Indirect Cost Rates & Cost Allocation Plans 6 Indirect Cost...Session 6: Indirect Costs Rates & Cost...

70

Indirect Cost Rates & Cost Allocation Plans APRIL 17, 2018 / SESSION 6

Transcript of Indirect Cost Rates & Cost Allocation Plans 6 Indirect Cost...Session 6: Indirect Costs Rates & Cost...

Indirect Cost Rates & Cost Allocation Plans

APRIL 17, 2018 / SESSION 6

Learning Objectives

• Distinguish between direct and indirect costs.

• Recognize changes to indirect costs.

• What are the types of indirect costs rate and base.

• Review considerations and deciding to obtain an indirect cost rate.

• Understand cost allocation process, plans and problems

2

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

A Few WordsThe Uniform Guidance

3

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

4

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

The Office of Management and Budget (OMB) merged eight previously separate OMB grant circulars into 2 CFR 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.

This document is a uniform grant guidance for all Nonfederal Entities and is commonly referred to by several names, the uniform guidance, super circular or omnibus circular.

There are going to be differences because there are different types of nonfederal entities (State and Local governments, nonprofit organizations, Indian Tribes and Institutions of higher educations).

Accordingly, differences are in the provisions for indirect costs.

5

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Reference documents for indirect cost and cost allocation plans are foundin 2CFR200, subpart A, for definitions, subpart D for post award issues,subpart E, cost principles and appendices III-VII, in addition to appendixVIII, which is a listing of nonprofit organizations that operate ascommercial, for-profit organizations and are treated accordingly (so theydo not used Appendix E as their cost principles – they use 48 CFR 31.2)and Appendix IX for hospitals.

Also reference, program law for restrictions that may prohibit indirectcost as an allowable cost or place limitations on the amount ofadministration maybe charged on the award or indirect limitations set bycaps.

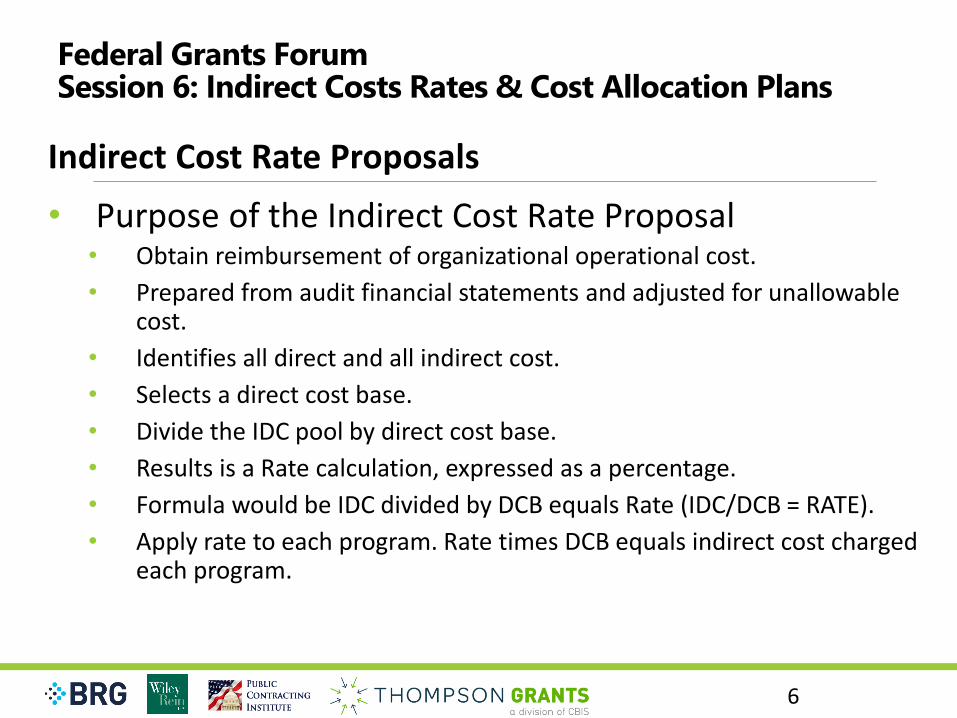

Indirect Cost Rate Proposals

• Purpose of the Indirect Cost Rate Proposal• Obtain reimbursement of organizational operational cost.

• Prepared from audit financial statements and adjusted for unallowable cost.

• Identifies all direct and all indirect cost.

• Selects a direct cost base.

• Divide the IDC pool by direct cost base.

• Results is a Rate calculation, expressed as a percentage.

• Formula would be IDC divided by DCB equals Rate (IDC/DCB = RATE).

• Apply rate to each program. Rate times DCB equals indirect cost charged each program.

6

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Complex Process

• Time consuming.

• Meticulous detail.

• Must do annual reconciliation by fiscal year.

• Requires knowledge and skills to develop and manage properly.

• Must list all direct and indirect costs.

• Many nonfederal entities forego the burdensome process.

• Then what are the alternatives?

7

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Learning Objective #1Distinguish between direct and indirect costs

(IDC)

8

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Definitions and Cost Principles

• Definitions in Subpart A• Differences between direct and indirect costs.

• Types of expenses.

• Cost principles in Subpart E• Indirect costs are based on cost principles.

• Allowable and unallowable costs.

9

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Direct Costs (§200.413)

• Direct costs are those costs that can be identified specifically with a particular final cost objective, meaning federal award, program or project. Some cost are straight forward and some are more difficult. Cost that specifically benefit the awards are charged to that award. Examples are those identified on SF-424a budget as direct cost. • Staff salaries.

• Materials and Supplies

• Equipment.

• Contractual.

• Travel AND Other direct cost.

10

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Indirect Costs (§200.56, 200.414 and Appendices III-IX)

• Indirect costs are costs for a common or joint purpose within a NFE and that benefit all program or project. Examples may include:• Payroll processing and accounting.

• Procurement & Property offices.

• Human Resources (HRM).

11

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Expenditures (§200.34)

• “Expenditures means charges made by a nonfederal entity to a project or program for which a federal award was received.”• Direct expenditures or costs.

• Indirect expenditures or costs.

• Administrative costs (direct or indirect, but not both).

12

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

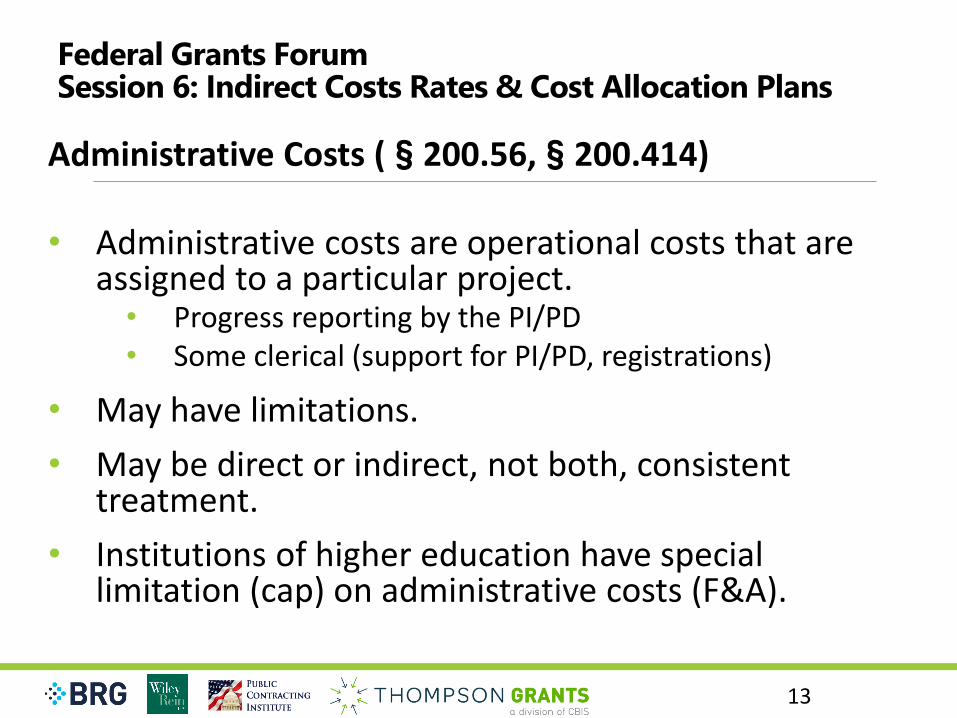

Administrative Costs (§200.56,§200.414)

• Administrative costs are operational costs that are assigned to a particular project.• Progress reporting by the PI/PD• Some clerical (support for PI/PD, registrations)

• May have limitations.

• May be direct or indirect, not both, consistent treatment.

• Institutions of higher education have special limitation (cap) on administrative costs (F&A).

13

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Modified Total Direct Costs (MTDC) (§200.68)

• MTDC means all direct salaries and wages, fringe benefits, materials and supplies, services, travel, and subawards and subcontracts up to the first $25,000.

• MTDC excludes equipment, capital expenditures, charges for patient care, rental costs, tuition remission, scholarships and fellowships, participant support costs and the portion of each subaward and subcontract in excess of $25,000.

14

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Rules for Determining the Difference (§200.412)

• There is no universal rule for classifying certain costs as either direct or indirect.

• Each item of cost should be treated consistently to avoid possible double-charging of federal awards.

15

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

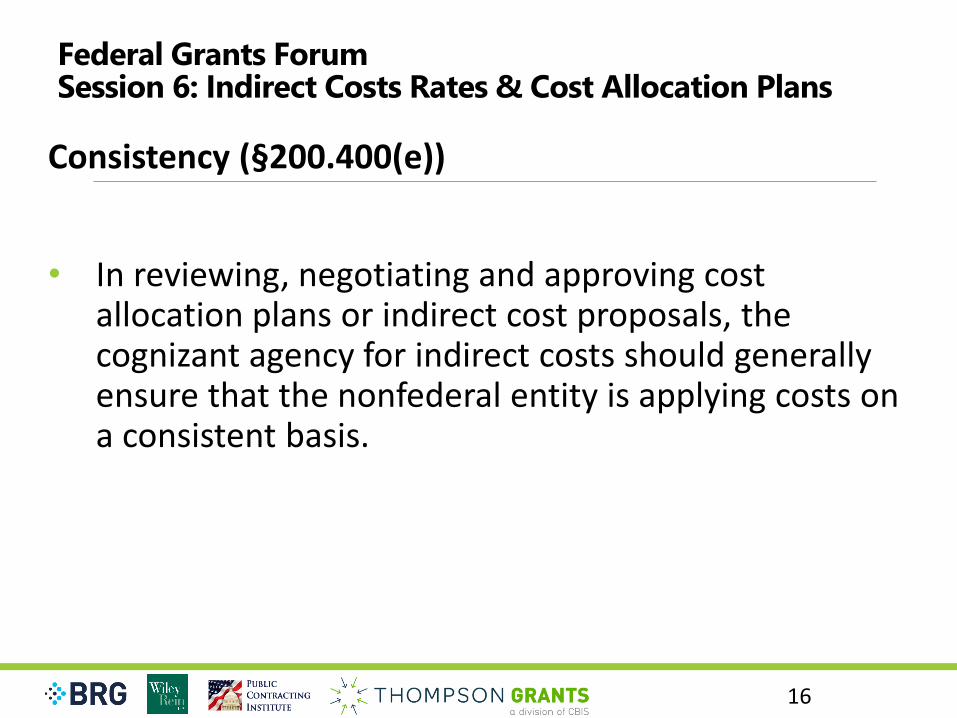

Consistency (§200.400(e))

• In reviewing, negotiating and approving cost allocation plans or indirect cost proposals, the cognizant agency for indirect costs should generally ensure that the nonfederal entity is applying costs on a consistent basis.

16

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

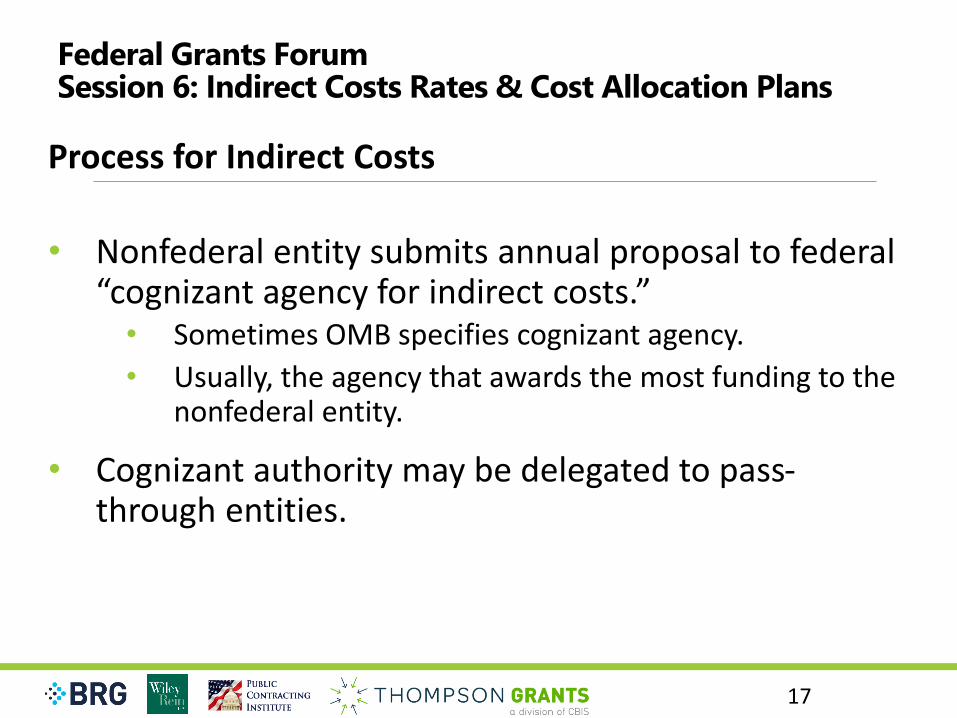

Process for Indirect Costs

• Nonfederal entity submits annual proposal to federal “cognizant agency for indirect costs.”• Sometimes OMB specifies cognizant agency.

• Usually, the agency that awards the most funding to the nonfederal entity.

• Cognizant authority may be delegated to pass-through entities.

17

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

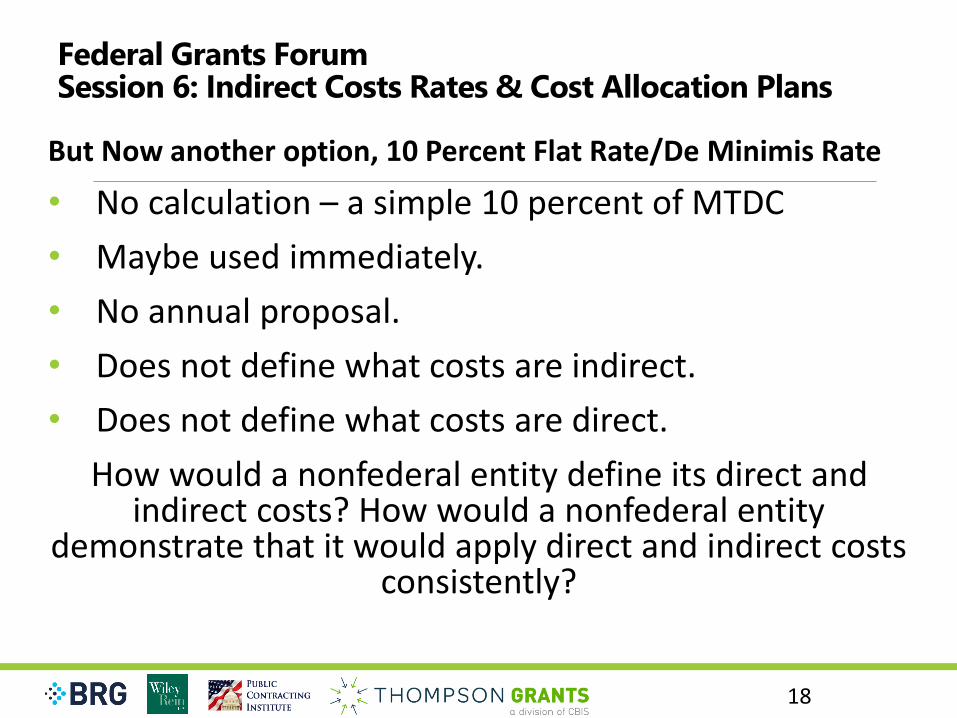

But Now another option, 10 Percent Flat Rate/De Minimis Rate

• No calculation – a simple 10 percent of MTDC

• Maybe used immediately.

• No annual proposal.

• Does not define what costs are indirect.

• Does not define what costs are direct.

How would a nonfederal entity define its direct and indirect costs? How would a nonfederal entity

demonstrate that it would apply direct and indirect costs consistently?

18

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

De Minimis Rate

• Written policy or certification.• To define costs as designated direct or indirect.

• To demonstrate consistent application of costs.

• To provide “reasonable assurance” (internal controls §200.303) that costs would not be double-charged as both direct and indirect.

19

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Learning Objective #2Recognize Changes to Indirect Costs

20

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Uniform Guidance

• There have been several notable changes to indirect costs from the prior OMB circulars to the uniform guidance.

• Indirect costs are mentioned 217 times and cost allocation plans 84 times in Subparts A - F and in the appendices.

21

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Acceptance of Rate (§200.414(c)(1))

• Federal agencies and pass-through entities must accept a nonfederal entity’s approved negotiated rate unless there is a program statute or approved agency regulation otherwise.

• The negotiated IDC agreement stands as agreed to and a federal agencies (FA) or pass-through entities (PTE) cannot restrict or deny any indirect costs.

22

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Pass-through Entities (§200.331)

• Pass-through entities must accept a subrecipient’s federally approved negotiated rate, or if there is no rate:• Negotiate an IDC rate for said subrecipient requesting,

or

• Allow the 10 percent de minimis rate to eligible subrecipients, never had an IDC rate.

23

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Extension of Rate (§200.414(g))

• A nonfederal entity that has a federally negotiated indirect cost rate may apply for an extension of a current final indirect cost rate for a period of up to four years.

• Renegotiated after extension period (four years).

• Requires prior written approval.

24

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Unrecovered Indirect Costs (§200.306(c))

• Unrecovered IDC results from expenses in the pool exceeding the revenue received from each program. An example is a NFE that spent $500K in IDC pool and received $450K from programs using the services. Rate % X DCB for each program equals money that goes to pay pool expenses.

• The deficit must be corrected (eliminated) and that is usually accomplished by bring revenue in line with expenses. Deficits are normally resolved from nonfederal funds (NFF) since this is not an allowable cost for federal awards. Each program is to pay its proportional share of nonfederal funds.

• Accordingly, a program that has nonfederal share requirements (matching or cost sharing) may have their nonfederal share IDC deficit used to satisfy program matching or cost share requirements, with the prior approval of their FA.

25

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Closeout and Adjustments (200.343, 344, 345)

• Submit final FFR SF-425 which contains both direct and indirect cost.

• Then after audit, submit an adjusted FFR in agreement with audited (SEFA) balances for each program.

• Obligations to return any funds due to later refunds, corrections or transactions including a final indirect cost rate adjustment.

• If collections are not paid in 90 days, federal claims act is to be engaged by FA or PTE and interest is to be charged on collection amounts at the prime rate.

26

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Certification (§200.415)

• To assure that expenditures are attested to as allowable cost.

• Signed by an official who is authorized to legally bind the nonfederal entity.

‘‘By signing this report, I certify to the best of my knowledge and belief that the report is true, complete, and accurate...I am aware that any false, fictitious, or fraudulent information, or the omission of any material fact, may subject me to criminal, civil or administrative penalties for fraud, false statements, false claims or otherwise. (U.S. Code Title 18, Section 1001 and Title 31, Sections 3729–3730 and 3801–3812).’’

27

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Learning Objective #3Different Indirect Cost Rates

28

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

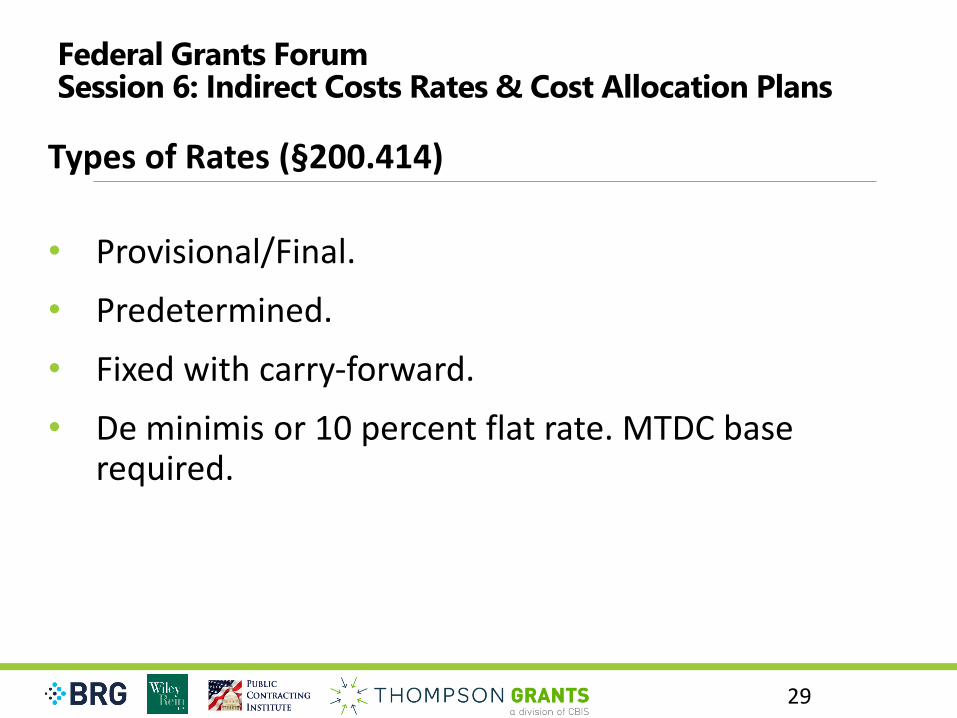

Types of Rates (§200.414)

• Provisional/Final.

• Predetermined.

• Fixed with carry-forward.

• De minimis or 10 percent flat rate. MTDC base required.

29

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Special Rate for IHE Facilities and Administrative .414

• Facilities and Administrative (F & A).

• Facilities address campus buildings and related cost i.e. property taxes, maintenance, insurance and etc.

• Administrative addresses general operational cost.

• Fringe benefits maybe be calculated through a type of indirect cost rate.

30

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

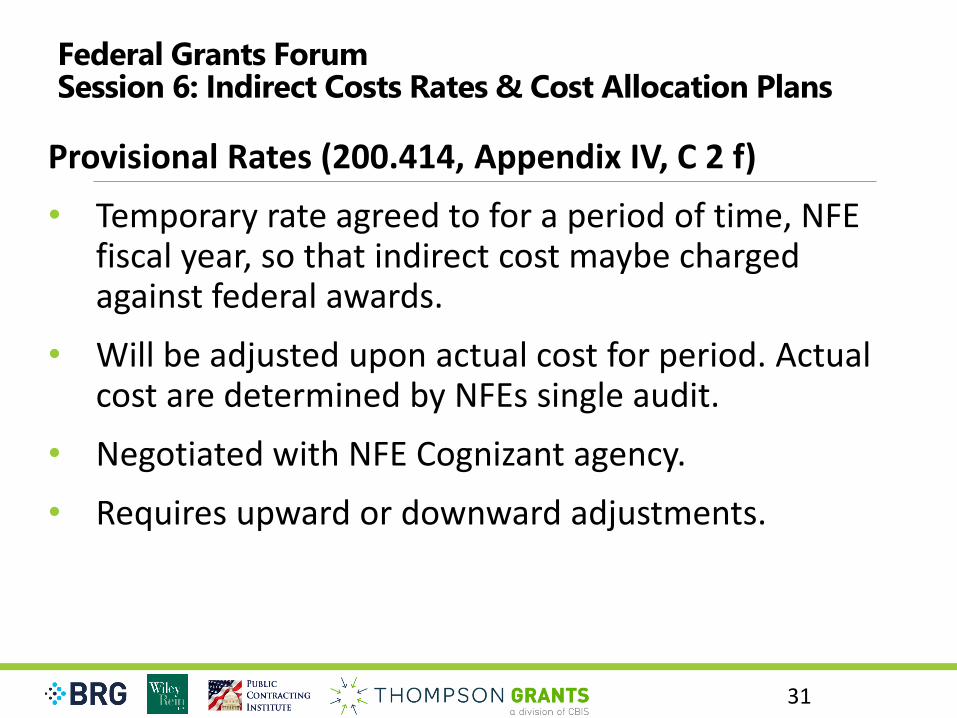

Provisional Rates (200.414, Appendix IV, C 2 f)

• Temporary rate agreed to for a period of time, NFE fiscal year, so that indirect cost maybe charged against federal awards.

• Will be adjusted upon actual cost for period. Actual cost are determined by NFEs single audit.

• Negotiated with NFE Cognizant agency.

• Requires upward or downward adjustments.

31

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

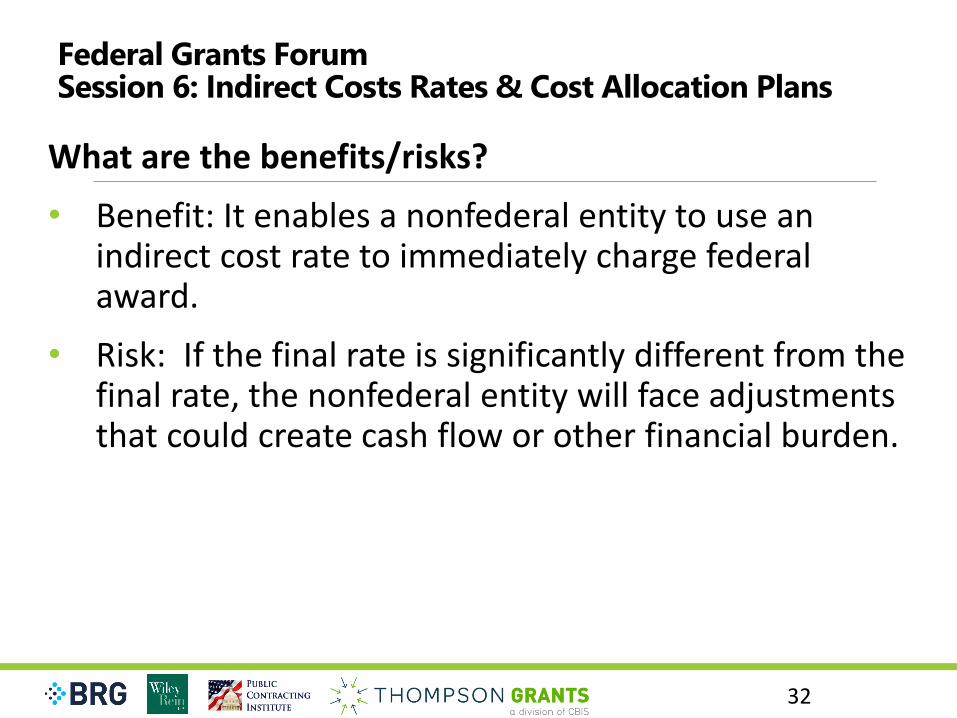

What are the benefits/risks?

• Benefit: It enables a nonfederal entity to use an indirect cost rate to immediately charge federal award.

• Risk: If the final rate is significantly different from the final rate, the nonfederal entity will face adjustments that could create cash flow or other financial burden.

32

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

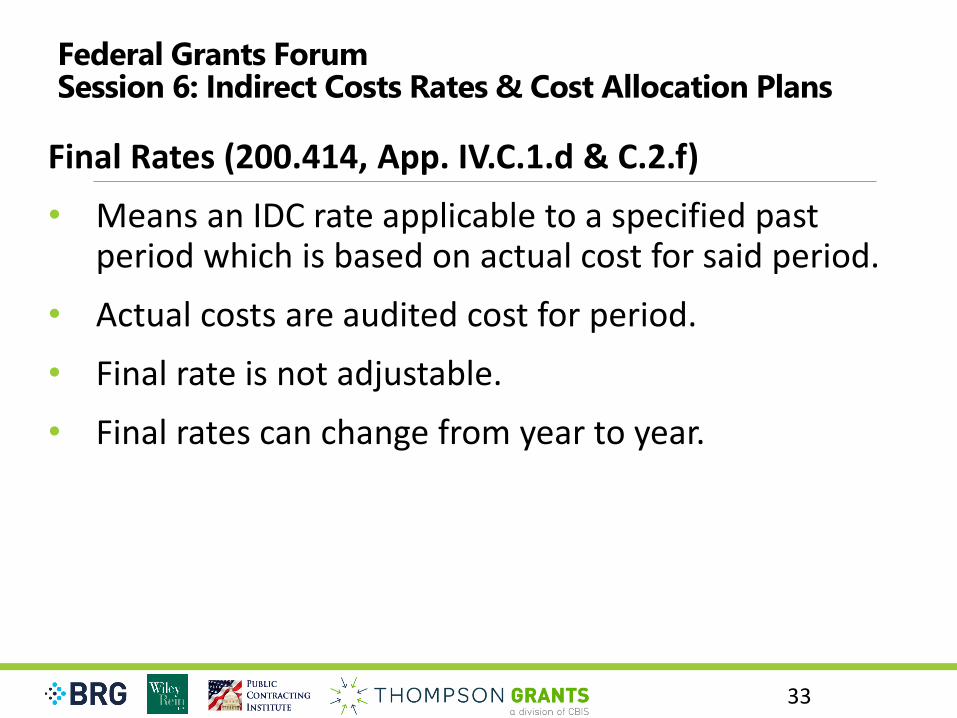

Final Rates (200.414, App. IV.C.1.d & C.2.f)

• Means an IDC rate applicable to a specified past period which is based on actual cost for said period.

• Actual costs are audited cost for period.

• Final rate is not adjustable.

• Final rates can change from year to year.

33

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Predetermined Rates (200.414, App. IV.C.1.b)

• Means an IDC rate applicable to a specific current or future period of time usually NFE fiscal year.

• Based on estimated costs.

• Best for stable recipients, organizational structure firm no changes, receive same level of funding each year with little fluctuation. Not subject to adjustment.

34

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Fixed Rate with Carry Forward (App. IV.C.1.c & C.2.e.)

• Same characteristics as a predetermined rate, except that differences between estimated and actual cost for the period.

• This difference is carried forward as an adjustment to the rate computation of a subsequent period.

• This rate allows the NFE to break even over a two year period.

• Cannot be extended four years (200.414(g)).

35

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

De Minimis (Flat Rate) of 10 Percent (§200.414(f))

• A nonfederal entity that has never received a negotiated indirect cost rate, except for those nonfederal entities described in Appendix VII, may elect to charge a de minimis rate of 10 percent of modified total direct costs (MTDC) which may be used indefinitely.

• Costs must be consistently charged as either indirect or direct costs, but may not be double-charged.

• No formal written policies have been developed by FAs. A NFE developing policies and procedures before implementing would be a best practice.

36

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Benefits:

• No complicated work papers, forms or negotiations which are usually timely.

• No negotiation needed. Declare, certify, FA or PTE approval and implement.

• May use indefinitely until the nonfederal entity chooses to negotiate a rate (200.414(f)).

37

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Risk:

• Must charge all programs 10% MTDC.

• Must develop own internal policies and procedures based on current FA IDC guidance.

• There are no previous models to operate from, nothing tested or success stories.

38

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Let your direct cost base (DCB) ensure an equitable distribution of IDC. Types of DCB:

• Salary and Wages – for NFEs that administer programs that are labor intensive.

• Salary and wages and fringe benefits – fringe benefits make a difference and programs are labor intensive.

• Total direct cost (TDC) – total of all cost categories (account) expenditures. For multiple types of programs.

• Modified total direct cost (MTDC) – total cost less distorting items and unallowable. For multiple types of programs.

39

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

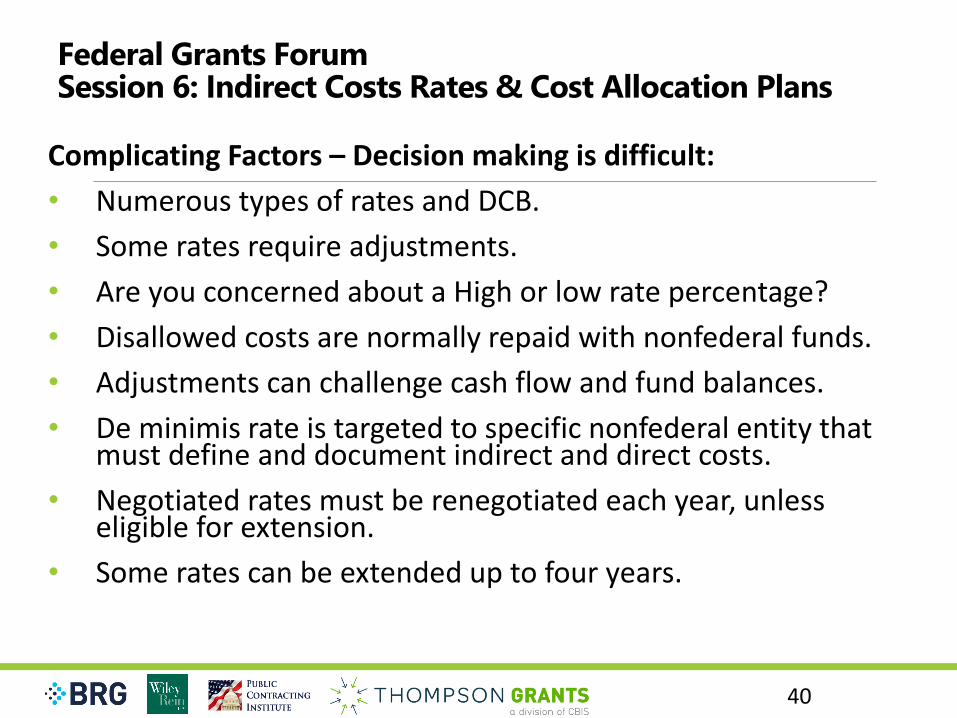

Complicating Factors – Decision making is difficult:

• Numerous types of rates and DCB.

• Some rates require adjustments.

• Are you concerned about a High or low rate percentage?

• Disallowed costs are normally repaid with nonfederal funds.

• Adjustments can challenge cash flow and fund balances.

• De minimis rate is targeted to specific nonfederal entity that must define and document indirect and direct costs.

• Negotiated rates must be renegotiated each year, unless eligible for extension.

• Some rates can be extended up to four years.

40

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Learning Objective #4Considerations for indirect cost rates

41

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

To Pursue or Not Pursue a Negotiated Indirect Cost Rate

• Takes time to prepare proposal.

• Requires knowledge and skills.

• Needs resources to prepare the proposal.

• Requires review and negotiation of the proposal.

• Often subject to audit findings.

• Requires written policy and procedures.

• Once approved, awarding agencies (FAs) must accept it unless there is a program statute or regulation otherwise.

42

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

To Charge or Not To Charge Indirect Costs

• If indirect costs are not charged, our alternative is to charge operational cost directly.

• Recipient program staff generally like direct costs, financial and administrators prefer IDC.

• Awarding agencies generally prefer indirect direct costs.

• Charging indirect costs shares or spreads operational financial cost within NFE programs.

43

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

To Charge or Not To Charge Indirect Costs

Unless there is a program statute or regulation to the contrary, it is the recipient organization’s choice to charge

indirect costs or waive some or all of its indirect costs.

44

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

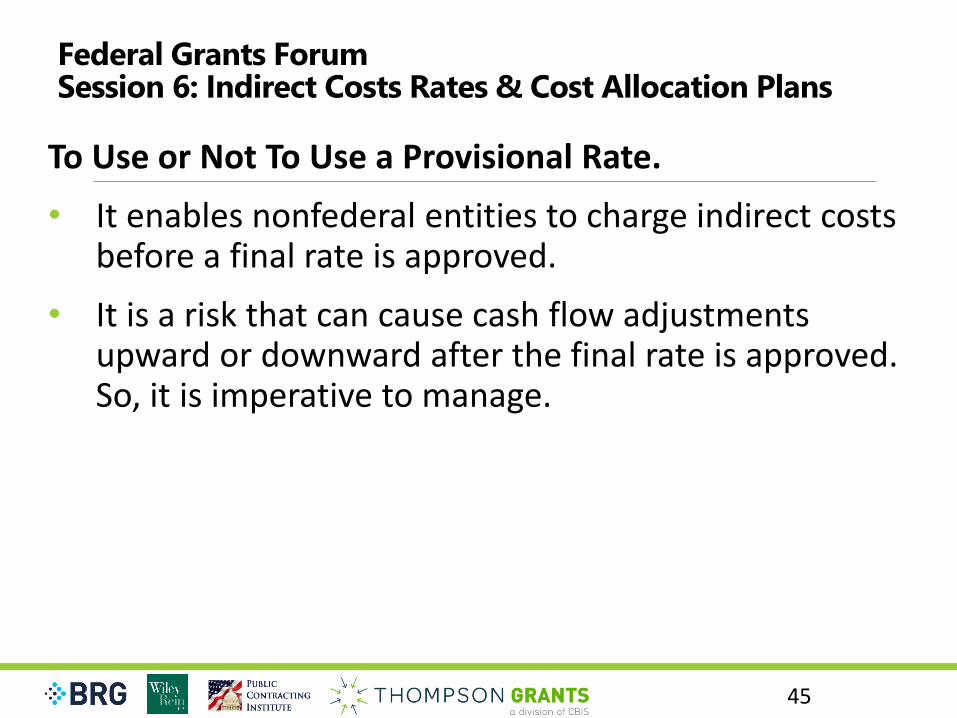

To Use or Not To Use a Provisional Rate.

• It enables nonfederal entities to charge indirect costs before a final rate is approved.

• It is a risk that can cause cash flow adjustments upward or downward after the final rate is approved. So, it is imperative to manage.

45

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

To Use or Not To Use the De Minimis Rate

• Must be eligible.

• Never had a negotiated rate.

• Under a certain threshold of awards.

• Based on MTDC which is the most challenging base to manage.

• All NFEs should understand allowable cost and have an accounting system to properly account for direct and indirect cost.

• Provide reasonable assurance that – no double dipping will occur!

• Create internal policy and procedures to manage.

46

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Learning Objective #5The cost allocation process

47

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Cost Allocation Plans

• Cost allocation plan means are central service cost allocation plan for state and local governments and Indian tribe.

• Central service cost (CSC) allocation plan means documentation identifying, accumulating and allocating or developing billing rates based on allowable cost of services provided by state or local governments or Indian tribes on a centralized basis to its departments and agencies. Costs for these services maybe billed or allocated. (200.9)

• Basically CSC are direct cost that are distributed to users by billing or allocating said services.

48

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

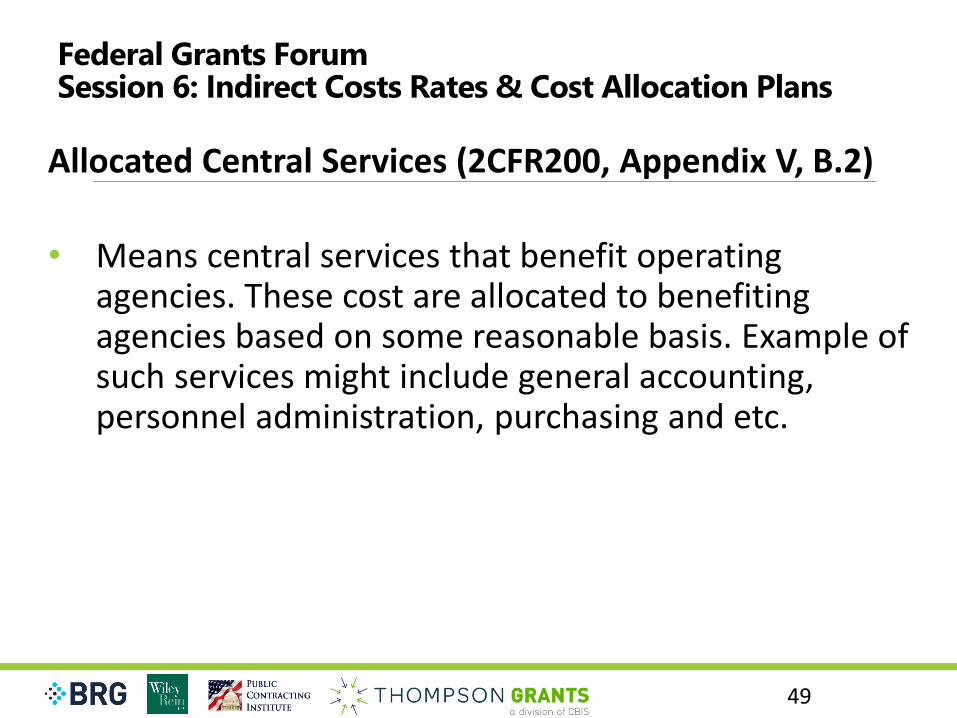

Allocated Central Services (2CFR200, Appendix V, B.2)

• Means central services that benefit operating agencies. These cost are allocated to benefiting agencies based on some reasonable basis. Example of such services might include general accounting, personnel administration, purchasing and etc.

49

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Billed Central Services (2CFR200, Appendix V, B.3)

• Means central services that are billed to benefiting agencies or programs on an individual fee-for-service or similar basis. Typical examples of billed central services include computer services, transportation services, insurance and fringe benefits.

50

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Cognizant Agency for Indirect Cost and Central Service Cost Allocation Plans (2CFR200, 200.19, Appendix V, B.4, and F.1)

• Example: HHS is responsible for Public assistance and state-wide cost allocation plans (SWCAP) for all states (including District of Columbia and Puerto Rico), state and local hospitals, libraries and heath districts.

• DOI is responsible for Indian Tribes, territorial governments, and state and local parks and recreational districts.

51

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Scope of Central Service Cost Allocation Plans (2CFR200, Appendix V, C)

• The central service cost allocation plan will include all central service costs that will be claimed, either as a billed or allocated cost) under a federal awards and will be documented as describes in section E. Cost omitted from the plan will not be reimbursed.

52

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Cost Allocation Plans and Indirect Cost proposals (200.416 (a))

• For states, local governments and Indian tribes that provide centralized or shared services to related operating agencies, there needs to be a process whereby these central service costs can be identified and assigned to benefiting users on a reasonable basis.

• Central services not charged as a direct cost may be included the calculation of the NFEs indirect cost proposal.

• Central service cost charged as a direct cost should not also be charged as an indirect cost.

53

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Major Local Governments (2CFR200, Appendix V, B.5)

• Means local government that receive more than $100 million in direct federal awards are subject to this part.

54

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Resource Document for State and local governments and Indian tribes (2CFR200, Appendix V, A.2)

• Brochure published by the Department of Health and Human Services (HHS) entitled, ‘‘A Guide for State, Local and Indian Tribal Governments: Cost Principles and Procedures for Developing Cost Allocation Plans and Indirect Cost Rates for Agreements with the Federal Government. ASMB C-10.

55

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Public assistance Cost Allocation Plan 2CFR200, Appendix VI

• Public Assistance Cost Allocation Plans

• Programs funded predominately by HHS.

• HHS published requirements under 45 C.F.R. Part 95.

• Requirements extended to all federal agencies whose programs are implemented by state public assistance agencies.

• Programs include Temporary Aid to Needy Families (TANF), Medicaid, Food Stamps, Child Support, Enforcement, Adoption Assistance and Foster Care, and Social Services Block Grant.

56

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Special Considerations (200.417)

• Interagency Service – Cost of services provided by one agency to another within the government unit may include allowable direct cost plus a pro-rated share of indirect cost.

57

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Allocation of Costs (2CFR200, Subpart E, 200.405)

• A cost allocation plan provides a process, similar to the process for indirect cost rate proposals, so that central service costs shared by agencies can be identified and assigned to indirect costs, as reasonable and appropriate.

• A key word is assigned or allocated based on the benefit of the users. Basis must be equitable distribution.

58

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Learning Objective #6Potential problems with cost allocation plans

59

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Reimbursements

• Costs of central services omitted from the plan will not be reimbursed.

• Costs must be allowable under 2CFR200, Subpart D, 200,403.

• Adjustments will be imposed for costs that are later determined to be improper or unallowable.

60

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Adjustments• Negotiated cost allocation plans later found to have included costs that:

(a) are unallowable by Federal Program law or by 2CFR200, Subpart D, 200.403. As well as conditions in the selected items of costs or by the terms and conditions of the award, must be adjusted, or a refund must be made at the option of the cognizant agency for indirect costs.

• Like disallowed costs, adjustments could create a financial burden for the nonfederal entity since repayment is from nonfederal funds of the NFE.

• Adjustments are generally considered a debt owed and can be remedied by cash refunds, offsets, and or credits at the option of the cognizant agency for indirect costs.

• There may be interest charged, if applicable, by the cognizant agency for indirect costs.

• Adjustments could affect the indirect cost rate or cost allocation plan, as unallowable cost will reduce from the CAP.

61

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Collections of Amounts Due (200.345(a))

• Require cash back, and/or.

• Require administrative offset.

• Applied against subsequent request for reimbursement.

• Or other action permitted by federal statute.

62

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Applicable Credits (200.406, 200.436, 200.468)

• Applicable credits, under the uniform guidance, refers to receipts or reduction of federal expenditures, including:

• Allowances, insurance refunds, discounts, rebates, refunds, adjustments of overpayments or erroneous charges, depreciation, specialized service facilities.

• Adjustments to applicable credits, if any, must be credited to the federal award, either as a cash refund or a cost reduction, as appropriate.

63

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Accounting System

• The accounting systems for all recipients and subrecipients must meet the standards in 2CFR200, Subpart D, financial management, 200.302. This will ensure that federal funds are properly accounted for and are not commingled with funds from other federal awards or other sources.

64

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Learning Objective #7Recognize changes to cost allocation plans

65

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Common Audit Findings

• Time and effort reporting.

• Improper documentation.

• Inadequate accounting system.

• Lack of written policies and procedures.

• Allocation basis improper.

• Unallowable cost charged to direct and indirect cost.

• Lack of internal controls.

• Indirect cost charged as direct.

• Subrecipients not monitored by PTE.

66

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Allowable Costs

• Ensure that costs included in the cost allocation plan are allowable based on Subpart E, 200.403, factors affecting allowability cost. There are nine criteria plus in practice we include following state and local law.

• Hospitals follow 45 C.F.R. Part 75, appendix IX.

• Commercial, for-profit eligible subrecipients follow, 48 CFR 31.2/

67

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Time and Effort

• Ensure that costs for time and effort included in the cost allocation plan are based on the actual time spent on federal award and not budgetary amounts.

• Personnel Activity Reports (PARs) are not required but may be used to support time charged, as well as time and effort reports.

68

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Written Business Management Systems should be developed:

Financial Management Policies and Procedures

• Ensure written procedures for determining allowable cost are monitored and updated in accordance changes and new provisions as they occur in 2CFR200.

• Other policies and procedures include: personnel, procurement, property and travel.

69

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans

Questions?

70

Federal Grants ForumSession 6: Indirect Costs Rates & Cost Allocation Plans