In the Eye of the Chaos of Growth Entrepreneurship

52

IN THE EYE OF THE CHAOS OF GROWTH ENTREPRENEURSHIP MATTI HEIKKONEN, +47 47 922 170, [email protected], @MHEIKKONEN Ficta Technology CEO Seminar, 28.11.2014, Kittilä, Finland

-

Upload

matti-heikkonen -

Category

Leadership & Management

-

view

165 -

download

3

Transcript of In the Eye of the Chaos of Growth Entrepreneurship

IN THE EYE OF THE CHAOS OF GROWTH ENTREPRENEURSHIPMATTI HEIKKONEN, +47 47 922 170, [email protected], @MHEIKKONEN

Ficta Technology CEO Seminar, 28.11.2014, Kittilä, Finland

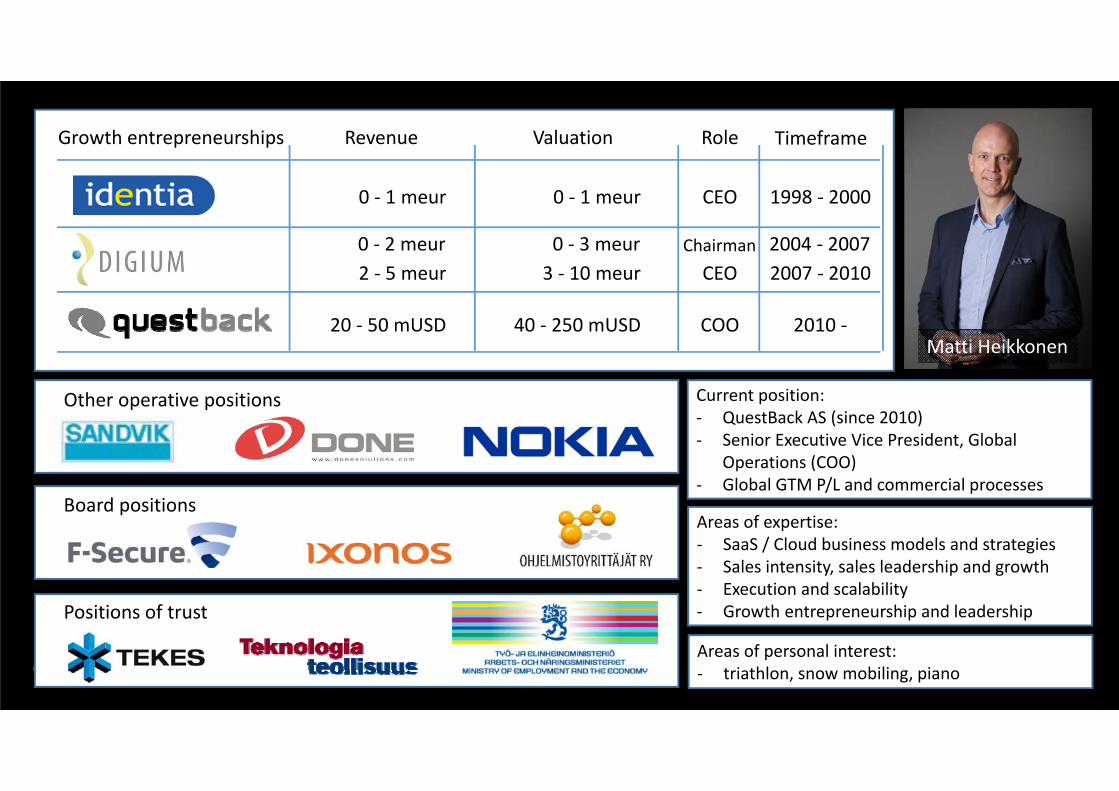

Board positions

Other operative positions

Positions of trust

Matti Heikkonen

Areas of expertise: ‐ SaaS / Cloud business models and strategies‐ Sales intensity, sales leadership and growth‐ Execution and scalability‐ Growth entrepreneurship and leadership

Areas of personal interest:‐ triathlon, snow mobiling, piano

Current position:‐ QuestBack AS (since 2010)‐ Senior Executive Vice President, Global

Operations (COO)‐ Global GTM P/L and commercial processes

0 ‐ 1 meur

2 ‐ 5 meur

20 ‐ 50 mUSD

Revenue Valuation

0 ‐ 1 meur

3 ‐ 10 meur

40 ‐ 250 mUSD

Growth entrepreneurships Role

CEO

CEO

COO

Timeframe

1998 ‐ 2000

2007 ‐ 2010

2010 ‐

0 ‐ 2 meur 0 ‐ 3 meur Chairman 2004 ‐ 2007

FICTA?WHAT’S THAT?

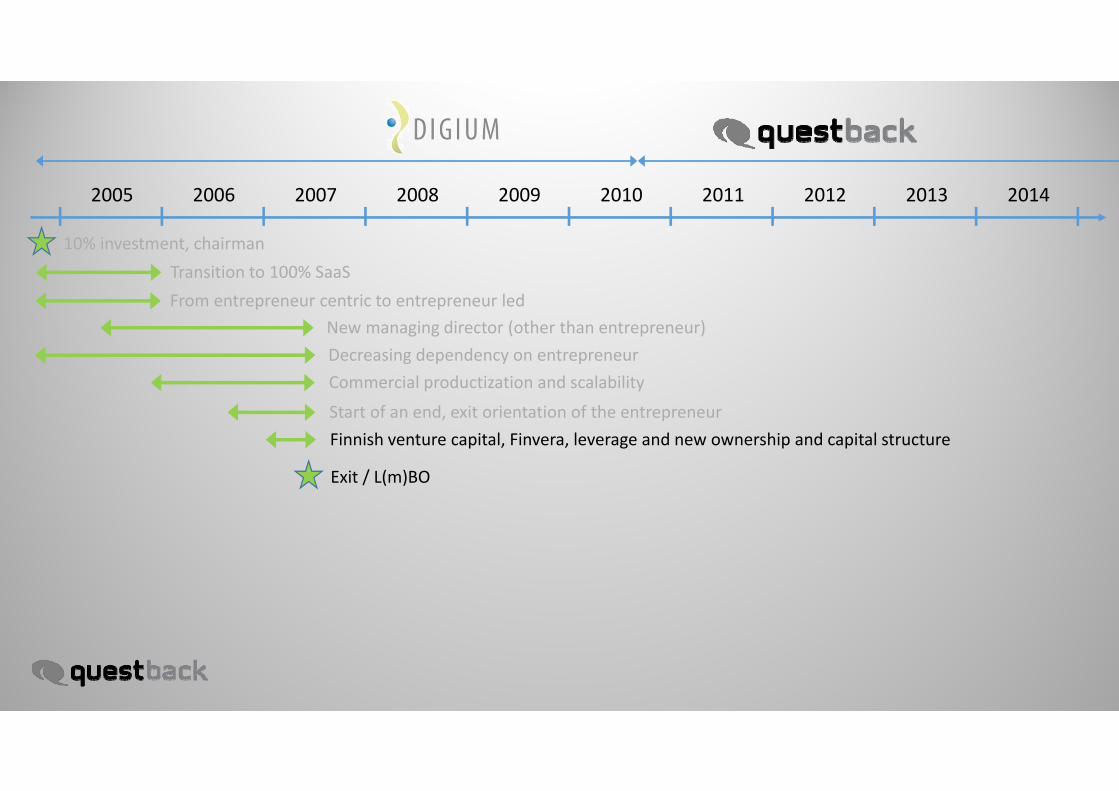

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

10% investment, chairmanTransition to 100% SaaSFrom entrepreneur centric to entrepreneur led

Decreasing dependency on the entrepreneurCommercial productization and scalability

Start of an end, exit orientation of the entrepreneur

New managing director (other than entrepreneur)

START OF AN END OF EN ERA FOR ENTREPRENEUR– EXIT FEVER

CHAIRMAN’S GUIDELINE IN MANOUVERINGTHROUGH ENTREPRENEUR’S EXIT FEVER

‐ DECIDE OBJECTIVELY WHAT IS BEST FOR THE BUSINESS ‐ ACCOMODATE ENTREPRENEUR’S INTERESTS UP TO WHAT IS A

”FAIR BALANCE” / DOABLE‐ DESCRIBE ALL RELEVANT SCENARIOS INCLUDING THE WORST

CASE(S)‐ FORCE MOVEMENT TO MAKE IT OR BREAK IT

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

10% investment, chairmanTransition to 100% SaaSFrom entrepreneur centric to entrepreneur led

New managing director (other than entrepreneur)Decreasing dependency on entrepreneurCommercial productization and scalability

Start of an end, exit orientation of the entrepreneurFinnish venture capital, Finvera, leverage and new ownership and capital structure

Exit / L(m)BO

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Digium takeover

Clean‐up and professionalization

Cash flow issue

New managing director (who is the entrepreneur again)

3xP (people, planning, process)

Consolidate or become consolidated / Nordics & Finland

CONFIDENTIAL PRODUCTIVE ENTERPRISE FEEDBACK MANAGEMENT

Market Positioning of Digium / Nordics 2009

DISTRIBUTEDCENTRALIZED

TACT

ICAL

STRA

TEG

IC

POSI

TIO

NIN

G O

F U

SAG

E W

ITH

IN T

HE

CUST

OM

ER

DEPLOYMENT MODEL WITHIN THE CUSTOMER

Competition to acquire Digium

CONFIDENTIAL PRODUCTIVE ENTERPRISE FEEDBACK MANAGEMENT

DISTRIBUTEDCENTRALIZED

TACT

ICAL

STRA

TEG

IC

POSI

TIO

NIN

G O

F U

SAG

E W

ITH

IN T

HE

CUST

OM

ER

DEPLOYMENT MODEL WITHIN THE CUSTOMER

Market Positioning of Digium / Nordics 2009Competition possible for Digium to acquire

CONFIDENTIAL PRODUCTIVE ENTERPRISE FEEDBACK MANAGEMENT

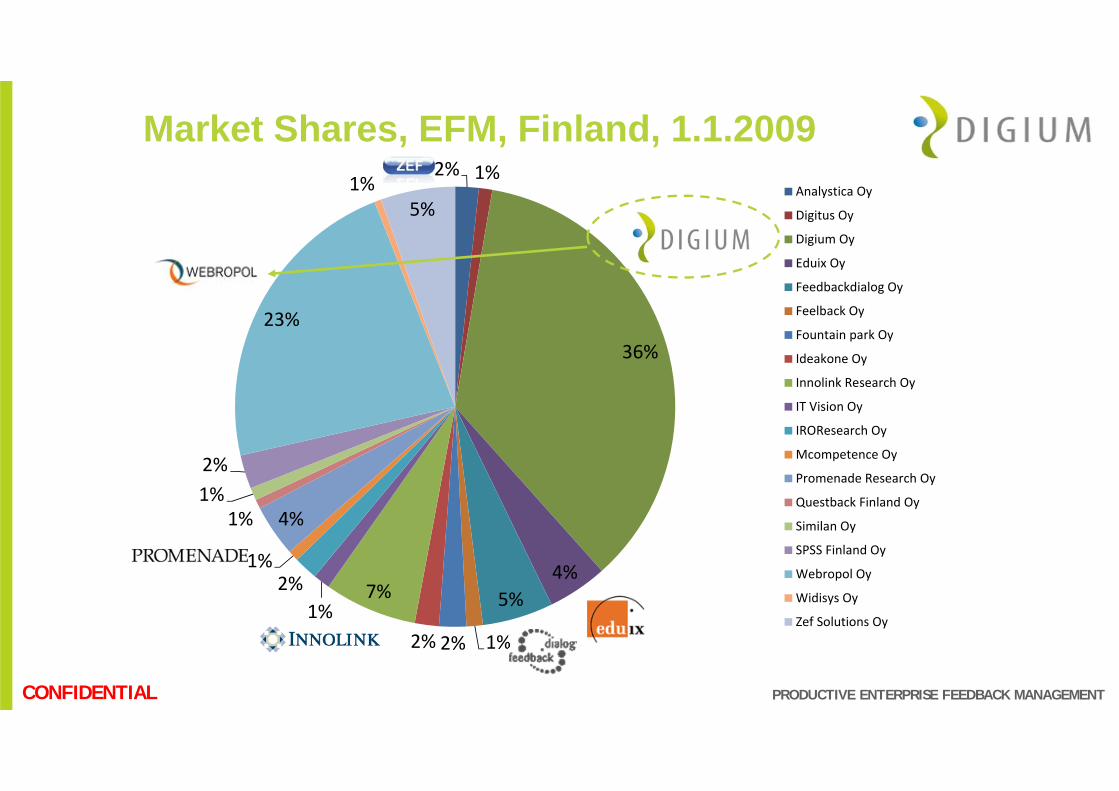

2% 1%

36%

4%5%

1%2%2%

7%1%

2%1%

4%1%1%2%

23%

1%5%

Analystica Oy

Digitus Oy

Digium Oy

Eduix Oy

Feedbackdialog Oy

Feelback Oy

Fountain park Oy

Ideakone Oy

Innolink Research Oy

IT Vision Oy

IROResearch Oy

Mcompetence Oy

Promenade Research Oy

Questback Finland Oy

Similan Oy

SPSS Finland Oy

Webropol Oy

Widisys Oy

Zef Solutions Oy

Market Shares, EFM, Finland, 1.1.2009

HOW TO BUY MINORITY OWNERSHIP WITH CONFIDENCEAS THE SOLE VEHICLE ‐ EXAMPLE WEBROPOL

‐ DO YOUR RESEARCH AND USE ALL SOURCES‐ USE OWNER’S REAL‐LIFE SITUATION AS A KEY ELEMENT

IN YOUR TACTICS‐ MONEY ON THE TABLE IS MUCH MORE THAN MONEY

ON THE PAPER‐ PROMISE NOTHING BUT SECURE, CLEAN CUT EXIT

CONFIDENTIAL PRODUCTIVE ENTERPRISE FEEDBACK MANAGEMENT

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

New sales, non-recurring

New sales, recurring

Recurring revenue

EBIT

Revenue by type€

R&D spendbreakdown %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Product gen 3

Product gen 2

Product gen 1

Low end product

ASP platform

Key points in Digium’s evolution up to 2009

1

1 END OF ASP

2

2 SIGNIFICANT INVESTMENTIN PURE-PLAY SAAS PLATFORMDEVELOPMENT

3

3 CUSTOMER-CENTRICOPERATING MODEL

INCREASED R&D PRODUCTIVITYAND SALES EFFICIENCY

KEY TECHNOLOGY AND BUSINESS MODEL CAPABILITIES

MARGINAL CHURN RATE ANDLOW PRICE EROSION

4

4 SCALABILITY DEVELOPMENTACROSS BUSINESS MODEL

CRITICAL MASS OF RECURRING REVENUE BASE

PROFITABILITY ANDCASH FLOW TO INVEST INGROWTH

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Digium takeover

Clean‐up and professionalization

New managing director (who is the entrepreneur again)

3xP (people, planning, process)

Consolidate or become consolidated / Nordics & Finland

1st QuestBack exit discussion

Webropol 45% deal

Various merger discussions

QuestBack merger

Cash flow issue

The QuestBack Era

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

New CEO

Re‐invention of enterprise market strategy

Integration of Digium, EasyResearch and GlobalPark to QuestBack

Decreasing dependency on current CEO

Top mgmt clean‐up, setting up the foundation

GRO program

Acquisition of GlobalPark

Sales intensity to a new level

HOW HAS THIS WORKED FOR US?

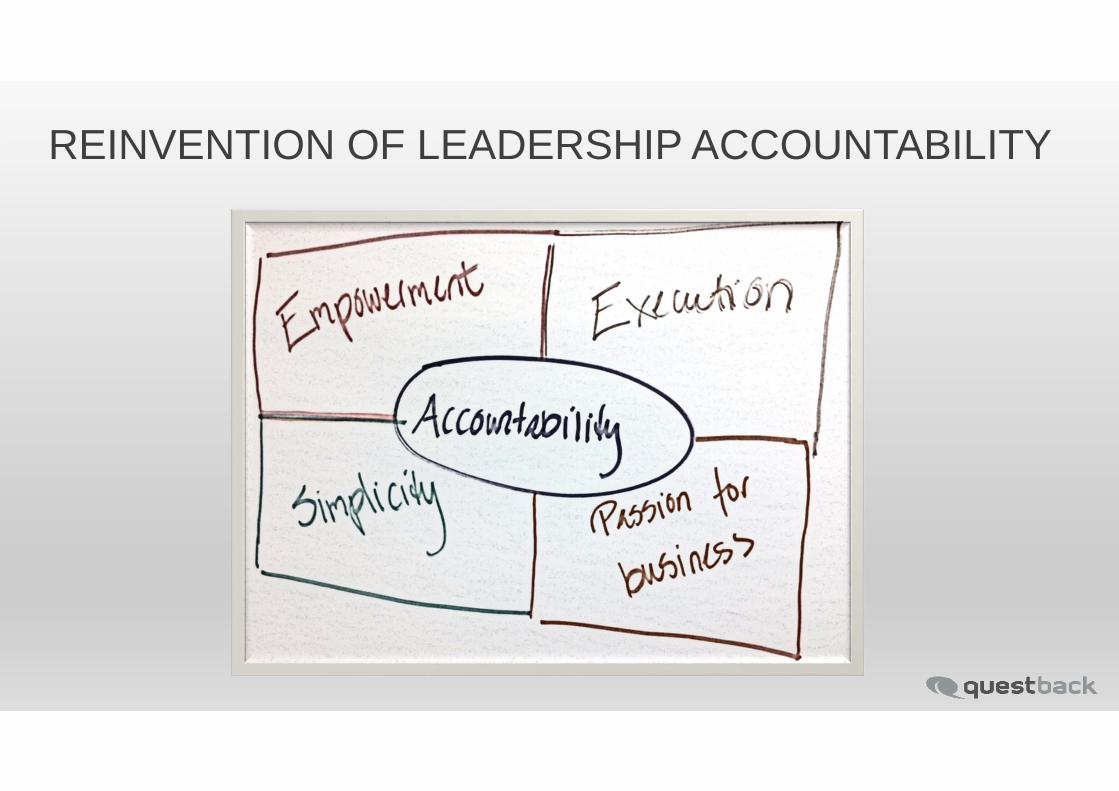

REINVENTION OF LEADERSHIP ACCOUNTABILITY

Vers

ion

Q3

2014

, v2.

3

19

GRO – Strategic Program for Delivering the Strategy

Vers

ion

Q3

2014

, v2.

3

20

We Have 10 Focus Areas We Need to Work With

Channel Sales

Sales Productivity

Renewals

Enterprise sales

Up-sell

GROWTH

Planning

Processes

People

ONE COMPANY

R&D PlatformsInnovation

Vers

ion

Q3

2014

, v2.

3

21

Vers

ion

Q3

2014

, v2.

3

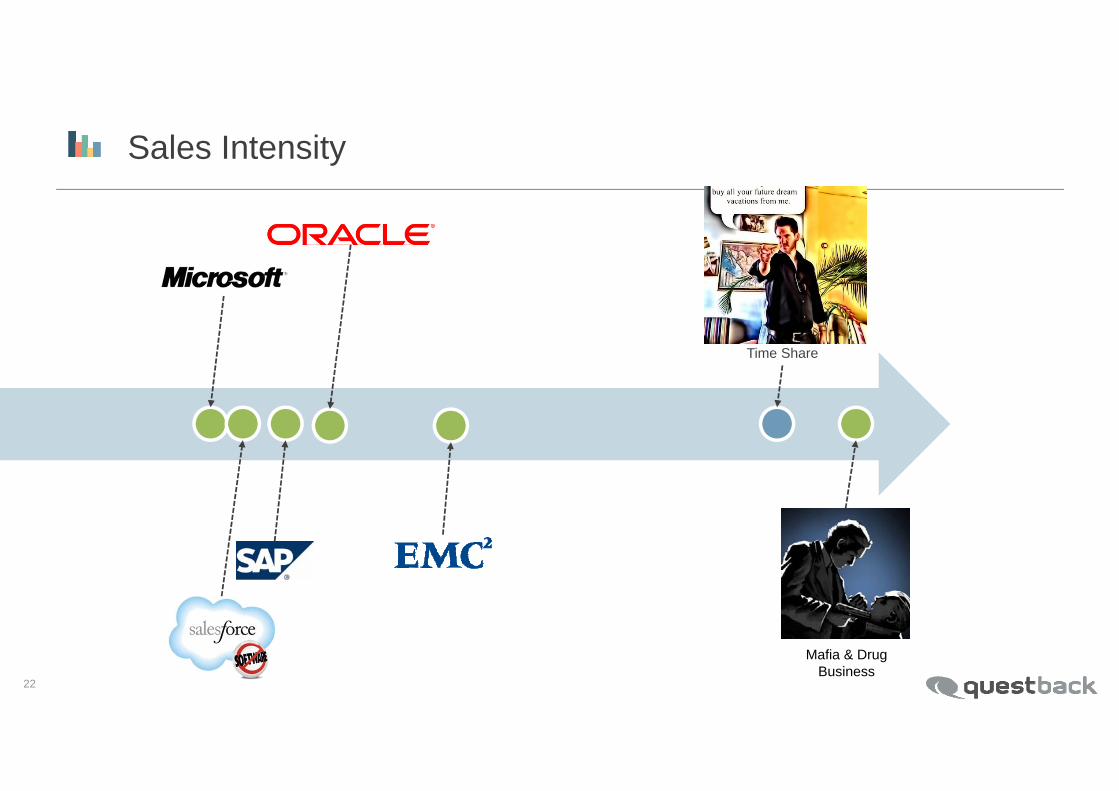

Mafia & DrugBusiness

Time Share

Sales Intensity

22

Vers

ion

Q3

2014

, v2.

3

Mafia & DrugBusiness

Time Share

Sales Intensity

23

Vers

ion

Q3

2014

, v2.

3Sales Intensity

24

Vers

ion

Q3

2014

, v2.

3Sales Intensity

25

Vers

ion

Q3

2014

, v2.

3

This way to QuestBack

Sales Intensity

26

Vers

ion

Q3

2014

, v2.

3Sales Intensity

27

Vers

ion

Q3

2014

, v2.

3

Hold on, we will get there

Sales Intensity

28

Vers

ion

Q3

2014

, v2.

3

AND LUCKILY; OUR COMPETITIONIS NOT THAT MUCH BETTER...

...BUT IS GETTINGMORE AGGRESSIVE

Sales Intensity

29

Vers

ion

Q3

2014

, v2.

3

Salvation Army

Red Cross

Sales Intensity

AND LUCKILY; OUR COMPETITIONIS NOT THAT MUCH BETTER...

...BUT IS GETTINGMORE AGGRESSIVE

30

Vers

ion

Q3

2014

, v2.

3

= POTENTIAL TO MAKE A SIGNIFICANT IMPACT

= POTENTIAL TO MAKE A SIGNIFICANT IMPACT

Sales Intensity

31

SALES IS THE MOST EXACT FORM OF ART THAT EXISTS ON THE FACE OF EARTH

Vers

ion

Q3

2014

, v2.

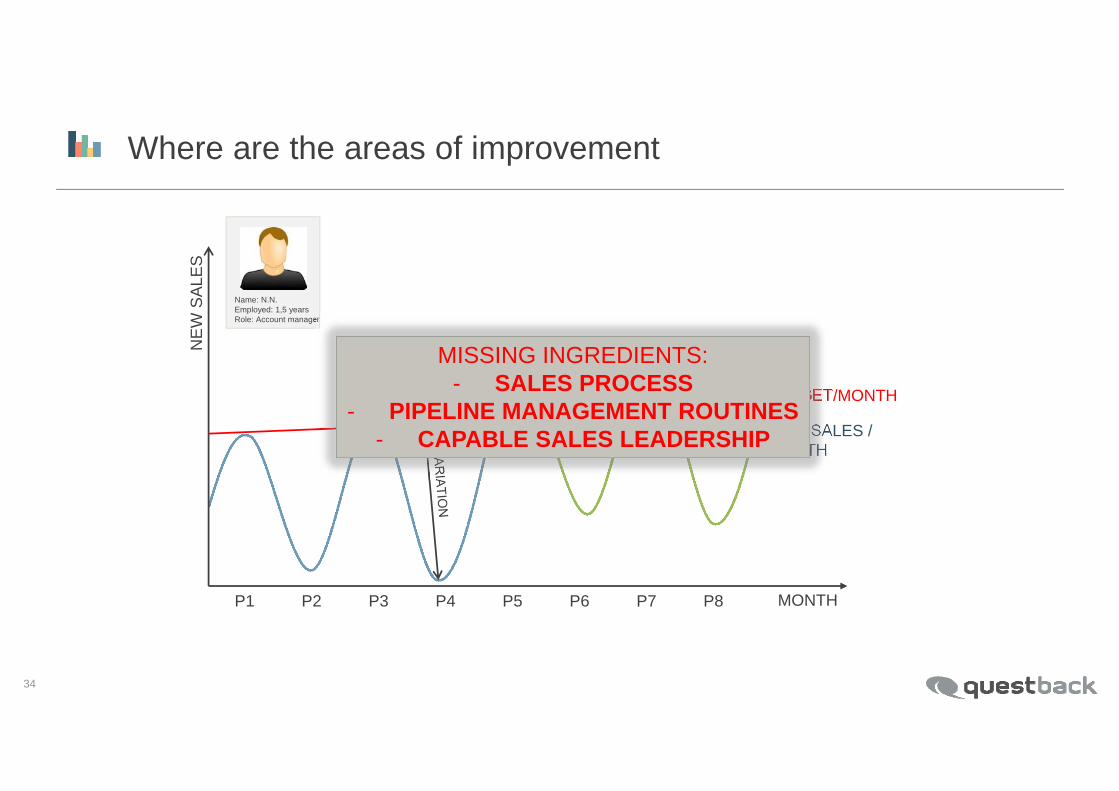

3Where are the areas of improvement

P1 P2 P3 P4 P5 P6 P7 P8

NE

W S

ALE

S

MONTH

TARGET/MONTH

NEW SALES /MONTH

Name: N.N.Employed: 1,5 yearsRole: Account manager

33

Vers

ion

Q3

2014

, v2.

3Where are the areas of improvement

P1 P2 P3 P4 P5 P6 P7 P8

NE

W S

ALE

S

MONTH

TARGET/MONTH

NEW SALES /MONTH

Name: N.N.Employed: 1,5 yearsRole: Account manager

MISSING INGREDIENTS:- SALES PROCESS

- PIPELINE MANAGEMENT ROUTINES- CAPABLE SALES LEADERSHIP

34

Vers

ion

Q3

2014

, v2.

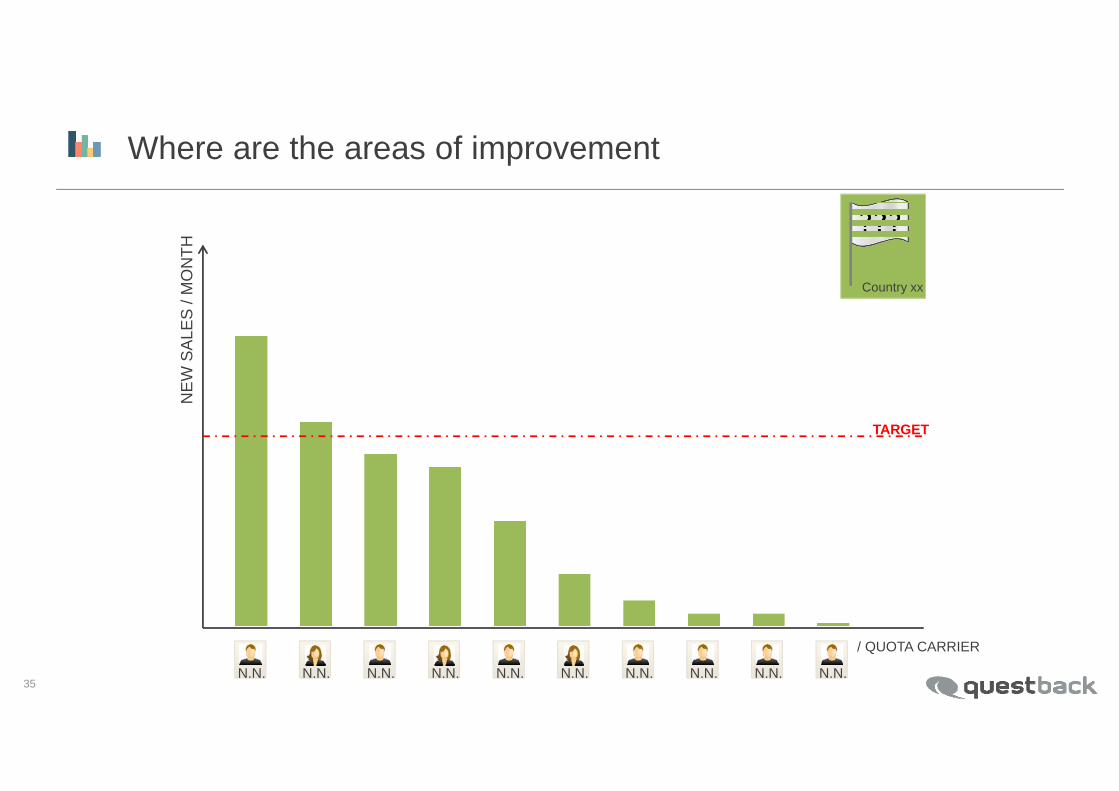

3Where are the areas of improvement

TARGET

NE

W S

ALE

S /

MO

NTH

N.N. N.N. N.N. N.N. N.N. N.N.N.N. N.N.N.N. N.N.

/ QUOTA CARRIER

Country xx

35

Vers

ion

Q3

2014

, v2.

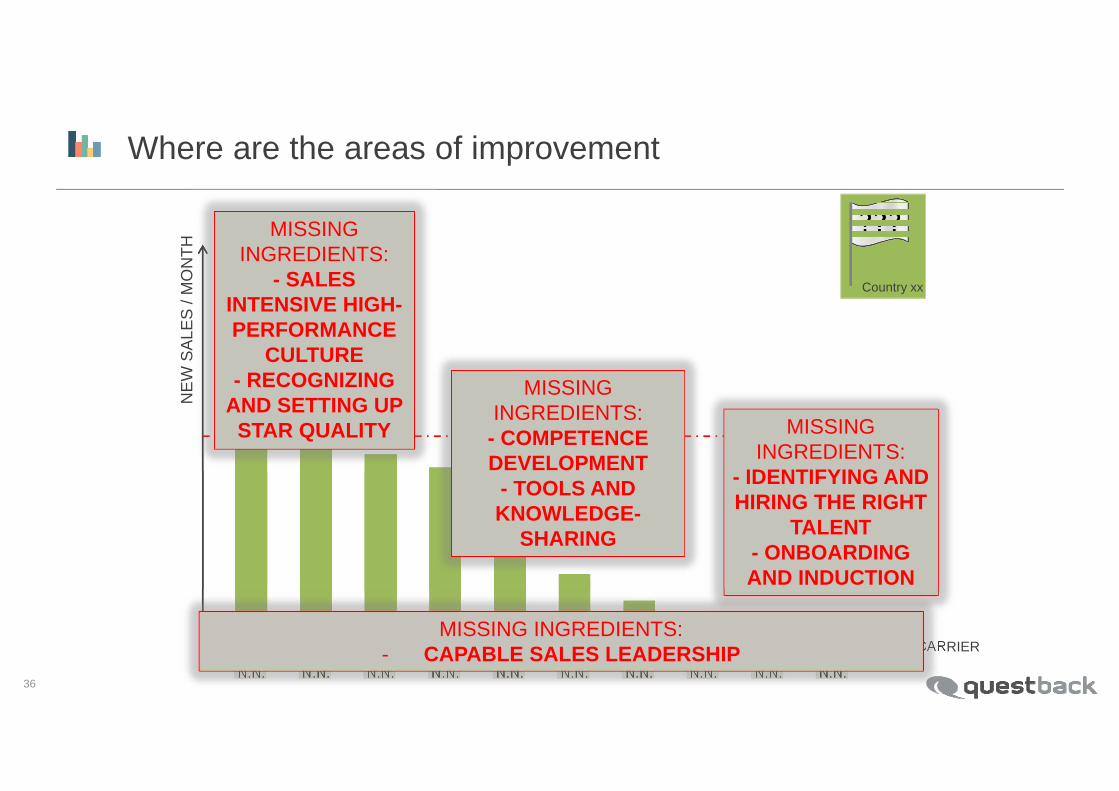

3Where are the areas of improvement

TARGET

MISSING INGREDIENTS:

- SALES INTENSIVE HIGH-PERFORMANCE

CULTURE- RECOGNIZING

AND SETTING UP STAR QUALITY MISSING

INGREDIENTS:- IDENTIFYING AND HIRING THE RIGHT

TALENT- ONBOARDING AND INDUCTION

MISSING INGREDIENTS:- COMPETENCE DEVELOPMENT

- TOOLS AND KNOWLEDGE-

SHARING

NE

W S

ALE

S /

MO

NTH

N.N. N.N. N.N. N.N. N.N. N.N.N.N. N.N.N.N. N.N.

/ QUOTA CARRIER

Country xx

MISSING INGREDIENTS:- CAPABLE SALES LEADERSHIP

36

Vers

ion

Q3

2014

, v2.

3We’re reshaping our performance pyramidS

ALE

S P

ER

FOR

MA

NC

E

IND

UC

TIO

N

UNDERPERFORMERS

STEADY-EDDIES

OVER-ACHIEVERS

STARS

STEADY-EDDIES

OVER-ACHIEVERS

STARS

TARGET

ACCELERATINGSALES

PROGRAM

37

Vers

ion

Q3

2014

, v2.

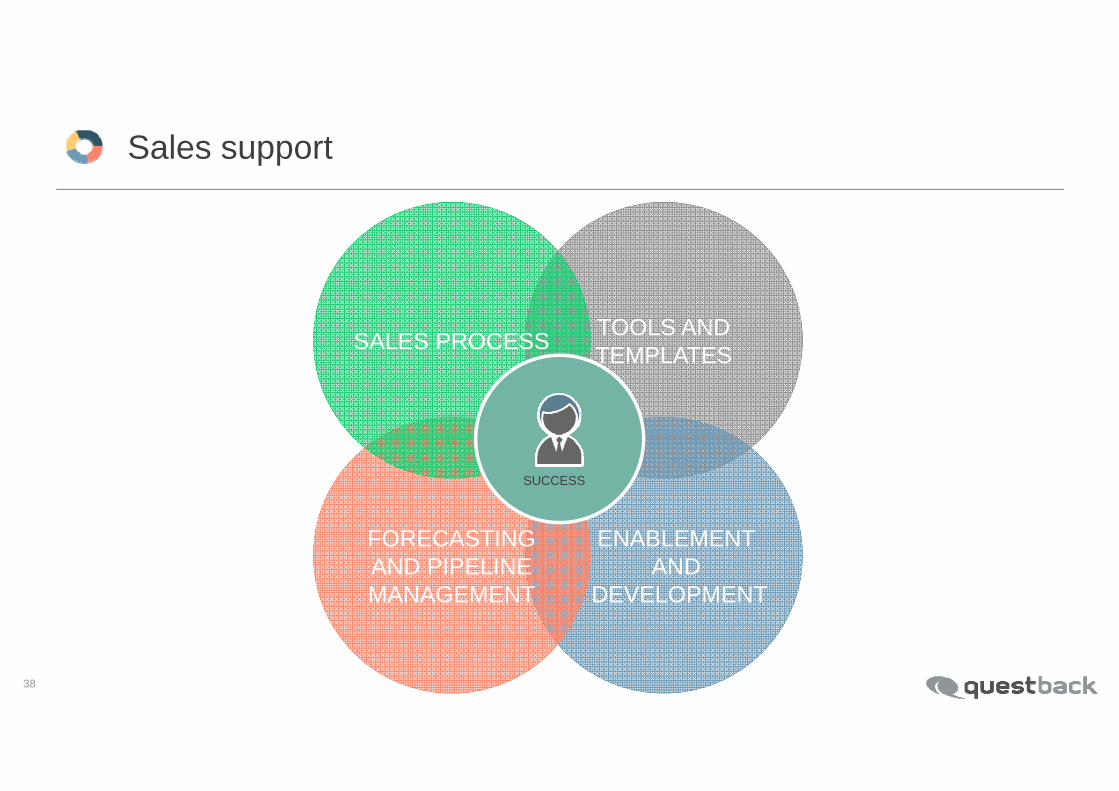

3Sales support

TOOLS AND TEMPLATES

ENABLEMENT AND

DEVELOPMENT

FORECASTING AND PIPELINE MANAGEMENT

SALES PROCESS

SUCCESS

38

Vers

ion

Q3

2014

, v2.

3Various milestones are supported with tools and templates for better control and efficiency

39

Vers

ion

Q3

2014

, v2.

3Account executive’s effectiveness and control over salesfunnel is supported by Salesforce

40

Vers

ion

Q3

2014

, v2.

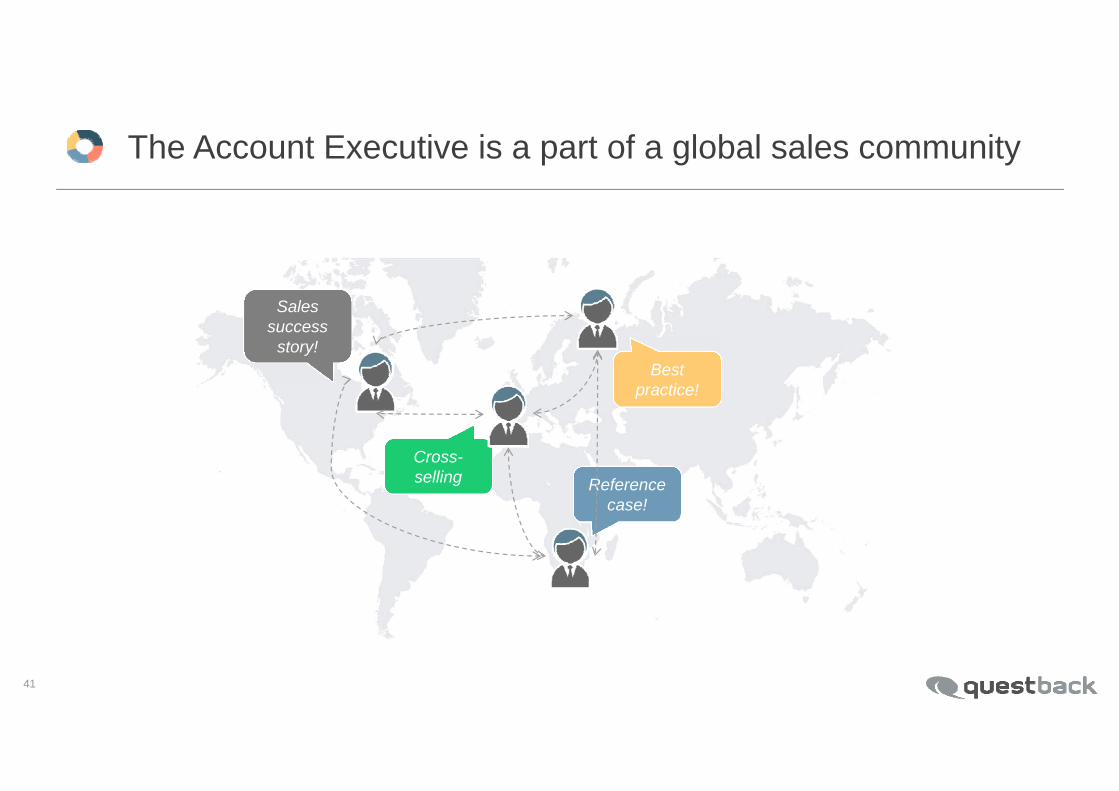

3The Account Executive is a part of a global sales community

Sales success

story!Best

practice!

Cross-selling Reference

case!

41

MY PERSONAL TAKE ON ELEMENTS YOU NEED TO MASTER IN FAST GROWING AND CHANGING SOFTWARE BUSINESS

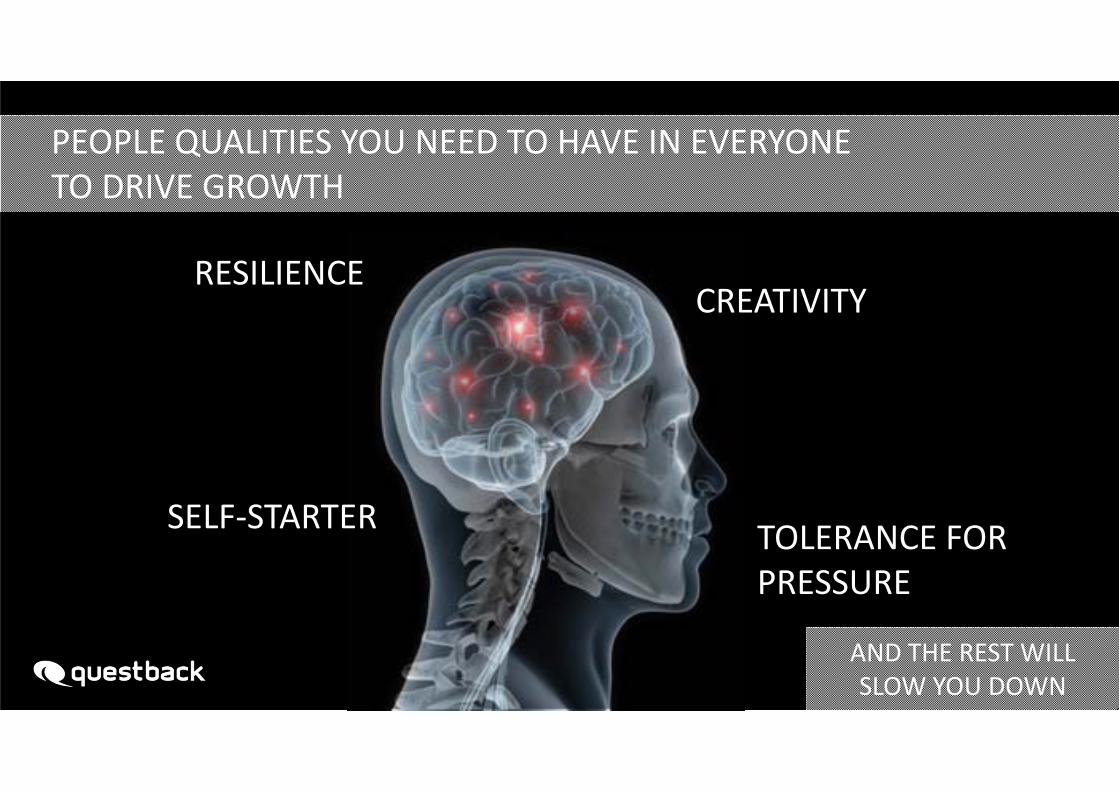

CREATIVITYRESILIENCE

SELF‐STARTER

PEOPLE QUALITIES YOU NEED TO HAVE IN EVERYONE TO DRIVE GROWTH

TOLERANCE FOR PRESSURE

AND THE REST WILL SLOW YOU DOWN

BUILDING A‐TEAM REQUIRES A‐PEOPLE TO ATTRACT AND HIRE THE RIGHT TALENT AROUND THEM (A)

A A

B CAND YOU NEED TO START FROM THE TOP (YOURSELF)

#1 driver of employee engagement: PROGRESS OF MEANINGFUL WORK

How to make leaders tick‐ Responsibility with authority‐ Job with meaning and progress‐ Empowerment with access to resources

How to make employees tick‐ Exposure to leadership that operates through admiration and inspiration

‐ Sense of belonging and acceptance

ENGAGING (RIGHT) PEOPLE WITH THE AMBITIONS IS AFUNDAMENTAL REQUISITE

HIGH AMBITION LEVEL

YES: DEEP ENGAGEMENT

WHY

MOTIVATING PEOPLENO:

EXCUSES

WHAT

FOR MARTYRS TO EXHAUS FOR GUILTY TO EXHAUS

E1 E2MYSELF?

OTH

ERS FO

R ME?

YOU NEED A FINE CONTROL OF DOING THINGS BY ONESELF VS. DELEGATING PEOPLE TO DO THINGS FOR EACHOTHER

KEY IS TO ENSURE THE INDIVIDUALS EXHAUST E1 PRIOR TO GOING E2

MANAGEMENT NEEDS TO BE FULLY CAPABLE OF EXECUTING E1 THEMSELVES TO BE ABLE TO MASTER GROWTH

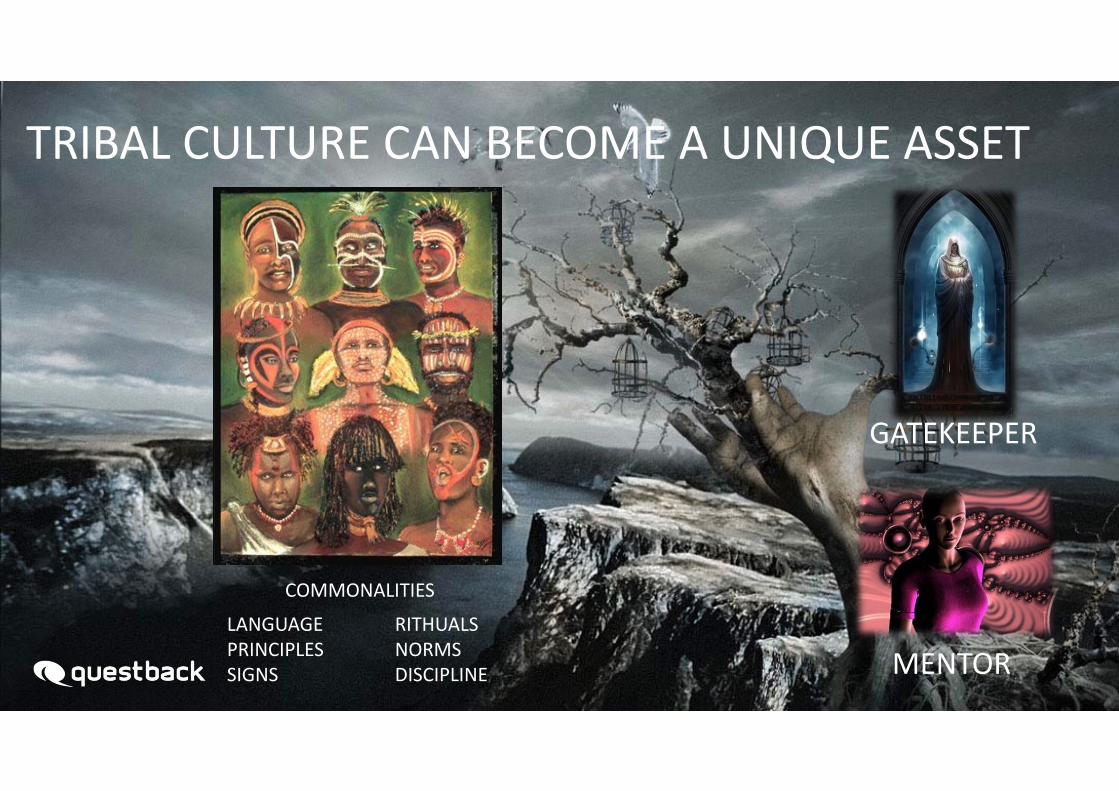

GATEKEEPER

MENTORLANGUAGE RITHUALSPRINCIPLES NORMSSIGNS DISCIPLINE

TRIBAL CULTURE CAN BECOME A UNIQUE ASSET

COMMONALITIES

EACH EMOTIONAL VAMPIRE IS CAPABLE OF SUCKING LIFE OUT OF 5 COLLEAGUES OF HIS/HER

EXTINCT EMOTIONAL VAMPIRES

THE FASTER YOU GROW, THE MORE IT REQUIRES CAPABILITY OF DOING PLANNING AND FINDING WISDOM THROUGH FAILURE TO SUCCEED

AND THIS IS VERY, VERY

HARD TO MASTER !

WORLD OF GROWTH ENTREPRENEURSHIP IS NON‐LINEAR AND CAN ONLY BE OPERATED THROUGH CHAOS

Fragmentation is the natural state of nature

Lack of predictability and control leads to chaos

Chaos is disoriented, but not random

Survival requires to mastering chaos

CHAOS

3 CARDINAL DIRECTIONSTO NAVIGATE CHAOS

PATIENCE

USING CHAOS TO NAVIGATE AS A LEADER IN THE WORLD OF COMPLETE UNCERTAINTY