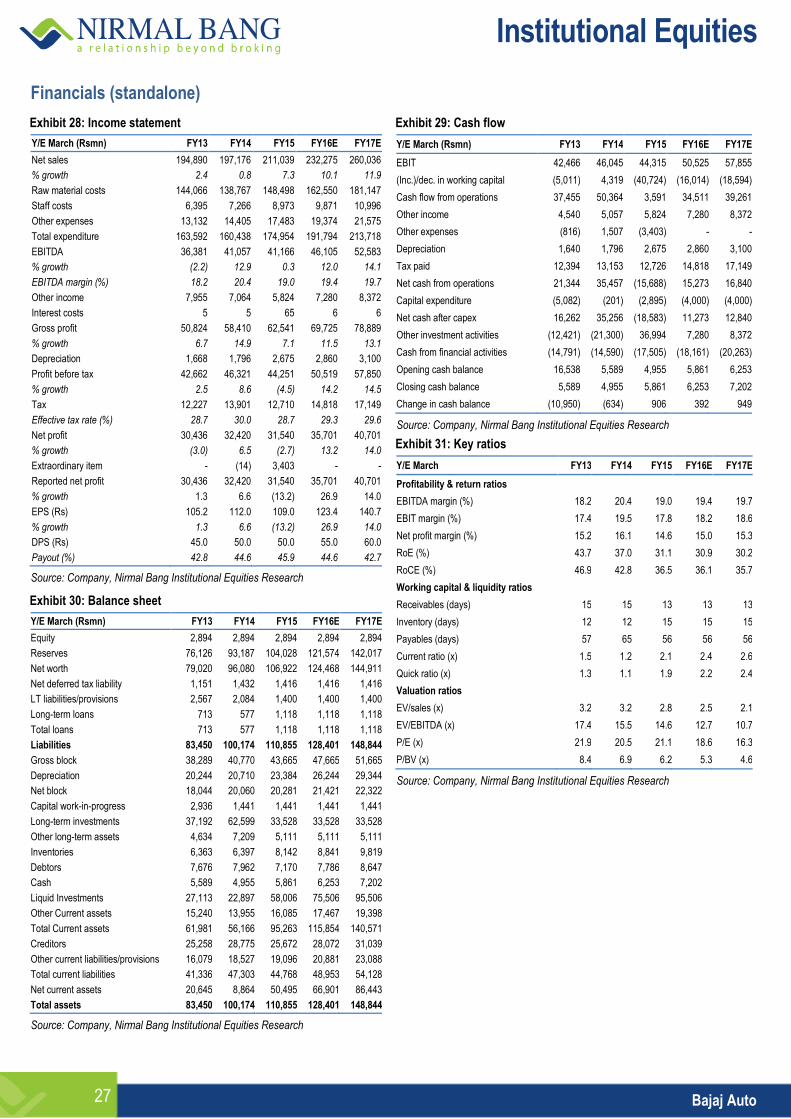

Exhibit 28: Income statement

Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E

Net sales 194,890 197,176 211,039 232,275 260,036

% growth 2.4 0.8 7.3 10.1 11.9

Raw material costs 144,066 138,767 148,498 162,550 181,147

Staff costs 6,395 7,266 8,973 9,871 10,996

Other expenses 13,132 14,405 17,483 19,374 21,575

Total expenditure 163,592 160,438 174,954 191,794 213,718

EBITDA 36,381 41,057 41,166 46,105 52,583

% growth (2.2) 12.9 0.3 12.0 14.1

EBITDA margin (%) 18.2 20.4 19.0 19.4 19.7

Other income 7,955 7,064 5,824 7,280 8,372

Interest costs 5 5 65 6 6

Gross profit 50,824 58,410 62,541 69,725 78,889

% growth 6.7 14.9 7.1 11.5 13.1

Depreciation 1,668 1,796 2,675 2,860 3,100

Profit before tax 42,662 46,321 44,251 50,519 57,850

% growth 2.5 8.6 (4.5) 14.2 14.5

Tax 12,227 13,901 12,710 14,818 17,149

Effective tax rate (%) 28.7 30.0 28.7 29.3 29.6

Net profit 30,436 32,420 31,540 35,701 40,701

% growth (3.0) 6.5 (2.7) 13.2 14.0

Extraordinary item - (14) 3,403 - -

Reported net profit 30,436 32,420 31,540 35,701 40,701

% growth 1.3 6.6 (13.2) 26.9 14.0

EPS (Rs) 105.2 112.0 109.0 123.4 140.7

% growth 1.3 6.6 (13.2) 26.9 14.0

DPS (Rs) 45.0 50.0 50.0 55.0 60.0

Payout (%) 42.8 44.6 45.9 44.6 42.7

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 30: Balance sheet

Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E

Equity 2,894 2,894 2,894 2,894 2,894

Reserves 76,126 93,187 104,028 121,574 142,017

Net worth 79,020 96,080 106,922 124,468 144,911

Net deferred tax liability 1,151 1,432 1,416 1,416 1,416

LT liabilities/provisions 2,567 2,084 1,400 1,400 1,400

Long-term loans 713 577 1,118 1,118 1,118

Total loans 713 577 1,118 1,118 1,118

Liabilities 83,450 100,174 110,855 128,401 148,844

Gross block 38,289 40,770 43,665 47,665 51,665

Depreciation 20,244 20,710 23,384 26,244 29,344

Net block 18,044 20,060 20,281 21,421 22,322

Capital work-in-progress 2,936 1,441 1,441 1,441 1,441

Long-term investments 37,192 62,599 33,528 33,528 33,528

Other long-term assets 4,634 7,209 5,111 5,111 5,111

Inventories 6,363 6,397 8,142 8,841 9,819

Debtors 7,676 7,962 7,170 7,786 8,647

Cash 5,589 4,955 5,861 6,253 7,202

Liquid Investments 27,113 22,897 58,006 75,506 95,506

Other Current assets 15,240 13,955 16,085 17,467 19,398

Total Current assets 61,981 56,166 95,263 115,854 140,571

Creditors 25,258 28,775 25,672 28,072 31,039

Other current liabilities/provisions 16,079 18,527 19,096 20,881 23,088

Total current liabilities 41,336 47,303 44,768 48,953 54,128

Net current assets 20,645 8,864 50,495 66,901 86,443

Total assets 83,450 100,174 110,855 128,401 148,844

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 29: Cash flow

Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E

EBIT 42,466 46,045 44,315 50,525 57,855

(Inc.)/dec. in working capital (5,011) 4,319 (40,724) (16,014) (18,594)

Cash flow from operations 37,455 50,364 3,591 34,511 39,261

Other income 4,540 5,057 5,824 7,280 8,372

Other expenses (816) 1,507 (3,403) - -

Depreciation 1,640 1,796 2,675 2,860 3,100

Tax paid 12,394 13,153 12,726 14,818 17,149

Net cash from operations 21,344 35,457 (15,688) 15,273 16,840

Capital expenditure (5,082) (201) (2,895) (4,000) (4,000)

Net cash after capex 16,262 35,256 (18,583) 11,273 12,840

Other investment activities (12,421) (21,300) 36,994 7,280 8,372

Cash from financial activities (14,791) (14,590) (17,505) (18,161) (20,263)

Opening cash balance 16,538 5,589 4,955 5,861 6,253

Closing cash balance 5,589 4,955 5,861 6,253 7,202

Change in cash balance (10,950) (634) 906 392 949

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 31: Key ratios

Y/E March FY13 FY14 FY15 FY16E FY17E

Profitability & return ratios

EBITDA margin (%) 18.2 20.4 19.0 19.4 19.7

EBIT margin (%) 17.4 19.5 17.8 18.2 18.6

Net profit margin (%) 15.2 16.1 14.6 15.0 15.3

RoE (%) 43.7 37.0 31.1 30.9 30.2

RoCE (%) 46.9 42.8 36.5 36.1 35.7

Working capital & liquidity ratios

Receivables (days) 15 15 13 13 13

Inventory (days) 12 12 15 15 15

Payables (days) 57 65 56 56 56

Current ratio (x) 1.5 1.2 2.1 2.4 2.6

Quick ratio (x) 1.3 1.1 1.9 2.2 2.4

Valuation ratios

EV/sales (x) 3.2 3.2 2.8 2.5 2.1

EV/EBITDA (x) 17.4 15.5 14.6 12.7 10.7

P/E (x) 21.9 20.5 21.1 18.6 16.3

P/BV (x) 8.4 6.9 6.2 5.3 4.6

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

28 Bajaj Auto

This page has been intentionally left blank

Please refer to the disclaimer towards the end of the document.

Institutional Equities

Reuters: HROM.BO; Bloomberg: HMCL IN

Hero MotoCorp

Re-

initi

atin

g C

over

age