Income Tax Reporting Revsine/Collins/Johnson/Mittelstaedt: Chapter 13 McGraw-Hill/Irwin Copyright ©...

16

Income Tax Reporting Revsine/Collins/Johnson/Mittelstaedt: Chapter 13 McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

-

Upload

nathaniel-hubbard -

Category

Documents

-

view

216 -

download

1

Transcript of Income Tax Reporting Revsine/Collins/Johnson/Mittelstaedt: Chapter 13 McGraw-Hill/Irwin Copyright ©...

Income Tax Reporting

Revsine/Collins/Johnson/Mittelstaedt: Chapter 13

McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Learning objectives

1. The different objectives underlying income determination for financial reporting (book) purposes versus tax purposes.

2. The distinction between temporary (timing) and permanent differences, the items that cause these differences, and how each affects book income versus taxable income.

3. The distortions created when the deferred tax effects of temporary differences are ignored.

4. How tax expense is determined with interperiod tax allocation and the relation between taxes payable, changes in deferred taxes and tax expense.

5. Measuring and reporting valuation differences for deferred tax assets.

13-2

Learning objectives:Concluded

6. How changes in tax rates are measured and recorded.

7. The reporting rules for net operating loss carrybacks and carry-forwards.

8. How to read and interpret tax footnote disclosures and how these footnotes can be used to enhance comparisons across firms.

9. Financial statement disclosures on uncertain tax positions.

10.How tax footnotes can be used to evaluate the degree of conservatism in firms’ book (GAAP) accounting choices.

11.Key differences between IFRS and U.S. GAAP rules for reporting of income taxes.

13-3

Book income and taxable income

Intended to reflect increases in the firm’s “well-offness”.

Includes all earned inflows of net assets, even when the inflow is not immediately convertible into cash.

Reflects expenses as they accrue, not just when they are paid.

Governed by the “constructive receipt/ability to pay” doctrine.

The timing of taxation usually (but not always) follows the inflow of cash or equivalents.

Deductions generally are allowed only when the expenditures are made or when a loss occurs.

Book Income:Income computed for

financial reporting purposes

Taxable Income:Income computed for

tax compliance purposes≠

Divergence complicates the way income taxes are reflected in financial reports

13-4

Understanding income tax reporting:Timing differences

A timing difference results when a revenue (gain) or expense (loss) enters book income in one period but affects taxable income in a different (earlier or later) period.

Book Income

Taxable Income

≠

Timingdifferences:

Permanentdifferences

• Depreciation expense• Bad debt expense• Installment sales• Revenues received in advance

Current period

Later period

$100

$0

$0

$100

Originating

Reversing

Book income

Taxable income Type

Timing differences give rise to deferred tax assets and deferred tax liabilities because they are temporary (they eventually reverse):

13-5

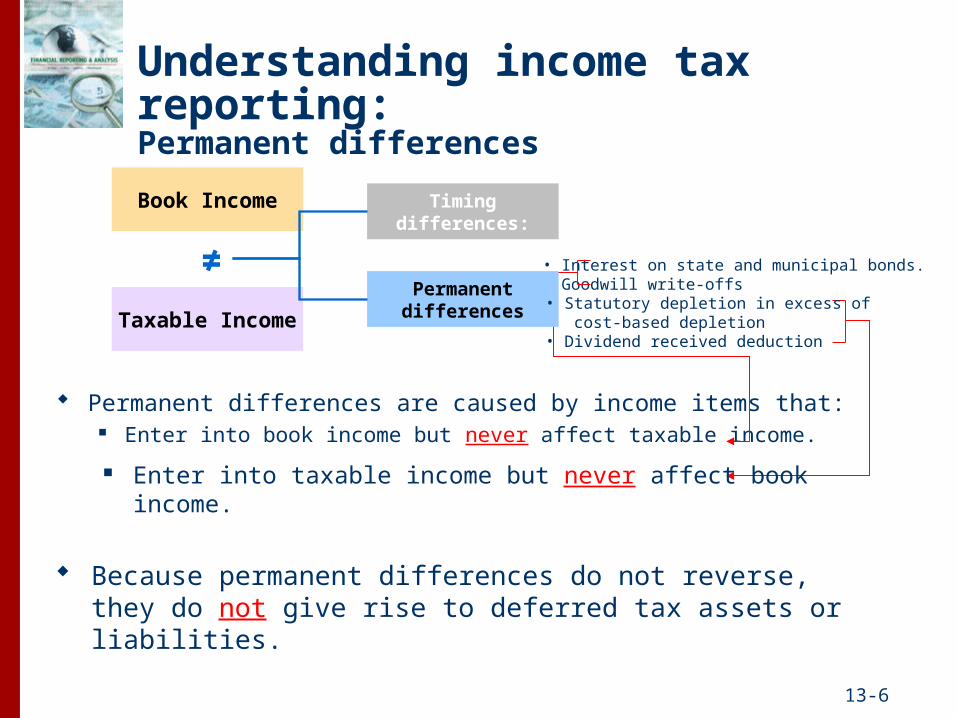

Understanding income tax reporting:Permanent differences

Permanent differences are caused by income items that: Enter into book income but never affect taxable income.

• Interest on state and municipal bonds.• Goodwill write-offs

Book Income

Taxable Income

≠

Timingdifferences:

Permanentdifferences

Enter into taxable income but never affect book income.

Because permanent differences do not reverse, they do not give rise to deferred tax assets or liabilities.

• Statutory depletion in excess of cost-based depletion• Dividend received deduction

13-6

Understanding income tax reporting:The FASB’s solution

Interperiod tax allocation overcomes the mismatch problem.

The “extra” tax depreciation in early years will be offset by lower tax depreciation in later years.

The “extra” tax depreciation thus generates a liability for future taxes.

Recording this deferred tax liability as it accrues eliminates the mismatch.

$3,333

$2,000

$1,333 of “extra” depreciation

in year 1

Tax depreciation

Book depreciation

Future tax liability is $1,333 X 35% or $467

13-7

Deferred income tax accounting:Calculating tax expense

Relation between tax expense, taxes payable, and changes in deferred tax liabilities

$7,000 $6,533= + $467

13-8

Deferred income tax assets:Computing income tax expense

Relation between tax expense, taxes payable, and changes in deferred tax assts and liabilities

13-9

Deferred income tax assets:Valuation allowances

The FASB requires firms with deferred tax assets to assess the likelihood that those assets may not be fully realized in future periods.

Realization depends on whether or not the firm has future taxable income.

0% 50% 100%

“More likely than not ”

• DTA carrying value is reduced until the new amount falls within this range

Probability that DTA will NOT be realized

• Deferred tax asset (DTA) valuation allowance is then required

13-10

The U.S. Income Tax code allows firms reporting operating losses to offset those losses against either past or future tax payments.

Net operating losses:Carrybacks and carryforwards

2007 2008 2009 2010 2011Years

Lossincurred

Carry forwardCarry back

Carry forward

2007 2008 2009 2010 2011Years

LossCarry back

LossCarry forward only

Option 1

Option 2

Firms can elect one of two options: Both carry back and carry forward incurred losses. Only carry forward incurred losses.

13-11

Measuring and Reporting Uncertain Tax Positions

Tax position – refers to a position in a previously filed tax return or a position expected to be taken in a future tax return that is reflected in measuring current taxes payable or deferred income taxes. Uncertain tax positions arise, for example, when the firm claims a deduction for an expense that the IRS auditors may later disallow

GAAP procedures require a two-step process to determine how much benefit to recognize from an uncertain tax position and how to report its tax contingency reserve as a liability for unrecognized tax benefits.

Step 1 – determine if the threshold of more likely than not (more than 50%) is applicable.

Step 2 – measure the tax benefit as the largest amount of benefit that is greater than 50% likely of being realized.

Recorded as an increase in the Tax Contingency Reserve

account

13-12

Understanding the tax footnote:Analytical insights

Large increases in deferred income tax liabilities are a potential sign of deteriorating earnings quality.

Consider ChipPAC. The depreciation-induced increase in the company’s deferred tax liability could be due to:

Growth in capital expenditures Change in estimated useful lives of existing equipment

Sudden decreases in deferred income tax assets are also a potential sign of deteriorating earnings quality.

13-13

Global Vantage PointKey differences between IFRS and U.S. GAAP income tax accounting rules

Difference GAAP IFRSApproach for recognizing deferred tax assets

Uses a valuation account for deferred tax asset if book basis is different from the tax basis

No valuation account

Reconciliation of statutory and effective tax rates

Uses the domestic federal statutory rate

Uses a statutory rate

Reporting of deferred taxes on the balance sheet

Classifies deferred tax assets and liabilities as current or noncurrent depending on the nature of the temporary difference

Deferred tax assets and liabilities are reported as noncurrent

Disclosure of income tax amount recognized directly in equity

Not required Must disclose the aggregate amount of current or deferred income tax income or expense to Other Comprehensive Income

Uncertain tax positions Extensive guidance under FASB ASC 740

No specific guidance. IAS 12 calls for tax assets and liabilities to be measured at the amount expected to be paid

13-14

Summary

The rules for computing income for financial reporting purposes—book income—differ from those for computing income for tax purposes.

The differences between book income and taxable income are caused by both permanent and temporary (timing) differences in the revenue and expense items reported on a company’s books versus its tax return.

Temporary differences give rise to both deferred tax assets and deferred tax liabilities.

Deferred tax accounting allows firms to report tax costs (or benefits) on the income statement in the same period as the related revenue or expense items are reported (matching principle).

13-15

Summary concluded

The income tax footnote provides useful information for understanding how much tax is paid and how much is deferred each year. Tax footnotes also help explain why effective tax rates may differ from statutory rates.

Tax footnotes provide a wealth of information that can be exploited to improve interfirm comparability and evaluate firms’ earnings quality.

GAAP disclosures are useful in assessing a firm’s uncertain tax positions and whether the firm is aggressive or conservative in recognizing the benefits associated with these positions.

There are a number of differences between IFRS and U.S. GAAP rules for accounting for income taxes that you should be aware of.

13-16