In Touch October 2010

28

CHAMBER IN THIS ISSUE 4President’s Message 4Chamber’s activities: Programme on IT Enablent Food for Thought programme on `The Employment V/s Unemployability Debate’ 4General Committee 4Expert Committees 4Spotlight - Financial Inclusion 4Policy watch 4Representations 4Trade Fairs & Exhibitions 4Economic Review 4Others TN Sales Tax (Settlement of Arrears) Act 2010. TN Ordinance No.7 of 2010 Food for Thought Programme on `Employment V/s. Unemployability Debate’ Programme on IT Enabled Supply Chain Management The Madras Chamber has recently introduced a “Food for Thought”(FFT) monthly programme...P3 Business, the world over, is struggling to sustain competitiveness in a rapidly globalizing economy. The challenge lies in creating economic value through innovations and the application of strategic tools. In such a challenging environment, supply chain...P2 Volume 24 – No.07 – October 2010

-

Upload

madraschamber -

Category

Documents

-

view

223 -

download

2

description

In Touch October 2010

Transcript of In Touch October 2010

CHAMBER

IN THIS ISSUE4President’s Message

4Chamber’s activities:

Programme on IT Enablent

Food for Thought programme on `The Employment V/s Unemployability Debate’

4General Committee

4Expert Committees

4Spotlight - Financial Inclusion

4Policy watch

4Representations

4Trade Fairs & Exhibitions

4Economic Review

4Others

TN Sales Tax (Settlement of Arrears) Act 2010. TN Ordinance No.7 of 2010

Food for Thought Programme on `Employment V/s. Unemployability Debate’

Programme on IT Enabled SupplyChain Management

The Madras Chamber has recently introduced a “Food for Thought”(FFT) monthly programme...P3

Business, the world over, is struggling to sustain competitiveness in a rapidly globalizing economy. The challenge lies in creating economic value through innovations and the application of strategic tools. In such a challenging environment, supply chain...P2

Volume 24 – No.07 – October 2010

PRESIDENT’S MESSAGE

Dear Member

Let me wish you all a very Happy Festive Season.

The Chamber’s monthly bulletin has started rolling out in its new avatar, as ‘Chamber In-Touch’, from last month, with improved look and feel. Hope you like it. Every issue will now be focussing on a specific theme. In the last issue we took up an important and pertinent subject - the employability of our youth force. I would like to seek from you suggestions on themes which you would like to be covered in the coming months.

We are all aware of RBI’s proposal to give licences to new private banks and the Chamber has already forwarded its inputs on the discussion paper. One of the key objectives of this move as stated by RBI, is `To achieve Financial Inclusion’ (FI). This makes me think more on this subject.

The encyclopaedic meaning of `FI’ is stated to be the delivery of financial service at affordable costs to a vast section of disadvantaged and low income groups of people. Dr C. Rangagarajan, Chairperson of The Committee on Financial Inclusion in India, also confirms with this definition, stating that FI is “The process of ensuring access to financial services and timely and adequate credit

where needed by vulnerable groups such as weaker sections and low income groups at an affordable cost.”

The term `FI’ has gathered momentum since 2000 and this is viewed as a direct weapon for fighting poverty thus complying with the Millennium Development Goals (MDG).

When we say `FI’, this covers both the urban poor and the rural masses. According to UIDAI’s estimates, currently there are around 600 million bank accounts in the country but only 200-250 million individuals have bank accounts since many have multiple accounts. This translates into just 20% of the population having bank accounts. Nearly 90% of the population do not get loans.

This is obviously financial exclusion and many reasons have been stated for such a situation, like, high costs of accessibility, financial illiteracy, attitude of banks and financial institutions.

The once thought successful models like the micro finance institutions and the banks’ lending through NGOs and SHGs are also not trouble free, especially with the recent controversies concerning MFIs. The move by the Andhra Pradesh Government, the State in which MFIs actually had their genesis, to bring them under strict regulations is again a point widely discussed.

On the same note, RBI’s policy to promote new banks with the objective of Financial Inclusion should definitely have a very clear approach. One cannot again go back to the universal banking model but should really focus on extending of banking facilities to those who are hitherto not covered. This may require different kind of products, different kind of systems and governance. Low cost models alone will be viable in under-banked areas. Financing micro and small

enterprises also would form part of Financial Inclusion.

Today, besides the bank branches in the rural and urban places, some of the non-banking finance companies could actually play a more effective role in inclusive finance, because these are the institutions which have a wide range of products to suit the middle and lower middle class groups and they are comparatively easily accessible. It is learnt that Reserve Bank of India’s vision for 2020 is to open nearly 600 million new customers’ accounts and service them through a variety of channels by leveraging on IT.

Leveraging on the government’s financial inclusion agenda, the Unique Identification Authority of India (UIDAI) has decided to pay Rs.50 per enrolment to banks and Life Insurance Corporation of India, which are acting as its registrars, for signing up residents till March 2011. But banks will be paid only when an Aadhaar is generated and not for just opening a new bank account.

Financial Inclusion being a national priority, innovative models should be thought about while a committed will from the policy makers is a must.I invite your views on this subject.

With Best Wishes

T T Srinivasaraghavan President

1

CHAMBER’S ACTIVITIES20th October 2010

Programme on IT Enabled Supply Chain

Management

Businesses world over, are struggling to sustain competitiveness in a rapidly globalizing economy. The challenge lies in creating economic value through innovations and the application of strategic tools. In such a challenging environment, supply chain management has become the most powerful cost reduction tool in the business. Effective supply chain management and creation of value by managing its key factors will help an organisation develop distinctive competence and create a competitive edge.

Information Technology has a substantial role to play in the Supply Chain Management system. The developments in IT have resulted in many possible solutions for managing the supply chain effectively.

To understand more on the usefulness of IT in SCM, the Chamber in association with Quality Council of India organized a half a day programme on 20th October atHotel Deccan Plaza.The programme was handled byMr S N Umakanthan, a qualified Technocrat supplemented with management qualification along with certification as PMP from PMI, Black Belt in Six Sigma from ASQ and e-Commerce from Anna University having over 25 years of rich and extensive experience in Automotive and IT/Electronics Sector and involved in Supply Chain Management.

The core objective of the programme was to make all the participants aware of the various IT systems available

including the web and explain the features and how it helps to integrate the various functions of supply chain like the Upstream(inbound) suppliers, Manufacturing and Downstream (Outbound) customers.

Ms K Saraswathi, Secretary General, welcomed the participants.

In his opening remarks, Mr R Vittal Raj, Chairman of the IT/ITES Committee of the Chamber said IT can completely transform the business especially with regard to Supply Chain Management. Organisations world over which have succeeded are those which have responded to changes first. He said each industry is unique and different. With the kind of population we have, the potential for business is phenomenonal and new markets are opening up.

While this is the case, organisations are now coming up with new strategies to improve their business and this can only be done through the use of IT which would benefit the industry enormously.He said social media like the`Facebook’ is used for customer response and SME’s have been extensively using twitter.In India we have different dynamics of business he said. The challenge is for our software in the Supply Chain Management to capture every bottleneck. IT is playing a very critical role through which information on manufacturing, movement of goods, the demand, and optimizationreaches fast.

He emphasised that this programme is certainly one of the most beneficial programmes for many of the industries and requested the participants to make full use of the same.

He then introduced the speakerMr S N Umakanthan, who opened his speech with a definition ofSupply-Chain, a term that describes

how organizations (suppliers, manufacturers, distributors and customers) are linked togetherand supply chain management is a total system approach to managingthe entire flow of information, materials and services from raw material suppliers through factoriesand warehouses to the end customer.He referred to Porter’s value chain which is a systematic approach for examining the development of competitive advantage. The chain consists of a series of activities that create and build value. He referred to Information Technology as a supply-chain enabler. E-Commerce is buying and selling of products or services over electronic systems like internet and other computer networks.He gave the example of direct delivery model of Dell. He also referred to various brands of ERPs and the basic modules of ERP. He described the advantages of IT enabled JIT (Just-in-Time)delivery and how customer relationship management works.

Mr Umakanthan listed a few of the advantages of `cloud computing’ as:4Anyone can login and do transaction from anywhere since it is web based4No capital investment is required in terms of own servers and software licensing4No maintenance burden4Easy to implement in a short duration4No need to buy the entire range of ERP system which may be a costly affair

The programme ended with a brief Q&A session.

2

CHAMBER’S ACTIVITIES30th October 2010

Food for Thought Programme on “Employment V/s. Unemployability Debate”

The Madras Chamber has recently introduced a `Food for Thought’(FFT) monthly programme. The objective of FFT is to take up larger issues of topical nature which could involve the economy, civil society, business and the community as a whole, and provide a platform for open discussion and interaction.

The programme held on 30th October was on the topic `The Employment V/s Unemployability Debate’.Dr R Mahadevan, Group Technology Director, India Pistons and a Member of the General Committee of the Chamber presided.

In his opening remarks Dr Mahadevan said India is a country of mixed cultures, a culture of diversity. We have the rich, the poor, as well as the highest order of intellectuals and we manage to live with equal comfort. He said we have one of the biggest talent pool in the world and the largest number of engineering graduates

coming out of our colleges every year. It is a quantity improvement in the last 3-4 decades. However, only one-third of our engineering graduates are employable and hence we need to produce employable numbers. There is shortage of skilled labour and many initiatives have been taken by the Government like the setting up of a National Skill Development Mission to meet the needs of emerging India.The Panelists then gave their views as follows:-

Rev.Fr Casimir RajFounder Director, LIBA & Former Director, XLRI

Expressing his happiness to be a Panelist, Fr Casimir Raj said that we have to be watchful of the skills levels of China. India is abundant in population and in the next two decades India will have a populationof 55% below the age of 25 who will be skill-rich, creative and innovative people. India should take this opportunity to make use of it tobe the leader in the world.

In India only about 20 million go to colleges. Coming to the quality, 60% of the Indian universities and 90% of the colleges are below average. He referred to a recent study which shows that fresh graduates need to be trained as they are not employable. Higher education is just not for imparting skills but to impart cutting-edge knowledge he said.

He referred to the current state of affairs wherein one has to go to a coaching centre for additional training to appear for competitive exams like CAT, GMAT etc. He said Government is

not interested in good curriculum but only in giving a certificate. We donot concentrate on the curricula or courses and students do not take the courses seriously. The curriculum should be creative and joyful to learn. Creative people can lead the country he pointed out.

Referring to teachers he said, we need, not just learned teachers, but learning teachers. Good teachers are costly but bad teachers cost more. Teaching is a vocation and unless we do something about the teachers, we cannot offer good education. A teacher has tomake a difference not only in skillsbut also in the character of themselves and the children.

He said we have to rise up, and build really qualitative educational institutions. This can be done onlyby good teachers who can deliverthe knowledge.

Mr V JayanthSenior Associate Editor, The Hindu

Expressing that this subject has been close to his heart, Mr Jayanth said about The Hindu’s initiative in starting The Education Plus as also Education Plus clubs in Andhra Pradesh and Karnataka. He said there is no dearth for colleges but unemployability is a huge problem.The job market is hovering back and the salaries are back to the 2008 levels. The economy is on the upswing and 2011 is going to be a bright year.

Referring to the curricula, he felt it is outdated – there is very little practical work. Companies spend huge sums of money and time to train the students

3

CHAMBER’S ACTIVITIES

coming fresh out of colleges.We need to completely revamp the education system which is a booming industry today.

He wondered how licences are given to about 40-50 colleges every year. He also said we have some successful autonomous colleges who have job-oriented or market-oriented courses. A good autonomous college offers latest courses like mass media, journalism, visual communications, etc. and the students of these colleges find quick employment. He urged that it is time for us to foster industry-institute tie ups. Industry should take over some courses and provide training as well as faculty, he said.

He referred to the job fairs being organized by The Hindu and the Business Line Clubs started by the Hindu-Business Line. The Hindu in association with industry groups has started the Asian College of Journalism and most of the students passing out of this college are absorbed by The Hindu.

Ms Maya NarasimhanPrincipal, TVS Vocational College

Ms Maya referred to a recent survey by a US consultancy company which highlights the fact that in India, more than 60 years after independence, less than 10% of school going students complete their 12th standard. As a result of this, a vast proportion of youth are being turned into unskilled labourers with poor employment and earning capabilities, which in turn, affects the growth of the country.

She referred to another survey which points out that India needs 400 million trained manpower in the next 10 years, which is 40 million a year. In contrast there are only 4 million trained persons available every year, revealing a gigantic gap between supply and demand. This state of affairs

calls urgently for skill development programs of a high standard that will enable our young people to get better jobs and better wages.

The Government has understood the seriousness of the situation and has taken up steps for dealing with the problem by setting up PM’s National Council on Skill Development. She also referred to the ambitious plans for establishing l500 new ITIs and 50,000 skill development centres. But she said this will achieve very little without large scale private investment in the idea of skilling. To bring in private players, the Government needs to loosen up and give up old ways of thinking.

In this age of information technology, she felt it is unfortunate that any kind of information with regard to employment or training statistics is not available. Ministries have outdated information and employment exchanges which have the information are unwilling to part with it. Lack of information makes it difficult for training providers to decide on courses.

Referring to vocational education she said the curricula has to be constantly reviewed and revitalized with inputs from industry and business. Quality in education, besides strict governance, depends so much on the quality of faculty. She said the will to deliver is the need of the hour.

There was floor discussion which followed the presentations. Some of the views expressed were that4corporate training is required to build a person. 4At the ITI level and diploma level, there is much more quality. 4Evaluation of teachers by the students works well in some places. 4 Industry-education should connect and work together and Industry should give value added courses.

4The value systems and creativity should be built from a very younger age and the parents also have a very important role to play.4Many reforms in the education system are required

Mr M Ramakrishnan, Co-Chairman of the Chamber’s Expert Committee on HR proposed the vote of thanks.

4

In the long run, only economic prosperity

can produce progress. And prosperity, in

turn, cannot be willed into existence by

governments. Prosperity arises out of innovation

and enterprise, from the technological

ingenuity and the skills that are housed in the great companies of the world. And from there,

prosperity needs to move seamlessly across the

world so that no country is left behind.- Indra Nooyi

GENERAL COMMITTEE9th October 2010

5

Suggestions for XII Plan 2012-17

Attention of members was drawn to the press report in The Hindu dated 5th October wherein it has been indicated that the Planning Commission has launched a website to elicit suggestions on the Approach Paper to the XII Plan (2012-2017) so as to make the document more inclusive and effective. It is understood from the press report that as of now, the views uploaded on the website would be available only to the officials concerned. However, by the end of this month, a more dynamic version of the website is expected to be launched and this would be more interactive.

The Planning Commission has solicited suggestions from the public as well as stakeholders to help them in preparing the plan document.

The President invited suggestions from members and one of the members agreed to send few actionable points on which members’ views can bebuilt around.

Subsequently the Chamber has sent the Approach Paper to all members indicating the 10 key basic matrics.

These ten areas include:

1. Citizens’ expectations - What are the citizens’ expectations in individual sectors? How can we set targets to reflect these expectations?

2. Governance and Institutions - How does government or public institutions affect us in different sectors? How can we make them work better?

3. Markets - Are markets performing their role in these sectors satisfactorily? How can we improve the functioning of markets?

4. Global Developments - How will global developments affect us in individual sectors? How can we use global developments to our advantage?

5. Demography and Skills - How does the age / sex / geographical/ skill distribution of our population affect our performance or potential? How can we cope with demographic changes already underway?

6. Science and Technology - What kinds of science and technology are available and appropriate? How can we get more useful S&T?

7. Information - Do we all have appropriate information to take informed decisions? How can we improve the availability and usefulness of information?

8. Land Climate and Environment - How does land use and environmental considerations affect us? How do we build strategies to take them into account?

9. Innovation and Enterprise - Are we creating enough innovations and enterprise for inclusive and sustainable growth? If not, how can we do so?

10. Financing the Plan - What are the financial requirements, both public and private of achieving our targets? Can we meet them?

The Chamber’s suggestions will be sent to the Planning Commission shortly.

On setting up of new banks in the private sector, the matter had already been discussed earlier and the Chamber has sent a representation to the RBI. This has also been covered in our Bulletin for September.

Reinventing the Madras Chamber –

report on the progress

The Consultants had now identified five key focus areas and there may be a need to redefine the scope and also the time frame for handholding. Some of the actionable points suggested are already being implemented. The webpage has been redesigned with more features. Communications from the Chamber are now being sent to multiple people in the company unlike only to the Chief Executive or the nominated representative, as in the past. It was felt the Consultants could be involved in our plans to improvise the web page as one of the focus areas suggested by them is enhancing our digital presence.On the membership drive, a list of potential companies has been prepared and letters and emails inviting them to become members are being sent. The special focus is on new generation industries like healthcare, hospitality, BPOs, etc. and others.

Food for Thought Breakfast meeting -

October 2010

Under War for Talent the Chamber had organized some programmes 3-4 years ago with the participation of academia and industry representatives. It was not possible for the Chamber to organize it on a large scale. However, it created some awareness about the

GENERAL COMMITTEE

6

employability gap. The State churns out a large number of graduates every year but they are not employable and need to be trained further. We are still grappled with the same problem.During October, it was proposed to have a `Food for Thought’ programme on The Employment V/s Unemployability.

Programme on GST, DTC & IFRS atSriperumbudur

It is proposed to organize a programme on taxation at Sriperumbudur with the support of Hyundai Motors and Hiranandani in the month of November since a number of SMEs are located there. This will enable the Chamber to reach to such of those companies located outside Chennai and to take the Chamber’s expertise especially on Finance and Taxation to these companies.

Forming a Committee for setting up a MCCI

Training Centre

The Chamber has purchased land at Koppur Village on Thiruvallore-Sriperumbudur High Road. (9 Kms from Sriperumbudur). The land is on the main road with good accessibility. Efforts are being made with the help of VAO & Panchayat Board officials to convert the land from Agricultural to Commercial use. Since the land is in a potential industrial place with a number of manufacturing companies situated in and around, a suggestion was put forth whether the Chamber may consider setting up a Skill Development Centre, preferably tying up with one or two leading industries.

Appropriate Government scheme could be tapped if set up as PPP model.

The Committee considered the matter and suggested the following:

4Meet the HR Managers of industries in and around that area and makea survey as to what types of skillsare required4Start training in 2/3 skills 4Seek Government funding

A small committee is to be formed under the Chairmanship ofDr R Mahadevan of India Pistons toguide the Chamber to take this initiative further. It was felt that apart from imparting training in skills like fitter, turner, electrician, etc. there was also great demand for soft skills, training in administration, accounts, etc.

EmergingEntrepreneurs – To partner with a Fund

A member suggested that there are many people who do not know how to access capital. The Chamber should spot youngsters who have ideas but do not have capital to start their own enterprises. If the Chamber canorganize funding 10 entrepreneurs a year, and bring them into the limelight, this would be a brand building exercise for the Chamber. It was felt that Chamber can be a catalyst in promot-ing new entrepreneurs.

I will put together a number of ideas which allow us to

think about what India can be. If we can totally leverage the strength of India, which is this huge population base,

we can create 200 million graduates and 500 million

trained professionals in every fi eld of human endeavor. Whether it is a carpenter,

whether it is an electrician, whether it is a cab driver,

whether it is a brick layer, it does not make any diff erence to me. Professionally trained,

professional conduct and ethics and at the same time compensated appropriately, and each one of them will be able to compete with

anybody else in the world. Th at means, we train them

with global standards in mind. Th ere are very few countries that can even

aspire to be like us.We can do it because of India’s size. And if we

do it we can become an intellectual hub, not only for India’s development but for global development and it

will make a huge diff erence to the quality

of life for every Indian.

-C.K. Prahalad

12th October 2010

Environment, Pollution Prevention& Control

A representative of one of the member companies of the Chamber brought out some crucial issues faced by the Chemical companies situated at SIPCOT, Cuddalore.

The Committee expressed its concern on the issues raised and felt that those affected should take up the matter seriously and also provide all the related documents giving the facts of the matter to the concerned authorities and seek an amicable solution.

Chamber’s website:The Committee felt that the Chamber could try and place the latest amendments and important notifications issued by the TNPCB and other related agencies in the MCCI website.

Work plan for the year:A number of programmes were suggested to be organized during the year among them being conducting a programme under the title `Responsible Care for Industries’, inviting the TNPCB Chairman and senior officials for an interactive meet with our members and a Training Programme on OHS.

The Chamber will try to get inputs from Chambers in Andhra, Karnataka and Kerala, to understand some of the best pollution control practices being followed in these States.

14th October 2010

Energy

The Committee decided to organize a full day programme on 14th December which is the National Energy Conservation Day. The main focus of the programme would be Energy Efficiency. The tentative topics were identified by the Committee.A climate change team from UK is expected to visit Chennai during January / February 2011 and the Chamber is exploring the possibility of organizing a joint programme with them.

19th October 2010

Company Law/Corporate Matters

The Committee suggested organising an IFRS programme not only in Chennai but also in other places like Coimbatore, Madurai and Sriperumbudur. The programme is likely to be held in the first week of January 2011 at Coimbatore. The Committee suggested that sector wise programmes on IFRS could also be planned since manufacturing, real

estate, pharma and finance have major impact in IFRS system.

Other programmes suggested were: (a) Interaction with Officials of MCA, New Delhi and Chennai,(b) Investor Awareness Programme jointly with reputed institutes and stock exchanges and(c) Seminar on India’s Capital Market: Companies Bill 2009 – Report of the Standing Committee on Finance

The Companies Bill 2009 had been handed over to the Standing Committee on Finance and the Standing Committee had submitted its recommendations to the Ministry. Hopefully the Companies Bill 2009 would be placed in the Parliament in the forthcoming winter session. MCCI had given its recommendations to the Standing Committee. The Committee viewed that there are still a number of issues which are yet to be looked into by the Ministry. Some of the major issues of concern were:4Subsidiaries 4Managerial Remuneration 4 CFO Salary 4Voluntary Corporate Governance 4 Auditors Appointment

The Chamber would send a representation to the MCA after getting inputs from members.

EXPERT COMMITTEES

7

Whenever society is stuck or has an opportunity to seize a new opportunity, it needs an entrepreneur to see the opportunity and then

to turn that vision into a realistic idea and then a reality and then, indeed, the new pattern all across society. We need such entrepreneurial leadership at least as much in education and human rights as we do in communications and hotels. This is the work of social entrepreneurs.

-Bill Drayton

EXPERT COMMITTEES

8

26th October 2010

IT / ITES

Members felt that to attract membership from IT companies, more specialized programmes and activities on IT related subjects should be taken up.

MCCI websiteA number of new features are being added to the current website. A demo of the new site was given and members were requested to give their views. The re-designing of the website with a number of useful features for members is under process.

Work plan for the yearThe Committee discussed the opportunities for SMEs in IT sector and decided to plan a programme for SMEs to sensitise them about the

usefulness of technological tools likeIT for their businesses.

Members were requested to provide articles for the Chamber’s monthly bulletin `Chamber In –Touch’.

28th October 2010

Direct Taxes

The Committee considered the work plan for the year and decided to organize a Seminar on Transfer Pricing - Current Trends and Recent Decisions covering subjects like Transfer Pricing & Intangibles, Approaches to Transfer Pricing, Case studies on transfer pricing and compliance and documentation.

The Committee felt that the revised discussion paper on DTC had been passed on to the Standing Committee

on Finance to finalise the document. It is likely that this might be placed in the Parliament during the forthcoming session. However DTC would be effective from April 2012. To educate the tax and finance executives over the implications of DTC, the committee decided to organize suitable capsule programmes and also identified the topics to be covered.

Tax Issues in Real Estate Sector

It was felt that a number of issues, both on Direct and Indirect taxes,are emerging from the real estate sector and a specialised programme could be planned by the Chamber. This programme would be scheduled in consultation with Indirect taxes Committee.

REPRESENTATIONS

Mr Rajeev Ranjan, IAS., 29th October 2010 Principal SecretaryIndustries DepartmentGovernment of Tamil NaduFort St GeorgeChennai 600009.

The Secretary to the Deputy Chief MinisterGovernment of Tamil NaduFort St. GeorgeChennai 600009.

Dr. V Irai Anbu IAS.,Secretary to GovernmentEnvironment & Forest DepartmentGovernment of TamilnaduFort St.GeorgeChennai 600009.

Dear Sir

Sub: SIPCOT Phase I & II at Cuddalore – request for recommending to Ministry of Environment & Forest, (MoEF), Government of India, for lifting of temporary restriction on setting up / expansion / modernization of industries in the above area.

Tamil Nadu is one of the well-developed States in terms of industrial development. The State has emerged as one of the front-runners by attracting a large number of domestic and foreign investments.The Government of Tamil Nadu have taken up a number of policy initiatives to facilitate growth in the manufacturing sector. The State for many years has strong manufacturing culture. The Government has also been offering composite in principle approval on a fast track mode for many projects in the Industrial Estates developed by SIPCOT. The major industries in the manufacturing sectors in Tamil Nadu are, Sugar, Leather, Textiles, Chemicals, Petrochemicals, Fertilizers, Cement, Paper, Engineering and Automobile industries. Tamil Nadu is now in the third position in industrialization thanks to investor friendly policies.

The State Industries Promotion Corporation of Tamil Nadu(SIPCOT), has played a major role in developing Industrial Estates in different parts of the State for the promotion of industries by providing necessary infrastructure and incentives. Among the Industrial Estates developed by SIPCOT, Cuddalore has been in existence since 1984, where a large number of Pharma and Chemical industries have been established.The SIPCOT, Cuddalore, has Phase I and Phase II spread over an area of 700 acres of land. The industrial estate has a total of 60 industries over the years, 55 industries in Phase I and 5 in Phase II. However, today only 31 (26 in Phase I and 5 in Phase II) industries are in operation.

The Tamil Nadu Pollution Control Board (TNPCB) since its formation has been monitoring the environmental status of SIPCOT Cuddalore area and has been regulating the industries by issuing directions and action plans to improve environmental performance.

Central Pollution Control Board (CPCB), in association with Indian Institute of Technology,(IIT) Delhi, carried out an environmental assessment of industrial clusters across the country based on which, a Comprehensive Environmental Pollution Index (CEPI) was developed. The main objectives of the study are as follows.4Identifying critically polluted industrial clusters/areas from the point of view of pollution and taking concerted action and for being centrally monitored at the national level to improve the current status of

9

The Chamber has sent a representation to the Government of Tamil Nadu for lifting of temporary restriction at SIPCOT Phase I & II at Cuddalore.

REPRESENTATIONSenvironmental components, for example, air and water quality data, public complaints, ecological damage, and visual environmental conditions.4To facilitate the definition of critically polluted industrial clusters/areas based on the environmental parameter index and prioritization of an economically feasible solution through the formulation of an adequate action plan for environmental sustainability.CEPI is a rational number to characterize the environmental quality at a given location following the algorithm of source, pathway and receptor. The index captures the various health dimensions of environment including air, water and land.

A total of 88 industrial clusters were selected across India for CEPI study. The analysis was done based on data available on hand pertaining to the year 2007 and earlier. Industrial clusters having CEPI score of 70 and above were declared as critically polluted. 43 industrial clusters fell in this category and 4 out of them were from Tamil Nadu, namely, Manali(Chennai), Ranipet, Vellore District, SIPCOT I & II Cuddalore and SIPCOT Coimbatore.The respective State Pollution Control Boards were informed about this and were asked to report on the action plans to improve the environmental performance in the industrial clusters. As per Office Memorandum of MoEF dated 13th January 2010, a review of the study was proposed during August 2010 and until such time of review, a temporary restriction on setting up of new industries / expansion or modernization of existing industries was invoked.

As a sequel to the announcement by MoEF, TNPCB had taken stock of the situation and had directed the individual industries within the clusters, with action plans to improve the environmental performance.With specific reference to SIPCOT Phase I & II, Cuddalore, the TNPCB had given various action plans to the individual industries. TNPCB also made the entire analysis of CEPI based on recent analytical studies prepared by them and also from third party labs as per their directions. TNPCB has presented a detailed report to CPCB and MoEF during the review meetings in August 2010, about the latest environmental status pertaining to Cuddalore.

The TNPCB report for Cuddalore Phase I & II presented the current improved status on the following:I. Water: Present status of water environment with latest analytical reports. The report compares the status as of 2009-10 with 2010-11 and the improvement that has happened because of the implementation of action plans. It also gives the current status of various other action plans given to the industries within the cluster. It concludes the CEPI score for water environment at present is 50 which is normal as per CEPI nomenclature against a score of 65.25 in the original study by CPCB – establishing a significant welcome improvement. II. Air: Present status of the ambient air quality in Cuddalore SIPCOT Phase I and II. The report presents reduction in VOC (Volatile organic compounds) when compared with the data of 2009. It lists the various air pollution control measures adopted by every industry and concludes that the recalculated CEPI score is 28 which is well within normal value as per CEPI nomenclature as against a score of 54 in the original study by CPCB – a significant improvement.

III. Land (Soil): Present status of soil environment with reports from NGRI Hyderabad and also the ground water status were analyzed by TNPCB. Based on these studies TNPCB concludes that there is no significant pollution because of the industrial activity and also says that River Uppanar (Salty backwater river), has a major impact on the ground water salinity based on Hydro geological study. There calculated CEPI score for Land/soil is 33.5 (which is well within the normal level) as against the score of 64 in the original report as per CEPI nomenclature.

IV. Conclusion: As per TNPCB study, the overall CEPI score was 54.69 based on recent analysis as against 77.45 based on data pertaining to 2007 and earlier as stated in CPCB study. The reduction in score signifies considerable improvement in the environmental status of the cluster over the past three years.

It is also pertinent to note that industries in the Cuddalore area have made considerable investment in Zero Liquid Discharge plants. Also, TNPCB have rolled out a new Care Air initiative in Cuddalore, amongst other regions in the State, wherein individual units are connected online to TNPCB who can monitor in real-time the air emissions data.

10

REPRESENTATIONS

Given all this, and based on the results of their action plan, TNPCB made a detailed presentation before CPCB and MoEF in August 2010 seeking a removal of temporary restriction with respect to Cuddalore. CPCB and MoEF are yet to come out with their final decision.

We understand that even though the environmental performance of Cuddalore industrial cluster has improved significantly, as evident from the TNPCB studies, there is a delay in the review to lift the temporary restriction imposed on Cuddalore. This is causing serious concern to the industries in this cluster as even legitimate expansions are being put on hold, at great cost to the industrial development of the State and the country.This delay will also be an impediment to the Tamil Nadu Government’s objective of creating a Petrochemical and Petroleum Investment Region (PCPIR) from Cuddalore - Nagapattinam.

We are also given to understand that State Governments and Pollution Control Boards of other States namely, Maharashtra, Gujarat, Andhra Pradesh, Karnataka etc., have taken up the issue relating to clusters in their States with CPCB and MoEF, Government of India, seeking the removal of temporary restriction on industrial expansion / modernization.

To conclude, we request the Government of Tamilnadu to strongly represent, to the Government of India, for the immediate removal of the temporary restriction on industries in the Cuddalore area for the following reasons:

4The CEPI score relied upon by the CPCB and MoEF is based on old, 2007 data4More recent data pertaining to 2010, as evidenced in the TNPCB study, reveals the CEPI score as 54.45 , well within the normal levels4Significant improvements, including investment in Zero Liquid Discharge plants, as also a first-of-its-kind initiative in the nature of Care Air, have been implemented by units at Cuddalore4In the absence of the removal, industries which have made significant investments in their plants and have also proved to be responsible corporate citizens by implementing environmental solutions, are prevented from legitimate expansions – such restriction will also prove to be an impediment to sustained industrial growth in the State of Tamilnadu

We would be grateful for early action in this regard. We would be happy to provide any further information that may be required.

Thanking you,

Yours faithfully,

Sd/………..

K. SaraswathiSecretary General

cc: The Member Secretary Tamil Nadu Pollution Control Board Guindy Chennai 600032.

11

Water 65.25 50.00

Air 54.00 28.00

Land 64.00 33.50

Overall 77.45 54.69

CCEPI Score as per TNPCB study based

on 2010 data

CEPI Elementdescription

CEPI Score as per Original CPCB Study

(2007 and earlier data)

POLICY WATCH

New Telecom licence renewal policy soon

The Department of Telecommunications is planning to issue fresh guidelines that would allow telecom operators to continue using the spectrum after the expiry of their licence period which is 20 years from the day of issue of a licence.The DoT has decided to take this step to do away with any kind of ambiguity on the issue as there were no clear guidelines now for the renewal of licences. It would also help the government generate revenues once these telecom companies approach them for renewal of their licences.

Micro finance institutions (MFIs) –Subpanel to submit report

Amid growing criticism over the use of coercive ways of micro finance institutions to recover loans, the RBI is looking into the functioning of such lenders and its sub-panel wouldsubmit its report in 3 months.The RBI has set up a sub-committee of the Central Board of Directors of the Central Bank to study the issues and concerns of the microfinance sector, including interest rates charged by the lenders in this area. Mr Y H Malegam, senior member on the Central Board of Directors of RBI will chair the sub-committee.

India-EU FTA unlikely by December

Formal signing of the long negotiated India-European Union Free Trade Agreement is unlikely during PM’s visit to Europe in early December. Sharp differences on various issues including public procurement and the list of

sensitive items are likely to delay the process.The signing of the treaty is likely to stretch into early next year – in all probability in May or June 2011.

Ceiling for retail investors in public issues doubled –SEBI defers decision on the much awaited takeover norms

The Securities and Exchange Board of India has decided to increase the maximum application size for retail individual investors to Rs 2 lakh across all issues.

However, SEBI has deferred a decision on the much awaited takeover norms, recommended by the Achuthan Committee.

RBI targets inflation forcefully

The Reserve Bank of India’s unrelenting focus on inflation was once again in evidence. This time the policy stance is intended to (a) contain inflation and anchor inflationary expectations while being prepared to respond to any further build up of inflationary pressures; (b) maintain an interest rate regime consistent with price, output and financial stability and (c) actively manage liquidity to ensure that it remains broadly in balance.

Mega container terminal proposal gets clearance

The Cabinet Committee on Infrastructure recently approved the proposal for construction of a Mega Container Terminal at Chennai Port

involving an investment of Rs 3,680 crore. The new terminal will change the face of the port. The earlier proposal of `dirty’ cargo (coal and mineral) being shifted to the Ennore Port will be taken up again.

The project would be developed under the Public Private Partnership mode and implemented on the Design, Build, Finance, Operate and Transfer basis.The investment by the concessionaire would be Rs 3125 crore and Chennai Port would invest Rs 561 crore. The mega container terminal would have the capacity to handle 4 million TEUsper annum.

The terminal will be able to handle ultra large container vessels and deep draft vessels. It will enable Chennai Port to compete with international ports and reduce the need for trans-shipment from Singapore and Colombo.It will boost import and export fromthe region.

TNEB reorganized

The 53-year old Tamilnadu Electricity Board ceased to exist with effect from 1st November 2010 with the reorganization of the Board into the holding company, TNEB Ltd., and two subsidiaries, Tamilnadu Transmission Corporation (TANTRANSCO) and Tamilnadu Generation and Distribution Corporation. (TANGEDCO).

12

Happiness is not the absence of problems but the ability to deal

with them.

-Jack Brown

POLICY WATCH

13

Highlights of theSecond Quarter Review of Monetary Policy 2010-11

On the basis of the current assessment and in line with the policy stance, the Reserve Bank announced the following measures on 2nd November 2010.

Bank Rate 4The Bank Rate has been retained at 6.0 per cent.

Repo Rate It has been decided to: 4increase the repo rate under the liquidity adjustment facility (LAF) by 25 basis points from 6.0 per cent to 6.25 per cent with immediate effect.

Reverse Repo Rate It has been decided to: 4increase the reverse repo rate under the LAF by 25basis points from 5.0 per cent to 5.25 per cent with immediate effect.

Cash Reserve Ratio The cash reserve ratio (CRR) of scheduled banks has been retained at 6.0 per cent of their net demand and time liabilities (NDTL).

Expected Outcomes These actions are expected to: a) Sustain the anti-inflationary thrust of recent monetary actions and outcomes in the face of persistent inflation risks. b) Rein in rising inflationary expectations, which may be aggravated by the structural nature of food price increases. c) Be moderate enough not to disrupt growth.

TAMIL NADU ORDINANCE NO. 5 OF 2010An ordinance to amend the Tamilnadu Sales Tax (Settlement of Arrears) Act 2010

Whereas the Legislative Assembly of the State is not in session and the Governor of Tamilnadu is satisfied that circumstances exist which render it necessary for him to take immediate action for the purpose hereinafter appearing.Now, therefore, in exercise of the powers conferred by clause (1) of Article 213 of the Constitution, the Governor hereby promulgates the following Ordinance:1. (1)This Ordinance may be called the Tamilnadu Sales Tax (Settlement of Arrears) Amendment Ordinance 2010. (2)It shall come into force at once.2. In section 2 of the Tamilnadu Sales Tax (Settlement of Arrears) Act 2010, (hereinafter referred to as the principal Act) in subsection (1) in clause (b) for the expression `for which assessment has been made prior to the 1st day of April 2007’, the expression `upto the assessment year 2006-07, for which assessment has been made prior to the 1st day of June 2010’ shall be substituted.3. In section 4 of the principal Act, for the expression `in respect of which assessment has been made under the relevant Act, prior to the 1st day of April 2007, the expression “upto the assessment year 2006-07 in respect of which assessment has been made under the relevant Act, prior to the 1st day of June 2010” shall be substituted. Surjit Singh Barnala Governor of Tamilnadu

Good management is the art of making problems so interesting and their solutions so constructive that everyone

wants to get to work and deal with them.

14

4Process, Engineering, Plant Equipment 4Automation 4Environment & Water Technology 4Pumps & Valves 4EPC -Engineering Procurement Construction

4Pharma, Plant & Machinery 4Packaging Machines & Services 4Biotechnology & Application 4Analytical & Laboratory Systems 4Consulting Services.

Chemtech + Pharma-BIO-Tech World Expo 2011 23rd to 26th February 2011

`The Ministry of Chemicals & Fertilizers’ is supporting Chemtech World Expo 2011. Leading International Associations and Indian Associations are supporting this event.

MCCI is a supporter of this event.We invite our members to participate in this EXPO.

For more info log on to our website www.madraschamber.in

`The CHEMTECH + PHARMA-BIOTECH WORLD EXPO 2011’

International Exhibition and conference is taking place in Mumbai,

and will witness participation from all major national private and public sector and

International companies associated with the Chemical & Petrochemical Industry.

25th edition of

CHEMTECH | PHARMA-BIO | INDUSTRY AUTOMATION & CONTROL | WATEREX World Expo 2011will be organized from

23rd to 26th February 2011 at Bombay Exhibition Centre, Goregaon (East), Mumbai.

The event will cover the following segments:

Water Expo 2011

Water Today’s Water Expo 2011, an International Exhibition and Conference on Water and Waste Water Management will be held at Chennai Trade Centre from 16th to 18th March 2011.

The Expo will highlight the latest technologies and developments in the field of water and wastewater management. This mega event will bring together suppliers and users of various water related services and products on one platform. This year the special focus will be on Packaged Drinking Water Industry.Water has a significant role to play in the industry as they have to be aware of the pressing concerns, environment issues and water quality needs for the industry.

Your participation in this Expo will help you to:

4Network with local and international water andwastewater technology providers.4Get the latest knowledge in water and wastewatertreatment technologies.4Get first hand information on opportunities for newwater and waste water projects.4Discover strategies for sustainable water and wastewatermanagement.4Develop and enhance understanding of water and wastewater issues confronting the country.

MCCI is partnering Water Today in the organisation of Water Expo 2011.For more information, please log on to

www.waterexpo.biz

15

SPOTLIGHTFinancial Inclusion

On 29th December 2003, former UN Secretary-General Kofi Annan said “The stark reality is that most poor people in the world still lack access to sustainable financial services, whether it is savings, credit or insurance. The great challenge before us is to address the constraints that exclude people from full participation in the financial sector. Together, we can and must build inclusive financial sectors that help people improve their lives.”

According to the United Nations the main goals of Inclusive Finance are as follows:-

1. Access at a reasonable cost of all households and enterprises to the range of financial services for which they are ‘bankable,’ including savings, short and long-term credit, leasing and factoring, mortgages, insurance, pensions, payments, local money transfers and international remittances

2. Sound institutions, guided by appropriate internal management systems, industry performance standards, and performance monitoring by the market, as well as by sound prudential regulation where required

3. Financial and institutional sustainability as a means of providing access to financial services over time

4. Multiple providers of financial services, wherever feasible, so as to bring cost-effective and a wide variety of alternatives to customers (which could include any number of combinations of sound private, non-profit and public providers).

The major three aspects of Financial

Inclusion make people to4Access financial markets4Access credit markets4Learn financial matters (financial education)

Financial Inclusion includes accessing of financial products and services like,4Savings facility4Credit and debit cards access4Electronic fund transfer4All kinds of commercial loans4Overdraft facility4Cheque facility4Payment and remittance services4Low cost financial services4Insurance (Medical insurance)4Financial advice4Pension for old age and investment schemes4Access to financial markets4Micro credit during emergency4Entrepreneurial credit

Financially Excluded People;The financially excluded sections largely comprise4Marginal farmers4 Landless labourers4Oral lessees4Self employed and unorganised sector enterprises4Urban slum dwellers4 Migrants4 Ethnic minorities and socially excluded groups4 Senior citizens4Women4The North East, Eastern and Central regions contain most of the financially excluded population.

Factors affecting access to financial services4Legal identity4Limited literacy

4 Level of income 4Terms and conditions 4Complicated procedures4 Psychological and cultural barriers 4 Place of living 4 Lack of awarenessConsequences of Financial Exclusion - Major two threats :4 Losing opportunities to grow 4 Country’s growth will retard

Other Consequences :4Business loss to banks4Exclusion from mainstream society4 All transactions cannot be made in cash 4 Loss of opportunities to thrift and borrow4 Employment barriers 4 Loss due to theft4 Other allied financial services

Benefits of Inclusive Financial Growth4 Growth with equity 4 Get rid of poverty4 Financial Transactions Made Easy4 Safe savings along with financial services4 Inflating National Income 4 Becoming Global Player

Expectations of poor people from financial system taking into account their4 Seasonal Inflow of Income from agricultural operations4 Migration from one place to another4 Seasonal and irregular work

availability and income; the existing financial system needs to be designed to suit their requirements4 Security and safety of deposits4 Low transaction cost4 Convenient operating time4 Minimum paper work

Financial Inclusion for Inclusive Growth-An overview

16

SPOTLIGHT

Overcoming high costs, financial illiteracy and self-exclusion by the poor is needed to bring banking to the urban underprivileged.The country’s urban population is increasing at a faster rate than the total population. By 2030, about 40% of Indians will be living in cities and towns compared to the current proportion of 30%, according to a recent study by McKinsey Global Institute.

This will also lead to an increase in the number of urban poor, currently pegged at 80 million by NSSO in a report. It is this large section of the population that lacks access to even the most basic banking services: savings accounts, credit, remittances and payment services, financial advisory services, amongst others. In order to facilitate financial inclusion in this segment, we need to first understand the reasons and sources of financial exclusion, which are quite distinct from the financial exclusion of rural India. Urban financial exclusion typically results from the inability to access necessary financial services in an appropriate form.

Urban financial exclusion is also a result of problems with conditions imposed, pricing, marketing or self-exclusion in response to negative experience, or actual or perceived absence of benefits in betterment of their social or economic conditions.

Physical access is not a critical issue for financial exclusion among the urban poor.

PricingBanks and financial institutions running financial inclusion initiatives tend to incur a high cost due to inactive accounts with insufficient or nil balances.

However, in the context of the urban poor, extension counters and mobile banking services along with appropriate technologies — biometrics and handheld collection devices — can be low cost solutions to achieve reach within limited geographical areas with high density of potential clients. The price here not only includes the cost of service by the service provider, but the cost incurred by the client in availing the service, e.g., loss of wages due to involvement of the client in availing the financial service.

It has been observed that the urban consumer is more comfortable in paying electricity bill with late payment once a quarter than paying on a monthly basis as the loss of wages is more than the penalty incurred in case of non-regular payment.

Establishing identityAbsence of relevant know your-customer (KYC) documents is perceived as a key reason for financial exclusion given the profile of the urban poor:Migrants from the same state or other states,Living in ghettos and groups (4-5 individuals living in one room) with no independent references,Employed in unorganised sector,

frequent job changes and inability and cost implications for the bank to verify addresses in distant villages. The above are not unsurmountable as there are several government schemes and regulations that have created identities for a large section of the urban underprivileged to satisfy the KYC criterion and the UID project will be a huge step in this direction.

Lack of financial literacy or marketing: Insufficient effort at creating financial literacy is an important reason for urban financial exclusion. Efforts at spreading financial literacy by banks and other financial institutions among the urban poor have been limited — and probably restricted to the metros — as this social class is not perceived to be an economically viable banking proposition.

However, a recent study by the Skoch Development Foundation shows that there is a huge need for savings, insurance and remittance products for the urban low-income and weaker sections. Thus, technology and product innovation with a clear profitability objective can — like in the telecom sector—achieve the goal of a mass-based and profitable service through economies of scale.

Self-exclusionSelf-exclusion by the urban poor is a critical issue. Given the low income levels and absence of meaningful surplus along with uncertainties in income, interest rates on small periodic savings cannot compensate

Financial inclusion:Game changer for urban renewal

Courtesy: Economic Times - September 20, 2010Author: Rana Kapoor, Founder Managing Director and CEO of Yes Bank

17

SPOTLIGHT

the cost and effort in frequentwithdrawals needed for daily or weekly consumption.

With daily wage earners either as labourers, household help or small entrepreneurs like tailors, carpenters, cobblers, autorickshaw drivers, handcart vendors, hawkers, plumbers, mechanics, dabbawallahs, etc, time involved in banking activities means time lost on earning livelihood. Hence, doorstep banking on a periodic basis is a key requirement for this segment and anything involving more time from their side has very low marginal utility. In urban areas, building peer pressure is a difficult task for institutions as well as individuals, and hence, institutions following only the group methodology fail to deliver the services. However, the urban poor need to be clearly educated about the benefits of compulsory and forced savings and insurance. Insurance premium with no immediate benefit but a protective cover against financial shocks in the form of ill-health or death or accident or loss of productive assets is considered a wasteful expenditure that their incomes can ill-afford.

A bank remittance product that saves time, cost — informal channels of money transfer charge large fees — and risk of loss is the first step to get the urban poor and weaker sections introduced to the benefits of banking.

This literacy would be a key turning point towards sustainable financial inclusion, especially in the urban poor. These products should be designed considering the credit needs, earning patterns, riskbearing ability and bankability of the individual. While there are several challenges in achieving urban financial inclusion, two macro-enablers, the Unique

Identification Authority of India (UIDAI) and National Payment Corporation of India (NPCI), will take the financial inclusion to the next level. The UIDAI has two core objectives: to provide a unique ID to every Indian citizen basis biometrics and to authenticate any citizen based on this UID. This mega-project is unparalleled in its scope and scale, and the UID and ancillary developments will usher in massive socio-political changes, especially through successful facilitation of targeted benefit programmes by enabling financial inclusion and these developments will also radically change how banking is done in the country. The biggest roadblock in financial inclusion has always been the difficulty in establishing identity. Now, with the UID project establishing recognition on the basis of biometric details — fingerprints, photograph and iris scan — banks will be able to identify customers, thus taking care of KYC issues and use the UID based authentication service to process transactions. Innovative solutions leveraging UID authentication ability can bring about the true last-mile connectivity. In conjunction with the work being done by the UIDAI, the National Payments Council of India (NPCI) has also been mandated with creating the financial infrastructure on several major projects: other than managing the National Financial Switch (NFS)for domestic ATMs, the NPCI is working on creating a National Automated Clearing House (ACH) system, a switch for mobile-to-mobile payments — called India Pay Mobile Switch — and creating an infrastructure to enable UID-to-UID micropayments.

The vision is to link the UID to a bank account and a mobile number in a central database. Once this

mapping is done, a payment can be initiated through any bank or mobile phone-enabled business correspondent, and routed to the beneficiary’s UID or mobile number, and this will be automatically credited to the bank account linked to that UID.

The UID-based payments initiative, coupled with the mobile payments switch, is going to be a major enabler for financial inclusion, and has the potential to completely redefine the country’s payments landscape, a representation of which is given in the accompanying graph. The UID and NPCI infrastructure, supported by bank and associated business correspondent or retailer networks, can help bridge the banked-unbanked divide by enabling channels like micro-ATMs and mobile banking.This transformation will be further accelerated in urban areas covered by Jawaharlal Nehru National Urban Renewal Mission (JNNURM) as its sub-mission for providing basic facilities for urban poor is creating a complementary infrastructure to facilitate financial inclusion. Banks will also need to gear up to meet the challenges of managing a significant increase in the number of customers and transactions, while improving service levels across all channels and developing market-based solutions for financial inclusion that address the unique requirements of the bottom-ofpyramid market.

The immediate effect of these macro-projects will be demonstrated in the urban areas, where banks can leverage their existing infrastructure to enable and closely monitor urban financial inclusion programmes.

18

ECONOMIC REVIEW

ECONOMY

WPI food Inflation at 12.30 per centAnnual food inflation based on the Wholesale Price Index (WPI) stood at 12.30 per cent for the week ended October 30, 2010 as against 12.5 per cent a year ago. Food inflation for the previous reported week was recorded at 12.63 per cent on a year-on-year basis.

The index for major group of ‘Primary Articles’ rose by 0.3 per cent. The index

for ‘Food Articles’ group rose by 0.4 per cent for the previous week due to higher prices of barley, fruits & vegetables, egg, fish-inland, poultry chicken and gram.

The index for ‘Non-Food Articles’ group declined by 0.1 per cent for the previous week due to lower prices of gaur seed, raw silk, niger seed and cotton seed.

The index for major group of ‘fuel, power, light & lubricants’ remains unchanged at its previous week’s level 10.67 percent.

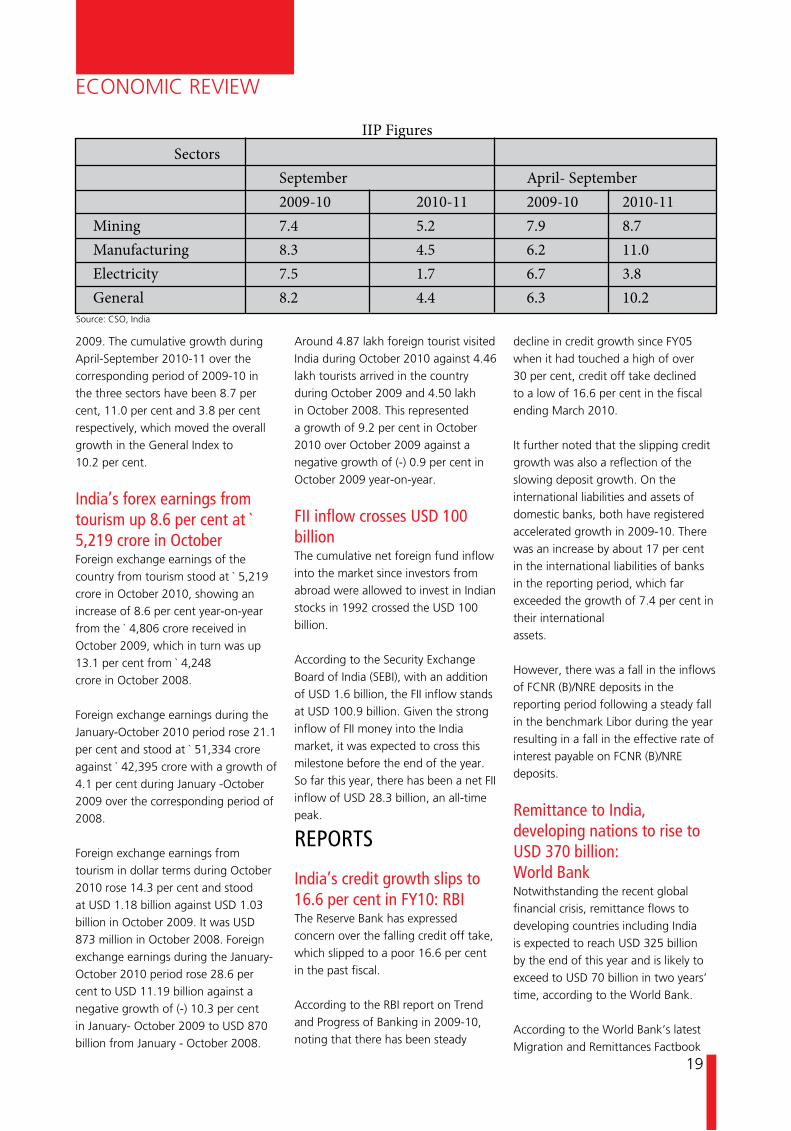

Industrial output growth dips to 4.4 per cent in September 2010Industrial production in the country grew at an even slower pace of 4.4 per cent year-on-year in September 2010 against the 5.6 per cent growth recorded in the previous month.

The indices of Industrial Production for the Mining, Manufacturing andElectricity sectors for the month of September 2010 recorded growth rates of 5.2 per cent, 4.5 per cent and 1.7 per cent as compared to the September

Highlights

ECONOMY

4 WPI food Inflation at 12.30 per cent

4 Industrial output growth dips to 4.4 per cent in October 2010

4 India’s forex earnings from tourism up 8.6 per cent at ` 5,219 crore in October

4 FII inflow crosses USD 100 billion

REPORTS

4 India’s credit growth slips to 16.6 per cent in FY10: RBI4 Remittance to India, developing nations to rise to USD 370 billion: World Bank4 India has above ground gold stocks worth USD 800 billion: WGC

INTERNATIONAL

4 Trade defi cit in U.S. shrinks as exports climb to two-year high4 China infl ation spikes in October 20104 Euro area GDP up by 0.4 per cent

19

ECONOMIC REVIEW

2009. The cumulative growth during April-September 2010-11 over the corresponding period of 2009-10 in the three sectors have been 8.7 per cent, 11.0 per cent and 3.8 per cent respectively, which moved the overall growth in the General Index to10.2 per cent.

India’s forex earnings from tourism up 8.6 per cent at ` 5,219 crore in OctoberForeign exchange earnings of the country from tourism stood at ` 5,219 crore in October 2010, showing an increase of 8.6 per cent year-on-year from the ` 4,806 crore received in October 2009, which in turn was up 13.1 per cent from ` 4,248crore in October 2008.

Foreign exchange earnings during the January-October 2010 period rose 21.1 per cent and stood at ` 51,334 crore against ` 42,395 crore with a growth of 4.1 per cent during January -October 2009 over the corresponding period of 2008.

Foreign exchange earnings from tourism in dollar terms during October 2010 rose 14.3 per cent and stood at USD 1.18 billion against USD 1.03 billion in October 2009. It was USD 873 million in October 2008. Foreign exchange earnings during the January-October 2010 period rose 28.6 per cent to USD 11.19 billion against a negative growth of (-) 10.3 per cent in January- October 2009 to USD 870 billion from January - October 2008.

Around 4.87 lakh foreign tourist visited India during October 2010 against 4.46lakh tourists arrived in the country during October 2009 and 4.50 lakh in October 2008. This represented a growth of 9.2 per cent in October 2010 over October 2009 against a negative growth of (-) 0.9 per cent in October 2009 year-on-year.

FII inflow crosses USD 100 billionThe cumulative net foreign fund inflow into the market since investors fromabroad were allowed to invest in Indian stocks in 1992 crossed the USD 100billion.

According to the Security Exchange Board of India (SEBI), with an addition of USD 1.6 billion, the FII inflow stands at USD 100.9 billion. Given the stronginflow of FII money into the India market, it was expected to cross this milestone before the end of the year. So far this year, there has been a net FII inflow of USD 28.3 billion, an all-time peak.

REPORTS

India’s credit growth slips to 16.6 per cent in FY10: RBI The Reserve Bank has expressed concern over the falling credit off take, which slipped to a poor 16.6 per cent in the past fiscal.

According to the RBI report on Trend and Progress of Banking in 2009-10, noting that there has been steady

decline in credit growth since FY05 when it had touched a high of over 30 per cent, credit off take declined to a low of 16.6 per cent in the fiscal ending March 2010.

It further noted that the slipping credit growth was also a reflection of theslowing deposit growth. On the international liabilities and assets of domestic banks, both have registered accelerated growth in 2009-10. There was an increase by about 17 per cent in the international liabilities of banks in the reporting period, which far exceeded the growth of 7.4 per cent in their internationalassets.

However, there was a fall in the inflows of FCNR (B)/NRE deposits in thereporting period following a steady fall in the benchmark Libor during the yearresulting in a fall in the effective rate of interest payable on FCNR (B)/NREdeposits.

Remittance to India, developing nations to rise to USD 370 billion:World BankNotwithstanding the recent global financial crisis, remittance flows todeveloping countries including India is expected to reach USD 325 billion by the end of this year and is likely to exceed to USD 70 billion in two years’ time, according to the World Bank.

According to the World Bank’s latest Migration and Remittances Factbook

IIP Figures Sectors September April- September 2009-10 2010-11 2009-10 2010-11Mining 7.4 5.2 7.9 8.7Manufacturing 8.3 4.5 6.2 11.0Electricity 7.5 1.7 6.7 3.8General 8.2 4.4 6.3 10.2

Source: CSO, India

20

ECONOMIC REVIEW

2011,remittance flows to developing countries is expected to reach USD 325 billion by the end of this year, up from USD 307 billion in 2009. Worldwide, remittance flows are expected to reach USD 440 billion by the end of this year.

Remittance flows to developing countries is expected to cross USD 370 billion, but this outlook is subject to the risks of a fragile global economic recovery, volatile currency and commodity price movements, and rising anti-immigration sentiment in many destination countries.

As per the report, India, China, Mexico, the Philippines, and France have beentop recipient countries in 2010 so far. According to the Factbook 2011, the top migrant destination country is the United States, followed by Russia, Germany, Saudi Arabia, and Canada.

The top immigration countries relative to population are Qatar (87 per cent),Monaco (72 per cent), the United Arab Emirates (70 per cent), Kuwait (69 percent) and Andorra (64 per cent).

Some developing regions in Europe and Central Asia, Latin America and theCaribbean, the Middle East and North Africa, and Sub-Saharan Africa witnessed larger-than-expected falls in remittances in 2009, while flows to South Asia in 2009 grew more than expected. Those to East Asia and Pacific rose modestly.

India has above ground gold stocks worth USD 800 billion: WGCIndia owns over 18,000 tonnes of above ground gold stocks worth approximately USD 800 billion and representing at least 11 per cent of global stock, according to estimates of World Gold Council.

“This is equivalent to nearly half an ounce of gold ownership per capita, a figure which is significantly below

consumption in Western markets, representing scope for additional future growth”, says a WGC research paper entitled ‘India: Heart of Gold’.

In 2009, total Indian gold demand reached USD 19 billion, ` 974 billion, which accounts for 15 per cent of the global gold market, according to WGC.

Over the past ten years, the value of gold demand in India has increased at an average rate of 13 per cent per year, outpacing the country’s real GDP, inflation and population growth by six per cent, eight per cent and 12 per cent respectively.

The country currently has one of the highest saving rates in the world, estimated at around 30 per cent of total income, of which 10 per cent is already invested in gold.

INTERNATIONAL

Trade deficit in U.S. shrinks as exports climb to two-year highThe U.S. trade deficit shrank more than forecast in September as exports climbed to the highest level in two years, showing a weaker dollar is helping strengthen the economic recovery.

The gap narrowed by 5.3 percent to USD 44 billion. A 7.5 percent drop in the dollar over the past four months is making American goods cheaper overseas as demand in emerging economies.

U.S. exports increased 0.3 percent to USD 154.1 billion, the most since August 2008. The outlook for U.S. exports is holding up as emerging economies from China to India and Brazil modernize infrastructure and more affluent households are able to afford goods and services from abroad.

Imports dropped in September,

reflecting less demand for foreign made autos and consumer goods like pharmaceuticals and clothing. American demand for capital goods made overseas climbed to a record, indicating business investment in computers and software continues to improve.

China inflation spikes in October 2010China’s consumer prices increased at their fastest pace in two years in October 2010, strengthening expectations the central bank might continue to tighten monetary policy to curb inflationary pressures.

Fueled by a spike in food prices, the consumer price index jumped 4.4 per cent in October, well above the 3.6 per cent reading in September. The nation’s producer price index accelerated 5 per cent during the month.

Food prices soared more than 10 per cent during the month, while non-foodprice increases, although relatively modest at 1.6 per cent, were higher than the 1.4 per cent increase recorded in September.

The spike in October inflation came even as some other economic indicators softened slightly, with the nation’s industrial output increasing at a 13.1 per cent rate from the same month last year, while retail sales expanded 18.6 per cent. In September, industrial production had risen by 13.3 per cent, while retail salesincreased 18.8 per cent.

Urban fixed-asset investments, meanwhile, rose 24.4 per cent in the first 10 months of this year, also edging down from a 24.5 per cent growth in the January-to-September period.

21

ECONOMIC REVIEW

Euro area GDP up by 0.4 per centGDP increased by 0.4 per cent in both the euro area (EA16) and the EU27 during the third quarter of 2010, compared with the previous quarter, according to Eurostat, the statistical office of the European Union.

In the second quarter of 2010, growth rates were +1.0 percent in both zones.Compared with the same quarter of the previous year, seasonally adjusted GDP increased by 1.9 per cent in the euro area and by 2.1 per cent in the EU27 in the third quarter of 2010, after +1.9 per cent and +2.0 per cent respectively in the previous quarter.

Ad SizesFull Page (With Bleed) 210 mm (W) x 300 mm(H) Full Page (Without Bleed) 170 mm (W) x 260 mm (H) Half Page (With Bleed) 210 mm (W) x 150 mm (H) Half Page (Without Bleed) 170 mm (W) x 130 mm (H) Quarter Page Vertical (With Bleed) 105 mm (W) x 150 mm (H) Quarter Page Vertical (Without Bleed) 85 mm (W) x 130 mm (H) Quarter Page Horizontal (With Bleed) 210 mm (W) x 75 mm (H) Quarter Page Horizontal (Without Bleed) 170 mm (W) x 65 mm (H)

Artwork layout specificationsDocument colour mode must be in CMYK for Colour adand in Greyscale for B/W.Document must be submitted in EPS or editable PDF format withall fonts and logos outlined in Vector format or fonts must besupplied separately.Images must be in CMYK with a resolution of 300 dpi at their final size in TIFF, EPS, High resolution PDF or JPG format.

To advertise in this monthly magazineplease follow these specifications.

Submission deadlineArtwork and advertising material must be supplied via email or post on CD or DVD by not later than 2 weeks before publication date.Booking & submission deadline

Booking deadline Submission deadline Issue ThemeNov 30 Dec 10 Nov2010 To be advisedDec 31 Jan 10 Dec 2010 To be advisedJan 31 Feb 10 Jan 2011 To be advisedFeb 28 Mar 10 Feb 2011 To be advised

Full page

1/2 page1/4 page

Horizontal

1/4 page

Vertical

There are risks and costs to a program of action. But they are far less than the long-range

risks and costs of comfortable inaction.

- John F. Kennedy

24

TAMIL NADU GOVERNMENTTAMIL NADU ORDINANCE No. 7 OF 2010

CHENNAI, 29th OCTOBER 2010

An Ordinance to bring provision of the Tamil Nadu Value Added Tax(Second Amendment) Act, 2010 into force with retrospective effect

WHEREAS, the Legislative Assembly of the State is not in session and the Governor of Tamil Nadu is satisfied that circumstances exist which render it necessary for him to take immediate action for the purpose hereinafter appearing;

NOW, THEREFORE, in exercise of the powers conferred by clause (1) of Article 213 of the Constitution, the Governor hereby promulgates the following Ordinance:—

1. This Ordinance may be called the Tamil Nadu Value Added Tax (Special Provision) Ordinance, 2010.

2. Notwithstanding anything contained in sub- section (2) of section 1 of the Tamil Nadu Value Added Tax (Second Amendment) Act, 2010 (hereinafter referred to as the 2010 Act) and in the notification of the State Government in the Commercial Taxes and Registration Department No. II (2)/CTR/527(b)/2010, published at page 1 in Part II - Section 2 of the Tamil Nadu Government Gazette Extraordinary, dated the 19th day of August 2010, section 2 of the 2010 Act shall be deemed to have come into force on the 1st day of January 2007.

28th October, 2010

SURJIT SINGH BARNALA Governor of Tamil Nadu

EXPLANATORY STATEMENT

In order to protect the revenue of the Government, Section 19 of the Tamil Nadu Value Added Tax Act, 2006 (Tamil Nadu Act 32 of 2006) has been amended suitably by Tamil Nadu Act 22 of 2010 providing for reversal of the amount of the input tax credit for the goods over and above the output tax of those goods, in a case where a registered dealer has sold goods at a price less than the price of the goods purchased by him and the said amendment has been given effect to from the 19th August 2010.

2. Now, the Government have decided to give effect to the said amendment from the date of coming into force of the said Tamil Nadu Act 32 of 2006 (i.e.) from the 1st day of January 2007 itself, in order to prevent any loss to the State exchequer from that date.

3. The Ordinance seeks to give effect to the above decision.