Innovations in HUD Property Preservation in HUD... · Innovations in HUD Property Preservation ......

31

5/4/2017 1 Innovations in HUD Property Preservation Presented by Gates Dunaway, Donald Manning and Shannon Lestan LeadingAge New York Annual Meeting May 23, 2017 What is Preservation? The long-term physical and financial sustainability of HUD-assisted affordable multifamily rental housing. Preservation may include: Recapitalizing the property Securing long-term rental assistance Improving and modernizing properties The Importance of Preservation Mission Protection for the residents Scarcity of new funding Possibility of increased revenue to Non-profit Public Policy marketing

Transcript of Innovations in HUD Property Preservation in HUD... · Innovations in HUD Property Preservation ......

5/4/2017

1

Innovations in HUD Property PreservationPresented by Gates Dunaway, Donald Manning and Shannon Lestan

LeadingAge New York Annual Meeting

May 23, 2017

What is Preservation?

The long-term physical and financial sustainability of HUD-assisted affordable multifamily rental housing.

Preservation may include:

Recapitalizing the property

Securing long-term rental assistance

Improving and modernizing properties

The Importance of Preservation

Mission

Protection for the residents

Scarcity of new funding

Possibility of increased revenue to Non-profit

Public Policy marketing

5/4/2017

2

Preservation Process Steps

4

HUD Insured 236 State uninsured 236 Loans

HUD 202 Direct Loan Section 8

RAP

Rental Supplement Contract

Flexible Subsidy Loan

Low Income Housing Tax Credits LIHPRHA or Title VI

Look familiar? Built in the 1970’s, early 1980’s, financed with HUD 202 or 236 loan, Section 8 contract, and built to last.

5/4/2017

3

Look familiar? Outdated fixtures and cabinets

Today we will help you understand the specific issues with your HUD-financed affordable senior properties, and we’ll help you understand your options and the paths for preserving and improving your property.

Our emphasis is on finding the

simplest path to your goals.

Your property is nearing 40 years old and loan maturity….

Pressures AGAINST Preservation

Repeated offers to purchase

Capital needs – too hard to keep up with it all

Board fatigue

Unsure of the best path forward

5/4/2017

4

How to move forward to Preservation

Repeated offers to purchase – Don’t sell until you are ready!

Capital needs – Recapitalize

Board fatigue – Board training and re-energize

Unsure of the best path forward – Education, training and consultation

Know your Property (and the Programs)

11

UNDERSTAND THE HUD PROGRAMS

5/4/2017

5

Section 8

Section 8 Contracts

➢Do you have old reg or new reg contract?▪ Old reg = NO RESIDUAL RECEIPTS REQUIREMENTS;

at expiration of regulatory agreements, owner keeps surplus cash (before early 1980)

▪ New reg = Residual receipts requirements no matter what type of underlying financing you have

OLD REG vs. NEW REG can influence choices based on cash flow options.

Section 8 Contracts➢What contract term should you select?▪ 20 years is the goal

➢What Renewal Option should you select?▪ Option 1 – NON-PROFIT SENIOR HOUSING OWNERS ARE ELIGIBLE!

▪ Option 2 – Budget-based; no “lesser-of” test; RCS adjustments – IF RENTS ARE BELOW MARKET NO NEED FOR THIS

▪ Option 4 – ONLY VALUABLE IF RENTS ABOVE MARKET; don’t forget “lesser-of” test at renewal

5/4/2017

6

Section 8 Contracts

HUD wants to make sure you are maximizing your

rent potential…

Section 8 Contract Rent Increases

➢ NEW! - Mark-up-to-Market under Option 1b -Available to non-profit senior housing providers. Does not require a budget to support the rents.▪ Use a new RCS to set rents▪ PCNA/scope (if going for post-rehab rents)▪ Understand where extra cash flow will go▪ 5 to 20 year contracts

Option 4 contracts that are above market are not eligible for a rent increase.

Option 4 Contracts Renewals

➢ Lesser-of test at renewal must support over-market rents: Can impact prepayment options for 202 owners.

➢ Rents might be UNDER MARKET Mark rents up under Option 1b

5/4/2017

7

KNOW YOUR PROPERTY: Key Section 8 Documents

➢ Original Sec. 8 Contract (new reg vs. old reg)

➢ Most recent Sec. 8 Contract (current renewal option, term)

➢ Most recent RCS, if available (market rents)

➢ Most recent Sec. 8 rents (rents above, below, at market)

RAP and Rent Supp

RAP and Rent Supplement

➢Contracts cannot be renewed

➢Convert to long-term subsidy through RAD 2▪ Can convert to PBV or PBRA▪ Rents determined by RCS▪ Can increase the number of subsidy when

unsubsidized units qualify for Enhanced Vouchers

5/4/2017

8

KNOW YOUR PROPERTY: RAP and Rent Supplement

➢ Original Subsidy Contract (original number of units)

➢ Most recent Subsidy Contract (expiration date)

➢ Most recent RCS, if available (market rents)

➢ Income of unsubsidized units (who can get more subsidy)

HUD 202 Direct Loans

HUD 202 Direct Loans

➢Why prepay the 202 loan?▪ Prepay because capital needs cannot wait and new

financing is needed to address them.▪ Prepay to protect Option 4 over-market rents with new

debt service (and also complete capital repairs).▪ Prepay to refinance with lower interest debt.

5/4/2017

9

HUD 202 Direct Loans

• 202 Loans made before 1974: Must prove “substantial rehab” for permission to prepay:➢ Waivers are available

• 202 Loans made after 1974: Must prove “debt service savings” for permission to prepay.➢ Can be an issue in the “lesser-of test”

• 202 Loans made between 1977 – 1982: May not require HUD permission to prepay.

HUD 202 Direct Loans

Note that HUD prepayment permission requires…

20 year Regulatory Agreement Extension

NOTE: The residual receipts requirements will continue on for another 20 years. Owners with “old reg” Section 8 contracts may want to think carefully about prepaying vs. allowing loan to mature.

HUD 202 Direct Loans

If your loan matures, there is the potential for PBV subsidy for unsubsidized residents.

See HUD Notice PIH 2016-12

5/4/2017

10

KNOW YOUR PROPERTY: Key HUD 202Documents

➢ 202 Regulatory Agreement (tenancy restrictions, term)

➢ 202 Loan Note (prepayment permission, interest rate, term)

HUD Insured 236 and State Uninsured 236 Loans

HUD 236 Insured Loans

➢Prepayment:▪ Most non-profit owners require HUD permission to

prepay a 236 Loan.▪ HUD permission requires 150 day tenant notice.

➢Decoupling:▪ Remove the IRP balance and apply to a new loan.▪ Decoupling requires a 5-year extension of the 236

Use Agreement

5/4/2017

11

KNOW YOUR PROPERTY: Key HUD 236 Documents

➢ 236 Regulatory Agreement (tenancy restrictions, term)

➢ 236 Loan Note (prepayment permission, interest rate, term)

➢ IRP Agreement and Amortization (IRP balance)

LIHPRHA or Title VI

LIHPRHA or Title VI

➢Program to prevent loss of AH units (typically 221d3 or 236 projects)

➢HUD Notice 2016-16 – Use Agreement can be amended:▪ Allows unlimited distributions from surplus cash▪ Unrestricted access to residual receipts▪ Remove restrictions on use of refi or sale proceeds

5/4/2017

12

LIHPRHA or Title VI

➢Requirements▪ Existing UA is base affordability restrictions▪ REAC of 60+ and “Satisfactory” MOR▪ Must be in compliance with UA▪ Must fund any needed capital repairs (PCNA)

➢Secret Ingredient for Refi▪ Not subject to Rent Comparability▪ Can request rent increase above market to support

refi, rehab and new debt service

KNOW YOUR PROPERTY: Key LIHPRHA Documents

➢ Use Agreement

Flexible Subsidy Loans

5/4/2017

13

Flexible Subsidy Loan

Deferral of Operating Assistance Flex Sub loans possible in a refinancing scenario.

Deferral under Notice 2011-05:➢Typically part of a refinancing

➢Prepare to pay something at closing

➢Must pay entire loan within new loan term

KNOW YOUR PROPERTY: Key Flex Sub Documents

➢ Flex Sub Regulatory Agreement (tenancy restrictions, term)

➢ Residual Receipts Note (type, interest rate)

IMPORTANT HUD NOTICESHUD 236 LoansNotice H 2013-25 – clarification for IRP decoupling

Notice H 2011-31 – guidance on NP selling

Notice 2006-11 – requirements for obtaining pre-payment permission

For HUD 202 LoansJune 26, 2013 Memo – Clarifies HUD Notice H 2013-17

Notice H 2013-17 – updates prior Notices regarding pre-payment of 202 Loans, including guidance on taking out equity

Notice H 2010-26 – guidance for subordinating a 202 loan

Notice H 2004-21 – refinancing rules for 202’s; some aspects superseded by Notices 2012-08 and 2013-17

Flexible Subsidy LoansNotice H 2013-02 – Gives more specifics on maturing Flex Subs and the process for deferring

Notice H 2011-05 (extended by Notice 2012-04) –establishes the process by which an owner can request a Flexible Subsidy Loan deferral

5/4/2017

14

Know your Property

Key documents and information

Loan Agreements and Regulatory Agreements

Rental Subsidy agreements (original and current)

Audit

Rent Roll

Capital Needs Assessment

Ok, I understand my property, now what?

NOW WHAT?

5/4/2017

15

SET PRESERVATION GOALS

Decide on your GOALS for the refinancing

This will be your roadmap AND a way to keep the team and board on track….

Typical goals… Lower your interest rate (new 202 loans) Capital Improvements Modernization of units TPVs for unassisted units Protect “debt service” line item Receive Developer Fee Improved common and amenity space for residents Deal with your Flexible Subsidy Loan

GOALS typically include completing repairs

What do you want to do with your repair funds?

Checklist for use of funds… Address the agreed upon GOALS PCNA – useful life of systems, options for “greening up” Prioritize your wishlist – you may have to cut scope Understand lender requirements Cost Estimates

5/4/2017

16

Refinancing requires Net Operating Income = NOI

Before you start, can you increase NOI?

➢ Rent Comparability Study will indicate potential growth of INCOME Mark-up-to-Market

➢ Consider the “post rehab” comparable rents through the MU2M process

➢ Increased income through RAD conversion?➢ Decrease operating expenses?

Choose your preservation optionsDo you need a recapitalization?Explore financing options.Explore rental assistance options.

Conventional Loans

FHA 223(f) Loans

FHA 221(d)4 Loans

Tax Exempt Bonds with 4% LIHTCs

9% LIHTCs

FINANCING OPTIONS

Universe of properties that can be refinanced with this type of financing

Leve

l of r

eh

ab t

hat

can

be

aff

ord

ed

5/4/2017

17

Conventional Loans

PROS➢Non-HUD product➢Fast timeline➢Lowest fees➢Broad applicability

CONS➢Recourse➢80% LTV and ➢1.20 DCR➢Market interest rate➢5-10 year terms➢Sec 8 unfamiliarity➢Small rehab budget

FHA Loans➢ Insured by HUD

➢ MAP Lenders

➢ Higher fees, lower rates

➢ Favorable terms for 236 and 202 refi’s

➢ No affordability restrictions

FHA 223(f) Loan

“Repair Loan”

What repairs can I do?

Must complete repairs in 12 months from closing

No more than one major system replaced

5/4/2017

18

FHA 223(f) Loan

“Repair Loan”

223(f) PROS➢Non-recourse➢Up to 90% LTV➢1.10 DCR➢35 year term➢Low interest rates➢Medium Rehab➢No Davis-Bacon wage rates

FHA 223(f) Loan

“Repair Loan”

223(f) CONS

➢Longer timelines

➢HUD world

➢Moderate fees

FHA 221(d)4 Loan

“Sub Rehab Loan”

221(d)4 PROS➢Non-recourse➢Up to 90% LTV➢1.10 DCR➢40 year term➢Low interest rates➢High Rehab budget

5/4/2017

19

FHA 221(d)4 Loan

“Sub Rehab Loan”

221(d)4 CONS

➢Longest timelines

➢HUD world

➢High fees

➢Davis-Bacon wage rates

➢Equity might be needed

Low Income Housing Tax Credits

➢ Equity generated

➢ Change in ownership required

➢ Property Taxes

➢ Complicated process

➢ New compliance

4% LIHTCs and Tax Exempt Bonds

➢ Non-competitive LIHTC program

➢ Requires “experienced” partners

➢ Substantial rehabilitation

➢ Soft (gap) financing typically needed

➢ 15+ year affordability period

➢ High up-front expenses and fees

5/4/2017

20

9% LIHTCs➢ Highly Competitive LIHTC program

➢ Complicated and expensive process; requires “experienced” partners

➢ Largest amount of rehabilitation

➢ Soft (gap) financing typically needed

➢ 30+ year affordability period

➢ High up-front expenses and fees

New York Homes & Community Renewal Funding

State-wide Resources: New York State Homes & Community Renewal (NYSHCR)• Federal LIHTC issuer, plus has State LIHTC• New York State HOME• Low-Income Housing Trust Fund Program• Housing Development Fund• Community Investment Fund• Farmworker Housing Program• Homes for Working Families Initiative• Legislative Member Item Program• Rural Rental Assistance

New York State Housing Finance Agency

State-wide Resources: New York State Housing Finance Agency• All Affordable Housing Program• Second Mortgage “Subsidy Loans”• 4% LIHTCs with Tax-exempt Bonds• Mitchell Lama Rehab and Preservation• Taxable Mortgage Initiative• NYSERDA• State of New York Mortgage Agency

5/4/2017

21

NYC Dept of Housing Preservation and Development

NYC City Resources: Dept of Housing Preservation & Development• Green House Preservation Program• HPD HUD Multifamily Program

Tax Exemption

Subsidy

• LIHTC Preservation Program• MF Housing Rehabilitation Program• Primary Prevention Program• Senior Affordable Rental Apartments Program

NYC Housing and Development Corporation

NYC City Resources: NYC Housing and Development Corporation• Preservation Program• Repair Loan Program• Mortgage Restructuring Program• NYC Residential Mortgage Insurance Corp• Housing Assistance Corporation• Housing New York Corporatino• NYCHDC Real Estate Corp

Thank you. I now know my refinancing options….

NOW WHAT?

5/4/2017

22

Moving to a Preservation

1. Know your property: Gather the documents and due diligence.

2. Owner education and strategy:▪ Training/Advising▪ Set the goals for the property▪ Match the goals to the best funding option▪ Set-aside funding for pursuing option

3. Discuss plan with HUD

4. Move forward with HUD approvals and funding applications

St. John’s Towers

St. John’s Towers

OVERVIEW OF PROPERTY ➢ Senior 7-story, 57 unit

coastal Havre de Grace, MD

➢ Non-profit owned

➢ 202 Direct loano Closed 7/27/66o Matured 2016o 3% Interest Rate

➢ Section 8 o 53 of 57 unitso Option 4

➢ Flex Sub Loan due at maturity ($783k)

5/4/2017

23

St. John’s Towers

PRESERVATION HURDLES1. Unsure of options

2. Current Sec 8 rents under-market

3. 202 Prepayment process

4. Flex Sub deferral

5. Refinancing and Rehab options

St. John’s Towers

PRESERVATION STRATEGIES1. Unsure of options Training, education & advisement

2. Current Sec 8 rents under-market Terminate and replace with new 20-year MU2M Section 8 Contract

3. 202 Prepayment process Obtained waiver for “sub rehab”, obtained HUD prepayment permission

4. Flex Sub deferral Flex Sub deferral approved

5. Refinancing and Rehab options Team decisions on scope of work, best financing options

St. John’s Towers

PRESERVATION OUTCOMES1. Increased Section 8 Rental income

BEFORE: $528,000 PGI AFTER: $635,000 PGI $107,000 annual increase = 20% increase!

2. Flexible Subsidy Loan Deferral BALANCE DUE: $783K AMT PAID WITH NEW FINANCING: $371K $400K available for

repairs!

3. Refinanced with FHA 223(f) Loan and AHP Grant NEW LOAN: $1.6M; AHP GRANT: $176K = $1,776k in proceeds REPAIR BUDGET $1.225K

5/4/2017

24

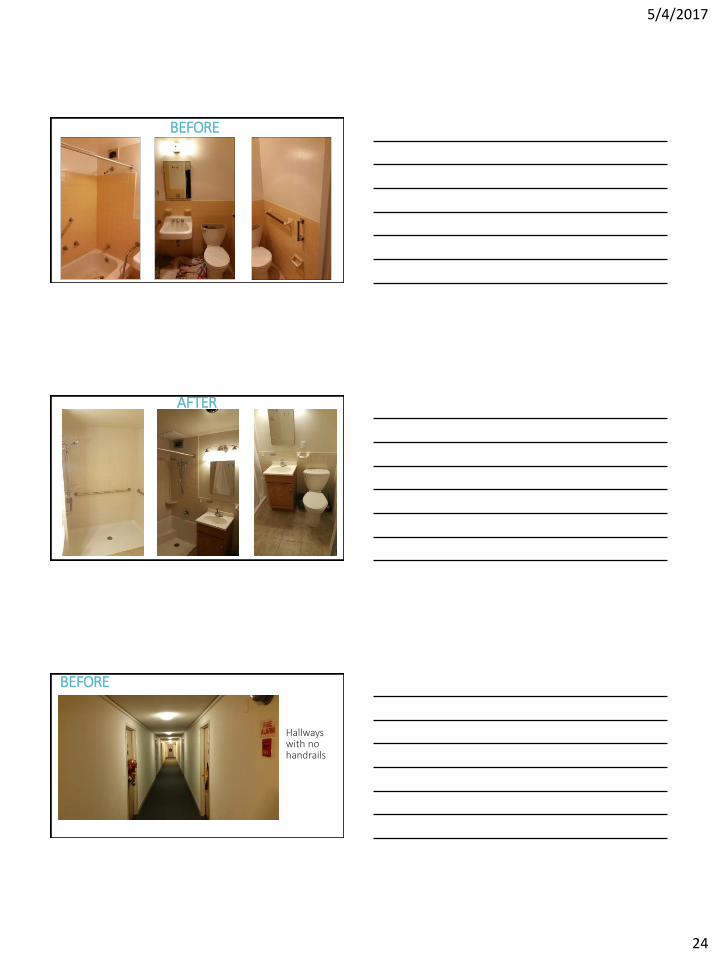

BEFORE

AFTER

BEFORE

Hallways with no handrails

5/4/2017

25

AFTER

Hallways with new handrails to improve accessibility

St. John’s Towers

TIMELINE➢ HUD Preservation Training - April 2012

➢ Preservation Study – Summer 2012

➢ Rent increase approved – December 2013

➢ Lender, contractor, architect selection – 2014

➢ FHA Application assembly – 2015

➢ AHP – November 2015

➢ Closing on FHA 223(f) – December 2015

➢ Construction completion – November 2016

Lutheran Towers

5/4/2017

26

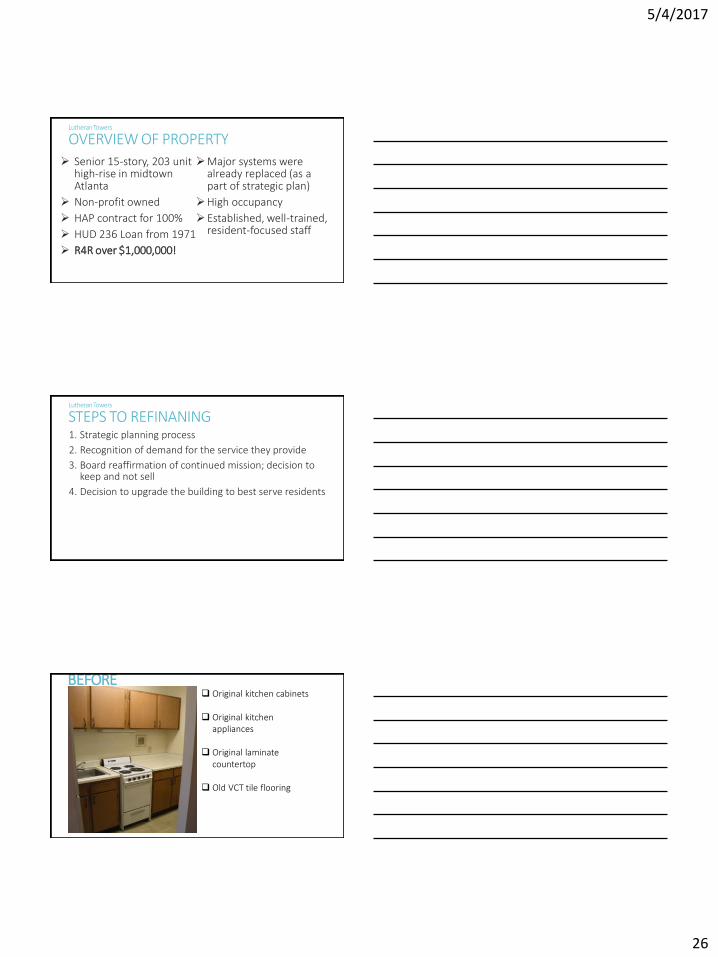

Lutheran Towers

OVERVIEW OF PROPERTY

➢ Senior 15-story, 203 unit high-rise in midtown Atlanta

➢ Non-profit owned

➢ HAP contract for 100%

➢ HUD 236 Loan from 1971

➢ R4R over $1,000,000!

➢Major systems were already replaced (as a part of strategic plan)

➢High occupancy

➢Established, well-trained, resident-focused staff

Lutheran Towers

STEPS TO REFINANING1. Strategic planning process

2. Recognition of demand for the service they provide

3. Board reaffirmation of continued mission; decision to keep and not sell

4. Decision to upgrade the building to best serve residents

BEFOREADD BEFORE PICTURE Original kitchen cabinets

Original kitchen appliances

Original laminate countertop

Old VCT tile flooring

5/4/2017

27

BEFORE

Photos show how kitchen was closed-in and had no natural light

AFTERHardwood cabinets

New lighting

New appliances

New granite countertops

New under-mounted stainless sink

New tile flooring

Kitchen opened up to living room to allow natural light

AFTER

5/4/2017

28

BEFOREOriginal bathroom fixtures and tile

AFTER

New tile (tub walls and floor)

New toilet, sink, tub valves and accessories

New lighting

Lutheran Towers

TIMELINE FOR PRESERVATION2007 – Started process to select developer/consultant

2008 – Selected consultant

2008 – Presented with 3 financing options: 223(f), 221(d)4, and 9% LIHTC with a recommendation to pursue 223(f)

… Delayed making final decision due to Board resistance …

2009 – Restarted refinancing process

April 2011 – Closed on loan

May 2011 – Began renovations

April 2012 – Completed renovations

5/4/2017

29

Lutheran Towers

THE NUMBERS….

Source Amount

FHA 223(f) Loan $2,200,000

R4R and ResidualReceipts Reserves

$1,000,000

TOTAL $3,200,000

Uses Amounts

Loan Pay-off $537,000

3rd Party $273,500

R4R (upfront) $274,000

Temp Relo $50,000

Legal $47,500

Financing Fees $131,000

Construction $1,887,000

TOTAL $3,200,000

SOURCES USES

Lutheran Towers

THE SCOPE OF WORKConstruction Line Item Amount Spent

Asbestos (ACM) Removal $242,830

ADA conversions (11 units) and grab bars in all bathrooms $52,135

Corridor handrails $28,300

Kitchen Cabinets (hardwood) $216,703

Granite Countertops w/ new under-mounted kitchen sinks $41,615

New tile, accessories, plumbing fixtures in bathrooms $414,941

New Appliances (fridge and range) $165,272

New wireless emergency call system $157,215

New ceiling fans and light fixtures $180,752

General construction, overhead, trash, clean-up, etc $387,237

TOTAL $1,887,000

PHOTOS – Phase 2Lutheran TowersAtlanta, Georgia

5/4/2017

30

Exterior Entrance Before After

Atrium Before After

Lobby Before After

5/4/2017

31

For more information contact:THE GATES DUNAWAY GROUP

Gates Kellett Dunaway(404) [email protected]

JASA HOUSING MANAGEMENT FOR THE AGED

Donald Manning(212) [email protected]

RECAP ADVISORS

Shannon Lestan(617) [email protected]