IN THE SUPREME COURT OF FLORIDA THE SUPREME COURT OF FLORIDA CITY OF FERNANDINA BEACH, Appellant, v....

58

IN THE SUPREME COURT OF FLORIDA CITY OF FERNANDINA BEACH, Appellant, v. Case No.: SC14-299 L.T. No.: 13-CA-485 STATE OF FLORIDA et al., Appellees. / ON APPEAL FROM THE CIRCUIT COURT, FOURTH JUDICIAL CIRCUIT IN AND FOR NASSAU COUNTY, FLORIDA ANSWER BRIEF OF APPELLEE JOANNE CONLON John S. Mills Thomas D. Hall Andrew D. Manko The Mills Firm, P.A. 203 North Gadsden Street, Suite 1A Tallahassee, Florida 32301 Michael G. Tanner Thomas E. Bishop Gilbert L. Feltel, Jr. Tanner Bishop One Independent Drive, Suite 1700 Jacksonville, Florida 32202 E. Clinch Kavanaugh, III Clinch Kavanaugh, P.A. 10 North Second Street Fernandina Beach, Florida 32034 Attorneys for Appellee Joanne Conlon Filing # 12862013 Electronically Filed 04/23/2014 06:39:49 PM RECEIVED, 4/23/2014 18:44:09, John A. Tomasino, Clerk, Supreme Court

Transcript of IN THE SUPREME COURT OF FLORIDA THE SUPREME COURT OF FLORIDA CITY OF FERNANDINA BEACH, Appellant, v....

IN THE SUPREME COURT OF FLORIDA CITY OF FERNANDINA BEACH, Appellant, v. Case No.: SC14-299 L.T. No.: 13-CA-485 STATE OF FLORIDA et al., Appellees. /

ON APPEAL FROM THE CIRCUIT COURT, FOURTH JUDICIAL CIRCUIT

IN AND FOR NASSAU COUNTY, FLORIDA

ANSWER BRIEF OF APPELLEE JOANNE CONLON

John S. Mills Thomas D. Hall Andrew D. Manko The Mills Firm, P.A. 203 North Gadsden Street, Suite 1A Tallahassee, Florida 32301

Michael G. Tanner Thomas E. Bishop Gilbert L. Feltel, Jr. Tanner Bishop One Independent Drive, Suite 1700 Jacksonville, Florida 32202 E. Clinch Kavanaugh, III Clinch Kavanaugh, P.A. 10 North Second Street Fernandina Beach, Florida 32034 Attorneys for Appellee Joanne Conlon

Filing # 12862013 Electronically Filed 04/23/2014 06:39:49 PM

RECEIVED, 4/23/2014 18:44:09, John A. Tomasino, Clerk, Supreme Court

i

TABLE OF CONTENTS

TABLE OF CONTENTS ........................................................................................... i

TABLE OF CITATIONS ........................................................................................ iii

STATEMENT OF THE CASE AND OF THE FACTS ........................................... 1

SUMMARY OF ARGUMENT ...............................................................................20

ARGUMENT ...........................................................................................................24

I. The Standard of Review for the Trial Court’s Legal Conclusion Is De Novo, and the Standard for Its Findings of Fact Is Competent, Substantial Evidence. .......................................................25

II. The Trial Court Applied the Dual Rational Nexus Test, and the City’s Arguments Regarding the Florida Impact Fee Act Are Waived, Unpreserved, Harmless, and Meritless. ................................26

III. The Trial Court Correctly Concluded That the Impact Fees Fail the Dual Rational Nexus Test. .............................................................31

A. Having Failed to Explain How the Impact Fees Satisfy the Dual Rational Nexus Test, the City Has Shown No Error. .........................................................................................31

B. Alternatively, the City Has Failed to Demonstrate Error in Judge Davis’s Alternative Conclusion That Conlon Proved the Impact Fees Violate the Dual Rational Nexus Test ............................................................................................36

1. The Impact Fees Do Not “Accommodate Future Growth,” They Repay Debt Service on the Utility as a Whole. (Responding to Initial Brief Point III(A))..............................................................................36

2. The City’s Consultant Gave No Consideration to the Requirements of the Dual Rational Nexus Test. (Responding to Initial Brief Points III(B) and IV) .........40

3. That the Usage Fees Charged to New and Existing Customers Are Sufficient To Pay for the Entire

ii

Utility Is Yet Another Reason the Impact Fees Cannot Meet the Dual Rational Nexus Test. (Responding to Initial Brief Point V) .............................46

IV. The Impact Fees Are Not “User Fees.” (Responding To Initial Brief Point VI) .....................................................................................47

CONCLUSION ........................................................................................................50

CERTIFICATE OF SERVICE ................................................................................51

CERTIFICATE OF COMPLIANCE .......................................................................52

iii

TABLE OF CITATIONS

CASES

Applegate v. Barnett Bank of Tallahassee, 377 So. 2d 1150 (Fla. 1980) ............................................................................ 3

Citizens Advocating Responsible Envir. Solutions v. City of Marco Island, 959 So. 2d 203 (Fla. 2007) .............................................................................. 7 Contractors & Builders Ass’n of Pinellas County v. City of Dunedin, 329 So. 2d 314 (Fla. 1976) .....................................................................passim City of Clermont v. Rumph, 450 So. 2d 573 (Fla. 1st DCA 1984) ............................................................. 31 City of Gainesville v. State, 863 So. 2d 138 (Fla. 2003) ............................................... 7, 19, 20, 25, 47, 48 Dober v. Worrell, 401 So. 2d 1322 (Fla. 1981) .......................................................................... 28 Donovan v. Okaloosa County, 82 So. 3d 801 (Fla. 2012) .................................................................... 3, 25, 26 Hollywood, Inc. v. Broward County, 431 So. 2d 606 (Fla. 4th DCA 1983) ........................................... 10, 33, 34, 41 Hoskins v. State, 75 So. 3d 250 (Fla. 2011) .............................................................................. 28 Kenz v. Miami-Dade County, 116 So. 3d 461 (Fla. 3d DCA 2013) .............................................................. 31 Keys Citizens for Responsible Gov’t, Inc. v. Fla. Keys Aqueduct Auth., 795 So. 2d 940 (Fla. 2001) .............................................................................. 7 Lake Sarasota, Inc. v. Pan Am. Sur. Co., 140 So. 2d 139 (Fla. 2d DCA 1962) .............................................................. 29

iv

Liberty County v. Baxter’s Asphalt & Concrete, 421 So. 2d 505 (Fla. 1982) .............................................................................. 9 Pensacola Beach Pier, Inc. v. King, 66 So. 3d 321 (Fla. 1st DCA 2011) ............................................................... 29 St. Johns County v. Northeast Florida Builders Ass’n, 583 So. 2d 635 (Fla. 1991) ..................................... 7, 9, 10, 11, 12, 32, 33, 34 Santa Rosa Island Auth. v. Pensacola Beach Pier, Inc., 834 So. 2d 261 (Fla. 1st DCA 2002) ............................................................... 9 State v. City of Daytona Beach, 158 So. 300 (Fla. 1934) ................................................................................... 9 State v. City of Port Orange, 650 So. 2d 1 (Fla. 1994) ................................................................................ 25 Sullivan v. Mayo, 121 So. 2d 424 (Fla. 1960) ............................................................................ 31 Town of Riviera Beach v. State, 53 So. 2d 828 (Fla. 1951) ............................................................................ 8, 9 Turner v. City of Clearwater, 789 So. 2d 273 (Fla. 2001) .............................................................................. 8 Volusia County v. Aberdeen at Ormond Beach, 760 So. 2d 126 (Fla. 2000) ............................................................ 7, 10, 32, 33 Wald Corp. v. Metropolitan Dade County, 338 So. 2d 863 (Fla. 3d DCA 1976) ........................................................ 33, 34 Webster v. N. Orange Mem’l Hosp. Tax Dist., 187 So. 2d 37 (Fla. 1966) ................................................................................ 9

STATUTES, CONSTITUTIONAL PROVISIONS, AND RULES OF COURT

§ 75.01, Fla. Stat. (2013) ............................................................................................ 7

v

§ 75.09, Fla. Stat. (2013) ............................................................................................ 7

§ 163.31801, Fla. Stat. (2013) .............................................................................. 8, 30

§ 163.31801(1), Fla. Stat. (2013) ............................................................................... 8

§ 163.31801(3), Fla. Stat. (2013) ............................................................................. 27

§ 163.31801(5), Fla. Stat. (2013) ............................................................. 8, 26, 28, 29

Rule 9.110(i), Fla. R. App. P. .................................................................................... 3

Rule 9.210(a)(2), Fla. R. App. P. ............................................................................. 52

SECONDARY SOURCES

70C Am. Jur. 2d, Special or Local Assessments § 2 (2000) .................................... 48

1

STATEMENT OF THE CASE AND OF THE FACTS

The City of Fernandina Beach appeals the trial court’s order denying the

City’s request to validate revenue bonds. The bonds would be secured by certain

fees it imposed in 2003 to finance a portion of the purchase price the City paid for

a water utility. The utility had been built and operated by a privately-owned utility

company and it had more capacity to serve customers than the City needed at the

time of purchase. Although the technical posture of this case is a bond validation

appeal, the true nature of this proceeding is an adjudication of the legality of the

impact fees. As the trial court found, and the City does not dispute in its initial

brief, the City brought this bond validation proceeding as a stratagem to preclude

Appellee/Intervenor Joanne Conlon from reaching the merits of her previously

filed and still pending class action challenging the fees.

The primary issue is whether the trial court erred in concluding that the

impact fees violate Florida’s Dual Rational Nexus Test, which requires reasonable

connections both (1) between the need for additional facilities and the anticipated

growth in population and (2) between the impact fees and the benefits accruing to

those paying the fees. The City makes no argument as to how the test was satisfied,

but instead contends that the trial court was required to simply defer to the City’s

judgment that it should charge the fees. An alternative issue is whether the fees are

really user fees that are not subject to the Dual Rational Nexus Test.

2

The City instituted the proceeding below by filing a complaint seeking

validation of the City’s Utility System Refunding Revenue Bonds, Series 2013B

(the “2013B Bonds”). (City App. 26-44.) The bonds were to be secured by revenue

the City received from what it characterized as “water capacity fees, sometimes

referred to as impact fees” (the “Impact Fees”), which it charges to any new

customer seeking to hook up to the City’s water utility. (City App. 36.)

The City had not served Conlon with the complaint, and she would not have

known that her right to challenge the Impact Fees was being undermined until she

independently happened to learn about the complaint. (Conlon App. 1-9, 189-203.)

Conlon intervened in the proceeding below as a matter of right on the basis that she

was a property owner and citizen of the City (who had also paid an Impact Fee),

and she filed an answer to the City’s complaint. (Conlon App. 1-9.) Conlon raised

one affirmative defense: that the Series 2013B Bonds could not be validated

because the Impact Fees which secure the bonds are unlawful. (Conlon App. 6-8.)

Circuit Judge Brian J. Davis presided over a two-day bench trial in early

December 2013. (City App. 839-1427; Conlon App. 204-21.)1 He ultimately

entered a final judgment that contained detailed, concise findings of fact, fully set

1 The City provided the bulk of the trial transcript in its appendix, but

that copy of the transcript abruptly ends in the middle of a line during Conlon’s rebuttal closing argument. Because the City refused to correct the appendix, Conlon provides the remaining seventeen pages in her appendix.

3

forth the legal standards he found governed, and how he applied those standards,

which involved mixed questions of law and fact. (City App. 1-25.) In sum, Judge

Davis concluded that Conlon had proven by a preponderance of the evidence that

the Impact Fees did not satisfy the Dual Rational Nexus Test and that they were, in

fact, impact fees and not user fees, as the City claimed in the alternative. (City

App. 22-24.) Accordingly, the final judgment denied the relief sought by the City

with prejudice. (City App. 25.)

The initial brief mischaracterizes the standards that Judge Davis applied and

how he applied them. With two exceptions dealt with in the argument section, the

initial brief does not challenge Judge Davis’ findings of fact. For these reasons,

Judge Davis’ findings and legal analysis are set forth below verbatim:2

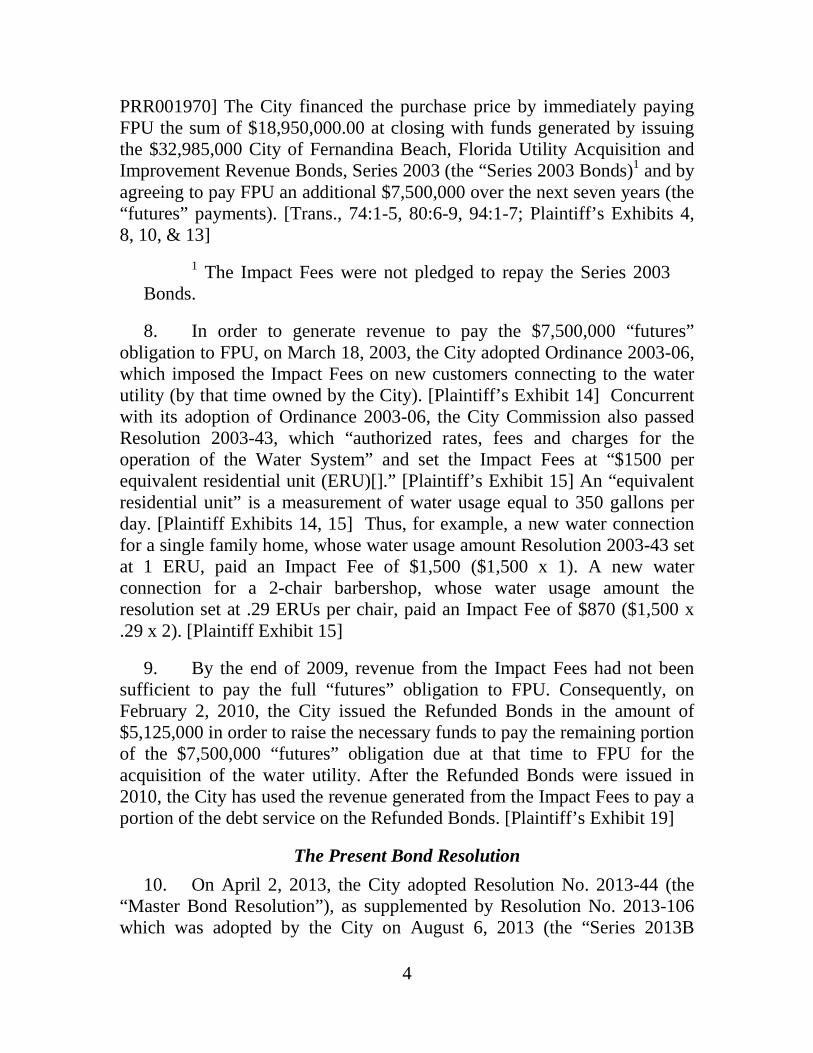

History of the City’s Purchase and Financing of the Water Utility 7. On December 3, 2002, the City Commission adopted Resolution No. 2002-165 (the “Purchase Resolution”) approving the City entering into an agreement to purchase the water utility from Florida Public Utilities Company (“FPU”), a privately-owned utility company. [Plaintiff’s Exhibits 8, 10] In March 2003, the City closed on its purchase of the water utility from FPU for a total purchase price of $26,450,000.00. [Trans., 216:18-23, 366:25-367:2, 457:17-458:6; Plaintiff’s Exhibit 10 at CFB001013-CFB001015; Conlon Exhibit 28 at pp. 75, 78-79; Conlon Exhibit 88 at

2 The citations in the judgment are to the trial transcript and evidentiary

exhibits. Most of these exhibits are not included in the City’s appendix. As the appellant, the City has the burden of providing an adequate record for this Court to review. Donovan v. Okaloosa County, 82 So. 3d 801, 805 (Fla. 2012); Applegate v. Barnett Bank of Tallahassee, 377 So. 2d 1150, 1152 (Fla. 1980). The Court also has the authority to order a formal record be prepared and transmitted. Fla. R. App. P. 9.110(i).

4

PRR001970] The City financed the purchase price by immediately paying FPU the sum of $18,950,000.00 at closing with funds generated by issuing the $32,985,000 City of Fernandina Beach, Florida Utility Acquisition and Improvement Revenue Bonds, Series 2003 (the “Series 2003 Bonds)1 and by agreeing to pay FPU an additional $7,500,000 over the next seven years (the “futures” payments). [Trans., 74:1-5, 80:6-9, 94:1-7; Plaintiff’s Exhibits 4, 8, 10, & 13]

1 The Impact Fees were not pledged to repay the Series 2003 Bonds.

8. In order to generate revenue to pay the $7,500,000 “futures” obligation to FPU, on March 18, 2003, the City adopted Ordinance 2003-06, which imposed the Impact Fees on new customers connecting to the water utility (by that time owned by the City). [Plaintiff’s Exhibit 14] Concurrent with its adoption of Ordinance 2003-06, the City Commission also passed Resolution 2003-43, which “authorized rates, fees and charges for the operation of the Water System” and set the Impact Fees at “$1500 per equivalent residential unit (ERU)[].” [Plaintiff’s Exhibit 15] An “equivalent residential unit” is a measurement of water usage equal to 350 gallons per day. [Plaintiff Exhibits 14, 15] Thus, for example, a new water connection for a single family home, whose water usage amount Resolution 2003-43 set at 1 ERU, paid an Impact Fee of $1,500 ($1,500 x 1). A new water connection for a 2-chair barbershop, whose water usage amount the resolution set at .29 ERUs per chair, paid an Impact Fee of $870 ($1,500 x .29 x 2). [Plaintiff Exhibit 15]

9. By the end of 2009, revenue from the Impact Fees had not been sufficient to pay the full “futures” obligation to FPU. Consequently, on February 2, 2010, the City issued the Refunded Bonds in the amount of $5,125,000 in order to raise the necessary funds to pay the remaining portion of the $7,500,000 “futures” obligation due at that time to FPU for the acquisition of the water utility. After the Refunded Bonds were issued in 2010, the City has used the revenue generated from the Impact Fees to pay a portion of the debt service on the Refunded Bonds. [Plaintiff’s Exhibit 19]

The Present Bond Resolution 10. On April 2, 2013, the City adopted Resolution No. 2013-44 (the “Master Bond Resolution”), as supplemented by Resolution No. 2013-106 which was adopted by the City on August 6, 2013 (the “Series 2013B

5

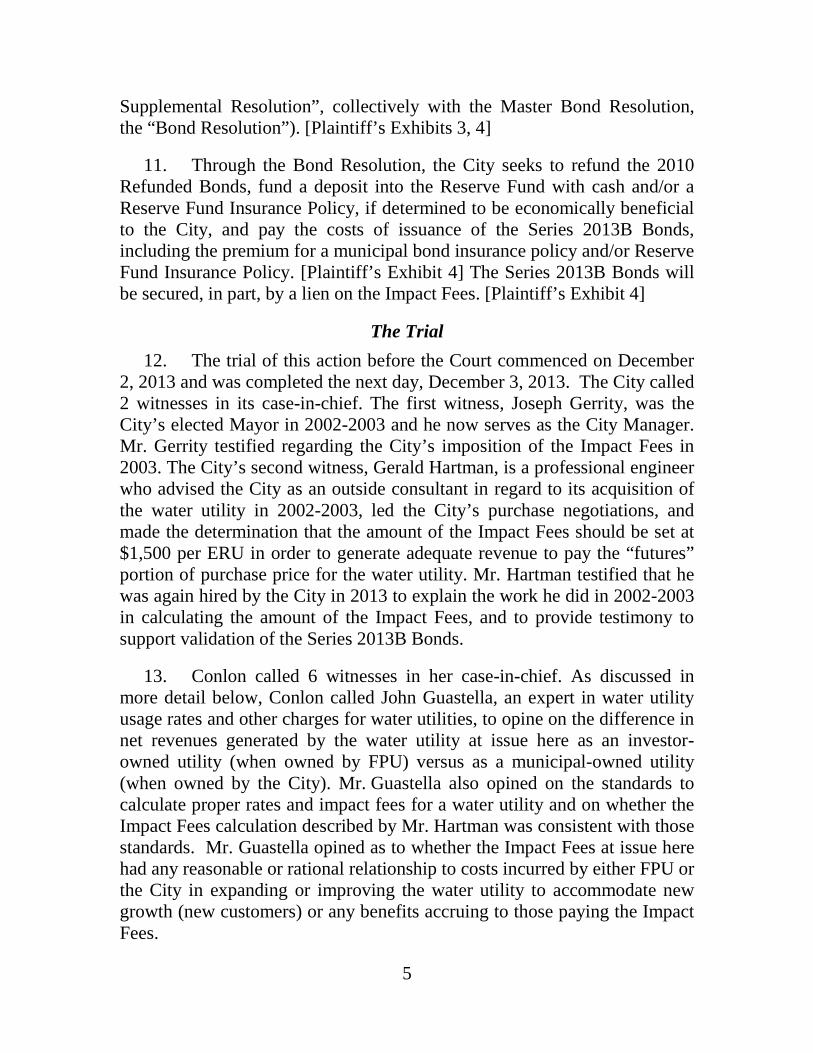

Supplemental Resolution”, collectively with the Master Bond Resolution, the “Bond Resolution”). [Plaintiff’s Exhibits 3, 4]

11. Through the Bond Resolution, the City seeks to refund the 2010 Refunded Bonds, fund a deposit into the Reserve Fund with cash and/or a Reserve Fund Insurance Policy, if determined to be economically beneficial to the City, and pay the costs of issuance of the Series 2013B Bonds, including the premium for a municipal bond insurance policy and/or Reserve Fund Insurance Policy. [Plaintiff’s Exhibit 4] The Series 2013B Bonds will be secured, in part, by a lien on the Impact Fees. [Plaintiff’s Exhibit 4]

The Trial 12. The trial of this action before the Court commenced on December 2, 2013 and was completed the next day, December 3, 2013. The City called 2 witnesses in its case-in-chief. The first witness, Joseph Gerrity, was the City’s elected Mayor in 2002-2003 and he now serves as the City Manager. Mr. Gerrity testified regarding the City’s imposition of the Impact Fees in 2003. The City’s second witness, Gerald Hartman, is a professional engineer who advised the City as an outside consultant in regard to its acquisition of the water utility in 2002-2003, led the City’s purchase negotiations, and made the determination that the amount of the Impact Fees should be set at $1,500 per ERU in order to generate adequate revenue to pay the “futures” portion of purchase price for the water utility. Mr. Hartman testified that he was again hired by the City in 2013 to explain the work he did in 2002-2003 in calculating the amount of the Impact Fees, and to provide testimony to support validation of the Series 2013B Bonds.

13. Conlon called 6 witnesses in her case-in-chief. As discussed in more detail below, Conlon called John Guastella, an expert in water utility usage rates and other charges for water utilities, to opine on the difference in net revenues generated by the water utility at issue here as an investor-owned utility (when owned by FPU) versus as a municipal-owned utility (when owned by the City). Mr. Guastella also opined on the standards to calculate proper rates and impact fees for a water utility and on whether the Impact Fees calculation described by Mr. Hartman was consistent with those standards. Mr. Guastella opined as to whether the Impact Fees at issue here had any reasonable or rational relationship to costs incurred by either FPU or the City in expanding or improving the water utility to accommodate new growth (new customers) or any benefits accruing to those paying the Impact Fees.

6

14. Conlon then called Mr. Gerrity, via deposition. Mr. Gerrity acknowledged that the City’s revenues from the sale of water at the usage rates in effect at the time the City purchased the utility were sufficient to pay the utility acquisition debt without the need for additional revenue from the Impact Fees. [Trans., 452:18-453:5] Conlon next called Robert Mearns, also by deposition. Mr. Mearns was the City Manager in 2002-2003 and was the City employee most involved in the City’s negotiations with FPU for the acquisition of the water utility. Mr. Mearns testified that while he was the City’s lead negotiator for the acquisition of the water utility, he had no prior experience with such transactions, and that he gave Mr. Hartman, the City’s outside consultant, “carte blanche” to structure the transaction, and negotiate the price to be paid by the City. [Trans., 472:13-474:2] Next, Conlon offered the deposition testimony of the City, through its designated corporate representative, John Mandrick. Mr. Mandrick confirmed that the Impact Fees were used solely to pay the City’s “futures” debt to FPU, and that the City did not use Impact Fees to expand or improve the water utility to accommodate new customers. [Trans., 494:19-495:10] The City, through Mr. Mandrick, also testified to having no familiarity with the Dual Rational Nexus Test until many years after the Impact Fees were first imposed. [Conlon Exhibit 28 at 135:1-17, 138:1-19] Conlon last called Tammi Bach, the current City Attorney, who testified about the City’s reasons for filing this bond validation action [Trans., 514:7-516:10], and about the City’s characterization of the Impact Fees as an impact fee (as opposed to a user fee), in the pleadings in this action and in the Class Action Case, and in official records of the City. [Trans., 501:15-509:13] In addition to the foregoing testimonial evidence, Conlon published certain interrogatory responses from the City.

15. The City called Mr. Hartman in rebuttal. The Court received into evidence, and has duly considered, the City’s Exhibits numbered 1 through 19 and 21 through 23, and Conlon’s Exhibits 1 through 92, 94, 107 through 108, 110, 114 through 116, 118, 121 through 133, 135 through 139, and 149 through 156.

FINDINGS OF FACT AND CONCLUSIONS OF LAW

The Scope of Bond Validation Proceedings and Applicable Legal Standards

16. The Court incorporates the foregoing facts and procedural history (paragraphs 1 through 15) into these findings of fact and conclusions of law.

7

17. Section 75.01, Florida Statutes, vests this Court with “jurisdiction to determine the validation of bonds and certificates of indebtedness and all matters connected therewith. §75.01, Fla. Stat. (2013). The final judgment in a bond validation proceeding is

forever conclusive as to all matters adjudicated against plaintiff and all parties affected thereby, including all property owners…and all others having or claiming any right, title or interest in property to be affected by the issuance of said bonds, certificates or…to be affected in any way thereby, and the validity of said bonds, certificates or other obligations…or of the proceedings authorizing the issuance thereof…shall never be called in question in any court by any person or party.

§ 75.09, Fla. Stat. (2013). The objective of a bond validation proceeding is to put in repose any question of law or fact affecting the validity of the bonds. Keys Citizens for Responsible Gov’t, Inc. v. Fla. Keys Aqueduct Auth., 795 So. 2d 940, 947 (Fla. 2001) (citation omitted).

18. The parties agree that in this bond validation proceeding, the Court must:

(1) determine if a public body has the authority to issue the subject bonds; (2) determine if the purpose of the obligation is legal; and (3) insure that the authorization of the obligation complies with the requirements of law.

City of Gainesville v. State, 863 So. 2d 138, 143 (Fla. 2003) (citation omitted). The parties also agree that “[s]ubsumed within the inquiry as to whether the public body has the authority to issue the subject bond is the legality of the financing agreement upon which the bond is secured.” Id.; see also Keys Citizens for Responsible Gov’t, 795 So. 2d at 947. Based on this authority, Conlon asserts, and the Court agrees, that the lawfulness of the Impact Fees under the Dual Rational Nexus Test is an issue for the Court’s determination from the evidence presented at trial because the Impact Fees secure the Series 2013B Bonds. See, id.; Citizens Advocating Responsible Envir. Solutions v. City of Marco Island, 959 So. 2d 203, 206 (Fla. 2007); Volusia Cnty. v. Aberdeen at Ormond Beach, 760 So. 2d 126 (Fla. 2000), St. Johns Cnty. v. Ne. Fla. Builders Ass’n, Inc., 583 So. 2d 635 (Fla. 1991); Contractors & Builders Ass’n of Pinellas Cnty. v. City of Dunedin, 329 So. 2d 314 (Fla. 1976).

8

19. The City, as the Plaintiff in this action, generally bears the burden of proving, by a preponderance of the evidence, that the Series 2013B Bonds are entitled to judicial validation. See generally, Turner v. City of Clearwater, 789 So. 2d 273 (Fla. 2001). Additionally, the Impact Fees at issue were initially imposed by the City in 2003 under Ordinance 2003-06, which was amended in 2009. On August 6, 2013, the City, through Ordinance 2013-21, repealed the 2009 amendment to Ordinance 2003-06 and reinstated the Impact Fees in the same form as passed in 2003. The City repealed the 2009 amendment because it failed to comply with certain notice requirements under Florida’s 2006 Impact Fee Act, section 163.31801, Florida Statutes. [Transcript of Final Hearing (hereinafter abbreviated as “Trans.”) at 507:21-508:19] Accordingly, because the Impact Fees pledged in Resolution 2013-106 for repayment of the Series 2013B Bonds, which are at issue in this case, were reinstated by the City in Ordinance 2013-21, the Court’s analysis of the evidence is also governed by the Florida Impact Fee Act, which provides, in relevant part, that:

[i]n any action challenging an impact fee, the government has the burden of proving by a preponderance of the evidence that the imposition or amount of the fee meets the requirements of state legal precedent or this section. The court may not use a deferential standard.

§ 163.31801(1), (5), Fla. Stat. (2013). Nevertheless, as discussed below, the Court finds that even if Intervener Conlon has the burden of proof that the Impact Fees are unlawful under the Dual Rational Nexus Test, she has met that burden by a preponderance of the evidence.

20. Also, while the Court properly gives deference to certain of the City’s discretionary policy decisions, such as the decision to purchase the water utility and the price paid for the water utility, see Turner, 789 So. 2d at 278-79, whether the Impact Fees comply with Florida’s Dual Rational Nexus Test is an issue for the Court because the City has no discretion to impose fees that do not comply with applicable law.

Conlon’s Assertions of Improper Purpose 21. It must also be noted that no deference can be given to municipal legislative action if it is shown that “fraud, corruption, improper motives or influence, plain disregard of duty, gross abuse of power or violation of law enter into and characterize the result.” Town of Riviera Beach v. State, 53

9

So. 2d 828, 831 (Fla. 1951) (citation omitted); see also Webster v. N. Orange Mem’l Hosp. Tax Dist., 187 So. 2d 37, 42 (Fla. 1966); Santa Rosa Island Auth. v. Pensacola Beach Pier, Inc., 834 So. 2d 261, 262-63 (Fla. 1st DCA 2002) (citing Liberty Cnty. v. Baxter’s Asphalt & Concrete, 421 So. 2d 505 (Fla. 1982)); State v. City of Daytona Beach, 158 So. 300, 305 (Fla. 1934). Conlon contends that the motives of the City in initiating this bond validation were not in fact for the proper purpose of taking advantage of financing opportunities, but rather were an attempt to circumvent the claims being advanced by Conlon in the Class Action Case by having the lawfulness of the Impact Fees resolved in this action.

22. In support of this contention, Conlon points to the timing of the filing of this action, just 10 days after the Court certified the class in the Class Action Case, and to the City’s efforts to obtain an expedited final hearing. Time records of counsel for the City defending the Class Action Case and counsel prosecuting this bond validation action show collaboration in the development of a strategy designed to preclude the claims in the Class Action Case regarding the lawfulness of the Impact Fees. [Conlon Exhibit 9, at pp. CPR07373, CPR07544; Conlon Exhibit 155] Notably, the evidence here is undisputed that the revenues from the Impact Fees are not necessary to repay the debt of the Series 2013B Bonds which the City seeks to validate in this action. [Trans., 91:6-15; Conlon Exhibit 10 at p.13] Counsel for the City acknowledged that the City’s purpose in this validation action is to resolve all challenges to the lawfulness of the Impact Fee. [Trans., 33:2-34:1]

23. Although the Court finds that the evidence does suggest that this action was motivated as part of a stratagem by the City to preclude Conlon’s claims concerning the Impact Fees in the Class Action Case, the evidence does not show fraud or improper purpose of the character described in Town of Riviera Beach and other such authorities. Consequently, the Court does not base its rulings in this Final Judgment to any extent on Conlon’s assertion that the City has acted with an improper purpose in initiating this bond validation action.

The Requirements of the Dual Rational Nexus Test 24. In Florida, impact fees imposed by a local government must satisfy the Dual Rational Nexus Test to be lawful. See St. Johns Cnty., 583 So. 2d at 637. The Dual Rational Nexus Test requires a local government to demonstrate:

10

a reasonable connection, or rational nexus, between the need for additional capital facilities and the growth in population generated by the subdivision. In addition, the government must show a reasonable connection, or rational nexus, between the expenditures of the funds collected [the impact fees] and the benefits accruing to the subdivision. In order to satisfy this latter requirement, the ordinance must specifically earmark the funds collected for use in acquiring capital facilities to benefit the new residents.

Id. (citing Hollywood, Inc. v. Broward Cnty., 431 So. 2d 606, 611-612 (Fla. 4th DCA 1983)).

25. Also, for an impact fee to be lawful, a local government must assess the need for the fee prospectively – i.e. before it is collected – not retrospectively. See St. Johns Cnty., 583 So. 2d at 642 (holding “no impact fee may be collected under the ordinance until the second prong of the dual rational nexus test has been met”). Florida law contemplates that a local government seeking to impose an impact fee will perform a sufficiently detailed analysis to determine whether the proposed fee meets the requirements of the Dual Rational Nexus Test. See generally, id. at 637-41; Volusia Cnty. v. Aberdeen at Ormond Beach, 760 So. 2d 126 (Fla. 2000); Contractors & Builders Ass’n of Pinellas Cnty. v. City of Dunedin, 329 So. 2d 314 (Fla. 1976). As discussed below, the evidence shows there was no meaningful consideration of the Dual Rational Nexus Test in connection with the imposition of the Impact Fees at issue here.

26. Mr. Mearns was the primary City official supervising the transaction by which the City acquired the water utility and imposed the Impact Fees. [Trans., 451:22-24, 462:11-13, 477:20-478:4; Conlon Exhibits 51-54, 56] He conceded he was unaware of any contemporaneous calculations or analyses with regard to the Impact Fees to insure their compliance with the Dual Rational Nexus Test [Trans., 475:10-476:23], and he stated that Mr. Hartman, the City’s consultant, would have done any such analysis. [Trans., 474:3-18, 478:5-23] Although Mr. Hartman asserted that he performed “calculations” to support the Impact Fees, he conceded that “calculations” were not an Impact Fee analysis, and that no Impact Fee study was performed. [Trans., 273:10-274:22]

27. Notably, there is no documentary evidence of any calculations or analysis performed by the City or its consultant in connection with the imposition of the Impact Fees in 2002-2003 to insure that the fees complied

11

with the Dual Rational Nexus Test. Although Mr. Hartman claimed at trial (in 2013) that he had prepared “worksheets” reflecting his 2002-2003 calculations, such worksheets were not produced at trial by either Mr. Hartman or by the City. [Trans., 251:14-254:1]

28. For other impact fees imposed by the City, the City performed detailed analyses to insure compliance with the Dual Rational Nexus Test. [Conlon Exhibits 45, 121] Mr. Mearns described how the City had retained Dr. James Nicholas2, a respected expert consultant in the area of impact fees and their proper calculation, for the imposition of other impact fees. [Trans., 482:8-484:14]

2 Dr. Nicholas and his work are described in a seminal case on the application of the Dual Rational Nexus Test in regard to impact fees. See St. Johns Cnty., 583 So. 2d at 637-40. The description of the fee analysis in that opinion illustrates the kind of detailed analysis that is intended to insure the impact fees comply with the Dual Rational Nexus Test. Id.

29. Mr. Hartman was retained by the City in 2002 to explore the possibility of purchasing the FPU water utility [Trans., 148:12-22], to perform due diligence regarding the utility, to value the utility, and to advise and act on behalf of the City in negotiations with FPU. [Trans., 149:15-150:19] Mr. Hartman described the negotiations with counsel for FPU concerning the purchase price for the utility, including the multiple offers and counter-offers exchanged, and he testified that the amount of the “futures” payments to FPU was a key negotiating point. [Trans., 178:6-12] He described his calculation of the amount of Impact Fees necessary to fund the “futures” payments as a “simple” one, and he described the formula he said he used in 2002-2003. [Trans., 179:13-180:3] He described this formula as the replacement cost new of the utility assets, undepreciated, at the time the City purchased the utility from FPU ($19.8 million) divided by the number of ERUs of capacity in the utility at that time (13,500), which yielded a dollar figure approximately equal to the $1,500 amount of the Impact Fees the City imposed. [Id.] He testified he believed this was a simple enough calculation that no further analysis or study was necessary to set the amount of the Impact Fees. [Trans., 179:13-180:3, 250:10-18, 251:10-13, 273:10-14, 275:1-5, 285:9-14] The Court finds that Mr. Hartman’s “calculations” in 2002-2003 to support the Impact Fees were at best perfunctory, inaccurate and incomplete.

12

30. On cross-examination, Mr. Hartman’s detailed notes describing the negotiations with FPU, step-by-step, revealed that he had created the structure of the transaction and had injected the concept of “futures” and the use of the Impact Fees to pay the “futures.” [Trans., 178:6-12, 204:7-205:2] He described that at one point in the negotiations, he suggested that from each new customer’s $1,500 Impact Fee payment, FPU would receive $1,000 with the City retaining the remaining $500. [Trans., 265:12-266:5, 288:16-289:15; Conlon Exhibit 53 at HAI006146, HAI006172-HAI006173; Conlon Exhibit 54] Under the final purchase agreement, the City remitted to FPU the entire $1,500 Impact Fee paid by each new customer in order to pay the “futures” obligation. [Trans., 266:13-267:1; Conlon Exhibit 53 at HAI006173; Conlon Exhibit 59] Thus, Mr. Hartman’s contemporaneous notes of the transaction show that the amount of the Impact Fees was arrived at solely in order to fund the amount of the purchase price in excess of what the City could pay in cash at closing from the amount it borrowed through bonds. Mr. Hartman’s notes did not show any analysis that equated the Impact Fees with either the cost of facilities to accommodate new growth or with the benefit new customers received from hooking up to the utility. See generally, St. Johns Cnty., 583 So. 2d at 638-39.

31. Mr. Hartman further testified that in 2002-2003 he relied on methods described in authoritative materials from the American Water Works Association (AWWA). In particular, he opined that the AWWA Manual M1 in its 5th Edition [Conlon Exhibit 156] is authoritative, and provides, through the “Equity Buy in Method,” the appropriate measure for setting an impact fee in order to comply with Florida law. [Trans., 178:21-25, 179:24-180:3, 197:2-25, 213:2-214:6, 231:9-23] But on cross-examination, Mr. Hartman conceded that the method he used in the calculation of the Impact Fees at issue here does not fully comport with the method described in the AWWA Manual. [Trans., 230:17-238:1] He acknowledged that he omitted two critical factors described in the manual, i.e., depreciation of the utility, and debt on the utility. Mr. Hartman provided no credible explanation as to why he omitted these considerations. Conlon’s expert witness, John Guastella explained, infra, that had Mr. Hartman considered these factors, no impact fee was justified.

32. In 2013, Mr. Hartman was asked by counsel for the City to prepare a memorandum describing the calculations he would have done at the time the Impact Fees were imposed in 2003. [Plaintiff’s Exhibit 16; Conlon Exhibit 40] The Court notes that Mr. Hartman’s memorandum simply states

13

that it memorializes his “thoughts” on what had been done. Because the 2002-2003 “calculations” were not produced by either Mr. Hartman or the City, the Court cannot assess whether the 2013 memorandum accurately memorializes his work in 2002-2003.

33. Mr. Hartman also testified that he used the “equity buy-in” method to calculate the Impact Fees. [Trans., 178:18-25] Using this approach, he testified that because “capacity is perpetual,” yet the utility assets providing that capacity “do not last forever,” the City must replace the capacity at some time in the future. [Trans., 177:10-25; 539:16-23] For this reason, Mr. Hartman stated he used the “Replacement Cost New” without taking depreciation into account. [Trans., 176:8-177:1; 539:-24-540:2] Yet it is difficult for the Court to reconcile this testimony with the Florida Supreme Court’s directive in City of Dunedin—a case cited by Mr. Hartman as the basis for his methodology. [Trans., 176:8-12; 237:19-25; 536:17-25; 551:1-15; 553:23-555:9] Dunedin held:

it is not ‘just and equitable’ for a municipally owned utility to impose the entire burden of capital expenditures, including replacement of existing plant, on persons connecting to a water and sewer system after an arbitrarily chosen time certain. The cost of new facilities should be borne by new users to the extent new use requires new facilities, but only to that extent. When new facilities must be built in any event, looking only to new users for necessary capital gives old users a windfall at the expense of new users. When certificates of indebtedness are outstanding, new users, like old users, pay rates which include the costs of retiring the certificates, which represent original capitalization. State v. City of Miami, supra. New users thus share with old users the cost of original facilities. For purposes of allocating the cost of replacing original facilities, it is arbitrary and irrational to distinguish between old and new users, all of whom bear the expense of the old plant and all of whom will use the new plant.

City of Dunedin, 329 So. 2d at 320-21. Mr. Hartman’s Impact Fee calculation imposed just such an arbitrary and irrational fee on new users of the water utility.

34. Finally, Mr. Hartman’s testimony shows that he did not correctly understand the Dual Rational Nexus Test. Mr. Hartman described the test as follows:

14

Q And in connection with our engagement of Parker & Associates in the City of Fernandina Beach in 2002 and 2003 in connection with this acquisition, did you perform a dual rational nexus test?

A Well, what it is, is the benefit and then -- and then the cost of the benefit being appropriate. And the benefit here is capacity, capacity that the entity, whoever's buying it, doesn't have, and they can't utilize their property. You know, they can't use water on their property, potable water without buying capacity.

So there's a defined public, health, safety and welfare benefit, very clear. And then the cost for that benefit, the matching of that, was the impact fee payment, and that was the $1,500.

And I think I've gone over how that was calculated, so that you have the dual rational nexus accomplished there.

[Trans., 195:2-195:19]

35. From his testimony as described above, the Court finds that Mr. Hartman did not make an adequate determination, as required by the first prong of the Dual Rational Nexus Test, that there was a rational nexus between projected new customers for the water utility and the need for additional capital facilities for the utility. The Court further finds that in setting the Impact Fees at $1,500 per ERU, Mr. Hartman did not determine that there is a rational nexus between the fee each new customer pays and the benefit the customer obtains from hooking up to the utility as required by the second prong of the Dual Rational Nexus Test.

36. The Court also had an opportunity to assess Mr. Hartman’s credibility and candor during his testimony on both direct and cross-examination and in that regard, makes the following findings:

(a) Mr. Hartman appeared forthright during questioning by counsel for the City, but on cross-examination, he repeatedly failed to forthrightly answer questions put to him by counsel for Conlon concerning his opinions and the work he performed in this matter. [E.g., Trans. at 222:24-223:19, 245:20-246:5] Eventually, the Court was required to admonish Mr. Hartman to answer the questions posed absent proper objection. [Trans. 277:2-278:1]

15

(b) The Court observed instances of Mr. Hartman’s failure to accurately recall important events that occurred in the course of his work in setting the Impact Fees. One example of this concerned an email from Daryll Parker, an employee of Mr. Hartman who had worked on the transaction to purchase the water utility. [Conlon Exhibits 76, 115] When confronted with an email in which Mr. Parker advised City officials not to include the Impact Fees calculations in Ordinance 2003-06 so as not to expose them to public scrutiny [Conlon Exhibit 76], Mr. Hartman first denied that Mr. Parker was involved in any meaningful way in the engagement relating to the purchase of the utility. [Trans., 528:17-25, 540:14-542:9, 545:19-546:23] He also maintained that Mr. Parker overstepped his bounds by sending the email to the City Attorney and the City Manager. [Trans., 547:3-548:2] But when he was confronted with City Commission minutes showing that Mr. Parker was involved at least to the extent that he appeared before and addressed the City Commission in regard to the Impact Fees, Mr. Hartman equivocated and appeared less than candid. [Trans., 548:20-550:1]

(c) A second example of Mr. Hartman’s failure to accurately recall events was his denial that there was any urgency in the FPU negotiations that influenced the way in which the purchase price and terms were set. [Trans., 269:5-15] On cross-examination, Mr. Hartman denied that FPU had threatened to end the negotiations to sell the utility and to pursue its own alterative public securities offering. But later, he was confronted with his own contemporaneous correspondence to the City in which he described that very concern. [Conlon Exhibit 58 at HAI006049]

(d) Mr. Hartman’s failure to recall or acknowledge these significant aspects of this transaction, his failure to candidly respond to questions during cross-examination, and his demeanor in providing his testimony cause the Court to conclude that his testimony lacked complete candor and credibility.

(e) One further consideration in the weight the Court gives to Mr. Hartman’s testimony is that he has an interest in the outcome of this litigation. He was the lead negotiator for the City for the acquisition of this water utility in 2002-2003, he recommended the purchase price and terms which the City ultimately accepted, including the use of “futures” to fund a portion of the purchase price, and he determined the amount of the Impact Fees to fund the “futures.” [Trans., 178:6-12, 204:7-205:2] He also testified that he has used this same “futures” concept, funded by

16

impact fees, in other transactions. [Trans., 200:22-201:4] Consequently, the Court finds that Mr. Hartman comes to this proceeding not only as a testifying expert [Trans., 206:12-19; Conlon Exhibit 33; Conlon Exhibit 80], but also with an interest in defending his own work. The Court finds that this gives Mr. Hartman a degree of bias which adversely affects the weight of his testimony.

37. Finally, the Court notes previous positions taken by the City concerning the lawfulness of the Impact Fees. In order to support a statute of limitations defense which it asserted in the Class Action Case, the City asserted there that the ordinance imposing the Impact Fees (Ordinance 2003-06) was facially unlawful. [Conlon Exhibit 17 at 10-11] The City later changed its position in that regard after the Court ruled against it on its statute of limitations defense. [See e.g., Conlon Exhibits 20-26]

Conlon’s Evidence that the Impact Fees are Unlawful 38. Conlon presented the testimony of John Guastella. Mr. Guastella is an expert in utility rates and valuation, and his experience in the setting of rates includes the proper calculation of impact fees. In contrast to Mr. Hartman, Mr. Guastella answered the questions posed to him on direct examination and on cross-examination directly and succinctly.

39. Mr. Guastella described the general principles applicable to setting rates and charges for water utilities, including impact fees, generally. [Trans., 334:4-18; 335:21-336:4] He explained that the considerations for setting rates and fees for investor-owned utilities are very different than those for municipally-owned utilities. He described the process by which rates are set for investor-owned utilities by the Florida Public Service Commission and by similar agencies in other states as an exercise to enable an investor-owned utility to recover its costs, including invested capital and costs of operation. By contrast, he explained that for municipally-owned utilities, the goal in setting rates is to enable the utility to recover the cost of its debt service to acquire the utility, i.e., the principal and interest on bonds and other debt instruments, while acting in the best interest of all ratepayers. [Trans., 346:6-18] Mr. Guastella explained that municipally-owned utilities do not incur certain substantial costs that investor-owned utilities must incur, including public service commission fees, property taxes and income taxes. [Trans., 346:19-347:4] He also explained that, generally, a municipality’s cost of capital, through bonds or other debt instruments, is substantially lower than that of an investor-owned utility which must pay a market equity

17

rate of return. He explained that these principles apply to the water utility previously owned by FPU (as an investor-owned utility) which was acquired by the City in 2003 (becoming a municipally-owned utility). He explained that for these reasons, the water utility has been able to generate substantially greater cash flow when operated by the City than it had been able to generate when operated by FPU using the same water usage rates. [Trans., 346:25-347:4, 367:6-13, 369:14-20]

40. Relying on financial documents relating to the operation of the water utility by FPU, including a February 7, 2000 rate determination order from the Florida Public Service Commission, Mr. Guastella testified that the cash generated by the water utility following the day it was acquired by the City was sufficient to pay the indebtedness for the full amount of the negotiated purchase price ($26,450,000), without the need for the City to impose the Impact Fees on new customers.3 [Trans., 349:14-351:3] For these reasons, Mr. Guastella opined that maintaining usage rates for the City’s water customers at the same level as FPU’s rates did not require the imposition of the Impact Fees at issue in this case. [Trans., 354:7-16]

3 The ability of the City to pay all debt associated with the utility acquisition through monthly water usage rates, without the need for impact fees, was confirmed by the testimony of City Manager Joseph Gerrity. [Trans., 91:6-15]

41. Mr. Guastella also testified from FPU financial documents and Florida Public Service Commission documents that the depreciated value of the assets of the water utility at the time the City purchased it was approximately eight million dollars. [Trans., 352:6-11] He testified that this included all of the capital facilities of the utility which generated its capacity to serve approximately 13,500 ERUs (customers). [Trans., 352:12-17] He testified that FPU had not spent $7,500,000 to build the utility to that level of capacity at the time the utility was acquired by the City. [Id.] He further testified that the City likewise had not spent $7,500,000 to expand the capital facilities of the utility. [Trans., 351:20-352:17, 360:6-14] For these reasons, Mr. Guastella testified that there was no rational relationship between amounts spent by FPU to construct the utility to its capacity at the time the City acquired it, and the $7,500,000 in “futures” obligations upon which Mr. Hartman testified he based the $1,500 per ERU Impact Fees. The Court notes there was no evidence presented that either FPU or the City had spent $7,500,000 to expand the capital facilities of the utility to its current capacity of 13,500 ERU’s.

18

42. Mr. Guastella further testified that because all customers using the water utility after its acquisition by the City (both customers using the utility prior to the acquisition and those hooking up to the utility after the acquisition) pay water usage rates which generate revenues sufficient to pay all of the City’s indebtedness to acquire the utility, there was no rational relationship between the benefit any new customer obtained by hooking up to the utility and the amount of the $1,500 Impact Fees imposed on new customers. [Trans., 364:9-17]

43. Finally, Mr. Guastella opined on the same AWWA Manual methodology referred to by Mr. Hartman. Mr. Guastella was familiar with the AWWA methods because he sat on the committee that published prior versions of AWWA’s M1 manual. [Trans., 338:25-339:23] Mr. Guastella demonstrated that, using Mr. Hartman’s own figures from contemporaneous documents, the Equity Buy-In Method, properly calculated using the AWWA methodology of subtracting out depreciation and the bond debt issued by the City, showed that no impact fee was needed to balance equity between new and exiting users of the water utility. Consequently, no Impact Fees should have been imposed.

44. The Court finds that Mr. Guastella’s testimony was clear and that his explanations were reasonable and consistent with all of the evidence presented to the Court in the case. The Court also finds that Mr. Guastella’s demeanor at trial, particularly the forthright manner with which he answered all questions put to him, both on direct examination as well as on cross-examination, demonstrated candor.

45. For the reasons described in the foregoing paragraphs, the Court accepts the testimony and opinions offered by Mr. Guastella, and does not accept the testimony and opinions offered by Mr. Hartman.

46. Based on a preponderance of the evidence, the Court finds that the Impact Fees do not satisfy either prong of the Dual Rational Nexus Test because (1) the Impact Fees were used solely to purchase the water utility as a whole (by paying the “futures” component of the purchase price for the entire utility); (2) the amount of the Impact Fees was arrived at through a wholly arbitrary negotiation process with no consideration given to the requirements of the Dual Rational Nexus Test; (3) the Impact Fees have not been used to expand the water utility to accommodate new customers or to add additional infrastructure for anticipated new customers; (4) the revenues generated from the water usage rates paid by both new and existing

19

customers have been sufficient to pay for the water utility without additional fees; (5) there is no rational relationship between the projected growth in the service area of the water utility and the need for new or expanded facilities of the utility; and (6) the persons paying the Impact Fees have received no benefit from their fees which is rationally related to $1,500 per ERU.

47. The Court further finds, based on the foregoing findings, that it was clear error for the City to rely on the calculations of Mr. Hartman to pass Ordinance 2003-06 and impose the Impact Fees.

The “Water Capacity Fee” is an Impact Fee, Not a “User Fee” 48. The City advanced the argument at trial that the Impact Fees at issue are in fact not impact fees, but rather are “user fees.” This change takes place after more than two years of litigation and numerous City admissions that the fees are impact fees. [City Exhibit 18; Conlon Exhibits 3, 14-27; Complaint for Validation; Trans. at 501:20-23, 503:9-12, 507:12-509:5]

49. “User fees” are generally charges based upon the proprietary right of a governing body for use of a facility and they share common traits, including: (1) they are paid in exchange for a particular governmental service which benefits the party paying the fee in a manner not shared by other members of society; and (2) they are paid by choice in that the party paying the fee has the option of not utilizing the governmental service and thereby avoiding the charge. City of Gainesville, 863 So. 2d at 144. Certain factors are considered in determining whether a fee constitutes a user fee, including:

the name given to the charge; the relationship between the amount of the fee and the value of the service or benefit; whether the fee is charged only to users of the service or is charged to all residents in a given area; whether the fee is voluntary-that is, whether a property owner may avoid the fee by refusing the service; whether the fee is a monthly charge or a one-time charge; whether the fee is charged to recover the costs of improvements to a defined area or infrastructure or for the routine provision of a service; whether the fee is for a traditional utility service; and whether the fee is statutorily authorized as a fee.

Id. at 145. While none of these factors is controlling or necessarily exclusive, “user fees” are generally “those which are charged only to the person actually using the service, and the amount of the charge generally is

20

related to the actual goods or services provided and is a monthly charge rather than a one-time charge.” Id. (citation omitted). In addition to the fact that the City has consistently characterized the Impact Fees as such, the undisputed evidence showed that the fee is a one-time charge imposed strictly for access to the utility, not for usage of water. The Impact Fees are due whether the customer ever turns on the tap or uses an ounce of water. [Trans., 517:20-518:6] The City’s final hearing memorandum, filed at the end of this case, was the first occasion on which the City has asserted that the Impact Fees at issue here are anything other than impact fees.4

4 Notwithstanding its argument that the “Water Capacity Fee” is a user fee [City Memorandum of Law in Support of Complaint Validation, pp. 47-52], the City devoted a subsequent section of its Memorandum in Support to the argument that the term “water capacity fee” is synonymous with “Impact Fee.” [Memo. in Support, pp. 68-69] At no point in its Complaint for Validation does the City refer to the Impact Fees as a user fee. Rather, the City refers to the “Water Capacity Fee” as an impact fee. [Complaint, ¶ 9(K)]

50. Consequently, the Court finds by a preponderance of the evidence that the Impact Fees are an impact fee and not a user fee.

Conclusion The pleadings and the evidence offered by the City and by Conlon at the final hearing have been carefully considered by this Court. The Intervenor, Conlon, has shown cause, by a preponderance of the evidence, as to why the Series 2013B Bonds should not be validated, and the prayers set forth in the City’s Complaint for Validation should not be granted. The City has failed to show by a preponderance of the evidence that the bonds should be validated.

(City App. 3-24 (alterations and omissions in original).)

SUMMARY OF ARGUMENT

This Court should affirm because the City violated its non-discretionary,

legal duty to satisfy the Dual Rational Nexus Test before enacting the Impact Fees.

21

I. In Part I of the initial brief, the City ignores two important limitations

on this Court’s standard of review. While the City is correct that the legal question

of whether the Impact Fees are valid is reviewed de novo, it omits that (1) as the

appellant, it still has the burden of demonstrating error in Judge Davis’ analysis

and (2) Judge Davis’ findings of fact must be accepted if supported by competent,

substantial evidence.

II. In Part II of the initial brief, based on a collateral ruling that Judge

Davis made clear did not impact the result in this case, the City materially

mischaracterizes his legal analysis in an attempt to discredit it through a straw man

retroactivity argument that he applied some new test required by the recent Florida

Impact Fee Act instead of the common law Dual Rational Nexus Test that Judge

Davis so clearly explained and applied throughout his opinion. Judge Davis

referenced the Act solely for the burden of proof. Any claim by the City that he

erred in this regard is (1) waived because the City does not address the burden of

proof in its initial brief, (2) unpreserved because it did not argue the issue below,

(3) harmless because the burden was on the City as plaintiff in any event, (4)

doubly harmless because Judge Davis made clear that Conlon satisfied the burden

of proof if it belonged on her, and (5) meritless because the burden and quantum of

proof are procedural issues governed by the law in place at the time the action is

filed, regardless of when the cause of action arose.

22

III. In Points III, IV, and V of the initial brief, the City quibbles with

Judge Davis’ reasoning in concluding that Conlon met any burden of proof by

showing that the Impact Fees violate the Dual Rational Nexus Test for several

different reasons. These arguments fail because (A) they do not attempt to

overcome Judge Davis’ dispositive finding that the City failed to prove that it

complied with the Dual Rational Nexus Test before imposing the Impact Fees and

(B) even if the City had a preserved and meritorious argument that it had no such

burden, Judge Davis correctly found that Conlon proved that the Impact Fees

violated the test. The latter is true for three reasons.

First, the City’s argument in Point III(A) that the Impact Fees

“accommodate future growth” by funding improvements that created excess water

capacity is belied by the evidence. The City’s claim that it bought two separate

assets is pure fiction. The so-called “excess capacity” is a characteristic of the

already built and operational single asset the City purchased, and the $7.5 million

portion of the total purchase price arbitrarily attributed to the excess capacity bears

no relation to whatever investments FPU may have made to increase the utility’s

capacity before the City bought it. Thus, the Impact Fee is just a way to raise

revenue from new customers. It is not to pay for additional costs incurred in

expanding the utility to serve them, but instead simply to acquire the entire utility

in the first place. Because of: (i) the lucrative water usage fees collected from

23

existing and new customers alike; (ii) the depreciation of the utility through the

time new users connect; and (iii) the debt the City undertook to acquire the facility,

no impact fee could satisfy the Dual Rational Nexus Test in this case.

Second, the City’s argument in Points III(B) and IV that it was entitled to

rely on its consultant’s recommendations fails because they were not based on the

governing Dual Rational Nexus Test. As his staff’s contemporaneous

communications revealed, the consultant not only failed to conduct that analysis,

but did so purposefully. The deference the City seeks is not deference to its

discretionary policy decisions or even to any legislative findings of fact; rather it is

a rubber stamp inconsistent with constitutionally required judicial review of

whether the fees comply with applicable law.

Third, the nature of the Dual Rational Nexus Test defeats the City’s

argument in Point V that Judge Davis exceeded his scope of review by answering

the question of whether the revenue from the usage fees paid by new and existing

customers was sufficient to pay for the entire utility with its excess capacity. Judge

Davis did not question the City’s discretionary determinations that it needed to buy

the utility, pay the agreed price, or finance a portion of the purchase through

revenue bonds.

IV. Finally, the City’s argument in Point VI that the same fees it has

consistently recognized were impact fees are actually user fees is devoid of merit.

24

Judge Davis correctly concluded that the Impact Fees are impact fees, not user

fees, because they are a one-time charge with no relationship to the amount of

water usage.

ARGUMENT

As Judge Davis found based on ample evidence, the City instituted this

litigation as a tactic to circumvent Conlon’s (and the rest of the class she

represents) day in court on the validity of the Impact Fees. (City App. 10-11.) Even

though the City has acknowledged that the Impact Fees are not necessary to repay

the 2013B Bonds and the City did not seek validation of the prior bonds that are

being refinanced, it did so this time for the specific purpose of precluding Conlon’s

pending class action challenge to those fees. (City App. 11.)

Part I reveals two critical limitations on this Court’s standard of review that

the counterpart in the initial brief ignores. Part II answers its counterpart by

demonstrating that the City’s position in this appeal is based on a clear

mischaracterization of Judge Davis’ reasoning and depends on an assertion of error

that is waived, unpreserved, doubly harmless, and meritless. Part III rebuts the

disjointed and overlapping arguments in Parts III, IV, and V of the initial brief that

the Impact Fees comply with the Dual Rational Nexus Test. Finally, part IV

exposes the frivolous nature of the City’s claim in Part VI of the initial brief that

25

the Impact Fees are really user fees free from the confines of the Dual Rational

Nexus Test.

I. THE STANDARD OF REVIEW FOR THE TRIAL COURT’S LEGAL CONCLUSION IS DE NOVO, AND THE STANDARD FOR ITS FINDINGS OF FACT IS COMPETENT, SUBSTANTIAL EVIDENCE.

The City is correct in noting that the standard Judge Davis was required to

apply in deciding whether to validate the 2013B Bonds was (1) whether the City

has authority to issue them, (2) whether their purpose is legal, and (3) whether the

authorization of the bonds complies with the requirements of the law. City of

Gainesville v. State, 863 So. 2d 138, 143 (Fla. 2003). It is also correct that the

specific issue in this case falls under the first prong: the validity of the Impact Fees

which the City offers as security for the bonds. See id. (“Subsumed within the

inquiry as to whether the public body has the authority to issue the subject bond is

the legality of the financing agreement upon which the bond is secured.” (Quoting

State v. City of Port Orange, 650 So. 2d 1, 3 (Fla. 1994))).

The City is only partially correct that the standard of review for this Court is

de novo. This is an incomplete statement of the standard of review because it

overlooks this Court’s clear pronouncements that (1) the appellant in a bond

validation appeal has the burden of demonstrating error and, more importantly, (2)

the trial court’s findings of fact are reviewed under the deferential competent,

substantial evidence test. E.g., Donovan v. Okaloosa County, 82 So. 3d 801, 805

26

(Fla. 2012). Thus, except to the extent the City demonstrated in its initial brief that

a finding was not supported by any competent, substantial evidence, this Court is

bound by Judge Davis’ findings.

II. THE TRIAL COURT APPLIED THE DUAL RATIONAL NEXUS TEST, AND THE CITY’S ARGUMENTS REGARDING THE FLORIDA IMPACT FEE ACT ARE WAIVED, UNPRESERVED, HARMLESS, AND MERITLESS.

The City’s primary argument is that instead of applying the common law

Dual Rational Nexus Test, which the City concedes is the governing standard,

Judge Davis applied the standards imposed under the Florida Impact Fee Act,

section 163.31801(5), Florida Statutes (2013) (the “Act”). With one unpreserved

and inconsequential exception discussed below, this is simply untrue as is evident

on the face of Judge Davis’ judgment. He cast the issue before him as “the

lawfulness of the Impact Fees under the Dual Rational Nexus Test.” (City App. 8.)

He devoted two numbered paragraphs to setting forth “The Requirements of the

Dual Rational Nexus Test,” twelve numbered paragraphs to his analysis of why the

City failed to prove that it had satisfied this test, and ten more to his analysis of

why Conlon proved by a preponderance of the evidence that the test was not met.

(City App. 11-23.)

Nowhere did Judge Davis analyze whether the Impact Fee satisfied the

standards imposed by the Act, which are (a) that the “calculation of the impact fee

be based on the most recent and localized data,” (b) that the government provide

27

for “accounting and reporting of impact fee collections and expenditures,” (c) that

administrative charges for collecting impact fees be limited to “actual costs,” and

(d) that 90-day advance notice be provided before imposition of a new or increased

impact fee.3 § 163.31801(3), Fla. Stat. The City ironically constructs (In. Br. 19-

21) and then tries to rebut (In. Br. 21-23) an artificial argument that the effect of

the Act “is to change the common law ‘dual rational nexus’ test which Florida

courts have used to determine the validity of impact fees for over 30 years.” (In.

Br. 19.) Conlon declines to weigh in on this straw man argument because it is

simply not implicated by the decision under review in this case. Judge Davis made

it as clear as possible that he was applying the Dual Rational Nexus Test as

established by decisions of this Court long ago.

The only provision of the Act that Judge Davis referenced in determining the

validity of the Impact Fees was paragraph 5, which provides:

In any action challenging an impact fee, the government has the burden of proving by a preponderance of the evidence that the imposition or amount of the fee meets the requirements of state legal precedent or this section. The court may not use a deferential standard.

(City App. 9.) Judge Davis cited this standard only for the burden of proof and

3 Judge Davis did note that this last requirement was the reason that a

2009 ordinance increasing the amount of the impact fees was invalid. (City App. 9.) But the City not only agrees, but emphasizes the illegality of its own ordinance under the Act in arguing why its 2013 ordinance repealing the rate increase did not “reinstate” the original impact fee for retroactivity purposes. (In. Br. 15.)

28

never suggested that it impacted the level of deference he afforded the City. To the

contrary, he made clear that he did give deference “to certain of the City’s

discretionary policy decisions, such as the decision to purchase the water utility

and the price paid for the water utility.” (City App. 9.) He then stated that “whether

the Impact Fees comply with Florida’s Dual Rational Nexus Test is an issue for the

Court because the City has no discretion to impose fees that do not comply with

applicable law.” (City App. 9-10.) That truism was as valid before the Act as it is

after. In any event, the City has failed to show Judge Davis’ isolated invocation of

section 163.31801(5) was reversible error for no less than five reasons.

1. The City makes no argument that Judge Davis erred in finding that the

City bore the burden of proof. Its argument is that Judge Davis applied the wrong

substantive standard, which is patently incorrect. By failing to argue in the initial

brief that Judge Davis erred with regard to the burden of proof, the City has waived

this issue. E.g. Hoskins v. State, 75 So. 3d 250, 257 (Fla. 2011).

2. The City did not preserve the issue below. The City provides no

indication that it made this argument to Judge Davis, and Conlon has been unable

to find any place in the trial transcript, or in any document or argument submitted

to Judge Davis, where the City made any argument whatsoever regarding whether

any part of the Act, much less paragraph 5, applies to this case. See, e.g., Dober v.

Worrell, 401 So. 2d 1322, 1323-24 (Fla. 1981) (holding that an appellant cannot

29

raise an argument for the first time on appeal). The City certainly did not object to

the form of the final judgment on this ground or move for rehearing on any ground.

See, e.g., Pensacola Beach Pier, Inc. v. King, 66 So. 3d 321, 324 (Fla. 1st DCA

2011) (when an issue appears for the first time in the trial court’s final order, the

appellant must have moved for rehearing to preserve the issue for appeal); Lake

Sarasota, Inc. v. Pan Am. Sur. Co., 140 So. 2d 139, 142 (Fla. 2d DCA 1962)

(same).

3. Any error in concluding that the City bore the burden of proof

pursuant to the Act was harmless because Judge Davis also relied on alternative

grounds that the City does not challenge. He noted that “as the Plaintiff in this

action,” the City generally bore the burden of proof, a conclusion that the City does

not challenge. (City App. 9.) While the question of whether section 163.31801(5)

changes the burden of proof in a case like the class action where Conlon is the

plaintiff is not presented by this case. The City chose to invoke the trial court’s

authority to validate the 2013B Bonds in an attempt to preclude Conlon’s

challenge, so it clearly undertook the burden of proof.

4. Any error in finding that the City bore the burden of proof was

harmless for another reason. Judge Davis made a clear alternative finding that

Conlon would have satisfied the burden of proof it she bore it. (City App. 10.) He

also made clear in his findings of fact that Conlon’s evidence was sufficient to

30

demonstrate that the Impact Fees violated the Dual Rational Nexus Test by a

preponderance of the evidence. (City App. 19-23.)

5. The City is wrong on the merits. Its retroactivity arguments made for

the first time in this Court might have merit regarding the substantive standards

imposed on Impact Fees in paragraph 3 of the Act, but they have no application to

the procedural requirements for a challenge to the Impact Fees contained in

paragraph 5. § 163.31801, Fla. Stat. The City concedes that paragraph 5 applies

retroactively to 2009 (In. Br. 18-19), which is about two years before Conlon

brought her 2011 class action challenge to the Impact Fees and four years before

the City initiated the 2013 bond validation proceedings.

The City seeks to avoid the obvious result that applying paragraph 5 in this

case therefore poses no retroactivity problem by contending that the date of the

challenge to the fees is immaterial because the Act changes the substantive

standards for impact fees. (In. Br. 19-21.) But it is paragraph 3 of the Act that

governs substantive standards, and paragraph 5 purely governs the procedures to

be applied in litigation. § 163.31801, Fla. Stat. Had the City ever made this

argument to Judge Davis, he likely would have rejected it in light of ample case

law holding that changes to the burden and quality of proof required in litigation

are procedural matters that apply in actions filed after the effective date, even

where the underlying cause of action arose well before the effective date. E.g.,

31

Kenz v. Miami-Dade County, 116 So. 3d 461, 463-66 (Fla. 3d DCA 2013); City of

Clermont v. Rumph, 450 So. 2d 573, 575 (Fla. 1st DCA 1984) (citing Sullivan v.

Mayo, 121 So. 2d 424 (Fla. 1960)).

III. THE TRIAL COURT CORRECTLY CONCLUDED THAT THE IMPACT FEES FAIL THE DUAL RATIONAL NEXUS TEST.

Judge Davis concluded that the Impact Fees were invalid under the Dual

Rational Nexus Test through two alternative paths. First, based on his conclusion

that the City bore the burden of proof, he explained the requirements of the test,

reviewed the City’s evidence, and concluded that the City had not met its burden

under either prong. (City App. 11-19.) Second, to demonstrate that he would have

reached the same result had Conlon born the burden of proof, he reviewed her

evidence and alternatively concluded that she had affirmatively established six

different reasons why the Impact Fees failed the test. (City App. 19-23.) This Court

should affirm Judge Davis’ conclusion that the Impact Fees are invalid under the

Dual Rational Nexus Test because (A) the City has made no attempt to

demonstrate error in Judge Davis’ primary rationale and (B) even if the City had

preserved a meritorious argument that Conlon bore the burden of proof, its

challenges to his alternative reasoning are meritless.

A. Having Failed to Explain How the Impact Fees Satisfy the Dual Rational Nexus Test, the City Has Shown No Error.

Noticeably absent from the initial brief is an argument as to how the Impact

32

Fees satisfy the two prongs of the Dual Rational Nexus Test. The City never even

articulates the test, much less attempts to apply it to the facts. Other than knowing

that the City agrees that the Dual Rational Nexus Test governs the validity of the

Impact Fees (subject to its desperation argument that the Impact Fees are really

user fees), a reader of the initial brief would have no idea what the test requires.

One can suppose from the name that it requires two kinds of rational relationships,

but the initial brief gives no indication as to what those required relationships

might be. An appellant simply cannot meet its burden of demonstrating that the

trial court erred in finding that a legal test is not met without first explaining what

the test is and why the appellant believes all its requirements have been satisfied.

Thus, unless the Court were to excuse the City from that burden and comb through

the initial brief to see if the City’s arguments are tantamount to showing that the

unstated dual requirements of the test are satisfied, it should simply skip the rest of

this section and move on to Part IV.

But even if the Court were to undertake such a search, it would be in vain.

None of the City’s arguments correlate to the requirements of the Dual Rational

Nexus Test. In stark contrast to the City, Judge Davis’ judgment thoroughly

considered and applied the requirements of the test from this Court’s decisions in

Volusia County v. Aberdeen at Ormond Beach, L.P., 760 So. 2d 126 (Fla. 2000),

St. Johns County v. Northeast Florida Builders Ass’n, 583 So. 2d 635 (Fla. 1991),

33

and Contractors & Builders Ass’n of Pinellas County v. City of Dunedin, 329

So. 2d 314 (Fla. 1976). (City App. 11-23.)

The City fails to cite either the lead case on which Judge Davis relied (St.

Johns County) or the most recent case (Volusia County). It does cite City of

Dunedin, but that decision predated this Court’s adoption of the Dual Rational

Nexus Test by close to fifteen years. See Volusia County, 760 So. 2d at 134 (noting

that “this Court in St. Johns County adopted the dual rational nexus test exactly as

it was enunciated in Hollywood, Inc. v. Broward County, 431 So. 2d 606 (Fla. 4th

DCA 1983)). Moreover, as shown below, that decision is only relevant to the

second prong.

As the name suggests, the Dual Rational Nexus Test has two prongs. To

satisfy the first prong,

the local government must demonstrate a reasonable connection, or rational nexus, between the need for additional capital facilities and the growth in population generated by the subdivision.

St. Johns County, 583 So. 2d at 637 (quoting Hollywood, Inc., 431 So. 2d at 611).

The first requirement is drawn not from City of Dunedin, but from Wald Corp. v.

Metropolitan Dade County, 338 So. 2d 863 (Fla. 3d DCA 1976), which held that

“impact fee ordinances are valid when there is a reasonable connection between

the required…fee and the anticipated needs of the community because of the new

34

development.” Hollywood, Inc., 431 So. 2d at 611 (citing Wald Corp, 338 So. 2d at

867-68).

The second prong requires the local government to

show a reasonable connection, or rational nexus, between the expenditures of the funds collected [the impact fees] and the benefits accruing to the subdivision. In order to satisfy this latter requirement, the ordinance must specifically earmark the funds collected for use in acquiring capital facilities to benefit the new residents.

St. Johns County, 583 So. 2d at 637 (quoting Hollywood, Inc., 431 So. 2d at 611-

12). This requirement is derived from City of Dunedin, which recognized that

when a municipality needs to expand its water system to satisfy new demand, new

users can be made to bear the cost through connection fees, but only “[i]f use of the

money collected is limited to meeting the costs of expansion.” City of Dunedin,

329 So. 2d at 320. Specifically, the City of Dunedin Court stated