INDIA’S UNION BUDGET: CHANGING SCOPE AND THE … Rajeev Malhotra.pdf · 252 SCIENCE AND CULTURE,...

22

252 SCIENCE AND CULTURE, JULY-AUGUST, 2011 INDIA’S UNION BUDGET: CHANGING SCOPE AND THE EVOLVING CONTENT* RAJEEV MALHOTRA** The paper reflects on the changing scope of the Union Budget and the Finance Minister’s speech and assesses the evolving content of these policy instruments in recent years. The analysis undertaken is based on a framework highlighting some inter-related objectives that government budget serves in public policy making. These objectives include the use of budget as a tool for implementing fiscal policy, as an accountability tool for government functioning, a planning tool to operationalise a multi-year plan perspective and as a tool for anchoring policy coherence and coordination. The paper identifies some assessment criteria implicit in these objectives for assessing the budget content and its preparatory process. It suggests several measures and some pending reforms in fiscal policy and the underlying budget processes to address the identified objectives more effectively and makes a case for speeding up their implementation. ARTICLE * Reprinted from Research and Information System (RIS) for Developing Countries, Discussion Paper # 171 (2010). ** The author is a civil servant, on a sabbatical from the Department of Economic Affairs, Ministry of Finance, Government of India and was associated with Research and Information System for Developing Countries, New Delhi, when this paper was written. The author can be contacted at [email protected]. Introduction O n the Indian economic policy canvas, the Union Budget, in general, and the Finance Minister’s budget speech, in particular, has a unique relevance. As a policy event, the attention it receives stands out in comparison to other domestic policy announcements and the routine presentation of government budgets in the developed world or even in the emerging economies. In part, this is due to the nature of the Indian economy, where development process until well into 1990s has been largely state-dependent, driven predominantly by the public sector and where discretion in respect of tax and expenditure policies enjoyed by the government of the day have been amenable to influences exerted by different interest groups. Indeed, multiplicity of tax rates, the constant lobbing for tinkering those tax rates and the demand for expanding tax exemptions, though contributing to avoidable policy risks in the medium term, have been relentlessly pursued by investors and rent seeking business houses and entrepreneurs. As a result, the Union Budget has acquired unusual importance and there is significant hype, led by the media looking for sound bytes, in the days leading up to its presentation in Parliament. Fortunately, this aspect of the budget is gradually changing. With the launch of the economic reforms in 1991, the policy thrust has been on creating a stable and liberal fiscal policy regime based on moderate tax rates. Moreover, this trend is set to be further reinforced with the implementation of the proposals on the Direct Tax Code (DTC) and the Goods and Service Tax (GST) in the near future. There is another reason because of which the Union Budget and the Finance Minister’s budget speech has become an important economic policy event in the country. It relates to the limited public involvement and the nature of discussions on economic issues within and outside Parliament. One has to just recall the debate on inflation

Transcript of INDIA’S UNION BUDGET: CHANGING SCOPE AND THE … Rajeev Malhotra.pdf · 252 SCIENCE AND CULTURE,...

252 SCIENCE AND CULTURE, JULY-AUGUST, 2011

INDIA’S UNION BUDGET:CHANGING SCOPE AND THE EVOLVING CONTENT*

RAJEEV MALHOTRA**

The paper reflects on the changing scope of the Union Budget and the Finance Minister’s speechand assesses the evolving content of these policy instruments in recent years. The analysisundertaken is based on a framework highlighting some inter-related objectives that governmentbudget serves in public policy making. These objectives include the use of budget as a tool forimplementing fiscal policy, as an accountability tool for government functioning, a planning toolto operationalise a multi-year plan perspective and as a tool for anchoring policy coherence andcoordination. The paper identifies some assessment criteria implicit in these objectives for assessingthe budget content and its preparatory process. It suggests several measures and some pendingreforms in fiscal policy and the underlying budget processes to address the identified objectivesmore effectively and makes a case for speeding up their implementation.

ARTICLE

* Reprinted from Research and Information System (RIS) forDeveloping Countries, Discussion Paper # 171 (2010).

** The author is a civil servant, on a sabbatical from theDepartment of Economic Affairs, Ministry of Finance,Government of India and was associated with Research andInformation System for Developing Countries, New Delhi,when this paper was written. The author can be contacted [email protected].

Introduction

On the Indian economic policy canvas, the UnionBudget, in general, and the Finance Minister’sbudget speech, in particular, has a unique

relevance. As a policy event, the attention it receives standsout in comparison to other domestic policy announcementsand the routine presentation of government budgets inthe developed world or even in the emerging economies.In part, this is due to the nature of the Indian economy,where development process until well into 1990s has beenlargely state-dependent, driven predominantly by the publicsector and where discretion in respect of tax andexpenditure policies enjoyed by the government of theday have been amenable to influences exerted by differentinterest groups. Indeed, multiplicity of tax rates, the

constant lobbing for tinkering those tax rates and thedemand for expanding tax exemptions, though contributingto avoidable policy risks in the medium term, have beenrelentlessly pursued by investors and rent seekingbusiness houses and entrepreneurs. As a result, the UnionBudget has acquired unusual importance and there issignificant hype, led by the media looking for sound bytes,in the days leading up to its presentation in Parliament.

Fortunately, this aspect of the budget is graduallychanging. With the launch of the economic reforms in 1991,the policy thrust has been on creating a stable and liberalfiscal policy regime based on moderate tax rates. Moreover,this trend is set to be further reinforced with theimplementation of the proposals on the Direct Tax Code(DTC) and the Goods and Service Tax (GST) in the nearfuture.

There is another reason because of which the UnionBudget and the Finance Minister’s budget speech hasbecome an important economic policy event in the country.It relates to the limited public involvement and the natureof discussions on economic issues within and outsideParliament. One has to just recall the debate on inflation

VOL. 77, NOS. 7–8 253

in Parliament in the last two years, especially in the lowerhouse, to recognise this. While the engagement on topicaleconomic issues is perhaps at its best during the budgetsession of Parliament, in general the quality of discussionsby political parties on economic and development policyissues leaves much to be desired. There is paucity ofprofessional talent in Parliament and inadequate expertisein the secretariat supporting various ParliamentaryCommittees that are tasked to examine the demand forgrants (budget proposals) of various ministries. A relatedfactor that contributes to the quality of public debates isthe near absence of institutionalised backstopping andresearch capacity in the mainstream political parties tosupport and lend credence to their political agendas. Thishandicaps the quality of their engagement on economicpolicy issues.

The Union Budget and its attendant process has notonly reckoned with these realities of public policy makingin India, but over the last two decades has become animportant instrument of policy change and implementationof economic reforms in the country.

In this context, a question that begs an answer is -has the Union Budget and the Finance Minister’s budgetspeech evolved sufficiently in its scope and content inrecent years to respond to the changing domestic andinternational economic policy context? This issue meritsconsideration from another perspective also. Given thattax reforms, currently being contemplated, covering thedirect and indirect taxes are likely to be in place in thecourse of the coming year or two, a large portion of thespace in the budget speech would be available foraddressing issues that require fundamental changes inpolicy content, coordination, institutions or procedures.Should the Budget speech be an instrument to concertand present these measures? Perhaps, the answer is yes.Some issues that need be considered in this context arediscussed in what follows.

The paper reflects on the changing scope of theUnion Budget and the Finance Minister’s speech andassesses the evolving content of these instruments. Itmakes a case for speeding up progress in this regard andadvocates for an early implementation of some of thepending reforms in fiscal policy and the underlying budgetprocesses. The analysis is organised in five sections. Thefirst section, following the introduction, briefly lays downa framework that highlights the objectives that agovernment budget serves in public policy making andbrings out the assessment criteria implicit in thoseobjectives for assessing the budget content and itspreparatory process. The subsequent four sections analyse

India’s Union budgetary developments in the last fewyears, particularly since 2003-04, with respect to theidentified objectives and the corresponding criteria anddiscuss the gaps that remain to be addressed. Theconcluding section brings together some of thesuggestions that emerge from this analysis.

I. Budget Imperatives and Criteria forAssessment

Typically, a budget for a household or an organisationis a statement of accounts reflecting the flow of receiptsand expenditure on different ends. However, for agovernment the budget is much more. It is an instrumentthat reflects the operational content of government policiesfor now and signals the policies to come in future. Thedetails on annual revenue and public expenditure captureonly a part of those policy priorities. With developmentand economic reforms, the focus of economic activity hasdecidedly shifted towards the non-governmental actors,not all of whom are directly affected by the allocations tovarious public programmes and activities. For them theUnion Budget is important for its implications on theeconomy, including the macroeconomic parameters that setthe tenor of expectations on growth and inflation for theinvestors as well as the consumers. Potentially, the budget(including Finance Minister’s speech) by presenting acoordinated policy framework that goes beyond fiscalmeasures, on one hand, and the means to bring aboutsome coherence and convergence of public and privateeconomic activities towards common development goals,on the other hand, is a vital instrument for conductingpublic policy.

A government budget serves some interrelatedobjectives, which help in operationalising public policy andimplementing the consequent programme of action. Theseobjectives include:

budget as a fiscal tool to align governmentspending with its revenues and ensuringmacroeconomic balance, thereby creating anenvironment for economic stability, growth anddevelopment sustainability;

budget as an accountability tool to lay down theframework for monitoring and regulating publicexpenditure in accordance with (budgeted)allocations and revenues;

budget as a planning tool to operationalise a multi-year plan perspective by providing resources formeeting expenditure on activities in accordancewith plan objectives and targets. By prioritising

254 SCIENCE AND CULTURE, JULY-AUGUST, 2011

development activities and effecting allocation ofresources among competing ends, in keeping withpolitical manifesto of the ruling party, the budgetis also an important political tool for thegovernment and the opposition parties in thelegislature;1 and

budget as an anchorage for policy coherence andcoordination to address macroeconomic concernsand challenges with multifaceted, cross-sectoraland economy wide implications.

From these objectives that a government budget isexpected to address, one could identify several criteria toassess the budget process. For example, as a principaltool for conducting fiscal policy in an economy, the budgetmeasures could be assessed for promoting growth (orprivate economic activity), equity (inter-personal, inter-regional and inter-generational), economic stability (impacton inflation and macroeconomic parameters) or thesustainability of the fiscal policy, which would includeassessing the relative role of tax and expenditure policiesin meeting these objectives. Similarly, as a tool forpromoting accountability of public expenditure andgovernment’s power to mobilise revenues, it is importantfor the budget proposals (documentation) and the budgetprocess to be accessible, transparent, non-discretionary(non-discriminatory), participatory (reflecting stakeholderinterests) and result (outcome) oriented.2 Adherence tothese principles not only helps in making the publicauthorities accountable both ex ante and ex poste, butalso contributes to realising other objectives of publicpolicy, including those related to priority setting (planning)and policy coherence. Therefore, criterion based on theseprinciples could be used to assess budget developmentsover a period of time.

In recent years, there have been several deliberate,but apparently isolated changes in practices and policiesthat have influenced the Union Budget process, thepresentation of data related to the budget and itssubstantive content. Let us assess how some of thesechanges measure up to the criteria that are embedded inthe objectives that government budgets are meant toaddress. At the same time, identify areas where furtheraction is needed in making this instrument more effectiveand comprehensive in its scope to tackle domestic andglobal economic policy imperatives.

II. Fiscal Policy and the Budget

The enactment of the Fiscal Responsibility andBudget Management Act (FRBMA) 2003 gave a new

mandate to government budgets and lent credibility to thefiscal reforms process. It created an institutional frameworkfor conducting prudent fiscal policy and contribute topublic accountability by promoting inter-generational equityin fiscal management and ensuring long-termmacroeconomic stability. It sought to achieve this bycreating sufficient revenue surplus, removing fiscalimpediments in the effective conduct of monetary policyand encouraging prudent debt management through limitson borrowings and deficits. The Rules framed to implementthe FRBMA in 2004 not only made explicit annual reductiontargets in the revenue and fiscal deficits, management ofcontingent and total liabilities (domestic and external debt),but also the requirement for a macroeconomic frameworkand the medium term fiscal policy and strategy statements.The Rules also made it mandatory for the CentralGovernment to disclose any changes in accountingstandards, policies and practices that had a bearing onthe fiscal indicators. This requirement of statutory annualfiscal targets guiding the preparation of successivebudgets, while integrating the annual budgets, helped inplacing the fiscal policy in a medium term perspective.

The gradual liberalisation of the interest rates in theeconomy, the decision (reflected in the FRBMA 2003) tonot borrow from the Reserve Bank of India (RBI), exceptby way of advances to meet temporary excess of cashdisbursements over cash receipts and the RBI ceasing tosubscribe to the primary issue of Central Governmentsecurities (discontinuing the use of quantitative easing asa policy tool) from 1 April 2006, contributed to policyindependence of the monetary authority while enforcingprudence in the conduct of fiscal policy.

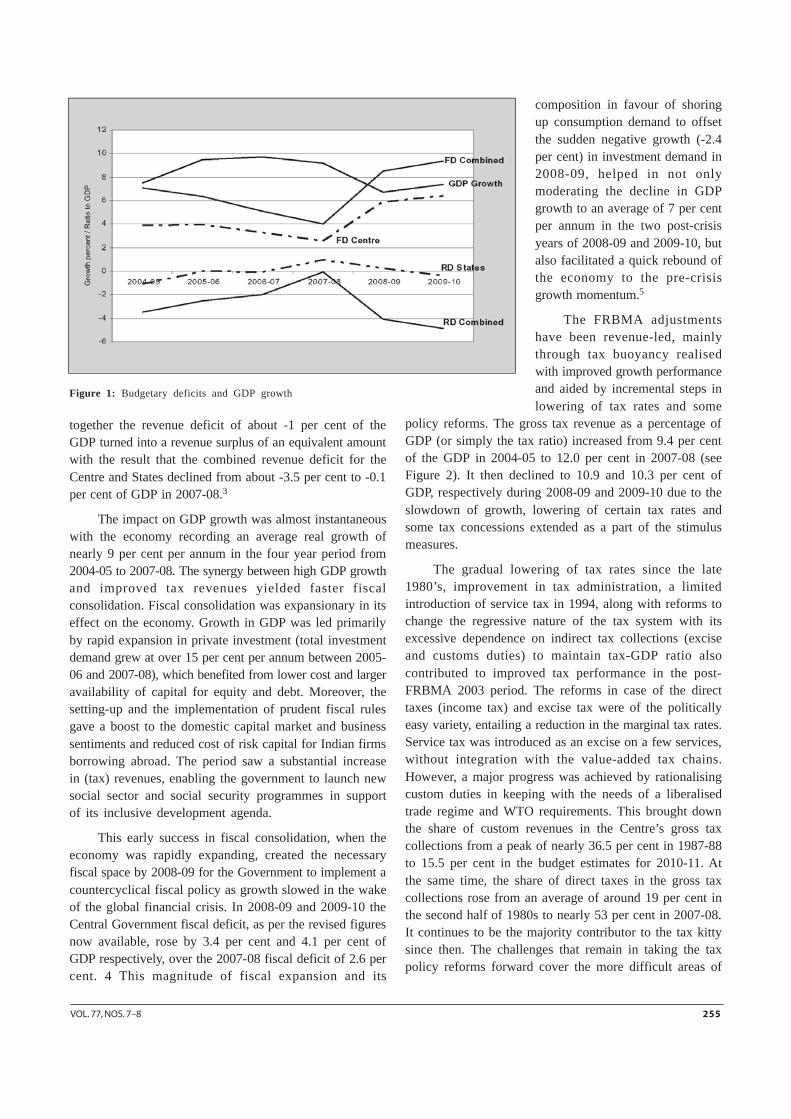

The frontloading of fiscal consolidation (from 2004-5to 2007-08) against the backdrop of a medium term fiscalperspective under the FRBMA 2003 demonstratedGovernment’s resolve and improved its credibility. It createda conducive environment for high growth in the economy.Thus, the fiscal deficit (which indicates the total borrowingrequirements of the Government from all sources and isdefined as the difference between revenue receipts pluscertain non-debt capital receipts and the total expenditureincluding loans, net of repayments) for the CentralGovernment declined from about 3.9 per cent of GrossDomestic Product (GDP) in 2004-05 to 2.6 per cent in 2007-08 and the corresponding decline in the combined fiscaldeficit for Centre and States was from 7.1 per cent to 4.0per cent (Figure 1). During this period the revenue deficit(defined as the excess of revenue expenditure over revenuereceipts) of the Central Government declined from -2.4 percent to -1.1 per cent of the GDP. For the States taken

VOL. 77, NOS. 7–8 255

together the revenue deficit of about -1 per cent of theGDP turned into a revenue surplus of an equivalent amountwith the result that the combined revenue deficit for theCentre and States declined from about -3.5 per cent to -0.1per cent of GDP in 2007-08.3

The impact on GDP growth was almost instantaneouswith the economy recording an average real growth ofnearly 9 per cent per annum in the four year period from2004-05 to 2007-08. The synergy between high GDP growthand improved tax revenues yielded faster fiscalconsolidation. Fiscal consolidation was expansionary in itseffect on the economy. Growth in GDP was led primarilyby rapid expansion in private investment (total investmentdemand grew at over 15 per cent per annum between 2005-06 and 2007-08), which benefited from lower cost and largeravailability of capital for equity and debt. Moreover, thesetting-up and the implementation of prudent fiscal rulesgave a boost to the domestic capital market and businesssentiments and reduced cost of risk capital for Indian firmsborrowing abroad. The period saw a substantial increasein (tax) revenues, enabling the government to launch newsocial sector and social security programmes in supportof its inclusive development agenda.

This early success in fiscal consolidation, when theeconomy was rapidly expanding, created the necessaryfiscal space by 2008-09 for the Government to implement acountercyclical fiscal policy as growth slowed in the wakeof the global financial crisis. In 2008-09 and 2009-10 theCentral Government fiscal deficit, as per the revised figuresnow available, rose by 3.4 per cent and 4.1 per cent ofGDP respectively, over the 2007-08 fiscal deficit of 2.6 percent. 4 This magnitude of fiscal expansion and its

Figure 1: Budgetary deficits and GDP growth

composition in favour of shoringup consumption demand to offsetthe sudden negative growth (-2.4per cent) in investment demand in2008-09, helped in not onlymoderating the decline in GDPgrowth to an average of 7 per centper annum in the two post-crisisyears of 2008-09 and 2009-10, butalso facilitated a quick rebound ofthe economy to the pre-crisisgrowth momentum.5

The FRBMA adjustmentshave been revenue-led, mainlythrough tax buoyancy realisedwith improved growth performanceand aided by incremental steps inlowering of tax rates and some

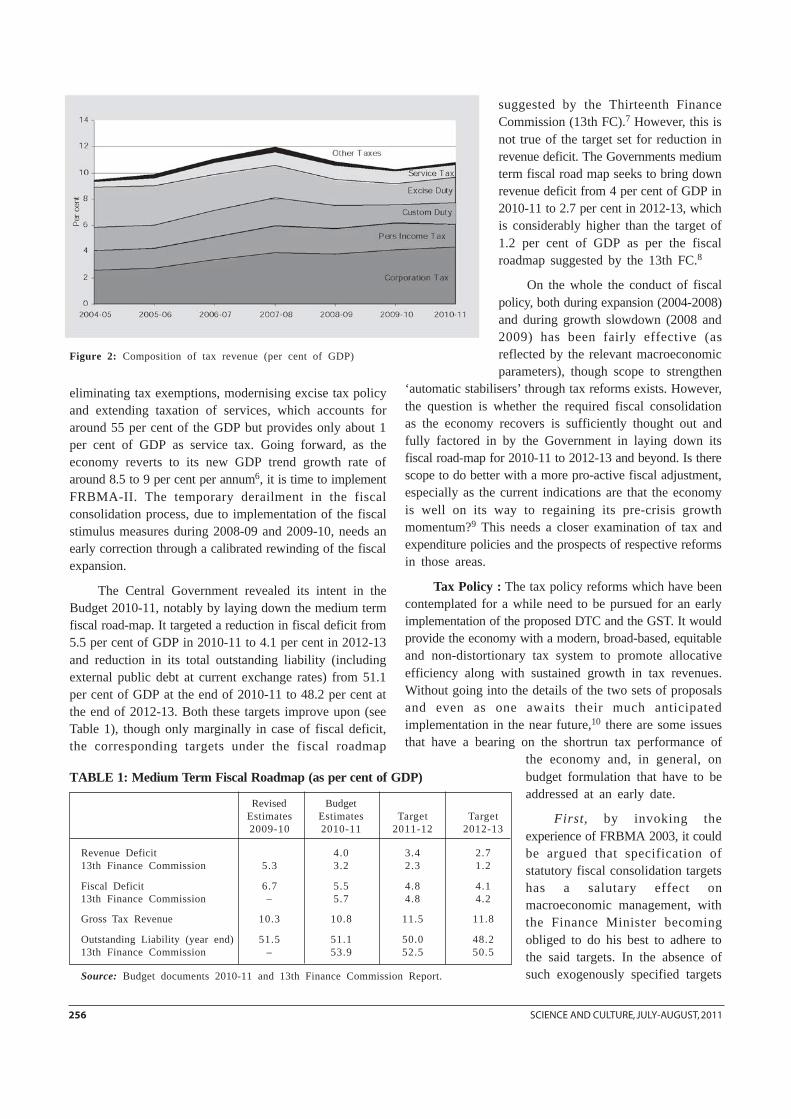

policy reforms. The gross tax revenue as a percentage ofGDP (or simply the tax ratio) increased from 9.4 per centof the GDP in 2004-05 to 12.0 per cent in 2007-08 (seeFigure 2). It then declined to 10.9 and 10.3 per cent ofGDP, respectively during 2008-09 and 2009-10 due to theslowdown of growth, lowering of certain tax rates andsome tax concessions extended as a part of the stimulusmeasures.

The gradual lowering of tax rates since the late1980’s, improvement in tax administration, a limitedintroduction of service tax in 1994, along with reforms tochange the regressive nature of the tax system with itsexcessive dependence on indirect tax collections (exciseand customs duties) to maintain tax-GDP ratio alsocontributed to improved tax performance in the post-FRBMA 2003 period. The reforms in case of the directtaxes (income tax) and excise tax were of the politicallyeasy variety, entailing a reduction in the marginal tax rates.Service tax was introduced as an excise on a few services,without integration with the value-added tax chains.However, a major progress was achieved by rationalisingcustom duties in keeping with the needs of a liberalisedtrade regime and WTO requirements. This brought downthe share of custom revenues in the Centre’s gross taxcollections from a peak of nearly 36.5 per cent in 1987-88to 15.5 per cent in the budget estimates for 2010-11. Atthe same time, the share of direct taxes in the gross taxcollections rose from an average of around 19 per cent inthe second half of 1980s to nearly 53 per cent in 2007-08.It continues to be the majority contributor to the tax kittysince then. The challenges that remain in taking the taxpolicy reforms forward cover the more difficult areas of

256 SCIENCE AND CULTURE, JULY-AUGUST, 2011

eliminating tax exemptions, modernising excise tax policyand extending taxation of services, which accounts foraround 55 per cent of the GDP but provides only about 1per cent of GDP as service tax. Going forward, as theeconomy reverts to its new GDP trend growth rate ofaround 8.5 to 9 per cent per annum6, it is time to implementFRBMA-II. The temporary derailment in the fiscalconsolidation process, due to implementation of the fiscalstimulus measures during 2008-09 and 2009-10, needs anearly correction through a calibrated rewinding of the fiscalexpansion.

The Central Government revealed its intent in theBudget 2010-11, notably by laying down the medium termfiscal road-map. It targeted a reduction in fiscal deficit from5.5 per cent of GDP in 2010-11 to 4.1 per cent in 2012-13and reduction in its total outstanding liability (includingexternal public debt at current exchange rates) from 51.1per cent of GDP at the end of 2010-11 to 48.2 per cent atthe end of 2012-13. Both these targets improve upon (seeTable 1), though only marginally in case of fiscal deficit,the corresponding targets under the fiscal roadmap

Figure 2: Composition of tax revenue (per cent of GDP)

suggested by the Thirteenth FinanceCommission (13th FC).7 However, this isnot true of the target set for reduction inrevenue deficit. The Governments mediumterm fiscal road map seeks to bring downrevenue deficit from 4 per cent of GDP in2010-11 to 2.7 per cent in 2012-13, whichis considerably higher than the target of1.2 per cent of GDP as per the fiscalroadmap suggested by the 13th FC.8

On the whole the conduct of fiscalpolicy, both during expansion (2004-2008)and during growth slowdown (2008 and2009) has been fairly effective (asreflected by the relevant macroeconomicparameters), though scope to strengthen

‘automatic stabilisers’ through tax reforms exists. However,the question is whether the required fiscal consolidationas the economy recovers is sufficiently thought out andfully factored in by the Government in laying down itsfiscal road-map for 2010-11 to 2012-13 and beyond. Is therescope to do better with a more pro-active fiscal adjustment,especially as the current indications are that the economyis well on its way to regaining its pre-crisis growthmomentum?9 This needs a closer examination of tax andexpenditure policies and the prospects of respective reformsin those areas.

Tax Policy : The tax policy reforms which have beencontemplated for a while need to be pursued for an earlyimplementation of the proposed DTC and the GST. It wouldprovide the economy with a modern, broad-based, equitableand non-distortionary tax system to promote allocativeefficiency along with sustained growth in tax revenues.Without going into the details of the two sets of proposalsand even as one awaits their much anticipatedimplementation in the near future,10 there are some issuesthat have a bearing on the shortrun tax performance of

the economy and, in general, onbudget formulation that have to beaddressed at an early date.

First, by invoking theexperience of FRBMA 2003, it couldbe argued that specification ofstatutory fiscal consolidation targetshas a salutary effect onmacroeconomic management, withthe Finance Minister becomingobliged to do his best to adhere tothe said targets. In the absence ofsuch exogenously specified targets

TABLE 1: Medium Term Fiscal Roadmap (as per cent of GDP)

Revised BudgetEstimates Estimates Target Target2009-10 2010-11 2011-12 2012-13

Revenue Deficit 4.0 3.4 2.713th Finance Commission 5.3 3.2 2.3 1.2

Fiscal Deficit 6.7 5.5 4.8 4.113th Finance Commission – 5.7 4.8 4.2

Gross Tax Revenue 10.3 10.8 11.5 11.8

Outstanding Liability (year end) 51.5 51.1 50.0 48.213th Finance Commission – 53.9 52.5 50.5

Source: Budget documents 2010-11 and 13th Finance Commission Report.

VOL. 77, NOS. 7–8 257

(at a point in time), as was the case while preparing thebudget proposals for 2010-11, the resolve may have beenjust that bit relaxed, with a preference to play it safe. As aresult, in comparison to an average 0.65 percentage pointsannual increase realised in the tax ratio in the pre-crisishigh growth period from 2004-05 to 2007-08, the averageincrease in the tax ratio projected in the Medium TermFiscal Policy Statement 2010-11 for the period 2009-10 to2012-13 was only 0.38 percentage points per annum. Thisis not only a conservative assumption,11 but also overlooksthe fact that some of the measures undertaken to improvetax administration and compliance in the recent past arelikely to bear fruit in the current period.12 Thus, there is acase for making more realistic projections on tax revenuesand the resulting fiscal consolidation targets. There is alsoa case for an early enactment of the FRBMA-II and itsoperative rules for conducting a prudent fiscal policy inthe coming years.13 These are important considerations asthey have significant bearing on the behaviour of privateinvestors and critical macroeconomic parameters thatunderpin expectations and the consequent transactions ofeconomic agents.

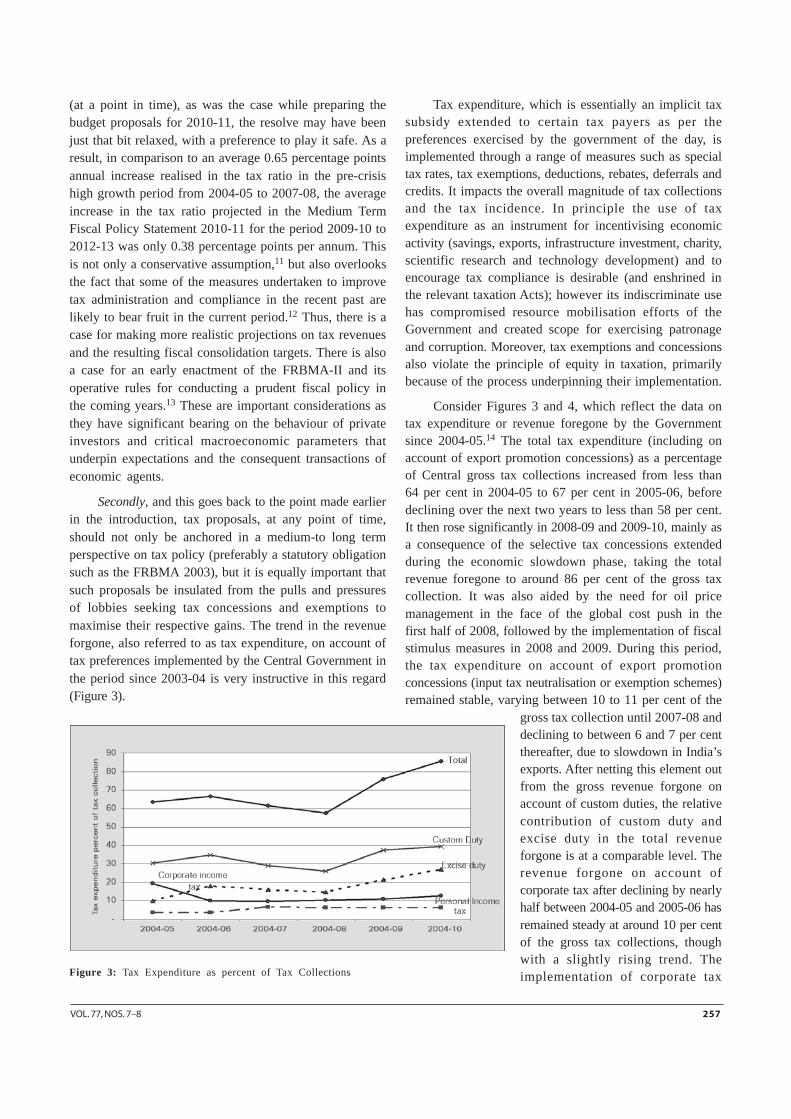

Secondly, and this goes back to the point made earlierin the introduction, tax proposals, at any point of time,should not only be anchored in a medium-to long termperspective on tax policy (preferably a statutory obligationsuch as the FRBMA 2003), but it is equally important thatsuch proposals be insulated from the pulls and pressuresof lobbies seeking tax concessions and exemptions tomaximise their respective gains. The trend in the revenueforgone, also referred to as tax expenditure, on account oftax preferences implemented by the Central Government inthe period since 2003-04 is very instructive in this regard(Figure 3).

Tax expenditure, which is essentially an implicit taxsubsidy extended to certain tax payers as per thepreferences exercised by the government of the day, isimplemented through a range of measures such as specialtax rates, tax exemptions, deductions, rebates, deferrals andcredits. It impacts the overall magnitude of tax collectionsand the tax incidence. In principle the use of taxexpenditure as an instrument for incentivising economicactivity (savings, exports, infrastructure investment, charity,scientific research and technology development) and toencourage tax compliance is desirable (and enshrined inthe relevant taxation Acts); however its indiscriminate usehas compromised resource mobilisation efforts of theGovernment and created scope for exercising patronageand corruption. Moreover, tax exemptions and concessionsalso violate the principle of equity in taxation, primarilybecause of the process underpinning their implementation.

Consider Figures 3 and 4, which reflect the data ontax expenditure or revenue foregone by the Governmentsince 2004-05.14 The total tax expenditure (including onaccount of export promotion concessions) as a percentageof Central gross tax collections increased from less than64 per cent in 2004-05 to 67 per cent in 2005-06, beforedeclining over the next two years to less than 58 per cent.It then rose significantly in 2008-09 and 2009-10, mainly asa consequence of the selective tax concessions extendedduring the economic slowdown phase, taking the totalrevenue foregone to around 86 per cent of the gross taxcollection. It was also aided by the need for oil pricemanagement in the face of the global cost push in thefirst half of 2008, followed by the implementation of fiscalstimulus measures in 2008 and 2009. During this period,the tax expenditure on account of export promotionconcessions (input tax neutralisation or exemption schemes)remained stable, varying between 10 to 11 per cent of the

gross tax collection until 2007-08 anddeclining to between 6 and 7 per centthereafter, due to slowdown in India’sexports. After netting this element outfrom the gross revenue forgone onaccount of custom duties, the relativecontribution of custom duty andexcise duty in the total revenueforgone is at a comparable level. Therevenue forgone on account ofcorporate tax after declining by nearlyhalf between 2004-05 and 2005-06 hasremained steady at around 10 per centof the gross tax collections, thoughwith a slightly rising trend. Theimplementation of corporate taxFigure 3: Tax Expenditure as percent of Tax Collections

258 SCIENCE AND CULTURE, JULY-AUGUST, 2011

preferences have ensured that the effective tax rate atsectoral and overall level remains well below the statutorytax rate (Table 2). Moreover, tax expenditure incurred bythe government in respect of the private sector companiesturns out to be higher than that for the public sectorcompanies.

TABLE 2: Effective Corporate Tax Rates

Sector 2008-09 2007-08 2006-07

Public 27.14 25.69 23.35

Private 21.56 21.28 19.50

Manufacturing 21.97 22.46 21.91

Services 23.53 22.00 19.01

Overall Effective taxrate 22.77 22.24 20.60

Statutory tax rate 33.99 33.99 33.66

Source: Budget documents for various years.Note: The effective tax rates are based on sample companies andinclude surcharge and education cess.

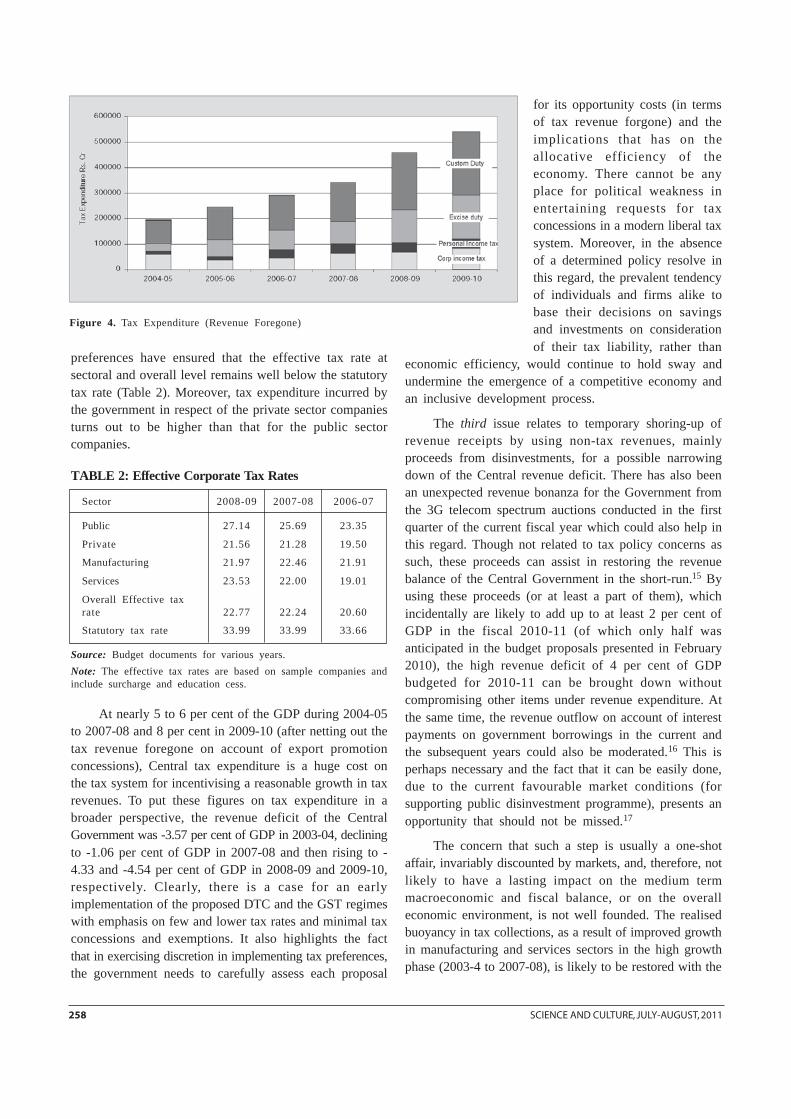

At nearly 5 to 6 per cent of the GDP during 2004-05to 2007-08 and 8 per cent in 2009-10 (after netting out thetax revenue foregone on account of export promotionconcessions), Central tax expenditure is a huge cost onthe tax system for incentivising a reasonable growth in taxrevenues. To put these figures on tax expenditure in abroader perspective, the revenue deficit of the CentralGovernment was -3.57 per cent of GDP in 2003-04, decliningto -1.06 per cent of GDP in 2007-08 and then rising to -4.33 and -4.54 per cent of GDP in 2008-09 and 2009-10,respectively. Clearly, there is a case for an earlyimplementation of the proposed DTC and the GST regimeswith emphasis on few and lower tax rates and minimal taxconcessions and exemptions. It also highlights the factthat in exercising discretion in implementing tax preferences,the government needs to carefully assess each proposal

Figure 4. Tax Expenditure (Revenue Foregone)

for its opportunity costs (in termsof tax revenue forgone) and theimplications that has on theallocative efficiency of theeconomy. There cannot be anyplace for political weakness inentertaining requests for taxconcessions in a modern liberal taxsystem. Moreover, in the absenceof a determined policy resolve inthis regard, the prevalent tendencyof individuals and firms alike tobase their decisions on savingsand investments on considerationof their tax liability, rather than

economic efficiency, would continue to hold sway andundermine the emergence of a competitive economy andan inclusive development process.

The third issue relates to temporary shoring-up ofrevenue receipts by using non-tax revenues, mainlyproceeds from disinvestments, for a possible narrowingdown of the Central revenue deficit. There has also beenan unexpected revenue bonanza for the Government fromthe 3G telecom spectrum auctions conducted in the firstquarter of the current fiscal year which could also help inthis regard. Though not related to tax policy concerns assuch, these proceeds can assist in restoring the revenuebalance of the Central Government in the short-run.15 Byusing these proceeds (or at least a part of them), whichincidentally are likely to add up to at least 2 per cent ofGDP in the fiscal 2010-11 (of which only half wasanticipated in the budget proposals presented in February2010), the high revenue deficit of 4 per cent of GDPbudgeted for 2010-11 can be brought down withoutcompromising other items under revenue expenditure. Atthe same time, the revenue outflow on account of interestpayments on government borrowings in the current andthe subsequent years could also be moderated.16 This isperhaps necessary and the fact that it can be easily done,due to the current favourable market conditions (forsupporting public disinvestment programme), presents anopportunity that should not be missed.17

The concern that such a step is usually a one-shotaffair, invariably discounted by markets, and, therefore, notlikely to have a lasting impact on the medium termmacroeconomic and fiscal balance, or on the overalleconomic environment, is not well founded. The realisedbuoyancy in tax collections, as a result of improved growthin manufacturing and services sectors in the high growthphase (2003-4 to 2007-08), is likely to be restored with the

VOL. 77, NOS. 7–8 259

roll-back of tax concessions (implemented as a part of thefiscal stimulus) and as the economy reverts to its trendGDP growth path of 8.5 to 9 per cent per annum. Thiswould help offset the temporary enhanced revenues dueto higher disinvestment proceeds, or due to the one timespike in non-tax revenues (3G spectrum proceeds) in theshort-term (i.e. 2010-11 and if required also in 2011-12).Moreover, the imminent implementation of the DTC andthe GST, with the latter alone expected to add another 2percentage points to the tax ratio, as per the estimates ofthe Task Force on the implementation of the FRBMA 2003(Government of India 2004, page 7 and Appendix B), thereare good reasons for a more optimistic growth in taxrevenues over the next few years. Therefore, there is acase for undertaking a more confident and aggressive fiscalconsolidation in the remaining period of 2010-11 and 2011-12, which will help boost business confidence, cut policyambiguity and create the required thrust for the muchneeded reforms of public expenditure.

Expenditure Policy

Attention has to be accorded to expenditure policymanagement, not necessarily to consolidate publicexpenditure, but to better orient it towards the productionof public goods (defence, law and order) and quasi publicgoods (education, health and certain kind ofinfrastructure).18 There are at least three facets of theexpenditure policy that are interrelated and need urgentattention with a view to realise the fiscal policy objectivesof the Union Budget.

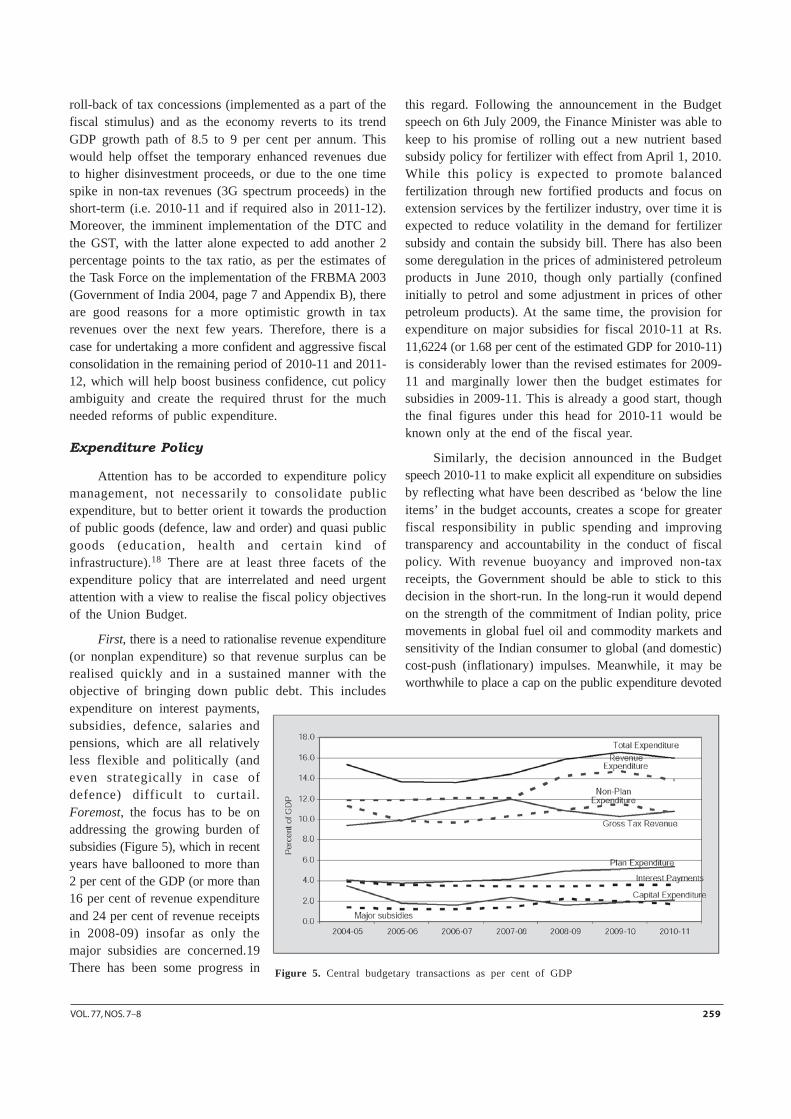

First, there is a need to rationalise revenue expenditure(or nonplan expenditure) so that revenue surplus can berealised quickly and in a sustained manner with theobjective of bringing down public debt. This includesexpenditure on interest payments,subsidies, defence, salaries andpensions, which are all relativelyless flexible and politically (andeven strategically in case ofdefence) difficult to curtail.Foremost, the focus has to be onaddressing the growing burden ofsubsidies (Figure 5), which in recentyears have ballooned to more than2 per cent of the GDP (or more than16 per cent of revenue expenditureand 24 per cent of revenue receiptsin 2008-09) insofar as only themajor subsidies are concerned.19There has been some progress in

this regard. Following the announcement in the Budgetspeech on 6th July 2009, the Finance Minister was able tokeep to his promise of rolling out a new nutrient basedsubsidy policy for fertilizer with effect from April 1, 2010.While this policy is expected to promote balancedfertilization through new fortified products and focus onextension services by the fertilizer industry, over time it isexpected to reduce volatility in the demand for fertilizersubsidy and contain the subsidy bill. There has also beensome deregulation in the prices of administered petroleumproducts in June 2010, though only partially (confinedinitially to petrol and some adjustment in prices of otherpetroleum products). At the same time, the provision forexpenditure on major subsidies for fiscal 2010-11 at Rs.11,6224 (or 1.68 per cent of the estimated GDP for 2010-11)is considerably lower than the revised estimates for 2009-11 and marginally lower then the budget estimates forsubsidies in 2009-11. This is already a good start, thoughthe final figures under this head for 2010-11 would beknown only at the end of the fiscal year.

Similarly, the decision announced in the Budgetspeech 2010-11 to make explicit all expenditure on subsidiesby reflecting what have been described as ‘below the lineitems’ in the budget accounts, creates a scope for greaterfiscal responsibility in public spending and improvingtransparency and accountability in the conduct of fiscalpolicy. With revenue buoyancy and improved non-taxreceipts, the Government should be able to stick to thisdecision in the short-run. In the long-run it would dependon the strength of the commitment of Indian polity, pricemovements in global fuel oil and commodity markets andsensitivity of the Indian consumer to global (and domestic)cost-push (inflationary) impulses. Meanwhile, it may beworthwhile to place a cap on the public expenditure devoted

Figure 5. Central budgetary transactions as per cent of GDP

260 SCIENCE AND CULTURE, JULY-AUGUST, 2011

to the major subsidies, for instance as a proportion ofGDP (say 1.5 to 1.75 per cent of GDP). This could continueat least until such time that the ‘Aadhaar’ programme ofthe Unique Identification Authority of India (UIDAI) isrolled out in the country and government is able to deliverits major subsidies efficiently.

The other important item of revenue expenditurewhich needs to be tackled is interest payments. It wasnearly 4 per cent of the GDP in 2004-05. Though it declinedto about 3.4 per cent of GDP in 2008-09, it accounted formore than 24 per cent of the revenue expenditure andabout 36 per cent of revenue receipts. Since then it hasrisen to 3.6 per cent of GDP due to the increasedgovernment borrowings due to the implementation of fiscalstimulus measures. It is a function of the size of therevenue deficit, fiscal deficit and interest costs (inflation)and can be tackled through better tax and non-tax revenuemobilisation, using proceeds from disinvestments in theshort-term (as discussed in the earlier section of the paper)and, in the medium to long-term, through bettermanagement of inflationary pressures on hardening ofinterest rates.

Expenditure on pensions has been among the fastestgrowing items of public spending. It has doubled from0.36 per cent of GDP in 1990-91 and accounts for nearly50 per cent of the expenditure on pay and allowances. Toaddress the growing burden of pensions in the face ofimproving longevity, the Government initiated (with effectfrom January 2004) a new defined pension system for newentrants to Central Government, other than defenceservices. The new scheme provides for a definedcontribution to be shared equally between the employeesand the employer. In respect of other elements of revenueexpenditure, including expenditure on defence services,police and economic and social services of the government,the feasibility of rationalising expenditure is less obvious,though there is considerable scope to improve theefficiency of public spending in these areas as well.

The second issue in respect of the expenditure policyrelates to the composition of public expenditure. Whilethe dual economic and functional classification of publicexpenditure is not free of categorisation problems (someof these and related issues are discussed in a subsequentsection), it is helpful to consider trends in plan and non-plan expenditure on one hand, and in revenue and capitalexpenditure on the other hand. The Plan expenditure whichhas been averaging around 4 per cent of the GDP from2004-05 up until 2007-08, jumped by nearly one percentagepoint of GDP in 2008-09, as the Government unveiled itsstimulus spending to counter the economic slowdown

(Figure 5). It has retained the upward trend over the lasttwo years and is budgeted at 5.4 per cent of the GDP in2010-11. While this upward trend in plan spending iswelcome, there is need to exercise caution on the natureof this spending. Ideally more of plan spending should bedirected towards capital formation as conventionallydefined and on human capital formation (throughexpenditure on education and health services) rather thanon social transfers that mostly influence consumptionexpenditure. Thus, programmes like Mahatma GandhiNational Rural Employment Guarantee Scheme (NREGS)accounting for nearly 8 to 9 per cent of the total CentralPlan outlay in the last two years, though useful intransferring purchasing power to the rural poor, especiallyin times of economic stress and labour displacement, hasa limited role in capital formation for sustaining growthover time. Moreover, there is need to forge and strengthenthe link between such programmes and creation of publicand quasi public goods, including through a largerprovision for capital expenditure, so that plan expenditureis better oriented to meet the objectives of India’s publicpolicy.

The trend in capital expenditure reflects this concernwith the composition of plan spending. The total capitalexpenditure witnessed a sharp decline from 3.5 per cent ofGDP in 2004-05 to 1.8 per cent in 2005-06 and further to1.6 per cent in 2006-07. This was mainly on account of asteep decline in non-plan capital expenditure though theplan capital expenditure also fell. There was someimprovement in 2007-08 as capital expenditure touched 2.4per cent of GDP, but it declined again in the next twoyears before recovering to 2.2 per cent of GDP in thebudget estimates for 2010-11. In the most recent yearssince 2007-08, expenditure on subsidy shows a strongnegative correlation with capital expenditure. Also therehas been a significant rise in grants to State and UnionTerritories since 2005-06 (nearly a doubling in nominal termsbetween 2004-05 and 2005-06 from Rs. 14,784 crore to Rs.30,475 crore, or an increase from about 0.45 per cent ofGDP in 2004-05 to on an average of 0.8 per cent of GDP inthe subsequent years) to fund the implementation of theGovernment’s flagship programmes. These grants areclassified as non-plan revenue expenditure, even though apart of expenditure from these grants is for capital worksof the flagship programmes. This has not only led to anunderestimation of capital expenditure in the totalgovernment expenditure, but increase in these grants hasalso contributed to crowding out of the total capitalexpenditure of the Government. This trend needs detailedanalysis and correction for the medium to long termsustainability of the growth process.20

VOL. 77, NOS. 7–8 261

The third set of issues in respect of the expenditurepolicy relates to the urgent need for institutional reformsto improve the efficiency of government expenditure. Thisincludes some system-wide issues like the review andmodification of public procurement policy, the need foroverhauling the prevalent incentive structure in publicsector for ensuring administrative efficiency, addressinginfirmities in planning and public implementation processat the Central, State and local levels, and tacklingweaknesses in monitoring and evaluation systems. Thereare some sector specific issues, for example the role ofpublic-private partnerships in improving the effectivenessof government spending (infrastructure), improvingdevelopment delivery and targeting of benefits (povertyalleviation and social security), strengthening of regulatoryframeworks (education, health, insurance and consumerprotection) and outsourcing or withdrawal of public sectorfrom the production of certain goods and services. Whileall these issues have a bearing on the fiscal (expenditure)policy outcomes, they need not be addressed in the contextof the budget process alone. Some of these issues areelaborated in the following section of the paper, where anattempt has been made to assess the Union Budget at itspreparatory process for the progress that has been madein promoting accountability in the use of public resources.

Budget as an Accountability Tool

There are two aspects to the use of budgetdocumentation (including the Finance Minister’s budgetspeech) as an accountability tool for the functioning ofthe government. The first relates to the need forinformation sharing and transparency in documentation tofacilitate a broad based understanding of the budgetarytransactions and the methodology for the preparation ofthe budget. This includes availability of the documentationin the public domain, amenability of the documentation tosupport social monitoring and evaluation, and the needfor it to be based on a process that while reflecting thedevelopment vision of the government, takes into accountthe views and concerns of the major stakeholders in theeconomy. The second aspect of the budget as anaccountability tool requires it to focus on outcomes ratherthan mere outlays. The budget needs to periodically(annually where feasible) present an assessment of theunderlying planning and implementation processes ofpublic programmes for the delivery of intended outcomes.Thus, the budget has to support both ex-ante and ex-poste accountability of government activity.

On these two aspects of accountability, the budgetprocess and its documentation as it has evolved in the

last few years, has made significant progress.21 Some tasks,however, remain to be addressed or require furtherimprovement.

There are several recent steps that have contributedto an improvement in the transparency and accountabilityof the budgetary transactions. These include: thediscontinuation of ‘below the budget line’ modality ofissuing government bonds to finance some of the majorsubsidies (oil and fertilizers) and the decision to extend allfuture subsidies in cash, thereby including all subsidyrelated liabilities explicitly in the budget accounting (budget2010-11); placing the tax reform proposals covering theDTC and the GST in the public domain with a view tobuild consensus and informed decision making (2009-10);the presentation of information on revenue forgone onaccount of implementation of the Central Government’s taxpreferences in the budget documents (since budget 2006-07 and as a separate statement since budget 2010-11); thedecision to prepare ‘outcome budgets’ to reflect thephysical dimensions and attainments of the financialoutlays under the budget (budget 2005-06 onwards); thesetting up of a ‘National Investment Fund’ outside theConsolidated Fund of India in January 2005 for depositingthe disinvestment proceeds and the use of income fromthe said fund for investment in social sectors projects andfor meeting capital investment in profitable and revivablePublic Sector Enterprises; the enactment of the FRBMA in2003, the adoption of its Rules in 2004, along with thepresentation of the Macroeconomic framework Statement,the Medium-term Fiscal Policy Statement and Fiscal PolicyStrategy Statement (budget 2004-05); introduction of astatement as a part of the budget documentation outliningthe implementation status of announcements made in thebudget speech (since budget 2001-02); and making explicitsome of the assumptions on the projected variables (viz.nominal GDP growth) in the budget documentation.

Even as this paper was being written, the Governmentof India published a ‘Budget Manual’ (Government of India2010b), which for the first time brings together theinformation on content and process of Union Budgetpreparation and its larger Constitutional and proceduraldetails. It is a significant contribution to strengthening ofinstitutional memory, transparency and continuity in a vitaltool of governance and policy making. It provides allguidelines and instruction in one place for those civilservants who are, or become part of the budget makingprocess at some points in their career. More importantly,this manual goes a long way in demystifying a processthat has been an enigma to all the stakeholders who donot have a hands-on experience in the preparation of the

262 SCIENCE AND CULTURE, JULY-AUGUST, 2011

Budget, including the policy analysts, media and thepeople who are the object of this exercise.

Some further steps for making the budget moretransparent and improve its use as an accountability toolfor monitoring public expenditure could be grouped in threebroad areas. The first relates to changes and improvementin information presentation and budget documentation. Thesecond relates to areas where the budget process couldbenefit from coordinated and qualitative inputs forreforming certain institutional practices related to budgetpreparation and its implementation. The third relates tothe importance accorded to and the capacity improvementrequired in undertaking budget analysis, including at thelegislative level (before the proposals for the ensuing yearare voted and accorded Parliamentary approval), in theexecutive oversight process and among the civil societystakeholders. Some measures in each of these three areasare briefly discussed in the remaining part of this section.

A system of performance monitoring for governmentministries/departments that were implementing developmentprogrammes was introduced in 1969. However, in theabsence of a clear one-to-one correspondence betweenthe financial outlays and the performance budgets, andthe fact that there has been inadequate focus on physicaltarget setting in the annual departmental budgets, theperformance budgeting exercise become ineffective. In orderto address this weakness in performance budgeting and,more importantly, to forge a link between the measurableintermediate ‘physical outputs’ and the somewhat distant‘outcomes’ they support, led to the introduction of‘outcome budget’ by the Government in 2005-06. Theintention being to assess and monitor the conversion ofoutlays into outcomes or impacts, which are the ultimateobjectives of state intervention. Though expenditureincurred is an important indicator of the progress of publicprogrammes, it does not measure the effectiveness of theexpenditure undertaken in generating the desired outputsand outcomes. It is, therefore, desirable to move awaysystematically from financial to output and outcomemonitoring.

Detailed guidelines have been issued by theDepartment of Expenditure in the Ministry of Finance forpreparation of outcome budgets. These guidelines requireministries to separately prepare their outcome budgets, asper a standard template, and table the document inParliament well before the concerned Parliamentary StandingCommittees examines the budget proposals of that ministry(and also release it to the public through their website).The full impact of this initiative is yet to be felt.

The real value of outcome budget lies in its role as avital instrument of ‘closure’ for the budgeting and planningprocess. The lack of effective feedback loop of evaluationand assessment into planning and implementation process,neglect of efficiency in transforming public outlays intooutputs and desired outcomes, a general apathy in theuse of government resources, chronic weaknesses in publicdelivery systems, leakages and sub-optimal targeting ofintended beneficiaries have compromised accountability ofpublic agencies.

Some of the measures that have been identified, butneed to be rapidly and effectively implemented in order tomake outcome budgets a potent tool in improving publicaccountability of government agencies include improvementof statistical systems and identification of monitoringindicators (output and outcome) for public programmes atthe level of ministries/ departments; setting-up independentevaluation or external peer-review of on-going publicprogrammes; linking-up the release of budgeted funds withquarterly monitorable targets on selected indicators;making the continuation of public programmes oversuccessive years and plans a function of attaining targetson specified indicators; and presenting a consolidatedoutcome document on the performance of CentralGovernment as a part of the Union Budget documentation(as distinct from the separate outcome budget documentsthat each ministry/department places in Parliament aspresent). The latter would contribute to improving thevisibility and hence relevance of the outcome budgetexercises. The success of the outcome budget exercisealso requires an active engagement of civil society forwhich web-enabled dissemination of information and detailson the exercise by the concerned ministry is of vitalimportance.

There are also specific issues related to modificationin the presentation of budget allocations and expenditure,such as providing in one place the total annual flow ofresources from the Union Budget to each State Governmentby way of all modalities, including Central Plan Assistance,Additional Central Assistance, special assistance, CentrallySponsored Schemes, Central Sector Schemes, etc. Atpresent the scheme wise flow of resources to the States isalso not readily available in the budget relateddocumentation. If this gap is addressed, it will revealunderlying motivation of the Central Government in thetransfer of resources (where it enjoys some discretion) toStates and contribute to transparency and accountabilityin an era of coalition politics, proliferation of regionalparties and a multi-party polity in the country. There areissues related to the classification of public expenditure

VOL. 77, NOS. 7–8 263

as well that need to be addressed for more effective useof public resources. Some of these issues are addressedin the next section where the budget is assessed for itsrole as a planning tool.

There are at least two institutional practices relatedto the process of budget preparation that could help inimproving the overall transparency, credibility andaccountability of government functioning in the formulationand implementation of economic policy. The first concernsthe Finance Minister’s pre-budget consultations with thestakeholders. The normal practice in this context has beento organise meetings with different interest groups suchas those representing agriculturalists and agricultureresearch, labour and trade unions, industrialists, exporters,civil society organisations, academics and economic policyanalysts, and financial institutions. Occasionally, theFinance Minister also meets with the State FinanceMinisters, as was the case in the course of the budgetexercise for 2010-11. It would be desirable to make themeeting with the State Finance Ministers a regular part ofthe pre-budget consultations. With the policy content ofthe Union Budget, beyond the resource allocations toCentral ministries, set to increase and the economybecoming more integrated domestically (the impending GSTwill add to that trend), as well as globalized, the StateGovernments will have a greater stake in the formulationand implementation of Central Government policies. At thesame time, there is also a case for including inputs frommarket regulators (as to how they see their respectivemarkets developing in the ensuing period), ensuring a morerobust engagement with the civil society and schedulingthese discussions appropriately in the calendar for thepreparation of the budget. These consultations not onlyallow for a broad based public participation in the policymaking process, but also enable the policy makers to havea better understanding of the stakeholders expectationsand concerns.

The second institutional practice issue relates toimplementation of the budget proposals, particularly whenthe normal process is challenged by certain unanticipatedor sudden developments (viz. failure of monsoons, naturalcalamities, etc.) necessitating a revision in the budgetedtax and expenditure proposals. The preferred course ofaction in such instances has been to either place an acrossthe board cut on spending (as a part of austeritymeasures), or to raise resources through surcharges ontaxes. Such measures though scoring high onconsiderations of policy transparency and administrativeconvenience invariably undermine allocative efficiency andaccountability in the use of public resources. They may

end up sending a strong contractionary signal to themarkets (viz. influencing consumption spending), eventhough their direct impact on the economy may not be so,or create expectations among the economic agents thatmay be contrary to the intended policy measure.22

Moreover, given the inflexibility in curtailing revenueexpenditure, adjustment process ends up cutting down oncapital (developmental) expenditure, compromising themedium to long term capacity of the economy to sustaingrowth. There are also instances where expenditure onsome public programmes have a lumpy character or whensome ministries are more efficient in implementing theirprogrammes and may, therefore, end up being treated onpar with others due to this ‘one-size fit all’ approach inadministering expenditure cuts. It results in sub-optimalbudgetary outputs and outcomes. Further, there is theissue related to delay in the release of approved budgetedfunds in the course of the year, resulting in bunching ofpublic expenditure in the fourth quarter and in manyinstances on 31st of March- the closing day of the fiscalyear. This yields sub-optimal outcomes for expenditureundertaken. These concerns in implementing the budgetedprogrammes require a flexible, more evolved and acoordinated, but transparent procedural approach. Thoughthere have been some refinements, such as benchmarkingof releases for each quarter of the year, it has not yetsolved the problems of expenditure bunching, diversion,delay and cost overruns in implementation of programmes.Some of these concerns relate to the weakness in planningprocess and have to be addressed by overcoming theweaknesses therein.

Finally, any tool is only as useful as the use to whichit is put. There is a need to improve the capacity for budgetanalysis, particularly among the political parties and thecivil society organisations in the country, if the budgethas to play its role as an instrument for enforcing publicaccountability. In recent times, Parliament has not devotedadequate time for discussing budget proposals. Invariably,other political issues have hijacked the time usually keptaside for budget discussions. As a result Parliament(Speaker) has resorted to using the ‘guillotine’, a device(practice) to bring the debate on financial proposals to anend within a specified time, with the results that severaldemands for grants have to be voted by the members ofParliament without discussions. This undermines publicoversight of government policies and the potential role ofa budget in enforcing accountability and transparency ofpublic action.

There is paucity of expertise available in theParliament Secretariat to assist the various Standing

264 SCIENCE AND CULTURE, JULY-AUGUST, 2011

Parliamentary Committees in the examination of the budgetproposals from different ministries /departments. At thesame time, as pointed earlier, there is practically noinstitutional backstopping research and capacity for budgetanalysis in the mainstream political parties to support theirdeliberations in Parliament. In some countries, there arewell established civil society organisations and ‘think tanks’that specialise in undertaking budget analysis and budgetmonitoring to assess the use of public resources. In Indiaalso there are a few organisations that work in this area,however, there is considerable scope to strengthen capacityon this issue in the civil society domain.

Indeed, the Indian political system needs to learn andevolve, for example like the Westminster model, where acontinuous tracking of government performance enablesthe shadow ministers (from the opposition party) to builda ready knowledge on policy issues and governancepractices of specific (their shadow) ministries. In theprocess, they contribute to the public oversight capacity,raise the quality of debates in the public domain and ‘hitthe ground running’ when they form the government. Themajor political parties, for example in the USA, theNetherlands and Australia, among others, use either in-house professional expertise supported by interns andvolunteers for undertaking research on issues beingpolitically debated, or they commission studies throughindependent think-tanks that provide the necessaryknowledge for the parties to present their case. Politicalparties not only work out the fiscal implications ofimplementing their political manifestos, but they also seekalternative growth and policy scenarios to pitch theirprogramme agenda at operationally realistic levels.Presently, the recourse to such measures, when undertakenby the mainstream political parties in India, is entirely adhoc and individual-driven.23 It is essential that the capacityto undertake meaningful budget analysis and, moregenerally, economic policy analysis and developmentmonitoring is encouraged in the civil society to supportpolitical parties and other social interest groups in theiroversight of public bodies.

IV. Budget and the Planning Process

The budget operationalises the annual plan, which inturn implements the agreed national developmentobjectives, strategy and the programme of action asreflected in the Five Year Plans of the country.24 Whilethe Annual Plan is anchored in a five year planning cycle,25

up until recently the fiscal policy framework of the Budgetwas bereft of an explicit medium term perspective.26 It waswith the enactment of the FRBMA, 2003 that fiscal policy

acquired a multi-year perspective based on statutorymedium-term fiscal targets, with the objective of sustaininglong-term macro economic stability. To the extent there areweaknesses in the planning process, and in particular inthe annual planning cycles, there would be weaknesses inthe preparation and implementation of the budget. At thesame time, improvement in the budget formulation and itsimplementation would have beneficial consequences forthe planning process in the country.

There are several conceptual issues that arise fromthe extant planning methodology and the adopted structureof plan financing that have a bearing on the transparencyand the overall effectiveness of the budget in deliveringon its objectives, including as a vital planning tool. Someof these have been summarised in the Eleventh Plandocument (see Government of India 2008, Vol. I, page 47-51). These include issues related to the classification ofpublic expenditure, which has implications for overall publicexpenditure management and hence on fiscal policy; themechanisms and the criteria for Central Plan transfers (alsohorizontal devolution of Central grants); the treatment ofinvestment financed by own resources of the publicenterprises and other innovative methods of raisingresources for public investment.

The practice adopted for the classification of publicexpenditure in India has been much debated, but themultiple layers of issues that it throws up remain largelyunaddressed so far. The foremost concern relates to thedistinction adopted between plan and non-planexpenditure. There has been misconstrued understandingof the distinction between the two categories ofexpenditure, with non-plan expenditure being seen aswasteful - to be checked for ensuring fiscal prudence. Overthe years this practice has become dysfunctional and evencounterproductive in the face of other fiscal developments.On one hand, it has led to proliferation of plan schemesand the tendency to let them linger from one five-yearplan period to another, with little effort or incentive tocomplete them. This is largely due to the in-built proceduraldifficulties in creating employment on the non-plan sideor due to an outright ban on creating non-planemployment. A case to point is the numerous plan schemesfor building irrigation capacity both in the Central and theState domains, some of which were initiated as far back asthe Second and the Third Five Year Plans in the 1950sand early 1960s and remain incomplete to date. On theother hand, it has compromised the maintenance of assetsbuilt during the course of earlier plans. Once an asset iscompleted during a plan (for example a new road or a newschool building), it is transferred to the non-plan head

VOL. 77, NOS. 7–8 265

from the ensuing plan period, where its maintenancesuffers due to limited funds that are spread thinly acrosscompeting demands.

An aspect of the plan non-plan distinction of publicexpenditure is also impacting the funding of social sectorprogrammes, which have grown significantly in recentyears under the inclusive development agenda of thepresent Central Government. Expansion in education andpublic health services involves proportionately largeexpenditure on staff salaries which are typically categorisedas non-plan (revenue) expenditure. This poses problemsof service delivery. Thus, while political and administrativeenergies are expended in raising the plan size, year afteryear, public expenditure management and implementationhave suffered. There are huge gaps in coverage andmaintenance of public services across the country, failurein timely realisation of project/programme outcomes anddepletion of existing capacity and assets, problems thatare largely rooted in prevalent planning practices as theyhave evolved over time.

Secondly, there is the issue of the relative share ofcapital expenditure in total public expenditure and thecategorisation of public spending between revenue andcapital expenditure. This issue becomes particularlyimportant in the context of the FRBMA, which focuses onelimination of revenue deficits. Given that more than 85per cent of the total Central Government spending andabout 75 per cent of the plan expenditure is on the revenueaccount alone, implementation of FRBMA has a directbearing on the Centre’s capacity to formulate plan schemesdirected at national priorities and at supplementing Stateefforts in provisioning of public services. This wouldparticularly impact the sustainability of social sectorflagship programmes of the present Central Governmentthat have a large revenue expenditure component. On thecategorisation of expenditure between revenue and capital,there are currently entries on both sides that require arevision in keeping with the economic classification innational accounts and the Constitutional provision andunderstanding for the same. Thus, as indicated earlier, theCentral grants to the State Governments are classified asrevenue expenditure even when some of it is being usedfor capital expenditure. Similarly, recapitalisation of publicsector enterprises, though classified as capital expenditure,is not resulting in investment, in most instances.Equityinjection is in fact a subsidy in case of the lossmaking enterprises. At the same time, in seekingconsistency with the Constitutional understanding on theissue of expenditure on revenue account, there may be acase to put defence capital expenditure as revenue

expenditure as it is not self-financing expenditure and hasto be met from government revenues. There may also be acase for conceptualising capital expenditure more broadlyto include expenditure on human capital formation, suchthat expenditure undertaken on public expansion ofeducation and health services could be categorised ascapital expenditure. While these revisions may help in abetter planning and utilisation of public expenditure, it willalso contribute to the implementation of budgetarycommitments on the FRBMA.

Thirdly, there has been a gradual shift in the modalityof plan transfers to the States from the Normal CentralAssistance route (NCA, which is untied and is allocatedusing the revised Gadgil formula or Gadgil–Mukherjeeformula), towards the use of Centrally Sponsored Schemes(CSS, which are sector specific and governed by Centralguidelines). Moreover, within the CSS a large proportionof fund transfers are made directly to the district(Panchayati Raj Institutions) and state level implementingagencies, bypassing the State Governments. This hasimplications for planning outcomes (accountability) andbudget modalities.

The CSS provides the Central Government with aninstrument that enables it to earmark resources to bridgedevelopment gaps at state-level in areas of nationalimportance. By transferring funds directly to state anddistrict level implementing agencies it helps in avoidingdelays in the rollout of the plan schemes and preventsdiversion of funds by the State Governments to meettemporary requirements for their ways and means position,or on other issues. However, this may be resulting in animplicit precedence being given to national (CentralGovernment) priorities visà-vis state-specific (StateGovernment) priorities, which has implications for politicalcommitment in the implementation of plan schemes due tothe perceived ownership of these schemes and onaccountability in public spending. At the same time, itmeans more budget related responsibilities to the Centralministries running the various CSS programmes, but withlittle direct control on proper utilisation of funds at theimplementation level and weak monitoring and evaluationfeedback loops. This has, perhaps, led to a tendencyamong the Central ministries to assess their success interms of the increase managed in the outlay of their planschemes over successive years, which in turn is dependenton the utilisation of allocated amounts in the precedingyear. It has encouraged a culture of financial targetingrather than physical (outcome) targeting, led by the year-end (March end) spending frenzy of public agencies. All

266 SCIENCE AND CULTURE, JULY-AUGUST, 2011

this has compromised the effectiveness of the budgetprocess and public spending.

Though some measures have been taken to addressthese planning and budget weaknesses, a fresh conceptualrethinking is required. There is a strong case for making alarger share of transfers, including plan transfers, linkedto performance benchmarks that are ratified by independentsocial auditing processes and are based on best practicesin that regard. This is also true for the horizontal transferof Central grants, which need to be based on revisedcriteria of allocation with higher weightage being given todynamic performance criteria (for example progress of theState in moderating population growth rate as against totalpopulation or progress in bringing down the incidence ofpoverty rather than the proportion of poor at a point oftime) to support a developmental culture as againstpopulist governance and the urge to highlight perversedevelopment outcomes at the State level for corneringgreater share of Central Government resources.27 Thiswould have to be balanced by consolidation of the CSSacross sectors and restoring the allocation of Central grantsto the NCA route, based on the said revisions in itsdevolution criteria. In an effort to address developmentgaps at state-level and often due to political motivation,public interventions (through the CSS and state schemes)have taken place in an ad hoc manner resulting in alabyrinth of plan schemes and programmes.28 This hasresulted in administrative overload in tracking and reportingon these schemes that has compromised effectiveness intheir implementation.29 There has been some steps takenin consolidating CSS and review of Central Schemes bythe Planning Commission, especially in the course of theformulation of last two five year plans, but these stepsneed to be more comprehensive, based on objectiveassessment (free of political considerations) and time-bound.

Fourthly, the public sector domain has been graduallyshrinking with privatisation and divestments of publicenterprises. With the strengthening of Panchayati RajInstitutions, Public Private Partnerships (PPP) and specialpurpose societies and agencies, there are new modalitiesof implementing the public sector plan. This hasimplications for the size of the public sector plan and thebudget and there are issues of consistency andcomparability, intertemporally and across states. There isa need to streamline the methodology to address thesechanges for their planning and budgetary consequences,including a more accurate assessment of availableresources with these entities for public investment,monitoring and evaluation of their outcomes in so far as

public funds are being contributed for their working andfor identifying and strengthening policy tools (regulatoryregimes and measures) in the context of their diminishingdependence on the government budgets, with a view toinfluence their contribution to the realisation of nationaldevelopment objectives and priorities.

Fifthly, some of the prevalent public accountingpractices are compromising the effectiveness of planningand undermining budgeting, monitoring and policy makingprocess. The existing accounting system does not capturetransaction-oriented information, nor does it distinguishbetween transfers to States, final expenditure and advancepayments against which accounts have to be rendered.Moreover, as pointed out earlier, it does not support State-wise and scheme wise details of fund released by theCentral Government nor the actual utilisation for theintended purpose.30

Most of the issues that have been addressed in thissection require action to be taken by the PlanningCommission in consultation with the Department ofExpenditure and the Central ministries. While some of theissues need to be tackled at the earliest, the preparationof the Twelfth Five Year Plan (2012-2017) presents anopportunity that cannot be missed for improving the extantplanning practices. For that the action needs to be takennow on priority, so that the ground work for the relevantchanges can be competed in the next 12 to 15 months andimplemented with effect from fiscal 2012-13, the first yearfor the next Five Year Plan.

Budget as a Tool for Policy Coherence (andspatial diffusion of reforms)

In a globalized world, where developments unfold andget transmitted rapidly and where these impulses arefurther conveyed to different part of the economy throughincreasingly integrated domestic markets, the policyresponse has to be instantaneous and well coordinated.Budget as a policy instrument, with an annual operationalhorizon, and the flexibility to intervene rapidly and byintegrating policy announcements with the required fiscalmeasures, is uniquely placed to respond to suchchallenges. This was demonstrated, for example, in thewake of recent global economic slowdown precipitated bythe unprecedented financial crisis in the developed world.The Government of India addressed the crisis by executingsuccessive tranches of fiscal stimulus between December2008 and July 2009, synchronising several policy measures(trade, credit, social security and financial prudence) withbills seeking supplementary budgetary grants forimplementing fiscal expansion. These measures created a

VOL. 77, NOS. 7–8 267

coherent policy response which worked to arrest theslowdown in the Indian economy and helped in a quickrecovery of the growth momentum.

While policy announcement in the course of a yearcan be linked post facto to the required fiscal measures,but by doing so in the Budget Speech, especially whenthere is scope to do so, creates policy synergies andpositive externalities, including through convergence ofexpectations among investors (business sentiments) andconsumers (consumer confidence), which then creates abetter chance for the policy measures to yield the desiredresults.

Of course, such a step requires budget to be more ofa collaborative exercise between Central ministries andgovernments at state-level and based on rigorous analysisthat ensures coherence and coordination in policyformulation and its implementation. There have been somemeasures taken in this direction in the past few years,some were mentioned briefly in the preceding sections;however a significant amount of work in this contextremains to be addressed.

There are three levels at which the Union Budgetand the Finance Minister’s budget speech can be usefulin bringing about greater policy coherence and encouragespatial diffusion of reforms. These relate to thecoordination between the Central ministries and the UnionFinance Ministry, between Union Finance Ministry (andCentral ministries) and the State Governments and betweenthe Union Government (Union Finance Ministry) and theglobal economy. Each of these levels of engagement andthe scope for further improvement in the context of budgetpreparation is addressed in the following paragraphs.

Central Ministries and the Union FinanceMinistry : The coordination required between the Centralministries and the Union Finance Ministry, in the contextof the budget is not confined only to the inter-ministerialallocations for plan and non-plan resources, but it alsocovers (with the Department of Expenditure) pre-sanctionappraisal of major schemes/projects (on both plan and non-plan side), the overall expenditure management, preparationof the Central Government Accounts, financial aspects ofCentral Government, human resource management andmonitoring of public expenditure outcomes. Sector specificpolicy initiatives are largely the mandate of the concernedsubject ministry and are generally discussed andcoordinated with the Ministry of Finance only if there arefinancial and macroeconomic implications, or there arecross-sectoral implications.

Based on the approved Five Year Plans, the progress