Inflation Targeting in an Uncertain External Backdrop Lynch - Emerging Markets...Inflation Targeting...

35

1 Inflation Targeting in an Uncertain External Backdrop Mário Mesquita October 2008 Inflation Targeting in an Uncertain External Backdrop Mário Mesquita October 2008

Transcript of Inflation Targeting in an Uncertain External Backdrop Lynch - Emerging Markets...Inflation Targeting...

1

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008

2

I. An Uncertain External Backdrop

3

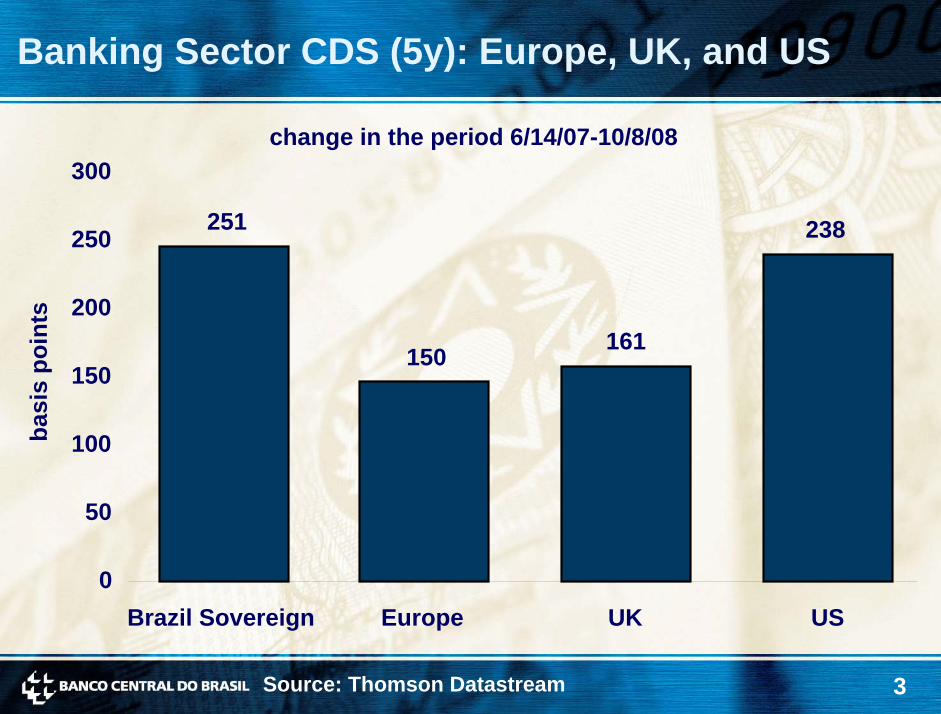

Banking Sector CDS (5y): Europe, UK, and US

change in the period 6/14/07-10/8/08300

Source: Thomson Datastream

basi

s po

ints

251 238250

200161150

150

100

50

0Brazil Sovereign UK USEurope

4

Ibovespa x Global Stock Exchange Indices

change in the period 6/14/07-10/10/085

MumbayShanghai CAC 40Nikkei FTSEDAX S&P HangSeng

Ibovespa IBEX 355

% c

hang

e

15

25

35

45

55Japan France UK Brazil Hong

KongChina Germany USA Spain India

Source: Bloomberg

5

Stock Price Indices: Banking Sector

change in the period 6/14/07-10/8/080

-49-51 -51

-10

% c

hang

e

-20

-30

-33-40

-50

-53-60

Brazil US UK Japan EuropeanUnion

6

Country Risk and Risk Aversion Index (RAVI)

BRL floating

basi

s po

ints

Russian crisis ARS floating

Brazil confidence crisis

subprime “first strike”

subprime “second strike”

credit crisis

0

500

1000

1500

2000

2500

-2.2

-1.2

-0.2

0.8

1.8

2.8

3.8

EMBI+ EMBI+ BR IARJan May Oct Feb Jul Nov Apr Aug Oct*98 99 00 02 03 04 06 07 08

Sources: JP Morgan Chase and Merrill Lynch *up to 10/8

7

CDS (5y): LatAm

Brazil

Argentina

Venezuela

Mexico

Latin

Chile0

200

400

600

800

1000

1200

1400

1600

6/14 7/21 8/27 10/3 11/912/16 1/22 2/28 4/5 5/12 6/18 7/25 8/31 10/8

18006/14/07-10/8/08

basi

s po

ints

Source: Thomson Datastream

8

CDS (5y): LatAm

change in the period 6/14/07-10/8/081800

15891600

basi

s po

ints

1400

1200 1069

1000

800 639600

400 251218187200

0Chile BrazilMexico LatinArgentinaVenezuela

Source: Thomson Datastream

9

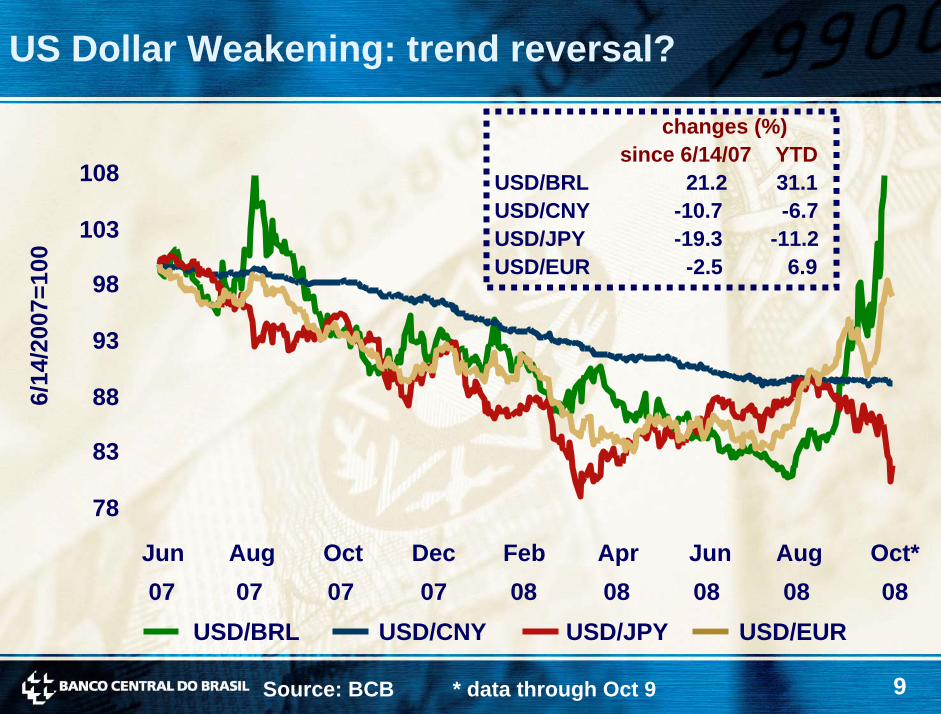

US Dollar Weakening: trend reversal?

changes (%)since 6/14/07 YTD

USD/BRL 21.2 31.1USD/CNY -10.7 -6.7USD/JPY -19.3 -11.2USD/EUR -2.5 6.9

108

6/14

/200

7=10

0

103

98

93

88

83

78

Jun Aug Oct Dec Feb Apr Jun Aug Oct*07 07 07 07 08 08 08 08 08

USD/BRL USD/CNY USD/JPY USD/EUR

Source: BCB * data through Oct 9

10

CPIs and Food Inflation - Selected Countries12

mon

th-a

ccum

ulat

ed %

CPI99 00 01 02 03 04 05 06 07

China **

-12-7-238

1318

Jan Jan Jan Jan Jan Jan Jan Jan Jan Aug08

Brazil

-505

1015202530

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

USA*

0.51.52.53.54.55.56.5

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

South Africa*

0

4

8

12

16

20

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

food inflation

Source: Datastream *CPI – Jul/08 **food inflation – Jul/08

11

II. Brazil: Increased Resilience to Shocks

12

Real Effective Exchange Rate

basket of 15 currencies180

99.4

160

Jun

94=1

00

140

120

100

80

60

Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Aug

88 90 92 94 96 98 00 02 04 06 08

Source: BCB

13

Current Account Balance

-33.4-28.8

-33.1

14.0

-1.9

-4.3 -4.2

-1.8

1.8

US$ bi

% of GDP

20 2

110

0

US$

bill

ion

0

% o

f GD

P-1-10

-2

-20-3

-30 -4

-5-4096 97 98 99 00 01 02 03 04 05 06 07 08* 09*

Source: BCB *2007: preliminary data; 2008/09: projection

14

Current Account/GDP

3210

% o

f GD

P

Source: BCB; 2008/09: projection

-8-7-6-5-4-3-2-1

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2009

-1.8 -1.9

15

Net FDI vs. Current Account

current account

accumulated in 12 months

net FDI

40

30

20

US$

bill

ion 10

0

-10

-20

-30

-40Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

Source: BCB

16

Trade Balance

12-month accumulated

exports

imports

US$

bill

ion

12-monthsurplus:

US$28.8 bi

194.9

166.1

40

80

120

160

200

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Sep08

Source: MDIC

17

Diversification of Exports Markets: 2008

Exports (12m through September)

USA14.5%

others20.2%

European Union24.2%

LatinAmerica

23.1%

Asia (exc. Middle East)

18.0%

Source: MDIC

18

Diversification of Exports by Products: 2008

Exports (12m through September)

primary products

semi-manufacturedproducts

37.2%

manufactured products48.8%

14.0%

Source: MDIC

19

BCB Purchases in the FX Market

9078.6

2.3

-7.2 -9.1

1.6 5.3

21.5

34.329.7

75

60

US$

bill

ion

45

30

15

0

-152000 2001 2002 2003 2004 2005 2006 2007 2008*

Source: BCB *12m through August

20

BCB Purchases in the FX Market (Accumulated Flows since Jan 2004)

US$

bill

ion

157.8

0

20

40

60

80

100

120

140

160

Jan04

Jun04

Nov04

Apr05

Sep05

Feb06

Jul06

Dec06

May07

Oct07

Aug08

Source: BCB

21

Net FDI and Net Foreign Investment in Stocks and Short- and Long-Term Fixed-Income

45

net FDI

equities + long-term fixed income

short-term fixed income-5

5

15

25

35

US$

bill

ion

-15Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

Source: BCB

22

International Reserves and Sovereign SpreadU

S$ b

illio

n

basi

spo

ints

reserves

avg EMBI+BR

Sources: BCB e JPMorgan Chase

0

300

600

900

1200

1500

1800

2100210

180

150

120

90

60

30

0

Jan May Sep Jan May Sep Jan Sep99 00 01 03 04 05 07 08

23

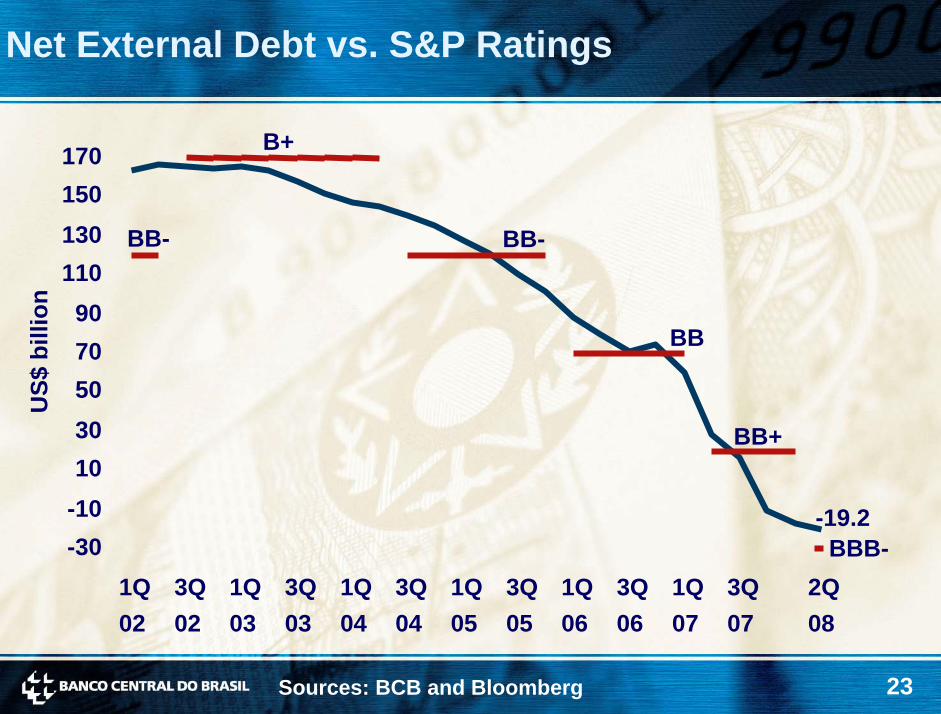

Net External Debt vs. S&P RatingsU

S$ b

illio

n

Sources: BCB and Bloomberg

BBB-

BB+

BB

BB-

B+

BB-

-19.2

170150130110

9070503010

-10-30

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

2Q08

24

External Sustainability Indicators

net external debt/exports net external debt/GDP

from 3.1 to -0.1* from 32.7 to –1.1%* 3.5 35

Source: BCB * Record low since the start of the series in 1970; 2008 – estimates.

%

(Aug)(Aug)

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0 30

25

20

15

10

5

0

-5

00 01 02 03 04 05 06 07 0800 01 02 03 04 05 06 07 08

25

External Vulnerability Indicators – Reserves

3006

reserves/short-term debt* (right)reserves/debt service (left)

96 98 00 02 04 06 08**95

2505

2004

%1503

1002

501

00

Source: BCB *includes medium- and long-term debt ammortizationsdue in the next 360 days. **estimates for August

26

Response of Debt/GDP Ratio to a 1% Exchange Rate Change

basi

spo

ints

-11.4-12

-8-4048

121620242832

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Aug08

Source: BCB

27

III. Brazil: Inflation Targeting in Practice

28

Contribution of Domestic and External Demandto GDP Growth

9 compared to the same quarter in the previous year

domestic demandexternal demand

8.08.5

-2.5-1.8

-2.6

8.6

7

5

3

%

1

-1

-3

-5

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

2Q08

Sources: IBGE and BCB

29

Inflation Targets

IPCA14IPCA (consensus)12.5targets12tolerance interval

%

10 9.38.9

0

2

4

6

8

1999

7.77.6

6.0

3.1

5.7

4.5

2000 2001 2002 2003 2004 2005 2006 2007

6.1 4.9

20092008

Source: BCB

30

IPCA Inflation

%

7.6

5.7

3.1

4.5

6.1

4.9

0

2

4

6

8

2004 2005 2006 2007 2008* 2009*

Sources: BCB and IBGE *market expectations (Oct 3)

% p

.m.

-0.3-0.2-0.10.00.10.20.30.40.50.60.70.80.9

avg. 2006:0.26%

avg. 2007:0.36%

avg. 2008:0.52%

avg. 2005:0.46%

Jan05

Jul05

Jan06

Jul06

Jan07

Jul07

Jan08

Sep08

31

Core Inflation

6-month moving average, annualized18

smoothednon-smoothed

exclusion16

14

12

% p

.a. 10

8

6

4

2

0Jan02

Jul02

Jan03

Jul03

Jan04

Jul04

Jan05

Jul05

Jan06

Jul06

Jan07

Jul07

Jan08

Sep08

Source: BCB

32

IPCA – 12-month change

6.509.5

non-tradables

services

%

6.258.56.00

7.55.75

% 5.506.5

5.255.55.00

4.54.75

4.503.5Jan Apr Jul Oct Jan Apr Sep07 07 07 07 08 08 08

33

IPCA Expectations and Target

15

central target

12-month IPCA expectations

upper limit

lower limit3

6

9

12

% p

.a.

0

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Dec10

Sources: BCB and IBGE

34

2009 IPCA Market Expectations

35Jul 31: 5.00Aug 29: 5.00Oct 3: 4.85

30

rela

tive

freq

uenc

y(%

)

25

20

15

10

5

0

<4.1 <4.3 <4.5 <4.7 <4.9 <5.1 <5.3 <5.5 <5.7 <5.9 <6.1

Source: BCB

35

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008

Inflation Targeting in an Uncertain External Backdrop

Mário MesquitaOctober 2008