Industrial Big Box Research & Forecast Report EASTERN ...

5

$4.00 $4.50 $5.00 $5.50 0% 2% 4% 6% 8% 10% 12% 14% 2016 2017 2018 2019 2020 Forecasted Eastern Pennsylvania I-78/I-81 SUBMARKETS Highlights > Industrial big-box demand has only accelerated since the onset of the pandemic. Occupiers have signed 16.9 MSF of new deals year-to-date, the largest Q3 total in the market’s history. Year-to-date net absorption, 11 MSF, is also at an all-time high for the third quarter. > There is less square footage under construction in 2020 than in 2019, 12.6 MSF vs. 21.2 MSF. Last year, construction activity reached a cycle peak due to many 750K+ SF projects throughout the market. Construction has returned to the historic norm. > Though Pennsylvania temporarily halted non-essential construction in March/April in response to the pandemic, there was little impact on the supply pipeline beyond some brief delays. The YOY decrease in construction volume was expected pre-pandemic, particularly among large-format projects in Central & Northeast PA. Construction starts rebounded in Q3 though the supply of large-format, spec construction remains tight. > Market-wide, vacancy is expected to decrease in the fourth quarter as there are many large, pending deals and relatively few speculative deliveries in the pipeline. > Available subleases have decreased since the start of the pandemic. The subleases that have come to market are not concentrated among any high-risk industry sector such as apparel. > The average asking rent rose from $5.27 to $5.30 psf from Q2 to Q3. Increasing rates for speculative product, particularly in the Lehigh Valley Core & Central PA’s I-83 Corridor, are driving the growth. > Year-to-date occupancy gains have been greatest in Northeast PA and the I-78 W/Berks County region. YTD net absorption in I-78 W/Berks County stands at 3.7 MSF, a 300% increase over 2019, with no new vacancies expected in the fourth quarter. Industrial Big Box Research & Forecast Report EASTERN PENNSYLVANIA I-78/I-81 SUBMARKETS | LEHIGH VALLEY, CENTRAL PA & NORTHEAST PA I-95 CORRIDOR | GREATER PHILADELPHIA Q3 2020 Vacancy & Asking Rental Rates $5.30 9.4% 15.3 13.3 13.5 17.5 16.5 16.3 17.3 16.4 16.7 27.1 13.3 10.2 11.1 11.7 15.0 0 5 10 15 20 25 30 2016 2017 2018 2019 2020 Forecasted Annual Deliveries, New Occupier Transactions & Net Absorption (MSF) “The demand for warehouse and fulfillment spaces is at record levels that will lead to reduced inventory levels and sustained rental growth through 2021.” — MARK CHUBB > Northeast PA, the smallest submarket, led the region in quarterly new transactions (2.3 MSF). Quarterly net absorption, 2.2 MSF, was the highest in three years. Notable deals this quarter include user purchases by Ball Container (1 MSF) and Niagara Water (800K SF). YTD transaction volume is 4.8 MSF, only 30K SF shy of the previous annual record set in 2017. > Following an exceptional first half of the year, Q3 transaction volume dipped in Central PA & Lehigh Valley, but is forecasted to reach record levels in Q4. The near-term deal pipeline is robust and there is a marked increase in new requirements greater than 800,000 SF compared to the last year. Annual Deliveries Annual Transactions Annual Absorption V Va ac ca an nc cy y R Ra at te e A Av vg g A As sk ki in ng g R Re en nt ta al l R Ra at te e

Transcript of Industrial Big Box Research & Forecast Report EASTERN ...

9.4%

$5.30

$4.00

$4.50

$5.00

$5.50

0%2%4%6%8%

10%12%14%

2016 2017 2018 2019 2020 Forecasted

VVaaccaannccyy vvss.. AAvveerraaggee AAsskkiinngg RReennttaall RRaattee ((PPSSFF))

VVaaccaannccyy RRaattee WWeeiigghhtteedd AAvvgg RReennttaall RRaattee PPSSFF

Eastern PennsylvaniaI-78/I-81 SUBMARKETS

Highlights > Industrial big-box demand has only accelerated since the

onset of the pandemic. Occupiers have signed 16.9 MSF of new deals year-to-date, the largest Q3 total in the market’s history. Year-to-date net absorption, 11 MSF, is also at an all-time high for the third quarter.

> There is less square footage under construction in 2020 than in 2019, 12.6 MSF vs. 21.2 MSF. Last year, construction activity reached a cycle peak due to many 750K+ SF projects throughout the market. Construction has returned to the historic norm.

> Though Pennsylvania temporarily halted non-essential construction in March/April in response to the pandemic, there was little impact on the supply pipeline beyond some brief delays. The YOY decrease in construction volume was expected pre-pandemic, particularly among large-format projects in Central & Northeast PA. Construction starts rebounded in Q3 though the supply of large-format, spec construction remains tight.

> Market-wide, vacancy is expected to decrease in the fourth quarter as there are many large, pending deals and relatively few speculative deliveries in the pipeline.

> Available subleases have decreased since the start of the pandemic. The subleases that have come to market are not concentrated among any high-risk industry sector such as apparel.

> The average asking rent rose from $5.27 to $5.30 psf from Q2 to Q3. Increasing rates for speculative product, particularly in the Lehigh Valley Core & Central PA’s I-83 Corridor, are driving the growth.

> Year-to-date occupancy gains have been greatest in Northeast PA and the I-78 W/Berks County region. YTD net absorption in I-78 W/Berks County stands at 3.7 MSF, a 300% increase over 2019, with no new vacancies expected in the fourth quarter.

Industrial Big Box Research & Forecast Report

EASTERN PENNSYLVANIA I-78/I-81 SUBMARKETS | LEHIGH VALLEY, CENTRAL PA & NORTHEAST PAI-95 CORRIDOR | GREATER PHILADELPHIA

Q3 2020

Vacancy & Asking Rental Rates

$5.30

9.4%

15.313.3 13.5

17.5 16.516.3 17.3 16.4 16.7

27.1

13.3

10.2 11.1 11.715.0

0

5

10

15

20

25

30

2016 2017 2018 2019 2020 Forecasted

Annual Deliveries, Occupier Transactions, Net Absorption (MSF)

AAnnnnuuaall DDeelliivveerriieess AAnnnnuuaall TTrraannssaaccttiioonnss AAnnnnuuaall AAbbssoorrppttiioonn

Annual Deliveries, New Occupier Transactions & Net Absorption (MSF)

“The demand for warehouse and fulfillment spaces is at record levels that will lead to reduced inventory levels and sustained rental growth through 2021.” — MARK CHUBB

> Northeast PA, the smallest submarket, led the region in quarterly new transactions (2.3 MSF). Quarterly net absorption, 2.2 MSF, was the highest in three years. Notable deals this quarter include user purchases by Ball Container (1 MSF) and Niagara Water (800K SF). YTD transaction volume is 4.8 MSF, only 30K SF shy of the previous annual record set in 2017.

> Following an exceptional first half of the year, Q3 transaction volume dipped in Central PA & Lehigh Valley, but is forecasted to reach record levels in Q4. The near-term deal pipeline is robust and there is a marked increase in new requirements greater than 800,000 SF compared to the last year.

15.313.3 13.5

17.5 16.516.3 17.3 16.4 16.7

27.1

13.3

10.2 11.1 11.715.0

0

5

10

15

20

25

30

2016 2017 2018 2019 2020 Forecasted

Annual Deliveries, Occupier Transactions, Net Absorption (MSF)

AAnnnnuuaall DDeelliivveerriieess AAnnnnuuaall TTrraannssaaccttiioonnss AAnnnnuuaall AAbbssoorrppttiioonn

9.0%

$4.90

$2.00

$3.00

$4.00

$5.00

$6.00

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020Forecasted

Vacancy & Asking Rental Rate

VVaaccaannccyy RRaattee AAvvgg AAsskkiinngg RReennttaall RRaattee

2 Industrial Big Box Research & Forecast Report | Q3 2020 | Eastern PA | Logistics & Transportation Solutions Group

Q3 Highlights

Third Quarter YTD Inventory

(SF)Vacant

Space (SF)Vacancy

RateAvailability

Rate

Occupier Transactions

(SF)Absorption

(SF)Construction Starts (SF)

Deliveries (SF)

Under Construction

(SF)

Avg Asking Rental (PSF) Transactions

Net Absorption Deliveries

Market Growth

Subtotal Lehigh Valley/I-78 Corridor 80,611,201 6,973,689 8.7% 15.8% 579,440 2,276,240 2,464,165 2,949,679 5,571,384 $6.30 6,441,672 5,498,732 5,526,358 6.8%

Eastern I-78/Core Lehigh Valley 64,746,627 4,222,948 6.5% 13.8% 135,360 946,560 1,452,515 2,064,079 4,559,734 $6.67 3,364,387 1,812,537 4,640,758 2.8%

Western I-78/Berks County 15,864,574 2,750,741 17.3% 23.7% 444,080 1,329,680 1,011,650 885,600 1,011,650 $5.36 3,077,285 3,686,195 885,600 23.2%

Subtotal Central PA/Southern I -81 104,026,027 9,345,107 9.0% 10.7% 236,177 (83,419) 2,851,255 2,144,489 5,658,211 $4.90 6,028,349 1,302,318 2,144,489 1.3%

I-83 Corridor/York 27,938,591 1,280,280 4.6% 6.2% 0 0 0 663,920 1,253,758 $5.30 1,106,254 374,254 663,920 1.3%

Southern I-81 Corridor 76,087,436 8,064,827 10.6% 12.3% 236,177 (83,419) 2,851,255 1,480,569 4,404,453 $4.80 4,922,095 928,064 1,480,569 1.2%

Subtotal Northeast PA/Northern I-81 56,156,809 6,339,475 11.3% 14.9% 2,344,081 2,248,943 563,000 3,058,630 1,343,000 $4.61 4,400,107 4,145,190 5,184,698 7.4%

TOTAL 240,794,037 22,658,271 8.1% 14.5% 3,159,698 4,441,764 5,878,420 8,152,798 12,572,595 $5.30 16,870,128 10,946,240 12,855,545 2.8%

State of the Market

The foregoing information was furnished to us by sources which we deem to be reliable, but no warranty or representation is made as to the accuracy thereof. Subject to correction of errors, omissions, change of price, prior sale or withdrawal from market without notice.

Eastern PennsylvaniaI-78/I-81 SUBMARKETS

New Occupier TransactionsSUBMARKET TENANT OWNER ADDRESS SIZE (SF) TYPE

NEPA Ball Container Endurance Real Estate Group Interstate Distribution Center, Pittston, PA 1,078,200 Sale to End User

NEPA Niagara Water MRP Industrial Humboldt Industrial Park NW, Hazleton, PA 800,000 Sale to End User

LV Saddle Creek Logistics Duke Realty 53 Central Blvd, Myerstown, PA 444,080 Spec

NEPA Johnson Health Tech NorthPoint Development TradePort 164, Bldg 5, Wilkes Barre, PA 356,553 Spec

LV Pet Supplies Plus The Rockefeller Group 250 Radar Road, Northampton, PA 135,650 Spec

CompletionsSUBMARKET DEVELOPER TENANT ADDRESS SIZE (SF) TYPE

CPA Equus Capital Partners Available Shippensburg 81 Logistics Center, Shippensburg, PA 1,100,500 Spec

NEPA Endurance Real Estate Group Ball Container Interstate Distribution Center, Pittston, PA 1,078,200 Spec

NEPA Trammell Crow Company Available Valley View Trade Center, Jessup, PA 1,027,660 Spec

NEPA NorthPoint Development Chewy.com Archbald Logistics Center, Archbald, PA 1,016,480 Build to Suit

NEPA NorthPoint Development Available TradePort 124, Bldg 1, Frackville, PA 1,014,490 Spec

Under ConstructionSUBMARKET DEVELOPER TENANT ADDRESS SIZE (SF) TYPE EST DELIVERY

CPA Matrix Development Available United Business Pk, Shippensburg, PA 2,000,000 Spec Q3 2021

LV Prologis Knoll / Avail. 8783 Congdon Hill Drive, Alburtis, PA 1,088,000 Build to Suit Q4 2020

LV Majestic Realty Co. Available 3633 Commerce Ctr Blvd, Bethlehem, PA 1,041,600 Spec Q4 2020

LV NorthPoint Development Available Berks Park 78, Bethel, PA 1,011,719 Spec Q3 2021

CPA Hershey’s Hershey’s Killinger Road, Annville, PA 851,255 Build to Suit Q2 2021

Eastern PennsylvaniaI-78/I-81 SUBMARKETS

3 Industrial Big Box Research & Forecast Report | Q3 2020 | Eastern PA | Logistics & Transportation Solutions Group

5.6 5.76.3 6.4

3.2

6.3

9.7

7.1

5.7

12.7

2.9

5.3 5.54.8 4.8

0

2

4

6

8

10

12

14

2016 2017 2018 2019 2020Forecasted

Annual Deliveries, Transactions, & Net Absorption (MSF)

Summary Statistics

Current Q3 2020

Previous Q3 2019

ForecastYE 2020

Inventory 80,611,201 70,924,711 82,953,561

Vacancy Rate 8.7% 8.5% 10.0%

Availability Rate 15.8% 18.4% 14.8%Construction Starts (YTD) 5,331,424 5,308,561 7,941,124 Construction Deliveries (YTD) 5,526,358 2,610,070 7,868,718

Under Construction 5,571,384 9,824,178 5,838,724 Occupier Transactions (YTD) 6,441,672 4,714,113 9,914,476

Absorption (YTD) 5,498,732 2,610,920 6,551,492

Avg. Asking Rental $6.30 $6.15 $6.30

Lehigh Valley Eastern I-78/Lehigh Valley & Western I-78/Berks County

8.7%

$6.30

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020Forecasted

Vacancy & Asking Rental Rate

Vacancy Rate Rental Rate

Vacancy & Asking Rental Rate

$6.30

8.7%

7.9

4.15.5

7.27.9

6.8

2.7

6.1

8.0

9.9

8.1

1.3

4.95.9

6.6

0

2

4

6

8

10

12

2016 2017 2018 2019 2020Forecasted

Annual Deliveries, Occupier Transactions, & Net Absorption (MSF)

Annual Deliveries Annual Occupier Transactions Annual Net Absorption

Annual Deliveries, New Occupier Transactions & Net Absorption (MSF)

Central PA Southern I-81 & I-83 Corridor/York

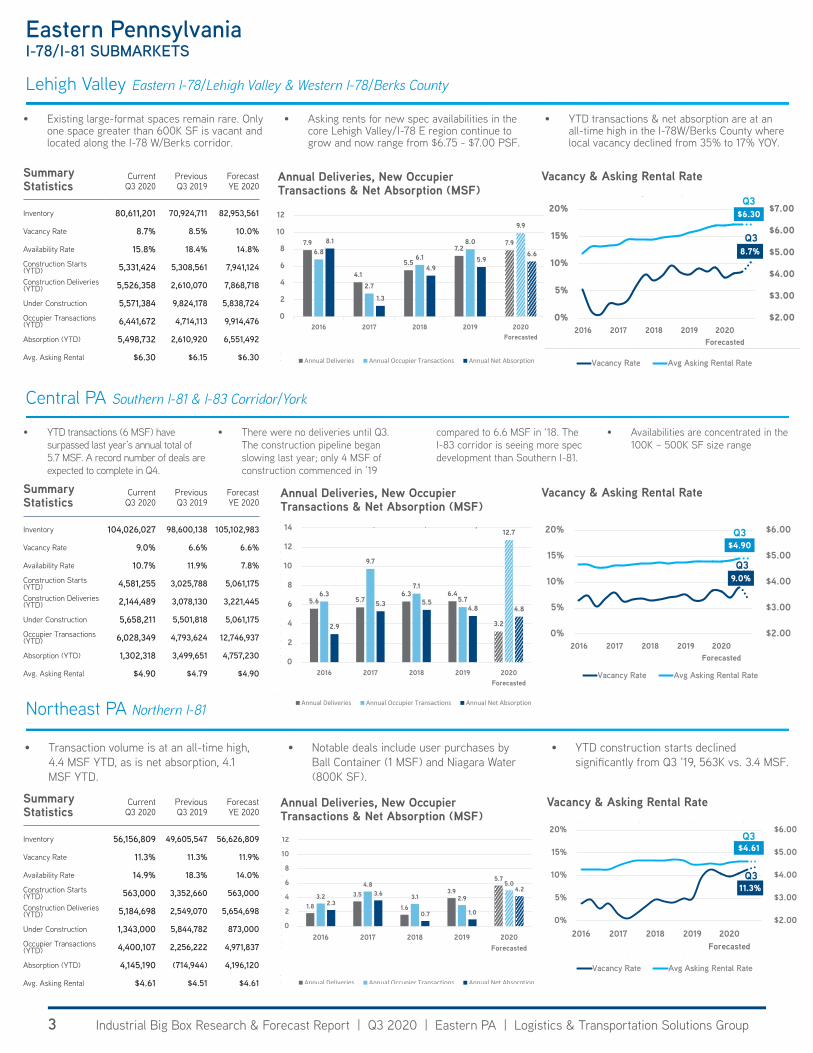

• Existing large-format spaces remain rare. Only one space greater than 600K SF is vacant and located along the I-78 W/Berks corridor.

• Asking rents for new spec availabilities in the core Lehigh Valley/I-78 E region continue to grow and now range from $6.75 - $7.00 PSF.

• YTD transactions & net absorption are at an all-time high in the I-78W/Berks County where local vacancy declined from 35% to 17% YOY.

7.9

4.15.5

7.27.9

6.8

2.7

6.1

8.0

9.9

8.1

1.3

4.95.9

6.6

0

2

4

6

8

10

12

2016 2017 2018 2019 2020Forecasted

Annual Deliveries, Occupier Transactions, & Net Absorption (MSF)

Annual Deliveries Annual Occupier Transactions Annual Net Absorption

Summary Statistics

Current Q3 2020

Previous Q3 2019

ForecastYE 2020

Inventory 104,026,027 98,600,138 105,102,983

Vacancy Rate 9.0% 6.6% 6.6%

Availability Rate 10.7% 11.9% 7.8%Construction Starts (YTD) 4,581,255 3,025,788 5,061,175 Construction Deliveries (YTD) 2,144,489 3,078,130 3,221,445

Under Construction 5,658,211 5,501,818 5,061,175 Occupier Transactions (YTD) 6,028,349 4,793,624 12,746,937

Absorption (YTD) 1,302,318 3,499,651 4,757,230

Avg. Asking Rental $4.90 $4.79 $4.90

9.0%

$4.90

$2.00

$3.00

$4.00

$5.00

$6.00

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020Forecasted

Vacancy & Asking Rental Rate

VVaaccaannccyy RRaattee AAvvgg AAsskkiinngg RReennttaall RRaattee

Vacancy & Asking Rental Rate

$4.90

9.0%

Annual Deliveries, New Occupier Transactions & Net Absorption (MSF)

• YTD transactions (6 MSF) have surpassed last year’s annual total of 5.7 MSF. A record number of deals are expected to complete in Q4.

• There were no deliveries until Q3. The construction pipeline began slowing last year; only 4 MSF of construction commenced in ’19

compared to 6.6 MSF in ‘18. The I-83 corridor is seeing more spec development than Southern I-81.

• Availabilities are concentrated in the 100K – 500K SF size range

7.9

4.15.5

7.27.9

6.8

2.7

6.1

8.0

9.9

8.1

1.3

4.95.9

6.6

0

2

4

6

8

10

12

2016 2017 2018 2019 2020Forecasted

Annual Deliveries, Occupier Transactions, & Net Absorption (MSF)

Annual Deliveries Annual Occupier Transactions Annual Net Absorption

Summary Statistics

Current Q3 2020

Previous Q3 2019

ForecastYE 2020

Inventory 56,156,809 49,605,547 56,626,809

Vacancy Rate 11.3% 11.3% 11.9%

Availability Rate 14.9% 18.3% 14.0%Construction Starts (YTD) 563,000 3,352,660 563,000 Construction Deliveries (YTD) 5,184,698 2,549,070 5,654,698

Under Construction 1,343,000 5,844,782 873,000 Occupier Transactions (YTD) 4,400,107 2,256,222 4,971,837

Absorption (YTD) 4,145,190 (714,944) 4,196,120

Avg. Asking Rental $4.61 $4.51 $4.61

11.3%

$4.61

$2.00

$3.00

$4.00

$5.00

$6.00

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020Forecasted

Vacancy & Asking Rental Rate

Vacancy Rate Avg Rental Rate

Vacancy & Asking Rental Rate

$4.61

11.3%

1.8

3.5

1.6

3.9

5.7

3.2

4.8

3.1 2.9

5.0

2.33.6

0.7 1.0

4.2

0

2

4

6

8

10

12

2016 2017 2018 2019 2020Forecasted

MSF

Annual Deliveries, Annual Occupier Transactions Annual Net Absorption (MSF)

Annual Deliveries Annual Transactions Annual Net Absorption

Annual Deliveries, New Occupier Transactions & Net Absorption (MSF)

• Transaction volume is at an all-time high, 4.4 MSF YTD, as is net absorption, 4.1 MSF YTD.

• Notable deals include user purchases by Ball Container (1 MSF) and Niagara Water (800K SF).

• YTD construction starts declined significantly from Q3 ‘19, 563K vs. 3.4 MSF.

7.9

4.15.5

7.27.9

6.8

2.7

6.1

8.0

9.9

8.1

1.3

4.95.9

6.6

0

2

4

6

8

10

12

2016 2017 2018 2019 2020Forecasted

Annual Deliveries, Occupier Transactions, & Net Absorption (MSF)

Annual Deliveries Annual Occupier Transactions Annual Net Absorption

Q3

Q3

Q3

Q3

Q3

Q3

9.0%

$4.90

$2.00

$3.00

$4.00

$5.00

$6.00

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020Forecasted

Vacancy & Asking Rental Rate

VVaaccaannccyy RRaattee AAvvgg AAsskkiinngg RReennttaall RRaattee

9.0%

$4.90

$2.00

$3.00

$4.00

$5.00

$6.00

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020Forecasted

Vacancy & Asking Rental Rate

VVaaccaannccyy RRaattee AAvvgg AAsskkiinngg RReennttaall RRaattee

Northeast PA Northern I-81

> While there remains lingering uncertainty related to COVID-19, the greater Philadelphia Market continues to flourish. Q3 saw robust activity in the market with over 1MM SF of absorption. Vacancy ticked down to 3.4% in Q3 in large part due to Amazon leasing the largest two remaining blocks of space in the market.

> The lack of supply will not last long as multiple projects will break ground in Q4 of 2020 and deliver almost 2MM SF of Class-A industrial product in mid-to-late 2021 – the largest of these buildings being the 420,000 SF at Alliance HSP’s Delco Logistics Center.

> Existing tenants are seeking out the efficiencies and amenities new Class A projects can provide. Additionally, we continue to see strong demand from tenants which are new to the market seeking closer proximity to the dense population pockets and the labor that this population can provide.

> Developers and capital sources continue to seek out opportunities in these markers as demand from these tenants validates their interest.

4 Industrial Big Box Research & Forecast Report | Q3 2020 | Eastern PA | Logistics & Transportation Solutions Group

0.8

0.10.0

0.8

0.5

1.6

0.91.0

1.2

2.0

1.6

0.6

-0.4

0.3

1.1

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2016 2017 2018 2019 2020Forecasted

MSF

Annual Deliveries, Occupier Transactions & Net Absorption (MSF)

Annual Deliveries Annual Transactions Annual Absorption

Q3 Highlights

Greater PhiladelphiaI-95 CORRIDOR

“Leasing activity remains robust as newly delivered product is absorbed by both the existing tenant base and new occupiers seeking urban-proximate facilities.” — TOM GOLARZ

Summary Statistics

Current Q3 2020

Previous Q3 2019

ForecastYE 2020

Inventory 17,969,888 17,269,243 17,969,888

Vacancy Rate 3.4% 2.7% 2.7%

Availability Rate 4.6% 6.4% 15.3%Construction Starts (YTD) 552,300 235,240 2,601,660Construction Deliveries (YTD) 465,405 574,059 465,405

Under Construction 765,892 235,240 2,815,252Occupier Transactions (YTD) 1,250,040 659,100 1,956,915

Absorption (YTD) 1,009,000 745,184 1,130,875

Avg. Asking Rental $6.82 $7.54 $6.31

3.4%

$6.82

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

0%

2%

4%

6%

8%

10%

2016 2017 2018 2019 2020Forecasted

Vacancy Vs. Average Asking Rate PSFVacancy & Asking Rental Rate

$6.82

3.4%

Annual Deliveries, New Occupier Transactions & Net Absorption (MSF)

7.9

4.15.5

7.27.9

6.8

2.7

6.1

8.0

9.9

8.1

1.3

4.95.9

6.6

0

2

4

6

8

10

12

2016 2017 2018 2019 2020Forecasted

Annual Deliveries, Occupier Transactions, & Net Absorption (MSF)

Annual Deliveries Annual Occupier Transactions Annual Net Absorption

11.3%

$4.61

$2.00

$3.00

$4.00

$5.00

$6.00

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020Forecasted

Vacancy & Asking Rental Rate

Vacancy Rate Avg Rental Rate

Q3

Q3

New Occupier TransactionsSUBMARKET TENANT OWNER ADDRESS SIZE (SF) TYPE

PHL Amazon Angelo, Gordon & Co. 1 Geoffrey Rd, Fairless Hills 415,000 Older Gen

PHL Amazon LBA Logistics 3750 State Rd, Bensalem 235,240 Spec

PHL Baldor Foods NorthPoint Development 7071 Milnor St, Philadelphia 222,000 Sale to End User

PHL Amazon Black Creek Group 3025 Meetinghouse Rd, Philadelphia 207,500 Spec

CompletionsSUBMARKET DEVELOPER TENANT ADDRESS SIZE (SF) TYPE

PHL NorthPoint Development KLS 11601 Roosevelt Blvd, Philadelphia 465,405 Build to Suit

Under ConstructionSUBMARKET DEVELOPER TENANT ADDRESS SIZE (SF) TYPE EST DELIVERY

PHL Foxfield Industrial Available 900 Schuylkill River Rd 330,000 Spec Q2 21

PHL NorthPoint Development Baldor Foods 7071 Milnor St, Philadelphia 222,000 Build to Suit Sale Q2 21

Colliers International Eastern Pennsylvania Team Logistics & Transportation Solutions GroupEight Tower Bridge, 161 Washington St Suite 1090, Conshohocken, PA 19428+1 610 684 1850

The foregoing information was furnished to us by sources which we deem to be reliable, but no warranty or representation is made as to the accuracy thereof. Subject to correction of errors, omissions, change of price, prior sale or withdrawal from market without notice.

FEATURED AVAILABILITIES

Prologis Carlisle 1600 Distribution Drive, Allentown, PA 119,310 SF For LeaseContact: Mark Chubb

2040 N. Union Street Middletown, PA 507,045 SF For LeaseContact: Michael Zerbe

Mark ChubbSr. Managing Director | Principal +1 610 684 [email protected]

Michael ZerbeSr. Managing Director | Principal +1 610 684 [email protected]

Summer CoulterSr. Vice President+1 610 684 [email protected]

Kirsten KurzLogistics Market Analyst +1 610 615 [email protected]

FOR MORE INFORMATION Contact the Logistics & Transportation Solutions Group today.

Prologis Lehigh Valley West 8250 Industrial Blvd, Breinigsville, PA 120,000 SF For LeaseContact: Michael Zerbe

CLICK TO VISIT

Michael GolarzSenior Vice President+1 215 928 [email protected]

Tom GolarzVice President+1 215 928 [email protected]

EASTERN PENNSYLVANIA EXPERTS

GREATER PHILADELPHIA EXPERTS

Colliers InternationalGreater Philadelphia TeamTen Penn Center, 1801 Market StreetSuite 500, Philadelphia, PA 19103+1 215 925 4600

Core5 Logistics Center at Park 31 Wambold & Schoolhouse Road, Souderton, PA Building 1: 199,360 SF | Building 2: 199,000 SF For LeaseContact: Tom Golarz

5501 Whitaker AvenuePhiladelphia, PA1,312,706 SF For LeaseContact: Michael Golarz

Delaware Logistics Center1290 S. DuPont Hwy, New Castle, DEBuilding 1: 577,829 SF | Building 2: 217,748 SF For LeaseContact: Mark Chubb