Infra Insights Q3 CY17 - Building a better working world - … Insights Q3 CY17, October 2017 | 3...

18

Infra Insights Q3 CY17 October 2017

Transcript of Infra Insights Q3 CY17 - Building a better working world - … Insights Q3 CY17, October 2017 | 3...

Infra Insights Q3 CY17October 2017

2 | Infra Insights Q3 CY17, October 2017

The growth in the Indian economy slowed down in the last quarter, but the markets were abuzz. The stock market continued to remain bullish, with Sensex and NIFTY rising by 0.2% and 2% respectively this quarter. The rupee also strengthened and ended the quarter at an exchange rate of US$1 = INR65.289. The G-Sec 10-year bond yield stood at 6.7% (as of 30 September 2017) compared to 6.5% (as of 30 June 2017) and SBI Overnight MCLR remained constant for the quarter (though it has reduced significantly over the last one year from 8.65% (as of 1 October 2016)). The stress on the debt side continued and RBI announced a second list of 30 companies for potential insolvency action. During its monetary policy review in August 2017, the central bank cut repo rate by 25 basis points to 6%, the lowest in six-and-a-half-years, and maintained a neutral policy stance with the objective of limiting the medium-term inflation to 4%. On the growth side, international agencies cut India’s growth forecasts going forward (IMF projected India to grow at 6.7% in 2017 and 7.4% in 2018, which are 0.5 and 0.3 percentage points less than the projections from earlier this year).

Editorial

Kuljit Singh

Head, Infrastructure Partner, Transaction Advisory Services Tel: +91-11-66233110 Email: [email protected]

3Infra Insights Q3 CY17, October 2017 |

Infrastructure also saw a lot of action. The S&P BSE Infrastructure Index rose 3.84% compared to a decline of 0.76% in the previous quarter. The sector saw a series of IPOs — one in transportation, five in construction, one in ports and two in logistics – a handsome share of 15% of the IPOs in the last quarter in India. However, stress remains high among local infrastructure players, with thermal power being in the eye of the storm.

The sector continues to enjoy intense focus from the Government, being perceived as the driver of future growth. The big initiatives in this quarter include the recently announced “Saubhagya” scheme, which targets electrification of all willing households in rural and urban areas by the end of December 2018 with a total investment outlay of INR16,320cr (US$2.5b). This holds promise for 21 GW of stressed thermal capacity that is in want of power purchase agreements (PPAs) — the recent spike in merchant prices providing some short-term relief in the meanwhile. The Government has also tried to mobilize investment through multilateral agencies (with the largest commitment being from AIIB this quarter), and NIIF is also slated to close the first tranche of its fund soon. Facilitating Infrastructure Investment Trusts (InvITs) and creating a Government-owned asset reconstruction company also hold promise.

In terms of private sector investments, renewables holds the position of the “blue-eyed boy,” with most active participation from domestic and international investors – both strategic and financial. According to CEA’s draft National Electricity Plan, in FY2022, coal will be the leading fuel source for power generation (45%) followed by renewable energy sources (37%). However, in the next five years till FY2027, coal installed capacity will drop to 39% and renewables will be the main source of generation with a share of 44%. In terms of electricity generation, coal-fired power will always be ahead because of a better capacity utilization than renewable energy sources. Taking the push for cleaner fuels further, the Government also announced its target to transform the entire country from fuel-based transportation to electric vehicle (EV) transportation by 2030. With the exception of EVs, the transportation sector has been missing the action with very few large new asset creations being launched this quarter on the highways and railways side. On the aviation side, privatization of Airports Authority of India (AAI) and regional connectivity have been the focus areas. Smart Cities is the area of focus on the urban infrastructure side.

With the recent cabinet reshuffle leading to a change in keys ministries such as railways, power and new and renewable energy, it will take a while for the new ministers to acclimatize in their new role and set out new priorities for themselves. However, the Indian infrastructure sector still holds promise because of the large anticipated demographic dividend that India holds for the future and the significant investments that the sector requires to achieve that dividend.

4 | Infra Insights Q3 CY17, October 2017

Srishti Ahuja Taneja

Director, Transaction Advisory Services Tel: +91-11-66718234 Email: [email protected]

The buzz around renewable bidding

Keeping up with the momentum of the last few quarters, wind and solar saw hectic bidding activity this quarter as well. The sector saw auctions of 2 GW capacity in Q3 CY17 (0.5 GW solar and 1.5 GW wind) – a decline from the 2.5 GW bid out in the earlier quarter (all solar). The pace of new capacity addition on the ground also slowed down significantly as states did a re-think on signing PPAs for projects already awarded and no new wind PPAs were signed under the feed-in tariff (FiT) regime. Interestingly, states accounted for approximately 50% of the tendered quantity. State tenders were well received and states such as Tamil Nadu and Gujarat have already started experimenting with the new process of wind auctions.

Despite several operational and financial challenges (discom credit risk, difficulties in land acquisition and grid connectivity problems), almost all tenders have been oversubscribed (by an average 3x) and have generally seen a declining tariff. The concern that the falling tariffs are unsustainable looms large, even though some of these concerns have been mitigated post-facto by sharp decline in module prices.

5Infra Insights Q3 CY17, October 2017 |

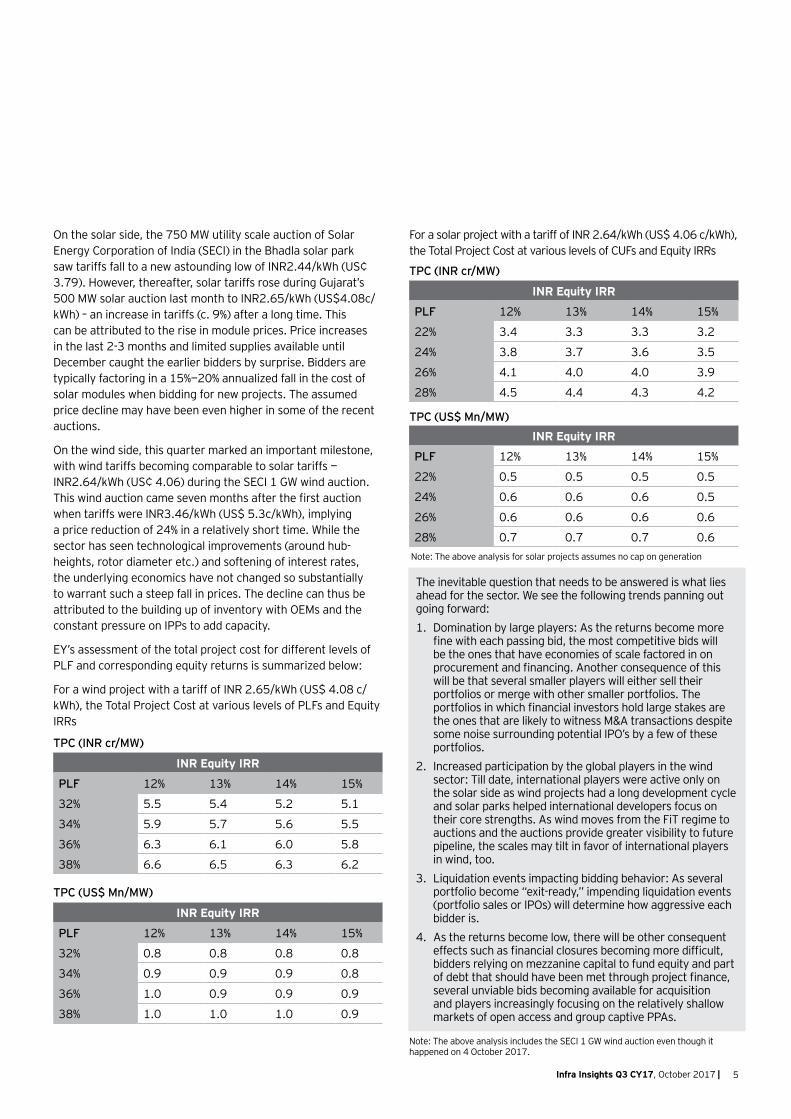

On the solar side, the 750 MW utility scale auction of Solar Energy Corporation of India (SECI) in the Bhadla solar park saw tariffs fall to a new astounding low of INR2.44/kWh (US¢ 3.79). However, thereafter, solar tariffs rose during Gujarat’s 500 MW solar auction last month to INR2.65/kWh (US$4.08c/kWh) – an increase in tariffs (c. 9%) after a long time. This can be attributed to the rise in module prices. Price increases in the last 2-3 months and limited supplies available until December caught the earlier bidders by surprise. Bidders are typically factoring in a 15%—20% annualized fall in the cost of solar modules when bidding for new projects. The assumed price decline may have been even higher in some of the recent auctions.

On the wind side, this quarter marked an important milestone, with wind tariffs becoming comparable to solar tariffs — INR2.64/kWh (US¢ 4.06) during the SECI 1 GW wind auction. This wind auction came seven months after the first auction when tariffs were INR3.46/kWh (US$ 5.3c/kWh), implying a price reduction of 24% in a relatively short time. While the sector has seen technological improvements (around hub-heights, rotor diameter etc.) and softening of interest rates, the underlying economics have not changed so substantially to warrant such a steep fall in prices. The decline can thus be attributed to the building up of inventory with OEMs and the constant pressure on IPPs to add capacity.

EY’s assessment of the total project cost for different levels of PLF and corresponding equity returns is summarized below:

For a wind project with a tariff of INR 2.65/kWh (US$ 4.08 c/kWh), the Total Project Cost at various levels of PLFs and Equity IRRs

INR Equity IRR

PLF 12% 13% 14% 15%

32% 5.5 5.4 5.2 5.1

34% 5.9 5.7 5.6 5.5

36% 6.3 6.1 6.0 5.8

38% 6.6 6.5 6.3 6.2

INR Equity IRR

PLF 12% 13% 14% 15%

32% 0.8 0.8 0.8 0.8

34% 0.9 0.9 0.9 0.8

36% 1.0 0.9 0.9 0.9

38% 1.0 1.0 1.0 0.9

INR Equity IRR

PLF 12% 13% 14% 15%

22% 3.4 3.3 3.3 3.2

24% 3.8 3.7 3.6 3.5

26% 4.1 4.0 4.0 3.9

28% 4.5 4.4 4.3 4.2

INR Equity IRR

PLF 12% 13% 14% 15%

22% 0.5 0.5 0.5 0.5

24% 0.6 0.6 0.6 0.5

26% 0.6 0.6 0.6 0.6

28% 0.7 0.7 0.7 0.6

For a solar project with a tariff of INR 2.64/kWh (US$ 4.06 c/kWh), the Total Project Cost at various levels of CUFs and Equity IRRs

TPC (INR cr/MW)

TPC (US$ Mn/MW)

TPC (INR cr/MW)

TPC (US$ Mn/MW)

Note: The above analysis for solar projects assumes no cap on generation

Note: The above analysis includes the SECI 1 GW wind auction even though it happened on 4 October 2017.

The inevitable question that needs to be answered is what lies ahead for the sector. We see the following trends panning out going forward: 1. Domination by large players: As the returns become more

fine with each passing bid, the most competitive bids will be the ones that have economies of scale factored in on procurement and financing. Another consequence of this will be that several smaller players will either sell their portfolios or merge with other smaller portfolios. The portfolios in which financial investors hold large stakes are the ones that are likely to witness M&A transactions despite some noise surrounding potential IPO’s by a few of these portfolios.

2. Increased participation by the global players in the wind sector: Till date, international players were active only on the solar side as wind projects had a long development cycle and solar parks helped international developers focus on their core strengths. As wind moves from the FiT regime to auctions and the auctions provide greater visibility to future pipeline, the scales may tilt in favor of international players in wind, too.

3. Liquidation events impacting bidding behavior: As several portfolio become “exit-ready,” impending liquidation events (portfolio sales or IPOs) will determine how aggressive each bidder is.

4. As the returns become low, there will be other consequent effects such as financial closures becoming more difficult, bidders relying on mezzanine capital to fund equity and part of debt that should have been met through project finance, several unviable bids becoming available for acquisition and players increasingly focusing on the relatively shallow markets of open access and group captive PPAs.

6 | Infra Insights Q3 CY17, October 2017

Key sector highlights

Renewable EnergyThe sector, which started as a subsidy-driven, environmentally focused alternative to conventional power, is now the mainstay of capacity additions in the country — the quarter saw new capacity of 2 GW being awarded. The sector continued to see frantic M&A and fund raising activity. However, the regulatory changes in the background need to be watched closely as some of the underlying sector fundamentals may get affected going forward.

7Infra Insights Q3 CY17, October 2017 |

While consolidation has picked up momentum in solar, activity in the wind space has been conspicuous by its absence.IDFC completes exit from Sembcorp Green Infra • Sembcorp Industries acquired IDFC PE’s remaining 28% stake in

Sembcorp Green Infra for INR1,437cr (US$221m). With this, the company is now fully owned by Sembcorp Industries. Sembcorp Industries had acquired a 60% stake in 2015 for INR1,105cr (US$170m).

IDFC infrastructure fund acquires First Solar’s India portfolio

• IDFC Alternatives made its biggest acquisition in the renewable space till date by acquiring the entire 200 MW of First Solar’s operational solar portfolio for an enterprise value of INR1,950cr (US$300m).

ReNew Power Ventures Pvt. Ltd. eyes Orange's portfolio to bulk up before IPO

• ReNew Power, backed by Goldman Sachs, is believed to be in active discussions with Orange Renewable to merge its renewable portfolio of ~ 600 MW (predominantly wind) into ReNew for INR6,175cr (US$950m).

• ReNew has already submitted a non-binding offer and is conducting diligence. At the same time, Orange is said to be exploring potential sale dialogues.

Equis Energy rolls out the sale process for its renewable portfolio

• Equis Energy has a 1 GW operational portfolio across Japan, India and other smaller Asian markets such as Taiwan, the Philippines, Indonesia and Thailand and a pipeline of additional ~ 4 GW.

Orient Green Power’s proposed merger with ILFS may not consummate

• The company invited bids for 100% acquisition. Several large global utilities were evaluating the transaction but diverse geographies being clubbed together affected market appetite. In India, the Equis portfolio is held under Energon.

• Orient Green Power and ILFS Wind’s proposed merger is believed to have run into tax-related issues. Thereafter, Orient Green Power announced a restructuring exercise, under which its biomass operations will be transferred to a subsidiary.

On the debt side, the sector saw a spate of green bond issuances.Greenko, Azure and Continuum approach international markets to raise green bonds

• Greenko raised US$1b from an overseas bond issue, making it Asia’s largest green bond till date. Placed at a 5.1% yield, it is also the largest high yield corporate bond by a privately held company globally. The bond obtained oversubscription of 1.5x the actual size.

• Azure Power raised US$500m from an overseas bonds sale. The notes offering a yield of ~5.5% were oversubscribed by 2x the size of the offering.

• Continuum Energy also set out to raise US$400m as green bonds. However, the issue was not closed.

• All the three bond issuances occurred in July in quick succession, and over-supply led to the yields climbing up.

• NHPC and Tata Power also proposed to raise US$300m and US$1b respectively through a similar route.

Financiers raise US$850m debt internationally for on-lending to projects domestically

• REC raised US$450m through 10-year bonds, at an annual yield of 3.965%. The bond was oversubscribed 3.9x. REC has become the first Indian PSU to launch US$ green bonds. The bonds have been offered under REC’s existing US$1b medium-term note program and have been listed on the London and the Singapore Stock Exchange.

• IREDA became the first Indian FI to raise “green masala bonds.” The US$300m issue is listed on the London Stock Exchange and was subscribed by 1.7x.

• On similar lines, L&T Infrastructure Finance Co. also issued its first green bond of US$103m. These bonds were issued to International Finance Corporation.

8 | Infra Insights Q3 CY17, October 2017

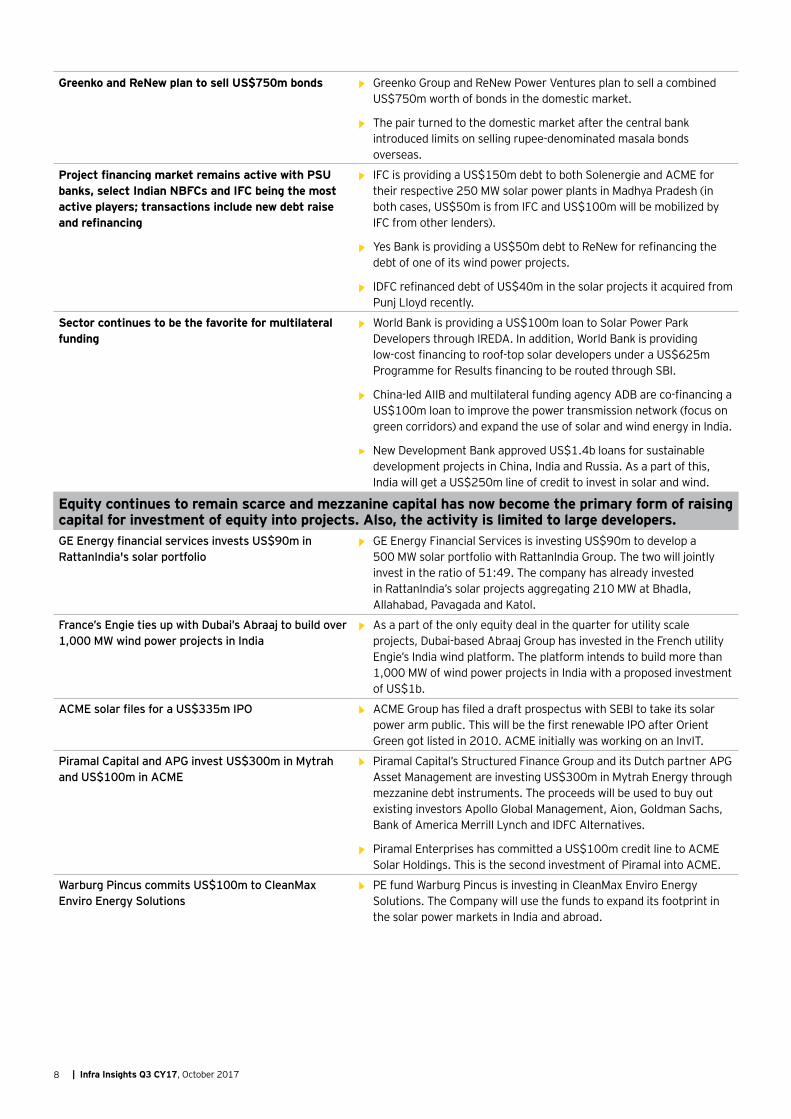

Greenko and ReNew plan to sell US$750m bonds • Greenko Group and ReNew Power Ventures plan to sell a combined US$750m worth of bonds in the domestic market.

• The pair turned to the domestic market after the central bank introduced limits on selling rupee-denominated masala bonds overseas.

Project financing market remains active with PSU banks, select Indian NBFCs and IFC being the most active players; transactions include new debt raise and refinancing

• IFC is providing a US$150m debt to both Solenergie and ACME for their respective 250 MW solar power plants in Madhya Pradesh (in both cases, US$50m is from IFC and US$100m will be mobilized by IFC from other lenders).

• Yes Bank is providing a US$50m debt to ReNew for refinancing the debt of one of its wind power projects.

• IDFC refinanced debt of US$40m in the solar projects it acquired from Punj Lloyd recently.

Sector continues to be the favorite for multilateral funding

• World Bank is providing a US$100m loan to Solar Power Park Developers through IREDA. In addition, World Bank is providing low-cost financing to roof-top solar developers under a US$625m Programme for Results financing to be routed through SBI.

• China-led AIIB and multilateral funding agency ADB are co-financing a US$100m loan to improve the power transmission network (focus on green corridors) and expand the use of solar and wind energy in India.

• New Development Bank approved US$1.4b loans for sustainable development projects in China, India and Russia. As a part of this, India will get a US$250m line of credit to invest in solar and wind.

Equity continues to remain scarce and mezzanine capital has now become the primary form of raising capital for investment of equity into projects. Also, the activity is limited to large developers.GE Energy financial services invests US$90m in RattanIndia's solar portfolio

• GE Energy Financial Services is investing US$90m to develop a 500 MW solar portfolio with RattanIndia Group. The two will jointly invest in the ratio of 51:49. The company has already invested in RattanIndia’s solar projects aggregating 210 MW at Bhadla, Allahabad, Pavagada and Katol.

France’s Engie ties up with Dubai’s Abraaj to build over 1,000 MW wind power projects in India

• As a part of the only equity deal in the quarter for utility scale projects, Dubai-based Abraaj Group has invested in the French utility Engie’s India wind platform. The platform intends to build more than 1,000 MW of wind power projects in India with a proposed investment of US$1b.

ACME solar files for a US$335m IPO • ACME Group has filed a draft prospectus with SEBI to take its solar power arm public. This will be the first renewable IPO after Orient Green got listed in 2010. ACME initially was working on an InvIT.

Piramal Capital and APG invest US$300m in Mytrah and US$100m in ACME

• Piramal Capital’s Structured Finance Group and its Dutch partner APG Asset Management are investing US$300m in Mytrah Energy through mezzanine debt instruments. The proceeds will be used to buy out existing investors Apollo Global Management, Aion, Goldman Sachs, Bank of America Merrill Lynch and IDFC Alternatives.

• Piramal Enterprises has committed a US$100m credit line to ACME Solar Holdings. This is the second investment of Piramal into ACME.

Warburg Pincus commits US$100m to CleanMax Enviro Energy Solutions

• PE fund Warburg Pincus is investing in CleanMax Enviro Energy Solutions. The Company will use the funds to expand its footprint in the solar power markets in India and abroad.

9Infra Insights Q3 CY17, October 2017 |

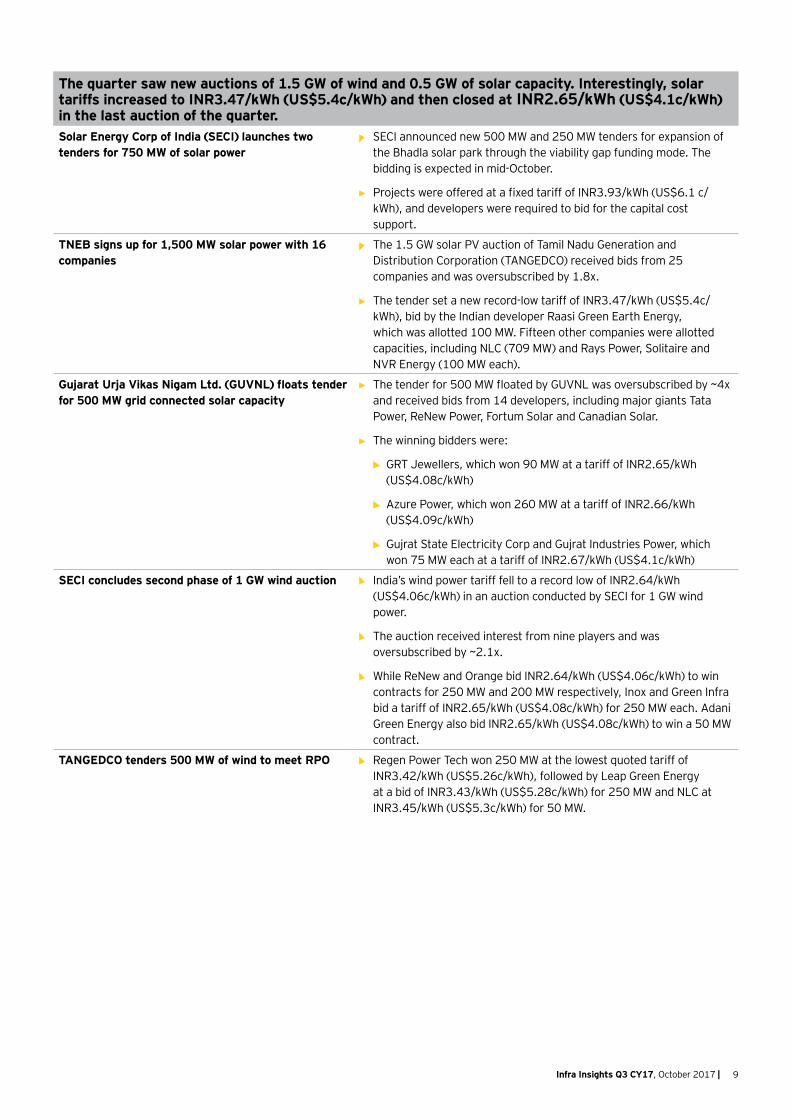

The quarter saw new auctions of 1.5 GW of wind and 0.5 GW of solar capacity. Interestingly, solar tariffs increased to INR3.47/kWh (US$5.4c/kWh) and then closed at INR2.65/kWh (US$4.1c/kWh) in the last auction of the quarter.Solar Energy Corp of India (SECI) launches two tenders for 750 MW of solar power

• SECI announced new 500 MW and 250 MW tenders for expansion of the Bhadla solar park through the viability gap funding mode. The bidding is expected in mid-October.

• Projects were offered at a fixed tariff of INR3.93/kWh (US$6.1 c/kWh), and developers were required to bid for the capital cost support.

TNEB signs up for 1,500 MW solar power with 16 companies

• The 1.5 GW solar PV auction of Tamil Nadu Generation and Distribution Corporation (TANGEDCO) received bids from 25 companies and was oversubscribed by 1.8x.

• The tender set a new record-low tariff of INR3.47/kWh (US$5.4c/kWh), bid by the Indian developer Raasi Green Earth Energy, which was allotted 100 MW. Fifteen other companies were allotted capacities, including NLC (709 MW) and Rays Power, Solitaire and NVR Energy (100 MW each).

Gujarat Urja Vikas Nigam Ltd. (GUVNL) floats tender for 500 MW grid connected solar capacity

• The tender for 500 MW floated by GUVNL was oversubscribed by ~4x and received bids from 14 developers, including major giants Tata Power, ReNew Power, Fortum Solar and Canadian Solar.

• The winning bidders were:

• GRT Jewellers, which won 90 MW at a tariff of INR2.65/kWh (US$4.08c/kWh)

• Azure Power, which won 260 MW at a tariff of INR2.66/kWh (US$4.09c/kWh)

• Gujrat State Electricity Corp and Gujrat Industries Power, which won 75 MW each at a tariff of INR2.67/kWh (US$4.1c/kWh)

SECI concludes second phase of 1 GW wind auction • India’s wind power tariff fell to a record low of INR2.64/kWh (US$4.06c/kWh) in an auction conducted by SECI for 1 GW wind power.

• The auction received interest from nine players and was oversubscribed by ~2.1x.

• While ReNew and Orange bid INR2.64/kWh (US$4.06c/kWh) to win contracts for 250 MW and 200 MW respectively, Inox and Green Infra bid a tariff of INR2.65/kWh (US$4.08c/kWh) for 250 MW each. Adani Green Energy also bid INR2.65/kWh (US$4.08c/kWh) to win a 50 MW contract.

TANGEDCO tenders 500 MW of wind to meet RPO • Regen Power Tech won 250 MW at the lowest quoted tariff of INR3.42/kWh (US$5.26c/kWh), followed by Leap Green Energy at a bid of INR3.43/kWh (US$5.28c/kWh) for 250 MW and NLC at INR3.45/kWh (US$5.3c/kWh) for 50 MW.

10 | Infra Insights Q3 CY17, October 2017

Regulatory moves by various states were at a different wavelength vis-à-vis the Center.Madhya Pradesh proposes to take away must-run status of renewable projects; MNRE issues fresh guidelines for competitive solar bidding in response

• Madhya Pradesh has proposed ranking of the available sources of generation based on the ascending order of prices, following the footsteps of Tamil Nadu and Rajasthan, which issued random backing down instructions.

• The move is not in line with the provisions of the Electricity Act, National Electricity Policy and National Tariff Policy to promote the use of energy from renewable sources by according it a “must run” status. A shift to the merit order dispatch would push costly solar and wind power down the pecking order.

• In response to this, the Ministry of New and Renewable Energy (MNRE) issued fresh guidelines for competitive bidding for procuring solar power under which it proposed generation compensation for constraints and stressed on the “must-run” status for solar projects, alongside a stipulation that unilateral termination or amendment of PPAs for solar projects be disallowed.

Uttar Pradesh Electricity Regulatory Commission (UPERC) issues letter to 15 solar power project developers for lower solar tariffs

• Due to the steep fall in solar tariffs in the past two years, UPERC issued letters to 15 solar power project developers with which contracts had been signed, to voluntarily agree to lower solar tariffs of INR7.02/kWh (US$10.8 c/kWh), the lowest price bid during the 2015 auction.

Wind power developers upset over Karnataka tariff revision

• KERC order reduced wind tariffs from INR4.5/kWh (US$6.92 c/kWh) to INR3.74/kWh (US$5.75 c/kWh) for the 599 MW of signed wind projects pending before the regulator for approval.

• Of these, 273 MW have already been commissioned and supplying power to BESCO, HESCO and GESCO at the old tariffs.

• Andhra Pradesh, Tamil Nadu and Gujarat are the other states seeking to lower wind tariffs.

PPAs signed for first wind auction totaling 1,050 MW • PPAs were executed for 1,050 MW of wind power capacity between PTC and winning bidders identified under MNRE’s first wind auction.

11Infra Insights Q3 CY17, October 2017 |

Recent developments in stressed assetsHike in merchant tariffs provides temporary relief to IPPs

• Merchant power tariff rose to as high as INR9.9/kWh (US$15.23 c/kWh) in August. The average tariff this quarter was INR3.27/kWh (US$5.03 c/kWh) vis-a-vis INR2.27/kWh (US$3.49 c/kWh) during Q3 2016.

NLC India Ltd. plans to take over stressed assets of other PSUs

• As part of the Government’s efforts to revive stranded assets, NLC is planning to take over the Raghunathpur TPP in West Bengal, a stressed TPP of the Damodar Valley Corporation. NLC has also shortlisted two other plants for acquisition.

• There has been buzz in the market about NTPC mulling to take over some stressed assets.

Tata Power to receive compensation for change in cost of electricity generation

• CERC has allowed Coastal Gujarat Power (CGPL), the Tata Power arm that runs the beleaguered 4,150 MW Mundra ultra mega power plant, to receive compensation for change in cost of electricity generation arising from revisions in various taxes and duties during its construction period between October 2007 and March 2013.

M&A and fund-raiseEdelweiss ARC buys Adhunik Power under the SDR scheme

• An SBI-led consortium of banks has closed the first successful sale under the SDR scheme.

• Edelweiss Asset Reconstruction Company purchased a majority stake in Adhunik Power from the banks for INR500cr (US$77m) in cash.

GMR to sell Kakinada power plant for INR410cr (US$63m)

• GMR Group announced the sale of its 220 MW gas-based, barge mounted, power plant in Kakinada, Andhra Pradesh, for INR410cr (US$63m).

Banks, led by PNB, look to sell stake in Jindal India Thermal Power

• Lenders to Jindal India Thermal Power Ltd. (a B.C. Jindal Group company), led by consortium leader Punjab National Bank, have sought bids from interested investors to sell their 51% stake in the company.

• The 1,200 MW thermal power plant in Angul, Odisha, owes ~INR5,900cr (US$908m) to a consortium of 17 lenders.

GVK Power plans to divest Jegurupadu Unit II • After the 2016 divestment of the 217 MW Unit I of the Jegurupadu gas-fired power plant, GVK plans to divest the 228 MW Unit II.

• The company might sell other gas plants under the portfolio as well.

New norms to ease PPAMoP working on a proposal for reviving distressed thermal assets

• As most discoms have been shying away from new PPAs for thermal capacity, MoP is mooting a new proposal whereby discoms have the flexibility to discontinue payment of fixed cost to generators if no power is being purchased.

• The Government is also planning a fund with initial corpus of INR6,500cr (US$1,000m) to enable alternative financing options for power assets that are stalled due to shortage of capital and lack of fuel linkages and PPAs.

• The PPA easing will largely help stressed coal-fired projects with a capacity of 16,000 MW that are complete but could not run as fuel linkage is not being provided in the absence of a long-term PPA.

Thermal powerStress in the sector continues, requiring further policy intervention. The Government reviewed the status of 34 stressed thermal power projects with an estimated debt of about INR1.77 lakh crore (US$27.23b) and has taken some steps to ease the stress by revising the PPA norms and creating a corpus for stalled assets.

12 | Infra Insights Q3 CY17, October 2017

Aggregate financial losses of state power distribution companies under UDAY decline by 21.5%

• The decrease in losses has been primarily driven by lower interest costs for the discoms as the states took over 75% of their short term liabilities.

• While discoms in Rajasthan, Madhya Pradesh, Uttar Pradesh, Tamil Nadu and Maharashtra witnessed a drop in losses by 54%, 14%, 16%, 35%, 8% respectively, the losses for discoms in Punjab, Jharkhand and Bihar increased by 20%, 72%, 53% respectively. Also, there was a reduction of 1% in the AT&C losses.

Indian Energy Exchange (IEX) proposes IPO • IEX, the largest exchange for trading of electricity products in the country, is planning to raise INR1,000cr (US$150m) from its IPO in October 2017.

Adani Transmission’s expansion plans • Adani Transmission has acquired Hadoti Power Transmission Services Ltd. from Rajasthan Rajya Vidyut Prasaran Nigam Ltd. (RVPN).

• It is also looking to raise fresh equity capital of up to INR3,000cr (US$462m) through a QIP.

PGCIL continues capacity expansion financed largely by debt and internal accruals

• Sources of funding for Power Grid Corp include:

• Rupee term loan of up to INR3,270cr (US$503m) from ICICI Bank for five years

• INR20,000cr (US$3,077m) from issue of bonds to select investors.

• Loan of INR3,250cr (US$500m) from the Asian Development Bank (ADB) for its various projects.

Sterlite to invest in creating new assets while it sells its existing assets to IndiGrid

• Sterlite Power Grid Ventures Ltd. has proposed to invest around INR6,500cr (US$1,000m) per year in the next few years to build power lines in Brazil.

• IndiGrid is acquiring three projects under the right of first refusal from its sponsor, Sterlite. The transaction is expected to complete in October.

Adani is the front-runner in the Reliance Infrastructure's Mumbai power business after exclusivity with Greenko ends

• Greenko’s talks with Anil Ambani-led Reliance Infrastructure to acquire its Mumbai electricity business for an enterprise value of INR10,000cr—INR13,000cr (US$1,750—US$2,000m) fell through. The transaction was initially planned as a stake sale to PSP, the Canadian pension fund.

• Adani Transmission has now entered into an exclusive dialogue on the transaction.

Transmission and distributionThe sector continues to ail from the perception of being an “ancillary sector” to power generation and hence the investments continue to just catch pace with the generation sector.

13Infra Insights Q3 CY17, October 2017 |

Highway sector headed for consolidation; M&A activity seen picking upM&As • Dilip Buildcon is selling its stake in 24 road projects with a total

project value of INR10,500cr (US$1615m) for US$250m to Shrem Group over a period of the next two years. The company plans to make an additional investment of INR858cr (US$132m) in the projects out of these funds. The portfolio includes 14 operational projects and 10 under-construction projects (6 recently awarded HAM projects). The company will receive an additional INR40cr (US$6m) for O&M of these assets over the life of these projects

• Brookfield Asset Management acquired two toll road projects — Rayalaseema Expressway and Simhapuri Expressway — for INR1,950cr (US$300m). These were 100% acquisitions from KMC Infrastructure Ltd and BSCPL Infrastructure Ltd.

• IRB Infrastructure plans to sell IRB Pathankot Amritsar Toll Road Limited at an enterprise value of INR1,593cr (US$245m) to IRB InvIT Fund.

Refinancing of debt by Sadbhav Infrastructure Projects Ltd.

• Two out of 11 highway assets — Shreenathji Udaipur Tollway (SUTPL) and Ahmedabad Ring Road Infrastructure (ARRIL) — have already completed the refinancing exercise.

• For the other nine subsidiaries, Sadbhav Infrastructure is in the process of refinancing debt and is expecting savings of over INR13cr (US$2m) annually.

IPO of Srei Infrastructure Finance-led firm • The issue constituted 34.9% of the post-issue paid-up equity share capital and offered shares in the INR195—INR205 price range.

• The issue was oversubscribed by 1.8x the issue size but has seen a steep decline in market price after the issue.

Fund raise • Cube Highways is looking at a US$200m raise from PFs and SWFs, with two players in advanced stages of dialogue.

• Ashoka Buildcon is said to be looking for fund raise/potential liquidity events.

Progress of National Highway Programmes launched by the GovernmentProjects allotted by NHAI under the hybrid annuity model

• Welspun was awarded the Aunta Simariya (Ganga Bridge) project; NHAI estimated the project cost at INR787cr (US$121m).

• PNC was awarded the Chakeri Allahabad project; the NHAI project cost was INR1,430cr (US$220m).

Multiple projects inaugurated by MoRTH • 12 national highway projects worth US$863m were inaugurated.

• 11 projects worth US$1.5b were launched in Rajasthan.

NHAI to award O&M contracts on TOT basis • NHAI has decided to undertake operation/maintenance of the listed highway projects through PPP on TOT basis for a period of 30 years.

• Ten projects with a total length of 646 km have been included in the first bundle to be awarded by NHAI.

• It comprises six projects in Andhra Pradesh (NH 5) with a total length of 404 km. The remaining 242 km stretch to be awarded includes four projects in Gujarat (NH8).

Transportation The PPP activity in the sector saw a new low with only two new projects being awarded by NHAI under the hybrid annuity model. The sector players, however, are anticipating the Toll Operate and Transfer (TOT) bids in the coming months should add momentum. The sector saw a handful of large M&A deals – but the action was sporadic.

14 | Infra Insights Q3 CY17, October 2017

Other projects allotted by the authorities • NHAI has granted in principal approval for the construction of the Delhi-Panipat and Delhi-Anwar regional rapid transit system (RRTS) projects worth INR53,500cr (US$8.23m).

• IL&FS Transportation Networks emerged as the lowest bidder for the construction, operations and maintenance of the Zojila Pass Tunnel project on EPC basis.

Other transportation

Kamarajar to utilize a INR650cr (US$100m) loan to construct a new coal-loading berth for Tamil Nadu

• Kamarajar Port, the only Central Government-owned port that is run as a company, will raise INR650cr (US$100m) from Axis Bank to part-fund an INR1,220cr (US$188m) expansion of the port located at Ennore near Chennai.

Railway station revamp: The Government may open railway lines to private players

• The Railways is offering up to 400 stations to private entities in one of the biggest station redevelopment programs in the world. The scheme envisages a minimum investment of INR100,000cr (US$15b).

• Under the scheme, companies winning the bids will have to modernize the stations and provide world-class passenger amenities, for which they will, in return, get the ancillary land on lease for 99 years for commercial development.

Air India (AI) on the block Cabinet Committee on Economic Affairs (CCEA) has finalized a three-pronged strategy for the disinvestment of AI:

• Demerger and strategic disinvestment of three profit-making subsidiaries (AI Express Limited, AI Air Transport Services Limited and AI’s JV with SATS Limited for ground handling activities in Mumbai, Delhi, Trivandrum and Bengaluru)

• Hiving off certain assets into a separate SPV

• Addressing the “unsustainable debts”; the total debt of AI is~INR49,000cr (US$7.5b) — INR17,000cr (US$2.6b) in aircraft loans and the remaining in the form of capital loans

As a part of the above process, AI concluded the bidding process of 14 of its properties (10 properties sold at higher than reserve price). In the next stage, 30 more properties valued at over INR500cr are to be auctioned.

Thrust on regional connectivity continues • Airports Authority of India (AAI) plans to revive and operationalize around 50 airports in India over the next 10 years to improve regional and remote air connectivity. These will be developed under the “no-frills” model.

• The Central Government is likely to offer 20 airports in the second round of bidding for flights under the Regional Connectivity Scheme. Two major changes applicable in the case of the North Eastern region and island states are the waiver of the 150 km distance condition between two airports for availing concessions and seating regulations for aircrafts landing at advanced landing grounds.

GVK exits the Bangalore airport project after selling its residual stake to Fairfax India

• Fairfax India Holdings acquired an additional 10% stake in Kempegowda International Airport Limited (Bangalore International Airport Limited) from GVK Power & Infrastructure for a consideration of INR1,290cr (US$200m). In March this year, Fairfax had acquired a 38% stake in the project company.

Sources:I. Thomson Reuters

II. Factiva

III. Bloomberg

IV. Megermarket

V. Times of India

VI. Economic Times

VII. Business Standard

VIII. EY analysis

15Infra Insights Q3 CY17, October 2017 |

For details please contact

Amit Khandelwal

National Leader, Transaction Advisory Services Tel: +91-11-66718180 Email: [email protected]

Sushi S V.

Partner, Transaction Advisory Services Tel: +91-22-61920570 Email: [email protected]

Kuljit Singh

Head, Infrastructure Partner, Transaction Advisory Services Tel: +91-11-66233110 Email: [email protected]

Srishti Ahuja Taneja

Director, Transaction Advisory Services Tel: +91-11-66718234 Email: [email protected]

16 | Infra Insights Q3 CY17, October 2017

Disclaimer

The information in the newsletter is derived from public and private sources, articles and press releases, which we believe to be reliable and accurate but which, without further investigation cannot be warranted as to their accuracy, completeness or correctness.

This information is supplied on the condition that neither Ernst & Young LLP (EY) nor any other member of the global Ernst & Young organization are not liable for any error or inaccuracy contained herein, whether negligently caused or otherwise, or for loss or damage suffered by any person due to such error, omission or inaccuracy as a result of such a supply.

Ernst & Young LLP, including its affiliates, partners, employees, agents, and subcontractors accepts no responsibility and shall have no liability in contract, tort or otherwise to you or any other third party in relation to the contents of the newsletter or the Information contained therein;

Ernst & Young LLP neither represent it to be comprehensive or sufficient for making business decisions nor as replacement of professional advice.

Our officesAhmedabad

2nd floor, Shivalik IshaanNear C.N. VidhyalayaAmbawadiAhmedabad - 380 015Tel: + 91 79 6608 3800Fax: + 91 79 6608 3900

Bengaluru

6th, 12th & 13th floor“UB City”, Canberra BlockNo.24 Vittal Mallya RoadBengaluru - 560 001Tel: + 91 80 4027 5000 + 91 80 6727 5000 + 91 80 2224 0696Fax: + 91 80 2210 6000

Ground Floor, ‘A’ wingDivyasree Chambers# 11, O’Shaughnessy RoadLangford GardensBengaluru - 560 025Tel: +91 80 6727 5000Fax: +91 80 2222 9914

Chandigarh

1st Floor, SCO: 166-167Sector 9-C, Madhya MargChandigarh - 160 009 Tel. +91 172 331 7800Fax: +91 172 331 7888

Chennai

Tidel Park, 6th & 7th Floor A Block (Module 601,701-702)No.4, Rajiv Gandhi Salai Taramani, Chennai - 600 113Tel: + 91 44 6654 8100 Fax: + 91 44 2254 0120

Delhi NCR

Golf View Corporate Tower BSector 42, Sector RoadGurgaon - 122 002Tel: + 91 124 464 4000Fax: + 91 124 464 4050

3rd & 6th Floor, Worldmark-1IGI Airport Hospitality DistrictAerocity, New Delhi - 110 037Tel: + 91 11 6671 8000Fax + 91 11 6671 9999

4th & 5th Floor, Plot No 2B Tower 2, Sector 126 NOIDA - 201 304Gautam Budh Nagar, U.P.Tel: + 91 120 671 7000Fax: + 91 120 671 7171

Hyderabad

Oval Office, 18, iLabs CentreHitech City, MadhapurHyderabad - 500 081Tel: + 91 40 6736 2000Fax: + 91 40 6736 2200

Jamshedpur

1st Floor, Shantiniketan BuildingHolding No. 1, SB Shop AreaBistupur, Jamshedpur – 831 001Tel: +91 657 663 1000BSNL: +91 657 223 0441

Kochi

9th Floor, ABAD NucleusNH-49, Maradu POKochi - 682 304Tel: + 91 484 304 4000Fax: + 91 484 270 5393

Kolkata

22 Camac Street3rd Floor, Block ‘C’Kolkata - 700 016Tel: + 91 33 6615 3400Fax: + 91 33 2281 7750

Mumbai

14th Floor, The Ruby29 Senapati Bapat MargDadar (W), Mumbai - 400 028Tel: + 91 22 6192 0000Fax: + 91 22 6192 1000

5th Floor, Block B-2Nirlon Knowledge ParkOff. Western Express HighwayGoregaon (E)Mumbai - 400 063Tel: + 91 22 6192 0000Fax: + 91 22 6192 3000

Pune

C-401, 4th floorPanchshil Tech ParkYerwada (Near Don Bosco School)Pune - 411 006Tel: + 91 20 6603 6000Fax: + 91 20 6601 5900

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in.

Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016

© 2017 Ernst & Young LLP. Published in India. All Rights Reserved.

EYIN1710-008 ED None

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

YG

Ernst & Young LLP

EY | Assurance | Tax | Transactions | Advisory

ey.com/in

@EY_India EY|LinkedIn EY India EY India careers