Informal/formal sector partnerships: Fidelity Bank...

16

BUSINESS UNIT: MICROFINANCE DATE: 22 nd February 2013 Informal/formal sector partnerships: Fidelity Bank Ghana Dr. William Derban Director, Financial Inclusion, CSR & PMO Fidelity Bank Ghana

Transcript of Informal/formal sector partnerships: Fidelity Bank...

BUSINESS UNIT: MICROFINANCE DATE: 22nd February 2013

Informal/formal sector partnerships: Fidelity Bank Ghana

Dr. William Derban

Director, Financial Inclusion, CSR & PMO

Fidelity Bank Ghana

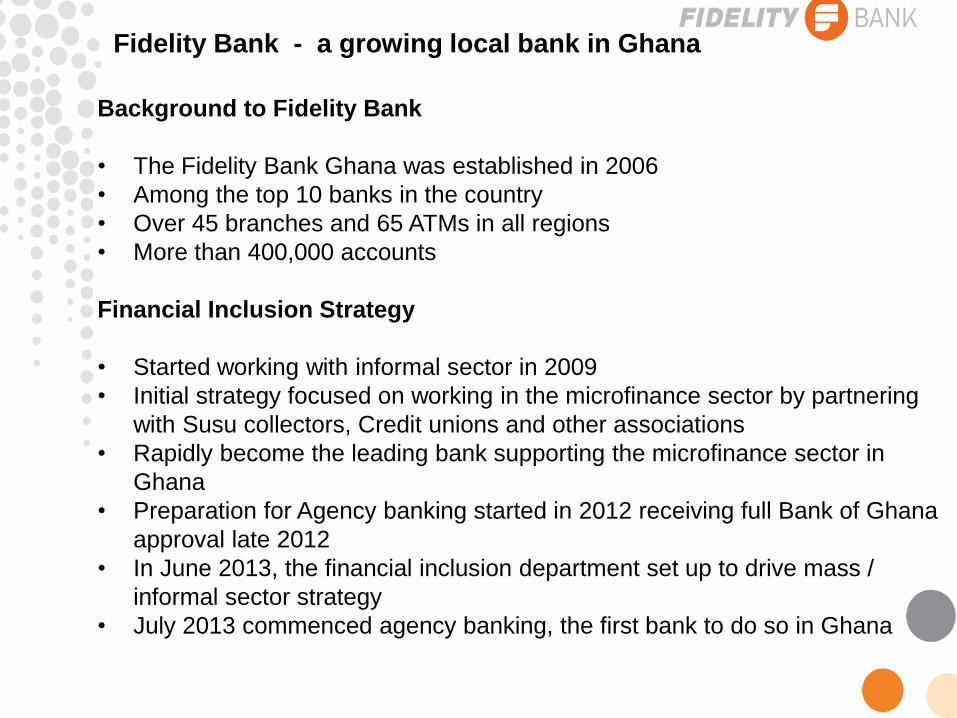

Background to Fidelity Bank

• The Fidelity Bank Ghana was established in 2006

• Among the top 10 banks in the country

• Over 45 branches and 65 ATMs in all regions

• More than 400,000 accounts

Financial Inclusion Strategy

• Started working with informal sector in 2009

• Initial strategy focused on working in the microfinance sector by partnering

with Susu collectors, Credit unions and other associations

• Rapidly become the leading bank supporting the microfinance sector in

Ghana

• Preparation for Agency banking started in 2012 receiving full Bank of Ghana

approval late 2012

• In June 2013, the financial inclusion department set up to drive mass /

informal sector strategy

• July 2013 commenced agency banking, the first bank to do so in Ghana

Fidelity Bank - a growing local bank in Ghana

3

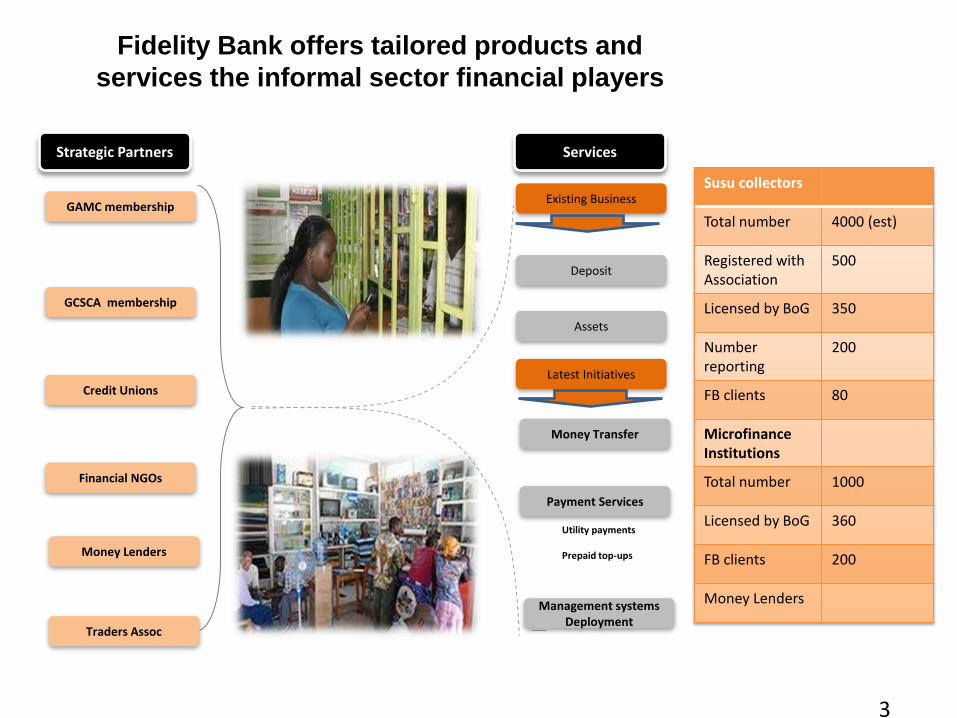

Strategic Partners Services

GAMC membership

Credit Unions

Financial NGOs

Money Lenders

GCSCA membership

Deposit

Assets

Latest Initiatives

Money Transfer

Payment Services

Utility payments Prepaid top-ups

Existing Business

Management systems Deployment

Traders Assoc

Fidelity Bank offers tailored products and

services the informal sector financial players

Susu collectors

Total number 4000 (est)

Registered with Association

500

Licensed by BoG 350

Number reporting

200

FB clients 80

Microfinance Institutions

Total number 1000

Licensed by BoG 360

FB clients 200

Money Lenders

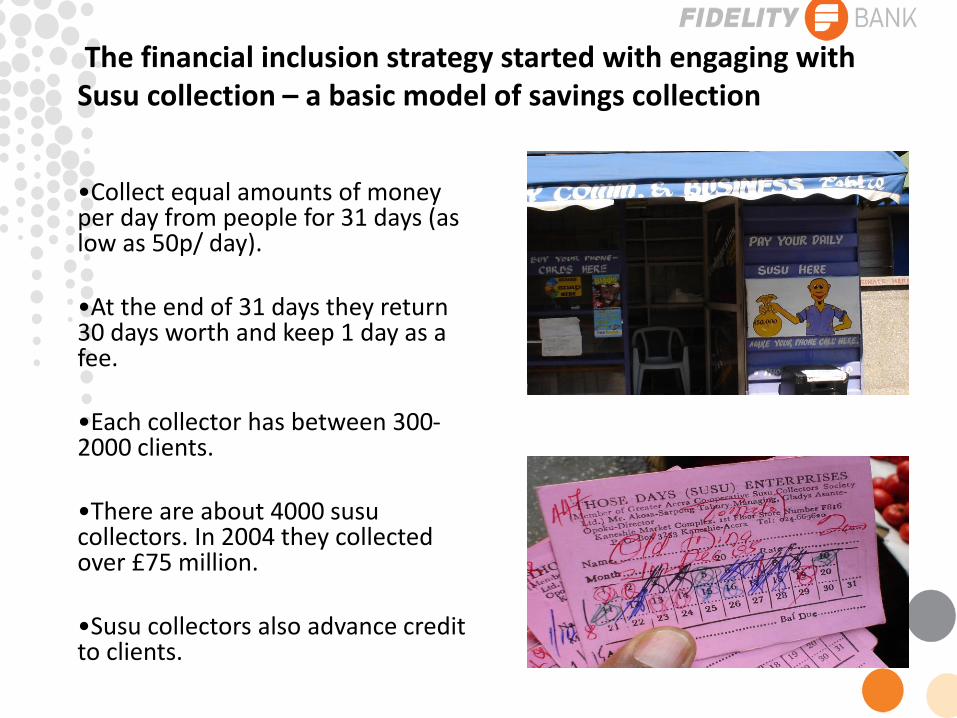

The financial inclusion strategy started with engaging with Susu collection – a basic model of savings collection

•Collect equal amounts of money per day from people for 31 days (as low as 50p/ day).

•At the end of 31 days they return 30 days worth and keep 1 day as a fee.

•Each collector has between 300-2000 clients.

•There are about 4000 susu collectors. In 2004 they collected over £75 million.

•Susu collectors also advance credit to clients.

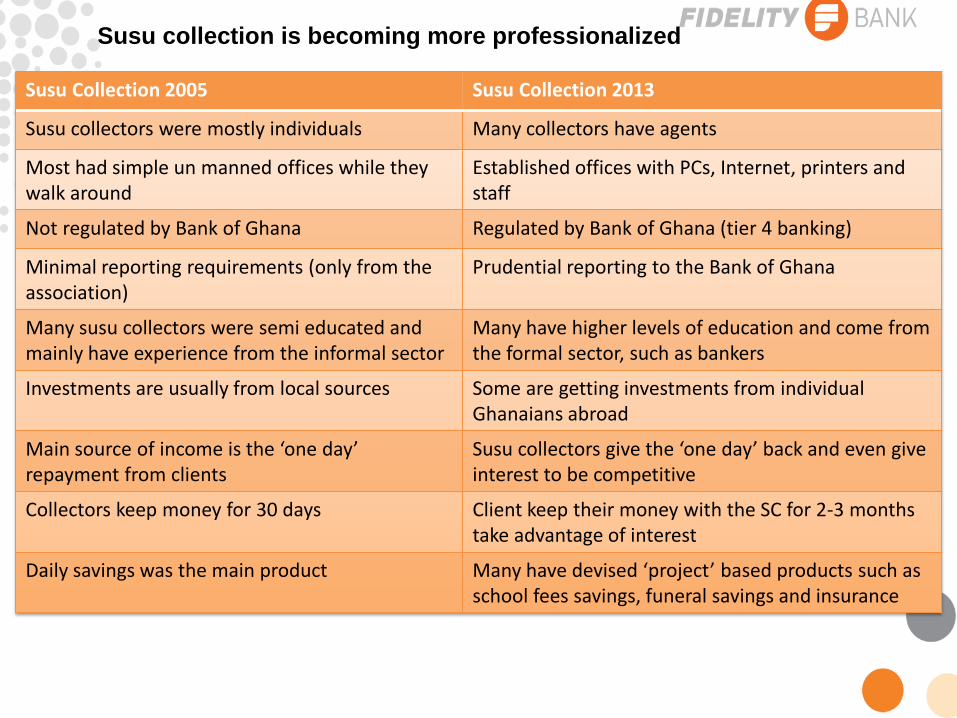

Susu Collection 2005 Susu Collection 2013

Susu collectors were mostly individuals Many collectors have agents

Most had simple un manned offices while they walk around

Established offices with PCs, Internet, printers and staff

Not regulated by Bank of Ghana Regulated by Bank of Ghana (tier 4 banking)

Minimal reporting requirements (only from the association)

Prudential reporting to the Bank of Ghana

Many susu collectors were semi educated and mainly have experience from the informal sector

Many have higher levels of education and come from the formal sector, such as bankers

Investments are usually from local sources Some are getting investments from individual Ghanaians abroad

Main source of income is the ‘one day’ repayment from clients

Susu collectors give the ‘one day’ back and even give interest to be competitive

Collectors keep money for 30 days Client keep their money with the SC for 2-3 months take advantage of interest

Daily savings was the main product Many have devised ‘project’ based products such as school fees savings, funeral savings and insurance

Susu collection is becoming more professionalized

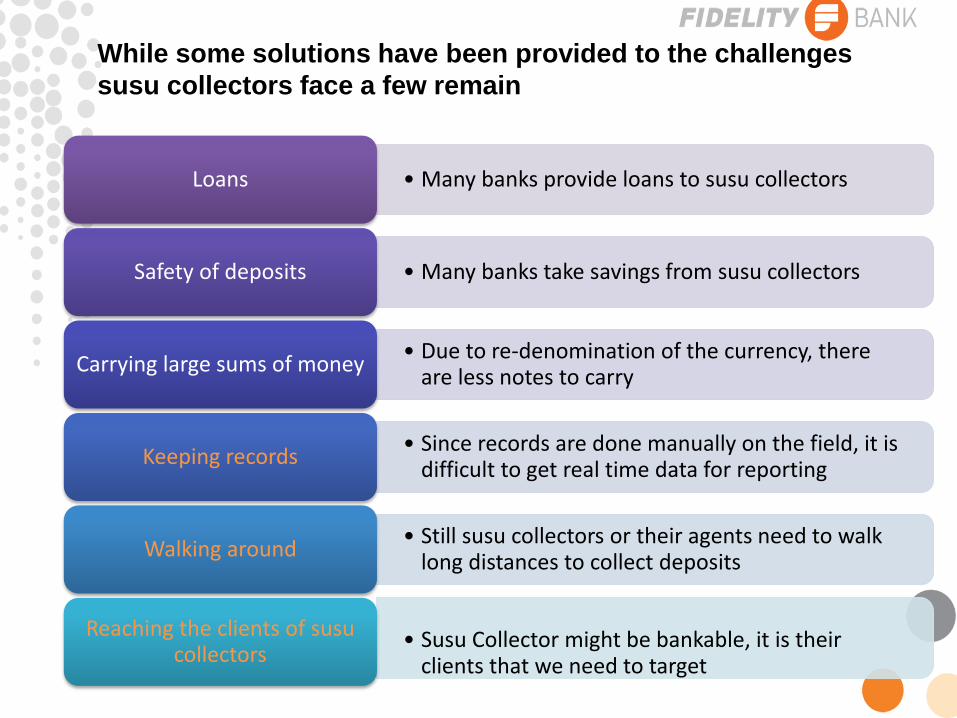

While some solutions have been provided to the challenges

susu collectors face a few remain

• Many banks provide loans to susu collectors Loans

• Many banks take savings from susu collectors Safety of deposits

• Due to re-denomination of the currency, there are less notes to carry

Carrying large sums of money

• Since records are done manually on the field, it is difficult to get real time data for reporting

Keeping records

• Still susu collectors or their agents need to walk long distances to collect deposits

Walking around

• Susu Collector might be bankable, it is their clients that we need to target

Reaching the clients of susu collectors

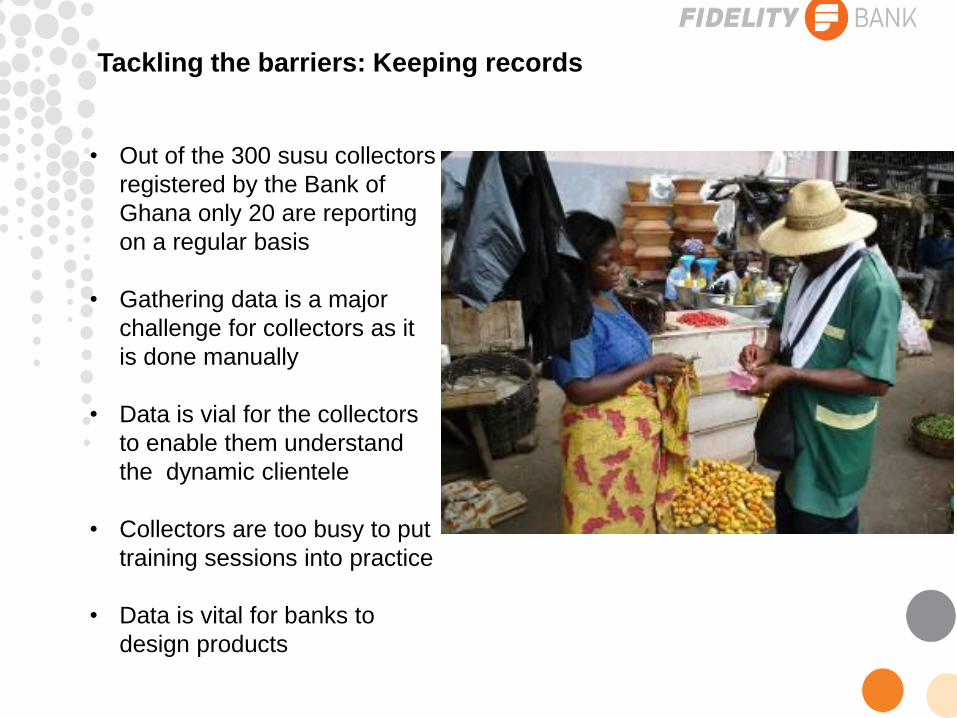

Tackling the barriers: Keeping records

• Out of the 300 susu collectors

registered by the Bank of

Ghana only 20 are reporting

on a regular basis

• Gathering data is a major

challenge for collectors as it

is done manually

• Data is vial for the collectors

to enable them understand

the dynamic clientele

• Collectors are too busy to put

training sessions into practice

• Data is vital for banks to

design products

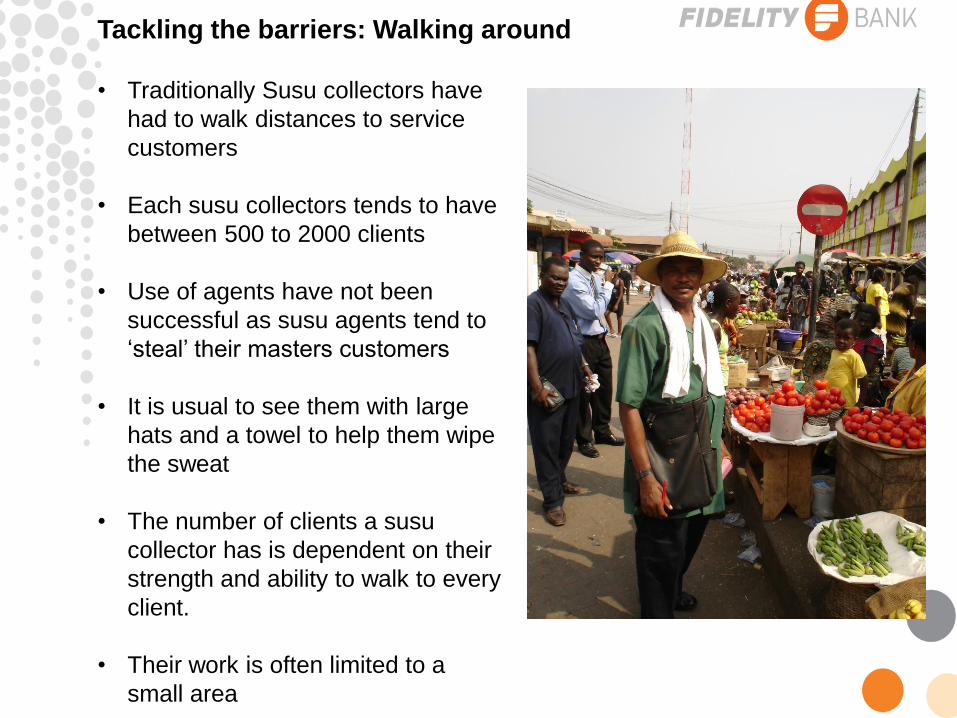

Tackling the barriers: Walking around

• Traditionally Susu collectors have

had to walk distances to service

customers

• Each susu collectors tends to have

between 500 to 2000 clients

• Use of agents have not been

successful as susu agents tend to

‘steal’ their masters customers

• It is usual to see them with large

hats and a towel to help them wipe

the sweat

• The number of clients a susu

collector has is dependent on their

strength and ability to walk to every

client.

• Their work is often limited to a

small area

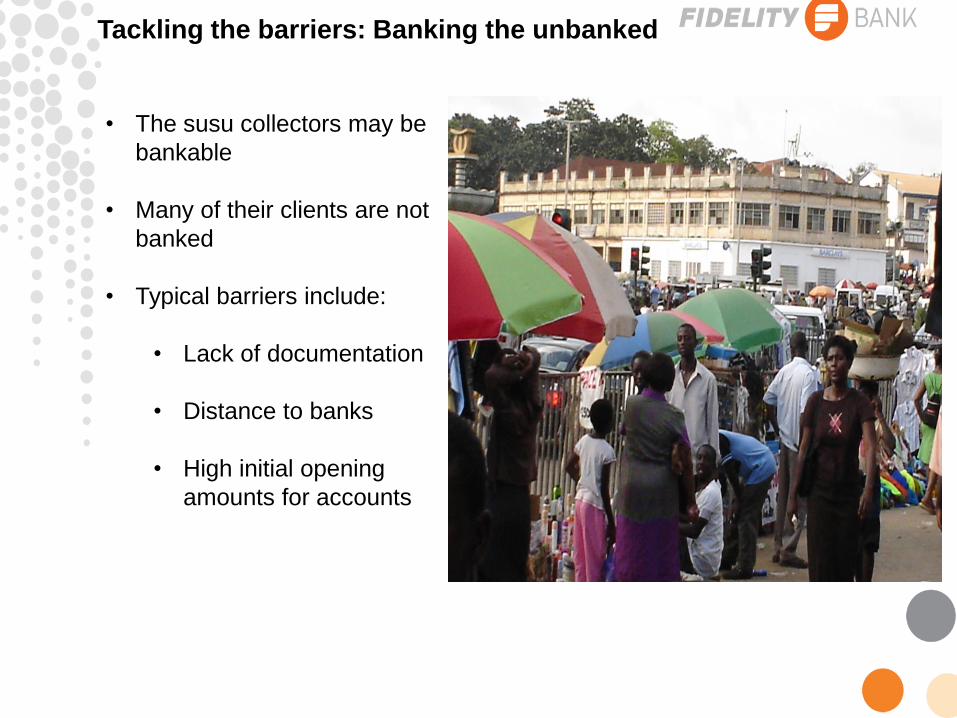

Tackling the barriers: Banking the unbanked

• The susu collectors may be

bankable

• Many of their clients are not

banked

• Typical barriers include:

• Lack of documentation

• Distance to banks

• High initial opening

amounts for accounts

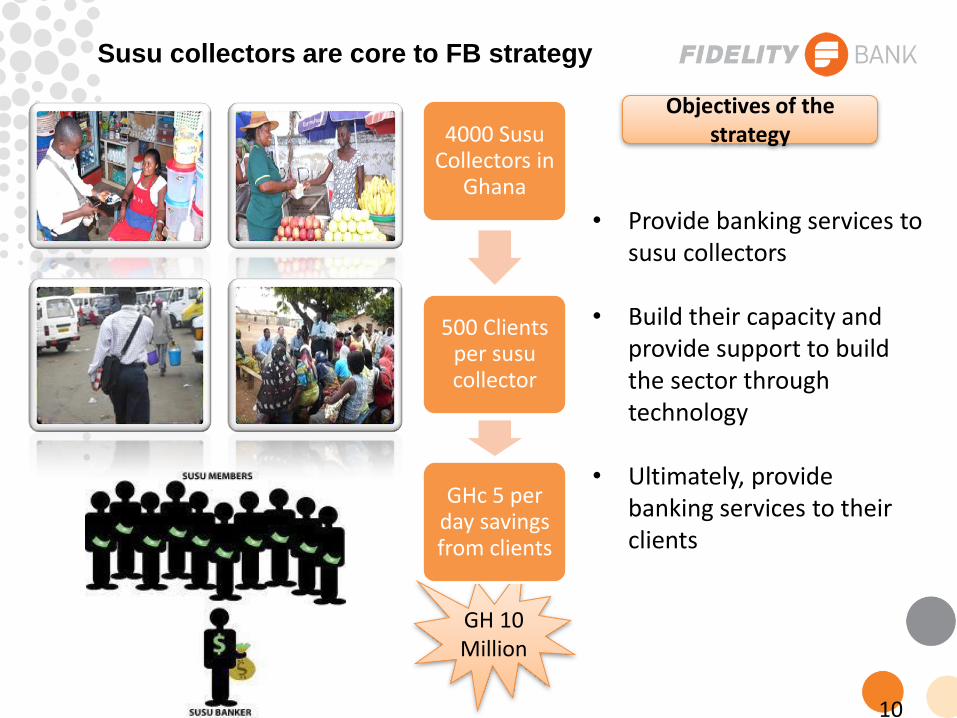

10

• Provide banking services to

susu collectors • Build their capacity and

provide support to build the sector through technology

• Ultimately, provide banking services to their clients

Objectives of the strategy

GH 10 Million

4000 Susu Collectors in

Ghana

500 Clients per susu collector

GHc 5 per day savings from clients

Susu collectors are core to FB strategy

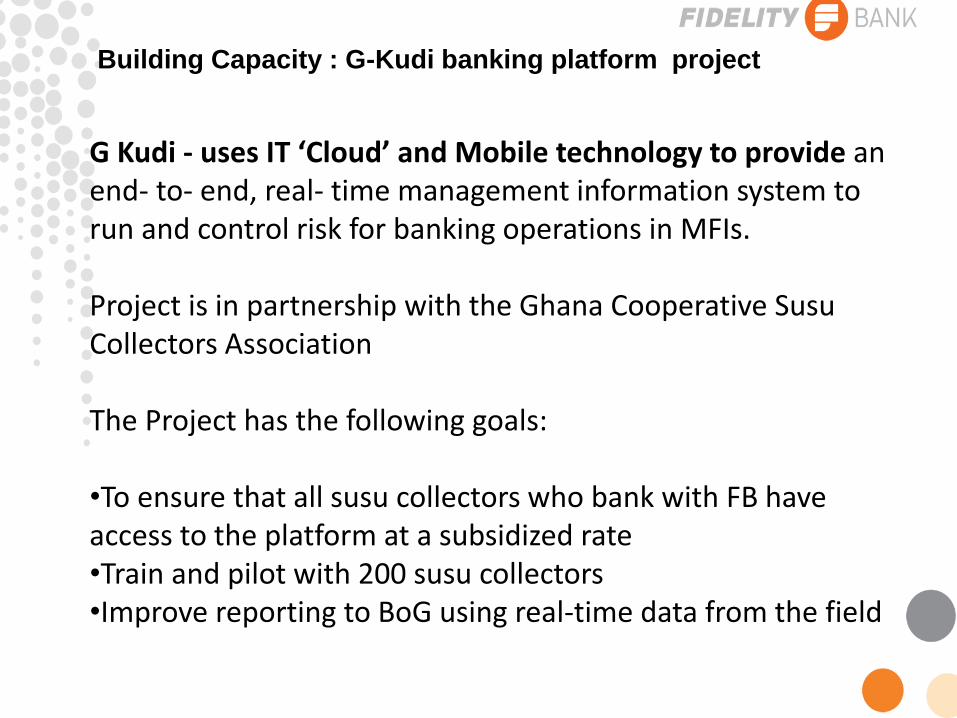

Building Capacity : G-Kudi banking platform project

G Kudi - uses IT ‘Cloud’ and Mobile technology to provide an end- to- end, real- time management information system to run and control risk for banking operations in MFIs. Project is in partnership with the Ghana Cooperative Susu Collectors Association The Project has the following goals: •To ensure that all susu collectors who bank with FB have access to the platform at a subsidized rate •Train and pilot with 200 susu collectors •Improve reporting to BoG using real-time data from the field

Using technology to improve collections

SC searches

for clients by name or number on

phone

View account

info

Select withdrawal or deposit

SC collects money or

gives it out

SMS is sent to client to

confirm transaction

Info hits backend

Banking the unbanked: Agency banking

• To provide a full fledged account that is convenient for the unbanked to access.

• Developed the ‘Smart Account’ and agency banking

• First bank in Ghana to be receive approval from Bank of Ghana for agency banking

• Opened over 2,000 accounts since 25th July 2013 with 10 agents including super

markets and their vendors – no adverts!

Key features of Smart account

• People can open account with $5. $2.50 for the card and $2.50 as a minimum

balance on the account.

• Open an account with one national ID (approved by BoG) in 5 min

• With the chip and pin enabled Smart Account card, one can:

Check balances mobile money

Withdraw Funds transfer

Deposit

• Channels are:

Smart Agents (merchants) Dedicated e-tellers at the branch

ATMs Internet

Mobile phone

Agency banking and Susu collection – the way forward

• Susu collectors can act as FB smart agents to facilitate opening of

accounts for clients

• Collectors can sell other services such as mobile top up and bill payments

• Insurance companies have shown interest in using agency banking to sell

their products

• Susu collectors can earn commissions on transactions that take place on

their POS in their offices

For Clients:

• They can deposit and withdraw into their accounts at any agent not only

their local susu collector

• Many companies see this as a solution to pay their low income workers

• Clients have more choice in the market place, they can transact directly

with the bank, through a susu collector or an agent

Thank you