Implementing MiFID II for Retail Business - · PDF fileImplementing MiFID II for Retail...

54

@uktisa @uktisa Implementing MiFID II for Retail Business Tuesday 11 th July 2017 Dentons LLP, One Fleet Place, London EC4M 7RA

Transcript of Implementing MiFID II for Retail Business - · PDF fileImplementing MiFID II for Retail...

@uktisa@uktisa

Implementing MiFID II for Retail BusinessTuesday 11th July 2017

Dentons LLP, One Fleet Place, London EC4M 7RA

@uktisa@uktisa

Jeffrey Mushens - ChairTechnical Policy Director, TISA

@uktisa@uktisa

Agenda

• Opening remarks by Jeffrey Mushens, Technical Policy Director, TISA – Chair

• Stephen Hanks, Institutional Business Policy, FCA ‘FCA Policy Update’

• Michael Wainwright, Partner, Dentons LLP ‘Legal Framework for Retail Investments’

• Steve Jenner, Head of Customer Strategy, Janus Henderson ‘Product Governance for manufacturers’

• Coffee Break

• Poppy Achilles, Programme Manager, Vanguard ‘Roles & Responsibilities of manufacturers and distributors’

• Alex Denny, Director – Investment Management, Fidelity ‘Appropriateness’

• Panel Session: Costs & Charges on ex post and ex ante disclosure

• Closing remarks from Jeffrey Mushens - Chair

@uktisa@uktisa

Costs & Charges – the Challenges

• Ex ante

• Ex post

• Timing of reporting

• Illustrating the cumulative effect of charges

• What's in scope

@uktisa@uktisa

Costs & Charges – the Challenges

• Strawmen - ex ante

• Example of universe of charges

@uktisa@uktisa

Stephen HanksInstitutional Business Policy, FCA

@uktisa@uktisa

Michael WainwrightPartner, Dentons LLP

MiFID II

Legal Framework for Retail Investments

Doc. 48872998v1

11/07/2017

8

Michael Wainwright

Partner

Dentons UKMEA LLP

+44 20 7246 [email protected]

• MiFID II

• Financial advice market study

• Redefinition of investment advice

• Asset management market study

• Senior management and certification regime

13/07/2017 9

Introduction

• MiFID II product governance

o Extensive information exchange between product providers and distributors

• House policies – inducements, best execution, conflicts

• New responsibilities and powers under SMCR

• Requirement to appoint NEDs

o Value for money framework

o Personal responsibility under SMCR

13/07/2017 10

Governance

• Alignment of UK rules with EU definition of advice

o Advice only regulated where it comes with a personal recommendation

• Greater scope for online services, including complex products

• Platform industry sustaining financial advisers after RDR

o new market study on investment platforms

13/07/2017 11

Advice

• Impact of low interest rates and RDR ban on commission

• Adviser charges encourage ongoing client relationships

• Platforms and model portfolio services support financial advisers at additional cost to the

investor

o Attitude to risk (ATR) models

• B2C platforms provide support for DIY investing in low cost collectives

13/07/2017 12

Prospects for distribution of retail investments

• Variation of permissions

• Competition analysis and powers

o Benchmark submissions

o State Aid rules on bank bail outs

• ESMA product intervention powers under MiFID II

oRetail CFDs

13/07/2017 13

Regulatory Intervention

• Transparency and transaction reporting

• Telephone recording

• Disclosure of costs and charges

• Reporting on performance

• Notification of 10% depreciation on portfolio

13/07/2017 14

Reporting and data

• On exchange, clearing and margin requirements

o Derivatives less accessible?

• Regulators threatening action on retail contracts for differences, once new MiFID powers

become available

• Track record of poor outcomes in relation to SME interest rate hedges

13/07/2017 15

Derivatives

• Changing landscape for advice on retail investments

• MiFID II is part of a much larger picture

• Unbundling under RDR seems to have increased overall costs

• FCA want to use governance as a tool to squeeze margins

13/07/2017 16

Conclusion

Thank you

Dentons UKMEA LLP

One Fleet Place

London

EC4M 7WS

United Kingdom

Dentons is the world's largest law firm, delivering quality and value to clients around the globe. Dentons is a leader on the Acritas Global Elite

Brand Index, a BTI Client Service 30 Award winner and recognized by prominent business and legal publications for its innovations in client

service, including founding Nextlaw Labs and the Nextlaw Global Referral Network. Dentons' polycentric approach and world-class talent

challenge the status quo to advance client interests in the communities in which we live and work. www.dentons.com

© 2016 Dentons. Dentons is a global legal practice providing client services worldwide through its member firms and affiliates. This publication is not designed to provide legal or other advice and you should not take, or refrain from taking, action based on its content. Please see dentons.com for Legal Notices.

13/07/2017 17

@uktisa@uktisa

MiFID II Product Governance for Manufacturers

July 11 2017

Steve JennerHead of Customer StrategyJanus Henderson Investors

@uktisa

MiFID II Product Governance for Manufacturers

1. Product Governance structure

2. Product Lifecycle

3. Target Market

4. Industry consensus

5. Practical application

@uktisa

Product Governance structure

• Defined organisation and operating requirements

• Formal governance and controls

• Appropriate senior management oversight

• Investment and fund boards

• Other corporate entities

• Explicit provisions for Compliance oversight

• Appropriate staff, knowledge and expertise

• Role profiles

• Training

• Manufacturer product governance structure and process to be made available to distributors

TISA/IA Good Practice Guide on MiFID II Product Governance

@uktisa

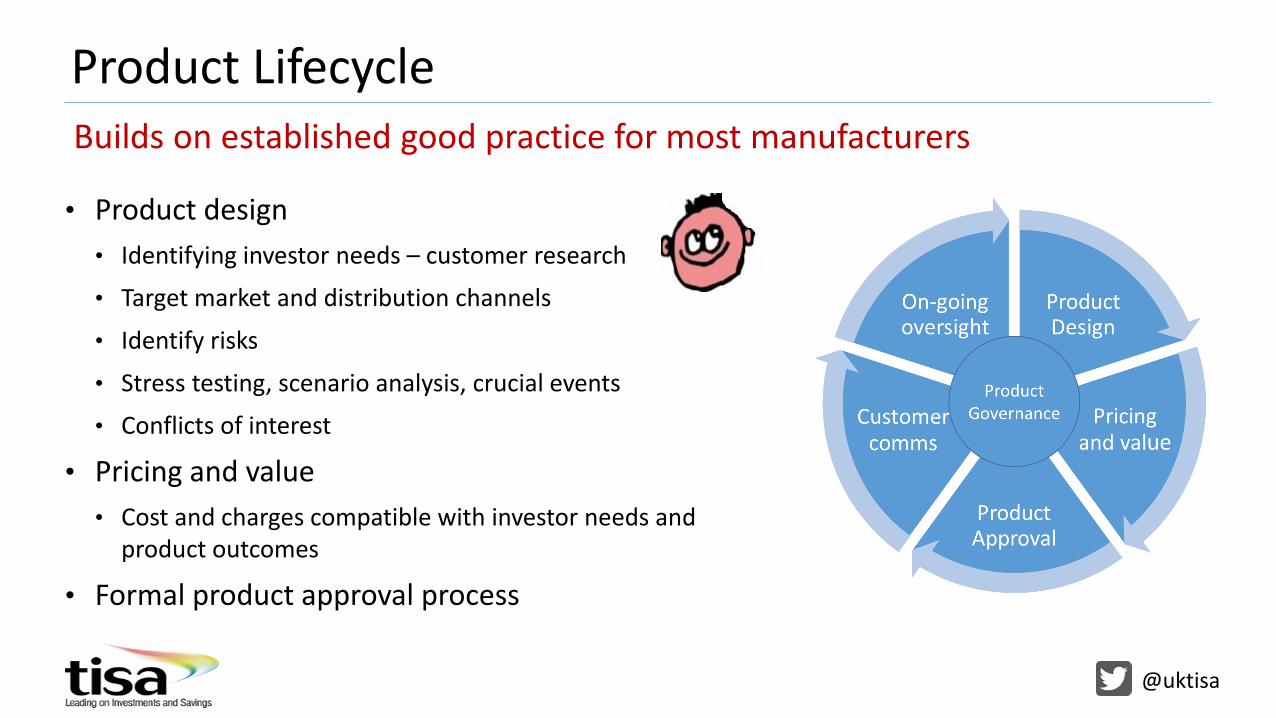

Product Lifecycle

• Product design

• Identifying investor needs – customer research

• Target market and distribution channels

• Identify risks

• Stress testing, scenario analysis, crucial events

• Conflicts of interest

• Pricing and value

• Cost and charges compatible with investor needs and product outcomes

• Formal product approval process

Builds on established good practice for most manufacturers

@uktisa

Product Lifecycle

• Customer communication

• Timely, clear, fair, not misleading

• Appropriate for audience - customer testing

• On-going oversight

• Sales and distribution

• Target market and distribution channel

• Product information and training

• Post launch product assessment

• Still meeting investor expectations

Builds on established good practice for most manufacturers

@uktisa

Target Market – substantial progress made

• Significant industry collaboration

• Interpretation and practical application

• Product manufacturers and distributors

• Trade bodies

• Data vendors

• Regulators

• ESMA guidance shows a clear consideration of the EFAMA target market framework and feedback

• Extensive input from the TISA, IA and members

• EWG draft European MiFID II standard data format – EMT

But 6 months to go and still ground to cover

@uktisa

Known knowns and known unknowns

• Responsibilities for non MiFID II manufacturers – UCITs and AIFMs• FCA – most MiFID II regulations apply directly or as guidance for non-MiFID II

products

• ESMA - TM oversight as good practice for non-MiFID II manufacturers

• Other national regulator approaches still being confirmed• Especially for complexity and appropriateness tests

• ESMA June guidance seems to revert to “all AIFs are complex”

• FCA will continue to apply Article 57 “complexity” tests

• Local variation has implications for both cross border distribution and target market data standards (28 fields!)

• Inter-relationship with target market, PRIPPs and IDD • e.g. comprehension alerts and recommended holding periods

Regulatory approach and scope still bedding in

@uktisa

Target Market – EFAMA modelSimple, unambiguous, data friendly

• Cross border collaboration

• 5 ESMA target market criteria + Distribution channel

1. Client type

2. Knowledge and experience

3. Ability to bear losses

4. Client objectives and needs

5. Risk appetite

(6.) Distribution channel

• Data format responses – Yes, Null, No

• “Null" is crucial grey area – “neither + or -”, “it depends”

• Can be applied to all products, not just funds

@uktisa

Further industry consensus needed

• Final alignment across target market models and industry groups • EFAMA, EWG, WM Daten, banking, structured products and insurance bodies

• High level consensus needed on asset classes and product types• Absolute return• Open ended property funds• Frontier markets• Share classes• Complex products• Professional/experienced investor only products – e.g. QIFs

• Distributor risk appetite still to be determined• Limited to “plainest vanilla” non-complex mass market products?

• Treatment of “diversified” portfolios

The devil remains in the detail to avoid inconsistency

@uktisa

Final decisions required on practical delivery

• Consensus on delivery approach still to emerge – but not crucial• Data +/or narrative• UCITs KIIDs, PRIIPs KIDs or prospectus’• Stand-alone target market documents• Information for end investors• NB: Consistency across all communications will still be required

• Practical target market oversight still under debate• Proportionate approach = complex products only?• Build on existing sales data for all products?• What does an exception look like? (+‘ve or –’ve)• Distributor willingness and ability to provide or just “enable” • How far down the chain can manufacturers realistically go?• Infrastructure build and cost – third party vendors

Industry infrastructure remain a focus for TISA working groups

@uktisa

And the clock is ticking

• The industry is still digesting ESMA and FCA guidelines

• But the end of the regulatory engagement process now forces all stakeholders to work (quickly) with what we have

• January 3 2018 – MiFID II Day.

@uktisa@uktisa

Poppy AchillesProgramme Manager, Vanguard Asset Management

@uktisa@uktisa

Implementing MiFID II for retail businesses

Roles & Responsibilities of manufacturers and distributors

@uktisa@uktisa

Good Practice Guide

• Product Governance Target Market sub-group

• Focused information exchange between manufactures and

distributors

• Key area of discussion – Sales MI

• Group made up of manufacturers, intermediate distributors

and some end distributors

• Sales MI recommendations have been developed

@uktisa@uktisa

Areas of debate

Manufacturer &

Distributor Product

Governance obligations

What information do we

need

Negative target market

reporting

Information exchange

mechanisms

Proportionality

Next steps

@uktisa@uktisa

Manufacturer & Distributor product governance responsibilities

MiFID II Delegated Directive require manufacturers and distributors to review products on a regular

basis to assess whether the product remains consistent with the needs, characteristics and objectives

of the identified target market and whether the intended distribution strategy remains appropriate.

1. Make TM information

available to distributors

2. Consider, on a

proportionate basis, what

information is needed to

complete product reviews

Manufacturer

1. Define actual target market

(can be same as potential)

2. Change distribution

strategy - notify

manufacturer

3. Negative target market

sales – notify the

manufacturer

4. Must provide

manufacturers with

information

Distributor

1. Intermediate distributors

need to enable passing of

information from

manufacturer and

distributor (2 way)

Intermediate distributor

@uktisa@uktisa

Proportionality

• Factors driving proportionality:

• Regulator comments

• Complexity of product

• Distribution strategy

• Distributor oversight

• Availability of information

FCA

A firm must comply with the PROD rules in a way that is

proportionate and appropriate. In doing so, the firm must

take into account the nature of the instrument or service and

the target market.

ESMA

Manufacturers should consider, on a proportionate basis,

what information they need in order to complete their review

and how to gather that information.

@uktisa@uktisa

What information do we need

• Industry consensus is developing

• Non-complex product - focus on basic sales MI

• Complex product - focus is on additional MI, “client type”, “distribution channel”, “results of appropriateness

test”

• Complaints information

• Negative target marketing reporting

• Manufacturers will rely upon first distributor in the chain for MI e.g. A platform

• UK Platforms ahead of the game

• Need to engage our European distributors

• Working towards reporting to be available Q1 2018

@uktisa@uktisa

Negative target market reporting

• Challenges

• End Distributors who plan to sell outside of the TM i.e. broaden distribution strategy – how will this work

in practice?.

• End distributors selling into the negative TM have to report to manufacturer – no reporting infrastructure

exists

• Manufacturers reliant on intermediate distributors to supply MI - but not all MI is available

• MI not available for XO/non-advised channel sales – cannot report on these sales

• MI required where diversification used – no consensus on how this will work

• Sub-group working through these questions

@uktisa@uktisa

Exchanging information

• TISA sub-group formed to look at mechanics of data exchange

• Information exchange already a reality but no standards exist

• Challenges:

• Multiple distributors in a chain causes a look through issue

• Agreeing a standard firms can work with

• Negative target market reporting

• Only 6 months to go

• Need to engage with European partners

@uktisa

Manufacturers - things to consider

• Be prepared to act on MI

• MI is not the whole solution, its complimentary

• Should be part of wider KYD activity

Due diligence -

onboarding

Distribution

agreements

Due diligence -

ongoingSales MI

@uktisa

Distributors - things to consider

• Product governance is your obligation too

• Put in place/enhance product governance framework

• Consider impact on people, process and technology

• Be aware of your reporting obligations • Selling outside of manufacturer target market• Selling into the negative target market• Product reviews• Complaints

• End IFAs need to be engaged

@uktisa

Thank You!

TISADakota House

25 Falcon CourtPreston Farm Business Park

STOCKTON-ON-TEESTS18 3TX

www.tisa.uk.com01642 666999

@uktisa

@uktisa@uktisa

Alex DennyDirector – Investment Management, Fidelity

For investment professional use only and not for general public distribution

MiFID II – Appropriateness and ComplexityTISA working group approach

July 2017

Alex Denny

Fidelity International

Contents

1) What is a complex product?

FCA vs ESMA

2) How can you check appropriateness?

3) Simple, Complex / Non-complex, Not

simple… The MiFID vs PRIIPs dilemma

|44 MiFID II Appropriateness & Complexity

FCA vs ESMA?

|45 MiFID II Appropriateness & Complexity

Well, in the UK, the FCA are the competent authority…

So who is right?

ESMA Q&A 6/6/17 https://www.esma.europa.eu/sites/default/files/library/esma35-43-349_mifid_ii_qas_on_investor_protection_topics.pdf

Page 67: Can shares in non-UCITS collective investment undertakings explicitly excluded under point

(i) of Article 25(4)(a) of MiFID II be nevertheless assessed against the criteria set out in Article 57 of

the MiFID II Delegated Regulation

Answer

No…Shares in non-UCITS explicitly excluded from the universe of non-complex products are

complex per se and cannot be reassessed against the criteria set out in Article 57 of the MiFID II

Delegated Regulation.

FCA Policy Statement 17/14, 3/7/17 https://www.fca.org.uk/publication/policy/ps17-14.pdf

Page 89 Updated rules on the appropriateness test

12.5 In CP16/29, we said that, in our view, investment trusts and non-UCITS retail schemes (NURS)

are neither automatically non-complex nor automatically complex, but must be assessed against the

criteria set out in the MiFID II delegated regulation. We also said that when firms apply these criteria,

they should adopt a cautious approach if there is any doubt as to whether a financial instrument is

non-complex. This remains our view of how t

Commission Delegated Regulation (published after final ESMA recommendations) 25/4/16http://ec.europa.eu/transparency/regdoc/rep/3/2016/EN/3-2016-2398-EN-F1-1.PDF

Page 75 Article 57

A financial instrument which is not explicitly specified in Article 25(4)(a) of Directive 2014/65/EU shall

be considered as non-complex for the purposes of Article 25(4)(a)(vi) of Directive 2014/65/EU if it

satisfies the following criteria… (Art 57 tests)

|46 MiFID II Appropriateness & Complexity

And what is it not?

What is a complex product?

UCITS are non complex – but what about everything else?

• Article 25(4)a sets out non-complex instruments

• Shares (not in collectives), Bonds, Money market, UCITS, most structured deposits and…

• Other non-complex instruments

• Article 57 sets out criteria (A-F) by which “other non-complex instruments” can be judged:

A. Not a derivative

B. Frequent opportunities to redeem / withdraw at public prices

C. No chance of losing more than you invest

D. No trigger or clause to alter risk (convertibles)

E. No charges that make it effectively illiquid

F. Adequately comprehensive information available

But aren’t all non-UCITS complex?

• We believe not, because otherwise Article 57 is “dead-end” regulation which can never be applied.

|47 MiFID II Appropriateness & Complexity

CIS Manager / Pension Manager

Exempt from MiFID

No Appropriateness test required

Other Firms

Not performing MiFID business

Other MiFID business

Advice / Managing

Perform Suitability

test

Execution or ‘Reception & Transmission’

Clearly inform client that no Appropriateness test has been performed (unless there is an

embedded derivative in the product)

Listed shares

Non-Complex

UCITSBonds / Debt

Other

Perform Appropriateness test

• Derivatives• Potential liability

exceeds cost• Insufficient public

information• Little opportunity

to redeem

Performing MiFID business

• TBC

Confirm re ongoing

SuitabilityNon-Deriv

DerivNon-Deriv

DerivNon-Deriv

Deriv

|48 MiFID II Appropriateness & Complexity

Non-complex (examples):

• Most NURS funds

• Most ETFs

• Most investment trusts

Complex (examples):

• Split-cap investment trusts (nature of risk)

• Convertible loan stock (nature of risk)

• Subscription shares (derivative / nature of risk)

• Some property / infrastructure funds (liquidity)

So what is complex and what is not?

|49 MiFID II Appropriateness & Complexity

What exactly are you trying to test?

How can you check appropriateness?

Non Complex / Non Complex

• Compare with the nearest comparable non-complex instrument.

• What makes it different?

• Article 57 A to F – does the customer understand what they are buying?

|50 MiFID II Appropriateness & Complexity

Complex but simple? Not simple, but non-complex?

The MiFID PRIIPs dilemma

PRIIPs and MiFID cannot be intended to lead to confusion. Simple products are non-complex

|51 MiFID II Appropriateness & Complexity

Amendments to the Commission Delegated Regulation of 30.06.2016

24.10.2016 – ESMA “non-paper” on PRIIPs:

New provisions on comprehension alert

“In developing the criteria for the inclusion of the comprehension alert in KID, the ESAs should ensure

that all of the following factors are fully taken into account:

(a) the likelihood of retail investors not understanding the risks incurred by acquiring the PRIIP;

(b) the likelihood of retail investors not understanding the PRIIP being offered;

(c) the criteria specified in Point 10 of the ESMA Opinion on MiFID practices for firms selling

complex products (ESMA Opinion on MiFID practices);

(d) the criteria specified in Point 11 of ESMA Opinion on MiFID practices;

(e) the International Organization of Securities Commissions' (IOSCO) related work streams.”

|52 MiFID II Appropriateness & Complexity

http://www.tisa.uk.com/minutes/170_MiFIDIIAppropriateness-ApproachtoImplementation.pdf

Alternatively search for “TISA appropriateness” in Google

This document is to be updated following recent publications by ESMA and the FCA.

Further reading

The TISA guide to implementation

The full TISA “Approach to implementation” guide on Appropriateness and complexity can be found here:

@uktisa@uktisa

Panel SessionCosts & Charges on ex post and ex ante disclosure

@uktisa

Thank You!

TISADakota House

25 Falcon CourtPreston Farm Business Park

STOCKTON-ON-TEESTS18 3TX

www.tisa.uk.com01642 666999

@uktisa