INDUSTRIAL CAPITAL EXPENDITURE SURVEY 2017 … · INDUSTRIAL CAPITAL EXPENDITURE SURVEY 2017 ......

13

INDUSTRIAL CAPITAL EXPENDITURE SURVEY 2017 INVESTING AND BUILDING IN CHANGING MANUFACTURING MARKETS

Transcript of INDUSTRIAL CAPITAL EXPENDITURE SURVEY 2017 … · INDUSTRIAL CAPITAL EXPENDITURE SURVEY 2017 ......

INDUSTRIAL CAPITAL EXPENDITURE SURVEY 2017INVESTING AND BUILDING IN CHANGING MANUFACTURING MARKETS

CON

TEN

TS1

. F

ore

wo

rd

2.

Ex

ecu

tiv

e s

um

ma

ry

3.

Re

sea

rch

ov

erv

iew

3

.1 In

tro

du

cti

on

to

th

e r

ese

arc

h

3

.2 In

du

stry

ou

tlo

ok

4.

Se

ve

n k

ey

th

em

es

an

d t

ren

ds

4

.1 B

ett

er

retu

rns

an

d im

pro

ve

d s

pe

ed

to

ma

rke

t

4

.2 F

lexib

ility

an

d a

gili

ty

4

.3 S

ust

ain

ab

ility

in c

ap

ita

l p

rog

ram

s

4

.4 S

up

plie

r in

teg

rati

on

an

d c

om

mu

nic

ati

on

4

.5 In

tern

al st

ake

ho

lde

r e

ng

ag

em

en

t

4

.6 C

en

tra

lizati

on

4

.7 T

he

wa

r fo

r ta

len

t

5.

Arc

ad

is S

ev

en

Ste

p M

od

el

- th

e r

ou

te t

o s

ucce

ss

6.

Co

nclu

sio

n

7.

Me

tho

do

log

y

8.

Fu

rth

er

rea

din

g

9.

Co

nta

ct

us

1. F

ORE

WO

RDIt

is m

y pl

easu

re to

intr

oduc

e th

e A

rcad

is In

dust

rial C

apita

l Exp

endi

ture

Su

rvey

201

7 - I

nves

ting

and

build

ing

in

chan

ging

man

ufac

turin

g m

arke

ts.

Wit

h In

du

stry

4.0

ad

va

ncin

g a

s a

ca

taly

st f

or

ch

an

ge

fo

r

tod

ay

’s m

an

ufa

ctu

rin

g in

du

stry

, ch

an

ge

s in

th

is a

lre

ad

y

dy

na

mic

an

d f

ast

mo

vin

g e

nv

iro

nm

en

t a

re e

xp

ec

ted

to

be

mo

re e

xte

nsi

ve

an

d r

ap

id t

ha

n e

ve

r b

efo

re.

Th

is c

om

es

at

a t

ime

wh

en

glo

ba

l m

an

ufa

ctu

rers

are

alr

ea

dy

wo

rkin

g h

ard

to

ke

ep

pa

ce w

ith

fa

st c

ha

ng

ing

con

sum

er

de

ma

nd

s, d

ue

to

glo

ba

l so

cio

eco

no

mic

fac

tors

, su

ch

as

glo

ba

liza

tio

n, p

op

ula

tio

n g

row

th a

nd

em

erg

ing

ma

rke

t d

yn

am

ics,

to

na

me

bu

t a

fe

w.

Wh

eth

er

it b

e c

ha

ng

es

in t

he

la

bo

r fo

rce

, ne

w

tech

no

log

y a

nd

sy

ste

ms,

dig

itiz

ati

on

, or

rob

oti

cs,

th

e

ne

ed

to

incre

ase

effi

cie

nc

y a

nd

re

du

ce c

ost

s, w

hile

imp

rov

ing

sp

ee

d o

f g

ett

ing

pro

du

cts

to

ma

rke

t, is

of

pa

ram

ou

nt

imp

ort

an

ce.

De

spit

e lim

ite

d c

ap

ita

l, m

an

ufa

ctu

rers

mu

st in

ve

st

in b

uild

ing

an

d u

pg

rad

ing

bu

ilt a

sse

ts a

nd

fa

cilit

ies

to

me

et

ch

an

gin

g d

em

an

ds.

An

d w

ith

th

e n

ew

sp

ee

d

of

bu

sin

ess

an

aly

tics

an

d in

sig

ht

into

re

spo

nd

ing

to

ma

rke

t, t

he

se f

acilit

ies

are

ex

pe

cte

d t

o b

e b

uilt

qu

icke

r,

wit

h m

ore

fle

xib

ilit

y, a

nd

at

less

co

st.

At

the

sa

me

tim

e, I

nd

ust

ry 4

.0 c

on

tin

ue

s a

t p

ace

, in

wh

ich

en

d-t

o-e

nd

ma

nu

fac

turi

ng

va

lue

ch

ain

s a

re

be

com

ing

se

am

less

ly c

on

ne

cte

d, u

nd

erp

inn

ed

by

furt

he

r d

igit

iza

tio

n, t

ech

nic

al a

dv

an

ces

in b

ig d

ata

an

d

da

ta a

na

lyti

cs,

th

e In

tern

et

of

Th

ing

s, r

ob

oti

cs,

art

ificia

l

inte

llig

en

ce a

nd

dri

ve

n b

y t

he

ex

po

ne

nti

al g

row

th o

f

com

pu

tati

on

al p

ow

er

an

d a

va

ila

ble

info

rma

tio

n. W

e a

re

wit

ne

ssin

g t

he

wo

rld

mo

vin

g t

ow

ard

s m

ore

on

-de

ma

nd

pro

cess

es,

en

ab

led

by

te

ch

no

log

ies

such

as

ad

dit

ive

ma

nu

fac

turi

ng

an

d r

ea

l ti

me

big

da

ta p

roce

ssin

g.

Th

is a

ll r

eq

uir

es

‘Sm

art

Ass

ets

’, th

at

no

t o

nly

su

pp

ort

an

d d

rive

, bu

t a

lso

eff

ec

tive

ly im

pro

ve

bu

sin

ess

pe

rfo

rma

nce

.

Fle

xib

ilit

y a

nd

re

silie

nce

in b

uilt

ass

et

po

rtfo

lio

s a

nd

ove

rall

va

lue

ch

ain

s a

re k

ey,

as

is t

he

ne

ed

to

en

sure

resp

on

sib

le u

se o

f n

atu

ral re

sou

rce

s a

nd

sa

fe a

nd

sust

ain

ab

le o

pe

rati

on

of

ass

ets

, in

lin

e w

ith

co

rpo

rate

bra

nd

va

lue

s.

Th

is h

as

a f

un

da

me

nta

l im

pa

ct

on

th

e w

ay

ma

nu

fac

ture

rs d

esi

gn

, cre

ate

, op

era

te a

nd

eve

ntu

ally

re-p

urp

ose

th

eir

bu

ilt a

sse

t p

ort

folio

s, w

he

the

r it

be

th

e

ma

nu

fac

turi

ng

pla

nt,

th

e R

ese

arc

h a

nd

De

ve

lop

me

nt

cen

tre

, or

the

infr

ast

ruc

ture

th

at

sup

po

rts

it.

Re

ach

ing

ou

t to

ove

r 7

0 le

ad

ing

ind

ust

ry e

xp

ert

s in

ma

nu

fac

turi

ng

acro

ss t

he

wo

rld

, ou

r re

po

rt p

rov

ide

s

insi

gh

t in

to t

he

la

test

tre

nd

s in

bu

ilt a

sse

t ca

pit

al

pro

jec

t a

nd

pro

gra

m d

elive

ry a

cro

ss t

he

ind

ust

ria

l

ma

nu

fac

turi

ng

se

cto

rs. I

t a

sse

sse

s co

mp

an

ies

an

d

sec

tors

to

se

e h

ow

re

ad

y t

he

y p

erc

eiv

e t

he

mse

lve

s to

be

to

re

spo

nd

to

to

da

y’s

ch

all

en

ge

s b

rou

gh

t b

y In

du

stry

4.0

. It

als

o p

rov

ide

s a

se

ve

n-s

tep

ro

ute

to

su

cce

ss f

or

ma

nu

fac

ture

rs t

o im

pro

ve

th

eir

ca

pit

al d

elive

ry a

nd

ga

in a

co

mp

eti

tive

ad

va

nta

ge

.

Ou

r fi

nd

ing

s p

rese

nt

an

ove

rall

pic

ture

of

pra

gm

ati

c

op

tim

ism

, wit

h m

an

ufa

ctu

rers

co

nfi

de

nt

in t

he

va

lue

the

ir c

ap

ita

l in

ve

stm

en

ts in

bu

ilt a

sse

ts b

rin

g t

o t

he

ir

wid

er

bu

sin

ess

. Ho

we

ve

r, w

ith

co

nst

rain

ts o

n a

va

ila

ble

fun

ds

ran

kin

g a

s th

e t

op

ch

all

en

ge

to

ca

pit

al p

roje

cts

, it

is c

rucia

l th

at

com

pa

nie

s le

arn

fro

m p

ee

rs a

nd

ta

ke b

est

pra

cti

ce f

rom

oth

er

sec

tors

, to

me

et

the

aff

ord

ab

ilit

y

ch

all

en

ge

an

d m

ax

imiz

e t

he

va

lue

of

bu

ilt a

sse

ts

de

live

red

, in

th

e m

idst

of

a t

ran

sfo

rmin

g s

up

ply

ch

ain

.

I h

op

e y

ou

fin

d t

he

re

po

rt a

s in

form

ati

ve

an

d e

ng

ag

ing

as

ou

r e

xp

eri

en

ce w

as

in p

rod

ucin

g it

. Am

idst

th

e

cu

rre

nt,

ra

pid

ch

an

ge

s in

th

e m

an

ufa

ctu

rin

g in

du

stri

es,

it is

gre

at

to s

ee

ho

w w

e a

ll c

an

lea

rn f

rom

ou

r v

iew

s

on

th

e c

ha

lle

ng

es

at

ha

nd

, no

tin

g s

imila

riti

es

an

d

diff

ere

nce

s fr

om

va

rio

us

pe

rsp

ec

tive

s. I w

ou

ld lik

e t

o

tha

nk t

he

ind

ust

ry le

ad

ers

wh

o s

ha

red

th

eir

insi

gh

ts

an

d c

on

trib

ute

d t

o t

his

re

sea

rch

, an

d Ip

sos

MO

RI fo

r

the

ir in

sig

htf

ul re

sea

rch

pro

gra

m.

Tje

rk v

an

de

r M

ee

r

Glo

bal S

ecto

r Lea

der

Indu

stria

ls, C

ongl

omer

ates

& C

onsu

mer

Goo

ds

“Ip

sos

wa

s d

eli

gh

ted

to

wo

rk w

ith

Arc

ad

is t

o

co

nd

uc

t a

pio

ne

eri

ng

ex

plo

rati

on

of

the

tre

nd

s

in c

ap

ita

l p

lan

nin

g a

nd

de

liv

ery

in

in

du

str

ial

ma

nu

fac

turi

ng

ma

rke

ts. A

s p

art

of

a c

ross

-se

cto

r,

glo

ba

l e

xp

lora

tio

n o

f th

ese

im

po

rta

nt

issu

es, w

e

sp

ok

e w

ith

se

nio

r e

xe

cu

tiv

es

fro

m w

orl

d-l

ea

din

g

ma

nu

fac

ture

rs f

ac

ing

th

e im

pe

rati

ve

of

sp

en

din

g

sig

nifi

ca

nt

ca

pit

al

bu

dg

ets

in

a w

orl

d o

f sh

ort

en

ing

tim

e h

ori

zo

ns

an

d o

ng

oin

g t

ec

hn

olo

gy

dis

rup

tio

n.

Th

is a

pp

roa

ch

ha

s e

na

ble

d A

rca

dis

to

pro

vid

e a

de

tail

ed

pic

ture

of

the

be

ha

vio

rs a

nd

att

itu

de

s o

f

a d

ive

rse

mix

of

co

mp

an

ies, id

en

tify

ing

co

mm

on

the

me

s, tr

en

ds

an

d b

en

ch

ma

rks, a

s m

an

ufa

ctu

rers

see

k t

o m

ee

t th

e c

om

me

rcia

l a

nd

op

era

tio

na

l

pre

ssu

res

in a

ra

pid

ly c

ha

ng

ing

ma

rke

t.”

Ma

tth

ew

Ch

att

ert

on

,

Hea

d of

Bus

ines

s Res

earc

h, Ip

sos M

ORI

2. E

XEC

UTI

VE

SUM

MA

RYIn

a re

volu

tioni

zing

indu

stria

l lan

dsca

pe, it

is e

vide

nt th

at m

any

man

ufac

ture

rs a

re

look

ing

to e

mbe

d th

eir b

uilt

asse

t cap

ital p

rogr

ams i

nto

thei

r cor

e va

lue

chai

n of

de

liver

ing

prod

uct t

o m

arke

t.

Wo

rkin

g w

ith

wo

rld

lea

din

g c

om

pa

nie

s a

cro

ss

a w

ide

ra

ng

e o

f in

du

stri

al se

cto

rs, A

rca

dis

is in

a

un

iqu

e p

osi

tio

n t

o s

ha

re o

ur

reco

rd o

f b

est

pra

cti

ce

me

tho

do

log

ies.

In t

his

re

po

rt, w

e p

oo

l th

at

kn

ow

led

ge

to

pro

vid

e

insi

gh

t in

to h

ow

th

e in

du

stri

al se

cto

rs, a

s a

wh

ole

,

are

pla

nn

ing

an

d d

elive

rin

g b

uilt

ass

ets

aro

un

d t

his

ch

an

gin

g la

nd

sca

pe

- a

nd

ho

w in

div

idu

al co

mp

an

ies

are

pe

rfo

rmin

g in

th

e c

on

tex

t o

f th

eir

pe

ers

.

Pa

rtn

eri

ng

wit

h Ip

sos

MO

RI, t

his

ne

w r

ese

arc

h s

ha

res

ho

w b

uilt

ass

et

ca

pit

al p

rog

ram

s a

re b

ein

g p

lan

ne

d,

de

live

red

an

d m

an

ag

ed

acro

ss t

he

ind

ust

ria

l

ma

nu

fac

turi

ng

se

cto

rs.

Ou

r fi

nd

ing

s d

ep

ict

a p

osi

tive

ou

tlo

ok a

cro

ss t

he

ind

ust

ria

l se

cto

rs, i

n w

hic

h c

ap

ita

l p

rog

ram

s a

re c

lea

rly

vie

we

d a

s si

gn

ifica

nt

dri

ve

rs o

f v

alu

e f

or

bu

sin

ess

es

as

a w

ho

le.

Hig

hlig

hti

ng

wh

ich

se

cto

rs a

re a

do

pti

ng

be

st p

rac

tice

,

the

re

po

rt r

eve

als

se

ve

n k

ey

th

em

es

an

d t

ren

ds,

wh

ich

be

st-i

n-c

lass

ma

nu

fac

ture

rs m

ust

na

vig

ate

to

be

be

tte

r

ab

le t

o d

elive

r to

fu

ture

ma

rke

t d

em

an

d:

A s

um

ma

ry o

f th

e s

ev

en

ke

y t

he

me

s a

nd

tre

nd

s:

1 B

ett

er

retu

rns

an

d im

pro

ve

d s

pe

ed

to

ma

rke

t:

A h

ea

lth

y 8

8%

of

com

pa

nie

s a

re c

on

fid

en

t th

at

the

y c

an

de

mo

nst

rate

th

e v

alu

e t

ha

t th

eir

ca

pit

al

inve

stm

en

t p

roje

cts

bri

ng

to

th

e w

ide

r b

usi

ne

ss.

Ho

we

ve

r, o

nly

on

e in

fo

ur

com

pa

nie

s a

do

pt

be

st

pra

cti

ce a

nd

be

nch

ma

rk a

ga

inst

pe

ers

an

d o

nly

on

e in

five

be

nch

ma

rk c

ross

-se

cto

r. T

his

ra

ise

s

the

qu

est

ion

of

wh

eth

er

the

re is

op

po

rtu

nit

y t

o

imp

rove

co

nfi

de

nce

in c

om

pe

titi

ve

pe

rfo

rma

nce

by

con

du

cti

ng

be

nch

ma

rkin

g b

oth

wit

hin

th

eir

ind

ust

ry

an

d in

oth

er

sec

tors

.

2 F

lex

ibil

ity

an

d a

gil

ity

: W

ith

incre

ase

d fl

ex

ible

ma

nu

fac

turi

ng

re

qu

irin

g a

gile

fa

cilit

ies,

a m

ere

52

%

of

com

pa

nie

s b

elie

ve

th

at

the

ir p

ort

folio

of

facilit

ies

is fl

ex

ible

en

ou

gh

to

me

et

the

ch

all

en

ge

s fa

cin

g

the

ir b

usi

ne

ss. T

his

is d

esp

ite

60

% o

f co

mp

an

ies

ha

vin

g a

mu

lti-

ye

ar

inve

stm

en

t p

lan

in p

lace

, wh

ich

wa

s p

osi

tive

ly lin

ked

to

hig

he

r co

nfi

de

nce

in t

he

fle

xib

ilit

y o

f a

sse

ts. T

his

la

ck o

f fl

ex

ibilit

y s

ug

ge

sts

a

fun

da

me

nta

l ri

sk f

or

the

ind

ust

ry in

bo

th r

em

ain

ing

com

pe

titi

ve

an

d g

ett

ing

pro

du

ct

to m

ark

et

on

tim

e.

3 S

ust

ain

ab

ilit

y in

ca

pit

al

pro

gra

ms:

Six

in t

en

glo

ba

l

com

pa

nie

s ra

ted

re

du

cin

g e

nv

iro

nm

en

tal fo

otp

rin

t

as

sig

nifi

ca

nt

in h

ow

th

ey

ap

pro

ach

ma

jor

ca

pit

al

inve

stm

en

t p

roje

cts

. Me

an

wh

ile, a

ll c

om

pa

nie

s in

th

e

ch

em

ica

ls s

ec

tor

rate

d t

his

as

sig

nifi

ca

nt,

lik

ely

du

e t

o

a m

ix o

f re

gu

lato

ry a

nd

so

cie

tal p

ress

ure

s. W

e e

xp

ec

t

to s

ee

th

is d

em

an

d in

cre

ase

as

glo

ba

l e

nv

iro

nm

en

tal

sta

nd

ard

s a

re a

pp

lie

d.

4 S

up

pli

er

inte

gra

tio

n a

nd

co

mm

un

ica

tio

n: T

he

ma

jori

ty o

f co

mp

an

ies

take

or

are

loo

kin

g t

o t

ake

an

inte

gra

ted

, en

terp

rise

-wid

e a

pp

roa

ch

to

ma

na

gin

g

sup

plie

r re

lati

on

ship

s. H

ow

eve

r, m

an

y c

om

pa

nie

s

do

no

t fu

lly

co

mm

un

ica

te a

nd

en

ga

ge

wit

h t

he

ir

sup

plie

rs; o

nly

57

% r

ep

ort

ed

th

at

the

y s

ha

red

th

eir

pro

jec

t g

oa

ls w

ith

su

pp

lie

rs a

nd

less

th

an

ha

lf s

ha

red

the

ir w

ide

r b

usi

ne

ss g

oa

ls. T

his

ma

y lin

k t

o o

ne

in

thre

e c

om

pa

nie

s re

po

rtin

g a

sig

nifi

ca

nt

dis

pu

te

wit

h a

su

pp

lie

r in

th

e la

st t

wo

ye

ars

. En

ha

nce

d

com

mu

nic

ati

on

an

d o

bje

cti

ve

sh

ari

ng

will

he

lp a

vo

id

dis

pu

tes

an

d p

roje

ct

failu

res,

an

d e

nsu

re a

be

tte

r

inte

gra

ted

va

lue

ch

ain

th

at

is o

rie

nte

d t

ow

ard

s th

e

en

d c

ust

om

er.

5 I

nte

rna

l st

ak

eh

old

er

en

ga

ge

me

nt:

On

ly a

rou

nd

ha

lf

of

com

pa

nie

s b

elie

ve

th

at

the

y a

re g

oo

d a

t e

ng

ag

ing

the

ir in

tern

al st

ake

ho

lde

rs o

n c

ap

ita

l in

ve

stm

en

t

pro

gra

ms.

Be

tte

r co

lla

bo

rati

on

an

d c

om

mu

nic

ati

on

wa

s id

en

tifi

ed

as

the

mo

st s

ign

ifica

nt

fac

tor

to

imp

rove

sta

keh

old

er

en

ga

ge

me

nt

an

d t

he

su

cce

ssfu

l

ou

tco

me

of

pro

jec

ts

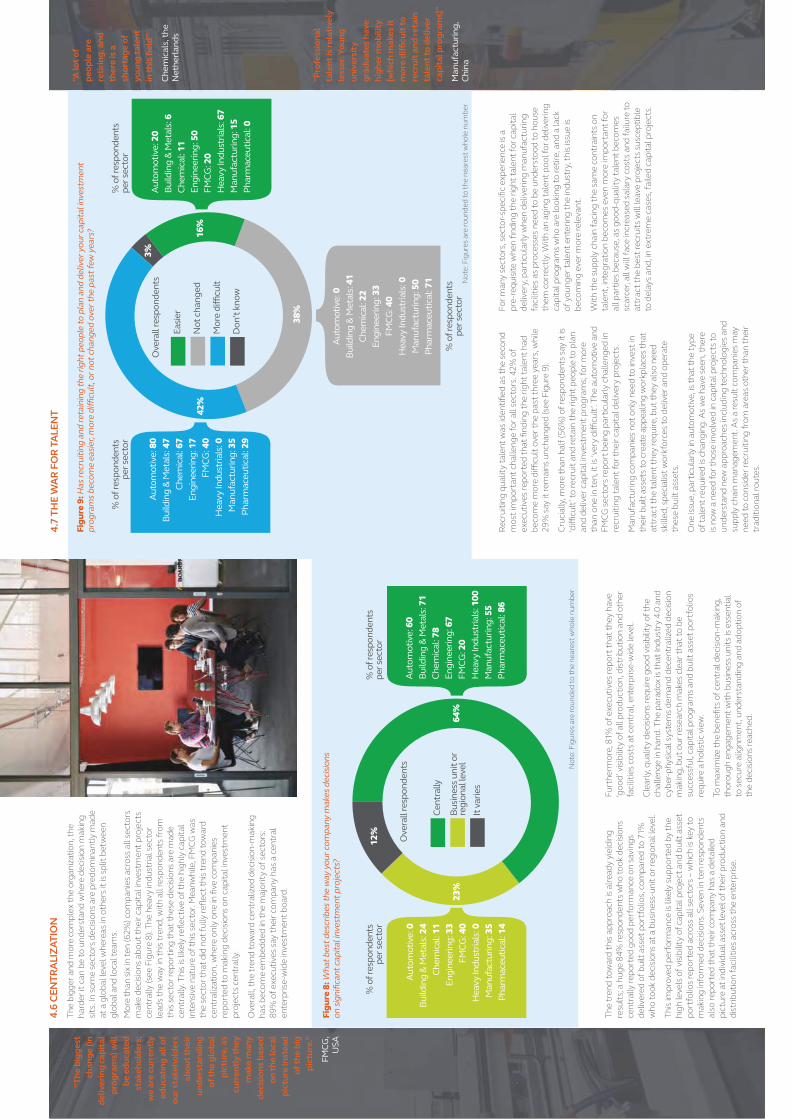

6 C

en

tra

liza

tio

n: 6

2%

of

ind

ust

ria

l m

an

ufa

ctu

rin

g

com

pa

nie

s m

ake

de

cis

ion

s a

bo

ut

ca

pit

al in

ve

stm

en

t

pro

jec

ts c

en

tra

lly,

an

d 8

9%

of

com

pa

nie

s h

ave

a

cen

tra

l, e

nte

rpri

se-w

ide

inve

stm

en

t b

oa

rd. T

he

he

av

y

ind

ust

ria

ls s

ec

tor

lea

ds

the

wa

y in

th

is t

ren

d, w

ith

all

resp

on

de

nts

fro

m t

his

se

cto

r re

po

rtin

g t

ha

t th

ese

de

cis

ion

s a

re m

ad

e c

en

tra

lly.

7 T

he

wa

r fo

r ta

len

t: O

ve

r h

alf

of

com

pa

nie

s sa

y

recru

itin

g a

nd

re

tain

ing

th

e r

igh

t p

eo

ple

to

pla

n a

nd

de

live

r ca

pit

al in

ve

stm

en

t p

rog

ram

s is

diffi

cu

lt a

nd

42

% o

f co

mp

an

ies

rep

ort

th

is h

as

be

com

e m

ore

diffi

cu

lt o

ve

r th

e la

st t

wo

ye

ars

. Wh

ile w

ork

ing

clo

sely

wit

h u

niv

ers

itie

s w

ill im

pro

ve

th

is, i

t is

on

ly a

sm

all

pa

rt o

f th

e s

olu

tio

n a

nd

co

mp

an

ies

are

loo

kin

g t

o

diff

ere

nt

ave

nu

es

to a

ttra

ct

an

d u

p-s

kill

ta

len

t.

In t

his

re

po

rt w

e e

xa

min

e t

he

se t

ren

ds

an

d w

ha

t th

ey

me

an

fo

r m

an

ufa

ctu

rers

’ en

d-g

oa

ls o

f g

ett

ing

th

eir

pro

du

cts

to

ma

rke

t a

nd

inn

ov

ati

ng

cu

ttin

g-e

dg

e

pro

du

ct

lin

es.

We

go

on

to

dis

cu

ss s

eve

n p

rac

tica

l

ste

ps

tha

t co

mp

an

ies

ca

n t

ake

to

pro

-ac

tive

ly r

esp

on

d

to t

he

se t

ren

ds,

usi

ng

insi

gh

t fr

om

ou

r e

xp

ert

s w

ho

reg

ula

rly

pa

rtn

er

wit

h h

igh

pe

rfo

rmin

g o

rga

niz

ati

on

s

an

d t

ake

s le

arn

ing

s fr

om

acro

ss s

ec

tors

.

BET

TER

R

ETU

RN

S A

ND

IM

PRO

VED

SPE

ED

TO M

AR

KET

FLEX

IBIL

ITY

AN

D A

GIL

ITY

SUST

AIN

AB

ILIT

Y IN

CA

PITA

L PR

OG

RA

MS

SUPP

LIER

IN

TEG

RAT

ION

AN

D

COM

MU

NIC

ATIO

N

INTE

RN

AL

STA

KEH

OLD

ER

ENG

AG

EMEN

T

THE

WA

R

FOR

TA

LEN

T

CEN

TRA

LIZA

TIO

N

SEV

ENK

EYTH

EMES1

2

3

4

56

7

3. R

ESEA

RCH

OV

ERV

IEW

1 htt

p:/

/ww

w.u

nid

o.o

rg/n

ew

s/p

ress

/glo

ba

l-m

an

ufa

ctu

rin

g.h

tml

Wit

h m

an

ufa

ctu

rin

g in

cre

asi

ng

bu

t in

ve

stm

en

t fa

llin

g,

a g

ap

is b

ein

g c

rea

ted

th

at,

if n

ot

ad

dre

sse

d, w

ill r

esu

lt

in m

an

ufa

ctu

rers

no

t b

ein

g a

ble

to

me

et

de

ma

nd

. Th

is

ga

p w

ill o

nly

wid

en

if t

his

tre

nd

co

nti

nu

es

resu

ltin

g in

hu

ge

mis

sed

op

po

rtu

nit

ies.

Th

is a

lre

ad

y c

ha

lle

ng

ing

Ca

pE

x e

nv

iro

nm

en

t si

ts

ag

ain

st a

ba

ckd

rop

of

key

ind

ust

ry d

rive

rs t

ha

t a

re

infl

ue

ncin

g h

ow

ind

ust

ria

l m

an

ufa

ctu

rin

g c

om

pa

nie

s

pla

n a

nd

co

nst

ruc

t th

eir

fa

cilit

ies:

dig

ita

liza

tio

n,

au

tom

ati

on

an

d t

ech

no

log

y a

dv

an

cem

en

t, f

orm

ing

Ind

ust

ry 4

.0, g

lob

aliz

ati

on

, co

nso

lid

ati

on

an

d a

wa

r

for

tale

nt.

It is

ev

ide

nt

tha

t m

an

y c

om

pa

nie

s a

re a

lre

ad

y

resp

on

din

g t

o t

he

se c

ha

lle

ng

es.

Ye

t th

ere

are

fe

w

sou

rce

s o

f in

sig

ht

into

ho

w t

he

ind

ust

ria

l se

cto

rs, a

s a

wh

ole

, are

re

spo

nd

ing

an

d h

ow

ind

ivid

ua

l co

mp

an

ies

are

pe

rfo

rmin

g in

co

nte

xt

of

the

ir p

ee

rs. O

ur

rese

arc

h

ad

dre

sse

d t

his

by

pro

vid

ing

un

iqu

e in

sig

ht

into

ho

w

the

ea

ch

ind

ust

ria

l se

cto

r is

re

spo

nd

ing

, an

d m

ake

s

ove

rarc

hin

g c

om

pa

riso

ns

be

twe

en

se

cto

rs, i

nd

ica

tin

g

wh

ere

co

mp

an

ies

ca

n le

arn

fro

m b

oth

th

eir

pe

ers

an

d

oth

er

sec

tors

.

3.1

IN

TR

OD

UC

TIO

N T

O T

HE

RE

SE

AR

CH

We

inte

rvie

we

d 7

3 e

xe

cu

tive

s a

t in

du

stri

al

ma

nu

fac

turi

ng

co

mp

an

ies

fro

m a

cro

ss t

he

glo

be

, all

wit

h a

re

spo

nsi

bilit

y f

or

ma

na

gin

g t

he

ir c

om

pa

ny

’s

ca

pit

al d

elive

ry p

rog

ram

s. T

og

eth

er,

th

e r

esp

on

de

nts

rep

rese

nt

lea

din

g m

an

ufa

ctu

rin

g c

om

pa

nie

s g

en

era

tin

g

ove

r U

S$

30

0 b

illio

n in

re

ve

nu

es

ea

ch

ye

ar,

sp

an

nin

g

the

au

tom

oti

ve

, ph

arm

ace

uti

ca

l, c

he

mic

al, b

uild

ing

an

d m

eta

l, h

ea

vy

ind

ust

ria

l, f

ast

mo

vin

g c

on

sum

er

go

od

s (F

MC

G -

inclu

din

g f

oo

d a

nd

be

ve

rag

e)

ele

ctr

ica

l,

en

gin

ee

rin

g a

nd

ge

ne

ral m

an

ufa

ctu

rin

g s

ec

tors

.

Th

e in

terv

iew

s w

ere

co

nd

uc

ted

by

Ip

sos

MO

RI in

20

16

,

an

d f

ocu

sed

on

ke

y a

spe

cts

in c

ap

ita

l d

elive

ry

to id

en

tify

ho

w c

om

pa

nie

s m

an

ag

e a

nd

op

tim

ize

the

ir c

ap

ita

l e

xp

en

dit

ure

(C

ap

Ex)

pro

gra

ms

an

d t

he

ch

all

en

ge

s th

ey

are

fa

cin

g in

re

spo

nd

ing

to

ma

rke

t a

nd

bu

sin

ess

dis

rup

tors

.

Acc

ord

ing

to

UN

IDO

, glo

ba

l m

an

ufa

ctu

rin

g o

utp

ut

wa

s

ex

pe

cte

d t

o in

cre

ase

by

2.8

% in

20

16

. Ma

nu

fac

turi

ng

pro

du

cti

on

wa

s like

ly t

o r

ise

by

1.3

% in

ind

ust

ria

lize

d

cou

ntr

ies

an

d b

y 4

.7%

in d

eve

lop

ing

eco

no

mie

s.

At

the

sa

me

tim

e, g

lob

al C

ap

Ex

ha

s b

ee

n s

tru

gg

lin

g t

o

ma

ke h

ea

dw

ay

ove

r th

e p

ast

co

up

le o

f ye

ars

. Glo

ba

l

no

n-fi

na

ncia

l C

ap

Ex

sp

en

din

g t

ota

led

$2

,70

2 b

illio

n in

20

15

an

d is

fo

reca

st t

o d

rop

to

$2

,54

1 b

illio

n in

20

17.

3.2

IN

DU

ST

RY

OU

TLO

OK

In t

he

mid

st o

f a

re

vo

luti

on

, in

du

stri

al m

an

ufa

ctu

rin

g

exe

cu

tive

s a

re p

osi

tive

ab

ou

t th

e o

ve

rall

fu

ture

of

the

ir

ind

ust

ry: m

ore

th

an

on

e-t

hir

d (

36

%)

be

lie

ve

th

at

the

ir

sec

tor

will

imp

rove

ove

r th

e n

ex

t ye

ar,

an

d o

ve

r h

alf

(51

%)

say

th

at

the

ir s

ec

tor

will

re

ma

in t

he

sa

me

(se

e

Fig

ure

2).

Th

ese

are

en

cou

rag

ing

sig

ns

follo

win

g t

he

low

-gro

wth

ye

ars

in t

he

wa

ke o

f th

e g

lob

al fi

na

ncia

l

cri

sis

an

d a

re

cen

t d

ow

ntu

rn in

Ca

pE

x s

pe

nd

ing

, le

d in

a la

rge

pa

rt b

y n

orm

aliz

ati

on

aft

er

the

co

mm

od

itie

s

bo

om

.

De

spit

e t

his

ge

ne

ral o

pti

mis

m, e

xe

cu

tive

s re

tain

a

de

gre

e o

f ca

uti

on

wh

en

it c

om

es

to m

an

ag

ing

th

eir

ca

pit

al in

ve

stm

en

t p

roje

cts

. Th

e la

rge

st c

ha

lle

ng

e,

acc

ord

ing

to

mo

re t

ha

n o

ne

-qu

art

er

of

the

inte

rvie

we

d

exe

cu

tive

s is

th

e la

ck o

f a

va

ila

ble

inve

stm

en

t o

r fi

na

nce

.

An

d o

ne

in fi

ve

als

o r

ep

ort

ed

th

at

tale

nt

recru

itm

en

t is

a k

ey

ch

all

en

ge

(se

e T

ab

le 1

).

On

to

p o

f ju

gg

lin

g t

he

se d

ay

to

da

y c

ha

lle

ng

es

of

Ca

pE

x, c

om

pa

nie

s a

re s

tart

ing

to

th

ink a

bo

ut

the

futu

re a

nd

th

e im

pa

ct

ne

w t

ech

no

log

y a

nd

so

cio

-

eco

no

mic

fa

cto

rs w

ill h

ave

on

th

eir

ca

pit

al

inve

stm

en

ts t

o r

em

ain

co

mp

eti

tive

.

"Th

e k

ey

ch

all

en

ge

s fo

r

us

are

to

gra

sp

the

in

du

stry

tre

nd

in

tim

e,

the

em

erg

en

ce

an

d u

se o

f

of

hig

h-e

nd

tec

hn

olo

gy

an

d t

he

la

ck

of

hig

h-e

nd

tale

nt.

"

Auto

mot

ive,

Ch

ina

"Th

e b

igg

est

ch

all

en

ge

is

to g

en

era

te

ca

sh t

o in

ve

st

be

ca

use

th

e

ma

rke

t is

slu

gg

ish

" -

Build

ing

& M

etal

s, F

ranc

e

51%

10%

3%

36%

Impr

ove

Stay

the

sam

e

Get

wor

se

Don

’t kn

ow

Auto

mot

ive:

0Bu

ildin

g &

Met

als:

41

Chem

ical

: 22

Engi

neer

ing:

50

FMCG

: 20

Hea

vy In

dust

rials

: 0M

anuf

actu

ring:

50

Phar

mac

eutic

al: 2

9

Auto

mot

ive:

80

Build

ing

& M

etal

s: 5

9Ch

emic

al: 5

6En

gine

erin

g: 3

3FM

CG: 6

0H

eavy

Indu

stria

ls: 6

7M

anuf

actu

ring:

40

Phar

mac

eutic

al: 4

3

% o

f res

pond

ents

per s

ecto

r%

of r

espo

nden

ts

per s

ecto

r

Ove

rall

resp

onde

nts

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

4,00

0

3,50

0

3,00

0

2,50

0

2,00

0

1,50

0

1,00

0

500 0

+25.

0

+20.

0

+15.

0

+10.

0

+5.0

0.0

-5.0

-10.

0

-15.

0

Capi

tal E

xpen

ditu

re (U

S$ B

N)

Capi

tal E

xpen

ditu

re G

row

th (Y

OY%

)

Tabl

e 1:

The

top

five

chal

leng

es in

man

agin

g ca

pita

l in

vest

men

t pro

ject

s

CHA

LLEN

GE

% O

F RE

SPO

ND

ENTS

1A

va

ila

bil

ity

of

fin

an

ce

27

%

2L

ac

k o

f a

va

ila

ble

ta

len

t2

1%

3In

cre

asin

g p

rod

uc

tio

n c

osts

15

%

4D

em

on

str

ati

ng

re

turn

on

in

ve

stm

en

t1

2%

5Q

ua

lity

of

serv

ice

/pro

du

ct

10

%

Figu

re 2

: Ove

rall,

do

you

thin

k th

e ou

tlook

for y

our s

ecto

r will

impr

ove,

st

ay th

e sa

me

or g

et w

orse

ove

r the

nex

t 12

mon

ths?

Figu

re 1

: Glo

bal n

on-fi

nanc

ial C

apEx

(200

3 –

2017

F)

Sour

ce: S

&P G

loba

l Mar

ket I

ntel

ligen

ce, S

&P G

loba

l Rat

ings

.N

ote

: Fig

ure

s a

re r

ou

nd

ed

to

th

e n

ea

rest

wh

ole

nu

mb

er

No

te: F

igu

res

are

ro

un

de

d t

o t

he

ne

are

st w

ho

le n

um

be

r

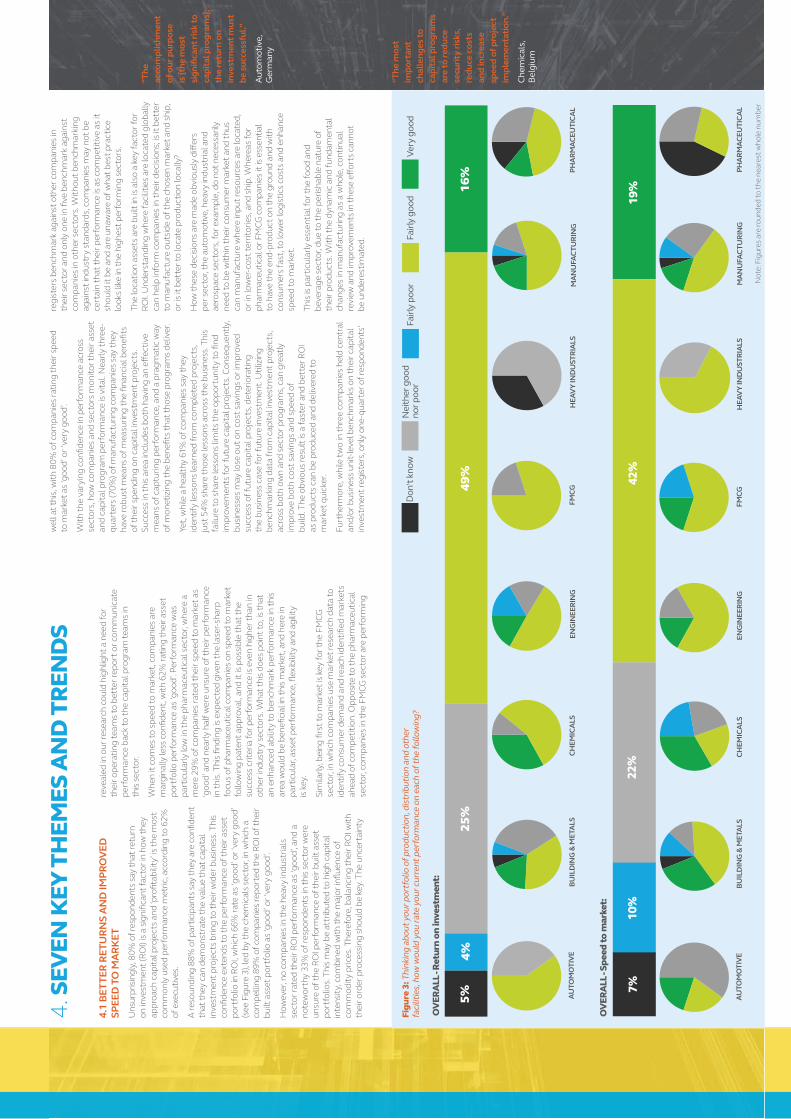

4. S

EVEN

KEY

TH

EMES

AN

D T

REN

DS

4.1

BE

TT

ER

RE

TU

RN

S A

ND

IM

PR

OV

ED

SP

EE

D T

O M

AR

KE

T

Un

surp

risi

ng

ly, 8

0%

of

resp

on

de

nts

sa

y t

ha

t re

turn

on

inve

stm

en

t (R

OI)

is a

sig

nifi

ca

nt

fac

tor

in h

ow

th

ey

ap

pro

ach

ca

pit

al p

roje

cts

an

d ‘p

rofi

tab

ilit

y’ i

s th

e m

ost

com

mo

nly

use

d p

erf

orm

an

ce m

etr

ic, a

cco

rdin

g t

o 6

2%

of

exe

cu

tive

s.

A r

eso

un

din

g 8

8%

of

pa

rtic

ipa

nts

sa

y t

he

y a

re c

on

fid

en

t

tha

t th

ey

ca

n d

em

on

stra

te t

he

va

lue

th

at

ca

pit

al

inve

stm

en

t p

roje

cts

bri

ng

to

th

eir

wid

er

bu

sin

ess

. Th

is

con

fid

en

ce e

xte

nd

s to

th

e p

erf

orm

an

ce o

f th

eir

ass

et

po

rtfo

lio

in R

OI, w

hic

h 6

6%

ra

te a

s ‘g

oo

d’ o

r ‘v

ery

go

od

’

(se

e F

igu

re 3

), le

d b

y t

he

ch

em

ica

ls s

ec

tor,

in w

hic

h a

com

pe

llin

g 8

9%

of

com

pa

nie

s re

po

rte

d t

he

RO

I o

f th

eir

bu

ilt a

sse

t p

ort

folio

as

‘go

od

’ or

‘ve

ry g

oo

d’.

Ho

we

ve

r, n

o c

om

pa

nie

s in

th

e h

ea

vy

ind

ust

ria

ls

sec

tor

rate

d t

he

ir R

OI p

erf

orm

an

ce a

s ‘g

oo

d’,

an

d a

no

tew

ort

hy

33

% o

f re

spo

nd

en

ts in

th

is s

ec

tor

we

re

un

sure

of

the

RO

I p

erf

orm

an

ce o

f th

eir

bu

ilt a

sse

t

po

rtfo

lio

s. T

his

ma

y b

e a

ttri

bu

ted

to

hig

h c

ap

ita

l

inte

nsi

ty, c

om

bin

ed

wit

h t

he

ma

jor

infl

ue

nce

of

com

mo

dit

y p

rice

s. T

he

refo

re, b

ala

ncin

g t

he

ir R

OI w

ith

the

ir o

rde

r p

roce

ssin

g s

ho

uld

be

ke

y. T

he

un

cert

ain

ty

"Th

e

ac

co

mp

lish

me

nt

of

ou

r p

urp

ose

is [

the

mo

st

sig

nifi

ca

nt

risk

to

ca

pit

al

pro

gra

ms]

;

the

re

turn

on

inv

est

me

nt

mu

st

be

su

cce

ssfu

l.”

Auto

mot

ive,

G

erm

any

“T

he

mo

st

imp

ort

an

t

ch

all

en

ge

s to

ca

pit

al

pro

gra

ms

are

to

re

du

ce

sec

uri

ty r

isk

s,

red

uce

co

sts

an

d in

cre

ase

sp

ee

d o

f p

roje

ct

imp

lem

en

tati

on

.”

Chem

ical

s,

Belg

ium

reve

ale

d in

ou

r re

sea

rch

co

uld

hig

hlig

ht

a n

ee

d f

or

the

ir o

pe

rati

ng

te

am

s to

be

tte

r re

po

rt o

r co

mm

un

ica

te

pe

rfo

rma

nce

ba

ck t

o t

he

ca

pit

al p

rog

ram

te

am

s in

this

se

cto

r.

Wh

en

it c

om

es

to s

pe

ed

to

ma

rke

t, c

om

pa

nie

s a

re

ma

rgin

ally

less

co

nfi

de

nt,

wit

h 6

2%

ra

tin

g t

he

ir a

sse

t

po

rtfo

lio

pe

rfo

rma

nce

as

‘go

od

’. P

erf

orm

an

ce w

as

pa

rtic

ula

rly

low

in t

he

ph

arm

ace

uti

ca

l se

cto

r, w

he

re a

me

re 2

9%

of

com

pa

nie

s ra

ted

th

eir

sp

ee

d t

o m

ark

et

as

‘go

od

’ an

d n

ea

rly

ha

lf w

ere

un

sure

of

the

ir p

erf

orm

an

ce

in t

his

. Th

is fi

nd

ing

is e

xp

ec

ted

giv

en

th

e la

ser-

sha

rp

focu

s o

f p

ha

rma

ceu

tica

l co

mp

an

ies

on

sp

ee

d t

o m

ark

et

follo

win

g p

ate

nt

ap

pro

va

l, a

nd

it is

po

ssib

le t

ha

t th

e

succ

ess

cri

teri

a f

or

pe

rfo

rma

nce

is e

ve

n h

igh

er

tha

n in

oth

er

ind

ust

ry s

ec

tors

. Wh

at

this

do

es

po

int

to, i

s th

at

an

en

ha

nce

d a

bilit

y t

o b

en

ch

ma

rk p

erf

orm

an

ce in

th

is

are

a w

ou

ld b

e b

en

efi

cia

l in

th

is m

ark

et,

an

d h

ere

in

pa

rtic

ula

r, a

sse

t p

erf

orm

an

ce, fl

ex

ibilit

y a

nd

ag

ilit

y

is k

ey.

Sim

ila

rly,

be

ing

firs

t to

ma

rke

t is

ke

y f

or

the

FM

CG

sec

tor,

in w

hic

h c

om

pa

nie

s u

se m

ark

et

rese

arc

h d

ata

to

ide

nti

fy c

on

sum

er

de

ma

nd

an

d r

ea

ch

ide

nti

fie

d m

ark

ets

ah

ea

d o

f co

mp

eti

tio

n. O

pp

osi

te t

o t

he

ph

arm

ace

uti

ca

l

sec

tor,

co

mp

an

ies

in t

he

FM

CG

se

cto

r a

re p

erf

orm

ing

OVE

RALL

- Ret

urn

on in

vest

men

t:

OVE

RALL

- Spe

ed to

mar

ket:

AU

TO

MO

TIV

EB

UIL

DIN

G &

ME

TA

LS

CH

EM

ICA

LS

EN

GIN

EE

RIN

GF

MC

GH

EA

VY

IN

DU

ST

RIA

LS

MA

NU

FA

CT

UR

ING

PH

AR

MA

CE

UT

ICA

L

AU

TO

MO

TIV

EB

UIL

DIN

G &

ME

TA

LS

CH

EM

ICA

LS

EN

GIN

EE

RIN

GF

MC

GH

EA

VY

IN

DU

ST

RIA

LS

MA

NU

FA

CT

UR

ING

PH

AR

MA

CE

UT

ICA

L

5%49

%16

%25

%4%

10%

7%19

%42

%

Ver

y go

od F

airly

goo

d F

airly

poo

rN

eith

er g

ood

nor p

oor

Don

't kn

ow

22%

VE

we

ll a

t th

is, w

ith

80

% o

f co

mp

an

ies

rati

ng

th

eir

sp

ee

d

to m

ark

et

as

‘go

od

’ or

‘ve

ry g

oo

d’.

Wit

h t

he

va

ryin

g c

on

fid

en

ce in

pe

rfo

rma

nce

acro

ss

sec

tors

, ho

w c

om

pa

nie

s a

nd

se

cto

rs m

on

ito

r th

eir

ass

et

an

d c

ap

ita

l p

rog

ram

pe

rfo

rma

nce

is v

ita

l. N

ea

rly

th

ree

-

qu

art

ers

(7

0%

) o

f m

an

ufa

ctu

rin

g c

om

pa

nie

s sa

y t

he

y

ha

ve

ro

bu

st m

ea

ns

of

me

asu

rin

g t

he

fin

an

cia

l b

en

efi

ts

of

the

ir s

pe

nd

ing

on

ca

pit

al in

ve

stm

en

t p

roje

cts

.

Su

cce

ss in

th

is a

rea

inclu

de

s b

oth

ha

vin

g a

n e

ffe

cti

ve

me

an

s o

f ca

ptu

rin

g p

erf

orm

an

ce, a

nd

a p

rag

ma

tic w

ay

of

mo

ne

tizi

ng

th

e b

en

efi

ts t

ha

t th

ose

pro

gra

ms

de

live

r.

Ye

t, w

hile

a h

ea

lth

y 6

1%

of

com

pa

nie

s sa

y t

he

y

ide

nti

fy le

sso

ns

lea

rne

d f

rom

co

mp

lete

d p

roje

cts

,

just

54

% s

ha

re t

ho

se le

sso

ns

acro

ss t

he

bu

sin

ess

. Th

is

failu

re t

o s

ha

re le

sso

ns

lim

its

the

op

po

rtu

nit

y t

o fi

nd

imp

rove

me

nts

fo

r fu

ture

ca

pit

al p

roje

cts

. Co

nse

qu

en

tly,

bu

sin

ess

es

ma

y lo

se o

ut

on

co

st s

av

ing

s o

r im

pro

ve

d

succ

ess

of

futu

re c

ap

ita

l p

roje

cts

, de

teri

ora

tin

g

the

bu

sin

ess

ca

se f

or

futu

re in

ve

stm

en

t. U

tiliz

ing

be

nch

ma

rkin

g d

ata

fro

m c

ap

ita

l in

ve

stm

en

t p

roje

cts

,

acro

ss b

oth

ow

n a

nd

se

cto

r p

rog

ram

s, c

an

gre

atl

y

imp

rove

bo

th c

ost

sa

vin

gs

an

d s

pe

ed

of

bu

ild. T

he

ob

vio

us

resu

lt is

a f

ast

er

an

d b

ett

er

RO

I

as

pro

du

cts

ca

n b

e p

rod

uce

d a

nd

de

live

red

to

ma

rke

t q

uic

ker.

Fu

rth

erm

ore

, wh

ile t

wo

in t

hre

e c

om

pa

nie

s h

eld

ce

ntr

al

an

d/o

r b

usi

ne

ss u

nit

-le

ve

l b

en

ch

ma

rks

on

th

eir

ca

pit

al

inve

stm

en

t re

gis

ters

, on

ly o

ne

-qu

art

er

of

resp

on

de

nts

’

reg

iste

rs b

en

ch

ma

rk a

ga

inst

oth

er

com

pa

nie

s in

the

ir s

ec

tor

an

d o

nly

on

e in

five

be

nch

ma

rk a

ga

inst

com

pa

nie

s in

oth

er

sec

tors

. Wit

ho

ut

be

nch

ma

rkin

g

ag

ain

st in

du

stry

sta

nd

ard

s, c

om

pa

nie

s m

ay

no

t b

e

cert

ain

th

at

the

ir p

erf

orm

an

ce is

as

com

pe

titi

ve

as

it

sho

uld

it b

e a

nd

are

un

aw

are

of

wh

at

be

st p

rac

tice

loo

ks

like

in t

he

hig

he

st p

erf

orm

ing

se

cto

rs.

Th

e lo

ca

tio

n a

sse

ts a

re b

uilt

in is

als

o a

ke

y f

ac

tor

for

RO

I. U

nd

ers

tan

din

g w

he

re f

acilit

ies

are

loca

ted

glo

ba

lly

ca

n h

elp

info

rm c

om

pa

nie

s in

th

eir

de

cis

ion

s; is

it b

ett

er

to m

an

ufa

ctu

re o

uts

ide

of

the

ch

ose

n m

ark

et

an

d s

hip

,

or

is it

be

tte

r to

loca

te p

rod

uc

tio

n lo

ca

lly?

Ho

w t

he

se d

ecis

ion

s a

re m

ad

e o

bv

iou

sly

diff

ers

pe

r se

cto

r, t

he

au

tom

oti

ve

, he

av

y in

du

stri

al a

nd

ae

rosp

ace

se

cto

rs, f

or

ex

am

ple

, do

no

t n

ece

ssa

rily

ne

ed

to

be

wit

hin

th

eir

co

nsu

me

r m

ark

et

an

d t

hu

s

ca

n m

an

ufa

ctu

re w

he

re in

pu

t re

sou

rce

s a

re lo

ca

ted

,

or

in lo

we

r-co

st t

err

ito

rie

s, a

nd

sh

ip. W

he

rea

s fo

r

ph

arm

ace

uti

ca

l o

r F

MC

G c

om

pa

nie

s it

is e

sse

nti

al

to h

ave

th

e e

nd

-pro

du

ct

on

th

e g

rou

nd

an

d w

ith

con

sum

ers

fa

st, t

o lo

we

r lo

gis

tics

cost

s a

nd

en

ha

nce

spe

ed

to

ma

rke

t.

Th

is is

pa

rtic

ula

rly

ess

en

tia

l fo

r th

e f

oo

d a

nd

be

ve

rag

e s

ec

tor,

du

e t

o t

he

pe

rish

ab

le n

atu

re o

f

the

ir p

rod

uc

ts. W

ith

th

e d

yn

am

ic a

nd

fu

nd

am

en

tal

ch

an

ge

s in

ma

nu

fac

turi

ng

as

a w

ho

le, c

on

tin

ua

l

rev

iew

an

d im

pro

ve

me

nts

in t

he

se e

ffo

rts

ca

nn

ot

be

un

de

rest

ima

ted

.

Figu

re 3

: Thi

nkin

g ab

out y

our p

ortf

olio

of p

rodu

ctio

n, d

istrib

utio

n an

d ot

her

faci

litie

s, h

ow w

ould

you

rate

you

r cur

rent

per

form

ance

on

each

of t

he fo

llow

ing?

No

te: F

igu

res

are

ro

un

de

d t

o t

he

ne

are

st w

ho

le n

um

be

r

4.2

FL

EX

IBIL

ITY

AN

D A

GIL

ITY

Ch

em

ica

ls s

ec

tor

ah

ea

d in

fle

xib

ilit

y

Th

e r

ise

of

fle

xib

le m

an

ufa

ctu

rin

g h

as

pu

t p

ress

ure

on

bu

ilt a

sse

ts t

o b

e a

gile

to

acc

om

mo

da

te p

rod

uc

tio

n o

f

va

rio

us

pro

du

cts

, or

sma

ll-b

atc

h p

rod

uc

ts, s

uch

as

in

the

bio

ph

arm

a a

nd

sp

ecia

lty

ch

em

ica

ls s

ec

tors

.

Ou

r fi

nd

ing

s sh

ow

th

at

com

pa

nie

s in

th

e c

he

mic

als

sec

tor

pe

rce

ive

th

em

selv

es

to b

e m

ore

re

ad

y t

o

ad

ap

t to

ch

an

ge

th

an

co

mp

an

ies

in o

the

r se

cto

rs.

78

% o

f re

spo

nd

en

ts in

th

e c

he

mic

als

se

cto

r sa

y t

ha

t

the

ir c

urr

en

t p

ort

folio

of

pro

du

cti

on

, dis

trib

uti

on

an

d o

the

r fa

cilit

ies

is fl

ex

ible

en

ou

gh

to

me

et

the

ch

all

en

ge

s fa

cin

g t

he

ir b

usi

ne

ss, c

om

pa

red

wit

h 5

2%

acro

ss a

ll s

ec

tors

(se

e F

igu

re 4

). T

his

ma

y b

e b

eca

use

,

tho

ug

h c

he

mic

al co

mp

an

ies

oft

en

ta

ke c

en

tra

l

ove

rall

de

cis

ion

s, it

is n

ot

un

com

mo

n in

th

is s

ec

tor

for

ind

ivid

ua

l si

tes

to c

om

pe

te f

or

inve

stm

en

t fr

om

th

e

cen

ter.

Th

ere

fore

, th

ere

is a

ne

ed

fo

r fl

ex

ibilit

y t

o b

e

ab

le t

o s

wit

ch

pro

du

ct

lin

es

to s

ecu

re b

oa

rd a

pp

rov

al

for

fun

din

g a

nd

sh

ow

low

er

cost

s in

ge

ttin

g p

rod

uc

t

to m

ark

et.

Th

is is

un

like

se

cto

rs s

uch

as

au

tom

oti

ve

,

wh

ere

co

mp

an

ies

are

mo

re lik

ely

to

ha

ve

a g

lob

al

ma

nu

fac

turi

ng

str

ate

gy,

wh

ich

all

ow

s th

em

to

sh

ift

pro

du

ct

line

s a

rou

nd

th

e w

orl

d.

Th

is fl

ex

ibilit

y a

nd

diff

ere

nce

in a

pp

roa

ch

ca

n, h

ow

eve

r,

imp

ac

t ca

pa

cit

y. S

om

e s

ec

tors

ha

ve

a t

en

de

nc

y t

o

op

era

te f

or

ove

rca

pa

cit

y, w

hilst

oth

ers

su

ffe

r fr

om

no

t b

ein

g a

ble

to

pro

du

ce s

uffi

cie

nt

pro

du

cts

qu

ickly

en

ou

gh

. Ha

vin

g a

fa

cilit

y t

ha

t ca

n a

da

pt

to c

ha

ng

es

in

pro

du

ct

line

s o

r h

ou

se m

ore

th

an

on

e p

rod

uc

t re

sult

s

in c

ost

sa

vin

gs

an

d m

ore

su

sta

ina

ble

re

turn

s. W

he

n

pa

rtn

eri

ng

, pa

rtic

ula

rly

wit

h a

uto

mo

tive

co

mp

an

ies,

we

see

ho

w fl

ex

ible

th

ey

ha

ve

ma

de

th

eir

fa

cilit

ies

to h

elp

the

m t

ackle

ma

rke

t d

em

an

d s

hif

ts a

nd

th

ere

is m

uch

tha

t ca

n b

e le

arn

t fr

om

th

is s

ec

tor

by

oth

ers

.

Giv

en

60

% o

f re

spo

nd

en

ts s

ay

th

at

the

y h

ave

a m

ult

i-

ye

ar

inve

stm

en

t p

lan

in p

lace

, it

is c

on

cern

ing

th

at

52

%

are

la

ckin

g c

on

fid

en

ce t

ha

t th

eir

bu

ilt a

sse

t p

ort

folio

s

are

fle