Recent Changes in Dutch Health Insurance: Individual Mandate or

INDIVIDUAL CHANGES

BUSINESS CHANGES

ESTATE & GIFT CHANGES

Tax Cuts & Jobs Act

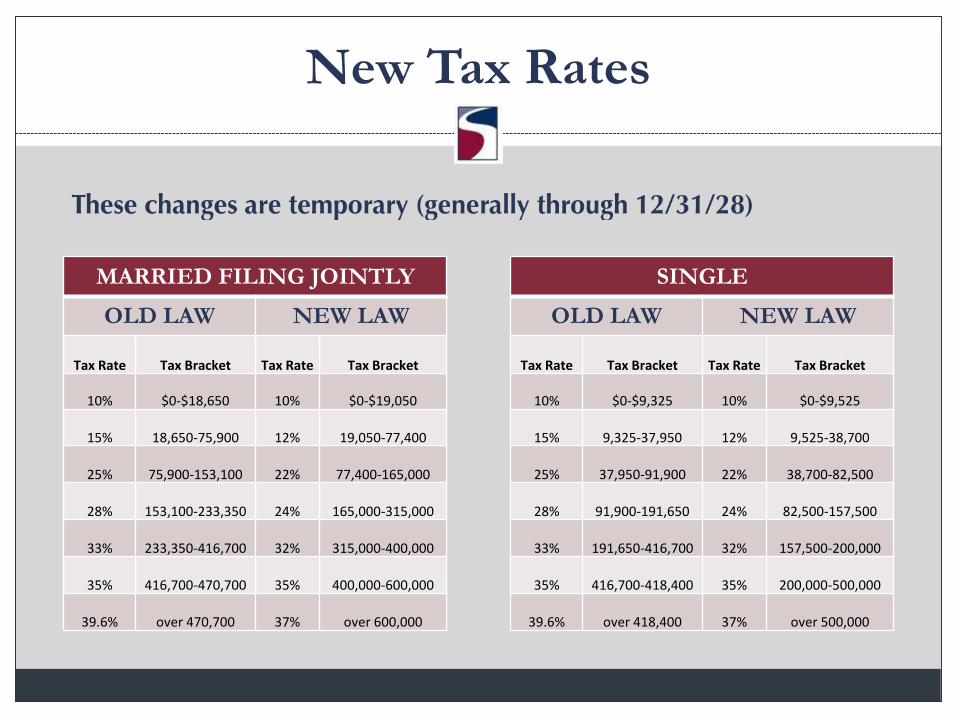

New Tax Rates

MARRIED FILING JOINTLY

OLD LAW NEW LAW

Tax Rate Tax Bracket Tax Rate Tax Bracket

10% $0-$18,650 10% $0-$19,050

15% 18,650-75,900 12% 19,050-77,400

25% 75,900-153,100 22% 77,400-165,000

28% 153,100-233,350 24% 165,000-315,000

33% 233,350-416,700 32% 315,000-400,000

35% 416,700-470,700 35% 400,000-600,000

39.6% over 470,700 37% over 600,000

SINGLE

OLD LAW NEW LAW

Tax Rate Tax Bracket Tax Rate Tax Bracket

10% $0-$9,325 10% $0-$9,525

15% 9,325-37,950 12% 9,525-38,700

25% 37,950-91,900 22% 38,700-82,500

28% 91,900-191,650 24% 82,500-157,500

33% 191,650-416,700 32% 157,500-200,000

35% 416,700-418,400 35% 200,000-500,000

39.6% over 418,400 37% over 500,000

Individual Changes

Personal Exemptions Eliminated

EXEMPTION OLD LAW NEW LAW

Deduction for each taxpayer, spouse, & dependent $4,050 NONE

Individual Changes

Standard Deduction Increased

FILING STATUS OLD LAW NEW LAW

Single $6,350 $12,000

Married Filing Jointly and Surviving Spouses $12,700 $24,000

Heads of Households $9,350 $18,000

Additional Amount for Aged or Blind $1,250 for each $1,300 for each

Additional Amount for Aged or Blind if Unmarried

and Not a Surviving Spouse

$1,550 for each $1,600 for each

Individual Changes

State, Local, & Real Estate Tax Limited

• Married Filing Separate: $5,000 combined limit

• Married Filing Jointly, Single, Head of Households:

$10,000 combined limit

Individual Changes

Mortgage & Home Equity Interest Limited

OLD LAW

• $1 million of debt, plus home equity debt of $100,000

• Home equity could be used for any purpose

NEW LAW

• $750,000 of debt which includes any home equity loans

• Home equity loans must be used to buy, build, or substantially improve

the taxpayer’s home

Individual Changes

Charitable Donations• Remain fully deductible

• Limit on 50% of AGI increased to 60% of AGI

Individual Changes

Casualty & Theft Loss Deduction• Eliminated in new law

• Exception for losses in federally

declared disaster area

Individual Changes

Moving Expense Deduction• Moving Expense Deduction and Income Exclusion for

qualified moving reimbursements eliminated.

• Exception for members of armed forces on active duty.

Individual Changes

Miscellaneous Itemized Deductions Subject

to 2% Limit Eliminated

Examples:

• Union Dues

• Investment Fees

• Safe Deposit Fees

• Professional Dues

• IRA Fees

Individual Changes

Alimony Deduction and Income Inclusion Repealed

For divorces or separation agreements executed AFTER 2018 (or

modified after 2018)

No longer deduction for alimony paid

AND

Recipient does not include alimony in income

Individual Changes

Alternative Minimum Tax

OLD LAW NEW LAW

AMT Exemption:

Married filing jointly or qualifying widow(er) $86,200 $109,400

Single or head of household $55,400 $70,300

Married filing separate $43,100 $54,700

Exemption Reduced by 25% of AMTI Over:

Married filing jointly or qualifying widow(er) $164,100 $1,000,000

Single or head of household $123,100 $500,000

Married filing separate $82,050 $500,000

Individual Changes

529 Plans (Qualified Tuition Programs)

OLD LAW

Allowed for tax-free distribution of earnings for college,

vocational schools, and post secondary

NEW LAW

Allows for above PLUS up to $10,000 per tax year at elementary and

secondary (public, private, or religious)

These distributions are taxable in Illinois if previously

deducted on IL-1040

Individual Changes

Child Tax CreditIncreases from $1,000 to $2,000 ($1,400 of this is refundable) per

qualifying child under age 17

Phase Out Updates:

OLD LAW

Single or HOH $75,000

Married Filing Jointly $110,000

Married Filing Separate $55,000

NEW LAW

Single, HOH, or Married Filing Separate $200,000

Married Filing Jointly $400,000

Individual Changes

Nonchild Tax Credit

New law adds a $500 credit for qualifying dependents

• Child 17 or older

• Parent

• Grandparent

• other

Individual Changes

Affordable Care Act Individual Mandate Repealed

For months beginning AFTER 2018, there is no penalty for

people without health insurance.

Individual Changes

Kiddie Tax ModifiedOLD LAW

Unearned income of child over $2,100 was taxed at parents’ tax rate

(children under 18 and full-time college students under 24)

NEW LAW

First $1,050 of unearned income has no tax. Second $1,050 is taxed at

child’s rate and all unearned income in excess of $2,100 is now taxed

at trust rates

TAX RATE THRESHOLDS

10% $0 - $2,550

24% $2,551 - $9,150

35% $9,151 - $12,500

37% Over $12,500

TAX RATE THRESHOLDS

0% $0 - $2,600

15% $2,601 - $12,700

20% Over $12,700

Individual Changes

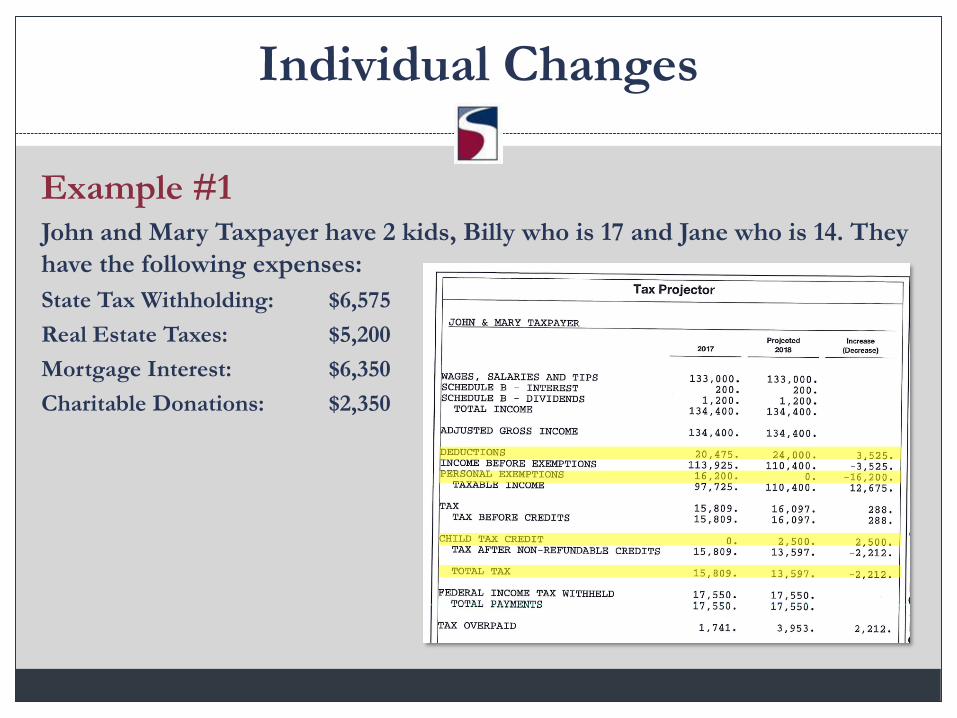

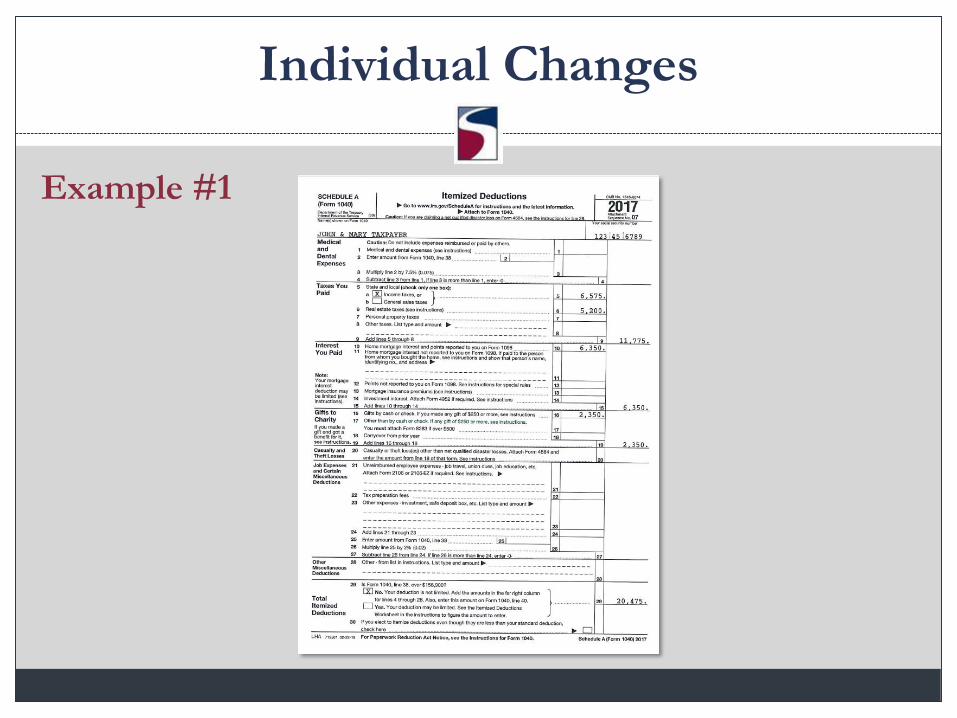

Example #1John and Mary Taxpayer have 2 kids, Billy who is 17 and Jane who is 14. They

have the following expenses:

State Tax Withholding: $6,575

Real Estate Taxes: $5,200

Mortgage Interest: $6,350

Charitable Donations: $2,350

Individual Changes

Example #1

Individual Changes

Example #2John and Mary Taxpayer file jointly. John is 72 and Mary is 70. John is

receiving IRA RMD and they have the following expenses:

Medical: $11,300

Sales Tax: $976

Real Estate Taxes: $5,200

Mortgage Interest: $6,350

Charitable Donations: $7,500

Individual Changes

Example #2

Individual Changes

Example #3John and Mary Taxpayer file jointly. John is 72 and Mary is 70. John is

receiving IRA RMD and they have the following expenses:

Medical: $11,300

Sales Tax: $976

Real Estate Taxes: $5,200

Mortgage Interest: $6,350

Charitable Donations: $7,500

*But in this example, John pays his

donations directly from his IRA RMD.

BUSINESS CHANGES

C CORPS

S CORPS

PARTNERSHIPS

SOLE PROPRIETOR

Business Changes

C Corp Tax Rates: Permanent

OLD LAW

NET INCOME TAX RATE

0 – 50,000 15%

50,000 – 75,000 25%

75,000 – 100,000 34%

100,000 – 335,000 39%

335,000 – 10,000,000 34%

NEW LAW

Flat Rate 21%

Business Changes

Dividend Received Deduction

OLD LAW NEW LAW

If Corp owned > 20% of another Corp 80% 65%

If Corp owned > 50% of another Corp 100% 100%

If Corp owned < 20% of another Corp 70% 50%

Business Changes

Corporate AMT

New law repeals corporate AMT for years after 2017

Business Changes

Section 179 Deduction

OLD LAW NEW LAW

Limit on 179 Deduction $520,000 $1,000,000

Phaseout Threshold $2,070,000 $2,500,000

Business Changes

Bonus Depreciation

New law allows immediate expensing of either new or used

property

Property Placed in Service Percentage of Write-Off

2018 - 2022 100%

2023 80%

2024 60%

2025 40%

2026 20%

Business Changes

Section 199A Deduction

For tax years 2018-2025, individuals generally may deduct 20% of

Qualified Business Income (QBI) from the income of a Qualified

Trade or Business (QTB) operating as a partnership, s corp, or sole

proprietor.

The 20% deduction will NOT reduce AGI, but will be a deduction in

computing taxable income.

Limitations will be based on type of business involved, taxable

income of the individual, W-2 wages paid by business, and/or

property owned.

Business Changes

Section 199A Deduction: Limitations

• A QTB generally includes any trade or business except a Specified Service

Trade or Business (SSTB)

• An SSTB includes any business involved in the fields of:

• Health

• Law

• Accounting

• Actuarial Sciences

• Performing Arts

• Consulting

• Professional Athletics

• Financial services, brokering services, investing and investing management

• Or a business where principal asset is the reputation or skill of one or more of its

employees or owners

Business Changes

Section 199A Deduction: Limitations

• The SSTB exclusion does not apply for taxpayers with taxable

income of less than $315,000 (MFJ) and $157,500 (S, MFS,

HOH)

• Phase out of exclusion from

• 315,000 – 415,000 for MFJ

• 157,000 – 207,500 for S, MFS, HOH

Business Changes

Meals & Entertainment

Old law limited deduction for meals and entertainment to 50%

of expenditure

New law allows 50% for meals in course of business, BUT no

deduction for any entertainment expenses

• Ball tickets

• Concert tickets

• Hunting clubs

Business Changes

Interest Expense Limitation

• Certain businesses will be subject to net interest disallowance

• Net interest expense in excess of 30% of company’s adjusted

taxable income will be disallowed

• Adjusted taxable income defined as taxable income adding

back depreciation, amortization, and depletion

• Only applies to businesses with average annual gross receipts

for prior 3 years of more than $25 million

• Exception for auto dealers

Business Changes

Like Kind Exchanges

New law limits like kind exchange rules to only apply to real

property that is not held primarily for sale

Business Changes

Net Operating Losses

New law generally repeals the 2 year carryback for NOL’s.

NOL’s can now be carried forward indefinitely.

Use limited to 80% of taxable income

GIFT & ESTATE

Gift & Estate

OLD LAW

Unified credit for estate and gift purposes was $5.6 million ($11.2

million for married couple)

NEW LAW

For decedents dying or gifts made after 2017 and before 2026,

the estate and gift unified credit has been increased to $11.2

million ($22.4 million for married couple)

ILLINOIS

Only $4 million exclusion

E x c e p t i o n a l P e o p l e . I n n o v a t i v e I d e a s . S u c c e s s f u l C l i e n t s .

Questions?

Mike Fitzgerald, CPA

Office: 618.465.4288

www.schef felboyle.com