Incoterms and the Incoterms®2010 logo are …€¦ · Incoterms and the Incoterms®2010 ... the...

50

© Mantissa Ltd 2017 All rights reserved. “Incoterms” and the Incoterms®2010 logo are trademarks of the International Chamber of Commerce (ICC). The text of the Incoterms 2010 rules is available as the ICC Publication 715E (English Edition.) This document has been supplied under your organisation’s licence agreement with Mantissa Ltd, for internal use only. You are not allowed to distribute this document to other parties outside the scope of this agreement. Warning: this document contains hidden identifying information for use in tracing unauthorised copying and distribution.

Transcript of Incoterms and the Incoterms®2010 logo are …€¦ · Incoterms and the Incoterms®2010 ... the...

© Mantissa Ltd 2017 All rights reserved.

“Incoterms” and the Incoterms®2010 logo are trademarks of the International

Chamber of Commerce (ICC). The text of the Incoterms 2010 rules is available as

the ICC Publication 715E (English Edition.)

This document has been supplied under your organisation’s licence agreement with

Mantissa Ltd, for internal use only. You are not allowed to distribute this document

to other parties outside the scope of this agreement.

Warning: this document contains hidden identifying information for use in tracing

unauthorised copying and distribution.

Contents

1 History and purpose of the rules ............................................................................. 1

2 Use of the Incoterms rules....................................................................................... 3

3 The logic of the rules................................................................................................ 5

3.1 “All transport modes” or “Sea & inland waterway only” ................................. 5

3.2 Who pays for main transport ............................................................................ 8

3.3 Where does risk transfer – before or after main transport? ........................... 9

4 How is an Incoterms rule chosen? ......................................................................... 10

5 The rules in detail................................................................................................... 11

5.1 Ex Works EXW ................................................................................................. 11

5.2 Free Carrier FCA .............................................................................................. 13

5.3 Carriage Paid To CPT ....................................................................................... 15

5.4 Carriage & Insurance Paid To CIP .................................................................... 17

5.5 The “arrival” rules DAT, DAP, DDP – general considerations ......................... 19

5.6 Delivered At Terminal DAT.............................................................................. 22

5.7 Delivered At Place DAP ................................................................................... 24

5.8 Delivered Duty Paid DDP ................................................................................. 26

5.9 Free Alongside Ship FAS .................................................................................. 28

5.10 Free On Board FOB ...................................................................................... 29

5.11 Cost & Freight CFR ....................................................................................... 31

5.12 Cost Insurance & Freight CIF ....................................................................... 33

5.13 Qualifications of an Incoterms rule. ............................................................ 35

6 The US perspective ................................................................................................ 36

6.1 Incoterms rules vs the Uniform Commercial Code ......................................... 36

6.2 Ex Works, EAR and routed transactions ......................................................... 37

Appendix A: Letters of credit and collections .............................................................. 38

I. What are letters of credit and collections? ........................................................... 38

II. How the Incoterms rules work with letters of credit ............................................ 40

III. Practical steps with the “F” rules ....................................................................... 41

IV. Letters of credit in practice - things to watch for .............................................. 42

V. Checklist for the transport document ................................................................... 45

Appendix B: Freight insurance and the rules ............................................................... 46

Incoterms 2010: A practical guide p. 1

1 History and purpose of the rules

The global economy and modern logistical networks give both importer and

exporters unprecedented opportunities for doing business with counterparties in

other parts of the world.

However when trading partners use different languages, legal systems and practices

for the movement of goods, it is vital to avoid misunderstandings and to achieve

precision as to how transactions are to be conducted.

The ICC created the first edition of the Incoterms rules back in 1936. It immediately

gained widespread acceptance in the international business community, and has

been revised from time to time to reflect changes in trading and transport practices.

The most recent revision is Incoterms 2010, which replaced the previous edition,

Incoterms 2000.

Incoterms 2010 consists of eleven packages of provision, designed to suit typical

requirements of international business. Each of these Incoterms rules is identified

by a name and by three-letter abbreviation – for example: “CIP Carriage and

Insurance Paid to”

By agreeing on the use of one of the eleven Incoterms rules and incorporating it into

their commercial agreement, buyer and seller can quickly and efficiently achieve

precision and clarity on a wide range of issues, including:

• Transport – who will arrange and pay for transport, and to what destination?

• Loading and unloading of goods

• Responsibility for export and import procedures and payment of applicable duty

and taxes

• Where during the journey responsibility for the goods passes from the seller to

the buyer – important in the event of loss or damage

The details of the rules are set out in the ICC publication no. 715 “Incoterms 2010:

ICC rules for the use of domestic and international trade terms.

This is available from the ICC Bookstore. http://store.iccwbo.org/

It is available in various languages, and in both conventional print and digital formats.

This publication is essential reading for those responsible for the development of an

Incoterms policy, and for negotiating agreements with trading partners and service

providers such as carriers and freight forwarders.

Incoterms 2010: A practical guide p. 2

NOTE: The selected Incoterms rule will be part of the commercial agreement between the buyer and seller. It will not be part of the agreement between either party and service providers such as carriers and freight forwarders. The party who arranges carriage should ensure that the terms and conditions of the carriage contract align with the selected Incoterms rule.

Incoterms 2010: A practical guide p. 3

2 Use of the Incoterms rules

The agreed Incoterms rule should be included in the commercial agreement in a

form such as this:

Note these three elements:

• The three-letter abbreviation – in this case CIP, which stands for Carriage and

Insurance Paid

• A place, Hong Kong Terminal 4. This is the destination to which the seller has

contracted to transport the goods. This should be defined as precisely as

possible, as many transport hubs are very large.

This place will have a defined meaning within each of the rules. For some rules –

but not all – it will be the point where risk transfers from seller to buyer.

(However as you will see later, for the CIP Incoterms rule and other the point of

risk transfer is earlier in the journey, before the main transport)

• The rubric “Incoterms 2010” indicates the revision of the rules that should apply.

This will normally be the latest revision. However trading partners with complex

agreements that they do not want to revise are free to specify earlier revisions

such as Incoterms 2000.

CIP Hong Kong Terminal 4 Incoterms 2010

Incoterms 2010: A practical guide p. 4

Note: There are some key aspects of the commercial agreement on which

the Incoterms rules are silent. For example:

• The rules deal with the transfer of responsibility for the goods, but they say nothing about transfer of ownership or title.

(This omission is intentional, because these concepts are subject to different treatments in various legal systems.)

• The rules say nothing about how and when the goods are to be

paid for, e.g. whether this is to be payment in advance, open account, use of letters of credit or collections

• The rules say nothing about remedies for breach of contract or how disputes are to be dealt with

So these matters need to be addressed in the commercial agreement

Incoterms 2010: A practical guide p. 5

3 The logic of the rules

The eleven rules may be classified according to these three criteria.

• Applicable transport methods.

Seven rules (EXW, FCA, CPT, CIP, DAT, DAP, DDP) can be used for any

transport mode (road, sea, air, rail etc.), or where the journey involves more

than one transport mode.

However four rules (FAS, FOB, CFR, CIF) can only be used for transport by sea

or inland waterway.

• Who arranges and pays for the main transport – buyer or seller?

• Where the seller arranges the main carriage, where does risk transfer from

seller to buyer – before or after the main carriage?

Let’s look at each of these aspects in turn

3.1 “All transport modes” or “Sea & inland waterway

only”

What is the significance of this distinction?

When the Incoterms rules were introduced in 1936, the standard mode of

international transport was by sea, and goods were typically loaded as individual

items (crates etc.) into the hold of the ship. To accomplish this, sellers delivered the

goods directly to the quay alongside the vessel.

The “sea and inland waterway” rules reflect this traditional mode of delivery and

loading, with the transfer of responsibility from seller taking place once the goods

have been loaded on board the vessel (or as expressed in the earlier Incoterms

revisions, when the goods have crossed the ship’s rail.)

With the advent of containerisation, all this changed. At container terminals, sellers

do not have direct access to the vessel. Instead, sellers deliver containers to

container yards or depots operated by the terminal, for later transfer to the vessel.

Once the container has been taken in charge by the terminal operator, the seller has

given up effective control of the goods.

Consider now the consequence of an accident at the terminal causing damage to the

container before it is loaded. Under the application of a “traditional” Incoterms rule

Incoterms 2010: A practical guide p. 6

such as CIF, the seller is still responsible for the goods, even though security and

effective control of the goods is now in the hands of the terminal operator.

A dramatic example of why these distinctions matter was the Japanese tsunami in

March 2011, which wrecked the Sendai container terminal, damaging many

hundreds of consignments awaiting loading. As a consequence, exporters using the

“traditional” Incoterms rules (FOB, CFR and CIF) found themselves facing losses that

could have been avoided.

The principle of risk transferring from seller to buyer at the point where the goods

are taken in charge by the carrier also applies to air transport and to multi-modal

operations.

In today’s integrated logistical systems, it is not uncommon for a consignment to go

through several transport stages before getting loaded onto a container vessel.

For example a “less than container load” consignment (LCL) may be collected by

truck by a “carrier” who does not own any ships (NVOCC or non-vessel operating

common carrier); then taken to a freight forwarder’s depot where it is consolidated

with other goods to create a full container load; then taken to a container freight

station before being loaded onto the ship.

Let us consider the implications of using an “all transport modes” rule such as

Carriage Paid To (CPT) versus a “sea and inland waterway only” rule such as Cost and

Freight (CFR).

In this scenario, if the Incoterms rule is CPT (destination), then the seller is “off risk”

from the moment the goods are first collected. However with the Incoterms rule

CFR, the seller remains at risk until the container is loaded onto the ship.

The practical implication is that the seven “All transport modes” rules are the rules of

choice for all movements of goods except those where the seller has direct access to

the ship for loading.

In these cases, one of the four “Sea or inland waterway only” rules is appropriate.

Such transactions will include:

• transport of bulk commodities such as oil, minerals, grain, etc., where loading

takes place from specialised installations

• heavy machinery or plant that is too large to be containerised

• loose “break-bulk” cargo where individual items are loaded onto the vessel.

Incoterms 2010: A practical guide p. 7

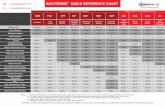

ALL TRANSPORT MODES SEA & INLAND WATERWAY ONLY

Ex Works EXW

Free Carrier FCA

Free On Board FOB Free Alongside Ship FAS

Carriage Paid To CPT Carriage and Insurance Paid To CIP

Cost and Freight CFR Cost Insurance and Freight CIF

Delivered At Place DAP Delivered At Terminal DAT Delivered Duty Paid

Use for: Containerised goods, multi-modal transport, air and road freight etc.

Use for: Bulk commodities, large machinery, break-bulk cargo loaded directly onto vessel

This recognition of the different requirements for containerised traffic is not new – it

is a feature of the 1990 revision of the rules, and all subsequent revisions.

Unfortunately historic practices within the industry can be resistant to change. So it

is still very common for importers and exporters to seek to use the “traditional” rules

FOB, CFR and CIF inappropriately, usually on the grounds that “we have always done

it this way” or “this is how our counterparty (or the bank or the customs authorities)

want it done”

Incoterms 2010: A practical guide p. 8

3.2 Who pays for main transport

As you can see from this table, for EXW and all the “F” rules, the buyer pays for the

main transport.

However for the “C” and “D” rules, the seller pays for main transport.

ALL TRANSPORT MODES SEA & INLAND WATERWAY WHO PAYS?

Ex Works EXW

Buyer pays for main transport

Free Carrier FCA

Free On Board FOB Free Alongside Ship FAS

Buyer pays for main transport

Carriage Paid To CPT Carriage and Insurance Paid To CIP

Cost and Freight CFR Cost Insurance and Freight CIF

Seller pays for main transport

Delivered At Place DAP Delivered At Terminal DAT Delivered Duty Paid

Delivered At Place DAP Delivered At Terminal DAT Delivered Duty Paid

Seller pays for main transport

As you will see in the next section, the major difference between the “C” and the “D”

rules is where in the journey the risk transfers from the seller to the buyer.

Incoterms 2010: A practical guide p. 9

3.3 Where does risk transfer – before or after main

transport?

Where the buyer arranges the main transport – Ex Works, Free Carrier, Free

Alongside Ship, Free on Board – then it is logical that the risk should transfer from

seller to buyer before the journey.

However when the seller arranges the main transport, there are two possibilities.

• For the “C” rules – Carriage Paid To, Carriage and Insurance Paid To, Cost and

Freight, Cost Insurance and Freight – risk transfers from seller to buyer BEFORE

the main transport.

• But for the “D” rules – Delivered At Terminal, Delivered At Place, Delivered Duty

Paid – the seller retains responsibility for the goods throughout the main

transport, and until they have been delivered to the specified place

ALL TRANSPORT MODES SEA & INLAND WATERWAY

Ex Works EXW

Buyer pays for main transport

Free Carrier FCA

Free On Board FOB Free Alongside Ship FAS

Buyer pays for main transport

Carriage Paid To CPT Carriage and Insurance Paid To CIP

Cost and Freight CFR Cost Insurance and Freight CIF

Seller pays for main transport, but seller is “off risk” during transport

Delivered At Place DAP Delivered At Terminal DAT Delivered Duty Paid

Seller pays for main transport, remains “on risk” during transport

This special feature of the “C” rules has some important implications, which will be

explained in the detailed coverage later on.

One of the implications is that when a C rule is cited, e.g. “CIP Long Beach California

Terminal 3 Incoterms 2010”, it is not apparent from this where the buyer will assume

risk for the cargo – the destination of the goods is stated, but not the place where

the goods are taken in charge before the journey.

Incoterms 2010: A practical guide p. 10

4 How is an Incoterms rule chosen?

Before moving on to the detailed provisions of the eleven rules, let’s look at some of

the major factors that buyers and sellers may consider when deciding on a suitable

Incoterms rule.

• Skills and resources of the parties – a buyer or seller with limited experience of

international trade may be happy to limit their obligations and leave as much of

the work as possible to the other party.

• Relative volumes of international business. A large company that does a lot of

importing or exporting will have existing relationships with carriers and other

service providers, and will be able to obtain better rates than a smaller one –

freight rates are usually highly dependent on volumes that the customer can

commit to.

• Policy and/or appetite with respect to controlling as much of the transaction as

possible. An exporter may regard the timely and efficient delivery of the goods as

an important aspect of overall product quality, and so will wish to have maximum

control over the transport arrangements

• Risk issues around local transport infrastructure and/or bureaucracy. For

example, an exporter sending goods to a country with unreliable transport

infrastructure and inefficient customs procedures may wish to avoid

responsibility for delivering the goods to the buyers’ premises and for clearing the

goods for import.

Incoterms 2010: A practical guide p. 11

5 The rules in detail

5.1 Ex Works EXW

This rule represents the minimum cost and responsibility for the seller, and the

maximum cost and responsibility for the buyer. The seller is obliged to do little

more than make the goods available at their premises, packed and ready for

collection by the buyer or the buyer’s appointed carrier.

Risk transfers from seller to buyer as soon as the goods have been made available,

i.e. before they have been loaded onto the vehicle – even though the seller may be

better placed to undertake loading.

The buyer is responsible for any export clearance procedures; for loading the goods

and transporting them at their own cost and risk; for import procedures and

payment of any duty or local taxes.

Inexperienced exporters are attracted by the apparent simplicity of this rule.

However there are very significant pitfalls for both the buyer and the seller.

The most important of these is that of export clearance. This is the only rule in

which the buyer, and not the seller, is responsible for export clearance. This will

usually be done by the buyer-appointed freight forwarder or carrier using

information that the seller will need to supply.

However in many countries exporters need to engage with the local authorities for

many reasons – for example, to demonstrate compliance with embargos or

restrictions on dealing with questionable persons, business entities or countries. US

exporters should take particular note of the concept of US Principal Party in Interest

(USPPI), which places obligations on the seller that cannot be avoided by use of the

Ex Works rule.

In summary, Ex Works may be practical for domestic sales or for sales within an

economic area such as the EU.

However in most other cases, the exporter should consider FCA - Free Carrier

(exporter’s premises)

Incoterms 2010: A practical guide p. 12

The provisions of Free Carrier are very similar to those of Ex Works, except that the

exporter is obliged to undertake export procedures.

One important use of Ex Works is as a well-understood basis for quotations – it

represents the cost of the goods themselves - packed, but without any of the

“extras” – transport, loading and unloading, duties, insurance and so on. Buyers

who are familiar with these others costs, or who have their own logistical contracts,

can assess the merits of the offer and make their own decisions.

Things to watch for.

Packing.

This rule obliges the seller to package the goods, at their own expense, in a manner

appropriate for their transport. However a danger arises if an agreement is reached

before the mode of transport has been decided or communicated to the seller –

different transport modes have their own packaging requirements. So it is

important for the seller to establish the proposed transport mode, include this in the

commercial agreement and then pack the goods accordingly.

If the goods need to be loaded into a container for transport, then this will not be

covered by the seller’s obligations under the Ex Works rule – responsibility for this

will need to addressed in the commercial agreement

Loading of the goods

The Ex Works rule does not oblige the seller to load the goods onto the buyer’s

vehicle. The seller will often be better placed to do this, and most sellers are willing

to load the goods as a matter of general convenience. However unless agreed

otherwise, loading of the goods will be at the buyer’s risk.

Diversion of goods.

An exporter may have purely commercial concerns about the actual destination of

the goods.

Consider a manufacturer who has a long-standing, exclusive arrangement with a

distributor for all domestic sales.

They receive an order for export to a distant overseas country. They proceed to deal

with this buyer on Ex Works terms, only to find that the goods are never exported,

but find their way onto the domestic market!

Incoterms 2010: A practical guide p. 13

5.2 Free Carrier FCA

This very flexible rule can be used for all situations where the buyer assumes

responsibility for the main carriage to the buyer’s destination.

The seller delivers the goods, cleared for export, to the named place, which can be a

terminal, a transport hub, a freight forwarder’s warehouse etc.

Delivery takes place when the goods are made available to the carrier at the named

place, still loaded on the arriving vehicle.

There is an important usage of this rule – Free Carrier (sellers’ premises.) In this

case, the goods are collected from the seller’s factory or depot. Delivery is

completed when the seller has loaded the goods onto the carrier’s vehicle.

(NB this is an important difference from Ex Works, where the buyer is responsible for

loading onto the vehicle.)

Free Carrier (sellers premises) is very often a more appropriate choice of rule than Ex

Works – the latter can pose all sorts of problems around the outsourcing of export

clearance. (See Ex Works above for more on this.)

Free Carrier can be used for all transport modes and for multi-modal operations. It

is also suitable for groupage and consolidation situations.

This rule should not be used where

• the goods are transported by sea or inland waterway only

and

• the seller has direct access to the vessel or to the quay for purposes of loading

Examples where Free Carrier should not be used include transport of bulk

commodities such as oil, mineral ore, grain etc. – usually handled by special-purpose

equipment at the terminal; large machinery that cannot be containerised; other

“break-bulk” cargo where items require individual loading.

Incoterms 2010: A practical guide p. 14

In such cases, the appropriate rules are “Free On Board FOB” – delivery is completed

when goods have been loaded on board the vessel – and “Free Alongside Ship FAS” –

delivery is completed when goods are place alongside the ship at the specified place.

Things to watch for

Where does the risk transfer?

If there is more than one carrier, then risk transfers to the buyer when the goods

have been delivered to the first carrier, unless otherwise specified in the commercial

agreement. This may be an issue for the buyer if the first carrier is a small company

with limited financial or other resources for dealing with problems.

Packing

This rule obliges the seller to package the goods, at their own expense, in a manner

appropriate for their transport. However a danger arises if an agreement is reached

before the mode of transport has been decided or communicated to the seller –

different transport modes have their own packaging requirements. So it is

important for the seller to establish the proposed transport mode, include this in the

commercial agreement and then package the goods accordingly.

Containers

The Incoterms 2010 rules are clear that loading goods into containers is a separate

issue from packaging of the goods. So if the buyer or buyer-appointed agent is

expecting to take delivery of a loaded container, this should be spelled out in the

commercial agreement.

Incoterms 2010: A practical guide p. 15

5.3 Carriage Paid To CPT

This is one of four rules where the seller is responsible for arranging and paying for

transport to the named place, but where delivery and transfer of risk take place at an

earlier point before the main carriage.

For example, if the Incoterms rule for a consignment is CPT Pier T Long Beach,

California, an exporter in the UK may deliver a container to the carrier at Felixstowe

(UK), and contract with the carrier for transport to the named place (Long Beach).

The key point is that delivery and transfer of risk takes place before the main

carriage, when the container has been taken in charge by the carrier, and not at the

destination place named in the Incoterms rule.

So when this rule is used, the details of the journey, including the delivery point,

must be included in the commercial agreement – note that the Incoterms reference

will only mention the destination point.

This rule is appropriate for all modes of transport, and for multi-modal operations.

It is one of the rules of choice for containerised movements, which constitute the

vast majority of sea cargo operations.

This rule does not oblige the seller to take out cargo insurance for the consignment –

see “Carriage & Insurance Paid to CIP” if the seller is required to provide this. So

buyers may wish to take out their own cargo insurance, covering the point of delivery

through to the final destination.

Things to watch for

Terminal Handling Charges (THC) at the destination

Containerised operations typically involve a number of stages between the points

where sellers deliver (and buyers collect) the containers and the container vessels.

Terminal operators typically make charges for these movements, but there is no

standard practice for how carriers treat these charges.

Incoterms 2010: A practical guide p. 16

In some instances the Terminal Handling Charges at the destination will be included

in the freight rate; but in other cases these charges will be for the account of the

buyer.

So to avoid nasty surprises when collecting goods, buyers should raise this question

with their exporters and should agree on the treatment of applicable THCs at the

destination.

Letters of credit

This rule, along with the other “C” rules (CIP, CFR, CIF) work well with letters of credit

and collections, because the seller controls the main transport, and so can be sure of

getting a transport document that evidences delivery.

NB the letter of credit may call for a transport document stating that the goods have

been “taken in charge” by the carrier OR “loaded on board” a vessel – the seller

should ensure that the carrier can supply the document with the required wording.

The other rules (EXW, FAS, FOB, FCA, DAT, DAP, DDP) all pose potential problems –

see the “Letters of credit and collections” section for more details.

Incoterms 2010: A practical guide p. 17

5.4 Carriage & Insurance Paid To CIP

This is one of four rules where the seller is responsible for arranging and paying for

transport to the named place, but where delivery and transfer of risk take place at an

earlier point before the main carriage.

For example, if the Incoterms rule for a consignment is CIP Pier T Long Beach,

California, an exporter in the UK may deliver a container to the carrier at Felixstowe

(UK), and contract with the carrier for transport to the named place (Long Beach).

The key point is that delivery and transfer of risk takes place before the main

carriage, when the container has been taken in charge by the carrier, and not at the

destination place named in the Incoterms rule.

So when this rule is used, the details of the journey, including the delivery point,

must be included in the commercial agreement – note that the Incoterms reference

will only mention the destination point.

This rule is appropriate for all modes of transport, and for multi-modal operations.

It is one of the rules of choice for containerised movements, which constitute the

vast majority of sea cargo operations.

The other major obligation of the seller is to obtain and pay for cargo insurance for

the journey to the named destination.

The insurance cover required by this rule is Institute Cargo Clauses C or equivalent,

which excludes various risks that the buyer may regard as necessary; so the exact

cover requirements should be discussed and included in the commercial agreement.

Things to watch for

Terminal Handling Charges (THC)

Containerised operations typically involve a number of stages between the points

where sellers deliver (and buyers collect) the containers and the container vessels.

Terminal operators typically make charges for these movements, but there is no

standard practice for how carriers treat these charges.

Incoterms 2010: A practical guide p. 18

In some instances the Terminal Handling Charges at the destination will be included

in the freight rate; but in other cases these charges will be for the account of the

buyer.

So to avoid nasty surprises when collecting goods, buyers should raise this question

with their exporters and should agree on the treatment of applicable THCs

Insurance

As noted earlier, the minimum level of cover mandated by this rule is Institute Cargo

Clauses C, which excludes war, strikes and some other risks that a buyer may regards

as necessary.

So the level of cover needs to be specified in the commercial agreement.

As the seller will be “off risk” for the main transport and beyond, the insurance

documents need to be made out in a form that will allow the buyer to claim under

the policy if necessary. It is also good practice for the buyer to establish a channel of

communication with the carrier beforehand, so that claims can be lodged promptly.

Letters of credit

This rule, along with the other “C” rules (CPT, CFR, CIF) work well with letters of credit

and collections, because the seller controls the main transport, and so can be sure of

getting a transport document that evidences delivery.

NB the letter of credit may call for a transport document stating that the goods have

been “taken in charge” by the carrier OR “loaded on board” a vessel – the seller

should ensure that the carrier can supply the document with the required wording.

The other rules (EXW, FAS, FOB, FCA, DAT, DAP, DDP) all pose potential problems –

see the “Letters of credit and collections” section for more details.

Incoterms 2010: A practical guide p. 19

5.5 The “arrival” rules DAT, DAP, DDP – general

considerations

For these three rules, the seller’s obligations now extend to delivering the goods to

the named place (usually) in the buyer’s country, and risk remains with the seller

until delivery has been completed.

This is an important difference from the “C” rules (CFR, CIF, CPT, CIP), where the

seller delivers the goods - and risk transfers to the buyer - before the main carriage.

• Delivered At Terminal. Delivery is completed when the goods have been

unloaded from the arriving vehicle at the defined place. Import clearance and

payment of all duties and taxes is the responsibility of the buyer

• Delivered At Place. Delivery is completed when the goods are available on the

arriving conveyance, ready for unloading by the buyer. Import clearance

payment of all duties and taxes is also the responsibility of the buyer.

• Delivered Duty Paid. Delivery is completed when the goods have been unloaded

from the arriving vehicle at the defined place. The seller is responsible for import

clearance and payment of all duty and taxes

The first two of these (Delivered At Place, Delivered At Terminal) often present an

issue of coordination of the actions of the seller-appointed carrier and the buyer.

In many instances, import clearance (responsibility of the buyer) must take place

before the seller has completed delivery of the goods to the named place.

So for the goods to proceed smoothly to their delivery point, it is necessary that

import clearance is done in a timely manner. The buyer – or buyer’s freight

forwarder - is responsible for this, but they are dependent on receiving accurate

information and complete documentation from the seller or the seller’s freight

forwarder.

Delays in import clearance can arise in a number of ways. The seller (or a party

acting for the seller) may provide incomplete information; information or documents

may arrive late; there may be inefficiency or lack of cooperation the part of the buyer

or the customs authorities. Whatever the cause, the effect will be late delivery

and/or penalties by way of storage charges or demurrage – and often a dispute

about who should pay these!

So when these rules are used, it is important that buyer and seller have a shared

understanding of the liaison that will be necessary. Ideally the commercial

agreement should also deal with responsibility for charges that may arise in the

event of delays in import clearance.

Incoterms 2010: A practical guide p. 20

(Note that these problems of coordination between delivery and clearance do not

arise if the goods can be delivered “uncleared” – for example, to a depot in a Free

Trade Zone.)

Here are some examples of how these “arrival” rules may work in practice.

1. China to UK, air transport

A UK manufacturer buys components from a supplier in China on a DAP basis.

The Chinese supplier employs a UK-based freight forwarder to arrange delivery to

the UK factory.

Upon arrival of the goods, the freight forwarder sends copies of the air waybill

and invoice to the buyer, who in return provides the freight forwarder with VAT

numbers and other information needed for import clearance. The freight

forwarder can now clear the goods for import on the buyer’s behalf. There is an

agreement with UK Customs that duty and handling fees for clearance are for the

buyer’s account.

It has been agreed that in the event of delays caused by failure of the buyer to

supply the required information, storage charges etc. will be the responsibility of

the buyer.

2. Turkey to Azerbaijan, road transport

Machine tools are transported from Turkey to Azerbaijan by road on a DAP basis.

The route involves travel through Georgia, but the transport document used by

the trucks allows entry to and exit from Georgia on an “in transit” basis.

On arrival at the Azerbaijan border, the buyer must clear the goods and pay the

duty without the opportunity to inspect the goods.

This arrangement poses a degree of risk for the seller – if the buyer fails to clear

the goods at the border promptly, there will be significant costs by way of drivers’

wages etc. In this case the seller’s solution is to require a deposit from the

buyer, which can be used to defray these costs if necessary.

Incoterms 2010: A practical guide p. 21

Delivered Duty Paid

In Delivered Duty Paid, the seller is responsible for import clearance and payment of

duties and tax, so liaison around clearance is less of an issue. However there are

other serious concerns for both parties – these will be explained below in section 5.8

on DDP.

Sellers should also be cautious in using any of the “D” rules for consignments to

“difficult” destinations, where their obligations to compete delivery may be

frustrated by poor transport infrastructure, bureaucratic delays and so on.

Conversely, the use of DAT and DAP should be more straightforward in these

situations:

• where delivery is to another country within a customs union such as the EU

• where the destination is within a Free Trade Zone - duty is not levied on arrival

Incoterms 2010: A practical guide p. 22

5.6 Delivered At Terminal DAT

This rule can be used for any transport mode, or where there is more than one

transport mode.

The seller is responsible for arranging carriage and for delivering the goods, unloaded

from the arriving conveyance, at the named place.

Risk transfers from seller to buyer when the goods have been unloaded.

‘Terminal’ can be any place – a quay, container yard, warehouse or transport hub. It

can also be the buyer’s premises, which is useful when “deliver-to-door” integrated

carriers are used.

The buyer is responsible for import clearance and any applicable local taxes or

import duties.

A useful rule, well suited to container operations where the seller bears

responsibility for the main carriage.

Things to watch for

Identification of the delivery point

Modern transport hubs can be very large, so it is essential that the delivery point be

specified in detail, e.g. an exact address, terminal number etc.

Liaison around import clearance

As noted in a previous section, there is a risk that failure of communication between

the seller (or sellers’ representatives) and the buyer can lead to delays in import

clearance, which will have consequences by way of demurrage, detention fees,

storage charges etc.

Incoterms 2010: A practical guide p. 23

Terminal Handling Charges THC

Carriers have different policies about whether freight charges include Terminal

Handling Charges at the destination. So if the delivery point is a port, these costs

should be identified, and agreement reached as to whether they are for the account

of the buyer or the seller.

Delivery to buyer’s premises

Where DAT (buyers’ premises) is used, the seller is reliant on the buyer’s prompt

cooperation in accepting the consignment and allowing unloading of the goods.

Where there are doubts about this, then DAP is preferable – delivery is complete

when the goods arrive still loaded on the vehicle.

Incoterms 2010: A practical guide p. 24

5.7 Delivered At Place DAP

This rule can be used for any transport mode, or where there is more than one

transport mode.

The seller is responsible for arranging carriage and for delivering the goods, ready for

unloading from the arriving conveyance, at the named place. (An important

difference from Delivered At Terminal DAT, where the seller is responsible for

unloading.)

So it is not suitable for scenarios where a rapid turn-around of a container ship or

aircraft is important.

Risk transfers from seller to buyer when the goods are available for unloading; so

unloading is at the buyer’s risk.

The buyer is responsible for import clearance and any applicable local taxes or

import duties.

Uses for this rule include where there are no storage facilities at the destination,

and/or where the buyer’s vehicle is needed for unloading.

The specified place can also be the buyer’s premises.

Things to watch for

Identification of delivery point

Modern transport hubs can be very large, so it is essential that the delivery point be

specified in detail, e.g. an exact address, terminal number etc.

Liaison around import clearance

As noted in an earlier section, there is a risk that failure of communication between

the seller (or sellers’ representatives) and the buyer can lead to delays in import

clearance, which will have consequences by way of demurrage, detention fees,

storage charges etc.

Incoterms 2010: A practical guide p. 25

Terminal Handling Charges THC

As delivery takes place upon arrival with the goods ready to be unloaded, it follows

that if the destination is the port of arrival, then Terminal Handling charges at the

destination should be for the buyer’s account.

Delivery to buyer’s premises

This rule works well for the seller. As delivery is completed upon arrival of the

vehicle, costs arising from delays in acceptance of the goods and unloading will be

the buyer’s responsibility

Incoterms 2010: A practical guide p. 26

5.8 Delivered Duty Paid DDP

This rule represents the extreme of responsibility for the seller, who must deliver the

goods to the specified place, having completed import clearance and paid any

applicable duties and taxes.

This is the only Incoterms rule that obliges the seller to undertake import clearance.

The rule can be used for any transport mode, or when more than one transport

mode is used

Delivery is complete when the goods arrive at named place, and are available for

unloading from the arriving vehicle.

This rule is sometimes demanded by buyers, but it can be highly problematical for

sellers. It also poses some risks for buyers – see below

Things to watch for

Can the seller undertake import clearance?

In some countries, import clearance can be complex and bureaucratic. A seller who

is not familiar with the process will encounter many frustrations and delays, so it is

best left to the buyer with local knowledge.

In many countries, import clearance can only be undertaken by entities with a

business presence in the country. By the same token, local taxes such as VAT may

only be payable by businesses registered with the local authorities.

(If necessary, the rule can be modified thus: Delivered Duty Paid (VAT unpaid)

Incoterms 2010: A practical guide p. 27

Risks for the importer

Importers may seek to isolate themselves from the import process by the use of this

rule. However there are now cases such as the following.

A consignment of goods imported from Asia into Australia was found to have

been misrepresented by the importer by use of an incorrect goods classification,

with a consequent underpayment of duty.

The authorities took the view that recovery of money from the supplier was

unlikely to be successful, so a judgement was obtained in which the importer

was held liable.

Incoterms 2010: A practical guide p. 28

5.9 Free Alongside Ship FAS

Use of this rule is restricted to goods transported by sea or inland waterway.

In practice it should be used for situations where the seller has direct access to the

vessel for loading, e.g. bulk cargos (oil, coal, grain etc.) or non-containerised goods.

For containerised goods, “Free Carrier FCA” should be used.

Seller delivers goods, cleared for export, alongside the vessel at a named port, at

which point risk transfers to the buyer.

The buyer is responsible for loading the goods and all costs thereafter.

The commonest uses of this rule are

• for ship chartering, where the buyer arranges for loading

• for large loads of machinery etc. which cannot be containerised

• at smaller ports where ships can load goods without the need for quayside

facilities

Things to watch for

The location of the delivery point must be described in as much detail as possible.

Berths and quayside storage are both scarce resources, so it is essential that the

seller and the buyer/carrier work closely together to coordinate the arrival of the

ship and the goods.

Goods security and letters of credit

One common use of this rule is for commodities transactions, which are often of high

value. As the goods are being delivered before loading onto the vessel, there is no

transport document that can be used by the seller to maintain control over the

goods.

This is turn limits the use of this rule with letters of credit and other secure-terms

payment methods. See Appendix A for more on this.

Incoterms 2010: A practical guide p. 29

5.10 Free On Board FOB

Use of this rule is restricted to goods transported by sea or inland waterway.

In practice it should be used for situations where the seller has direct access to the

vessel for loading, e.g. bulk cargos (oil, coal, grain etc.) or non-containerised goods.

For containerised goods, “Free Carrier FCA” should be used.

Seller delivers goods, cleared for export, loaded on board the vessel at the named

port.

Once the goods have been loaded on board, risk transfers to the buyer, who bears all

costs thereafter.

Things to watch for

Cargo operations after loading

For some types of cargo, other things will need to be done before the vessel can

depart.

• Stowing and lashing – locating the cargo appropriately within the vessel

(taking into account balance of the ship, other items loaded etc.) and securing

cargo to prevent its movement in rough seas.

• Dunnaging – stabilisation & protection of cargo by using packing material, air

bags etc.

The “Free on Board” rule makes no reference to these operations – the seller’s

responsibilities are fulfilled when the goods are “loaded on board”.

So if these are necessary for a specific consignment and are to be performed by the

seller, the rule can be qualified thus:

FOB stowed and lashed ….

Alternatively, assignation of these costs can be included in the commercial

agreement.

Incoterms 2010: A practical guide p. 30

Goods security and letters of credits

One common use of this rule is for commodities transactions, which are often of high

value.

As with the other Incoterms “F” rules, Free on Board is not ideal for use in letters of

credit transactions, because the buyer arranges the main transport and has the

business relationship with the carrier. An unscrupulous buyer can frustrate the

transaction by cancelling the transport arrangements. See Appendix A for a

detailed discussion and possible work-arounds.

Incoterms 2010: A practical guide p. 31

5.11 Cost & Freight CFR

Use of this rule is restricted to goods transported by sea or inland waterway.

In practice it should be used for situations where the seller has direct access to the

vessel for loading, e.g. bulk cargos (oil, coal, grain etc.) or non-containerised goods.

For containerised goods, consider ‘Carriage Paid To CPT’ instead.

Seller arranges and pays for transport to named port. Seller delivers goods, cleared

for export, loaded on board the vessel.

However risk transfers from seller to buyer once the goods have been loaded on

board, i.e. before the main carriage takes place. This is the point of delivery, as

defined by this rule.

NB seller is not responsible for insuring the goods for the main carriage. If they

buyer wants the seller to arrange insurance for the journey, “Cost Insurance and

Freight CIF” should be used.

As with the other “C” rules, this is a good choice where letters of credit are being

used. The seller contracts with the carrier for the transport, and so can be sure of

obtaining the transport document that will be needed to trigger payment by the

bank

Things to watch for

Specified destination

This should be as precise as possible, and should match the transport contract. Costs

arising beyond this point will be for the account of the buyer.

Transport document

This will usually be a bill of lading or a sea waybill, and must be provided by the

seller. It must indicate that the goods have been “loaded on board” and that freight

has been paid by the seller.

Incoterms 2010: A practical guide p. 32

Insurance

As the seller is not providing this, the buyer will normally arrange this for the

journey, as a matter of commercial prudence.

Incoterms 2010: A practical guide p. 33

5.12 Cost Insurance & Freight CIF

Use of this rule is restricted to goods transported by sea or inland waterway.

In practice it should be used for situations where the seller has direct access to the

vessel for loading, e.g. bulk cargos (oil, coal, grain etc.) or non-containerised goods.

For containerised goods, consider ‘Carriage and Insurance Paid CIP’ instead.

Seller arranges and pays for transport to named port. Seller delivers goods, cleared

for export, loaded on board the vessel.

However risk transfers from seller to buyer once the goods have been loaded on

board, i.e. before the main carriage takes place.

Seller also arranges and pays for insurance for the goods for carriage to the named

port.

However as with “Carriage and Insurance Paid To”, the rule only require a minimum

level of cover, which may be commercially unrealistic. Therefore the level of cover

will need to be addressed elsewhere in the commercial agreement.

As with the other “C” rules, this is a good choice where letters of credit are being

used. The seller contracts with the carrier for the transport, and so can be sure of

obtaining the transport document that will be needed to trigger payment by the

bank

Things to watch for

Specified destination

This should be as precise as possible, and should match the transport contract. Costs

arising beyond this point will be for the account of the buyer.

Incoterms 2010: A practical guide p. 34

Transport document

This will usually be a bill of lading or a sea waybill, and must be provided by the

seller. It must indicate that the goods have been “loaded on board” and that freight

has been paid by the seller.

Insurance

It should be borne in mind that although the seller arranges cargo insurance, the

seller is “off risk” once the goods have been loaded; so responsibility for making the

claim rests with the buyer. The insurance document must be made out accordingly,

e.g. endorsed in favour of the buyer.

Incoterms 2010: A practical guide p. 35

5.13 Qualifications of an Incoterms rule.

It is possible to add further wording to an Incoterms rule, in order to achieve a more

precise definition of obligations.

For example, with some types of cargo there are cost arising from operations such as

stowing the cargo on the vessel after loading. The Incoterms rule “FOB stowed” will

make it clear that the seller is responsible for these costs as well as those for loading.

Operations that may be required for the securing of cargo may include lashing and

dunnage – packing around the load to prevent movement in heavy seas.

Other examples:

• DDP, VAT unpaid – seller is responsible for paying import duty but not VAT

(which can often only be paid by a business entity in the country of arrival.)

• Ex Works, loaded – seller is responsible for loading onto the vehicle

Note:

Qualifications of the rules should be used with

caution, as they may be open to different

interpretations should problems arise.

For example with “Ex Works loaded”, there have

been disputes as to whether loading is at the

buyer’s or the seller’s risk!

Incoterms 2010: A practical guide p. 36

6 The US perspective

The Incoterms 2010 revision is of particular interest to companies in the United

States (and their trading partners) for the following reasons.

6.1 Incoterms rules vs the Uniform Commercial Code

Trade practitioners in the U.S. will be aware that the terms FOB, CIF and so on are

defined within the United States federal Uniform Commercial Code (UCC).

First published in 1952, UCC covers many aspects of commercial contracts. It

contains “shipment and delivery” provisions that have similar aims to those of the

Incoterms rules.

Some UCC expressions have the same three-letter abbreviations as those within the

Incoterms system; but their definitions are totally different. Notoriously, “FOB” can

have several different meanings within UCC, most of which do not correspond with

the ICC Incoterms FOB definition.

The situation is confused further by variations between different US states. In 2004,

there was a major revision of the UCC, which abolished many of these terms.

However for reasons unrelated to its “shipment and delivery” provisions, many

states have failed to adopt the 2004 revision; so in these states, the former UCC

revision remains law.

Companies in the US are therefore faced with the prospect of mastering two versions

of the UCC for use with domestic transactions, plus ICC Incoterms rules for use with

cross-border transactions.

The logical solution to this confusion is to standardise on the use of ICC Incoterms

rules for all transactions, whether domestic or international.

The Incoterms 2010 revision has been drafted to make the interpretation of the rules

very straightforward for domestic trades.

For example, all obligations in respect of import or export procedures need only be

considered ‘where applicable.’

Incoterms 2010: A practical guide p. 37

6.2 Ex Works, EAR and routed transactions

The Ex Works rule places the burden of export clearance on the buyer, not the seller.

However US exporters who are attracted by this opportunity to avoid work should be

aware of US Export Administration Regulations.

These make it clear that any infringement of regulations or defects in the

information filed remain the responsibility of the exporter as US Principal Party of

Interest (USPPI.)

Furthermore, transactions in which transport arrangements are made by the

overseas buyer and not the seller will be defined as “routed” transactions, and will

be subject to extra scrutiny.

The use of Ex Works therefore creates significant compliance risk for the exporter.

Ideally the seller should control the transportation by using a rule such as CIP or CPT.

But if this is not possible, then it is better to undertake export clearance oneself and

use Free Carrier (seller’s premises.)

Incoterms 2010: A practical guide p. 38

Appendix A: Letters of credit and collections

I. What are letters of credit and collections?

These are sometimes referred to as “secure terms” settlement methods. Their

common feature is that buyer and seller operate in a situation of limited trust.

The seller may be concerned that the buyer will be unable to pay for the goods –

either due to their own financial difficulties or because of country-related issues such

as political instability and shortage of foreign exchange. The buyer may be

concerned that the supplier may fail to deliver the goods as per the agreement.

• Documentary letter of credit.

A payment undertaken given by a bank to a seller on behalf of a buyer, given

before the goods are despatched. The bank undertakes to pay the seller upon

presentation of documents representing the goods to be supplied. These

documents will include a transport document as evidence of delivery of goods to

the carrier (or loading of goods on board the vessel.)

• Documentary collection

.

Documents representing the goods are presented to the buyer through the

banking system. If they are in order, the buyer pays the seller (or if credit terms

have been extended, accepts a term draft, committing itself to pay at a future

date.)

Less secure that a letter of credit, because there is no prior payment undertaking

from a bank. Nonetheless with some transport modes this can allow the seller to

retain control of the goods until the buyer has paid or agreed to pay.

Typical uses are where the seller can readily find other buyers for the goods if

necessary; or where the buyer is financially secure, but where an incentive for

prompt payment is needed.

Incoterms 2010: A practical guide p. 39

The security offered by a letter of credit

The documentary letter of credit works for the seller, because a bank backs the

transaction with its reputation and financial resources. Provided that the seller

presents documents that comply with its terms and conditions, the bank will pay the

amount due, even if:

• the buyer is in financial difficulties and cannot pay

• for a confirmed letter of credit, there are economic or political factors that

interfere with payment

The buyer is protected because the bank will only pay if the documents meet all the

terms and conditions that the buyer has set out in the letter of credit. So the

transport document will need to show despatch of the goods no later than the date

that the buyer has specified in the credit, specified places of despatch and delivery

and so on.

Buyers who have concerns about the quality or specification of the goods can require

presentation of a certificate of inspection issued by an independent company.

NB letters of credit are sometimes required for purely administrative reasons, e.g. as

part of a country’s regime of import control or foreign exchange management. In

such cases the following cautions on the choice of Incoterms rule may not apply.

Incoterms 2010: A practical guide p. 40

II. How the Incoterms rules work with letters of credit

The “C” rules – CPT, CIP, CFR, CIF – work well with letters of credit; however all the

other rules may present problems for either the buyer or the seller.

For the “C” rules, the seller is responsible for arranging the main transport, and so

has the business relationship with the carrier. Let’s look at the example of a

container being sent by sea using CIP.

The sequence of events is as follows:

1. The seller delivers the container to the carrier at the container terminal. The

seller is given a bill of lading, which is marked “taken in charge” by the carrier.

2. The seller presents this to the bank, along with the other documents required by

the letter of credit. Provided the documents all comply with the terms of the

letter of credit, the bank pays the seller.

3. All documents, including the bill of lading, are given to the buyer, so the goods

can be claimed at their destination.

LETTER OF CREDIT UTILISATION PROCESS

Now consider the same scenario with the corresponding “F” rule – for a container,

this will be Free Carrier FCA.

With this rule, it is the buyer who is responsible for the main transport, and who has

the business relationship with the carrier. An unscrupulous buyer may be able to

frustrate the contract by cancelling the shipping arrangements or interfering with

delivery of the bill of lading to the seller. Without the bill of lading, the seller cannot

make a valid presentation and so cannot get paid.

Incoterms 2010: A practical guide p. 41

With Ex Works EXW, the position is even more problematical. Under this rule,

“delivery” is a matter arranged between seller and buyer. There is no carrier who

can serve as neutral intermediary, and therefore no document that can serve as

evidence of delivery for the purposes of the letter of credit.

Now let us consider a scenario using a “D” rule, Delivered at Place. Suppose that the

final destination is the buyer’s premises, so the seller must arrange sea transport,

followed by transport by truck to the specified location. Under this rule, “delivery”

is defined as arrival at the final destination.

What document can the letter of credit call for as evidence of completion of the

seller’s obligations?

For sea transport, the usual document called for by a letter of credit is a bill of lading

showing the goods taken in charge (or in some cases, loaded on board the ship)

before the main transport.

This will suit the seller, who can present the bill of lading and get paid before the

goods arrive at their destination. But it is not ideal for the buyer, who must now

trust the seller to complete their obligation to deliver to the buyer’s premises, as set

out in the DAP rule.

(In principle the letter of credit could call for a delivery note issued by the buyer

upon arrival of the goods. But there is nothing to prevent an unscrupulous buyer

from refusing to take delivery and/or provide this document.)

III. Practical steps with the “F” rules

If it is necessary to use one of the “F” rules in conjunction with a letter of credit, and

if the seller is concerned about the reliability of the buyer, then there is a potential

work-around, which is based upon specifying within the letter of credit an alternative

set of documents, that can be substituted by the seller in the event that a bill of

lading cannot be provided.

The typical set of documents specified for this contingency will be along the lines of:

• Forwarders’ certificate of receipt as evidence that the goods called for by the

letter of credit have been taken in charge

• Copy of beneficiary’s notice of cargo readiness sent to applicant

• Beneficiary’s certificate attesting that the agreed transport arrangements are not

available (e.g. non-arrival of vessel)

Incoterms 2010: A practical guide p. 42

IV. Letters of credit in practice - things to watch for

The letter of credit process starts with the buyer and seller agreeing on the details of

transaction, which will include the product and its price, the transport method and

shipment date etc., the Incoterms rule that will apply. The latter will determine

what documents the letter of credit will call for. For example, if this is Carriage and

Insurance Paid, there will need to be a transport document and an insurance

document.

The details of the transaction will be incorporated into the buyer’s application for the

letter of credit, which will serve as the basis for the letter of credit instrument that

the seller will be advised of through the banking system.

The experience of banks and trading companies is that producing a set of documents

that comply with all the terms and conditions of a letter of credit is not

straightforward. Industry statistics show at as many of 50% of presentations by

exporters to their banks are rejected in the first instance due to discrepancies, often

about very trivial matters.

It is therefore good practice for the seller to ask to see the buyer’s application for the

letter of credit at an early stage, before it is submitted to the bank. The seller will

need to check that this reflects the commercial agreement, and that it will be

possible to produce documents that will match all the credit’s terms and conditions.

Specifically, the seller will need to check the following:

• Do the journey stages on the letter of credit (e.g. place of receipt/taking in charge

by the carrier, port of loading, port of unloading, place of final destination) match

the agreed route for the consignment? Note that for multi-modal transport

there can be up to four pieces of information to consider – when and where

goods were taken in charge; when and where goods were loaded onto a vessel;

when and where good were unloaded from vessel; when and where goods finally

delivered.

• Can the latest date of shipment be complied with?

• Can the carrier provide the required transport document with the required

wording, e.g. a date of taking in charge or a date of loading on board, as

specified?

There are many other aspects of the transport document that may need to be

considered in relation to the wording on the letter of credit.

Incoterms 2010: A practical guide p. 43

Successful letter of credit transactions require detailed knowledge of two ICC

publications

• UCP 600: ICC Uniform Customs and Practice for Documentary Credits 2007

revision. ICC Publication No. 600

The rules for drafting of letters of credit and for examining documents for

compliance

• ISBP International Standard Banking Practice for the Examination of Documents

under Documentary Credits. 2013 edition. ICC Publication No. 745

A supplementary guide for the examination process and interpretation of the

rules

See Appendix V for a checklist for checking the transport document against the letter

of credit, to be used in conjunction with the above publications.

Journey points, letter of credit for multi-modal transport

Incoterms 2010: A practical guide p. 44

The letter of credit documents – the devil is in the detail.

Anybody who has worked with letters of credit will know the frustration of having

documents rejected by the bank due to apparently trivial discrepancies between the

requirements of the letter of credit and the documents that have been presented.

Not surprisingly, the Incoterms rules provide their own opportunities for error!

The SWIFT MT700 Letter of Credit message format does not have a separate field for

the Incoterms rule. If specified on the credit, the rule will usually appear as part of

“Description of Goods and Services”.

However there will be implications for documentary requirements, e.g. transport

document and insurance document.

Where a rule such as CIP is used, the buyer will want to be sure that the seller has

indeed paid for carriage to the agreed place, so the documents section of the credit

will include wording such as “Bill of lading marked …. freight paid to Long Beach,

California”.

Consider a transport document that is annotated with two separate statements:

1. Freight paid

2. CIP Long Beach, California

Does this transport document signify that freight was paid to Long Beach?

Common sense would suggest that it does – after all, CIP is well known to mean that

the seller pays for carriage to the named place.

However in the real world of letters of credit, documents such as these are

sometimes rejected, using arguments along the lines that it is not the role of the

examiner to understand terms such as CIP and apply this understanding to the case!

Incoterms 2010: A practical guide p. 45

V. Checklist for the transport document

(To be used in conjunction with UCP 600 and ISBP)

• The document is a transport document as defined by UCP (e.g. not a freight

forwarder’s certificate etc.)

• Transport document appropriately signed, with capacity of signatory if

necessary

• If a charter party bill of lading presented, credit must allow this

• Transport document must be clean, not claused (no damage or defects noted)

• Consignee details as per the credit

• Bill of lading consigned correctly, e.g. to order and endorsed as required

• Places of receipt/loading/unloading/delivery correct

• Showing “shipped on board “ and not on deck

• Name of vessel correct

• Showing shipped on or before latest shipment date

• Transhipment only if permitted by credit

• Marked freight paid if required

• Goods description consistent with credit

Incoterms 2010: A practical guide p. 46

Appendix B: Freight insurance and the rules

The general approach of the Incoterms 2010 rules is that only two of the rules,

Carriage and Insurance Paid to (CIP) and Cost Insurance and Freight (CIF) impose any

obligation on any party to arrange freight insurance.

In all other cases, parties are free to make their own decisions as to the need for

freight insurance for those portions of the journey where they have responsibility for

the goods.

(Buyers and sellers should bear in mind that although carriers may have insurance

cover for consignments in their care, the various international conventions on the

transport of goods set limits on carriers’ liabilities which are typically well below the

commercial value of cargos.)

As noted in the detailed coverage of CIP and CIF:

• The level of cover mandated by these two rules is minimal, and corresponds

to Institute Cargo Clauses C. Important risks such as war and strikes are not

covered; therefore the appropriate level of cover needs to be discussed and

incorporated into the commercial agreement

• Although the seller procures the insurance, the seller will be “off risk” before

the main transport, and hence it will be the responsibility of the buyer to

make a claim. The insurance documents need to be made out appropriately,

e.g. endorsed in favour of the buyer; and the buyer should establish a line of

communication with the carrier and/or insurer in case a claim needs to be

made.

Warning to sellers

Your customer’s insurance arrangements may be of more than

theoretical interest!

Consider a consignment shipped using CFR or CPT – the seller is

not required to insure the goods, and the buyer fails to do this.

If the goods are damaged and the sale is on open account terms,

an unscrupulous buyer may choose to walk away from the

transaction

A cautious seller may feel it necessary to see evidence that the

buyer has taken out insurance, with the seller named as

beneficiary.

Incoterms 2010: A practical guide p. 47

Whilst this arrangement may appear to suit the seller very well, some sales

departments are uncomfortable with it from a “customer service”

perspective, and would prefer to take responsibility for handling insurance

claims.

If the seller wishes to offer this facility, it can be achieved with a letter of

subrogation, in which the buyer relinquishes rights under the insurance policy

in favour of the seller.

Incoterms 2010: A practical guide p. 48

Comments

Resolve references to Appendix??

Something on transport documents generally, e.g. the types, and who provides what.

Check on font size consistency for body text

Things to watch for – another hierarchy level or different font size

String sales catered for, e,g. the seller does not need to ship the goods, they can

procure a contract of carriage by taking over an existing one.