Indian depository receipt(IDR)

26

Indian Depository Receipts

-

Upload

rohit-kumar -

Category

Education

-

view

95 -

download

1

Transcript of Indian depository receipt(IDR)

Indian Depository Receipts

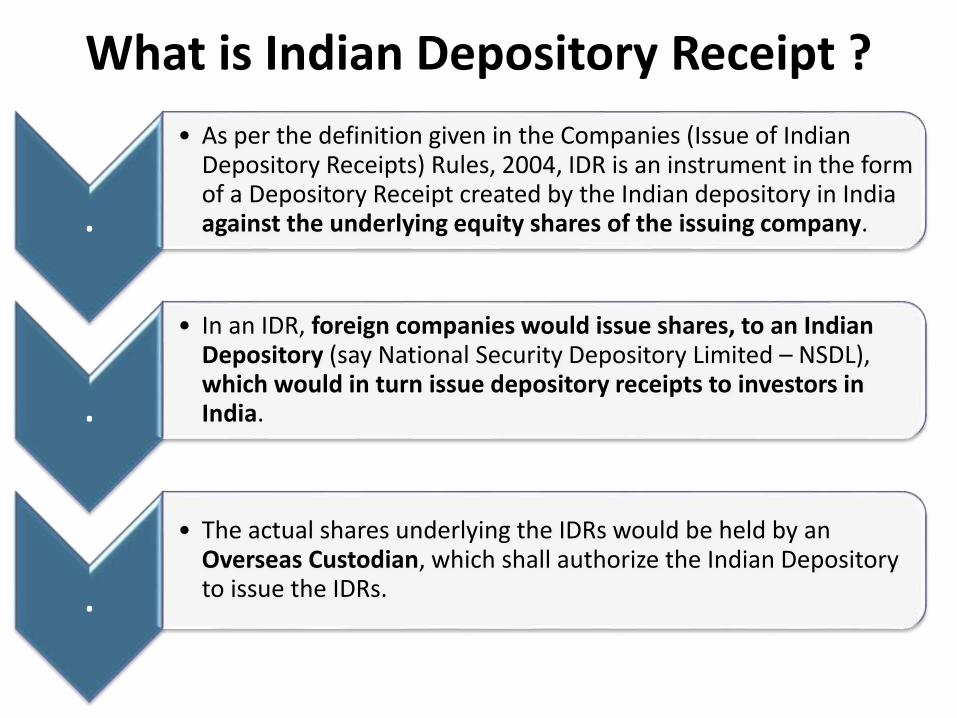

What is Indian Depository Receipt ?

.

.

• As per the definition given in the Companies (Issue of Indian Depository Receipts) Rules, 2004, IDR is an instrument in the form of a Depository Receipt created by the Indian depository in India against the underlying equity shares of the issuing company.

.

• In an IDR, foreign companies would issue shares, to an Indian Depository (say National Security Depository Limited – NSDL), which would in turn issue depository receipts to investors in India.

.

• The actual shares underlying the IDRs would be held by an Overseas Custodian, which shall authorize the Indian Depository to issue the IDRs.

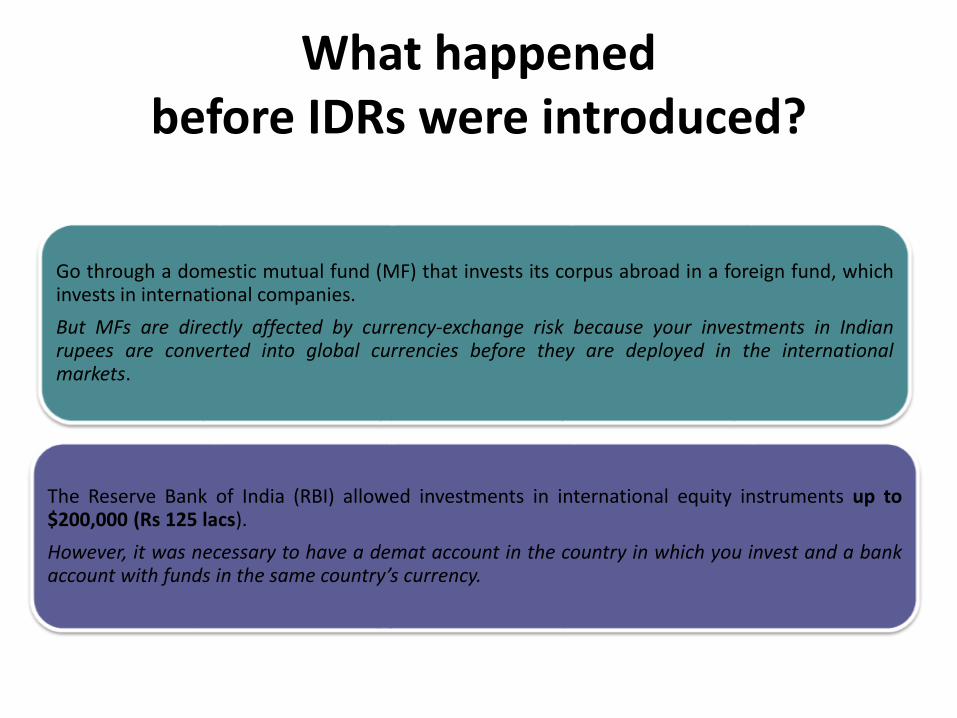

What happened before IDRs were introduced?

Go through a domestic mutual fund (MF) that invests its corpus abroad in a foreign fund, whichinvests in international companies.

But MFs are directly affected by currency-exchange risk because your investments in Indianrupees are converted into global currencies before they are deployed in the internationalmarkets.

The Reserve Bank of India (RBI) allowed investments in international equity instruments up to$200,000 (Rs 125 lacs).

However, it was necessary to have a demat account in the country in which you invest and a bankaccount with funds in the same country’s currency.

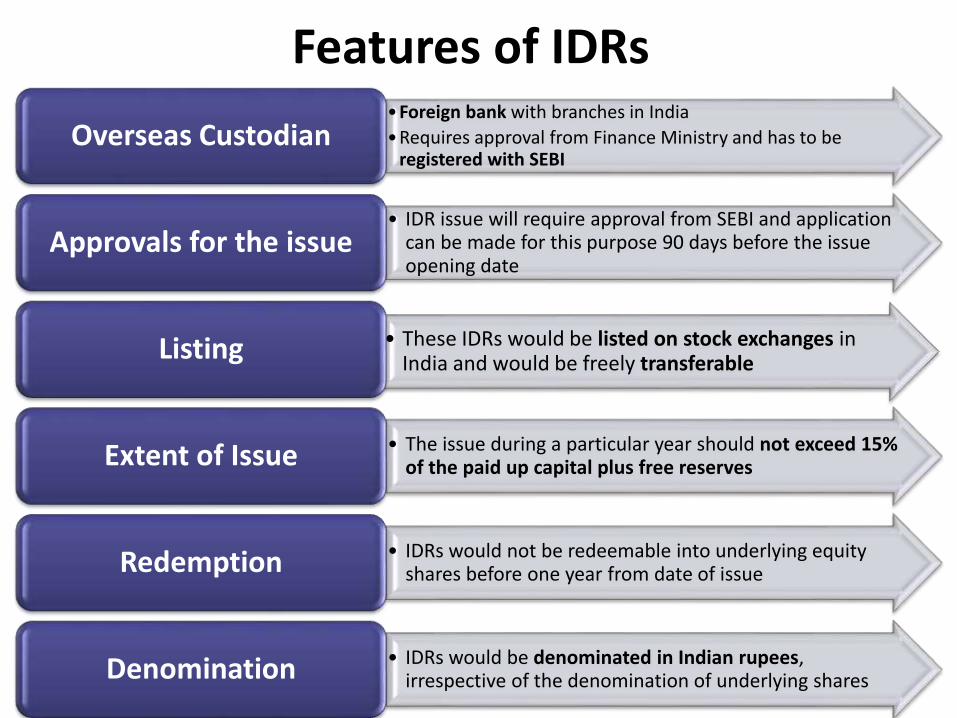

Features of IDRs•Foreign bank with branches in India

•Requires approval from Finance Ministry and has to be registered with SEBI

Overseas Custodian

• IDR issue will require approval from SEBI and application can be made for this purpose 90 days before the issue opening date

Approvals for the issue

• These IDRs would be listed on stock exchanges in India and would be freely transferable

Listing

• The issue during a particular year should not exceed 15% of the paid up capital plus free reservesExtent of Issue

• IDRs would not be redeemable into underlying equity shares before one year from date of issueRedemption

• IDRs would be denominated in Indian rupees, irrespective of the denomination of underlying sharesDenomination

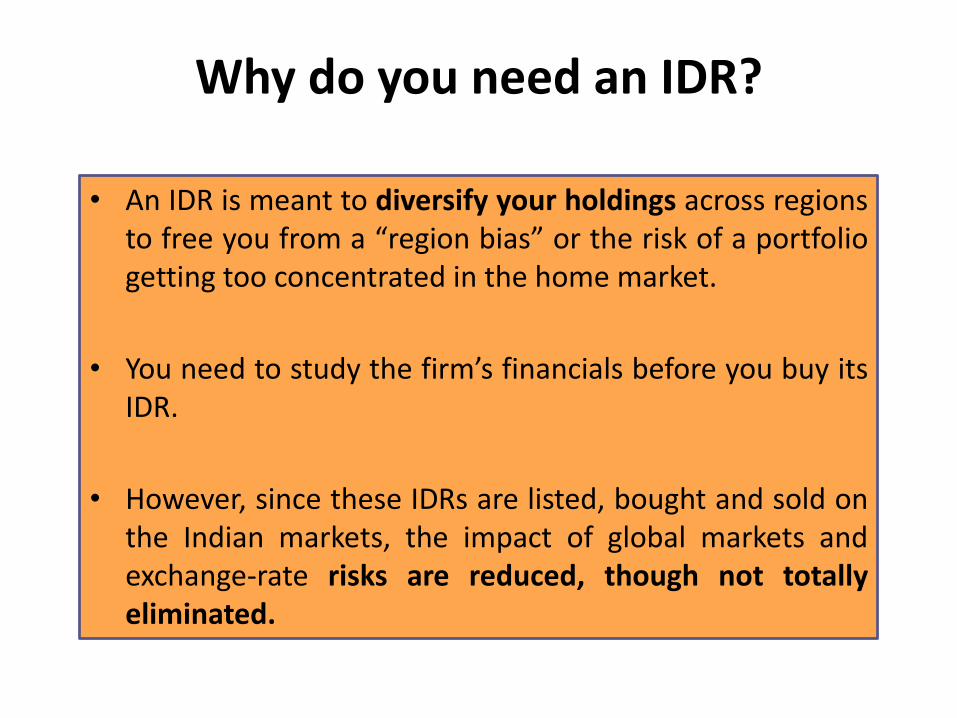

Why do you need an IDR?

• An IDR is meant to diversify your holdings across regionsto free you from a “region bias” or the risk of a portfoliogetting too concentrated in the home market.

• You need to study the firm’s financials before you buy itsIDR.

• However, since these IDRs are listed, bought and sold onthe Indian markets, the impact of global markets andexchange-rate risks are reduced, though not totallyeliminated.

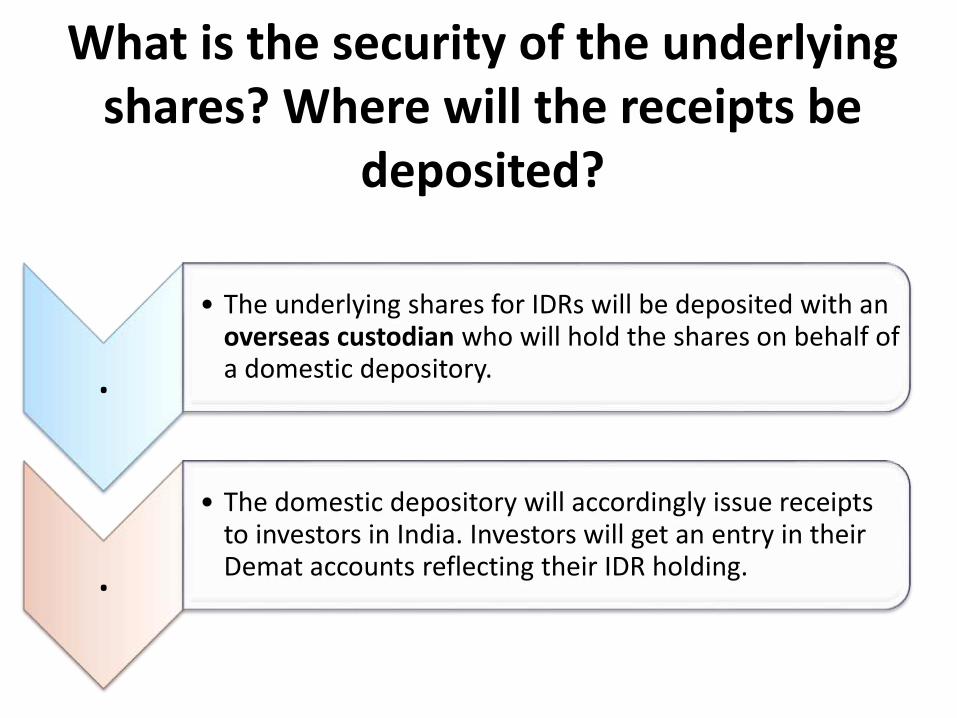

What is the security of the underlying shares? Where will the receipts be

deposited?

.

• The underlying shares for IDRs will be deposited with an overseas custodian who will hold the shares on behalf of a domestic depository.

.

• The domestic depository will accordingly issue receipts to investors in India. Investors will get an entry in their Demat accounts reflecting their IDR holding.

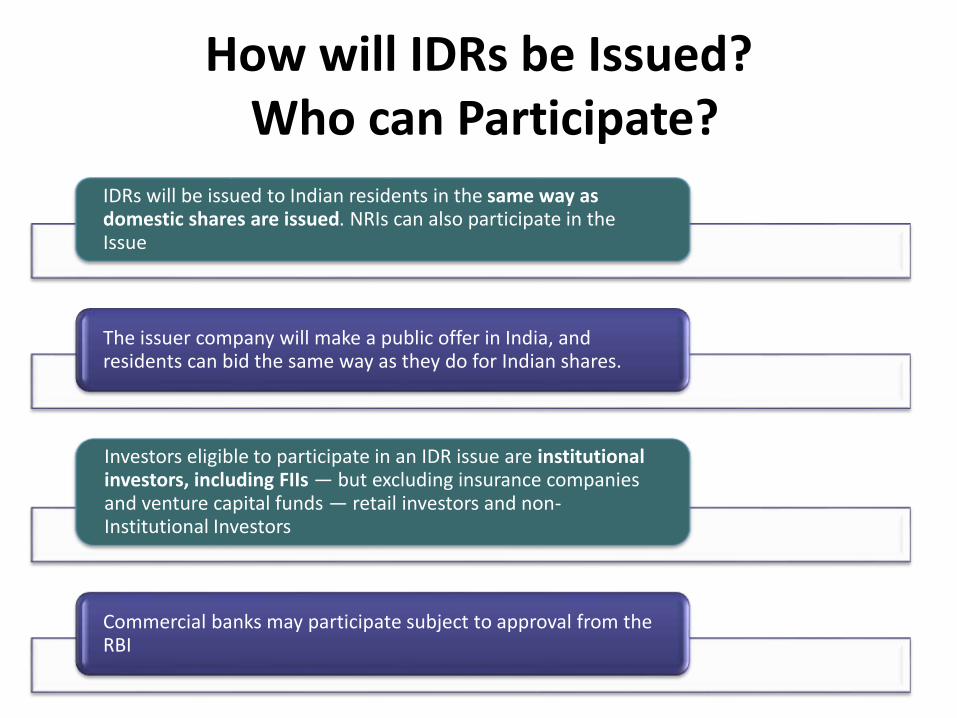

How will IDRs be Issued?Who can Participate?

..IDRs will be issued to Indian residents in the same way as domestic shares are issued. NRIs can also participate in the Issue

The issuer company will make a public offer in India, and residents can bid the same way as they do for Indian shares.

Investors eligible to participate in an IDR issue are institutional investors, including FIIs — but excluding insurance companies and venture capital funds — retail investors and non-Institutional Investors

Commercial banks may participate subject to approval from the RBI

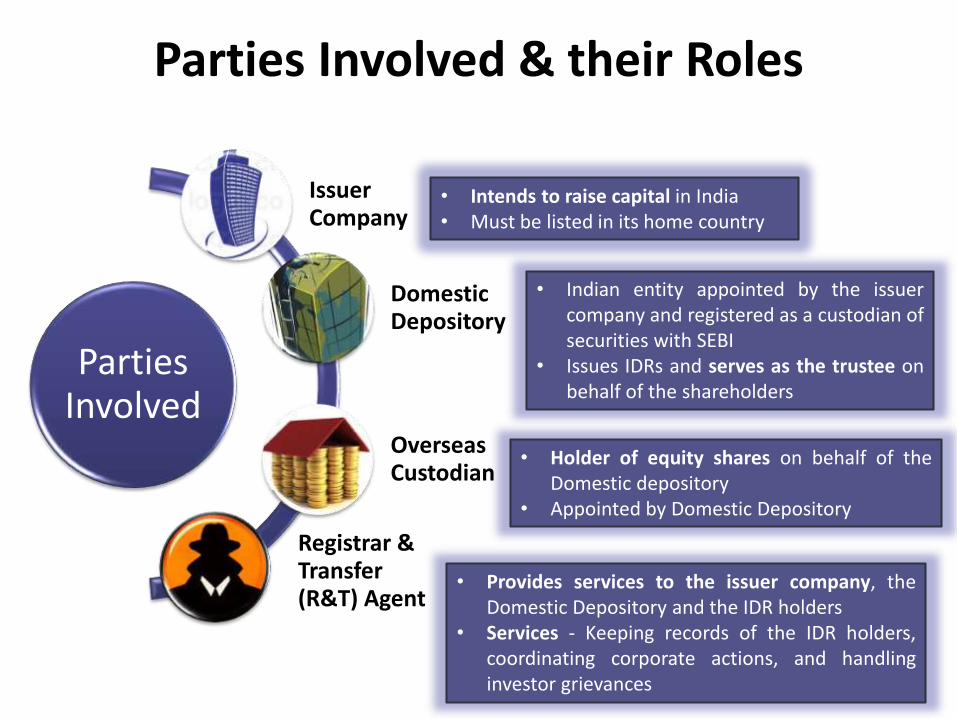

Parties Involved & their Roles

Parties Involved

Issuer Company

Domestic Depository

Overseas Custodian

Registrar & Transfer (R&T) Agent

• Intends to raise capital in India• Must be listed in its home country

• Indian entity appointed by the issuercompany and registered as a custodian ofsecurities with SEBI

• Issues IDRs and serves as the trustee onbehalf of the shareholders

• Holder of equity shares on behalf of theDomestic depository

• Appointed by Domestic Depository

• Provides services to the issuer company, theDomestic Depository and the IDR holders

• Services - Keeping records of the IDR holders,coordinating corporate actions, and handlinginvestor grievances

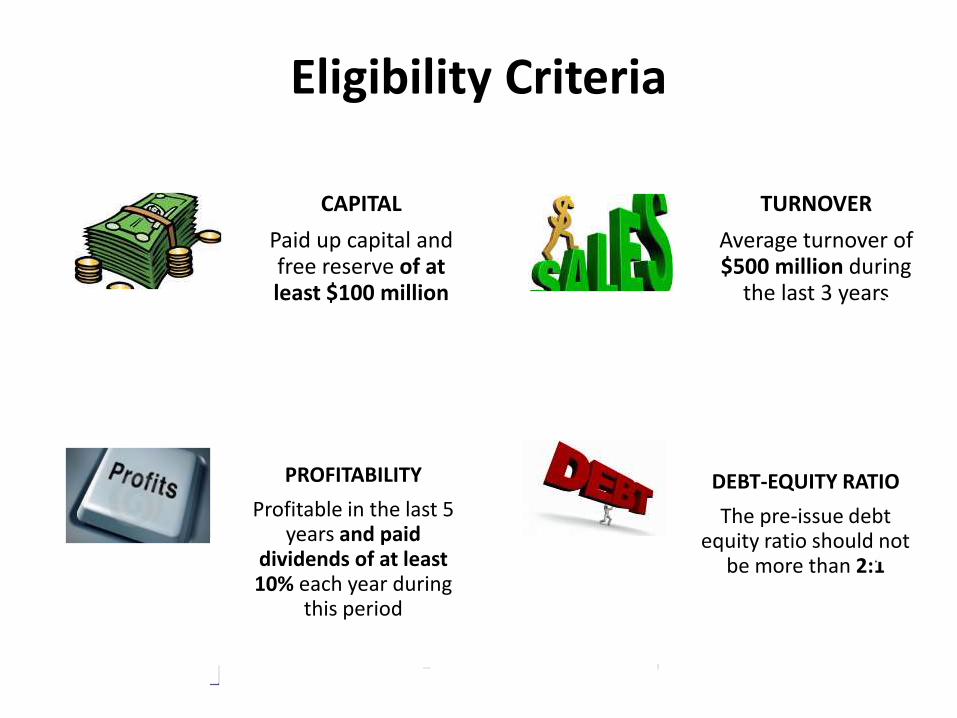

Eligibility Criteria

CAPITAL

Paid up capital and free reserve of at least $100 million

PROFITABILITY

Profitable in the last 5 years and paid

dividends of at least 10% each year during

this period

DEBT-EQUITY RATIO

The pre-issue debt equity ratio should not

be more than 2:1

TURNOVER

Average turnover of $500 million during

the last 3 years

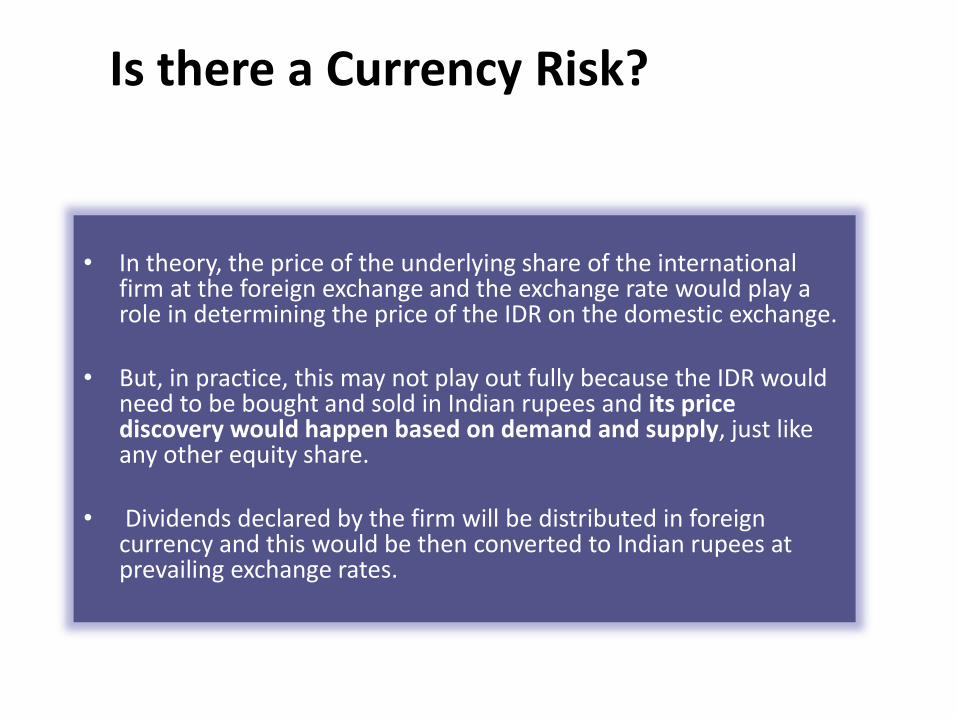

Is there a Currency Risk?

• In theory, the price of the underlying share of the international firm at the foreign exchange and the exchange rate would play a role in determining the price of the IDR on the domestic exchange.

• But, in practice, this may not play out fully because the IDR would need to be bought and sold in Indian rupees and its price discovery would happen based on demand and supply, just like any other equity share.

• Dividends declared by the firm will be distributed in foreign currency and this would be then converted to Indian rupees at prevailing exchange rates.

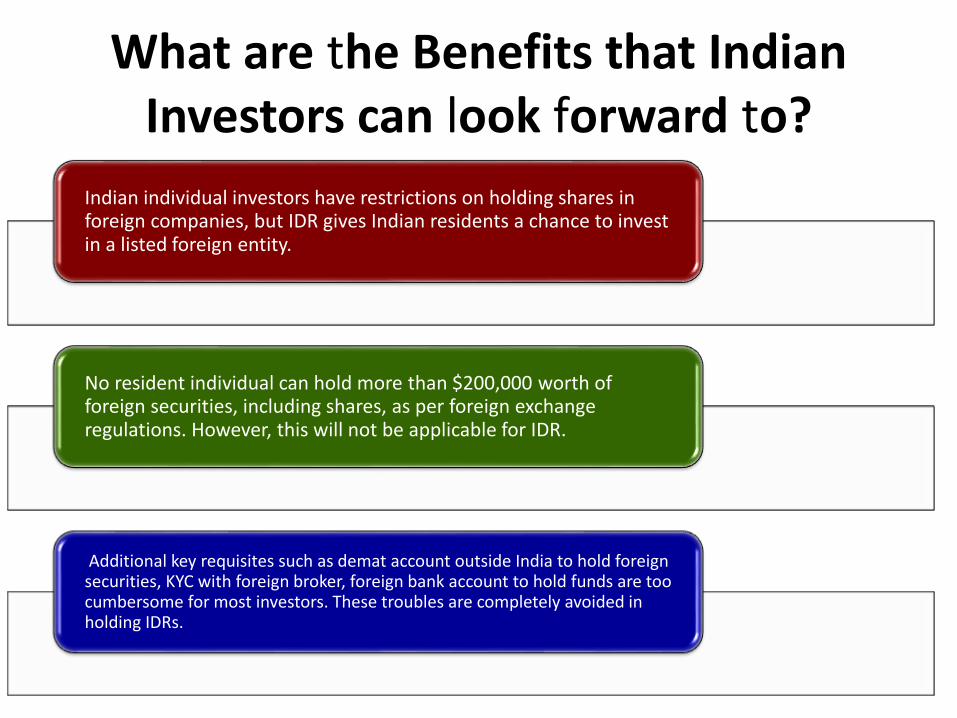

What are the Benefits that Indian Investors can look forward to?

Indian individual investors have restrictions on holding shares in foreign companies, but IDR gives Indian residents a chance to invest in a listed foreign entity.

No resident individual can hold more than $200,000 worth of foreign securities, including shares, as per foreign exchange regulations. However, this will not be applicable for IDR.

Additional key requisites such as demat account outside India to hold foreign securities, KYC with foreign broker, foreign bank account to hold funds are too cumbersome for most investors. These troubles are completely avoided in holding IDRs.

Will Indian Investors get Equal Rights as Shareholders?

Indian investors haveequivalent rights asshareholders

They can vote on EGMresolutions through theoverseas custodian.They can’t attendAGMs.

Whatever benefitsaccrue to the shares, byway of dividend, rights,splits or bonuses will bepassed on to the IDRholders also, to theextent permissible underIndian law

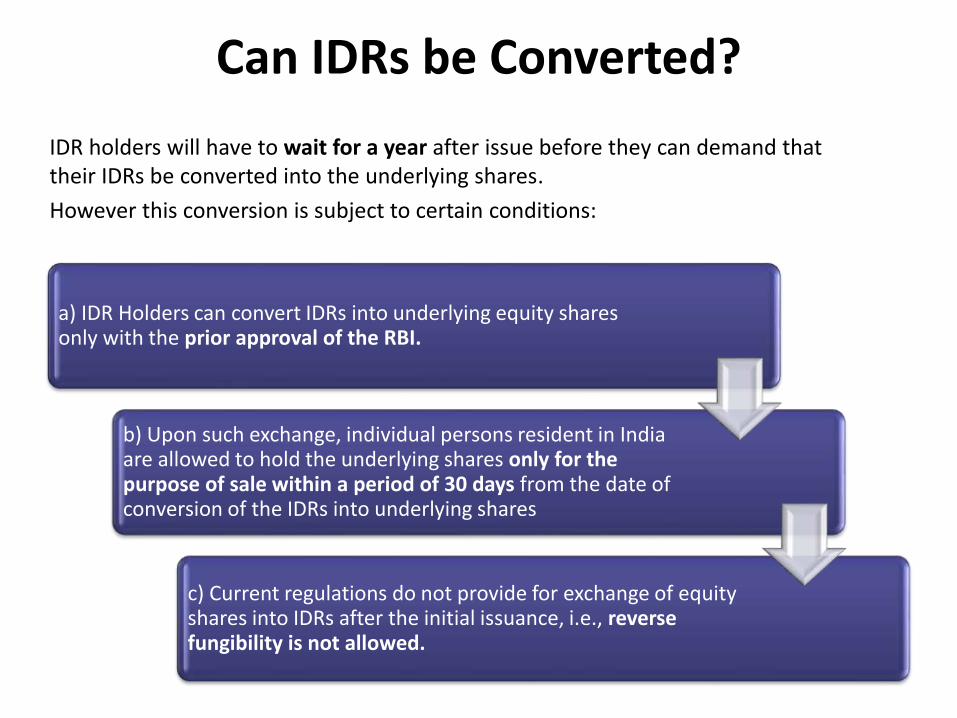

Can IDRs be Converted?

IDR holders will have to wait for a year after issue before they can demand that their IDRs be converted into the underlying shares.

However this conversion is subject to certain conditions:

a) IDR Holders can convert IDRs into underlying equity shares only with the prior approval of the RBI.

b) Upon such exchange, individual persons resident in India are allowed to hold the underlying shares only for the purpose of sale within a period of 30 days from the date of conversion of the IDRs into underlying shares

c) Current regulations do not provide for exchange of equity shares into IDRs after the initial issuance, i.e., reverse fungibility is not allowed.

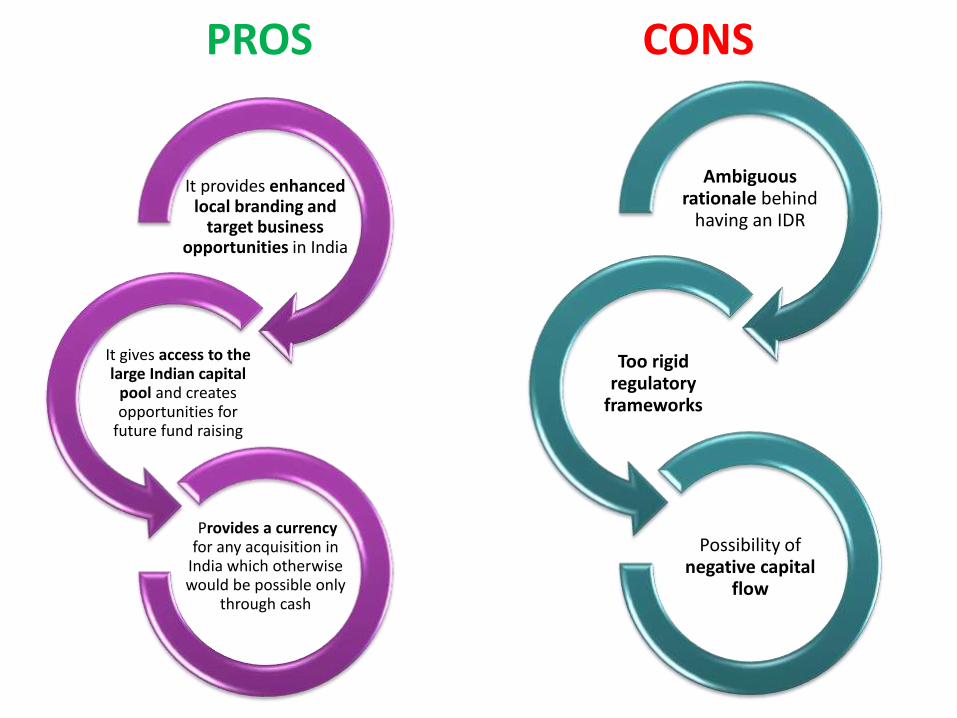

PROS

It provides enhanced local branding and

target business opportunities in India

It gives access to the large Indian capital

pool and creates opportunities for

future fund raising

Provides a currency for any acquisition in

India which otherwise would be possible only

through cash

CONS

Ambiguous rationale behind

having an IDR

Too rigid regulatory

frameworks

Possibility of negative capital

flow

Disclosure & Investor Protection (DIP) Guidelines

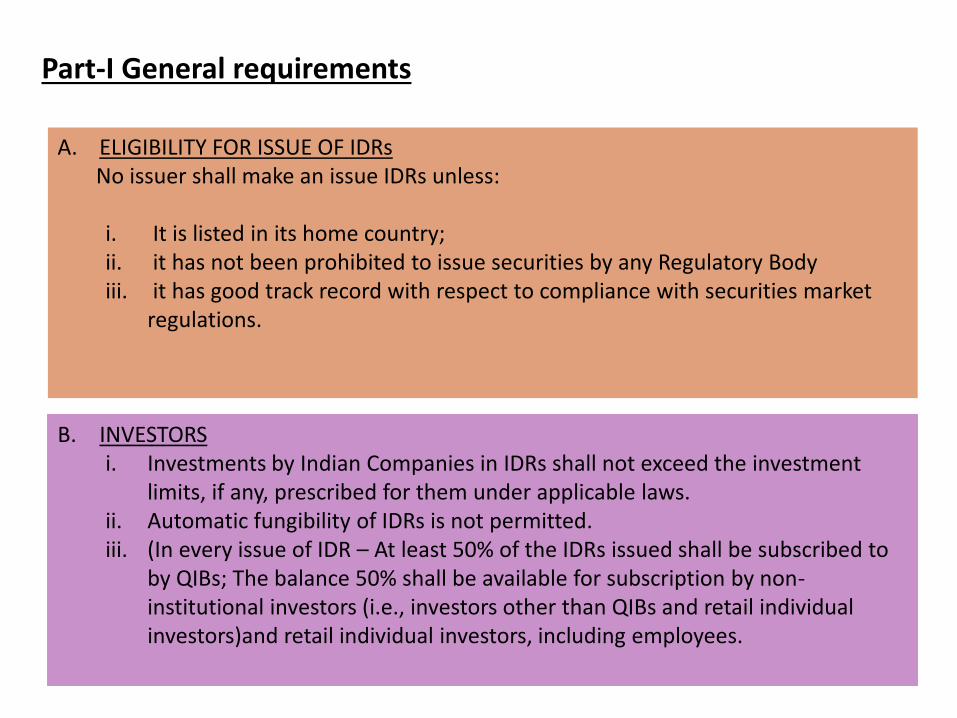

Part-I General requirements

A. ELIGIBILITY FOR ISSUE OF IDRsNo issuer shall make an issue IDRs unless:

i. It is listed in its home country;ii. it has not been prohibited to issue securities by any Regulatory Bodyiii. it has good track record with respect to compliance with securities market

regulations.

B. INVESTORS i. Investments by Indian Companies in IDRs shall not exceed the investment

limits, if any, prescribed for them under applicable laws.ii. Automatic fungibility of IDRs is not permitted.iii. (In every issue of IDR – At least 50% of the IDRs issued shall be subscribed to

by QIBs; The balance 50% shall be available for subscription by non-institutional investors (i.e., investors other than QIBs and retail individual investors)and retail individual investors, including employees.

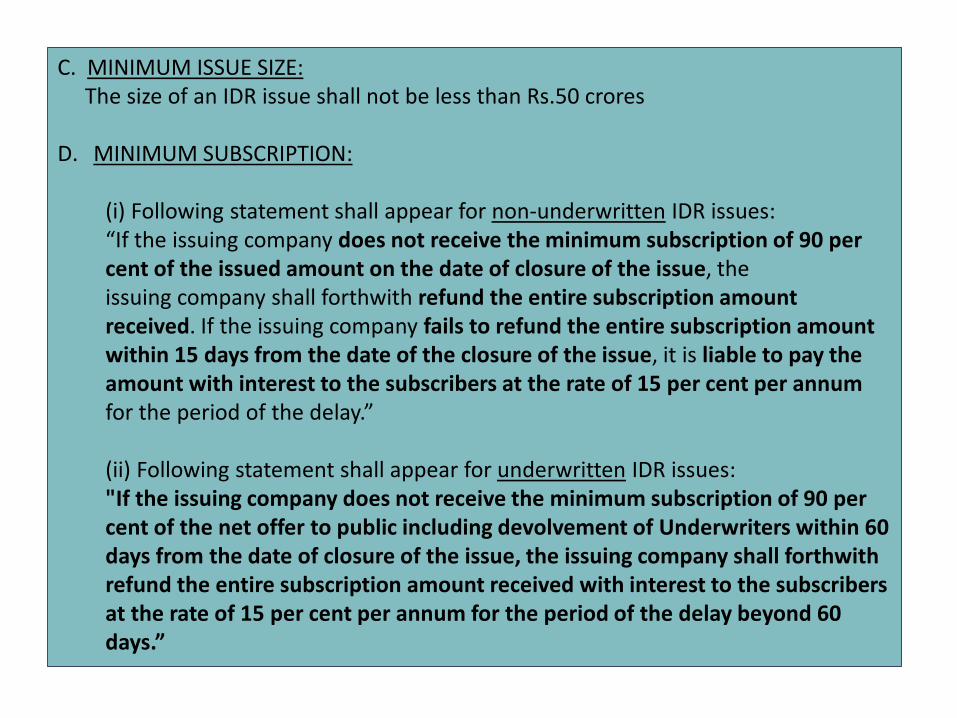

C. MINIMUM ISSUE SIZE:The size of an IDR issue shall not be less than Rs.50 crores

D. MINIMUM SUBSCRIPTION:

(i) Following statement shall appear for non-underwritten IDR issues:“If the issuing company does not receive the minimum subscription of 90 percent of the issued amount on the date of closure of the issue, theissuing company shall forthwith refund the entire subscription amountreceived. If the issuing company fails to refund the entire subscription amountwithin 15 days from the date of the closure of the issue, it is liable to pay theamount with interest to the subscribers at the rate of 15 per cent per annumfor the period of the delay.”

(ii) Following statement shall appear for underwritten IDR issues:"If the issuing company does not receive the minimum subscription of 90 percent of the net offer to public including devolvement of Underwriters within 60days from the date of closure of the issue, the issuing company shall forthwithrefund the entire subscription amount received with interest to the subscribersat the rate of 15 per cent per annum for the period of the delay beyond 60days.”

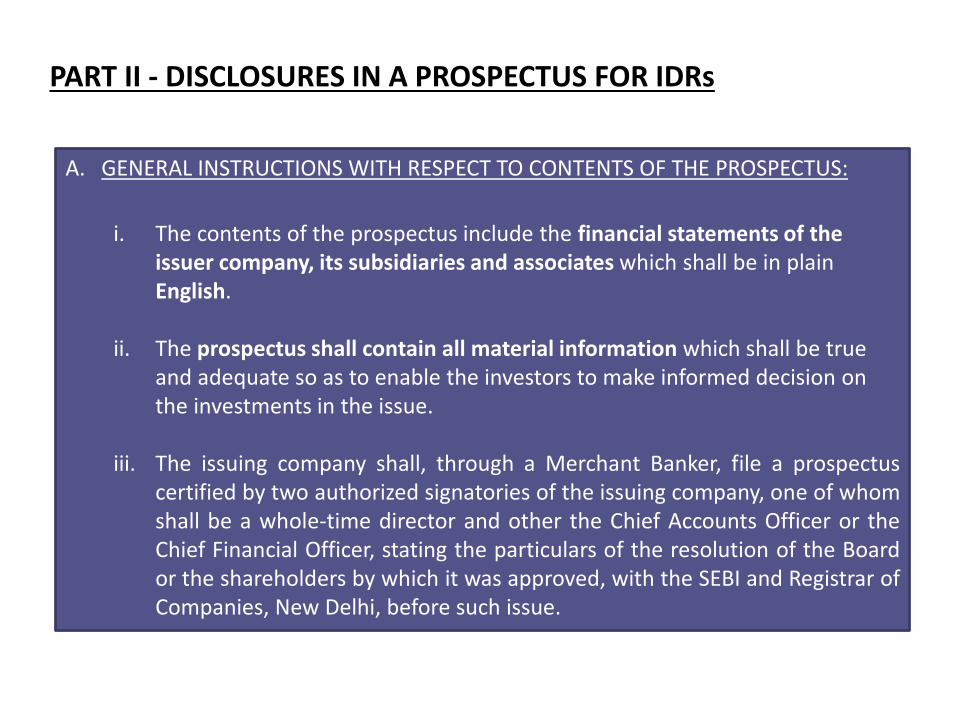

PART II - DISCLOSURES IN A PROSPECTUS FOR IDRs

A. GENERAL INSTRUCTIONS WITH RESPECT TO CONTENTS OF THE PROSPECTUS:

i. The contents of the prospectus include the financial statements of the issuer company, its subsidiaries and associates which shall be in plain English.

ii. The prospectus shall contain all material information which shall be true and adequate so as to enable the investors to make informed decision on the investments in the issue.

iii. The issuing company shall, through a Merchant Banker, file a prospectuscertified by two authorized signatories of the issuing company, one of whomshall be a whole-time director and other the Chief Accounts Officer or theChief Financial Officer, stating the particulars of the resolution of the Boardor the shareholders by which it was approved, with the SEBI and Registrar ofCompanies, New Delhi, before such issue.

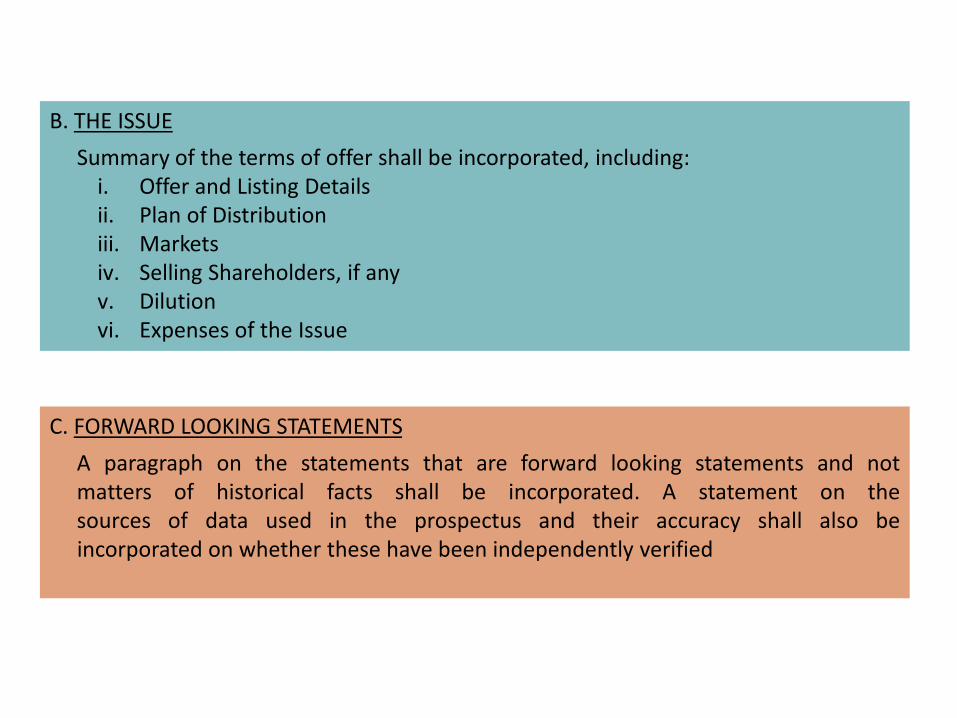

B. THE ISSUE

Summary of the terms of offer shall be incorporated, including:i. Offer and Listing Detailsii. Plan of Distributioniii. Marketsiv. Selling Shareholders, if anyv. Dilutionvi. Expenses of the Issue

C. FORWARD LOOKING STATEMENTS

A paragraph on the statements that are forward looking statements and notmatters of historical facts shall be incorporated. A statement on thesources of data used in the prospectus and their accuracy shall also beincorporated on whether these have been independently verified

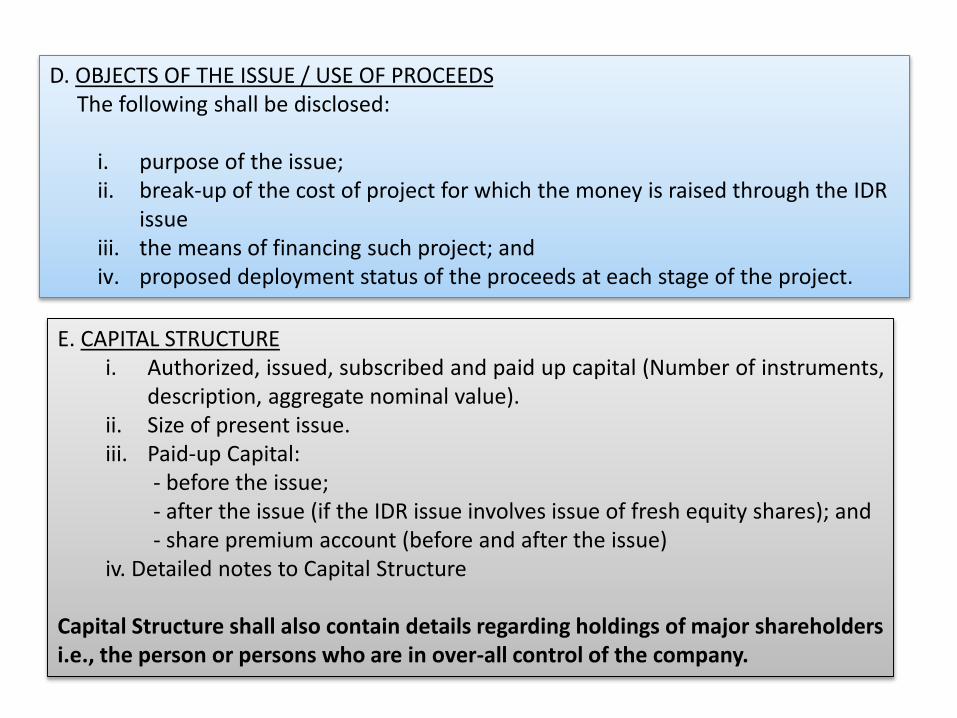

D. OBJECTS OF THE ISSUE / USE OF PROCEEDSThe following shall be disclosed:

i. purpose of the issue;ii. break-up of the cost of project for which the money is raised through the IDR

issueiii. the means of financing such project; andiv. proposed deployment status of the proceeds at each stage of the project.

E. CAPITAL STRUCTUREi. Authorized, issued, subscribed and paid up capital (Number of instruments,

description, aggregate nominal value).ii. Size of present issue.iii. Paid-up Capital:

- before the issue;- after the issue (if the IDR issue involves issue of fresh equity shares); and- share premium account (before and after the issue)

iv. Detailed notes to Capital Structure

Capital Structure shall also contain details regarding holdings of major shareholdersi.e., the person or persons who are in over-all control of the company.

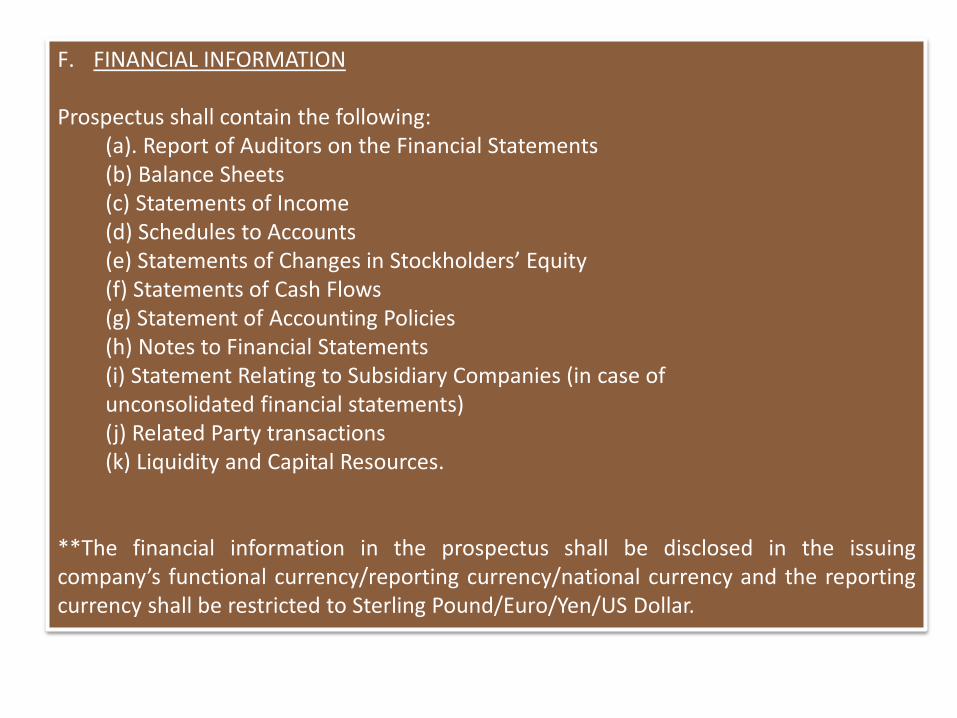

F. FINANCIAL INFORMATION

Prospectus shall contain the following:(a). Report of Auditors on the Financial Statements(b) Balance Sheets(c) Statements of Income(d) Schedules to Accounts(e) Statements of Changes in Stockholders’ Equity(f) Statements of Cash Flows(g) Statement of Accounting Policies(h) Notes to Financial Statements(i) Statement Relating to Subsidiary Companies (in case ofunconsolidated financial statements)(j) Related Party transactions(k) Liquidity and Capital Resources.

**The financial information in the prospectus shall be disclosed in the issuingcompany’s functional currency/reporting currency/national currency and the reportingcurrency shall be restricted to Sterling Pound/Euro/Yen/US Dollar.

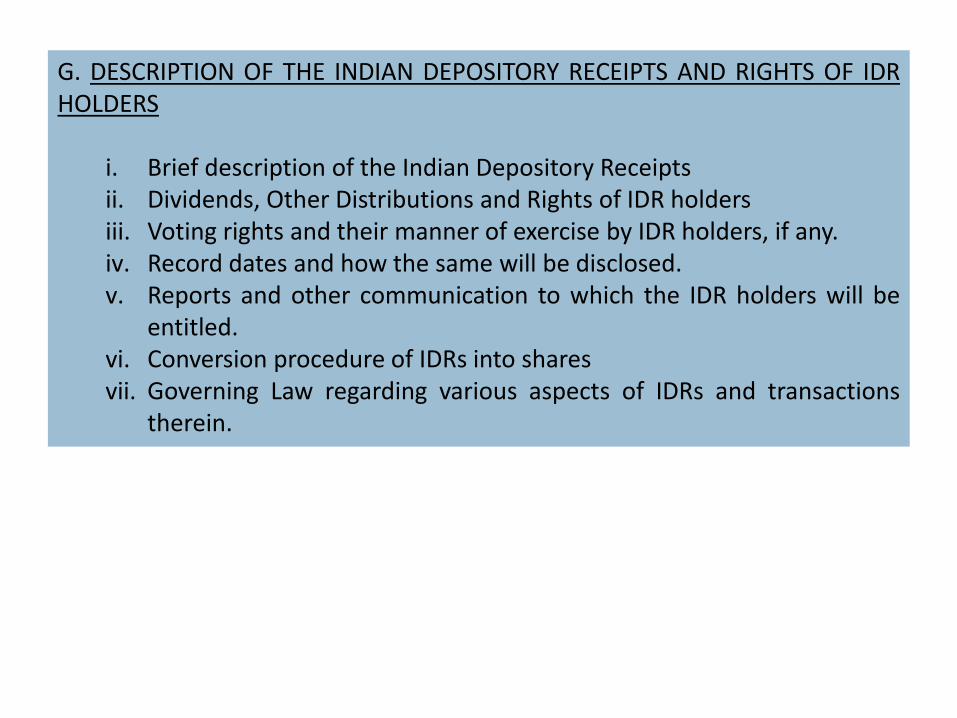

G. DESCRIPTION OF THE INDIAN DEPOSITORY RECEIPTS AND RIGHTS OF IDRHOLDERS

i. Brief description of the Indian Depository Receiptsii. Dividends, Other Distributions and Rights of IDR holdersiii. Voting rights and their manner of exercise by IDR holders, if any.iv. Record dates and how the same will be disclosed.v. Reports and other communication to which the IDR holders will be

entitled.vi. Conversion procedure of IDRs into sharesvii. Governing Law regarding various aspects of IDRs and transactions

therein.

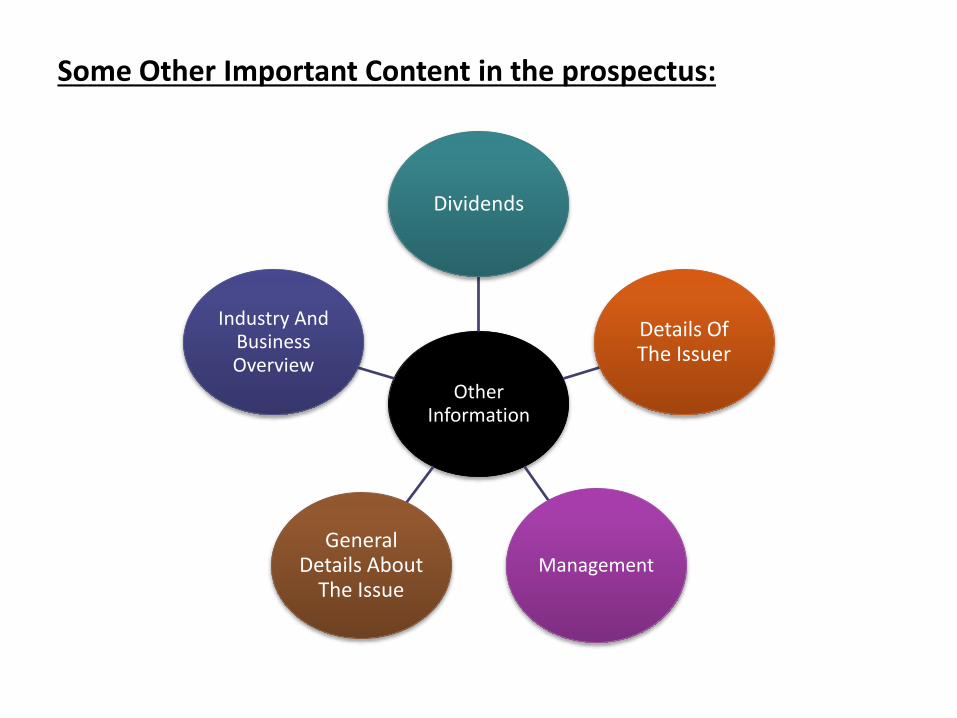

Some Other Important Content in the prospectus:

Other Information

Dividends

Details Of The Issuer

ManagementGeneral

Details About The Issue

Industry And Business Overview

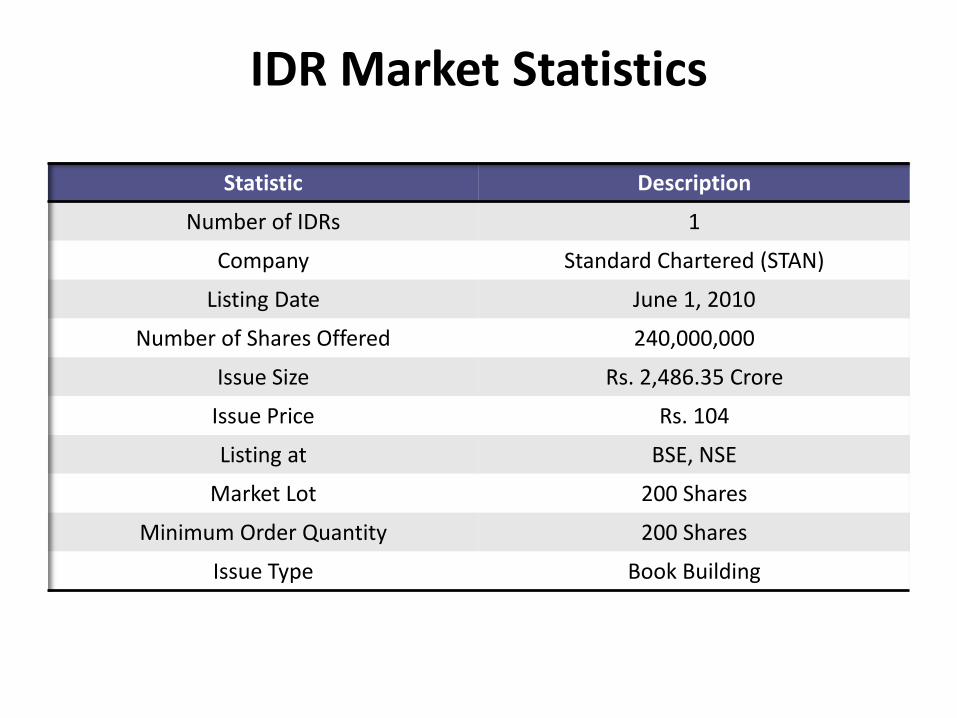

IDR Market Statistics

Statistic Description

Number of IDRs 1

Company Standard Chartered (STAN)

Listing Date June 1, 2010

Number of Shares Offered 240,000,000

Issue Size Rs. 2,486.35 Crore

Issue Price Rs. 104

Listing at BSE, NSE

Market Lot 200 Shares

Minimum Order Quantity 200 Shares

Issue Type Book Building

• It is clear that India’s plan to replicate the ADR and GDR success story has failed totake off due to the differences in capital market regulations, quixotic policies, andtheir perfunctory implementation.

• This also throws focus on the lack of depth and breadth of our equity markets, andthe lack of risk appetite of investors for foreign assets. As of now, very fewcompanies will like to raise funds from India, and establish their Indian association, asSCB PLC did, and gain the first-mover advantage.

• With the cost of compliance increasing in the US and other global markets, India canbe an alluring option for international companies to raise funds at a lower cost andwith less rigorous compliance.

• While the regulatory framework on IDRs has been modified several times over tomeet the needs of issuers, the policy jinx needs to be broken to make the SCB IDR asuccess story.