Indirect Taxes In India - RSM India publication (2012)

92

Astute Consulting Indirect Taxes In India - A Brief Insight

Transcript of Indirect Taxes In India - RSM India publication (2012)

Astute Consulting

Indirect Taxes In India- A Brief Insight

RSM Astute Consulting Group

Indian Member of RSM International

Personnel strength of about 900

Consistently ranked amongst India’s top 6 Accounting and Consulting groups(Source : International Accounting Bulletin - September 2010 and September 2011)

Nationwide presence

International delivery capabilities

RSM International

6th largest network of independentaccounting and consulting firms in the world

Annual combined fee income of US$ 3.9 billion

714 offices across 83 countries

www.astuteconsulting.com

Indirect Taxes In India A Brief Insight

| INDIRECT TAXES IN INDIAAstute Consulting

Contents

Contents

Chapter 1 : Indirect Taxes In India – An Overview 1

Chapter 2 : Central Excise Act 3

Chapter 3 : The Customs Act 19

Chapter 4 : Service Tax 37

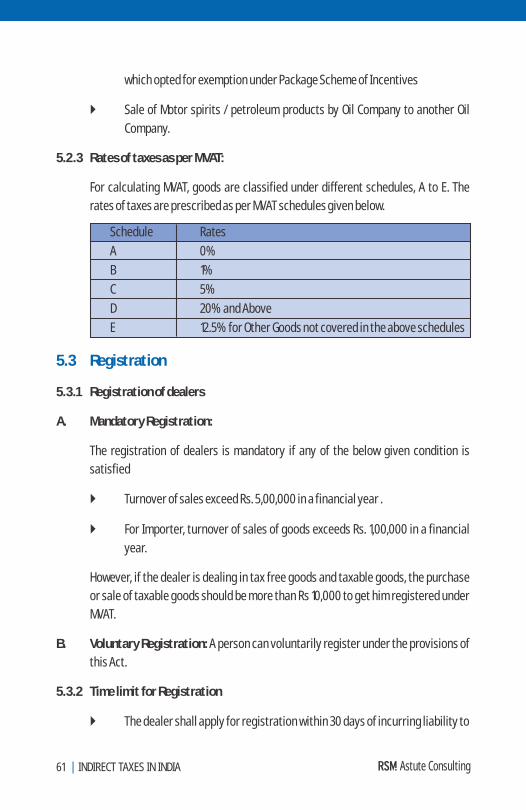

Chapter 5 : Maharashtra Value Added Tax 59

Chapter 6 : Central Sales Tax 73

Indirect Taxes In India A Brief Insight

| INDIRECT TAXES IN INDIAAstute Consulting

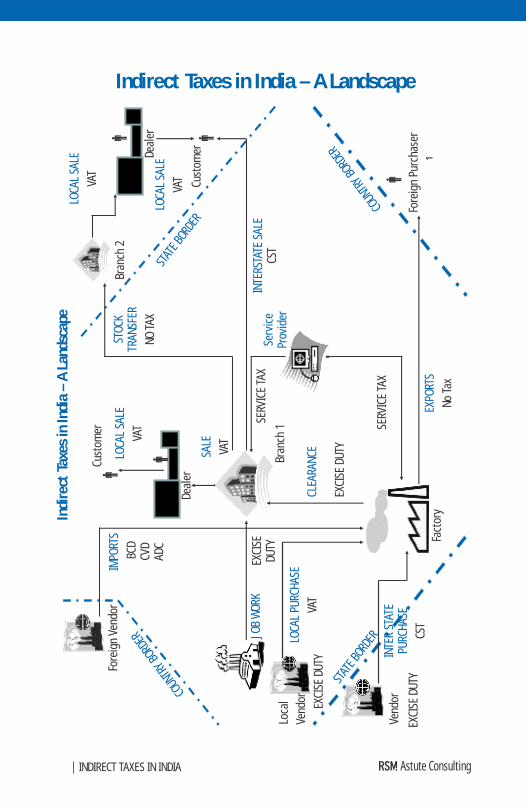

Indirect Taxes in India – A Landscape

1

€

€€ €

€

Indi

rect

Tax

es in

Indi

a –

A La

ndsc

ape

Fore

ign

Vend

or

COUN

TRY B

ORDE

R

IMPO

RTS

BCD

CVD

ADC

JOB

WOR

KEX

CISE

DU

TY

LOCA

L PU

RCHA

SE

VAT

EXCI

SE D

UTY

Loca

l

Vend

or

STAT

E BOR

DER

INTE

R ST

ATE

PURC

HASE

CST

Vend

or

Fact

ory

EXPO

RTS

No T

ax

SERV

ICE

TAX

SERV

ICE

TAX

Bran

ch 1

CLEA

RANC

E

EXCI

SE D

UTY

Deal

er

SALE

VAT

Cust

omer

LOCA

L SA

LE

VAT

Serv

ice

Prov

ider

STAT

E BOR

DER

COUN

TRY B

ORDE

R

Fore

ign

Purc

hase

r

Bran

ch 2

Deal

er

Cust

omer

LOCA

L SA

LE

VAT

STOC

KTR

ANSF

ER

NO T

AX

INTE

RSTA

TE S

ALE

CST

LOCA

L SA

LE

VAT

EXCI

SE D

UTY

| INDIRECT TAXES IN INDIA Astute Consulting

| INDIRECT TAXES IN INDIAAstute Consulting

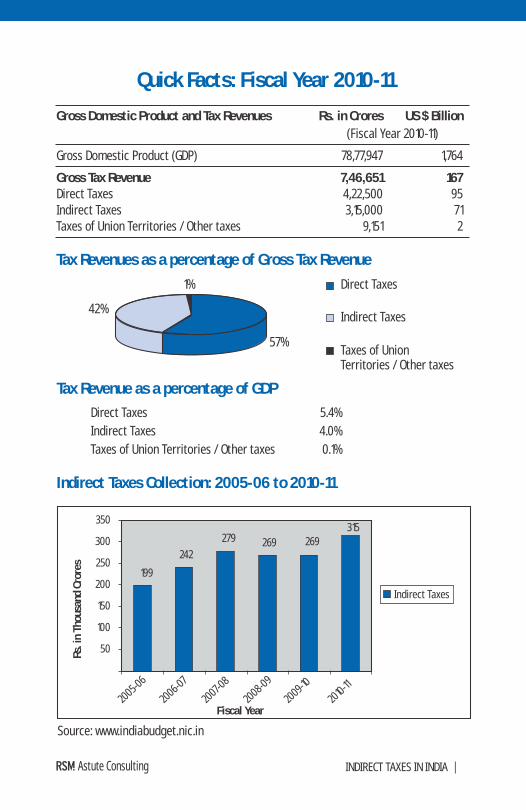

Quick Facts: Fiscal Year 2010-11

Fiscal Year20

05-06

2006-07

2007-0

8

2008-09

2009-10

2010-11

Rs. i

n Th

ousa

nd C

rore

s

Indirect Taxes

50

100

150

200

250

300

350

199

242

279 269 269315

Direct Taxes 5.4%Indirect Taxes 4.0%Taxes of Union Territories / Other taxes 0.1%

Indirect Taxes Collection: 2005-06 to 2010-11

Gross Domestic Product and Tax Revenues Rs. in Crores US $ Billion(Fiscal Year 2010-11)

Gross Domestic Product (GDP) 78,77,947 1,764

Gross Tax Revenue 7,46,651 167Direct Taxes 4,22,500 95 Indirect Taxes 3,15,000 71Taxes of Union Territories / Other taxes 9,151 2

Tax Revenues as a percentage of Gross Tax Revenue

Direct Taxes

Indirect Taxes

Taxes of UnionTerritories / Other taxes

42%

1%

57%

Tax Revenue as a percentage of GDP

Source: www.indiabudget.nic.in

Chapter 1Indirect Taxes In India - An Overview

1.1 Introduction

1.2 Meaning

1.3 Levy Of Indirect Taxes

The size of Indian economy is US $ 1.75 trillion in terms of Gross Domestic Product (GDP) and is growing at the real rate of 8%. The indirect taxes are one of the major sources of revenue with a Compound Annual Growth Rate (CAGR) of 16% and constitute significantly to the GDP of India.

The current structure of Indirect Taxes in India is complex with taxes levied by both the Central Government and the State Governments. The major taxes levied by Central Government are Excise Duty, Import Duty, Service Tax and Central Sales Tax (CST) while taxes levied by the State Governments are Value Added Tax (VAT), Luxury Tax, State Excise and other levies.

In this publication, we have tried to capture the snapshot of all the major indirect taxes applicable in India. Our aim is to create awareness among readers towards applicability of indirect taxes, indirect tax laws and various exemptions available. We have also brought out on the need for external review of indirect taxes in the organization.

Indirect taxes are the taxes which are levied on a product or a service, the incidence of which is borne by the person who ultimately consumes such product / service. The seller of goods or the supplier of services collects the tax by including the same in the selling price. Since indirect taxes get absorbed in the price of goods / services, the ultimate cost is borne by the final consumer, though the immediate liability falls on the seller.

Power to levy and collect taxes - direct as well as indirect, emerges from the Constitution of India. Article 246 of the Constitution of India gives authority to the Union and the States to levy taxes. Seventh Schedule to the Constitution of India contains lists which set out matters under which the State and the Union have authority to make laws.

Chapter 1: Indirect Taxes In India – An Overview

2 | INDIRECT TAXES IN INDIAAstute Consulting

Chapter 2Central Excise Act

4 | INDIRECT TAXES IN INDIAAstute Consulting

2.1 Background

Central Excise duty is an indirect tax, which is levied on excisable goods produced or manufactured in India. The power to levy Excise duty flows from Entry 84 of the Union List of the Constitution of India.

Central Excise or Central Value Added Tax (CENVAT) is essentially a charge on manufacture of excisable goods. Power to impose excise on alcoholic liquors, opium and narcotics is granted to States and it is called ‘State Excise.’

Central Excise Duty is imposed and levied through the various provisions contained in the Central Excise Act, 1944 and other related rules and regulations. It is administered by the Department of Revenue under the Ministry of Finance through the Central Board of Excise and Customs (‘CBEC’).

Some of the significant regulations which govern the Central Excise Levy are as under:

} Central Excise Act, 1944.

} The Central Excise Tariff Act, 1985 and related schedules

} Central Excise Rules, 2002

} Cenvat Credit Rules, 2004

} Central Excise Valuation (Determination of Price of Excisable Goods) Rules,

2000

} Central Excise (Removal of Goods at Concessional Rate of Duty for

Manufacture of Excisable Goods) Rules, 2001

} Central Excise (Determination of Retail Sale Price of Excisable Goods) Rules,

2008

} Other Rules such as Central Excise (Compounding of Offences) Rules, 2005,

Central Excise (Appeal) Rules, 2001, etc.

Chapter 2: Central Excise Act

5 | INDIRECT TAXES IN INDIA Astute Consulting

}

Central Excise is a duty on manufacture of excisable goods specified in the First Schedule and Second Schedule to the Central Excise Tariff Act, 1985 (CETA) which are produced or manufactured in India.

Central Excise Duty can be levied if the article is ‘goods’, it has come into existence as a result of ‘manufacture’ and such article is manufactured or produced in India.

Duty is levied as a certain percentage of the assessable value of the goods. The classification of goods and the rates of duty are specified in the First and Second Schedule to the CETA. First Schedule specifies the ‘Basic Rate’ of excise duty while the Second Schedule specifies the ‘Special Rate’ of excise duty. The classification of goods is based on ‘Harmonised System of Nomenclature’ (HSN) adopted by 130 countries worldwide for the purpose of international trade. The valuation of goods is dealt with in the forthcoming paragraphs.

As per the law ‘manufacture’ is inclusive of any process that is incidental or ancillary to the completion of the manufactured product or is an activity mentioned in the Section or Chapter notes of the First Schedule to the Central Excise Tariff Act, 1985 or are goods specified in the Third Schedule involving such activity as mentioned therein.

Excise law does not define goods as such. However, the law laid down by the Honourable Supreme Court in Delhi Cloth and General Mills Co. Ltd. Vs. U.O.I [(1977 (1) .L.T.(J. 199) (S.C.) (Constitutional Bench)], proves beyond doubt that in order to qualify as ‘goods’ an article must be known to the market as such. Though actual sale is not necessary, the product should be capable of being brought to the market for the purpose of sale.

According to explanation to section 2(d) inserted by Finance Act of 2008, ‘goods’ includes any article, material or substance which is capable of being bought and sold for a consideration and such goods shall be deemed to be marketable.

Notifications issued from to time to time.

2.2 Levy Of Duty

2.3 Manufacture

2.4 Goods

6 | INDIRECT TAXES IN INDIAAstute Consulting

2.5 Valuation

2.6 CENVAT Credit Scheme

The duty liability is determined as a certain percentage of the ‘value’ of the goods, and hence valuation of excisable goods assumes utmost importance. The modes of valuation of excisable goods are:

2.5.1 Specific duty: In case of certain excisable goods, excise duty is payable on the

basis of certain unit like length, weight, volume, etc. (e.g. in case of cigarettes, it is payable on the basis of length.)

2.5.2 Tariff value: The Central Government has declared tariff values in respect of

certain goods. The tariff value is a notional value and the duty of excise is calculated as a specified percentage of such notional value.

2.5.3 MRP value: The Government has notified certain goods on which excise duty is

payable as a percentage of the Maximum Retail Price (MRP) of the goods.

2.5.4 Transaction value: In respect of goods not covered above, the ‘transaction value’

is considered as the assessable value which is the value at which goods are sold by an assessee for delivery at the time and place of removal, where the assessee and the buyer are not related and price is the sole consideration.

Adoption of transaction value ensures that the sale is at arm’s length price, i.e. a price charged by a knowledgeable and willing seller to a knowledgeable and willing purchaser at an unbiased value.

2.5.5 Reference to Central Excise Valuation Rules, 2000: In case any of the above

conditions relating to transaction value are not fulfilled, the valuation of the goods is done by referring to Central Excise Valuation Rules (Valuation Rules.) Valuation rules provide for the adjustment to the actual sale price, so as to bring it in line or nearest to the ‘transaction value.’

2.6.1 CENVAT credit is a scheme, whereby the duty paid on inputs used in manufacturing the final goods is available for set-off from the duty payable on clearance of final goods. This eliminates the cascading effect of the duty levied on the final product. In effect, only the net value addition is taxed at each subsequent stage of manufacture.

CENVAT credit scheme (earlier known as Modvat credit) was introduced in 2004.

Today, CENVAT credit is available across goods and services, i.e. credit of excise

duty and service tax paid on inputs, capital goods and input services, is available to

be set off against the excise duty / service tax on output and output services.

The terms ‘capital goods’, ‘inputs’ and ‘input services’ are defined extensively

under the rules.

Broadly, the capital goods include machineries, mechanical appliances, boilers,

nuclear reactors and equipments of various types like optical / photographic /

cinematographic / medical and surgical instruments and parts thereof.

Inputs are the goods used directly or indirectly in the factory of the manufacturer

of final products. It also includes accessories which are cleared with the final

product.

Input service means a service used by a provider of taxable service for providing

an output service; or used by the manufacturer, whether directly or indirectly, in or

in relation to the manufacture of final products. It also includes services that are

used in relation to modernization, renovation or repairs of a factory premises of a

person providing service or an office relating to such factory or premises,

advertisement or sales promotion, market research, storage upto the place of

removal, procurement of inputs, activities relating to business - such as

accounting, auditing, financing, recruitment and quality control, coaching and

training, computer networking, credit rating, share registry and security,

transportation of inputs or capital goods and transportation charges incurred for

transporting goods after manufacture.

2.6.2 Availment of CENVAT credit:

Manufacturer of final goods or a provider of taxable services is eligible to avail

CENVAT credit of

} any input or capital goods received in the factory of manufacturer of final

product or in the premises of the provider of output service and

} any input service received by the manufacturer of final product or by the

provider of output service.

7 | INDIRECT TAXES IN INDIA Astute Consulting

8 | INDIRECT TAXES IN INDIAAstute Consulting

2.6.3 Conditions for availing CENVAT credit

} For Inputs: The CENVAT Credit in respect of inputs can be taken

immediately on receipt of the inputs in the factory of the manufacturer or in the premises of the provider of output service.

} For Input Services:

l CENVAT Credit in respect of input service shall be allowed, on or after the day on which the invoice, bill or challan, is received.

l In case the payment of the value of input service and the service tax is not made within 3 months of the date of the invoice, the manufacturer or the service provider who has taken credit on such input service shall pay an amount equal to the CENVAT credit availed on such input service. Thereafter, upon payment, the manufacturer or output service provider shall be entitled to take the credit of the amount equivalent to the CENVAT credit paid.

l If any payment or part thereof, made towards an input service is refunded or a credit note is received by the manufacturer or the service provider who has taken credit of such input service, he shall pay an amount equal to the CENVAT credit availed in respect of the amount so refunded or credited.

l Further, in case of an input service where the service tax is paid on reverse charge by the recipient of the service, the CENVAT credit in respect of such input service shall be allowed on or after the day on which payment is made of the value of input service and the service tax paid or payable as indicated in invoice.

} For Capital Goods

l Capital goods removed / cleared from the factory in the same

financial year: 100% of CENVAT credit can be availed in the same

financial year.

l Capital goods retained for more than one financial year:

– Maximum 50% of the CENVAT credit can be availed in the

9 | INDIRECT TAXES IN INDIA Astute Consulting

financial year of receipt of capital goods in the factory of the manufacturer and

– Balance in subsequent financial years

l CENVAT Credit of the additional duty leviable under sub-section (5) of section 3 of the Customs Tariff Act, in respect of capital goods shall be allowed immediately on receipt of the capital goods in the factory of the manufacturer.

l CENVAT Credit is not allowed on the amount of duty on capital goods, on which the manufacturer or provider of output service claims depreciation under section 32 of the Income – tax Act, 1961.

l CENVAT credit is available on capital goods acquired by manufacturer or service provider on lease, hire purchase or loan agreement, from a financing company.

l CENVAT Credit is allowed in respect of jigs, fixtures, moulds and dies sent by a manufacturer of final products to another manufacturer for the production of goods or to a job worker for the production of goods on his behalf according to his specifications.

2.6.4 Utilization of CENVAT Credit:

CENVAT Credit may generally be utilized for payment of certain specified duties / taxes which can be broadly classified into two categories:

} Any duty of excise on any final product.

} Service Tax on any output service.

CENVAT credit can utilized only to the extent such credit is available on the last day of the month / quarter, for payment of duty or tax relating to that month / quarter.

CENVAT credit cannot be generally utilized for payment of any duty of excise on goods in respect of which the benefit of an exemption is availed.

2.6.5 Types of duties on which CENVAT Credit is allowable

CENVAT Credit is allowed in respect of certain specified duties / taxes. Some of the

10 | INDIRECT TAXES IN INDIAAstute Consulting

significant specified duties include:

} The duty of excise specified in the First and Second Schedule to the CETA.

} Service Tax leviable under Service Tax Regulations.

} Education Cess and Secondary and Higher Education Cess on excisable

goods and taxable services.

} The additional duty leviable under Customs Law, which is equivalent to the

duty of excise as specified (commonly known as Countervailing Duty).

} The additional duty leviable under Customs Law (commonly known as

Special Additional Duty) which is in relation to VAT/ sales tax. It may be noted that the provider of taxable service is not eligible to avail Credit of such additional duty.

2.6.6 CENVAT Credit can be availed on certain specified documents (subject to conditions) including the following

} An invoice issued by the manufacturer for clearance of inputs or capital

goods.

} An Invoice issued by an Importer, from his depot or from the premises of

the consignment agent of the said importer if the said depot or the premises, as the case may be, is registered in terms of the provisions of Central Excise Rules, 2002.

} An Invoice issued by a first stage dealer or a second stage dealer under

Central Excise Law.

} A bill of entry.

} A challan evidencing payment of service tax.

} An invoice, a bill or challan issued by a provider of input service.

} An invoice, bill or challan issued by an input service distributor under the

provisions of Service Tax Law.

2.6.7 Rules where a manufacturer/ provider of output service avails CENVAT Credit in

11 | INDIRECT TAXES IN INDIA Astute Consulting

respect of any inputs / input services and manufactures final products / provides such output services which are chargeable to duty or tax as well as exempted goods or services.

The CENVAT Credit Rules provide for various options for claiming Cenvat Credit in case the manufacturer / provider of taxable output services manufactures final products / provides such output services which are chargeable to duty or tax as well as exempted goods or services.

} Option 1: Maintain separate inventory and accounts for receipt and use of

inputs and input services which are used for exempted goods / exempted services.

} Option 2: Pay an amount equal to 5% of value of exempted goods /

exempted services.

} Option 3: Pay an amount equal to proportionate CENVAT Credit attributable

to exempted final products / exempted output services as provided in the CENVAT Credit Rules.

} Option 4: Maintain separate records for inputs and pay amount (as

determined in accordance with the specific method prescribed) in respect of input services.

2.6.8 Transfer of Credit

} If a manufacturer of the final products shifts his factory to another site or

the factory is transferred on account of change in ownership or on account of sale, merger, amalgamation, lease or transfer of the factory to a joint venture with the specific provision for transfer of liabilities of such factory, then, the manufacturer is allowed to transfer the CENVAT Credit lying unutilized in his accounts to such transferred, sold, merged, leased or amalgamated factory.

} Similar provisions have been incorporated if the provider of output service

shifts or transfers his business.

} The transfer of the CENVAT Credit in respect of the above is allowed only if

the stock of inputs as such or in process, or the capital goods is also

12 | INDIRECT TAXES IN INDIAAstute Consulting

transferred along with the factory or business premises to the new site or ownership and the inputs or capital goods on which Credit has been availed are duly accounted for to the satisfaction of the Deputy / Assistant Commissioner of Central Excise.

2.6.9 Input Service Distributor

In the case of company, there may be some units which are not directly involved in the manufacture of goods or providing output service, e.g. Corporate Office. However, the corporate offices may be making payment of service tax for the input services received by them which are used in providing taxable services. In order to enable the units providing taxable services / manufacturing excisable goods to avail such credit of input services, the concept of input service distributor has been introduced in the Cenvat Credit Rules, 2004, wherein the corporate office can distribute the credit to its various units who provide taxable services / manufacture excisable goods.

The term 'Input Service Distributor' means generally an office of the manufacturer of final products or provider of output service, which receives invoices towards purchases of input services and thereafter issues invoice / challan for the purposes of distributing the credit of service tax paid on the said services to units providing taxable services / manufacturing excisable goods.

The Service Tax (Registration of Special Category of Persons) Rules, 2005 provide for the registration of input service distributor. Thus, in order to distribute the credit, the Input Service Distributor needs to obtain Service Tax Registration.

Manner of distribution of credit by input service distributor: The input service

distributor can distribute the CENVAT Credit in respect of the service tax paid on the input service to its manufacturing units or units providing output service, subject to the following conditions:

} The credit of the tax amount so distributed to various units shall not exceed

the total Service Tax amount contained in the original invoice/bill.

} Credit of service tax attributable to service used in a unit exclusively

engaged in manufacture of exempted goods or providing of exempted services shall not be distributed.

13 | INDIRECT TAXES IN INDIA Astute Consulting

2.6.10 Refund of CENVAT Credit

} Where any input or input service is used in the manufacture of final product

which is cleared for export under bond / letter of undertaking / used in the intermediate product cleared for export / used in providing output service which is exported, the CENVAT Credit in respect of input or input service so used can be utilized by the manufacturer / provider of output service towards payment of duty of excise on any final product cleared for home consumption / for export on payment of duty or service tax on output service.

} Further, where for any reason such adjustment is not possible, the

manufacturer / the provider of output service is allowed refund of such amount subject to certain conditions.

In order to provide an incentive to smaller industrial units, the Central Excise Law grants certain exemptions to units covered under the SSI scheme. For this purpose a manufacturing unit is considered as SSI unit if the total value of clearances of excisable goods for home consumption does not exceed Rs. 4 crore during the preceding financial year. Following is the brief summary of SSI exemption scheme.

} The scheme is governed by Notification 8/2003 dated 1 March 2003.

} The exemption is available only in respect of the goods which have been

specified in the said Notification No. 8/2003.

} The unit is not required to pay Excise duty till its clearances in a financial

year does not exceed Rs. 1.5 crores.

} The limit will be calculated by taking into account the clearances in respect

of one manufacturer from one or more factories or from one factory by one or more manufacturers.

} No CENVAT credit is available in respect of inputs upto the clearances of Rs.

1.5 crores in the financial year.

} Assessee can avail CENVAT credit on capital goods, however the same can

be utilized, once the limit of Rs. 1.5 crores is crossed.

2.7 Small Scale Industries (SSI)

14 | INDIRECT TAXES IN INDIAAstute Consulting

} Assessee has the option of not availing the benefit of this notification and

pay the normal rate of duty, by utilizing CENVAT credit. However, this needs to be intimated to the concerned authorities before removal of goods.

} Value of clearances to be excluded for the purpose of this scheme:

l Clearances of intermediate goods/goods captively consumed in case the final product is eligible for SSI exemption.

l Clearances, which are exempt from the whole of the excise duty leviable thereon.

l Clearances bearing the brand name or trade name of another person.

l Export clearances.

} The term 'job work' is defined under the CENVAT Credit Rules, 2004 and

Notification No. 214/86-CE dated 25 March 1996 to mean processing or working upon of raw material or semi-finished goods supplied to the job worker, so as to complete a part or whole of the process resulting in the manufacture or finishing of an article or any operation which is essential for aforesaid process.

} In case, the activities carried on by the job worker amount to manufacture,

the job worker would be liable to pay duty of excise on the goods so manufactured unless the supplier of the raw materials or semi-finished goods gives an undertaking to the Central Excise Authorities having jurisdiction over the factory of the job worker that the said goods shall be used in or in relation to the manufacture of the final products in his factory or removed on payment of duty from his factory or cleared for export, etc. as specified in the regulations.

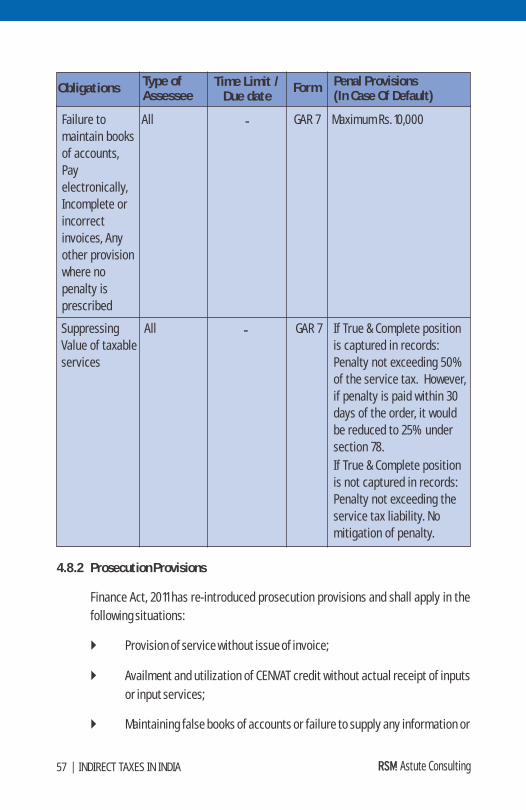

2.9.1 Registration

Some of the categories of persons who require Central Excise Registration include

2.8 Job Work

2.9 Procedural Aspects

15 | INDIRECT TAXES IN INDIA Astute Consulting

the following:

} Manufacturer of excisable goods on which excise duty is leviable.

} Person who desires to issue Cenvatable invoices under the CENVAT Credit

Rules, 2004.

} Persons holding warehouses for storing non-duty paid goods.

} Persons who obtain excisable goods for availing end use based exemption.

} Exporter-manufacturers under rebate/bond procedure; Export Oriented

Units, which have interaction with the domestic economy (through sales within India or procurement of duty free inputs).

2.9.2 Exemption from registration

Some of the categories of persons who are exempted from obtaining Central Excise Registration (subject to certain terms and conditions) include the following:

} Manufacturers of goods which are chargeable to 'nil' rate of duty or are

fully exempt.

} Every person (except certain specified), who gets his goods manufactured

on his account by others.

} Persons manufacturing excisable goods by following warehousing

procedure as required by or under the Customs Act, 1962.

} Person who carries on wholesale trade or deals with excisable goods

except first stage dealer or second stage dealer as defined in CENVAT Credit Rules, 2004.

} Small Scale Units availing the slab exemption based on value of clearances

under a notification.

2.9.3 Invoice System

} As per Rule 11 of the Central Excise Rules, 2002, excisable goods must be

removed from a factory or a warehouse under an invoice signed by the owner of the factory or his authorized agent.

16 | INDIRECT TAXES IN INDIAAstute Consulting

} The invoice should be issued in triplicate and must contain the particulars

set out in Rule 11.

} Before utilizing the invoice book, the serial numbers of the same must be

intimated to the jurisdictional Superintendent of Central Excise.

} The invoice needs to be prepared in triplicate in the following manner,

namely :

l the original copy being marked as ORIGINAL FOR BUYER

l the duplicate copy being marked as DUPLICATE FOR TRANSPORTER

l the triplicate copy being marked as TRIPLICATE FOR ASSESSEE

2.9.4 Filing of Returns

Every assessee is required to file return (depending upon the category of the assessee) in the form and time as specified. E.g.

th} A manufacturer is generally required to file Return in Form ER-1 by 10 day

of every month for removals during the previous month.

th} In the case of registered dealer, a quarterly return should be filed by 15

day of the month following the particular quarter.

} With effect from 1 October 2011, all assessees are mandatorily required to

file the returns electronically.

2.9.5 Excise Audit 2000 :

Excise Audit 2000 (EA) was initiated from 1 December 1999. The essential philosophy of EA 2000 is that this audit is based on the scrutiny of business records of the assessee.

The EA is a systematic form of audit wherein the auditors are required to gather basic information about the assessee and analyze them to find out vulnerable areas. At every stage the assessee is consulted thus making the entire audit process user friendly.

17 | INDIRECT TAXES IN INDIA Astute Consulting

2.9.6 Payment of Duty

The Excise Duty needs to be paid generally as under:

Type of Assessee Due date for payment

All (other than SSI) Generally 5 day of every month (for removals thduring the previous month) (6 day of every

month for e-payment) except March stFor March – By 31 March

th

Assessee availing or eligible to avail exemption based on value of clearance (SSIs)

Generally 5 day (6 day in the case of e-payment) of the month following the quarter except March.

stFor March - By 31 March.

th th

18 | INDIRECT TAXES IN INDIAAstute Consulting

Summary of Central Excise Provisions

When the activity amounts to manufacture

Transfer of Raw Materials to Job Worker

Registration under Central Excise regulations

Manufacturer

Purchase of Raw Material / Capital Goods / Input Services

(payment of Excise Duty / Service Tax)

Removal / Clearance of final products

Liability to pay Excise Duty

CENVAT Credit

Net payment of Excise Duty / Service Tax

Issue of Excise Invoice

Chapter 3Chapter 3: The Customs Act

3.1 Background

} Customs Act, 1962 - This is the main Act, which provides for levy and

collection of customs duty, import / export procedures, prohibitions on

importation and exportation of goods, penalties, offences, etc.

} Customs Tariff Act, 1975 (CTA) - The Act contains two schedules.

First Schedule gives classification and rate of duties for imports, while

Second Schedule gives classification and rates of duties for exports. In

addition, the CTA makes provisions for duties like additional duty (CVD),

preferential duty, anti-dumping duty, protective duties, etc.

3.1.1 Rules under Customs Act

} Customs Valuation Rules, 1988: For valuation of imported goods for

calculating duty payable;

} Customs and Central Excise Duties Drawback Rules, 1995: Prescribe

mode of calculating rates of duty drawback on exports;

} Baggage Rules, 1998: Rules and allowances for bringing in baggage from

abroad by Indians and tourists;

} Customs (Import of goods at concessional rate of duty for

manufacture of excisable goods) Rules, 1996: Prescribes the procedure

to be followed when goods are imported for export purposes;

} Other rules

3.1.2 Important definitions under Customs Act

Import: Import means bringing any goods into India from a place outside India. As

per Customs Act, 1962 India includes the installation, structure and vessels located in the continental shelf of India and exclusive zone of India, for the purpose of prospecting or extracting or production of mineral oil and natural gas and

Chapter 3: The Customs Act

20 | INDIRECT TAXES IN INDIAAstute Consulting

21 | INDIRECT TAXES IN INDIA Astute Consulting

supply thereof.

‘Goods’ under Customs Act: 'Goods' include

l vessels, aircrafts and vehicles

l stores

l baggage

l currency and negotiable instruments and

l any other kind of movable property.

Dutiable Goods: Dutiable goods are those goods which are chargeable to duty and on which duty has not been paid. Thus, goods continue to be 'dutiable' till they are not cleared from the port. However, once goods are assessed at 'Nil' rate of duty, they no more remain 'dutiable goods.'

Imported Goods: Imported goods are any goods brought into India from a place outside India, but do not include goods which have been cleared for home consumption. Thus, once goods are cleared by customs authorities from customs area, they are no longer ‘imported goods'.

Export Goods: Export goods mean any goods which are to be taken out of India to a place outside India. Goods brought near customs area for export purpose will be ‘export goods'.

3.2.1 Basic requirements to import goods

} Any body intending to import goods for commercial purpose has to submit an application to the Directorate General of Foreign Trade and obtain Importer and Exporter Code (IEC) number.

} In the case of 100% Export Oriented Units (EOUs) / Export Processing Zones (EPZs) the IEC number is allocated by the Development Commissioner of EPZ concerned. This number has to be indicated in the documents filed with the Customs for clearance of the imported goods.

} This number is not required in the case of import of gifts and baggage.

3.2 Procedure For Import Of Goods

22 | INDIRECT TAXES IN INDIAAstute Consulting

3.2.2 Restrictions on import of goods

Import of all items is freely permitted except few items which are mentioned as prohibited, restricted or canalized items in ITC (HS) classification. There is no need to obtain permission for importing goods which can be freely imported.

3.2.3 Import General Manifest (IGM)

Import General Manifest (IGM) is a document which is to be filed by the carriers of the goods with the Customs authorities before arrival / within 24 hours after arrival of vehicle carrying the imported goods. The ship is then granted entry inwards by the Customs authorities after which the goods can be unloaded in the port.

3.2.4 Bill of Entry

} Bill of entry can normally be filed to clear the goods after the IGM is

presented to the Customs Officers by the Steamer Agents / Airlines, as the case may be.

} If all the documents are available, the bill of entry can be presented 30 days

in advance and will be assessed and the duty will be paid, if any. Thus, as the goods land, they can be examined and the delivery taken without any loss of time and without paying demurrage charges.

3.2.5 Time limit to clear the imported goods

Imported goods should be cleared for home consumption or warehoused or transshipped within 30 days from the date of unloading the goods at a Customs station or within such extended time allowed by the proper officer.

3.2.6 Time limit allowed for paying duty on a Bill of Entry assessed to duty

Duty has to be paid within 5 days from the date on which the Bill of entry is returned after assessment to the importer / agent for payment of duty. Non payment of duty within the stipulated time attracts interest .

3.2.7 Foreign exchange rate applied to the value of invoice

} The rate of exchange applicable is the rate in force on the date on which a

Bill of entry (whether it is home consumption Bill of entry or Bill of entry for

23 | INDIRECT TAXES IN INDIA Astute Consulting

warehousing) is presented under Section 46 of the Customs Act, 1962.

} The same exchange rates are applicable to the Ex-bond bill of entry filed for

clearing the goods for home consumption form the bonded warehouse.

} The exchange rates are notified by the Central Government by issue of

notifications from time to time.

3.2.8 No duty payable if the title to the imported goods is relinquished

} The owner of any imported goods may relinquish his title to the goods at

any time before an order for clearance of goods for home consumption or an order permitting the deposit of the goods in the warehouse is passed.

} No duty would be payable if the title is relinquished by the importer.

} In case of warehoused goods, the owner of warehoused goods can

relinquish the title of goods any time before order for home clearance is made. No duty would be payable in such cases. However, the importer would be required to pay rent, interest, other charges and penalties that have been accrued.

3.2.9 Warehousing

If the importer does not want to use the entire stock immediately or he is not in the position to pay customs duty leviable on the goods, he can file into bond bill of entry for warehousing the goods. The normal warehousing period is 1 year except for 100 % Export Oriented Warehousing where warehousing period is 5 years for capital goods and 3 years for other goods.

3.2.10 Remission on lost / pilfered / damaged goods

} Remission on lost / pilfered goods: Section 23(1) of Customs Act provides

for remission of duty on imported goods lost (other than pilferage) or destroyed, if such loss or destruction is at any time before clearance for home consumption.

} Remission after goods are warehoused: Remission of duty on goods

warehoused is permissible under section 23, as goods cleared for warehousing are not ‘goods cleared for home consumption’.

24 | INDIRECT TAXES IN INDIAAstute Consulting

} Pilferage of Goods: Section 13 provides that duty on pilfered goods is not

payable if the imported goods are pilfered before order of clearance is

made.

} Duty on pilfered goods is payable by port authorities: Under section

45(3) if goods are pilfered after they are unloaded but before they are

cleared from the port, the customs duty is payable by port trust authorities

or airport authorities under whose custody the goods were lying.

} Abatement of duty on damaged goods: Section 22 provides for reduction

in duty if goods are damaged or deteriorated in any of the following cases:

l damaged before or during unloading in India

l damaged by accident after unloading but before examination of

goods for assessment by Customs Officer - provided that the

accident is not due to willful act, negligence or default of importer,

his employee or agent

l damaged by accident in warehouse before clearance of goods.

3.3.1 Nature of Customs Duty

Section 12 of Customs Act, often called charging section, provides that duties of

customs shall be levied at such rates as may be specified under ‘The Customs Tariff

Act, 1975’, or any other law for the time being in force, on goods imported into, or

exported from, India.

3.3.2 Taxable event for import duty

Goods become liable to import duty or export duty when there is 'import into, or

export from India'. Import of goods in India commences when they enter into

territorial waters but continues and is completed when the goods become part of

the mass of goods within the country. The taxable event is reached at the time

when the goods reach customs barrier and bill of entry for home consumption is

filed. In case of warehoused goods, the goods continue to be in customs bond.

Hence, 'import' takes place only when goods are cleared from the warehouse.

3.3 Levy, Classification And Rate Of Duty

25 | INDIRECT TAXES IN INDIA Astute Consulting

3.3.3 Types of Customs Duties

} Basic Customs Duty: The rate of customs duty applicable will be as

provided in Customs Act, subject to exemption notifications, if any, applicable. In case of imports from preferential area, the preferential rate is applicable, if mentioned in the Tariff. It is needless to mention that if partial or full exemption has been granted by a notification, the effective rate (as per notification) will apply and not the tariff rate (as mentioned in Customs Tariff). Normally, it is levied as a percentage of 'Value' as determined under section 14(1). The rates vary for different items, but general rate at present is 10%.

} Education Cess and Secondary and Higher Education Cess: It is

imposed on imported goods @ 2% and 1% respectively.

} Additional Customs Duty (CVD): This is often called ‘Countervailing Duty'

(CVD). Rate for CVD will be as mentioned in Central Excise Tariff Act, subject to any general exemption notification. It was observed that CVD is imposed when excisable articles are imported, in order to counter balance the excise duty, which is leviable on similar goods if manufactured within the State. If such goods are imported, duty will be payable on basis of MRP printed on the packing, i.e. at MRP specified on the packing carton less abatement as permissible under section 4A of Central Excise Act.

} Additional Duty of Customs: In addition to Additional Duty under section

3(1) of Customs Tariff Act; which is chargeable on all goods, further additional duty can be levied by Central Government to counter-balance excise duty leviable on raw materials, components, etc. similar to those used in production of such article.

} Safeguard duty and product specific safeguard duty on imports from

China: Central Government is empowered to impose 'safeguard duty' on

specified imported goods if Central Government is satisfied that the goods are being imported in large quantities and under such conditions that they are causing or threatening to cause serious injury to domestic industry.

} NCCD of Customs: A ‘National Calamity Contingent Duty’ (NCCD) of

customs has been imposed vide section 129 of Finance Act, 2001. NCCD of

26 | INDIRECT TAXES IN INDIAAstute Consulting

customs of 1% was imposed on PFY, motor cars, multi utility vehicles and two wheelers and NCCD @ Rs. 50 per ton was imposed on domestic crude oil, vide section 134 of Finance Act, 2003.

} Export duty: Export Duty is defined on few products.

} Protective Duties: Countervailing duty on subsidized goods and Anti

Dumping Duty on dumped articles.

3.3.4 Classification of Goods

The Classification of goods is as per Customs Tariff Act which is based on the internationally accepted HSN. Method of classification and the principles of classification are generally the same as per the Central Excise Law.

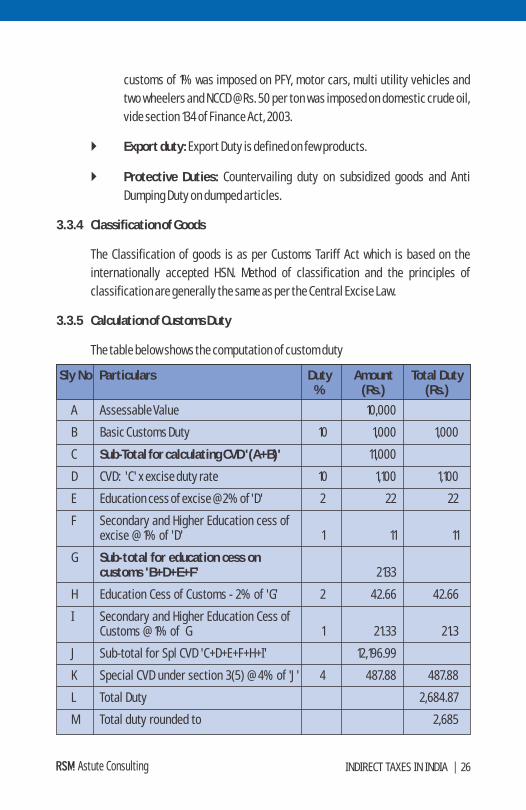

3.3.5 Calculation of Customs Duty

The table below shows the computation of custom duty

Sly No Particulars Duty Amount Total Duty % (Rs.) (Rs.)

A Assessable Value 10,000

B Basic Customs Duty 10 1,000 1,000

C Sub-Total for calculating CVD '(A+B)' 11,000

D CVD: 'C' x excise duty rate 10 1,100 1,100

E Education cess of excise @ 2% of 'D' 2 22 22

F Secondary and Higher Education cess of excise @ 1% of 'D' 1 11 11

G Sub-total for education cess on customs 'B+D+E+F' 2133

H Education Cess of Customs - 2% of 'G' 2 42.66 42.66

I Secondary and Higher Education Cess of Customs @ 1% of G 1 21.33 21.3

J Sub-total for Spl CVD 'C+D+E+F+H+I' 12,196.99

K Special CVD under section 3(5) @ 4% of 'J' 4 487.88 487.88

L Total Duty 2,684.87

M Total duty rounded to 2,685

27 | INDIRECT TAXES IN INDIA Astute Consulting

3.4 Valuation

3.4.1 Value for purpose of Customs Act

As per section 14 of the Customs Act, valuation needs to be done at transaction value.

Transaction value at the time and place of importation or exportation, when price

is sole consideration and buyer and sellers are unrelated is the basic criteria for ‘value’ under section 14 of Customs Act. Thus, CIF (Cost, Insurance and Freight) value in case of imports and FOB value in case of exports is relevant. However in the event the value cannot be arrived at in terms of section 14 of Customs Act, then Customs Valuation (Determination of Value of Imported Goods) Rules, 2007 would be applicable.

In case of high sea sale, price charged by importer to assessee would form the

assessable value and not the amount invoiced to the importer by foreign supplier.

3.4.2 Customs Valuation (Determination of Value of Imported Goods) Rules, 2007

The methods of valuation for imported goods are as follows

} Transaction Value of Imported goods [Section 14(1) and Rule 3(1)]

} Transaction Value of Identical Goods [Rule 4]

} Transaction Value of Similar Goods [Rule 5]

} Deductive Value which is based on identical or similar imported goods sold

in India [Rule 7]

} Computed value which is based on cost of manufacture of goods plus

profits [Rule 8]

} Residual method based on reasonable means and data available [Rule 9]

These methods are to be applied sequentially.

3.4.3 Export Goods - Valuation for Assessment

Customs value of export goods is to be determined under section 14 of Customs Act, read with Customs Valuation (Determination of Value of Export Goods), Rules

28 | INDIRECT TAXES IN INDIAAstute Consulting

2007. Transaction value at the time and place of exportation, when price is sole consideration and buyer and sellers are unrelated is the basic criteria. If there is no sale or buyer or sellers are related or price is not the sole consideration, value of the goods will be determined as per Valuation Rules.

3.5.1 ‘Self assessment procedure’ for clearance of imported goods

} According to this procedure the importers of repetitive imports can assess

their own Bills of Entry showing previous clearances and assessment of the same goods.

} The amount of duty payable is mentioned on the Bill of Entry. Physical

examination of imported goods will be done by using Risk Management Systems (RMS) on a computer based system.

3.5.2 Provisional Assessment

} When an importer or exporter is unable to produce any documents or

furnish any information necessary for assessment of duty on the imported or export goods, he may request for provisional assessment of the goods pending production of such documents and furnishing such information.

} Where the importer or the exporter has produced all the requisite

documents and furnished full information but the proper officer of customs may deem that it is necessary to make further enquiry for assessing the duty, he may resort to provisional assessment, pending such enquiry.

3.5.3 Exemption from duty

} Exemptions by Notification: Section 25 (1) of Customs Act, 1962

authorizes Central Government to issue notifications granting exemptions from duty.

} Imports by privileged persons and organizations: Import by U N

agencies, Governors, Ford Foundation, Vice President of India, specified equipment by foreign news agency, personal effects of deceased persons,gifts imported by CARE have been granted various exemptions. The

3.5 Assessment, Exemption, Demand And Refund Of Customs Duty

29 | INDIRECT TAXES IN INDIA Astute Consulting

diplomats (High Commissioner, Ambassadors, Consultant, General, etc) are allowed duty free import of goods for their personal use or official use.

} Import for repairs, reconditioning, etc.: Goods can be imported for

repairs, reconditioning or re-engineering. These have to be re-exported within 3 years of import. After imports, the repairs, reconditioning or re-engineering has to be done in a bonded warehouse under customs bond.

} Ad hoc exemptions: Section 25(2) of Customs Act empowers the Central

Government to issue ad-hoc exemption from customs duty by issue of a special order in exceptional circumstances.

} Exemptions of Imports for export: Various schemes have been formed to

allow duty free imports of raw materials and components for exports. These include schemes like FTZ, 100% EOU, STP, EHTP, Advance Licenses, etc. Import of materials for job work and return are also permitted.

} Project Imports: Heavy Customs duty on imported machinery for projects

make the initial project cost very high and project may become unviable. Hence, concept of ‘project Import’ has been introduced to bring machinery, etc. required for initial setup or substantial exemption at a concessional rate of customs duty. The goods are classified under heading 98.01 of the CTA though the machinery and its parts may actually fall under different tariff heading. The current rate of basic custom duty payable on project import is 5%.

3.5.4 Refund of Duty

Refund may be obtainable if customs duty was paid in excess while clearing the goods. Refund claim can be of customs duty and interest paid on such duty.

3.5.5 Time limit for filing refund claim

} Refund claim should be lodged within 1 year from the ‘relevant date.’

} This period is 1 year in case of imports made by individual for personal use

or by Government or by any educational, research or charitable institution.

} If duty was paid under protest, time limit of 1 year is not applicable. If duty

was paid on provisional basis, period of 1 year will be calculated from the

30 | INDIRECT TAXES IN INDIAAstute Consulting

date of adjustment of duty after final assessment.

3.5.6 Refund of Export duty

Export duty is charged on very few items but Customs Act also makes provisions for refund of export duty. Export duty is refundable if (a) Goods are re-imported within 1 year (b) the goods returned are not ‘re-sold’ and (c) refund claim is lodged within 6 months from date of clearance by customs officer for re-importation. This refund is not subject to provisions of unjust enrichment.

3.6.1 Preferential Area Exemption Notifications

Government has issued various notifications granting exemption of customs duties for importing specified goods from ‘preferential areas' like Singapore, ASEAN, SAFTA, etc. subject to the fulfillment of conditions pertaining to Rules of Origin. The certificate of origin is very important in order to avail of the benefits of such concessional rates of duty.

3.6.2 Duty Entitlement Pass Book (DEPB)

DEPB was basically an export incentive scheme and was very popular among exporters. The objective of DEPB scheme was to neutralize the incidence of basic custom duty on the import content of the exported products. However this scheme has been withdrawn since the same was not compliant with World Trade Organization Rules.

3.6.3 Duty Drawback

Here, the excise duty and customs duty paid on inputs is refunded to the exporter of finished product by way of ‘duty drawback’. If inputs are obtained without payment of customs/excise duty, no drawback will be paid. If customs/excise duty is paid on part of inputs or rebate/refund is obtained, only that part on which duty is paid and on which rebate/refund is not obtained will be eligible for drawback. Three types of Drawback Rates are prescribed - All Industry Rates for General Class, Brand Rate for special type of products and Special Brand Rate for a particular manufacturer if he finds that the actual duty paid on inputs is higher than All Industry Rate fixed for his product.

3.6 Various Benefits Under Customs Act, 1962

31 | INDIRECT TAXES IN INDIA Astute Consulting

3.6.4 Duty Free Import Authorizations (DFIA)

DFIA is issued to allow duty free import of inputs which are used in the

manufacture of the export products (making normal allowance for wastage), and

fuel, energy, catalyst, etc. which are consumed or utilized in the course of their use

to obtain the export product. DFIA is issued on the basis of inputs and export items

given under Standard Input and Output Norms (SION). Minimum value addition of

15% is required except for items in gems and jewellery section and other specified

items.

3.6.5 Deemed Exports

‘Deemed Exports’ means those transactions in which the goods supplied do not

leave the country and the payment for the supplies is received either in foreign

exchange or Indian Rupees. Deemed exporters are eligible for any of the following

benefits subject to specified terms and conditions.

l Advance License for intermediary supply of deemed export

l Deemed Export Drawback

l Refund of terminal excise duty

3.6.6 Agri Export Zones

Various importers that come under the Agri Export Zones are entitled to all the

import facilities and incentives.

3.6.7 Served from India

In order to create a powerful ’Served from India’ brand all over the world, the

Government has provided different type of import incentive to the invisible export

providers. Under the ‘Served from India’ Scheme, import incentive is given for

import of any capital goods, spares, office equipment and professional equipment.

It will cover duty free credit entitlement benefit @ 10% of total foreign exchange

earned, even for individual service providers who are able to earn total foreign

exchange of Rs. 5 lakhs or more in the preceding financial year and other service

providers who are able to earn total foreign exchange of Rs. 10 lakhs or more in the

preceding financial year or current financial year.

32 | INDIRECT TAXES IN INDIAAstute Consulting

3.6.8 Manufacture under Bond

In the ‘Manufacture under Bond’ Scheme, all factories registered to produce their

goods for export are exempted from import duty and other taxes on inputs, used to

manufacture such goods. As per this facility the manufacturer is allowed to import

goods without payment of customs duty. The production is made under the

supervision of customs or excise authority.

3.6.9 Export Promotion Capital Goods Scheme (EPCG)

EPCG is a special type of incentive given to the EPCG license holder. Capital goods

imported under EPCG Scheme are subject to actual user condition and the same

cannot be transferred / sold till the fulfillment of export obligation specified in the

license. Under Export Promotion Capital Goods (EPCG) scheme, a license holder

can import capital goods (including second hand) such as plant, machinery,

equipment, components and spare parts of the machinery at concessional rate of

customs duty of 3.09% and without CVD and special duty.

Zero Duty EPCG scheme: It is a liberalized version of EPCG scheme but with limited

validity upto 31 March 2011 and applicable to certain specified sectors.

3.7.1 High Sea Sale Transactions

} Imports through transfer of documents of title to goods before the goods

cross the customs frontier of India are popularly known as High Sea sales

(HSS).

} HSS is a sale carried out by the carrier document consignee to another

buyer while the goods are yet on high seas or after their dispatch from the

port / airport of origin and before their arrival at the port / airport of

destination.

} HSS contract / agreement should be signed after dispatch of goods from

origin and prior to their arrival at destination.

} In case of HSS, no sales tax is payable in case of transfer of documents of

goods since it is a sale in course of import.

3.7 General

33 | INDIRECT TAXES IN INDIA Astute Consulting

3.7.2 Accredited Clients Program for importer (ACP)

} With a view to reduce clearance time and lower the transaction costs, ACP

for the importer (with clean track record) has been introduced.

} The importers desirous of availing the facility are required to apply for

registration under ACP scheme.

} The main eligibility condition is that they should have imported goods of Rs.

10 Crores or paid Customs duty or Central excise duty of Rs. 1 Crore in the previous financial year.

3.7.3 Special Additional Duty (SAD) Refund

} Central Government exempts the goods falling within the First Schedule to

the CTA, when imported into India for subsequent sale, from the whole of the additional duty of customs leviable thereon under sub-section (5) of section 3 of the CTA subject to conditions as specified in the notifications.

} This refund provision is beneficial to import of trading goods by

manufacturer / trader.

3.7.4 Certain terms of pricing used in International Trade

} Ex-Work: Ex Works means that the seller is responsible to make the goods

available to the buyer at the Seller’s works or factory.

} Free on Board: The seller's responsibility ends the moment the contracted

goods are placed on board the ship or direct transport vehicle from the seller’s premises to the buyer’s premises.

} Cost and Freight (C & F): The seller must on his own risk and not as an

agent of the buyer, contract for carriage of the goods to the port of destination named in the sales contract and pay the freight .

} Cost, Insurance and Freight (CIF): In addition to C & F, insurance has to

be obtained by the seller.

3.7.5 Custom House Agent (CHA)

In order to assist importers and exporters, the services of Custom House Agents or

34 | INDIRECT TAXES IN INDIAAstute Consulting

clearing agents are available at international ports and airports. They are the persons who hold a valid license issued by the Commissioner of Customs under Customs Act, 1962 for clearing the goods.

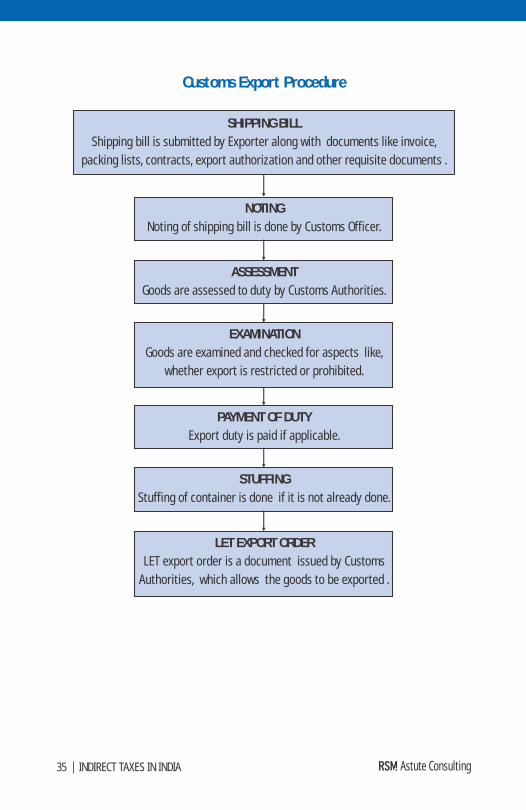

Customs Export Procedure

SHIPPING BILL

Shipping bill is submitted by Exporter along with documents like invoice, packing lists, contracts, export authorization and other requisite documents .

NOTING

Noting of shipping bill is done by Customs Officer.

ASSESSMENT

Goods are assessed to duty by Customs Authorities.

EXAMINATION

Goods are examined and checked for aspects like, whether export is restricted or prohibited.

PAYMENT OF DUTY

Export duty is paid if applicable.

STUFFING

Stuffing of container is done if it is not already done.

LET EXPORT ORDER

LET export order is a document issued by Customs Authorities, which allows the goods to be exported .

35 | INDIRECT TAXES IN INDIA Astute Consulting

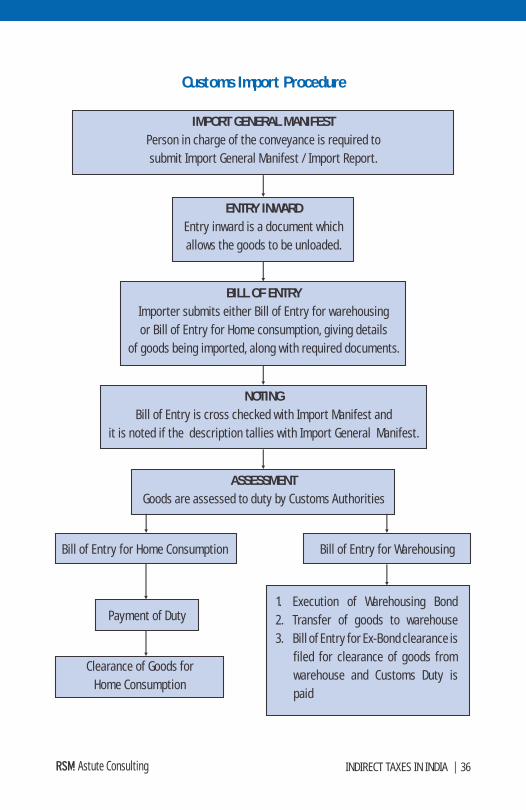

Customs Import Procedure

IMPORT GENERAL MANIFEST

Person in charge of the conveyance is required to submit Import General Manifest / Import Report.

ENTRY INWARD

Entry inward is a document which allows the goods to be unloaded.

BILL OF ENTRY

Importer submits either Bill of Entry for warehousing or Bill of Entry for Home consumption, giving details

of goods being imported, along with required documents.

NOTING

Bill of Entry is cross checked with Import Manifest and it is noted if the description tallies with Import General Manifest.

ASSESSMENT

Goods are assessed to duty by Customs Authorities

Bill of Entry for WarehousingBill of Entry for Home Consumption

Payment of Duty

Clearance of Goods for Home Consumption

1. Execution of Warehousing Bond2. Transfer of goods to warehouse3. Bill of Entry for Ex-Bond clearance is

filed for clearance of goods from warehouse and Customs Duty is paid

36 | INDIRECT TAXES IN INDIAAstute Consulting

Chapter 4Service Tax

4.1 Background

Service Tax was introduced in India in the year 1994. It is a tax on ‘services

rendered’ by one person to another. As an indirect tax, the final levy is borne by the

consumer of services, though the intermediate liability falls on the supplier.

Service tax is collected at each stage by the service provider by charging it to the

recipient of the service. Service Tax is applicable to all States in India except the

State of Jammu and Kashmir.

4.1.1 Constitutional validity

Article 265 of the Constitution of India lays down that no tax shall be levied or

collected except by the authority of law. Schedule VII to the Constitution of India

divides this subject into three categories:

a) Union list (only Central Government has power of legislation)

b) State list (only State Government has power of legislation)

c) Concurrent list (both Central and State Government can pass legislation).

To enable Parliament to formulate the law principles for determining the

modalities of levying the Service Tax by the Central Government and collection of

the proceeds thereof by the Central Government and the State, the amendment

vide Constitution (92nd amendment) Act, 2003 has been made. Consequently, new

article 268A has been inserted for Service Tax levy by Union Government,

collected and appropriated by the Union Government, and amendment of schedule

VII to the constitution, in list I-Union list after entry 92B, entry 92C has been

inserted for taxes on services as well as in article 270 of the constitution the clause

(1) article 268A has been included.

4.1.2 Administrative mechanism

Service Tax is administered by the Central Excise and Service tax Commissionerate

and the Service Tax Commissionerate working under the Central Board of Excise

and Customs, Department of Revenue, Ministry of Finance, Government of India.

38 | INDIRECT TAXES IN INDIAAstute Consulting

Chapter 4: Service Tax

They also collect Service Tax from the Large Tax paying units (LTU) registered with

them.

4.1.3 Statutes governing the taxation relating to Service Tax

l The Finance Act, 1994.

l The Service Tax Rules, 1994.

l The CENVAT Credit Rules, 2004.

l The Export of Service Rules, 2005.

l Point of Taxation Rules, 2011

l The Service Tax (Registration of Special categories of persons) Rules, 2005.

l The Taxation of Services (Provided from Outside India and Received in

India) Rules, 2006

l The Service Tax (Determination of Value) Rules, 2006

l Dispute Resolution Scheme Rules, 2008

l Service Tax Dispute Resolution Scheme, 2008

l Service Tax (Provisional Attachment of Property) Rules, 2008

l The Service Tax (Publication of Names) Rules, 2008

l Service Tax (Advance Rulings) Rules, 2003

l Authority for Advance Rulings (Central Excise, Customs and Service Tax)

Procedure Regulation, 2005

l Service Tax Return Preparer Scheme, 2009

l Works Contract (Composition Scheme for payment of Service Tax ) Rules,

2007

l Service Tax (Removal of Difficulty) Order, 2010

39 | INDIRECT TAXES IN INDIA Astute Consulting

4.2 Levy, Classification And Rate Of Service Tax

4.2.1 Liability to pay service tax

Generally, the ‘person’ who provides the taxable service is responsible for paying

Service Tax to the Government. Taxable Services have been specified under

Section 65(105) of the Finance Act, 1994 (the Act). Initially levy of Service Tax was

confined to 3 services in the organized sector, viz. Telephone, General Insurance

Services and Stock broking. Since then the Act has been amended year after year

and various services were brought into the tax net. Presently, there are around 120

categories of services liable to Service Tax including some of the prominent

services such as, Management Consultant, Banking and Other Financial Service,

Business Auxiliary Service, Maintenance or Management Service, Business

Support Service, Renting of Immovable Property Service, Works Contract Service,

Information Technology Software Service, Copyright Service, Restaurant Service,

etc.

However, in certain situations, the receiver of the services is responsible for the

payment of Service tax, e.g.

} Service provided or to be provided by a person from outside India and is

received by a person in India,

} For the services in relation to Insurance Auxiliary Service provided by an

Insurance Agent, the Service Tax is to be paid by any person carrying on the

general insurance business or the life insurance business, as the case may

be in India,

} For the taxable services provided by Goods Transport Agency, for transport

of goods by road, the person who pays or is liable to pay freight is liable to

pay Service Tax , if the consignor or the consignee falls under any of the

seven categories viz. (a) factory, (b) company, (c) corporation, (d) society,

(e) co-operative society (f) registered dealer of excisable goods, (g) body

corporate or a partnership firm,

} For the taxable services provided by Mutual Fund Distributors in relation to

distribution of Mutual Fund, the Service Tax is to be paid by the Mutual Fund

distributor or the Asset Management Company receiving such service,

40 | INDIRECT TAXES IN INDIAAstute Consulting

} Body corporate or firm located in India receiving sponsorship services.

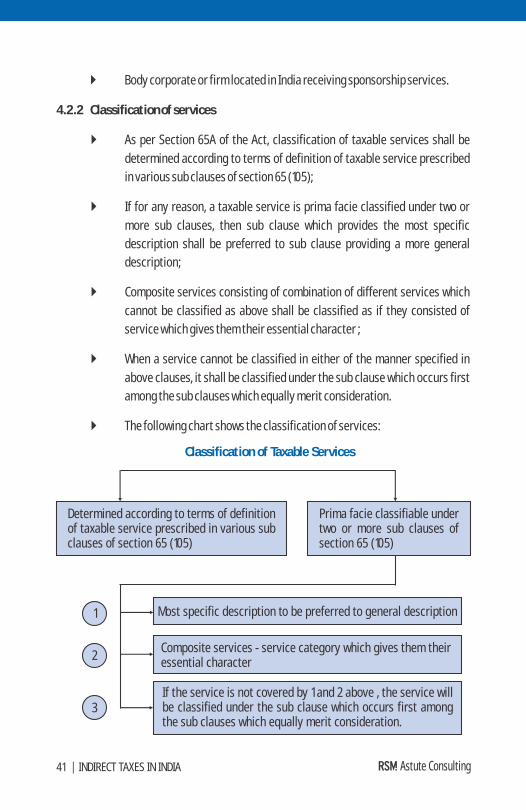

4.2.2 Classification of services

} As per Section 65A of the Act, classification of taxable services shall be

determined according to terms of definition of taxable service prescribed in various sub clauses of section 65 (105);

} If for any reason, a taxable service is prima facie classified under two or

more sub clauses, then sub clause which provides the most specific description shall be preferred to sub clause providing a more general description;

} Composite services consisting of combination of different services which

cannot be classified as above shall be classified as if they consisted of service which gives them their essential character ;

} When a service cannot be classified in either of the manner specified in

above clauses, it shall be classified under the sub clause which occurs first among the sub clauses which equally merit consideration.

} The following chart shows the classification of services:

41 | INDIRECT TAXES IN INDIA Astute Consulting

Classification of Taxable Services

Determined according to terms of definition of taxable service prescribed in various sub clauses of section 65 (105)

Prima facie classifiable under two or more sub clauses of section 65 (105)

Most specific description to be preferred to general description

Composite services - service category which gives them their essential character

If the service is not covered by 1 and 2 above , the service will be classified under the sub clause which occurs first among the sub clauses which equally merit consideration.

1

2

3

4.2.3 Rate of Service Tax

At present, the effective rate of Service Tax is 10.3% on the value of the taxable service. It comprises of Service Tax @ 10% payable on the ‘Gross Value of Taxable Service’, Education Cess @ 2% on the service tax amount, and Secondary and Higher Education Cess @ 1% on the Service Tax amount.

The above rate is subject to certain abatements as provided under various categories of taxable services (subject to certain conditions). E.g. Goods Transport Agency Services, Commercial or Industrial Construction Service, Restaurant Services, etc.

4.3.1 Every person liable to pay Service Tax must mandatorily obtain registration within prescribed time and manner. Central Government has notified following persons for the purpose of obtaining mandatory registration:

} Every person who has provided a taxable service of value exceeding Rs. 9

lakhs, i.e. Small Scale Service providers whose aggregate value of taxable services does not exceed Rs. 9 lakhs initially, are not liable to obtain Service Tax Registration.

} Recipient of service (In case a recipient is liable to pay service tax.)

} ‘Input Service Distributors’.

4.3.2 Time limit for registration

} When a person commences business of providing a taxable service, he is

required to register himself within 30 days from commencement of business.

} In case Service Tax levy is extended to a new service, an existing service

provider must register himself, unless he is eligible for exemption under any notification, within a period of 30 days from the date of new levy.

} Small Scale Service providers whose aggregate value of taxable services is

less than or equal to Rs. 10 lakhs during the previous financial year, must make an application for registration within a period of 30 days of the date

4.3 Registration

42 | INDIRECT TAXES IN INDIAAstute Consulting

of the financial year in which the aggregate value of taxable service has exceeded Rs. 9 lakhs.

} Recipient of the taxable services shall obtain registration within 30 days from the date of becoming liable to pay service tax.

4.3.3 Procedure for registration

A prospective Service Tax assessee (service provider or service receiver) or 'Input Service Distributor’ should file an application in Form ST-1 electronically at ACES wherein registration number is obtained immediately online. However, registration certificate in form ST-2 can be obtained after submitting certified / attested copies of the following documents to the jurisdictional Central Excise / Service Tax officer:

} Form - ST1 as e-filed along with acknowledgement of submission of the same.

} Permanent Account Number (‘PAN’) of the person / company.

} Residential Address proof of Directors / Proprietor/Partners/Authorized Person

} Power of Attorney / Board Resolution for appointing Authorized Signatory.

} Proof of constitution of the entity viz. Memorandum and Articles of Association along with Certificate of Incorporation or Partnership deed, etc.

} Address proof of the Company / Proprietary Business Premises.

‘ACES’ is abbreviated form of ‘Automation of Central Excise and Service Tax’. It is a Centralized, web based software application where Service Tax and Excise applications such as Registration, Returns, Refunds, ST-3A, Audit, Dispute Resolution can be done.

4.3.4 Issuance of Registration Certificate

The Registration certificate should be issued within a period of 7 days from the date of submission of application in form ST-1 along with all relevant details / documents. In case the registration certificate is not issued within 7 days, the

43 | INDIRECT TAXES IN INDIA Astute Consulting

registration applied for is deemed to have been granted provided the same is

complete and properly filled up.

4.3.5 Centralized registration

Service providers and service receivers having centralized accounting or

centralized billing system and located in one or more premises, may at their

option, register such premises or office from where centralized billing takes place

or centralized accounting systems are located and thus have centralized

registration.

4.3.6 Multiple services provided by an assessee

} Only one Registration certificate needs to be obtained if the person

provides multiple services from a single premise.

} However, while making application for registration, all taxable services

provided by the person should be mentioned, i.e. registration is needed for

each category of service.

4.3.7 Cessation of business of providing taxable service

The Service Tax Registration certificate (ST-2) should be surrendered

electronically to the respective Central Excise / Service Tax authorities

immediately on cessation of business. After surrender of the Registration

Certificate online, following documents need to be generally submitted for

cancellation of the certificate:

} Covering letter explaining the reasons for surrender, etc.

} Original Certificate of Registration (Form ST-2).

} Acknowledgements of Online surrender of the Form ST-2.

} Declaration in the specified format

} Last Half yearly returns filed.

4.3.8 Transfer of business to another person

In the event of transfer of the business, the transferee should obtain a fresh

44 | INDIRECT TAXES IN INDIAAstute Consulting

certificate of Service Tax registration based on his own PAN.

4.4.1 Value of taxable service

Service Tax is payable on the value of taxable services. The 'value of taxable service’ means, the gross amount charged by the service provider for the taxable service provided or to be provided by him. Taxable value has to be determined as per the provisions under Section 67 of the Finance Act, 1994, read with Service Tax (Determination of Value) Rules, 2006. For certain services, a specified percentage of abatement / exemption is allowed from the gross amount charged for rendering the services subject to the conditions prescribed under Service Tax Regulations.

4.4.2 Inclusion / Exclusion of certain expenditure or cost

} When certain expenditure or costs are incurred by the service provider in

the course of providing taxable services, all such expenditure or costs shall be treated as consideration for taxable service provided. It also includes reimbursement of ‘out of pocket expenses.’

} As per Rule 5 (2) of Service Tax (Determination of Value) Rules, 2006,

expenditure or cost that a service provider incurs, as pure agent of client shall be excluded from value if service provider fulfils certain specified conditions.

} Rule 6 provides for certain specific items for inclusion and exclusion in the

value of taxable services.

4.5.1 Returns

} The Service Tax return (Form ST – 3) is required to be filed by any person

liable to pay service tax.

} The Return is required to be filed twice in a financial year – on half yearly th stbasis. Return for half year ending 30 September and 31 March are

th threquired to be filed by 25 October and 25 April respectively. Input Service Distributor is required to furnish half yearly Service Tax Returns to

4.4 Valuation

4.5 Returns, Assessment, Records And Payment

45 | INDIRECT TAXES IN INDIA Astute Consulting

jurisdictional Superintendent of Central Excise by last day of the month following the half year period.

4.5.2 Revised Returns

An assessee may submit a revised return, in Form ST-3 to rectify a mistake or omission, within a period of 90 days from the date of submission of the original return in accordance with the Service Tax Rules, 1994 as amended.

4.5.3 E-filing of returns mandatory

With effect from 1 October 2011, all the assessees are mandatorily required to file the returns electronically.

4.5.4 Self Assessment

Generally, under Service Tax regulations the service taxpayer himself has to assess his tax liability due on the service provided and file a service tax return accordingly in the prescribed manner.

4.5.5 Provisional Assessment

If an assessee is unable to correctly estimate the actual amount payable as Service Tax for any particular month or quarter, as the case may be, he may make a request in writing to the Assistant / Deputy Commissioner of Service Tax / Central Excise as provided under Service Tax Rules, 1994, giving reasons for seeking payment of Service tax on provisional basis. On receipt of such request for provisional assessment, the authority may allow payment of Service Tax on provisional basis on such value of taxable service and subject to conditions as may be specified by him. Upon finalization of such assessment, if a liability of service tax arises, the differential amount along with interest has to be paid by the assessee. If he has paid excess amount he may claim refund.

4.5.6 Records

} The assessee is required to provide to the jurisdictional Superintendent of Central Excise / Service Tax at the time of filing the first return a list, in duplicate, of all the records maintained by the assessee for

l transactions in regard to providing of any service, whether taxable or exempted,

46 | INDIRECT TAXES IN INDIAAstute Consulting

l receipt or procurement of input services and payment for such

input services

l receipt, purchase, manufacture, storage, sale, or delivery, other

activities, such as manufacture and sale of goods and

l all other financial records maintained by him in the normal course

of business.

} Invoice / Bill / Challan

l Issue of Invoice / Bill / Challan by a Service Tax assessee is

mandatory as per Service Tax Rules. The same should be issued

within 14 days from the date of completion of taxable service or

receipt of payment towards the service, whichever is earlier.

l However, if the service is provided continuously for successive

periods of time and the value of such taxable service is determined

or payable periodically, the Invoice / Bill / Challan shall be issued

within 14 days from the last day of the said period.

} Contents of Invoice / Bill / Challan

l Serial number of the Invoice / Bill / Challan.

l Name, address and registration number of the service provider.

l Name and address of the service receiver.

l Description, classification and value of taxable service being

provided or to be provided.

l The amount of Service Tax payable (Service Tax and Education and

Secondary and Higher Education Cess should be shown separately).

It is mandatory to separately indicate the amount of Service Tax