Industrial Minerals Research

86

Oilfield bonanza Oil and gas drilling demands industrial minerals Mike O’Driscoll Global Head of Research, Industrial Minerals

Transcript of Industrial Minerals Research

Oilfield bonanza Oil and gas drilling demands industrial minerals

Mike O’Driscoll

Global Head of Research, Industrial Minerals

Outline

1. Overview

2. Barite

3. Proppants

4. Market potential indicators

5. Conclusions

Structure

Trends

Overview Primary mineral application fields in drilling

Drilling fluids (muds) • water- or non-water-based

• lubrication

• cuttings removal

• pressure control

• fluid loss control

Well cementing • cementing steel pipes

or casing to side of well

• sealing annulus

• sealing lost circulation zone

• plugging wells

Stimulation • to restore/enhance well

productivity

• acidizing

• hydraulic fracturing

Production • after successful exploration &

development hydrocarbons

drained from oil or gas field

Overview Simplified drilling operation

Source: OGP/IPIECA

Industrial minerals:

drilling fluids

Industrial minerals:

well cement

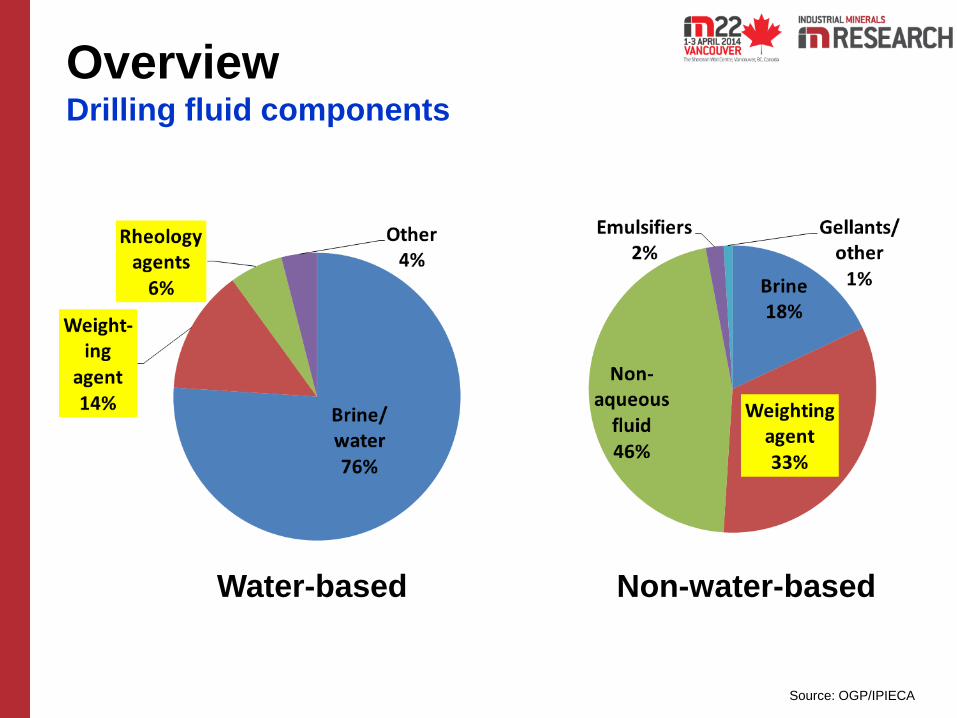

Overview Drilling fluid components

Water-based Non-water-based

Source: OGP/IPIECA

Overview Drilling fluid functions

• density, or weight

• viscosity

• filtration control

• rheology control, or

thinning/dispersing

• alkalinity, or ph-control

• lost-circulation control

• surface activity modification

• lubrication

• flocculation

• shale stabilization

• protection from toxic and/or

corrosive agents

Source: OGP/IPIECA

Overview Primary mineral applications

Weighting agents

high SG; help offset pressure; control liquid flow into wellbore from

formation; keep the hole open

eg. barite, haematite, calcium carbonate

Bridging agents

plug pore spaces at wellbore, restricting invasion of solids and fluids into

the formation

eg. calcium carbonate, salt

Viscosifiers

Carry cuttings to surface; build a cake against permeable formations;

lubricates drill string.

eg. sodium bentonite, treated calcium bentonite for freshwater muds;

attapulgite and sepiolite for saltwater muds; organophillic clays for oil muds

Overview Primary mineral applications

Lost circulation materials

used to plug or seal pores and cracks in the formation

eg. gilsonite, mica, diatomite, expanded perlite and vermiculite

(bentonites, organophilic clays)

Cross-linker

Hydrated polymers or gels (guar gum) are cross linked by borate ions to

provide increased viscosity. Benefits include, good proppant transport,

stable fluid rheology at high temperatures, low fluid loss, and good clean

up properties. eg. sodium borates

Stabilisers

Prevents dissolution of formation

eg. Gilsonite, salt, gypsum

Lubricants

Lubrication of drill bit and drill pipe

eg. graphite, bentonite

Proppants

Hold open fractures to enable oil and gas flow

eg. silica sand, calcined bauxite, calcined kaolin, magnesium silicate

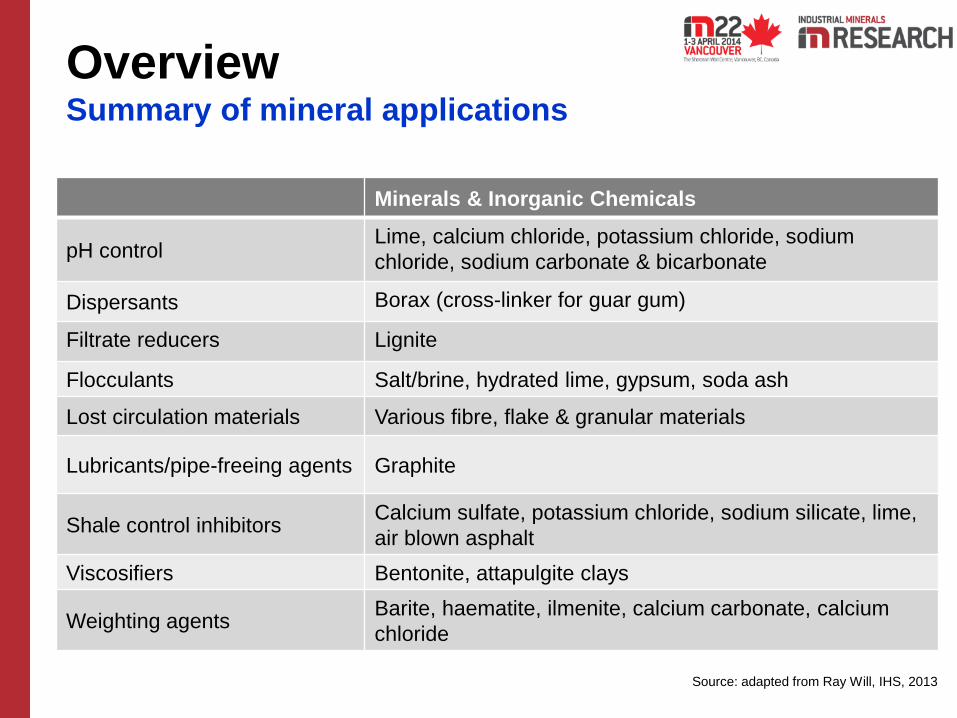

Overview Summary of mineral applications

Minerals & Inorganic Chemicals

pH control Lime, calcium chloride, potassium chloride, sodium

chloride, sodium carbonate & bicarbonate

Dispersants Borax (cross-linker for guar gum)

Filtrate reducers Lignite

Flocculants Salt/brine, hydrated lime, gypsum, soda ash

Lost circulation materials Various fibre, flake & granular materials

Lubricants/pipe-freeing agents Graphite

Shale control inhibitors Calcium sulfate, potassium chloride, sodium silicate, lime,

air blown asphalt

Viscosifiers Bentonite, attapulgite clays

Weighting agents Barite, haematite, ilmenite, calcium carbonate, calcium

chloride

Source: adapted from Ray Will, IHS, 2013

Overview Summary of mineral applications

Minerals & Inorganic Chemicals

Cementing

Accelerators Calcium chloride, sodium chloride, sodium sulphate, sodium

silicate

Dispersants Sodium chloride

Lost Circulation materials Gilsonite, perlite, mica, bentonite, silicates

Retarders Borax

Weighting agents Haematite, barite, sand, ilmenite, bentonite, attapulgite, pozzolan,

gilsonite, silicates

Stimulation

Fluid loss additives Silica flour, calcium carbonate

Proppants Silica sand, calcined bauxite, calcined kaolin, mag-silicate

Production

Hydrogen sulphide control Zinc & iron oxides

Water clarifiers Ferric chloride

Water injection chemicals Sodium sulphite

Source: adapted from Ray Will, IHS, 2013

Overview Supply chain

Mineral producer

Mineral processor/distributor

Oilfield service provider

Exploration/production Co.

Mineral trader

Trad. Captive Direct Captive

route processing buy production

Exploration, reserves, mining,

processing

Sourcing, logistics, financing

Sourcing, processing, storage,

logistics

Sourcing, processing, storage,

logistics, formulating, application

Application

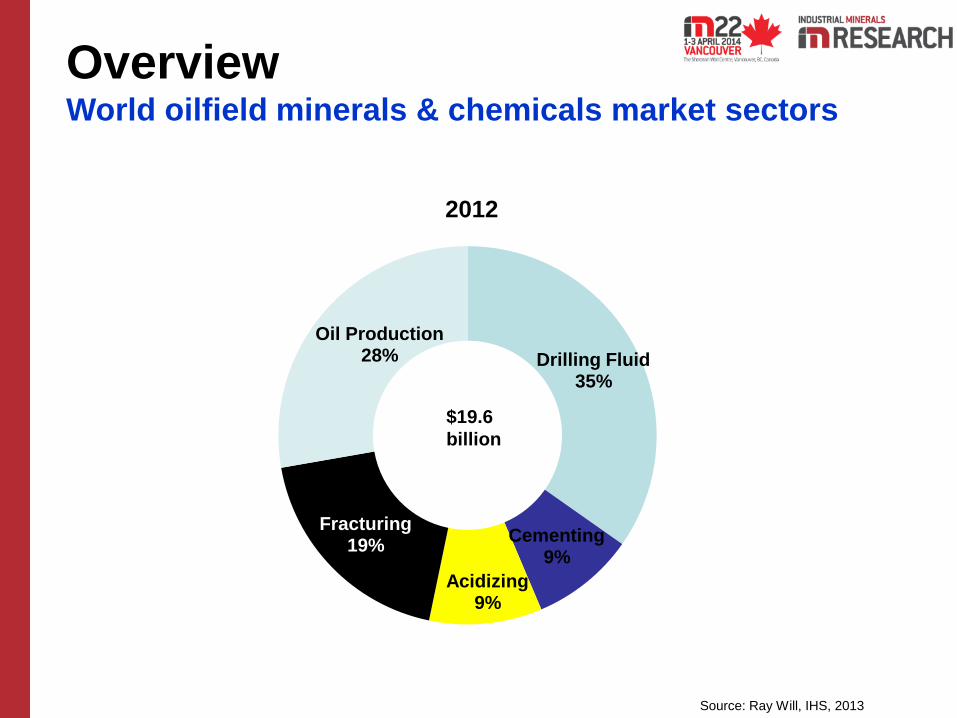

Overview World oilfield minerals & chemicals market sectors

Source: Ray Will, IHS, 2013

Drilling Fluid 35%

Cementing 9%

Acidizing 9%

Fracturing 19%

Oil Production 28%

2012

$19.6

billion

Overview World oilfield minerals & chemicals market sectors

by region

Source: Ray Will, IHS, 2013

North America 55%

Latin America 11%

Europe 6%

CIS 8%

Africa 7%

Middle East 7%

Asia Pacific 6%

2012

$19.6

billion

Barite

Barite Properties

Barite (barytes) and known as “heavy

spar”, is the naturally occurring mineral of

barium sulphate BaSO4 (65.7% BaO,

34.30% SO3).

Occur as either as bedded or

residual/eluvial deposits or vein and

cavity fillings

• natural product

• non-toxic

• relatively inexpensive

• inert - chemically and

physically unreactive

• high specific gravity (3.9-4.6)

• good sound-deadening and

radiation-shielding

• low oil adsorption

Barite API specifications

Density SG min. 4.10 & 4.22g/ml

Water soluble alkaline

earth metal

max. 250 ppm

>75um residue

<8um fines

max. 3%

max. 30%

Cadmium

Mercury

Extractable carbonates

Extractable sulphides

max. 3ppm

max. 1ppm

3,000mg/l max

50 mg/l max

But also need to consider: Pb, As toxic metals

EPA regs offshore

SiO2, Fe2O3, Al2O3 grindability

Barite World production 8.5m tonnes 2013

Source: data from The Barytes Association

USA

0.7

Mexico

0.12

Peru

0.12

India

1.7

Morocco

0.92 Turkey

0.25

Iran

0.2

Kazakhstan

0.2

China

3.5

Europe

0.16

Thailand

0.10

Vietnam

0.09

Also from: Algeria Russia Pakistan

Barite World production 8.5m tonnes 2013

43%

21%

11%

9%

3% 3%

2% 2%

2% 2%

1% 1% China

India

Morocco

USA

Turkey

Iran

Kazakhstan

Europe

Mexico

Peru

Thailand

Vietnam

Source: The Barytes Association

95% from:

Barite World production trend 2003-2013

0

1

2

3

4

5

6

7

8

9

10

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Mill

ion

s

Source: based on USGS data

Barite

Cobachi barite deposit, Sonora, Mexico Courtesy: Ken Santini

Mangampet, Andhra Pradesh, India Courtesy: IBC Ltd

Barite World consumption by market 8.4m tonnes 2013

Source: The Barytes Association

Barite World consumption by region 8.4m tonnes 2013

Source: The Barytes Association

38%

21% 10%

9%

5%

5% 5%

4% 3% USA

China

Gulf States

Europe

S. America

Russia/CIS

India

Africa

Malaysia

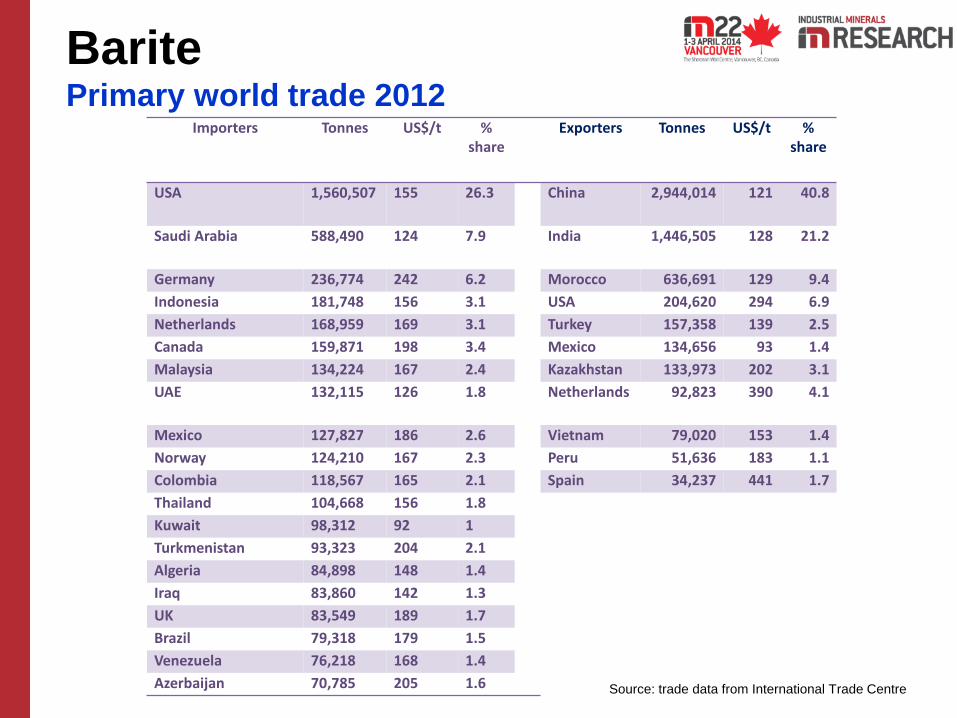

Barite Primary world trade 2012

Importers Tonnes US$/t % share

Exporters Tonnes US$/t % share

USA 1,560,507 155 26.3 China 2,944,014 121 40.8

Saudi Arabia 588,490 124 7.9 India 1,446,505 128 21.2

Germany 236,774 242 6.2 Morocco 636,691 129 9.4

Indonesia 181,748 156 3.1 USA 204,620 294 6.9

Netherlands 168,959 169 3.1 Turkey 157,358 139 2.5

Canada 159,871 198 3.4 Mexico 134,656 93 1.4

Malaysia 134,224 167 2.4 Kazakhstan 133,973 202 3.1

UAE 132,115 126 1.8 Netherlands 92,823 390 4.1

Mexico 127,827 186 2.6 Vietnam 79,020 153 1.4

Norway 124,210 167 2.3 Peru 51,636 183 1.1

Colombia 118,567 165 2.1 Spain 34,237 441 1.7

Thailand 104,668 156 1.8

Kuwait 98,312 92 1

Turkmenistan 93,323 204 2.1

Algeria 84,898 148 1.4

Iraq 83,860 142 1.3

UK 83,549 189 1.7

Brazil 79,318 179 1.5

Venezuela 76,218 168 1.4

Azerbaijan 70,785 205 1.6 Source: trade data from International Trade Centre

Barite US barite supply-demand & drilling 2003-2013

0

500

1000

1500

2000

2500

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

B-H rig count

Source: based on USGS data

Note: net import reliance of around 80% for US barite market; China has been main source accounting for 90-95% imports 2003-13

2013

US production

US consumption Baker Hughes

rig count

tonnes

Barite Key trends & developments

• Prices have stabilised in US$120-150/t FOB range

• Issues with Chinese and Indian supply have encouraged consumers

to seek alternative sources

• Global resource availability has been extended through acceptance

and increasing use of 4.0 and 4.1 SG barite; API added 4.1 SG

• At same time, concerns over HM impurities from new sources

eg. As, Pb contents – talk of incorporating into API specs.

• Major players increasing processing capacity at traditional bases

eg. India: RockFin, IBC

USA: Baroid, Baker-Hughes, Excalibar, Superior Weighting

• Emergence of potential new supply sources:

- greenfield & existing/dormant

- move to establish sources & processing near markets

• Use of micronised barite: reduces sag in shallow, horizontal wells

Barite Trends & developments – potential/emerging new sources

Guatemala

Mexico

Morocco

Liberia

Zimbabwe

Thailand/Laos

Kazakhstan

Pakistan

Proppants

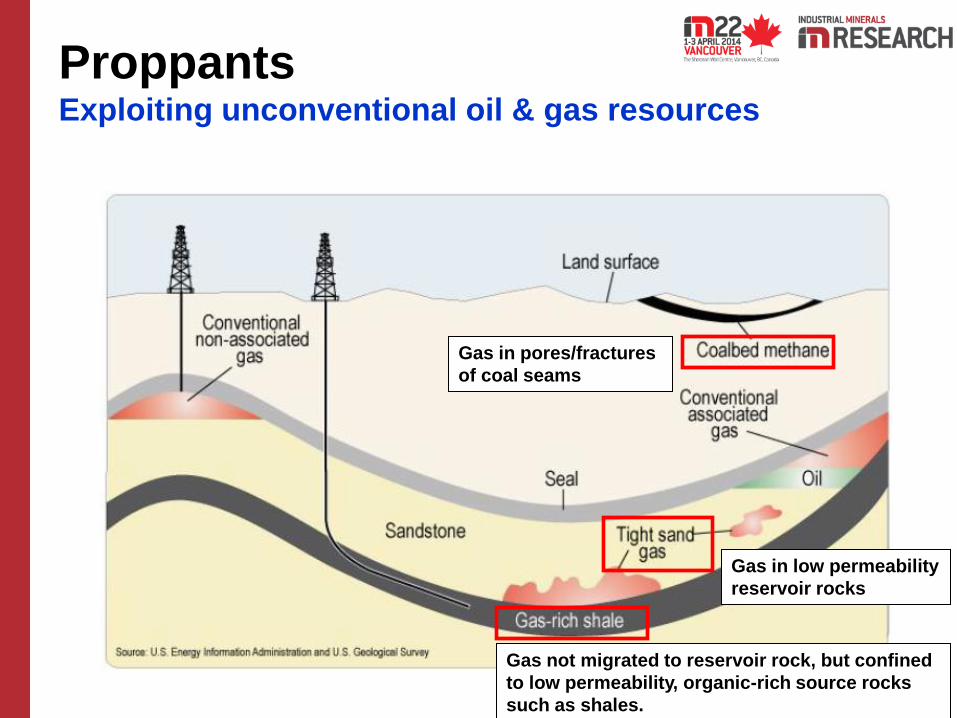

Proppants Exploiting unconventional oil & gas resources

Gas in pores/fractures

of coal seams

Gas in low permeability

reservoir rocks

Gas not migrated to reservoir rock, but confined

to low permeability, organic-rich source rocks

such as shales.

Propping agent

= “proppant”

Props open

fracture

Permits

oil/gas flow

(conductivity)

Proppants Hydraulic fracturing

Source: Baker Hughes

Drinking water acquifer

<1,000ft (305m)

Target rock formation

6-10,000ft (1,829-3,048m),

fractures extend ’00s ft

8,000ft (2,438m)

Proppants Fracturing depth perspective

1860s

“oilwell

shooting”

1930s

“well

acidizing”;

“pressure-

parting”

1947

Harris/ Clark

Stanolind Oil &

Gas Co.,

Hugoton, KS

20,000lbs sand

1949

patent filed;

excl. lic.

Halliburton,

Stephens OK,

Orchard TX;

100-150lbs,

332 wells; 75%

up in output

mid-1950s

more patents;

3,000

wells/mth;

400 lbs sand,

20/40 mesh

mid-1960s

water as

standard;

additives;

higher volume

proppants,

& coarser

1968

1st 1.5m lb

frac, Pan

American

Petroleum

Corp.

Proppants Evolution of fracturing:

1860-1970: early days, small proppant volumes

1981

George

Mitchell

Barnett

Shale, TX

1983

First ceramic

proppant used

1984

First resin

coated

proppant

1990-99

Mitchell Energy

perfected use of

proppants + water

in horizontal

wellbores

2000

ceramic and

resin coated

proppants to

exceed 1bn

lbs/yr

2008+

>50,000 frac stages

completed worldwide,

8-40 frac stages/well;

US oil production

increased by est. 30%

and gas 90%;

average 60,000 gal,

100,000lbs sand/well,

to >1m gal and 4-6m

lbs proppant/well

Proppants Evolution of fracturing:

1980-present: technology matures, larger proppant volumes

Source: Montgomery & Smith 2010

17 March 1949

Duncan, OK

1st fracturing by

Halliburton for

Stanolind Oil Co.

Proppants Evolution of fracturing: Past

Source: Baker Hughes

Proppants Evolution of fracturing: Present

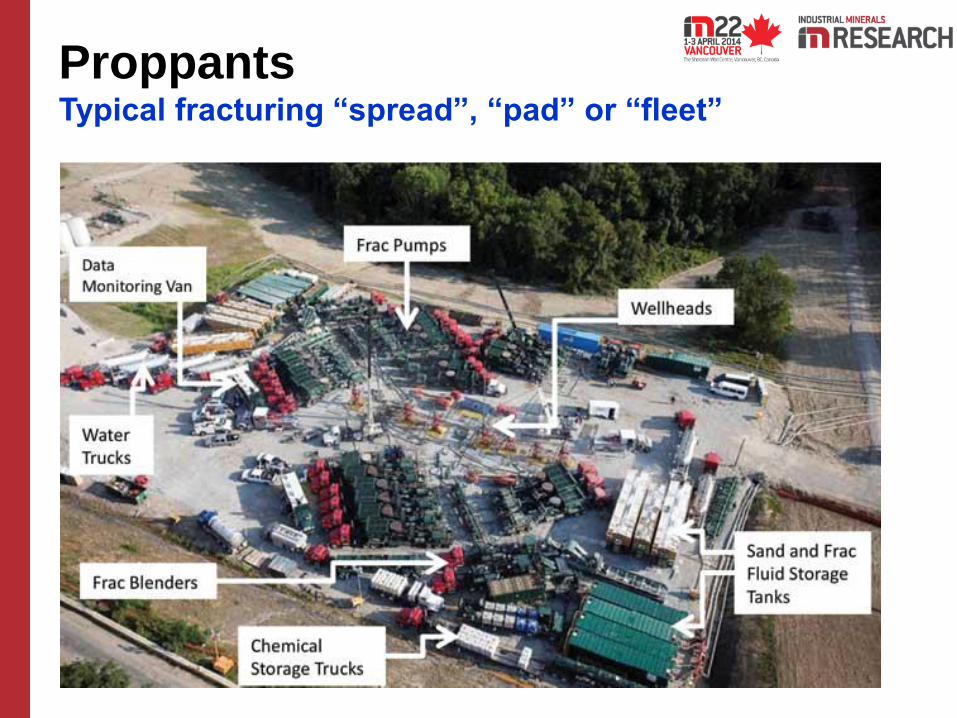

Proppants Typical fracturing “spread”, “pad” or “fleet”

Largest fracturing treatment = 661,500lbs

ceramic proppant @ 10,000HP

Proppants Example: Priobskoe oilfield, Western Siberia

• walnut shells

• silica sand

• alumino-silicates

• resin coated proppants

• fused zirconia

• plastic pellets

• steel shot

• glass beads

• aluminium pellets

• fly ash

“The ideal proppant is one that has:

• the specific gravity of water,

• the strength of iron,

• and is cheaper than dirt!”

Proppants Made from a variety of raw materials

Silica sand (“frac sand”) Ceramic proppants

Resin coated proppants

Proppants Primary proppant categories

Silica sand (“frac sand”) Ceramic proppants

Derived from silica sand

deposits, 99% SiO2

Derived mainly from

calcined bauxite, kaolin,

blends of bauxite & kaolin,

>50% Al2O3

(also magnesium silicate,

high purity alumina)

Proppants Primary proppant categories

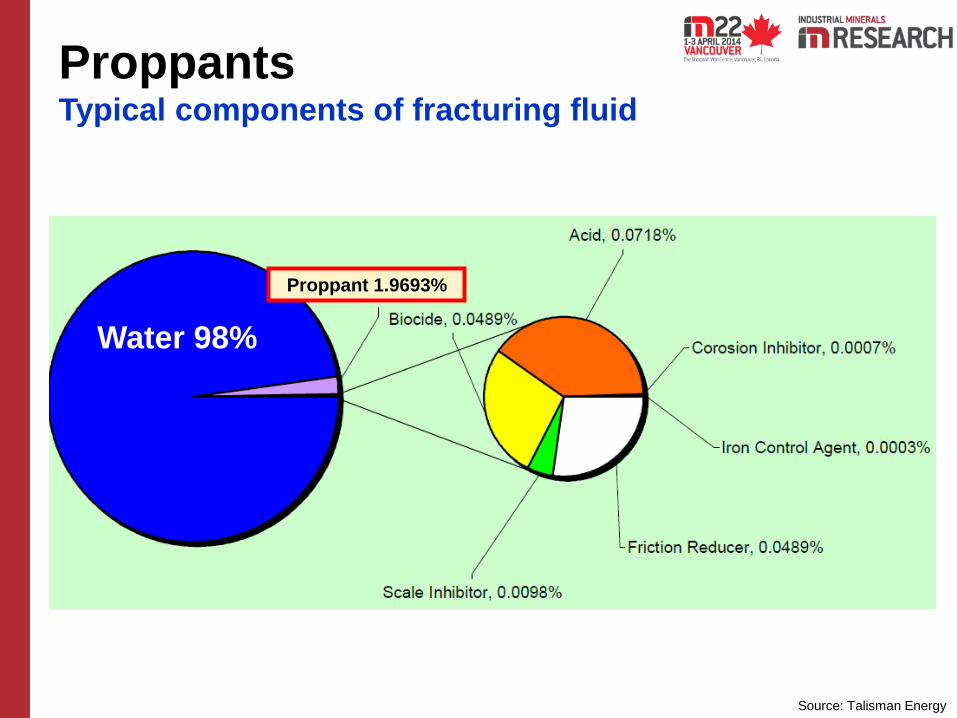

Proppants Typical components of fracturing fluid

Water 98%

Proppant 1.9693%

Source: Talisman Energy

American Petroleum

Institute

API RP 56

API RP 60

• Chemical composition

• Size fraction

• Roundness & sphericity

• Crush resistance

• Acid solubility

• Turbidity

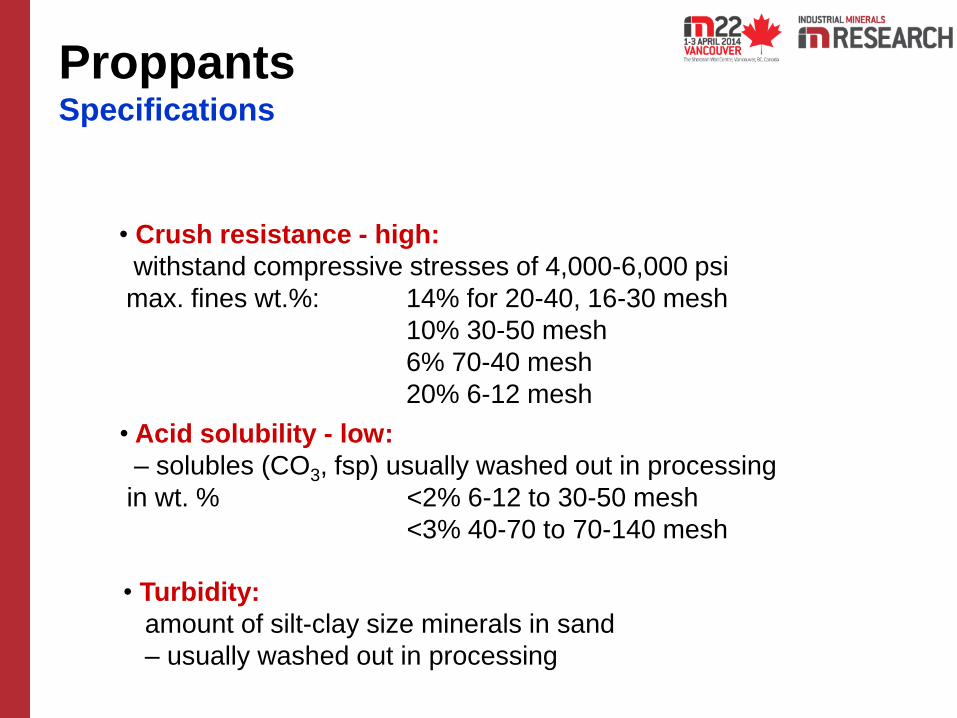

Proppants Specifications

Frac sand

Quartz composition

99+% SiO2

Ceramic proppants

Alumina composition

>50% Al2O3

Proppants Specifications

90% to fall within range

Proppants Specifications

Source: redrawn from

Krumbein & Sloss 1955

API

≥ 0.6

Proppants Specifications

• Crush resistance - high:

withstand compressive stresses of 4,000-6,000 psi

max. fines wt.%: 14% for 20-40, 16-30 mesh

10% 30-50 mesh

6% 70-40 mesh

20% 6-12 mesh

• Acid solubility - low:

– solubles (CO3, fsp) usually washed out in processing

in wt. % <2% 6-12 to 30-50 mesh

<3% 40-70 to 70-140 mesh

• Turbidity:

amount of silt-clay size minerals in sand

– usually washed out in processing

Proppants Specifications

Source: IM Research

Proppants Proppant comparison

Source: IM Research

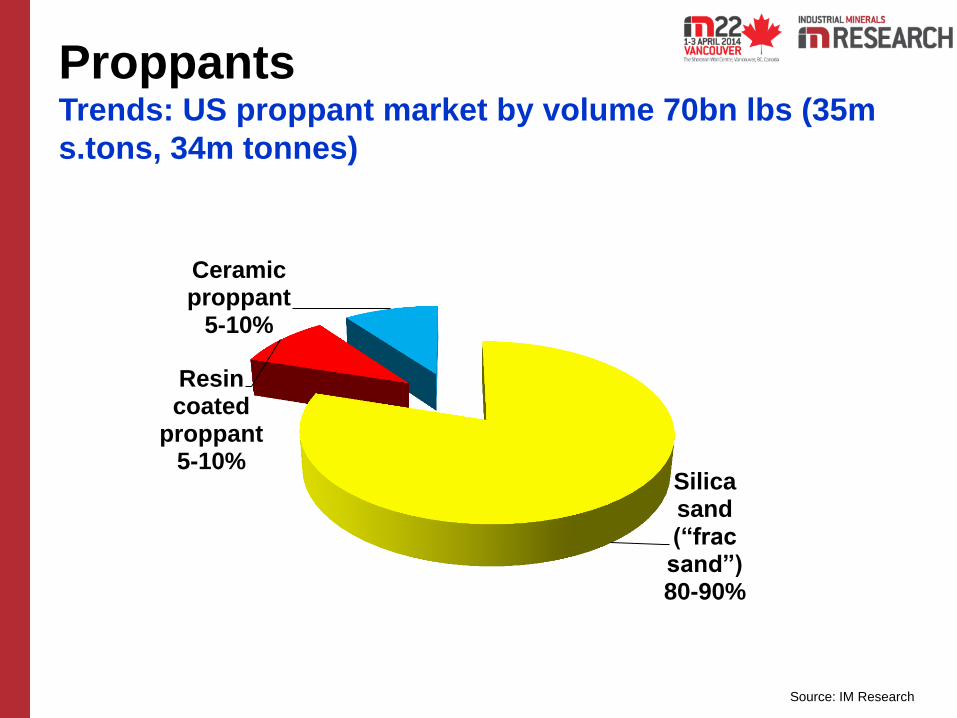

Proppants Trends: US proppant market by volume 70bn lbs (35m

s.tons, 34m tonnes)

Silica sand (“frac sand”) 80-90%

Resin coated

proppant 5-10%

Ceramic proppant

5-10%

Source: based on USGS data

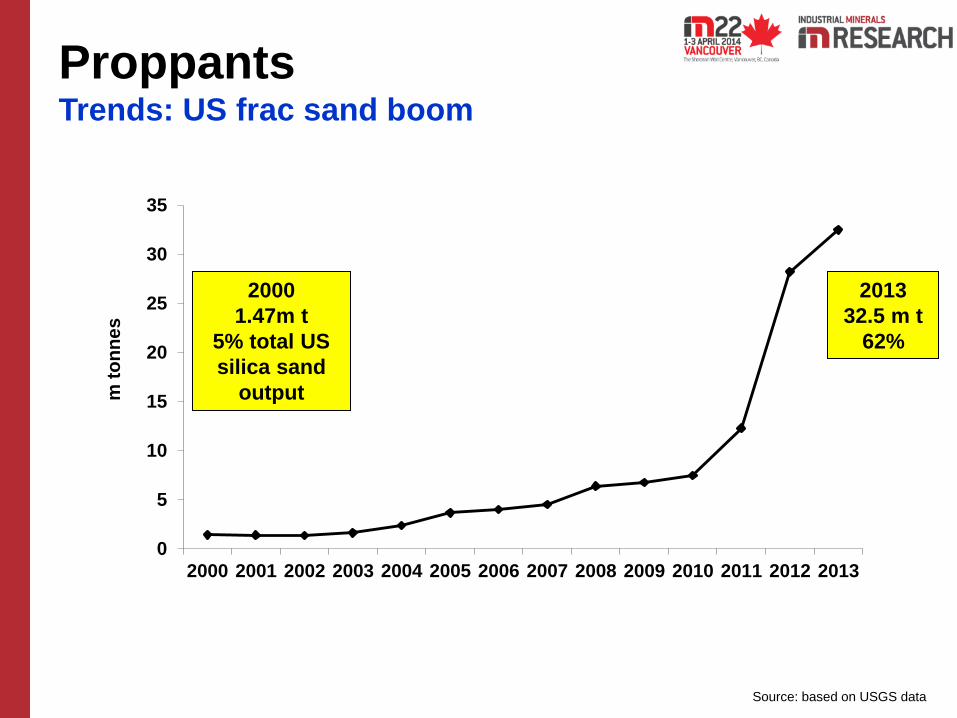

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

m t

on

nes

2000

1.47m t

5% total US

silica sand

output

2013

32.5 m t

62%

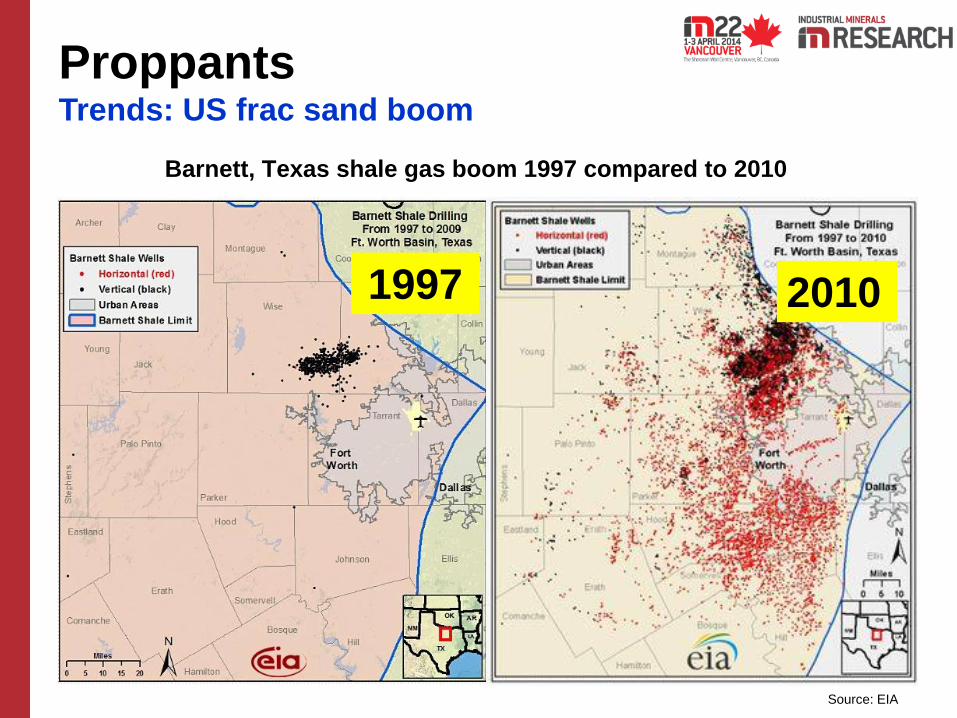

Proppants Trends: US frac sand boom

Source: Imerys 2014

Potential market demand Trends: World proppant demand growth

tonnes

Source: EIA

Proppants Trends: US frac sand boom

Barnett, Texas shale gas boom 1997 compared to 2010

1997 2010

Proppants Trends: Key US frac sand deposits

Cambrian-Ordovician

sandstone formations

• St Peter (Ottawa):

MN, MS, IL, NE, SD, WI

• Hickory (Brady): TX

• Jordan: MN, WI

• Wonowoc: WI

• Mt Simon: IL, MN, OH, WI

• Riley: TX

• Old Creek: OK

• Bidahochi: AZ

• river deposits

• inter-coastal plain deposits

• dune deposits

State of Wisconsin, USA

Frac sand operations

October 2013:

84 operational

15 in development

25 permitted

17 proposed

4 stalled

Source: Wisconsin Center for Investigative Journalism

Proppants Trends: US frac sand boom; Wisconsin hub

Mine/plant truck Transload rail Transload truck Frack pad

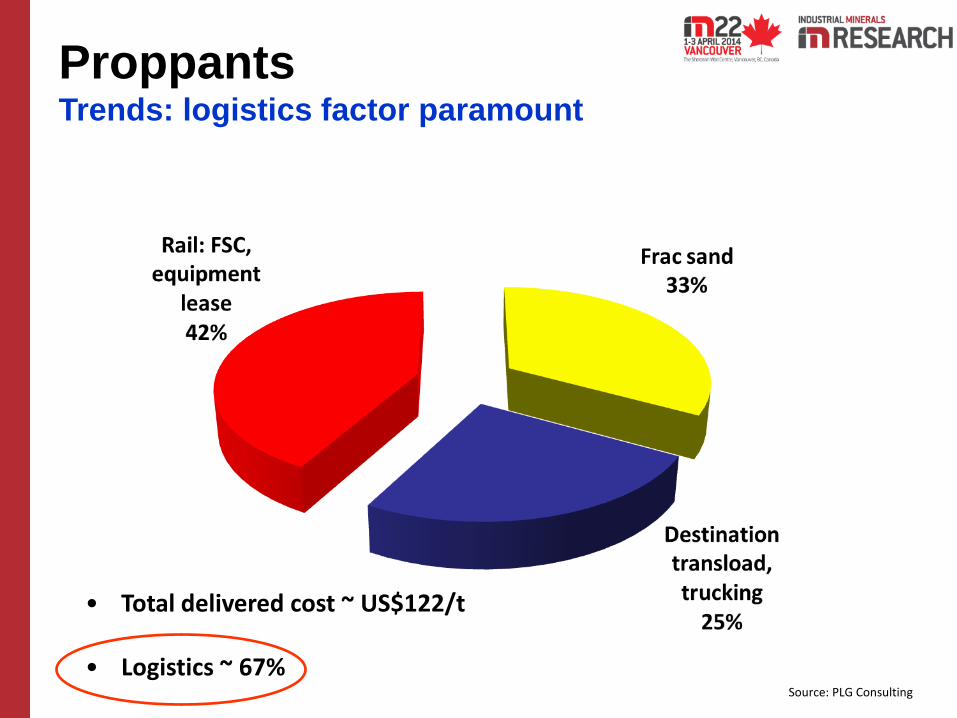

Proppants Trends: logistics factor paramount

Typical requirements of a 30-stage frac well • 40 rail car loads from

source to transload facility

• 160 truck loads from

transload to well site

Proppants Trends: logistics factor paramount

Source: PLG Consulting

• Total delivered cost ~ US$122/t • Logistics ~ 67%

Proppants Trends: logistics factor paramount

Preferred Sands running own rail

line for frac sand freight

13 January 2012

US Silica opens new storage facility in Ohio

4 October 2012

Santrol rail terminals expand proppant

supply to Eagle Basin

28 August 2012

Canadian Railway to service

2.4m tpa frac sand facility

14 August 2012

Frac sand partnership for Smart Sand

and Canadian Pacific

19 July 2012

US Silica inks rail freight deal with

Canadian Pacific

27 June 2012

Unimin secures long-term rail agreement

for Wisconsin sand

16 March 2012

Halliburton goes large with

new frac sand terminal

June 2013

Frac sand storage facility to open in N.

Dakota – Unimin, CP

13 August 2013

Jumbo bins cuts costs for frac sand

logistics

6 August 2013

CN frac sand revenue up 52% Q2

26 July 2013

Proppants Trends: logistics factor paramount

From Russia

Proppants Trends: ceramic proppant imports

From China

M/V Macuru Arrow at the Port of

Olympia, WA, unloading bagged

ceramic proppants

China Ceramic Proppant (Guizhou) Ltd,

Xiuwen, Guizhou in Bakken, N Dakota

Source: bauxite province map Hill & Sehnke 2007

Bauxitic kaolin: Alabama

Bauxite: Arkansas

Kaolin: Georgia Carbo Ceramics, AR, AL

Imerys, GA

Saint-Gobain, AR

CoorsTek, CO

Bauxite, Minas Gerais Mineracao Curimbaba, MG

Bauxite: Henan,

Guizhou,

Shanxi, Sichuan ~100 producers

Kaolin:

Novgorod Borovichi,

Novgorod

Serpentinite (MgSiO2):

Sverdlovsk Fores, Chelyabinsk

Bauxite, kaolin:

north India Hallmark,

Maharashtra

Proppants Trends: CP producer proximity to raw material source

Bauxite:

Komi Carbo,

Kopeysk

Source: based on ITC data; HS code 691490

articles of ceramics not elsewhere specified

194% growth in Chinese

ceramic proppant exports

Proppants Trends: China major CP exporter

USA

83%

697,657 t

US$540/t

Chinese ceramic

proppant export

markets

Source: based on ITC data; HS code 691490

articles of ceramics not elsewhere specified

Proppants Trends: China major CP exporter

2012:897,237 tonnes, US$604m. (US$673/t)

Source: based on ITC data; HS code 691490

articles of ceramics not elsewhere specified

Sharp rise in Chinese proppant

exports to emerging unconventional

oil and gas drilling regions

Proppants Trends: China major CP exporter

Source: Baker Hughes; ITC; HS code 691490 articles of ceramics not elsewhere specified

92

866

443

1,103

698 698

0

200

400

600

800

1,000

1,200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2008 2009 2010 2011 2012 2013

Vertical Horizontal

Directional Chinese proppant exports to US

Linear (Chinese proppant exports to US)

Increasing horizontal drilling & proppant imports

Baker

Hughes

Rig

Count

avg./yr

Ch

ine

se

ce

ram

ic p

rop

pa

nt e

xp

orts

(‘00

0s

ton

ne

s)

63% 29%

Source: based on ITC data; HS code 691490

articles of ceramics not elsewhere specified

VERTICAL

HORIZONTAL

DIRECTIONAL

Proppants Trends: China major CP exporter

Market potential indicators

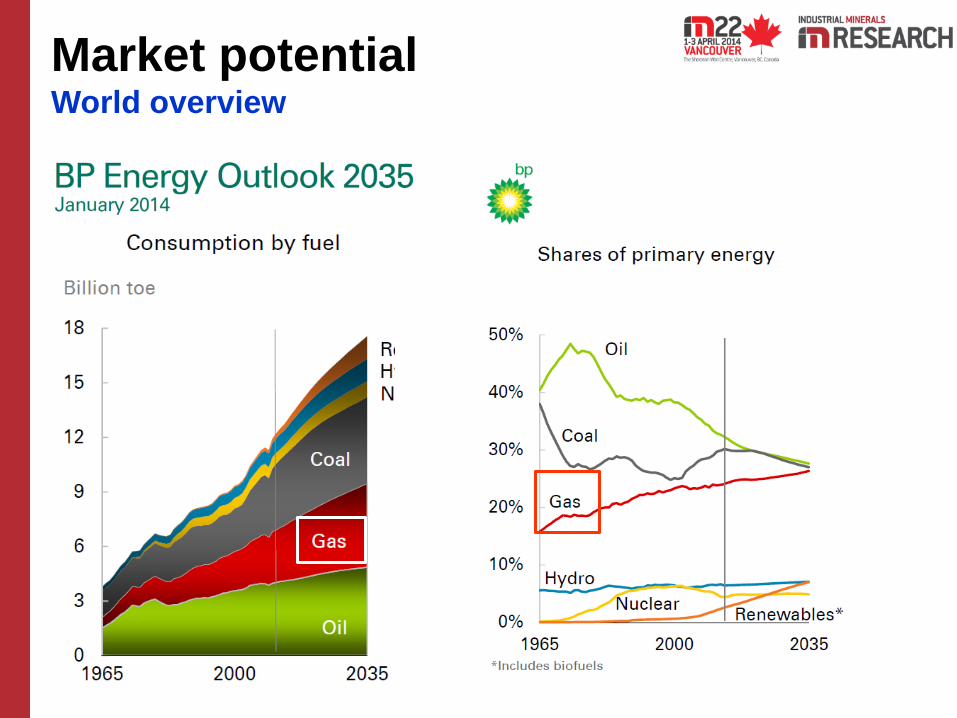

Market potential World overview

Source: World Energy Outlook 2013, IEA

Market potential World overview

Market potential World overview

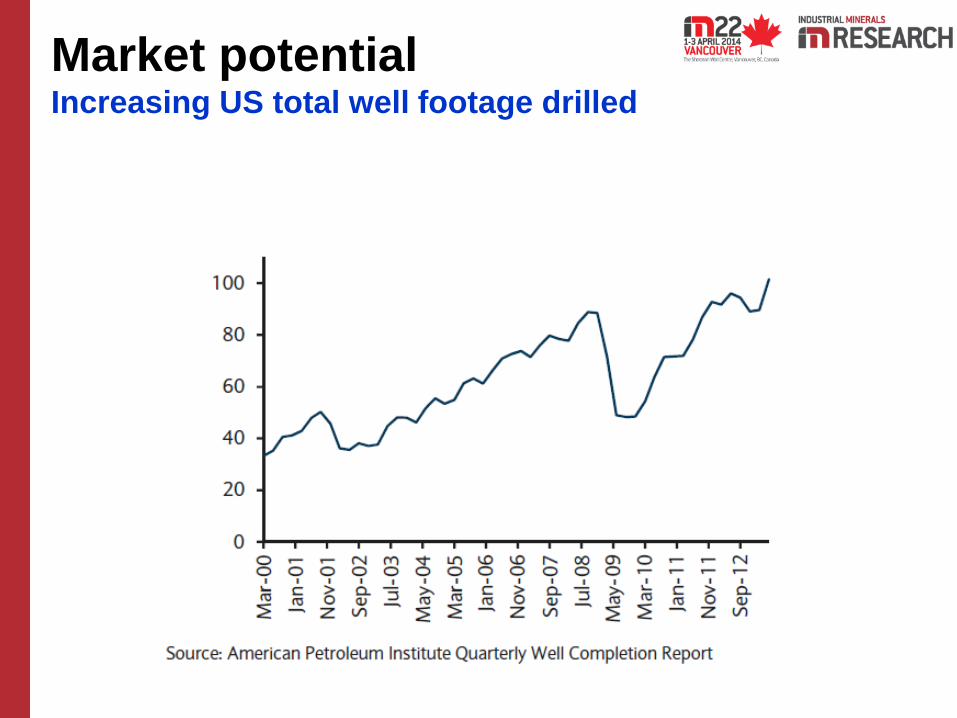

Market potential Increasing US total well footage drilled

China

USA

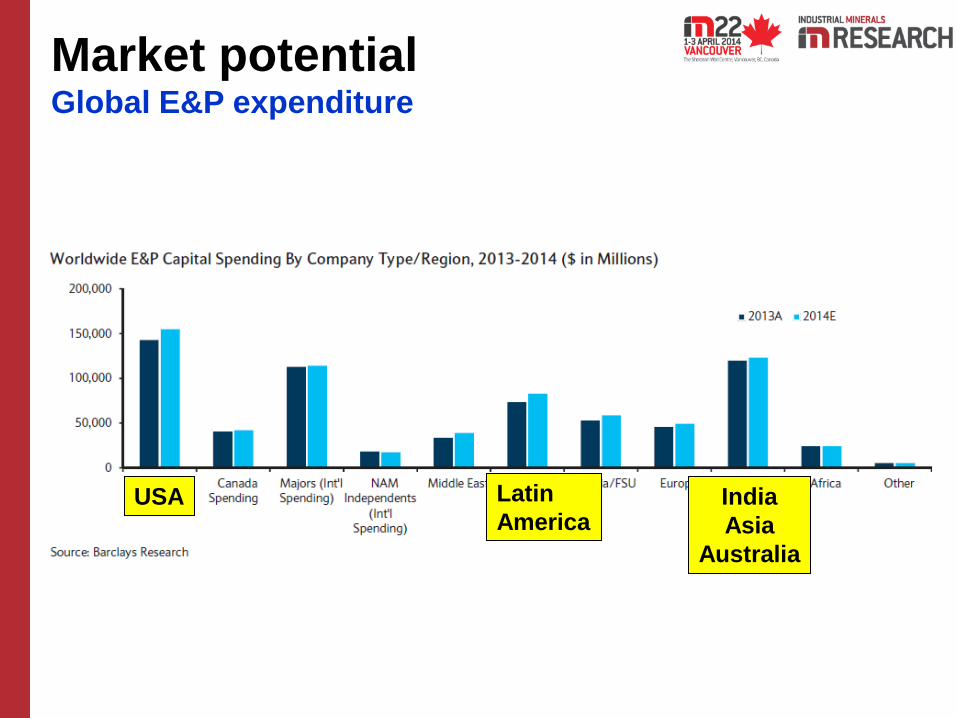

Market potential Global E&P expenditure

China

USA USA Latin

America India

Asia

Australia

Market potential Increasing E&P expenditure

China

USA

Market potential US shale gas and tight oil to contribute to future energy

China

USA

Source: EIA

Market potential US shale gale to continue: shale gas share of US energy

production

China

USA

Market potential World overview – Chinese consumption

China

USA

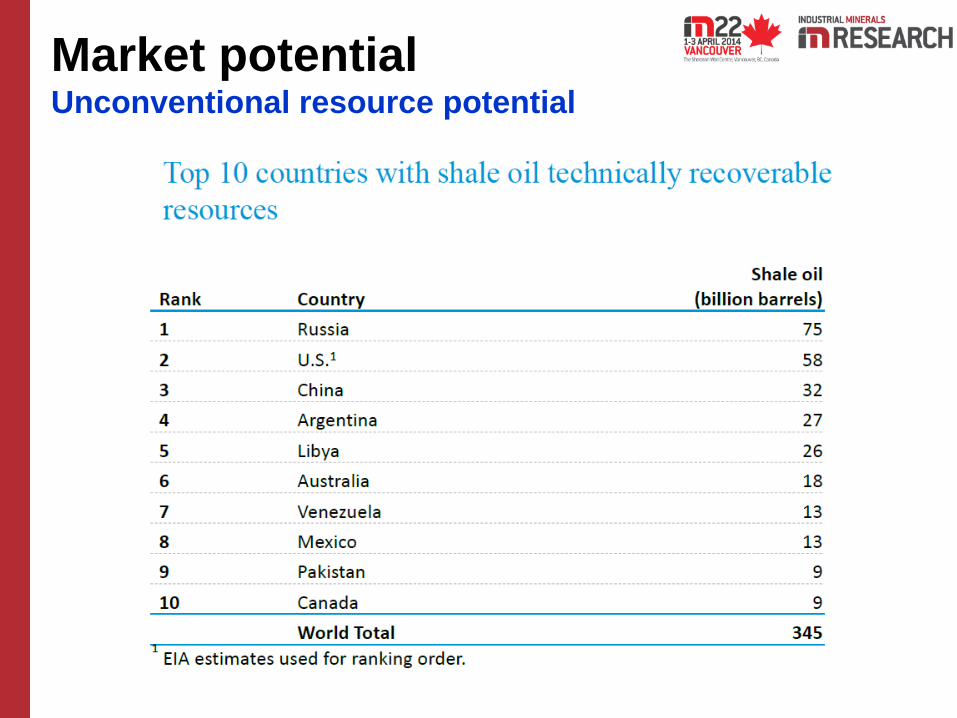

Market potential Unconventional resource potential

Market potential Unconventional resource potential

Market potential Asia Pacific shale gas & oil potential

IEA: SEA energy demand

to increase by 80% to 2035 96.3, 5%

46.5, 3%

4.4, 0%5.4, 0%105.2, 6%

436.7, 24%

1115.1, 62%

Australia

China

India

Indonesia

Mongolia

Pakistan

Thailand

3.7, 5%

7.94, 11%

3.4, 5%

9.09, 12%

32.18, 43%

17.49, 24%

Shale gas (tcf)

Shale oil (bbo)

Source: EIA June 2013

Market potential World proppant demand growth

World demand for well stimulation materials projected to increase

>12% p.a. to over 65m tonnes 2017, $23bn

2007 2012 2017 Annual growth %

‘000s tonnes 2007-12 2012-17

USA 7,582 28,630 48,240 30.4 11.0

Canada 1,669 4,162 8,930 20.1 16.5

China 316 1,373 2,585 34.2 13.5

Russia 560 1,074 2,155 13.9 14.9

Other 713 1,544 3,310 16.7 16.5

World 10,840 36,783 65,220 27.7% 12.1%

Source: Freedonia 2013

Market potential US proppant market growth

Source: PacWest Consultants 2013

Annual growth

Frac sand 9%

RCS 7%

CP 12%

Market potential US proppant market growth

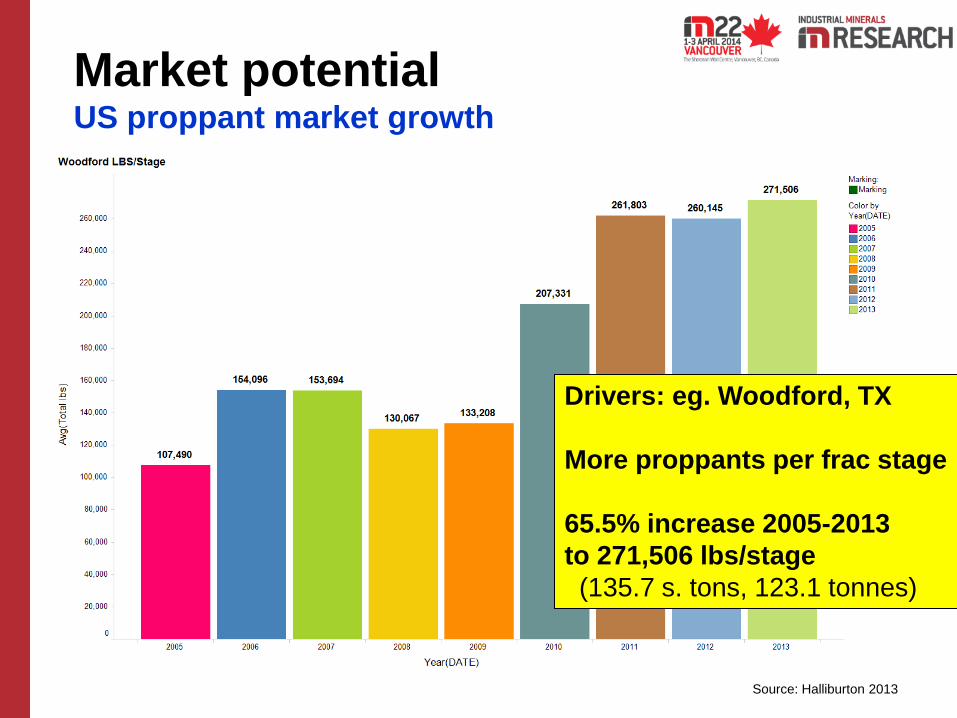

Source: Halliburton 2013

Drivers: eg. Woodford, TX

More proppant used per well

(avg. lbs/well)

39% increase 2006-2012

to 2,300,000 lbs/well

(1,150 s. tons, 1,043 tonnes)

Elsewhere can be up to

6,000,000 lbs/well

(3,000 s.tons, 2,721 tonnes)

Drivers: eg. Woodford, TX

More proppants per frac stage

65.5% increase 2005-2013

to 271,506 lbs/stage

(135.7 s. tons, 123.1 tonnes)

Market potential US proppant market growth

Source: Halliburton 2013

Market potential Chinese shale gas development outlook

Drivers:

China’s energy demand

Shift to shale, tight, CBM

Shale gas

Standard Chartered Research Sept. 2013:

expect shale gas output in China to grow 85%

p.a. during 2015-2020 to reach 61bn cm 2020…

shale gas will account for 15% of China’s total

gas supply in 2020, and 30% in 2030

Market potential Chinese shale gas development outlook

= Increased drilling and fracturing activity

Conclusions

• Overall, industrial mineral demand for oil and gas drilling is assured

• Significant shift of focus of energy production to Asia Pacific where

consumption expected to grow rapidly

• North America (Mexico) and Asia Pacific expected to be major growth

markets, followed by Middle East and Latin America

• For barite: if prices remain stable, new sources will emerge to feed

expanding and new processing plants; China and India will be

challenged; wider acceptance of 4.0 and 4.2 SG grades; move to

establish regional sources of supply

• For proppants: N. America will continue to be a growth market; frac

sand logistics factors will streamline US supply sector; more suppliers

of CP will emerge, especially to supply new overseas growth markets;

= bauxite deposit development; Watch out for China shale gas market

evolution next 5 years and its impact on world CP trade

• Energy production and consumption increasing driving E&P growth

Conclusions New shale gas potential growth markets

1

2

3

4

5

Thank you