INSIGHT - The IRRV · Lester Dinnie tracks down the winners of last ... Andy Cummins, Business...

36

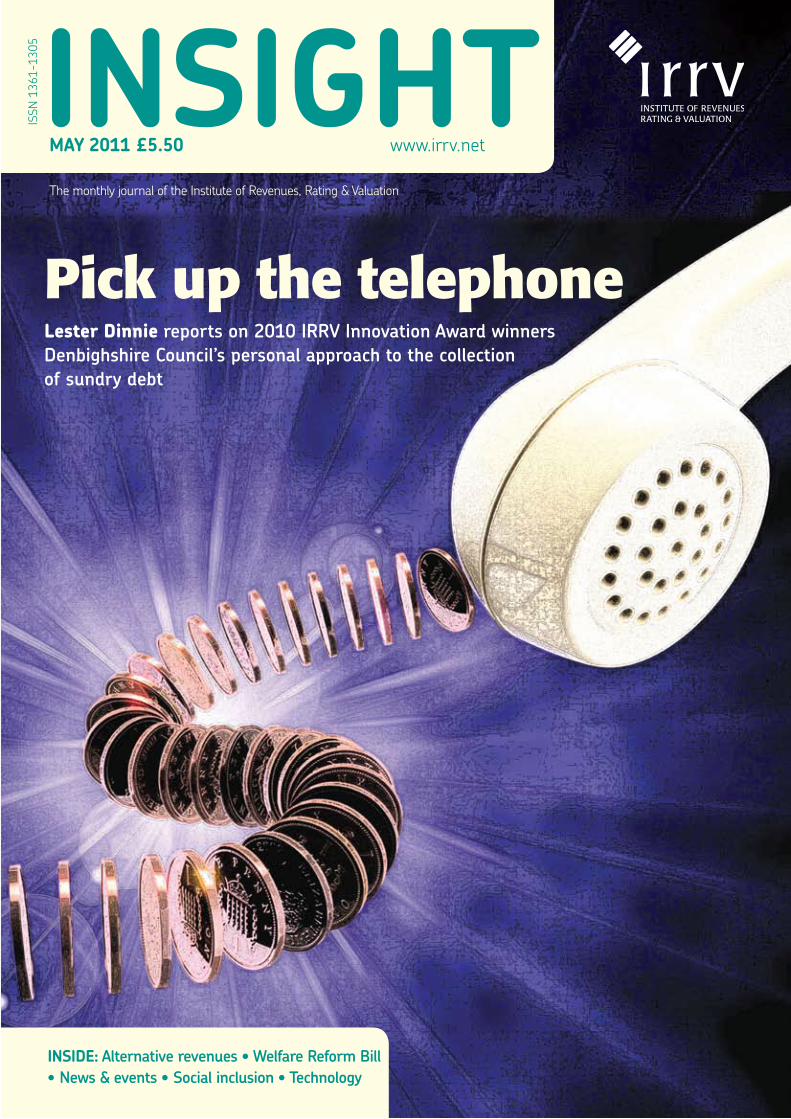

INSIGHT INSIDE: Alternative revenues • Welfare Reform Bill • News & events • Social inclusion • Technology MAY 2011 £5.50 www.irrv.net ISSN 1361-1305 Pick up the telephone Lester Dinnie reports on 2010 IRRV Innovation Award winners Denbighshire Council’s personal approach to the collection of sundry debt The monthly journal of the Institute of Revenues, Rating & Valuation

Transcript of INSIGHT - The IRRV · Lester Dinnie tracks down the winners of last ... Andy Cummins, Business...

INSIGHT

INSIDE: Alternative revenues • Welfare Reform Bill• News & events • Social inclusion • Technology

MAY 2011 £5.50 www.irrv.net

ISSN

136

1-13

05

Pick up the telephoneLester Dinnie reports on 2010 IRRV Innovation Award winners Denbighshire Council’s personal approach to the collection of sundry debt

The monthly journal of the Institute of Revenues, Rating & Valuation

IRRV INSIGHT

Managing Editor

John Roberts

Editorial Director

Lester Dinnie

Art Director

Don Tregartha

Designers

Clare Barker

Roddy Clenaghan

Publisher

Tregartha Dinnie Ltd

IRRV

Chief Executive David Magor, OBE IRRV (Hons) Northumberland House 5th Floor 303-306 High Holborn, London WC1V 7JZ T 020 7831 3505 E [email protected] W www.irrv.net

Enquiries Membership 020 7691 8996 Conferences 020 7691 8987 Subscriptions 020 7691 8996

Advertising T 020 7691 8996 E [email protected]

Editorial John Roberts IRRV (Hons) T 07952 659 258 E [email protected]

Tregartha Dinnie Ltd Ibex House, 5 Keller Close, Kiln Farm, Milton Keynes MK11 3LL T 01908 306500 W www.tregartha-dinnie.co.uk

IRRV Insight is produced by Tregartha Dinnie Ltd on behalf of the IRRV.

Unless otherwise indicated, copyright in this publication belongs to the IRRV.

May 2011 ISSN 1361-1305

© IRRV 2011. Reproduction in whole or in part of any article is prohibited without prior written consent. The views expressed in this magazine do not necessarily represent the views of the Institute. Whilst all due care is taken regarding the accuracy of information, no responsibility can be accepted for errors. Any advice given does not constitute a legal opinion.

IRRV Council: IRRV President Kerry Macdermott IRRV (Hons); Senior Vice-President Roger Messenger BSc (Est Man) FRICS IRRV (Hons) MCIArb REV; Junior Vice-President David Chapman IRRV (Hons); Honorary Treasurer Allan Traynor FCCA IRRV (Hons); Phil Adlard Tech IRRV MlnstLM MCMI; Alan Bronte FRICS IRRV (Hons); Robert Brown BSc

FRICS IRRV (Hons); Tracy Crowe CPFA IRRV (Hons); Carol Cutler IRRV (Hons); Tom Dixon RD BSc (Est Man) FRICS IRRV (Hons); Ian Ferguson IRRV (Hons); Geoff Fisher FRICS (Dip Rating) IRRV (Hons) REV; Richard Guy FRICS (Dip Rating) IRRV (Hons) MCIArb; Richard Harbord MPhil CPFA FCCA IRRV (Hons) FIDP FBIM FRSA; Mary Hardman IRRV (Hons) FRICS MCMI; Gordon Heath BSc IRRV (Hons); Julie Holden IRRV (Hons) MCMI CMg; Caroline Hopkins IRRV (Hons); Maureen Neave Tech IRRV; Tony Masella MRICS MCIOB IRRV (Hons) AFA F.Inst.AM; Graham Ryall FRICS IRRV (Hons); Peter Scrafton IRRV (Hons) FCIArb MRSA (Hons); Kevin Stewart IRRV (Hons) MAAT MCMI; Angela Storey Tech IRRV MCMI; Bob Trahern IRRV (Hons);

Chief Executive’s notes 05Hastily concocted plans to localise council tax rebates and business rates are fundamentally flawed, says David Magor, and must be readdressed before it’s too late

News and events 06

Letters to the editor 07

Running the Institute 08

Education & membership 10

Management 25In the second of his new series on developing staff, Sean Langley reflects on race-cards, bubble and squeak and a loaf of bread...

Alternative revenues 26Risk – how do you measure, let alone audit, what you cannot see? Alan Clark suggests a solution

Insight introduces a new regular supporter of the Institute, JBW Group, and finds out what’s making the debt management and enforcement solution providers tick

Legal view 28

Technology 30

Doherty’s despatch 32

Viewpoint 34Richard Harbord takes his turn on the Viewpoint round

Cover story 20Want to collect £27 million in sundry debt?Lester Dinnie tracks down the winners of last year’s IRRV Innovation Award, Denbighshire Council

Regular items Features

2

INsI

GH

t w

ww

.irrv

.net

Editor’s welcome

What’s in the next issue ... – 2010 Performance Award winners

Knowsley MBC tell their tale – Forthright views from ‘Viewpoint’

columnist John Frost– All the recent case law reviewed

Faculty board update 13With county court changes and the effect of benefit reform, there’s still plenty of action in the Local Taxation and Revenues Faculty Board, says Dave Chapman

Revenues roundup 14Don’t take your foot off the pedal, advises Alistair Townsend

Social inclusion 15Now’s the time to ‘hunker down’ and prepare for some tough challenges in all sectors, says Colin Holden

Valuation corner 16Richard Taylor is on hand to outline the European valuation standards project

Peter Brown presents some of the highlights from the Chancellor’s Budget that affect our members in the valuation profession

Benefits bulletin 18Dave Hendy is on the housing benefit case with some practical suggestions

Faculty review

As I write this editorial, the green shoots of spring are more obvious that the green shoots of economic recovery, and that’s all the more reason to pay attention to the words of the enforcement professionals, both private and public sector, as we approach the Institute’s June Collection and Enforcement Conference. This year’s event is as important as ever as reform continues to emerge, and in this month’s Insight we introduce a new regular contributor, JBW Group, together with a special feature on the collection initiatives employed by Denbighshire Council, winners of the prestigious 2010 IRRV ‘Innovation’ Performance Award. Your membership magazine is also always on hand to bring the latest news and views from IRRV headquarters, and this month we bring news of the forthcoming election to the IRRV’s National Council. Perhaps you’ve been involved in the work of your local Institute Association, and you have ambitions to step up to work on the national platform, and to learn about the areas of IRRV activity that have remained outside your immediate sphere of responsibility. Now is the time to consider a move in that direction, and seek election to the group that directs your professional body. Finally, a big ‘thank you’ to those of you that have responded to my request for comments on contributors’ views. Our ‘letters’ column is now a regular feature, and we will continue to print your views and observations as we strive to make Insight an even better read.

John Roberts IRRV (Hons) is Managing Editor

of IRRV magazines

“Your membership magazine is always on hand to bring the latest news and views from IRRV headquarters.”

INsI

GH

t M

AY 2

011

3

Prices Reduced for 2011

www.irrv.org.uk

IRRV Collection and Enforcement Conference and Exhibition 2011 Majestic Hotel, Harrogate, 07 – 08 June

The IRRV Collection and Enforcement conference is the ideal event for local taxation professionals, whether in the public or the private sector, to keep up to date with current issues, best practice and management techniques.

Never before has the collection and enforcement of revenues to local government been more important. This is a key event in the Institute calendar. In a changing and challenging world, officers involved in these important roles need to be at the leading edge of practice and professionalism. The program addresses all the major issues facing local government including Enforcement Reform, the Proposed Changes to Distress, Avoiding and Evading Empty Rate, the review of Local Government Finance, Case Law on the Prejudiced Ratepayer, High Court Enforcement, Welfare Reform and Enforcement and much more. The conference will again be supported by an excellent exhibition.

Collection and Enforcement is at a significant crossroads. This conference will help you negotiate the difficult times ahead and after holding prices for three years running we have been able this year to reduce prices.

You must be there to share in the expertise of the excellent speakers.

[email protected] 020 7691 8987

More information, fees and online booking www.irrv.org.uk

Sponsorship [email protected] 7691 8996

Exhibition contact [email protected]@tregartha-dinnie.co.uk01908 306 500

Programme – Day 109.45 REGISTRATION AND COFFEE

10.25 OPENING OF CONFERENCE

10.30 ENFORCEMENT IN THE RECESSION Kerry Macdermott, President, IRRV

11.15 THE LOCAL GOVERNMENT RESOURCES REVIEW Richard Harbord, CEO, Boston BC

12.00 AVOIDING THE EMPTY RATE Peter Scrafton, non-practising Solicitor

12.45 LUNCH BREAK

13.45 PREJUDICED RATEPAYER – A CRITIQUE OF THE NORTH SOMERSET CASE

David Magor OBE, CEO, IRRV

14.30 RECENT DEVELOPMENTS IN INSOLVENCY Phil Chadwick, Director, KPMG LLP

15.15 ARE YOU THERE? EFFECTIVE COMMUNICATION BY TELEPHONE James Morgan, Consultant, Action on Arrears

16.00 REFRESHMENT BREAK

16.30 EXCELLENCE IN REVENUE COLLECTION Ian Ferguson, Revenues & Benefits Manager, Durham CC

17.15 COMMITTAL – IS IT STILL A VIABLE OPTION? Dave Chapman, Customer Services Director, Rossendales

Day 209.00 REGISTRATION AND COFFEE

09.30 ENFORCEMENT – A NEW WORLD Alyn Lewis, Jacobs

10.15 ENFORCEMENT REFORM Colin Naylor, Managing Director, Dukes

11.00 REFRESHMENT BREAK

11.30 TAKING CONTROL OF GOODS – A VIEW FROM ALL SIDES Led by David Magor OBE, CEO, IRRV Alan Murdie, Lawyer, Zaccaheus 2000 Trust Paul Sharpe, Equita

13.00 LUNCH BREAK

14.00 FEES AND CHARGES IN ENFORCEMENT Andy Cummins, Business Development Director,

Phoenix Commercial

14.45 HOW TO MANAGE YOUR BAILIFF David Martin, Local Taxation & Revenues Faculty Board

Member, IRRV

15.30 THE UNIVERSAL CREDIT AND ENFORCEMENT Bob Trahern, Assistant Chief Executive

(Community Engagement), North Warwickshire BC

16.45 END OF CONFERENCE

The two latest examples of ‘policy on the hoof’ are the

localised council tax rebate scheme and the localisation of business rates. These are two perfect examples of totally

unrehearsed policy announcements without a shred of thought

for the implications of the statements.

The localisation of council tax rebate needs to be carefully

thought through. There needs to be a common thread

through English local authorities and the three devolved

administrations, and there also needs to be continuity with the

existing council tax benefit scheme. To base the new localised

scheme on anything other than needs and resources would be

of the utmost folly. The existing scheme is a significant factor

in the relief of poverty – to suddenly plunge the neediest in

our communities into debt would be irresponsible. The new

scheme must follow five basic rules. It must be based on:

a measurement of needs and resources similar to that of the •

Universal Credit

administration and rebate cost which is significantly funded by •

subsidy from central government

sufficiently progressive arrangements for incentivising the •

return to work

data that is only collected once•

an application process which should primarily utilise electronic •

channels whilst recognising the need of the customer.

Hastily concocted plansto localise council tax rebates and business rates arefundamentally flawed, says David Magor, and must be readdressed before it’s too late

The localisation of business rates is an enormous challenge.

The key issue is “what exactly does localism really mean?”

This statement leads to five questions that can only be

answered by the government – they need to be answered

before the scheme is developed. The questions are:

does it give the local authority freedom to fix a local levy?•

will central government reserve the right to include •

supplements in the levy?

will there be an equalisation scheme, and if so, •

how will it work?

will there be local discretion in the awarding of reliefs and •

in the creation of transition schemes?

how will the cost and losses on collection be met?•

Consultation on these first two elements of localism is

underway. The professional bodies must respond with

constructive suggestions that will enhance the resources

available to local government whilst recognising the needs

of the ratepayer.

Chief Executive’s notes

INSIGHT

MAY

201

1

5David Magor OBE IRRV (Hons) is Institute Chief Executive

“To base the new localised scheme on anything other than needs and resources would be of the utmost folly.”

The ‘press release’ and ‘briefing’ approach to policy delivery continues to be the style of the coalition government. Every day a new ill thought out idea appears, which seems to have emanated from the coffee shops and bars of Westminster rather than properly researched advice from the civil service.

6

INSIGHT

ww

w.ir

rv.n

et

News and events

IRRV meets RSA!IRRV Council member Graham Ryall has been elected as President of the

Rating Surveyors’ Association (RSA) at the Annual Members Dinner at

the Oriental Club, London. Insight sends its congratulations, and wishes

Graham a successful period of office. Graham is pictured with outgoing RSA

President John Elcox (photo by Richard Guy).

LATEST NEWSScottish Association The IRRV Scottish Association held its Annual General Meeting at the Municipal Chambers, Falkirk, in February, with over 85 people attending. Jim McCafferty of West Lothian Council was elected the new President of the Scottish Association, succeeding Brian Jeffrey.A presentation was also made to successful students in the recent IRRV Examinations.

IRRV Council Member and Education

Liaison Officer for the Northern Counties

Association, followed with a presentation on

the importance of professional qualifications

and the portability of what’s on offer from the

IRRV. Julian Mead, National Manager for Self

Service in Revenues and Benefits with Inform

Communications then gave an overview of self

service and its benefits, in terms of return on

investment and efficiencies.

The event included three presentations.

First, Jim McCafferty, incoming IRRV Scottish

Association President, gave members a

preview of the Institute’s Committee of

Inquiry into local taxation in Scotland,

with proposals for improving local taxation

buoyancy and yield and proposals relative

to benefits, discounts and exemptions. The

inquiry recommendations will represent a

major influence on the debate on the future

of council tax and alternatives. Ian Ferguson,

NEWS of MEMbERS

And more congratulations...

...go to IRRV Immediate Past President Geoff Fisher, who is

pictured with Strettons colleagues celebrating his 65th birthday.

Belated good wishes, Geoff!

Jim McCafferty with successful IRRV students

The IRRV Scottish Association Executive (missing are Hillary

Kelly, Lesley Henderson, Paul Ferguson and Billy Phillips)

IRRV makes its views known In two key recent submissions, the IRRV has first set out its position of

support for the principles behind ‘Dynamic Benefits’ and the introduction of

the Universal Credit, but is very clear that it cannot support the inclusion of

housing costs in Lord Freud’s proposals.

The Institute has also announced the findings of its Scottish Association’s

Committee of Inquiry into the local taxation system in Scotland. This latest

study has been undertaken by the revenues and benefits professionals who

administer the current council tax and non-domestic rates systems.

Both documents can be viewed on the Institute’s website, www.irrv.net

Gary L Watson IRRV (Hons) is Institute

Deputy Chief Executive

1 The objectives of the Institute and its Associations are to provide a consistent level of support to members through education, training and continual professional and personal development. Associations have responsibility for electing an Executive Committee. Key postholders within each Association are:

•President/Chairman •Secretary •Treasurer •Auditor •EducationLiaisonOfficer •WebMaster. 2 Whilst Associations act as separate legal entities, a

set of ‘model’ rules was approved by the Institute’s Council in 1990. An Association is able to vary the ‘model’ rules at their Annual Meeting (or an Extraordinary General Meeting) if agreed by the majority of those members in attendance. Variations may also need to be approved by the Council of the Institute or the Chief Executive.

3 Each Association is expected to arrange an annual

programme of events. This will be a combination of professional meetings and social gatherings, often in the form of an annual dinner. The location and timing of events will be dictated by the Association executive after taking into consideration the interests of members from within their area.

4 Association Representative Meetings are held twice

ayear–April/MayandSeptember/October.Tworepresentatives from each Association are nominated to attend a meeting. The National President, Chief Executive and Deputy Chief Executive would also normallyattend,asex-officiomembers.Achairman,vice chairman and secretary would be elected at their Annual General Meeting.

5 The meetings are designed to provide an effective link between the Associations and IRRV headquarters. TheyprovideaplatformforAssociationofficerstocommunicate directly with the Institute on matters of mutual interest, and ensure a uniform approach is taken by Associations, facilitating and spreading good practice. They also provide a forum where matters of concern to Associations can be discussed, and recommendations made to the Institute.

Getting to know your InstituteIn the tenth of our series, Gary Watson continues his focus on the Institute’s Associations... or branches, as they use to be

INSIGHT

MAY

201

1

7

News and events

LETTERS TO THE

EDITO

R

Recent changes to Small Business

Rate Relief (SBRR) also appear

to have created an incentive for

landlords to evade taxation, by all of

a sudden ‘becoming’ occupiers of

their properties, who diligently advise

their local authority accordingly.

A fraudulent claim for SBRR then

follows, resulting in 100% rate

relief. Do local authorities have the

resources to fully investigate?

The ‘liquidation line’ is clear

evasion, however, and if I may say

quite a clever one. It highlights

an incompatibility between the

Insolvency Act 1986 and the Local

Government Finance Act 1988 and

its ensuing regulations. I would

suggest that only primary legislation

will effectively solve this little

problem – and that will take time.

In the second letter it is interesting

to note that Mr Scrafton refers to

the ‘prerogative of the legislature to

make the law’. I quite agree, but the

problem, as often happens, is that

legislature fails to fully appreciate

the consequences of its actions. The

closure of loopholes should be an

absolute priority.

Adrian Johnson, Senior Revenues Officer, South Kesteven District Council

Dear editor,I read with interest the article ‘Is there anybody there? ’ in the

January/February edition of Insight

that was written by Alistair Townsend

and the letters it provoked in the

April edition.

Both respondents appear, with

all due respect to them, to have

overlooked the second paragraph of

the article where Mr Townsend states

that he is not intending to get into a

debate as to what constitutes evasion

and what constitutes avoidance, and

that he is simply pointing out what is

happening, giving practitioners food

for thought as to how these issues

might be approached. It is unfortunate

that both writers seemed to make

inferences regarding Mr Townsend’s

personal views that I have to say are

not apparent to me from the

original article.

I, like Mr Townsend, come at

this issue from a local authority

perspective. I have no problem with

ratepayers (landlords or otherwise)

who stay within the law in order

to avoid taxation. However, is it

reasonable to expect local authorities

to somehow absorb the administrative

burden of inspecting the (alleged)

newly occupied properties, charities

or otherwise, in addition to the

unoccupied (or partly unoccupied)

properties it has traditionally

inspected? Where is the incentive?

After all, local authorities are expected

to undertake the work with no direct

gain, given that rates collected are

paid over to central government. If the

‘six week rule’ of occupation were

to be extended, then perhaps there

would be less of an incentive to avoid

taxation, leading to a greater return for

the Chancellor in these difficult times.

Dear editor,I found your March Insight NNDR calculator to be extremely useful.

However am I correct in thinking that

the SBRR percentage relief decrease

should currently be 1% per £60

Editor’s note – yes you are, Mark!

Apologies from the author and editorial

team, and good spotting!

of RV, then 1% per £120 of RV from

1st October 2011?

Mark Pickup Tech IRRV, Revenues Officer (Valuation), Erewash Borough Council

8

INSIGHT

ww

w.ir

rv.n

et

Running the Institute

the IRRV. Finally you can also update your

Continuing Professional Development (CPD)

by this. Please do give it a go, and let us know

if there is anything that we can do to improve

this online resource for members.

We are fast approaching the IRRV examinations again, and the website is used

to keep both tutors and students updated.

Exam and syllabus announcements are given

at http://www.irrv.net/education/item.asp?Iid=1187&WAI=6 with previous exam

papers and comments given at http://www.irrv.net/education/examinationpapers.asp. The education home page is at

http://www.irrv.net/education/page.asp?Wad=8 and keeps you updated on the

current syllabus for both examinations and the

NVQs. This page has a link to details of pass

lists for IRRV exams back to June 2006, and

also features the exam timetable for

June 2011.

Another important part of the Institute’s

activities remains its conferences, giving

members an opportunity to learn and network

with their peers. The website gives details

of the conference and event programmes,

and also has photographs, for example

from the recent IRRV Benefits Conference

held in Southport. Full details of the IRRV conferences are given at http://www.irrv.net/conferences/.

If you would like to find a member who

perhaps you have lost contact with, you can

do so at http://www.irrv.net/membership/list/index.asp provided that

the other member has not opted out of this

search facility. This can be done by logging

into the members’ secure access area.

Also, local Associations use the website to

keep members informed of local meetings

and social events. Keep logging in, and where

requested please inform your local Association

of your email address so that they can keep

you regularly updated.

Responses by the Institute to consultation

IRRV websiteupdate

The IRRV’s website continues to be a key

medium in keeping members up to date with

news about the Institute. First of all, many of

you will have noted from the website that the

Institute has moved its headquarters on the

21 March 2011 from Doughty Street to new

offices in High Holborn. This is also the time

to think about Annual Conference and

particularly the IRRV Performance Awards.

Details of the 2011 Performance Scheme

including the closing date for applications is

given at http://www.jsdesigner.co.uk/IRRV/index.html. Good luck to all that apply!

There is a member website for you

to access. Your user name is your IRRV

registration number, and if you forget

your password there is a facility to remind

you. Once you are logged in you can view

magazines including Insight going right back

to 2001. You can also opt to receive future

magazines electronically rather than in hard

copy through the post once you are logged in.

Members can also ask technical questions and

pay their subscriptions via this facility. Contact

detail changes, etc can be also notified to

It’s all there on the IRRV’s website, says Kevin Stewart!

Kevin Stewart IRRV (Hons) MAAT MCMI

is Chair of the IRRV’s Education and

Membership Committee and Lead Council

Member for Communications, which includes

the website, publications and magazines

papers are mainly pulled together by the

Faculty Boards. The boards are made up of

leading practitioners in their field, including

Council members, and they have helped the

Institute punch above its weight on many

occasions. Click on the Faculty of your choice

– Revenues, Benefits or Valuation – on the

website home page. Keep logging on, as the

Institute will publish many of its responses

to proposed changes in legislation on

these pages.

In case you need to contact Institute staff, you may want to add this link to your internet

favourites. It is http://www.irrv.net/staff/index.asp and provides contact details of all

staff at the IRRV Headquarters, including

email addresses.

As an Institute we like to get things right

first time every time. However on the odd

occasion we may not satisfy you completely,

the Institute does have a Complaints and Grievance Procedure at http://www.irrv.net/complaints/ just in case you feel that

you have an issue. The IRRV s Deputy Chief

Executive Gary Watson will then consider it

and respond accordingly.

As you can see, the Institute continues to

use its website to inform members and other

stakeholders. I get a weekly schedule of the

hits to our website, and the Arctic is now

the only continent where we have not yet

persuaded someone to check our website!

At this year’s Annual Conference, we will be

using the website to bring the first news of

the IRRV Performance Awards winners once

they are announced on stage. This has proved

extremely successful in previous years, given

the number of hits.

It continues to be important to me that

we get feedback from you to improve the

website. Please do let me know if you have

any comments or suggestions, as we are

continually looking to see if the website can

be improved. You can email me at

INSIGHT

MAY

201

1

9

Annual Conference review

The IRRVANNUALCONFERENCE

201121-23 September 2011Telford International Centre (TIC), Telford

For further details and booking information, go to www.irrv.net

It will be an extremely challenging year for everyone working within the profession. This year’s Annual Conference will be an opportunity for practitioners and exhibitors to gather together and discuss the major issues. A key message received by the Institute is that whilst delegates are keen to support the event, they are looking not only for the venue to be easily accessible (minimising the time out of the office) but also for it to demonstrate real ‘value for money’. Telford is at the heart of the national motorway network, situated just off the M54 motorway and linking directly to the M6. There is on-site parking (free to all delegates) at the venue for up to 1,250 cars with the vast majority of hotels in the area having their own private car parks. It is also easily accessible both by air and rail – the railway station being very close to the conference centre, hotels and shopping centre. The conference will this year open on Wednesday morning and finish Friday lunchtime, and on the Thursday evening the Institute will be holding the Performance Awards Gala Dinner at the Centre.

Attention all Professional Diplomastudents! Bill Lovell is on hand with some timely advice and an analysis of the first examination paper in the new IRRV qualification

IRRV Honorary Member Bill Lovell is a former examiner and

member of the Institute’s Examinations and Assessment Board.

He is a freelance local government consultant and trainer.

“Swift has yielded consistently high collection rates since 1996” Paul Russell, Revenues Manager, Vale of Glamorgan Council.

“A great bunch of guys and excellent service.” Paula Allum, Council Tax Recovery Offi cer, Stevenage Borough Council.

Call Huw Lloyd-Lewis today on: 0844 546 6910 or email your enquiry to: [email protected]

www.swiftcredit.co.uk

Paula Allum, Council Tax Recovery Offi cer,

today on:

or email your enquiry to: [email protected]

www.swiftcredit.co.uk

COUNCIL TAX ARREARS?

ENFORCEMENT AT ITS BEST.

10

INSIGHT

ww

w.ir

rv.n

et

That is a comprehensive spread across the subject, but it’s also

enlightening to note that among the topics not covered are:

valuation appeals•

completion notices•

exemptions•

discount discretion on second homes/ empty properties•

information gathering powers•

liability of owners, caravans/boats and joint liability•

disabled person reductions•

billing issues, including demand notices•

instalments, including the reminder process•

payment incentive schemes•

non-valuation appeals•

penalties•

distress and committal•

the council tax base, setting the council tax, and the Collection Fund.•

All of that leaves the examiner a lot of scope for future papers, even before

topics are repeated, which inevitably some will be more than others.

Moving into Section B of the Paper, the NDR topics covered in the five

questions were:

the four ingredients of rateable occupation•

Business Improvement Districts (BIDs)•

completion notices•

empty property rating, and •

transitional adjustments. •

These are five diverse areas of the syllabus, but all are central to the

subject. It can also be seen that some topics not covered under one part

of the paper may be included in the other, for example completion notices

not included for council tax are included for NDR.

The paper still leaves the examiner with a lot of scope to set future

questions on other aspects of NDR not covered last December,

for example:

• valuationforrating

• exemptionsfromNDR

• theRatingListandappeals

• theCentralRatingList

• interestonrefunds

• nationalratespooling

• reliefs–mandatory,discretionary,hardshipands.44A

• smallbusinessrelief

• ruralsettlementreliefs

• billing,collectionandinstalments

• summonsandliabilityorder

• enforcementunderaliabilityorder,distress,insolvencyandcommittal.

We shall soon see how many of these issues have been included in

the June examination, but for the student, the message that comes

across is that this subject provides a very practical test of knowledge

and understanding, which can only help to do the day job, and to help

Diplomaholderstodirectothers–whichintheendiswhattheDiploma

qualification is all about.

December 2010 saw the first examinations for the IRRV’s new Professional Diploma. As a result, potential students have now got access to a past

examination paper that can help them prepare to boost their careers by

taking this qualification. To analyse the whole Diploma assessment process

would need a small text book, so within the confines of this page we will

limit ourselves to look at one aspect of the December 2010 examinations, to

see what lessons can be drawn. The chosen aspect is the Revenues Option,

focusing on one subject for the England and Wales candidates, The Law of Council Tax and Non-Domestic Rating (LCTNDR). It was a challenging

but fair paper, so let’s see what it was all about.

TheLCTNDRexampaperhastwoparts–PartAonthelawofcounciltax

lawandPartBonthelawofnon-domesticratinglaw–withthreequestions

out of five to be attempted on each part, so altogether the exam is six

questions out of ten, with three hours allowed. As two of the five questions in

each Part of the paper do not need to be answered, this makes a fair means

of assessment as well as a thorough one.

In the council tax section of the December 2010 paper, the five questions

covered five topics. It may not always be the case that the number of topics

equals the number of questions, as sometimes a question may be multi-part

and cover more than one topic, but on this occasion the five topics were:

valuation for council tax•

Magistrates’ court proceedings for a liability order•

discount administration and two example disregards•

sole or main residence, and •

enforcement sanctions authorised by a liability order.•

INSIGHT

MAy

201

1

11

New members

N/SVQ successes (cont/d) Name emPLoyeR QuaLifiCaTioN

Neil Parfitt Rhonnda Cynon Taff CC Housing and Council Tax BenefitsPaulIveson HarrowLB HousingandCouncilTaxBenefitsStuart Alba Tech IRRV Swansea CC Housing and Council Tax BenefitsSteven Hyatt Restormel DC Housing and Council Tax BenefitsClaire Hewitt Stockport MBC Housing and Council Tax BenefitsKatie Mill Bath & NE Somerset UA Housing and Council Tax BenefitsKaren Robinson Castle Point DC Housing and Council Tax BenefitsLisaLafferty MedwayUA HousingandCouncilTaxBenefitsMarie Booker Medway UA Housing and Council Tax BenefitsUrsula Cain Crewe & Nantwich BC Housing and Council Tax BenefitsJane Wilkinson Darlington BC Housing and Council Tax BenefitsKatrina Fitton (Not available) Housing and Council Tax BenefitsYvonneCarter CamdenLB LocalTaxationDorotaChutkowska HarrowLB LocalTaxationAlastairRabess HarrowLB LocalTaxationAndrewTaylor FlintshireCC LocalTaxationCarwynJones FlintshireCC LocalTaxationJasonDavies SwanseaCC LocalTaxationJefferyWilliams SwanseaCC LocalTaxationMauricioGarcia IslingtonLB LocalTaxationMichelleGethings StockportMBC LocalTaxationRichardMallonTechIRRV FlintshireCC LocalTaxationAngelaChandler ShepwayDC LocalTaxationJulietYeboah HarrowLB LocalTaxationMargaretRoberts SwanseaCC LocalTaxationRebeccaDean FlintshireCC LocalTaxationUshmaElder HarrowLB LocalTaxationClaireMorton AmberValleyDC LocalTaxationGoldaTetteh WalthamForestLB LocalTaxationRachelPain ShepwayDC LocalTaxationAllanRamsay EdinburghCC LocalTaxationPhilipMcAusland EdinburghCC LocalTaxationAllisonLeitch EastAyrshireC LocalTaxationElaineMcConnell EastAyrshireC LocalTaxationGeorginaHalliday EdinburghCC LocalTaxationMichelleFarrow EastAyrshireC LocalTaxationJoanneHognet EastAyrshireC LocalTaxationJeanetteRogers EdinburghCC LocalTaxationLauraGibson EastAyrshireC LocalTaxationDavid Knox Edinburgh CC Housing and Council Tax BenefitsLisaBuchanan EdinburghCC HousingandCouncilTaxBenefitsCheryl Montgomery Glasgow CC Housing and Council Tax Benefits

Student members Name emPLoyeR

Sharon Bevins Melton Borough CouncilAlison Wilson Melton Borough CouncilAlastairMacdonald IslingtonLondonBoroughCouncilJulie Borthwick North Tyneside Council Julie Dowson Durham County CouncilFay Endean North Tyneside CouncilGemmaMcLellan NorthumberlandCountyCouncilNeil Renform North Tyneside CouncilJamie Ruddell Durham County CouncilKirsty Bohun Sedgemoor District CouncilRyan Roberts Sedgemoor District CouncilSamantha Schrieber Wycombe District Council

Technician members DeborahCastle VOA,LambethRichard Mallon Flintshire County CouncilChristine Ifill Bath & North East Somerset Council

Honours members Darrel Brown Valuation Office Agency Assessment CentreGavinLongy ValuationOfficeAgencyAssessmentCentre

Affiliate members GaryCarr EquitaLimitedDebbie Gibbons Rushmoor Borough Council

Preliminary notice is given, in accordance with paragraph 1 of Schedule

2 to the Articles of Association of the Institute, that six vacancies for

members of the Council who are Fellows, Members (Diploma Holders)

and Members (Honours) of the Institute will arise at the conclusion of the

Annual General Meeting on 21 September 2011. Nominations for election

are invited from members in these categories.

Four of the vacancies arise by the retirement in rotation of the serving

members, as listed below. One vacancy arises by rotation in the Council

seat to which Mr Roger Messenger BSc FRICS MCIArb was elected in

2008. Mr Messenger is Senior Vice-President of the Institute, and if

elected as President would be an ex officio member of the Council for the

coming year. In order to preserve an even rotation of retirements this seat

is to be filled for a full term this year. The final vacancy to be filled is in a

seat which falls vacant by rotation, but which has been filled since 2010

as a casual vacancy by Mr Graham Ryall FRICS IRRV (Hons). This casual

vacancy was caused by the resignation of Mrs Barbara Culverhouse CPFA

IRRV (Hons) in 2010.

The four Council members who are retiring in rotation are:

Carol Cutler iRRV (Hons) Tom Dixon RD BSc fRiCS iRRV (Hons) Richard Guy fRiCS Dip Rating iRRV (Hons) mCiarb Kevin Stewart iRRV (Hons) maaT mCmi

N/SVQ successes Name emPLoyeR QuaLifiCaTioN

Carrie Maskell Rugby BC Housing and Council Tax BenefitsJenny McCarthy Castle Point DC Housing and Council Tax BenefitsMaria Richards Swansea CC Housing and Council Tax BenefitsRebecca Hewitt Castle Point DC Housing and Council Tax BenefitsRebecca Warren Medway UA Housing and Council Tax BenefitsChristopher Branaghan Kettering BC Housing and Council Tax BenefitsCallum Caggiano Canterbury CC Housing and Council Tax BenefitsCharles Wilkins South Gloucestershire DC Housing and Council Tax BenefitsEvertonAdudu LambethLB HousingandCouncilTaxBenefitsJasonLee RochadaleMBC HousingandCouncilTaxBenefitsLukeCahill TunbridgeWellsBC HousingandCouncilTaxBenefitsLaishaChudasama HarrowLB HousingandCouncilTaxBenefits

The previous seats designated for Scotland and Northern Ireland will be

discontinued, in accordance with amendments to the Articles of Association

agreed in 2008, and the members currently holding those seats (Allan

Traynor FCCA IRRV (Hons) and Alan Bronte FRICS IRRV (Hons) respectively)

retire. The seat designated for Wales was discontinued in 2009.

Nominations should be received by the Director, The institute of Revenues, Rating and Valuation, 5th floor, Northumberland House, 303 – 306 High Holborn, London WC1V 7JZ, not later than 5pm on friday 8 July, 2011. Nominations may be accompanied by a photograph

of the candidate, which will be included with the voting material. Retiring

members are eligible for re-election.

Nominations by fax (020 7831 2048) are acceptable, so long as

confirmed by delivery of a hard copy within three working days of receipt

of the fax. Nominations may also be made by e-mail to [email protected]. Requests for nomination forms should be addressed to Rachel

Toombs at the Institute (020 7691 8972–e-mailaddressasabove).

If the election is contested, voting papers will be sent out to all those

eligible to vote not later than 12 August 2011.

By order of the Council

David magor oBe iRRV (Hons), Chief executive. may 2011

IRRV Council elections 2011

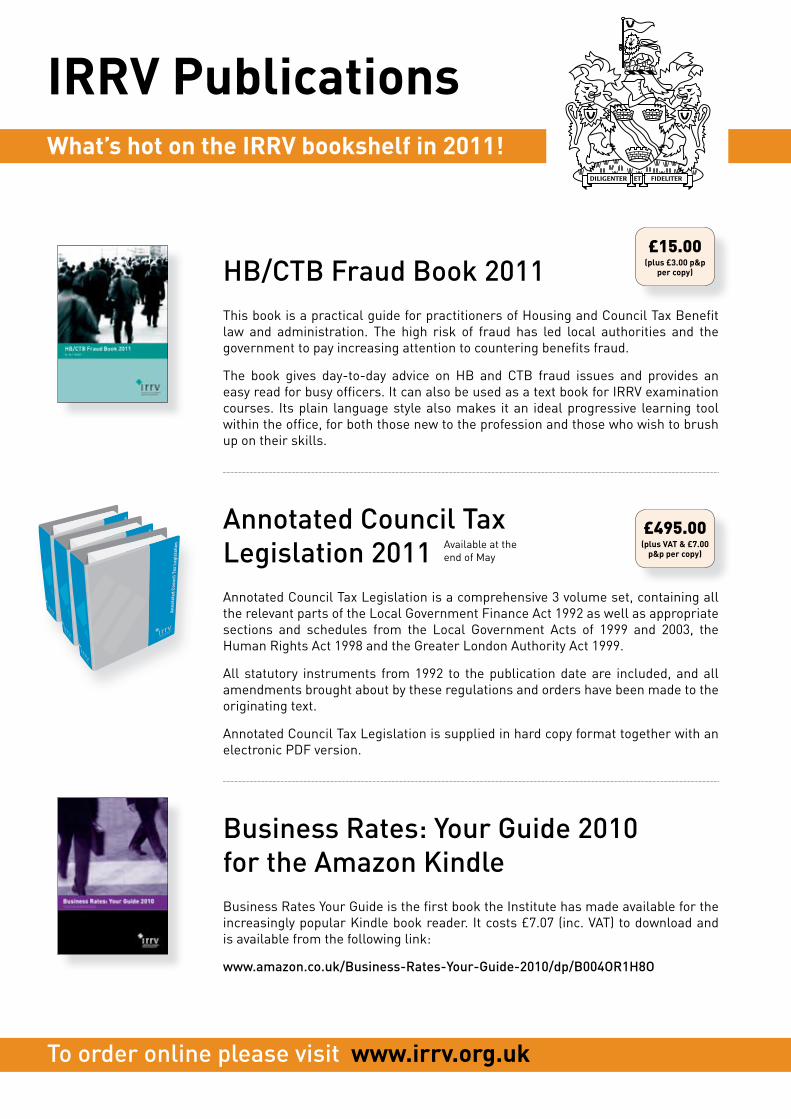

IRRV PublicationsWhat’s hot on the IRRV bookshelf in 2011!

HB/CTB Fraud Book 2011This book is a practical guide for practitioners of Housing and Council Tax Benefit law and administration. The high risk of fraud has led local authorities and the government to pay increasing attention to countering benefits fraud.

The book gives day-to-day advice on HB and CTB fraud issues and provides an easy read for busy officers. It can also be used as a text book for IRRV examination courses. Its plain language style also makes it an ideal progressive learning tool within the office, for both those new to the profession and those who wish to brush up on their skills.

Annotated Council Tax Legislation 2011Annotated Council Tax Legislation is a comprehensive 3 volume set, containing all the relevant parts of the Local Government Finance Act 1992 as well as appropriate sections and schedules from the Local Government Acts of 1999 and 2003, the Human Rights Act 1998 and the Greater London Authority Act 1999.

All statutory instruments from 1992 to the publication date are included, and all amendments brought about by these regulations and orders have been made to the originating text.

Annotated Council Tax Legislation is supplied in hard copy format together with an electronic PDF version.

Business Rates: Your Guide 2010for the Amazon KindleBusiness Rates Your Guide is the first book the Institute has made available for the increasingly popular Kindle book reader. It costs £7.07 (inc. VAT) to download and is available from the following link:

www.amazon.co.uk/Business-Rates-Your-Guide-2010/dp/B004OR1H8O

To order online please visit www.irrv.org.uk

£15.00(plus £3.00 p&p

per copy)

£495.00(plus VAT & £7.00

p&p per copy)Available at the end of May

FACULTY BOARD UPDATE

INSIGHT

MAY

201

1

13

With county court changes and the effect of benefit reform, there’s still plenty of action in the Local Taxation and Revenues Faculty Board, says Dave Chapman

Dave Chapman IRRV (Hons) is Chairman of

the Institute’s Local Taxation and Revenues

Faculty Board and IRRV Junior Vice President

for information applications, requests and

orders for information on debtors.

Further proposals concern the streamlining of

internal processes for charging orders and third

party debt orders, with the aim of making these

mechanisms more effective and administrative

(and therefore less judicial) functions, but with

the appropriate safeguards still in place. I look

forward to reporting on the Board’s response to

this paper in due course.

Those revenues officers who don’t have

routine dealings with benefits matters in their

authorities might do well to follow the current

developments on council tax benefit, or rebate,

under the forthcoming Universal Credit. No

clear picture is emerging on how support for

council tax costs will be handled, apart from

an announcement that it will be reformed and

determined locally, with a grant of 10% less

than the expenditure in 2012/13. The new

scheme is expected to start in April 2013. IRRV

is playing its full part in the current debates.

There may be advantages in opting for a

mainstream scheme with some local discretion,

in order to have at least a degree of conformity.

Awarding the amount as a discount on the

council tax bill and not as a separate benefit

is an option, as this could interact well with

council tax software and therefore negate

the need for, and cost of, a separate system.

However, discounts and exemptions would

need to be examined to ensure that the

scheme had perceived fairness in approach.

Revenues sections may have more change

ahead of them, depending on which way the

final decisions go on this matter.

No clearpicture emerging

enforcement process overall, and to consider

which enforcement mechanisms need to be

linked to a judicial process at all. In this the MoJ

seek a balance between the legitimate right

of the creditor to enforce their court judgment

by means of a wide ranging and robust

enforcement system against those who won’t

pay or seek to ignore their judgment debts, and

the need to understand the position of debtors

who genuinely cannot immediately pay.

MoJ are looking at implementation of the

enforcement related provisions of Part 4 of the

TCE Act 2007, which have been approved by

Parliament, namely:

whether to allow applications for charging •

orders on all judgment debts regardless of

whether or not the debtor is paying by, and

up to date with, instalments

introducing a minimum threshold on •

applications for orders for sale in Consumer

Credit Act debts (the Coalition Government

Commitment)

introducing fixed tables to the attachment of •

earnings process, similar to those used for

criminal fines and council tax recovery

introducing a mechanism to trace a •

debtor’s current employer in attachment

of earnings applications

introducing a new enforcement mechanism •

I begin this column with a big ‘thank you’ to all

those of you who took the time to complete

the IRRV survey issued a few months ago,

regarding the impact of changes to committal

fees in England and Wales. Respondents

supplied some very helpful data which will

make for interesting reading in the Faculty

Board’s final report. We are in the final stage of

seeking additional information on some specific

topics. Some of the data sought concerns

some perceived recent trends in remitting

debt following the fees increases, and if we

get a good return on the second short survey

it will have been worth the wait. Thanks in

advance for your help with the short follow-up

questionnaire. And of course, all of you who

have responded will receive a full copy of the

final report as soon as it is published.

At the time of writing, the Board have had

an initial brief read through the recently issued

Ministry of Justice (MoJ) consultation on

reform of the civil justice system for England

and Wales. Relating specifically to reforms in

the county court, the paper runs to 100 pages,

poses over 70 questions, and is open for

comment until 30th June. Institute members’

main (though not exclusive) interest may be

in section 4 of the paper, concerning debt

recovery and enforcement. The full title of the

paper is ‘Solving disputes in the county courts: creating a simpler, quicker and more proportionate system’ – and the

report content may live up to that title. It seems

somewhat strange to report that for once in

respect of a consultation paper of this size,

there is not much the Board takes issue with in

the proposals!

The MoJ’s stated aim is to reaffirm the

authority of judgment orders by improving the

efficiency and speed of enforcement processes.

In particular, they address wider questions

about how to improve confidence in the

“Relating specifically to reforms in the county court, the paper runs to 100 pages, poses over 70 questions, and is open for comment until 30th June.”

revenues roundup

14

Maximum in-year council tax collection must be the target, for the good of all, asserts Alistair Townsend

INSIGHT

ww

w.ir

rv.n

et

Alistair Townsend IRRV (Hons) MCMI is

Service Delivery Manager for Mouchel

Government and Business Services.

people in debt tend to pay the creditor that

shouts loudest, and you can be assured that

commercial creditors are shouting louder and

louder all the time. It is all very well delaying

reminders and summonses to give people a

bit longer to pay, but all that will happen is that

over time they will realise that the council isn’t

shouting as loud, and pay someone else – and

all our work to change attitudes to paying

council tax will be undone. I believe that the

council tax collection system has a life of about

three or four years. By this I mean that a more

robust recovery stance can take up to four

years to manifest itself in increased collection,

and conversely, a weakened recovery strategy

will slowly damage collection over the same

period. Of course, if this is correct it means

that the data revenues teams are collecting

on the effects of sending reminders late, etc.

is flawed, because it won’t affect this year –

it will slowly erode attitudes to council tax and

affect years two, three and four.

We need to ensure that we aren’t storing up

problems for the future by taking our foot off

the pedal now in a misguided attempt to help

our customers. It isn’t in their interests, and it

isn’t in ours, to extend arrangements to a point

where we create a cycle of debt.

Don’t take your foot off the pedalCouncil tax is unlike

most other types of debt.

If you suggested to a bank

that at the beginning of

each financial year it should

reissue credit cards to all of its

worst debtors, you can imagine

the response! But let’s face it,

that’s in effect what we do every

year. Not only can we not choose

the people that we allow to owe us

money, we can’t limit our exposure

when they prove to be bad payers!

This is why the responsible thing is to continue

to do everything we can to make sure council

tax is paid within the year it becomes due,

and to make arrangements that reduce

indebtedness, rather than increase it. We

need to get back to the basics of encouraging

payment methods with low failure rates, such

as direct debit, and continue to take prompt

recovery action not only to enforce payment,

but to coerce it.

I have spent the last twenty years telling

our customers that “council tax is a priority

debt, and should take precedence over

other non-essentials, etc”, yet there remain

many people who either don’t agree or don’t

care. In addition, it is a sad fact of life that

Around the country, we have just seen

the most contentious local government budget setting process in recent memory,

with spending reductions resulting in cuts

to many non-essential services. Very often,

due to the nature of services generally, each

council’s room for manoeuvre is limited, and

decisions are being made about relatively small

spends. This in turn concentrates the mind on

the importance of collecting every penny of

council tax. However, with the cost of living

rising for everyone, it is understandable that

many revenues services find themselves in a

difficult position collecting debts in this climate.

It would seem quite reasonable for councils

to be as understanding as possible in agreeing

to compromises that they wouldn’t have

considered a few years ago. I know of many

councils who are being much more flexible

with arrangements, extending instalments to

twelve (some without any legal agreement)

and many suspending recovery action such as

attachments of earnings and distress.

Many people find themselves in difficult

situations where credit card and loan

companies who were previously happy

to keep extending credit to them are now

reigning it in, and they then find themselves

more exposed than they expected. Therefore,

on the face of it, being more generous with

council tax repayments could not only seem

reasonable, but the admirable actions of a

caring council. However, over the years I have

seen that this course is the fastest route to

accruing indebtedness and a cycle of debt

that is almost impossible for many people

to break. Many local authorities have anti-poverty policies, which can actually do little

more than increase debt, and in turn increase

poverty by delaying repayments to such an

extent that they create the cycle of debt.

“the responsible thing is to continue to do everything we can to make sure council tax is paid within the year it becomes due, and to make arrangements that reduce indebtedness, rather than increase it.”

sociAl inclusion

INSIGHT

MAY

201

1

15

Now’s the time to ‘hunker down’ and prepare for some tough challenges in all sectors, says colin Holden

Colin Holden IRRV (Hons) is

General Manager of East Sussex

Credit Union. Contact him on

The next few months will also be interesting

for the ‘Big Society’. It was interesting to see

Liverpool City Council pulled out of being a

pilot as they did not get the expected grants

from the government to prop up their work.

I think people are beginning to realise that this

is still a ‘work in progress’ for the government,

and that there will not be shed loads of money

for local government in it. Also I’ve noted

with rising concern how there seems to be an

increasing number of consultants around who

are offering to help organisations prepare –

at a price. So as I said, we all need to ‘hunker down’ and watch the gathering storm.

account, and then the credit union pays the

benefit over to the landlord, with any balance

staying in the tenant’s savings account. They

then charge the landlord a fee per payment

for the service. The landlords love the scheme,

and are more than happy to pay up, as they

get their rent without a lot of chasing around,

and the tenants like it because they don’t

have to worry about paying the rent.

Unfortunately, the government issued new

guidance at Christmas that, depending on

who you talk to, seems to be interpreted in

one of two ways. The first is that there is no

fundamental change, which is fine, and the

landlord scheme will

continue as before.

However the

second

interpretation

seems to be that

after this April, councils

will be able to pay all tenants direct. The

second option is all well and good, but will

have the effect of taking the credit union out

of the equation, with potentially a huge loss of

income for them. For instance, at East Sussex Credit Union we have had to reduce our

estimated income for next year by £10,000

due to a local council intending to allow all

landlords to be paid direct. This may not seem

much on the face of it, but to a third sector

organisation this is a real body blow.

Well I wish I had a bet on what is currently

happening now to the councils and the third

sector, as it is all pretty much as I predicted in

previous articles! Individual council budgets

have been set now, and we have had the

Chancellor’s budget to boot. Most people

are finding themselves worse off, with those

that earn more losing less, as is the wont of

our current government. I guess the majority

of people reading this are probably ‘middle income’, meaning they are earning more than

the minimum wage but don’t qualify for the

higher tax bands. Well folks, in the long term it

is you guys that will be suffering most, so now

is the time to ‘hunker down’ and prepare for

the future.

One way you can do this is to save. In the

credit union sector there has been loads of

research over the last couple of years that

show that the people that survive these times

best are those who have savings, so now is

the time to start – or if you already do, then

think about saving more. If you need a loan,

interestingly most credit unions offer better

rates than banks for loans of up to £10,000,

because the high street generally find these

‘small’ loans not profitable. For instance, a

customer of ours was quoted a rate of 22%

by a high street bank for a £5,000 loan for her

wedding, whereas we were able to offer a loan

at 12%. Credit unions are not just for poor

people – they are for everyone.

The changes in the law and guidance

imposed by government on its town hall

buddies also sometimes have hidden effects

for the third sector. One such effect is the

recent guidance on housing benefit concerning

direct payment of rent to landlords.

Currently this can only be done where it is

in the claimant’s interests to do so due to an

inability to manage their finances. To help

those tenants that don’t fall within this but

have problems paying their rent, credit unions

have a scheme whereby the tenant has their

housing benefit paid into their credit union

“The changes in the law and guidance imposed by government on its town hall buddies also sometimes have hidden effects for the third sector.”

Watching the gathering storm

valuation corner

16

richard taylor is on hand to outline the European valuation standards DEFVAS project

INSIGHT

ww

w.ir

rv.n

et

Richard Taylor is the IRRV’s

European Projects Manager

The target groups of beneficiaries will be:

Professional valuer trainees, and their •

employers, who wish to offer an improved

and more transparent form of training. It is

estimated there are 100,000 valuers in 42

countries who would have an interest in

engaging with this material

Individuals across the European Union who •

have an interest in valuation, either by virtue

of the fact that they might be considering

a career in valuation, or have an interest

through working in local government

Consumers, who have an interest in ensuring •

that they are being fairly assessed for property

tax. An increase in cross border activity

means that ‘fair assessment’ has taken

on another dimension, and taxpayers need

to have confidence in the system. European

valuation standards, supported by a recognised

transnational training initiative, will go a long way

towards meeting the concerns of consumers.

Summing up, the partners have an asset, the

‘Blue Book’, which is a standards manual. This is

currently owned by and marketed by TEGoVA,

and is an innovative piece of work in its own field,

covering virtually all countries in Europe. IRRV is

leading the project to develop it into a practice

manual which can also be used as a serious

training resource. While only six countries are

involved at this stage in the project, it is expected

that this important work will continue, involving

more countries at a later stage.

With the emphasis on professional practice and

training, the partnership has the opportunity to

make a huge contribution to valuation standards

and practice internationally, through trans-European

collaboration. The impetus has been created by

the rapid expansion of the EU and the desire of

all member states to become part of a European

best practice and standards network, and the

recognition by the Commission that Europe should

have a powerful voice in this important area. The

funding granted for this project will enable these

plans and ideas to be implemented.

IRRV leadinginnovativepartnership

working in the valuation profession

3. To enhance the links and cooperation

between the different organisations in

the project

4. To increase employment opportunities

for people working in the sector,

especially transnationally

5. To make an improved training model a

reality beyond the period of European

funding and ‘intervention’

6. In the longer term, it is envisaged that the

project will result in increased mobility of

valuer professionals, so that, subject to

meeting local requirements, people working

in one member state will be able to offer

advice and services in relation to, and even

in, another member state without hindrance

7. To bring to reality and implement the idea

of a trans-European vocational qualifications

framework for European valuers.

The partners in the project are:

IRRV•

SNPI• , a French trade association which

is a leader in its field

TEGoVA• , a transnational umbrella

organisation for national valuer associations

the Polish Federation of Valuers Association •

(PFVA)

ANEVAR• , the Romanian Valuers’ Association

Registru Centras• , The Lithuanian State

Register of Property.

The lead partner (the IRRV) has a well

developed education department which offers

its own training and qualifications, accredited

by UK QCDA. This role was critical at the

application stage to providing the necessary

credibility in the area of training, and it

has developed innovative methods for the

delivery of training and qualifications, and this

expertise will be used to provide advice on

and support for practical implementation of

qualifications development and accreditation

at a European level.

An EU-funded project is well under way, with

IRRV as the lead partner. The project has been

granted funding under the Leonardo da Vinci, ‘Transfer of Innovation’ programme, for a

period of 24 months commencing October 1st

2009, and involves partners from six countries.

This innovative project is aimed at supporting

European Valuation Standards and

encouraging best practice in valuation. A

publication has already been produced which

details valuation standards (known in the industry

as the ‘Blue Book’). However, the partners wish

to transfer this material and adapt it for use as

training material in the different partner member

states – the output will be a series of modules

which will be a logical extension of ‘the Book’.

This is being achieved by expanding sections,

updating others, and, crucially, introducing local

practice manuals and case studies as a series of

papers, available online and in hard copy, which

will enable the book to be used both in a training

context and as a guide for professional practice

in the industry.

The ‘Blue Book’ was compiled by members

of The European Group of Valuers’ Associations (TEGoVA). It was a lengthy

task, but is a first rate example of European

cooperation and collaboration. However, this

work highlighted the need to extend it to

include professional practice, qualifications

and training, which would be incorporated in a

logical and worthwhile extension of the book.

This need is particularly evident, as there is a

requirement for much greater sophistication in

valuation practice and training incorporating a

transnational dimension to meet the needs of

an increased level of cross border work.

The specific objectives of the project are:

1. To improve professional standards within

the sector

2. To improve general skills levels of all people

17

Peter Brown is on hand to present some of the highlights from the Chancellor’s Budget that affect our members in the valuation profession

Peter Brown is former Professor of Property Taxation at Liverpool John Moores

University and Consultant to Legal Owen, Chartered Surveyors, Chester

1 CAPITAL GAINS TAX

The ‘entrepreneur’s relief’ has been increased from

£5 million to £10 million.

The annual exempt amount changes to £10,600 for the

current tax year.

1.1 TAX RATES

The government highlighted the importance of corporation tax internationally and recognised that the UK level of tax was

making it uncompetitive in this respect. As a result, reductions

in the rates have been proposed which will restore the UK’s

competitive advantage. Further reductions to the rate will be

made in subsequent years.

4 LANDFILL TAXThe standard rate of landfill tax will increase £8 per tonne to

£56 per tonne with effect from 1st April 2011, and to £64 per

tonne from 1st April 2012.

5.1 SMALL BUSINESS RELIEF

Small business rate relief will continue to be available for

a further period of twelve months. Ratepayers with a rateable

value of £6,000 or less with effect from 1st April 2010

will be entitled to 100% relief from rates. Ratepayers with

assessments between £6,000 and £12,000 will be entitled

to tapered relief.

5.2 ENTERPRISE ZONESThe government has announced the creation of 21 enterprise zones which will offer up to 100% relief from rates for five

years, as well as other benefits including a simplified

planning framework.

5 BUSINESS RATES

2 STAMP DUTY LAND TAX (SDLT) 1

3 CORPORATION TAX

valuation corner

INSIGHT

MAY

201

1

POST 22/6/10

2011-12

Standard rate 18%, 28% 18%, 28%

Entrepreneurs’ relief effective rate

10% 10%

Annual Exempt Amount £10,100 £10,600

Entrepreneurs’ relief lifetime limit of gains

£5,000,000 £10,000,000

BUSINESS RATESRATE PER POUND OF A BUSINESS PROPERTY’S RATEABLE vALUE

2010-11 2011-12

Standard multiplier 41.4p 43.3p

Small business multiplier 40.7p 42.6p

2011-2012 2012-2013

£300,000 20% To be confirmed

£300,001 - £1,500,000 Marginal rate Marginal rate

£1,500,001 or more 26% 25%

RESIDENTIAL NON-RESIDENTIAL

2010-11 2011-12 2010-11 2011-12

TOTAL vALUE OF CONSIDERATION

0%£0 - £125,000

£0 - £125,000

£0 - £150,000

£0 - £150,000

1%£125,000 - £250,000

£125,000 - £250,000

£150,000 - £250,000

£150,000 - £250,000

3%£250,000 - £500,000

£250,000 - £500,000

£250,000 - £500,000

£250,000 - £500,000

4% >£500,000£500,000 - £1,000,000

>£500,000 >£500,000

5% >£1,000,000

Peter Brown adds:

The Budget announced a wide scale review of the planning system which

should focus and support economic growth and sustainability. The review will

remove central targets and encourage councils to bring forward proposals for

residential development. The initial proposals include:

a presumption in favour of sustainable development with a presumption of •

a grant of permission rather than a refusal, but with continued protection of the

green belt and areas of outstanding natural beauty (Consultation by

May 2011)

to simplify the bureaucracy for the planning process with is preventing growth. •

It proposes to clarify the system with the publication of a single National Planning policy Framework (publication by end of 2011)

Changes to the • Use Classes Order to remove the need for planning

permission, for example for change of use of commercial premises to residential

Local authorities should positively encourage growth in their local decisions to •

update development plans which should identify opportunities for growth and to

review s.106 agreements where developments have stalled due to their costs

The government will release and auction surplus public sector land with •

planning permission already granted

Give businesses the right to initiate • Neighbourhood Development OrdersRemove arbitrary central government targets•

Remove bureaucracy from the planning process•

Councils should co-operate with each other on cross boundary planning issues•

The fast tracking of major infrastructure applications.•

1 First time buyers can claim relief from SDLT on residential transactions up to £250,000 between 25 March 2010 and 25 March 2012

Benefits Bulletin

18

Soifhousing benefitis going,how dowekeep upthemomentum?Dave Hendyisonthecasewithsomepracticalsuggestions

INSIGHT

ww

w.ir

rv.n

et

Benefits Bulletin is produced by

Dave Hendy IRRV (Hons)

will there be? What about administration cost

subsidy – when and how will these changes

impact its value? Clearly councils will need

to know the answers to at least these basic

questions to plan resources sensibly into

2012/2013 and beyond.

Then there is the question of maintaining

that pool of expertise on existing cases, all the

way through to the potential full handover date.

A number of factors can help here:

Most HB staff are conversant with council tax •

because of their work on CTB and second

adult rebates. Rather than wasting these skills,

looking at generic working arrangements,

even on council tax and CTB only cases, will

not only improve customer service, but will

mean that as HB roles diminish some staff

can be reassigned to revenues roles

As some HB staff will perhaps not look to •

return to the workforce after leaving to start

families, their expertise can be maintained

and nurtured by offering contracts on much

more flexible hours and homeworking

Better informal partnership working •

arrangements between councils, sharing

the use of their expert resources. You don’t

have to fully join up to an expensive and

complicated legal partnership arrangement to

still benefit from some straightforward skills

sharing exercises.

My final thoughts on this problem are much

more straight-forward and carry no additional

costs whatsoever – just keep staff informed

of your plans and ideas, and what any likely

impacts are going to be. Fear of the unknown

is what is keeping most benefit officers awake

through the night at the moment. An honest

reflection of the truth may be much more

digestible and provide the degree of certainty

that so many of them crave and deserve.

And as many of the best ideas for future

plans come from within the organisation,

the answers we are seeking could well be

out there!

to be handled after this April’s series, councils

will need to ‘backfill’ staff vacancies to avoid

backlog problems. But with keen eyes on their

budgets, and the reality of HB going from 2013

onwards, maybe short term fixed contracts will

be all that will be on offer. More likely still we

will see the demand for temporary agency staff

take a steep rise upwards again. And we know

what that means as assessor hungry benefit

managers scour the CVs from the agencies for

good claim processors – the price, in hourly

rate terms starts to rocket. But even if budgets

are running on empty, what other options

will there truly be to avoid the dreaded

‘B-word’ – backlogs!

So thinking ahead, what other options are

available to avoid the backlog crisis? Well,

a good start would be some better forward

planning by our masters at the DWP. What

we need to know now is the reality for 2013

and the run up to 2017. What is really going

to happen? What cases, such as exempt

accommodation and any other specialist

claims, will definitely be left with councils.

Will councils definitely get community care

grant work – and what caseloads/level of

administration will come with these awards?

Then what’s really going to happen with council

tax benefit (CTB)? Will it be part of Universal

Credit or not, and what if any rule changes

As soon as the word came out that housing

benefit (HB) was transferring to Universal Credit, most benefit offices were buzzing with

thoughts like:

What’s going to happen to our jobs?•

Could we get a job in the DWP?•

Will we be able to pay our bills and maintain •

our current living standards?

Whilst these questions may well have also

tracked across many benefit managers’ minds,

their subsequent thoughts will have turned to

questions like, “How on earth will we keep up

the momentum on existing cases, as staff are

going to be so worried about their futures? ”

This is a difficult situation, and there are

many imponderables in the mix. First, how

likely is it that Universal Credit, with its

housing costs element, will actually be ready

for service delivery by 2013? This major new

benefit will require software to be produced,

staff to be recruited and trained, forms and

new procedures developed. Add to this the

somewhat unimpressive record of government

departments in delivering major new IT

projects on time and on budget, and the

problems are clear.

Second, simply knowing that their jobs

are at risk for the future will mean that many

staff will be now checking job websites every

single day looking for possible opportunities

elsewhere. Hence an inevitable haemorrhaging

of some very good quality staff (as it ’s always

the ones we most miss who get the new jobs

first!) to work in other fields. On the positive

side for employers however is the shape of the

current job market – with so many councils

downsizing, there is little good news out there

in the form of actual vacancies.

Third, as a direct knock-on effect of the

loss of good staff and the need to keep work

output levels up, with so many changes still

“simply knowing that their jobs are at risk for the future will mean that many staff will be now checking job websites every single day looking for possible opportunities elsewhere.”

It’s the fear of the unknown

20

INSIGHT

ww

w.ir

rv.n

et

Five core modules were identified for the

development of the service:

New initiatives•

New business•

Customer focus•

Training and recruitment•

Best practice.•

The new initiatives which contributed

to winning the IRRV’s Innovation Award

included the introduction of a streamlined

automated invoicing service which reduced

errors and time, satisfied audit procedures

and reduced paper usage by an astonishing

66%. Development cost was insignificant but

savings in excess of £30,000 were identified.

In addition, the authority introduced an

income reversal procedure on the ledger

which meant budget loss against unpaid

invoices after 65 days and crucially, the

decision was taken in 2005 to create an

in-house bailiff/collection agent team.

As part of their ‘armoury’, Denbighshire

created a refreshed customer service

programme which involved:

A customer charter•

A focused customer case service•

Strong relationships with voluntary bodies.•

Training the team, which was recruited

primarily from the credit industry, ensured

that the right people developed the right

skills; in particular the ability to collect

sundry debt using the telephone call as

the mainstay method.

Ken takes up the story again.

“We developed a tailored training

Want to collect £27 million in sundry debt? Then pick up the telephone

Cover story

Lester Dinnie tracks down the winners of last year’s IRRV Innovation Award, Denbighshire Council, and finds out how they did it and what advice they have for others

Ken Jones, Head of Revenues and

Benefits at Denbighshire County Council says his award winning authority favours the

personal approach to collecting sundry debt and lays down a blueprint for success.

In 2010, Denbighshire County Council

Revenues and Benefits Team won the IRRV’s

Performance Award for Innovation, with an

approach to the collection of sundry debt that

established a new performance benchmark.

Formed as one of Wales’ new unitary

authorities in April 1996, the area has a mixed

economy that is heavily reliant on tourism

and agriculture, but also has high levels of

deprivation with five of the most socially

deprived wards in the country.

Even with a recent history of outstanding

achievement (Denbighshire was the first

Revenues Department in Wales to achieve

Charter Mark status in 2006 and was awarded

Customer Service Excellence status in 2010),

when the authority turned its attention to the

‘Cinderella of revenues, sundry debt’ it was

aware of the challenges it faced.

“Sundry debt is just not well understood

by many people in local authorities,” says

Ken Jones, “It covers arrears on virtually any

chargeable council service which is supplied

to the local population, from removing a

wasp’s nest from your premises to supplying

major special needs provisions. So right at

the outset our priority was to raise the profile

of sundry debt within our own authority. With

£27 million in revenue at stake, it was clearly