income from salary.docx

37

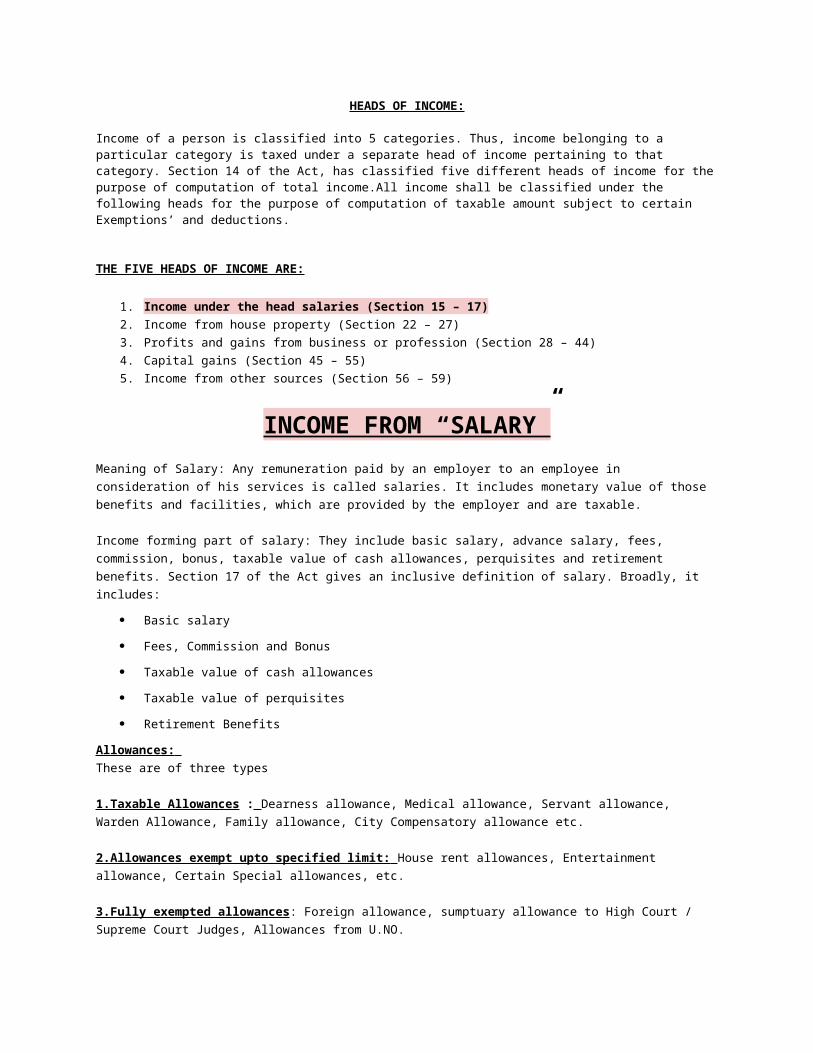

HEADS OF INCOME: Income of a person is classified into 5 categories. Thus, income belonging to a particular category is taxed under a separate head of income pertaining to that category. Section 14 of the Act, has classified five different heads of income for the purpose of computation of total income.All income shall be classified under the following heads for the purpose of computation of taxable amount subject to certain Exemptions’ and deductions. THE FIVE HEADS OF INCOME ARE: 1. Income under the head salaries (Section 15 – 17) 2. Income from house property (Section 22 – 27) 3. Profits and gains from business or profession (Section 28 – 44) 4. Capital gains (Section 45 – 55) 5. Income from other sources (Section 56 – 59) INCOME FROM “SALARY” Meaning of Salary: Any remuneration paid by an employer to an employee in consideration of his services is called salaries. It includes monetary value of those benefits and facilities, which are provided by the employer and are taxable. Income forming part of salary: They include basic salary, advance salary, fees, commission, bonus, taxable value of cash allowances, perquisites and retirement benefits. Section 17 of the Act gives an inclusive definition of salary. Broadly, it includes: Basic salary Fees, Commission and Bonus Taxable value of cash allowances Taxable value of perquisites Retirement Benefits Allowances: These are of three types 1.Taxable Allowances : Dearness allowance, Medical allowance, Servant allowance, Warden Allowance, Family allowance, City Compensatory allowance etc. 2.Allowances exempt upto specified limit: House rent allowances, Entertainment allowance, Certain Special allowances, etc. 3.Fully exempted allowances : Foreign allowance, sumptuary allowance to High Court / Supreme Court Judges, Allowances from U.NO.

-

Upload

nicholas-owens -

Category

Documents

-

view

20 -

download

0

Transcript of income from salary.docx

HEADS OF INCOME:

Income of a person is classified into 5 categories. Thus, income belonging to a particular category is taxed under a separate head of income pertaining to that category. Section 14 of the Act, has classified five different heads of income for the purpose of computation of total income.All income shall be classified under the following heads for the purpose of computation of taxable amount subject to certain Exemptions’ and deductions.

THE FIVE HEADS OF INCOME ARE:

1. Income under the head salaries (Section 15 – 17)

2. Income from house property (Section 22 – 27)

3. Profits and gains from business or profession (Section 28 – 44)

4. Capital gains (Section 45 – 55)

5. Income from other sources (Section 56 – 59)

INCOME FROM “SALARY”

Meaning of Salary: Any remuneration paid by an employer to an employee in consideration of his

services is called salaries. It includes monetary value of those benefits and facilities, which are

provided by the employer and are taxable.

Income forming part of salary: They include basic salary, advance salary, fees, commission, bonus,

taxable value of cash allowances, perquisites and retirement benefits. Section 17 of the Act gives an

inclusive definition of salary. Broadly, it includes:

Basic salary

Fees, Commission and Bonus

Taxable value of cash allowances

Taxable value of perquisites

Retirement Benefits

Allowances:

These are of three types

1.Taxable Allowances : Dearness allowance, Medical allowance, Servant allowance, Warden

Allowance, Family allowance, City Compensatory allowance etc.

2.Allowances exempt upto specified limit: House rent allowances, Entertainment allowance,

Certain Special allowances, etc.

3.Fully exempted allowances: Foreign allowance, sumptuary allowance to High Court / Supreme

Court Judges, Allowances from U.NO.

Fully taxable allowances

Dearness Allowance and Dearness Pay

City Compensatory Allowance

Tiffin / Lunch Allowance

Warden or Proctor Allowance

Overtime Allowance

Fixed Medical Allowance

Servant Allowance

Other allowances

Partially exempt allowances

This category includes allowances which are exempt up to certain limit.

House Rent Allowance (H.R.A.) Sec.10(13A)

An allowance granted to a person by his employer to meet expenditure incurred on payment of rent in

respect of residential accommodation occupied by him is exempt from tax to the extent of least of the

following three amounts:

Format for computation of H.R.A

1)Rent-10% of Salary- XXX

2)House Rent Allowance actually received by the assessee- XXX

3) 50% of salary (If accommodation is situated in Mumbai,

Kolkata, Delhi, Chennai) OR 40% of salary (if accommodation is situated in any other place).- XXX

Least of the Above XXX

If an employee is living in his own house and receiving HRA, it will be fully taxable.

Entertainment Allowance Sec.16 (ii)

This allowance is first included in gross salary under allowances and then deduction is given to only

government employees under Section 16 (ii).

Limit

Gross Salary XXXXXX

1) 5000

2) 1/5 of the Salary

3) Actual Amount

Least of the Above XXX

Special Allowances for meeting official expenditure

Certain allowances are given to the employees to meet expenses incurred exclusively in performance

of official duties and hence are exempt to the extent actually incurred for the purpose for which it is

given. These include travelling allowance, daily allowance, conveyance allowance, helper allowance,

research allowance and uniform allowance.

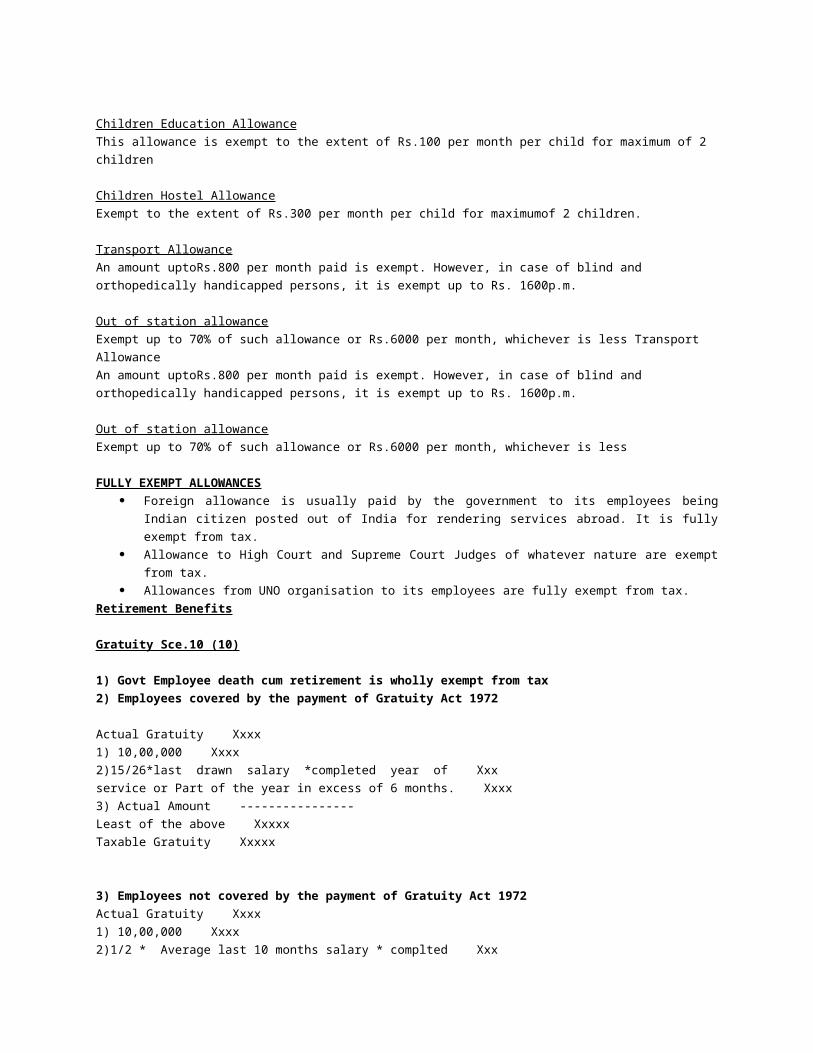

Children Education Allowance

This allowance is exempt to the extent of Rs.100 per month per child for maximum of 2 children

Children Hostel Allowance

Exempt to the extent of Rs.300 per month per child for maximumof 2 children.

Transport Allowance

An amount uptoRs.800 per month paid is exempt. However, in case of blind and orthopedically

handicapped persons, it is exempt up to Rs. 1600p.m.

Out of station allowance

Exempt up to 70% of such allowance or Rs.6000 per month, whichever is less Transport Allowance

An amount uptoRs.800 per month paid is exempt. However, in case of blind and orthopedically

handicapped persons, it is exempt up to Rs. 1600p.m.

Out of station allowance

Exempt up to 70% of such allowance or Rs.6000 per month, whichever is less

FULLY EXEMPT ALLOWANCES

Foreign allowance is usually paid by the government to its employees being Indian citizen

posted out of India for rendering services abroad. It is fully exempt from tax.

Allowance to High Court and Supreme Court Judges of whatever nature are exempt from tax.

Allowances from UNO organisation to its employees are fully exempt from tax.

Retirement Benefits

Gratuity Sce.10 (10)

1) Govt Employee death cum retirement is wholly exempt from tax

2) Employees covered by the payment of Gratuity Act 1972

Actual Gratuity Xxxx

1) 10,00,000 Xxxx

2)15/26*last drawn salary *completed year of Xxx

service or Part of the year in excess of 6 months. Xxxx

3) Actual Amount ----------------

Least of the above Xxxxx

Taxable Gratuity Xxxxx

3) Employees not covered by the payment of Gratuity Act 1972

Actual Gratuity Xxxx

1) 10,00,000 Xxxx

2)1/2 * Average last 10 months salary * complted Xxx

year of service Xxxx

3) Actual Amount ----------------

Least of the above Xxxxx

Taxable Gratuity Xxxxx

PENSION

Un commuted pension refers to pension periodically received by the employee. It is taxable in the

hands of the both Govt. and Non Govt Employees.

Commuted pension Sec.10 (10A) means lumsum amount taken by commuting the pension or part

of the pension. Any commuted pension received by a Govt employee is wholly exempt from tax.

LEAVE SALARY. Sec.10 (10AA)

Govt employee is wholly exempt from tax.

Others are following

Actual Amount Xxxx

1) 300,000 Xxxx

2)10* salary (Average last 10 months salary ) Xxx

3)cash equivalent leave* Average last 10 months Xxxx

salary ----------------

3) Actual Amount Xxxxx

Least of the above

Taxable Amount Xxxxx

RETRENCHEMENT COMPENSATION Sec.10(10B)

Actual Amount Xxxx

1) Amount calculated under the Industrial Disputes Xxxx

Act 1947. Xxx

2) 500,000 ---------------

Xxxxx

TaxableAmount Xxxxx

VOLUNTARY RETIREMENT SCHEME Sec.10(10C)

Employee who has completed 10 years of service or completed 40 years of age Xxxx

Actual Amount

1) last drawn salary *3* complted years service Xxxx

OR Xxx

last drawn salary * remaining months of service xxxx

whichever is lower ----------------

2)500,000 Xxxxx

3)actual Amount Received

Taxable Amount xxxxx

What's Salary Income?

Section 15 is the charging section for the head "Salaries". It provides for charge to income tax of

certain incomes from an employer or a former employer to an assessee under the head "Salaries".

The taxability of the salary income in a previous year is as under: -

1. Any salary due in the previous year, whether paid or not;

2. Any salary paid/allowed in the previous year, though not due or before it became due to him;

3. Any arrears of salary paid/allowed in the previous year, if not charged to income tax for any

earlier previous year.

4. However, if any salary paid in advance is included in the total income of any person for any

previous year, then it shall not be included again in the total income of the person when the

salary becomes due.

In short, Salary Income is chargeable to income tax on "due" basis or "receipt" basis whichever is

earlier.

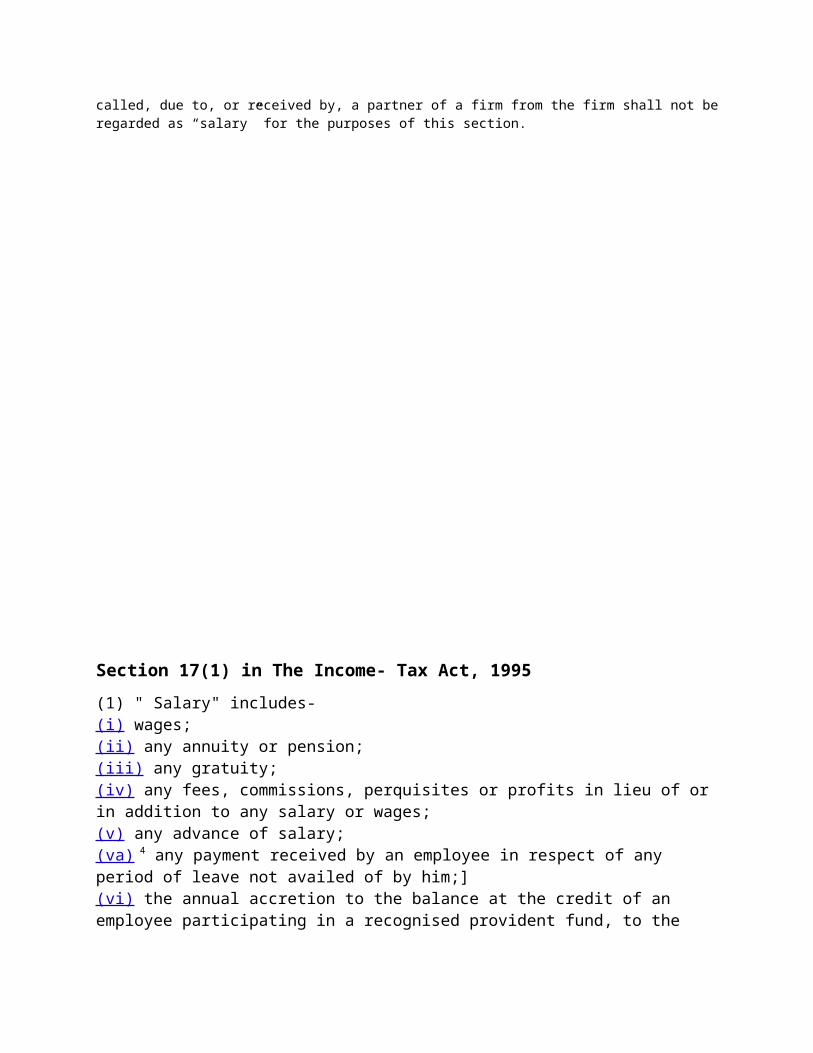

Note: Any salary, bonus, commission or remuneration, by whatever name called, due to, or received

by, a partner (even if under representative capacity) of a firm, from the firm shall not be regarded as

"salary" for the purposes of this section.

Top

Employer & Employee Relationship

Section 15 brings to charge under the head "Salary", any amount due from, or amount paid or allowed

by, an employer or a former employer to an assessee employee.

Therefore, only if there is an employer and employee relationship (either in the present or in the past),

the income can be charged to income- tax under the head "Salaries".

It is necessary to distinguish the relationship of master and servant from that of an employer and

independent contractor.

The test laid down is that in the case of master and servant, the master can order or require what is to

be done and how it is to be done (control & supervision) but in case of an independent contractor an

employer can only say what is to be done but not how it shall be done.

In essence, the real test would be whether the employment is a "Contract of Service" (in which case it

is chargeable as "Salary") or "Contract for Service" (in which case it is chargeable as "Profits and Gains

of Business or Profession" or "Other Sources").

Note:

The salary received by MLA and MPs are chargeable only under the head "Other Sources", since there

is no employer-employee relationship.

The salary paid to partners by firm is taxable as "Profits and Gains of Business or Profession" as the

partners and firm are not different and they are self-employed.

However, the salary of Judges is chargeable as "Salaries".

Top

Salary Definition u/s 17(1)

The term "Salary" has been defined under Section 17(1) to include -

1. Wages;

2. Any annuity or pension;

3. Any gratuity;

4. Any fees, commissions, perquisites or profits in lieu of or in addition to any 'salary or wages';

5. Any advance of salary;

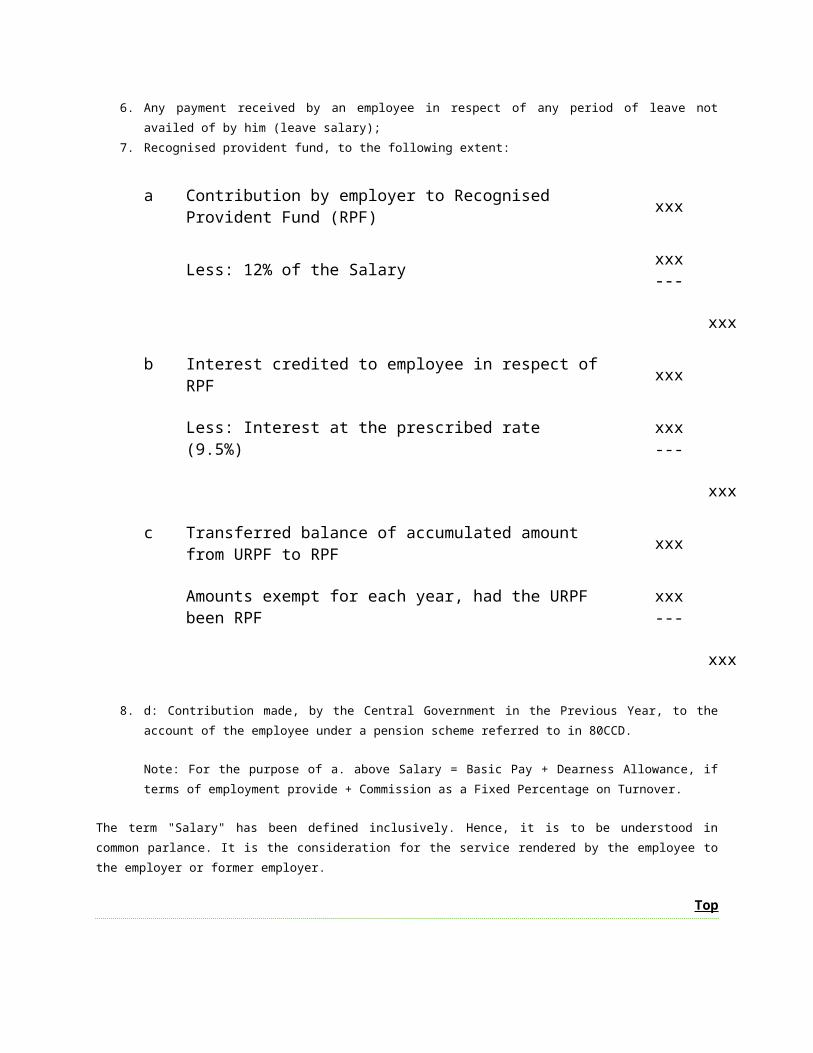

6. Any payment received by an employee in respect of any period of leave not availed of by him

(leave salary);

7. Recognised provident fund, to the following extent:

a Contribution by employer to Recognised Provident Fund (RPF) xxx

Less: 12% of the Salaryxxx---

xxx

b Interest credited to employee in respect of RPF xxx

Less: Interest at the prescribed rate (9.5%)xxx---

xxx

c Transferred balance of accumulated amount from URPF to RPF xxx

Amounts exempt for each year, had the URPF been RPFxxx---

xxx

8. d: Contribution made, by the Central Government in the Previous Year, to the account of the

employee under a pension scheme referred to in 80CCD.

Note: For the purpose of a. above Salary = Basic Pay + Dearness Allowance, if terms of

employment provide + Commission as a Fixed Percentage on Turnover.

The term "Salary" has been defined inclusively. Hence, it is to be understood in common parlance. It is

the consideration for the service rendered by the employee to the employer or former employer.

Top

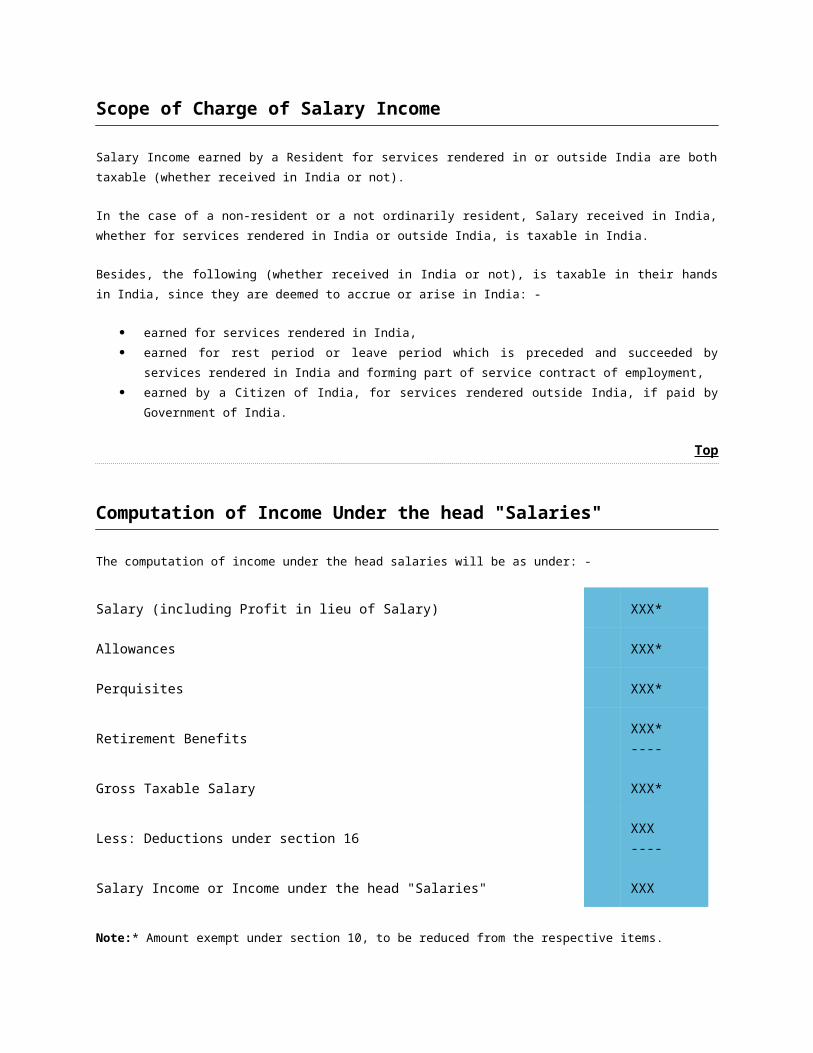

Scope of Charge of Salary Income

Salary Income earned by a Resident for services rendered in or outside India are both taxable (whether

received in India or not).

In the case of a non-resident or a not ordinarily resident, Salary received in India, whether for services

rendered in India or outside India, is taxable in India.

Besides, the following (whether received in India or not), is taxable in their hands in India, since they

are deemed to accrue or arise in India: -

earned for services rendered in India,

earned for rest period or leave period which is preceded and succeeded by services rendered

in India and forming part of service contract of employment,

earned by a Citizen of India, for services rendered outside India, if paid by Government of

India.

Top

Computation of Income Under the head "Salaries"

The computation of income under the head salaries will be as under: -

Salary (including Profit in lieu of Salary) XXX*

Allowances XXX*

Perquisites XXX*

Retirement BenefitsXXX*

----

Gross Taxable Salary XXX*

Less: Deductions under section 16XXX

----

Salary Income or Income under the head "Salaries" XXX

Note:* Amount exempt under section 10, to be reduced from the respective items.

u/s 15

15. Salaries.- The following income shall be chargeable to income-tax under the head “Salaries”—

(a) any salary due from an employer or a former employer to an assessee in the previous year, whether paid or not;

(b) any salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer though not due or before it became due to him;

(c) any arrears of salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer, if not charged to income-tax for any earlier previous year.

Explanation 1.—For the removal of doubts, it is hereby declared that where any salary paid in advance is included in the total income of any person for any previous year it shall not be included again in the total income of the person when the salary becomes due.

Explanation 2.—Any salary, bonus, commission or remuneration, by whatever name called, due to, or received by, a partner of a firm from the firm shall not be regarded as “salary” for the purposes of this section.

Section 17(1) in The Income- Tax Act, 1995

(1) " Salary" includes-

(i) wages;(ii) any annuity or pension;(iii) any gratuity;(iv) any fees, commissions, perquisites or profits in lieu of or in addition to any salary or wages;(v) any advance of salary;(va) 4 any payment received by an employee in respect of any period of leave not availed of by him;](vi) the annual accretion to the balance at the credit of an employee participating in a recognised provident fund, to the extent to which it is chargeable to tax under rule 6 of Part A of the Fourth Schedule; and(vii) the aggregate of all sums that are comprised in the transferred balance as referred to in sub- rule (2) of rule 11 of Part A of the Fourth Schedule of an employee participating in a recognised provident fund, to the extent to which it is chargeable to tax under sub- rule (4) thereof;

Section 17(2) defines perquisites to include:

Chargeable to Tax in the hands of Specified + Non- Specified Employees both.

The value of Rent Free Accommodation provided to the assessee by his employer (whether Furnished or Unfurnished);

The value of any Concession w.r.t any accommodation provided to the assessee by his employer;

Any sum paid by the Employer w.r.t any obligation liable to be discharged by the Employee;

Any sum payable by Employer towards a Life assurance Policy or towards a Contract of Annuity;

Chargeable to Tax in the hands of only Specified Employees.

The value of any amenity granted at Free of Cost or Concessional rate to the assessee by his employer;

The value of Fringe Benefits or amenities (not being the ones chargeable in the hands of the employer u/s 115WB):-

o Interest free concessional rent

o Use of moveable assets

o Transfer of moveable assets

o Medical facilities to employees

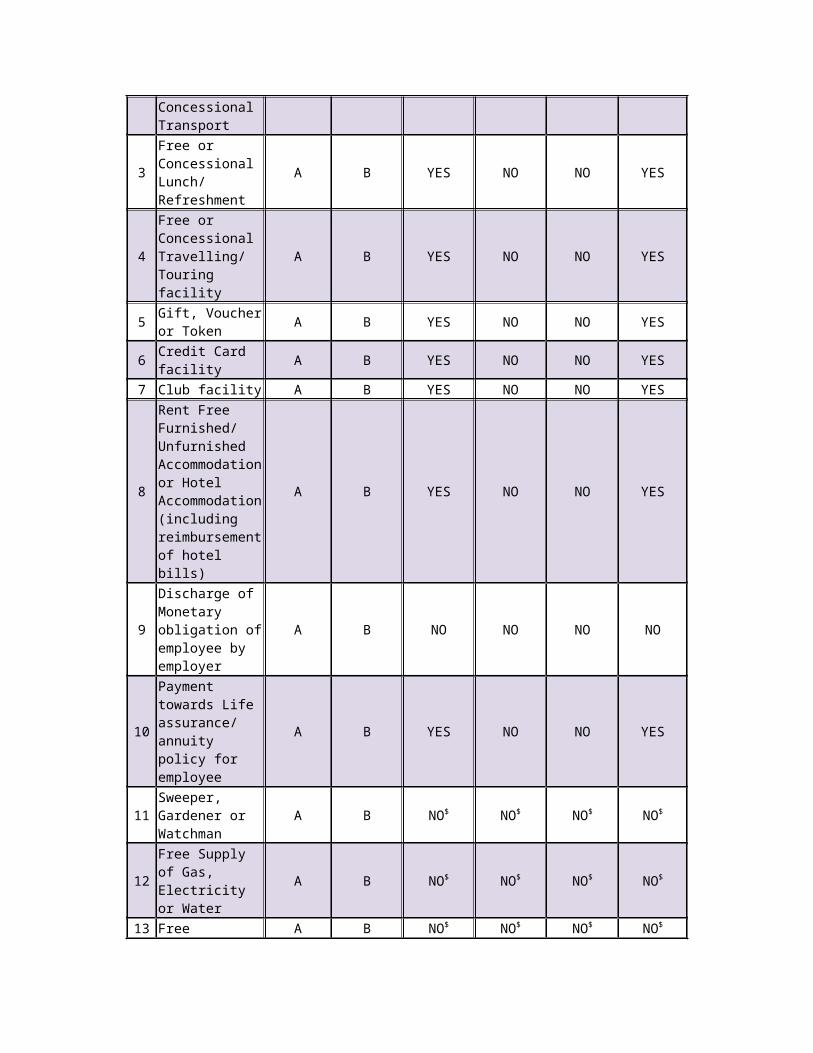

PLEASE NOTE:The Perquisites chargeability is decided on the Nature of the Employer & consequent levy of Fringe Benefit Tax on such Employer as per Income Tax Act. The following table would clarify the scenario to a great extent, however this list is not of an exhaustive nature though a thoughtful attempt is made to include all possible types of perquisites in practical circumstances:

Sr. No.

Nature of Perquisite

Nature of Employee*

FBT chargeability as per nature of

Employer

Taxed as Perquisite in hands of Employee

Category A

Category B

Category A

Category B

1Motor Car (Owned or Hired)

A B YES NO NO YES

2Free or Concessional Transport

A B YES NO NO YES

3 Free or Concessional Lunch/

A B YES NO NO YES

Refreshment

4

Free or Concessional Travelling/ Touring facility

A B YES NO NO YES

5 Gift, Voucher or Token

A B YES NO NO YES

6 Credit Card facility

A B YES NO NO YES

7 Club facility A B YES NO NO YES

8

Rent Free Furnished/ Unfurnished Accommodation or Hotel Accommodation (including reimbursement of hotel bills)

A B YES NO NO YES

9

Discharge of Monetary obligation of employee by employer

A B NO NO NO NO

10

Payment towards Life assurance/ annuity policy for employee

A B YES NO NO YES

11Sweeper, Gardener or Watchman

A B NO$ NO$ NO$ NO$

12Free Supply of Gas, Electricity or Water

A B NO$ NO$ NO$ NO$

13 Free Education A B NO$ NO$ NO$ NO$

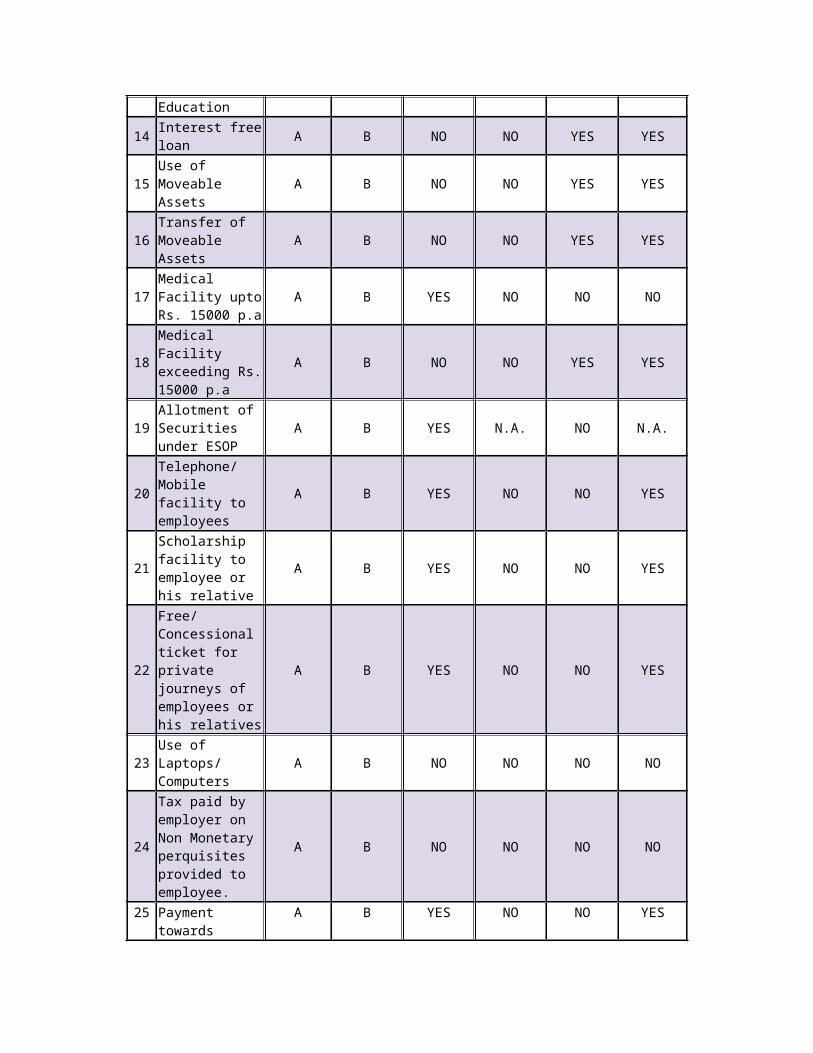

14 Interest free loan

A B NO NO YES YES

15Use of Moveable Assets

A B NO NO YES YES

16Transfer of Moveable Assets

A B NO NO YES YES

17Medical Facility upto Rs. 15000 p.a

A B YES NO NO NO

18Medical Facility exceeding Rs. 15000 p.a

A B NO NO YES YES

19Allotment of Securities under ESOP

A B YES N.A. NO N.A.

20Telephone/ Mobile facility to employees

A B YES NO NO YES

21

Scholarship facility to employee or his relative

A B YES NO NO YES

22

Free/ Concessional ticket for private journeys of employees or his relatives

A B YES NO NO YES

23 Use of Laptops/ Computers

A B NO NO NO NO

24

Tax paid by employer on Non Monetary perquisites provided to employee.

A B NO NO NO NO

25

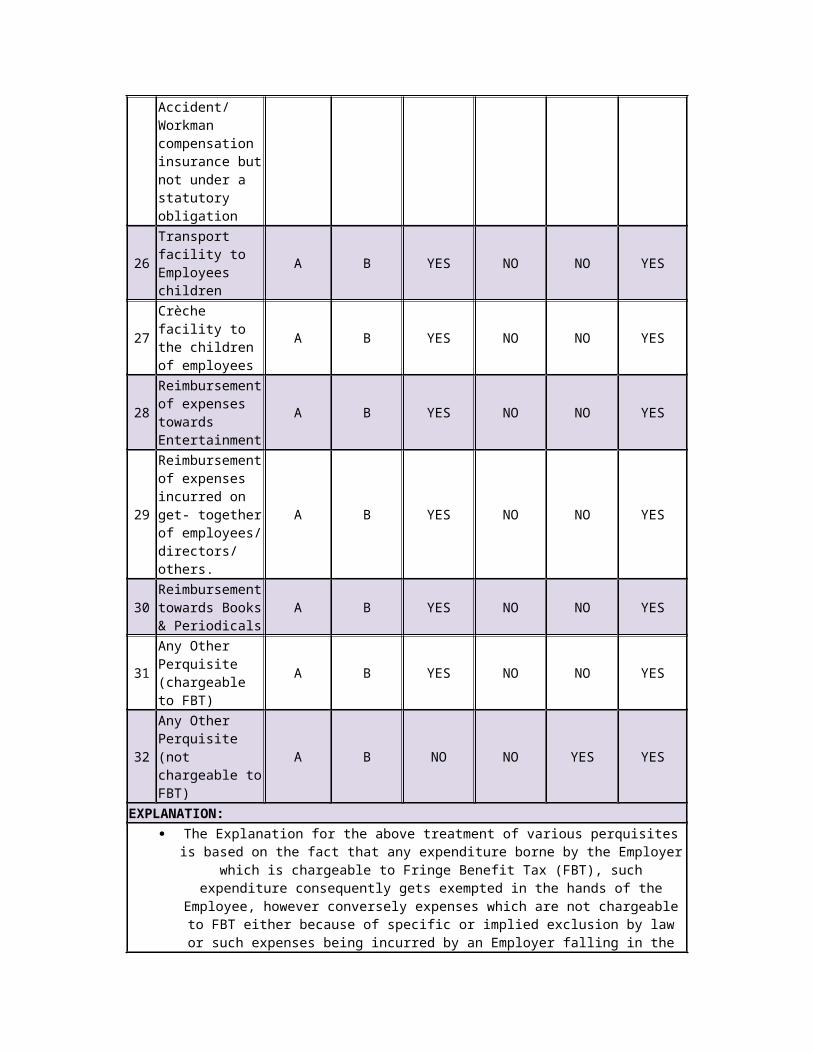

Payment towards Accident/ Workman compensation insurance but not under a statutory obligation

A B YES NO NO YES

26

Transport facility to Employees children

A B YES NO NO YES

27Crèche facility to the children of employees

A B YES NO NO YES

28

Reimbursement of expenses towards Entertainment

A B YES NO NO YES

29

Reimbursement of expenses incurred on get- together of employees/ directors/ others.

A B YES NO NO YES

30

Reimbursement towards Books & Periodicals

A B YES NO NO YES

31

Any Other Perquisite (chargeable to FBT)

A B YES NO NO YES

32

Any Other Perquisite (not chargeable to FBT)

A B NO NO YES YES

EXPLANATION: The Explanation for the above treatment of various perquisites is based on

the fact that any expenditure borne by the Employer which is chargeable to Fringe Benefit Tax (FBT), such expenditure consequently gets exempted in the hands of the Employee, however conversely expenses which are not

chargeable to FBT either because of specific or implied exclusion by law or such expenses being incurred by an Employer falling in the ‘Category B’ as stated below then such expenses shall be chargeable in the hands of the

Employee under ‘Income from Salaries’ for Income tax purposes.

Expenditure incurred by the Employer which is fully exempted from tax e.g. Item 23 & 24 above shall not be chargeable to tax both in the hands of

employer & employee.

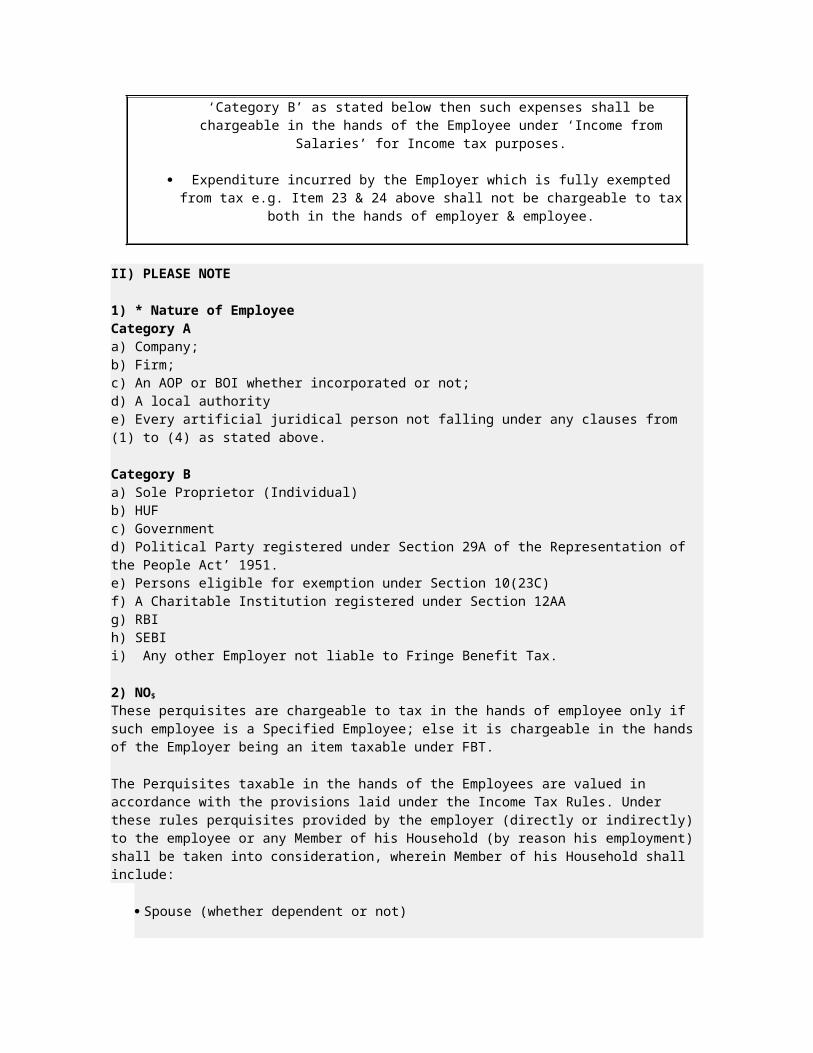

II) PLEASE NOTE

1) * Nature of EmployeeCategory Aa) Company;b) Firm;c) An AOP or BOI whether incorporated or not;d) A local authoritye) Every artificial juridical person not falling under any clauses from (1) to (4) as stated above.

Category Ba) Sole Proprietor (Individual)b) HUFc) Governmentd) Political Party registered under Section 29A of the Representation of the People Act’ 1951.e) Persons eligible for exemption under Section 10(23C)f) A Charitable Institution registered under Section 12AAg) RBIh) SEBIi) Any other Employer not liable to Fringe Benefit Tax.

2) NO$

These perquisites are chargeable to tax in the hands of employee only if such employee is a Specified Employee; else it is chargeable in the hands of the Employer being an item taxable under FBT.

The Perquisites taxable in the hands of the Employees are valued in accordance with the provisions laid under the Income Tax Rules. Under these rules perquisites provided

by the employer (directly or indirectly) to the employee or any Member of his Household (by reason his employment) shall be taken into consideration, wherein Member of his Household shall include:

Spouse (whether dependent or not)

Children (whether dependent or not)

Parents (whether dependent or not)

Servants & Dependents

Central Government ActSection 17(3) in The Income- Tax Act, 1995

(3) " profits in lieu of salary" includes-(i) the amount of any compensation due to or received by an assessee from his employer or former employer at or in connection with the termination of his employment or the modification of the terms and conditions relating thereto;

(ii) any payment (other than any payment referred to in clause (10), 3 , clause (10A)] 4 , clause (10B)], clause (11), 5 clause (12) 6 , clause (13)] or clause (13A)] of section 10), due to or received by an assessee from an employer or a former employer or from a provident or other fund 7 (not being an approved superannuation fund)], to the extent to which it does not consist of contributions by the assessee or interest on such contributions.1. Inserted by the Finance Act, 1992, w. e. f. 1- 4- 1993.2. Omitted by the Finance Act, 1985, w. e. f. 1- 4- 1985. it was inserted by the Taxation Laws (Amendment) Act, 1984, w. e. f. 1- 4- 1985, thus having never come into operation. The consequential amendments in sub- clauses (iv) and (v) were also made and omitted simultaneously.3. Inserted by the Finance (No. 2) Act, 1965, w. r. e. f. 1- 4- 1962.4. Inserted by the Finance Act, 1975, w. e. f 1- 4- 1976.5. Substituted for" or clause (12)" by the Direct Taxes (Amendment) Act, 1964, w. e. f. 6- 10- 1964.6. Being inserted by the Finance Act, 1995, w. e. f. 1- 4- 1996.7. Being omitted, ibid.

gardeners, night watchman and sweepers provided by the employer should be calculated on an ad hoc basis as given in Letter No. 40 25 69, dated 8- 6- 1971 (reproduced below) only when the services of sweeper are provided by the employer, i. e. the sweeper is recruited by the employer and remunerated by him but his services are placed at the disposal of the employee. 2 Rent- free accommodation.- While determining the fair rental value of an accommodation owned by the company, the cost of acquisition and other capital expenses on renovation, etc. incurred by the company should be taken into account. In respect of premises taken on lease or rent by the company the actual payment by the company should be taken as fair rental value of the premises. 3 Reimbursement of medical expenses.- The value of the perquisite arising by way of payment or reimbursement by an employer of expenditure on medical treatment incurred by his employee on himself or on his spouse, children or parents including the provision of free medical treatment or treatment at a concessional rate will not be included in the taxable salary of the employee in the following cases:(i) where the medical treatment is availed at hospitals, clinics, etc. maintained by the employer;(ii) where the medical treatment is availed at hospitals maintained by the Government or local authorities or hospitals approved for the purposes of CGHS or the Central Medical Scheme;(iii) where the expenditure is on medical insurance premia;(iv) where the medical treatment is availed of from any doctor outside the institutions schemes mentioned above, an expenditure of upto Rs. 10, 000 in a year in the aggregate; and(v) where the medical treatment is availed of in a hospital outside India and the expenditure is incurred for treatment including on travel and stay abroad in connection with such treatment, as also on travel and stay abroad of one attendant, to the extent permitted by RBI subject to the condition that the amount qualifying for such tax exemption would not include expenditure incurred on travel in the case of employees whose gross total

income as computed without considering the amount paid or reimbursed for expenditure in connection with medical treatment exceeds Rs. 1 lakh. 4 Rent- free residential accommodation.- Keeping in view the steep escalation in rents, it has been decided that in the case of rent- free accommodation provided by an employer to an employee at Bombay, Calcutta, Delhi and Madras, the perquisite value will be calculated by adding the excess over 60 per cent of the salary of the employee. The valuation in regard to other places in India would be with reference to the excess over 50 per cent. In the case of rent- free furnished accommodation and addition in respect of the perquisite by way of furniture at 10 per cent per annum of the original cost of such furniture is to be made. Perquisite value of free furniture, including television sets, radio sets, refrigerators, other household appliances and air- conditioning plant and equipment provided to all categories of salaried taxpayers will be taken to be 15 per cent of the original cost of such furniture or where the furniture is hired, the hire charges payable by the employer. In the case of person,,, employed by the RBI, statutory corporations, government companies, bodies or undertakings financed wholly or mainly by the government and officers of government whose services have been lent to or who are employed after retirement from Government service with any company inwhich not less than 40 per cent of the shares are held by the Government of RBI or a corporation owned by RBI, the perquisite value of unfurnished rent- free residential accommodation will be taken to be 10 per cent of the salary due to the person in respect of the period during which the accommodation was occupied by him. If residential accommodation is provided by the employer at a concessional rent the value of the perquisite will be determined as if the employee had been provided with rent- free residential accommodation and the amount so computed will be reduced by the rent payable by the employee. 5 Motor car conveyance.- If a motor car is provided by the employer for the use by the employee partly for his private or personal purpose and partly for use in the performance of his duties, a proportionate part of the expenditure incurred by the employer on the running and maintenance of the motor car and of the amount representing normal wear and tear of the motor car, which is attributable to the user of the car by the employee for his private or personal purposes the duties of employment are to be performed or from back to his residence will be regarded as use motor car for private or personal purposes will be taken as the value of the perquisite in the hands of the employee. Where the employee is provided with or allowed the use of motor car for his private or personal purposes at a concessional rate, the value of the perquisite will first be computed as if the perquisite had been provided by the employer free of charge and the amount so computed will be reduced by the amount payable by the employee to the employer. 6 Payments to servants.- The amount spent on the salary of a gardener by the employer does not represent a sum paid by the employer in respect of any obligation which but for such payment would have been payable by the employee. The payment

of salary to a gardener as such cannot be regarded as a perquisite so as to justify that amount being taxed in the hands of' the employees. However, the expenses incurred by way of maintenance of a gardener may be taken into account for the purposes of estimating the value of rent- free residential accommodation provided by the employer under rule 3. The taxable perquisite in the hands of the employee on account of services of servants provided by the employer will be calculated at 75 per cent of actual wages or Rs. 60 per month whichever is less in the case of sweeper and 50 per cent of actual wages or Rs. 60 per month whichever is less in the case of gardeners and watchman. 7 Sumptuary allowance.- Sumptuary allowance has to be treated as an entertainment allowance. Accordingly such allowance received by a person who is in receipt of salary from Government to the extent that such allowance is required to be deducted in computing the income chargeable under the head' salaries' may be regarded as an allowance exempt and may not be included in the term' salary' for the purposes of rule 3. 8 Children' s education allowance.- Payments towards children' s education made to the employee or on behalf of the employee will be liable to income- tax (i) where fixed allowances are given in cash by the employer to the employee to meet the cost of education of the latter' s children; (ii) where the education fees are paid by the employer directly to the school; and (iii) where the employee incurs the expenses in the first instance and gets reimbursement from the employer. 9 Premium for annuity.- The premium paid by an ex- employer to purchase an annuity payable to an ex- employee is taxable only under section 17 (3) (ii). The payment will not be admissible as revenue expenditure in the hands of the employer.1 Chapter sub- heading' B.- Interest on securities' and sections 18 to 21 omitted by the Finance Act, 1988 w. e. f. 1- 4- 1989 .]1. Prior to the omission, the chapter sub- heading, section 18, as amended by the Finance Act, 1965, w. e. f. 1- 4- 1965 and the Finance Act, 1988, w. e. f. 1- 4- 1988; section 19; section 20, as amended by the Finance Act, 1979, w. e. f. 1- 4- 1980; and section 21 read as under:" B.- Interest on securities18. Interest on securities.- (1) The following amounts due to an assessee in the previous year shall be chargeable to income- tax under the head" Interest on securities",- (i) interest on any security of the Central or State Government; (ii) interest on debentures or other securities for money issued by or on behalf of a local authority or a company or a corporation established by a Central, State or Provincial Act. (2) Nothing contained in sub- section (1) shall be construed as precluding an assessee from being charged to income- tax in respect of any interest on securities received by him in a previous year if such interest had not been charged to income- tax for any earlier previous year.19. Deductions from interest on securities.- Subject to the provisions of section 21, the income chargeable under the head" Interest on securities" shall be computed after making the following deductions- (i) any reasonable sum expended by the assessee for the purpose of realising such interest; (ii) any interest payable on moneys borrowed for the purpose of investment in the securities by the assessee.20. Deductions from interest on securities in the case of a banking company.- (1) In the case of a banking- company- (i) the sum to be regarded as a sum reasonably expended for the purpose referred to in clause (i) of section 19 shall be an amount bearing to the aggregate of its expenses as are admissible under the provisions of sections 30, 31, 36 and 37 (other than clauses (iii), (vi), (vii) and (viia) of sub- section (1) of section 36) the same proportion as the gross receipts from interest on securities (inclusive of tax deducted at source) chargeable to

income- tax under section 18 bear to gross receipts of the company from all sources which are included in the profit and loss account of the company; (ii) the amount to be regarded as interest payable on moneys borrowed for the purpose referred to in clause (ii) of section 19 shall be an amount which bears to the amount of interest payable on all moneys borrowed by the company the same proportion as the gross receipts from interest on securities (inclusive of tax deducted at source) chargeable to income- tax under section 18 bear to the gross receipts from all sources which are included in the profit and loss account of the company. (2) The expenses deducted under clauses (i) and (ii) of sub- section (1) shall not again form part of the deductions admissible under sections 30 to 37 for the purposes of computing the income of the company under the head" Profits and gains of business or profession". Explanation.- For the purposes of this section," moneys borrowed" includes moneys received by way of deposits.21. Amounts not deductible from interest on securities.- Notwithstanding anything contained in sections 19 and 20 any interest chargeable under this Act which is payable outside India (not being interest on a loan issued for public subscription before the 1st day of April, 1938 ) on which tax has not been paid or deducted under Chapter XVII- B, and in respect of which there is no person in India who may be treated as an agent under section 163 shall not be deducted in computing the income chargeable under the head" Interest on securities."

Leave Encashment Salary [Sec. 10(10AA)] Tax Treatment of leave

encashment is as under : Cases Treatment A. During service tenure Fully taxable [Sec. 17(1)(va)] B. At the time of retirement by employee of: Government Exempted [Sec.10(10AA)(i) ] Other Employer Minimum of the following shall be exempted from tax u/s 10(10AA)(ii): Actual amount received; Rs.300000; 10 months average salary Cash equivalent of 30 days average salary for every completed year of service as reduced by actual leave availed or encashed during the tenure of service. Note: The period of 30 days is the maximum ceiling. If employer allows leave for less than 30 days p.a. then such lesser days shall be considered. Average salary means Basic + DA (forming part of retirement benefit) + Commission (as a fixed percentage on turnover) being last 10 months average salary from the date of retirement . While calculating completed year of service, ignore any fraction of the year. While claiming the statutory amount (i.e. Rs.300000) any deduction claimed earlier as leave encashment shall be reduced from Rs.300000 Assessee can claim Relief u/s 89(1). Leave salary paid to the legal heir: Leave salary paid to the legal heir of deceased employee is not taxable as salary. The Act is silent on treatment of leave encashment received after death of employee. However, on following grounds, it can be concluded that leave salary received by a legal heir shall not be taxable in the hands of the recipient a) A lump sum payment made gratuitously to widow or legal heir of employee, who dies while in service, by way of compensation or otherwise is not taxable under the head 'Salaries'. [Circular No.573, Dated 21.08.1990] b) Unutilised deposit under the capital gains deposit account scheme shall not be taxable in the hands of legal heir. [Circular No.743 dated 6/5/1996 ] c) Legal representative is not liable for payment of tax on income that has not accrued to the deceased till his death. d) Leave salary paid to the legal heir of deceased employee is not taxable as salary. [Circulars Letter No. F.35/1/65-IT(B), dated 5/11/19 65 ]. Further, leave salary by a legal heir of the Government employee who died in harness is not taxable in the hands of the recipient [Circulars No.309, dated 3/7/1981 ]. Taxpoint: If leave salary becomes due before the death of the assessee (no matter when and by whom received), it shall be taxable in the hands of employee. Whereas if such salary becomes due after the death of assessee, it shall not be taxable (even in the hands of legal heir of the assessee)

Read more at: http://www.caclubindia.com/forum/leave-encashment-salary-sec-10-10aa--239833.asp#.VFScHTSUe0A

Section 10(10A)(i) of the Income-tax Act, 1961—Commutation of pension—Extent of Exemption Clarification regarding

Circular No. 286 dated 17-10-1980, File No. 174/79/80 IT(AI) Central Board of Direct Taxes Bulletin, Vol. XXVI No. 3 page 172.

In the case of government servants who are allowed to retire prematurely and are permitted to be absorved in a public undertaking on or after 24-7-1971, only the lump sum amount not exceeding the commuted value of one third of pension admissible in accordance with the provisions of Civil Pensions (Commutation) Rules, under clause (1)(a) of Rule 37A, would be excluding from the total income under section 10(10A) of the Income-tax Act.

The remaining two-thirds amount received by the person by way of terminal benefit under rule 37A(1)(b) would be includible in the total income subject to relief under section 89(1) of the Income-tax Act, 1961 read with Rule 21A of the Income-tax Rules, 1962. This cannot be regarded as payment in commutation of pension as the same is in lieu of surrender of right to two third of pension. The mere adoption of a formula for calculation of terminal benefit, would not convert its character into that of computed pension, since other ingredients are absent. This position has also been clarified by the Government of India vide its O.M. No. 44(1)-EV/71, dated 13-4-1973.

In cases where entire amount of commuted pension has been exempted under section 10(10A)(i) of the Income-tax Act, 1961 suitable remedial action to revise the assessment preferably u/s 263 may be taken.

[I/1191-CBDT F. No. 174/29/77-IT(AI), dated the 1st July, 1978—CBDT Bulletin Tech. XXIV/170-172.]

In one of the cases the Delhi High Court has relied upon Rule 37A of the Pension Rules, 1972 which provides for payment of lump sum amount to persons absorbed in public sector Corporation. As per this Rule payment of lump sum is made in lieu of pension. In the light of

this any payment under any similar scheme applicable to the members of the civil services of the Union the 'entire amount of commutation was held as exempt under section 10(10A)(i). This decision has been accepted by the Board. The instruction No. 1191 has been withdrawn.

[Circular No. 286 dated 17-10-1980, File No. 174/79/80 IT(AI) Central Board of Direct Taxes Bulletin, Vol. XXVI No. 3 page 172.]

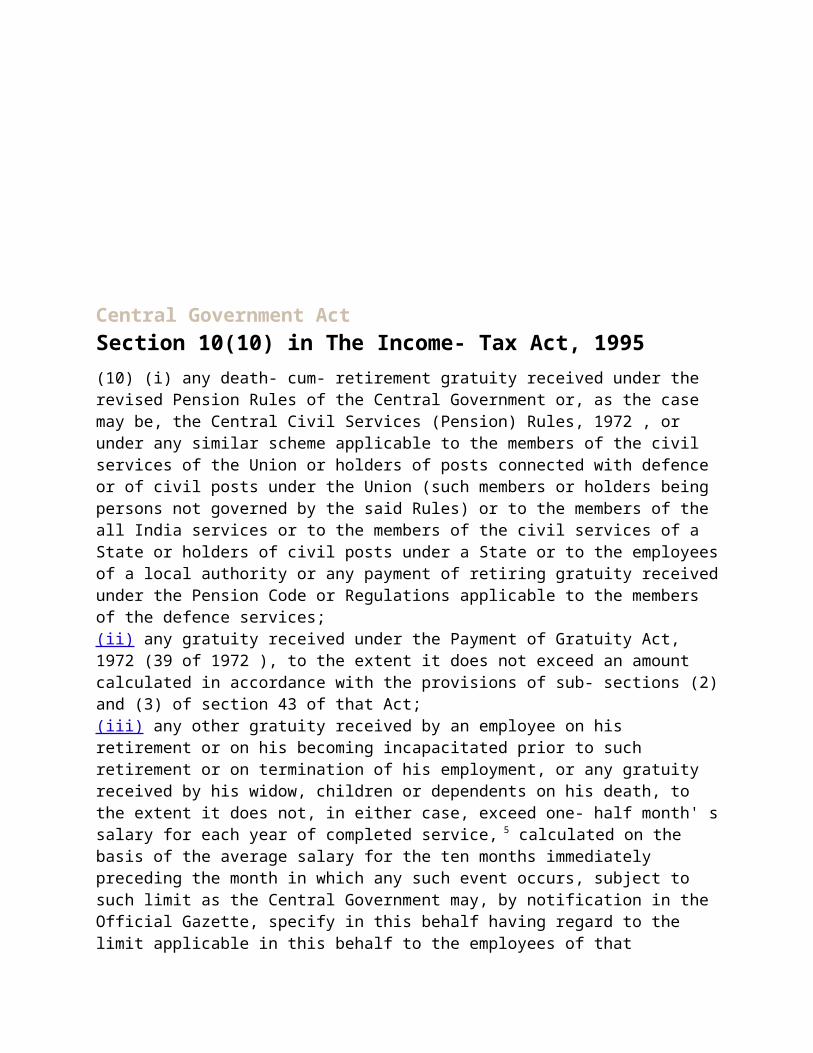

Central Government ActSection 10(10) in The Income- Tax Act, 1995(10) (i) any death- cum- retirement gratuity received under the revised Pension Rules of the Central Government or, as the case may be, the Central Civil Services (Pension) Rules, 1972 , or under any similar scheme applicable to the members of the civil services of the Union or holders of posts connected with defence or of civil posts under the Union (such members or holders being persons not governed by the said Rules) or to the members of the all India services or to the members of the civil services of a State or holders of civil posts under a State or to the employees of a local authority or any payment of retiring gratuity received under the Pension Code or Regulations applicable to the members of the defence services;(ii) any gratuity received under the Payment of Gratuity Act, 1972 (39 of 1972 ), to the extent it does not exceed an amount calculated in accordance with the provisions of sub- sections (2) and (3) of section 43 of that Act;(iii) any other gratuity received by an employee on his retirement or on his becoming incapacitated prior to such retirement or on termination of his employment, or any gratuity received by his widow, children or dependents on his death, to the extent it does not, in either case, exceed one- half month' s salary for each year of completed service, 5 calculated on the basis of the average salary for the ten months immediately preceding the month in which any such event occurs, subject to such limit as the Central Government may, by notification in the Official Gazette, specify in this behalf having regard to the limit applicable in this behalf to the employees of that Government]: Provided that where any gratuities referred to in this clause are received by an employee from more than one employer in the same previous year, the aggregate amount exempt from income- tax under this clause 6 shall not exceed the limit so specified]:

1. Inserted by the Finance (No. 2) Act, 1991, w. e. f 1- 4- 19912. Substituted by the Finance Act, 1974, w. e. f. 1- 4- 1975. Earlier, it was amended by the Finance Act, 1972, w. e. f. 1- 4- 1973 and the Finance Act, 1974 itself w. r. e. f. 1- 6- 1972 1- 4- 1962.5. Substituted for' calculated on the basis of the average salary for the three years immediately preceding the year in which the gratuity is paid, subject to a maximum of thirty- six thousand rupees or twenty months' salary so calculated, whichever is less' by the Direct Tax Laws (Amendment) Act, 1987, w. e. f. 1- 4- 1989. The italicised words were substituted for' thirty thousand' by the Finance Act, 1983, w. r. e. f. 1- 4- 1982.6. Substituted for' shall not exceed thirty- six thousand rupees" by the Direct Tax Laws (Amendment) Act, 1987, w. e. f. 1- 4- 1989. The italicised words were substituted for" thirty thousand' by the Finance Act, 1983, w. r. e. f. 1- 4- 1982.

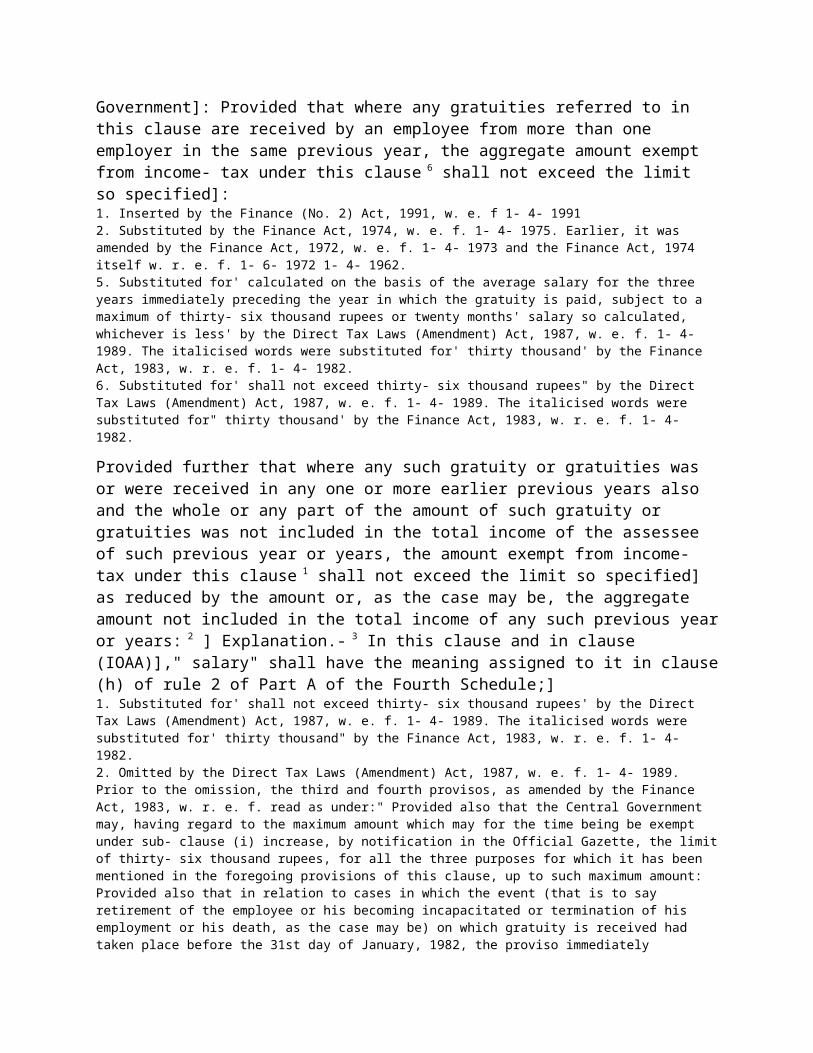

Provided further that where any such gratuity or gratuities was or were received in any one or more earlier previous years also and the whole or any part of the amount of such gratuity or gratuities was not included in the total income of the assessee of such previous year or years, the amount exempt from income- tax under this clause 1 shall not exceed the limit so specified] as reduced by the amount or, as the case may be, the aggregate amount not included in the total income of any such previous year or years: 2 ] Explanation.- 3 In this clause and in clause (IOAA)]," salary" shall have the meaning assigned to it in clause (h) of rule 2 of Part A of the Fourth Schedule;]1. Substituted for' shall not exceed thirty- six thousand rupees' by the Direct Tax Laws (Amendment) Act, 1987, w. e. f. 1- 4- 1989. The italicised words were substituted for' thirty thousand" by the Finance Act, 1983, w. r. e. f. 1- 4- 1982.2. Omitted by the Direct Tax Laws (Amendment) Act, 1987, w. e. f. 1- 4- 1989. Prior to the omission, the third and fourth provisos, as amended by the Finance Act, 1983, w. r. e. f. read as under:" Provided also that the Central Government may, having regard to the maximum amount which may for the time being be exempt under sub- clause (i) increase, by notification in the Official Gazette, the limit of thirty- six thousand rupees, for all the three purposes for which it has been mentioned in the foregoing provisions of this clause, up to such maximum amount: Provided also that in relation to cases in which the event (that is to say retirement of the employee or his becoming incapacitated or termination of his employment or his death, as the case may be) on which gratuity is received had taken place before the 31st day of January, 1982, the proviso immediately preceding this proviso shall not apply and the remaining provisions of this clause shall have effect as if for the words" thirty six thousand rupees", at the three places where they occur, the words" thirty thousand rupees" had been substituted."3. Substituted for" In this clause' by the Direct Tax Laws (Amendment) Act, 1987, w. e. f. 1- 4- 1989.

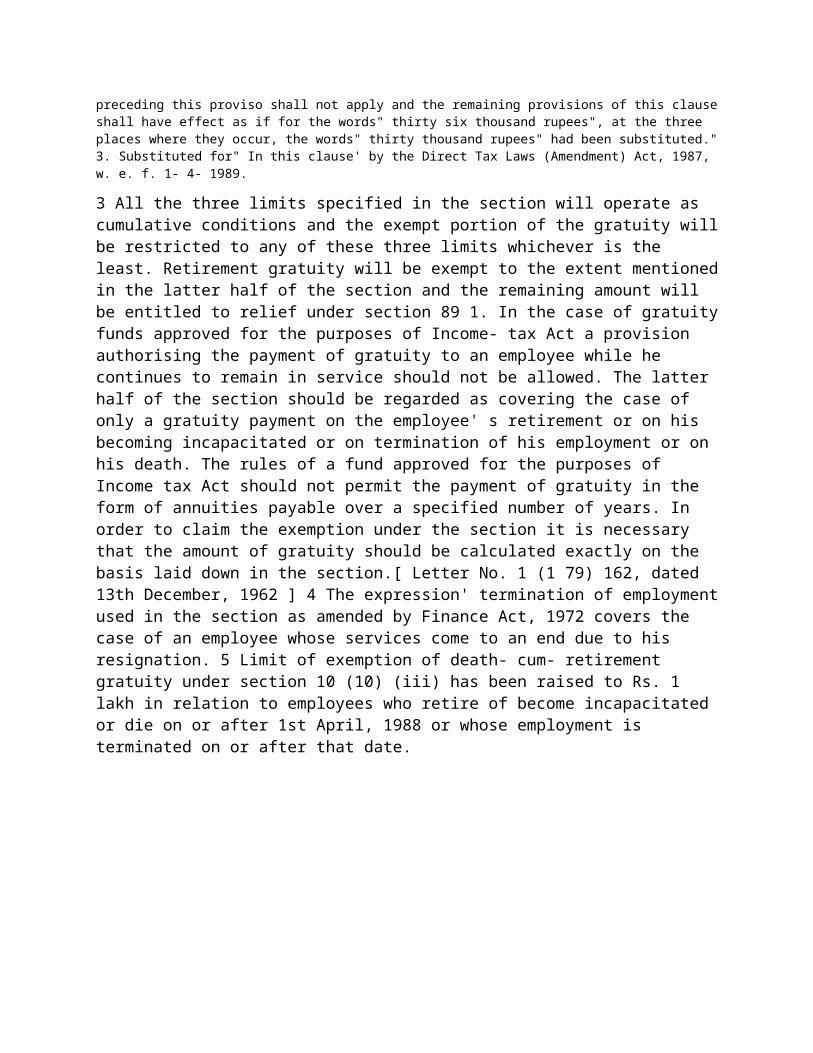

3 All the three limits specified in the section will operate as cumulative conditions and the exempt portion of the gratuity will be restricted to any of these three limits whichever is the least. Retirement gratuity will be exempt to the extent mentioned in the latter half of the section and the remaining amount will be entitled to relief under section 89 1. In the case of gratuity funds approved for the purposes of Income- tax Act a provision authorising the payment of gratuity to an employee while he continues to remain in service should not be allowed. The latter half of the section should be regarded as covering the case of only a gratuity payment on the employee' s retirement or on his becoming incapacitated or on termination of his employment or on his death. The rules of a fund approved for the purposes of Income tax Act should not permit the payment of gratuity in the form of

annuities payable over a specified number of years. In order to claim the exemption under the section it is necessary that the amount of gratuity should be calculated exactly on the basis laid down in the section.[ Letter No. 1 (1 79) 162, dated 13th December, 1962 ] 4 The expression' termination of employment used in the section as amended by Finance Act, 1972 covers the case of an employee whose services come to an end due to his resignation. 5 Limit of exemption of death- cum- retirement gratuity under section 10 (10) (iii) has been raised to Rs. 1 lakh in relation to employees who retire of become incapacitated or die on or after 1st April, 1988 or whose employment is terminated on or after that date.

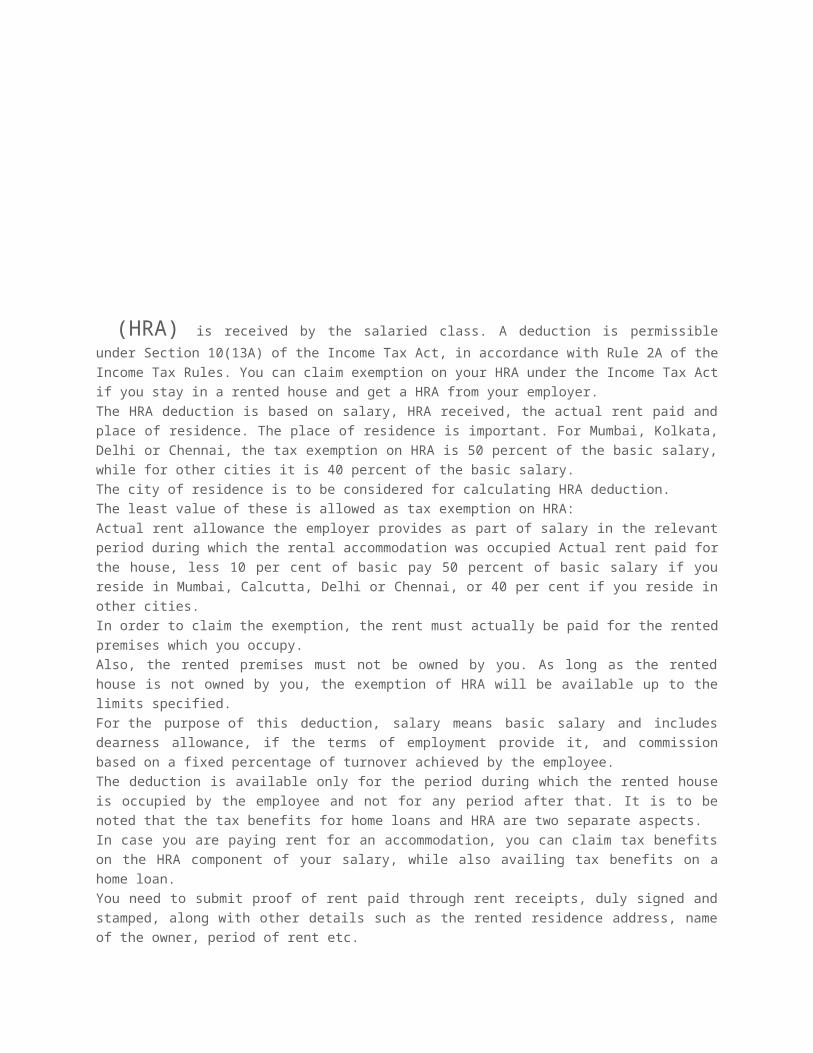

(HRA) is received by the salaried class. A deduction is permissible under Section 10(13A) of the

Income Tax Act, in accordance with Rule 2A of the Income Tax Rules. You can claim exemption on your

HRA under the Income Tax Act if you stay in a rented house and get a HRA from your employer.

The HRA deduction is based on salary, HRA received, the actual rent paid and place of residence. The

place of residence is important. For Mumbai, Kolkata, Delhi or Chennai, the tax exemption on HRA is 50

percent of the basic salary, while for other cities it is 40 percent of the basic salary.

The city of residence is to be considered for calculating HRA deduction.

The least value of these is allowed as tax exemption on HRA:

Actual rent allowance the employer provides as part of salary in the relevant period during which the

rental accommodation was occupied Actual rent paid for the house, less 10 per cent of basic pay 50

percent of basic salary if you reside in Mumbai, Calcutta, Delhi or Chennai, or 40 per cent if you reside in

other cities.

In order to claim the exemption, the rent must actually be paid for the rented premises which you occupy.

Also, the rented premises must not be owned by you. As long as the rented house is not owned by you,

the exemption of HRA will be available up to the limits specified.

For the purpose of this deduction, salary means basic salary and includes dearness allowance, if the

terms of employment provide it, and commission based on a fixed percentage of turnover achieved by the

employee.

The deduction is available only for the period during which the rented house is occupied by the employee

and not for any period after that. It is to be noted that the tax benefits for home loans and HRA are two

separate aspects.

In case you are paying rent for an accommodation, you can claim tax benefits on the HRA component of

your salary, while also availing tax benefits on a home loan.

You need to submit proof of rent paid through rent receipts, duly signed and stamped, along with other

details such as the rented residence address, name of the owner, period of rent etc.

How it applies :-For example, assume one earns a basic salary of Rs 20,000 per month and rents a flat

in Mumbai for Rs 5,000 per month. His actual HRA is Rs 8,000. He is eligible for 50 percent of the basic

pay for HRA exemption.

Least of:

Actual HRA received – Rs 8,000

50 percent of basic salary – Rs 10,000

Excess of rent paid over 10 percent of salary, i.e., Rs 5,000 less Rs 2,000 – Rs 3,000.

As such, Rs 3,000 per month is the least and will be the exemption allowable for HRA deduction.- See more at: http://taxguru.in/income-tax/deduction-under-section-1013a-for-house-rent-allowance.html#sthash.ulqJfmQ8.dpuf

Voluntary Retirement – Assessee can claim both exemption u/s 10(10C) & rebate u/s 89 The assessee is entitled to the exemption under section 10(10C) of the Act and also rebate under section 89 of the Act in respect of the amount received in excess of Rs.5,00,000 on account of voluntary retirement. Thus their Lordships have held that the assessee, who opts for voluntary retirement, is not only entitled to exemption under section 10(10C) but also rebate under section 89 of the Income Tax Act. Similar view is taken by the Hon’ble Karnataka High Court in the case of CIT v. P. Surendra Prabhu (supra) wherein their Lordships held as under : That the assessee, employee of the respondent bank was not only entitled to the benefit of exemption under section 10(10C) of the Act to the extent prescribed in the provision itself but for any amount over and above the prescribed limit; under the aforesaid provision, the assessee was also entitled to relief under section 89(1) of the Act read with rule 21A. INCOME TAX APPELLATE TRIBUNAL, CHANDIGARH ITA No. 507/Chd/2012 – Assessment Year: 2007-08 Shri Manmohan Singh Bedi v. A.C.I.T. Date of Pronouncement: 26.07.2012 ORDER PER T.R. SOOD, A.M In this appeal the assessee has raised the following ground: “That on facts and circumstances of the case, the ld. CIT(A) was not justified in upholding the disallowance of exemption u/s 10(10C) of the Income-tax Act.” 2. The appeal has been filed late by 541 days. The assessee has filed an application for condonation of delay which is duly supported by the affidavit. The ld. counsel of the assessee referred to the application and pointed out that originally the assessee has filed return declaring income of Rs. 13,10,521/- on which

total tax due including interest was Rs. 80,950/-. Later on this return was revised declaring total income of Rs. 8,10,521/- after claming deduction u/s 10(10C) amounting to Rs. 5.00 lakhs and total tax remained only at Rs. 50,369/-. However, the Assessing Officer did not allow the deduction u/s 10(10C) of the Act. Accordingly rectification application was moved for allowing deduction u/s 10(10C). The rectification application was rejected vide Rectification order dated 16.2.2010 on which tax due was determined at Rs. 80,954/-. The assessee was advised not to file the appeal because total benefit which the assessee could have received was less than Rs. 30,000/- and the assessee was advised that after paying fee to the Tribunal and Advocate Fee 2 nothing would be gained. Accordingly no appeal was filed. However, later on the Assessing Officer passed another rectification order u/s 154 on 6.3.2012 in which net tax payable was shown at Rs. 3,43,607/-. When such a huge demand was raised then the assessee was left with no option but to file appeal before the Tribunal. Therefore, the appeal was filed late because of the sufficient cause and the same may be condoned particularly in view of the fact that the issue raised in appeal is covered in favour of the assessee. 3. On the other hand, the ld. DR for the revenue submitted that once the assessee had accepted the decision by not filing any appeal then later on the same could not be made as reason for explaining the delay. 4. We have heard the rival submissions carefully and we are satisfied that the assessee had a sufficient cause for not filing the appeal in time. The assessee being an employee might have initially accepted the decision of the Department because additional tax payable was only Rs. 30,000/- to avoid litigation expenses. However, the demand has been increased to Rs. 3,43,607/- vide Rectification order dated 6.3.2012 then the assessee was forced to file the appeal. We are of the opinion that this is reasonable and sufficient cause for filing the appeal late and accordingly we condone the delay. 5. As far as the merits of the case are concerned, we find that the issue is squarely covered in favour of the assessee by the order of the Tribunal in case of Shri Bikran Jit Passi V DCIT dated 9.11.2011, ITA NO. 925/Chd/2011 A.Y 2008-09. In this case the Tribunal has held as under:- “”The present appeal filed by the assessee is directed against the order, dated 14.07.2011 of the ld. CIT(A) Panchkula passed u/s 250(6) of the Income-tax Act,1961 (in short hereinafter referred to as ‘the Act’) 2. The assessee has raised the following grounds of appeal : “1. That the ld. CIT(A) has erred in law in upholding the withdrawal of exemption of Rs.5,00,000/- claimed under Section 10(10C) of the Act which is arbitrary and unjustified. 2. That the ld. CIT(A) has further erred in law as well as on facts in holding that the ‘Exit Option Scheme” does not satisfy the conditions laid under Section 10(10C) read with rule 2BA which is incorrect and as such the exemption withdrawn and upheld is wholly unwarranted. 3. That the order of the ld. CIT(A) is erroneous, arbitrary, opposed to law and facts of the case and is, thus untenable.” 3. The facts of the case in brief are that the assessee Bikram Jit Passi filed return of income, on 11.08.2008 for the assessment year 2008-09. During the course of assessment proceedings, the AO noted that the assessee had claimed exemption u/s 10(10C) of the Act amounting to Rs.5,00,000/-. The AO disallowed the claim of the assessee’s as not being eligible for exemption u/s 10(10C) of the Act. 4. The CIT(A) upheld the order of the AO. The relevant findings of the CIT(A) are as under : “Keeping in view the clear conditions in the scheme regarding filling up of vacancies caused by the release of officers and the confirmation by the Bank at point No.10 above that the scheme does not comply with Section 10(10C) of the IT Act and is not approved by Income Tax Department conditions No. (iii) & (iv) of Rule 2BA are violated. Therefore, the scheme is not eligible for exemption under Section 10(10C) of the IT Act,1961. As a result, the assessees are not held eligible for exemption u/s 10(10C) of the Act.” 5. We have heard both the parties and carefully perused and considered the facts of the appeal. The ld. ‘AR’ placed reliance, on the decision, in the case of Pandya Vinod Chandra Bhogilae V ITO (2010) 045 DTR 105 ITAT, Ahmedabad, to state that the fact- situation of the present appeal is squarely covered by the decision. Having considered the decision, we found that the same is applicable to the facts of the present cases. The relevant and operative part of the decision is reproduced hereunder : “2. Thus the only issue involved in this appeal is about allowability of exemption under section 10(10C) of the Income Tax Act, 1961. 3. The facts of the case are that assessee is a Deputy Manager in SBI and has taken VRS on 31-5-2006 under exit option scheme introduced by the bank of India with effect from 7-5-2005. The assessee

received salary and pension amounting to Rs.3,81,894 (including exgratia). On examination of Form No.16 the Assessing Officer noticed that assessee received exgratia of Rs.3,07,236 on VRS. He claimed exemption under section 10(10C) of the Act. The Assessing Officer disallowed the claim by following circular No. Chief CIT, Baroda letter BRD/Chief CIT/Tech/MICS/10(10C)/2009-10, dated 17-6-2006. The assessee relied on the decision of Tribunal, Kolkata in the case of Dy.CIT v. Krishna Gopal Saha (2009) 29 DTR (Kol)(TM)(Trib) 385 but the learned Assessing Officer did not agree and made the addition. The learned Commissioner (Appeals) also confirmed the disallowance by trying to distinguish the decision of Third Member in Dy.CIT v. Krishna Gopal Sahas case (supra). 4. We have heard the parties and perused the material on record. In our considered view the distinction cited by the learned Commissioner (Appeals) is not sound and does not stand to reason. The only basis for not allowing the claim has been that scheme for VRS is not in accordance with rule 2BA. However,, it has not been pointed out how the employer has not framed the scheme in accordance with rule 2BA. Earlier till 2002 schemes were required to be approved by the Chief Commissioner but thereafter such requirement has been dispensed with and, therefore, it is only for the employer to frame the scheme for VRS or for earlier exit option. If Assessing Officer had any doubt about the scheme he could have enquired from the employer. So far as the assessee employee is concerned, he cannot be penalized and tax will be levied on him on the assumption that the scheme framed by employer is not in accordance with rule 2BA. In any case, the judgment of Third Member in Dy.CIT v. Krishna Gopal Saha (supra) is clearly applicable and we do not find any reason to take a different view. For the sake of convenience we refer to following para from the Third Member judgment in Dy.CIT v. Krishna Gopal Sahas case (supra) as under: 5. At the time of hearing before me, none appeared on behalf of the assessee-respondent. I have, therefore, heard the learned department Representative and perused the material placed before me. I find that the issue has been considered by the Hon’ble jurisdictional High Court in the case of SAIL DSP VR Employees Association 1998 v. Union of India (supra) in which their Lordships held as under : Section 10(10C) of the Income Tax Act, 1961, uses the expression any amount received by an employee…. At the time of his voluntary retirement in accordance with any scheme or schemes of voluntary retirement…. if a plain literal interpretation of statutory provision produced a manifestly absurd and unjust result, which the legislature could not have intended, the court is supposed to modify the language used by the legislature even to do some violence to it so as to achieve the obvious intention of the legislature and produce a rational construction. An expression used in the statute is not always to be interpreted literally or grammatically. Sometimes it has to be interpreted having regard to the context in which the expression is used and having regard to the object and purpose for which the same is enacted. Sec.10(10C) was inserted in order to make voluntary retirement attractive so as to reduce human complements for securing economic viability of certain companies. This object was elaborated by various departmental circulars and explanatory statements issued from time to time. Similarly, rule 2BA of the Income Tax Rules, 1962, which was inserted by IT (Sixteenth Amendment) Rules, 1962, was amended from time to time. All these go to show that this was intended to make voluntary retirement more attractive and beneficial to the employee opting for voluntary retirement. Therefore, this has to be interpreted in a manner beneficial to the optee for voluntary retirement, if there is any ambiguity. Sums paid on voluntary retirement to the extent of rupees five lakhs are exempted from being charged to tax by reason of section 10(10C). Even if the payment is stretched over a period of years, the same would not become chargeable to tax in any subsequent assessment year. From the above it is evident that their Lordships of the jurisdictional High Court held that an employee, who takes voluntary retirement, is entitled to deduction under section 10(10C) even if the payment is stretched over a period of years. They have also held that provision of section 10(10C) should be interpreted in a manner beneficial to the optee for voluntary retirement. It may be pointed out that in the above-mentioned case, the employer i.e. SAIL was of the opinion that the employees were not entitled to exemption under section 10(10C) and accordingly, SAIL had been deducting tax at source on the amount paid under their voluntary retirement scheme. The facts are similar in the assesses case, because in the case of the assessee also, the employer believing that the assessee

is not entitled to deduction under section 10(10C) has deducted tax at source on the amount paid on voluntary retirement. The facts being identical, the above decision of Hon’ble jurisdictional High Court would be squarely applicable to the case under appeal before the Tribunal. 6. Similarly, Hon’ble Bombay High Court in the case of CIT v. Nagesh Devidas Kulkarni (supra) held as under : The assessee is entitled to the exemption under section 10(10C) of the Act and also rebate under section 89 of the Act in respect of the amount received in excess of Rs.5,00,000 on account of voluntary retirement. Thus their Lordships have held that the assessee, who opts for voluntary retirement, is not only entitled to exemption under section 10(10C) but also rebate under section 89 of the Income Tax Act. Similar view is taken by the Hon’ble Karnataka High Court in the case of CIT v. P. Surendra Prabhu (supra) wherein their Lordships held as under : That the assessee, employee of the respondent bank was not only entitled to the benefit of exemption under section 10(10C) of the Act to the extent prescribed in the provision itself but for any amount over and above the prescribed limit; under the aforesaid provision, the assessee was also entitled to relief under section 89(1) of the Act read with rule 21A. 6. From the above it is evident that while the learned AM relied upon the decision of Hon’ble Madras High Court in the case of CIT v. M.Chelladurai & Ors. (2009) 317 ITR 370(Mad) : (2009) 176 Taxman 31, he has not taken into account the decisions of other High Courts including the jurisdictional High Court. The Hon’ble jurisdictional High Court under the identical facts held the assessee, i.e., the retired employee, to be entitled to deduction under section 10(10C). Similar view is taken by Hon’ble Bombay as well as Karnataka High Courts. The decision of Hon’ble jurisdictional High Court is binding upon us and moreover if two views are possible, while interpreting the provision, a view which is favourable to the assessee has to be adopted. Hon’ble jurisdictional High Court in the above- referred case of SAIL DSP VR Employees Association 1998 v. Union of India (supra) has also held that the provisions of section 10(10C) are to be interpreted liberally in a manner which is beneficial to retired employees in view of the above. I respectfully following the decisions of Hon’ble jurisdictional High Court, Bombay High Court and Karnataka High Court agree with the learned JM and hold that the assessee is entitled to exemption under section 10(10C) to the extent of Rs.5 lakhs.” Respectfully following the above decision of the Tribunal, we allow the claim of assessee.” 6. The issue in question is covered by the decision of the Hon’ble Tribunal, as reproduced above. The assessee/appellant was also employed in the State Bank of India. Respectfully following the said decision, the appeal is decided in favour of the assessee.” 6. Following the above decision we decide the issue in favour of the assessee. 7. In the result, appeal filed by the assessee is allowed. - See more at: http://taxguru.in/income-tax-case-laws/assessee-opts-voluntary-retirement-claim-exemption-1010c-rebate-89.html#sthash.83l9QvT3.dpuf

Tax on perquisite In recent times a large number of foreign companies have been deputing their employees to India for employment. These individuals are liable to pay Income tax on their earnings in India. At the same time, they could also be liable to pay tax in their home country, depending on their home country tax laws. To mitigate their hardship taxes are paid by the employers on behalf of their employees. Such payments are in the nature of perquisite in the hands of employees, which is reasonably settled matter. However, the litigation exists for a long in respect of treatment of this payment as a monetary or non-monetary perquisite.

Recently, Income Tax Appellate Tribunal, Delhi ruled that the income tax that an employer pays on behalf of its employee is a non-monetary benefit and exempt from tax under section 10(10CC) of the Income Tax Act. In the discussion to follow, the relevant provisions of the Act are analyzed in the light of aforementioned ruling of the tribunal.Perquisites under the Act

Section 2(24) of the Income Tax Act, 1961 deals with the perquisites under the definition of 'Income'. Perquisite is an advantage received by the holder of an office over and above the salary. Any benefit received incidental to employment in excess of salary is a Perquisite. Perquisite postulates relationship of employer and employee.[Shalilendra Kumar v.Union of India (1989) 175 ITR 494 (All.).

Tax on 'tax perquisite' paid by the employer If an employer paid the tax on behalf of an employee, which is otherwise payable by the employee is considered as taxable perquisite. However, under section 10(10CC) of the Income Tax Act, 1961, an employer has been given an option to pay tax on the whole or part of the value of perquisite on behalf of employee without deduction of it from the salary of an employee. When the tax actually paid by an employer as non-monetary perquisite, it is not taxable in the hands of employees. Such tax payment is not allowable as business expenditure in the tax assessment of an employer. But the exemption is available only on non-monetary perquisite paid by the employer. In the case of RBF Rig Corporation LLC (RBFRC) v. CIT( 2007 ) 165 Taxman 101(Delhi), Delhi Tribunal held that if tax on salary is paid by the employer on behalf of employee, it is a perquisite provided for by way of non-monetary payment and therefore, exemption under the provisions of Sec. 10(10CC) will be applicable.

It is almost a settled matter that tax payment by the employer on behalf of employees is in the nature of perquisite in the hands of the employee. But whether this is a monetary or non-monetary perquisite, has been a matter of litigation for long time. The issue assumed significance after insertion of section 10(10CC) in the Income Tax Act, 1961. Accordingly, tax paid by the employer on behalf of the employee on non-monetary perquisite which is exempt from tax in the hands of employees. In this regard, it is pertinent to note that under section 200 of the Companies Act, 1956 registered companies are prohibited from making payment of remuneration free of any tax to its employees and officers.

Recent case before Delhi Tribunal In a recent case, Triton Holdings Limited v. Deputy Director of Income Tax, Deharadun (ITA No.2541-Delhi-2009) , ITAT, Delhi held that tax paid by the employer on behalf of their employees must be treated as non-monetary perquisite for claiming exemption under section 10(10CC) of the Income Tax Act, 1961. Further tribunal held that this payment is subject to one stage grossing up only while computing the salary of employees.

In this case, employees of a company known as 'Triton Holdings Limited' claimed the income tax paid on their behalf by their employer as a non-monetary perquisite and further claimed it as an exemption under section 10(10CC) of the Income Tax Act, 1961. However, the Assessing Officer did not accept this view and contended that tax perquisite is subject to multiple grossing up and clubbing with the taxable income of the employees and no exemption could be allowable under section 10(10CC) of the Income Tax Act.

Issues for decision

The tribunal had to consider a issue of whether tax perquisite provided to the employees should be subject to multiple grossing up or should it be considered as a non-monetary perquisite for the

purpose of claiming exemption u/s 10(10CC) of the Income Tax Act or not in the backdrop of earlier decision of its special bench in RBF Rig Corporation LLC (RBRC) v. CIT( 2007 ) 165 Taxman 101(Delhi).

The Tribunal’s DecisionIn this case after hearing both sides, Delhi Income Tax Appellate Tribunal held that the tax perquisite constituted as a non-monetary perquisite in the hands of the employees, by placing reliance on the earlier decision of Special Bench. Accordingly, an exemption under section 10(10CC) was available in respect of the tax payment and the appeal was disposed off without ordering for refund of appeal fee. If the Commissioner of Income Tax (Appeals) had followed the order of the special bench in RBF Rig Corporation case, the unwarranted appeal would not have arisen. At the same time, as the Commissioner of Income Tax (Appeals) had not any intention to harass the appellant or cause any monetary loss to the assessee, no costs had been awarded by the tribunal.

Conclusion

This ruling reiterates the principle pronounced in the case of RBF Rig Corporation that the tax paid by the employer in respect of salary paid to the employees would constitute non-monetary perquisite in the hands of the employees, eligible for exemption under section 10(10CC) of the Income Tax Act,1961 and the payment must be subject to single stage grossing up while computing the taxable salary income of the employees. However, a challenge to the ruling by the department in a High Court cannot be ruled out.

![INCOME FROM HOUSE PROPERTY - Income Tax …. Income-from-House... · [As amended by Finance Act, 2018] INCOME FROM HOUSE PROPERTY Income chargeable to tax under the head “house](https://static.fdocuments.in/doc/165x107/5b67e9b87f8b9af77c8bf7bd/income-from-house-property-income-tax-income-from-house-as-amended-by.jpg)

![Income from · PDF fileIncome from Salaries ... Sections of Income Tax Act 1961(herein referred to the Act) governing Income from Salary . ... Deductions [Section 16]](https://static.fdocuments.in/doc/165x107/5aade0757f8b9a190d8b6d85/income-from-from-salaries-sections-of-income-tax-act-1961herein-referred-to.jpg)