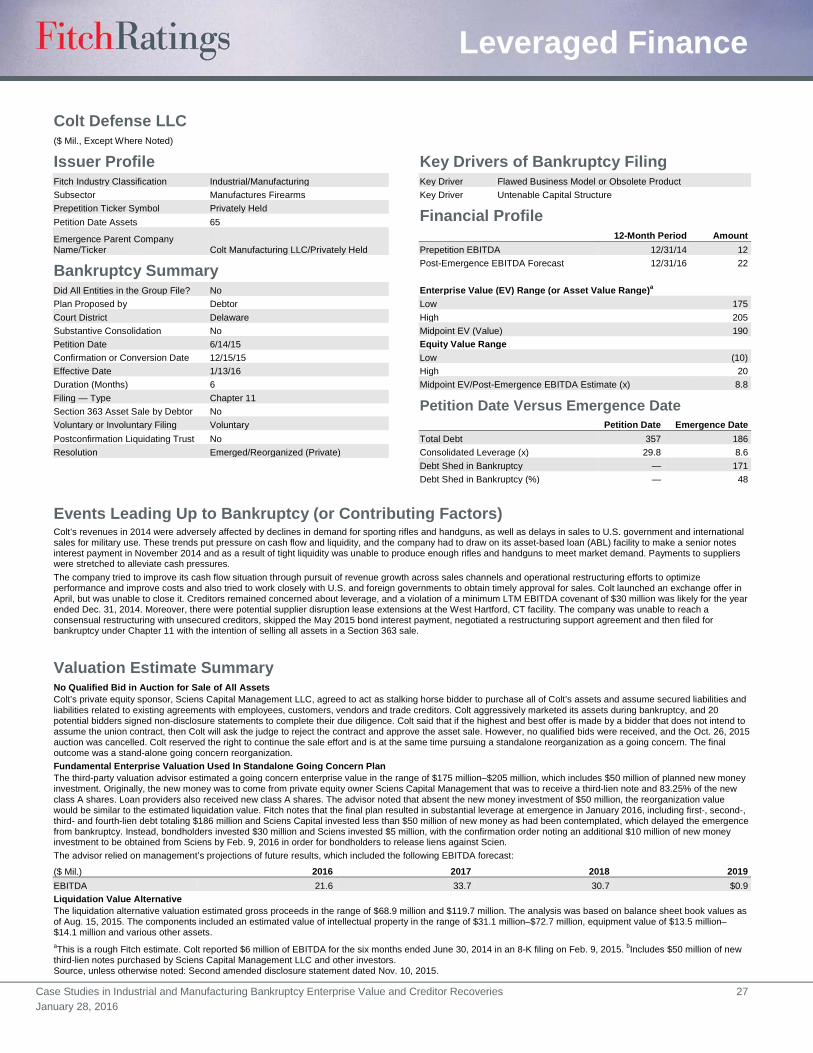

Industrial and Manufacturing Bankruptcy Enterprise …2a746fa1-b692-4bda-af51... · Case Studies in...

95

January 2016 Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries Fitch Case Studies — Edition IX

Transcript of Industrial and Manufacturing Bankruptcy Enterprise …2a746fa1-b692-4bda-af51... · Case Studies in...

January 2016

Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries Fitch Case Studies — Edition IX

Leveraged Finance

www.fitchratings.com January 28, 2016

Corporates / U.S.A.

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries Special Report

Relatively High Valuation Multiples: There was a 6.3x median multiple of reorganization enterprise value/forward EBITDA for the Industrial and Manufacturing (I&M) sector cases analyzed in this edition of the bankruptcy case study series. The I&M sector median is modestly higher than the 6.0x cross-corporate sector exit multiple in Fitch Ratings’ U.S. bankruptcy case study database. Of the I&M sample, 39% reorganized at a multiple above 7x.

Outstanding First-Lien Recoveries: The average ultimate recovery rate on the 41 first-lien issues of the I&M defaulters was 82% of par value. Of the first-lien debt claims, 68% received distributions of 91% or more of par value, which is equivalent to Fitch’s highest, RR1 category. Many of the first-lien issues with less robust recoveries had a first-lien security interest limited to non-working capital assets and had a second-lien interest on inventory and receivables.

Material Debt Reduction Achieved: The I&M cases analyzed achieved average balance sheet debt reduction of 62% from the bankruptcy date to the emergence date, which was slightly below the 68% cross-sector average, but consistent with higher sector exit multiples. The median debt/forward EBITDA was 3.8x at emergence, compared with an unsustainable level of 12.2x as of filing, using EBITDA for the year prior to filing (medians exclude companies with negative EBITDA and those that lacked disclosure of forecasted or historical EBITDA).

Few Liquidations: Just 11% of the I&M cases were resolved through a liquidation outcome, which was slightly below the 13% piecemeal asset sale liquidation rate among the 204 companies in Fitch’s case study database. The most common case outcome was reorganization as a privately held going concern, which encompassed 63% of the sector case outcomes.

Low Sector Default Rate: The I&M sector’s 2.4% average annual default rate was materially lower than the 4.1% average U.S. high-yield bond market rate from 1980 to 2015. Sector default rate peaks were also lower, and the I&M rate was just 0.6% in 2015. This may be explained by the fact that general manufacturers are a diverse group with a broad range of business risks and lack sector-wide exposure to swings in any single commodity price

Idiosyncratic Default Drivers: Most bankruptcy filings were made by highly leveraged companies that were confronted by individual liquidity or business challenges that could not be overcome out of court. Drivers included flawed business models, production problems, accounting issues, higher raw material costs, lack of funding market access and steep declines in demand for key products due to cyclical downturns or competition. More than half the sample defaulted in the recessionary period from 2008 to 2010.

Small Issuers at Risk: The I&M sector is dominated by global-scale competitors with billions of dollars in assets and investment-grade credit profiles. However, over 85% of the I&M cases analyzed had assets of less than $1 billion, and most were significantly smaller. Most of the general manufacturers in the study had relatively limited product or customer diversity. Median petition date assets and debt for sector cases were $347 million and $380 million, respectively. Across all corporate sectors, defaulters in the database had median assets of $732 million and debt of $613 million (as the early editions focused on the largest cases).

Disclaimer: Fitch cautions that the case studies are not intended to provide exact recovery outcomes, valuations or legal opinions. Estimates in this report may vary significantly from final case outcomes. Related Research Fitch U.S. High Yield Default Insight (January 2016) Fitch U.S. Leveraged Loan Default Insight (December 2015) Healthcare, Food, Beverage and Consumer Bankruptcy Enterprise Value and Creditor Recoveries (Fitch Case Studies ― Edition VIII) (August 2015) Energy, Power and Commodities Bankruptcy Enterprise Value and Creditor Recoveries (Fitch Case Studies — Edition VII) (April 2015) Automotive Sector Bankruptcy Enterprise Value and Creditor Recoveries (Fitch Case Studies Edition VI) (December 2014)

Analysts Leveraged Finance Sharon Bonelli +1 212 908-0581 [email protected] John Shen-Sampas +1 212 612-7881 [email protected] Industrials Akin Adekoya +1 212 908-0312 [email protected]

Craig Fraser +1 212 908-0310 [email protected]

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 2 January 28, 2016

Case Study Table of Contents Case Study Page Case Study Page Aleris International, Inc. 12 National RV Holdings, Inc. 54 American LaFrance, LLC 15 Neenah Enterprises, Inc. 57 AMTROL Holdings, Inc. 18 The Newark Group, Inc. 60 Atrium Companies, Inc. 21 Oneida Ltd. 63 Chassix Inc. 24 O’Sullivan Industries, Inc. 66 Colt Defense LLC 27 Panolam Industries International, Inc. 69 EaglePicher Holdings Inc. 30 Propex Inc. 72 Exide Technologies 33 Reddy Ice Holdings, Inc. 75 Fedders Corporation 36 Simmons Company 78 Global Power Equipment Group Inc. 39 Solyndra LLC 81 International Aluminum Corp. 42 True Temper Sports, Inc. 84 Masonite Corporation 45 Wellman Inc. 87 Momentive Performance Materials Inc. 48 Wolverine Tube, Inc. 90 Motor Coach Industries International 51

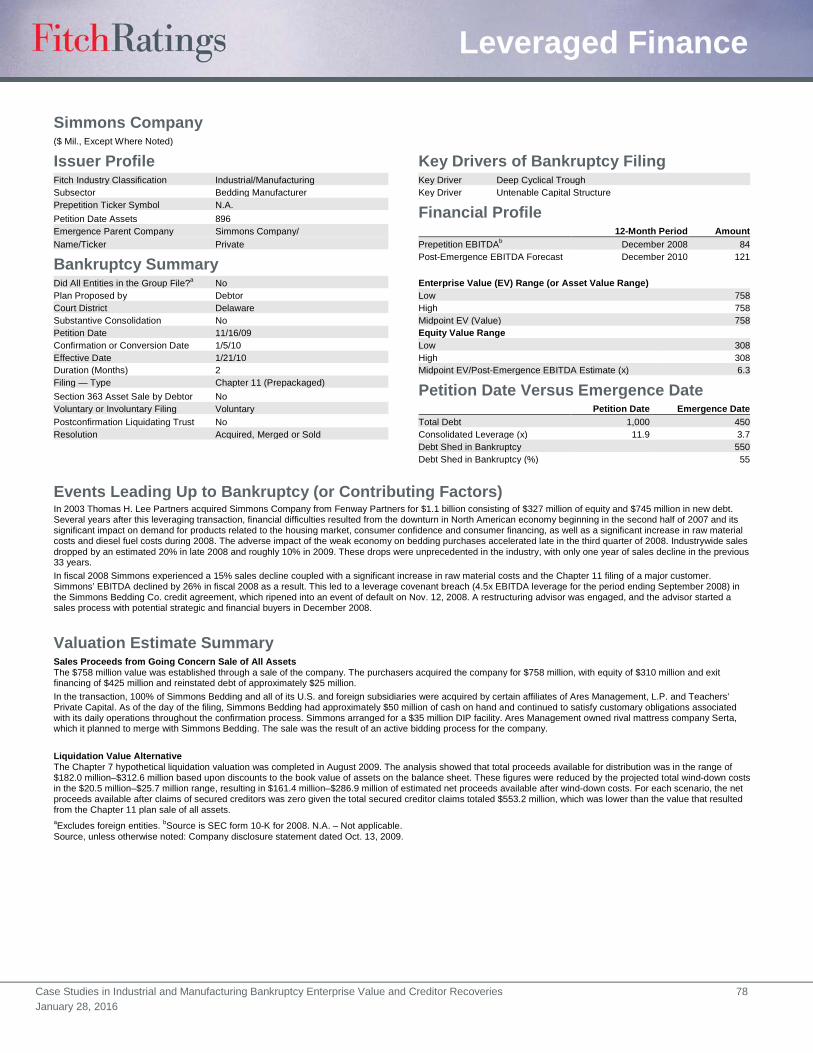

Going Concern Reorganizations Are Customary The vast majority of the 27 I&M cases studied emerged from bankruptcy as going concern operations. This includes companies that emerged as independent stand-alone entities and those that operated under new owners that bought all assets and continued to run the business. The going concern enterprise valuations are detailed on page 3.

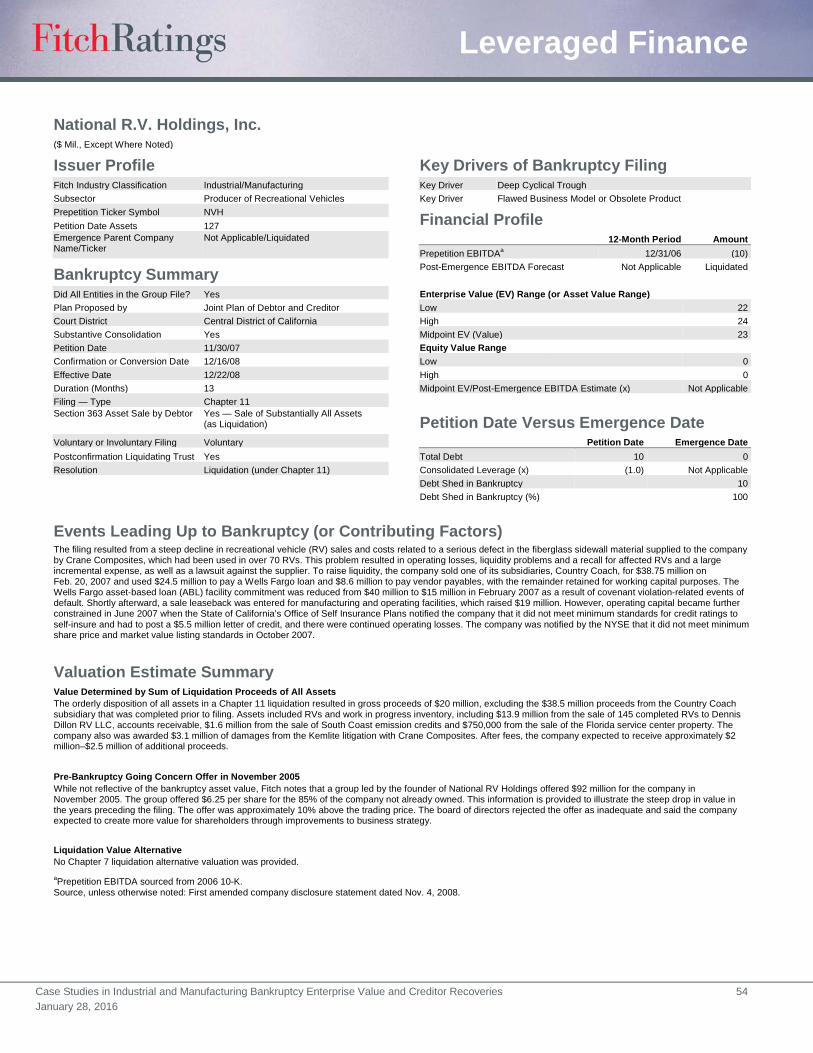

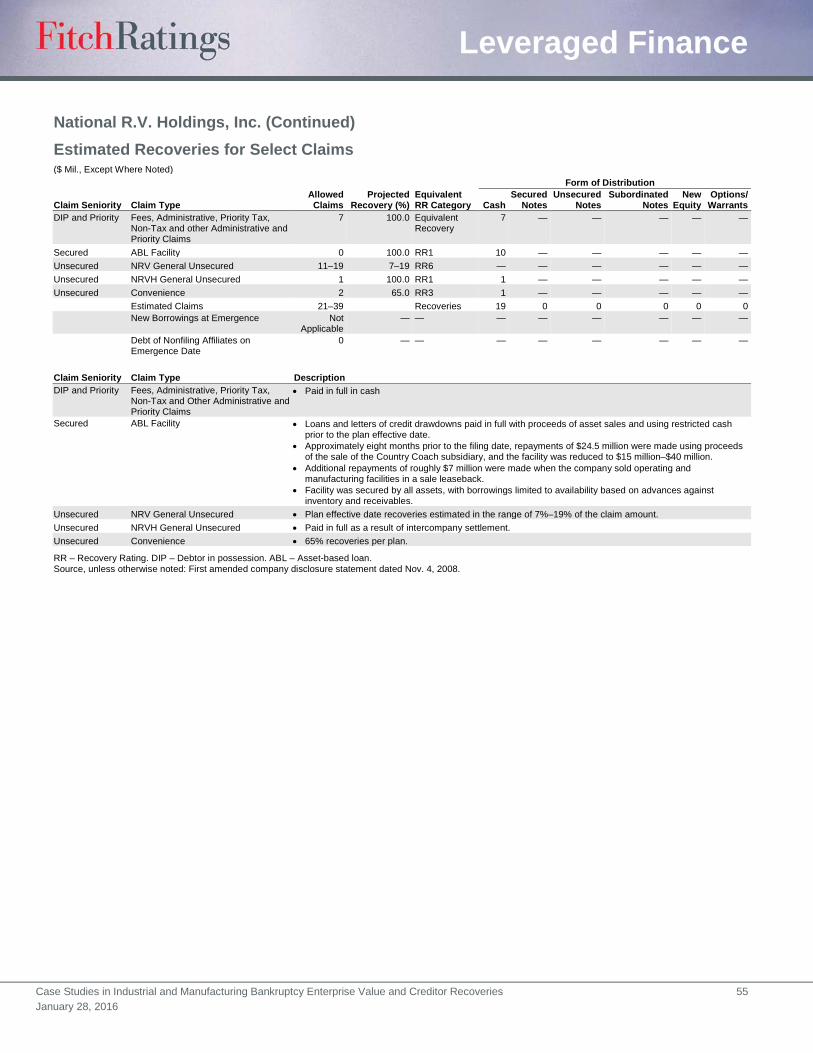

However, three of the 27 companies, Fedders Corp., Solyndra LLC and National RV Holdings, Inc., liquidated all assets in piecemeal sale processes and ceased to exist.

Fedders was a heating and air conditioning manufacturer that had shrinking margins in its residential air conditioner and dehumidifier business because of pricing pressures from its two largest customers, Walmart and Home Depot. A decision was made to exit this business. The company made acquisitions in other heating, ventilation and air conditioning business lines, including commercial customer products, but the transition did not go smoothly. New government regulations on energy efficiency also slowed sales. In the liquidation, assets in various business lines were sold piecemeal in numerous transactions and Fitch estimated a company value by summing the proceeds of the sales. Unsecured recoveries were poor.

Solyndra was a startup formed in 2005 that raised money to build and operate photovoltaic solar panel fabrication plants. The company was unable to compete with foreign, state-sponsored manufacturers on price or meet production milestones required by lenders. Cash flow challenges were exacerbated when European government subsidies for solar power were

Related Criteria Recovery Ratings and Notching Criteria for Non-Financial Corporate Issuers (November 2014)

Acquired/Merged/Sales of All Assets

15%

Emerged/Reorganized Private

63%

Liquidated11%

Emerged/Reorganized Public

11%

Industrial and Manufacturing Case Outcome

Source: Company disclosure statements, Fitch Ratings.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 3 January 28, 2016

reduced. The company was unable to raise additional debt to bridge fund operations until cash flows turned positive following more borrowing to fund construction of a second fabrication facility. All operations were suspended and liquidation ensued, with the sale of the headquarters building bringing in most of the total proceeds. Unsecured creditors were wiped out in the liquidation and junior secured creditors obtained low recoveries.

National RV Holdings was a manufacturer of recreational vehicles. It was a small company with $127 million of petition date assets and limited financial resources. The filing resulted from a steep decline in sales and an increase in costs relating to a serious defect in a sidewall material used in certain of its RVs. This led to recalls and liquidity problems. One division was sold prior to filing to raise cash, and remaining assets, including real estate, work in progress and completed inventory, were sold piecemeal following the filing.

Enterprise Valuation Fundamental enterprise valuations for going concern reorganization plans are usually prepared by third-party advisors and included in the disclosure statement for the proposed reorganization plan that is filed on the case docket. The valuations and estimated claims by priority establish estimated recoveries for each level of creditor prior to claimholder voting on a plan. Fitch uses these fundamental enterprise valuation estimates in many of the cases studies to establish the estimated enterprise value and exit multiples.

In other case studies, Fitch used the proceeds of actual going concern asset sales or piecemeal balance sheet asset liquidations to estimate the amounts available for distributions to prepetition creditors and other claimants on the plan effective date (emergence).

Determining an appropriate going concern valuation used for plan purposes is critical to a successful reorganization and often hotly contested by creditors at different levels of a capital structure, because it determines which seniority of claimholders will assume a control position in the new stock.

Twenty-three of the 27 I&M cases studied by Fitch had sufficient fundamental valuation and EBITDA forecast data available for Fitch to estimate a reorganization multiple of enterprise value to forward EBITDA. Fitch uses the management forecast of EBITDA for the first full year following the year of emergence in calculating reorganization multiples.

Nearly half of the 23 sector cases emerged at exit multiples between 5x and 7x the post-emergence year 1 forecasted cash flow. The distribution chart above compares reorganization multiple for the I&M sector and the total corporate group and illustrates the relative lack of low reorganization multiple outliers below 5x in the I&M sector. Nine of 23 sector defaulters

05

101520253035

≤5.0 5.1–6.0 6.1–7.0 7.1–9.0 ≥9.0

% Total Industrial % Total Cross Sector

Source: Company disclosure statements, Fitch Ratings.

Reorganization Multiple Comparison(Enterprise Value/Forward EBITDA, x)

(% of Sample)

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 4 January 28, 2016

reorganized at a multiple above 7x, which is relatively rich for a bankruptcy emergence valuation.

The 6.3x median reorganization multiple for the I&M defaulters is modestly higher than the 6.0x cross-sector exit multiple in Fitch’s bankruptcy case database. The cross-sector multiple is based on 155 of 204 cases in the database that had multiples available.

The full list of sector reorganization multiples is above.

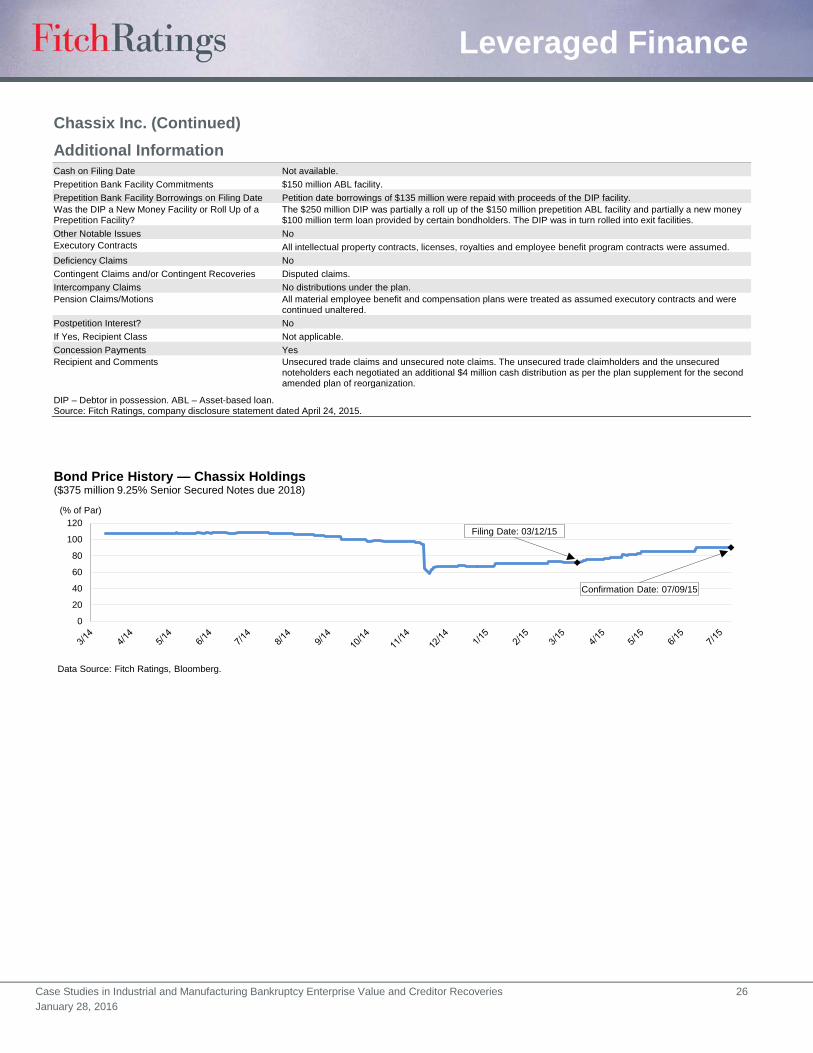

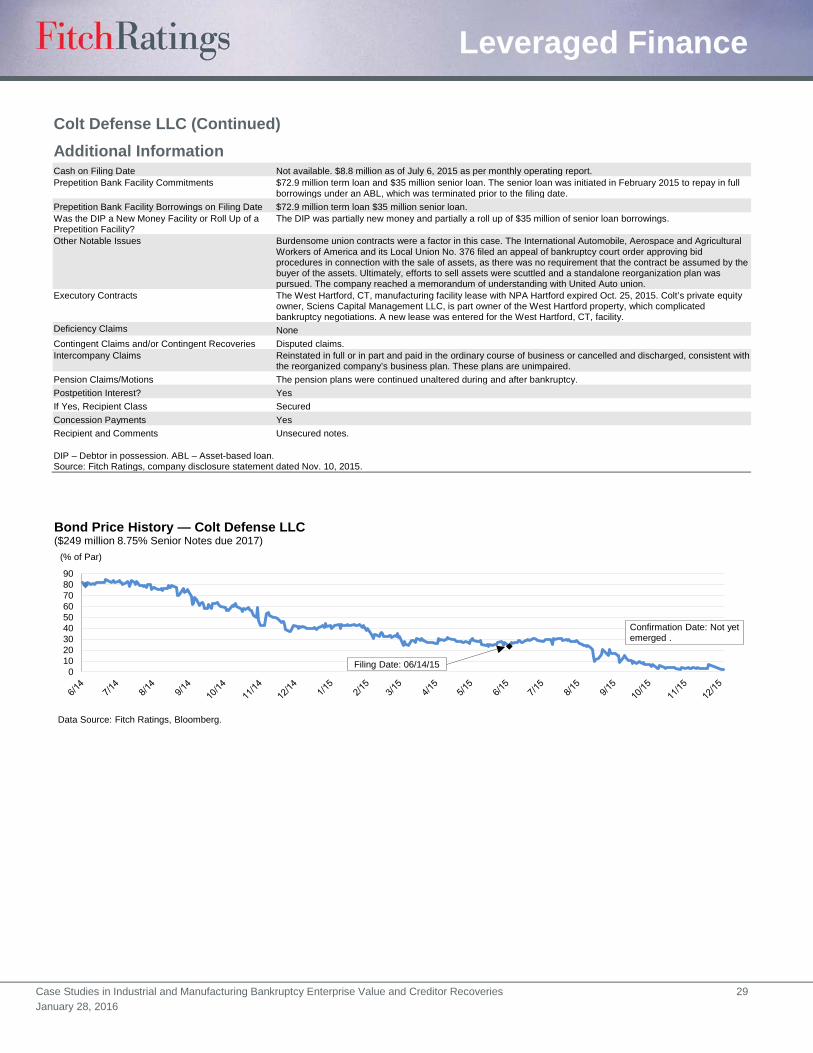

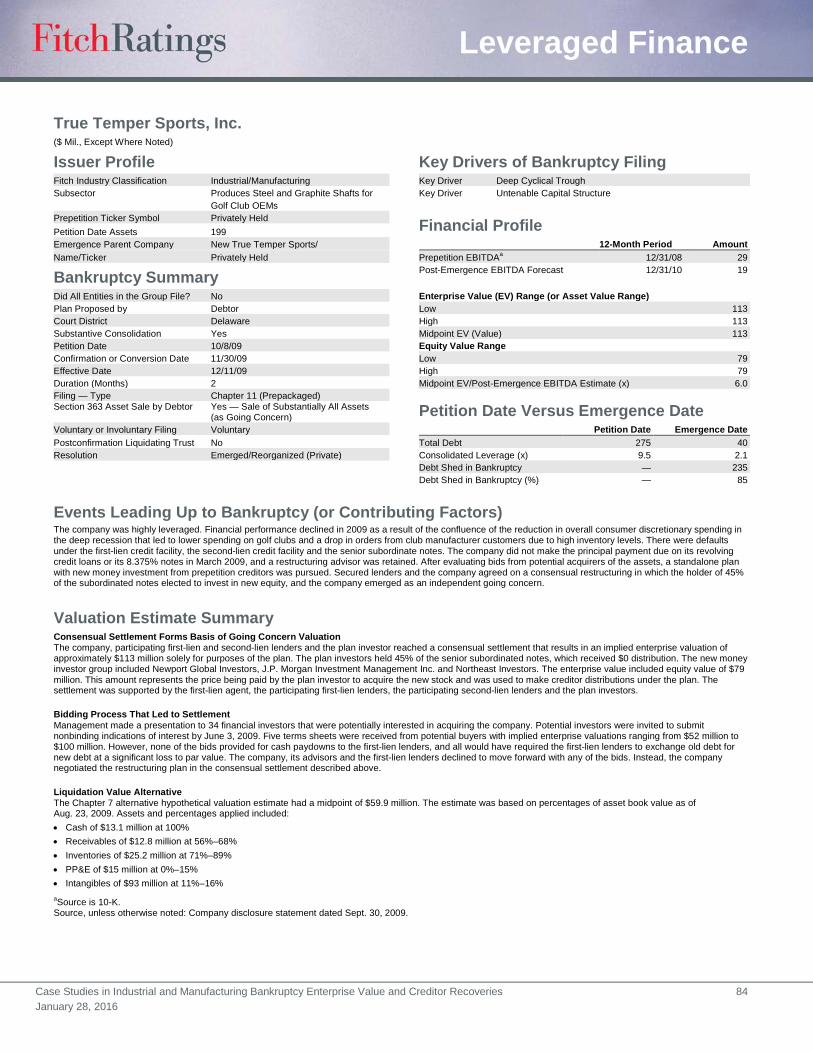

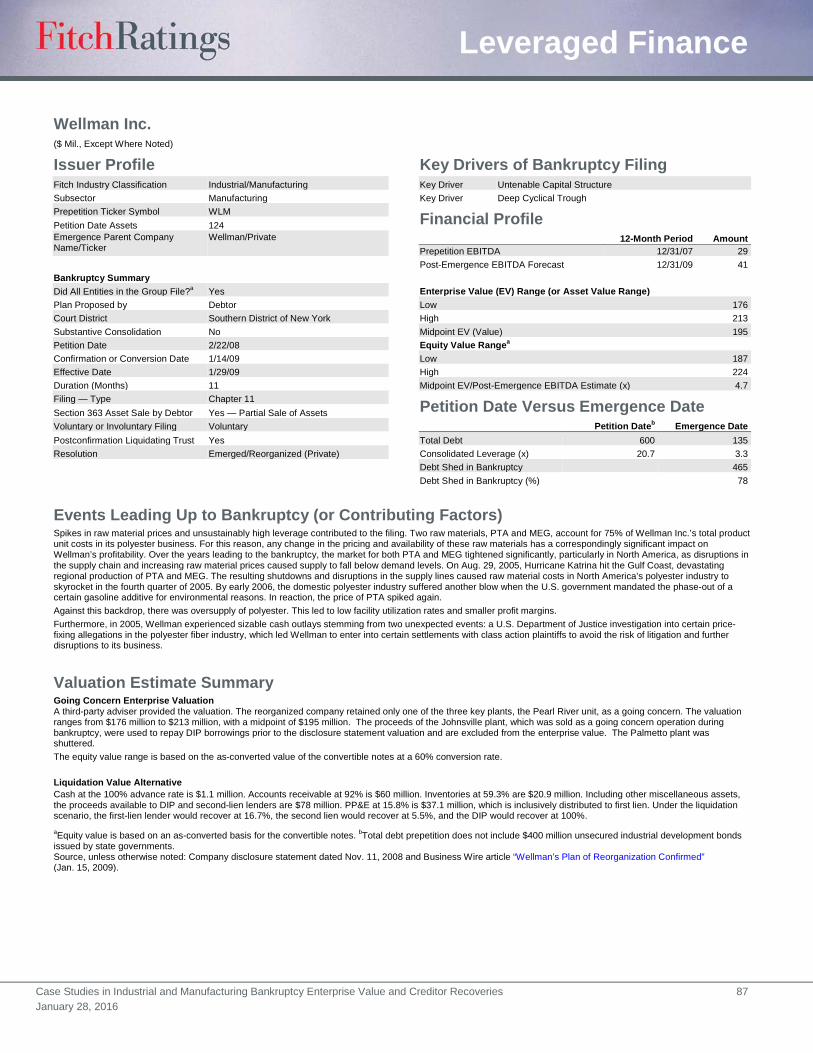

Two I&M defaulters were reorganized at a very low exit multiple: Chassix Inc. (3.9x) and Wellman Inc. (4.7x) were the two low-end outliers.

Chassix is a producer of precision casting and machining for the automotive sector that was formed in 2013 via the merger of two private equity owned auto equipment manufacturers. The company filed in 2015 due to large decreases in cash flow stemming from production and cost issues. The company’s production facilities required extensive upgrades and repairs, and when auto production levels spiked, the company had trouble keeping up with customer volumes. Manufacturing costs increased and quality suffered.

Chassix’s third-party valuation advisor estimated an enterprise value that was 3.9x of forecasted year 1 (2016) exit EBITDA of $128 million. The management forecast also showed slight declines in EBITDA to $116 million by 2019, and the continuing lackluster cash flow outlook through the later years of the forecast period likely weighed on the estimated valuation. Despite the low multiple, the asset based lending (ABL) lenders obtained full recovery via a debtor in possession (DIP) rollup of their loan, and first-lien note claims received 98% recovery in a debt for equity swap. See the Related Research link to an automotive sector bankruptcy case study published in December 2014 for information on earlier auto sector cases.

Industrial and Manufacturing Bankruptcy Reorganization Multiples Company

EV/EBITDA Reorganization Multiple (x)

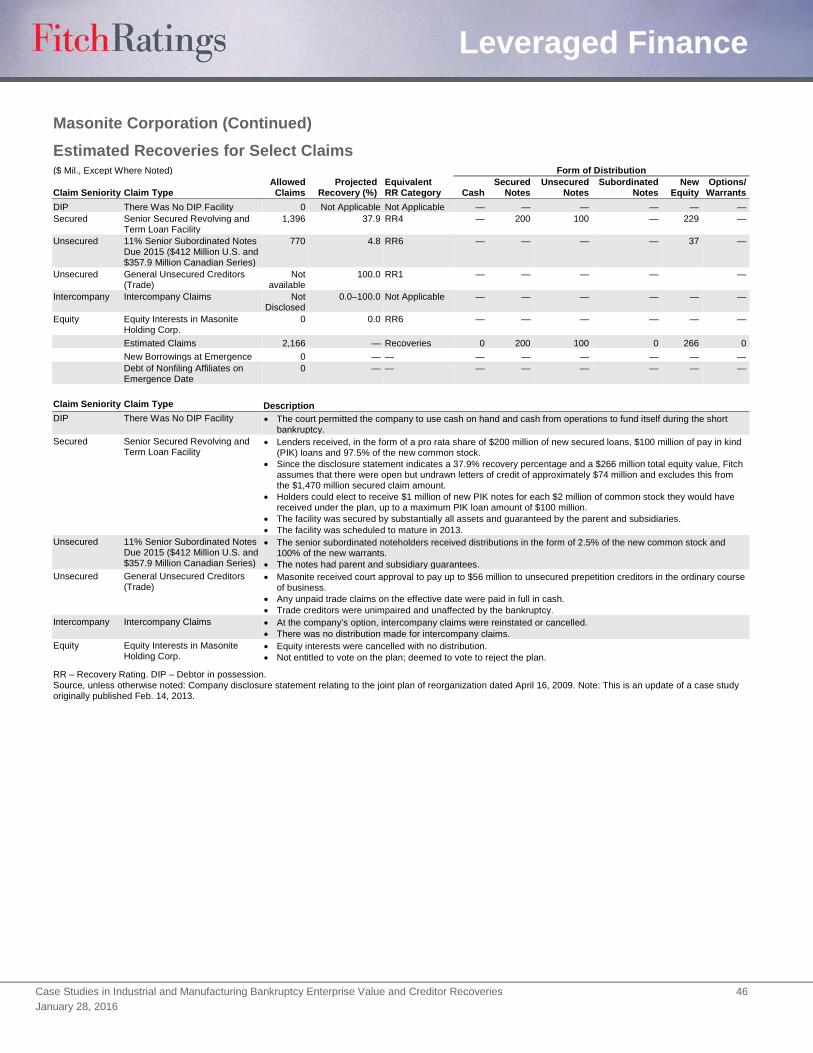

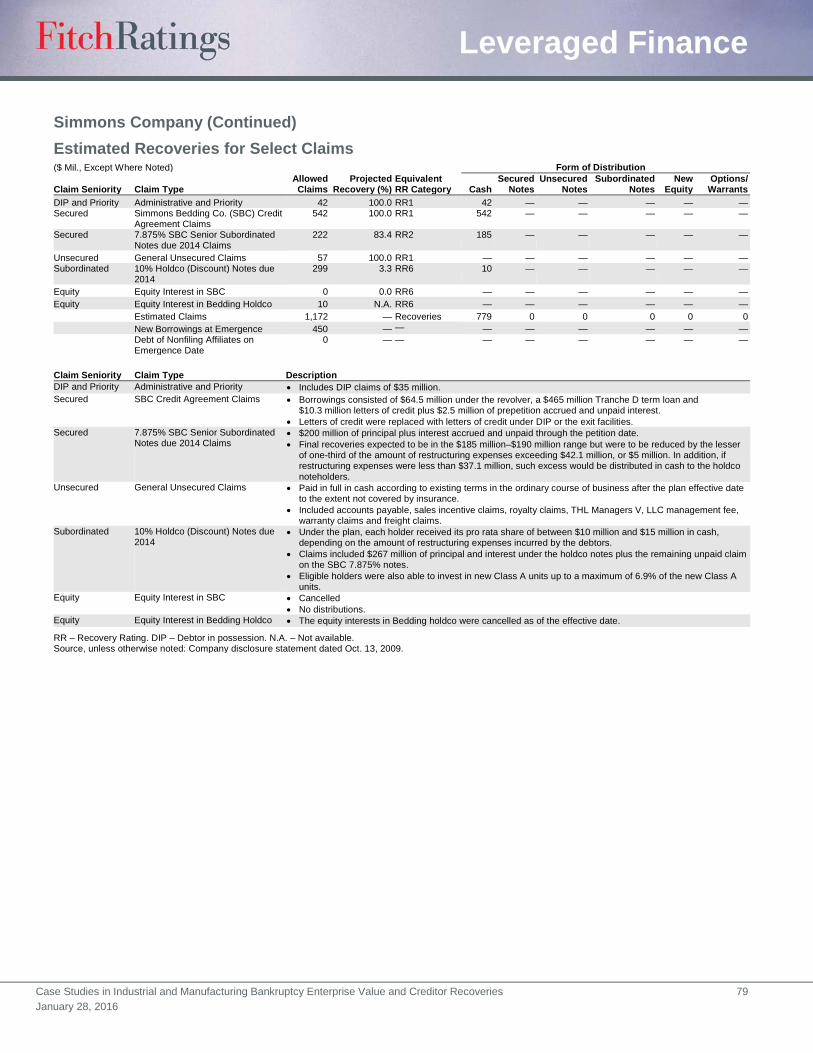

Chassix Inc. 3.9 Wellman Inc 4.7 Oneida Ltd. 5.0 The Newark Group, Inc. 5.1 American LaFrance, LLC 5.4 Aleris International, Inc. 5.6 Neenah Enterprises, Inc. 5.7 True Temper Sports, Inc. 6.0 Reddy Ice Holdings, Inc. 6.2 Simmons Company 6.3 Atrium Companies 6.3 Exide Technologies 6.3 AMTROL Holdings, Inc. 6.5 Motor Coach Industries International 6.7 EaglePicher Holdings Inc. 7.3 Momentive Performance Materials Inc. 7.5 O’Sullivan Industries, Inc. 7.8 Masonite Corporation 8.2 Colt Defense LLC 8.8 Wolverine Tube, Inc. 9.5 Global Power Equipment Group Inc. 9.9 Panolam Industries International, Inc. 10.8 International Aluminum Corp. 54.7 Median EV/EBITDA 6.3 EV – Enterprise value. Source: Company disclosure statements and SEC filings, Fitch Ratings.

6.3x Median I&M Sector Reorganization Multiple

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 5 January 28, 2016

Wellman was a polyester manufacturer that had several business challenges at the time it was valued at a point of low market valuations during the recession in 2008. Both factors likely contributed to the below-average 4.7x multiple. Capacity utilization was low and raw material cost increases were pressuring cash flows. Wellman’s revolver debt was also paid in full via a DIP takeout; however, the first-lien noteholders received a much lower, 34%, recovery.

An outlier on the high end of exit multiples was International Aluminum Corp. The 54.7x multiple reflects management’s very low EBITDA forecast in the first fiscal year following exit of only $1.4 million. In later forecast years, projected EBITDA improves significantly, to $5.6 million in year 2, $11.3 million in year 3 and $15.9 million by year 4. If the year 2 EBITDA forecast is used to estimate the exit multiple, it would be a more typical 6.8x.

Most of the I&M management forecasts anticipated higher post-emergence EBITDA compared with prepetition cash flows. Sixteen of the 27 sector cases had forecasts incorporating growth of EBITDA, six had expectations of lower EBITDA and five had insufficient cash flow information to compare due to going-out-of-business liquidations or lack of disclosure. A comparison of prepetition EBITDA for the year prior to bankruptcy filing and year 1 post-emergence forecasts is shown in Appendix A.

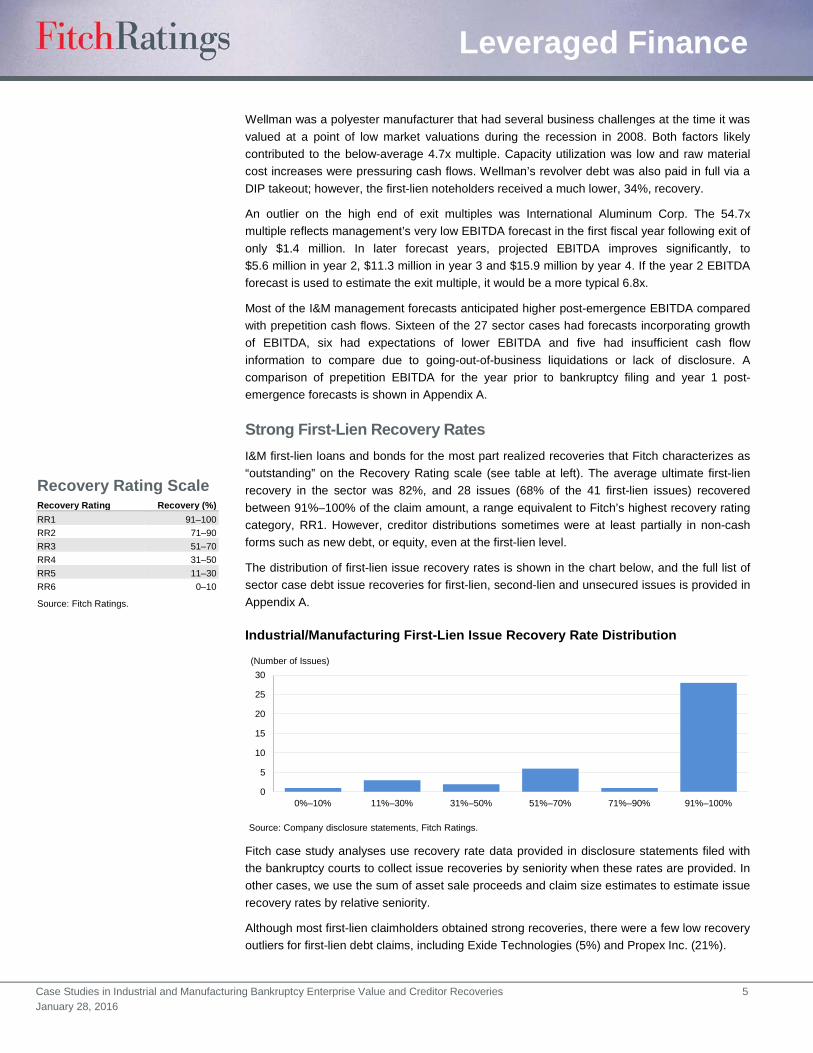

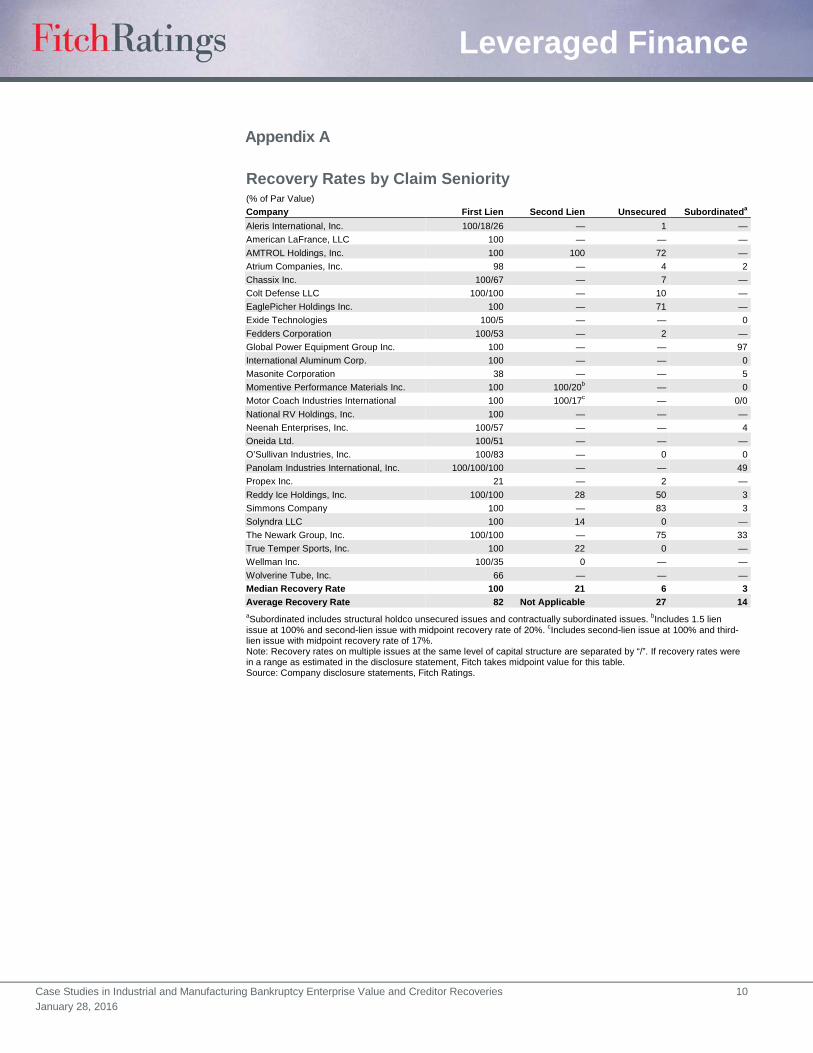

Strong First-Lien Recovery Rates I&M first-lien loans and bonds for the most part realized recoveries that Fitch characterizes as “outstanding” on the Recovery Rating scale (see table at left). The average ultimate first-lien recovery in the sector was 82%, and 28 issues (68% of the 41 first-lien issues) recovered between 91%–100% of the claim amount, a range equivalent to Fitch’s highest recovery rating category, RR1. However, creditor distributions sometimes were at least partially in non-cash forms such as new debt, or equity, even at the first-lien level.

The distribution of first-lien issue recovery rates is shown in the chart below, and the full list of sector case debt issue recoveries for first-lien, second-lien and unsecured issues is provided in Appendix A.

Fitch case study analyses use recovery rate data provided in disclosure statements filed with the bankruptcy courts to collect issue recoveries by seniority when these rates are provided. In other cases, we use the sum of asset sale proceeds and claim size estimates to estimate issue recovery rates by relative seniority.

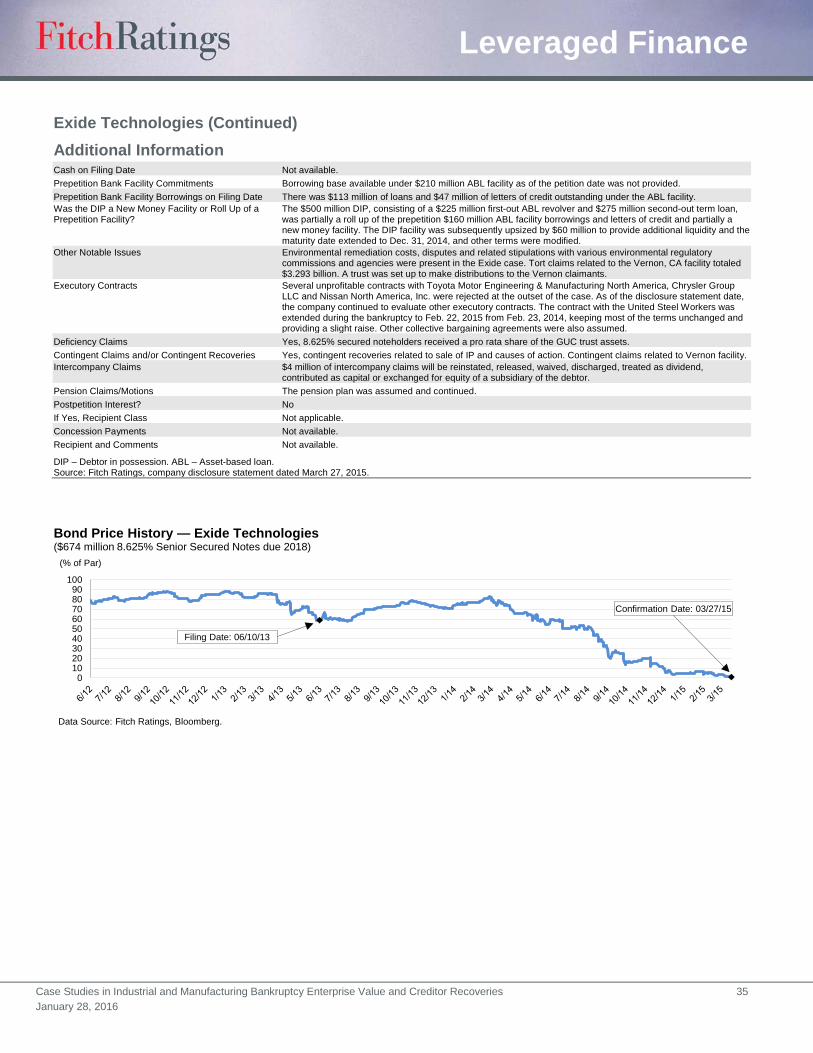

Although most first-lien claimholders obtained strong recoveries, there were a few low recovery outliers for first-lien debt claims, including Exide Technologies (5%) and Propex Inc. (21%).

Recovery Rating Scale Recovery Rating Recovery (%) RR1 91–100 RR2 71–90 RR3 51–70 RR4 31–50 RR5 11–30 RR6 0–10

Source: Fitch Ratings.

0

5

10

15

20

25

30

0%–10% 11%–30% 31%–50% 51%–70% 71%–90% 91%–100%

(Number of Issues)

Source: Company disclosure statements, Fitch Ratings.

Industrial/Manufacturing First-Lien Issue Recovery Rate Distribution

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 6 January 28, 2016

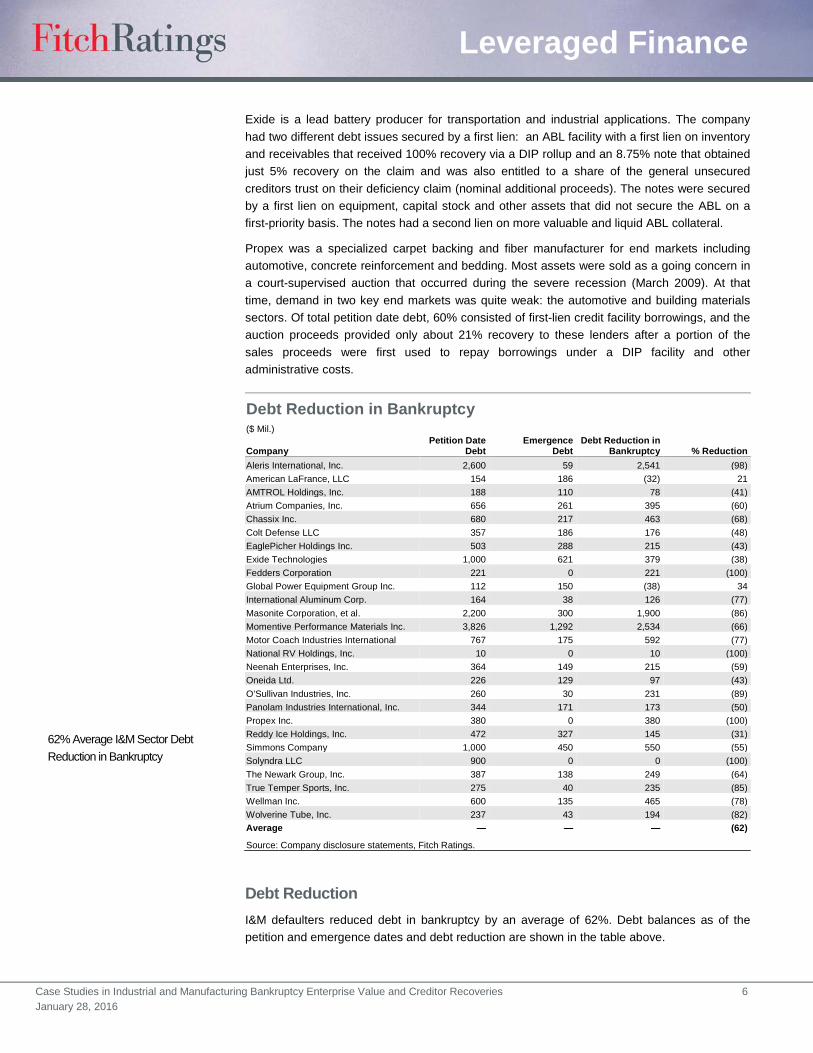

Exide is a lead battery producer for transportation and industrial applications. The company had two different debt issues secured by a first lien: an ABL facility with a first lien on inventory and receivables that received 100% recovery via a DIP rollup and an 8.75% note that obtained just 5% recovery on the claim and was also entitled to a share of the general unsecured creditors trust on their deficiency claim (nominal additional proceeds). The notes were secured by a first lien on equipment, capital stock and other assets that did not secure the ABL on a first-priority basis. The notes had a second lien on more valuable and liquid ABL collateral.

Propex was a specialized carpet backing and fiber manufacturer for end markets including automotive, concrete reinforcement and bedding. Most assets were sold as a going concern in a court-supervised auction that occurred during the severe recession (March 2009). At that time, demand in two key end markets was quite weak: the automotive and building materials sectors. Of total petition date debt, 60% consisted of first-lien credit facility borrowings, and the auction proceeds provided only about 21% recovery to these lenders after a portion of the sales proceeds were first used to repay borrowings under a DIP facility and other administrative costs.

Debt Reduction I&M defaulters reduced debt in bankruptcy by an average of 62%. Debt balances as of the petition and emergence dates and debt reduction are shown in the table above.

Debt Reduction in Bankruptcy ($ Mil.)

Company Petition Date

Debt Emergence

Debt Debt Reduction in

Bankruptcy % Reduction Aleris International, Inc. 2,600 59 2,541 (98) American LaFrance, LLC 154 186 (32) 21 AMTROL Holdings, Inc. 188 110 78 (41) Atrium Companies, Inc. 656 261 395 (60) Chassix Inc. 680 217 463 (68) Colt Defense LLC 357 186 176 (48) EaglePicher Holdings Inc. 503 288 215 (43) Exide Technologies 1,000 621 379 (38) Fedders Corporation 221 0 221 (100) Global Power Equipment Group Inc. 112 150 (38) 34 International Aluminum Corp. 164 38 126 (77) Masonite Corporation, et al. 2,200 300 1,900 (86) Momentive Performance Materials Inc. 3,826 1,292 2,534 (66) Motor Coach Industries International 767 175 592 (77) National RV Holdings, Inc. 10 0 10 (100) Neenah Enterprises, Inc. 364 149 215 (59) Oneida Ltd. 226 129 97 (43) O’Sullivan Industries, Inc. 260 30 231 (89) Panolam Industries International, Inc. 344 171 173 (50) Propex Inc. 380 0 380 (100) Reddy Ice Holdings, Inc. 472 327 145 (31) Simmons Company 1,000 450 550 (55) Solyndra LLC 900 0 0 (100) The Newark Group, Inc. 387 138 249 (64) True Temper Sports, Inc. 275 40 235 (85) Wellman Inc. 600 135 465 (78) Wolverine Tube, Inc. 237 43 194 (82) Average — — — (62)

Source: Company disclosure statements, Fitch Ratings.

62% Average I&M Sector Debt Reduction in Bankruptcy

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 7 January 28, 2016

Four companies that liquidated or sold all assets as a going concern had 100% debt reduction: Fedders, National RV Holdings, Propex and Solyndra.

In two cases, Global Power Equipment Group, Inc. and American LaFrance LLC, the company emerged from Chapter 11 with higher debt balances than at the timing of filing. In Global Power’s case, a rights offering and large exit facility were completed with proceeds used to make distributions to prepetition creditors. In American LaFrance’s case, the company emerged with still high leverage and later ceased all operations and liquidated assets in an auction six years after emerging from bankruptcy.

Relatively Low Sector Default Rates Average annual high-yield bond default rates for I&M sector issuers ranged from 0.0% to 8.7% from 1980 to 2015, with a long-term annual average of 2.4% over that span. The sector performed better than the high-yield market as a whole in terms of defaults. The annual default rate range for the U.S. market over the same period was 0.20% to 16.4% and the 35-year long-term market average rate was 4.1% (index includes Yankee bonds and rate is par-weighted). The sector and market rate time series is shown in the chart below.

Over the past five years, I&M sector defaults have been sparse, with annual rates below 1% each year. This is a reflection of the diversity of businesses within the sector, an expanding economy and the robustness of capital markets that enabled issuers to push out maturities and raise additional liquidity. The sector has no overarching driver of performance as do more homogeneous commodity sectors, nor is it as volatile as tech-heavy sectors. Fitch classifies certain types of manufacturers in unique sectors, including auto, food, packaging, etc. (see Related Research for case studies), but has included a few of these cases in this edition as they are newer cases that were filed after publication of the sector case study for that particular type of manufacturer.

Sector bankruptcies were concentrated among relatively small, leveraged companies that were unable to cope with business or accounting issues or refinance their debts. More than 50% of the 27 I&M cases studied were filed in the recession years of 2008–2010 amid moribund credit markets and shrinking demand from industrial customers. The sector bankruptcy filings in this report were made from 2005 to 2015.

The median sector case duration from filing date to bankruptcy plan confirmation date was relatively short at five months, and about three-quarters of the cases were resolved within a year. Ten of the sector cases were either prepackaged or prenegotiated filings, for which terms of the restructuring plan were negotiated by the filing date. The short duration of many cases

02468

1012141618

(% of Par)Industrial/Manufacturing Total Market

Source: Fitch Ratings, Bloomberg.

U.S. High-Yield Bond Default Rates(Fitch High-Yield Default Index)

Relatively Low Defaults

• Average I&M Default Rate 2.4%

• Average Cross-Sector U.S. Corporate Default Rate 4.1%

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 8 January 28, 2016

reflects a lack of filings by heavily unionized or regulated companies and companies with complex capital structures and inter-company transactions.

Sector Default Drivers Causes of sector bankruptcy filings tended to be idiosyncratic, company-specific operating problems. While I&M default rates peaked during the recession, the sector rate lagged the cross-sector market rate. Fitch selects two key drivers from a list of seven for each of its case studies (in addition to providing a more detailed paragraph on the specific case drivers within each write-up). There were no cases where fraud, litigation or extreme events were chosen from the list of seven as key drivers in this sector, although they were contributing factors in some of the cases.

Cyclical Trough More than 50% of the sector defaults analyzed in this edition occurred during the deep recession years of 2008–2010; see distribution chart below.

Cases that were driven by a cyclical trough that reduced sales included Atrium Companies, a manufacturer of windows and doors that suffered from weak new construction and remodeling market demand during the recession. International Aluminum Corp., a producer of aluminum and vinyl building materials, filed for similar market downturn reasons in the same year (2010).

In another cyclical downturn related case, O’Sullivan Industries, Inc., a producer of ready to assemble furniture, was a victim of lower demand for its products, higher costs for particleboard and fiberboard raw materials, and foreign competition.

Flawed Business Model Fitch attributed nine of the I&M filings to “flawed business models” as a key driver: American LaFrance; Chassix; Colt Defense LLC; EaglePicher Holdings Inc.; Exide Technologies; Fedders; Global Power Equipment Group; O’Sullivan; and Solyndra.

There were wide-ranging business model issues affecting these nine defaulters, ranging from supply chain issues to accounting and systems problems to start ups that never reached positive cash flow.

For example, American LaFrance, a venerable manufacturer of fire trucks and emergency vehicles, was spun off from another owner in 2005 and began to experience serious tracking

I&M Bankruptcy Characteristics Low Sector Default Rates Short Duration of Bankruptcies Wide Range of Causal Factors Relatively Small Companies Few Liquidation Outcomes

Key I&M Default Drivers Deep Cyclical Trough Flawed Business Model Legacy Liabilities Untenable Capital Structure

02468

101214161820

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

(% of Cases)Industrial Manufacturing Sample

Source: Company disclosure statements, Fitch Ratings.

Bankruptcy Filing Year

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 9 January 28, 2016

issues for sales, inventory and accounting when it was monitoring on a stand-alone basis. This caused production and delivery delays.

In a second example, component maker Eagle Picher Industries experienced higher costs due to disruptions in steel supply, higher mining and energy costs, lower selling prices, and plant restructuring and start-up costs in China.

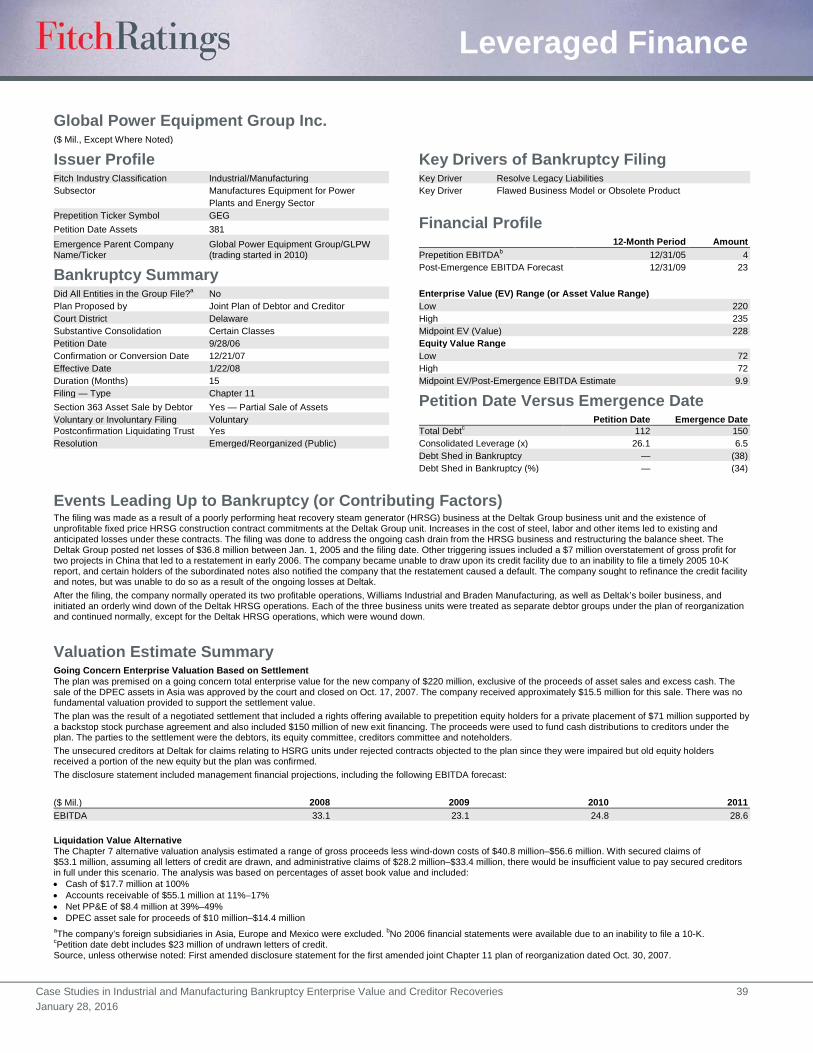

Legacy Liabilities The need to resolve legacy liabilities was a key factor in the Exide Technologies and Global Power Equipment Group filings.

In Exide’s case, a major lead recycling facility in California that provided raw materials for battery production was shut down by regulators for violating environmental standards and the company faced large tort claim liabilities relating to this facility.

In Global Power’s case, the company had an unprofitable fixed-price contract for construction of a heat recovery steam generator. This burdensome contract was rejected in bankruptcy.

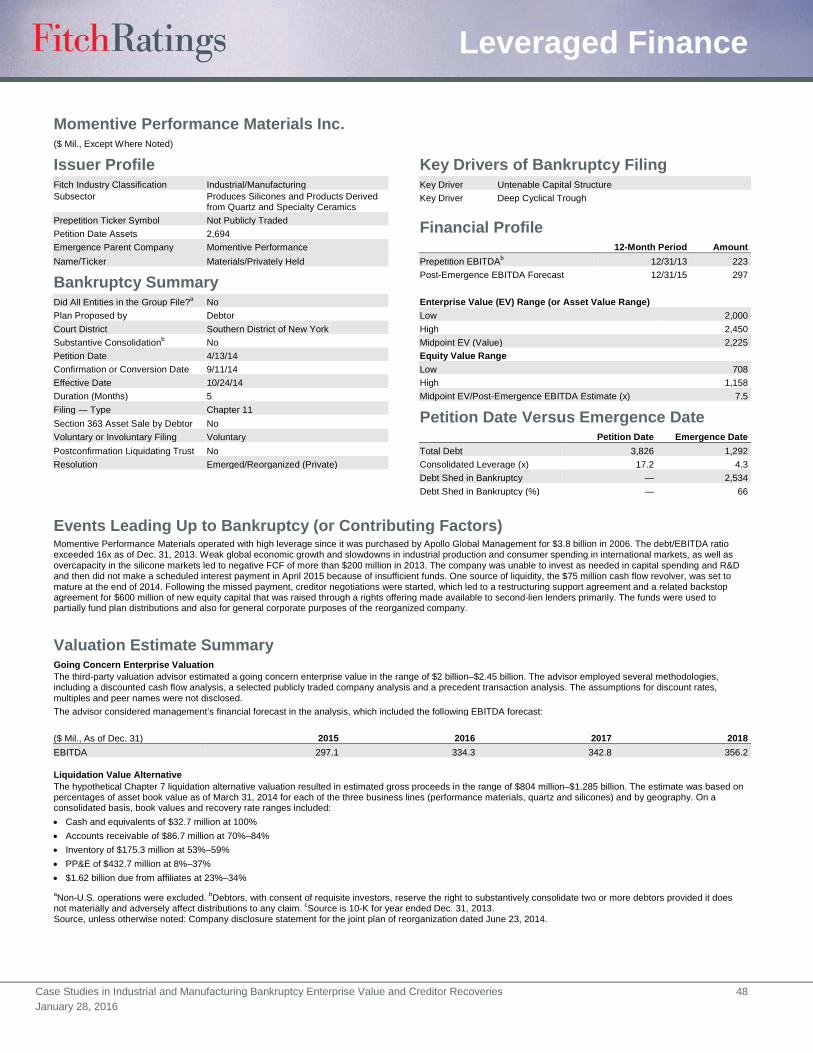

Untenable Capital Structure This was the most common key driver selected by Fitch from the list of seven. An unsustainable capital structure was a key factor for 20 of the cases. In some, leverage became high well prior to the filing date as a result of a going private or other leveraging transaction done based on rosy projections that did not pan out. In other cases, the company faced looming maturities or had covenant violations that could not be resolved outside of restructuring and faced a more sudden liquidity crisis.

The median petition date leverage for 19 I&M cases for which this ratio could be estimated was 12.2x. The median emergence date leverage was a much more manageable 3.8x.

I&M Sector vs. Cross-Sector Case Studies Key attributes of the I&M case sample compared to the cross-sector database are summarized in the table above.

Comparison of I&M and Overall U.S. Corporate Bankruptcies

Industrial and Manufacturing Sector

Cross-Sector U.S. Corporate Cases

Number of Bankruptcy Cases Analyzed 27 204 Median Petition Date Assets ($ Mil.) 347 649 Median Petition Date Debt ($ Mil.) 380 585 Case Length (Months to Confirmation) 5 9 Percentage of Filings with Prepackaged or Prenegotiated Plans (%) 37 36 Percentage of Cases with Liquidation Outcomes (%) 11 13 Median Reorganization Multiple (x) 6.3 6.0 Median Debt Reduction in Bankruptcy (%) 60 72 Prepetition Leverage Ratio (Debt/EBITDA)a (x) 12.2 9.4 Emergence Date Leverage Ratio (x) 3.8 3.6 aMedian prepetition leverage ratio includes 19 industrial sector companies. The median excludes six industrial sample companies with negative prepetition EBITDA and two companies with no EBITDA disclosure. Note: Median emergence date leverage ratio for the cross-sector group includes 152 companies. The ratio was negative or not available for the remaining 52 companies in Fitch’s case database. Source: Company reports, Fitch Ratings.

Median Petition Date Leverage 12.2x

Median Emergence Date Leverage 3.8x

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 10 January 28, 2016

Appendix A

Recovery Rates by Claim Seniority (% of Par Value)

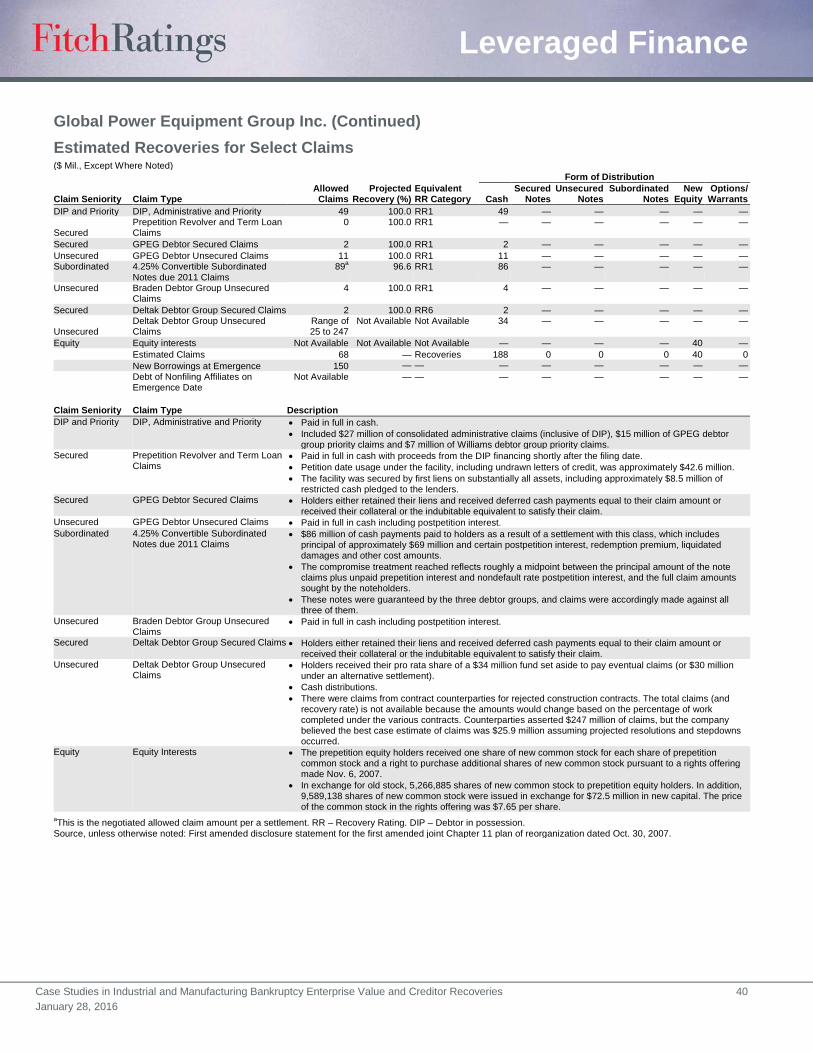

Company First Lien Second Lien Unsecured Subordinateda Aleris International, Inc. 100/18/26 — 1 — American LaFrance, LLC 100 — — — AMTROL Holdings, Inc. 100 100 72 — Atrium Companies, Inc. 98 — 4 2 Chassix Inc. 100/67 — 7 — Colt Defense LLC 100/100 — 10 — EaglePicher Holdings Inc. 100 — 71 — Exide Technologies 100/5 — — 0 Fedders Corporation 100/53 — 2 — Global Power Equipment Group Inc. 100 — — 97 International Aluminum Corp. 100 — — 0 Masonite Corporation 38 — — 5 Momentive Performance Materials Inc. 100 100/20b — 0 Motor Coach Industries International 100 100/17c — 0/0 National RV Holdings, Inc. 100 — — — Neenah Enterprises, Inc. 100/57 — — 4 Oneida Ltd. 100/51 — — — O’Sullivan Industries, Inc. 100/83 — 0 0 Panolam Industries International, Inc. 100/100/100 — — 49 Propex Inc. 21 — 2 — Reddy Ice Holdings, Inc. 100/100 28 50 3 Simmons Company 100 — 83 3 Solyndra LLC 100 14 0 — The Newark Group, Inc. 100/100 — 75 33 True Temper Sports, Inc. 100 22 0 — Wellman Inc. 100/35 0 — — Wolverine Tube, Inc. 66 — — — Median Recovery Rate 100 21 6 3 Average Recovery Rate 82 Not Applicable 27 14 aSubordinated includes structural holdco unsecured issues and contractually subordinated issues. bIncludes 1.5 lien issue at 100% and second-lien issue with midpoint recovery rate of 20%. cIncludes second-lien issue at 100% and third-lien issue with midpoint recovery rate of 17%. Note: Recovery rates on multiple issues at the same level of capital structure are separated by “/”. If recovery rates were in a range as estimated in the disclosure statement, Fitch takes midpoint value for this table. Source: Company disclosure statements, Fitch Ratings.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 11 January 28, 2016

Appendix B

Comparing Prepetition and Post-Emergence EBITDA ($ Mil.)

Company Prepetition EBITDA Post-Emergence EBITDA Forecast American LaFrance, LLC (51) 28 AMTROL Holdings, Inc. 26 27 Atrium Companies, Inc. 54 67 Chassix Inc. 22 128 Colt Defense LLC 12 22 EaglePicher Holdings Inc. 70 65 Exide Technologies 104 102 Fedders Corporation (14) Not Applicable Global Power Equipment Group Inc. 4 23 International Aluminum Corp. 31 2 Momentive Performance Materials Inc. 223 297 Motor Coach Industries International 20 58 National RV Holdings, Inc. (10) Not Applicable Neenah Enterprises, Inc. (8) 52 Oneida Ltd. (20) 38 O’Sullivan Industries, Inc. 2 14 Panolam Industries International, Inc. 39 24 Propex Inc. 50 Not Applicable Simmons Company 84 121 Solyndra LLC Not Available Not Applicable True Temper Sports, Inc. 29 19 Wellman 29 41 Wolverine Tube, Inc. 7 11 Aleris International, Inc. (22) 190 Masonite Corporation 162 61 The Newark Group, Inc. Not Available 60 Reddy Ice Holdings, Inc. 44 66 Source: Company disclosure statements, Fitch Ratings.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 12 January 28, 2016

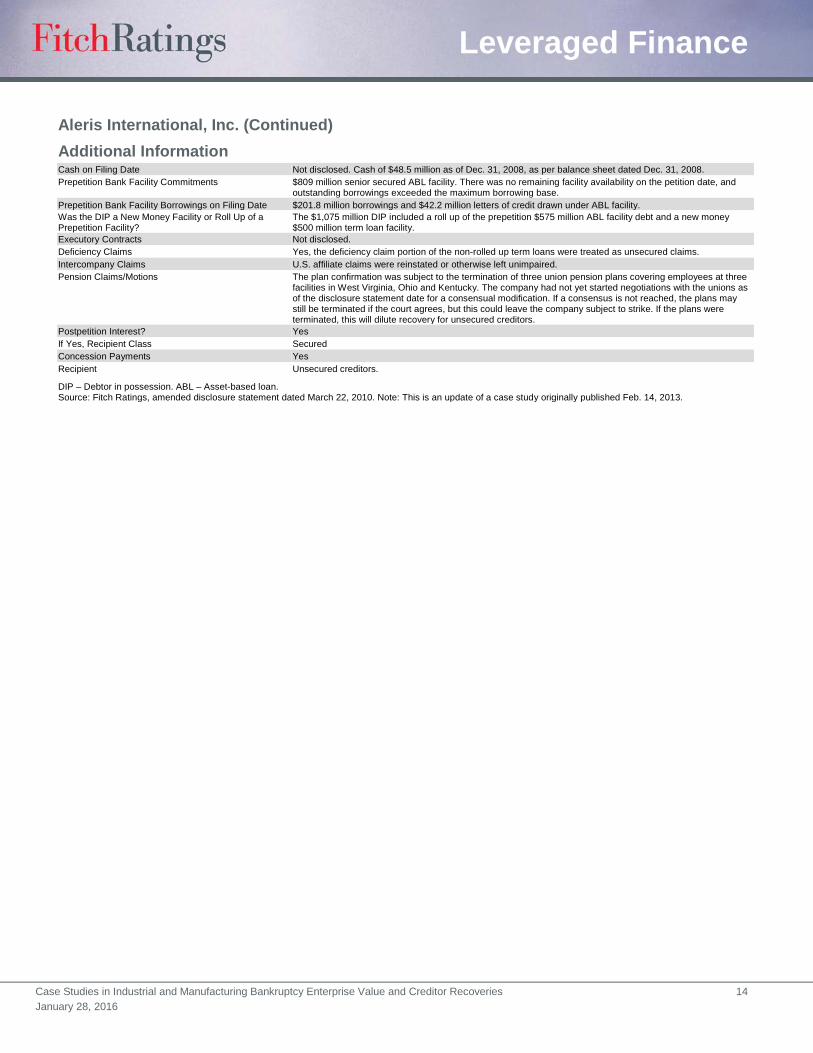

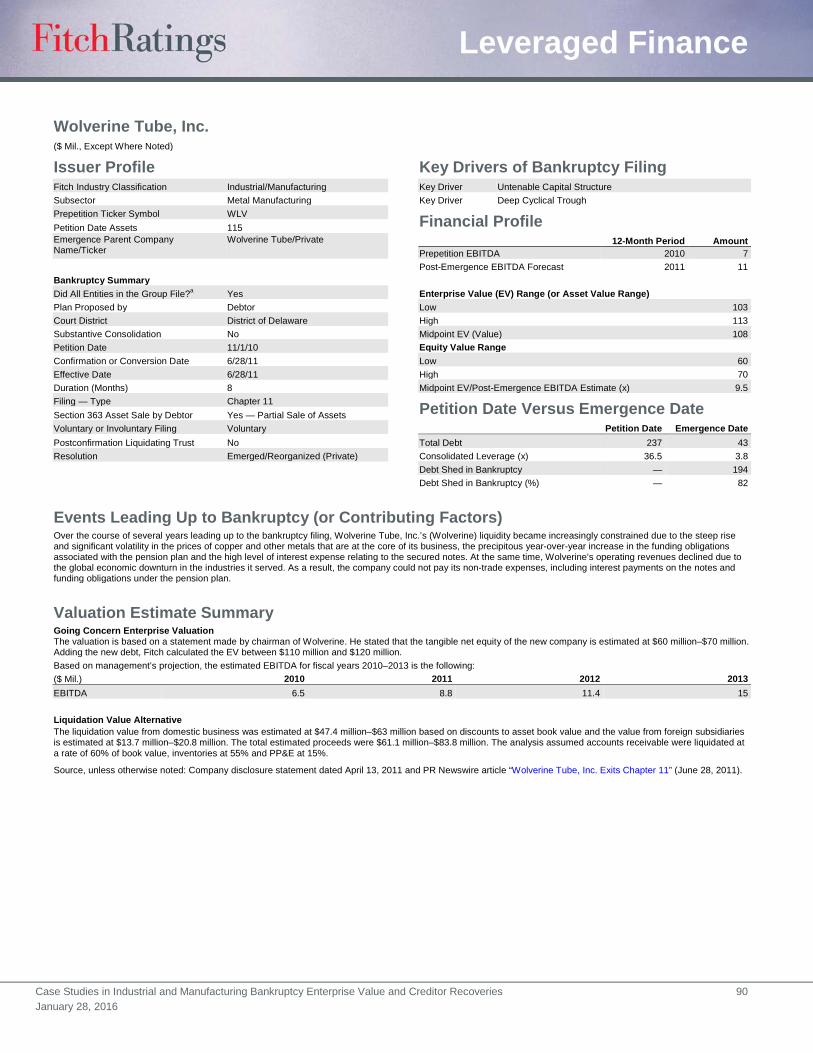

Aleris International, Inc. ($ Mil., Except Where Noted)

Issuer Profile Fitch Industry Classification Metals and Mining Subsector Aluminum Product Producer Prepetition Ticker Symbol Not Publicly Traded Petition Date Assets 5,121 Emergence Parent Company Name/Ticker Aleris International/Privately Held

Bankruptcy Summary Did All Entities in the Group File?a No Plan Proposed by Debtor Court District` Delaware Substantive Consolidation Yes Petition Date 2/12/09 Confirmation or Conversion Date 5/13/10 Effective Date 6/1/10 Duration (Months) 15 Filing — Type Chapter 11 Section 363 Asset Sale by Debtor No Voluntary or Involuntary Filing Voluntary Postconfirmation Liquidating Trust Not Available Resolution Emerged/Reorganized (Private)

Events Leading Up to Bankruptcy (or Contributing Factors) Aleris International, Inc. (Aleris) expanded through mergers and acquisitions in the years prior to the bankruptcy. In December 2006, the company was purchased by Texas Pacific Group in a going private transaction. In conjunction with the buyout, the company increased its bank facility commitments and issued $1 billion of new notes, which resulted in high leverage. The global economic downturn adversely affected the aluminum industry. Aleris’ customers in the building and construction and automotive industries reduced their aluminum purchases during the recession. The profitability of the company’s rolled and extruded products businesses suffered as a result of lower volumes, and margins were reduced because of decreasing per-pound selling prices. These factors led to a liquidity crunch as well as margin calls on transactional hedges and a high interest expense burden. The borrowing base on the asset-based loan facility declined by more than 50% in the six months prior to the petition date, and lenders demanded repayment of overage borrowings in excess of the remaining borrowing base. The bankruptcy plan was based on a debt to equity conversion with secured creditors becoming the majority owners of the new stock and included a new money investment by certain secured creditors in a $645 million rights offering and $45 million of new notes.

Valuation Estimate Summary Going Concern Valuation The third-party valuation advisor relied primarily on the discounted cash flow and comparable company approaches to estimate the midpoint going concern enterprise value of $1 billion, with $660 million–$830 million of the value attributed to U.S. operations and the remainder to the Aleris Deutschland Holding (ADH) European business. The estimated $1 billion enterprise value consists of the “plan value” or equity value before the proceeds from the rights offering plus the maximum $690 million cash proceeds of the rights offering of new common stock shares. Participation in the rights offering was available to holders of U.S. roll up term loan claims, European term loan claims and European roll up term loan claims that were accredited investors. Liquidation Alternative Valuation The valuation was based on discounts to asset book values as of Sept. 30, 2009 and resulted in gross liquidation proceeds of $464 million from U.S. operations and $1 million from European operations. The percentage of book value applied to various assets included: • Accounts receivable of $119.7 million at 70% of book value. • Inventory of $111 million at 79%. • Property plant and equipment of $146 million at 49%. • U.S. liquidation expenses were estimated at $50 million. • The intercompany receivable of $900 million on ADH’s balance sheet was assumed to have $0 value in the liquidation.

Source, unless otherwise noted: Company disclosure statement for the first amended joint plan of reorganization dated March 22, 2010. Note: This is an update of a case study originally published Feb. 14, 2013.

Key Drivers of Bankruptcy Filing Key Driver Deep Cyclical Trough Key Driver Untenable Capital Structure

Financial Profile 12-Month Period Amount Prepetition EBITDA 12/31/08 (22) Post-Emergence EBITDA Forecast 12/31/11 190 Enterprise Value (EV) Range (or Asset Value) Low 925 High 1,195 Midpoint EV 1,060 Equity Value Range (Including Cash on Hand) Low 222 High 271 Midpoint EV/Post-Emergence EBITDA Estimate (x) 5.6

Petition Date Versus Emergence Date Petition Date Emergence Date Total Debtb 2,600 59 Consolidated Leverage (x) (116.6) 0.3 Debt Shed in Bankruptcy 2,541 Debt Shed in Bankruptcy (%) 98

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 13 January 28, 2016

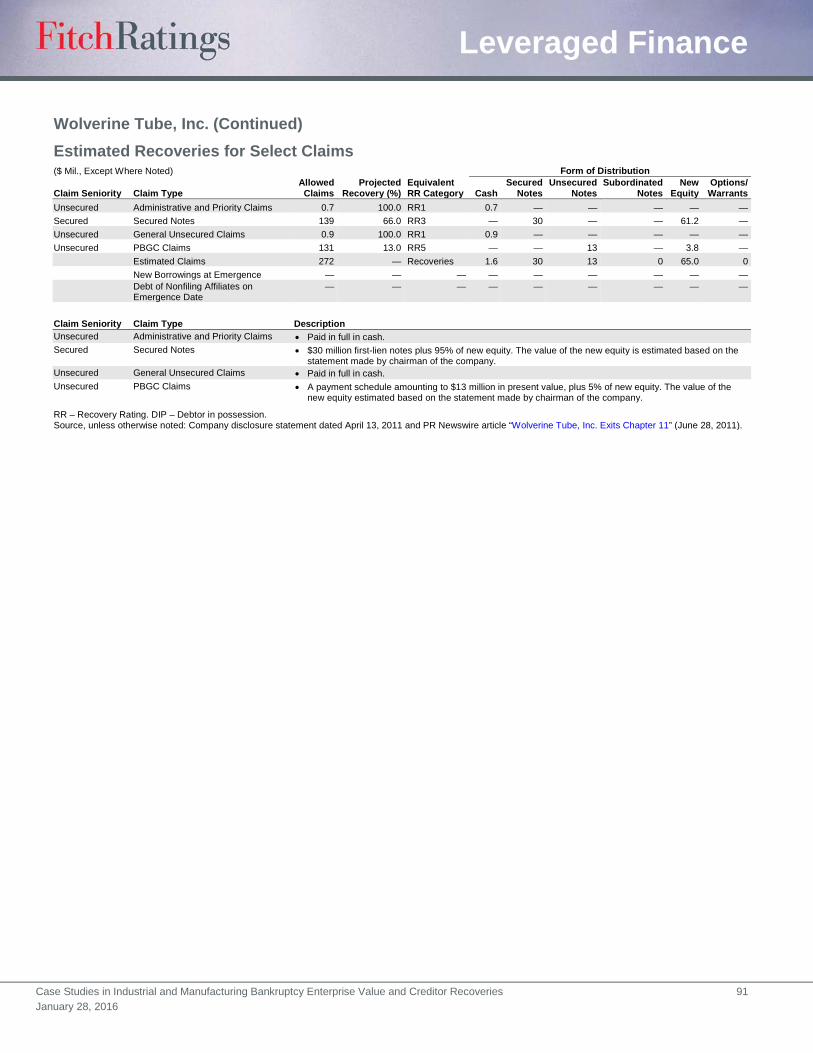

Aleris International, Inc. (Continued) Estimated Recoveries for Select Claims ($ Mil., Except Where Noted) Form of Distribution Claim Seniority Claim Type

Allowed Claims

Projected Recovery (%)

Equivalent RR Category Cash

Secured Notes

Unsecured Notes

Subordinated Notes

New Equity

Options/ Warrants

DIP $1,075 Million DIP Facility 650 100 RR1 650 — — — — — Secured U.S. Roll Up Term Loan Claims 527 28 RR5 — — — — 148 — Secured ADH European Roll Up Term Loan N.A. 94–100 RR1 25 — — — — — Secured ADH European Term Loan 340 21.0 RR5 — — — — 71 — Secured U.S. Term Loan Claims 306 1.0 RR6 86 — — — — — Unsecured Various Bond Issues 1,196 1.0 RR6 17 — — — — — Equity Holders of Aleris Equity Interests 0 0.0 RR6 — — — — — — Estimated Claims 3,020 — Recoveries 777 0 0 0 219 0 New Borrowings at Emergencea 59 — — — — — — — —

Debt of Nonfiling Affiliates on Emergence Date 0 — — — — — — — —

Claim Seniority Claim Type Description DIP $1,075 Million DIP Facility (Consisting of

$575 ABL Roll Up DIP and $500 New Money Term Loan DIP)

• $575 million ABL roll up revolver and $500 million new money term loan (claim amount is a rough Fitch estimate based on borrowings as of November 2009).

• The prepetition ABL debt was refinanced with the DIP. • Guaranteed by each U.S. debtor and other domestic subsidiary and certain European affiliates. • ABL DIP revolver collateral: first lien on accounts receivable, inventory and intangible assets and a second

lien on other collateral. • Term loan DIP collateral: first lien on property and equipment and second lien on the ABL collateral. • Repaid in cash using proceeds from the rights offering of up to $690 million of new common stock, which

was also used for other cash distributions under the plan and for liquidity post emergence. Secured U.S. Roll Up Term Loan Claims

(USD436 Million and USD Equivalent of EUR70.9 Million at $1.29 per Euro)

• Pursuant to the DIP order, prepetition term loan lenders were permitted to roll up a portion of the amount owed by the U.S. debtors into the DIP.

• Fitch estimates a blended recovery rate on the rolled up/non rolled up loan of approximately 18%. Received pro rata share of U.S. roll up stock and U.S. subscription rights or cash.

Secured ADH European Roll Up Term Loan • Received ADH roll up stock and the ADH roll up subscription rights or cash equal to $25 million. Secured ADH European Term Loan (USD286 Million

and USD Equivalent of EUR53.2 Million) • Secured by a separate collateral package than the U.S. term loan that included bank accounts, intellectual

property rights, certain stock in certain subsidiaries, and/or moveable property. • Received distributions in the form of ADH term loan stock or cash.

Secured U.S. Term Loan Clams (USD220.1 Million and USD Equivalent of EUR67 Million)

• The non-rolled up portions of the term loans were treated as unsecured claims in the plan.

Unsecured Various Bond Issues • Includes $598 million of 2006 notes plus prepetition interest, $105.4 million of 2007 notes and $399 million of unsecured notes.

Equity Holders of Aleris Equity Interests • Received $0 distributions. • Deemed to have rejected the plan of reorganization.

aNew borrowing estimate includes $45 million of subordinated notes and $14 million under new $500 million ABL facility. RR – Recovery Rating. DIP – Debtor in possession. ABL – Asset-based loan. N.A. – Not available. Source, unless otherwise noted: Company disclosure statement for the first amended joint plan of reorganization dated March 22, 2010. Note: This is an update of a case study originally published Feb. 14, 2013.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 14 January 28, 2016

Aleris International, Inc. (Continued) Additional Information Cash on Filing Date Not disclosed. Cash of $48.5 million as of Dec. 31, 2008, as per balance sheet dated Dec. 31, 2008. Prepetition Bank Facility Commitments $809 million senior secured ABL facility. There was no remaining facility availability on the petition date, and

outstanding borrowings exceeded the maximum borrowing base. Prepetition Bank Facility Borrowings on Filing Date $201.8 million borrowings and $42.2 million letters of credit drawn under ABL facility. Was the DIP a New Money Facility or Roll Up of a Prepetition Facility?

The $1,075 million DIP included a roll up of the prepetition $575 million ABL facility debt and a new money $500 million term loan facility.

Executory Contracts Not disclosed. Deficiency Claims Yes, the deficiency claim portion of the non-rolled up term loans were treated as unsecured claims. Intercompany Claims U.S. affiliate claims were reinstated or otherwise left unimpaired. Pension Claims/Motions The plan confirmation was subject to the termination of three union pension plans covering employees at three

facilities in West Virginia, Ohio and Kentucky. The company had not yet started negotiations with the unions as of the disclosure statement date for a consensual modification. If a consensus is not reached, the plans may still be terminated if the court agrees, but this could leave the company subject to strike. If the plans were terminated, this will dilute recovery for unsecured creditors.

Postpetition Interest? Yes If Yes, Recipient Class Secured Concession Payments Yes Recipient Unsecured creditors.

DIP – Debtor in possession. ABL – Asset-based loan. Source: Fitch Ratings, amended disclosure statement dated March 22, 2010. Note: This is an update of a case study originally published Feb. 14, 2013.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 15 January 28, 2016

American LaFrance, LLC ($ Mil., Except Where Noted)

Issuer Profile

Key Drivers of Bankruptcy Filing

Fitch Industry Classification Industrial/Manufacturing Key Driver Flawed Business Model or Obsolete Product Subsector Manufactures Ambulances and Other

Specialized Rescue Vehicles Key Driver Deep Cyclical Trough

Financial Profile Prepetition Ticker Symbol Not Publicly Traded Petition Date Assets 189 Emergence Parent Company Name/

Ticker American LaFrance/ Privately Held

12-Month Period Amount

Prepetition EBITDA 12/31/07 (51)

Bankruptcy Summary Post-Emergence EBITDA Forecast 12/31/09 28

Did All Entities in the Group File? Yes

Enterprise Value (EV) Range (or Asset Value Range) Plan Proposed by Debtor

Low 150

Court District Delaware

High 150 Substantive Consolidation Yes

Midpoint EV (Value) 150

Petition Date 1/28/08

Equity Value Range Confirmation or Conversion Date 5/23/08

Low (41)

Effective Date 7/24/08

High (41) Duration (Months) 4

Midpoint EV/Post-Emergence EBITDA Estimate (x) 5.4

Filing — Type Chapter 11 Section 363 Asset Sale by Debtor Yes — Sale of Substantially All Assets

(as Going Concern)

Petition Date Versus Emergence Date

Voluntary or Involuntary Filing Voluntary

Petition Date Emergence Date Postconfirmation Liquidating Trust Yes

Total Debt 154 186

Resolution Section 363 Sale and Liquidating Plan

Consolidated Leverage (x) (3.0) 6.7

Debt Shed in Bankruptcy — (32)

Debt Shed in Bankruptcy (%) — (21)

Events Leading Up to Bankruptcy (or Contributing Factors) American LaFrance, LLC’s (ALF) Chapter 11 filing was driven by several factors, including significant operational difficulties encountered when the business was separated from its former parent, Freightliner LLC, reduced demand for new firetrucks during the recession due to municipal budget cuts and other problems. When ALF initially separated into a standalone business in December 2005, many of its reporting systems and management roles were outsourced to Freightliner LLC per a transition services agreement. The services agreement terminated in 2007 and when ALF assumed responsibility, the company immediately experienced serious tracking issues for inventory, sales, vehicle orders, accounts receivable, and general ledger balances. The inventory tracking problems caused delays in timely vehicle deliveries to customers. This adversely affected cash flows and triggered a liquidity crisis. Moves to new production facilities and a new headquarters building caused additional business disruptions. The company was not generating sufficient cash flows to cover operating expenses and debt service and the company posted losses in 2006 and 2007. All of these problems were compounded by a depressed market for new emergency vehicles during the economic recession.

Valuation Estimate Summary Value Determined by Sale of All Assets in a Credit Bid The agent for the prepetition credit facility, Patriarch Partners Agency Services LLC (Patriarch), made a $150 million credit bid for ALF’s assets. There were no higher bids, and the company’s assets were transferred in the credit bid. Patriarch was also the owner of the company since 2005 as well as the DIP and secured prepetition lender. Patriarch invested $500,000 in new equity to fund a portion of the reorganization plan. Separately, the company emerged as a still-highly leveraged entity, and operating problems continued. ALF permanently ceased all operations and auctioned remaining inventory and other assets in 2014. Liquidation Value Alternative The liquidation alternative analysis was based on percentages applied to the unaudited asset book values on the balance sheet for Dec. 31, 2007 and resulted in estimated gross proceeds of $75.1 million under a forced auction in the current economy. The asset book values and percentages included: • Cash and equivalents of $28.7 million at 100% • Accounts receivables of $19.8 million at 75% • Raw materials of $40.4 million at 25% • Work in progress of $45.9 million at 18.5% • Net PP&E of $30.9 million at 37%. Under this alternative, the secured lenders would have recovered approximately 9%.

Source, unless otherwise noted: Fourth amended disclosure statement in support of the third amended plan of reorganization dated March 27, 2008.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 16 January 28, 2016

American LaFrance, LLC (Continued) Estimated Recoveries for Select Claims ($ Mil., Except Where Noted)

Form of Distribution

Claim Seniority Claim Type Allowed Claims

Projected Recovery (%)

Equivalent RR Category Cash

Secured Notes

Unsecured Notes

Subordinated Notes

New Equity

Options/ Warrants

DIP and Priority DIP Facility Loans 50 100.0 RR1 — 50 — — — — Secured $150 Million First-Lien Facility 138 100.0 RR1 — 134 — — 4 — Secured Performance Bonds and Letters of Credit 29 100.0 RR1 — 29 — — — — Unsecured Vendor, Warranty and Other 63 22.5 RR5 14 — — — — —

Estimated Claims 280 — Recoveries 14 213 0 0 4 0

New Borrowings at Emergence 186 — — — — — — — —

Debt of Nonfiling Affiliates on Emergence Date

0 — — — — — — — —

Claim Seniority Claim Type Description DIP and Priority DIP Facility Loans • The DIP was provided by the prepetition lender and owner of the company.

• Loans were paid in full using a portion of the proceeds from the $186 million exit facility. Secured $150 Million First-Lien Facility • Distributions consisted of $134 million of proceeds from the $186 million exit facility financing and $4 million

of new common equity. Secured Performance Bonds and Letters of

Credit • Fitch assumes that ALF performed as planned under various municipal and government contracts, and

these performance bonds rolled off when projects were completed. Unsecured Vendor, Warranty and Other • Warranty claims estimated at $7.1 million.

• Holders received recoveries in cash, with approximately $6 million paid on the effective date and the remaining recoveries paid from time to time post-emergence using proceeds from the trust that was created to administer assets left behind following the sale of the company. These include avoidance action and litigation trust proceeds.

RR – Recovery Rating. DIP – Debtor in possession. Source, unless otherwise noted: Fourth amended disclosure statement in support of the third amended plan of reorganization dated March 27, 2008.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 17 January 28, 2016

American LaFrance, LLC (Continued) Additional Information Cash on Filing Date $6.47 million of unrestricted cash and $24.7 million of restricted cash to secured obligations under certain

performance and bid bonds required in connection with ALF’s public projects. Prepetition Bank Facility Commitments $150 million credit facility. Prepetition Bank Facility Borrowings on Filing Date $150 million. Was the DIP a New Money Facility or Roll Up of a Prepetition Facility?

The $50 million DIP was a new money facility that was provided by the prepetition lender and owner, Patriarch.

Other Notable Issues None Executory Contracts Of the 316 fire trucks in the construction contract backlog on the petition date, ALF determined it may reject

over 30 unprofitable truck contracts. Deficiency Claims No Contingent Claims and/or Contingent Recoveries Litigation and avoidance action proceeds were to be distributed to unsecured creditors to the extent received.

Performance bonds secured by letters of credit would become claims if ALF did not perform obligations to the applicable customers.

Intercompany Claims — Pension Claims/Motions Not available. Postpetition Interest? Not available. If Yes, Recipient Class Not available. Concession Payments Yes Recipient and Comments Unsecured lenders.

DIP – Debtor in possession. Source: Fitch Ratings, company disclosure statement dated March 27, 2008.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 18 January 28, 2016

AMTROL Holdings, Inc. ($ Mil., Except Where Noted)

Issuer Profile

Key Drivers of Bankruptcy Filing

Fitch Industry Classification Industrial/Manufacturing Key Driver Untenable Capital Structure Subsector Manufactures Storage and Pressure

Control Products for Water and HVAC Systems

Key Driver Deep Cyclical Trough

Financial Profile Prepetition Ticker Symbol Not Publicly Traded Petition Date Assets 222

12-Month Period Amount Emergence Parent Company Name/ Ticker

AMTROL/ Privately Held

Prepetition EBITDA 12/31/05 26 Post-Emergence EBITDA Forecast 12/31/07 27

Bankruptcy Summary

Enterprise Value (EV) Range (or Asset Value Range)

Did All Entities in the Group File?a No Low 165 Plan Proposed byb Joint Plan of Debtor and Creditor

High 185

Court District Delaware

Midpoint EV (Value) 175 Substantive Consolidation Yes

Petition Date 12/18/06

Equity Value Range Confirmation or Conversion Date 5/24/07

Low 64

Effective Date 6/6/07

High 85 Duration (Months) 5

Midpoint EV/Post-Emergence EBITDA Estimate (x) 6.5

Filing — Type Chapter 11 Petition Date Versus Emergence Date Section 363 Asset Sale by Debtor No Voluntary or Involuntary Filing Voluntary

Petition Date Emergence Date Postconfirmation Liquidating Trust No

Total Debt 188 110

Resolution Emerged/Reorganized (Private)

Consolidated Leverage (x) 7.1 4.1

Debt Shed in Bankruptcy — 78

Debt Shed in Bankruptcy (%) — 41

Events Leading Up to Bankruptcy (or Contributing Factors) The company had a substantial working capital deficit in the year prior to the filing because all $187.5 million of the company’s secured and unsecured debt was scheduled to mature in December 2006. In addition, the company experienced higher raw materials costs for resins and other inputs to its products in 2005, and it was uncertain how much of the increase could be passed through to customers due to a competitive market. The company attempted to extend maturities and recapitalize prior to the looming maturity dates, and also had been trying to raise cash through sales of some or all assets. An out-of-court restructuring of the unsecured debt was proposed, which would have converted the 10.625% notes to a majority of the company’s equity, but after extensive due diligence in the second and third quarters of 2006, the noteholders informed the company that it did not want to complete the debt-for-equity swap transaction. Another attempt to sell the company resulted in no bid. The original majority holder of the 10.625% notes sold its holdings and the new holders of the majority of the notes reached an agreement with the company to support a conversion of the notes to equity under Chapter 11.

Valuation Estimate Summary Going Concern Enterprise Valuation The third-party valuation advisor estimated an enterprise value range of $165 million–$185 million. The advisor utilized a discounted cash flow analysis, a comparable company market value analysis and a comparable company acquisition multiple analysis to value the company. There was no disclosure of the assumptions used under these three methods. The advisor relied on management forecasts, which included EBITDA as follows: ($ Mil.) 2008 2009 2010 EBITDA 27.0 28.8 31.2 Liquidation Value Alternative The Chapter 7 alternative analysis estimated gross liquidation proceeds of $81 million, wind-down expenses of $3 million and Chapter 7 administrative and priority claims of $11 million. The $67 million of proceeds would have provided 68% recovery to the DIP holders and no recovery to the unsecured notes claims. The analysis was based on percentage of asset book value as of April 30, 2007 including: • Accounts receivable of $16 million at 85% of book value • Inventories of $18.6 million at 44.5% • Assumed sales proceeds from non-debtor European operations of $44.1 million • Intellectual property of $95.3 million at 5.2% aExcluded foreign subsidiaries that collectively accounted for 28.7% of fiscal year 2005 net sales (excluding Canada). bPlan jointly proposed by the debtors and the official committee of unsecured creditors. DIP – Debtor in possession. Source, unless otherwise noted: Disclosure statement dated March 3, 2007.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 19 January 28, 2016

AMTROL Holdings, Inc. (Continued) Estimated Recoveries for Select Claims ($ Mil., Except Where Noted)

Form of Distribution

Claim Seniority Claim Type

Allowed Claims

Projected Recovery (%)

Equivalent RR Category Cash

Secured Notes

Unsecured Notes

Subordinated Notes

New Equity

Options/ Warrants

DIP and Priority Administrative, DIP and Priority Tax 100 100.0 RR1 100 — — — — — Secured $30 Million of Borrowings Under the

First-Lien ABL Revolver and Term Loan Facilities due 2006

0 100.0 RR1 — — — — — —

Secured $59.8 Million Second-Lien Term Loan Facility (Pay in Kind) due 2006

0 100.0 RR1 — — — — — —

Secured Other Secured Claims Not Available 100.0 RR1 — — — — — — Unsecured 10.625% Senior Notes due 2006 103 62–82 RR3 — — — — 74 — Intercompany Intercompany Not Available 0.0 RR6 — — — — — — Equity Old Common Equity Not Available 0.0 RR6 — — — — — —

Estimated Claims 203 — Recoveries 100 0 0 0 74 0

New Borrowings at Emergencea 110 — — — — — — — —

Debt of Nonfiling Affiliates on Emergence Date

0 — — — — — — — —

Claim Seniority Claim Type Description DIP and Priority Administrative, DIP and Priority Tax • Paid in full in cash with proceeds of the exit facility.

• The DIP was used to refinance the $90 million of prepetition first-lien and second-lien borrowings. • Fitch estimates $10 million of administrative claims and priority tax claims based on the enterprise value and

the distributions to other claimholders. The actual amount of these claims was not provided. Secured $30 million of Borrowings Under the

First-Lien ABL Revolver and Term Loan Facilities due 2006

• $30 million of petition date borrowings were repaid in full with the DIP facility. • Borrowings included $2.1 million Term Loan A, $18.8 million Term Loan B and $8.9 million ABL revolver

borrowings. Secured $59.8 Million Second-Lien Term Loan

Facility (Pay in Kind) due 2006 • Petition date borrowings, including pay in kind interest and principal, were refinanced with the DIP facility. • Borrowings consisted of original term loan of $35 million plus $24.8 million of accrued 12% PIK interest.

Secured Other Secured Claims • Unimpaired. • Paid in cash, reinstated, paid on such other terms as the parties agree, or satisfied through the surrender of

collateral. Unsecured 10.625% Senior Notes due 2006 • Holders received distributions in the form of 100% of the new common equity, subject to dilution for the

management incentive plan. • Holders that voted to reject the plan or do not expressly elect to receive the new equity shares received 60%

distributions in cash. • Claim consists of $97.8 million of principal and $4.8 million of accrued and unpaid interest.

Intercompany Intercompany • Holders were not entitled to receive any distributions or retain any property on account of their claims. • Debtors had right to retain, transfer of setoff intercompany claims as appropriate for accounting, tax and

commercial reasons. Equity Old Common Equity • $0 recoveries.

• Deemed to have rejected the plan. aExit financing consisted of a $110 million term loan and a $25 million undrawn exit revolver. RR – Recovery Rating. DIP – Debtor in possession. Source, unless otherwise noted: Disclosure statement dated March 3, 2007.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 20 January 28, 2016

AMTROL Holdings, Inc. (Continued) Additional Information

Cash on Filing Date Not available. Prepetition Bank Facility Commitments ABL revolver providing the lesser of a) $30 million less the aggregate amount of outstanding Term Loan A less

letter of credit usage and b) the borrowing base formula amount less the letter of credit usage. Prepetition Bank Facility Borrowings on Filing Date $8.9 million of ABL revolver borrowings, plus $2.1 million Term Loan A, $18.8 million Term Loan B and

$59.8 million second-lien Term Loan C. Was the DIP a New Money Facility or Roll Up of a Prepetition Facility?

The $115 million DIP was partially a $25 million new money revolver and partially a $90 million roll up of the first-lien and second-lien prepetition revolver and term loan borrowings.

Other Notable Issues Asbestos-related claims and related insurance assets passed through the bankruptcy unaffected and were unimpaired.

Executory Contracts There were no details beyond the disclosure that supplemental retirement plan contracts were assumed. Deficiency Claims None. Secured lenders were paid in full. Contingent Claims and/or Contingent Recoveries No Intercompany Claims No distributions under the plan. The claims were cancelled or reinstated at company’s election. Pension Claims/Motions Supplemental employee retirement plans were treated as assumed executory contracts. Benefit, healthcare

and disability. Postpetition Interest? Yes If Yes, Recipient Class Secured Concession Payments Yes Recipient and Comments Non-debt unsecured claims were paid in full in cash or reinstated. No disclosure of the amount of this class of

claims.

DIP – Debtor in possession. Source: Fitch Ratings, company disclosure statement dated March 3, 2007.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 21 January 28, 2016

Atrium Companies, Inc. ($ Mil., Except Where Noted)

Issuer Profile Key Drivers of Bankruptcy Filing Fitch Industry Classification Industrial/Manufacturing Key Driver Untenable Capital Structure Subsector Manufactures Windows and Door Products

Key Driver Deep Cyclical Trough

Prepetition Ticker Symbol Not Publicly Rated Financial Profile Petition Date Assets 347 Emergence Parent Company

Name/Ticker Atrium Companies/Privately Held 12-Month Period Amount

Prepetition EBITDAb 12/31/09 54

Bankruptcy Summary Post-Emergence EBITDA Forecast 12/31/11 67

Did All Entities in the Group File?a No

Enterprise Value (EV) Range (or Asset Value Range) Plan Proposed by Debtor

Low 420

Court District Delaware

High 420 Substantive Consolidation No

Midpoint EV (Value) 420

Petition Date 1/20/10

Equity Value Range Confirmation or Conversion Date 4/28/10

Low 168

Effective Date 4/30/10

High 208 Duration (Months) 3

Midpoint EV/Post-Emergence EBITDA Estimate (x) 6.3

Filing — Type Chapter 11 (Prepackaged) Petition Date Versus Emergence Date Section 363 Asset Sale by Debtor Yes — Sale of Substantially All Assets (as

Going Concern) Voluntary or Involuntary Filing Voluntary

Petition Date Emergence Date Postconfirmation Liquidating Trust Choose

Total Debt 656 261

Resolution Acquired, Merged or Sold

Consolidated Leverage (x) 12.2 3.9

Debt Shed in Bankruptcy — 395

Debt Shed in Bankruptcy (%) — 60

Events Leading Up to Bankruptcy (or Contributing Factors) Atrium’s debt/EBITDA exceeded 12x by the time of filing. The company’s highly leveraged capital structure became untenable when demand for its window and door products significantly declined as a result of the collapse in housing prices and credit crunch. In addition, the lack of consumer confidence reduced demand from home remodelers, which further hurt sales. To try to cope with the adverse market environment, the company completed a debt-for-equity exchange of 97.4% of the ACIH Inc. notes, amended its credit facility and pursued cost reduction initiatives, such as headcount reduction to 3,990 from 7,300 and consolidation of manufacturing facilities. However, further realignment of the balance sheet was needed, and a restructuring support agreement was reached with senior lenders that provided for a new equity investment by the owner of the common stock.

Valuation Estimate Summary Fundamental Going Concern Valuation The third party valuation advisor estimated a going concern enterprise valuation of $420 million (midpoint, no range disclosed). The valuation resulted from several methodologies, including a discounted cash flow analysis, peer market trading values, and peer precedent merger and acquisition transaction values. The assumptions and names of peers were not provided. The valuation includes excess cash and net operating losses. The advisor’s considered various information, including management’s forecast of EBITDA:

($ Mil.) 2011 2012 2013 2014 EBITDA 66.7 81.00 97.3 110.0 Valuation Based on Settlement Agreement Incorporating New Money Equity Investment The plan of reorganization was based on a new equity investment by Kenner & Company, Inc. and Golden Gate Capital of $192.2 million in exchange for 92.5% of the new common equity. Proceeds of this new equity investment, along with proceeds of new exit debt of $261 million were used to fund payments under the plan. The enterprise value used for purposes of this settlement is approximately $460 million. During the bankruptcy, a sale process for the company was initiated. Interested parties received information for due diligence review. One bidder, Griffon, made a $463 million acquisition proposal ($456.5 million cash), but ultimately the new equity investment alternative was pursued and Kenner and Golden Gate became the majority shareholders.

Liquidation Value Alternative The Chapter 7 liquidation alternative estimated gross proceeds in the range of $80.6 million–$104.4 million. The analysis was based on percentages of the book value of assets on the balance sheet as of Nov. 30, 2009. The assets and percent ranges applied included: • Cash of $27.6 million at 100% • Accounts receivable of $18.8 million at 55%–70% • Inventory of $38 million at 33%–50% • Property, plant and equipment of $88.9 million at 34%–46% • Goodwill and other intangibles of 148.5 million at 0%–2% Under this alternative reorganization scenario, the senior secured credit facility lenders would have recovered 18%–22% of their claim amount. aThe Canadian subsidiary, Northstar Window, filed a separate reorganization proceeding in Canadian court. bPrepetition EBITDA is Fitch estimate based on disclosure statement note that prepetition debt leverage exceeded 12x. Source, unless otherwise noted: Second modified disclosure statement for the first modified joint plan of reorganization dated March 18, 2010.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 22 January 28, 2016

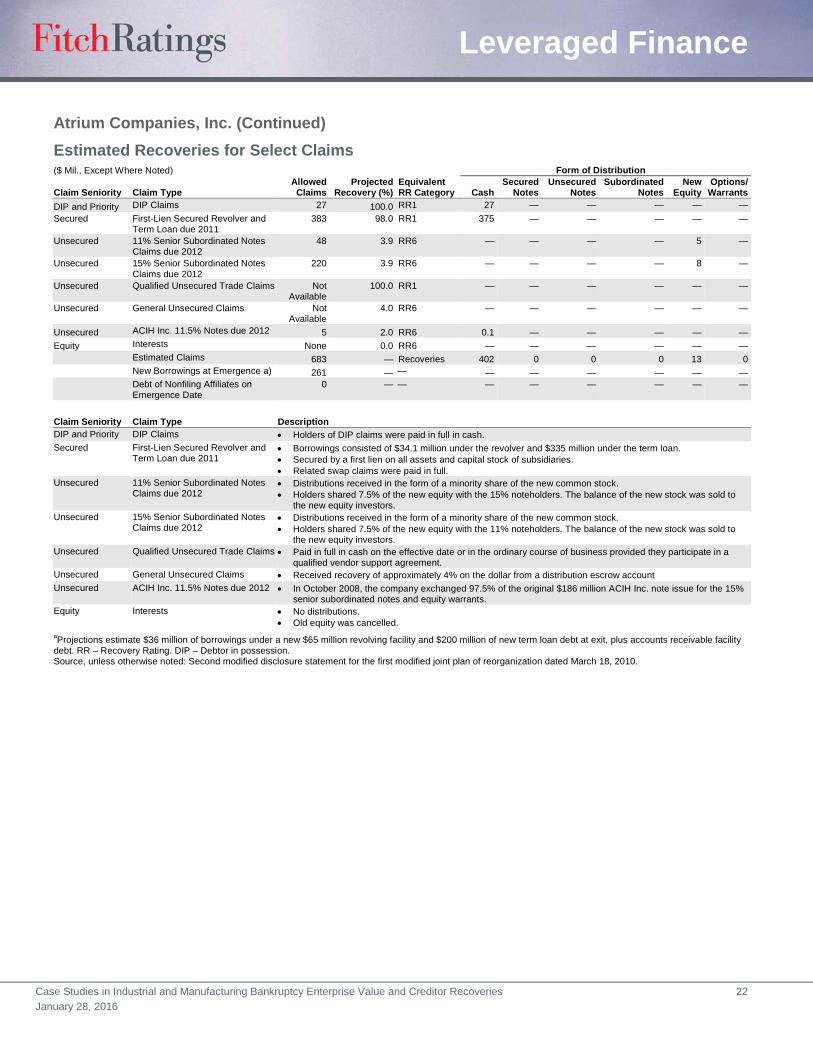

Atrium Companies, Inc. (Continued) Estimated Recoveries for Select Claims ($ Mil., Except Where Noted)

Form of Distribution

Claim Seniority Claim Type Allowed Claims

Projected Recovery (%)

Equivalent RR Category Cash

Secured Notes

Unsecured Notes

Subordinated Notes

New Equity

Options/ Warrants

DIP and Priority DIP Claims 27 100.0 RR1 27 — — — — — Secured First-Lien Secured Revolver and

Term Loan due 2011 383 98.0 RR1 375 — — — — —

Unsecured 11% Senior Subordinated Notes Claims due 2012

48 3.9 RR6 — — — — 5 —

Unsecured 15% Senior Subordinated Notes Claims due 2012

220 3.9 RR6 — — — — 8 —

Unsecured Qualified Unsecured Trade Claims Not Available

100.0 RR1 — — — — — —

Unsecured General Unsecured Claims Not Available

4.0 RR6 — — — — — —

Unsecured ACIH Inc. 11.5% Notes due 2012 5 2.0 RR6 0.1 — — — — — Equity Interests None 0.0 RR6 — — — — — —

Estimated Claims 683 — Recoveries 402 0 0 0 13 0

New Borrowings at Emergence a) 261 — — — — — — — —

Debt of Nonfiling Affiliates on Emergence Date

0 — — — — — — — —

Claim Seniority Claim Type Description DIP and Priority DIP Claims • Holders of DIP claims were paid in full in cash. Secured First-Lien Secured Revolver and

Term Loan due 2011 • Borrowings consisted of $34.1 million under the revolver and $335 million under the term loan. • Secured by a first lien on all assets and capital stock of subsidiaries. • Related swap claims were paid in full.

Unsecured 11% Senior Subordinated Notes Claims due 2012

• Distributions received in the form of a minority share of the new common stock. • Holders shared 7.5% of the new equity with the 15% noteholders. The balance of the new stock was sold to

the new equity investors. Unsecured 15% Senior Subordinated Notes

Claims due 2012 • Distributions received in the form of a minority share of the new common stock. • Holders shared 7.5% of the new equity with the 11% noteholders. The balance of the new stock was sold to

the new equity investors. Unsecured Qualified Unsecured Trade Claims • Paid in full in cash on the effective date or in the ordinary course of business provided they participate in a

qualified vendor support agreement. Unsecured General Unsecured Claims • Received recovery of approximately 4% on the dollar from a distribution escrow account Unsecured ACIH Inc. 11.5% Notes due 2012 • In October 2008, the company exchanged 97.5% of the original $186 million ACIH Inc. note issue for the 15%

senior subordinated notes and equity warrants. Equity Interests • No distributions.

• Old equity was cancelled. aProjections estimate $36 million of borrowings under a new $65 million revolving facility and $200 million of new term loan debt at exit, plus accounts receivable facility debt. RR – Recovery Rating. DIP – Debtor in possession. Source, unless otherwise noted: Second modified disclosure statement for the first modified joint plan of reorganization dated March 18, 2010.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 23 January 28, 2016

Atrium Companies, Inc. (Continued) Additional Information

Cash on Filing Date Not available. $27.6 million as of Nov. 30, 2009. Prepetition Bank Facility Commitments $46 million revolver and $335 million term loan. The company had a bankruptcy remote accounts receivable

securitization facility, which was maintained throughout the bankruptcy (not a debtor). Prepetition Bank Facility Borrowings on Filing Date $34.1 million of revolver usage, including $22.7 million of loans and $12.4 million of letters of credit. Was the DIP a New Money Facility or Roll Up of a Prepetition Facility? The $40 million DIP was a new money facility. Other Notable Issues None Executory Contracts The rejected executory contract exhibit in the plan supplement listed certain contracts, including lease

agreements, employee severance agreements, customer service agreement, license agreements, etc. There were also hundreds of assumed contracts listed in an exhibit to the plan.

Deficiency Claims None Contingent Claims and/or Contingent Recoveries Claims related to receivables and payables and litigation. Intercompany Claims Reinstated. Did not receive any distributions under the plan of reorganization. Pension Claims/Motions Not available. Postpetition Interest? No If Yes, Recipient Class Not applicable. Concession Payments Yes Recipient and Comments Holders of senior subordinated notes claims received distributions in the form of 7.5% of the new common stock

as a result of the settlement with the creditors committee, with two-thirds going to the holders of the 11% senior subordinated notes and one-third going to holders of the 15% senior subordinated notes. In addition, holders of unsecured trade claims will receive payment in full in cash following execution of a qualified vendor support agreement.

DIP – Debtor in possession. Source: Fitch Ratings, company disclosure statement dated March 18, 2010.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 24 January 28, 2016

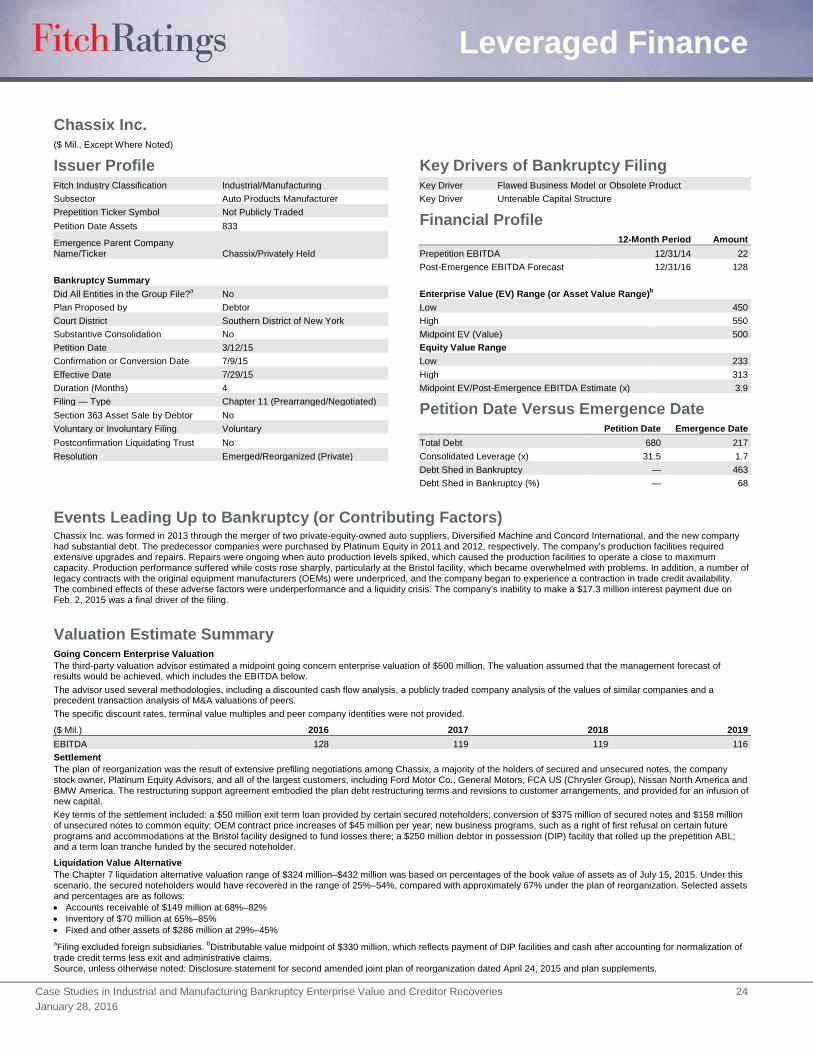

Chassix Inc. ($ Mil., Except Where Noted)

Issuer Profile Key Drivers of Bankruptcy Filing Fitch Industry Classification Industrial/Manufacturing Key Driver Flawed Business Model or Obsolete Product Subsector Auto Products Manufacturer

Key Driver Untenable Capital Structure

Prepetition Ticker Symbol Not Publicly Traded Financial Profile Petition Date Assets 833 Emergence Parent Company

Name/Ticker Chassix/Privately Held 12-Month Period Amount

Prepetition EBITDA 12/31/14 22

Post-Emergence EBITDA Forecast 12/31/16 128

Bankruptcy Summary Did All Entities in the Group File?a No

Enterprise Value (EV) Range (or Asset Value Range)b

Plan Proposed by Debtor

Low 450 Court District Southern District of New York

High 550

Substantive Consolidation No

Midpoint EV (Value) 500 Petition Date 3/12/15

Equity Value Range

Confirmation or Conversion Date 7/9/15

Low 233 Effective Date 7/29/15

High 313

Duration (Months) 4

Midpoint EV/Post-Emergence EBITDA Estimate (x) 3.9 Filing — Type Chapter 11 (Prearranged/Negotiated)

Petition Date Versus Emergence Date Section 363 Asset Sale by Debtor No Voluntary or Involuntary Filing Voluntary

Petition Date Emergence Date Postconfirmation Liquidating Trust No

Total Debt 680 217

Resolution Emerged/Reorganized (Private)

Consolidated Leverage (x) 31.5 1.7

Debt Shed in Bankruptcy — 463

Debt Shed in Bankruptcy (%) — 68

Events Leading Up to Bankruptcy (or Contributing Factors) Chassix Inc. was formed in 2013 through the merger of two private-equity-owned auto suppliers, Diversified Machine and Concord International, and the new company had substantial debt. The predecessor companies were purchased by Platinum Equity in 2011 and 2012, respectively. The company’s production facilities required extensive upgrades and repairs. Repairs were ongoing when auto production levels spiked, which caused the production facilities to operate a close to maximum capacity. Production performance suffered while costs rose sharply, particularly at the Bristol facility, which became overwhelmed with problems. In addition, a number of legacy contracts with the original equipment manufacturers (OEMs) were underpriced, and the company began to experience a contraction in trade credit availability. The combined effects of these adverse factors were underperformance and a liquidity crisis. The company’s inability to make a $17.3 million interest payment due on Feb. 2, 2015 was a final driver of the filing.

Valuation Estimate Summary Going Concern Enterprise Valuation The third-party valuation advisor estimated a midpoint going concern enterprise valuation of $500 million. The valuation assumed that the management forecast of results would be achieved, which includes the EBITDA below. The advisor used several methodologies, including a discounted cash flow analysis, a publicly traded company analysis of the values of similar companies and a precedent transaction analysis of M&A valuations of peers. The specific discount rates, terminal value multiples and peer company identities were not provided.

($ Mil.) 2016 2017 2018 2019 EBITDA 128 119 119 116 Settlement The plan of reorganization was the result of extensive prefiling negotiations among Chassix, a majority of the holders of secured and unsecured notes, the company stock owner, Platinum Equity Advisors, and all of the largest customers, including Ford Motor Co., General Motors, FCA US (Chrysler Group), Nissan North America and BMW America. The restructuring support agreement embodied the plan debt restructuring terms and revisions to customer arrangements, and provided for an infusion of new capital. Key terms of the settlement included: a $50 million exit term loan provided by certain secured noteholders; conversion of $375 million of secured notes and $158 million of unsecured notes to common equity; OEM contract price increases of $45 million per year; new business programs, such as a right of first refusal on certain future programs and accommodations at the Bristol facility designed to fund losses there; a $250 million debtor in possession (DIP) facility that rolled up the prepetition ABL; and a term loan tranche funded by the secured noteholder.

Liquidation Value Alternative The Chapter 7 liquidation alternative valuation range of $324 million–$432 million was based on percentages of the book value of assets as of July 15, 2015. Under this scenario, the secured noteholders would have recovered in the range of 25%–54%, compared with approximately 67% under the plan of reorganization. Selected assets and percentages are as follows: • Accounts receivable of $149 million at 68%–82% • Inventory of $70 million at 65%–85% • Fixed and other assets of $286 million at 29%–45% aFiling excluded foreign subsidiaries. bDistributable value midpoint of $330 million, which reflects payment of DIP facilities and cash after accounting for normalization of trade credit terms less exit and administrative claims. Source, unless otherwise noted: Disclosure statement for second amended joint plan of reorganization dated April 24, 2015 and plan supplements.

Leveraged Finance

Case Studies in Industrial and Manufacturing Bankruptcy Enterprise Value and Creditor Recoveries 25 January 28, 2016

Chassix Inc. (Continued) Estimated Recoveries for Select Claims ($ Mil., Except Where Noted)

Form of Distribution

Claim Seniority Claim Type Allowed Claims

Projected Recovery (%)

Equivalent RR Category Cash

Secured Notes

Unsecured Notes

Subordinated Notes

New Equity

Options/ Warrants

DIP and Priority

$250 Million DIP Facility Consisting of a $150 Million Roll Up Revolver and $100 Million New Money Term Loan

155 100.0 RR1 — 155 — — — —

Secured $150 Million ABL Revolving Credit Facility

0 100.0 RR1 0 — — — — —

Secured 9 1/4% Secured Notes due 2018 395 67.3 RR3 — — — — 266 — Secured Capital Lease Obligations 12 100.0 RR1 — 12 — — — —

Unsecured 10%/10.75% Senior PIK Toggle Unsecured Notes due December 2018

158 7.0 RR6 4 — — — 7 —

Unsecured Trade Claims 32 38 RR4 12 — — — — — Equity Old Equity Interests Not

Applicable 0.0 RR6 — — — — — —

Estimated Claims 752

Recoveries 16 167 0 0 273 0

New Borrowings at Emergencea 50 — — — — — — — —

Debt of Nonfiling Affiliates on Emergence Date

0 — — — — — — — —

Claim Seniority Claim Type Description DIP and Priority $250 million DIP facility consisting of a

$150 Million Roll Up Revolver and $100 Million New Money Term Loan

• The $55 million of DIP revolver claims $100 million of term loan claims were converted into exit facilities.

Secured $150 Million ABL Revolving Credit Facility

• The $135 million of petition date ABL borrowings were repaid in full in cash shortly following the filing date using proceeds of the DIP facility.

• Borrowing base calculated on percentages of value of accounts receivable and inventory. Secured 9 1/4% Secured Notes due 2018 • The secured notes were converted to new 97.5% of the new common equity.

• Recovery rate assumes midpoint fundamental value for new common equity. Secured Capital Lease Obligations • Reinstated.