IN THE SECOND DISTRICT COURT OF APPEAL IN AND FOR THE STATE OF FLORIDA … · 2017-04-06 · IN AND...

38

IN THE SECOND DISTRICT COURT OF APPEAL IN AND FOR THE STATE OF FLORIDA BRENDAN BRINDISE and, SUZANNE BRINDISE, Appellants, Case No. 2D14-3316 v. L.T. No.: 12-CA-56544 U.S. BANK NATIONAL ASSOCIATION, AS TRUSTEE, FOR THE BENEFIT OF HARBORVIEW 2005-3 TRUST FUND, Appellee. ___________________________________/ ON APPEAL FROM THE CIRCUIT COURT OF THE TWENTIETH JUDICIAL CIRCUIT IN AND FOR LEE COUNTY, FLORIDA __________________________________________________________________ APPELLANT’S INITIAL BRIEF ________________________________________________________________ _____________________________ Mark P. Stopa, Esquire FBN: 550507 STOPA LAW FIRM 2202 N. Westshore Blvd. Suite 200 Tampa, FL 33607 (727) 851-9551 [email protected] ATTORNEY FOR APPELLANTS

Transcript of IN THE SECOND DISTRICT COURT OF APPEAL IN AND FOR THE STATE OF FLORIDA … · 2017-04-06 · IN AND...

IN THE SECOND DISTRICT COURT OF APPEAL

IN AND FOR THE STATE OF FLORIDA

BRENDAN BRINDISE and,

SUZANNE BRINDISE,

Appellants,

Case No. 2D14-3316

v.

L.T. No.: 12-CA-56544

U.S. BANK NATIONAL ASSOCIATION,

AS TRUSTEE, FOR THE BENEFIT OF

HARBORVIEW 2005-3 TRUST FUND,

Appellee.

___________________________________/

ON APPEAL FROM THE CIRCUIT COURT

OF THE TWENTIETH JUDICIAL CIRCUIT

IN AND FOR LEE COUNTY, FLORIDA

__________________________________________________________________

APPELLANT’S INITIAL BRIEF

________________________________________________________________

_____________________________

Mark P. Stopa, Esquire

FBN: 550507

STOPA LAW FIRM

2202 N. Westshore Blvd.

Suite 200

Tampa, FL 33607

(727) 851-9551

ATTORNEY FOR APPELLANTS

i

TABLE OF CONTENTS

TABLE OF AUTHORITIES ....................................................................... ii-iv

STATEMENT OF THE CASE .................................................................... 1

SUMMARY OF ARGUMENT .................................................................... 8

STANDARD OF REVIEW .......................................................................... 10

ARGUMENT ................................................................................................. 11

I. THE LOWER COURT ERRED BY ENTERING THE

FINAL JUDGMENT OF FORECLOSURE WHERE

THE BANK DID NOT GIVE BRINDISE WRITTEN

NOTICE OF THE ASSIGNMENT OF THE DEBT,

AS REQUIRED BY FLA. STAT. 559.715. ..................................... 11

CONCLUSION .............................................................................................. 31

CERTIFICATE OF SERVICE ................................................................... 32

CERTIFICATE OF FONT COMPLIANCE ............................................. 32

ii

TABLE OF AUTHORITIES

American Integrity Ins. Co. of America v. Gainey,

100 So. 3d 720 (Fla. 2d DCA 2012) ..................................................... 10, 12

Andrews v. Direct Mail Express, Inc.,

1 So. 3d 131 (Fla. 4th DCA 2010) ........................................................ 10

Banco Espirito Santo, Ltd. v. BBO Int'l, B.V.,

979 So. 2d 1030 (Fla. 3d DCA 2008) ................................................... 10

Battle v. Gladstone Law Group, P.A.,

2014 U.S. Dist. LEXIS 91621 .............................................................. 19

Birster v. Am. Home Mortg. Servicing, Inc.,

481 App'x 579 (11th Cir. 2012) ............................................................ passim

Brown v. City of Vero Beach,

64 So. 3d 172 (Fla. 4th DCA 2011) ...................................................... 21

Burt v. Hudson & Keyse, LLC,

138 So. 3d 1193 (Fla. 5th DCA 2014) .................................................. passim

Carsillo v. City of Lake Worth,

995 So. 2d 1118 (Fla. 4th DCA 2008) .................................................. 19

Commercial Carrier Corp. v. Indian River County,

371 So. 2d 1010 (Fla. 1979) ................................................................. 24

Correa v. U.S. Bank, N.A.,

118 So. 3d 952 (Fla. 2d DCA 2013) ..................................................... 10, 29

Fla. Dept. of Revenue v. Fla. Municipal Power Agency,

789 So. 2d 320 (Fla. 2001) ................................................................... 27

iii

Freire v. Aldridge Connors, LLP,

994 F.Supp. 2d 1284 (S.D. Fla. 2014) .................................................. 19, 24

Freni v. Collier County,

588 So. 2d 291 (Fla. 2d DCA 1991) ..................................................... 24

Gann v. BAC Home Loans Servicing,

145 So 3d 906 (Fla. 2d DCA 2014) ...................................................... passim

Hall v. MLG, P.A.,

2013 U.S. Dist. LEXIS 157414 (S.D. Fla. 2013) ................................. 20

Hallstrom v. Tillamook County,

493 U.S. 20 (1989)................................................................................ 24

Lacombe v. Deutsche Bank Nat'l Trust Co.,

149 So. 3d 152 (Fla. 1st DCA 2014) .................................................... 10, 29

Lara v. Specialized Loan Servicing, LLC,

2013 U.S. Dist. LEXIS 127192 (S.D. Fla. 2013) ................................. 20

LeBanc v. Unifund CCR Partners,

601 F.3d 1185 (11th Cir. 2000) ............................................................ 28

Legg v. Voice Media Group, Inc.,

990 F.Supp. 2d 1351 (S.D. Fla. 2014) .................................................. 28

Lewis v. Marinosci Law Group, P.C.,

2013 U.S. Dist. LEXIS 156732 (S.D. Fla. 2013) ................................. 20

Martin County v. Polivka Paving, Inc.,

44 So. 3d 126 (Fla. 4th DCA 2010) ...................................................... 10

Motor v. Citrus County School Board,

856 So. 2d 1054 (Fla. 5th DCA 2003) .................................................. 11

iv

Neate v. Cypress Club Condo.,

718 So. 2d 390 (Fla. 4th DCA 1998) (en banc) ................................... 24

Pino v. Bank of New York,

121 So. 3d 23 (Fla. 2013) ..................................................................... 13

Read v. MFP, Inc.,

85 So. 3d 1151 (Fla. 2d DCA 2012) ..................................................... 27

Reese v. Ellis, Painter, Ratterree & Adams, LLP,

678 F.3d 1211 (11th Cir. 2012) ............................................................ passim

Sheriff of Orange County v. Boultbee,

595 So. 2d 985 (Fla. 5th DCA 1992) .................................................... passim

Smith v. Piezo Tech. and Prof. Administrators,

427 So. 2d 182 (Fla. 1983) ................................................................... 27

State v. Goode,

830 So. 2d 817 (Fla. 2002) ................................................................... 27

Temple v. Aujla,

681 So. 2d 1198 (Fla. 5th DCA 1996) .................................................. 26

Trent v. Mortg. Electronic Registration Systems, Inc.,

618 F.Supp. 2d 1356 (M.D. Fla. 2007) ................................................ passim

Wolkoff v. American Home Mortg. Servicing, Inc.,

Case No. 2D12-6460 (Fla. 2d DCA 2014) ........................................... 29

Fla. Stat. 559.55 .............................................................................................. passim

Fla.Stat. 559.715 ............................................................................................. passim

Fla.Stat. 559.72 ............................................................................................... passim

1

STATEMENT OF THE CASE AND FACTS

Appellee, U.S. Bank National Association, as Trustee for the Benefit of

Harborview 2005-3 Trust Fund (“the Bank”), initiated the lower court case by suing

to foreclose the homestead of Appellants, Brendan and Suzanne Brindise

(“Brindise”), and to recoup a deficiency. R.1-32; 55-91.

After a non-jury trial, the lower court entered a Final Judgment of Foreclosure.

The trial transcript reflects a litany of errors, see n.2, infra, but Brindise appeal on

just one: the lower court’s entry of judgment in favor of the Bank notwithstanding

the Bank’s failure to comply with a condition precedent, i.e. the notice required by

Fla. Stat. 559.715.

In its Amended Complaint, the Bank generally alleged compliance with

conditions precedent. R.55-91, ¶ 9. In their Answer to the Amended Complaint,

Brindise specifically denied such compliance. In particular, Brindise asserted the

Bank “did not comply with Fla. Stat. 559.715,”1 R.104-108, ¶ 9, which statute

1 In their Motion for Summary Judgment, Brindise expounded upon the

rationale for their specific denial of this condition precedent. R.123-125. To wit,

Brindise set federal case law interpreting the federal counterpart of Fla. Stat. 559.715

and argued the statute required that the Bank give Brindise written notice of the

assignment of the debt 30 days before filing this lawsuit. R.123-125. Brindise also

filed affidavits showing the Bank had not given them the notices. R.127-131.

Though time constraints prevented the Motion for Summary Judgment from being

heard before trial, these documents (coupled with the specific denial in their Answer)

2

provides:

559.715 Assignment of consumer debts.—This part does not prohibit the

assignment, by a creditor, of the right to bill and collect a consumer debt.

However, the assignee must give the debtor written notice of such

assignment as soon as practical after the assignment is made, but at least

30 days before any action to collect the debt.

(boldface added).

At trial, the Bank introduced no evidence to prove compliance with Fla. Stat.

559.715. Just one witness testified, an employee of Nationstar Mortgage, LLC

(“Nationstar”) named Jose Perez (“Mr. Perez”), and his testimony said absolutely

nothing about the Bank having given Brindise written notice of the assignment of

debt. R.246-247. In fact, the only time the Bank was even mentioned during its case

in chief was when Brindise objected to Mr. Perez, a Nationstar employee, testifying

on behalf of the Bank.2

plainly alerted the Bank to the existence of this defense and put the Bank on notice

of their intent to argue 559.715 non-compliance at trial. 2 The Power of Attorney relied upon by Nationstar to testify on the Bank’s

behalf made clear that it was “limited” to those trusts identified on Exhibit “A”

thereof, and the trust in question was not one of the trusts listed. R.157-174. While

Mr. Perez wanted to assert otherwise by pointing to line item #147 of that exhibit,

that trust was “HarborView Mortgage Loan Trust 2005-3 Mortgage Loan Pass-

Through Certificates, Series 2005-1,” whereas the trust named as the plaintiff herein

is “HarborView 2005-3 Trust Fund.” R.157-174.

Brindise considered appealing on this basis, not to mention the Bank’s lack of

standing at the inception of the case and the absence of any admissible evidence

showing compliance with paragraph 22. Candidly, however, Brindise chose to

3

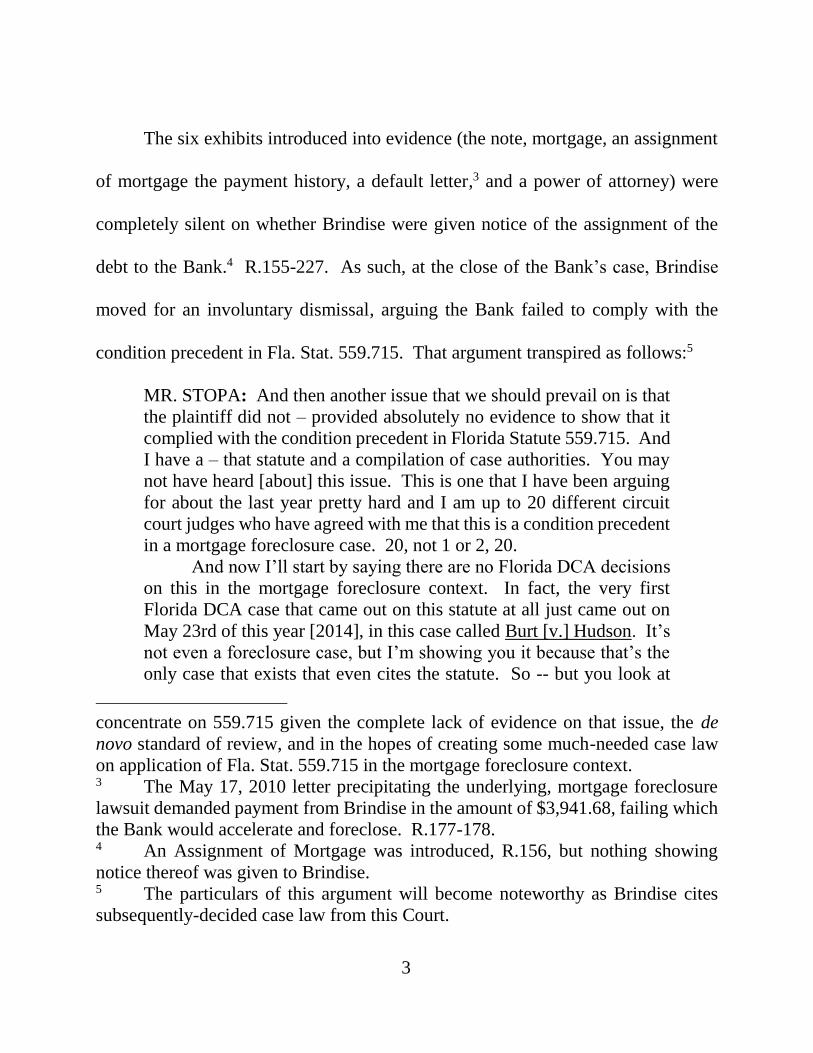

The six exhibits introduced into evidence (the note, mortgage, an assignment

of mortgage the payment history, a default letter,3 and a power of attorney) were

completely silent on whether Brindise were given notice of the assignment of the

debt to the Bank.4 R.155-227. As such, at the close of the Bank’s case, Brindise

moved for an involuntary dismissal, arguing the Bank failed to comply with the

condition precedent in Fla. Stat. 559.715. That argument transpired as follows:5

MR. STOPA: And then another issue that we should prevail on is that

the plaintiff did not – provided absolutely no evidence to show that it

complied with the condition precedent in Florida Statute 559.715. And

I have a – that statute and a compilation of case authorities. You may

not have heard [about] this issue. This is one that I have been arguing

for about the last year pretty hard and I am up to 20 different circuit

court judges who have agreed with me that this is a condition precedent

in a mortgage foreclosure case. 20, not 1 or 2, 20.

And now I’ll start by saying there are no Florida DCA decisions

on this in the mortgage foreclosure context. In fact, the very first

Florida DCA case that came out on this statute at all just came out on

May 23rd of this year [2014], in this case called Burt [v.] Hudson. It’s

not even a foreclosure case, but I’m showing you it because that’s the

only case that exists that even cites the statute. So -- but you look at

concentrate on 559.715 given the complete lack of evidence on that issue, the de

novo standard of review, and in the hopes of creating some much-needed case law

on application of Fla. Stat. 559.715 in the mortgage foreclosure context. 3 The May 17, 2010 letter precipitating the underlying, mortgage foreclosure

lawsuit demanded payment from Brindise in the amount of $3,941.68, failing which

the Bank would accelerate and foreclose. R.177-178. 4 An Assignment of Mortgage was introduced, R.156, but nothing showing

notice thereof was given to Brindise. 5 The particulars of this argument will become noteworthy as Brindise cites

subsequently-decided case law from this Court.

4

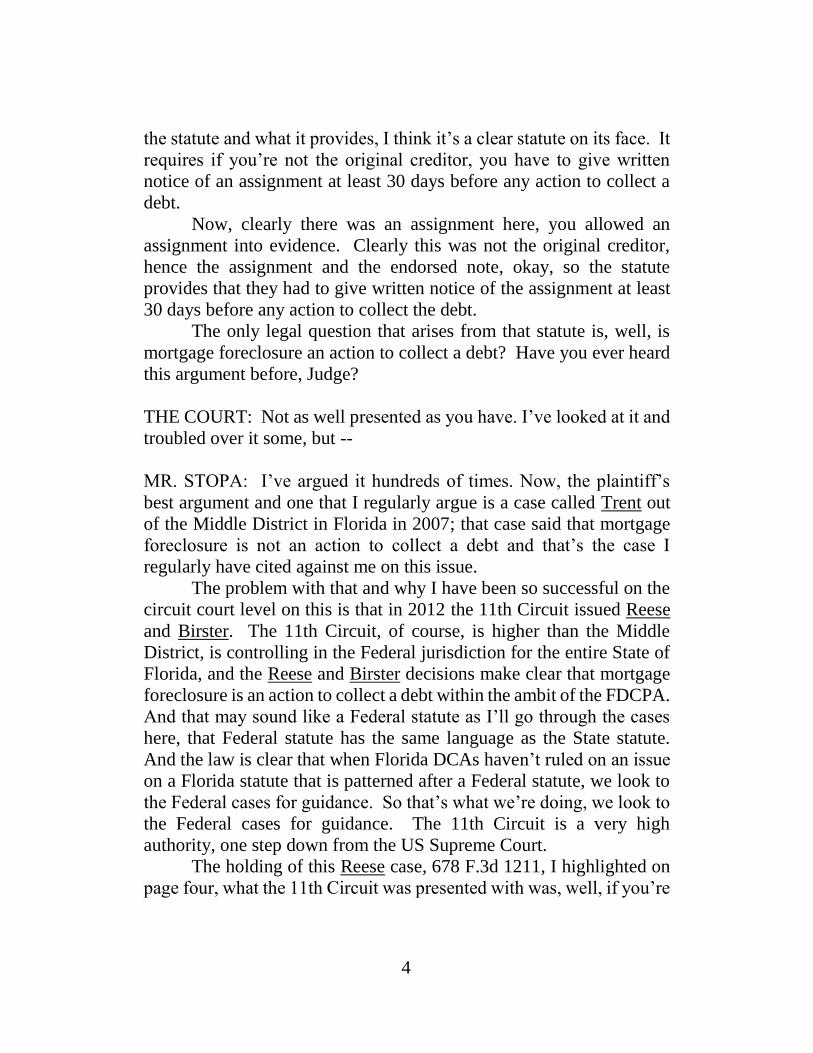

the statute and what it provides, I think it’s a clear statute on its face. It

requires if you’re not the original creditor, you have to give written

notice of an assignment at least 30 days before any action to collect a

debt.

Now, clearly there was an assignment here, you allowed an

assignment into evidence. Clearly this was not the original creditor,

hence the assignment and the endorsed note, okay, so the statute

provides that they had to give written notice of the assignment at least

30 days before any action to collect the debt.

The only legal question that arises from that statute is, well, is

mortgage foreclosure an action to collect a debt? Have you ever heard

this argument before, Judge?

THE COURT: Not as well presented as you have. I’ve looked at it and

troubled over it some, but --

MR. STOPA: I’ve argued it hundreds of times. Now, the plaintiff’s

best argument and one that I regularly argue is a case called Trent out

of the Middle District in Florida in 2007; that case said that mortgage

foreclosure is not an action to collect a debt and that’s the case I

regularly have cited against me on this issue.

The problem with that and why I have been so successful on the

circuit court level on this is that in 2012 the 11th Circuit issued Reese

and Birster. The 11th Circuit, of course, is higher than the Middle

District, is controlling in the Federal jurisdiction for the entire State of

Florida, and the Reese and Birster decisions make clear that mortgage

foreclosure is an action to collect a debt within the ambit of the FDCPA.

And that may sound like a Federal statute as I’ll go through the cases

here, that Federal statute has the same language as the State statute.

And the law is clear that when Florida DCAs haven’t ruled on an issue

on a Florida statute that is patterned after a Federal statute, we look to

the Federal cases for guidance. So that’s what we’re doing, we look to

the Federal cases for guidance. The 11th Circuit is a very high

authority, one step down from the US Supreme Court.

The holding of this Reese case, 678 F.3d 1211, I highlighted on

page four, what the 11th Circuit was presented with was, well, if you’re

5

a creditor and you’re suing for money, then the FDCPA requires that

you give notice of assignment of the debt before you sue –

THE COURT: I think you’ve made your argument. I’m not even sure

this is plead, is it?

MR. STOPA: It is, Judge. It’s in our answer, it’s specifically denied

in our answer, and I –

THE COURT: I didn’t see it when I looked at it.

MR. STOPA: It’s not an affirmative defense. It’s specifically denied

in the answer, so they generally plead condition precedent, we

specifically deny in our answer. It’s certainly a plead issue. I’ve done

it this way hundreds of times. And the Boultbee case that I’ve provided

you provides that – oh, here, I can give you Robert Motor, too – that

this is not an affirmative defense. A condition precedent gets

specifically denied just as we’ve done here; that’s at 856 So. 2d 1054.

So it is certainly a plead issue before the Court and I want to make sure

you understand what these federal cases say since that’s really all we

have here.

THE COURT: I’ve read some of them.

MR. STOPA: Reese explains that a debt is still a debt even if it is

secured. They called it a loophole that wouldn’t make sense to have

the FDCPA apply if a creditor is suing for money, but to have it not

apply if they’re suing to foreclose a security interest that secures that

money. So they call it – they say that can’t make sense, it doesn’t make

sense, and they say the FDCPA, the statute applies whether you’re

suing to foreclose or for money, that you have to give the notice either

way.

Then Birster specifically applies that to mortgage foreclosure;

that’s Birster. And then Battle – I’m trying to go quickly here – Battle

reconciles Trent. Remember, Trent is the plaintiff’s best case, that 2007

Middle District Case. Battle reconciles Trent and Reese. The Battle

case cites Trent but then it says –

6

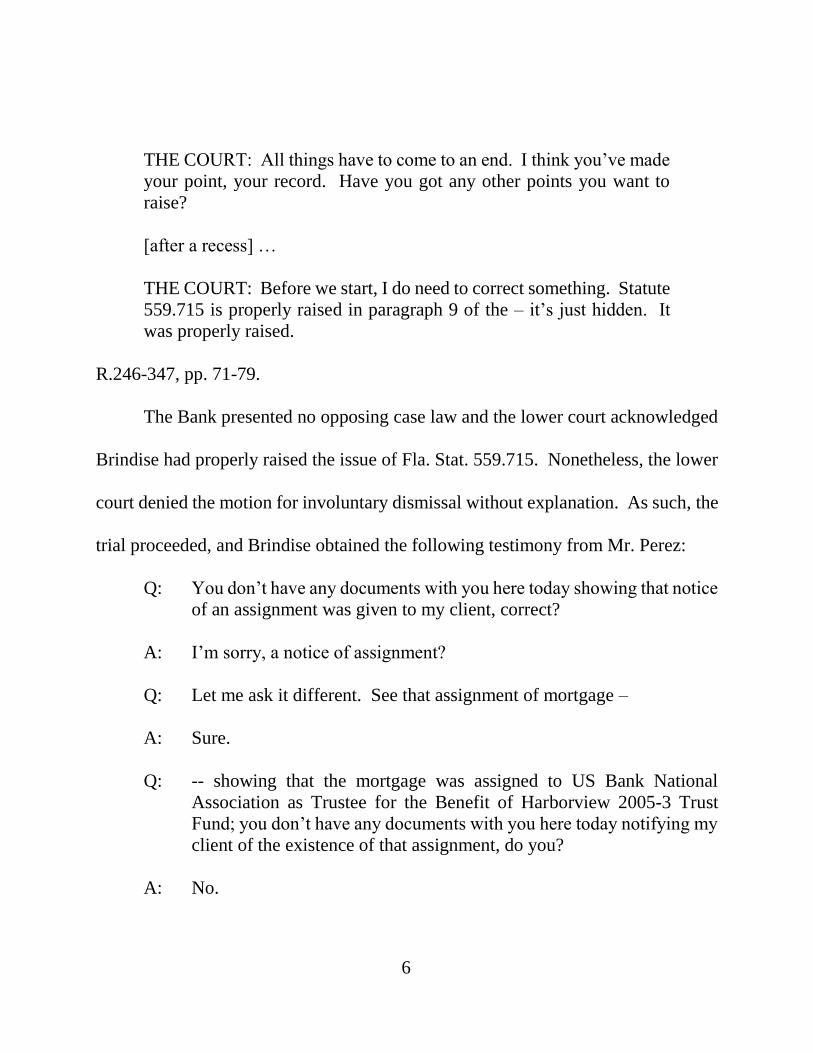

THE COURT: All things have to come to an end. I think you’ve made

your point, your record. Have you got any other points you want to

raise?

[after a recess] …

THE COURT: Before we start, I do need to correct something. Statute

559.715 is properly raised in paragraph 9 of the – it’s just hidden. It

was properly raised.

R.246-347, pp. 71-79.

The Bank presented no opposing case law and the lower court acknowledged

Brindise had properly raised the issue of Fla. Stat. 559.715. Nonetheless, the lower

court denied the motion for involuntary dismissal without explanation. As such, the

trial proceeded, and Brindise obtained the following testimony from Mr. Perez:

Q: You don’t have any documents with you here today showing that notice

of an assignment was given to my client, correct?

A: I’m sorry, a notice of assignment?

Q: Let me ask it different. See that assignment of mortgage –

A: Sure.

Q: -- showing that the mortgage was assigned to US Bank National

Association as Trustee for the Benefit of Harborview 2005-3 Trust

Fund; you don’t have any documents with you here today notifying my

client of the existence of that assignment, do you?

A: No.

7

Q: Nothing, no document with you here today indicating that to my client,

we’re now the holder of this loan, we’re the one who’s going to sue

you, nothing like that, correct?

A: No, I don’t have anything that says that, no.

R.236-347, pp. 79-81.

Notwithstanding the Bank’s admission that it had no notice of assignment, the

lower court again declined to enter an involuntary dismissal. Instead, the lower court

entered the Final Judgment of Foreclosure from which this timely appeal emanates.

8

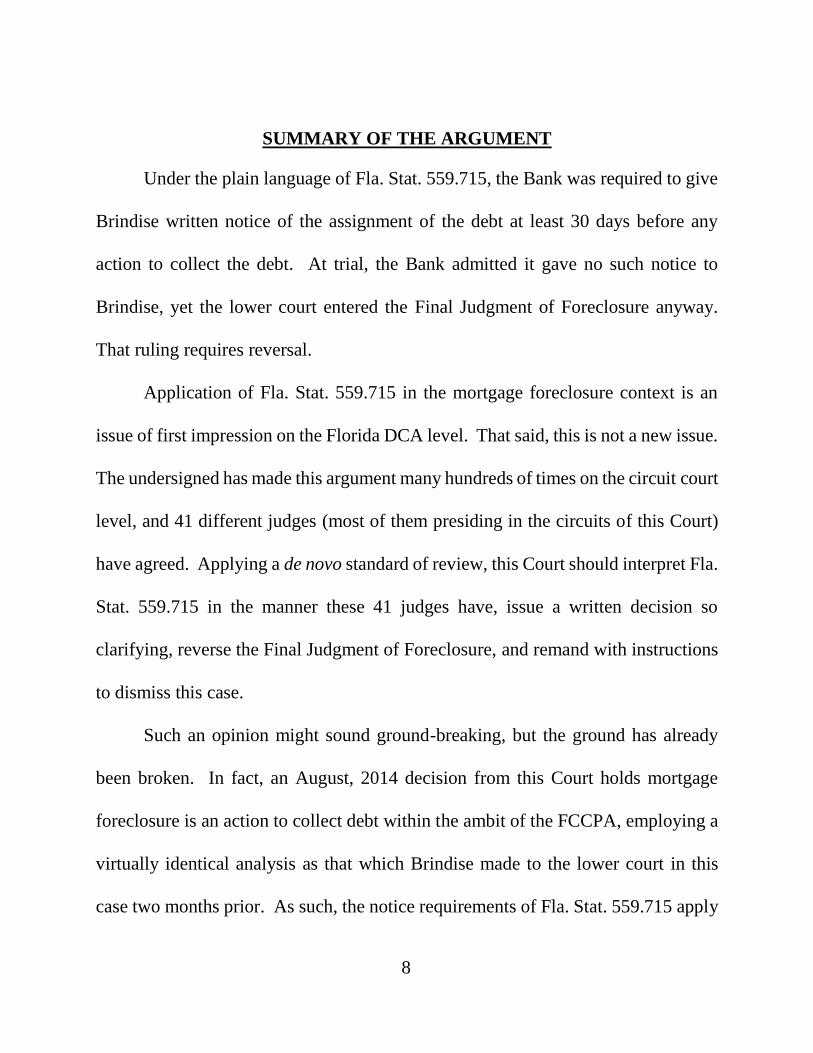

SUMMARY OF THE ARGUMENT

Under the plain language of Fla. Stat. 559.715, the Bank was required to give

Brindise written notice of the assignment of the debt at least 30 days before any

action to collect the debt. At trial, the Bank admitted it gave no such notice to

Brindise, yet the lower court entered the Final Judgment of Foreclosure anyway.

That ruling requires reversal.

Application of Fla. Stat. 559.715 in the mortgage foreclosure context is an

issue of first impression on the Florida DCA level. That said, this is not a new issue.

The undersigned has made this argument many hundreds of times on the circuit court

level, and 41 different judges (most of them presiding in the circuits of this Court)

have agreed. Applying a de novo standard of review, this Court should interpret Fla.

Stat. 559.715 in the manner these 41 judges have, issue a written decision so

clarifying, reverse the Final Judgment of Foreclosure, and remand with instructions

to dismiss this case.

Such an opinion might sound ground-breaking, but the ground has already

been broken. In fact, an August, 2014 decision from this Court holds mortgage

foreclosure is an action to collect debt within the ambit of the FCCPA, employing a

virtually identical analysis as that which Brindise made to the lower court in this

case two months prior. As such, the notice requirements of Fla. Stat. 559.715 apply

9

in mortgage foreclosure cases, particularly here, where the Bank’s lawsuit was

precipitated by a written demand for money and accompanied by a prayer for a

deficiency.

Once this Court concludes the statute applies, the only question left is what

remedy to employ for a violation thereof. The civil remedies statute of the FCCPA

authorizes a separate, civil action for violations of other portions of the FCCPA, but

not for a violation of Fla. Stat. 559.715. Hence, the only way to enforce the notice

requirement of the statute is to treat it as a defense, i.e. a condition precedent, and

dismiss lawsuits where the notice was not given. To rule otherwise would render

that portion of the statute meaningless and leave consumers without a remedy – the

wrong result in any context, but particularly so vis a vis a consumer protection

statute.

While most of the circuit judges within the ambit of this Court have agreed

with the analysis set forth herein,6 a few have not. Hence, a written decision is

necessary to clarify that Fla. Stat. 559.715 applies in the mortgage foreclosure

context and bars foreclosure where, as here, the notice is not given. This Court

should rule accordingly.

6 Well, most of the circuit judges who hear foreclosure cases, anyway.

10

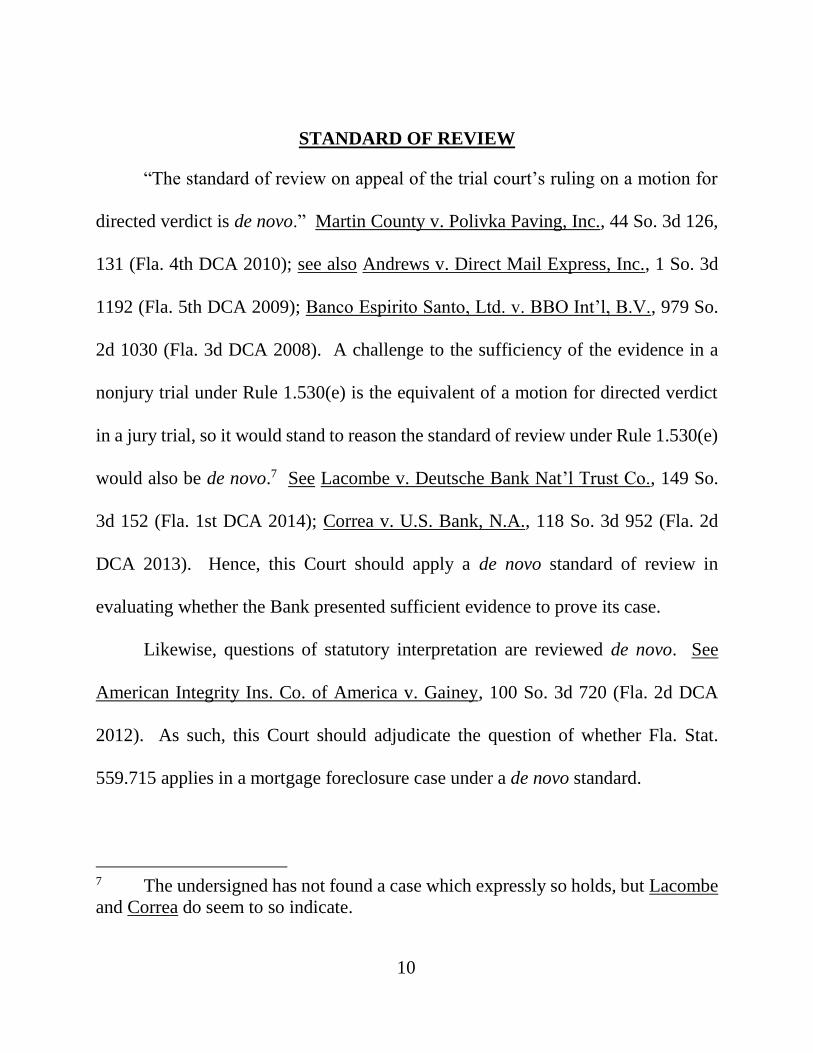

STANDARD OF REVIEW

“The standard of review on appeal of the trial court’s ruling on a motion for

directed verdict is de novo.” Martin County v. Polivka Paving, Inc., 44 So. 3d 126,

131 (Fla. 4th DCA 2010); see also Andrews v. Direct Mail Express, Inc., 1 So. 3d

1192 (Fla. 5th DCA 2009); Banco Espirito Santo, Ltd. v. BBO Int’l, B.V., 979 So.

2d 1030 (Fla. 3d DCA 2008). A challenge to the sufficiency of the evidence in a

nonjury trial under Rule 1.530(e) is the equivalent of a motion for directed verdict

in a jury trial, so it would stand to reason the standard of review under Rule 1.530(e)

would also be de novo.7 See Lacombe v. Deutsche Bank Nat’l Trust Co., 149 So.

3d 152 (Fla. 1st DCA 2014); Correa v. U.S. Bank, N.A., 118 So. 3d 952 (Fla. 2d

DCA 2013). Hence, this Court should apply a de novo standard of review in

evaluating whether the Bank presented sufficient evidence to prove its case.

Likewise, questions of statutory interpretation are reviewed de novo. See

American Integrity Ins. Co. of America v. Gainey, 100 So. 3d 720 (Fla. 2d DCA

2012). As such, this Court should adjudicate the question of whether Fla. Stat.

559.715 applies in a mortgage foreclosure case under a de novo standard.

7 The undersigned has not found a case which expressly so holds, but Lacombe

and Correa do seem to so indicate.

11

ARGUMENT

I. THE LOWER COURT ERRED BY ENTERING THE FINAL

JUDGMENT OF FORECLOSURE WHERE THE BANK DID NOT

GIVE BRINDISE WRITTEN NOTICE OF THE ASSIGNMENT OF

THE DEBT, AS REQUIRED BY FLA. STAT. 559.715.

Florida law requires plaintiffs to allege compliance with conditions precedent

generally; defendants must then specifically deny such compliance. See

Fla.R.Civ.P. 1.120(c). Here, the Bank pled compliance with conditions precedent

generally, R.55-91, ¶ 9, and Brindise denied compliance with Fla. Stat. 559.715

specifically, R.104-108, ¶ 9, so the burden of proving compliance with Fla. Stat.

559.715 at trial fell onto the Bank.8 In the words of the Fifth District:

In the instant case, appellee pled performance of all conditions

precedent as required by rule 1.120(c) of the Florida Rules of Civil

Procedure and, pursuant to the same rule, appellant specifically denied

that appellee complied with the requirements of section 768.28(6). A

specific denial of a general allegation of the performance or occurrence

of conditions precedent shifts the burden to the plaintiff to prove the

allegations concerning the subject matter of the specific denial.

Consequently, appellee had the burden to prove compliance with

8 A defendant’s specific denial of compliance with conditions precedent is

different than pleading an affirmative defense. As one judge put it:

“The denial of the occurrence of conditions precedent is not an

“affirmative defense,” which relates only to matters of avoidance.

Fla.R.Civ.P. 1.110(d). Rather, it is a special form of denial that must

be pled with specificity. Fla.R.Civ.P. 1.120(c).

Motor v. Citrus County School Board, 856 So. 2d 1054, 1055 n.1 (Fla. 5th DCA

2003) (Torpy, J., specially concurring).

12

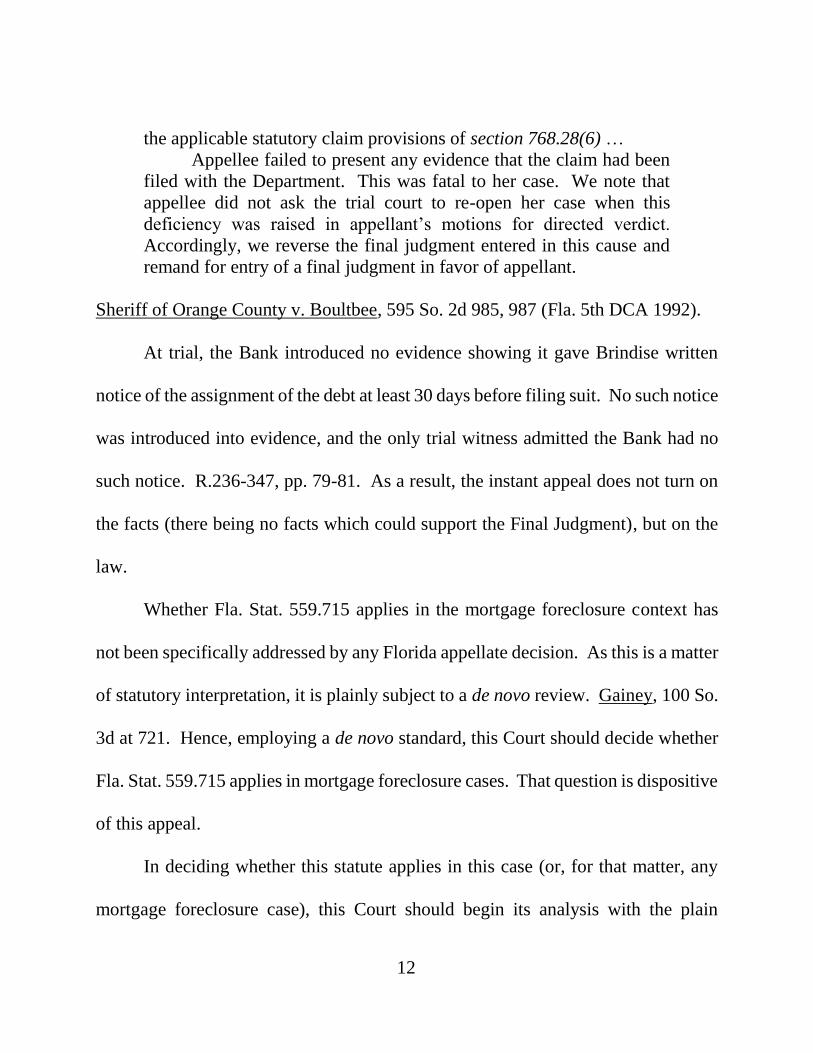

the applicable statutory claim provisions of section 768.28(6) …

Appellee failed to present any evidence that the claim had been

filed with the Department. This was fatal to her case. We note that

appellee did not ask the trial court to re-open her case when this

deficiency was raised in appellant’s motions for directed verdict.

Accordingly, we reverse the final judgment entered in this cause and

remand for entry of a final judgment in favor of appellant.

Sheriff of Orange County v. Boultbee, 595 So. 2d 985, 987 (Fla. 5th DCA 1992).

At trial, the Bank introduced no evidence showing it gave Brindise written

notice of the assignment of the debt at least 30 days before filing suit. No such notice

was introduced into evidence, and the only trial witness admitted the Bank had no

such notice. R.236-347, pp. 79-81. As a result, the instant appeal does not turn on

the facts (there being no facts which could support the Final Judgment), but on the

law.

Whether Fla. Stat. 559.715 applies in the mortgage foreclosure context has

not been specifically addressed by any Florida appellate decision. As this is a matter

of statutory interpretation, it is plainly subject to a de novo review. Gainey, 100 So.

3d at 721. Hence, employing a de novo standard, this Court should decide whether

Fla. Stat. 559.715 applies in mortgage foreclosure cases. That question is dispositive

of this appeal.

In deciding whether this statute applies in this case (or, for that matter, any

mortgage foreclosure case), this Court should begin its analysis with the plain

13

language of the statute. See e.g. Brown v. City of Vero Beach, 64 So. 3d 172 (Fla.

4th DCA 2011). Fla. Stat. 559.715 is part of the Florida Consumer Collection

Practices Act (“FCCPA”). The statute provides:

559.715 Assignment of consumer debts.—This part does not prohibit the

assignment, by a creditor, of the right to bill and collect a consumer debt.

However, the assignee must give the debtor written notice of such

assignment as soon as practical after the assignment is made, but at least

30 days before any action to collect the debt.

(boldface added).

Fla. Stat. 559.715 requires an assignee give a debtor written notice at least 30

days before any action to collect the debt. The term “debt” is defined by Florida

Statute 559.55(1). “Consumer debt” is given this same definition. While the

definition is quite broad, the statute is not 100% clear whether “mortgage

foreclosure” would constitute “debt” in this context. The question hence becomes

whether “mortgage foreclosure” is an “action to collect a debt” as defined by Fla.

Stat. 559.715.9

9 “Assignee” is not defined by Chapter 559. As such, this Court should resort to

its ordinary meaning, as from a dictionary. See Pino v. Bank of New York, 121 So.

3d 23 (Fla. 2013). “Assignment” is defined by West’s Encyclopedia of American

Law, Edition 2, Copyright 2008, as follows:

A transfer of rights in real property or personal property to another that

gives the recipient – the transferee – the rights that the owner or holder

of the property – the transferor – had prior to the transfer.

An “assignee,” hence, is anyone who receives such a transfer of rights in real or

14

Fla. Stat. 559.715 is mentioned in just one published decision, Burt v. Hudson

& Keyse, LLC, 138 So. 3d 1193 (Fla. 5th DCA 2014), and that was not a mortgage

foreclosure case. However, on August 15, 2014, this Court decided Gann v. BAC

Home Loans Servicing, LP, 145 So. 3d 906 (Fla. 2d DCA 2014), a ground-breaking

decision in that it held mortgage foreclosure plaintiffs are subject to the FCCPA, of

which Fla. Stat. 559.715 is part.

In Gann, “the bank argued that the enforcement of a security interest such as

a mortgage is not considered the collection of a consumer debt.” Id. at 908. In ruling

against the creditor, this Court began its analysis with a 2007 decision from the

Middle District of Florida, Trent v. Mortg. Electronic Registration Systems, Inc.,

618 F.Supp. 2d 1356 (M.D. Fla. 2007). Id. at 908. In 2007, Trent ruled “filing a

foreclosure lawsuit is not a debt collection practice under § 559.72 of the FCCPA.”

618 F.Supp. 2d at 1361.

As this Court clarified in Gann, however, Trent is no longer the law.

Following two 2012 decisions from the Eleventh Circuit (the Eleventh Circuit, of

personal property.

In the case at bar, there can be no doubt that the Bank fits the statutory

definition of “assignee.” As the face of the Note reflects, the Bank was not the

original creditor, but was transferred the Note and Mortgage in question via an

endorsed Note, R.199-202, and an Assignment of Mortgage. R.156.

15

course, being the controlling appellate court for the Middle District of Florida), this

Court explained:

The Bank filed a motion to dismiss the complaint and, with

respect to the FCCPA claim, argued that the enforcement of a security

interest such as a mortgage is not considered the collection of a

consumer debt …

Subsequent to Trent, the Eleventh Circuit considered a claim

under the Federal Act based on a letter and enclosed documents that a

law firm representing the lender sent to the debtors which demanded

payment of the debt and threatened to foreclose on the property if the

debtors did not pay. Reese v. Ellis, Painter, Ratterree & Adams, LLP,

678 F.3d 1211, 1214 (11th Cir. 2012). The law firm moved to dismiss

the complaint for failure to state a claim and argued, among other

things, that the letter and documents attached to the complaint did not

constitute debt collection activity but instead were only an attempt to

enforce its client's security interest. Id. at 1215. The district court

dismissed the claim, and the Eleventh Circuit reversed. Id. at 1218-19.

The Reese case involved both a promissory note and a security

interest, and the promissory note is a debt within the plain language of

the Federal Act. Id. at 1217. The letter stated "that the 'Lender hereby

demands full and immediate payment of all amounts due.'" Id. The

letter also threatened "that 'unless you pay all amounts due and owing

under the Note,' attorney's fees 'will be added to the total amount for

which collection is sought.'" Id. The other documents also had language

indicating [*8] that the law firm was "'ATTEMPTING TO COLLECT

A DEBT.'" Id.

The Eleventh Circuit rejected the law firm's argument that the

purpose of the letter and documents was only to enforce a security

interest. Id. "That argument wrongly assumes that a communication

cannot have dual purposes." Id. The court recognized that if it had

adopted the law firm's argument "[t]he practical result would be that the

[Federal] Act would apply only to efforts to collect unsecured debts. So

16

long as a debt was secured, a lender (or its law firm) could harass or

mislead a debtor without violating the [Federal Act]." Id. at 1218.

Rather, "[a] communication related to debt collection does not become

unrelated to debt collection simply because it also relates to the

enforcement of a security interest. A debt is still a 'debt' even if it is

secured." Id.; see also Birster v. Am. Home Mortg. Servicing, Inc., 481

App’x 579, 583 (11th Cir. 2012) ("Reese provides that an entity can

both enforce a security interest and collect a debt.").

Here, the language in the letters from the Bank to Gann do not

explicitly state that it is attempting to collect a debt as the documents

did in Reese. However, the first letter states that if the Bank does not

receive a specific amount due by a specified date, "foreclosure

proceedings [*9] may begin or continue." The second letter states that

"it is vital that the full amount currently due is paid" and asks Gann to

send "the total amount due, $414.30, immediately" or contact the

Bank's office. The letters plainly seek collection of an alleged debt.

Therefore, the trial court erred in determining that the letters did

not contain language that could be construed as an attempt to collect on

the underlying debt and only were attempts to enforce the Bank's

security instrument. Accordingly, we reverse the order to the extent it

dismisses the FCCPA claim in count one.

Id. at 908-909.

This Court’s August, 2014 decision in Gann is remarkably similar to the

argument Brindise’s undersigned counsel advanced below at trial two months

earlier. To wit, just as the undersigned acknowledged the Middle District’s 2007

decision Trent but argued it was no longer the law in light of the Eleventh Circuit’s

2012 opinions in Reese and Birster, so, too did this Court. Compare id. at 908-909

with R.246-247, pp. 71-79. Essentially, the undersigned argued Gann to the lower

17

court before Gann even existed. Suffice it to say Brindise not only preserved their

arguments, but they were correct in their interpretation of the law, while the lower

court, respectfully, was not.

Under Gann, mortgage foreclosure plaintiffs such as the Bank are subject to

the FCCPA. Id. As Fla. Stat. 559.715 is part of the FCCPA (just one number off

from the statute analyzed in Gann, Fla. Stat. 559.72), this Court’s precedent requires

it to conclude that Fla. Stat. 559.715 applies in mortgage foreclosure cases like the

case at bar. Gann, as well as a closer analysis of Reese, Birster, and the cases

following them (the very line of cases this Court relied upon in deciding Gann) lead

to no other conclusion.

In Reese, a secured creditor argued the Fair Debt Collections Practices Act

(“FDCPA,” the federal version of the FCCPA) did not apply because it was only

seeking to foreclose a security interest, not collect a debt. 678 F.3d at 1214. The

Eleventh Circuit disagreed, concluding such a distinction would create a “loophole”

in the FDCPA and “can’t be right.” In the Reese court’s words:

The rule the Ellis law firm asks us to adopt would exempt from the

provisions of § 1692e any communication that attempts to enforce a

security interest regardless of whether it also attempts to collect the

underlying debt. That rule would create a loophole in the FDCPA. A

big one. In every case involving a secured debt, the proposed rule would

allow the party demanding payment on the underlying debt to dodge

the dictates of § 1692e by giving notice of foreclosure on the secured

18

interest. The practical result would be that the Act would apply only to

efforts to collect unsecured debts. So long as a debt was secured, a

lender (or its law firm) could harass or mislead a debtor without

violating the FDCPA. That can't be right. It isn't. A communication

related to debt collection does not become unrelated to debt collection

simply because it also relates to the enforcement of a security interest.

A debt is still a “debt” even if it is secured.

Id. The Eleventh Circuit ruled similarly in Birster, applying the principle of law in

Reese specifically to mortgage foreclosure (in particular, the paragraph 22 letter that

precipitates lawsuits with the standard, Fannie Mae mortgage). 481 App’x at 583.

In the case at bar, the Bank sent Brindise a letter demanding payment of

$3,941.68, failing which it would accelerate and foreclose, which letter precipitated

this mortgage foreclosure lawsuit. R.177-178. This is precisely the fact pattern

which the 11th Circuit deemed an action to collect a debt. Id. Under Birster (and

Gann, which follows Birster), there is no way to conclude the Bank was not

collecting a debt where it sent Brindise this paragraph 22 letter demanding payment,

then sued Brindise for foreclosure and a deficiency.

In the months after Reese and Birster, several federal court cases have ruled

mortgage foreclosure is an action to collect a debt under the FDCPA, rejecting

arguments otherwise from financial institutions and their counsel. For instance, in

2014, the Southern District of Florida followed Reese and ruled a mortgage

foreclosure complaint was an action to collect a debt within the ambit of the FDCPA

19

where the foreclosing plaintiff asked the court to reserve jurisdiction to award a

deficiency. Freire v. Aldridge Connors, LLP, 994 F.Supp. 2d. 1284, 1288 (S.D. Fla.

2014). The Bank’s Complaint in the case at bar is the same, as it sought both

mortgage foreclosure and a deficiency. R.55-91.

In 2013, the Southern District of Florida ruled similarly:

Defendants argue that generally a foreclosure action is not debt

collection for purposes of the FDCPA and, therefore, the filing the state

court complaint is not a debt collection activity. [Trent, supra.]

However, money owed on a promissory note secured by a mortgage is

a debt for purposes of the FDCPA. [Reese, supra.]

Battle v. Gladstone Law Group, P.A., 2013 U.S. Dist. LEXIS 91621 (S.D. Fla.

2013). Notably, Battle so ruled immediately after citing the FDCPA’s definition of

“debt.” Significantly, that definition is exactly the same as set forth in the FCCPA,

Fla. Stat. 559.55(1).

Where the FDCPA and the FCCPA define “debt” the exact same way, it only

makes sense for this Court to conclude mortgage foreclosure is an action to collect

a debt under the FDCPA, just as federal courts have done. See Carsillo v. City of

Lake Worth, 995 So. 2d 1118, 1119 (Fla. 4th DCA 2008) (“It is well established that

if a Florida statute is patterned after a federal law, the Florida statute will be given

the same construction as the federal courts give the federal act.”). In other words,

where the Eleventh Circuit has concluded “a debt is still a debt even if it is secured,”

20

Reese, supra, so, too, should this Court. The Gann decision (employing this very

analysis) only cements such a conclusion.10

Rulings from Florida’s circuit court judges are obviously not binding on this

Court and are arguably unnecessary in light of Gann. However, these rulings should

persuade this Court, particularly given the sheer volume of them. To wit, when

presented with the authorities cited above, 41 different circuit court judges in Florida

have ruled in the undersigned’s favor on this issue (some of them many times).11

See Notice of Authority, 1. Not one. Not five. Forty-one different circuit court

judges.12 Essentially, all these judges did was agree with the same analysis the

10 The plethora of other, federal cases in Florida deeming mortgage foreclosure

an action to collect a debt under the FDCPA further support such a ruling. See Lara

v. Specialized Loan Servicing, LLC, 2013 U.S. Dist. LEXIS 127192 (S.D. Fla. 2013)

(“A home loan is a “debt” even if it is secured.”); Lewis v. Marinosci Law Group,

P.C., 2013 U.S. Dist. LEXIS 156732 (S.D. Fla. 2013) (following Reese, concluding

consumer stated a cause of action under the FDCPA for making false allegations in

a mortgage foreclosure case); Hall v. MLG, P.A., 2013 U.S. Dist. LEXIS 157414

(S.D. Fla. 2013) (same).

11 Some of these Orders (the ones which specify the dismissal was based on

failure to comply with the notice requirements of Fla. Stat. 559.715) are attached.

There are many others which ruled on this basis but are not included because the

face of the Order did not specify that statute as the basis of the ruling.

12 Most of these judges preside in circuits for which this Court acts as the

appellate court, including Hon. Mark Shames, Hon. Pamela Cambpell, Hon. John

Schaefer, Hon. Bruce Boyer, Hon. David Demers, Hon. Jack Day, Hon. Walt Logan,

Hon. Thomas Minkoff, Hon. Marion Fleming, Hon. Amy Williams, Hon. Sandra

Taylor, Hon. Perry Little, Hon. Donald Evans, Hon. Christine Vogel, Hon. Raul

21

undersigned made at trial in this case – the same analysis this Court employed in

Gann.

Once this Court concludes mortgage foreclosure is an action to collect a debt,

it is easy to see why this Court should reverse the Final Judgment of Foreclosure.

The Bank was not the original creditor, and this lawsuit, seeking to foreclose

Brindise’s home, was an action to collect a debt. Hence, the Bank was obligated to

give Brindise written notice of the assignment of the debt at least 30 days before

filing this lawsuit, see Fla. Stat. 559.715, yet the Bank failed to satisfy its burden of

proof in this regard at trial. As such, the Final Judgment at bar cannot stand.

Based on the undersigned’s extensive experience arguing this issue (literally,

hundreds of hearings before dozens of circuit judges over two-plus years, along with

two, recent oral arguments before this Court, see Case No. 2D13-3072 and Case No.

2D13-3078), the Bank may present other arguments as to why Fla. Stat. 559.715

does not justify reversal. Alternatively, this Court may have questions as to the

application of the statute in this context (which the Bank may not raise). Brindise

Palomino, Hon. Judy Biebel, Hon. J. Rodgers Padgett, Hon. Frank Gomez, Hon. Ray

Ulmer, and Hon. William McIver. Notably, this list includes every foreclosure

judge in both Hillsborough and Pinellas Counties except one, as all such judges have

agreed with the undersigned on this issue at least once. See Notice of Authority, 1.

22

address such issues in turn.

The Bank may contend it was not a “debt collector,” citing the definition set

forth in Fla. Stat. 559.55(6)(f). This would be a straw man argument. The term

“debt collector” is not set forth in Fla. Stat. 559.715, so it is not relevant in this

Court’s adjudication of this appeal. The question at bar, per the plain language of

Fla. Stat. 559.715, is whether mortgage foreclosure is an “action to collect a debt,”

not whether the person seeking such collection is a “debt collector.” Undoubtedly,

this is why this Court ruled, earlier this year, “the FCCPA applies not only to debt

collectors but also to any ‘person.’” Gann, 145 So. 3d at 910.

The Bank may contend Fla. Stat. 559.715 does not operate as a defense to the

filing of a lawsuit, as if to say it could ignore the plain language of the statute yet

still prevail. In other words, the Bank might contend Fla. Stat. 559.715 does not

operate as a “condition precedent” to foreclosure. Such a position would be

unavailing, for several reasons.

First, the only Florida DCA decision which has ever cited Fla. Stat. 559.715

plainly shows that a consumer must prevail where the requisite notice was not given.

Burt, 138 So. 3d at 1193. In Burt, the creditor plaintiff moved for summary

judgment, asserting it sent the notice required by Fla. Stat. 559.715, but the consumer

defendant denied such in an opposing affidavit. 138 So. 3d at 1194. The lower court

23

granted summary judgment, but the Fifth District reversed, deeming it a material

issue of fact whether the notice required by 559.715 had been given before filing

suit.13 Id.

If Fla. Stat. 559.715 did not require the creditor in Burt to give the notice

before filing suit, then the Fifth District would not have reversed on that basis. After

all, the issue of fact regarding the giving of notice would not have been material, and

certainly not a basis for reversal, because the notice, even if not given, could not

have changed the result of the case. Yes, the parties may have disputed whether the

559.715 notice was given (hence the conflicting affidavits), but if the notice was not

required, then Burt would not have reversed on that basis because the creditor would

have prevailed irrespective of whether it gave the notice. Clearly, the Fifth District

reversed because the giving of the notice before filing suit was required, and the

absence of such notice requires judgment for the consumer.14 Id. Here, the Bank

13 The Fifth District also reversed on a material issue of fact regarding identity,

i.e. whether the debt was actually the defendant’s debt or another person’s debt. Id.

It is clear, however, that the Fifth District also reversed given the question of fact

regarding compliance with the notice requirement of Fla. Stat. 559.715. Id. 14 Admittedly, Burt was not a mortgage foreclosure case. However,

Montgomery has already shown Fla. Stat. 559.715 applies in the mortgage

foreclosure context. See Argument, supra. Hence, Burt shows, contrary to what the

Bank may argue, the 559.715 notice must be given, failing which the consumer must

prevail. Were it otherwise, Burt would not have found the disputed issue of fact

24

failed to meet its burden of proving the requisite notice was given to Brindise, so the

Final Judgment at bar was erroneously entered.

Second, where a statute requires some type of notice be given before suit is

filed, Florida courts have regularly treated that notice obligation as a mandatory

“condition precedent” even where the legislature did not expressly call it such in the

statute. See Hallstrom v. Tillamook County, 493 U.S. 20 (1989) (treating 42 USCA

6972(b) as a condition precedent where the statute did not specifically indicate such);

Commercial Carrier Corp. v. Indian River County, 371 So. 2d 1010 (Fla. 1979)

(regarding Fla. Stat. 768.28(6)); Neate v. Cypress Club Condo., 718 So. 2d 390 (Fla.

4th DCA 1998) (en banc) (regarding Fla. Stat. 718.1255(4)(a)); Freni v. Collier

County, 588 So. 2d 291 (Fla. 2d DCA 1991) (regarding Fla. Stat. 125.01014(4)(a)).

Hence, there is simply no basis to ignore Burt and conclude 559.715 is not a

condition precedent merely because the magic words “condition precedent” are not

contained in the statute. Where the notice had to be given 30 days before “any

action” to collect the debt, and mortgage foreclosure is an action to collect debt, see

Gann (particularly when precipitated by a paragraph 22 letter, see Birster, and

coupled with a claim for deficiency, see Freire), the notice had to be given 30 days

regarding the giving of the notice to be material and would not have reversed on that

basis. Id.

25

before filing suit. It is really that simple.

Third, a creditor’s failure to comply with the notice requirement in Fla. Stat.

559.715 does not justify a consumer’s filing of a civil lawsuit, so treating the notice

in a defensive manner, i.e. as a condition precedent, is the only way to enforce the

plain language of the statute.

In the undersigned’s experience, foreclosing plaintiffs such as the Bank like

to argue that Florida courts should not treat the notice requirement of Fla. Stat.

559.715 as a defense because a consumer’s remedy under the FCCPA is to sue for

violation thereof. Admittedly, many of the cases in the FDCPA and FCCPA context

do emanate from lawsuits initiated by consumers. See e.g. Gann, 145 So. 3d at 906

(reversing order granting creditor’s motion to dismiss a suit filed by a consumer for

the creditor’s violation of Fla. Stat. 59.72).

Cases where consumers brought suit, however, are predicated on violations of

Fla. Stat. 559.72, and the civil remedies statute of the FCCPA, Fla. Stat. 559.77,

specifically authorizes suit for a violation of that statute. To quote Fla. Stat. 559.77:

A debtor may bring a civil action against a person violating the

provisions of s. 559.72 in the county in which the alleged violator

resides or has his or her principal place of business or in the county

where the alleged violation occurred.

Fla. Stat. 559.77.

26

Conversely, the case at bar deals with a violation of Fla. Stat. 559.715, and

nothing in Fla. Stat. 559.77 or anything else within the FCCPA authorizes a

consumer to file suit for a violation of Fla. Stat. 559.715. This distinction is

dispositive.

If the legislature intended to allow consumers to file suit for violations of the

notice requirements of Fla. Stat. 559.715, it could have done so – just as it authorized

suits in Fla. Stat. 559.77 for violations of Fla. Stat. 559.72. The legislature’s

inclusion of express language in Fla. Stat. 559.77 authorizing suit for a violation of

Fla. Stat. 559.72 but not for a violation of Fla. Stat. 559.715 shows that lawsuits for

the former are permitted, but the latter are not. See Temple v. Aujla, 681 So. 2d

1198 (Fla. 5th DCA 1996) (“as the Second District correctly noted, where the

legislature has spoken by delineating a specific remedy, it is not the judicial branch's

role to overstep the legislature's authority and create an additional remedy”).

Once one concludes consumers cannot bring an offensive action, i.e. cannot

sue, for a creditor’s violation of Fla. Stat. 559.715, the obvious question becomes

“what is the remedy?” The only answer, of course, is to treat the notice obligation

in Fla. Stat. 559.715 as a defense, i.e. a mandatory condition precedent. Any

contrary ruling would mean consumers could not sue yet could not assert the notice

violation as a defense, either – leaving them without a remedy.

27

The legislature does not write meaningless statutory provisions, and courts

must avoid interpreting statutes in such a way that portions of the statute would be

rendered meaningless. See State v. Goode, 830 So. 2d 817, 824 (Fla. 2002) (“A

basic rule of statutory construction provides that the Legislature does not intend to

enact useless provisions, and courts should avoid readings that would render part of

a statute meaningless.”); Fla. Dept. of Revenue v. Fla. Municipal Power Agency,

789 So. 2d 320, 324 (Fla. 2001) (“A court's function is to interpret statutes as they

are written and give effect to each word in the statute.”). Here, this Court must

construe the notice requirement of Fla. Stat. 559.715 as a defense, as any contrary

ruling would leave consumers such as Brindise without a remedy for a violation

thereof. See Smith v. Piezo Tech. and Prof. Administrators, 427 So. 2d 182, 184

(Fla. 1983) (“It must be assumed that a provision enacted by the legislature is

intended to have some useful purpose”). As this Court ruled in the context of an

FCCPA claim:

[C]ourts will not interpret a statute in such a way as to render portions

of it meaningless. If section 559.72(7) and/or section 559.72(9) were

interpreted to require a consumer debt collector to affirmatively

disclose identifying information to a Florida consumer without a

request from the consumer, this would render section 559.72(15),

which requires the disclosure of this information only upon request,

meaningless. We will not support such an interpretation. When, as here,

the FCCPA contains a specific provision addressing the conduct at

issue, a trial court may not ignore the FCCPA's plain language.

28

Read v. MFP, Inc., 85 So. 3d 1151, 1154 (Fla. 2d DCA 2012).

As this Court adjudicates the issue at bar, it should bear in mind the context

in which it is ruling. The FCCPA, Fla. Stat. 559.715 is a “consumer protection

statute,” LeBlanc v. Unifund CCR Partners, 601 F.3d 1185 (11th Cir. 2000), and,

under a long line of cases, must be “liberally construed” in favor of Brindise. See

e.g. Legg v. Voice Media Group, Inc., 990 F.Supp. 2d 1351 (S.D. Fla. 2014) (“a

consumer protection statute … should be construed liberally in favor of

consumers”). The liberal construction of FCCPA statutes is why Florida courts do

things like employ a “least sophisticated consumer” standard. LeBlanc, 601 F.3d at

1194. In the words of the Eleventh Circuit, the very “goal” of the FCCPA is “to

provide the consumer with the most protection possible.” Id. at 1192 (citing Fla.

Stat. 559.552 (“In the event of any inconsistency ... the provision which is more

protective of the consumer or debtor shall prevail.”)). Particularly with this liberal

construction, there is no way to conclude Fla. Stat. 559.715 does not apply to the

facts at bar.

Once this Court concludes Fla. Stat. 559.715 applies, it is easy to see why

reversal and remand with instructions to dismiss without prejudice is the only

appropriate result. After all, the Bank introduced no evidence to satisfy its burden

29

of proving it gave Brindise the 559.715 notice,15 and the only witness at trial

admitted there was no notice. This Court should rule accordingly and remand with

instructions to dismiss.16

15 Another issue that often arises in the 559.715 context is whether the notice

must be “given” or need only be “sent.” That distinction is irrelevant here because

the Bank did not prove it “gave” a notice or that it “sent” a notice. However, to the

extent this Court writes an opinion on Fla. Stat. 559.715, it should clarify that the

obligation is to “give” notice.

The legislature could have written Fla. Stat. 559.715 to require the creditor

“send” a notice. It did not. Instead, the plain language of the statute requires

creditors like the Bank “give” notice. Where the plain language of the statute

requires the notice be “given,” this Court should not impart a lesser/different

obligation.

The Bank may point to paragraph 15 of the Mortgage in support of an

argument that the 559.715 notice need only be “sent.” Any such contention must

fail. After all, paragraph 15 of the Mortgage only applies to notices required under

the terms of the Mortgage (not any notice; only notices required by the Mortgage).

R.212-213.

By way of example, the notice required by paragraph 22 of the standard,

Fannie Mae mortgage need only be “sent” because that notice is required by the

terms of the mortgage, so paragraph 15 applies to that type of notice. Conversely,

the notice required by Fla. Stat. 559.715 is a statutory obligation, not an obligation

in the Mortgage, so it is not modified by paragraph 15. As a result, the Bank was

plainly required to “give” notice, as the plain language of Fla. Stat. 559.715 requires

(not send, “give”). 16 Where a plaintiff fails to introduce evidence at trial proving it complied with

a condition precedent, dismissal is the proper remedy on remand. See Boultbee, 595

So. 2d at 986 (reversing final judgment and remanding with instructions to dismiss

because plaintiff introduced no evidence at trial to prove compliance with condition

precedent). Moreover, established precedent in the foreclosure context prevents the

Bank from getting a new trial, i.e. a second bite at the apple, given its failure of proof

at trial. See Lacombe v. Deutsche Bank Nat’l Trust Co., 149 So. 3d 152 (Fla. 1st

DCA 2014) (reversing final judgment of foreclosure and remanding with

30

Even in 2015, Florida courts remain flooded with foreclosures. Hence, the

undersigned could understand if this Court were hesitant, for pragmatic reasons, to

write a written opinion that could be viewed as creating another hurdle for lenders

to jump through before foreclosing. Such pragmatic concerns, however, cannot

carry the day. After all, judges must enforce statutes as they are drafted, irrespective

of how they may feel about the results. This Court should not “legislate from the

bench.”

That said, to the extent this Court harbors such pragmatic concerns, the

undersigned respectfully submits it should rest easy. The undersigned has been

arguing the 559.715 issue so extensively, for so long, and with so much success that

foreclosing lenders typically introduce the 559.715 notice at trial as a matter of

routine. Frankly, it’s often a matter of simply printing one letter from the bank’s

business records. Moreover, unlike the paragraph 22 issue, there are no arguments

instructions to dismiss where the lender failed to prove standing at trial); Wolkoff v.

American Home Mortg. Servicing, Inc., Case No. 2D12-6460 (Fla. 2d DCA 2014)

(“we see no reason to afford AHMSI a second opportunity to prove its case.”);

Correa v. U.S. Bank, N.A., 118 So. 3d 952 (Fla. 2d DCA 2014). That is particularly

so here, where: (i) Brindise had been litigating the 559.715 issue throughout the case,

including via a lengthy summary judgment motion with case citations, so her raising

of the issue at trial was hardly a surprise; and (ii) the Bank did not ask the lower

court to re-open the case after Brindise moved for an involuntary dismissal based on

its failure of proof.

31

regarding the content of the 559.715 notice and whether it contains the requisite

information – the notice was either given or it was not. In any event, again,

pragmatic concerns cannot carry the day here, particularly in the face of this Court’s

own precedent, see Gann, and a consumer protection statute with such clear

language.

CONCLUSION

In light hereof, and for all of the foregoing reasons, this Court should reverse

the Final Judgment of Foreclosure and remand with instructions to dismiss the case

without prejudice. In so ruling, this Court should issue a written decision clarifying

that the notice requirements of Fla. Stat. 559.715 apply in the mortgage foreclosure

context and preclude foreclosure where not satisfied.

32

CERTIFICATE OF SERVICE

I HEREBY CERTIFY that a true and correct copy of the foregoing has been

furnished via electronic mail to Morgan L. Weinstein, Esq., Van Ness Law Firm,

PLC, [email protected], on this 16th day of January, 2015.

___/s/ Mark P. Stopa

Mark P. Stopa, Esquire

FBN: 550507

STOPA LAW FIRM

2202 N. Westshore Blvd., Suite 200

Tampa, FL 33607

Telephone: (727) 851-9551

ATTORNEY FOR APPELLANTS

CERTIFICATE OF SERVICE

I HEREBY CERTIFY that the font used in this brief is Times New Roman

14-point, in compliance with Fla.R.App.Pro. 9.210(a)(2).

___/s/ Mark P. Stopa

Mark P. Stopa, Esquire

FBN: 550507