Industry Forecast Latest Trends and Key Issues in the ... · PDF file4.2.1 Overall Flexible...

16

www.canadean-winesandspirits.com Industry Forecast Latest Trends and Key Issues in the Turkish Retail Packaging Market The Outlook for Primary Packaging Containers, Closures and Outers Reference Code: PK1117MR Published: January 2014

Transcript of Industry Forecast Latest Trends and Key Issues in the ... · PDF file4.2.1 Overall Flexible...

www.canadean-winesandspirits.com

1.

Industry Forecast

Latest Trends and Key Issues in the Turkish Retail

Packaging Market

The Outlook for Primary Packaging Containers, Closures and

Outers

Reference Code: PK1117MR

Published: January 2014

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR 2

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

Table of Contents

1. Executive Summary ................................................................................... 7

2. Overview of the Turkish Packaging Market.............................................. 9

3. Consumer Drivers .................................................................................... 12

3.1 A dynamic population structure creates varied packaging demands .................. 12

3.1.1 Larger household sizes to influence demand for bigger pack formats .............................. 12

3.1.2 Younger consumers will drive packaging changes ........................................................... 13

3.2 Macroeconomic factors influence buying behavior ............................................. 16

3.2.1 Declining unemployment rate encourages experimentation by Turkish population .......... 16

3.2.2 Growing credit card penetration to influence impulse purchases ..................................... 17

3.2.3 Rising aspirations of middle class consumers will drive the use of premium packaging .. 17

3.2.4 Tourists will create demand for packaging that is modified to their specific needs........... 17

3.3 The changing structure of the retail market will create demand for

packaging .......................................................................................................... 18

3.3.1 Growth of organized retailing will stimulate demand for retail ready packaging ............... 18

3.3.2 Expansion of virtual sales networks is creating newer avenues for secondary packaging19

4. Market Dynamics ...................................................................................... 21

4.1 Overview ............................................................................................................ 21

4.1.1 Turkish Packaging Market by Material .............................................................................. 21

4.1.2 Turkish Packaging Market by Industry Sector ................................................................... 23

4.1.3 Turkish Packaging Market by Pack Type .......................................................................... 24

4.2 Flexible Packaging ............................................................................................. 25

4.2.1 Overall Flexible Packaging Market .................................................................................... 25

4.2.2 Number of Flexible Packaging Packs by Market ............................................................... 26

4.2.3 Number of Flexible Packaging Packs by Type .................................................................. 27

4.2.4 Number of Flexible Packaging Packs by Closure Material ............................................... 28

4.2.5 Number of Flexible Packaging Packs by Closure Type .................................................... 28

4.2.6 Number of Flexible Packaging Packs by Outer Material ................................................... 29

4.2.7 Number of Flexible Packaging Packs by Outer Type ........................................................ 30

4.3 Paper & Board ................................................................................................... 31

4.3.1 Overall Paper & Board Packaging Market......................................................................... 31

4.3.2 Number of Paper & Board Packs by Market ..................................................................... 32

4.3.3 Number of Paper & Board Packs by Type ........................................................................ 33

4.3.4 Number of Paper & Board Packs by Closure Material ...................................................... 34

4.3.5 Number of Paper & Board Packs by Closure Type ........................................................... 34

4.3.6 Number of Paper & Board Packs by Outer Material ......................................................... 35

4.3.7 Number of Paper & Board Packs by Outer Type .............................................................. 36

4.4 Rigid Plastics ..................................................................................................... 37

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR 3

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

4.4.1 Overall Rigid Plastic Packaging Market ............................................................................ 37

4.4.2 Number of Rigid Plastic Packs by Market ......................................................................... 38

4.4.3 Number of Rigid Plastic Packs by Type ............................................................................ 39

4.4.4 Number of Rigid Plastic Packs by Closure Material .......................................................... 40

4.4.5 Number of Rigid Plastic Packs by Closure Type ............................................................... 40

4.4.6 Number of Rigid Plastic Packs by Outer Material ............................................................. 41

4.4.7 Number of Rigid Plastic Packs by Outer Type .................................................................. 42

4.5 Rigid Metal ......................................................................................................... 43

4.5.1 Overall Rigid Metal Packaging Market .............................................................................. 43

4.5.2 Number of Rigid Metal Packs by Market ........................................................................... 44

4.5.3 Number of Rigid Metal Packs by Type .............................................................................. 45

4.5.4 Number of Rigid Metal Packs by Closure Material ............................................................ 46

4.5.5 Number of Rigid Metal Packs by Closure Type ................................................................ 46

4.5.6 Number of Rigid Metal Packs by Outer Material ............................................................... 47

4.5.7 Number of Rigid Metal Packs by Outer Type .................................................................... 48

4.6 Glass ................................................................................................................. 49

4.6.1 Overall Glass Packaging Market ....................................................................................... 49

4.6.2 Number of Glass Packs by Market .................................................................................... 50

4.6.3 Number of Glass Packs by Type ....................................................................................... 51

4.6.4 Number of Glass Packs by Closure Material .................................................................... 51

4.6.5 Number of Glass Packs by Closure Type ......................................................................... 52

4.6.6 Number of Glass Packs by Outer Material ........................................................................ 53

4.6.7 Number of Glass Packs by Outer Type ............................................................................. 53

5. Packaging Design and Manufacturing Trends ....................................... 54

5.1 Key Design Trends ............................................................................................ 54

5.1.1 Innovative packaging enhances consumer convenience .................................................. 54

5.1.2 Sustainability is one of the key packaging trends in Turkey .............................................. 57

5.1.3 Lightweight is used widely to reduce cost by saving upon packaging material ................ 59

5.1.4 Premium packaging used as a strategic tool to improve shelf impact .............................. 60

5.1.5 Packaging firms need to more closely align themselves with manufacturers’ needs ....... 64

5.2 Key Manufacturing Trends ................................................................................. 65

5.2.1 Form filling and sealing machinery ensure high efficiency and quality in producing cups 65

5.2.2 Superior quality labels produced from metallization .......................................................... 65

5.2.3 Difficulties in raw material procurement are driving up costs ............................................ 67

6. Regulatory Environment .......................................................................... 68

6.1 Overview ............................................................................................................ 68

6.2 Key Directives and Laws .................................................................................... 68

6.2.1 Turkish Food Codex Labeling Regulation ......................................................................... 68

6.2.2 Cosmetics Labeling ........................................................................................................... 68

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR 4

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

6.2.3 Regulation on Packaging and Packaging Waste Control .................................................. 69

6.2.4 Regulation for Tobacco & Tobacco Products .................................................................... 69

7. Competitive Landscape ........................................................................... 71

7.1 Competitive Landscape by Packaging Material .................................................. 71

7.1.1 Paper & Board ................................................................................................................... 71

7.1.2 Rigid Plastics ..................................................................................................................... 72

7.1.3 Flexible Packaging ............................................................................................................ 72

7.1.4 Glass.................................................................................................................................. 73

7.1.5 Metal .................................................................................................................................. 73

7.2 Key Companies in Turkey Packaging Industry ................................................... 74

7.3 Key Financial Deals ........................................................................................... 75

8. Appendix ................................................................................................... 76

8.1 What is this Report About?................................................................................. 76

8.2 Time Frame ....................................................................................................... 76

8.3 Product Category Coverage ............................................................................... 77

8.4 Packaging Definitions......................................................................................... 82

8.4.1 Primary Packaging Container ............................................................................................ 82

8.4.2 Primary Packaging Closure ............................................................................................... 84

8.4.3 Primary Packaging Outer .................................................................................................. 85

8.5 Methodology ...................................................................................................... 86

8.5.1 Overall Research Program Framework ............................................................................. 86

8.6 About Canadean ................................................................................................ 89

8.7 Disclaimer .......................................................................................................... 89

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR 5

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

List of Figures

Figure 1: Market share of various packaging materials (%), 2013.................................................................................... 9 Figure 2: Average household size in different European countries in 2012 .................................................................... 13 Figure 3: Turkey’s Population Pyramid, 2012 ................................................................................................................ 14 Figure 4: Milk products targeted towards Children ......................................................................................................... 15 Figure 5: Declining unemployment rate in Turkey, 2009–2012 ...................................................................................... 16 Figure 6: Organized retail is growing in Turkey, 2007–2017 .......................................................................................... 18 Figure 7: Online Sales and Online Penetration in Turkey is growing .............................................................................. 20 Figure 8: Turkey Packaging by Material (Number of Packs, Million), 2010–2016 ........................................................... 21 Figure 9: Sectors by Packaging Material with the Four Highest Growth Rates (%), 2010–2016 ..................................... 22 Figure 10: Sectors by Packaging Material with the Four Lowest Growth Rates (%), 2010–2016 .................................... 23 Figure 11: Number of Flexible Packaging Units (Millions) and Annual Growth (%), 2010–2016 ..................................... 25 Figure 12: Sectors with the Largest Market Share Gains and Losses in Turkey Flexible Packaging, 2010–2016 ........... 26 Figure 13: Packaging Types with the Largest Market Share Gains and Losses in Turkey Flexible Packaging, 2010–2016

..................................................................................................................................................................................... 27 Figure 14: Closure Types with the Largest Market Share Gains and Losses in Turkey Flexible Packaging, 2010–2016 29 Figure 15: Number of Paper & Board Packaging Units (Millions) and Annual Growth (%), 2010–2016 .......................... 31 Figure 16: Sectors with the Largest Market Share Gains and Losses in Turkey Paper & Board Packaging, 2010–2016 32 Figure 17: Packaging Types with the Largest Market Share Gains and Losses in Turkey Paper & Board Packaging

2010–2016 .................................................................................................................................................................... 33 Figure 18: Closure Types with the Largest Market Share Gains and Losses in Turkey Paper & Board Packaging, 2010–

2016 .............................................................................................................................................................................. 35 Figure 19: Outer Types with the Largest Market Share Gains and Losses in Turkey Paper & Board Packaging, 2010–

2016 .............................................................................................................................................................................. 36 Figure 20: Number of Rigid Plastic Packaging Units (Millions) and Annual Growth (%), 2010–2016 .............................. 37 Figure 21: Sectors with the Largest Market Share Gains and Losses in Turkey Rigid Plastic Packaging, 2010–2016 ... 38 Figure 22: Packaging Types with the Largest Market Share Gains and Losses in Turkey Rigid Plastic Packaging, 2010–

2016 .............................................................................................................................................................................. 39 Figure 23: Closure Types with the Largest Market Share Gains and Losses in Turkey Rigid Plastic Packaging, 2010–

2016 .............................................................................................................................................................................. 41 Figure 24: Outer Types with the Largest Market Share Gains and Losses in Turkey Rigid Plastic Packaging, 2010–2016

..................................................................................................................................................................................... 42 Figure 25: Number of Rigid Metal Packaging Units (Millions) and Annual Growth (%), 2010–2016 ............................... 43 Figure 26: Sectors with the Largest Market Share Gains and Losses in Turkey Rigid Metal Packaging, 2010–2016 ..... 44 Figure 27: Packaging Types with the Largest Market Share Gains and Losses in Turkey Rigid Metal Packaging, 2010–

2016 .............................................................................................................................................................................. 45 Figure 28: Closure Types with the Largest Market Share Gains and Losses in Turkey Rigid Metal Packaging, 2010–

2016 .............................................................................................................................................................................. 47 Figure 29: Number of Glass Packaging Units (Millions) and Annual Growth (%), 2010–2016 ........................................ 49 Figure 30: Sectors with the Largest Market Share Gains and Losses in Turkey Glass Packaging, 2010–2016 .............. 50 Figure 31: Closure Type with the Largest Market Share Gains and Losses in Turkey Glass Packaging, 2010–2016 ..... 52 Figure 32: Re-sealable meat package can be separated in two parts for consumer convenience .................................. 55 Figure 33: Metal can extends shelf life and provides convenience in usage .................................................................. 55 Figure 34: Aerosol closure for Oil ensuring controlled usage ......................................................................................... 56 Figure 35: New packaging design uses less packaging material and with reduced carbon footprint .............................. 57 Figure 36: Environmentally-friendly paper bottles replacing glass packaging to reduce carbon footprint ........................ 58 Figure 37: Bericap’s lightweight closure for Danone Hayat brand .................................................................................. 59 Figure 38: PE film replaces corrugated packaging - enhances material reduction and volume compression ................. 60 Figure 39: Quadpack Turkey’s airless cosmetic packaging in pumps and syringes format............................................. 61 Figure 40: Premium packaged liquid detergent increases shelf appeal .......................................................................... 62 Figure 41: Shrink sleeve label holds gifts in the bottle ................................................................................................... 63 Figure 42: Key concerns of consumer goods manufacturers and packaging manufacturers, 2013 ................................ 64 Figure 43: THM 16/48 machinery produce cups at a high rate of efficiency and ensure quality and hygiene. ................ 65 Figure 44: Superior BOPP labels produced through advanced metallization ................................................................. 66 Figure 45: Crude Oil prices have risen sharply since 2003, and are forecast to remain high .......................................... 67 Figure 46: Turkey Packaging Competitive Landscape ................................................................................................... 74 Figure 47: Methodology ................................................................................................................................................. 86

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR 6

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

List of Tables

Table 1: Turkey Organized Retail Sales (TRY Billion), 2007–2017 ................................................................................ 19 Table 2: Turkey Online Sales (TRY Billion) and Online Penetration (%), 2007–2017 ..................................................... 20 Table 3: Turkey Packaging by Material (Number of Packs, Million), 2010, 2013 and 2016 ............................................ 22 Table 4: Turkey Packaging by Market (Number of Packs, Million), 2010, 2013 and 2016 .............................................. 23 Table 5: Turkey Packaging by Type (Number of Packs, Million), 2010, 2013 and 2016 ................................................. 24 Table 6: Number of Flexible Packaging Units (Millions) and Annual Growth (%), 2010–2016 ........................................ 25 Table 7: Turkey Flexible Packaging by Market (Number of Packs, Million), 2010, 2013 and 2016 ................................. 26 Table 8: Turkey Flexible Packaging by Type (Number of Packs, Million), 2010, 2013 and 2016 .................................... 27 Table 9: Turkey Flexible Packaging by Closure Material (Number of Packs, Million), 2010, 2013 and 2016 .................. 28 Table 10: Turkey Flexible Packaging by Closure Type (Number of Packs, Million), 2010, 2013 and 2016 ..................... 28 Table 11: Turkey Flexible Packaging by Outer Material (Number of Packs, Million), 2010, 2013 and 2016.................... 29 Table 12: Turkey Flexible Packaging by Outer Type (Number of Packs, Million), 2010, 2013 and 2016 ........................ 30 Table 13: Number of Paper & Board Packaging Units (Millions) and Annual Growth (%), 2010–2016 ........................... 31 Table 14: Turkey Paper & Board Packaging by Market (Number of Packs, Million), 2010, 2013 and 2016 .................... 32 Table 15: Turkey Paper & Board Packaging by Type (Number of Packs, Million), 2010, 2013 and 2016 ....................... 33 Table 16: Turkey Paper & Board Packaging by Closure Material (Number of Packs, Million), 2010, 2013 and 2016 ..... 34 Table 17: Turkey Paper & Board Packaging by Closure Type (Number of Packs, Million), 2010, 2013 and 2016 .......... 34 Table 18: Turkey Paper & Board Packaging by Outer Material (Number of Packs, Million), 2010, 2013 and 2016 ......... 35 Table 19: Turkey Paper & Board Packaging by Outer Type (Number of Packs, Million), 2010, 2013 and 2016 ............. 36 Table 20: Number of Rigid Plastic Packaging Units (Millions) and Annual Growth (%), 2010–2016 ............................... 37 Table 21: Turkey Rigid Plastic Packaging by Market (Number of Packs, Million), 2010, 2013 and 2016 ........................ 38 Table 22: Turkey Rigid Plastic Packaging by Type (Number of Packs, Million), 2010, 2013 and 2016 ........................... 39 Table 23: Turkey Rigid Plastic Packaging by Closure Material (Number of Packs, Million), 2010, 2013 and 2016 ......... 40 Table 24: Turkey Rigid Plastic Packaging by Closure Type (Number of Packs, Million), 2010, 2013 and 2016 .............. 40 Table 25: Turkey Rigid Plastic Packaging by Outer Material (Number of Packs, Million), 2010, 2013 and 2016 ............ 41 Table 26: Turkey Rigid Plastic Packaging by Outer Type (Number of Packs, Million), 2010, 2013 and 2016 ................. 42 Table 27: Number of Rigid Metal Packaging Units (Millions) and Annual Growth (%), 2010–2016 ................................. 43 Table 28: Turkey Rigid Metal Packaging by Market (Number of Packs, Million), 2010, 2013 and 2016 .......................... 44 Table 29: Turkey Rigid Metal Packaging by Type (Number of Packs, Million), 2010, 2013 and 2016............................. 45 Table 30: Turkey Rigid Metal Packaging by Closure Material (Number of Packs, Million), 2010, 2013 and 2016 ........... 46 Table 31: Turkey Rigid Metal Packaging by Closure Type (Number of Packs, Million), 2010, 2013 and 2016 ............... 46 Table 32: Turkey Rigid Metal Packaging by Outer Material (Number of Packs, Million), 2010, 2013 and 2016 .............. 47 Table 33: Turkey Rigid Metal Packaging by Outer Type (Number of Packs, Million), 2010, 2013 and 2016 ................... 48 Table 34: Number of Glass Packaging Units (Millions) and Annual Growth (%), 2010–2016 ......................................... 49 Table 35: Turkey Glass Packaging by Market (Number of Packs, Million), 2010, 2013 and 2016 .................................. 50 Table 36: Turkey Glass Packaging by Type (Number of Packs, Million), 2010, 2013 and 2016 ..................................... 51 Table 37: Turkey Glass Packaging by Closure Material (Number of Packs, Million), 2010, 2013 and 2016 ................... 51 Table 38: Turkey Glass Packaging by Closure Type (Number of Packs, Million), 2010, 2013 and 2016 ........................ 52 Table 39: Turkey Glass Packaging by Outer Material (Number of Packs, Million), 2010, 2013 and 2016 ....................... 53 Table 40: Turkey Glass Packaging by Outer Type (Number of Packs, Million), 2010, 2013 and 2016 ........................... 53 Table 41: Key Financial Deals in Turkey Packaging, 2012–2013................................................................................... 75 Table 42: Product Category Coverage .......................................................................................................................... 77 Table 43: Primary Packaging Container Materials ......................................................................................................... 82 Table 44: Primary Packaging Container Types .............................................................................................................. 82 Table 45: Primary Packaging Closure Materials ............................................................................................................ 84 Table 46: Primary Packaging Closure Types ................................................................................................................. 84 Table 47: Primary Packaging Outer Materials ............................................................................................................... 85 Table 48: Primary Packaging Outer Types .................................................................................................................... 85

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR 7

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

1. Executive Summary

The Turkish packaging market is expected to witness notable growth throughout the 2010–2016 period.

The Turkish packaging industry recorded a Compound Annual Growth Rate (CAGR) of xx.xx% during

2010–2013 in terms of the number of packs used and although this growth rate is expected to reduce

slightly during the 2013–2016period,it will nevertheless remain strong at xx.xx%.

Turkey has been experiencing demographic, societal, and economic changes over the last few years;

while some of these are long term trends, each of these changes have significantly impacted the retail

market within the country. Turkey has a large young population that is emerging to become an important

consumer segment. Falling unemployment levels have driven an increase in the disposable income,

thereby leading to a rise in consumer spending. In conjunction with this, shopping on credit has also

begun to find favor with Turkish consumers. Tourism and the rise in the use of online retailing are further

expected to impact the retail packaging market in Turkey.

Changes in packaging will be driven by needs of children and young consumers in Turkey

A large proportion of the Turkish population falls into the 0–34 age bracket. This encompasses a number

of key consumer groups – making them the most important target groups for CPG companies and

packaging manufacturers. The consumers in this segment are more likely to be impulsive shoppers than

their older counterparts. Packaging thus attains a greater deal of significance, as attractive packaging

formats with a high degree of visual shelf appeal are expected to be preferred by this segment of

consumers. Children, in particular become an important sub-segment for manufacturers as they will

increasingly launch products targeted specifically at kids. Packaging that contains vibrant colors, strong

graphics and popular cartoon characters will be attractive to this segment. In addition, the larger average

household structure in Turkey will drive demand for larger volume packs.

Decreasing unemployment levels and growing organized retail to boost demand for packaged

goods

Turkey has been witnessing a decline in unemployment levels in recent years and this has a positive

influence on the disposable incomes and spending levels of the population. Coupled with growing income

levels, an increase in organized retail will shift the consumption habits of Turkish people from procuring

loose and unpackaged products from unorganized stores to packaged goods from organized retailers. In

addition, the growing middle class and increase in disposable incomes will drive the demand for masstige

(mass+prestige) products. Turkish consumers also increasingly prefer to shop online. This broadens the

scope of packaging, making secondary packaging as crucial as the primary packaging as manufacturers

attempt to reduce or completely eliminate the amount of damage sustained by the product during transit.

Plastics increasingly preferred in Turkey as an alternative over other packaging materials

Paper & Board held the largest share in the Turkish retail packaging industry in 2013; however it is

forecast to be overtaken by both Flexible packaging and Rigid Plastics by 2016. Paper & Board

packaging, which recorded a negative CAGR of xx.xx% in 2010–2013 as a result of reduced demand

from Tobacco & Tobacco Products, will witness a positive CAGR of xx.xx% in 2013–2016 driven by a

growing demand from Food. Flexible packaging demand will be driven by the Food and Household Care

markets, while the demand for Rigid Plastics will be influenced by the Food and Non-Alcoholic Drinks

markets.

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR 8

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

Enhanced convenience and sustainability are key factors impacting the Turkish packaging

industry

Rising disposable incomes among Turkish consumers have made them open to the idea of product

experimentation and more inclined to purchase premium products. As a result, manufacturers are

increasingly engaging efforts to add value to their offerings and make them stand out from their

competitors. Offering enhanced convenience as a value addition to their products is an important strategy

being adopted by manufacturers. This has led to ongoing innovation in the Turkish packaging industry.

One example of this is the launch of olive oil in an aerosol format in glass, by Anadolu cam Sanayii A.S.,

for convenient and controlled dispensing of the product.

Sustainability has been gaining popularity among Turkish manufacturers. Consequently, attempts are

being made to make product packaging more sustainable through the use of biodegradable materials.

This has become an important factor impacting innovation in the Turkish packaging industry. An

illustration of this is the biodegradable paper bottle that is being manufactured by GreenBottle as an

alternative to the traditional glass wine bottles; the new pack is expected to bring about both falling

transportation costs and carbon footprint.

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

9

2. Market Dynamics

2.1 Overview

The overall retail packaging market in Turkey will witness notable growth throughout 2010–2016. The

number of packs used in Turkey increased at a CAGR of xx.xx% during 2010–2013 and is forecast to

increase at a CAGR of xx.xx% during 2013–2016.

This section will explore the dynamics of Turkish packaging market, reviewing changes during 2010–

2013 and forecast how the market will evolve during 2013–2016. This is first covered at an overall level,

after which the market is broken down by material.

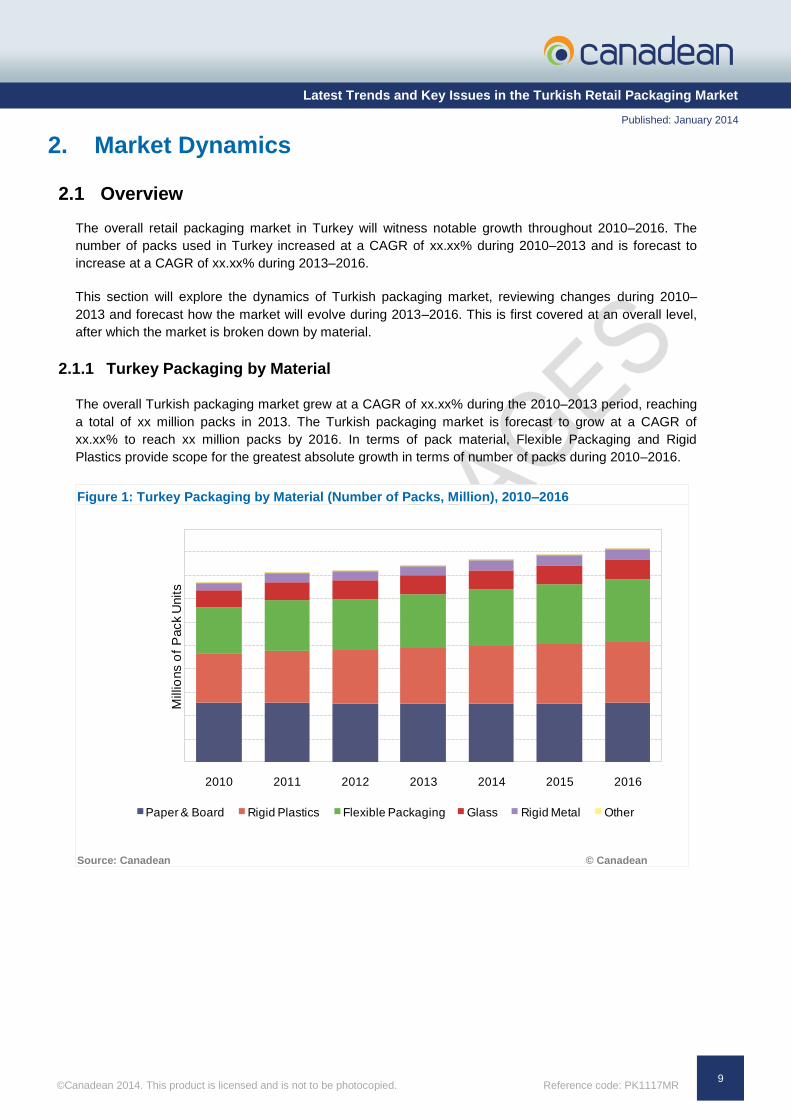

2.1.1 Turkey Packaging by Material

The overall Turkish packaging market grew at a CAGR of xx.xx% during the 2010–2013 period, reaching

a total of xx million packs in 2013. The Turkish packaging market is forecast to grow at a CAGR of

xx.xx% to reach xx million packs by 2016. In terms of pack material, Flexible Packaging and Rigid

Plastics provide scope for the greatest absolute growth in terms of number of packs during 2010–2016.

Figure 1: Turkey Packaging by Material (Number of Packs, Million), 2010–2016

Source: Canadean © Canadean

2010 2011 2012 2013 2014 2015 2016

Mill

ions o

f P

ack

Units

Paper & Board Rigid Plastics Flexible Packaging Glass Rigid Metal Other

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

10

Table 1: Turkey Packaging by Material (Number of Packs, Million), 2010, 2013 and 2016

Market 2010 2013 2016 CAGR 2010–2013 CAGR 2013–2016

Flexible Packaging

Glass

Other

Paper & Board

Rigid Metal

Rigid Plastics

Overall

Source: Canadean © Canadean

Rigid Plastics with largest number of rapidly-growing sectors

Rigid Plastics packaging has the largest number of high growth sectors: the number of packs used in

Beer & Cider, Soy Products and Ice Cream will record a CAGR in excess of xx.xx% along with Cat Care,

which will maintain a CAGR between xx.xx% and xx.xx%, during 2010–2016. Soy Products and Dog

Care in Paper & Board, Ice Cream and Cat Care sectors in Flexible packaging and Soy Products and

Beer & Cider in Rigid Metal will also witness a CAGR of more than xx.xx%.

The use of Rigid Metal for Textile Washing Products and Paper & Board for Cigarettes will register the

highest negative growth rates of more than xx.xx% CAGR in 2010–2016.

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

11

2.2 Flexible Packaging

2.2.1 Overall Flexible Packaging Market

The growth rate of Flexible Packaging in Turkey will increase steadily between 2013 and 2016. Overall

the Flexible packaging market in Turkey will experience steady and continuous growth, with the number

of packs increasing from xx million packs in 2010 to xx million packs in 2016.

Figure 2: Number of Flexible Packaging Units (Millions) and Annual Growth (%), 2010–2016

Source: Canadean © Canadean

Table 2: Number of Flexible Packaging Units (Millions) and Annual Growth (%), 2010–2016

2010 2011 2012 2013 2014 2015 2016

Number of Packs

Growth

Source: Canadean © Canadean

-xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

xxxx

2010 2011 2012 2013 2014 2015 2016

Annual G

row

th (

%)

Mill

ions o

f P

ack

Units

Pack Units (Millions) Annual Growth (%)

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

12

2.3 Paper & Board

2.3.1 Number of Paper & Board Packs by Market

The Food and Tobacco & Tobacco Products markets together accounted for xx.xx% of the total demand

for Paper & Board packs in 2013. Of these two markets, the Food industry will continue to drive the

growth of Paper & Board packs during 2013–2016 due to the growing demand from the Dairy Food

sector. The Non–Alcoholic Drinks industry will have the highest positive absolute growth in terms of the

number of packs in 2013–2016, influenced by the Soft Drinks sector. Demand for Tobacco & Tobacco

Products packaging will continue to decline during the 2013–2016 period. A steep decline in the volume

of Tobacco and Tobacco Products will be visible throughout 2010–2016. The Cigarettes sector will

witness the largest decline influenced by increasing regulations on Tobacco packaging.

Table 3: Turkey Paper & Board Packaging by Market (Number of Packs, Million), 2010, 2013 and

2016

Market 2010 2013 2016

CAGR 2010–

2013

CAGR 2013–

2016

Food

Health & Beauty

Household Care

Non-Alcoholic Drinks

Pet Care

Tobacco & Tobacco Products

Overall

Source: Canadean © Canadean

Figure 3: Sectors with the Largest Market Share Gains and Losses in Turkey Paper & Board

Packaging, 2010–2016

Source: Canadean © Canadean

Sector 2010 (Share %) 2016 (Share %) Change

Cigarettes xx.xx% xx.xx% xx.xx%

Sector 2010 (Share %) 2016 (Share %) Change

Soft Drinks xx.xx% xx.xx% xx.xx%

Dairy Food xx.xx% xx.xx% xx.xx%

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

13

2.4 Rigid Plastics

2.4.1 Number of Rigid Plastic Packs by Closure Type

Screw Top holds the largest share in closure types and accounted for xx.xx% of the market share in

2013. Increasing consumption of Soft Drinks will rapidly drive the growth in the use of Screw Top

closures. The demand for Foil, the second most preferred closure, will also increase, but will slowly face a

decline in its total market share in 2016.

Table 4: Turkey Rigid Plastic Packaging by Closure Type (Number of Packs, Million), 2010, 2013

and 2016

Closure Type 2010 2013 2016

CAGR 2010–

2013

CAGR 2013–

2016

Cap

Dispenser

Film

Flip/Snap Top

Foil

Lever Closure

None

Other

Prize Off

Screw Top

Sports Cap

Overall

Source: Canadean © Canadean

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

14

Figure 4: Closure Types with the Largest Market Share Gains and Losses in Turkey Rigid Plastic

Packaging, 2010–2016

Source: Canadean © Canadean

2.5 Rigid Metal

2.5.1 Number of Rigid Metal Packs by Outer Type

Paper & Board Boxes and Sleeves are the only outer pack types used for Rigid Metal packs in Turkey.

Both pack types will register growth in 2013–2016, albeit from a very small base.

Table 5: Turkey Rigid Metal Packaging by Outer Type (Number of Packs, Million), 2010, 2013

and 2016

Outer Type 2010 2013 2016

CAGR 2010–

2013

CAGR 2013–

2016

Box

None

Sleeve

Overall

Source: Canadean © Canadean

Type 2010 (Share %) 2016 (Share %) Change

Foil xx.xx% xx.xx% xx.xx%

Prize Off xx.xx% xx.xx% xx.xx%

Type 2010 (Share %) 2016 (Share %) Change

Screw Top xx.xx% xx.xx% xx.xx%

Sports Cap xx.xx% xx.xx% xx.xx%

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

15

3. Appendix

3.1 What is this Report About?

This report is the result of Canadean’s extensive market and company research covering the Turkish

packaging industry. It provides an analysis of changing packaging trends for eight key Consumer

Packaged Goods segments, competitive landscape, and the Turkish business environment. Consumption

of primary, outer, and closure packaging is analyzed in detail.

“Latest Trends and Key Issues in the Turkish Retail Packaging Market” provides a top-level overview and

detailed packaging, and company-specific insights into the operating environment for packaging

companies. It is an essential tool for companies active across the Turkish Packaging value chain, and for

new companies considering entering the market.

As such, this report is aimed at companies supplying to the following retail markets:

Alcoholic Drinks

Food

Health & Beauty

Home Improvement

Household Care

Non-Alcoholic Drinks

Pet Care

Tobacco & Tobacco Products.

3.2 Time Frame

For the purposes of this report, the following timeframes apply:

Historic period: 2010–2013*

Forecast period: 2014–2016

*The 2013 values are the latest estimates as on the publication date

©Canadean 2014. This product is licensed and is not to be photocopied. Reference code: PK1117MR

Latest Trends and Key Issues in the Turkish Retail Packaging Market

Published: January 2014

16

3.3 About Canadean

Canadean is a full-service business information provider with in-house market research capabilities. We

specialize in analysis across the Consumer Markets Value Chain, covering suppliers, producers,

distribution, and consumers.

Canadean’s dedicated research and analysis teams consist of experienced professionals with an industry

background in marketing, market research, consulting, and advanced statistical expertise. We offer value-

added market research, insight, and strategic analysis and our products help companies to make better,

more informed, strategic and tactical sales, and marketing decisions.

Canadean’s areas of expertise include online research, qualitative and quantitative research, industry

analysis, custom approaches, and actionable insights. In addition, Canadean has built a network of

consultants and specialist researchers across more than 60 countries, each with in-depth industry

experience and expertise enabling us to conduct unique and insightful research via our trusted business

communities.

3.4 Disclaimer

All Rights Reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by

any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of

the publisher, Canadean.

The facts of this report are believed to be correct at the time of publication but cannot be guaranteed.

Please note that the findings, conclusions and recommendations that Canadean delivers will be based on

information gathered in good faith from both primary and secondary sources, whose accuracy we are not

always in a position to guarantee. As such, Canadean can accept no liability whatsoever for actions taken

based on any information that may subsequently prove to be incorrect.

![arXiv:1812.11246v3 [econ.EM] 29 Jan 2019arXiv:1812.11246v3 [econ.EM] 29 Jan 2019. 1 Introduction ... Brock and Hansen,2017), and understanding household and professional forecast survey](https://static.fdocuments.in/doc/165x107/5e79028dedff0e11460ed47d/arxiv181211246v3-econem-29-jan-2019-arxiv181211246v3-econem-29-jan-2019.jpg)