INDIA SOLAR - Solare · PDF fileINDIA SOLAR MAP 2015 ASSAM ... Gurgaon, Haryana - 122002,...

2

| +91 11 6654 4708 Mr Tumul Dwivedi (Country Representative) [email protected] www.solarcapital.co.za > 250 MW installed LOWEST COST SOLAR POWER PRODUCER GRID SCALE >50MW INDEPENDANT POWER PRODUCER 266 65 153 KERALA 8,707 MW 4,060 MW 4,678 MW GUJARAT MAHARASHTRA KARNATAKA MADHYA PRADESH RAJASTHAN HARYANA PUNJAB JAMMU & KASHMIR UTTARAKHAND DELHI UTTAR PRADESH JHARKHAND BIHAR MEGHALAYA WEST BENGAL CHATTISGARH ODISHA TAMIL NADU 896 34 2,000 40 26 11 188 44 246 971 1,750 41 111 33 40 5 5 33 2 2 7 16 14 395 112 1 130 2 1 2 16 9 197 PUD 910 Tenders 250 40 128 863 Comm. Comm. Comm. 78 Comm. 18 PUD 155 930 250 Comm. Tenders 565 670 250 862 PUD 225 2,040 TELANGANA 5 76 35 Comm. Comm. PUD 1,750 Tenders Comm. PUD 40 35 PUD Comm. PUD 29 PUD Comm. 5 Tenders 127 395 100 10 PUD 10 10 10 35 PUD 811 Comm. 910 50 1,295 5 Comm. 29 5 Solar parks being developed by Solar Energy Corporation of India (Capacity) Risk profile of Distribution Companies (as per CRISIL, 2013) High Medium low All figures in MW www.bridgetoindia.com Tenders Comm. 250 1,031 Central PV allocation Commissioned (Comm.) Projects under development (PUD) Tenders in progress (Tenders) State PV allocation Other PV CSP 15 117 13 10 1,330 280 3,760 300 7,953 474 2,064 1,066 219 Comm. PUD 222 862 Comm. 13 13 50 150 Tenders 130 150 260 PUD 116 2,580 2,500 661 50 8 5 3 3 PUD Tenders Comm. 55 150 19 Comm. 7 INDIA SOLAR MAP 2015 ASSAM Premium sponsor Launch partner ANDHRA PRADESH 35 55 150 224 146 300 195 370 PUD 500 Comm. Tenders 50 403 500 67 136 200 40 10 80 100 Total utility scale solar capacity as of September 2015 (MW) 2,500 MW 1,000 MW 1,600 MW 750 MW 600 MW 2,700 MW 700 MW 150 MW 200 MW 31.2% Self EPC 6.7% STERLING & WILSON BELECTRIC 0.7% IBC SOLAR 0.5% PHOTON 0.6% OTHERS 5.7% 5.9% L&T 5.5% MOSER BAER TATA POWER SOLAR 4.5% LANCO 3.6% MAHINDRA 3.4% WAAREE 3.3% JUWI 3.6% RAYS POWER 3.4% INFRA UJAAS 2.2% RAYS EXPERTS 2.4% REFEX 2.6% MEIL 1.5% VIKRAM SOLAR 1.8% ENRICH 1.9% HARSHA ABAKUS 2.0% EMMVEE 1.5% BHEL 1.4% CHEMTROLS 0.9% JAKSON POWER 0.8% BOSCH 0.7% PREMIER 0.7% CIRUS SOLAR 1.5% EPC contractors 30.3% ABB 22.4% SMA OTHERS 1.1% REFUSOL 0.4% SHARP 0.5% TBEA 0.5% BONFIGLIOLI 15.2% SCHNEIDER 8.1% AEG 4.2% TMEIC 2.5% HITACHI 7.1% HELIOS 2.9% STATCON 1.0% SIEMENS 0.9% SANTERNO 0.9% DELTA 0.8% ELTEK 0.6% SUNGROW 0.5% Inverter suppliers 15.6% FIRST SOLAR 7.6% OTHERS 10.0% TRINA 9.3% CANADIAN 6.4% RENESOLA WAAREE 4.0% CHINT 3.5% EMMVEE 3.4% SHARP 2.7% VIKRAM SOLAR 2.7% HANWHA 2.6% YINGLI 2.3% NEXPOWER 2.1% CNPV 1.3% SOLAR FRONTIER 1.3% DU PONT 1.3% UJAAS 1.2% SUNWELL 1.2% REC 1.0% SUNTECH 1.0% BHEL 0.8% LDK 0.8% SCHUTTEN 0.7% QS SOLAR 0.7% WEBEL 0.6% EINNOVA 0.6% SHAN SOLAR 0.6% SCHEUCO 0.5% HAREON 0.5% BYD 0.5% JINKO 4.6% CSUN 4.5% TATA POWER SOLAR 4.2% Module suppliers Crystalline Thin film Both Cumulative market shares (for projects commissioned until August 2015) 7.6% WELSPUN 5.4% AZURE OTHERS 44.4% 4.6% SUNEDISON 3.8% ACME 3.4% MAHAGENCO 2.7% ESSEL INFRA 2.5% NTPC 2.3% TORRENT 2.0% HPPPL 1.9% MALPANI 1.7% ADITYA BIRLA 1.3% TATA POWER 1.1% RENEW 1.1% WANEEP 1.1% TODAY GROUP 1.1% ROHA 1.1% SOLAIREDIRECT 1.0% RELIANCE 1.0% PUNJ LLYOD 0.9% HERO 0.9% ADANI 0.9% IL&FS 0.9% LANCO 0.9% KIRAN ENERGY 0.8% MAHINDRA 0.8% SEMBCORP 0.8% MADHAV INFRA APEX CLOTHING 0.7% VIKRAM 0.7% SWELECT 0.6% Project developers

Transcript of INDIA SOLAR - Solare · PDF fileINDIA SOLAR MAP 2015 ASSAM ... Gurgaon, Haryana - 122002,...

| +91 11 6654 4708

Mr Tumul Dwivedi (Country Representative)[email protected]

> 250 MW installed

LOWEST COST SOLAR POWER

PRODUCER

GRID SCALE >50MWINDEPENDANT POWER PRODUCER

266

65

153

KERALA

8,707 MW

4,060 MW

4,678 MW

GUJARAT

MAHARASHTRA

KARNATAKA

MADHYA PRADESH

RAJASTHAN

HARYANA

PUNJAB

JAMMU & KASHMIR

UTTARAKHAND

DELHI

UTTAR PRADESH

JHARKHAND

BIHAR

MEGHALAYA

WEST BENGAL

CHATTISGARH

ODISHA

TAMIL NADU

896

34

2,000

40

26

11

188

44

246

971

1,750

41

111

33

40

5

533

2

2

7

16

14 395

112

1130

21 2

16

9

197

PUD

910Tenders

25040

128

863

Comm.

Comm.

Comm.

78

Comm.

18

PUD

155

930

250Comm. Tenders

565

670

250

862

PUD

225

2,040

TELANGANA5

76

35

Comm.

Comm. PUD

1,750

Tenders

Comm. PUD

4035

PUD

Comm. PUD

29PUD

Comm.

5

Tenders

127

395

100

10PUD

10

10

10

35

PUD811

Comm.

910

50

1,295

5Comm.

29

5

Solar parks being developed bySolar Energy Corporation of India (Capacity)

Risk profile of Distribution Companies(as per CRISIL, 2013)High Medium low

All figures in MW

www.bridgetoindia.com

TendersComm.

250

1,031

Central PV allocation

Commissioned (Comm.)

Projects under development (PUD)

Tenders in progress (Tenders)

State PV allocation Other PVCSP

15

117

13

10

1,330

280

3,760

300

7,953 474

2,064 1,066

219

Comm. PUD

222

862

Comm.

13

13

50

150Tenders

130150

260

PUD

116

2,580

2,500 661

50

8

53

3

PUD TendersComm.

55

150

19

Comm.

7

INDIA SOLARMAP 2015

ASSAM

Premium sponsor Launch partner

ANDHRA PRADESH

35

55 150

224

146

300 195

370

PUD500

Comm. Tenders

50

403

500

67

136

200

40

10

80

100

Total utility scale solar capacity as of September 2015 (MW)

2,500MW

1,000MW

1,600MW

750MW

600MW

2,700MW

700MW

150 MW

200 MW

31.2% Self EPC

6.7% STERLING & WILSON

BELECTRIC 0.7%IBC SOLAR 0.5%

PHOTON

0.6%

OTHERS 5.7%

5.9% L&T

5.5% M

OSER BAER

TATA

PO

WER

SO

LAR

4.5

%

LAN

CO 3

.6%

MAHINDRA 3.4%WAAREE 3.3%

JUW

I 3.6

%

RAYS P

OWER 3.4%

INFRA

UJAAS 2.2%

RAYS EXPERTS 2.4%

REFEX 2.6%

MEIL 1.5%

VIKRAM SOLAR 1.8%ENRICH 1.9%HARSHA ABAKUS 2.0%

EMMVEE 1.5%

BHEL 1.4%

CHEMTROLS 0.9%

JAKSON POWER 0.8%

BOSCH 0.7%

PREMIER 0.7%CIRUS SOLAR 1.5%

EPC contractors

30.3% ABB

22.4% SM

A

OTH

ERS 1.1%

REFU

SOL 0.4%

SHAR

P 0.5%TB

EA 0.5%

BONFI

GLIO

LI 15

.2%

SCHNEIDER 8.1%

AEG 4.2%

TMEIC 2.5%

HITACHI 7.1%

HELIOS 2.9%STATCON 1.0%

SIEMEN

S 0.9%SAN

TERNO 0.9%

DELTA 0.8%ELTEK 0.6%

SUN

GROW 0.5%

Inverter suppliers

15.6% FIRST SOLAR

7.6%

OTH

ERS

10.0% TRINA

9.3% CANADIAN6.4% REN

ESOLA

WAAREE 4.0%CHINT 3.5%

EMMVEE 3.4%

SHARP 2.7%

VIKRAM SOLAR 2.7%

HANWHA 2.6%

YINGLI 2.3%

NEXPOWER 2.1%

CNPV 1.3%

SOLAR FRONTIER 1.3%

DU PONT 1.3%

UJAAS 1.2%

SUNWELL 1.2%

REC 1.0%

SUNTECH 1.0%BHEL 0.8%LDK 0.8%

SCHU

TTEN 0.7%

QS SOLAR 0.7%W

EBEL 0.6%

EINN

OVA 0.6%SH

AN SOLAR

0.6%SCH

EUCO

0.5%H

AREO

N 0.5%

BYD

0.5%

JIN

KO

4.6

%

CSU

N 4

.5%

TATA

POW

ER S

OLAR

4.2

%

Module suppliers

Crystalline

Thin film

Both

Cumulative market shares(for projects commissioned until August 2015)

7.6%

WEL

SPU

N

5.4%

AZU

RE

OTHERS 44.4%

4.6% SUNEDIS

ON

3.8% ACME

3.4% MAHAGENCO

2.7% ESSEL INFRA

2.5% NTPC

2.3% TORRENT2.0% HPPPL1.9% MALPANI

1.7% ADITYA BIRLA

1.3% TATA POWER

1.1% RENEW

1.1% WANEEP

1.1% TODAY GROUP

1.1% ROHA

1.1% SOLAIREDIRECT

1.0% RELIANCE

1.0% PUN

J LLYOD

0.9% H

ERO

0.9% ADAN

I

0.9% IL&

FS

0.9% LAN

CO

0.9% KIR

AN EN

ERGY

0.8% M

AHIN

DR

A

0.8% SEM

BCO

RP

0.8% M

ADH

AV INFR

A

APEX

CLO

THIN

G 0

.7%

VIK

RAM

0.7

%SW

ELEC

T 0.

6%

Project developers

INVERTER SUPPLIERSHitachi Hi-Rel Power Electronics Pvt. Ltd.B-52, Corporate House, Judges Bungalow Road, Bodakdev, Ahmedabad - 380 054,Gujarat, IndiaContact Person: Mr. Sanjay Bhalekar E: [email protected] [email protected]: +91 8511134591P: +91 79 66046200F: +91 79 66046201www.hitachi-hirel.com

EPC CONTRACTORSVikram Solar Pvt. Ltd. "The Chambers" (8th Floor), 1865 Rajdanga Main Road,Kolkata - 700107Contact Person: Mr Saugata Datta(President - Business Development)E: [email protected] [email protected]: +91 33 24427299www.vikramsolar.com

Sponsored taxonomy

SEMIKRON Electronics P. Ltd.Plot No. - EL-148,TTC Industrial Area, MIDC Electronic Zone,Mahape, Navi Mumbai - 400710,Maharashtra, IndiaContact Person: Mr. Padmanabha Kamath E: [email protected]: +91 22 27628600www.semikron.com

PROJECT DEVELOPERSACME Cleantech Solutions Pvt. Ltd. Plot No. 152, Sector-44,Gurgaon, Haryana - 122002, IndiaContact Person:Mr. Manish Karna, Ms. Vijeta ChaudharyE: [email protected] [email protected]: +91 8588010331, +91 9873481330www.acme.in

Jakson Engineers Limited A-43, Phase – II (Extension), Hosiery Complex, Noida – 201305 (UP) IndiaContact Person: Mr Parshant KalraE: [email protected]: +91 9871122307P: +91 120 4526168 (direct line) +91 120 4302600www.jakson.com

SkyPower SkyPower New Delhi Office4th Floor, Rectangle No.1Behind Saket Sheraton HotelCommercial Complex D4, SaketNew Delhi - 110017, IndiaSkyPower GlobalFirst Canadian Place100 King Street West 30th FloorToronto Ontario Canada M5X 1C9Contact Person: Mr. Vikas VermaE: [email protected]

Commissioned

4,678MW

Our reports

INDIASOLARMAP2015

India Solar HandbookIndia Solar Handbook provides holistic assessment of the Indian solar market. Released every year at Intersolar Germany in July, it is a highly sought after publication in the industry.

India Solar MapThe India Solar Map is a simple, one-of-its-kind infographic that provides a quick snapshot of the Indian utility scale solar market. Referred to by more than 50,000 industry stakeholders, it contains vital market information and trends including state-wise installed project capacity, project tariffs and market shares of leading players. It is released every year in September at Renewable Energy India Expo.

India Solar Rooftop MapIndia Solar Rooftop Map is the country's most comprehensive publication on the rooftop solar segment, with a reach of over 25,000 domestic and international stakeholders. It contains vital market information and identifies key trends and themes in India's burgeoning solar rooftop segment. The India Solar Rooftop Map is released at Intersolar Mumbai in November every year.

Thought Leadership ReportsBRIDGE TO INDIA regularly partners with influential market stakeholders to publish thought leadership reports. We identify emerging market themes and provide our analyses based on rigorous evaluation of the economic, technical, regulatory and policy fundamentals of cleantech sector in India. Recently, we have worked with Tata Power Solar, Greenpeace and Prayas.

Our services

About BRIDGE TO INDIABRIDGE TO INDIA is the leading consulting and knowledge services provider in the Indian cleantech market. Our multi-functional experience expertise combined with comprehensive in-house research capability enables us to develop insightful and highly sought-after industry analyses. Our overarching goal is to provide customised cleantech solutions and enable innovative business models in India.

We work actively with all leading stakeholders including project developers and investors, energy customers, equipment suppliers, regulators, policy makers and development institutions. We have also helped a number of international top-tier cleantech companies in growing their business footprint in India by providing risk assessment and business partner selection services.

Business strategy Market environment White papers

Uniqueunderstanding

of the Indiancleantech market

Always up-to-date

Industry access

360 degree view

Financial advisory

Business restructuring

Due diligence

MarketIntelligence

Strategy Consulting

TransactionAdvisory

Head OfficeC-8/5, DLF Phase 1,Gurgaon - 122001 (HR)India

P +91 124 4204003E [email protected]

www.bridgetoindia.com

www.facebook.com/bridgetoindia

www.twitter.com/bridgetoindia

India Solar Future

Project under development

8,707MWTenders in progress

4,060MW

Premium sponsor Launch partner

India Solar Rooftop Map is the only comprehensive publication covering the country’s rooftop solar segment. This all-in-one-map acts as a ready reckoner and contains vital market information that helps the industry analyse key trends and themes in one of the most high potential solar markets in the world. Various stakeholders retain and refer this map in order to understand the market developments and make sound strategic decisions. The map's print copy is distributed to over 12,000 market participants, including all key public officials and policy makers. The map is also available for online download through the year.

For submitting project informationPlease share your project level data with us at [email protected]. We need data for rooftop projects where you have provided your products/services. The following five basic details are needed: customer name, system capacity, makes of modules and inverteers used, location and date of commissioning.

For sponsorship and advertisement opportunitiesPlease contact us at [email protected]

Current installed capacityby segment and geography

Market shares for moduleand inverter suppliersand EPC contractors

Trends in policies andbusiness models

and muchmore…

Segment-wisemarket projections

Key indicators ondemand for solar powerbased on parity markets

Make your presence felt in

INDIA SOLARROOFTOP MAP 2016

Due for release at Intersolar Mumbaiin November 2015

CompanyName

Azure

Acme

SunEdison

Essel Infra

Welspun

Torrent

Waneep

Renew

Solairedirect

Hero

Rank2014

7

5

3

-

2

4

-

-

-

-

Rank2015

1

2

3

4

5

6

7

8

9

10

Increase/ Decrease

Project developers

Notes1. BRIDGE TO INDIA has conducted an extensive data collection exercise and relied on multiple market sources to provide accurate, factual information as far as possible. However, we cannot guarantee completeness or accuracy of this information.

2. For almost all projects, the data available with BRIDGE TO INDIA has been cross-referenced with data provided by other market players.

3. Only grid connected projects above 1 MW have been considered.

4. For most of the analysis, we have relied on AC capacity numbers where available.

5. Market information for project developers: a. Market share for this category is based on available data for 4,459 MW of projects. b. Credit for the 50 MW Welspun-Mahagenco JV project has been given 50:50 to Mahagenco and Welspun respectively.

6. Market information for third-party EPC contractors: a. Market share for this category is based on available data for only 4,046 MW of projects. b. In some cases, procurement responsibilities for some or all of the equipment may be excluded from the scope.

c. In many projects, EPC contractor role is split between various parties. We have used multiple criteria for determining credits including final responsibility for commissioning and value of contracts.

7. Market information for module suppliers: a. Market share for this category is based on available data for only 4,139 MW of projects. b. The following companies were unreachable or have not confirmed the data: LDK, BHEL, CSun, BYD, Hareon, Webel, REC, Sunwell, Solar Frontier, Scheuco, Einnova, Shan Solar, Schutten, Suntech, Nexpower, Yingli.

8. Market information for inverter suppliers: a. Market share for this category is based on available data for only 3,890 MW of projects. b. The following companies were unreachable or have not confirmed the data: Bonfiglioli, Schneider, Siemens, Statcon, Santerno, Refusol, Sharp, Sungrow, Helios and Eltek.

Module suppliersCompany Name

First Solar

Trina

Canadian Solar

Renesola

Waaree

Emmvee

Tata Power Solar

Jinko

Vikram Solar

Chint

Rank2014

5

4

3

2

-

7

1

10

-

6

Increase/ Decrease

Inverter suppliersCompany Name

ABB

SMA

Hitachi

TMEIC

Schneider

Helios

Bonfiglioli

TBEA

Delta

Sungrow

Rank2014

1

5

4

-

3

9

2

-

-

7

Increase/ Decrease

EPC contractorsCompany Name

Mahindra Susten

S&W

Rays Power Infra

L&T

Juwi

Vikram Solar

Harsha Abakus

Waaree

BHEL

Emmvee

Rank2014

-

4

10

8

-

-

7

-

-

9

Increase/ Decrease

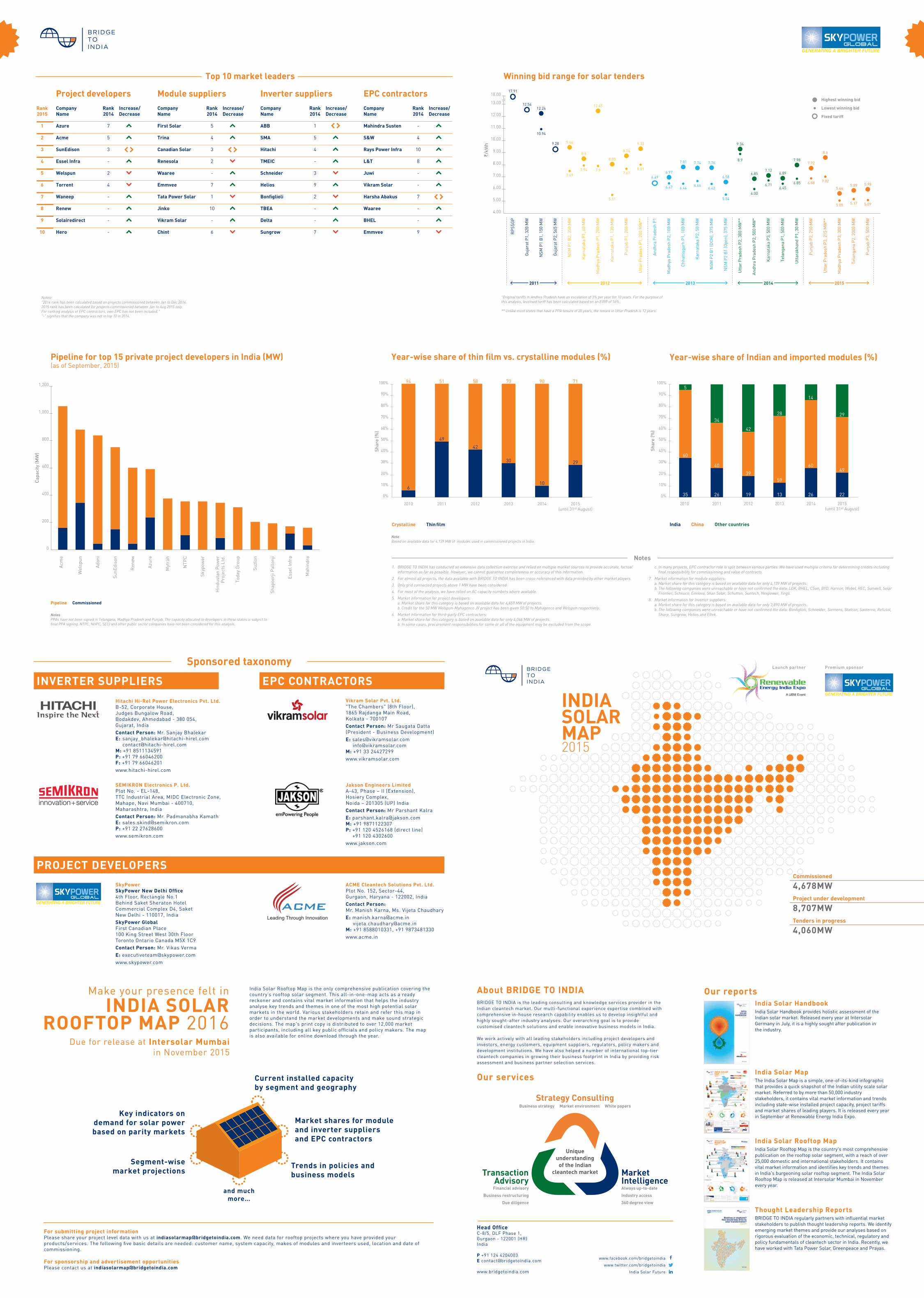

Top 10 market leaders

Notes:"2014 rank has been calculated based on projects commissioned between Jan to Dec 2014. 2015 rank has been calculated for projects commissioned between Jan to Aug 2015 only. For ranking analysis of EPC contractors, own EPC has not been included.""-" signifies that the company was not in top 10 in 2014.

Year-wise share of Indian and imported modules (%)

India China Other countries

2010 2011 2012 2013 2014 2015(until 31st August)

Shar

e (%

)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

35 26 19 13

59

28

26

60

14

22

49

29

39

42

40

34

60

5

Year-wise share of thin film vs. crystalline modules (%)

NoteBased on available data for 4,139 MW of modules used in commissioned projects in India.

Crystalline Thin film

2010 2011 2012 2013 2015(until 31st August)

2014

6

49

42

30

10

94 51 58 70 90

29

71

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Sh

are

(%)

Pipeline for top 15 private project developers in India (MW)(as of September, 2015)

NotesPPAs have not been signed in Telangana, Madhya Pradesh and Punjab. The capacity allocated to developers in these states is subject to final PPA signing. NTPC, NHPC, SECI and other public sector companies have not been considered for this analysis.

Pipeline Commissioned

0

200

400

600

800

1,000

1,200

Cap

acity

(MW

)

Acm

e

Wel

spun

Adan

i

SunE

diso

n

Ren

ew

Azur

e

Myt

rah

Esse

l Inf

ra

NTP

C

Skyp

ower

Hin

dust

an P

ower

Proj

ects

Ltd

.

Toda

y G

roup

Suzl

on

Shap

oorj

i Pal

lonj

i

Mah

indr

a

Winning bid range for solar tenders

"Original tariffs in Andhra Pradesh have an escalation of 3% per year for 10 years. For the purpose of this analysis, levelised tariff has been calculated based on an EIRR of 16%..

** Unlike most states that have a PPA tenure of 25 years, the tenure in Uttar Pradesh is 12 years.

5.00

4.00

6.00

7.00

8.00

9.00

10.00

11.00

12.00

18.00

RPS

SGP

Guj

arat

P1,

320

MW

NSM

P1

B1,

150

MW

Guj

arat

P2,

565

MW

NSM

P1

B2,

350

MW

Kar

nata

ka P

1, 6

0 M

W

Mad

hya

Prad

esh

P1, 2

00 M

W

Kar

nata

ka P

1, 1

30 M

W

Punj

ab P

1, 2

00 M

W

Utt

ar P

rade

sh P

1, 2

00 M

W**

Andh

ra P

rade

sh P

1

Mad

hya

Prad

esh

P2, 1

00 M

W

Chha

ttis

garh

P1,

100

MW

Kar

nata

ka P

2, 5

0 M

W

NSM

P2

B1

(DCR

), 37

5 M

W

NSM

P2

B1

(Ope

n), 3

75 M

W

M/k

Wh

2012

Highest winning bid

Lowest winning bid

Fixed tariff

17.91

12.5412.24

10.94

9.28 9.44

8.5

12.45

7.9

8.05

5.51

8.74

7.678.01

9.33

6.496.97

7.81 7.74 7.76

6.42

6.586.85

7.12

6.71

6.89

7.987.72

6.88

Punj

ab P

2, 2

50 M

W

Mad

hya

Prad

esh

P3, 3

00 M

W

Tela

ngan

a P2

, 200

0 M

W

Punj

ab P

3, 5

00 M

W

Utt

ar P

rade

sh P

3, 2

15 M

W**

8.6

7.02

5.64

5.05

5.89 5.98

5.095.17

6.856.45

6.005.54

Andh

ra P

rade

sh P

2, 5

00 M

W*

Kar

nata

ka P

3, 5

00 M

W

Tela

ngan

a P1

, 500

MW

Utt

arak

hand

P1,

30

MW

Utt

ar P

rade

sh P

2, 3

00 M

W**

9.34

8.9

6.666.446.47

7.947.49

13.00

2011 201520142013