Initiating Coverage December 8, 2017 Narayana...

25

December 8, 2017 Initiating Coverage ICICI Securities Ltd | Retail Equity Research Asset right + affordable + flexible Incorporated by renowned cardiac surgeon Dr Devi Prasad Shetty in 2000, Narayana Hrudayalaya (NH) operates as a chain of multispecialty hospitals. Started predominantly in Karnataka and Eastern India, the company is growing its footsteps in western and northern India as well. We initiate coverage on the company as we believe NH is well poised to thrive in the domestic healthcare delivery (hospitals) space on the back of its asset right business model with focus on quality and affordability. Investment rationale Blended model of affordable + high-quality services NH has a legacy model based on affordability over the years. Due to strict control over costs and capital, the company has been making reasonable profit. However, as it is looking to scale up in other regions, where the consideration for quality has more weight than affordability, the model is likely to be modified from ‘affordable’ to a mix of ‘affordable + quality’ at a premium. Cases in point are the recent acquisition of Gurugram hospital and buying out of the partner in the Cayman Islands hospital internationally where acquisition costs were optically higher. ‘’Asset right model’’, likely ARPOB improvement to improve return ratios Under this model, the company engages with partners who invest in land and building while it takes care of medical equipment and hospital management on a revenue share basis. This is why NH’s balance sheet is one of the lightest among peers. However, the management has maintained a flexible approach in this regard. Thus, it also owns some hospitals where the opportunity is right. Due to this focus on balance sheet and likely improvement in average realisation per operating bed (ARPOB) by optimising case mix, we expect an improvement in RoCE from 12.5% to 19% during FY17-20E. After effective cost, capital management focus shifts to improving ARPOB In a conducive but challenging space of Indian healthcare delivery, plagued by longer gestation periods, low operating margin, leveraged balance sheets and low return ratios, we believe NH is best placed among peers to sail through. Its legacy model is based on affordability. Hence, conscious efforts towards cost & capital control are embedded in the management’s long term strategy. This becomes even more pertinent in the backdrop of incremental government intervention via schemes and control over procedures & products. On the other hand, it is also determined to improve ARPOB by improving case mix, occupancies, thus fine-tuning affordability with profitability. We arrive at an SOTP target price of | 340 by valuing the matured hospitals and Cayman Islands hospital at 12x FY20E EV/EBITDA, other hospitals at 1.5x FY20E EV/sales and other businesses at 1.0x FY20E EV/sales. Key Financials (Year End March) FY16 FY17 FY18E FY19E FY20E Revenues (| crore) 1613.9 1878.2 2269.7 2665.0 3021.5 EBITDA (| crore) 174.6 228.9 254.3 311.4 409.7 Net Profit (| crore) 32.2 84.4 89.0 136.2 203.4 EPS (|) 1.6 4.1 4.4 6.7 10.0 P/E (x) 273.4 69.8 66.1 42.6 28.5 EV/EBITDA (x) 34.5 26.0 23.9 19.2 14.2 RoCE (%) 8.8 12.5 11.9 14.4 18.7 RoE (x) 3.7 8.8 8.5 11.5 14.6 Source: Company, ICICIdirect.com Research Narayana Hrudayalaya (NARHRU) | 284 Rating Matrix Rating : Buy Target : | 340 Target Period : 12-15 months Potential Upside : 20% Financial Parameters (| crore) (| Crore) FY17 FY18E FY19E FY20E Revenues 1878.2 2269.7 2665.0 3021.5 EBITDA 228.9 254.3 311.4 409.7 Adjusted PAT 84.4 89.0 136.2 203.4 EPS (|) 4.1 4.4 6.7 10.0 Current & Target Multiples FY17 FY18E FY19E FY20E PE (x) 68.7 65.2 42.6 28.5 Target PE (x) 82.3 78.1 51.0 34.2 EV to EBITDA (x) 26.0 23.9 19.2 14.2 Price to book (x) 6.0 5.5 4.9 4.2 RoE (%) 8.8 8.5 11.5 14.6 RoCE (%) 12.5 11.9 14.4 18.7 Stock Data Particular Bloomberg Code Average Volumes (6 months) Market Capitalisation Debt (FY17) Cash (FY17) EV 52 week H/L (|) 350/282 Equity capital Face value | 10 Amount | 5801 crore | 217 crore | 116 crore | 5901 crore | 204.4 crore NARH IN 164523 Comparative return matrix (%) 1M 3M 6M 1Y Narayana Hrudayalaya -3.6 -2.5 -9.7 -12.6 Apollo Hospitals 14.1 5.8 -11.1 -4.6 Fortis Healthcare 2.3 -3.7 -23.3 -13.2 Price movement 7,000 8,000 9,000 10,000 11,000 0 100 200 300 400 Dec-17 Jun-17 Dec-16 Jun-16 | Price (R.H.S) Nifty (L.H.S) Research Analyst Siddhant Khandekar [email protected] Mitesh Shah [email protected] Harshal Mehta [email protected]

Transcript of Initiating Coverage December 8, 2017 Narayana...

December 8, 2017 Initiating Coverage

ICICI Securities Ltd | Retail Equity Research

Asset right + affordable + flexible

Incorporated by renowned cardiac surgeon Dr Devi Prasad Shetty in 2000,

Narayana Hrudayalaya (NH) operates as a chain of multispecialty hospitals.

Started predominantly in Karnataka and Eastern India, the company is

growing its footsteps in western and northern India as well. We initiate

coverage on the company as we believe NH is well poised to thrive in the

domestic healthcare delivery (hospitals) space on the back of its asset right

business model with focus on quality and affordability.

Investment rationale

Blended model of affordable + high-quality services

NH has a legacy model based on affordability over the years. Due to strict

control over costs and capital, the company has been making reasonable

profit. However, as it is looking to scale up in other regions, where the

consideration for quality has more weight than affordability, the model is

likely to be modified from ‘affordable’ to a mix of ‘affordable + quality’ at a

premium. Cases in point are the recent acquisition of Gurugram hospital

and buying out of the partner in the Cayman Islands hospital

internationally where acquisition costs were optically higher.

‘’Asset right model’’, likely ARPOB improvement to improve return ratios

Under this model, the company engages with partners who invest in land

and building while it takes care of medical equipment and hospital

management on a revenue share basis. This is why NH’s balance sheet is

one of the lightest among peers. However, the management has

maintained a flexible approach in this regard. Thus, it also owns some

hospitals where the opportunity is right. Due to this focus on balance sheet

and likely improvement in average realisation per operating bed (ARPOB)

by optimising case mix, we expect an improvement in RoCE from 12.5%

to 19% during FY17-20E.

After effective cost, capital management focus shifts to improving ARPOB

In a conducive but challenging space of Indian healthcare delivery,

plagued by longer gestation periods, low operating margin, leveraged

balance sheets and low return ratios, we believe NH is best placed among

peers to sail through. Its legacy model is based on affordability. Hence,

conscious efforts towards cost & capital control are embedded in the

management’s long term strategy. This becomes even more pertinent in

the backdrop of incremental government intervention via schemes and

control over procedures & products. On the other hand, it is also

determined to improve ARPOB by improving case mix, occupancies, thus

fine-tuning affordability with profitability. We arrive at an SOTP target price

of | 340 by valuing the matured hospitals and Cayman Islands hospital at

12x FY20E EV/EBITDA, other hospitals at 1.5x FY20E EV/sales and other

businesses at 1.0x FY20E EV/sales.

Key Financials

(Year End March) FY16 FY17 FY18E FY19E FY20E

Revenues (| crore) 1613.9 1878.2 2269.7 2665.0 3021.5

EBITDA (| crore) 174.6 228.9 254.3 311.4 409.7

Net Profit (| crore) 32.2 84.4 89.0 136.2 203.4

EPS (|) 1.6 4.1 4.4 6.7 10.0

P/E (x) 273.4 69.8 66.1 42.6 28.5

EV/EBITDA (x) 34.5 26.0 23.9 19.2 14.2

RoCE (%) 8.8 12.5 11.9 14.4 18.7

RoE (x) 3.7 8.8 8.5 11.5 14.6

Source: Company, ICICIdirect.com Research

Narayana Hrudayalaya (NARHRU)

| 284

Rating Matrix

Rating : Buy

Target : | 340

Target Period : 12-15 months

Potential Upside : 20%

Financial Parameters (| crore)

(| Crore) FY17 FY18E FY19E FY20E

Revenues 1878.2 2269.7 2665.0 3021.5

EBITDA 228.9 254.3 311.4 409.7

Adjusted PAT 84.4 89.0 136.2 203.4

EPS (|) 4.1 4.4 6.7 10.0

Current & Target Multiples

FY17 FY18E FY19E FY20E

PE (x) 68.7 65.2 42.6 28.5

Target PE (x) 82.3 78.1 51.0 34.2

EV to EBITDA (x) 26.0 23.9 19.2 14.2

Price to book (x) 6.0 5.5 4.9 4.2

RoE (%) 8.8 8.5 11.5 14.6

RoCE (%) 12.5 11.9 14.4 18.7

Stock Data

Particular

Bloomberg Code

Average Volumes (6 months)

Market Capitalisation

Debt (FY17)

Cash (FY17)

EV

52 week H/L (|) 350/282

Equity capital

Face value | 10

Amount

| 5801 crore

| 217 crore

| 116 crore

| 5901 crore

| 204.4 crore

NARH IN

164523

Comparative return matrix (%)

1M 3M 6M 1Y

Narayana Hrudayalaya -3.6 -2.5 -9.7 -12.6

Apollo Hospitals 14.1 5.8 -11.1 -4.6

Fortis Healthcare 2.3 -3.7 -23.3 -13.2

Price movement

7,000

8,000

9,000

10,000

11,000

0

100

200

300

400

Dec-17

Jun-17

Dec-16

Jun-16

|

Price (R.H.S) Nifty (L.H.S)

Research Analyst

Siddhant Khandekar

Mitesh Shah

Harshal Mehta

Page 2 ICICI Securities Ltd | Retail Equity Research

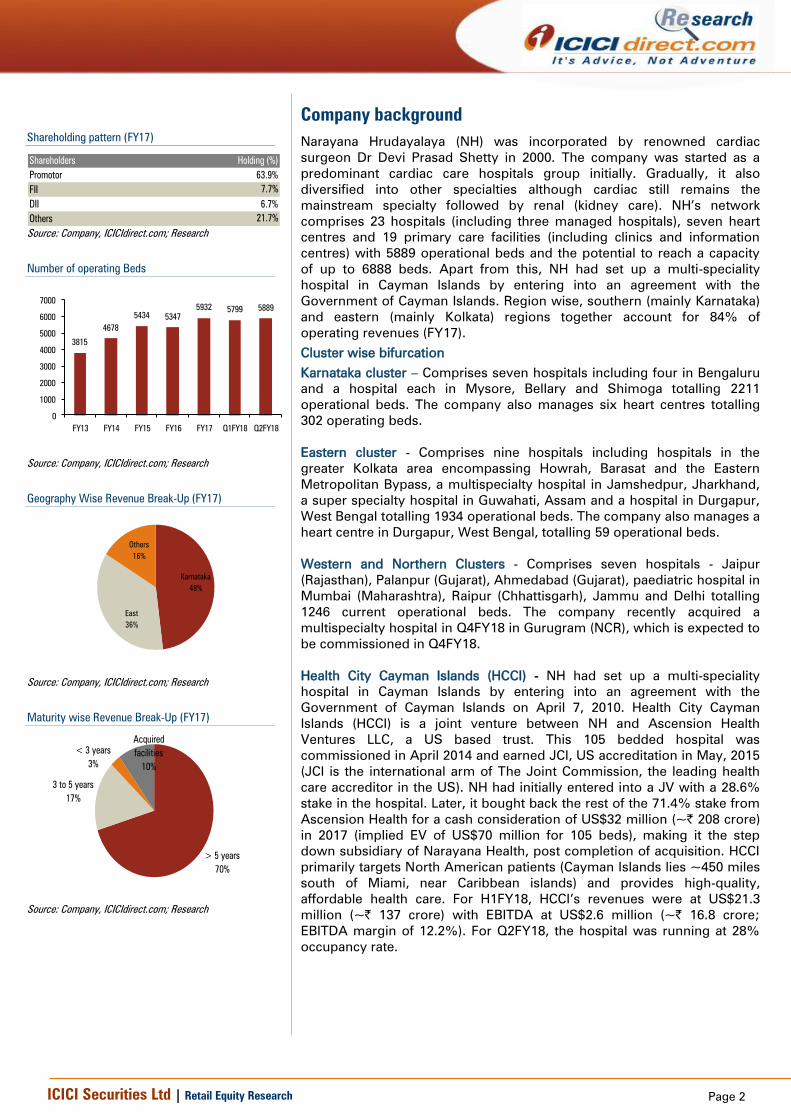

Company background

Narayana Hrudayalaya (NH) was incorporated by renowned cardiac

surgeon Dr Devi Prasad Shetty in 2000. The company was started as a

predominant cardiac care hospitals group initially. Gradually, it also

diversified into other specialties although cardiac still remains the

mainstream specialty followed by renal (kidney care). NH’s network

comprises 23 hospitals (including three managed hospitals), seven heart

centres and 19 primary care facilities (including clinics and information

centres) with 5889 operational beds and the potential to reach a capacity

of up to 6888 beds. Apart from this, NH had set up a multi-speciality

hospital in Cayman Islands by entering into an agreement with the

Government of Cayman Islands. Region wise, southern (mainly Karnataka)

and eastern (mainly Kolkata) regions together account for 84% of

operating revenues (FY17).

Cluster wise bifurcation

Karnataka cluster – Comprises seven hospitals including four in Bengaluru

and a hospital each in Mysore, Bellary and Shimoga totalling 2211

operational beds. The company also manages six heart centres totalling

302 operating beds.

Eastern cluster - Comprises nine hospitals including hospitals in the

greater Kolkata area encompassing Howrah, Barasat and the Eastern

Metropolitan Bypass, a multispecialty hospital in Jamshedpur, Jharkhand,

a super specialty hospital in Guwahati, Assam and a hospital in Durgapur,

West Bengal totalling 1934 operational beds. The company also manages a

heart centre in Durgapur, West Bengal, totalling 59 operational beds.

Western and Northern Clusters - Comprises seven hospitals - Jaipur

(Rajasthan), Palanpur (Gujarat), Ahmedabad (Gujarat), paediatric hospital in

Mumbai (Maharashtra), Raipur (Chhattisgarh), Jammu and Delhi totalling

1246 current operational beds. The company recently acquired a

multispecialty hospital in Q4FY18 in Gurugram (NCR), which is expected to

be commissioned in Q4FY18.

Health City Cayman Islands (HCCI) - NH had set up a multi-speciality

hospital in Cayman Islands by entering into an agreement with the

Government of Cayman Islands on April 7, 2010. Health City Cayman

Islands (HCCI) is a joint venture between NH and Ascension Health

Ventures LLC, a US based trust. This 105 bedded hospital was

commissioned in April 2014 and earned JCI, US accreditation in May, 2015

(JCI is the international arm of The Joint Commission, the leading health

care accreditor in the US). NH had initially entered into a JV with a 28.6%

stake in the hospital. Later, it bought back the rest of the 71.4% stake from

Ascension Health for a cash consideration of US$32 million (~| 208 crore)

in 2017 (implied EV of US$70 million for 105 beds), making it the step

down subsidiary of Narayana Health, post completion of acquisition. HCCI

primarily targets North American patients (Cayman Islands lies ~450 miles

south of Miami, near Caribbean islands) and provides high-quality,

affordable health care. For H1FY18, HCCI’s revenues were at US$21.3

million (~| 137 crore) with EBITDA at US$2.6 million (~| 16.8 crore;

EBITDA margin of 12.2%). For Q2FY18, the hospital was running at 28%

occupancy rate.

Shareholding pattern (FY17)

Shareholders

Promotor 63.9%

FII 7.7%

DII 6.7%

Others 21.7%

Holding (%)

Source: Company, ICICIdirect.com; Research

Number of operating Beds

3815

4678

5434 5347

5932 5799 5889

0

1000

2000

3000

4000

5000

6000

7000

FY13 FY14 FY15 FY16 FY17 Q1FY18 Q2FY18

Source: Company, ICICIdirect.com; Research

Geography Wise Revenue Break-Up (FY17)

Karnataka

48%

East

36%

Others

16%

Source: Company, ICICIdirect.com; Research

Maturity wise Revenue Break-Up (FY17)

> 5 years

70%

3 to 5 years

17%

< 3 years

3%

Acquired

facilities

10%

Source: Company, ICICIdirect.com; Research

Page 3 ICICI Securities Ltd | Retail Equity Research

Exhibit 1: NH’s footprint in India

Source: Company, ICICIdirect.com; Research

NH operates through a combination of following models:

1) Owned or long term/perpetual lease – It owns and operates on a

freehold basis or land taken on long term/perpetual lease. NH

operates eight hospitals of 2607 operating beds in FY17

2) Revenue share/rentals – NH operates and pays a revenue

share/rent to owner of the hospital premises. It operates 10

hospitals of 1817 operating beds in FY17

3) Management contract – NH provides healthcare services to third

parties for a management fee. It managed four hospitals of 720

operating beds in FY17

4) PPP – NH operates with nominal investment in partnership with

public entities. It operates two hospitals of 297 operating beds

5) Apart from this, the company has seven heart centres and 19

standalone clinics, primary care facilities and information centres

that it operates on a lease or license basis

Its centres provide advanced levels of care in over 30 specialties, including

cardiology and cardiac surgery, cancer care, neurology and neurosurgery,

orthopaedics, nephrology and urology and gastroenterology. In FY17, it

generated 90.7% of total revenues from 20 hospitals offering

multispecialty and super specialty services, 7.3% from heart centres while

the remaining was from the management fee received from four managed

hospitals, ancillary businesses and other standalone clinics & primary care

facilities.

As of FY17, it has 14330 employees, including 356 doctors, 11316 nurses,

paramedical staff and administrative personnel. Additionally, it has 469

student doctors, paramedics and administrative trainees. Further, it has

1,016 doctors on a consultancy basis (including visiting consultants).

Therapy wise revenue break-up (Q2FY18)

Cardiac

41%

Gastro

17%

Neuro

8%

Others

11%

Orthopaedics

4%

Oncology

10%

Renal

9%

Source: Company, ICICIdirect.com; Research

Payee-Profile (Q2FY18)

International

patients

9%

Insured

Patients

19%

Schemes

17%

Walk-in

patients

55%

Source: Company, ICICIdirect.com; Research

Page 4 ICICI Securities Ltd | Retail Equity Research

Exhibit 2: Narayana Hrudayalaya hospital network (ex-managed and heart centres)

Sr no Hospital Land

1 NICS, Bengaluru Owned

2 MSMC, Bengaluru Owned

3 RTIICS, Kolkata Leased

4 Brahmananda Narayana Multispeciality Hospital, Jamshedpur Leased

5 Narayana Multispeciality Hospital, Jaipur Leased

6 Narayana Multispeciality Hospital, Ahmedabad Leased

7 MMI Narayana Multispeciality Hospital, Raipur Revenue-share

8 Narayana Multispeciality Hospital, Mysore Leased

9 Sahyadri Narayana Multispeciality Hospital, Shimoga Revenue-share

10 Narayana Multispeciality Hospital, Whitefield, Bengaluru Revenue-share

11 Narayana Multispeciality Hospital, HSR Layout, Bengaluru Revenue-share

12 Narayana Superspeciality Hospital, Guwahati PPP

13 Rabindranath Tagore Surgical Centre, Kolkata, West Bengal Leased

Acquired Hospitals

14 Narayana Multispeciality Hospital, Barasat, WB Owned

15 Narayana Multispeciality Hospital, Howrah Owned

16 Narayana Superspeciality Hospital, Howrah Leased

New facilities 2016 onwards

17 Kakriyal, Jammu PPP

18 Dharamshila Narayana Hospital Revenue-share

19 Hospital in Gurugram (Acquired) Owned

20 SRCC Children Hospital, Mumbai Revenue-share

Source: Company, ICICIdirect.com; Research, NICS=Narayana Institute of Cardiac Sciences, MSCM=Mazumdar

Shaw Medical Centre, RTIICS=Rabindranath Tagore International Institute of Cardiac Sciences

Page 5 ICICI Securities Ltd | Retail Equity Research

Exhibit 3: Key events s

2000 Narayana Health City, Bengaluru, founded by Dr Devi Prasad Shetty

2008 Joins hands with Asia Heart Foundation to run the RTIICS hospital in Kolkata and NSC

2009 Sets up cardiac and cardiology centre at the SDM College of Medical Science & Hospital in Dharwad, Karnataka

2009 Institutes ‘Heart Centre’ at MS Ramaiah Medical College Hospital in Bengaluru

2009 Establishes a multispecialty hospital in Jamshedpur

2009 Starts multispecialty Mazumdar Shaw Cancer Centre in Bengaluru

2009 Sets up ‘Heart Centre’ at Chinmaya Mission Hospital in Bengaluru

2010 Starts multispecialty hospital in Hyderabad

2010 Sets up multispecialty hospital in Jaipur

2010 Sets up Rotary Narayana, a super-speciality cardiac care unit in Kolkata

2010 Sets up ‘Heart Centre’ in Kolar, Karnataka

2011 NICS receives accreditation from JCI

2011 Inaugurates a multispecialty hospital in Raipur

2012 Sets up multispecialty hospital in Ahmedabad

2012 Establishes heart centres at Davangere

2012 Narayana Multispecialty Hospital in Jaipur receives accreditation from JCI

2013 Sets up multispecialty hospitals at Shimoga, Mysore, Durgapur and HSR, Bengaluru

2013 Establishes super specialty hospital at Whitefield, Bengaluru and Guwahati

2013 Starts ‘Heart Centres’ at St Martha’s, West Bank, Suguna and Kuppam

2014 Inclusion of Barasat and Berhampore hospitals in NH Group

2014 Starts operations at Health City, Cayman Islands Phase 1 with 101 operational beds

2015 Acquires two Westbank Hospitals in Howrah

2015 Multispecialty hospitals set up at Palanpur, Mahua and Bellary

2015 Establishes a full-fledged cancer centre at Mysore to provide high-quality cancer treatment at an affordable cost

2015 Forms an association with Shri Mata Vaishno Devi Shrine Board, through PPP, to build a 230 capacity bed hospital in Kakriyal, Jammu

2016 Company lists its shares on Bombay Stock Exchange and National Stock Exchange India

2017 Forays into Northern India with commissioning of super-speciality hospital in Kakriyal, Jammu

2017 Enters into agreement for healthcare services with around 300 capacity bedded Dharamshila Hospital & Research Centre

2017 Acquires near completed ~230 bedded hospital in Gurugram (NewRise Healthcare) from Panacea Biotec

2017 Forays into Mumbai to with superspeciality Children’s Hospital - first of its kind in NH network

Nov-17 Proposes to buy back 71.4% outstanding shares in Health City Cayman Islands held by Ascension Health Ventures LLC, US for US$ 32.26 million to increase

Narayana Hrudalaya's effective stake to 100% in Health City Cayman Islands

Source: Company, ICICIdirect.com; Research

Exhibit 4: Key players in Indian hospital industry (FY17) s

Company No of Beds* Presence

Apollo Hospitals 6,997

Chennai, Madurai, Hyderabad, Karur, Karim Nagar, Mysore, Visakhapatnam, Bilaspur, Aragonda, Kakinada, Bengaluru, Delhi, Noida,

Kolkata, Ahmedabad, Mauritius, Pune, Raichur, Ranipet, Ranchi, Ludhiana, Indore, Bhubaneswar, Dhaka, Bacheli, Bellary, Goa,

Lavasa, Nashik, Nellore, Trivuannamalai, Trichi

Aravind Eye Hospitals 3,649 Theni, Tirunelveli, Coimbatore, Puducherry, Madurai, Amethi, Kolkata, Dindigul, Tirupur, Salem, Tuticorin, Udumalpet

CARE Hospitals 2,100 Hyderabad, Vijayawada, Nagpur, Raipur, Bhubaneswar, Surat, Pune, Visakhapatnam, Jabalpur, Raigarh

Fortis Healthcare 4,700

Mumbai, Bengaluru, Kolkata, Mohali, Noida, Delhi, Amritsar, Raipur, Jaipur, Chennai, Kota, Faridabad, also the company present in

Singapore, Dubai, Mauritius and Sri Lanka

Max Hospitals 2,016 Delhi, NCR, Punjab, Uttarakhand

Manipal Group of Hospitals 4,900 Udupi, Bengaluru, Manipal, Attavar, Mangalore, Goa, Tumkur, Vijaywada, Kasaragod, Visakhapatnam

Narayana Health 5,799

Ahmedabad, Bengaluru, Berhampore, Davangere, Dharwad,Durgapur, Guwahati, Hyderabad, Jaipur, Jamshedpur, Kolar, Kolkata,

Kuppam, Mahuva, Mysore, Raipur, Shimoga, Bellary, Palanpur, Mumbai

Source: IBEF.org, ICICIdirect.com; Research, * Operational Beds

Page 6 ICICI Securities Ltd | Retail Equity Research

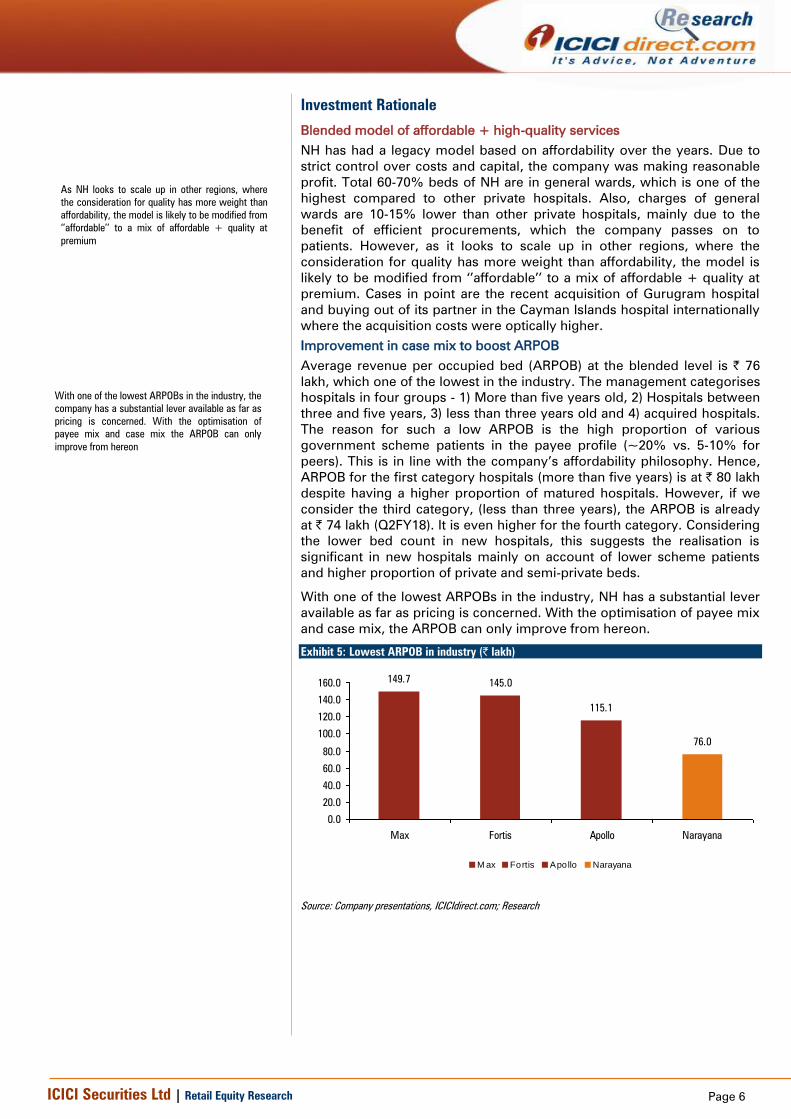

Investment Rationale

Blended model of affordable + high-quality services

NH has had a legacy model based on affordability over the years. Due to

strict control over costs and capital, the company was making reasonable

profit. Total 60-70% beds of NH are in general wards, which is one of the

highest compared to other private hospitals. Also, charges of general

wards are 10-15% lower than other private hospitals, mainly due to the

benefit of efficient procurements, which the company passes on to

patients. However, as it looks to scale up in other regions, where the

consideration for quality has more weight than affordability, the model is

likely to be modified from ‘’affordable’’ to a mix of affordable + quality at

premium. Cases in point are the recent acquisition of Gurugram hospital

and buying out of its partner in the Cayman Islands hospital internationally

where the acquisition costs were optically higher.

Improvement in case mix to boost ARPOB

Average revenue per occupied bed (ARPOB) at the blended level is | 76

lakh, which one of the lowest in the industry. The management categorises

hospitals in four groups - 1) More than five years old, 2) Hospitals between

three and five years, 3) less than three years old and 4) acquired hospitals.

The reason for such a low ARPOB is the high proportion of various

government scheme patients in the payee profile (~20% vs. 5-10% for

peers). This is in line with the company’s affordability philosophy. Hence,

ARPOB for the first category hospitals (more than five years) is at | 80 lakh

despite having a higher proportion of matured hospitals. However, if we

consider the third category, (less than three years), the ARPOB is already

at | 74 lakh (Q2FY18). It is even higher for the fourth category. Considering

the lower bed count in new hospitals, this suggests the realisation is

significant in new hospitals mainly on account of lower scheme patients

and higher proportion of private and semi-private beds.

With one of the lowest ARPOBs in the industry, NH has a substantial lever

available as far as pricing is concerned. With the optimisation of payee mix

and case mix, the ARPOB can only improve from hereon.

Exhibit 5: Lowest ARPOB in industry (| lakh)

149.7145.0

115.1

76.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Max Fortis Apollo Narayana

M ax Fortis Apollo Narayana

Source: Company presentations, ICICIdirect.com; Research

As NH looks to scale up in other regions, where

the consideration for quality has more weight than

affordability, the model is likely to be modified from

‘’affordable’’ to a mix of affordable + quality at

premium

With one of the lowest ARPOBs in the industry, the

company has a substantial lever available as far as

pricing is concerned. With the optimisation of

payee mix and case mix the ARPOB can only

improve from hereon

Page 7 ICICI Securities Ltd | Retail Equity Research

More focus on fast growing international patients

Over the years, India has grown to become a top notch destination for

international patients as it scores high over a range of factors that

determine the overall quality of care. From quality of therapy, range of

procedural and treatment options, infrastructure and availability of skilled

manpower to performing any medical procedure with zero waiting time

and lastly availability of generic drugs, the list of benefits in travelling for

medical treatment in India goes on. This is especially for costly and

delicate surgeries like coronary bypass, kidney and liver transplant, hip

replacement, dental services, cosmetic surgery and bariatric surgery.

Indian hospitals are offering standard services at comparatively low costs.

Statistics reveal that treatment of major surgeries in India cost ~20% of

those in developed countries.

Exhibit 6: Competitive surgery rates

Treatment (US$) US UK Thailand Singapore India

Heart Surgery 100,000 40,000 14,000 15,000 5,000

Bone marrow transplant 250,000 290,000 62,000 150,000 30,000

Liver transplant 300,000 200,000 75,000 140,000 45,000

Knee replacement 48,000 50,000 8,000 25,000 6,000

Source: CRISIL Report, ICICIdirect.com; Research

NH’s network has eight hospitals with domestic accreditation from NABH

while three hospitals have international accreditation from Joint

Commission International (JCI). These accreditations are an important

consideration for international patients. These patients are covered under

insurance while payments are guaranteed by foreign governments. Hence,

this is one of the most lucrative payee categories. The company has

official tie-ups with several major international medical insurance

companies to facilitate international patients.

‘International patients’ as a payee category are the highest in terms of

realisation and are growing at a faster rate vis-à-vis other categories. This

will further improve the blended ARPOBs as the product mix improves.

Similarly, with higher incremental proportion of international patients and

those covered under private insurance and corporate schemes, the pie of

government schemes is steadily coming down. In turn, this will improve

the ARPOBs.

NH has witnessed strong growth in the contribution of international

patients to total revenues, which has grown from 4.8% in FY16 to 9% in

Q2FY18.

Exhibit 7: Percentage of international patients

5%

8%

10%

9%

0%

2%

4%

6%

8%

10%

12%

FY16 FY17 Q1FY18 Q2FY18

Source: Company, ICICIdirect.com; Research

Exhibit 8: Lower schemes patients’ contribution

23%25%

21%

18% 18%

0%

5%

10%

15%

20%

25%

30%

FY13 FY14 FY15 FY16 FY17

Source: Company, ICICIdirect.com; Research

The NH network has eight hospitals with domestic

accreditation from NABH while three hospitals

have international accreditation from JCI. It has

witnessed strong growth in the contribution of

international patients to total revenues, which has

grown from 4.8% in FY16 to 9% in Q2FY18

Page 8 ICICI Securities Ltd | Retail Equity Research

‘’Asset right model’’ to improve return ratios

Over the years, the company has endeavoured to focus on opportunities

where it need not have to own out and out assets. The brick-and-mortar in

most cases is owned by like-minded partners. Under this model, the

company engages with partners who invest in land and building while it

takes care of medical equipment and the hospital management on a

revenue share basis. This is why NH’s balance sheet is one of the lightest

among peers.

Exhibit 9: Asset right model explained s

Engagement Framework Comments Number of Units

Number of

Operational

Beds

Gross Block +

CWIP (| cr)

Capital Cost per

Bed (| cr)

Owned Or Long-Term /Perpetual Lease

Owns and operates on freehold basis or land

taken on long-term / perpetual lease 8 Hospitals 2607 961.5 0.37

Revenue Share / Rentals

Operates and pays a revenue share / rent to

owner of the hospital premises 10 Hospitals 1817 318.0 0.18

Public-Private Partnership

Operates with nominal investment in partnership

with public entities 2 Hospitals 297 16.8 0.06

Managed Hospitals

Provides healthcare services to third parties for

a management fee 4 Hospitals 720 - -

Heart Centres

Runs cardiac sciences’ department out of 3rd

party hospitals and pays revenue share

7 Heart Centres

and 1 Clinic 386 51.1 0.13

Source: Company Annual Report, ICICIdirect.com; Research,

In the past 10 years, NH has added 22 hospitals, which comprises 5226

operating beds majority were under assets right model. As a result of this

strategy, NH’s average effective capital cost per operational bed in FY17

was just | 27 lakh against peer’s average of ~| 90 lakh. This has primarily

led to one of the lowest leverages on the balance sheet (net D/E of 0.2x) in

the private hospitals space.

Exhibit 10: Lowest average effective cost per bed (| lakh)

55

27

87

52

0

10

20

30

40

50

60

70

80

90

100

Apollo Hospitals Narayana Max India Healthcare Global

Apollo Hospitals Narayana Max India Healthcare Global

Source: Company presentations, ICICIdirect.com; Research, *Calculated on operational beds

The company engages with partners who invest in

land and building while it takes care of medical

equipment and hospital management on a revenue

share basis. This is why NH’s balance sheet is one

of the lightest among peers

Owning an asset right model, NHL’s average

effective capital cost per operational bed in FY17

was just | 27 lakh against peer’s average of ~|

90 lakh. This has primarily led to one of the lowest

leverage on the balance sheet (net D/E of 0.2x) in

the private hospitals space

Page 9 ICICI Securities Ltd | Retail Equity Research

Exhibit 11: Lowest D/E ratio (x)

0.5

0.3

0.8

0.2

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Max Fortis Apollo Narayana

Max Fortis Apollo Narayana

Source: Company presentations, ICICIdirect.com; Research

However, the management has maintained a flexible approach in this

regard. Thus, it also owns some hospitals with out and out ownership

where the opportunity is right. A case in point in this regard is the latest

acquisition of Gurugram based multi-speciality hospital NewRise

Healthcare from Panacea Biotech for | 180 crore. In this case, the cost of

acquisition per bed is almost 2.9x the blended cost of all beds for the

company. This acquisition is part of the long term strategy of penetrating

the northern market, especially the area in and around the NCR, which is

dominated by high-end players. Here, the strategy is to improve the

blended ARPOB by keeping procedure rates at a higher level vis-à-vis the

company rates but below levels charged by existing big players.

Similarly, the recent buy-out of Cayman Island based Health City hospital is

another example of higher per bed valuation where the cost per bed works

out to as high as | 5.2 crore per operating bed. Overall outgo in this deal

was ~| 208 crore. However, being an international asset, the revenue

earning capability of this hospital is also superior - ARPOB of ~| 12 crore.

However, as per the management’s own assertion, this strategy is more

opportunistic than a trend. Barring a few such instances, the focus will be

to maintain the asset right model.

Due to this focus on the balance sheet and likely improvement in average

realisation per operating bed (ARPOB) by optimising the case mix, we

expect an improvement in RoCE from 12.5% to ~19% in FY17-20E.

Exhibit 12: Improvement in ARPOB

4852

5864

76

88.6

95.5

103.1

0

10

20

30

40

50

60

70

80

90

100

110

120

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(|

crore)

ARPOB (| Lakh)

Source: Company, ICICIdirect.com; Research

Exhibit 13: Improvement in RoCE

8.27.5

10.7

5.9

8.8

12.511.9

14.4

18.7

0

5

10

15

20

FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(%

)

RoCE (%)

Source: Company, ICICIdirect.com; Research

Page 10 ICICI Securities Ltd | Retail Equity Research

Cost control, extensive use technology; instances of efficient cost

management

In the backdrop of lower ARPOBs, the company has over the years

implemented and followed some unique cost control measures right from

construction of hospital buildings to sourcing equipment and

consumables. Extensive use of technology for cost reduction is another

differentiator for the company.

In most of its hospitals, it enters into an agreement with the vendors of the

diagnostic machines for blood tests whereby it pays for reagents rather

than buying a machine outright. Given the sheer volume in the system, the

vendor still makes a profit just by selling reagents while the hospital saves

on the cost of the machine.

NH is one of the first few hospitals to switch to digital X-rays to save the

cost of film. It uses disposable gowns, drapes and sutures at almost half

price by sourcing the same locally.

Even the design of most of the owned hospitals has been meticulously

planned to optimise space utilisation, which brings down the cost per bed.

As mentioned earlier, ~70% of beds are general wards that allow fitting in

more beds thus bringing the cost per bed down.

In most NH hospitals, the junior doctors, nurses and technicians handle the

routine of preparing the patient for surgery and closing up after the

surgery is complete. Senior cardiac surgeons enter the theatre to perform

complex procedures only after the chest has been opened and the heart is

ready to be operated on. This way the hospital ensures its cardiac

surgeons are able to perform two to three procedures a day compared to

the average of one a day at other hospitals. The hospital in Bengaluru, for

instance, does up to 32-35 surgeries a day and has the infrastructure to

support almost 60 operations a day.

Electricity costs are controlled by installing ACs only in operational

theatres. All other rooms are naturally ventilated. A case in point is a 300-

bed hospital in Mysuru, which was built in 2012 in association with L&T.

Built in eight months on a | 40 crore budget, it is one of the cheapest super

specialty hospital ever built in India, with the cost-per-bed coming to about

| 13-14 lakh. Made of pre-fabricated materials, the building is on a single

level, thus doing away with the need for lifts. There is also no air-

conditioning, except in operation theatres.

To reduce the cost related to intensive care units (ICU), the company has

deployed software called I-care from Cognizant Technologies to help

streamline post-operation cardiac ICU care. Using the software, medical

staff will be able to monitor ICU patients from remote locations.

NH has partnered Cisco to offer affordable remote diagnostic capabilities.

This digital telemedicine solution would deliver advanced specialised

healthcare services remotely in various parts of the country. In the

process, this would bring the company goodwill and reputation.

NH has also adapted to the latest trends in surgeries such as laparoscopy,

robotic surgery, etc. These procedures generate higher realisation and

minimal patient stay due to minimum invasive procedures and lower risks

of hospital related infections. Similarly, it can be performed from remote

locations and with a leaner medical team. The company has performed

more than 150 robotic surgeries within just 10 months since the

introduction in FY17.

The company has, over the years, implemented

and followed some unique cost control measures

right from construction of hospital buildings to

sourcing equipment and consumables. Extensive

use of technology for cost reduction is another

differentiator for the company

The company has performed more than 150 robotic

surgeries within just 10 months since introduction

in FY17

Page 11 ICICI Securities Ltd | Retail Equity Research

Exhibit 14: Common size statement- consistency in cost management

Income Statement Variables FY15 FY16 FY17 FY18E FY19E FY20E

Net Sales 100% 100% 100% 100% 100% 100%

RM 25% 24% 23% 21% 21% 21%

Gross Profit 75% 76% 77% 79% 79% 79%

Employee exp 20% 21% 20% 18% 18% 18%

Professional Fees to Doctors 19% 20% 21% 21% 21% 21%

Others Expenditure 26% 25% 24% 30% 29% 27%

Operating Profit (EBITDA) 9% 11% 12% 11% 12% 13%

Adjusted PAT 0% 2% 4% 4% 5% 7%

Source: Company Annual Reports, ICICIdirect.com; Research

Government drive on affordability favours NH’s cost efficient, affordable

model

Growing government intervention with regard to pricing of products and

procedures (recent drive against stent and implant pricing) has emerged as

a major overhang for the sustainability of many private specialty and super

specialty hospital chains. In such a tough scenario, we believe NH, with its

cost efficient and predominantly affordable model is well placed to bring

value to the table. As discussed earlier, both the ARPOB and cost per bed

parameters are lowest in the company’s case. Its flexible model allows it to

modify its payee profile as per the requirement. NH’s track record of

providing standard quality, affordable healthcare services to the broader

population has positioned the company as a partner-of-choice for a

number of state governments that are seeking to improve and expand

their local healthcare infrastructure and accessibility to healthcare services.

Some of the related examples include super specialty hospital in

Guwahati, which was commissioned in December 2013, in partnership

with the Government of Assam and the multispecialty hospital in Vaishno

Devi in partnership with the Vaishno Devi Board.

Exhibit 15: Treatment wise comparison s

Therapy Therapy ALOS NABH Non-NABH India Fortis Apollo NH

Angiography daycare 11.5 13.2 12.0-14.0 35-40 15-35 7.5-15

Angioplasty (without implant) 2 days 80 92 65-75 125-200 90-180 55-80

Coronary bypass 7-8 days 127 146 300-400 350-500 280-360 100-250

Total Hip replacement 3-4 days 79 91 150-200

Total Knee replacement (without implant) 110 127 100-150 200-250 150-220 50-100

Intensity Modulated radiotherapy (IMRT) daycare 101 116 125-150

IGRT (Image guided radiotherapy) 147 169 175-200

Craniotomy and evacuation of Hematoma 8-10 days 50 58 85-110

Excision of Brain tumours 45 51 185-210

Cataract Extraction 1 day 13.5 15.5 13-15 30-40 45-50

Glaucoma surgery 6.9 7.9 16-18

Normal delivery 3 days 8 9.2 20-35 80-130 45-110 20-50

Caesarian section 4 days 14 16 40-60 90-130 70-120 35-65

Cholecystectomy Open 6 days 10 12 30-60 50-110 65-115 50-65

Cholecystectomy Laparoscopic 5 days 40-65 90-200 70-130 50-75

Appendectomy Open 5 days 8 9 30-50 50-140 70-100 55-75

Appendectomy Laparoscopic 4 days 40-80 60-140 80-115 50-85

Kidney (without implant) 10 days 200 230 480-550 480 800

Liver (without implant) 20 days 2250 2700

Costs (| '000)

Transplant

Neurosurgery

Opthalmology

Gynaecology

General Surgery

CGHS (Delhi/NCR)

Oncology

Cardiac

Orthopedics

Source: ICICI Lombard, CRISIL, Industry reports, ICICIdirect.com; Research, NABH- National Accreditation Board for Hospitals & Healthcare, CGHS-Central Government Health Scheme

Both the ARPOB and cost per bed parameters are

lowest in NH’s case. Its flexible model allows it to

modify payee profile as per the requirement. NH’s

track record of providing standard quality,

affordable healthcare services to the broader

population has positioned the company as a

partner-of-choice for a number of state

governments that are seeking to improve and

expand their local healthcare infrastructure and

accessibility to healthcare services

Page 12 ICICI Securities Ltd | Retail Equity Research

NHP 2017 - Government recognition for private sector capability

National Health Policy (NHP) 2017 has effectively charted out three clear

objectives - progressively achieve universal health coverage, reinforce

trust in public health care system and complement the growth of the

private healthcare sector with public health goal. The roadmap to involve

the hitherto untapped private sector to address the shortcomings of

government driven health deliveries is by far the most important outcome

of the new policy. It does acknowledge the extremely poor spending by

the state and inability to cover the entire spectrum of healthcare needs

through increased public investment, which has led to a rise in the out-of-

pocket expenditure and consequent impoverishment. It advocates a shift

from a primary focus on garnering additional financial resources from the

private sector or subsidising it, to an approach in which there is a well-

defined service delivery partnership between the government, as a

purchaser, and the private sector, as a provider.

The policy explains the need for coordination with private sector

enterprises by giving statistical instances. The private sector accounts for

90% of all hospitals (up from 8% in 1947), 60% of all beds, and 80-85% of

all doctors. Over 70% of an ailing population in rural areas and almost 80%

in urban areas utilise private facilities. As much as 75% of outpatient (OPD)

care is exclusively private while more than 55% of inpatient (IPD) care is

sought from private hospitals in India.

We believe, among all private players, NH is probably best suited to utilise

this opportunity as the company is already managing two hospitals under

the PPP model besides dealing with various government scheme patients.

Although quantification of this opportunity will be difficult at this stage, the

head start itself can count on huge volume.

Favourable macroeconomic factors

Significant infrastructural gaps persist in the Indian hospital industry. The

bed availability in India was at seven per 10,000 in 2012, significantly lower

than the WHO guideline of 30 beds per population of 10,000. Out of pocket

expenditure on healthcare in India is ~60%, one of the highest in the

world. On the other hand, India has among the lowest health insurance

penetration among developing countries with just 20% penetration.

Demand-supply mismatch with a combination of macroeconomic factors,

including changing demographics, increasing affluence of the Indian

population, greater health awareness, rising incomes, changes in the

disease profile (towards lifestyle-related ailments) and rising penetration of

health insurance are likely to lead to an increase in demand for quality

healthcare services.

We believe, among all private players, NH is

perhaps the best suited candidate to utilise this

opportunity as the company is already managing

two hospitals under PPP model besides dealing

with various government scheme patients

Significant infrastructural gaps persist

1) lower bed availability (seven per 10000)

2) 60% out of pocket expenditure, highest in

world

3) Lowest health insurance penetration (20%)

Page 13 ICICI Securities Ltd | Retail Equity Research

Exhibit 16: Inadequate bed infrastructure in India

63

3634

26 25

7

0

10

20

30

40

50

60

70

Europe Brazil US World

Average

China India

Source: IBEF.Org, ICICIdirect.com; Research

Exhibit 17: Highest out-of-pocket spend on healthcare (%)

67.9

14.811.0

52.6

33.7

59.062.4

11.0 9.7

54.8

35.332.0

0

10

20

30

40

50

60

70

80

India US Uk Singapore Malaysia China

2014 2010

Source: Shalby RHP, World Bank 2015, ICICIdirect.com; Research

Exhibit 18: Health Insurance premium per capita (US$; 2016)

3.6

57.9 44

110.9

567

0

100

200

300

400

500

600

India Singapore China UK US

India Singapore China UK US

Source: ICICI Lombard RHP; CRISIL 2016, ICICIdirect.com; Research

Exhibit 19: Break-up of health insurance in India

Government

Scheme, 28.7 crore,

80%

Private insurance,

7.2 crore, 20%

Source: ICICI Lombard RHP; CRISIL 2016, ICICIdirect.com; Research

Page 14 ICICI Securities Ltd | Retail Equity Research

Financials

Revenues expected to grow at CAGR of 17% in FY17-20E

Gross revenues grew at a CAGR of 22.3% over FY13-17 to | 1878 crore on

account of: 1) 1620 bps increase in occupancy rate to 61.0% followed by

2) 12.2% increase in ARPOB to | 76 lakh per share and 3) 12% increase in

operational beds to 5932. However, commercialising new hospitals

(Mumbai, Jammu and Delhi) as well as government regulations will impact

the near term ARPOB and occupancy rate. Over FY17-20E, we expect NH’s

revenues to grow 17.3% YoY to | 3032 crore mainly due to an

improvement in occupancy rate and ARPOB in less than five years

hospitals and Cayman.

Exhibit 20: Revenue (gross) growth drivers

1363.9

3021.5

224.7 84.2 94.3 0.0

165.2 71.9

235.9 33.2

13.1

218

16.9

-120.7218.7

1878.2

402.8

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

FY15 (

Revenue)

Hospit

al (>

5 y

rs)

Hospit

al (3-5 y

ears)

Hospit

als

(<

3 y

ears)

Acquir

ed H

ospit

als

Heart C

entres

HC

CI (C

aym

an)

Others

FY17

Hospit

al (>

5 y

rs)

Hospit

al (3-5 y

ears)

Hospit

als

(<

3 y

ears)

Acquir

ed H

ospit

als

Heart C

entres

HC

CI (C

aym

an)

Others

FY20

Source: Company, ICICIdirect.com; Research

Exhibit 21: ARPOB

4852

5864

76

88.6

95.5

103.1

0

10

20

30

40

50

60

70

80

90

100

110

120

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(|

crore)

ARPOB (| Lakh)

Source: Company, ICICIdirect.com; Research

Exhibit 22: Revenue break-up

3815

46784239 4144

4721 48005090 5210

45%48%

53% 54%

61.0%64%

67%68%

0

1000

2000

3000

4000

5000

6000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(|

crore)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Operating Beds Occupancy Rate (%)

Source: Company, ICICIdirect.com; Research

EBITDA margins expected to expand 137 bps over FY17-20E

EBITDA margins contracted 51 bps to 12.2% over FY13-17 mainly due to

addition of new hospitals. The company has added ~18 hospitals over

FY11-17. We believe FY18 EBITDA margins will remain under pressure

mainly due to the impact of government regulation on cardiac stents &

implants and loss at newly commissioned hospitals. However, a gradual

improvement in new hospital margins and occupancy rate is likely to

improve EBITDA margins by 137 bps in FY17-20E. We expect EBITDA in

value terms to grow 21% to | 410 crore in FY17-20E.

Over FY17-20E, we expect NH’s revenues to grow

17.3% YoY to | 3032 crore mainly due to an

improvement in occupancy rate and ARPOB in less

than five years hospitals and Cayman

EBITDA margin expected to expand ~137 bps in

FY17-20E mainly due to improvement in new

hospitals margins and occupancy rate

Page 15 ICICI Securities Ltd | Retail Equity Research

Exhibit 23: EBITDA & EBITDA margins

83.3

122.7 123.7

174.6

228.9

254.3

311.4

409.7

9.9

11.2

9.1

10.8

12.2

11.211.7

13.6

0

50

100

150

200

250

300

350

400

450

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(|

crore)

0

2

4

6

8

10

12

14

16

(%

)

EBITDA EBITDA Margins (%)

Source: Company, ICICIdirect.com; Research

Net profit expected to increase 34% CAGR in FY17-20E

Net profit grew at 26% CAGR over FY13-17 to | 84 crore mainly due to a

robust operational performance. We expect net profit to increase at 34%

CAGR in FY17-20E mainly on the back of robust operational performance

and lower interest cost.

Exhibit 24: Net profit trend

30.8 33.8 37.332.2

84.489.0

136.2

203.4

-5.8

-50

0

50

100

150

200

250

FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(|

crore)

Net Profit

Source: Company, ICICIdirect.com; Research

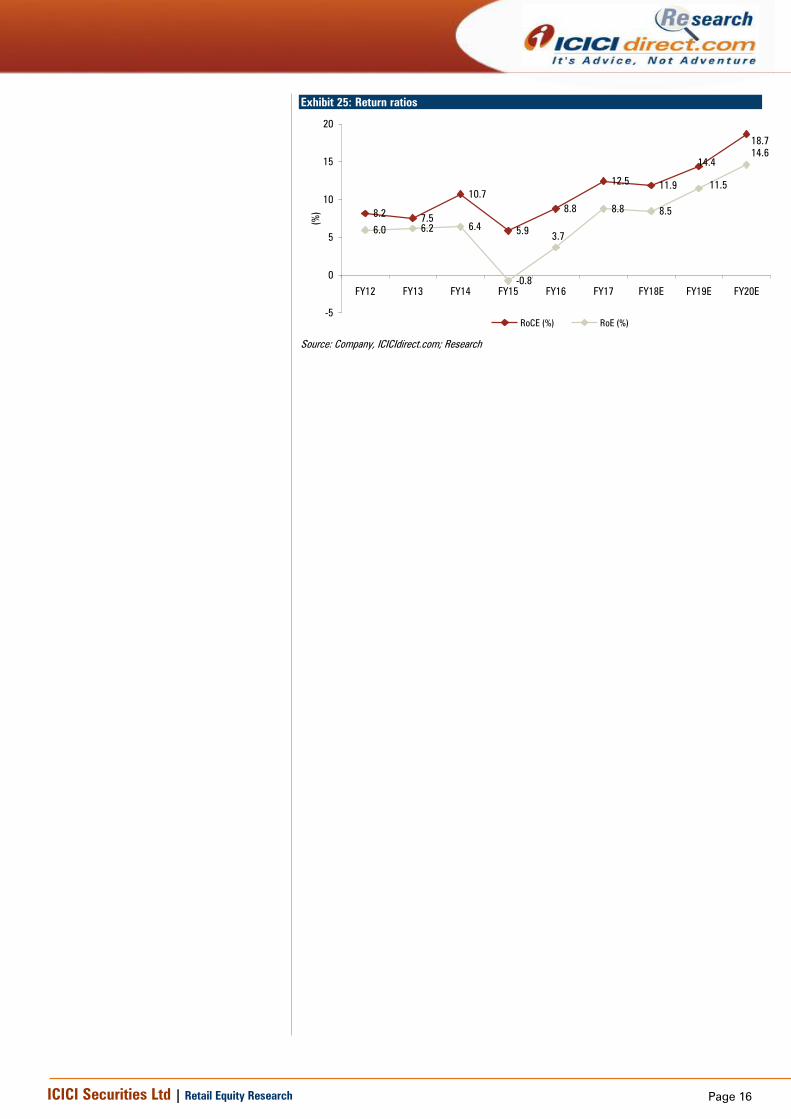

Improvement in return ratios

We expect RoCE to improve 620 bps to 18.7% in FY17-20 due to lower

base improvement in ARPOB and lower pace of gross block addition. Our

back of the envelope calculation shows that incremental capital employed

of ~| 432 crore can generate 38% ROCE during FY17-20E. (Assuming no

further gross block addition over and above the estimates.)

25.7% CAGR

34.1% CAGR

Net profit is expected to increase at 34% CAGR in

FY17-20E mainly on the back of a robust

operational performance

Page 16 ICICI Securities Ltd | Retail Equity Research

Exhibit 25: Return ratios

8.27.5

10.7

5.9

8.8

12.511.9

6.0 6.2 6.4

-0.8

8.8 8.5

14.4

18.7

3.7

11.5

14.6

-5

0

5

10

15

20

FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(%

)

RoCE (%) RoE (%)

Source: Company, ICICIdirect.com; Research

Page 17 ICICI Securities Ltd | Retail Equity Research

Risk & concerns

Government regulations

In the past six months, the government has voluntarily shifted cardiac

stents and knee implants to the national list of essential medicines (NLEM)

to cap the prices of both devices. The government has also put a

restriction of six months on hospitals for changing procedural prices. NH

derived 48% of FY17 revenues from cardiac treatment. Although NH’s

model is low cost, the disturbance in supplies on account of shortage and

uncertainty of stent availability has a direct impact on procedural revenues.

The management expects | 40-45 crore of loss in FY18 due to cardiac

stent price regulation. Of late, the government has also brought knee

implants under the NLEM ambit. These kinds of interventions are

detrimental to revenues if the government also starts regulating

procedures. Recently, two state governments, West Bengal and Karnataka

passed laws capping the prices of select private healthcare services.

PPP model in healthcare may be unviable with CGHS rates

NHP 2017 advocates active participation of private healthcare providers

with the government acting as service purchaser. The Niti Aayog’s report

on PPP gives details about the rates that can be charged to patients who

are not covered by National Health Protection Schemes (NHPS), Rashtriya

Swasthya Bima Yojana (RSBY), Central Government Health Scheme

(CGHS) or state insurance schemes. It proposes that where NHPS, RSBY

and state insurance schemes are not applicable, patients cannot be

charged over CGHS rates. Note that CGHS rates are substantially lower

than even the average rates of different procedures. Hence, any player

entering into these kind arrangements will face a substantially longer

payback achievement.

Delay in ramp-up of new facilities

Recently, the company started hospitals in Jammu, Mumbai and

Dharamshila in the NCR region. The company is also planning to

commission its newly acquired facility at Gurugram in Q4FY18. It has

reported a contraction in margins in FY17 and Q1FY18 mainly due to a loss

in new hospitals. We have already factored in the initial loss due to

commissioning of new hospitals. However, any further delay beyond our

expectation will further impact overall financials.

Concentrated in few hospitals and treatments

The company’s three key facilities, Narayana Institute of Cardiac Sciences

(NICS), Mazumdar Shaw Medical Centre (MSMC) and Rabindranath Tagore

International Institute of Cardiac Sciences (RTIICS) together contribute

more than half of the company’s overall revenues. Any material impact on

any of these facilities due to a reduction in patient footfall, reputational

harm, liabilities on account of medical negligence and loss due to natural

calamities and increased competition could significantly impact overall

revenues and profitability.

Page 18 ICICI Securities Ltd | Retail Equity Research

Valuation

We expect revenues, EBITDA and PAT to grow at a CAGR of 17%, 21%

and 34% in FY17-20E, respectively. This is expected to be driven by an

increase in occupancy ratio, mainly of less than five year’s hospitals and an

improvement in the case mix. On the EBITDA margin front, we expect near

term margins to remain under pressure mainly due to government

regulations and loss from new hospitals.

In a conducive but challenging space of Indian healthcare delivery,

plagued by longer gestation periods, low operating margin, leveraged

balance sheets and low return ratios, we believe NH is best placed among

peers to sail through. Its legacy model is based on affordability. Hence,

conscious efforts towards cost & capital control are embedded in the

management’s long term strategy. This becomes even more pertinent in

the backdrop of incremental government intervention via schemes and

control over procedures & products. On the other hand, it is also

determined to improve ARPOB by improving case mix, occupancies, thus

fine-tuning affordability with profitability. We arrive at an SOTP target price

of | 340 by valuing the matured hospitals and Cayman Islands hospital at

12x FY20E EV/EBITDA, other hospitals at 1.5x FY20E EV/Sales and other

businesses at 1.0x FY20E EV/sales.

Exhibit 26: Valuation

Particulers Valuation Matrix Multiple (x) Enterprise value (| cr)

Hospital (Matured) EV/EBITDA 12.0 4514.8

Cayman EV/EBITDA 12.0 923.5

Hospital (Others) EV/Sales 1.5 1385.2

Other Business EV/Sales 1.0 186.0

Net Debt FY20E (| cr) 29.9

EV (| cr) 6979.6

No of shares (cr) 20.4

Per Share Value (|) 340.0

Source: ICICIdirect.com; Research

Exhibit 27: Domestic peers comparison (FY17)

FY17 (| crore) Market Cap

No. of

operating

beds Revenue

EBITDA

margin EBITDA

Asset

Turnover EV/Sales EV/ EBITDA

Sales/Bed (|

lakhs)

EV/Bed (|

lakhs)

ARPOB (|

Lakh) ALOS

Apollo Hospitals (Hospital segment)* 11397.6 6997 4163.3 17.1 712.2 1.0 3.3 19.5 59.5 198.9 115.1 4.0

Narayana Hrudayaalaya 5995.0 5932 1895.6 13.0 246.3 1.6 3.2 24.9 32.0 103.5 76.0 4.0

Fortis (Hospital segment)* 4654.3 4700 3712.0 14.7 545.0 NA 1.8 11.9 79.0 138.5 145.0 3.6

Max India (Hospital segment)* 2654.0 2330 2567.0 10.9 281.0 1.1 1.5 13.4 110.2 161.2 149.7 3.2

HCG 2515.0 1364 700.1 15.0 105.0 0.9 3.9 26.3 51.3 202.5 106.3 2.9

* Market caps are implied by separating other businesses Source: Bloomberg, ICICIdirect.com; Research

Exhibit 28: Global peers comparison

Company Name Country Market Cap EV Revenues EBITDA EBITDA Margin PAT FCF D/E ROCE EV/EBITDA PE

Ramsay Health Care Ltd Australia 10705.9 13861.9 6326.8 884.8 14.0% 328.1 416.2 194.5 18.2 13.8 30.2

IHH Healthcare Bhd Malaysia 11404.7 12531.5 2420.7 525.2 21.7% 148.0 383.9 34.1 5.1 21.2 49.0

HCA Healthcare Inc United States 29464.2 62361.0 41490.0 8152.0 19.6% 2890.0 1883.5 NA 24.3 7.7 12.4

DaVita Inc United States 11168.5 20565.0 14745.1 2614.8 17.7% 879.9 118.4 196.0 28.2 8.2 16.2

Universal Health Services Inc United States 10027.1 14576.3 9766.2 1698.0 17.4% 702.4 631.9 91.8 18.1 8.3 14.5

US$ million US$ million

Source: Bloomberg, ICICIdirect.com; Research

Page 19 ICICI Securities Ltd | Retail Equity Research

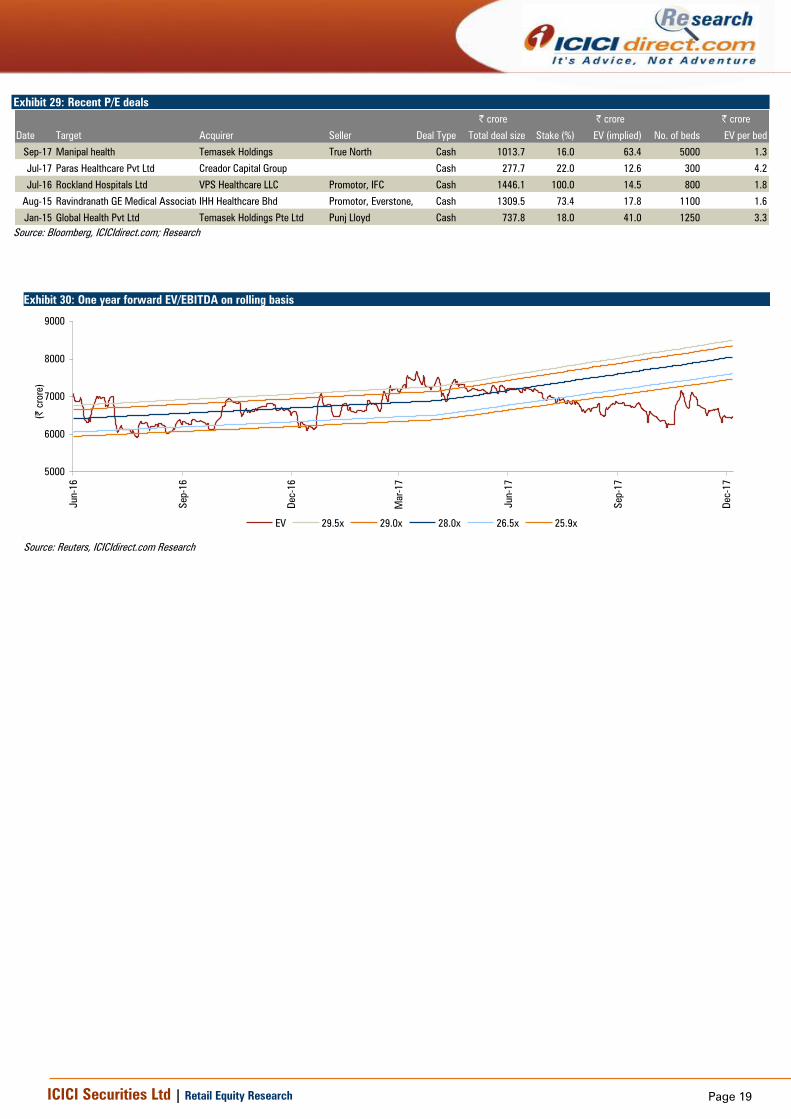

Exhibit 29: Recent P/E deals

| crore | crore | crore

Date Target Acquirer Seller Deal Type Total deal size Stake (%) EV (implied) No. of beds EV per bed

Sep-17 Manipal health Temasek Holdings True North Cash 1013.7 16.0 63.4 5000 1.3

Jul-17 Paras Healthcare Pvt Ltd Creador Capital Group Cash 277.7 22.0 12.6 300 4.2

Jul-16 Rockland Hospitals Ltd VPS Healthcare LLC Promotor, IFC Cash 1446.1 100.0 14.5 800 1.8

Aug-15 Ravindranath GE Medical Associates Pvt LtdIHH Healthcare Bhd Promotor, Everstone, IFC Cash 1309.5 73.4 17.8 1100 1.6

Jan-15 Global Health Pvt Ltd Temasek Holdings Pte Ltd Punj Lloyd Cash 737.8 18.0 41.0 1250 3.3

Source: Bloomberg, ICICIdirect.com; Research

Exhibit 30: One year forward EV/EBITDA on rolling basis

s

5000

6000

7000

8000

9000

Jun-16

Sep-16

Dec-16

Mar-17

Jun-17

Sep-17

Dec-17

(|

crore)

EV 29.5x 29.0x 28.0x 26.5x 25.9x

Source: Reuters, ICICIdirect.com Research

Page 20 ICICI Securities Ltd | Retail Equity Research

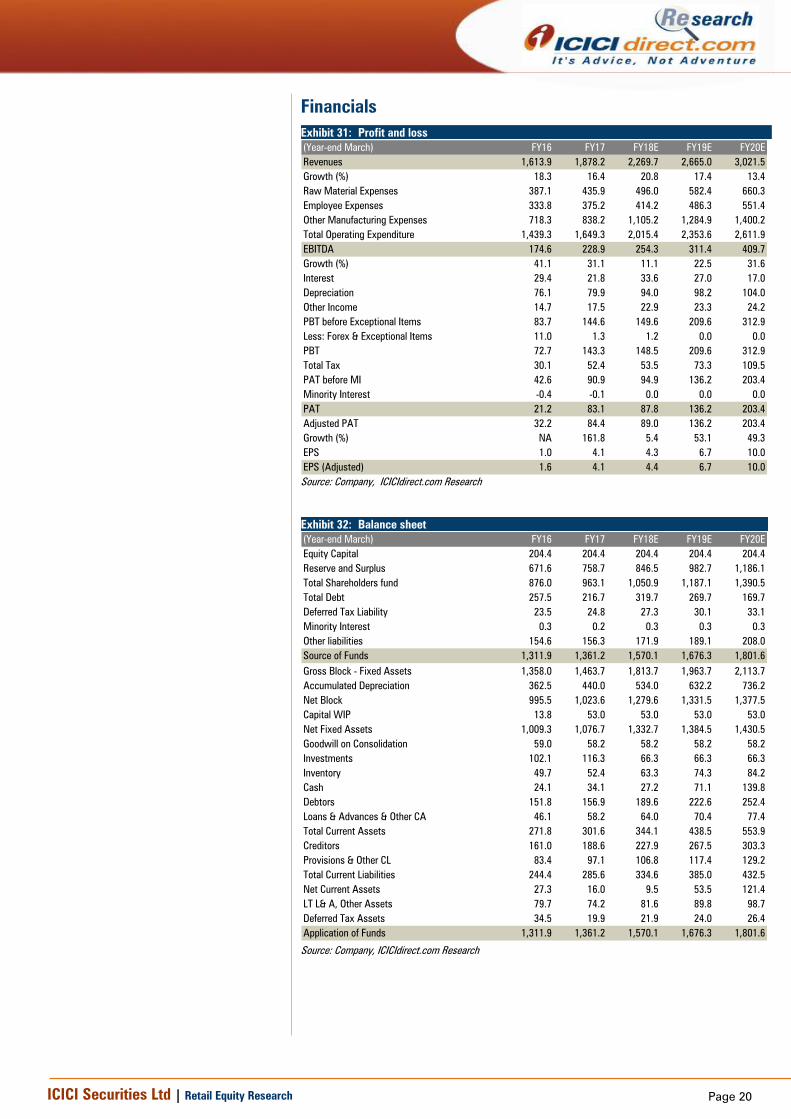

Financials

Exhibit 31: Profit and loss

(Year-end March) FY16 FY17 FY18E FY19E FY20E

Revenues 1,613.9 1,878.2 2,269.7 2,665.0 3,021.5

Growth (%) 18.3 16.4 20.8 17.4 13.4

Raw Material Expenses 387.1 435.9 496.0 582.4 660.3

Employee Expenses 333.8 375.2 414.2 486.3 551.4

Other Manufacturing Expenses 718.3 838.2 1,105.2 1,284.9 1,400.2

Total Operating Expenditure 1,439.3 1,649.3 2,015.4 2,353.6 2,611.9

EBITDA 174.6 228.9 254.3 311.4 409.7

Growth (%) 41.1 31.1 11.1 22.5 31.6

Interest 29.4 21.8 33.6 27.0 17.0

Depreciation 76.1 79.9 94.0 98.2 104.0

Other Income 14.7 17.5 22.9 23.3 24.2

PBT before Exceptional Items 83.7 144.6 149.6 209.6 312.9

Less: Forex & Exceptional Items 11.0 1.3 1.2 0.0 0.0

PBT 72.7 143.3 148.5 209.6 312.9

Total Tax 30.1 52.4 53.5 73.3 109.5

PAT before MI 42.6 90.9 94.9 136.2 203.4

Minority Interest -0.4 -0.1 0.0 0.0 0.0

PAT 21.2 83.1 87.8 136.2 203.4

Adjusted PAT 32.2 84.4 89.0 136.2 203.4

Growth (%) NA 161.8 5.4 53.1 49.3

EPS 1.0 4.1 4.3 6.7 10.0

EPS (Adjusted) 1.6 4.1 4.4 6.7 10.0

Source: Company, ICICIdirect.com Research

Exhibit 32: Balance sheet

(Year-end March) FY16 FY17 FY18E FY19E FY20E

Equity Capital 204.4 204.4 204.4 204.4 204.4

Reserve and Surplus 671.6 758.7 846.5 982.7 1,186.1

Total Shareholders fund 876.0 963.1 1,050.9 1,187.1 1,390.5

Total Debt 257.5 216.7 319.7 269.7 169.7

Deferred Tax Liability 23.5 24.8 27.3 30.1 33.1

Minority Interest 0.3 0.2 0.3 0.3 0.3

Other liabilities 154.6 156.3 171.9 189.1 208.0

Source of Funds 1,311.9 1,361.2 1,570.1 1,676.3 1,801.6

Gross Block - Fixed Assets 1,358.0 1,463.7 1,813.7 1,963.7 2,113.7

Accumulated Depreciation 362.5 440.0 534.0 632.2 736.2

Net Block 995.5 1,023.6 1,279.6 1,331.5 1,377.5

Capital WIP 13.8 53.0 53.0 53.0 53.0

Net Fixed Assets 1,009.3 1,076.7 1,332.7 1,384.5 1,430.5

Goodwill on Consolidation 59.0 58.2 58.2 58.2 58.2

Investments 102.1 116.3 66.3 66.3 66.3

Inventory 49.7 52.4 63.3 74.3 84.2

Cash 24.1 34.1 27.2 71.1 139.8

Debtors 151.8 156.9 189.6 222.6 252.4

Loans & Advances & Other CA 46.1 58.2 64.0 70.4 77.4

Total Current Assets 271.8 301.6 344.1 438.5 553.9

Creditors 161.0 188.6 227.9 267.5 303.3

Provisions & Other CL 83.4 97.1 106.8 117.4 129.2

Total Current Liabilities 244.4 285.6 334.6 385.0 432.5

Net Current Assets 27.3 16.0 9.5 53.5 121.4

LT L& A, Other Assets 79.7 74.2 81.6 89.8 98.7

Deferred Tax Assets 34.5 19.9 21.9 24.0 26.4

Application of Funds 1,311.9 1,361.2 1,570.1 1,676.3 1,801.6

Source: Company, ICICIdirect.com Research

Page 21 ICICI Securities Ltd | Retail Equity Research

Exhibit 33: Cash Flow

(Year-end March) FY16 FY17 FY18E FY19E FY20E

Profit/(Loss) after taxation 16.0 98.8 87.8 136.2 203.4

Add: Depreciation & Amortization 76.1 79.9 94.0 98.2 104.0

Net Increase in Current Assets -20.8 -20.4 -49.4 -50.4 -46.8

Net Increase in Current Liabilities 42.6 28.8 49.0 50.4 47.5

Others 60.3 32.3 33.6 27.0 17.0

CF from operating activities 174.1 219.4 214.9 261.3 325.1

(Inc)/dec in Fixed Assets -87.8 -118.4 -350.0 -150.0 -150.0

(Inc)/dec in Investments -30.2 -23.9 50.0 0.0 0.0

Others -79.6 -21.9 8.7 9.6 10.6

CF from investing activities -197.6 -164.2 -291.3 -140.4 -139.4

Inc / (Dec) in Equity Capital -1.1 0.0 0.0 0.0 0.0

Inc / (Dec) in Debt 44.5 -24.6 103.0 -50.0 -100.0

Dividend & Dividend Tax 0.0 0.0 0.0 0.0 0.0

Others -25.3 -20.6 -33.6 -27.0 -17.0

CF from financing activities 18.0 -45.1 69.4 -77.0 -117.0

Net Cash flow -5.5 10.1 -6.9 43.9 68.7

Opening Cash 29.5 24.1 34.1 27.2 71.1

Closing Cash 24.1 34.1 27.2 71.1 139.8

Free Cash Flow 86.3 101.0 -135.1 111.3 175.1

Source: Company, ICICIdirect.com Research

Source: Company, ICICIdirect.com Research

Exhibit 34: Ratio Analysis

(Year-end March) FY16 FY17 FY18E FY19E FY20E

Per share data (|)

EPS 1.6 4.1 4.4 6.7 10.0

Cash EPS 1.6 4.1 4.4 6.7 10.0

BV 42.9 47.1 51.4 58.1 68.0

DPS 0.0 0.0 0.0 0.0 0.0

Cash Per Share 17.7 21.5 26.1 30.9 36.0

Operating Ratios (%)

EBITDA margins 10.8 12.2 11.2 11.7 13.6

Net Profit margins 2.0 4.5 3.9 5.1 6.7

Cash Conversion cycle 9.2 4.0 4.0 4.0 4.0

Gross Assets Turnover 1.2 1.3 1.3 1.4 1.5

Return Ratios (%)

RoE 3.7 8.8 8.5 11.5 14.6

RoCE 8.8 12.5 11.9 14.4 18.7

RoIC 9.1 13.1 12.0 15.3 21.2

Valuation Ratios (x)

P/E 180.0 68.7 65.2 42.6 28.5

EV / EBITDA 34.5 26.0 23.9 19.2 14.2

EV / Revenues 3.7 3.2 2.7 2.2 1.9

Market Cap / Revenues 3.6 3.1 2.6 2.2 1.9

Price to Book Value 6.6 6.0 5.5 4.9 4.2

Solvency Ratios

Net Debt / Equity 0.3 0.2 0.3 0.2 0.1

Net Debt / EBITDA 1.3 0.7 1.1 0.6 0.0

Current Ratio 1.0 0.9 0.9 1.0 1.0

Page 22 ICICI Securities Ltd | Retail Equity Research

Appendix:

In-patient revenue

In patient revenue is defined as revenue generated from a patient who

lives in a hospital while under treatment.

Out-patient revenue

Outpatient revenue is defined as revenue generated from a patient who

does not stay in the hospital while under treatment.

Operational beds

Operational beds are defined as the beds, which have been commissioned

for service of the total capacity of beds

Occupied beds

Occupied beds are defined as the beds if a patient is physically in the bed

or the bed is being retained for a patient. Thus, a bed maybe operational

but not occupied.

ARPOB

ARPOB stands for Average Revenue Per Occupied Bed. To calculate the

average, divide the total revenue for each bed with the number of days the

bed has been occupied

Average effective capital cost per operational bed

The metric is calculated by dividing the gross block +CWIP by the number

of operational beds

ALOS

ALOS stands for average length of stay. To calculate ALOS, divide the sum

of inpatient days for a particular diagnosis with the number of patient

admitted for the diagnosis. In simpler terms, it refers to the number of

days a person stays in a hospital for a particular illness or disease.

Census beds (Revenue earning beds)

An official count, in the hospital setting. The total number of patients

admitted to the facility by midnight, or sometimes at another time of the

day or evening.

Organ Transplant

It is an operation in which an organ is transplanted

JCI accreditation

Joint Commission International (JCI) works to improve patient safety and

quality of health care in the international community by offering education,

publications, advisory services, and international accreditation and

certification

NABH accreditation

National Accreditation Board for Hospitals & Healthcare (NABH) is a

constituent board of Quality Council of India Certification, set up to

establish and operate accreditation programme for healthcare

organisations

Page 23 ICICI Securities Ltd | Retail Equity Research

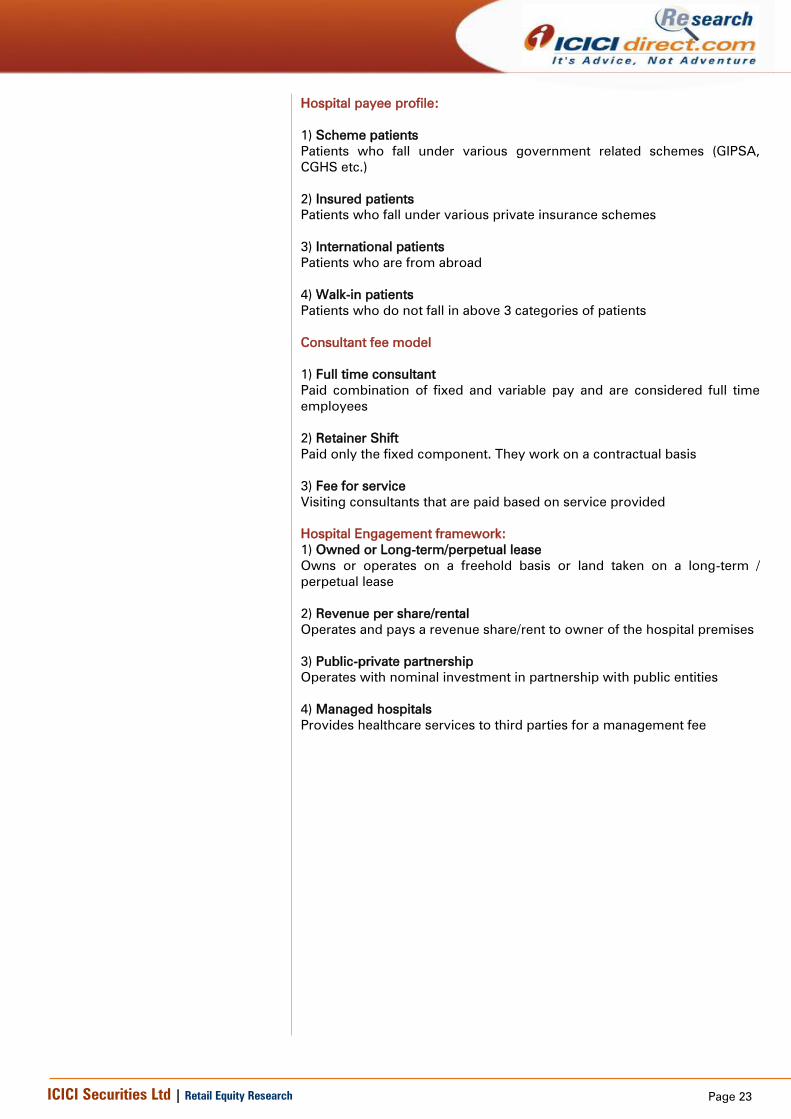

Hospital payee profile:

1) Scheme patients

Patients who fall under various government related schemes (GIPSA,

CGHS etc.)

2) Insured patients

Patients who fall under various private insurance schemes

3) International patients

Patients who are from abroad

4) Walk-in patients

Patients who do not fall in above 3 categories of patients

Consultant fee model

1) Full time consultant

Paid combination of fixed and variable pay and are considered full time

employees

2) Retainer Shift

Paid only the fixed component. They work on a contractual basis

3) Fee for service

Visiting consultants that are paid based on service provided

Hospital Engagement framework:

1) Owned or Long-term/perpetual lease

Owns or operates on a freehold basis or land taken on a long-term /

perpetual lease

2) Revenue per share/rental

Operates and pays a revenue share/rent to owner of the hospital premises

3) Public-private partnership

Operates with nominal investment in partnership with public entities

4) Managed hospitals

Provides healthcare services to third parties for a management fee

Page 24 ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

Page 25 ICICI Securities Ltd | Retail Equity Research

ANALYST CERTIFICATION

We /I, Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta M. Tech (Biotechnology) Research Analysts, authors and the names subscribed to this report, hereby certify that all of

the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or

indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI

Securities Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private

sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the

details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment

banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons

reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential

and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any

form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the

information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has

been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory

capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed.

This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or

other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of

their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently

evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities

whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure

Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not

predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other

assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for

services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific

transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies

mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not

receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor

Research Analysts and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts of this report have not received any compensation from the

companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the

month preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts do not serve as an officer, director or employee of the

companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such

distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such

jurisdiction. The securities