Inbound & OutboundInvestments - baroda-icai.org · Inbound & OutboundInvestments Baroda Branch of...

187

Inbound & Outbound Investments Baroda Branch of WIRC of ICAI Saturday, May 7, 2017 By: CA Shardul Dilip Shah www.mashahca.com

Transcript of Inbound & OutboundInvestments - baroda-icai.org · Inbound & OutboundInvestments Baroda Branch of...

Inbound & Outbound InvestmentsBaroda Branch of WIRC of ICAI

Saturday, May 7, 2017By: CA Shardul Dilip Shah

www.mashahca.com

Considerations• Tax Treaty Network• Repatriation of Income• Capital Gain Tax on Exit• Controlled Foreign Corporation Rules• GAAR• Thin Capitalisation• Corporate Laws• Setting up & maintenance Costs• Funding Options• Other Directives / Incentives• Ease of winding up• Exchange Control Regulations

www.mashahca.com

Inbound Investments - background

• Foreign Direct Investments at the end of February 2016 were USD 37 Billion, compared to USD 31 Billion over the previous 12 month period of 2014-15

• Inflation rate is going down gradually• India’s economic growth is expected to rise to

7.6% in 2016-17

www.mashahca.com

Doing business in India• Just got easier – new de-licensing and deregulation

measures are reducing complexity, and significantly increasing speed and transparency.

• Process of applying for Industrial License & Industrial Entrepreneur Memorandum made online on 24×7 basis through eBiz portal.

• Validity of Industrial license extended to three years.• States asked to introduce self-certification and third party

certification under Boilers Act.• Major components of Defense products’ list excluded from

industrial licensing.• Dual use items having military as well as civilian

applications deregulated.

www.mashahca.com

Doing business in India• Services of all Central Govt. Departments & Ministries are integrated with

the eBiz – a single window IT platform for services by 31 Dec.• Process of obtaining environmental clearances made online.• Following advisories sent to all Departments/ State Governments to

simplify and rationalize regulatory environment.• All returns should be filed on-line through a unified form.• A check-list of required compliances should be placed on

Ministry’s/Department’s web portal.• All registers required to be maintained by the business should be replaced

with a single electronic register.• No inspection should be undertaken without the approval of the Head of

the Department.• For all non-risk, non-hazardous businesses a system of self-certification to

be introduced.

www.mashahca.com

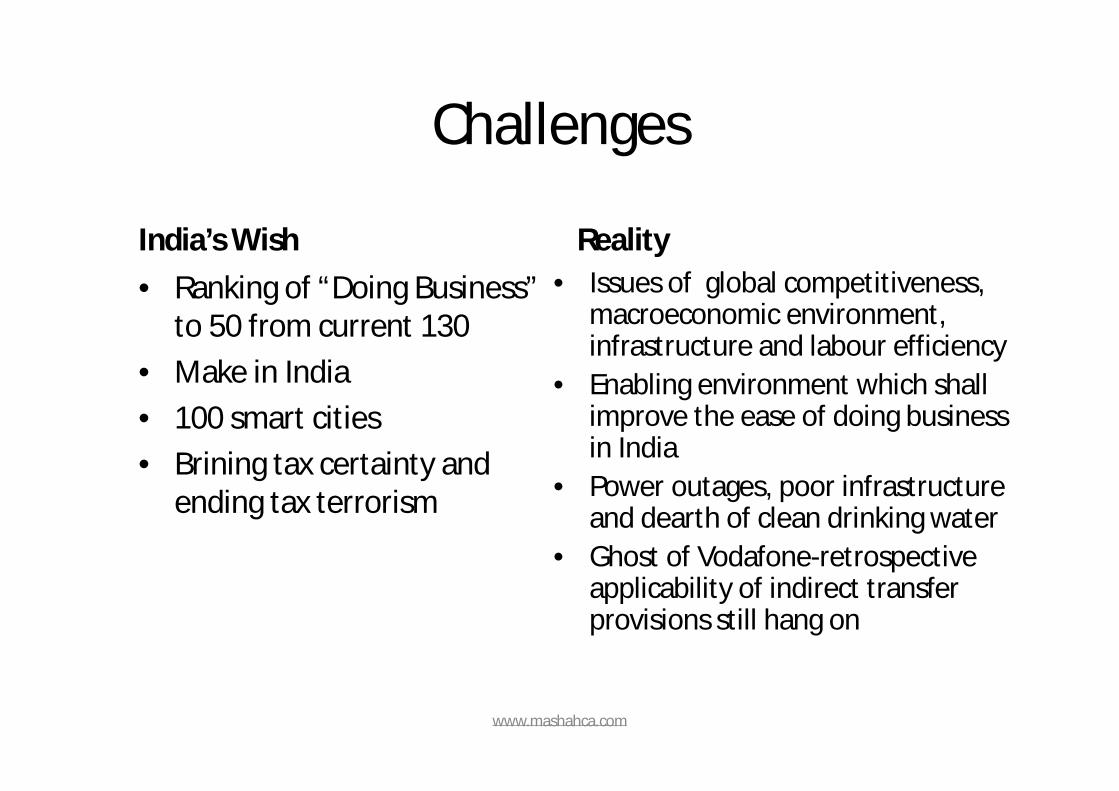

Challenges

India’s Wish• Ranking of “Doing Business”

to 50 from current 130• Make in India• 100 smart cities• Brining tax certainty and

ending tax terrorism

Reality• Issues of global competitiveness,

macroeconomic environment, infrastructure and labour efficiency

• Enabling environment which shall improve the ease of doing business in India

• Power outages, poor infrastructure and dearth of clean drinking water

• Ghost of Vodafone-retrospective applicability of indirect transfer provisions still hang on

www.mashahca.com

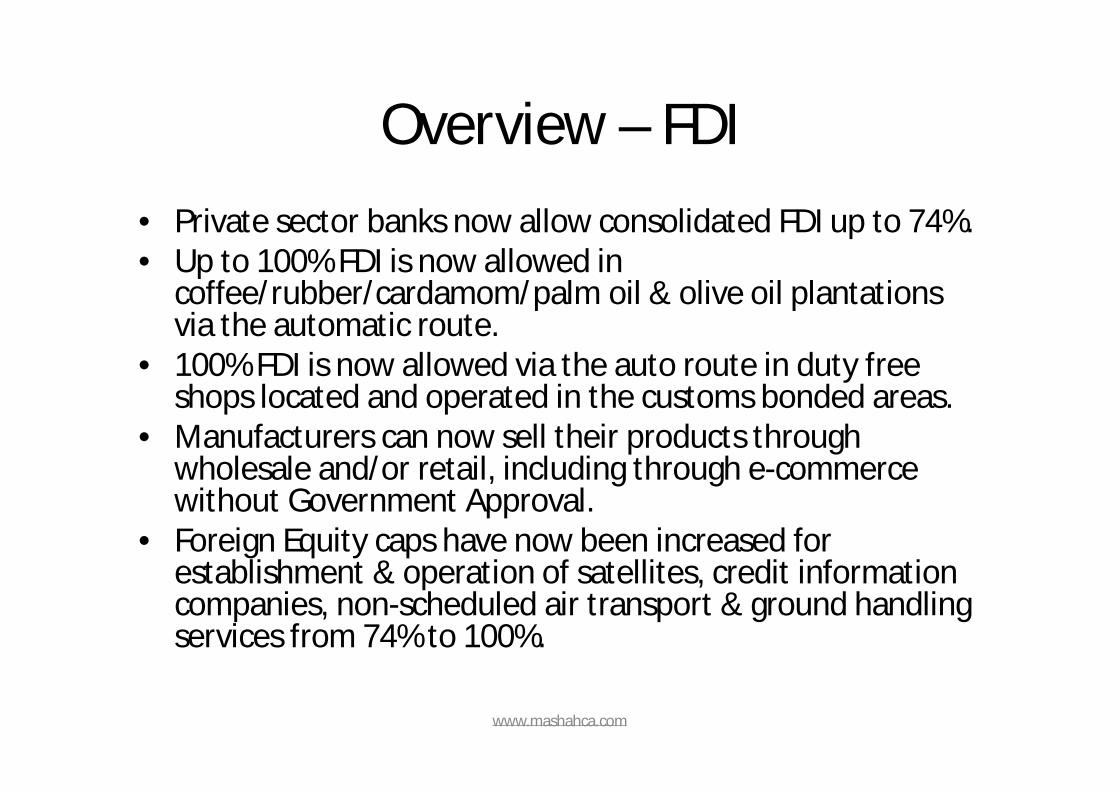

Overview – FDI• Government eases FDI norms in 15 major sectors.• Townships, shopping complexes & business centres –

all allow up to 100% FDI under the auto route. Conditions on minimum capitalisation & floor area restrictions have now been removed for the construction development sector.

• India's defence sector now allows consolidated FDI up to 49% under the automatic route. FDI beyond 49% will now be considered by the Foreign Investment Promotion Board. Govt approval route will be required only when FDI results in a change of ownership pattern.

www.mashahca.com

Overview – FDI• Private sector banks now allow consolidated FDI up to 74%.• Up to 100% FDI is now allowed in

coffee/rubber/cardamom/palm oil & olive oil plantations via the automatic route.

• 100% FDI is now allowed via the auto route in duty free shops located and operated in the customs bonded areas.

• Manufacturers can now sell their products through wholesale and/or retail, including through e-commerce without Government Approval.

• Foreign Equity caps have now been increased for establishment & operation of satellites, credit information companies, non-scheduled air transport & ground handling services from 74% to 100%.

www.mashahca.com

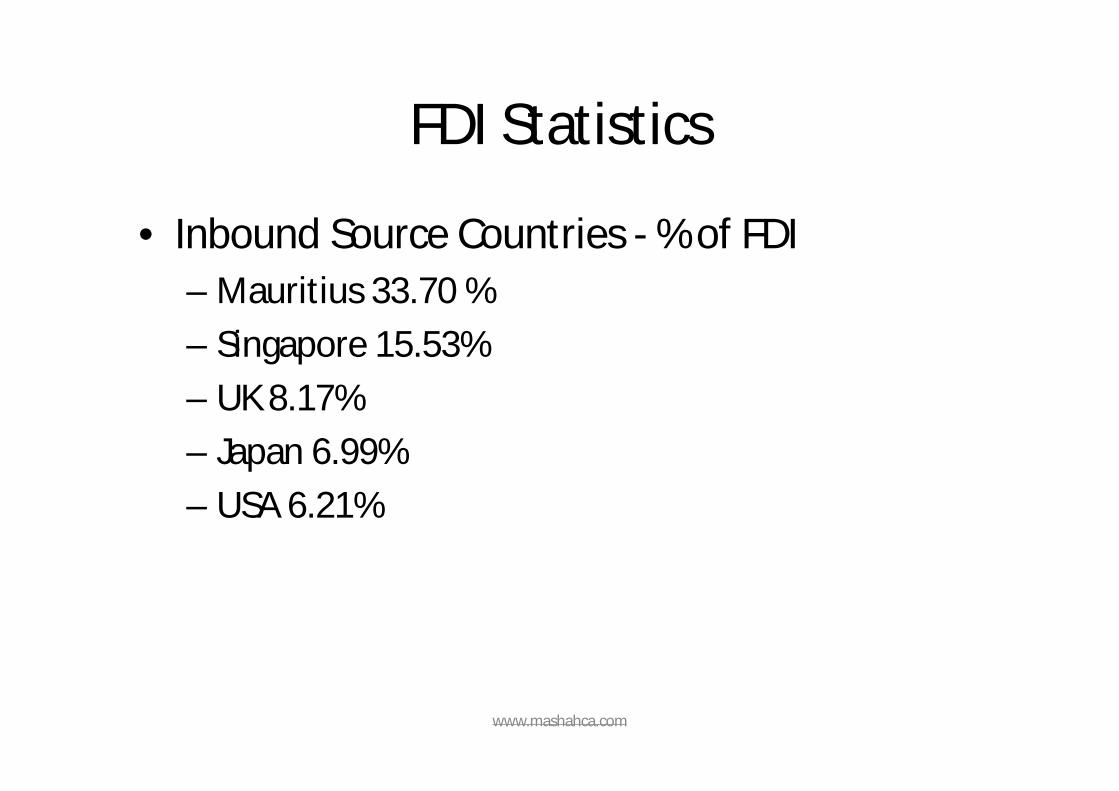

FDI Statistics

• Inbound Source Countries - % of FDI– Mauritius 33.70 %– Singapore 15.53%– UK 8.17%– Japan 6.99%– USA 6.21%

www.mashahca.com

Ranking CompanyOver all Funding Rank

2015 Growth Rank

Mindshare Rank

Employee Growth Rank

Website

1 Snapdeal 2 1 5 47 http://snapdeal.com

2 Ola 3 2 14 32 http://olacabs.com

3 Flipkart 1 3 9 56 http://flipkart.com

4 Bigbasket 18 4 58 1 http://bigbasket.com

5 Delhivery 11 5 31 28 http://delhivery.com

6 OYORooms 10 6 1 10 http://oyorooms.com

7 Zomato 7 7 18 77 http://zomato.com

8 Swiggy 57 8 94 39 http://swiggy.in

9 Practo 12 9 27 49 http://practo.com

10 Paytm 4 10 12 30 http://paytm.com

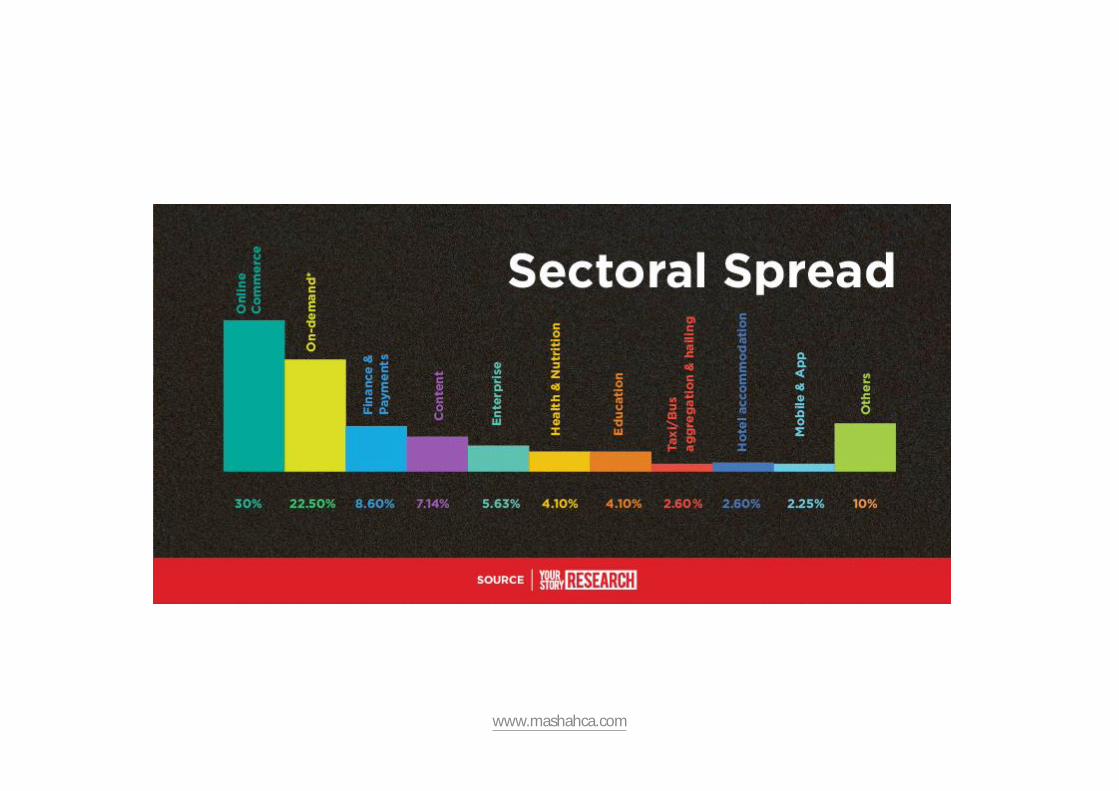

The top 10 Indian startups with a gravity defying momentum in 2015

www.mashahca.com

Overview – Foreign Direct Investments into India

• 100% FDI allowed in medical devices• FDI cap increased in insurance & sub-activities from 26% to 49%• FDI up to 49% has been permitted in the Pension Sector.• Construction, operation and maintenance of specified activities of Railway sector

opened to 100% foreign direct investment under automatic route.• FDI policy on Construction Development sector has been liberalised by relaxing the

norms pertaining to minimum area, minimum capitalisation and repatriation of funds or exit from the project. To encourage investment in affordable housing, projects committing 30 percent of the total project cost for low cost affordable housing have been exempted from minimum area and capitalisation norms.

• Investment by NRIs under Schedule 4 of FEMA (Transfer or Issue of Security by Persons Resident Outside India) Regulations will be deemed to be domestic investment at par with the investment made by residents.

• Composite caps on foreign investments introduced to bring uniformity and simplicity is brought across the sectors in FDI policy.

• 100% FDI allowed in White Label ATM Operations.

www.mashahca.com

Inbound Investments - Sectors

• Services Sector 17%• Telecommunication 7%• Computers 6%• Construction Development 10%• Drug & Pharma 55%• Others 5 %

www.mashahca.com

Sectors requiring GOI Approval• Tea sector, including plantations – 100%.• Mining and mineral separation of titanium-bearing minerals and ores, its value addition and

integrated activities -100%.• FDI in enterprise manufacturing items reserved for small scale sector – 100%.• Defence – up to 49% under FIPB/CCEA approval, beyond – 49% under CCS approval (on a case-to-

case basis, wherever it is likely to result in access to modern and state-of-the-art technology in the country).

• Teleports (setting up of up-linking HUBs/Teleports), Direct to Home (DTH), Cable Networks (Multi-system operators operating at National or State or District level and undertaking upgradation of networks towards digitalisation and addressability), Mobile TV and Headend-in-the Sky Broadcasting Service(HITS) – beyond 49% and up to 74%.

• Broadcasting Content Services: uplinking of news and current affairs channels – 26%, uplinking of non-news and current affairs TV channels – 100%.

• Publishing/printing of scientific and technical magazines/specialty journals/periodicals – 100%.• Print media: publishing of newspaper and periodicals dealing with news and current affairs- 26%,

Publication of Indian editions of foreign magazines dealing with news and current affairs- 26%.• Terrestrial Broadcasting FM (FM Radio) – 26%.

www.mashahca.com

Sectors requiring GOI Approval• Publication of facsimile edition of foreign newspaper – 100%.• Airports – brownfield – beyond 74%.• Non-scheduled air transport service – beyond 49% and up to 74%.• Ground-handling services – beyond 49% and up to 74%.• Satellites – establishment and operation - 74%.• Private securities agencies – 49%.• Telecom-beyond 49%.• Single brand retail – beyond 49%.• Asset reconstruction company – beyond 49% and up to 100%.• Banking private sector (other than WOS/Branches) – beyond 49% and up

to 74%, public sector – 20%.• Insurance - beyond 26% and up to 49%.• Pension Sector - beyond 26% and up to 49%.• Pharmaceuticals – brownfield – 100%.

www.mashahca.com

Entry Structures• INCORPORATING A COMPANY IN INDIA:• It can be a private or public limited company. Both wholly owned & joint

ventures are allowed. Private limited company requires minimum of 2 shareholders.

• LIMITED LIABILITY PARTNERSHIPS: Allowed under the Government route in sectors which has 100% FDI allowed under the automatic route and without any conditions.

• SOLE PROPRIETORSHIP/PARTNERSHIP FIRM: Under RBI approval. RBI decides the application in consultation with Government of India.

• EXTENSION OF FOREIGN ENTITY: Liaison office, Branch office (BO) or Project Office (PO). These offices can undertake only the activities specified by the RBI. Approvals are granted under the Government and RBI route. Automatic route is available to BO/PO meeting certain conditions.

• OTHER STRUCTURES: Foreign investment or contributions in other structures like not for profit companies etc. are also subject to provisions of Foreign Contribution Regulation Act (FCRA).

www.mashahca.com

Steps Involved• Identification of structure• Central Government approval if required• Setting up or incorporating the structure• Inflow of funds via eligible instruments and following pricing guidelines• Meeting reporting requirements of RBI and respective Act• Registrations/obtaining key documents like PAN etc.• Project approval at state level• Finding ideal space for business activity based on various parameters like

incentives, cost, availability of man power etc.• Manufacturing projects are required to file Industrial Entrepreneur’s

Memorandum (IEM), some of the industries may also require industrial license.• Construction/renovation of unit.• Hiring of manpower.• Obtaining licenses if any.• Other state & central level registrations.• Meeting annual requirements of a structure, paying taxes etc.

www.mashahca.com

Repatriation • REPATRIATION OF DIVIDEND :• Dividends are freely repatriable without any restrictions (net after

tax deduction at source or Dividend Distribution Tax.• REPATRIATION OF CAPITAL : AD Category-I bank can allow the

remittance of sale proceeds of a security (net of applicable taxes) to the seller of shares resident outside India, provided the security has been held on repatriation basis, the sale of security has been made in accordance with the prescribed guidelines and NOC / tax clearance certificate from the Income Tax Department has been produced.

• Investments are subject to lock-in period of 3 years in case of construction development sector.

• REPATRIATION OF INTEREST : Interest on fully, mandatorily & compulsorily convertible debentures is also freely repatriablewithout any restrictions (net of applicable taxes).

www.mashahca.com

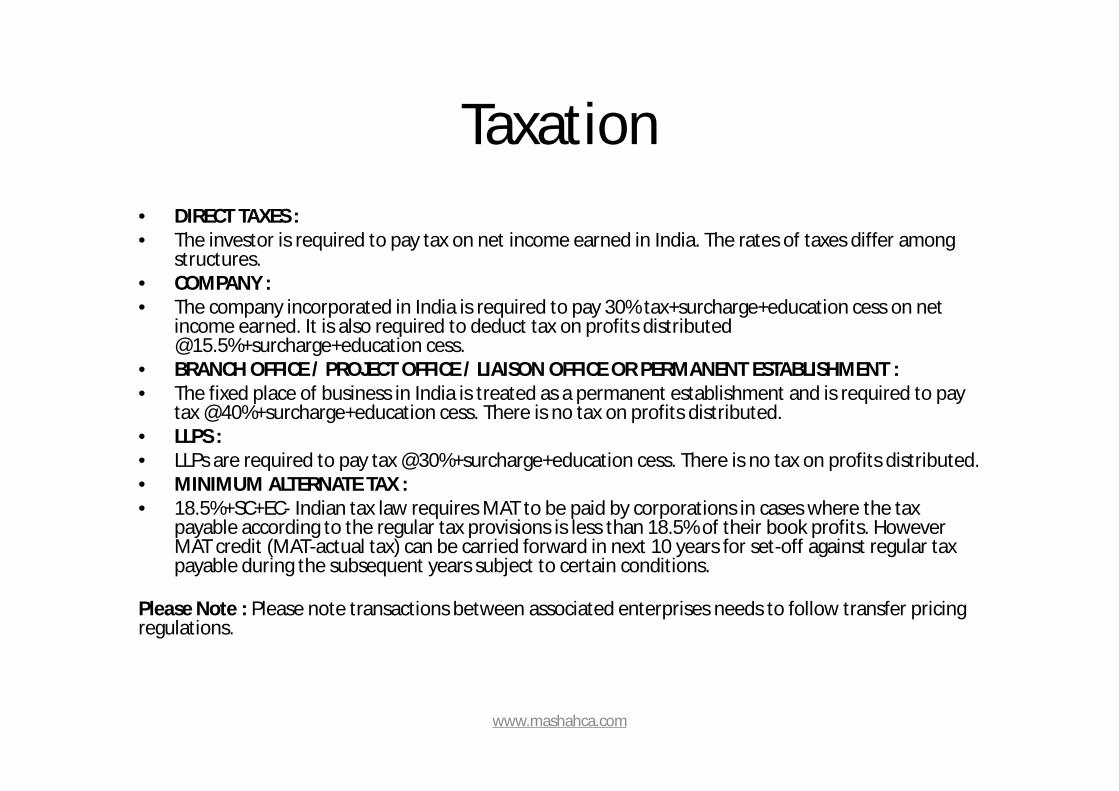

Taxation• DIRECT TAXES :• The investor is required to pay tax on net income earned in India. The rates of taxes differ among

structures.• COMPANY :• The company incorporated in India is required to pay 30% tax+surcharge+education cess on net

income earned. It is also required to deduct tax on profits distributed @15.5%+surcharge+education cess.

• BRANCH OFFICE / PROJECT OFFICE / LIAISON OFFICE OR PERMANENT ESTABLISHMENT :• The fixed place of business in India is treated as a permanent establishment and is required to pay

tax @40%+surcharge+education cess. There is no tax on profits distributed.• LLPS :• LLPs are required to pay tax @30%+surcharge+education cess. There is no tax on profits distributed.• MINIMUM ALTERNATE TAX :• 18.5%+SC+EC- Indian tax law requires MAT to be paid by corporations in cases where the tax

payable according to the regular tax provisions is less than 18.5% of their book profits. However MAT credit (MAT-actual tax) can be carried forward in next 10 years for set-off against regular tax payable during the subsequent years subject to certain conditions.

Please Note : Please note transactions between associated enterprises needs to follow transfer pricing regulations.

www.mashahca.com

2020 Challenge

• By 2020, India will be home to 1.35 billion people, of whom 906 million will be of working age.

• These 906 million will need jobs to sustain India’s growth, and these jobs can only be provided by the sustained growth of the manufacturing and service sectors in India.

www.mashahca.com

2020 Challenge

• To create the jobs to employ India’s rapidly growing youth base, and the only means of doing so is to catalyze increased private investment in India.

• Today’s investment equals tomorrow’s jobs, and so the Government of India has embarked on the ambitious Make in India initiative to create jobs

www.mashahca.com

Indian States - Ease of Doing Business

Benchmarking Guidelines1. Setting up a business 2. Allotment of land and obtaining construction permit 3. Complying with environment procedures 4. Complying with labour regulations 5. Obtaining infrastructure related utilities 6. Registering and complying with tax procedures 7. Carrying out inspections 8. Enforcing contracts

www.mashahca.com

Rank State Score Rank State Score 1 Gujarat 71.14% 17 Himachal Pradesh 23.95% 2 Andhra Pradesh 70.12% 18 Kerala 22.87% 3 Jharkhand 63.09% 19 Goa 21.74% 4 Chhattisgarh 62.45% 20 Puducherry 17.72% 5 Madhya Pradesh 62.00% 21 Bihar 16.41% 6 Rajasthan 61.04% 22 Assam 14.84% 7 Odisha 52.12% 23 Uttarakhand 13.36% 8 Maharashtra 49.43% 24 Chandigarh 10.04% 9 Karnataka 48.50% 25 Andaman and Nicobar Islands 9.73% 10 Uttar Pradesh 47.37% 26 Tripura 9.29% 11 West Bengal 46.90% 27 Sikkim 7.23% 12 Tamil Nadu 44.58% 28 Mizoram 6.37% 13 Telangana 42.45% 29 Jammu and Kashmir 5.93% 14 Haryana 40.66% 30 Meghalaya 4.38% 15 Delhi 37.35% 31 Nagaland 3.41% 16 Punjab 36.73% 32 Arunachal Pradesh 1.23%

www.mashahca.com

State wise FDINew Delhi –22%, Computer Software & ITES, Electronics & High Tech Industries Gujarat –5% Food Processing, Port related activities & Infrastructure, ChemicalsMaharashtra –29% Automobile, Textile, Food ProcessingKarnataka –7% Computer Software & ITES, Telecom, Automobiles, Industrial Parks, Power ProjectsTamil Nadu –8% Health Care, Infrastructure, chemicalsAndhra Pradesh –4% Computer Software & ITES, Tourism, Biotechnology, Mineral based industries

www.mashahca.com

Entry routes for investments in India

• Automatic Route: Under the Automatic Route, the foreign investor or the Indian company does not require any approval from the Reserve Bank or Government of India for the investment.

• Government Route: Under the Government Route, the foreign investor or the Indian company should obtain prior approval of the Government of India(Foreign Investment Promotion Board (FIPB), Department of Economic Affairs (DEA), Ministry of Finance or Department of Industrial Policy & Promotion, as the case may be) for the investment.

www.mashahca.com

Eligibility for Investment in India• A person resident outside India or an entity

incorporated outside India, can invest in India, according to the FDI Policy of the Government of India and Foreign Exchange Management (Transfer or issue of security by a person resident outside India) Regulations, 2000.

• It may be noted that a person who is a citizen of or an entity incorporated in Bangladesh/ Pakistan can invest in India under the FDI Scheme with the prior approval of the FIPB subject to terms and conditions mentioned in FDI Policy and Foreign Exchange Management (Transfer or issue of security by a person resident outside India) Regulations, 2000.

www.mashahca.com

Eligibility for Investment in India

• NRIs, resident in Nepal and Bhutan as well as citizens of Nepal and Bhutan are permitted to invest in shares and convertible debentures of Indian companies under FDI Scheme on repatriation basis, subject to the condition that the amount of consideration for such investment shall be paid only by way of inward remittance in free foreign exchange through normal banking channels.

www.mashahca.com

Eligibility for Investment in India• Overseas Corporate Bodies (OCBs) have been de-recognised as a

class of investor in India with effect from September 16, 2003. • Erstwhile OCBs which are incorporated outside India and are not

under adverse notice of the Reserve Bank can make fresh investments under the FDI Scheme as incorporated non-resident entities, with the prior approval of the Government of India if the investment is through the Government Route; and with the prior approval of the Reserve Bank, if the investment is through the Automatic Route.

• However, before making any fresh FDI under the FDI scheme, an erstwhile OCB should through their AD bank, take a one time certification from RBI that it is not in the adverse list being maintained with the Reserve Bank of India.

www.mashahca.com

Type of instruments

• Indian companies can issue equity shares, fully and mandatorily convertible debentures, fully and mandatorily convertible preference shares and warrants subject to the pricing guidelines / valuation norms and reporting requirements amongst other requirements as prescribed under FEMA Regulations.

www.mashahca.com

Type of instruments• Prior to December 30, 2013, issue of other types of preference

shares such as non-convertible, optionally convertible or partially convertible, were to be in accordance with the guidelines applicable for External Commercial Borrowings (ECBs).

• On and from December 30, 2013 it has been decided that optionality clauses may henceforth be allowed in equity shares and compulsorily and mandatorily convertible preference shares/debentures to be issued to a person resident outside India under the Foreign Direct Investment (FDI) Scheme.

• The optionality clause will oblige the buy-back of securities from the investor at the price prevailing/value determined at the time of exercise of the optionality so as to enable the investor to exit without any assured return.

www.mashahca.com

Type of instruments

• The provision of optionality clause shall be subject to the following conditions:– There is a minimum lock-in period of one year or a

minimum lock-in period as prescribed under FDI Regulations, whichever is higher (e.g. defence sector where the lock-in period of three years has been prescribed).

– The lock-in period shall be effective from the date of allotment of such shares or convertible debentures or as prescribed for defence sector, etc.

www.mashahca.com

Type of instruments• (b) After the lock-in period, as applicable above, the

non-resident investor exercising option/right shall be eligible to exit without any assured return, as under:– (i) In case of a listed company, the non-resident investor

shall be eligible to exit at the market price prevailing at the recognised stock exchanges;

– (ii) In case of unlisted company, the non-resident investor shall be eligible to exit from the investment in equity shares of the investee company at a price as per any internationally accepted pricing methodology on arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker.

www.mashahca.com

Type of instruments

• The guiding principle would be that the non-resident investor is not guaranteed any assured exit price at the time of making such investment/agreements and shall exit at the fair price computed as above at the time of exit, subject to lock-in period requirement, as applicable.

www.mashahca.com

Pricing guidelines• Fresh issue of shares: Price of fresh shares issued to

persons resident outside India under the FDI Scheme, shall be :– on the basis of SEBI guidelines in case of listed companies. – not less than fair value of shares determined by a SEBI

registered Merchant Banker or a Chartered Accountant as per as per any internationally accepted pricing methodology on arm’s length basis.

• The pricing guidelines as above are subject to pricing guidelines as enumerated in paragraph above, for exit from FDI with optionality clauses by non-resident investor.

www.mashahca.com

Pricing guidelines• The above pricing guidelines are also applicable for

issue of shares against payment of lump sum technical know how fee / royalty due for payment/repayment or conversion of ECB into equity or capitalization of pre incorporation expenses/import payables (with prior approval of Government).

• The pricing of the partly paid equity shares shall be determined upfront and 25% of the total consideration amount (including share premium, if any), shall also be received upfront; The balance consideration towards fully paid equity shares shall be received within a period of 12 months.

www.mashahca.com

Intermediate Holding Company• Mauritius

– Corporate Tax rate – 3 – 15%– Withholding tax rate in India ( As per DTAA)

• Interest – As per local laws ( 20 / 5) %• Royalties / FTS – 15 % , No FTS

– Capital gains Tax – Taxable in Mauritius – effectively NIL

– Tax treaty Networks – UK, Germany, France etc• The structure would have to meet with the

commercial substance test under the Indian GAAR provisions

www.mashahca.com

Intermediate Holding Company• Netherlands

– Corporate Tax rate – 20 – 25%– Withholding tax rate in India ( As per DTAA)

• Interest – As per local laws 10 %• Royalties / FTS – 10 %

• Capital gains Tax – Taxable in Netherlands (if sold to another resident –effective tax NIL)– Tax treaty Networks – Extensive DTAA

• The structure would have to meet with the commercial substance test under the Indian GAAR provisions

www.mashahca.com

Intermediate Holding Company• Singapore

– Corporate Tax rate – 17%– Withholding tax rate in India ( As per DTAA)

• Interest – As per local laws 15 %• Royalties / FTS – 10%

– Capital gains Tax – Taxable in Singapore – effectively NIL, subject to LOB

– Tax treaty Networks – UK, Germany, France etc• The structure would have to meet with the

commercial substance test under the Indian GAAR provisions

www.mashahca.com

Additional conditions for issue of partly paid shares and warrants

• The Indian company whose activity/ sector falls under government route would require prior approval of the Foreign Investment Promotion Board (FIPB), Government of India for issue of partly-paid shares/ warrants.

• The forfeiture of the amount paid upfront on non-payment of call money shall be in accordance with the provisions of the Companies Act, 2013 and Income tax provisions, as applicable;

www.mashahca.com

Indirect Transfers• Shares of ( E.g Netherlands) Hold Co would be deemed to

be located in India, if substantial value of such shares is derived from assets located in India (ie. Indian Co)

• Indirect transfer provisions would be applicable only if the value of Indian assets exceed INR 100 Mn AND such assets contribute alteast50% of the total value of the foreign hold co

• Certain exemptions to minority shareholders ie. shareholders having no right in management or control and holding less than 5% of the voting power, directly or indirectly

• Specified foreign amalgamations/ demergers shall not be subject to tax under these provisions

www.mashahca.com

Right Shares

• The price of shares offered on rights basis by the Indian company to non-resident shareholders shall be:– In the case of shares of a company listed on a

recognised stock exchange in India, at a price as determined by the company.

– In the case of shares of a company not listed on a recognised stock exchange in India, at a price which is not less than the price at which the offer on right basis is made to the resident shareholders.

www.mashahca.com

Acquisition / transfer of existing shares (private arrangement).

• The acquisition of existing shares from Resident to Non-resident (i.e. to incorporated non-resident entity other than erstwhile OCB, foreign national, NRI, FII) would be at a:-;– (a) negotiated price for shares of companies listed on a

recognized stock exchange in India which shall not be less than the price at which the preferential allotment of shares can be made under the SEBI guidelines, as applicable, provided the same is determined for such duration as specified therein, preceding the relevant date, which shall be the date of purchase or sale of shares. The price per share arrived at should be certified by a SEBI registered Merchant Banker or a Chartered Accountant.

www.mashahca.com

Acquisition / transfer of existing shares (private arrangement).

• negotiated price for shares of companies which are not listed on a recognized stock exchange in India which shall not be less than the fair value worked out as per any internationally accepted pricing methodology for valuation of shares on arm’s length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker.Further, transfer of existing shares by Non-resident (i.e. by incorporated non-resident entity, erstwhile OCB, foreign national, NRI, FII) to Resident shall not be more than the minimum price at which the transfer of shares can be made from a resident to a non-resident as given above.

www.mashahca.com

Acquisition / transfer of existing shares (private arrangement).

• The pricing of shares / convertible debentures / preference shares should be decided / determined upfront at the time of issue of the instruments. The price for the convertible instruments can also be a determined based on the conversion formula which has to be determined / fixed upfront, however the price at the time of conversion should not be less than the fair value worked out, at the time of issuance of these instruments, in accordance with the extant FEMA regulations.

• The pricing guidelines as above are subject to pricing guidelines as enumerated in paragraph above, for exit from FDI with optionality clauses by non-resident investor.

www.mashahca.com

Investment in Start-Ups- Technology Companies

• Eligible companies shall mean entity incorporated from April 1,2016 but before April 1,2019 and annual turnover does not exceed INR 250 Mninany fiscal year.

• 100% tax exemption for start-ups in any 3 consecutive years out of 5 years

• Tax exemption on capital gains invested in shares of start-ups, subject to fulfillment of conditions ie. for promoters

• Tax exemption upto INR 5 Mn available on capital gains invested in fund of funds ie. for investors

www.mashahca.com

Investment in Start-Ups- Manufacturing Companies

• Incentives to promote manufacturing set up in India with the aim of Make in India campaign

• Reduced corporate tax rate of 25% (plus sucharge and cess)

• Available provided no profit linked or investment linked deductions, investment allowance and accelerated depreciation

• Applicable to companies that have been setup or registered after March 1,2016

www.mashahca.com

Mode of payment• An Indian company issuing shares /convertible debentures under FDI

Scheme to a person resident outside India shall receive the amount of consideration required to be paid for such shares /convertible debentures by:– (i) inward remittance through normal banking channels.– (ii) debit to NRE / FCNR account of a person concerned maintained with an AD

category I bank.– (iii) conversion of royalty / lump sum / technical know how fee due for

payment /import of capital goods by units in SEZ or conversion of ECB, shall be treated as consideration for issue of shares.

– (iv) conversion of import payables / pre incorporation expenses / share swap can be treated as consideration for issue of shares with the approval of FIPB.

– (v) debit to non-interest bearing Escrow account in Indian Rupees in India which is opened with the approval from AD Category – I bank and is maintained with the AD Category I bank on behalf of residents and non-residents towards payment of share purchase consideration.

www.mashahca.com

Mode of payment• If the shares or convertible debentures are not

issued within 180 days from the date of receipt of the inward remittance or date of debit to NRE / FCNR(B) / Escrow account, the amount of consideration shall be refunded. Further, the Reserve Bank may on an application made to it and for sufficient reasons, permit an Indian Company to refund / allot shares for the amount of consideration received towards issue of security if such amount is outstanding beyond the period of 180 days from the date of receipt

www.mashahca.com

Foreign Investment Limits

• The details of the entry route applicable and the maximum permissible foreign investment / sectoral cap in an Indian Company are determined by the sector in which it is operating.

www.mashahca.com

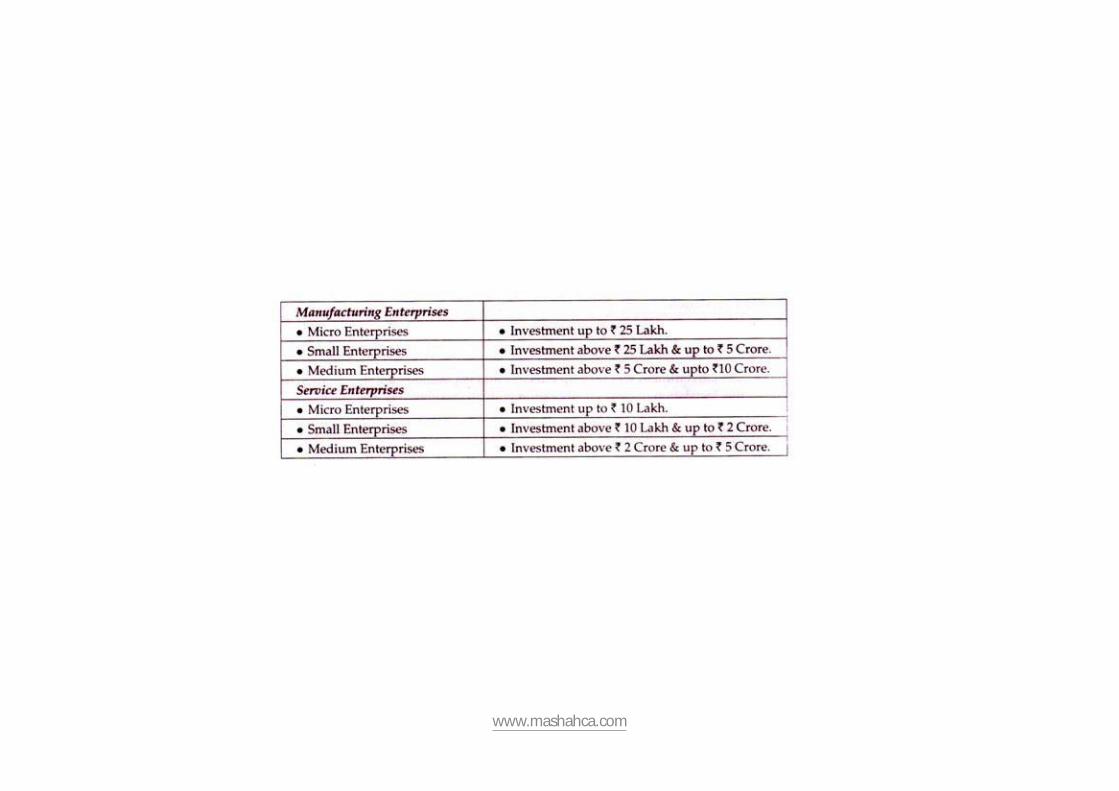

Investments in Micro and Small Enterprise (MSE)

• A company which is reckoned as Micro and Small Enterprise (MSE) (earlier Small Scale Industrial Unit) in terms of the Micro, Small and Medium Enterprises Development (MSMED) Act, 2006, including an Export Oriented Unit or a Unit in Free Trade Zone or in Export Processing Zone or in a Software Technology Park or in an Electronic Hardware Technology Park, and which is not engaged in any activity/sector mentioned in Annex 2 may issue shares or convertible debentures to a person resident outside India (other than a resident of Pakistan and to a resident of Bangladesh under approval route), subject to the prescribed limits as per FDI Policy, in accordance with the Entry Routes and the provision of Foreign Direct Investment Policy, as notified by the Ministry of Commerce & Industry, Government of India, from time to time.

www.mashahca.com

Investments in Micro and Small Enterprise (MSE)

• Any Industrial undertaking, with or without FDI, which is not an MSE, having an industrial license under the provisions of the Industries (Development & Regulation) Act, 1951 for manufacturing items reserved for the MSE sector may issue shares to persons resident outside India (other than a resident/entity of Pakistan and to a resident/entity of Bangladesh with prior approval FIPB), to the extent of 24 per cent of its paid-up capital or sectoral cap whichever is lower. Issue of shares in excess of 24 per cent of paid-up capital shall require prior approval of the FIPB of the Government of India and shall be in compliance with the terms and conditions of such approval.

www.mashahca.com

Prohibition on foreign investment in India

Foreign investment in any form is prohibited in a company or a partnership firm or a proprietary concern or any entity, whether incorporated or not (such as, Trusts) which is engaged or proposes to engage in the following activities: • Business of chit fund, or• Nidhi company, or• Agricultural or plantation activities, or• Real estate business, or construction of farm houses, or • Trading in Transferable Development Rights (TDRs)

www.mashahca.com

Prohibition on foreign investment in India

• However, it is clarified that only NRIs are eligible to subscribe to the chit funds on non- repatriation basis subject to the following conditions:– The Registrar of Chits or an officer authorised by the State

Government in accordance with the provisions of the Chit Fund Act in consultation with the State Government concerned, may permit any chit fund to accept subscription from Non-Resident Indians on non-repatriation basis;

– The subscription to the chit funds shall be brought in through normal banking channel, including through an account maintained with a bank in India

www.mashahca.com

Prohibition on foreign investment in India

• Further, It is clarified that “real estate business” means dealing in land and immovable property with a view to earning profit or earning income therefrom and does not include development of townships, construction of residential / commercial premises, roads or bridges, educational institutions, recreational facilities, city and regional level infrastructure, townships.

• It is also further clarified that partnership firms /proprietorship concerns having investments as per FEMA regulations are not allowed to engage in print media sector.

www.mashahca.com

Prohibition on foreign investment in India

In addition to the above, Foreign investment in the form of FDI is also prohibited in certain sectors such as :• (a) Lottery Business including Government/ private lottery, online lotteries, etc• (b) Gambling and Betting including casinos etc.• (c) Chit funds• (d) Nidhi company• (e) Trading in Transferable Development Rights (TDRs)• (f) Real Estate Business or Construction of Farm Houses• (g) Manufacturing of Cigars, cheroots, cigarillos and cigarettes, of tobacco or of

tobacco substitutes• (h) Activities / sectors not open to private sector investment e.g. (I) Atomic energy

and (II) Railway operations • Note: Foreign technology collaboration in any form including licensing for

franchise, trademark, brand name, management contract is also prohibited for Lottery Business and Gambling and Betting activities

www.mashahca.com

Group company

• “Group company” means two or more enterprises which, directly or indirectly, are in position to:

• (i) exercise twenty-six per cent, or more of voting rights in other enterprise; or

• (ii) appoint more than fifty per cent, of members of board of directors in the other enterpris

www.mashahca.com

Modes of Investment under Foreign Direct Investment Scheme

• Issuance of fresh shares by the companyAn Indian company may issue fresh shares /convertible debentures under the FDI Scheme to a person resident outside India (who is eligible for investment in India) subject to compliance with the extant FDI policy and the FEMA Regulation

www.mashahca.com

Modes of Investment under Foreign Direct Investment Scheme

• Acquisition by way of transfer of existing shares by person resident in or outside India

• Foreign investors can also invest in Indian companies by purchasing / acquiring existing shares from Indian shareholders or from other non-resident shareholders. General permission has been granted to non-residents / NRIs for acquisition of shares by way of transfer

www.mashahca.com

Modes of Investment under Foreign Direct Investment Scheme

• Transfer of shares by a Person resident outside India • a. Non Resident to Non-Resident (Sale / Gift): A person

resident outside India (other than NRI and OCB) may transfer by way of sale or gift, shares or convertible debentures to any person resident outside India (including NRIs but excluding OCBs).

• Note: Transfer of shares from or by erstwhile OCBs would require prior approval of the Reserve Bank of India.

• b. NRI to NRI (Sale / Gift): NRIs may transfer by way of sale or gift the shares or convertible debentures held by them to another NRI.

www.mashahca.com

Modes of Investment under Foreign Direct Investment Scheme

• Non Resident to Resident(Sale / Gift):(i) Gift: A person resident outside India can transfer any security to a person resident in India by way of gift.(ii) Sale under private arrangement: General permission is also available for transfer of shares / convertible debentures, by way of sale under private arrangement by a person resident outside India to a person resident in India in case where transfer of shares are under SEBI regulations and where the FEMA pricing guidelines are not met, subject to the following The original and resultant investment comply with the extant FDI policy/ FEMA regulations;The pricing complies with the relevant SEBI regulations (such as IPO, Book building, block deals, delisting, exit, open offer/ substantial acquisition / SEBI (SAST) and buy back); andCA certificate to the effect that compliance with relevant SEBI regulations as indicated above is attached to the Form FC-TRS to be filed with the AD bank. Compliance with reporting and other guidelines as given Note: Transfer of shares from a Non Resident to Resident other than under SEBI regulations and where the FEMA pricing guidelines are not met would require the prior approval of the Reserve Bank of India.iii) Sale of shares/ convertible debentures on the Stock Exchange by person resident outside India: A person resident outside India can sell the shares and convertible debentures of an Indian company on a recognized Stock Exchange in India through a stock broker registered with stock exchange or a merchant banker registered with SEBI

www.mashahca.com

Issue of shares under Employees Stock Option Scheme (ESOPs)

• An Indian company may issue “employees’ stock option” and/or “sweat equity shares” to its employees/directors or employees/directors of its holding company or joint venture or wholly owned overseas subsidiary/subsidiaries who are resident outside India, provided that :

1. The scheme has been drawn either in terms of regulations issued under the Securities Exchange Board of India Act, 1992 or the Companies (Share Capital and Debentures) Rules, 2014 notified by the Central Government under the Companies Act 2013, as the case may be.

2. The “employee’s stock option”/ “sweat equity shares” issued to non-resident employees/directors under the applicable rules/regulations are in compliance with the sectoral cap applicable to the said company.

3. Issue of “employee’s stock option”/ “sweat equity shares” in a company where foreign investment is under the approval route shall require prior approval of the Foreign Investment Promotion Board (FIPB) of Government of India.

4. Issue of “employee’s stock option”/ “sweat equity shares” under the applicable rules/regulations to an employee/director who is a citizen of Bangladesh/Pakistan shall require prior approval of the Foreign Investment Promotion Board (FIPB) of Government of India.

www.mashahca.com

Conversion of ECB• Indian companies have been granted general permission for conversion of External

Commercial Borrowings (ECB) [i.e other than import dues deemed as ECB or Trade Credit as per RBI guidelines] into shares / convertible debentures, subject to the following conditions and reporting requirements:

1. The activity of the company is covered under the Automatic Route for FDI or the company has obtained Government's approval for foreign equity in the company;

2. The foreign equity after conversion of ECB into equity is within the sectoral cap, if any;

3. Pricing of shares is determined as per SEBI regulations for listed company or fair value worked out as per any internationally accepted pricing methodology for valuation of shares for unlisted company;

4. Compliance with the requirements prescribed under any other statute and regulation in force;

5. The conversion facility is available for ECBs availed under the Automatic or Approval Route and is applicable to ECBs, due for payment or not, as well as secured / unsecured loans availed from non-resident collaborators.

www.mashahca.com

Issue of shares• General permission is also available for issue of shares

/ preference shares against lump-sum technical know-how fee, royalty due for payment/repayment, under automatic route or SIA / FIPB route, subject to pricing guidelines of RBI/SEBI and compliance with applicable tax laws.

• Units in Special Economic Zones (SEZs) are permitted to issue equity shares to non-residents against import of capital goods subject to the valuation done by a Committee consisting of Development Commissioner and the appropriate Customs officials.

www.mashahca.com

Issue of Shares• Issue of equity shares against Import of capital goods / machinery / equipment

(excluding second-hand machinery), is allowed under the Government route, subject to the compliance with the following conditions:

1. a) The import of capital goods, machineries, etc., made by a resident in India, is in accordance with the Export / Import Policy issued by the Government of India as notified by the Directorate General of Foreign Trade (DGFT) and the regulations issued under the Foreign Exchange Management Act (FEMA), 1999 relating to imports issued by the Reserve Bank;

2. (b) There is an independent valuation of the capital goods /machineries / equipments by a third party entity, preferably by an independent valuer from the country of import along with production of copies of documents /certificates issued by the customs authorities towards assessment of the fair-value of such imports;

3. (c) The application should clearly indicate the beneficial ownership and identity of the importer company as well as the overseas entity; and

4. (d) Applications complete in all respects, for conversions of import payables for capital goods into FDI being made within 180 days from the date of shipment of goods.

www.mashahca.com

Issue of equity shares against Pre-operative / pre – incorporation expenses

• Issue of equity shares against Pre-operative / pre – incorporation expenses (including payment of rent etc.) is allowed under the Government route, subject to compliance with the following conditions:

a) Submission of FIRC for remittance of funds by the overseas promoters for the expenditure incurred.b) Verification and certification of the pre-incorporation / pre-operative expenses by the statutory auditor.c) Payments being made by the foreign investor to the company directly or through the bank account opened by the foreign investor, as provided under FEMA regulations. (as amended vide AP DIR Circular No. 104 dated May 17, 2013).d) The applications, complete in all respects, for capitalisation being made within the period of 180 days from the date of incorporation of the company.

www.mashahca.com

General conditions for issue of equity shares

• General conditions for issue of equity shares against Import of capital goods / machinery / equipment and Pre-operative / pre –incorporation expenses:

(a) All requests for conversion should be accompanied by a special resolution of the company;(b) Government’s approval would be subject to pricing guidelines of RBI and appropriate tax clearance.

www.mashahca.com

Shares swap• Issue of shares to a non-resident against shares swap i.e., in lieu for

the consideration which has to be paid for shares acquired in the overseas company, can be done with the approval of FIPB.

(vii) Issue of shares against any other funds payable by the investee company, remittance of which does not require prior permission of the Government of India or Reserve Bank of India under FEMA,1999 or any rules/ regulations framed or directions issued thereunder, provided that:• (a) The equity shares shall be issued in accordance with the extant

FDI guidelines on sectoral caps, pricing guidelines etc. as amended by Reserve Bank of India, from time to time;

• (b) The issue of equity shares under this provision shall be subject to tax laws as applicable to the funds payable and the conversion to equity should be net of applicable taxes.

www.mashahca.com

Acquisition of shares under Scheme of Merger / Amalgamation

• Mergers and amalgamations of companies in India are usually governed by an order issued by a competent Court on the basis of the Scheme submitted by the companies undergoing merger/amalgamation. Once the scheme of merger or amalgamation of two or more Indian companies has been approved by a Court in India, the transferee company or new company is allowed to issue shares to the shareholders of the transferor company resident outside India, subject to the conditions that :

1. the percentage of shareholding of persons resident outside India in the transferee or new company does not exceed the sectoral cap, and

2. the transferor company or the transferee or the new company is not engaged in activities which are prohibited under the FDI policy

www.mashahca.com

Remittance of sale proceeds

• AD Category – I bank can allow the remittance of sale proceeds of a security (net of applicable taxes) to the seller of shares resident outside India, provided the security has been held on repatriation basis, the sale of security has been made in accordance with the prescribed guidelines and NOC / tax clearance certificate from the Income Tax Department has been produced

www.mashahca.com

Remittance on winding up/liquidation of Companies

• AD Category – I banks have been allowed to remit winding up proceeds of companies in India, which are under liquidation, subject to payment of applicable taxes. Liquidation may be subject to any order issued by the court winding up the company or the official liquidator in case of voluntary winding up under the provisions of the Companies Act, 2013. AD Category – I banks shall allow the remittance provided the applicant submits:

1. No objection or Tax clearance certificate from Income Tax Department for the remittance.

2. Auditor's certificate confirming that all liabilities in India have been either fully paid or adequately provided for.

3. Auditor's certificate to the effect that the winding up is in accordance with the provisions of the Companies Act, 2013.

4. In case of winding up otherwise than by a court, an auditor's certificate to the effect that there is no legal proceedings pending in any court in India against the applicant or the company under liquidation and there is no legal impediment in permitting the remittance

www.mashahca.com

Pledge of Shares• a) A person being a promoter of a company registered in India

(borrowing company), which has raised external commercial borrowings, may pledge the shares of the borrowing company or that of its associate resident companies for the purpose of securing the ECB raised by the borrowing company, provided that a no objection for the same is obtained from a bank which is an authorised dealer. – The authorized dealer, shall issue the no objection for such a pledge

after having satisfied itself that the external commercial borrowing is in line with the extant FEMA regulations for ECBs

• b) Non-resident holding shares of an Indian company, can pledge these shares in favour of the AD bank in India to secure credit facilities being extended to the resident investee company for bonafide business purpose

www.mashahca.com

Compounding of Offenses• Compounding refers to the process of voluntarily admitting the

contravention, pleading guilty and seeking redressal. • The Reserve Bank is empowered to compound any contraventions

as defined under section 13 of FEMA, 1999 except the contravention under section 3(a), for a specified sum after offering an opportunity of personal hearing to the contravener.

• It is a voluntary process in which an individual or a corporate seeks compounding of an admitted contravention.

• It provides comfort to any person who contravenes any provisions of FEMA, 1999 [except section 3(a) of the Act] by minimizing transaction costs.

• Willful, malafide and fraudulent transactions are, however, viewed seriously, which will not be compounded by the Reserve Bank.

www.mashahca.com

Sr. No. FEMA Regulation Brief Description of Contravention1 Paragraph 9(1)(A) of Schedule I to

FEMA 20/2000-RB dated May 3, 2000

Delay in reporting inward remittance for issue of shares.

2 Paragraph 9(1)(B) of Schedule I to FEMA 20/2000-RB dated May 3,

2000

Delay in filing form FC(GPR) after issue of shares.

3 Paragraph 8 of Schedule I to FEMA 20/2000-RB dated May 3,

2000

Delay in issue of shares/refund of share application money beyond 180 days, mode of receipt of funds, etc.

4 Paragraph 5 of Schedule I to FEMA 20/2000-RB dated May 3,

2000

Violation of pricing guidelines for issue of shares.

5 Regulation 2(ii) read with Regulation 5(1) of FEMA

20/2000-RB dated May 3, 2000

Issue of ineligible instruments such as non-convertible debentures, partly paid shares, shares with optionality clause, etc.

6 Paragraph 2 or 3 of Schedule I to FEMA 20/2000-RB dated May 3,

2000

Issue of shares without approval of RBI or FIPB respectively, wherever required.

7 Regulation 10A (b)(i) read with paragraph 10 of Schedule I to

FEMA 20/2000-RB dated May 3, 2000

Delay in submission of form FC-TRS on transfer of shares from Resident to Non-Resident.

8 Regulation 10B (2) read with paragraph 10 of Schedule I to

FEMA 20/2000-RB dated May 3, 2000

Delay in submission of form FC-TRS on transfer of shares from Non-Resident to Resident.

9 Regulation 4 of FEMA 20/2000-RB dated May 3, 2000

Taking on record transfer of shares by investee company, in the absence of certified from FC-TRS.

The powers to compound the following contraventions have been vested with the Regional Offices of Foreign Exchange Department(FED), RBI

www.mashahca.com

Outbound Investment• The RBI has been regularly been relaxing rules

and regulations and simplifying the procedure by creating an automatic route for outbound investment and regularly reducing the regulatory aspect. Outbound investments in joint venture (JV) / wholly owned subsidiary (WOS) are appreciated as Indian companies go global. This encourages export of raw material, plant & machinery from India and increases the foreign exchange earnings by way of dividend, royalty, technical know how fees and other receipt such as family remittances.

www.mashahca.com

FEMA

• Setion 6(3) of FEMA is the governing section for outbound investment. These regulation grant general permission to residents for acquisition and purchase of securities and sale of shares or securities so acquired India out of funds held in RFC account, as bonus shares on existing foreign currency shares held and out of foreign currency resources held in India.

www.mashahca.com

Prohibition

• FEMA prohibits Indian parties from making investments outside India in any entity which is engaged in banking business, real estate business without prior permission of RBI

www.mashahca.com

Investing & Routing Destinations

• USA – Netherlands• UAE – Singapore• UK – Mauritius• Switzerland – BVI• Singapore – Cayman Islands

www.mashahca.com

Limits• Regulation 6 provides an Indian party to make overseas

investment in JV /WOS upto 400% of its net work as on the date of last audit balance sheet in any legitimate activity permitted by the law in the host country under the automatic route. For the purpose of reckoning net worth of an Indian party, the net worth of it’s holding company (which holds at least 51% direct stake in the Indian Party) or its subsidiary company (in which the Indian party holds at least 51% direct stake) may be taken into account to the extent not availed of by the holding company or the subsidiary independently and has furnished a letter of disclaimer in favour of the Indian Party. However, this facility is not available to / from partnership firms

• LRS – USD 2,50,000 per person per year

www.mashahca.com

To Do• The Indian party has to submit an application in form ODI to the

authorized Dealer (AD) supported by the documents listed therein, i.e., certified copy of the Board Resolution, Statutory Auditors certificate and Valuation report (in case of acquisition of an existing company) as per the valuation norms listed and not to RBI for remitting funds abroad. The AD will upload the form to RBI which will automatically generate a unique identification number (UIN) and email the same to the Indian Party. The allotment of UIN does not constitute an approval from the Reserve Bank for the investment made/to be made in the JV/WOS. The issue of UIN only signifies taking on record of the investment for maintaining the database. The onus of complying with the provisions of FEMA regulations rests with the AD bank and / or the Indian party.

www.mashahca.com

UIN

• Further, with effect from June 01, 2012 an auto generated e-mail, giving the details of UIN allotted to the JV / WOS under the automatic route, is forwarded to the AD / Indian party as confirmation of allotment of UIN, and no separate letter is issued by the Reserve Bank to the Indian party and AD Category - I bank confirming the allotment of UIN.

www.mashahca.com

Loan / Guarantee• Loan or Guarantee cannot be granted without participation in equity

capital.• Proposals from the Indian party for undertaking financial commitment

without equity contribution in JV / WOS may be considered by RBI under approval basis. AD may forward the proposal form their branch after the insurance that the laws of the host country permit incorporation of a company without equity participation by the Indian party. For qualifying under automatic route, the Indian party should not be on RBI’s exporter, caution list, list of defaulter to the banking system or it should not be under investigation by ED, CBI, etc. Indian entities may offer any form of guarantee – corporate or personal / primary or collateral / guarantee by the promoter of the company provided that all financial commitments including all form of guarantee are overall with in the overall ceiling prescribed for overseas investment by the indian party i.e. currently within 400% of networth as on date of the last balance sheet of the Indian company

www.mashahca.com

AD• All investment related transaction of JV / WOS should

be routed through only one designated branch of ED. Where the investment is being made in an existing foreign company of more than 5 milliion USD, valuation of its shares must be made by a category 1 Merchant banker registered with SEBI or a merchant banker outside India which is registered with the appropriate regulatiory authority of the concerned country. In all other case, the valuation shares of the foreign entity should be done by a CA or CPA.

•

www.mashahca.com

Approvals

• Proposals not covered by the conditions under the automatic route require prior approval of the Reserve Bank for which a specific application in Form ODI with the documents prescribed therein is required to be made through the Authorized Dealer Category – I banks

www.mashahca.com

Approvals• Requests under the approval route are

considered by taking into account, inter alia, the prima facie viability of the JV / WOS outside India, likely contribution to external trade and other benefits that may accrue to India through such investment, financial position and business track record of the Indian party and the foreign JV / WOS, experience and expertise of the Indian party in the same or related line of activity of the JV / WOS outside India

www.mashahca.com

Funding Sources• Funding for overseas direct investment can be made by one or more of the

following sources:1. Drawal of foreign exchange from an AD bank in India.2. Swap of shares (refers to the acquisition of the shares of an overseas JV /

WOS by way of exchange of the shares of the Indian party).3. Capitalization of exports and other dues and entitlements.4. Proceeds of External Commercial Borrowings / Foreign Currency

Convertible Bonds.5. In exchange of ADRs / GDRs issued in accordance with the Scheme for

issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993 and the guidelines issued by Government of India in the matter.

6. Balances held in Exchange Earners Foreign Currency account of the Indian Party maintained with an Authorized Dealer.

7. Proceeds of foreign currency funds raised through ADR / GDR issues

www.mashahca.com

Partnerships• Partnership firms registered under the Indian

Partnership Act, 1932 can make overseas direct investments subject to the same terms and conditions as applicable to corporate entities. Individual partners can hold shares for and on behalf of the partnership firm in an overseas JV/WOS, where the entire funding for the investments has been done by the firm and further provided that the host country regulations or operational requirements warrant such holding.

www.mashahca.com

SPV• Direct investment through the medium of a SPV is

permitted under the Automatic Route, for the sole purpose of investment in JV/WOS overseas. Where the JV/WOS has been established through a SPV, all funding to the operating step down subsidiary should be routed through the SPV only. However, in the case of guarantees to be given on behalf of the first level step down operating subsidiary, these can be given directly by the Indian Party provided such exposures are within the permissible financial commitment of the Indian Party

www.mashahca.com

SPV• The shares of a JV/WOS can be pledged by an

Indian Party as a security for availing fund based or non-fund based facility for itself or for the JV/WOS, from an authorised dealer/ public financial institution in India or from an overseas lender, provided the overseas lender is regulated and supervised as a bank and the total financial commitments of the Indian party remains within the limit stipulated by the Reserve Bank for overseas investment from time to time

www.mashahca.com

Compliance An Indian Party will have to comply with the following: -• receive share certificates or any other documentary evidence of investment in the

foreign JV / WOS as an evidence of investment and submit the same to the designated AD within 6 months;

• repatriate to India, all dues receivable from the foreign JV / WOS, like dividend, royalty, technical fees etc.;

• submit to the Reserve Bank through the designated Authorized Dealer, every year, an Annual Performance Report in Part III of Form ODI in respect of each JV or WOS outside India set up or acquired by the Indian party;

• report the details of the decisions taken by a JV/WOS regarding diversification of its activities /setting up of step down subsidiaries/alteration in its share holding pattern within 30 days of the approval of those decisions by the competent authority concerned of such JV/WOS in terms of the local laws of the host country. These are also to be included in the relevant Annual Performance Report; and

• in case of disinvestment, sale proceeds of shares/securities shall be repatriated to India immediately on receipt thereof and in any case not later than 90 days from the date of sale of the shares /securities and documentary evidence to this effect shall be submitted to the Reserve Bank through the designated Authorised Deale

www.mashahca.com

Compliance• Where the law of the host country does not

mandatorily require auditing of the books of accounts of JV / WOS, the Annual Performance Report (APR) may be submitted by the Indian party based on the un-audited annual accounts of the JV / WOS provided:

• The Statutory Auditors of the Indian party certifies that ‘The un-audited annual accounts of the JV / WOS reflect the true and fair picture of the affairs of the JV / WOS’ and

• That the un-audited annual accounts of the JV / WOS has been adopted and ratified by the Board of the Indian party

www.mashahca.com

Resident IndiansResident individuals can acquire/sell foreign securities without prior approval in the following cases: -• as a gift from a person resident outside India;• by way of ESOPs issued by a company incorporated outside India under

Cashless Employees Stock Option Scheme which does not involve any remittance from India;

• by way of ESOPs issued to an employee or a director of Indian office or branch of a foreign company or of a subsidiary in India of a foreign company or of an Indian company irrespective of the percentage of the direct or indirect equity stake in the Indian company;

• as inheritance from a person whether resident in or outside India;• by purchase of foreign securities out of funds held in the Resident Foreign

Currency Account maintained in accordance with the Foreign Exchange Management (Foreign Currency Account) Regulations, 2000; and

• by way of bonus/rights shares on the foreign securities already held by them.

www.mashahca.com

Directors• Reserve Bank has given General Permission to a resident

individual to acquire foreign securities to the extent of the minimum number of qualification shares required to be held for holding the post of Director. Accordingly, resident individuals are permitted to remit funds under general permission for acquiring qualification shares for holding the post of a Director in the overseas company to the extent prescribed as per the law of the host country where the company is located and the limit of remittance for acquiring such qualification shares shall be within the overall ceiling prescribed for the resident individuals under the Liberalized Remittance Scheme (LRS) in force at the time of acquisition

www.mashahca.com

Disinvest without write offThe Indian Party may disinvest without write off under the automatic route subject to the following:• the sale is effected through a stock exchange where the shares of the overseas JV/

WOS are listed;• if the shares are not listed on the stock exchange and the shares are disinvested by

a private arrangement, the share price is not less than the value certified by a Chartered Accountant / Certified Public Accountant as the fair value of the shares based on the latest audited financial statements of the JV / WOS;

• the Indian Party does not have any outstanding dues by way of dividend, technical know-how fees, royalty, consultancy, commission or other entitlements and / or export proceeds from the JV or WOS;

• the overseas concern has been in operation for at least one full year and the Annual Performance Report together with the audited accounts for that year has been submitted to the Reserve Bank;

• the Indian party is not under investigation by CBI / DoE/ SEBI / IRDA or any other regulatory authority in India

www.mashahca.com

Disinvest with write offAn Indian Party may disinvest, under the automatic route, involving write off in the under noted cases:• i) where the JV / WOS is listed in the overseas stock

exchange;• ii) where the Indian Party is listed on a stock exchange in

India and has a net worth of not less than Rs.100 crore;• iii) where the Indian Party is an unlisted company and the

investment in the overseas JV / WOS does not exceed USD 10 million; and

• iv) where the Indian Party is a listed company with net worth of less than Rs.100 crore but investment in an overseas JV/WOS does not exceed USD 10 million.

www.mashahca.com

Foreign Currency Account

• With effect from April 2, 2012, an Indian party is allowed to open, hold and maintain Foreign Currency Account (FCA) abroad for the purpose of overseas direct investments wherever the host country regulation stipulate the same subject to certain terms and conditions

• LRS – USD 2,50,000 per person, per year

www.mashahca.com

LRS• All resident individuals, including minors, are allowed

to freely remit up to USD 2,50,000 per financial year (April – March) for any permissible current or capital account transaction or a combination of both. Form A2 is to be filed with AD

• If an individual remits any amount under LRS in a financial year, then the applicable limit for such individual would be reduced from USD 250,000 by the amount so remitted.

• In case of remitter being a minor, the LRS declaration form must be countersigned by the minor’s natural guardian.

www.mashahca.com

LRS• The investor can retain and reinvest the income earned on

investments made under the Scheme. • The residents are not required to repatriate the funds or

income generated out of investments made under the Scheme.

• A resident individual who has made overseas direct investment in the equity shares and compulsorily convertible preference shares of a Joint Venture or Wholly Owned Subsidiary outside India, within the LRS limit then he/she shall have to comply with the terms and conditions as prescribed by our overseas investment guidelines under Notification No. 263/ RB-2013 dated August 5, 2013.

www.mashahca.com

Overseas investment guidelines• Resident individual is prohibited from making direct investment in a JV or WOS abroad which is engaged in the real estate

business or banking business or in the business of financial services activity. • The JV or WOS abroad shall be engaged in bonafide business activity. • Resident individual is prohibited from making direct investment in a JV / WOS [set up or acquired abroad individually or in

association with other resident individual and / or with an Indian party] located in the countries identified by the Financial Action Task Force (FATF) as "non co-operative countries and territories" as available on FATF website www.fatf-gafi.org or as notified by the Reserve Bank.

• The resident individual shall not be on the Reserve Bank’s Exporters Caution List or List of defaulters to the banking system or under investigation by any investigation / enforcement agency or regulatory body.

• At the time of investments, the permissible ceiling shall be within the overall ceiling prescribed for the resident individual under Liberalised Remittance Scheme as prescribed by the Reserve Bank from time to time.

• [Explanation: The investment made out of the balances held in EEFC / RFC account shall also be restricted to the limit prescribed under LRS.]

• The JV or WOS, to be acquired / set up by a resident individual under this Schedule, shall be an operating entity only and no step down subsidiary is allowed to be acquired or set up by the JV or WOS.

• For the purpose of making investment under this Schedule, the valuation shall be as per Regulation 6(6)(a) of this Notification.

• The financial commitment by a resident individual to / on behalf of the JV or WOS, other than the overseas direct investments as defined under Regulation 2(e) read with Regulation 20A of this Notification, is prohibited.

• Post Investment Changes• Any alteration in shareholding pattern of the JV or WOS may be reported to the designated AD within 30 days including

reporting in the Annual Performance Report as required to be submitted in terms of Regulation 15 of this Notification.

www.mashahca.com

Royalty, Interest from foreign source including from WOS

In India• Taxable at a base rate of @ 30% effective rate as

any other normal sourced Income• Budget2016 proposes a reduced base rate of 10%

on Indian patentsOther Countries of the world• Holding company jurisdictions tax foreign sourced

income at concessional rates

www.mashahca.com

Dividend Income from foreign companies

In India• Subject to fulfillment of prescribed conditions,

taxable at a base rate @ 15% for this yearOther Countries of the world• Most countries have a favourable tax

treatment for foreign sourced dividend income and provide participation exemption or high quantum of exemption

www.mashahca.com

Capital Gains

In India• Long term gain taxable at base rate of 20%

and short term gains taxable at base rate of 30%

Other Countries of the world• Capital Gains on foreign assets is generally not

taxed inthe country of residence

www.mashahca.com

Minimum Alternate Tax

In India• Tax on book profit at base rate of 18.5% that

includes foreign source income Other Countries of the world• Such taxation of income is not seen in most

holding company jurisdictions

www.mashahca.com

Fiscal Consolidation

In India• No such option is currently availableOther countries of the world• Available in many jurisdictions enabling tax

efficiency

www.mashahca.com

Foreign Tax Credit

In India• India provides unilateral tax credit under

Indian Tax Law as well as under respective Tax Treaties

Other Countries of the world• Available under Tax Treaties and possibly

under respective Tax Laws

www.mashahca.com

GAAR

• GAAR provisions are targeted at arrangements undertaken where the main purpose is to take tax benefit

• The regulations empower the tax authorities to disregard residency of overseas Company, treating them as tax residents of India and the income so earned by them could be brought to tax in India

• GAAR shall be applicable from 1 April 2017

www.mashahca.com

POEM• Foreign company shall be considered to be a

resident in India if its place of effective management, in that year, is in India

• Concept of POEM similar to the one present in various tax treaties, rules to be framed in this regard

• If considered as a resident, worldwide income of foreign company may be taxable in India

• In December 2015, CBDT had issued draft guidelines for determination of place of effective management.

www.mashahca.com

Judicial Anti-avoidance

• Aditya Birla Nuvo–Prima facie, Disregarding legal ownership of shares

• Otis India –Disregarding buy-back scheme whereby only one shareholder had tendered shares

www.mashahca.com

BEPS

• BEPS is a term used to describe tax planning strategies that rely on mismatches and gaps that exist between the tax rules of different jurisdictions, to minimise the corporation tax that is payable overall, by the following:

• Either making tax profits “disappear” or • Shift profits to low tax jurisdictions where

there is little or no genuine activity.

www.mashahca.com

BEPS

• BEPS Project is an OECD initiative, approved by the G20, to identify ways of providing more standardised tax rules globally to avoid/ minimize BEPS

• In general BEPS strategies are not illegal; rather they take advantage of different tax rules operating in different jurisdictions, which may not be suited to the current global and digital business environment.

www.mashahca.com

BEPS – Focus Areas• Action 1 :Address the tax challenges of the digital

economy• Action 2: Neutralise the effects of hybrid

mismatch arrangements • Action 3: Strengthen CFC rules• Action 4: Limit base erosion via interest

deductions and other financial payments• Action 5: Counter harmful tax practices more

effectively, taking into account transparency and substance

www.mashahca.com

BEPS – Focus Areas

• Action 6: Prevent treaty abuse • Action 7: Prevent the artificial avoidance of

permanent establishment status• Action 8: Consider transfer pricing for

intangibles • Action 9: Consider transfer pricing for risks

and capital • Action 10: Consider transfer pricing for other

high-risk transactions

www.mashahca.com

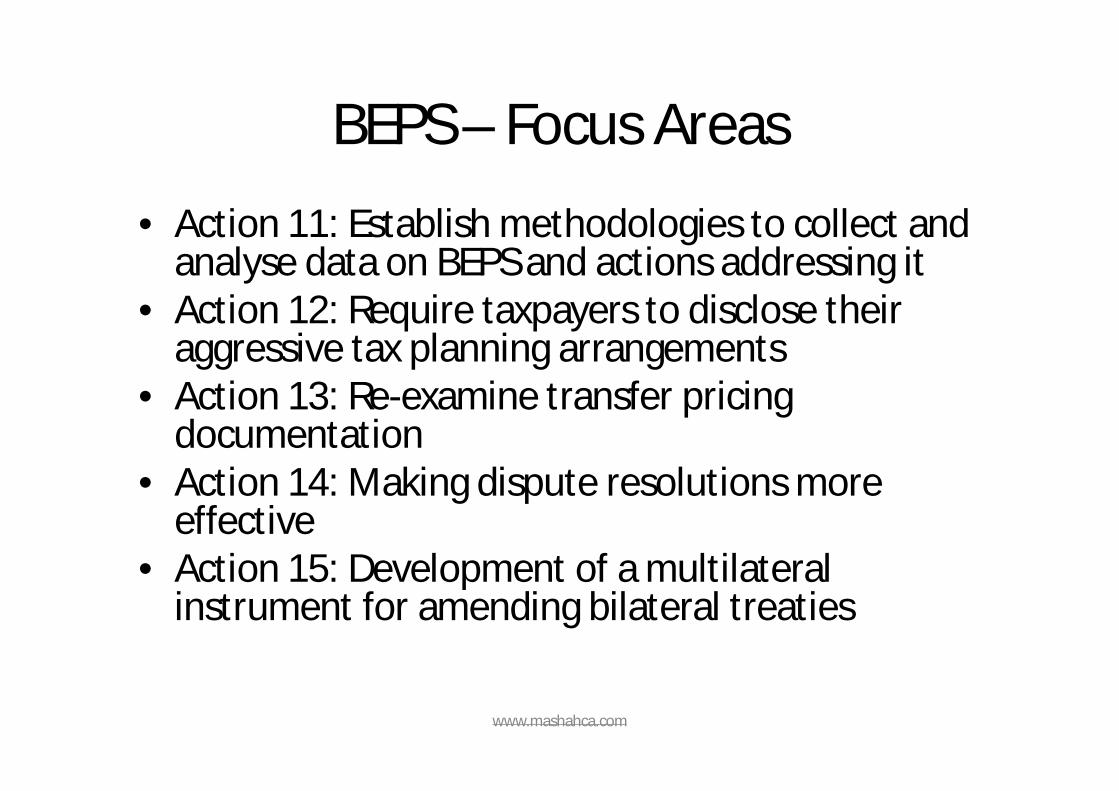

BEPS – Focus Areas• Action 11: Establish methodologies to collect and

analyse data on BEPS and actions addressing it• Action 12: Require taxpayers to disclose their

aggressive tax planning arrangements• Action 13: Re-examine transfer pricing

documentation• Action 14: Making dispute resolutions more

effective• Action 15: Development of a multilateral

instrument for amending bilateral treaties

www.mashahca.com

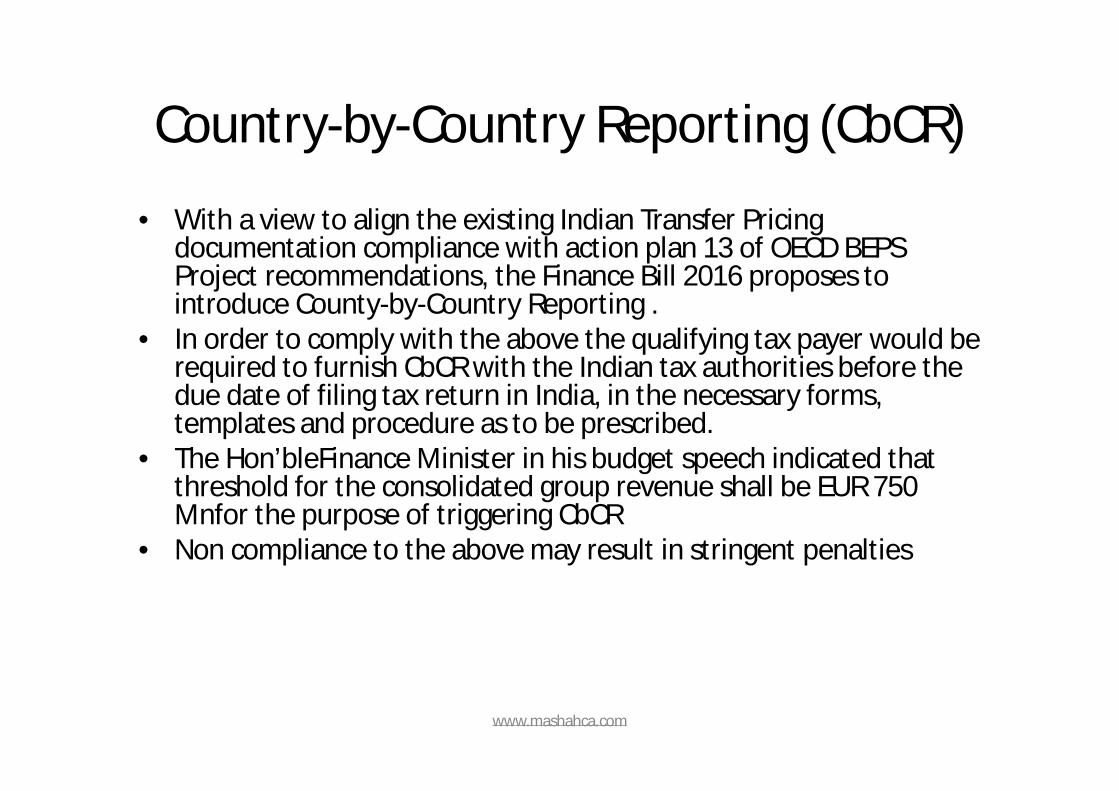

Country-by-Country Reporting (CbCR)• With a view to align the existing Indian Transfer Pricing

documentation compliance with action plan 13 of OECD BEPS Project recommendations, the Finance Bill 2016 proposes to introduce County-by-Country Reporting .

• In order to comply with the above the qualifying tax payer would be required to furnish CbCR with the Indian tax authorities before the due date of filing tax return in India, in the necessary forms, templates and procedure as to be prescribed.

• The Hon’bleFinance Minister in his budget speech indicated that threshold for the consolidated group revenue shall be EUR 750 Mnfor the purpose of triggering CbCR

• Non compliance to the above may result in stringent penalties

www.mashahca.com

![SELLING INBOUND: TRANSFORM YOUR REP'S INBOUND SELLING SKILLS [INBOUND 2014]](https://static.fdocuments.in/doc/165x107/55d54cf8bb61ebdb228b46ca/selling-inbound-transform-your-reps-inbound-selling-skills-inbound.jpg)