Industrial and logistics real estate

6

Industrial and Logistics real estate Dutch Market Report 2015 industrial.nl

-

Upload

rudolf-bak -

Category

Documents

-

view

33 -

download

2

Transcript of Industrial and logistics real estate

Industrial and Logistics real estate Dutch Market Report 2015

industrial.nl

Rob Mutsaerts

This report has been produced in close cooperation with: Bak Property Research

industrial.nl

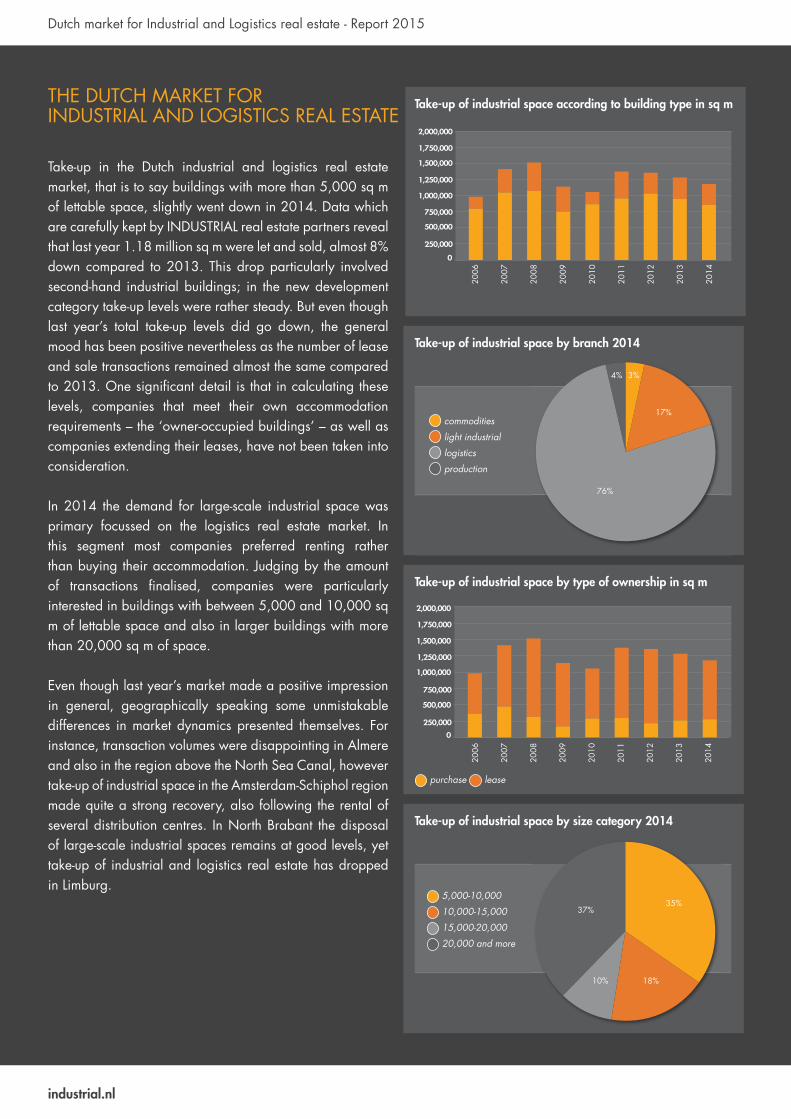

Dutch market for Industrial and Logistics real estate - Report 2015

Take-up in the Dutch industrial and logistics real estate market, that is to say buildings with more than 5,000 sq m of lettable space, slightly went down in 2014. Data which are carefully kept by INDUSTRIAL real estate partners reveal that last year 1.18 million sq m were let and sold, almost 8% down compared to 2013. This drop particularly involved second-hand industrial buildings; in the new development category take-up levels were rather steady. But even though last year’s total take-up levels did go down, the general mood has been positive nevertheless as the number of lease and sale transactions remained almost the same compared to 2013. One significant detail is that in calculating these levels, companies that meet their own accommodation requirements – the ‘owner-occupied buildings’ – as well as companies extending their leases, have not been taken into consideration.

In 2014 the demand for large-scale industrial space was primary focussed on the logistics real estate market. In this segment most companies preferred renting rather than buying their accommodation. Judging by the amount of transactions finalised, companies were particularly interested in buildings with between 5,000 and 10,000 sq m of lettable space and also in larger buildings with more than 20,000 sq m of space.

Even though last year’s market made a positive impression in general, geographically speaking some unmistakable differences in market dynamics presented themselves. For instance, transaction volumes were disappointing in Almere and also in the region above the North Sea Canal, however take-up of industrial space in the Amsterdam-Schiphol region made quite a strong recovery, also following the rental of several distribution centres. In North Brabant the disposal of large-scale industrial spaces remains at good levels, yet take-up of industrial and logistics real estate has dropped in Limburg.

THE DUTCH MARKET FOR INDUSTRIAL AND LOGISTICS REAL ESTATE

Take-up of industrial space according to building type in sq m

Take-up of industrial space by branch 2014

Take-up of industrial space by type of ownership in sq m

Take-up of industrial space by size category 2014

purchase lease

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,000

2,000,000

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,000

2,000,000

2006

2010

2008

2012

2007

2011

2009

2013

2014

2006

2010

2008

2012

2007

2011

2009

2013

2014

commodities

light industrial

logistics

production

5,000-10,000

10,000-15,000

15,000-20,000

20,000 and more

76%

10%

3%

18%

4%

37%

17%

35%

Dutch market for Industrial and Logistics real estate - Report 2015

THE OCCUPATIONAL MARKET FOR LOGISTICS REAL ESTATE

The year 2014 was dominated by considerable demand for logistics real estate. In the so-called open market, the amount of buildings rented or sold remained the same compared to last year. Approximately 900,000 sq m in total have welcomed new users. Many newly constructed distribution centres were taken up, however existing buildings were also given serious attention. As in previous years, in 2014 the amount of transactions realised was highest in the southern Netherlands as the west and centre of the province of North Brabant claimed much of this demand.

Last year Limburg witnessed a modest decrease in logistics real estate take-up, however INDUSTRIAL real estate partners is expecting this region to attract quite a deal of attention this year, a development that will serve Venlo in particular. This region is an interesting business location for international companies who sell their products online and who want their distribution centres to be in the proximity of the Cologne Bonn Airport.

Even though demand for logistics real estate maintained a good position last year, the number of distribution centres available for immediate occupation continued to climb nevertheless. Rising availability followed almost entirely due to speculative construction of distribution centres in places like Venlo, Utrecht and Schiphol. Interestingly, in addition to the immediately available supply, the number of plans to build sustainable distribution centres has grown as well. Even though more newly developed buildings were available for lease last year, the majority of the spaces on offer were old and quite often less marketable. In addition to municipalities with many vacant distribution centres for rent, vacancy was hardly an issue in places like Bergen op Zoom, Eindhoven, Moerdijk, Venlo and Waalwijk.

Take-up of logistics space according to building type in sq m

Take-up of logistics space by region in sq m

Supply of logistics space according to building type in sq m

Supply of logistics space as percentage of stocks

existing buildings new developments

existing buildings new developments

0

200,000

400,000

600,000

800,000

1,000,000

0

50,000

100,000

150,000

200,000

250,000

300,000

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

4

5

6

7

8

9

10

11

12

Utrech

t

Amsterda

m-

Schip

hol

Almere

Oost B

raban

t

Limbu

rg

Arnhem

Nijmeg

en

Rotte

rdam

Haagla

nden

Other

region

s

West

- en

Midden

Braba

nt

2006

2010

2008

2012

2007

2011

2009

2013

2014

2006

2010

2008

2012

2007

2011

2009

2013

2014

2006

2010

2008

2012

2007

2011

2009

2013

2014

industrial.nl

Dutch market for Industrial and Logistics real estate - Report 2015 Dutch market for Industrial and Logistics real estate - Report 2015

THE INVESTMENT MARKET FOR INDUSTRIAL AND LOGISTICS REAL ESTATE

Real estate in the Netherlands continued to attract investors in 2014 as low return on government loans and the large availability of funds made many investors embrace it. The logistics real estate market benefited from this development. Trusting that the available data on acquisitions and sales are correct, last year there was approximately € 835 million invested in distribution centres. As a result, investment volumes were very close to those of 2007, a record year in terms of logistics real estate investments. Last year investors clearly preferred distribution centres in North Brabant and Limburg, as well as Utrecht and Amsterdam - Schiphol.

Most buyers were American, Russian and Belgian investors. Investors were not only interested in build-to-suit projects, they also paid serious attention to buildings that existed already. The majority of the acquisitions realised last year involved buildings with relatively substantial investment volumes. Distribution centres worth less than € 5 million were hardly disposed of. One of the consequences of investors’ major demand for logistics real estate was that the gross initial yield of first-class distribution centres went down to less than 7 percent in some cases.

In 2014 investors also seriously considered light industrial buildings, as different large-scale complexes exchanged owners causing the gross initial yield to range from 9% to 13%. Remarkably, most investors who were interested in this market segment were British.

Investments in logistics space according to building type

Investments in logistics space by nationality

Investments in logistics space by region

existing buildings new developments

foreign investors dutch investors

0

200

400

600

800

1,000

0

50

100

150

200

250

300

350

0

200

400

600

800

1,000

values x million €

values x million €

values x million €

Rotte

rdam

Haagla

nden

Utrech

t

West

- en

Midden

Brab

ant

Arnhem

Nijmeg

en

Amsterda

m,

Schip

hol ,

Almere Othe

r

region

sOos

t-

Braba

nt/

Limbu

rg

2006

2006

2010

2010

2008

2008

2012

2012

2007

2007

2011

2011

2009

2009

2013

2013

2014

2014

DHG sold 107,000 sq m logistics facility in the Port of Amsterdam to Delin Capital for € 75 million.

industrial.nl

Dutch market for Industrial and Logistics real estate - Report 2015

TOP 10 TRANSACTIONS LOGISTICS REAL ESTATE

Size Location Occupier Lessor Type of building

1 55,000 sq m Moerdijk OWIM SPF Existing building

2 49,700 sq m Tilburg Tesla DOKVAST New development

3 40,000 sq m Nieuwegein Albert Heijn Borghese New development

4 40,000 sq m Oosterhout (Gld) Nabuurs Goodman New development

5 32,800 sq m Tiel Kuehne + Nagel WDP New development

6 32,600 sq m Breda Broekman Logistiek Greenery Existing building

7 25,800 sq m Oss Vos Logistics Montea New development

8 25,000 sq m Tilburg Coolblue Prologis New development

9 23,700 sq m Bergen op Zoom Forever21 Fashion ProDelta New development

10 22,500 sq m Maasbree Seacon Logistics Built to Build New development

TOP 10 INVESTMENTS INDUSTRIAL AND LOGISTICS REAL ESTATE

Size Location Building type Buyer Vendor Price

1 242,000 sq m several locations Logistics ProLogis Schroder Real estate € 170 million

2 370,000 sq m several locations Light industrial Hansteen BGP Investment Sarl € 106 million

3 107,000 sq m Amsterdam Logistics Delin Capital David Hart Group € 75 million

4 130,000 sq m several locations Light industrial Mstar Rockspring € 71 million

5 175,000 sq m several locations Light industrial Rockspring AXA REIM € 67 million

6 73,000 sq m Echt Logistics WDP Action € 57 million

7 63,000 sq m Tiel Logistics WDP Van de Ven € 50 million

8 102,000 sq m several locations Light industrial MBay Light Industrial Internos € 43 million

9 44,000 sq m Waddinxveen Logistics Delin Capital Distripark A12 € 38 million

10 54,000 sq m several locations Logistics LogiCor CBRE Global Investors € 34 million

Jasper Kiestra

TilburgNieuwegein

This report has been produced in close cooperation with: Bak Property Research

DOKVAST develops 49,700 sq m for TeslaBorghese develops 40,000 sq m for Albert Heijn / ND Logistics

Amsterdam RotterdamTilburg

Our services• Leasing• Buying and selling• Strategic real estate advice• Sale-and-leasebacks• Real estate portfolio consulting• Real estate investments

T. +31 (0)88 989 98 [email protected]

Despite careful preparation and monitoring of this report and the information it contains, INDUSTRIAL real estate partners cannot guarantee its completeness, accuracy or actuality. INDUSTRIAL real estate partners accepts no liability for any direct or indirect damage of whatever nature arising from or in any way related to the use of this report or the potential unavailability thereof.

DUTCH LAND PRICES & RENT LEVELS 2014/2015

land prices rent levels

1 Schiphol Airport 250 - 325 75 - 90

2 Amsterdam Port 215 * - 250 * 40 - 65

3 Almere 110 - 165 30 - 60

4 Utrecht 230 - 300 30 - 65

5 Arnhem/Nijmegen 150 - 170 25 - 60

6 Bleiswijk/Waddinxveen 150 - 230 40 - 65

7 Rotterdam Port 175 * - 265 * 40 - 65

8 Moerdijk 120 - 145 30 - 55

9 Roosendaal/Bergen op Zoom 100 - 150 35 - 50

10 Tilburg/Waalwijk 120 - 150 45 - 55

11 Eindhoven 155 - 200 40 - 50

12 Venlo/Venray 115 - 130 30 - 50

13 Maastricht/Heerlen 75 - 100 30 - 50

land prices in € per sq m / rent levels warehouse space in € per sq m per year / * = for 50 year leasehold

3

5

13

10

About INDUSTRIAL real estate partners INDUSTRIAL real estate partners is an independent real estate consultancy company with a strong focus on industrial and logistics real esate throughout the Netherlands.

They particularly focus on agency, investments, strategic real estate advice and developments. From their offices in Amsterdam Airport, Rotterdam Airport and Tilburg they cover the important logistics regions.

By combining their national scope, expertise and skills, they are committed to provide the best possible services to owners, occupiers, (re)developers and authorities.

Jasper Kiestra Bart SchravenMaurits Kortleven Marcel Hoekstra Rob Mutsaerts

6

7 5

4

132

11 12

8

9

This report has been produced in close cooperation with: Bak Property Research