INSTITUTE FOR PROSPECTIVE TECHNOLOGICAL STUDIES SEVILLE W

203

INSTITUTE FOR PROSPECTIVE TECHNOLOGICAL STUDIES SEVILLE W.T.C., Isla de la Cartuja, s/n, E-41092 Sevilla Climate Technology Strategy Within Competitive Energy Markets Energy Technology Strategy 1995-2030: Opportunities Arising from the Threat of Climate Change Edited by Antonio Soria (IPTS) Contributors N. Akutsu (International Institute for Applied System Analysis) M. Bess (Energy for Sustainable Development, ESD Ltd.) P. Criqui (Institut d’Economie et Politique Energetique – CNRS) D. Finon (Institut d’Economie et Politique Energetique – CNRS) S. Isoard (IPTS – Joint Research Centre) N. Kouvaritakis (ECOSIM Ltd.) Ph. Menanteau (Institut d’Economie et Politique Energetique – CNRS) S. Mima (Institut d’Economie et Politique Energetique – CNRS) L. Schrattenholzer (International Institute for Applied System Analysis) A. Soria (IPTS – Joint Research Centre) M. Whiteley (Energy for Sustainable Development, ESD Ltd.) EUR 18063 EN Work performed in partial fulfilment of JOULE contract n. JOS3-CT95-0008

Transcript of INSTITUTE FOR PROSPECTIVE TECHNOLOGICAL STUDIES SEVILLE W

INSTITUTE FOR PROSPECTIVE TECHNOLOGICAL STUDIESSEVILLEW.T.C., Isla de la Cartuja, s/n,E-41092 Sevilla

Climate Technology Strategy Within CompetitiveEnergy Markets

Energy Technology Strategy 1995-2030:Opportunities Arising from the Threat of Climate

Change

Edited by Antonio Soria (IPTS)

Contributors

N. Akutsu (International Institute for Applied System Analysis)M. Bess (Energy for Sustainable Development, ESD Ltd.)

P. Criqui (Institut d’Economie et Politique Energetique – CNRS)D. Finon (Institut d’Economie et Politique Energetique – CNRS)

S. Isoard (IPTS – Joint Research Centre) N. Kouvaritakis (ECOSIM Ltd.)

Ph. Menanteau (Institut d’Economie et Politique Energetique – CNRS)S. Mima (Institut d’Economie et Politique Energetique – CNRS)

L. Schrattenholzer (International Institute for Applied System Analysis)A. Soria (IPTS – Joint Research Centre)

M. Whiteley (Energy for Sustainable Development, ESD Ltd.)

EUR 18063 EN

Work performed in partial fulfilment of JOULE contract n. JOS3-CT95-0008

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 2

TABLE OF CONTENTS

CLIMATE TECHNOLOGY STRATEGY WITHIN COMPETITIVE ENERGY MARKETS ........................ 1

CHAPTER 1: INTRODUCTION ............................................................................................................................ 4

1.1 GLOBAL WARMING: ANALYTICAL APPROACHES AND POLICIES .............................................................................. 51.2 TECHNOLOGY CHANGES: A FOCUS IN POWER PRODUCTION SCHEMES .................................................................... 7

CHAPTER 2: ENERGY SYSTEMS: A GLOBAL VIEW..................................................................................... 9

2.1 THE EU CARBON EMISSIONS WITHIN THE OVERALL GREENHOUSE GAME............................................................... 92.1.1 Trends in carbon emissions...........................................................................................................................112.1.2 Trends in carbon intensity.............................................................................................................................132.1.3 Technology and policy responses..................................................................................................................15

2.2 A PROJECTION FOR WORLD ENERGY PATTERNS.....................................................................................................172.2.1 Lessons from world energy outlooks .............................................................................................................172.2.2 WE-2030 exogenous hypotheses: population and GDP growth in 11 world regions ....................................192.2.3 An outlook on world primary energy consumption .......................................................................................252.2.4 A check of final energy demand profiles: the energy service approach ........................................................30

2.3 CHANGES IN THE EU ELECTRICITY MARKETS: THE MOVING TOWARDS LIBERALIZATION......................................352.3.1 Possible industry structures ..........................................................................................................................362.3.2 Contracts and prices .....................................................................................................................................382.3.3 A changing role for the regulator .................................................................................................................402.3.4 The new technology mix................................................................................................................................412.3.5 Managing the grid.........................................................................................................................................41

2.4 FUTURE ENERGY TECHNOLOGY MARKETS AND EU COMPETITIVENESS.................................................................42

CHAPTER 3: CARBON REMOVAL, FUEL CYCLE SHIFT AND EFFICIENCY MEASURES: ASECTORAL VIEW..................................................................................................................................................45

3.1 CARBON REMOVAL AND SEQUESTRATION ............................................................................................................463.1.1 Separation and Recovery Processes .............................................................................................................473.1.2 CO2 Disposal and Storage Processes............................................................................................................503.1.3 Costs and Potentials of Carbon Sequestration, Removal, and Storage .........................................................53

3.2 OTHER REDUCTION OPTIONS ................................................................................................................................553.2.1 Demand-Side Measures ................................................................................................................................563.2.2 Dematerialization and Recycling..................................................................................................................563.2.3 Efficiency Improvements and Technological Change ...................................................................................563.2.4 Fuel-Mix Changes.........................................................................................................................................583.2.5 Removal and Sequestration...........................................................................................................................603.2.6 Energy conversion efficiency ........................................................................................................................623.2.7 Fuel-Mix Changes.........................................................................................................................................65

3.3 THE INDUSTRIAL SECTOR ............................................................................................................................... ......673.3.1 Dematerialization ........................................................................................................ .................................673.3.2 Energy Efficiency Improvement and Process Changes .................................................................................683.3.3 Fuel-Mix Changes.........................................................................................................................................753.3.4 Combined Measures in the Steel Industry .....................................................................................................75

3.4 THE TRANSPORTATION SECTOR............................................................................................................................763.4.1 Efficiency Improvements.................................................................................................. .............................763.4.2 Demand-Side Measures ................................................................................................................................773.4.3 Fuel switching........................................................................................................... ....................................78

3.5 THE RESIDENTIAL & COMMERCIAL SECTOR.........................................................................................................813.5.1 Efficiency Improvements.................................................................................................. .............................81

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 3

3.5.2 Fuel-Mix Changes.........................................................................................................................................84

CHAPTER 4: POWER GENERATION TECHNOLOGY CLUSTERS: PRESENT STATUS AND ITSPOTENTIAL ............................................................................................................................................................86

4.1 NUCLEAR INDUSTRY: A PARADIGM IN CRISIS ........................................................................................................864.2 CLEAN COAL TECHNOLOGIES ...............................................................................................................................914.3 FUEL CELLS FOR STATIONARY AND MOBILE APPLICATIONS.................................................................................1024.4 WIND POWER GENERATION .................................................................................................................................1094.5 PHOTOVOLTAIC ELECTRICITY .............................................................................................................................114

CHAPTER 5: TECHNOLOGY SCENARIOS TO 2030: BASELINE AND ALTERNATIVETECHNOLOGY STORIES...................................................................................................................................120

5.1 THE NATURE OF TECHNOLOGICAL PROGRESS AND BREAKTHROUGHS .................................................................1205.1.1 Energy technology trends in the longer time scale......................................................................................1205.1.2 Market penetration mechanisms and technological lock-in .................................................................. ......122

5.2 ENERGY TECHNOLOGY BASELINE PROJECTION....................................................................................................1255.3 A LOOK INTO THE FUTURE: WORLD ENERGY TECHNOLOGY SCENARIOS ..............................................................130

5.3.1 Centralized Electricity Production: The nuclear renaissance and incremental innovations.......................1315.3.2 The cleaner fossil-fuel-based baseload electricity production. ...................................................................1325.3.3 The Gas-Induced Decentralized Power Generation System........................................................................1335.3.4 The Energy Efficient Decentralised Power Generation System. .................................................................1355.3.5 A Future of Renewable Energy Technologies. ............................................................................................136

5.4 RUNNING THE SCENARIOS ...................................................................................................................................137

CHAPTER 6: TECHNOLOGY PERFORMANCE: TECHNOLOGICAL SCENARIOS AND MARKETPENETRATION ASSESSMENT..........................................................................................................................141

6.1 INTRODUCTION ...................................................................................................................................................1416.2 SAFIRE SCENARIO DESCRIPTIONS.....................................................................................................................1426.3 SAFIRE RESULTS ...............................................................................................................................................142

6.3.1 Scenario Results..........................................................................................................................................1426.3.2 Summary of Market Penetration of renewable energy Technologies ..........................................................1506.3.3 Comparative Analysis of Climate Mitigating Technologies ........................................................................151

6.4 CONCLUSIONS .....................................................................................................................................................162

CHAPTER 7: BASELINE AND ALTERNATIVE TECHNOLOGY SCENARIOS TO 2030: THE EFFECTONTO THE WORLD’S ENERGY SYSTEM......................................................................................................163

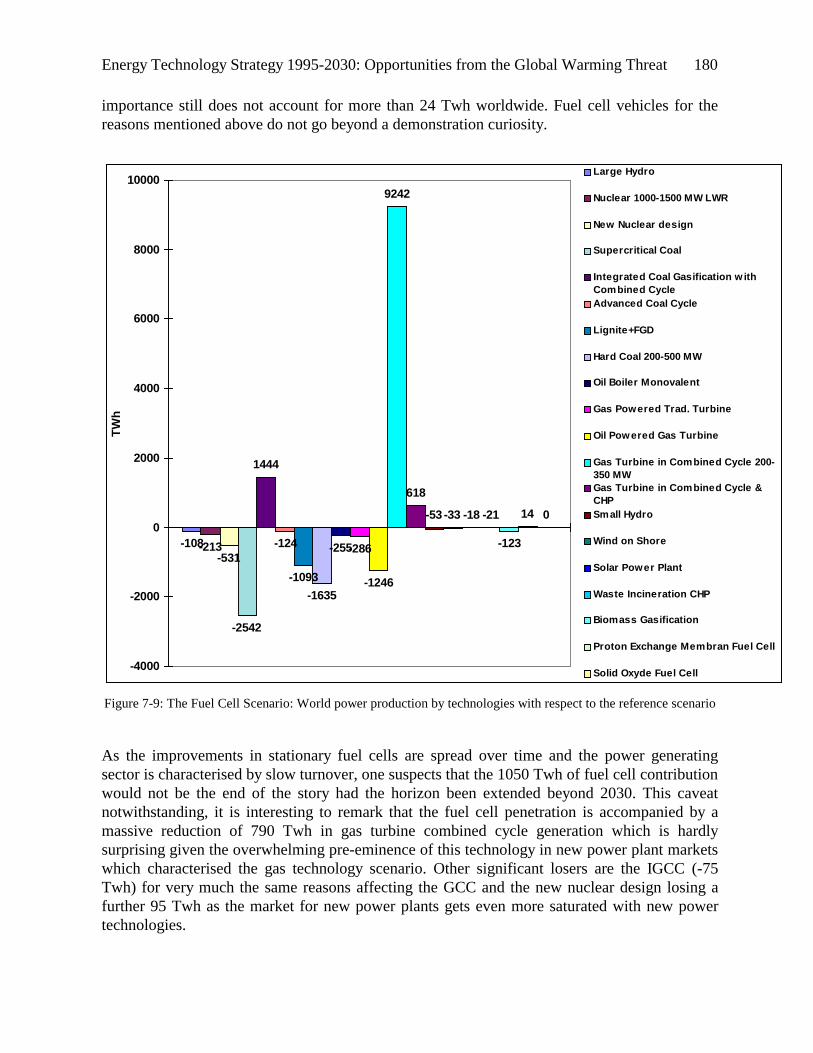

7.1 THE NUCLEAR SCENARIO ...................................................................................................................................1717.2 THE CLEAN COAL SCENARIO ..............................................................................................................................1737.3 THE GAS TECHNOLOGY SCENARIO .....................................................................................................................1767.4 THE FUEL CELL SCENARIO .................................................................................................................................1817.5 THE RENEWABLE ENERGY TECHNOLOGY SCENARIO..........................................................................................1837.6 CONCLUSION.......................................................................................................................................................186

CHAPTER 8: IMPLICATIONS FOR THE EU ENERGY R&D STRATEGY AND OTHER POLICIES...188

8.1 R&D PORTFOLIO, TECHNOLOGICAL PROGRESS AND MARKET STRUCTURE .......................................................1898.2 SHORT-TERM ISSUES: IMPROVEMENTS TO A CARBON-DOMINATED PANORAMA ..................................................1908.3 LONG-TERM OBJECTIVES: MANAGING THE BACKSTOP TECHNOLOGIES ...............................................................192

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 4

Chapter 1: Introductionby A. Soria, IPTS

The basic issue to be analyzed in this volume concerns the trends that may be identified withinthe energy technology field. Our scope here is first to determine up to what extend cantechnology contribute to a possible structural change within energy markets leading to a lesscarbon-intensive exploitation system, and second to determine what are the possiblemechanisms through which these changes may take place, and what are the conditions that mayfacilitate this transition. Ultimately, the key question to answer is what will be the energytechnologies that are likely to become crucial if energy planners consider with growing attentionthe necessity of limiting (with different degrees of intensity) the carbon emissions to theatmosphere. The identification of these technologies is, however, not the only task to do. Indeed,these technologies may be out of the market today, and could well be faced to enormousdifficulties to become operative within a competitive energy market unless some measuresaiming at facilitating its implementation are taken. These measures may be viewed as anecessary effort to conduct the status of the world energy system from a non-sustainablesituation, in which the free-riding behavior of some agents, the opacity of the market signals andthe induced barriers to technology renewal towards a more efficient and reliable system, wherecosts and benefits are granted to the pertinent agents and the inefficiencies are charged withequity, so as to produce a combination of positive incentives. The passage from the presentscheme to this improved situation is not automatic, and a sort of potential barrier has to beovercome. The task is to provide to policy makers an appropriate strategy so as this obstacle isovercome, ensuring a smooth and reliable transition to a environmental (climatic) safe energyexploitation schemes.

An outline of the remaining of the volume follows.

Section 1.1 recalls the basic analytical approaches and possible policy frameworks that havebeen used to assess the energy-environmental-economy problems, and, in particular, the globalwarming issue. Rather than focusing on a similar basis at all of them, it has been perceived thatthere are sectors (and, associated to them, the corresponding technologies) that are actuallyacting as catalyzers of the technology innovation process. The power generation sector seems tobe the big player within the overall picture. Arguments to support this hypothesis are given insection 1.2.

A general view onto the evolution of the energy system at a global scale is included in Chapter2. Trends on carbon emissions, both in absolute and per capita terms are included to serve as aframing discussion for the baseline world energy projection obtained with POLES. Thepeculiarities of the EU and other OECD countries are also discussed, with particular emphasison the changing structure of the power sector (liberalisation and unbundling), underlying the

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 5

role that technological diversity within the electricity market can play to foster the transitiontowards new exploitation schemes.

Chapter 3 presents a screening on the portfolio of mitigation measures from a sectoral end-usestandpoint. These include fuel mix shift, energy appliances improved efficiency as well ascarbon removal and sequestration. These technologies are summarized there by sake ofcompleteness, since, as it has been mentioned, focus will be given to power generationtechnologies. The emerging clusters of electricity generation technologies are described inChapter 4, including not only the present techno-economic status of the technologies, but alsothe prospects for each of them to the medium-long term (2000-2030). The possibletechnological scenarios foreseen, even if concerning the whole system, have been conceived andconstructed around different power generation paradigms: they are described in Chapter 5.

Based on the above-described energy technology scenarios, Chapter 6 shows the results obtainedconcerning the forecasts on market penetration on a technology-by-technology basis, as well asthe analysis of the environmental costs and benefits associated, as predicted by the technologydiffusion model SAFIRE.

The expected effects induced onto the global energy system by the technological hypothesisunderlying behind these technologically-driven scenarios are described in detail in Chapter 7.The analysis presented have been conducted using the POLES model, which allow to capturewith accuracy the regional specificities, as well as the integrated dynamics of the world marketsof primary energy carriers.

Finally, Chapter 8 summarizes the main conclusions and gives the guidelines for setting a cost-efficient energy technology R&D strategy.

1.1 Global warming: analytical approaches and policies

The global warming tread has become an important source of concern during the last decade.However, carbon emissions are not the first environmental problem that has worried energyplanners. Indeed, the problem of finding compatible solutions to fulfill the energy supplyrequirements and limiting sulfur and nitrogen oxide emissions was of extreme importanceduring the seventies and the eighties. The solution of the acid rain problem came basicallythrough technological solutions that were found after an aggressive environmental regulatoryframework. The global warming issue, being linked to carbon use in itself (although alsodepending on the carbon combustion modalities), seems a problem whose solution exceeds thestrict technological domain.

Two typical views have been adopted when studying the issue of energy systems and the relatedenvironmental effects:

• The bottom-up approach considers first the individual energy conversion techniques. Themodels based on this approach are therefore often referred to as ‘engineering’ models, andare frequently tools for optimal resource allocation, either for the long term (capacityplanning) as well as for the sort term (dispatching). Obviously, this approach is particularlysuited to simulate the behaviour of some centralized decision subsystem, typically the powersector. On the contrary, subsystems involving a multiplicity of agents (. i.e. the transportsector) are more difficult to analyze using this scheme.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 6

• The top-down approach uses macroeconomic models to investigate the mutual interactionbetween the economic variables of the aggregate under consideration and the carbonemission. Indeed, economic development and energy consumption are intimatelyintertwined. The causal relationships are far from being clearly understood: from one side,energy is demanded as a productive factor to generate welfare. On the other side, higherincome undoubtedly induces more consumption of energy-related services. The degree ofdetail of these models may vary depending on the scope of the analysis.

Putting forward the premise that the technology is not the unique aspect of the global warmingproblem, it should be stressed that it has an outstanding importance. It is also important toremark that the term technology has to be understood here on a broad basis. It includes not onlysupply-side technologies, but also demand-side technologies. Amongst the first, energytransformation (and, particularly, electric power generation) is a very important subset, since itaccounts for a remarkable share of the carbon emissions all around the world. From the demandside, energy efficient improvements in domestic and industrial appliances are also a fundamentalfactor to contribute to the greenhouse gas emissions reduction. Special mention should be madeto the transport sector, whose fast growing share of the global carbon emissions lies todayaround 22% (to be compared with the share of 18% corresponding to 1973).

The carbon emissions reduction strategy has to be based along four basic action lines:

• Changing the fossil share within the total primary energy production. This concerns mainlythe enhancement of the production of primary electricity via renewables (especiallyhydroelectric power) and nuclear. In the long run, syntethic fuels obtained from renewableresources could also play a role.

• Changing the fossil fuel mix towards a less carbon-intensive energy system. In principle, thisapplies to all the sectors concerned, although the power sector has shown much moreflexibility than the transport sector in modifying the primary input mix according to the pricesignals provided by the energy resources markets.

• Improving the energy conversion efficiency system as a whole in order to obtain more usefulfinal energy with the same amount of primary energy. Efficiency improvements concern theelectricity transformation system, electric power transmission, the refining industry, andother economic sectors. The universal trend for a more and more electrified world mayoffset the efficiency gains achieved by technological developments.

• Improving the GDP energy intensity, i.e. the final energy consumption required to produce aunit of output. The possibility to achieve this greatly depends not only on the degree ofdevelopment of the economy considered, but also on the structural characteristics of thesectors in which the economy is specialised. The progressive tertiarization of the worldeconomy may contribute to achieve this objective, although there exist several countrieswhose growth is still based on extremely intensive industrial sectors.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 7

1.2 Technology changes: a focus in power productionschemes

The technology issue is embedded in all these possible improvements to reduce carbonemissions. Concerning the first two points, the change of the fossil fuel mix or the fossil fuelshare towards a more carbon-saving situation can be possible only if the appropriate technologyis available and makes this shifting economically sensed, using given the primary energy carrierprices (present and expected). Energy conversion efficiency is an almost pure technologicalissue, although ‘external incentives’, such high primary energy prices work also favoringtechnological development. With respect to the fourth point, the overall GDP energy intensitydepends also on the technology, but it should be understood on a broader basis. Technologymeans there overall productive schemes, income-generation patterns and technological regimes,as clusters of technologies mutually connected.

The prospectives on the possible energy technology paths are fundamental in order to depictreliable multisectorial scenarios, which eventually could be used in the negotiating processesabout possible carbon emissions reduction. The actual energy technology trajectory is notindependent from what is happening in the overall economy. This expected feedback forces theconsideration of several possible technological trajectories, to which one could assign a certainprobability, depending on the future state of the world.

Energy technologies are crucial in incorporating energy to the productive process. Raw energycarriers have to be transformed into a form able to provide productive service. As a consequenceof the natural laws, there are clearly increasing marginal costs in the conversion of energyresources. In the same manner, the specific pollution (i.e. pollution per unit of useful or finalenergy use) and other external effects would also increase more than proportionally as thedepletion takes place.

Energy resource depletion would increase the overall energy intensity, since productiveprocesses always use the more accessible natural resources and the exploitation costs (in capital,labor and energy terms) increase as depletion proceeds, so the access to new fossil energyresources is also expected to exhibit increasing marginal costs. It is important to underline thatthis phenomenon takes place independently of the actual size of the resource reserves.Therefore, technology improvements are not unlimited, and they cannot avoid physicalexploitation limits or technical potential for each energy technology.

It may be concluded that, although it is clear that the global warming problem is a complexissue, and therefore requires an accurate description of the energy-economy-environmentinteractions, an adequate technology characterization is mandatory to describe and understandthe carbon-energy global system. In addition, technology prospects are fundamental since theymay provide the clues to the future characteristics of the backstop technological system. Thefeatures of this backstop energy structure are by no means predetermined: although we know apriori that only renewable energy technologies are sustainable in the long run, the precise futureexploitation schemes are still unknown. The path-dependency of the energy techno-economicsystem provides incentive for a further analyses in order to foster the dynamic tracking of thebest choice, minimizing the possibility of endeavouring suboptimal, non-reversible trajectories.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 8

Two main trends are detected in the world’s energy system today: increasing electrification ofstationary applications and increasing share of primary energy absorbed by the transportationsector. It generally acknowledged that the moving forces of the overall energy system (and, to alarge extent, of the global carbon emissions) are to be found within these two sectors. Anyserious attempt to assess the carbon mitigation possibilities in terms of costs has to incorporatethis statement as a framework consideration.

Amongst these two basic issues, major attention will be given in this study to the electric powerindustry. The reason for this is twofold: first, the technological diversity that is present withinthe electricity industry is by far much larger than the one corresponding to the transport sector:power generation technologies change faster and react to policy measures with a flexibilitywhich is not present within the transport sector. In addition, and perhaps connected to thepreceding remark, it is perceived that the structural changes within the power sector that arecurrently under way give the possibility to foster a more sustainable electrification pattern.Indeed, within the current exploitation schemes, electrification leaves more room for technologypolicy measures, whereas the transport sector has reached a deeper technological lock-in aroundthe standard explosion engine that makes it difficult to achieve significant advances vis-à-vis thecarbon emission issue from the technological point of view. Infrastructural changes, commandand control measures and deep social and individual behavioral changes would be required toachieve similar results in terms of carbon emissions abatement. This does not mean thattechnology has nothing to say with respect to transport-originated emissions, but rather thattechnology changes are not (today) a sufficient condition to achieve a more sustainabletransportation system, the bottleneck being placed around lifestyles and large infrastructures. Ina word, given the present trends, it is more likely than disruptive technology changes from thepower generation system would have an influence onto the transportation system than viceversa.This important question will be revisited in other parts of this volume.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 9

Chapter 2: Energy systems: a globalview

By P. Criqui, IEPE, A. Soria, IPTS and S. Isoard, IPTS

Energy is a key issue that is present in all the sectors of modern economies. Moreover, theavailability of cheap, abundant and safe energy sources is indeed a requisite for sustainedeconomic development in emerging economies. The ways in which it is consumed and used toproduce welfare is the matter of several disciplinary fields. Energy technologies are importantbecause energy crucial in the overall economic system, not only because of the scarcity of theresources (the world energy mix is based on non-renewable energy carriers), but also because ofthe environmental concerns. Indeed, environmental degradation is due, to a large extent, to theeffects of energy production, transformation and use.

The environmental aspects of energy consumption are becoming very important, but thevulnerability of the energy system to price shocks should not be forgotten: two out of the threelarge global economic recessions in the last fifty years were directly originated by a supplyshock in the energy sector.

Indeed, economic development and energy consumption are intimately intertwined. The causalrelationships between them are far from being clearly understood: on one side, energy isdemanded as a productive factor to generate welfare. On the other side, higher incomeundoubtedly induces more consumption of energy-related services.

The ultimate reason behind the massive increase of energy demand is not only the worldeconomic development (energy as productive factor) but also the demographic pressure thatpushes the demand of energy as a purely disembodied consumption good. In the OECDcountries, the average population annual growth rate in the period 1970-2010 is expected to be0.6%, whereas in developing countries, it will reach a 1.7% annual rate (2.1% on 1970-1992).Energy demand is driven in OECD countries mainly by the energy per capita increase, but indeveloping countries, both factors (per capita consumption and population growth) areimportant.

2.1 The EU carbon emissions within the overall greenhousegame

The environmental effects associated to the use of energy are undoubtedly an important drivingmechanism of the world energy system, as far as environmental concerns rapidly spread on thepublic opinion. Among the negative externalities associated to fossil fuels, CO2 emissions areprobably the most important one because of their global climate change implications. However,this threat is perceived with different degrees of concern by governments, decision-makers andgeneral public in different world zones. Amongst the developed nations, the European Union

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 10

has taken the leading role in recognizing the problem as an important issue to be solved, and inproposing coordinated efforts to achieve a cost-efficient solution. The global warming menace isalso differently regarded from developing countries. Large, rapidly growing countries, suchChina, India and some other in the Asian continent give priority to economic development, oftenaccompanied by massive increase in energy consumption. On the contrary, OECD countriesexhibit energy intensities of the GDP lower than unity, and are expected to contribute relativelyless to the global carbon emission increase. Under the IEA business-as-usual assumption, globalannual emissions are expected to increase by 40% between 1992 and 2010, concentrating indeveloping countries, whose emissions will reach the OECD levels by 2010: electricity supplyin two major developing countries, China and India, is coal-based (73%), which is the morecarbon-intensive energy carrier. In Europe and North-America, the nuclear reduction will bepartially compensated by gas use, whereas Japan is expected to enlarge the coal share in itsprimary energy mix. Within the entire world, however, the energy demand from the transportsector is expanding at a rate higher than the one corresponding to the GDP. Since it is primarilybased in oil and oil-derived fuels, it appears to be an important source of emissions, with a goodpotential for limiting.

Since the environmentally relevant variable is the total accumulated CO2 in the atmosphere, aneventual stabilization of emissions would not solve, in the long run, the greenhouse gasemissions problem. Many other factors, such as the speed of diffusion of carbon dioxide ontothe ocean, and the rate of carbon fixation in the vegetal cover are controlling the dynamics of thewhole carbon cycle, imposing several time constants and determining the actual evolution of thecarbon concentration in the atmosphere. Limiting, and, ultimately stabilizing the carbonemissions is not a well-posed objective unless an agreement is made upon the level on whichthis stabilization should take place. The Intergovernmental Panel for Climate Change oftenrefers to the standard target of 550 parts per million in volume (ppmv), which corresponds totwice as much the concentration in preindustrial times. The carbon concentration stabilizationpath greatly depends on the dynamics made to limit the carbon emissions, which would beaffects by a continuous cost-benefit analysis. The Framework Convention puts forward thepremise that the policies and measures to deal with climate change should be cost-effective so asto ensure global benefits at the lowest possible cost. The uncertainties about the spread overtime of both cost of carbon mitigation and damages to the global economic system is an issue ofutmost importance. Indeed, the reduction pathway is as important as the concentrationstabilization level in determining the total cost of the environmental policy. There exists a lineof thought (Wigley et al 96, Manne & Richels 92) arguing that delaying massive mitigationactions by 10-25 years would induce practically the same atmospheric and climatic harm, butthe costs to stabilize the carbon concentration would be significantly lower (due to thepossibility of exhausting recently new installed capacity and the probable reduction of costs forcarbon substitutes in the meantime). Other analysts share the opinion that, on the contrary, thereis a lot of no-cost (or low-cost) measures that could be taken already now, allowing for a moreaggressive carbon mitigation policy without, yielding a faster carbon concentration stabilizationand at a lower level without important economic effort (Grubb 97).

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 11

2.1.1 Trends in carbon emissions

While looking at the historical trends of CO2 emissions, it appears that large differences existamongst the main emitters. Looking first at the absolute value of emissions levels, the USA andthe EU appear to be the main polluters. Under starting from much modest levels, it is observedthat the increase rate of the carbon emissions by China and India will lead to these countries toemissions levels close to those of the USA and the EU within relatively few decades, since theyhave the highest annual growth rates (5.3% and 5.9% respectively). By comparing the emissionsannual growth rates on the 1973-1993 period on a country by country basis, with the central lineworldwide emissions growth rate of around 1.6%, the countries from the ASEAN group exhibitthe highest increase rate (6.5%). The OECD exhibits almost constant emissions, with an annualaverage growth rate around 0.5%. The EU-15 has even reduced slightly its level of emissionsabout 0.01% each year. More importantly, it shows that the EU has stopped since a long time toincrease its flow of CO2 emissions and this pattern may give more credibility to the propositionof the European Commission for the Kyoto negotiation table.

Worlwide CO2 Emissions

10000

100000

1000000

10000000

197 197 198 198 199 199

Years

WorldOECDEU-15ASEANChinaIndia

Figure 2-1Worldwide CO2 emissions

According to the more recent evaluations of 1997, the main CO2 emissions in the world aredistributed as follows:

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 12

Country/Zone CO2 Emissions (%) World PopulationShare(%)

US 25% 4.7%

EU (East Germany included) 19.6% 9.0%

China 13.5% 21.5%

Former Soviet Union 10.2% 2.6%

Japan 5.6% 2.2%

India 3.6% 16.3%

United Kingdom 2.5% 1.0%

South Korea 2.2% 0.8%

Canada 2.1% 0.5%

Australia 1.3% 0.3%

Table 2-1: Per year CO2 Emissions.

Amongst the world-wide CO2 emissions from fossil fuel consumption, the 20 largest carbonemitting countries in 1991 contributed over 81% the total carbon emissions. The top threecountries, i.e. the U.S., the former USSR and China, were responsible for around 49% of theworld emissions. From 1950 to 1990, global per capita emissions of CO2 from fossil fuelsincreased by a factor of 1.8, while global population increased by a factor of 2.1. Therefore,annual CO2 emissions have increased by a factor of 3.7.

These trends may be even reinforced, if one takes into account the emissions growth of thedifferent geographical zones as well as the foreseen population increase in the next threedecades. The EU emissions has been growing from the 1970’s at a mild rate (from 1985 to1994, the CO2 emissions annual rate from fossil fuels has been of 1.15%). A global reduction ofthe emissions from 1991 in electricity and heat production, the domestic and commercial use aswell as in the industry took place. On the contrary, emerging economies and developing onesexhibit high growth rates. Therefore, taking into account the foreseen population growth in theserespective zones, it appears that the EU will count only for a small share of the total CO2emissions in the next decades. Indeed, while France, UK, U.S. and Canada decreasedrespectively their emissions per capita during the 1973-1994 period of 2%, 0.9%, 0.6% and0.5% on average each year, China, India, Ex-USSR and Japan raised on average their emissionsby 3.77%, 3.75%, 1.5% and 0.4%.

An important issue is the analysis of the trends of emissions per capita and per GDP in theOECD and developing countries. The analysis of these trends may provide a very interestinginsight and contribute to the assessment of the future global emissions of the EU and discuss theinstruments to reach the targets

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 13

2.1.2 Trends in carbon intensity

Regarding the trends on emissions per capita, the emerging picture shows similar trends. Even ifsome developed countries exhibit high emissions rates per capita, the historical trends show ageneral stabilization in Europe of the emissions per capita and a catching-up of China and India.

CO2 Emissions Per Capita

0.1

1

10

100

1970 1975 1980 1985 1990 1995

Years

France

U.S

Japan

Canada

U.K

Ex-USSR

China

India

Figure 2-2: CO2 Emissions per capita.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 14

Source: Enerdata

Country Per-capita CO2 Emissions(metric tons)

USA 19.1

Canada 17.0

Australia 15.2

Former Soviet Union 14.1

Czech Republic 13.0

Poland 12.7

United Kingdom 9.8

Japan 8.8

Malaysia 3.7

China 2.3

Brazil 1.4

India 0.8

Table 2-2: Per capita CO2 emissions per country.

Considering these CO2 emissions data in relation with the GDP growth, a strong correlation isfound (not surprisingly). The developing countries, which exhibited two-digit growth rates inthe passed decade, have increasingly counted for a bigger share of total CO2 emissions, theeconomic growth having taken place without any concern of environmental protection ashappened earlier to the European countries. Indeed, in 1950, North America, Western Europeand Eastern Europe accounted for 89.2% of global CO2 emissions, Africa, Centrally PlannedAsia, Developing America, Far East and Oceania contributing for only 10.8%. Nowadays, thelatter regions contribute 40.5% of the CO2 emitted. In total, China has passed from the 10thrank in CO2 emissions in 1952 to the 3rd one in 1991, Japan from the 9th to the 4th, India fromthe 13th to the 6th, South Korea from the 58th to the 14th, North Korea from the 73rd to the16th and Iran from the 164th to the 17th. They are foreseen to become therefore the mainpolluters. The economic growth in the developing countries is expected to slow down but toremain much higher than OECD one. Economic and population growth are therefore the twomain driving-forces of CO2 emissions dynamics. Facing the global warming threat willtherefore require to include, sooner or later, the developing countries as active partners forreaching the emission targets.

During the 1973-1994 period, the rate of emissions/GDP has been very high in as well as in Ex-USSR and in India. While the developed countries have uniformly reduced their emissionsrespectively to the GDP (the average annual growth rate are: France: -3.6%, UK: 2.4%, Japan:2.32%, U.S.: 2% and Canada: 2.1%), India has increased the carbon-intensity of its economic

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 15

system (+1.2%/year) as well as the Ex-USSR (+0.3%/year). Although China exhibits animportant decreasing annual average rate of -3%, it remains amongst the most carbon-intensiveeconomies.

(Source: Enerdata)

CO2 Emi ssi ons/ GDP

0

2

4

6

8

1 0

1 2

1 9 7 0 1 9 7 5 1 9 8 0 1 9 8 5 1 9 9 0 1 9 9 5

Ye a r s Kg CO2 / US$ 9 0

France

U.S

Japan

Canada

U.K

Ex-USSR

China

India

Figure 2-3: CO2 Emissions/ GDP.

2.1.3 Technology and policy responses

Technological options and political instruments to reach the targets of CO2 emissions have to bediscussed. Several possible actions may be recommended, aiming at correcting externalitieseffects of polluting technologies, at the formation of correct price signals and at enhancing therelated technological progress.

A screening on the possible technology responses to cope with the problem of global warmingwill be presented in Chapter 3. The focus given there consists of a broad set of measures, fromcarbon sequestration and disposal to massive adoption of energy-efficient devices.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 16

Amongst possible policy measures, the internalisation of the external costs (in terms ofpollution) of the conventional technologies within the electricity costs per output unit wouldgive non-distorted price basis for the investment decision-making of the utilities. Indeed, thecompetitiveness of the renewables would be much more effective and would benefit a lot fromsuch an initiative. However, negotiations on its implementation as well as on the definition of aunified tax rate across Europe has been the source of delays in its introduction. Additionalinstruments may be used to enhance the diffusion of the new energy technologies which areenvironmental-friendly. R&D policies may contribute to facilitate fuel substitution for movingaway from fossil-fuel based technologies as well as for CO2 removal and sequestration. Finally,joint implementation may provide the opportunity to reduce the CO2 emissions in developingcountries, possibly the most important emitters in the future.

A simple extrapolation from the above-shown data indicates that the EU carbon emission trendwould be to remain roughly constant or even experience a mild increase in the years to come.This business as usual scenario has to be contrasted with the policy objectives of theCommission to reduce emissions to -8% in 2005 and to -13% by 2010 with respect to the 1990values, within the frame of the negotiations auspicated by the IPCC. Preliminary computationsbased on a bottom-up techno-economic approach have delivered a possible distribution of thedisaggregated emission reductions by Member State:

Country CO2 emission index in 2010 (1990 = 100)

B 85

DK 75

D 70

GR 105

E 115

F 95

IR 105

IT 90

L 60

NL 90

AT 75

P 125

FIN 90

SW 105

UK 80

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 17

Table 2-3: CO2 emission index in 2010.

When comparing these emissions reduction targets (which are the outcome of the 2nd ClimateConvention Conference held in Berlin), with the BAU projections, a significant gap appearsbetween what is desirable and what is likely to happen. It seems, therefore, that emerging energytechnologies have to fill this gap: the success of the achievement of the emission reductionobjectives is inevitably linked to the success of the energy research and technologicaldevelopment (RTD). The considered technological fields in which significant advances areexpected, and which have been retained to elaborate the above table are:

1. Improvements in energy efficiency in heavy industries.

2. Improvements in energy efficiency of electrical appliances.

3. Extended use of cogeneration.

4. Development of renewable energy technologies.

5. New car technologies.

6. Modal shifts in transport.

7. Regulations on energy efficiency of buildings.

8. Regulation on methane emissions from landfills.

9. Regulation of N2O Chemicals.

10. Regulation of Chlorofluorcarbonates (CFC) emissions.

Energy/CO2 taxation.

Notice that these measures do not include specifically any changes within the basic powergeneration system, but are rather focused on incremental innovations that concern itsfunctioning.

2.2 A projection for world energy patterns

2.2.1 Lessons from world energy outlooks

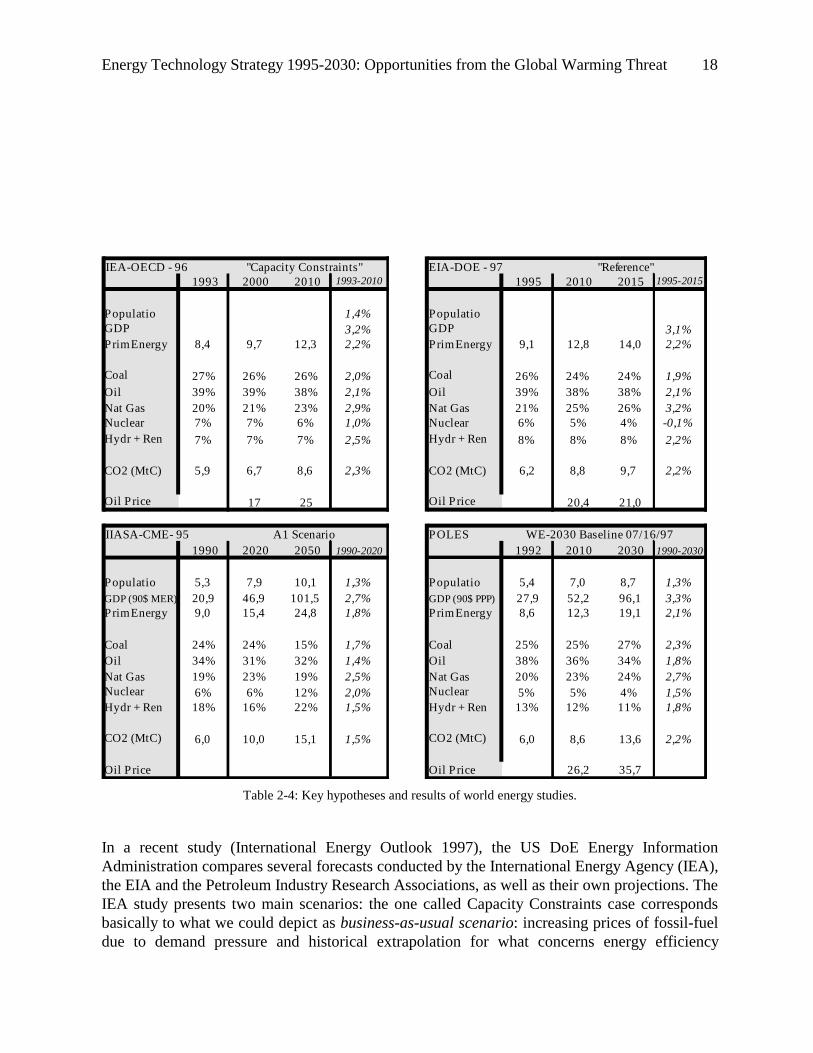

The prospective empirical analysis of the world energy system are nowadays fewer than theyused to be during the energy supply shock period. Nevertheless, several organisations havemaintained a certain activity within this domain. This is the case of the International EnergyAgency (IEA), the US Department of Energy and the Energy Information Administration (DoE-EIA) and the World Energy Council (WEC) The two first organisations have conducted studieswhose main objective has been to make mid-term, cross-checked projections reflecting, to alarge extent, a consensus on the trends within the sector. The scope of the World EnergyCouncil is different and also more ambitious, since their last analysis (conducted jointly with theInternational Institute of Applied System Analysis, IIASA), aims at showing the possibledevelopment within longer timescales (2020 and 2050).

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 18

IEA-OECD - 96 "Capacity Constraints" EIA-DOE - 97 "Reference"1993 2000 2010 1993-2010 1995 2010 2015 1995-2015

Populatio 1,4% PopulatioGDP 3,2% GDP 3,1%Prim Energy 8,4 9,7 12,3 2,2% Prim Energy 9,1 12,8 14,0 2,2%

Coal 27% 26% 26% 2,0% Coal 26% 24% 24% 1,9%Oil 39% 39% 38% 2,1% Oil 39% 38% 38% 2,1%Nat Gas 20% 21% 23% 2,9% Nat Gas 21% 25% 26% 3,2%Nuclear 7% 7% 6% 1,0% Nuclear 6% 5% 4% -0,1%Hydr + Ren 7% 7% 7% 2,5% Hydr + Ren 8% 8% 8% 2,2%

CO2 (MtC) 5,9 6,7 8,6 2,3% CO2 (MtC) 6,2 8,8 9,7 2,2%

Oil Price 17 25 Oil Price 20,4 21,0

IIASA-CME- 95 A1 Scenario POLES WE-2030 Baseline 07/16/971990 2020 2050 1990-2020 1992 2010 2030 1990-2030

Populatio 5,3 7,9 10,1 1,3% Populatio 5,4 7,0 8,7 1,3%GDP (90$ MER) 20,9 46,9 101,5 2,7% GDP (90$ PPP) 27,9 52,2 96,1 3,3%Prim Energy 9,0 15,4 24,8 1,8% Prim Energy 8,6 12,3 19,1 2,1%

Coal 24% 24% 15% 1,7% Coal 25% 25% 27% 2,3%Oil 34% 31% 32% 1,4% Oil 38% 36% 34% 1,8%Nat Gas 19% 23% 19% 2,5% Nat Gas 20% 23% 24% 2,7%Nuclear 6% 6% 12% 2,0% Nuclear 5% 5% 4% 1,5%Hydr + Ren 18% 16% 22% 1,5% Hydr + Ren 13% 12% 11% 1,8%

CO2 (MtC) 6,0 10,0 15,1 1,5% CO2 (MtC) 6,0 8,6 13,6 2,2%

Oil Price Oil Price 26,2 35,7

Table 2-4: Key hypotheses and results of world energy studies.

In a recent study (International Energy Outlook 1997), the US DoE Energy InformationAdministration compares several forecasts conducted by the International Energy Agency (IEA),the EIA and the Petroleum Industry Research Associations, as well as their own projections. TheIEA study presents two main scenarios: the one called Capacity Constraints case correspondsbasically to what we could depict as business-as-usual scenario: increasing prices of fossil-fueldue to demand pressure and historical extrapolation for what concerns energy efficiency

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 19

improvements. The Energy Savings case assumes an increase in energy efficiency measures,lower values of demand growth rates and essentially constant fossil-fuel prices. On the otherhand, the EIA presents three scenarios of low, medium and high economic growth.

Comparing different baseline projections or central scenarios is always problematic sinceaccounting conventions are not identical, especially in what refers to harmonising traditionalrenewable energies. However, results of this comparison reveal a great convergence concerningthe world-wide consumption of these energies, in any case until 2020: all these projections areinscribed, indeed, in a 12-13 Gtep trajectory in 2010 and 15-16 Gtep in 2020. A 19 Gtep in 2030for the POLES projection seems to be perfectly compatible with the continuation of this trend.

However, this apparent convergence of global results conceals potential incoherence, to anextent in which price estimations - once they are specified - are far from being the same. Thus,the DOE projection is supported by an almost stable price estimation of oil until 2015, whereasthis price is already increasing 40% for 2010, in the IEA projection and the POLES referencescenario. In this last projection, it can be noticed that there is a strong price increase after 2010,due to the production decrease of conventional fuel and the urgent necessity of non-conventionalresources.

According to power generation, detailed results are equally less convergent. However, in thescope of 2010 - that is, the deadline nowadays fixed by international greenhouse effectsnegotiations - the world-wide energetic supply should probably have little more than 3 Gtep ofcoal and natural gas and between 4.5 and 5 Gtep of oil. Considering the coefficients of carbon ofeach type of energy, the world-wide energy emissions of CO2 would be about 8,7 GtC, againstthe 6 GtC in 1990. The important difference between the stabilisation aims fixed in theinternational negotiations and the "business-as-usual" projections that lead to an almost 45%increase of the emissions in 20 years, starting from 1990 can be noted.

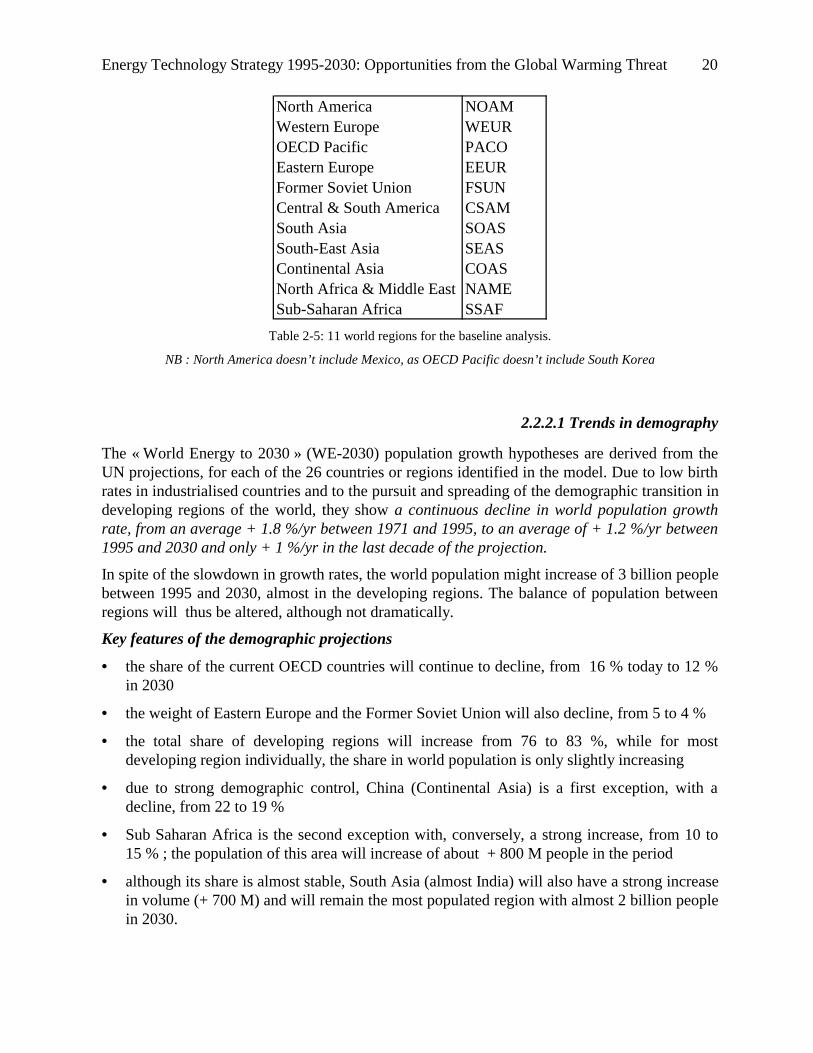

2.2.2 WE-2030 exogenous hypotheses: population and GDP growthin 11 world regions

While 26 countries or regions are individualised in the POLES model, most analyses of theBaseline exogenous hypotheses and results will be performed according to a worlddisaggregation in eleven geographical or geopolitical regions (acronyms from Table 2.5 are usedin the rest of the text or tables).

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 20

North America NOAMWestern Europe WEUROECD Pacific PACOEastern Europe EEURFormer Soviet Union FSUNCentral & South America CSAMSouth Asia SOASSouth-East Asia SEASContinental Asia COASNorth Africa & Middle East NAMESub-Saharan Africa SSAF

Table 2-5: 11 world regions for the baseline analysis.

NB : North America doesn’t include Mexico, as OECD Pacific doesn’t include South Korea

2.2.2.1 Trends in demography

The « World Energy to 2030 » (WE-2030) population growth hypotheses are derived from theUN projections, for each of the 26 countries or regions identified in the model. Due to low birthrates in industrialised countries and to the pursuit and spreading of the demographic transition indeveloping regions of the world, they show a continuous decline in world population growthrate, from an average + 1.8 %/yr between 1971 and 1995, to an average of + 1.2 %/yr between1995 and 2030 and only + 1 %/yr in the last decade of the projection.

In spite of the slowdown in growth rates, the world population might increase of 3 billion peoplebetween 1995 and 2030, almost in the developing regions. The balance of population betweenregions will thus be altered, although not dramatically.

Key features of the demographic projections

• the share of the current OECD countries will continue to decline, from 16 % today to 12 %in 2030

• the weight of Eastern Europe and the Former Soviet Union will also decline, from 5 to 4 %

• the total share of developing regions will increase from 76 to 83 %, while for mostdeveloping region individually, the share in world population is only slightly increasing

• due to strong demographic control, China (Continental Asia) is a first exception, with adecline, from 22 to 19 %

• Sub Saharan Africa is the second exception with, conversely, a strong increase, from 10 to15 % ; the population of this area will increase of about + 800 M people in the period

• although its share is almost stable, South Asia (almost India) will also have a strong increasein volume (+ 700 M) and will remain the most populated region with almost 2 billion peoplein 2030.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 21

1992 2000 2010 2020 2030

M habWorld WRD 5424 6150 7027 7893 8713

% of World totalNorth America NOAM 5 5 5 4 4Western Europe WEUR 8 7 7 6 6OECD Pacific PACO 3 3 2 2 2Eastern Europe EEUR 2 2 2 2 2Former Soviet Union FSUN 5 5 5 4 4Central & South America CSAM 8 9 9 9 9South Asia SOAS 22 22 22 22 23South-East Asia SEAS 10 10 10 10 10Continental Asia COAS 22 21 20 20 19North Africa & Middle East NAME 5 5 6 7 7Sub-Saharan Africa SSAF 10 11 13 14 15

Table 2-6: World population 1992-2030

2.2.2.2 Economic projections : the GDP dynamics

WE-2030 economic projection are derived from Worldscan economic projections, adjusted forthe changes from Market Exchange Rate to Purchasing Power Parity GDP growth rates. Whilemost economic forecasts present variations in MER-GDP, the economic variables used in thePOLES Database are expressed in the CEPII PPP conversion system. This is done in order toaccount both for the informal sector, which in most developing areas constitutes to a largeproportion of total economic activity and for the corresponding purchasing power of households.It is thus considered that the PPP-GDP is a better indicator for the energy consumption andenergy intensity of GDP and is also more suited for international comparisons.

MER-GDP and PPP-GDP projections show significantly different pictures of world economicstructure and dynamics. Using PPP, the initial GDP level is higher in developing regions, whilethe corresponding growth rate of the economy is lower. This results both in a very differentstructure of world GDP and, paradoxically, in a higher aggregated growth - in spite of lowerindividual rates - as the share of the rapidly growing regions is more important. Thisphenomenon is illustrated in Table 2.7, showing the differences in structure and growth rates forthe WE-2030 Baseline and for the original Worldscan economic projection.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 22

WE-2030 - Purchasing Power Parity Worldscan - Market Exchange Rate PPP-MER

1990 2020 1990-2020 1990 2020 1990-2020 1990-2020

World WRD G$90 PPP yagr G$90 MER yagr27,4 72,5 3,3% 21,6 54,6 3,1% 0,2%

% of World GDP % of World GDPNorth America NOAM 22 16 2,2% 28 21 2,2%Western Europe WEUR 23 16 2,0% 34 24 2,0%OECD Pacific PACO 10 7 2,2% 15 11 2,2%Eastern Europe EEUR 3 2 2,1% 2 2 3,4% -1,3%Former Soviet Union FSUN 9 5 1,4% 4 4 2,4% -1,0%Central & South America CSAM 9 11 4,1% 5 9 5,2% -1,1%South Asia SOAS 5 7 4,6% 2 5 6,7% -2,1%South-East Asia SEAS 6 10 4,8% 4 9 6,0% -1,2%Continental Asia COAS 9 20 6,2% 2 9 8,7% -2,5%North Africa & Middle East NAME 4 5 4,0% 3 4 4,1% -0,1%Sub-Saharan Africa SSAF 2 2 3,3% 1 2 4,0% -0,7%

Table 2-7: PPP and MER world economic structure and dynamics.

In both the PPP and MER projections, the resulting economic picture is one of a sustainedeconomic growth at world level with an average growth superior to 3 %/yr, between 1995 and2030 at world level. This is not much higher than the secular trend in world output growth of +3 %/yr between 1900 and 1990, according to Angus Maddison. This is also not much higherthan the growth experienced between 1971 and 1995 : + 3.1 %/yr (PPP). It has to be noted thatthis growth rate has been reached, in the past quarter of a century, in spite of a series of criseswhich affected successively the different regions of the world : the oil shocks for theindustrialised oil importing countries, the debt crisis in the LDCs and the decay of the CentrallyPlanned Economies.

For the future and in a decade by decade perspective, it appears that combining the hypothesis ofa recovery in the former CPEs and the one of a declining but still high growth in Asia, the 2000-2010 period might experience the highest growth rate with about + 3.8 %/yr on average. Worldgrowth rates are then declining, to + 3.3 and + 2.9 %/yr in the two following decades.

Key features of the economic projections

• according to the projection, OECD countries might experience a moderate growth in the2000-2010 period (about + 2.5 %/yr), while the growth rate will still decline in the twofollowing decades, in the range of 1 to 2 %/yr

• economies in transition might recover during the two first decades of the next century withgrowth rate around 3.5 %/yr and then experience more moderate growth, above 2 %/yr

• all developing regions might grow at rates higher than + 3.5 %/yr during the projectionperiod

• as compared to the 1971-1995 period, growth will accelerate in Latin America, Africa-Middle East and South Asia, while it will decelerate in South East and Continental Asia

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 23

• however Continental Asia will remain the region with the highest growth potential, speciallyat the beginning of the projection period, while after 2010 it is overwhelmed by otherregions, specially South Asia

yagr 1971-95 1995-2030 1971-80 1980-90 1990-2000 2000-10 2010-20 2020-30

NOAM 2,5% 2,1% 2,8% 2,7% 2,0% 2,5% 2,2% 1,7%WEUR 2,4% 2,1% 3,0% 2,4% 1,5% 2,5% 2,0% 1,7%PACO 3,6% 2,0% 4,3% 3,9% 2,2% 2,7% 1,6% 1,2%EEUR 0,3% 2,9% 3,6% -0,6% -0,4% 3,4% 3,3% 2,1%FSUN -0,1% 3,3% 3,1% 1,6% -3,3% 3,9% 3,7% 2,7%CSAM 3,3% 3,8% 5,5% 1,2% 3,5% 4,6% 4,1% 3,1%SOAS 4,4% 4,8% 3,4% 5,6% 4,3% 4,7% 4,9% 4,7%SEAS 6,7% 4,2% 7,6% 6,5% 5,3% 5,0% 4,2% 3,3%COAS 7,4% 5,1% 5,6% 8,5% 8,1% 6,3% 4,3% 3,6%NAME 3,3% 4,2% 5,1% 1,6% 3,6% 4,1% 4,5% 4,5%SSAF 2,4% 3,7% 3,0% 2,0% 2,5% 3,1% 4,3% 4,3%

WRD 3,1% 3,3% 3,7% 3,0% 2,7% 3,8% 3,3% 2,9%

Table 2-8: World economic growth (PPP).

2.2.2.3 Changes in per capita GDP profiles

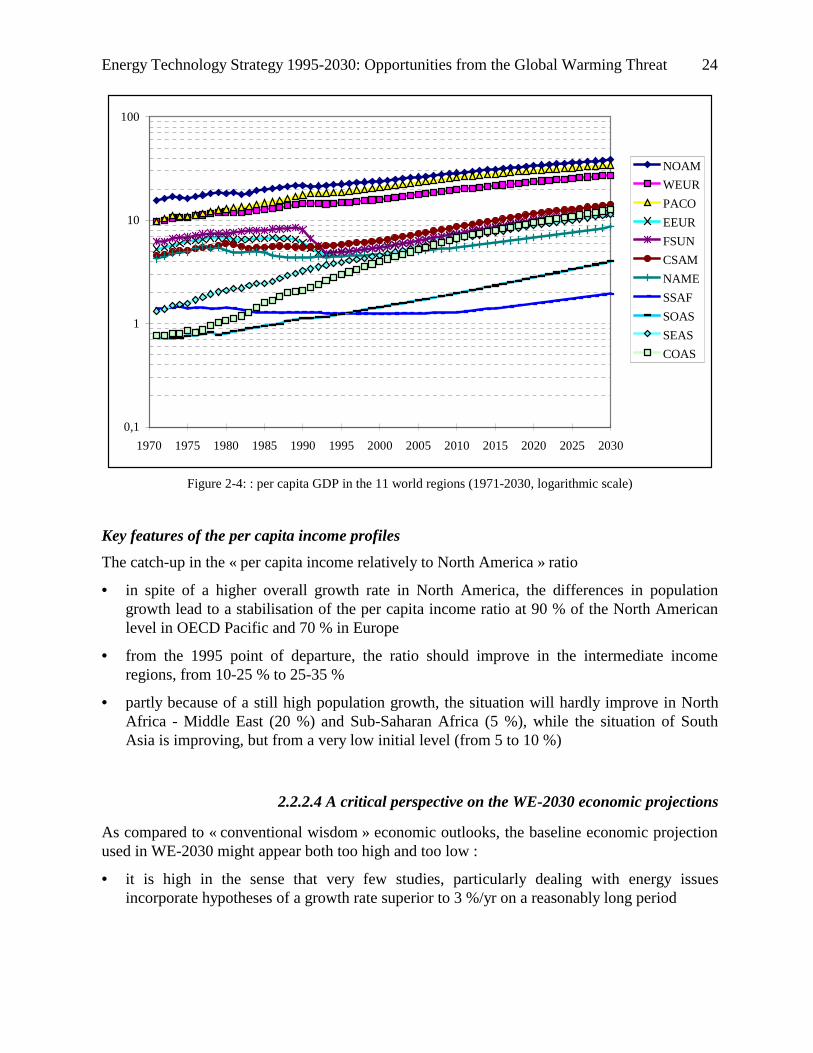

While combining demographic trends and GDP projections, it is possible to analyse the percapita GDP profiles and to characterise the changes in the dynamics in hierarchy of the differentregions considered. In this perspective, the situations in 1970, 1995 and 2030 can be describedas follows :

• in 1970 the North America region presents a clear advance on other industrialised areas witha yearly per capita GDP of 15 000 $ (1990$ PPP) against 10 000 $ in Europe and PacificOECD ; an intermediate group of 4 000 to 6 000 $ per capita is lead by the Soviet Union, italso incorporates Latin America and North Africa - Middle East ; at the bottom end, withrevenues between 750 and 1 400 $ lay the regions of Asia and Sub-Saharan Africa ;

• in 1995, the situation is already significantly altered ; while Pacific OECD is now in anintermediate position between North America and Europe, the former CPEs has slippedbehind Latin America, while South East and Continental Asia have almost caught-up withthe group of intermediate income countries ; only two regions lay behind, Sub-SaharanAfrica and South Asia ;

• in 2030, the picture might still look different ; while the convergence among industrialisedcountries may continue, it may appear quite strong among intermediate income regions withthe complete catch up of South East and Continental Asia to the group formed by LatinAmerica and the countries in transition ; meanwhile, South Asia’s take-off may continue at asteady speed, it may take until 2010 before the increase in per capita income of Sub-SaharanAfrica resumes.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 24

0,1

1

10

100

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

NOAM

WEUR

PACO

EEUR

FSUN

CSAM

NAME

SSAF

SOAS

SEAS

COAS

Figure 2-4: : per capita GDP in the 11 world regions (1971-2030, logarithmic scale)

Key features of the per capita income profiles

The catch-up in the « per capita income relatively to North America » ratio

• in spite of a higher overall growth rate in North America, the differences in populationgrowth lead to a stabilisation of the per capita income ratio at 90 % of the North Americanlevel in OECD Pacific and 70 % in Europe

• from the 1995 point of departure, the ratio should improve in the intermediate incomeregions, from 10-25 % to 25-35 %

• partly because of a still high population growth, the situation will hardly improve in NorthAfrica - Middle East (20 %) and Sub-Saharan Africa (5 %), while the situation of SouthAsia is improving, but from a very low initial level (from 5 to 10 %)

2.2.2.4 A critical perspective on the WE-2030 economic projections

As compared to « conventional wisdom » economic outlooks, the baseline economic projectionused in WE-2030 might appear both too high and too low :

• it is high in the sense that very few studies, particularly dealing with energy issuesincorporate hypotheses of a growth rate superior to 3 %/yr on a reasonably long period

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 25

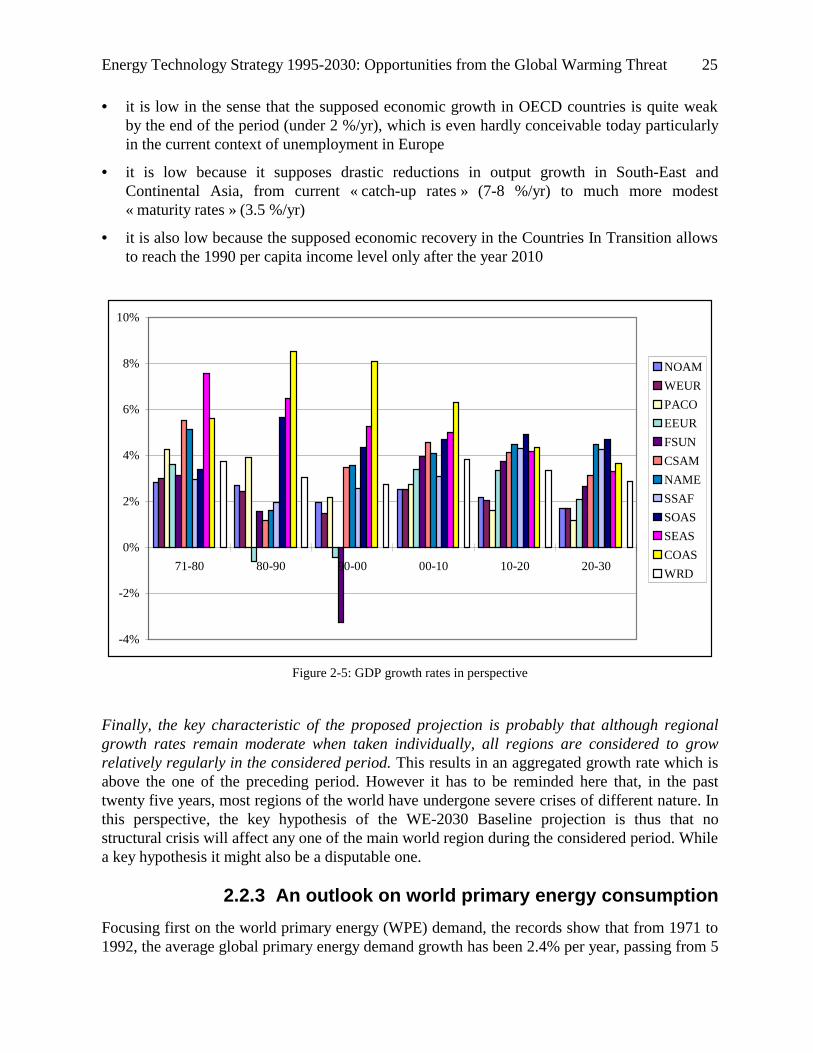

• it is low in the sense that the supposed economic growth in OECD countries is quite weakby the end of the period (under 2 %/yr), which is even hardly conceivable today particularlyin the current context of unemployment in Europe

• it is low because it supposes drastic reductions in output growth in South-East andContinental Asia, from current « catch-up rates » (7-8 %/yr) to much more modest« maturity rates » (3.5 %/yr)

• it is also low because the supposed economic recovery in the Countries In Transition allowsto reach the 1990 per capita income level only after the year 2010

-4%

-2%

0%

2%

4%

6%

8%

10%

71-80 80-90 90-00 00-10 10-20 20-30

NOAM

WEUR

PACO

EEUR

FSUN

CSAM

NAME

SSAF

SOAS

SEAS

COAS

WRD

Figure 2-5: GDP growth rates in perspective

Finally, the key characteristic of the proposed projection is probably that although regionalgrowth rates remain moderate when taken individually, all regions are considered to growrelatively regularly in the considered period. This results in an aggregated growth rate which isabove the one of the preceding period. However it has to be reminded here that, in the pasttwenty five years, most regions of the world have undergone severe crises of different nature. Inthis perspective, the key hypothesis of the WE-2030 Baseline projection is thus that nostructural crisis will affect any one of the main world region during the considered period. Whilea key hypothesis it might also be a disputable one.

2.2.3 An outlook on world primary energy consumption

Focusing first on the world primary energy (WPE) demand, the records show that from 1971 to1992, the average global primary energy demand growth has been 2.4% per year, passing from 5

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 26

Billion TOE to around 8 Billion TOE in 1992. Looking at the picture on a longer time scale, itmay be noticed that world primary energy consumption has passed from about 0.5 Billion TOEat the beginning of this century to today’s levels. This 1600% increase took placesimultaneously with the comparatively modest increase of 400% of the world population: percapita energy consumption increase accounted for the remaining 400% of WPE increase.

With respect to the fuel mix, it should be remembered that today, around 85% of the globalprimary energy comes from fossil fuels. Within the IEA Capacity Constraints (CC) case(basically a business as usual projection), the WPE is assumed to reach around 12 Billion TOEby 2010, whereas according to the EIA International Energy Outlook 97 in the reference case(IEO 97-RC), this could reach around 12.7 Billion TOE by the same date. The correspondingexpected average annual growth for the period 1990-2010 would be 2.2% and 2.0%,respectively. If this assumption obtains, current WPE demand will double in around 33 years.Under these assumptions, the fossil fuel share of the WPE could reach 90% by 2010, and naturalgas would exhibit the fastest-growing rate (an average annual rate of 2.9% in the next 15 years,according to IEA CC and IEO 97-RC). Nevertheless, the largest increase would take place in thecoal market: the global coal demand will expand from today’s 2400 MToe to 3000 MToe by2010. This expansion would be concentrated around developing economies: actually, the OECDcoal share is expected to shrink from 45% to 30% in the period 1990-2010.

Looking at WPE demand by zones, a noticeable fact is that the relative weight of the developedworld is expected to decrease from 65% in 1971 up to 47% in 2010. On the contrary, thedeveloping countries will expand their share from 26% in 1990 to 38% in 2010.

GDP growth is a key variable to determine energy demand. The standard forecast assumed bythe IEA to carry out the analysis whose results have been summarized above consists of a quiteuniform annual GDP growth of 3% in the forthcoming decades in OECD, whereas the expectedbehavior of the non-OECD countries is not homogeneous: East Asia will be the fastest growingzone (6.6%), followed by South Asia (5.4%), South and Central America and Africa (3.6%). By2010, the GDP of non-OECD countries (not including the Former Soviet Union and newindependent states), encompassing 80% of the world population, is expected to reach theaggregate GDP of OECD countries, that would account for 16% of the world population by thattime. These assumptions are in good agreement with the ones projected by the WEFA group,that have been taken for the IEO 97, with different aggregation patterns.

Although GDP is important, changes in GDP energy intensity can also motivate noticeablefluctuations in the overall energy demand. During the past, a persistent trend of diminishingGDP energy intensity has been observed, and it is expected to continue to decrease on a globalscale, but at lower rate. In OECD countries, the main trade-off will take place between aprogressive tertiarization of the economy vs. increasing transport intensity, both for freight andpassengers. The decline of the secondary sector weight will be particularly relevant in theeconomy of the former Soviet Union and the Central and Eastern Europe countries. Theindustrialization of developing countries will probably concern less energy-intensive processes.

2.2.3.1 World consumption by source of energy

According to the WE-2030 baseline projection, world primary energy consumption couldincrease at an average rate of 2.2 %/yr over the next three decades. Quite important changes may

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 27

occur in the world fuel mix as oil could incur a loss in market share - from 38 to 34 % , due tosubstantial price increases (see below table 2.9). This would benefit mainly to natural gas - from19 to 24 % - and also to coal. As for non fossil energies, the share of nuclear energy in worldsupply could decrease from 6 to 5%, while the regular increase in large hydro and the take-off ofnew renewables would be offset by the decline of traditional biomass : altogether, the share ofthe renewable sources of energy could slightly decrease from 12.7 to 11.2 % of world energyconsumption.

Mtoe Mtoe % of World total1992 2000 2010 2020 2030 1992 2000 2010 2020 2030

2152 2331 3026 3926 5064 25% 24% 25% 25% 27% Oil 3231 3700 4378 5257 6438 38% 38% 36% 34% 34% Natural 1670 2057 2771 3745 4626 19% 21% 23% 24% 24% Nuclear 457 577 628 708 805 5% 6% 5% 5% 4% Hydro+Geoth 477 557 702 865 1037 6% 6% 6% 6% 5% Trad.Biomass 429 373 315 268 230 5% 4% 3% 2% 1% Other 181 227 487 711 871 2% 2% 4% 5% 5%

P rimary 8596 9822 12307 15480 19070 100% 100% 100% 100% 100%

0,2%

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

1992 2000 2010 2020 2030

Other Renewables

Trad.Biomass

Hydro+Geoth

Nuclear

Natural gas

Oil

Solids

Table 2-9: Energy consumption and supply in WE-2030 Baseline

Figure 2-6: Energy consumption and supply in WE-2030 Baseline

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 28

2.2.3.2 International energy prices

One of the main features of the POLES model is its ability to produce endogenous changes forinternational energy prices. The price mechanisms incorporated in the model do take intoaccount the balance of supply and demand for oil, natural gas and coal : in the short run, pricesdepend on the demand variation and on oil supply capacities in the Gulf « swing producer »countries ; in the longer run prices depend on the Reserve on Production ratios for oil andnatural gas (see below .).

Price changes are quite significant in the Baseline projection, as oil price increase to 26 90$/blin 2010 and to 36 90$/bl in 2030. Natural gas prices, which are simulated for three mainregional markets, also show significant increases after 2000. These price increases are of coursedue to the total demand increases, they also contribute, in the model, to considerably moderatethese increases.

OIL 1973 1980 1990 2000 2010 2020 2030

World crude oil price 9,8 41,4 20,0 19,7 26,9 32,9 36,9

World RP ratio 24,5 25,9 40,6 39,4 33,3 28,2 22,7

NATURAL GAS 1975 1980 1990 2000 2010 2020 2030 Import prices ($90/boe) N. American market 20,4 30,0 10,8 14,5 19,0 24,4 28,4 European market 11,3 21,4 15,2 15,9 19,0 25,1 30,6 Asian market 19,2 36,5 20,6 28,6 34,0 36,3 42,3

Import prices ($90/Mbtu) N. American market 3,5 5,1 1,8 2,5 3,2 4,2 4,8 European market 1,9 3,6 2,6 2,7 3,2 4,3 5,2 Asian market 3,3 6,2 3,5 4,9 5,8 6,2 7,2

Table 2-10: Oil and gas prices in the WE-2030 Baseline.

2.2.3.3 Trends in energy intensities

In the POLES model, trends in energy intensities are dependent on the structural evolutions ofthe economy and on autonomous technology improvements. But they are also stronglyinfluenced by price-effects.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 29

toe / 1000 90$ (PPP) Annual % change1992 2000 2010 2020 2030 92-00 00-10 10-20 20-30

North America 369 340 287 247 218 -1,0% -1,7% -1,5% -1,2%Western Europe 220 217 192 173 159 -0,2% -1,2% -1,0% -0,8%OECD Pacific 205 196 174 159 150 -0,5% -1,2% -0,9% -0,6%Eastern Europe 479 335 270 236 211 -4,4% -2,1% -1,4% -1,1%Former Soviet Union 745 470 324 282 261 -5,6% -3,6% -1,4% -0,8%Central & South America 188 198 181 169 159 0,7% -0,9% -0,7% -0,6%South Asia 258 230 207 191 176 -1,4% -1,1% -0,8% -0,8%South-East Asia 250 240 204 187 173 -0,5% -1,6% -0,9% -0,8%Continental Asia 284 233 220 203 191 -2,5% -0,6% -0,8% -0,6%North Africa & Middle East 318 306 258 255 248 -0,5% -1,7% -0,2% -0,3%Sub-Saharan Africa 379 369 357 339 321 -0,3% -0,3% -0,5% -0,5%World 303 265 227 206 192 -1,7% -1,5% -1,0% -0,7%

Table 2-11: Energy intensities.

Up to 2000 and even 2010 world energy intensity decreases significantly, partly because ofstrong reductions in energy demand in the transition countries ; it has to be noted however thatin 2010 the energy intensity of the Former Soviet Union is still 13 % higher than that of the US.

The oil price increase of more than fifty percent between 2000 and 2020 puts a further pressureon energy intensities, in industrialised countries, but also in developing countries, with energyintensity declines of commonly - 1 %/yr. Intensity gains are lower by the end of the projection,largely because of more moderate oil price increases (less than ten percent in ten years).

2.2.3.4 World consumption by region

Energy demand growth will be low in OECD region, with growth-rate under 2 %/yr at thebeginning of the projection period and under 1 %/yr at the end. The economic recovery in thecountries in transition also induces a recovery in energy demand ; the corresponding increase inconsumption is however moderate, this implies continued improvements in energy efficiency(see below). Conversely, energy demand growth-rates are between 3 and 5 %/yr in alldeveloping regions ; exceptions are growth rates under 3 %/yr in North Africa-Middle East until2010 and South-East Asia after 2020 ; conversely, growth rates exceed 5 %/yr in China, until2010 (this rate has been of 4.4 %/yr between 1985 and 1995).

China’s energy consumption might exceed that of Western Europe by 2010 and that of NorthAmerica by 2020. In 2030 four regions will each represent a total consumption between 1.2 and1.7 Gtoe, i.e. the current consumption of Western Europe: the Former Soviet Union, LatinAmerica, South Asia and South-East Asia.

Energy Technology Strategy 1995-2030: Opportunities from the Global Warming Threat 30

Mtoe % of World total1992 2000 2010 2020 2030 1992 2000 2010 2020 2030

North America 2233 2469 2674 2852 2979 26% 26% 22% 19% 16%Western Europe 1404 1580 1787 1965 2138 17% 17% 15% 13% 12%OECD Pacific 568 642 746 796 847 7% 7% 6% 5% 5%

sub-total 50% 49% 44% 38% 32%

Eastern Europe 279 232 262 317 349 3% 2% 2% 2% 2%Former Soviet Union 1227 786 797 1003 1206 15% 8% 7% 7% 7%

sub-total 18% 11% 9% 9% 8%

Central & South America 474 659 938 1317 1684 6% 7% 8% 9% 9%South Asia 351 448 636 949 1384 4% 5% 5% 6% 8%South-East Asia 486 684 950 1307 1677 6% 7% 8% 9% 9%Continental Asia 786 1204 2095 2963 3974 9% 13% 18% 20% 22%North Africa & Middle East 372 473 595 906 1367 4% 5% 5% 6% 7%Sub-Saharan Africa 260 309 405 586 842 3% 3% 3% 4% 5%

sub-total 32% 40% 47% 54% 59%

Table 2-12: Primary energy consumption, by region

During the projection period a major shift in world energy consumption will thus take place :

• while OECD countries still represent half of total world energy consumption, their share willbe reduced to less than one third in 2030 ;

• conversely, developing countries now represent one third of world total, their share mightincrease up to 60 % in 2030.

This is shift is of course of paramount importance for many key issues, such as energy supplysecurity, financial requirements, new technology development and diffusion, climate changepolicy ...

2.2.4 A check of final energy demand profiles: the energy serviceapproach

World final energy (WFE) demand has passed from 4 Billion TOE in 1970 to something lessthan 6 Billion TOE in 1990, and is expected to reach around 8 Billion TOE by 2010. Thesefigures reflect an increased penetration of electricity, at least until 2000, the progressiveelectrification of the world final demand will being the main reason. Gains in technologicalenergy conversion efficiency are expected to facilitate overall energy efficiency increase from2000 on.