Indian Coal-Sector Today

53

A REVIEW OF INDIAN COAL SECTOR IGCC AND CCS: FURTHER DEVELOPMENT NEEDED Thanks to; MANOJ JHAWAR , MBA,IIT KANPUR

-

Upload

selfhelp-citizen-dream-merchant -

Category

Education

-

view

75 -

download

2

Transcript of Indian Coal-Sector Today

A REVIEW OF INDIAN COAL

SECTOR

IGCC AND CCS: FURTHER

DEVELOPMENT NEEDED

Thanks to; MANOJ JHAWAR , MBA,IIT KANPUR

INTRODUCTION

Coal was the key energy source for the first industrial revolution

before Oil and Gas were developed.

Through steam engine and steam turbine development, it has

provided amenities like railways, steam shipping for transport,

thermal plant for electricity, new materials (steel, cement and

fertilizers), and advanced communications.

Coal replaced wood combustion because of coal’s abundance,

its higher volumetric energy density and the relative ease of

transportation for coal.

Coal on Indian perspective

According to the Ministry of Coal, India is currently the

third largest producer of coal in the world, with a

production of about 407 million tons (MT) of hard coal

and 30 MT of lignite in 2005–06.

India has significant coal resources, but there is

considerable uncertainty about the coal reserve

estimates for the country.

Coal on Indian perspective

Without improvements in coal technology and

economics, the existing power plants and the new plants

added in the next 10–15 years could consume most of

India’s extractable coal over the course of the plants’

estimated 40- to 50-year lifespans.

Heavy investments in the coal sector, particularly in

underground mining, is needed to increase the pace of

domestic coal production.

Environmental Impact of coal combustion

Coal can have significant adverse

environmental impacts in its production and use.

Over the past two decades major progress has

been made in reducing the emissions of so-

called “criteria” air pollutants: sulfur oxides,

nitrogen oxides, and particulates from coal

combustion plants. It contributes to cost.

CO2 capture and sequestration (CCS) is the critical

enabling technology that would reduce CO2 emissions

significantly while also allowing coal to meet the India’s

pressing energy needs.

The priority objective with respect to coal should be the

successful large-scale demonstration of the technical,

economic, and environmental performance of the

technologies:

that make up all of the major components of a large-

scale integrated CCS system — capture, transportation

and storage.

Mitigation of GHG emission

Broad deployment at a large enough scale in

response to the adoption of a future carbon

mitigation policy, as well as for easing the trade-

off between restraining emissions from fossil

resource use and meeting the future energy

needs. Coal utilization has to consider this

aspect seriously.

o The risk of adverse climate change from global

warming forced in part by growing greenhouse

gas emissions is serious.

o While projections vary, there is now wide

acceptance among the scientific community that

global warming is occurring, that the human

contribution is important, and that

o the effects may impose significant costs on the

Indian economy.

Brief facts about India Coal Industry

India has the fifth largest coal reserves in the world.

88% are non-coking coal reserves & 12% coking coal

reserves

Indian coal is characterized by its high ash content

(45%) and low Sulphur content

Power sector is the largest consumer of coal followed by

the iron and steel and cement segments

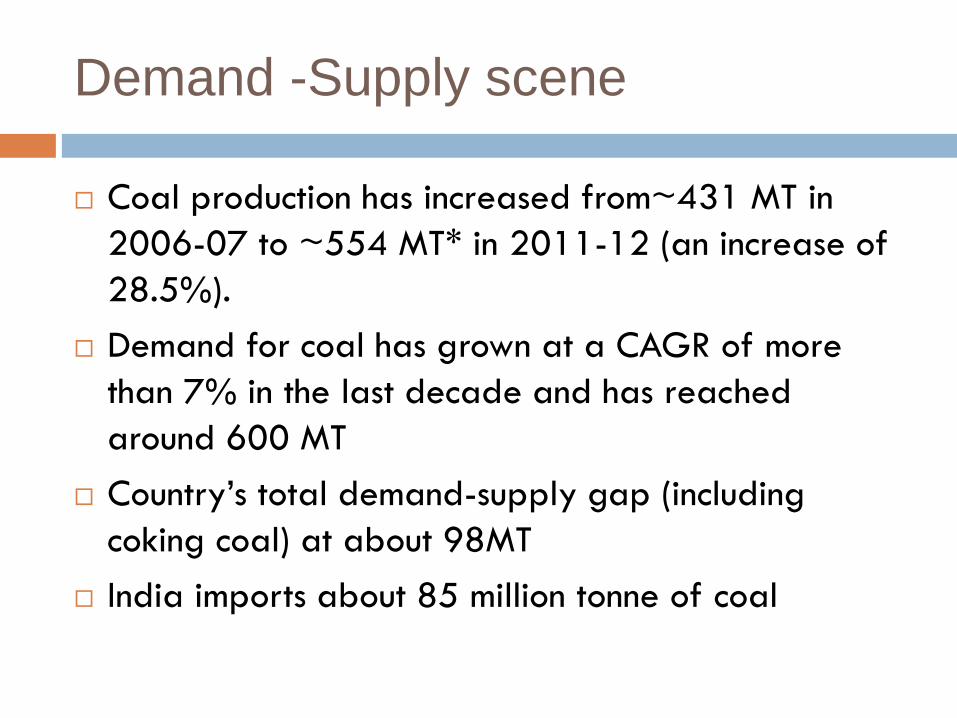

Demand -Supply scene

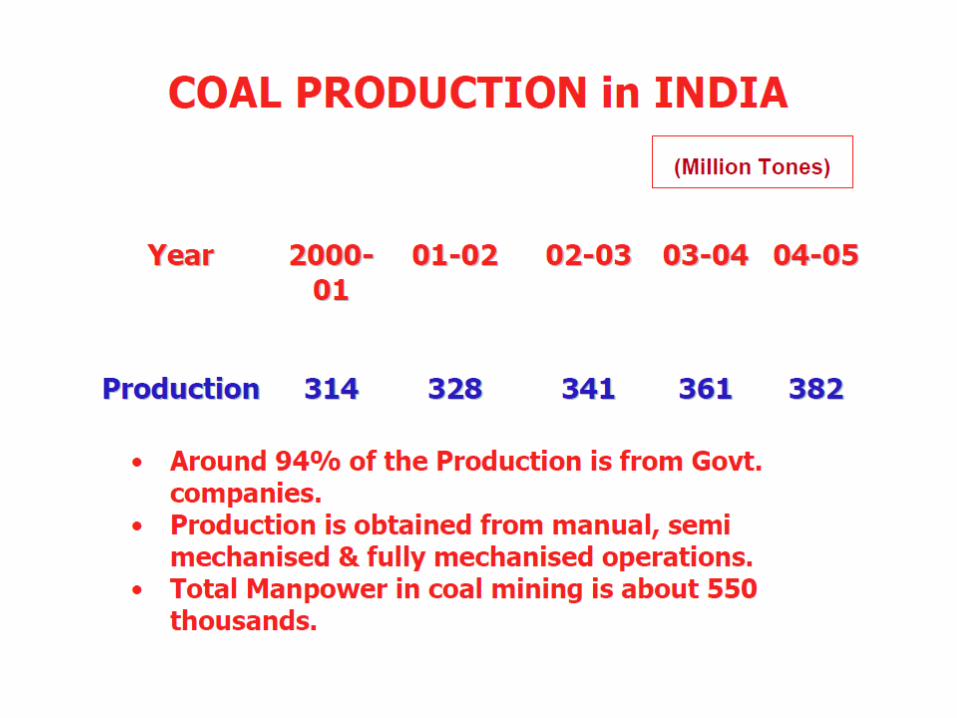

Coal production has increased from~431 MT in

2006-07 to ~554 MT* in 2011-12 (an increase of

28.5%).

Demand for coal has grown at a CAGR of more

than 7% in the last decade and has reached

around 600 MT

Country’s total demand-supply gap (including

coking coal) at about 98MT

India imports about 85 million tonne of coal

COAL DEMAND AND PRODUCTION

Trend in Coal consumption

Trend in industry wise consumption

Trends in Coal Import

Trends in Coal consumption (Industry

wise)

During 1970-71, the railways were the major

consumer of coal (15.58 MTs), followed by steel

and washery industries (13.53 MTs), electricity

generation (13.21 MT) and cement (3.52 MTs).

Since 1975, the electricity generation is the biggest

consumer of coal, followed by steel industries.

Estimated coal consumption for electricity

generation increased from 23 MTs during 1975-76

to 435 MTs during 2011-12.

Coal consumption has increased in almost all industry segments with

electricity contributing the highest consumption clocking a CAGR of

nearly 9% over the years from 1970 to 2011.Except cotton

industry which shows a negative CAGR, the consumption of coal for other industries has gone up over

the years.

For steel and cement sector, coal consumption almost remained

stagnant in 2007 to 2009 due to global slump. It recovered in 2009,

but recorded a down swing in 2010-11 indicating the slow

growth of the segment due to global recession and European

crisis.

Trend in Coal Import

Gross import of coal has steadily increased from 20.93 MTs during 2000-01 to 73.26 MTs during 2009-10.During this period, the quantum of coal exported increased from 1.29 MTs during 2000-01 to 2.45 MTs during 2009-10. However, there was a decline of 5.92% in gross import and 8.89% in net imports of coal in 2010-11 over the previous year. The exports to neighbouring countries increased by about 80% during the same period

Important observations: Coal import

China & India are the highest importer of the

coal.

India was traditionally a coking coal importer due

to unavailability of good quality coking coal for

steel. In the past five years the non coking coal

imports rose from countries like Indonesia and

South Africa.

Important observations: Coal import

Further, the coal washing capacity in the country

has not increased sufficiently, due to various

reasons, to generate the required quantity of

washed coal for consumption, particularly in

steel plants.

This necessitates the import of high quality coal

to meet the requirements of steel plants

Sector wise Coal consumption in India

2011-12 (Source : Coal Ministry)

Electricity Sector

India is the world’s fifth largest energy consumer,

accounting for 4.1% of the global energy consumption.

The current per capita consumption of energy in India

is 0.5 toe against the global average of 1.9 toe,

indicating a high potential for growth in this sector

Total electricity consumed in India approximately 60%

is produced from coal

Steel sector

In 2011, the world crude steel production reached

1,518 MT, reflecting a growth of 6.2% over 2010.

The per capita finished steel consumption in 2011

is estimated at 215 kg for world and 460 kg for

China, while that for India it is estimated currently

at 55 kg (provisional). This clearly indicates scope

for increasing the per capita steel consumption, a

factor which correlates to the coking coal

availability and production within the country.

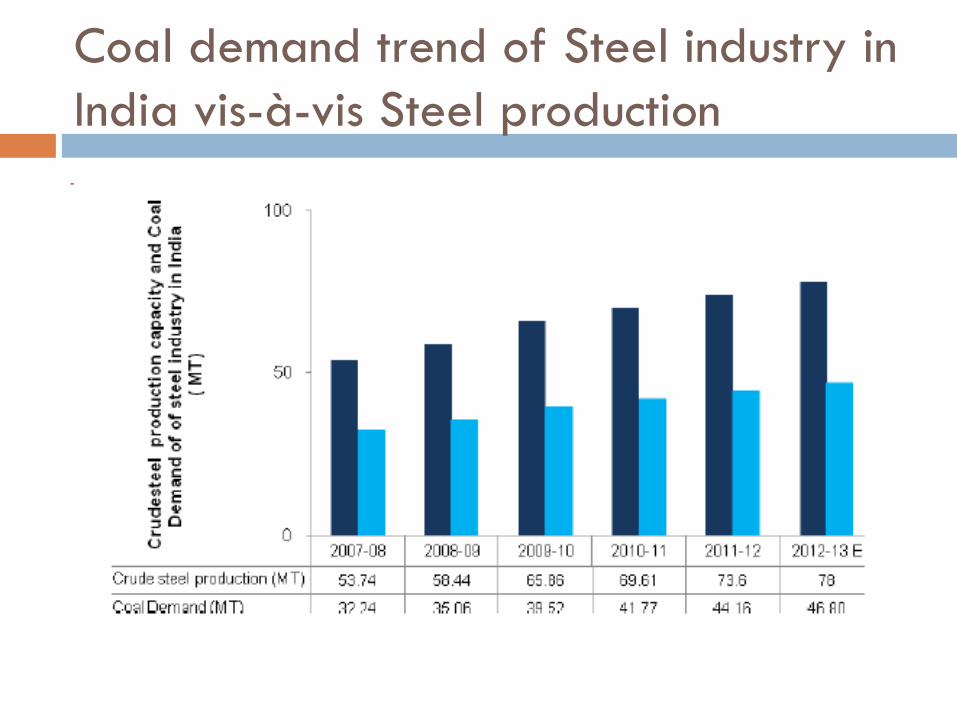

Coal demand trend of Steel industry in

India vis-à-vis Steel production

Coal imports by Steel industry

Cement sector

India is the second largest producer of cement

in the world

Around 450g of coal is consumed to produce

900g of cement. Ratio of 1:2

cement industry is the third largest consumer

of coal in the country.

Coal demand trend of cement Industry

in India vis-à-vis cement production

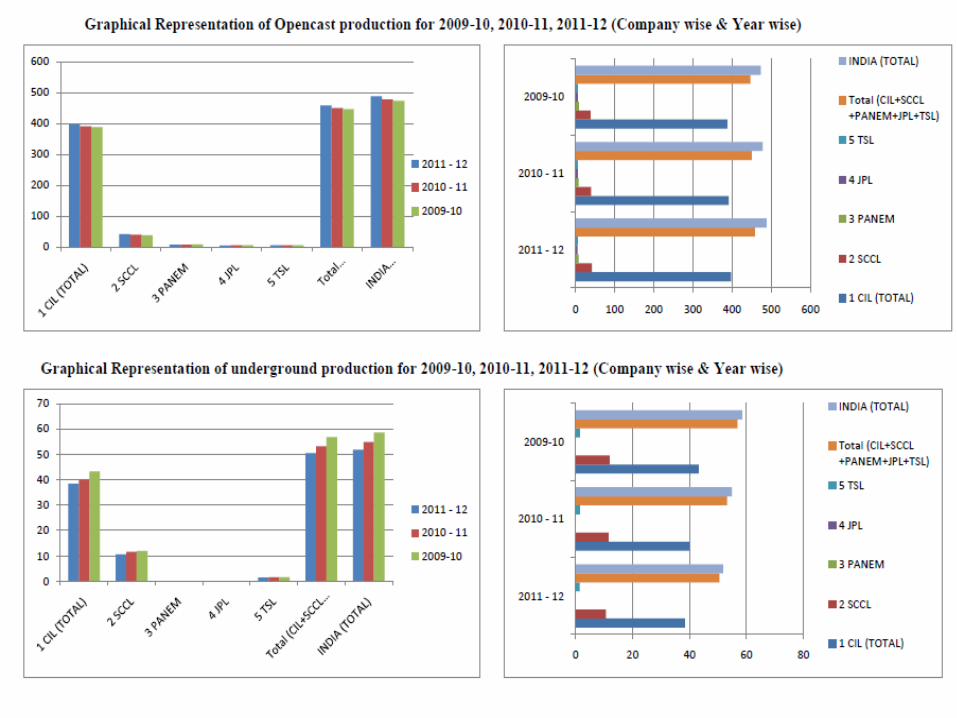

Major Coal Mining Companies

Based on production data from Coal controller

organization report 2011-12, top 5 coal producing

company in terms of coal production are :

1. CIL (PSU)

2. SCCL (PSU)

3. PANEM (Private)

4. TSL (Private)

5. JPL (Private)

NCDP (New Coal distribution Policy)

The category of Core/Non Core sector was dispensed with

Defense and Railways requirement of coal to be met in full

Power and Fertilizer sector normative requirement to be met with 100% supply

Other sectors demand to be met with 75% of their normative requirement

State nominated agencies to be provided with coal to further distribution to small and medium industries for capacity of 4200 tonnes per annum

Steel plants will be supplied coal, but price to be linked with import parity

Fuel Supply Agreement to be signed with all end consumers lifting coal from CIL

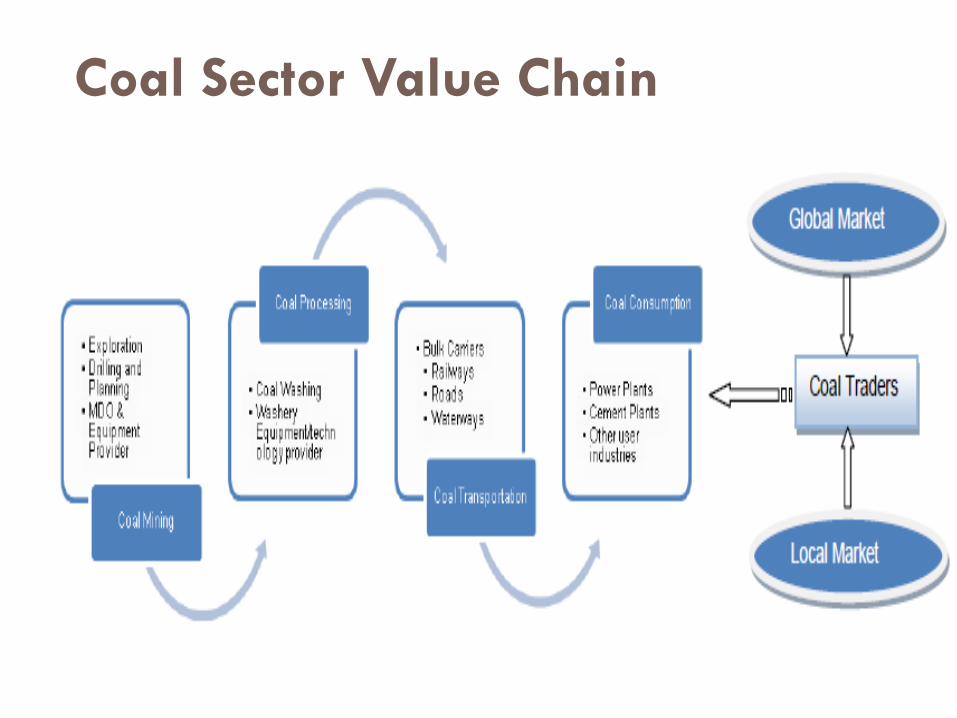

Coal Sector Value Chain

Mining Industry’s Contribution to the

GDP

Captive Coal Blocks

Ways to increase coal supplies in India

Operational or sustenance issues

Fund raising

Performance improvement

All the minerals are not reported as per UNFC classification

Key administrative issues

Long queue of mining applications pending at different levels with the state and centre: This is a deterrent for future investments.

Single window clearance agency (SWCA)

Large number of compliance reports to be filed by the investors to CCO, state DMG, DGMS, tribunals, state and central agencies

Multiple registration requirements for miners, transporters, traders and end-users

Ways to increase coal supplies in India...

Regulatory issues

Lack of policy support for transfer of mining concessions

Blocking of resources

Lack of incentives for exploration

Fiscal issues

Poor connectivity of mining areas and poor evacuation

facilities

Infrastructural issues

Cadastral (Khasra) maps are either not digitised or the geo-

referencing has not been done properly. This creates problems

in lease boundary determination, thus hampering genuine

miners.

Challenges in increasing the production

capacity

For CIL,179 forestry proposals are awaiting clearances and if all approvals are secured on time, it can more than double its output to 1,132 MT, given that mines start production from 2016-17.

Majority of the coal projects have been halted and delayed due to issues in acquiring land and strict rules and regulations (R&R).

Bottlenecks in domestic coal transportation and lack of proper road connectivity further increase the challenge. Also, availability of railway wagons and mismatch of demand and supply of wagons and coal offtake affect production capacity.

Delay in mining activities at captive coal blocks and concerns relating to the increasing ash content of run-of-mine (ROM) coal further hinder production

Way Forward for CIL

CIL needs to strengthen the operations in its

core area of mining

Aggressive investment of surplus available with

CIL, may go in for new technology and UG

mining, improvement in transport and logistics

Switch to market driven pricing for different

consumers (regulated pricing for power and

fertilizer sector and market price at par with

other unregulated sector)

Way forward for Coal Ministry

Attract private investment in exploration, drilling and

planning activities and also in mining through necessary

policy changes and welcome the private players

Competitive bidding for coal blocks but only after full

exploration of coal blocks

The government has initiated the process of competitive bidding

of 54 coal blocks and Crisil has submitted its report on coal

bidding guidelines. It is under evaluation from different stake

holders. The government has identified coal blocks and

segregated them so that the coal blocks come under different

categories for power, steel and state companies.

Way Forward for Private Players

Coal washeries is lucrative business option, need

to partner with state or central government, else

develop captive coal washery for own use

Aggressively foreign asset acquisition and

exploring arbitrage opportunity, whether to source

coal to the country or trade in global platform

Observations

Private players in coal mining operations have the best

opportunity as huge investment and big push in underground

mining is the future sustainability coal mining operations.

Only explored coal blocks are competitive for captive coal

block allocation and government should fast track the

process. Exploration offers the maximum opportunity for

private players, When opened fully, coal washing the next big

thing

The priority objective with respect to coal should be the

successful large-scale demonstration of the technical,

economic, and environmental performance of the

technologies that make up all of the major components of a

large-scale integrated CCS system — capture, transport and

storage.

Such demonstrations are a prerequisite for broad

deployment at large scale in response to the adoption of a

future carbon mitigation policy, as well as for easing the

trade-off between restraining emissions from fossil resource

use and meeting the world’s future energy needs

IGCC and CCS: Further development needed

CO2 capture for several alternative coal combustion and conversion technologies is needed.

At present Integrated Gasification Combined Cycle (IGCC) is the leading candidate for electricity production with CO2 capture.

It is estimated to have lower cost than pulverized coal with capture. It is critical that the government RD&D program develop a suitable technology for IGCC and CCS