Indian Financial System Dba1749

193

MBA (DISTANCE MODE) DBA 1749 INDIAN FINANCIAL SYSTEM III SEMESTER COURSE MATERIAL Centre for Distance Education Anna University Chennai Chennai – 600 025

-

Upload

captsanthosh -

Category

Documents

-

view

83 -

download

6

description

anna university

Transcript of Indian Financial System Dba1749

MBA(DISTANCE MODE)

DBA 1749

INDIAN FINANCIAL SYSTEM

III SEMESTERCOURSE MATERIAL

Centre for Distance EducationAnna University Chennai

Chennai – 600 025

DrDrDrDrDr.T.T.T.T.T.V.V.V.V.V.Geetha.Geetha.Geetha.Geetha.GeethaProfessor

Department of Computer Science and EngineeringAnna University Chennai

Chennai - 600 025

DrDrDrDrDr.H.P.H.P.H.P.H.P.H.Peereereereereeru Mohamedu Mohamedu Mohamedu Mohamedu MohamedProfessor

Department of Management StudiesAnna University Chennai

Chennai - 600 025

DrDrDrDrDr.C.C.C.C.C. Chella. Chella. Chella. Chella. ChellappanppanppanppanppanProfessor

Department of Computer Science and EngineeringAnna University Chennai

Chennai - 600 025

DrDrDrDrDr.A.K.A.K.A.K.A.K.A.KannanannanannanannanannanProfessor

Department of Computer Science and EngineeringAnna University Chennai

Chennai - 600 025

Copyrights Reserved(For Private Circulation only)

Editorial Board

ii

Author

MrMrMrMrMr. Mahammad R. Mahammad R. Mahammad R. Mahammad R. Mahammad Rafafafafafi Syi Syi Syi Syi Syed, AICWAed, AICWAed, AICWAed, AICWAed, AICWADeputy Manager Finance,

ETA General (P) Ltd, Seethakathi Chamber,5th Floor, 688, Anna Salai,

Chennai - 600 006

Reviewer

DrDrDrDrDr. J. J. J. J. J. Gopu. Gopu. Gopu. Gopu. GopuAssistant Professor,

Management Studies,BSA Crescent Engineering College

Chennai - 600 048

iii

ACKNOWLEDGEMENT

The author has drawn inputs from several sources fo©r the preparation of this course material, to meet therequirements of the syllabus. The author gratefully acknowledges the following sources:

(i) Indian Financial System by M Y Khan, the McGraw-Hill Companies.

(ii) The Indian Financial System Markets, Institutions and Services byBharati V. Pathak, Pearson Education.

(iii) Financial Management by Ravi M. Kishore, Taxman’s Publicaion.

(iv) Professional Approach to Corporate Laws and Secretarial Practice by Munish Bhandari, BharatLaw House Pvt. Ltd, New Delhi.

(v) Advanced Accounting Volume I issued by the Institute of Chartered Accountants of India.

(vi) SEBI website, RBI website, BSE, NSE and OTCEI websites.

In spite of at most care taken to prepare the list of references any omission in the list is only accidental andnot purposeful.

Mr. Mahammad Rafi Syed

Author

v

DBA 1749 INDIAN FINANCIAL SYSTEM

UNIT I INTRODUCTION

Indian financial system- Introduction – Institutional setup-savings and instruments- Money, Inflation and Interest,Banking and Non-Banking financial intermediaries- Financial markets-classification – Financial sector reforms-institutional structure- Discount Finance House of India (DFHI)- SEBI –Stock exchange- OTCEI –money andCapital markets –Characteristics and objectives –money market instruments –securities market in India –Regulatory framework.

UNIT II COMMERCIAL BANKS

Commercial banks –Functions and roles-Sources and application of funds-asset structure –Profitability –Regulatoryreforms –Deposits and advances –Lending rates –Reserve Bank of India.

UNIT III DEVELOPMENT BANKING

Development banking – Features, functions and roles-Term loans- Appraissal- Industrial Development Bank OfIndia – State Financial Corporation – Specialised development Finance insitutions – Investment banking-Merchantbanking- Institional framework- Venture capital- Credit ranking – Factoring services leasing and hire purchase –Insurance services.

UNIT IV NEW ISSUES MARKET

New issues market- Functions and issue mechanism- Book building – Reforms and investor protection –Relationshipbetween new isues market and stock exchange.

UNIT V MUTUAL FUNDS

Mutual funds in India – Regulatory mechanism – SEBI mutual fund guideliness – Mutual fund schemes – IRDA(Insurance Regulatory and Development Authority) regulations – Securitisation and assets reconstructioncompanies.

REFERENCE

1. Indian Financial System, M.Y.Khan, Tata Mcgraw Hill.

vii

CONTENTS

UNIT - IFINANCIAL SYSTEM IN INDIA

1.1 INTRODUCTION 11.2 LEARNING OBJECTIVES 21.3 INDIAN FINANCIAL SYSTEM 2

1.3.1 Savings and Investments 51.3.2 Types of Savings 81.3.3 Investments 91.3.4 Interest Rates and Inflation 10

1.4 FINANCIAL INSTITUTIONS 111.4.1 Financial Intermediaries 111.4.2 Financial Markets 181.4.3 Financial Instruments 271.4.4 Financial Services 28

1.5 FINANCIAL SECTOR REFORMS 281.6 BANKING SECTOR REFORMS 301.7 DISCOUNT AND FINANCE

HOUSE OF INDIA (DFHI) 311.8 MONEY LAUNDERING 321.9 DERIVATIVES MARKETS 331.10 OVER THE COUNTER EXCHANGE OF INDIA (OTCEI) 351.11 SECURITIES MARKET IN INDIA – REGULATORY REFORMS 371.12 REFORMS IN THE SECONDARY CAPITAL MARKET 39

UNIT IICOMMERCIAL BANKS

2.1 INTRODUCTION 472.2 LEARNING OBJECTIVES 472.3 BANKING HISTORY AND ITS DEVELOPMENT IN INDIA 472.4 TYPES OF BANKS 49

2.4.1 Public Sector Banks 492.4.2 Private Sector Banks 53

ix

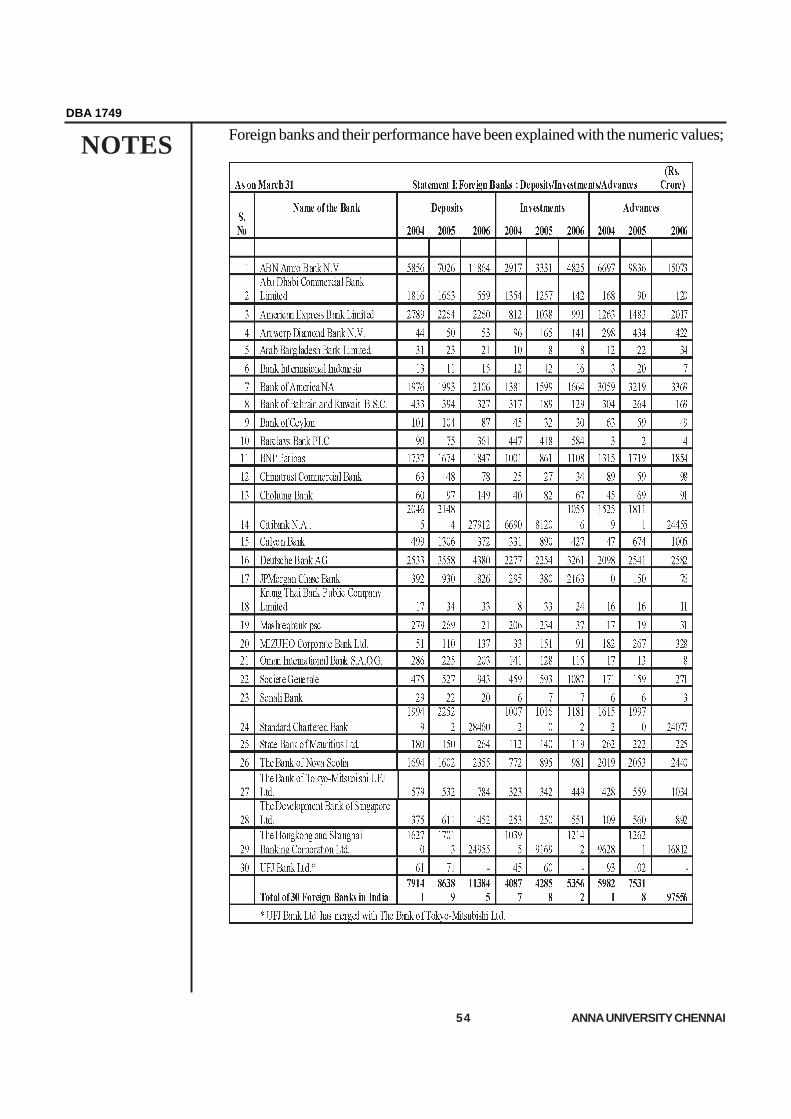

2.4.3 Foreign Banks in India 532.4.4 Regional Rural Banks 58

2.5 FUNCTIONS OF COMMERCIAL BANKS 592.6 ROLE OF COMMERCIAL BANKS 632.7 CHARACTERISTICS OF BANKS 642.8 SOURCES AND APPLICATION OF FUNDS 64

2.8.1 Source of Funds its Structure 652.8.2 Application of Funds and its structure 66

2.9 BANKING REGULATORY REFORMS 692.10 RESERVE BANK OF INDIA 70

2.10.1 Central Board 702.10.2 Functions Of The Board For Financial Supervision (Bfs) 712.10.3 The Main Functions Of The Reserve Bank Of India Are 722.10.4 Subsidiaries Of Reserve Bank Of India 74

UNIT IIIDEVELOPMENT BANKING

3.1 INTRODUCTION 773.2 LEARNING OBJECTIVES 783.3 FEATURES OF DEVELOPMENT BANKS 783.4 FUNCTIONS OF DEVELOPMENT BANKS 783.5 DEVELOPMENT BANKS 79

3.5.1 The Industrial Development Bank Of India(Idbi) 793.5.2 Industrial Investment Bank of India (IIBI) 803.5.3 Industrial Financial Corporation of India (IFCI) 813.5.4 The Export Import Bank of India (EXIM) 823.5.5 Tourism Finance Corporation of India (TFCI) 83

3.6 REFINANCE INSTITUTIONS 843.6.1 Small Industrial Development Bank of India (SIDBI) 843.6.2 National Bank for Agriculture and Rural

Development (NABARD) 853.7 SPECIALIZED FINANCIAL INSTITUTIONS 86

3.7.1 Infrastructure Development Finance Company (IDFC) 863.7.2 IFCI Venture Capital Funds 873.7.3 ICICI Venture Capital Fund 87

3.8 MERCHANT BANKING 883.9 VENTURE CAPITAL 90

x

3.10 CREDIT RANKING 933.10.1 Credit Rating Agencies in India 95

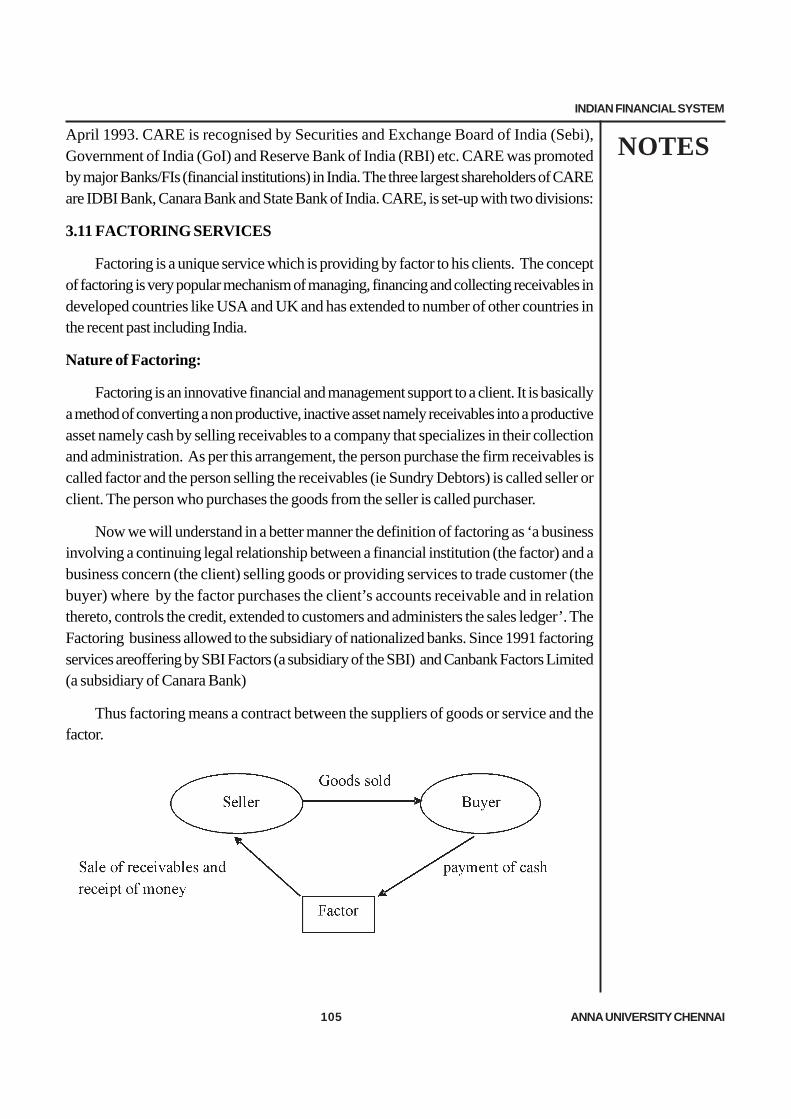

3.11 FACTORING SERVICES 1053.11.1 International Factoring: 1083.11.2 Forfaiting: 109

3.12 LEASING AND HIRE PURCHASE 1093.12.1 Leasing: 1093.12.2 Hire Purchase 112

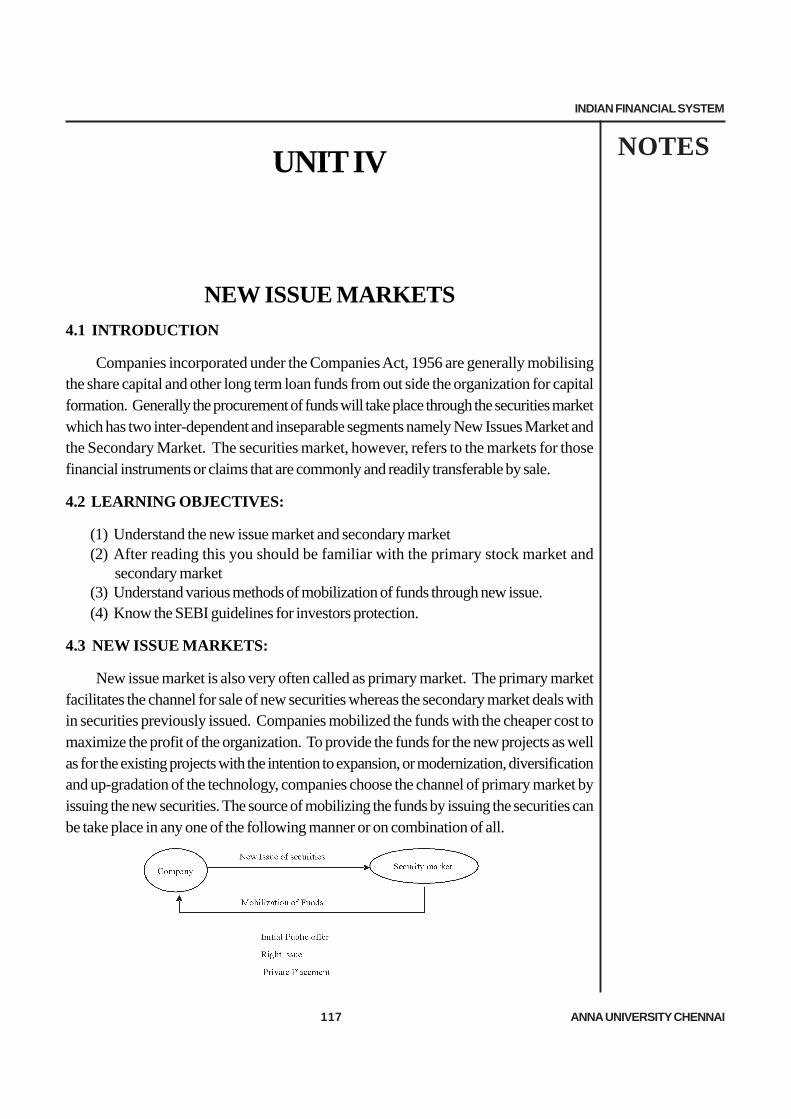

UNIT IVNEW ISSUE MARKETS

4.1 INTRODUCTION 1174.2 LEARNING OBJECTIVES 1174.3 NEW ISSUE MARKETS 117

4.3.1 Primary Stock Market 1184.3.2 Secondary Stock Market 118

4.4 NEW ISSUE MARKET – ISSUE MECHANISM 1204.4.1 Un-listed Companies – Initial Public Offer 1214.4.2 Pricing of Issues 1234.4.3 Initial Public Offer (IPO) 126

4.5 PRIVATE PLACEMENT 1344.5.1 Preferential Issues 1344.5.2 Qualified Institutional Placements (QIP’s) 1354.5.3 Issue of capital by designated financial institution 1354.5.4 OTCEI issues 135

4.6 SEBI (DISCLOSURE AND INVESTOR PROTECTION)GUIDELINES’ 2000 136

UNIT VMUTUAL FUNDS

5.1 INTRODUCTION 1395.2 LEANING OBJECTIVES 1405.3 MUTUAL FUNDS IN INDIA 1405.4 ADVANTAGES AND DISADVANTAGES OF MUTUAL FUNDS 141

5.4.1 Advantages of Mutual Funds 1415.4.2 Disadvantages of Mutual Fund 143

xi

5.5 TYPES OF MUTUAL FUNDS 1455.6 NET ASSET VALUE 1485.7 SEBI (MUTUAL FUND) REGULATIONS, 1996. 1495.8 ASSET MANAGEMENT COMPANY 1545.9 SEBI (MUTUAL FUND) REGULATIONS, 1996 1595.10 MUTUAL FUNDS AND CREDIT RATING 1655.11 INSURANCE 167

5.11.1 Introduction 1675.11.2 Life Insurance Businesses in India. 1695.11.3 Type of products under Life Insurance Business 1705.11.4 Types of general insurance policies 1725.11.5 Insurance Regulatory and Development Authority Act, 1999 173

5.12 SECURITISATION AND ASSETS RECONSTRUCTIONCOMPANIES 1755.12.1 Guidelines: Issued by the RBI Has Been Reproduced

Which are In The Nature of Recommendatory 177

xii

INDIAN FINANCIAL SYSTEM

NOTES

1 ANNA UNIVERSITY CHENNAI

UNIT I

FINANCIAL SYSTEM IN INDIA

1.1 INTRODUCTION

In general to survive and success we need to have an adequate finance and in fact thecredibility of an enterprise depends upon its sound financial position. The term Financecan be expressed as mobilization of funds to meet the desired objectives and goals of theorganization. The financial functions can be viewed as Investment decisions, Financial Mixdecisions, Dividend or Profit allocation decisions and short-term asset mix decision. Itmay be difficult to separate the finance functions from the other functions like production;marketing and so on.

For example, recruitment of skilled and unskilled employees in the productiondepartment is clearly a responsibility of the production department with the help of humanresource department; but it requires payment of wages and salaries and other monetarybenefits, and hence involvement of finance is an inseparable in the entire organization system.A system may be viewed as a set of sub-systems with so many elements which areinterdependent and interlinking with each other to produce the purposeful result with in theboundary. Hence, the term system in the context of finance means a set of complex andclosely connected financial institutions, instruments, agents, markets and so on which areinterdependent and interlinking with each other to produce the economic growth with inthe country.

A well organised financial system provides adequate capital formation through savings,finance and investments. An investment depends upon Savings and inturn Savings dependsupon earnings of an individual or profits of the organisation. For example Mr. X currentearnings Rs 10 lac per annum and his current expenditure is Rs 9 lac per annum then hissavings becomes Rs 1 lac, which he can invest, like wise if the company earns more profitsit leads to more investments into various sectors.

In fact savers may or may not have technical or professional skills to convert ortransfer their savings into active investments. This transfer process is effectively fulfilled bythe financial system to facilitate economic growth through the channel of finance. We can

NOTES

2 ANNA UNIVERSITY CHENNAI

DBA 1749

recollect at this point of time the term Financial Management which means procurement offunds and their effective utilization to maximize the profit of the organisation.

1.2 LEARNING OBJECTIVES:

(1) Learn the concept of financial growth in India(2) Understand about the financial intermediaries(3) Under standing about various financial instruments and services(4) Understand the regulations framed by the SEBI with respect to capital market and

financial market.

1.3 THE INDIAN FINANCIAL SYSTEM – AN OVERVIEW

In the early 1950’s India adopted a closed-circle character which denotes narrowgrowth in industrial entrepreneurship, limited industrial securities market and more restrictionson financial intermediaries and so on. In the recent past the Indian Financial System hasunder gone sea changes and invented many new channels of financial sub-systems throughthe process of financial reforms.

Institutional Setup:

The concept of nationalization came in the year 1948 by nationalizing the ReserveBank of India. The Reserve Bank of India was set up in the year 1935 with the sharecapital of Rs 5 Crore which was entirely owned by the private share holders in the beginning.The Reserve Bank of India is acting as central bank in India and it is different from theCentral Bank of India. After India’s Independence, in the context of close integration itspolicies and those of the Government, the Reserve Bank became a state owned institutionfrom 1st January 1949. The Banking Regulation Act was enacted in the same year (1949)to provide regulations and supervision of Commercial Banks.

In 1951, there were 566 private commercial banks in India and majority of whichwere confined to major cities, however the savings in the form of bank deposits accountedeven less than 1% of the national income, whereas expected 12% savings from householdsector. At this point of time, the RBI as well as Government of India emphasizes to prepareplans which will facilitate to mobilise savings in order to raise the investment rate andchannel resource to identified sectors of the economy, notably agriculture and industry.

In this context the first Five Year Plan was taken birth in the year 1951, the planningstrategy was based on the concept of a mixed economy were the public and private sectorsplays vital role with regard to mobilization of savings and enhancing the investment activitiesin India. Hence, the Reserve Bank of India was took the responsibility of developing theinstitutional infrastructure in the financial system. The Commercial Banking system in Indiawas expanded to take care of general banking activities of accepting the deposits andfacilitating the short term working capital loans to the industry. In the absence of well

INDIAN FINANCIAL SYSTEM

NOTES

3 ANNA UNIVERSITY CHENNAI

developed capital market, establishment of Development Finance Institutions (DFI’s) andState Finance Corporations (SFC’s) are inevitable to cater the long term financing needsof the industry at the national and state level respectively.

The concept of nationalization was followed in the subsequent period by setting up ofthe State Bank of India in the year 1956 by taking over the then Imperial Bank of India. Infact the Imperial Bank was formed in the year 1921 by the process of amalgamation ofthree presidency banks (namely the Bank of Bengal, the Bank of Bombay and the Bank ofMadras). The State Bank of India is not a nationalized bank; however it was set up by theGovernment of India by taking over the Imperial Bank of India.

It is important to note that the establishment of Unit Trust of India in the year 1963 byan Act of Parliament to provide a channel for retail investors for participating in the primaryas well as secondary market (namely capital market). The Unit Trust of India has beenestablished with the purpose of promoting the development of securities markets, bymobilizing household savings for investment in corporate stocks and bonds market. Initiallythe UTI was set up by the RBI and later on in the year 1978 UTI de-linked from the RBIand the Industrial Development Bank of India (IDBI) took over the regulatory andadministrative control in the place of RBI. Further the UTI has been bifurcated into twoseparate entities in the year 2003. One is the Specified Undertaking of the Unit Trust ofIndia which comes under the rules framed by the Government of India and other one iscalled UTI Mutual Funds Ltd which is functioning under the Mutual Funds Regulations.The Unit Trust of India is India’s first Mutual Fund Organisation.

The unforgettable history in the Indian Financial System is nationalization of 14 privatebanks in the year 1969 by way of an ordinance issued by the Government of India, whichwas later on replaced by an act of parliament. Further six major commercial banks in theprivate sector whose deposits worth more than or equal to Rs 200 crore were nationalisedin the year 1980.

For the purpose of providing the risk coverage security for the life of Individuals theLife Insurance Corporation of India was set up in the year 1956 by merging 245 domesticand foreign insurance companies that were operated in India. The Life Insurance of Indiais the largest Non-banking Financial Institution which mobilizes the huge savings from thepublic at large and the funds will be deployed to the best advantage of the investors as wellas with the best interest of the nation. In order to provide the security to non-life segmentthe General Insurance Corporation (GIC) was established in the year 1972. The GeneralInsurance Corporation is not meant to offer returns but is a protection against contingencieslike accidents, illness, fire, burglary etc. The General Insurance Corporation has foursubsidiaries namely (i) The National Insurance Company Limited (ii) New India AssuranceCompany Limited (iii) Oriental Insurance Company and (iv) United India InsuranceCompany Limited.

NOTES

4 ANNA UNIVERSITY CHENNAI

DBA 1749

In December, 2000, the subsidiaries of the General Insurance Corporation of Indiawere restructured as independent companies and at the same time GIC was converted intoa national re-insurer. Parliament passed a bill de-linking the four subsidiaries from GIC inJuly, 2002. At present there are 14 general insurance companies including the ECGC andAgriculture Insurance Corporation of India and 14 life insurance companies operating inthe country.

A land mark in the history of co-operative credit system was the establishment ofNational Bank for Agriculture and Rural Development (NABARD) in the year 1982 withthe objectives to create institutional arrangements at national level for financing, guiding andcontrolling the co-operative credit system.

The need to catering the capital market or securities market in India was fulfilled bythe stock exchanges; in fact the Bombay Stock Exchange (BSE) is the 1st stock exchangein India which was established in the year 1875. The main objectives of BSE are to promote,develop, and safeguard the interest of members as well as investors. Subsequently theNational Stock Exchange (NSE) was established in the year 1992 with the intention toprovide a nation wide stock trading facilities to the participants. Over The Counter Exchangeof India (OTCEI) was incorporated in 1990 under the Companies Act 1956 and isrecognized as a stock exchange under Section 4 of the Securities Contracts RegulationAct, 1956. The OTCEI was set up to aid small companies or enterprising promoters inraising finance for new projects in a cost effective manner and to provide investors with atransparent & efficient mode of trading.

Investor’s attention is highly dragged by the credit rating agencies in India. CreditRating is the assessment of a borrower’s credit performance. Credit Rating helps investorsto decide their investment pattern. Basically the credit rating has symbols which denote theperformance or credit worthiness of the respective companies. These symbols may beAAA, AA, BBB, B, C, D to denote the performance of the respective companies to theinvestor. For example AAA which means highest safety in terms of repayment of principaland interest and in case of BBB which means moderate safety in terms of timely paymentof interest and principal. In India the rating will start with the request of the company,however, the Reserve Bank of India and Securities and Exchange Board of India madecredit rating as mandatory for the issue of commercial paper and certain categories ofsecurities and debentures.

Accordingly following credit rating institutions are established in India namely (a) CreditRating Information Services of India Limited (CRISIL) was established in the year 1988,(b) Investment Information and Credit Rating Agency of India Limited was established inthe year 1990 and (c) Credit Ratings Analysis and Research Limited (CARE) was establishedin the year 1993.

INDIAN FINANCIAL SYSTEM

NOTES

5 ANNA UNIVERSITY CHENNAI

Apart from the above, the Non-Banking Financial Institutions namely the DevelopmentFinancial Institutions or Term lending financial institutions and Non-Banking FinancialCompanies (NBFC’s) are taken the birth since 1950. These institutions are playing vitalrole in the Indian Financial System by providing medium and long term financial assistanceand engaged in promotion and development of industry, agriculture and other key sectors.The Development Financial Institutions so called development banks performs the specialtasks which generally not undertaken by commercial banks. These financial institutions canbe grouped into all India Financial Institutions as well as State Level Institutions which canbe discussed in detail under Unit III.

It is needless to say that The Indian Financial System highly regulated by the regulatingauthorities namely Reserve Bank of India (RBI), The Securities Exchange Board of India(SEBI), Securities Contract (Regulation) Act, The Insurance Regulatory and DevelopmentAuthority (IRDA), The Foreign Exchange Management Act (FEMA), Companies Actand other regulatory bodies from time to time.

1.3.1 Savings and Investments

Domestic savings are inevitable for putting India on a high growth path. Substantialsavings are possible with liberalization of financial markets and strong structural reforms.Financial Intermediaries provide a link in between saving and investment. Basically thesaving of individuals depends on their income, their occupation and size of the city inwhich they resides. Like wise investments also depends on return, liquidity and security.At this junction we would like to discuss three types of saving (economic) units which areessential to understand relationship between savings and investments.

(i) Saving-surplus units or Surplus Spending Economic Units(ii) Saving-deficit units or Deficit Spending Economic Units(iii) Neutral Units

(i) Saving-surplus units or Surplus Spending Economic Units:

Excess of income over expenditure of house hold sectors and other sectors can beclassified as Saving-surplus units. These units try to lend or invest their surplus into profitableinvestments with the help of financial intermediaries. These financial intermediaries play avital role to transfer the savings of the Savings-surplus units to the Savings Deficit units.This process is Called capital formation.

(ii) Saving-deficit units or Deficit Spending Economic Units:

Excess of expenditure over income of the units or sectors. These units finance theirneed by borrowing or by decreasing their financial assets. The surplus saving units anddeficit units can be brought together by the Financial Intermediaries. In India, the corporatesectors and the Government sectors can be categorized as saving-deficit units.

NOTES

6 ANNA UNIVERSITY CHENNAI

DBA 1749

(iii) Neutral Units:

Means those units whose expenditures are equal to savings.

The role of financial system in the saving and investment can be measured in terms ofNational Income Accounts and Flow of Funds Accounts.

(i) National Income Accounts:

In India, the national income accounts prepared by the Central Statistical Organisation(CSO) and the same published by the Government of India. The National Income Accountsprepared based on the entire production in the Indian economy and earnings derived fromthe production. The Indian Economy can be classified into six categories:

(i) Agricultural Sectors, Mining Sectors, Fishing Sector and so on(ii) Manufacturing Sector, Real Estate Sector and Power Sector and so on.(iii) Service Sector, Transport Sector and Trade or commerce Sector etc.(iv) Banking and Insurance Sector and Development Banking sector etc.,(v) Public Administration and Defense Sector etc.,(vi) Export and Import Sector namely Foreign Sector.

On combination of all the above sectors out put net result can be termed as GrossNational Product (GNP). If we deduct from the GNP the non cash expenditure (monetarysavings) namely the depreciation we will get the Net National Product (NNP). The NetNational Product can be measured as net production of goods and services in the IndianEconomy during the year. It gives an idea of the net increase in the total production in thecountry.

So many times we use to read in the news papers and hear from our friends regardingthe Gross Domestic Product (GDP). It is nothing but gross out put of the Indian Economyexcept Foreign Sector. It means to say increase in savings causes increase in investmentswhich ultimately causes increase in agriculture yield, manufacture and service sectors output, as a result growth in trade and commerce, which leads to increase in the Gross DomesticProduct (GDP).

The National Income Accounts represents macro economic data such as GrossDomestic Product, Gross National Product and Net National Product along with savingsand investments. The National Income Accounts also provide us the information regardingSurplus Saving Units and Surplus Deficit Units but does not provide us link between theseunits. This gap can be filled up by the Flow of Funds Accounts by interlinking varioussectors of the Indian Economy.

INDIAN FINANCIAL SYSTEM

NOTES

7 ANNA UNIVERSITY CHENNAI

(ii) Flow of Funds Accounts:

The flow of funds explains us the role of financial system in the generation of income,savings and investments. These accounts highlight the channel of cross intersectioncomparison between savings and investments. The nature of financial activities in the IndianEconomy can be studied under the flow of funds accounts. Flow of Funds accounts providesthe information regarding the savings and investments of the Indian Economic Sectorsnamely Hose-hold Sectors, Private Sectors, Banking sectors, Public Sectors and so on soforth. These sectors participate in the financial activities by borrowing from surplus savingunits for the purpose of lending to the saving deficit units.

Domestic Savings:

Savings can be broadly based on the three sectors namely

(i) Household Savings(ii) Private Corporate Savings(iii) Public Sector Savings

(i) Household Savings:

(a) The household sector savings are a predominant source of domestic savings (about76 percent in 2004-05) and a substantial part of the growth in the GD rate emanates fromthe growth. The latest annual report of the Reserve Bank of India gives the data on householdsavings which forms the largest component of aggregate savings in India. The savings ofhouseholds can be viewed as Individuals, Proprietor ship or Partnership firms and allNon-corporate enterprises.

(b) Household savings consist of two segments namely savings in the form of physicalassets and financial assets. The physical assets include land and buildings, plant andmachinery and stocks held by individuals, firms and other non-corporate enterprises. Thefinancial assets consists of currency holdings of households, deposit holdings of banks andnon-bank companies, life insurance fund, provident and pension funds, the Unit Trust ofIndia and other financial institutions, claims on Government consisting of net purchases ofbonds and small savings assets by households, and the net purchases of shares anddebentures by households.

(c) Prior to financial sector reforms, household savings will primarily be in the form ofphysical assets and as the financial system matures, financial intermediation will channelisemore savings into the financial side and finance more productive investments. Till the mid-nineties, household savings in financial assets were more than household savings in theform of physical savings. Now as per the latest estimates available, it is the physical savingsthat are more than those in financial assets. In fact more than 52 per cent of the totalhousehold savings are in the form of physical assets compared to 44 per cent in the early

NOTES

8 ANNA UNIVERSITY CHENNAI

DBA 1749

nineties. This shift in saving towards physical assets shows is that, at present householdsavings in the system are being driven not by current incomes, but on expected future cashflows.

(ii) Private Sectors Savings:

Private corporate savings comprises of savings from private financial institutions, non-government institutions and non financial companies and so on so forth. As per the CentralStatistical Organisation, data on corporate finances indicate a general improvement incorporate profitability during the current year. The rate of private corporate savings stoodat around 3.7 per cent of GDP in the 1990s improved to 4.8 per cent in 2004-05. This ratecould be slightly lower in 2005-06 as reflected in a slowdown in profitability of the corporatesector as compared to 2004-05. Yet, corporate results for the first two quarters of 2006-07 indicate a buoyant growth in company profits which could translate into improved rateof corporate savings for the current financial year (2006-07).

(iii) Public Sector Savings:

Public Sector Savings consist of savings from Government sectors, AdministrativeDepartments and so on. The increases in public sector savings have been the result ofsignificant reductions in the dissavings of the government administration. The reduction indissavings by the government as mirrored in reducing revenue deficits of the central andstate governments have halved from 7 per cent of GDP in 2001-02 to 3.7 per cent in2004-05; it was further fallen to 3.1 per cent in 2005-06. Savings from departmententerprises like railways, telecom and infrastructure developments remained largely stagnantcontributors to the Gross Development Product (GDP).

With efforts being directed to meet the targets, public sector savings can be expectedto be further consolidated in the current year; the budget estimates for 2006-07 havepegged revenue deficits of the central government (as a percentage of GDP) at 2.1 percent. As per the RBI’s latest compilation of state budgets data reveal that the combinedrevenue deficits of states have declined from 1.2 per cent in 2004-05 to 0.5 per cent eachin the next two years.

1.3.2 Types of Savings

We have various types of savings which can be expect from the household savings,private sector savings and public sector savings as follows:(a)a)Regular Savings Accounts:

These accounts are termed as Savings Bank Account, Recurring Deposits and CurrentAccounts. Saving account and Recurring Deposits gives some interest, but current accountgives nil rate of interest but it allows you to operate with negative balance. Savings Bankaccounts are sometimes called “passbook” accounts. It is an easy way to start a saving

INDIAN FINANCIAL SYSTEM

NOTES

9 ANNA UNIVERSITY CHENNAI

program because of low opening deposit requirements. There may be limitations on thenumber of withdrawals. Today banks offer a wide range of financial services to help youto save.

(b) Certificates of Deposit (CDs):

Savings can be parked in the form of “term deposit” accounts in the banks becauseyou agree to leave your money in the account for a specified period (called the “term” or“maturity”) in return the institution giving you a higher rate of interest. Terms vary from1year to 10 years. Some CDs do not allow additional deposits. Typically, the funds arereinvested after the term is reached, unless you specify otherwise within a given period.Usually, there are also penalties for early withdrawal.

(c) Savings in the Bonds:

Savings can be converted into the various bonds like Government Bonds, PublicSector Undertaking Bonds, Corporate Bonds, State Loans, Treasury Bills and so on.

(d) Savings in the Institutional Investments:

The Life Insurance Corporation of India (LIC), The Unit Trust of India and EmployeesProvident Fund (EPF) bagged nearly one third of total financial savings in India. Savings inthe form of Insurance policies are products designed to cover the risks of losses fromcertain predetermined events. Savings in the form of Mutual Funds is an emerging area andstill 80% of the mutual funds market occupied by the UTI. Savings in the form of Pensionplans are designed to provide for the retirement of the investor. These institutional investorsprocure the savings from the household sectors, private sector and public sector units.

(e) Savings in company shares and securities:

Savings of the household, private and public sector units can be invested in to thecompany shares, debentures, bonds and deposits etc,. These savings may be short term;medium term or long term depends on the interest of investors.

1.3.3 Investments

The investment process starts when savings facilitate to invest in various profitableventures. Banks and financial institutions lend their funds to the household units and corporateunits. The investments should earn reasonable and expected rate of return on investments.Certain investments like bank deposits, public deposits, debentures bonds etc., will carryfixed rate of return namely interest payable periodically. In case of investments in shares ofcompanies, the periodical payments in the form of dividend are not assured, but it mayensure higher return than fixed income investments but carries higher risk.

NOTES

10 ANNA UNIVERSITY CHENNAI

DBA 1749

Sources of Investible Funds

Apart from the indicators of domestic savings, the other widely quoted indicators ofinvestment activities are the direct sources of investible funds, namely, capital raised bycompanies in the primary markets, loan disbursements by various financial institutions aswell as the banking sector and foreign investment inflows. While equities in capital marketsare an avenue for household sector savings, they also represent a portion of the investiblefunds available to the corporate sector. Investments in the shares and securities can bedirectly invest by the Foreign Direct Investments and indirectly invest by the ForeignInstitutional Investors. Investments highly influenced by the interest rates and inflation.

1.3.4 Interest Rates and Inflation

There is linear relationship between interest rates and inflation. In other words, bothtend to move either up or down together. However, the caveat is that interest rates willalways follow inflation rates or, put simply, when inflation goes up, interest rates go up andwhen inflation comes down, interest rates tend to fall. This relation ship can be explained inthe following chart.

Inflation rates increases when the economy is overheating. It means to say that whenReserve Bank of India prints lot of money or when macro economic policies go bad. Forexample we assume that the Reserve Bank and Government of India follows the righteconomic policies. hence, money becomes cheaper because of more printing or there islow interest rate. This position can be described as “Loose Money Policy”. We know thatMoney is the back bone of any economy. When the interest rate is low, persons start toborrow the money to invest into their business or buy things which they like. Over a periodof time the price they pay for the money is interest.

In India for the past few years the interest rates were low and people and corporateentities has been increased their borrowings for various purpose. For example Peoplebought residential houses, cars, air conditioners television set and so on and companiesbuilt factories, purchase plant and machineries, furniture and fixtures and so on.

INDIAN FINANCIAL SYSTEM

NOTES

11 ANNA UNIVERSITY CHENNAI

This situation denotes the economic growth which results rapid increase in incomesand profits as a whole increase in Gross Domestic Product. At this point of time prices forthe product will go up, as we know if demand increases the price of the product alsoincreases. Over a period of time, prices of goods tend to go up and that results in inflationbecause most of these goods are usually part of a basket that constitutes the WholesalePrice Index or the Consumer Price Index.

The Reserve Bank of India will take steps to increase the interest rates so as to coolthe economy. However, interest rates can not be increased beyond a particular level whichcauses the recession. At the level of higher interest rates money becomes costly this situationcan be called “tight money policy”. The intention of the Reserve Bank of India is that whenit increases rates, people and companies will borrow less and therefore there will be lesspurchases and investments.

Then over a period of time incomes of the people and profits of the companies willcome down as a result slow growth in Gross Domestic Product. At this point of timeinflation drops and the Reserve Bank of India will usually lower interest rates to strengthenthe economy. This cycle continues round the clock. This is an example through which wecan understand the interest, money and inflation relation ship. There are some other factorsmay also describe the relationship of interest, money and inflation.

1.4 FINANCIAL INSTITUTIONS

The Financial Institutions can be broadly grouped under (1) Financial Intermediaries,(2) Financial Markets, (3) Financial Instruments and (4) Financial Services which are mainpillars to the Indian Financial System

1.4.1 Financial Intermediaries

Financial Intermediaries also termed as Financial Institutions. We can classify thefinancial intermediaries into two groups one is organized financial intermediaries and otherone is unorganized financial intermediaries.

Organized financial intermediaries comes under the purview of regulating authoritiesnamely Reserve Bank of India, Securities Exchange Board of India, Companies Act,Securities Contract (Regulation) Act and so on. Whereas unorganized financial institutionsare not cover under the purview of these regulating authorities, such type of institutions are

Financial Internediaries Finanacial Markets Financial FinancialInrtruments Services

NOTES

12 ANNA UNIVERSITY CHENNAI

DBA 1749

called local money lenders, pawn brokers etc. Our study is mainly focusing on formal ororganized financial intermediaries only.

Organised financial intermediaries can be classified as Banking Institutions, Non-Banking Financial Institutions, Insurance Companies and Housing Finance Companies.These financial intermediaries plays vital role in the capital formation by means of mobilizingsavings and facilitating the allocation of funds in an effective manner.

These intermediaries provide the convenience to the small investors by mobilizingtheir savings in the form of divisibility and distribute the claims at the time of maturity orredemption.

The Structure of the Financial Intermediaries or Institutions can be depict as follows:

(A) Term Lending Financial Institutions (ie Development Banks)

(a) Industrial Financial Corporation of India (IFCI)(b) Industrial Investment Bank of India (IIBI)(c) Infrastructure Development Finance Company (IDFC)(d) Small Industrial Development Bank of India (SIDBI)(e) National Bank for Agriculture and Rural Development (NABARD)(f) The Export Import Bank of India(g) Industrial Development Bank of India (IDBI)(h) State Financial Corporations(i) State Industrial Development Corporations (SIDC’s) etc,

(B) Non-Banking Financial Companies (NBFC’s)

(a) Hire Purchase Finance Company(b) Equipment Leasing Companies(c) Housing Finance Companies(d) Venture Capital Fund Companies(e) Chit Fund Companies

INDIAN FINANCIAL SYSTEM

NOTES

13 ANNA UNIVERSITY CHENNAI

(f) Stock Broking Firms(g) Merchant Banking Companies etc,

(C) Investment Institutions

(a) Mutual Fund Companies (c) Pension Funds (d) Insurance Companies etc,

1.4.1.1 Banking Institutions

The term Financial Intermediary is handicapped in the absence of the banking sectors.The Indian Banking System regulated and monitored by Reserve Bank of India. The termbanking has been defined by the Banking Regulation Act as “the accepting, for the purposeof lending or investment, of deposits of money from the public, repayable on demand orotherwise and withdrawable by cheque, draft, order or otherwise”. From this definitionwe came to know two important functions of the banks one is acceptance of deposits andlending of funds.

The essential characteristics of banks:

(i) Acceptance of deposits from the public. (ii) Investment or lending the money to meet the short term, medium and long

term requirements. (iii) Repayable the deposits on demand or otherwise and (iv) Withdrawable by means of any instrument whether a cheque or otherwise.

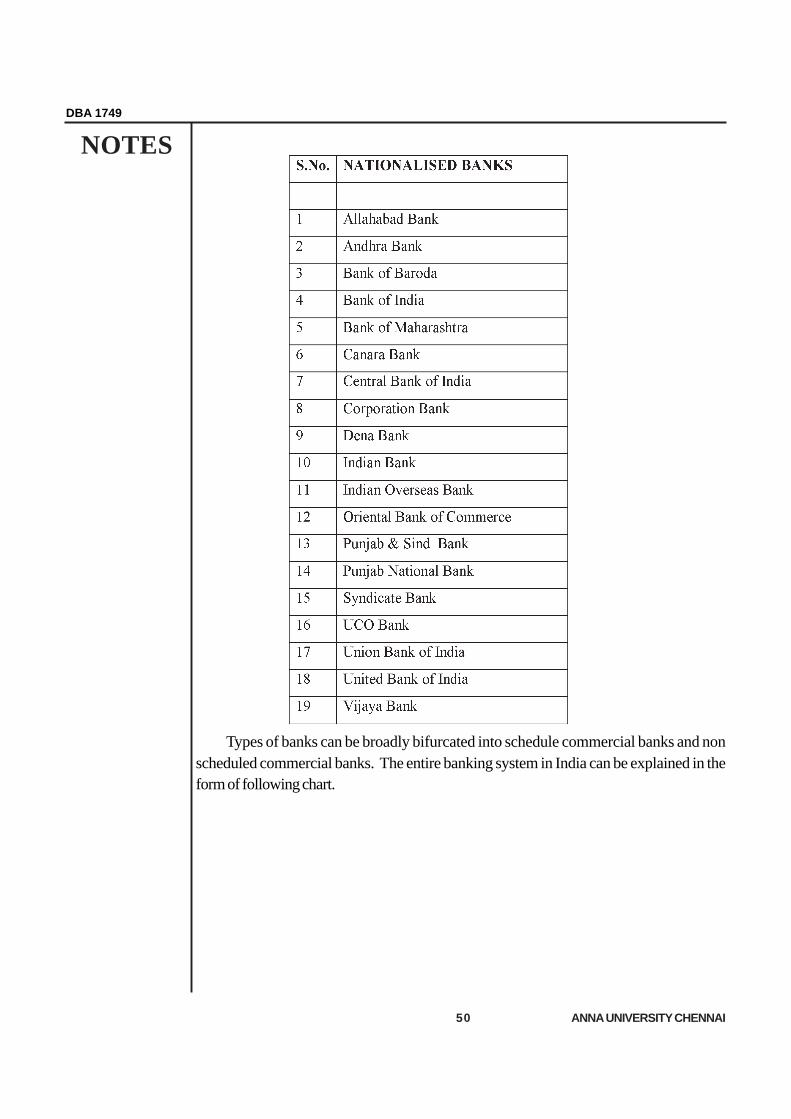

(a) Public Sector Banks in India

Public Sector Banks are those banks in which Government of India has major shareholding. No doubt public sector banks came to occupy dominant role in the bankingstructure. Before 1969, State Bank of India (SBI) was the only public sector bank inIndia, since then the following banks joined in the public sector banks list.

List of Public Sector Banks in India

(1) Indian Bank (2) Bank of India (3) Union Bank (4) Syndicate Bank (5) StateBank of Saurashtra (6) State Bank of Travancore (7) Bank of Maharashtra (8) VijayaBank (9) UCO Bank (10) Indian Overseas Bank (11) Punjab National Bank (12) DenaBank (13) State Bank of Hyderabad (14) State Bank of Bikaner & Jaipur (15) StateBank of India (16) State Bank of Mysore (17) State Bank of Indore (18) CorporationBank (19) Allahabad Bank (20) Andhra Bank (21) Canara Bank (22) Bank of Baroda(23) Oriental Bank (24) Punjab & Sind Bank (25) Industrial Development Bank of India(26) Industrial Credit and Investment Corporation of India (27) Unit Trust of India Bank(28) United Bank.

NOTES

14 ANNA UNIVERSITY CHENNAI

DBA 1749

(b) Private Sector Banks:

Private Banks have played a major role in the development of Indian banking industry.They have made banking more efficient and customer friendly. In the process they havejolted public sector banks out of complacency and forced them to become more competitive.

We have the following major private banks in India:

(1) Bank of Rajasthan (2) Bharat Overseas Bank (3) Catholic Syrian Bank (4)Centurion Bank of Punjab (5) Dhanalakshmi Bank (6) Federal Bank (7) HDFC Bank (8)ICICI Bank (9) IDBI Bank (10) IndusInd Bank (11) ING Vysya Bank (12) Jammu &Kashmir Bank (13) Karnataka Bank (14) Karur Vysya Bank (15) Kotak Mahindra Bank(16) SBI Commercial and International Bank (17) South Indian Bank (18) United WesternBank (19) UTI Bank (20) YES Bank

(c) Regional Rural Banks:

Regional rural banks in India penetrated every corner of the country and extended ahelping hand in the growth process of the country. Regional rural banks initially started itsbusiness to promote agricultural sector development. The State Bank of India has 30Regional Rural Banks spread over across 13 states in the country. There are other bankswhich function for the development of the rural areas in India. These Regional Rural Banksplays a vial role in rural banking in the economy of the country by providing the help andfinancing farmers, rural artisans, agriculturists, entrepreneurs and so on. They are The HaryanaState Co-operative Apex Bank Ltd, The National Bank for Agriculture and RuralDevelopment, The Haryana State Co-operative Apex Bank Ltd. commonly called asHARCOBANK, National Bank for Agriculture and Rural Development (NABARD),United Bank of India and Sindhanur Urban Southarda Co-operative Banks etc.,

(d) Co-operative Banks

Co-operative Banks in India are registered under the Co-operative Societies Act.The cooperative bank is also regulated by the RBI. They are governed by the BankingRegulations Act 1949 and Banking Laws (Co-operative Societies) Act, 1965. Cooperativebanks in India finance rural sectors in the areas such as farming, Cattle, Milk, personnelfinance, consumer finance and so on so forth.

By virtue of specialised knowledge, training, ability and professionalism theseintermediaries easily mobilise the funds in small denominations from the public at large andinvest in various types of investments by diversifying the risk involved in the investments togenerate optimum returns on investments which can be distributed by way of dividends orinterest to the investors at large.

INDIAN FINANCIAL SYSTEM

NOTES

15 ANNA UNIVERSITY CHENNAI

A well developed financial intermediary system promotes the sound financial marketswhich causes the economical growth in the country. Financial Intermediaries offer thefollowing services namely Issue Management, Underwriting, Portfolio Management,Corporate Advisory, Stock Broking, Capital Re-structuring, Merger and Acquisitionsand so on so forth. We will discuss in detail regarding banking sectors in the unit II.

1.4.1.2 Non Banking Financial Intermediaries

The term Non-Banking Financial Intermediaries can be bifurcate into three sub partsnamely (a) Term Lending Financial Institutions, (b) Non-Banking Financial Companiesand (c) Investments Institutions.

Term Lending Financial Institutions

These institutions also called as Development Banks. They are Industrial FinancialCorporation of India (IFCI), Industrial Investment Bank of India (IIBI), InfrastructureDevelopment Finance Company (IDFC), Small Industrial Development Bank of India(SIDBI), National Bank for Agriculture and Rural Development (NABARD), The ExportImport Bank of India, Industrial Development Bank of India (IDBI), State FinancialCorporations, State Industrial Development Corporations (SIDC’s) etc,

Industrial Finance Corporation of India (IFCI)

The Industrial Finance Corporation of India was established in the year 1948 asIndia’s first development bank. The main objective for which IFCI was established, are tomake medium and long term credit available to the industrial undertakings. The main functionsare direct financial support to industrial units for undertaking new projects, expansion,modernization, diversification etc., subscription and underwriting of public issues of sharesand debentures, guaranteeing of foreign currency loans and also deferred paymentguarantees, merchant banking, leasing and equipment finance.

Industrial Investment Bank of India (IIBI)

This institution was established in the year 1997 by converting the erstwhile IndustrialReconstruction Bank of India. The main functions of the Industrial Investment Bank ofIndia are; invest in the capital market instruments, leasing and hire purchase business,providing the short, medium and long term loans and underwriting the shares and so on.

Infrastructure Development Finance Company (IDFC)

IDFC was established in the year 1997 with the intention to promote consultancyand advisory services to state governments for formulating a power sector strategy, tointegrate the entire logistics chain in India, to provide the financial assistance to varioustelecommunication and Information Technology sectors, providing finance and projectservices for the development urban infrastructure and so on .

NOTES

16 ANNA UNIVERSITY CHENNAI

DBA 1749

Small Industrial Development Bank of India (SIDBI)

SIDBI was established by passing an Act under parliament in the year 1989. TheSIDBI provides services such as the principal financial institution for the promotion, financingand development of industries in the small scale sectors and to coordinate the functions ofother institutions engaged in similar activities.

National Bank for Agriculture and Rural Development (NABARD)

NABARD also came into exist in the year 1982 by an Act of parliament. It serves asan apex refinancing agency for the institutions providing investment and credit for promotingdevelopment activities in rural areas, coordinates and supervise the rural financing activitiesof all institutions engaged in developmental work etc,.

The Export Import Bank of India (EXIM Bank)

The Export Import Bank of India is a public sector financial institution was set up inthe year 1981. The main objective of this bank is financing, facilitating and promotingIndia’s trade and commerce, provides the project finance, Trade finance, Exim bank alsoact an intermediary for facilitating the forfeiting transaction between the Indian exporterand the overseas forfeiting agency etc.,

Industrial Development Bank of India (IDBI)

Industrial Development Bank of India (IDBI) was set up by an Act of parliament as awholly owned subsidiary of the Reserve Bank of India. Later on in the year 1976, theIDBI ownership was transferred to the Government of India. The main functions of IDBIare vested with the responsibility of co-ordinating the working of institutions engaged infinancing, promoting and developing industries.

It has evolved an appropriate mechanism for this purpose. IDBI also undertakes/supports wide-ranging promotional activities including entrepreneurship developmentprogrammes for new entrepreneurs, provision of consultancy services for small and mediumenterprises, up gradation of technology and programmes for economic upliftment and soon.

IDBI can finance all types of industrial concerns covered under the provisions of theIDBI Act. With over three decades of service to the Indian industry, IDBI has grownsubstantially in terms of size of operations and portfolio. IDBI has directly or indirectlyassisted all companies that are presently reckoned as major companies in the country.

INDIAN FINANCIAL SYSTEM

NOTES

17 ANNA UNIVERSITY CHENNAI

State Financial Corporations

State Financial Corporations were established in the respective states to meet the financialrequirements of small and medium enterprises. The State Financial Corporations providefinancial assistance by way of term loans, equity subscription, debentures, discounting ofbills of exchange seed capital assistance.

State Industrial Development Corporations (SIDC’s)

SIDC’s are incorporated under the Companies Act 1956 as wholly owned undertakingof the respective state governments. These corporations provide tax benefits under thestate government’s schemes to attract the investments. State Industrial DevelopmentCorporations provide the rupee loans, direct subscription to shares and securities and theyalso borrow funds from the house hold units, private companies and public sectorundertakings by way of issue of bonds or debentures.

Students are requested to refer the Unit III for detailed discussion regarding Termlending Financial Institutions.

1.4.1.3 Non-Banking Financial Companies (NBFC’s)

A Non-Banking Financial Company (NBFC) is a company registered under theCompanies Act, 1956 and is engaged in the business of loans and advances, acquisition ofshares/stock/bonds/debentures/securities issued by Government or local authority or othersecurities of like marketable nature, leasing, hire-purchase, insurance business, chit businessbut does not include any institution whose principal business is that of agriculture activity,industrial activity, sale/purchase/construction of immovable property.

A non-banking institution which is a company and which has its principal business ofreceiving deposits under any scheme or arrangement or any other manner, or lending inany manner is also a non-banking financial company (Residuary non-banking company).

The NBFC’s functions are similar to that of Banking Companies; however, there arefew differences as follows:

The various typer of NBFC’S are as follows:

(i) Non-Banking Financial Companies (NBFC’s) cannot accept demand deposits; whereasBanking Companies accepts deposits.

(ii) It is not a part of the payment and settlement system and as such cannot issue chequesto its customers by NBFC’s and

(iii) Non-Banking Financial Companies are not insured or guaranteed by any governmentbody unlike a bank deposit, where up to Rs 1 lac per bank is insured by the Deposit andCredit Insurance Corporation, a subsidiary of the Reserve Bank of India.

NOTES

18 ANNA UNIVERSITY CHENNAI

DBA 1749

(a) Hire Purchase Finance Company (b) Equipment Leasing Companies (c) Housing Finance Companies (d) Venture Capital Fund Companies (e) C hit Fund Companies (f) Stock Broking Firms (g) Merchant Banking Companies etc,

We have elaborately dealt with each one of the above NBFC’s in the Unit III namelyDevelopment Banking.

1.4.1.4 Investment Institutions:

Investment institutions means procurement of funds from public and institutionalinvestors at large to meet the long term, medium term and short term requirements of theinvestors by providing reasonable returns with negligible risk. They can be viewed in thefollowing terms. This list is only an illustrative but not exhaustive. The detailed study ofthese institution are explained in the Unit V.

(a) Mutual Fund Companies (c) Pension Funds (d) Insurance Companies etc,

1.4.2 Financial Markets

The Indian Financial Market promotes the enormous savings of the economy, byprovi ding an effective channel of returns to the investors from whom the savings are mobilized.Hence, the term Financial Markets can be defined as a market for the exchange of capitaland credit including the money markets and the capital markets. Financial Markets arefacilitating tools for procurement of funds and invest in to various assets. The main activitiesof Financial Markets can be viewed as sale or purchase of shares or stocks, bonds, bills ofexchange, commodities, future and options, foreign currency etc.

The Financial Markets can be classified into:

(i) Money market, (ii) Credit market, (iii) Capital market, (iv) Government securities market,and (v) foreign exchange market. In view of the importance of Government securitiesmarket in the Indian financial system it is bifurcated as separate segment though it is part ofdebt-market and thus of capital market. Each market is unique in terms of the nature ofparticipants and the instruments in the market. The process of financial sector reforms hasaimed at widening and deepening each market and moved towards integrating these marketsdomestically as also with global markets.

INDIAN FINANCIAL SYSTEM

NOTES

19 ANNA UNIVERSITY CHENNAI

Financial Markets

1.4.2.1 Money Market

The Money Market refers to the market for short term debt instrument which hasmaturity less than one year. The Money Market provides the borrower to borrow thefunds for shorter period with lowest cost of funds. At the same time it is also facilitates tothe investor a platform to invest his savings which can generate interest thereon. MoneyMarkets does not have an organised trading market place such as the stock exchange forits primary issue and secondary market trades.

The participants in the money market are banks, primary dealers, and financialinstitutions, mutual funds, non-bank financial companies, manufacturing companies, StateGovernments, provident funds, non-resident Indians, overseas corporate bodies, foreigninstitutional investors and trusts.

The RBI and Securities and Exchange Board of India (SEBI) regulate the participantsand use of instruments in the money market depending upon their respective roles in thefinancial system. For instance, financial institutions and mutual funds are allowed only aslenders in the call money market but are permitted to buy and sell Commercial Paper.

Functions of Money Market

Money market as we know it is a market for short term funds. The money marketgenerally expected to perform the following functions:

(1) It provide as an equilibrium mechanism to even out demand and supply the shortterm funds.

(2) It act as focal point for influencing liquidity and general level of interest rates inthe economy.

(3) It also provides reasonable access to the users and providers of short term fundsto fulfill their investment and borrowing requirements respectively.

NOTES

20 ANNA UNIVERSITY CHENNAI

DBA 1749

There are several instruments in the money market which can be summarized asfollows

i) Treasury Bills (T-Bills)ii) Certificate of Deposits (CD’s)iii) Gilt-edged Securitiesiv) Commercial Papersv) Repurchase Agreements (Repo’s)vi) Bankers Acceptancevii) Inter Bank Participation Certificateviii) Money Market Mutual Funds (MMMF’s)

(i) Treasury Bills (T-Bills):

Treasury Bills are generally issued by the Government for periods ranging from 14days to 364 days through regular auctions. T-Bills are highly liquid instruments and demandfrom banks, financial institutions and corporations. These T-Bills are issued by the ReserveBank of India on behalf of the Government of India. For mobilizing short term cash thesebills are created by the Government to meet its short term requirements. Treasury Bills canbe redeemed prior to the final date of maturity.

(ii) Certificate of Deposits (CD’s)

Certificate of Deposits are popular money market instruments having lock in periodof 15 days after which they can be sold. The Scheme of Certificate of Deposits wasintroduced by the Reserve Bank of India. As per the Reserve Bank of India these Certificateof Deposits can be issued by any scheduled commercial banks, co-operative banks butother than Land Development Banks. Certificate of Deposits can be subscribed by anindividual as well as by an institution.

The minimum size of the deposit is Rs 5 lakhs and thereafter in multipules of Rs 5lakhs. Premature closure of Certificate of Deposits is not permitted and buy –back ofthese deposits is prohibited. Certificate of Deposits can be compared with the FixedDeposits of the banks and the major difference between the two being that CD’s aretransferable from one party to another, where as Fixed Deposits are non-transferable.

Certificate of deposits are unsecured negotiable promissory notes issued by commercialbanks and development financial institutions while the commercial banks CD’s are issuedon discount to face value basis. The discount rates of commercial deposits are marketdriven.

The maturity period ranges from 91 days for the CD’s issued by the banks, one to 3years if CD’s issued by the Development Financial Institutions. Investing into the CD’s isuse full to the investors which can be explained in the following example.

INDIAN FINANCIAL SYSTEM

NOTES

21 ANNA UNIVERSITY CHENNAI

For Example: X ltd has Rs 20 lacs to invest in Certificate of Deposit of a leadingnationalized bank @8% per annum. What money is required to be invested now?

Answer:

Rate of interest = 8% No of days to maturity = 91 daysInterest on Re 1 for 91 days = 0.08 x 91/365 = 0.019945Maturity value after 91 days on Re 1 = Re. 1.019945Investment today = Rs 20 lacs / 1.019945

If we want Rs 20 lakhs after 91 days our investment today is Rs 19,60,890/-

(iii) Gilt-edged Securities

The Government securities and fixed rate bonds, floating rate bonds, zero couponbonds, capital index bonds etc., can be grouped under Gilt-edged securities. These arerisk less securities. The maturity pattern of Government securities are ranging from 1 yearto 10 years. These securities are less liquid than treasury bills and demand for thesesecurities is mainly from banks.

(iv) Commercial Papers

The concept of commercial paper was introduced in India during the year 1990 onthe recommendation of Vaghul Committee. Commercial Papers are now popular debtinstrument for short term borrowing which is one of the source of mobilizing the short termfunds to the highly rated corporate borrowers. Commercial papers are generally allowedto issue by the corporate borrowers having good ranking in the market as established by acredit rating agency.

Now a days Primary Dealers (PD’s) and Satellite Dealers (SD’s) were allowed toissue the commercial papers for short term borrowing. Commercial Papers are issued atdiscount rate which is determined by the issuing company based on its credit rating.Banks and companies are allowed to buy the commercial papers and the company whichis issuing commercial paper has to have not less than Rs 4 crores Net Worth. The commercialpapers can be issued in denominations of Rs 5 lakh

The concept of issue of commercial papers can be explained with the help of thefollowing example:

Example: X Ltd issued Commercial Paper worth Rs 10 crores as per the followingdetails:

Date of issue : 17th January. 2008

Date of maturity : 17th April, 2008

NOTES

22 ANNA UNIVERSITY CHENNAI

DBA 1749

No of days : 90 days (from 17th Jan 08 to 17th April 08)

Rate of interest : 11.25% per annum.

Net amount will best received by the company on issue of commercial paper is asfollows:

90 days 11.25Interest for 90 days = —————— x ———— = 2.7740

365 days 100

2.7740Rs10 crores x ————————— = Rs 26, 99,126 or say Rs 27 lakhs

100 + 2.7740

Net amount will be received by the company is Rs 9.73 crores (ie Rs 10 crores lessRs 27 lakhs).

(v) Repurchase Agreements (Repo’s)

Repurchase Agreements also called as buy back or ready forward and in shortRepo’s. Repurchase Agreement arises when one party sells a security to another partywith an agreement to buy it back at a specified time and price. Like wise the buyer purchasesthe securities, with an agreement to resell the same to the seller on an agreed date and at apredetermined price. The same transaction is called as repo from the seller point of viewand reverse repo from the viewpoint of the buyer. Basically repo’s are short term instrumentwith risk free for balancing short term liquidity needs.

Banks have often resorted to ready forward deals among themselves, as also withDiscount and Finance House of India (DFHI) and Securities Trading Corporation of India(STCI) to overcome short term financial crunches. At present the Reserve Bank of India isallowed repo’s trading between banks, cooperative banks, Discount and Finance Houseof India and Securities Trading Corporation of India. Repos are usually entered into witha maturity of 1-14 days. Initially, there were lot of restrictions on banks to deal with repo’sbecause securities scam and other scams. Later on due to libaralisation the restrictions aregradually reduced.

Types of Repo’s: we have at present two types of repo’s namely

• Inter-Bank Repo’s and• Reserve Bank of India Repo’s.

INDIAN FINANCIAL SYSTEM

NOTES

23 ANNA UNIVERSITY CHENNAI

Inter-Bank Repo’s

Banks, along with primary dealers are permitted to undertake ready forwardtransactions through the Special General Ledger (SGL) account maintained by the ReserveBank of India. At present all Central Government dated securities, State GovernmentSecurities and T-bills of all maturities have been made eligible of repo’s. The non bankentities holding SGL account with the Reserve Bank of India can enter into reverse repotransactions with banks or primary dealers, in all Government securities.

Reserve Bank Repo’s

Reserve Bank of India undertake the repo’s or reverse repo’s with the banks andPrimary Dealers as part of Open Market Operations (OMO’s). It is a mechanism throughwhich the Reserve Bank of India borrows money from banks. This process can be doneby selling the government securities to repurchase later to influence the short term liquidity.

Primary dealers include Discount and Finance House of India, Securities TradingCorporation of India, ICICI Securities, SBI Gilts, PNB Gilt and Gilt securities TradingCorporation.

(vi) Bankers Acceptance

A banker’s acceptance is a draft against a bank ordering the bank to pay somespecified amount of at a future date. The bankers’ acceptance is very safe security and isused as a money market instrument.

Banker Acceptance (BA) is an order to pay a specified amount of money to theholder of the instrument on a given date. These are usually used in foreign trade transactionsin which the seller wants to insure they will be paid for the goods sent. A commercial bankissues the BA to the seller in place of the buyer, who pays for the BA, and whose creditrating may not be as strong as the bank.

This is especially useful when the creditworthiness of a foreign trade partner is unknown.Acceptances sell at a discount from the face value:

One advantage of a banker’s acceptance is that it does not need to be held untilmaturity, and can be sold off in the secondary markets where investors and institutionsconstantly trade BAs.

NOTES

24 ANNA UNIVERSITY CHENNAI

DBA 1749

(vii) Inter Bank Participation Certificate

The Inter Bank Participation Certificate is yet another short term money instrument bywhich the banks can raise money or deploy short term surplus. Inter Bank ParticipationCertificates can be issued only by scheduled commercial banks these can be on risk sharingbasis and other one is without risk sharing basis.

(viii) Money Market Mutual Funds (MMMF’s)

Money Market Mutual Funds acts as bridge in-between small investors and moneyborrowers. MMMF’s mobilizes the funds from small saving savers and invest into shortterm debt instruments or money market instruments. MMMF’s are allowed to offer acheque writing facility in a tie up with banks to provide more liquidity.

1.4.2.2 Credit Markets

The credit market can be classified by maturity of finance - short-term and long-term.The distinction between the short-term and long-term credit institutions is increasingly gettingblurred, but it is still possible to classify them in terms of their traditional objectives. Short-term finance is extended in the form of cash credit limits and term loans with maturity of lessthan one year. Institutions mainly extending such loans are commercial banks, cooperativebanks and non-bank finance companies.

Recently, development financial institutions have also entered into this foray. Long-term finance is extended in the form of term loans technically for a period of over one yearbut substantively and in practice for a period of over three years. Institutions extendingsuch loans are developmental financial institutions, specialized financial institutions andinvestment institutions. Recently, commercial banks are extending their operations in thisarea.

Sources of credit can be classified into internal (rupee credit) and external (foreigncurrency loans through external commercial borrowings and foreign currency denominatednon-resident deposits under FCNR-B). Significant changes have been brought about incredit markets, particularly since April 1997. Banks are easily the most critical players inthis market.

The RBI is moving away from micro regulation to macro management of banks. Alldeposit rates are freed except for savings accounts and term deposits up to 30 days.Banks have been given the freedom to evolve their own methods of assessing workingcapital and also the freedom for credit dispensation without consortium obligations. Banksare now allowed to freely fix their lending rates beyond Rs. 2 lakh, and within a ceiling of13.5 per cent for loans amounting to Rs. 25,000 - Rs. 2 lakh. Of course, some lendingrates for export activity are also regulated.

INDIAN FINANCIAL SYSTEM

NOTES

25 ANNA UNIVERSITY CHENNAI

1.4.2.3 Capital Market

Capital Market is the market for long term finance with the maturity period more thanone year. The Capital Market deals with the stock markets which provide financing throughthe issuance of shares or common stock in the primary market, and enable the subsequenttrading in the secondary market, Capital Markets also deals with Bond Market whichprovide financing through issuance of Bonds in the primary market and subsequent tradingthereof in the secondary market.

Functions of Capita Markets:

1. The organised and regulated capital market motivates individual to save and investfunds. The availability of safe and profitable source of investment is an essential criteriato create propensity to save and invest on the part of the earning public.

2. It provides for the investors a safe and productive channels for investment of savingsand secure the recurring benefit of return thereon, as long as the savings are retained.

3. It provides liquidity to the savings of the investors, by developing a secondary capitalmarket, and thus makes even short term savings, consistently available for long-termusers

4. It thus mobilises savings of large number of individuals, families and associations andmake the same available for meeting the large capital needs of organised industry,trade and business and for progress and development of the country as a whole andits economy.

The primary financial assets in the capital market include the following:

(i) Treasury Bonds:(ii) Common Stock:(iii) Corporate Long Term Bonds(iv) Mortgages

1.4.2.4 Government Securities Market

The Government Securities market constitutes the principal segment of the debt market.The participants in this market as issuers are the Central and State Governments. The maininvestors are the RBI, insurance companies, banks, State Governments, provident funds,individuals, corporates, NBFCs, financial institutions, and to a limited extent FIIs andNRIs.

Reforms initiated in the recent period include, introduction of Treasury Bills of varyingmaturities, abolition of tax deduction at source on interest income from Government securities,and permitting FIIs to invest in debt instruments including dated Government securities asalso allowing them to hedge their foreign currency risk in the forward markets.

NOTES

26 ANNA UNIVERSITY CHENNAI

DBA 1749

The monetary policy of October 1997 announced the introduction of uniform priceauction in respect of 91-Day Treasury Bills as an experimental measure with a view tobroadening the investor base and removing the winners curse; the introduction of pre-announced notified amounts for all auctions of Government securities, and the intention toaccept non-competitive bids outside the notified amount in order to ensure moretransparency in the primary auction process. FIIs with 30 per cent ceiling on investment indebt, are being allowed to invest in Government securities in addition to corporate debt.

1.4.2.5 Foreign Exchange Market

When an organization or person in one country wants to buy goods or services inanother, they must normally exchange their own currency for that of the country they arebuying from. As a result, those who are dealing with foreign trade or commerce have aneed to buy the currency of another country to make transactions. This exchange is donein the foreign currency market.

State Bank of India is the single-largest participant in the forex market, accounting forabout 40 per cent of the value of total customer transactions. In the inter-bank segment ofthe market, SBI along with a few other banks constitute the market-makers, i.e., bankswhich are always ready to quote two-way price both in the spot and forward markets.Foreign banks are predominant among the other participants.

The customer segment is dominated by the Indian Oil Corporation and certain otherlarge public sector giants like Oil and Natural Gas Commission, Bharath Heavy ElectricalsLtd., Steel Authority of India Ltd., Maruti Udyog, etc. There is a perceptible presence oflarge private sector corporates like, Reliance Group, Tata Group, and Larsen and Tubro.Of late, foreign institutional investors have accounted for a large supply in the market.

The RBI also buys and sells foreign exchange at its discretion to ensure orderlyconditions in the market. Till recently, the market was dominated by trade-related flowsand was not driven by financial market expectations inasmuch as the arbitrage opportunitiesbetween the Indian and offshore money (financial asset) markets were highly restricted.Nevertheless, the market-makers are now better-placed to give quotes with narrowerspreads than before.

Some major initiatives in the Foreign Exchange Market

(i) Corporates are now allowed to sell and buy in the forward market beyond sixmonths on a presumptive basis, subject to certain conditions. This has resulted inextending the forward market beyond six months.

(2) In fact, forward quotes for periods of more than six months and up to 12 monthsare now available on a regular basis and at narrower spreads.

(3) Authorised Dealers (ADs) are now allowed to run long-term rupee-forex swapbooks.

INDIAN FINANCIAL SYSTEM

NOTES

27 ANNA UNIVERSITY CHENNAI

(4) This has resulted in better avenues of forex exposure management. Forward coverfor FIIs in debt instruments and for NRI depositors in respect of deposits held inNRI and FCNRB schemes has been allowed enabling these participants to hedgetheir exposures.

1.4.3 Financial Instruments

Financial instruments can be broadly divided into two parts namely primary securitiesand secondary securities. Primary securities are further divided into equity shares, preferenceshares, debt instruments and various combinations of these. Secondary markets furtherdivided into time deposits, Mutual Funds and insurance polices.

Some of the various financial instruments deal with in the international market alsobriefly discussed below:

(i) Euro Bonds(ii) Foreign Bonds(iii)Fully Hedged Bonds(iv)Floating Rate Notes(v) Euro commercial Papers(vi)Foreign currency options(vii)Foreign currency futures

(i) Euro Bonds

Euro bonds are debts instruments denominated in the currency issued out side thecountry of the that currency. For examples a Yen note floated in the Germany.

(ii) Foreign Bonds

These are the debts instruments denominated in a currency which is foreign to the borrowerand is sold in the country of that currency. For example a British firm placing dollardenominated bonds in USA.

(iii) Fully Hedged bonds

In foreign bonds, the risk of currency fluctuation exist. Fully hedged bonds eliminatesthe risk by selling in the forward markets the entire steam of principal and interest payment.

(iv) Floating Rate Notes

These are issued up to 7 years maturity. Interests are adjusted to reflect the prevailingexchange rates. They provide cheaper money than foreign loans.

(v) Euro commercial papers

Euro Commercial Papers are short term money market instruments. They are formaturities less than one year. They are usually designated in US dollars.

NOTES

28 ANNA UNIVERSITY CHENNAI

DBA 1749

(vi) Foreign Currency Option:

A foreign currency option is the right to buy or sell, spot, future or forwards, a specifiedforeign currency. It provides a hedge against financial and economic risks.

(vii) Foreign currency Futures:

Foreign currency Futures are obligations to buy or sell a specified currency in thepresent for settlement at a future date.

1.4.4 Financial Instruments

Financial services have been growing rapidly with the emergence of new investmentflows in financial reconstitute a large and growing sector in almost all economies. Trade andinvestment flows in financial services have been growing rapidly with the emergence of newand growing markets in developing and transition economies, with modernization, rapidtechnological change, use of new financial instruments, and financial and trade liberalization.

The financial services sector is also quite large and complex and covers a wide rangeof activities and instruments, including for instance, corporate banking, derivatives, factoring,foreign exchange trading, pensions and investment fund management, advisory andconsultancy services, insurance broking and underwriting, project finance, securities trading,venture capital, and wholesale and retail banking services. Given the range of instrumentsand activities that fall under the purview of the financial services sector, there are also alarge number of players

1.5 FINANCIAL SECTOR REFORMS

Financial Reforms has been excellently explained by Dr. Rakesh Mohan, DeputyGovernor, Reserve Bank of India at the International Monetary Fund, Washington D.C.-2004. We have discussed some of important issues dealt by him in the Reserve Bank ofIndia bulletin regarding financial reforms in India.

The initiation of financial reforms in the country during the early 1990s was to a largeextent conditioned by the analysis and recommendations of various Committees/WorkingGroups set-up to address specific issues. The process has been marked by ‘gradualism’with measures being undertaken after extensive consultations with experts and marketparticipants.

From the beginning of financial reforms, India has resolved to attain standards ofinternational best practices but to fine tune the process keeping in view the underlyinginstitutional and operational considerations. Reform measures introduced across sectorsas well as within each sector were planned in such a way so as to reinforce each other.Attempts were made to simultaneously strengthen the institutional framework while enhancingthe scope for commercial decision making and market forces in an increasingly competitive

INDIAN FINANCIAL SYSTEM

NOTES

29 ANNA UNIVERSITY CHENNAI

framework. At the same time, the process did not lose sight of the social responsibilities ofthe financial sector.

However, for fulfilling such objectives, rather than using administrative fiat or coercion,attempts were made to provide operational flexibility and incentives so that the desiredends are attended through broad interplay of market forces. The major aim of the reformsin the early phase of reforms, known as first generation of reforms, was to create anefficient, productive and profitable financial service industry operating within the environmentof operating flexibility and functional autonomy.

While these reforms were being implemented, the world economy also witnessedsignificant changes, ‘coinciding with the movement towards global integration of financialservices’. The focus of the second phase of financial sector reforms starting from thesecond-half of the 1990s, therefore, has been the strengthening of the financial system andintroduction of structural improvements.

Two brief points need to be mentioned here. First, financial reforms in the early 1990swere preceded by measures aimed at lessening the extent of financial depression. However,unlike in the latter period, the earlier efforts were not part of a well-thought out andcomprehensive agenda for extensive reforms.

Second, financial sector reform in India was an important component of thecomprehensive economic reform process initiated in the early 1990s. Whereas economicreforms in India were also initiated following an external sector crisis, unlike many otheremerging market economies where economic reforms were driven by crisis followed by aboom-bust pattern of policy liberalisation, in India, reforms followed a consensus drivenpattern of sequenced liberalisation across the sectors. That is why despite several changesin government there has not been any reversal of direction in the financial sector reformprocess over the last 15 years.

The main objectives of the financial reforms in India are