India’s Urban Infrastructure Development and Opportunities...

28

India’s Urban Infrastructure Development‐ Overview and Opportunities for PPP Dr. Sudhir Krishna Secretary(UD) Ministry of Urban Development

Transcript of India’s Urban Infrastructure Development and Opportunities...

India’s Urban Infrastructure Development‐ Overview and Opportunities for PPP

Dr. Sudhir KrishnaSecretary(UD)

Ministry of Urban Development

Category Population (Million)

Share in %

India‐

Total 1210.2 100

Rural 833.1 68.8

Urban 377.1 31.2

Million+ Cities 160.7 13.3

Between 100K & 1 Mn

104.2 8.6

Towns < 100K 216.4 17.923 April 2012

Demographic Profile of Urban India‐ Census 2011

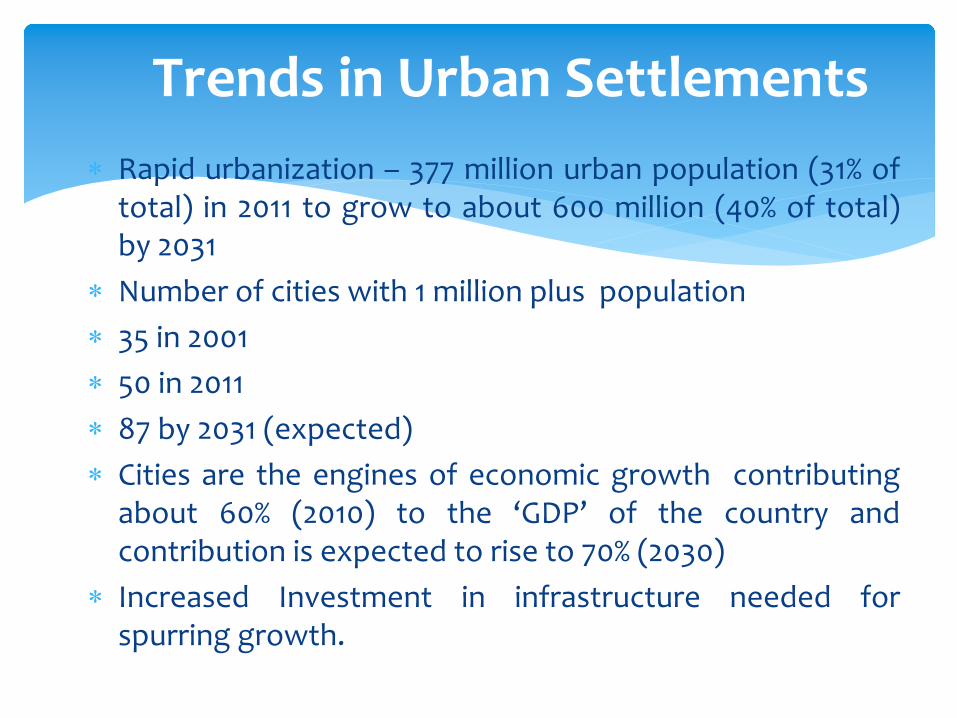

Trends in Urban Settlements

Rapid

urbanization

– 377

million

urban

population

(31%

of

total)

in

2011

to

grow

to

about

600

million

(40%

of

total) by 2031

Number of cities with 1 million plus population

35 in 2001

50 in 2011

87 by 2031 (expected)

Cities

are

the

engines

of

economic

growth contributing about

60%

(2010)

to

the

‘GDP’

of

the

country

and

contribution is expected to rise to 70% (2030)

Increased

Investment

in

infrastructure

needed

for

spurring growth.

23 April 2012

Urban Infrastructure Requirement

Report on Indian Urban Infrastructure and Services 2011

Urban Infrastructure investment requirement of US $ 871 Billion

• Additional US $ 444 Billion for operation and maintenance of assets –

old and new

5

870,81

6

384,20

9

99,872

90,879

71,313

53,931

42,451

22,613

21,774

10,796

4,12

9

68,848

‐100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000 900,000

1,000,000

Total Expen

diture

Urban R

oads

Urban T

ranspo

rt

Rene

wal an

d Re

developm

ent o

f Slum

s Water Su

pply

Sewerage

Storm W

ater Drains

Capacity Bu

ilding

Traffic Sup

port In

frastructure

Solid

Waste M

anagem

ent

Street Lightin

g

Othe

r Sectors

HPEC Estimates in Urban Infrastructure( US $ Million)

Estimates of Urban Services Backlog

6

• Large Backlogs in :• Water

Supply

– Production

varies

from

18% to

62%,

Distribution

extension ‐

25%

to

51%

and

Distribution upgradation ‐

49% to 75%

• Sewerage

– Network and Treatment varies from 53% to 100%

• Solid

Waste

Management

–

Collection

and Transport‐

13%

to

75%,

Processing

–

88%

to

100%

and

Scientific disposal –

100% • Urban

Transport:

Rail

based

MRTS

– 80%

and

Road

Based MRST 100% in Class –IA and IB

Capital Expenditure Estimates by Size Class of Cities‐

HPEC

City Class‐wise Estimates

Total Capital Investment( in $Billion)

Relative Share( %)

Class IA(> 5 Million) 191.1 27.8 Class IB( 1‐5 Million) 153.4 22.3 Class IC(100,000 ‐ 1 Million) 196.3 28.5 Class II(50,000 ‐ 100,000) 38.7 5.6 Class III(20,000 ‐50,000) 62.3 9.1 Class IV(<20,000) 46.6 6.8 Total 688.5 100.0

HPEC Estimates at 2009‐10 prices

Capital and O&M Expenditure Estimates by HPEC & Investment under JNNURM‐I (US$ Bn)

8

SECTORJNNURM

(2005‐2012)

CAPITAL INVESTMENT(2011‐2031)

OPERATION & MAINTENANCE(2011‐2031)

WATER SUPPLY 6.42 71.31 121.35 SEWERAGE 3.95 53.93 52.66 SOLID WASTE MANAGEMENT 0.53 10.80 60.87 URBAN ROADS 2.11 384.21 83.39 STORM WATER DRAINS 2.00 42.45 7.69 URBAN TRANSPORT 1.34 99.87 67.64 TRAFFIC SUPPORT INFRASTRUCTURE 0.19 21.77 8.15 STREET LIGHTING ‐ 4.13 1.05 OTHER SECTORS 0.03 68.85 40.28 RENEWAL AND REDEVELOPMENT 0.17 90.88 ‐ CAPACITY BUILDING ‐ 22.61 ‐

16.74 870.82 443.09 Note : HPEC Estimates are at 2009‐10 prices, all figures are in $ Billion

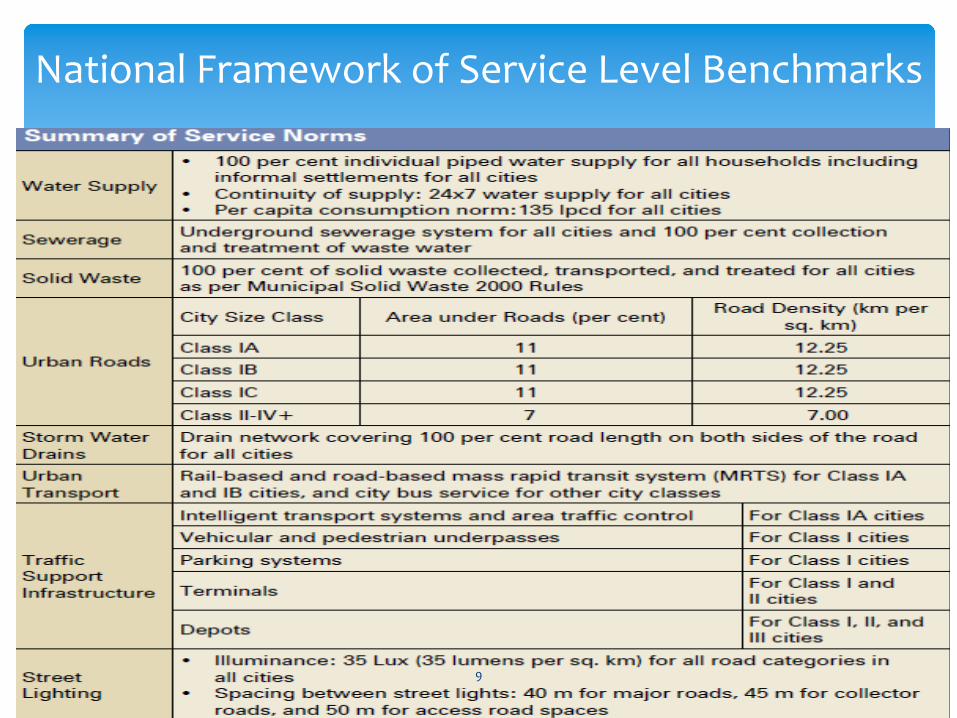

National Framework of Service Level Benchmarks

9

INITIATIVES TO ADDRES SECTOR CHALLENGES

National Framework for Service Level Benchmarking launched in 4 sectors, Water Supply, Sewerage, SWM & Drainage

Steps initiated for improving financial management & accounting system in ULBs thru’

Accrual Accounting

To address rationalization of tariff levels, Water Regulatory Authorities being set up in States

JNNURM Grants require Cities to collect user charges to meet O&M

Reforms focuses on reduction of Non‐revenue water (NRW) in newly sanctioned projects to 20%

10

Opportunities in Urban WatSan

Citizens’

Willingness to pay for better services; the PPP & Bankability of projects

Methodologies of metering‐

water audit & energy audit;

Models of proper Tariff for demand control

Water efficient sanitary fittings

Technology for treatment & reuse of waste water

Rain Water Harvesting; artificial recharge of ground water

11

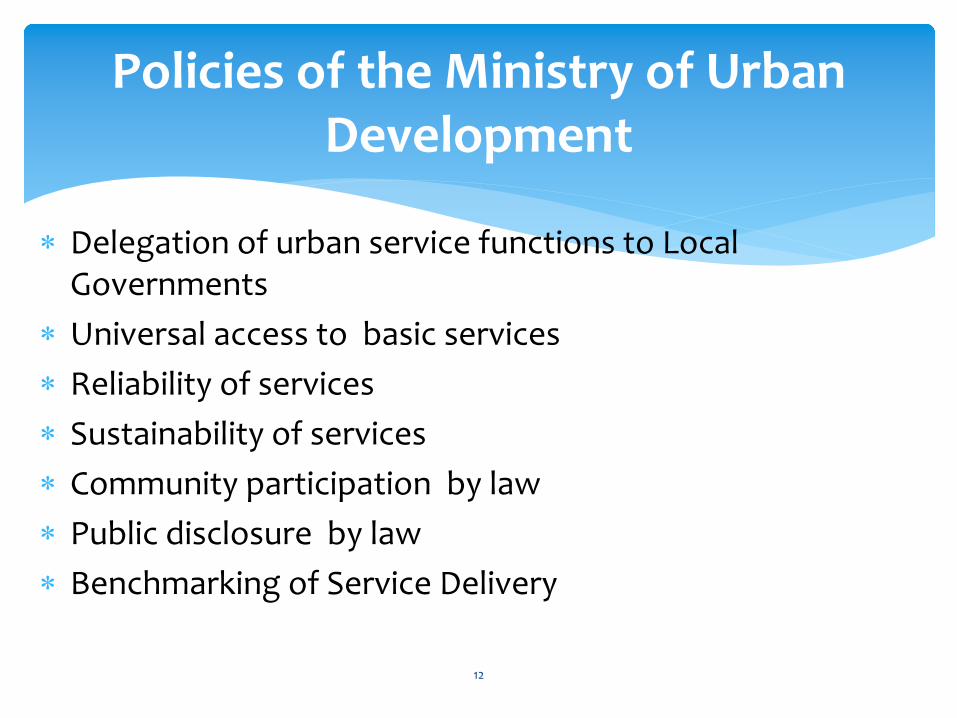

Policies of the Ministry of Urban Development

Delegation of urban service functions to Local Governments

Universal access to basic services

Reliability of services

Sustainability of services

Community participation by law

Public disclosure by law

Benchmarking of Service Delivery

12

Development Strategies

Water Supply Sector

Demand side management

Reduction in NRW , water economics and auditing

energy efficient methods

water saving technologies & appliances

Sewerage sector:

Innovative technologies for sewage treatment, recycling and reuse

Environment:

Groundwater Management thru’

recharge & rainwater harvesting

Governance Sector:

Information technology for managing Water‐Sanitation Utilities

All future development linked to Service Level Benchmarks13

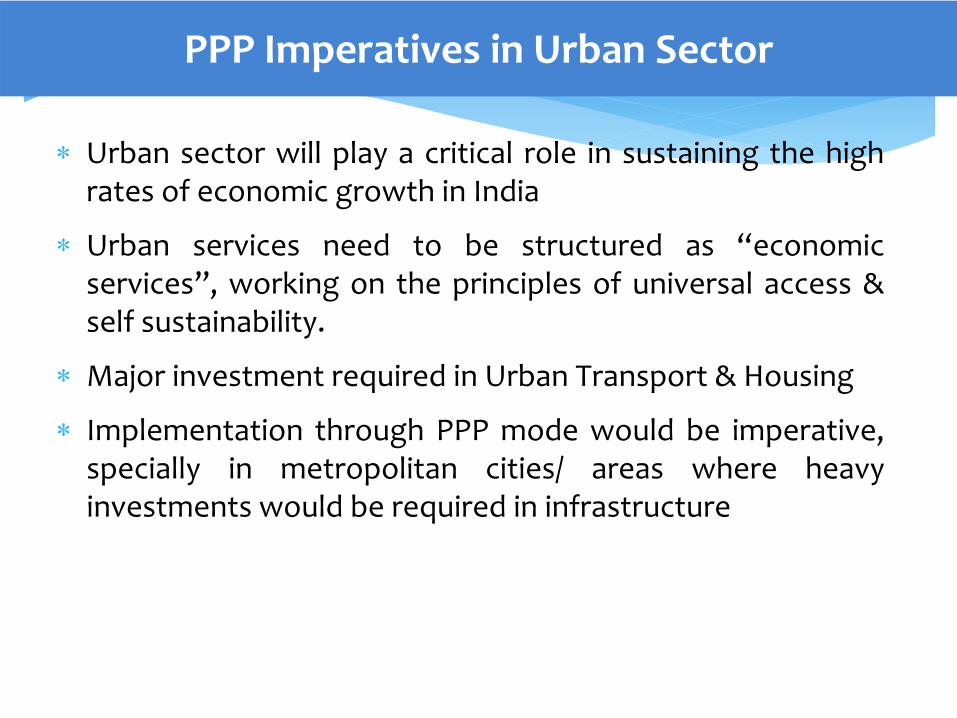

Urban

sector

will

play

a

critical

role

in

sustaining

the

high rates of economic growth in India

Urban

services

need

to

be

structured

as

“economic services”,

working

on

the

principles

of

universal

access

&

self sustainability.

Major investment required in Urban Transport & Housing

Implementation

through

PPP

mode

would

be

imperative, specially

in

metropolitan

cities/

areas

where

heavy

investments would be required in infrastructure

PPP Imperatives in Urban Sector

Growing urbanization => Spurt in travel demand.

Travel demand: 759.82 million passenger km per day in 1991

2001: 1038.8 million passenger km/ day

2021 (Projection):

2511.23

Predominant

modes

of

urban

travel

in

India

are

still

public transport and NMT.

Private ownership of vehicles has increased significantly

Population in 6 major metropolis increased by 1.9 times from 1981 to 2001 but motor vehicles, by 7.75 times.

Many cities are introducing rail–

and bus–

based MRTS.

PPP Imperatives in Urban Sector

Financing Models Urban TransportMode/ component Proposal

Urban Rail Transit Primarily Govt funded except in case of high

density and above ground construction

where PPP may be feasible

Bus Rapid Transit System Infrastructure provisioning by Govt. Bus

provisioning, O&M preferably on PPP with

revenue risk with Government

City Bus Service Bus provisioning, O&M preferably on PPP

with revenue risk with Government

Public Bicycle Scheme Cycle stations and Control centre by

Government, Cycles , O&M by PPP

Bus depots/ Terminal and work

shopsLand by Government, Development

preferably on PPP

Roads and NMT facilities New roads thru self‐financing/ PPP. Existing

roads upgradation by Govt

Source: Recommendations of Working Group on Urban Transport for

12th Five Year Plan

Investment Opportunities in METRO Rail Projects‐

in Kms

S. No.City Metro in

operationMetro under

ImplementationMetro

Planned/Total

Length

1 MUMBAI 0.00 53.90 103.00 156.90

2 KOLKATA 26.20 14.70 73.80 114.70

3 DELHI 189.77 117.00 71.09 377.86

4 CHENNAI 0.00 53.00 0.00 53.00

5 HYDERABAD 0.00 71.16 0.00 71.16

6 BANGALORE 7.00 35.30 75.00 117.30

7 AHMEDABAD 0.00 0.00 58.27 58.27

S. No. City Metro in

operation

Metro under Implementatio n

Metro PlannedTotal

Length

8 PUNE 0.00 0.00 31.51 31.51

9 JAIPUR 0.00 9.25 28.00 37.25

10 LUCKNOW 0.00 0.00 37.20 37.20

11 LUDHIANA 0.00 0.00 28.83 28.83

12 KOCHI 0.00 0.00 25.60 25.60

TOTAL 222.97 354.31 532.30 1109.58

Investment Opportunities in METRO Rail Projects‐

in Kms (contd.)

Kolkata Metro Rail : Work under progressKolkata Metro Rail : Work under progress

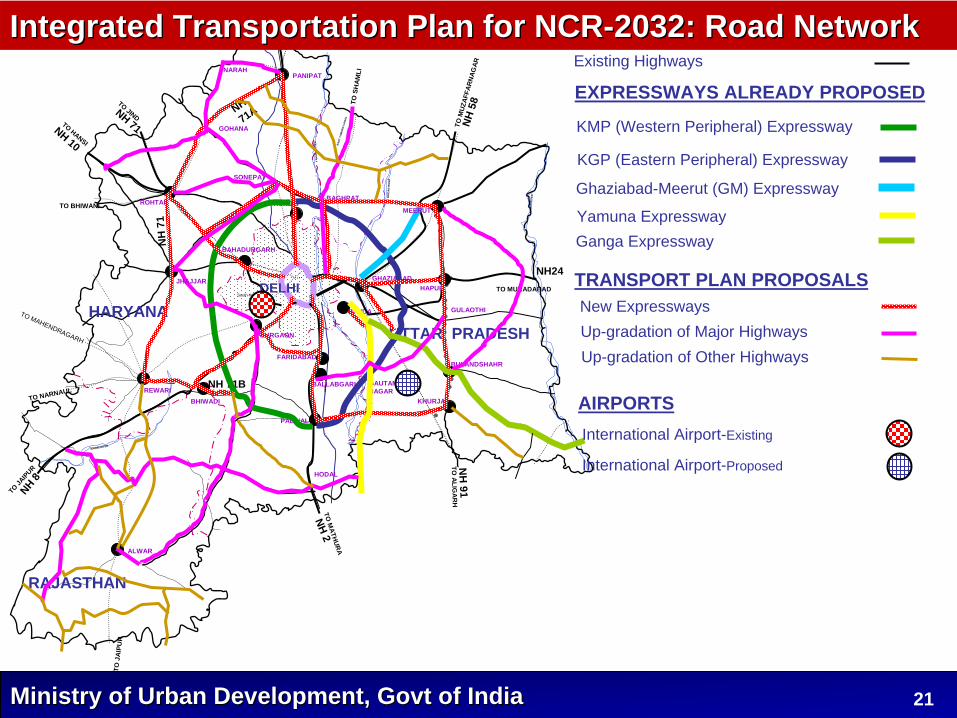

Opportunities for PPP in RRTS proposed in Integrated Opportunities for PPP in RRTS proposed in Integrated Transportation Plan (ITP) for National Capital RegionTransportation Plan (ITP) for National Capital Region‐‐20322032

Road System• Expressways• National Highways• State Highways• Other Roads

Bus System• Bus Fleet &

Infrastructure• Bus Terminals

Rail System• New Rail Lines• RRTS• Mass Rapid Transit

System

Airports• International• Domestic

Others• Logistic Hubs• Integrated Freight

Complexes• Highway Facilities

Centres

ITP for NCR‐2032 proposes following components:

Ministry of Urban Development, Govt of IndiaMinistry of Urban Development, Govt of India 21

Existing Highways

EXPRESSWAYS ALREADY PROPOSED

RAJASTHAN

SONEPAT

GURGAON

BULANDSHAHR

REWARI

ALWAR

NH24

NH 2

TO K

ARN

ALNH

1

TO S

HAM

LI

NH 5

8TO

MUZ

AFFA

RNAG

AR

TO MURADABAD

TO M

ATHURA

NH 8

TO JAIP

UR

TO NARNAUL

TO BHIWANI

TO HANSI

NH 10

AG

RA

CA

NA

L

EAST

YAM

UN

A C

AN

AL

HIN

DA

N R

IVE

R

YA

MU

NA

RIV

ER

SAHIBI RIVER

GA

NG

A R

IVE

R

TO A LI G

AR

HN

H 91

BAHADURGARH

South-West

PANIPAT

GAUTAMBUDHNAGAR

NOIDA

KHURJA

HAPUR

BHIWADI

GHAZIABAD

FARIDABAD

NH

71ANH 71

TO JIND

NH

71

TO J

AIPU

R

NH 71B

KUNDLIROHTAK BAGHPAT

PALWAL

BALLABGARH

TO MAHENDRAGARH

KMP (Western Peripheral) Expressway

KGP (Eastern Peripheral) Expressway

HARYANA UTTAR PRADESH

DELHI

Integrated Transportation Plan for NCRIntegrated Transportation Plan for NCR--2032: Road Network2032: Road Network

Ghaziabad-Meerut (GM) Expressway

New Expressways

Yamuna ExpresswayGanga Expressway

TRANSPORT PLAN PROPOSALS

GOHANA

NARAH

GULAOTHI

HODAL

Up-gradation of Major HighwaysUp-gradation of Other Highways

JHAJJAR

MEERUT

International Airport-Existing

International Airport-Proposed

AIRPORTS

Ministry of Urban Development, Govt of IndiaMinistry of Urban Development, Govt of India 22

TO K

ARN

A

LEGEND

Existing Rail Network

U .P.

RAJASTHAN

HARYANA

MEERUT

BARAUT

SONEPAT

ROHTAK

JHAJJAR

GURGAON

BULANDSHAHR

ALWAR

TO S

HAM

LI

TO MURADABAD

TO M

ATHURA

TO NARNAUL

TO MAHENDRAGARH

TO BHIWANI

R. H

IND

AN

R. Y

AM

UN

A

SAHIBI RIVER

R. G

AN

GA

FARIDABAD

PANIPAT

GAUTAMBUDHNAGAR

KUNDLI

KHURJA

HAPUR

BHIWADI

PALWAL

GHAZIABAD

TO JIND

TO JIND

TO BHIWANI

TO A

LIGAR

H

REWARI

TO HANSI

BALLABAGARH

Jahangirpuri

HolambiKalan

Dwarka

S. Lok

Rithala

Okhla

Dilshad Gn.

Airport

R. Chowk.

Barwala

MundkaShahdara

BAHADURGARH

ShivajiBridge

Badarpur

Dabur Chowk

Kirti nagar

Badli

Sec. 21

Trinagar

NOIDA

22

Integrated Transportation Plan for NCRIntegrated Transportation Plan for NCR--2032: Rail Network2032: Rail Network

DELHI

New Rail Link

Work in Progress- IR Projects

Survey in Progress- IR ProjectsSurvey Sanctioned – IR ProjectsInner Corridor- Proposed Under the Study

RRTS Corridors- Proposed Under the Study

DMRC Corridors -Under State Consideration

RRTS Corridors – Phase I

D.F.C. CORRIDOR

D.F

.C.

CO

RR

IDO

R

D.F.

C. C

ORR

IDO

R

DFC Corridor

DMRC Corridors- Operational

Ministry of Urban Development, Govt of IndiaMinistry of Urban Development, Govt of India 23

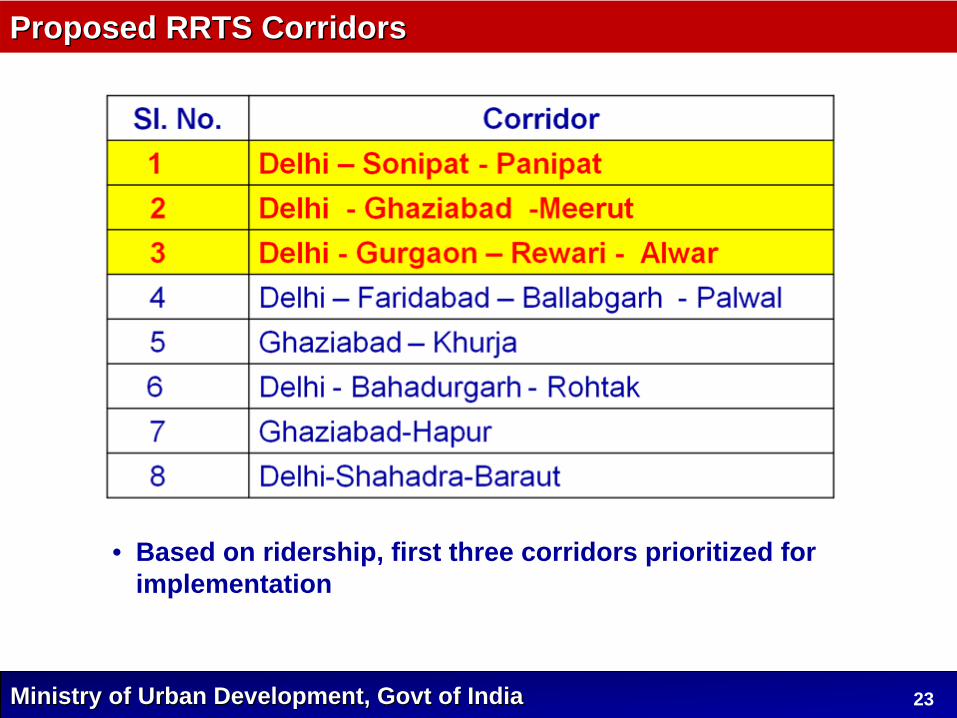

Proposed RRTS Corridors Proposed RRTS Corridors

• Based on ridership, first three corridors prioritized for implementation

Ministry of Urban Development, Govt of IndiaMinistry of Urban Development, Govt of India 24

Capital Cost SummaryCapital Cost Summary

Components Delhi - Panipat

Delhi - Meerut

Delhi - Alwar

Total

Total Base Project Cost including land(without Taxes)

2.93 3.32 4.92 11.17

Total Base Project Cost including land (with central and State Taxes)

3.31 3.82 5.44 12.57

Total Project cost including escalation and IDC (with central and State Taxes)

3.75 4.25 6.43 14.43

US $ Billion

Ministry of Urban Development, Govt of IndiaMinistry of Urban Development, Govt of India 25

Financial Contribution for Financial Contribution for PPRTsPPRTs-- A ModelA Model

Name of Entity Delhi-Panipat Delhi - Meerut Delhi - Alwar Total

% US $ Billion % US $ Billion % US $ Billion

Govt Funding

GoI (MOUD + NCRPB) 15.00% 0.56 15.00% 0.64 15.00% 0.96 15.00% 2.17

GNCTD 3.30% 0.12 2.70% 0.11 5.85% 0.38 4.26% 0.61

Govt of Haryana 11.70% 0.44 - 5.24% 0.34 5.37% 0.78Govt of UP 12.30% 0.52 3.63% 0.52Govt of Rajasthan 3.90% 0.25 1.74% 0.25Total funding by Govt 30.00% 1.13 30% 1.28 30.00% 1.93 30.00% 4.33

Loan - Soft loan, bonds, sub-debt from central & state Govt.

40.00% 1.50 40% 1.70 40.00% 2.57 40.00% 5.77

Investment by PPP partner 30.00% 1.13 30% 1.28 30.00% 1.93 30.00% 4.33

Total investment 100% 3.75 100.00% 4.25 100.00% 6.43 100.00% 14.43

Desalination PPP projects supported by MoUDDesalination PPP projects supported by MoUD

• 100

MLD

desalination

plant

at

Minjur,

Chennai

under DBOOT,

with

Bulk

Water

Purchase

Agreement

with

Chennai Metro Water for a period of 25 years

•Infrastructure

for

Transmission

of

water

from Desalination

Plant

at

KATTUPALLI,

MINJUR

to

City

distribution

network

implemented

under

JNNURM

at

a cost of Rs. 93 crore

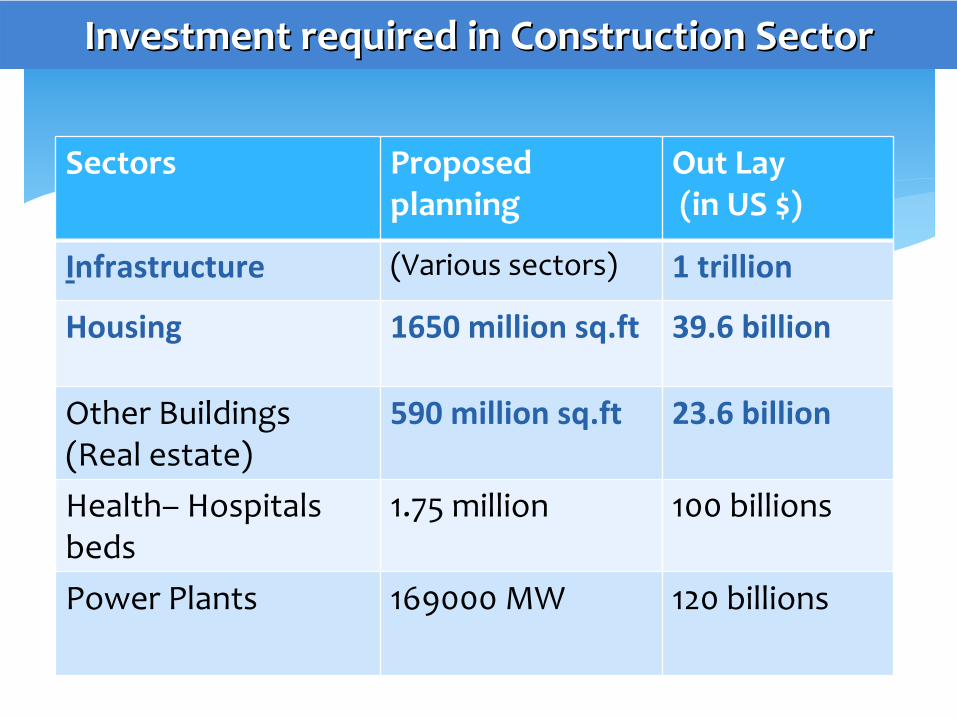

Sectors Proposed planning

Out Lay(in US $)

Infrastructure (Various sectors) 1 trillion

Housing 1650 million sq.ft 39.6 billion

Other Buildings (Real estate)

590 million sq.ft 23.6 billion

Health–

Hospitals beds

1.75 million 100 billions

Power Plants 169000 MW 120 billions

Investment required in Construction SectorInvestment required in Construction Sector

23 April 2012

Thank You

Thank You