Implementing a Royalty Compliance Program Presentation to the Federal Laboratory Consortium...

28

Implementing a Royalty Compliance Program Presentation to the Federal Laboratory Consortium Mid-Atlantic Regional Meeting September 15, 2005

-

Upload

chloe-gaines -

Category

Documents

-

view

215 -

download

0

Transcript of Implementing a Royalty Compliance Program Presentation to the Federal Laboratory Consortium...

Implementing a Royalty

Compliance Program

Presentation to the

Federal Laboratory ConsortiumMid-Atlantic Regional Meeting

September 15, 2005

2

Why a royalty compliance program?

3

Post-license considerations

How to… Maximize revenue from negotiated financial

terms

Maintain a good licensee relationship

Protect your IP rights

4

License process

Identify IP (patent) Get approval to out-license Research possible licensees Contact and sell idea to target Negotiate terms

Monitor / collect royalty

R&DR&D Prosecute Patent Application

Prosecute Patent Application

Pay Maintenance Fees

Pay Maintenance Fees

5

Post-license considerations

How to maximize revenue from negotiated financial terms? Avoid misinterpretation Avoid unintentional human errors

How to maintain a good licensee relationship? Minimize misunderstanding and improve trust

How to protect your IP rights? Licensor continues to assert IP rights even

after the license

6

Royalty compliance programsystems / procedures

7

Royalty compliance program systems / procedures

Flexibility Clear language Specific reporting requirements Agreed upon reporting policy Continued communication Desk audits On-site compliance audits

8

Flexibility

Include internal accounting representatives

Update the agreement as accounting systems change

9

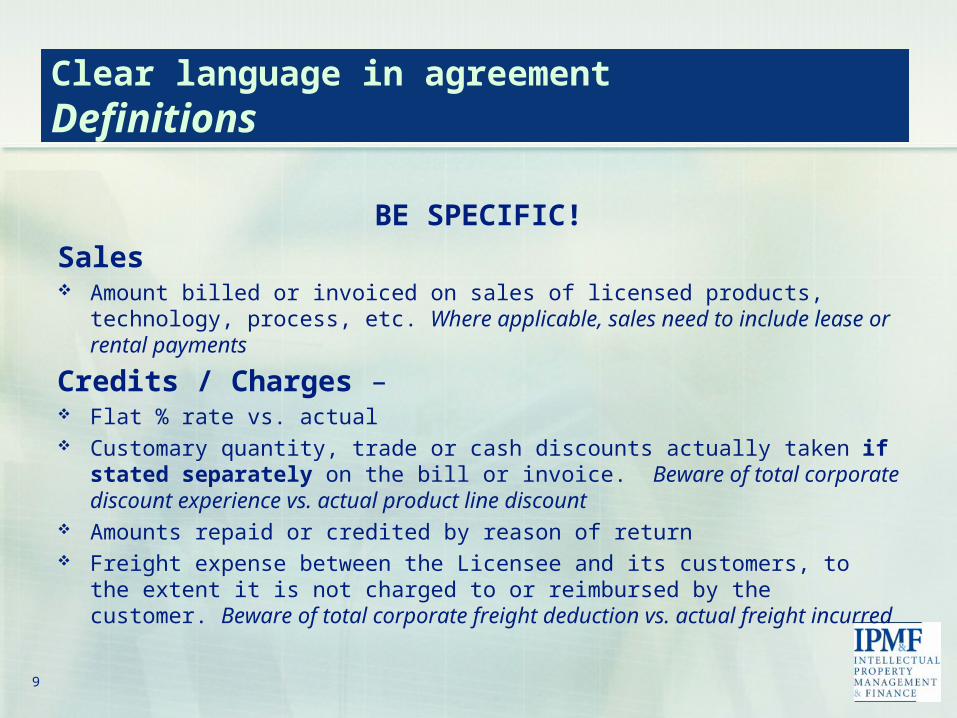

Clear language in agreementDefinitions

BE SPECIFIC!Sales Amount billed or invoiced on sales of licensed products, technology,

process, etc. Where applicable, sales need to include lease or rental payments

Credits / Charges – Flat % rate vs. actual Customary quantity, trade or cash discounts actually taken if stated

separately on the bill or invoice. Beware of total corporate discount experience vs. actual product line discount

Amounts repaid or credited by reason of return Freight expense between the Licensee and its customers, to the

extent it is not charged to or reimbursed by the customer. Beware of total corporate freight deduction vs. actual freight incurred

10

Clear language in agreement Grants

Licensor hereby grants to Licensee, subject to the terms and conditions herein, an exclusive/non-exclusive license, under the Licensed Patents to make, have made…

Disclose the name and location of the sub-contractor Bind the sub-contractor to all of the terms and

conditions Ensure all audit rights extend

11

Clear language in agreementAudit paragraph

Specify rights:

To audit, at least annually To audit for “completeness” of royalty

report To receive electronic files To inspect books and records

12

Clear language in agreementAudit paragraph

Right to inspect books and records should include but not be limited to:

Invoice registers and original invoices Sales analysis reports Accounting general ledgers Sub-license and distributor agreements Price lists, catalogs and marketing materials Audited financial statements and or income tax

returns Sales tax returns Inventory records Shipping documents Commission reports Purchasing documents

13

Clear language in agreementLate or underpaid royalties

Should bear interest Simple vs. compound Rate and source

Threshold for Licensee to bear audit fees and expenses:

>5% -- entire cost >2%-5% -- 50% cost

14

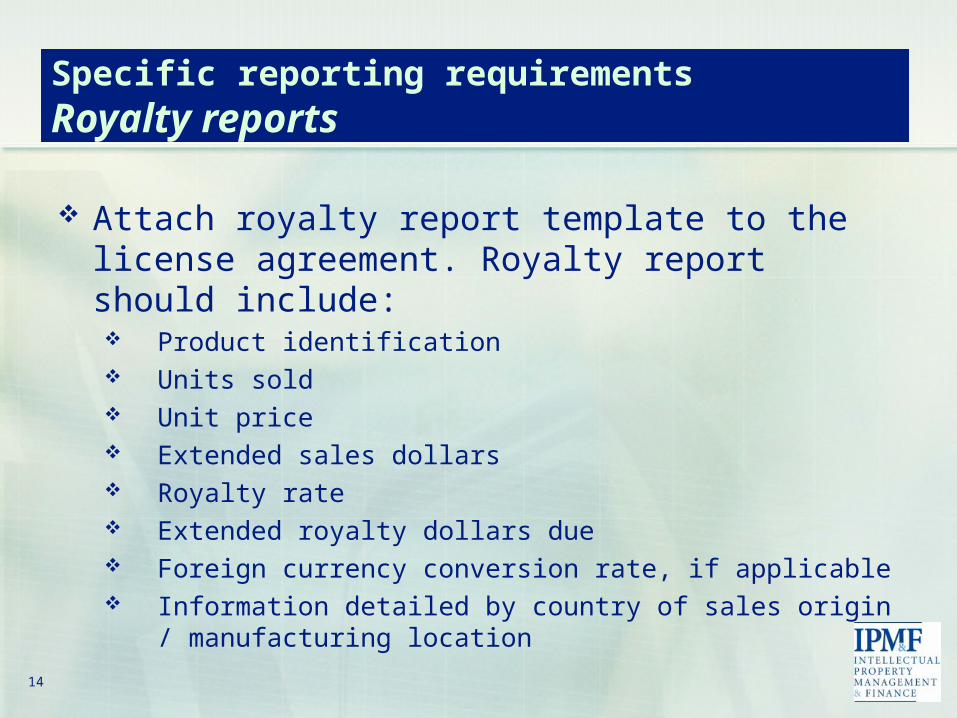

Specific reporting requirementsRoyalty reports

Attach royalty report template to the license agreement. Royalty report should include: Product identification Units sold Unit price Extended sales dollars Royalty rate Extended royalty dollars due Foreign currency conversion rate, if applicable Information detailed by country of sales origin /

manufacturing location

15

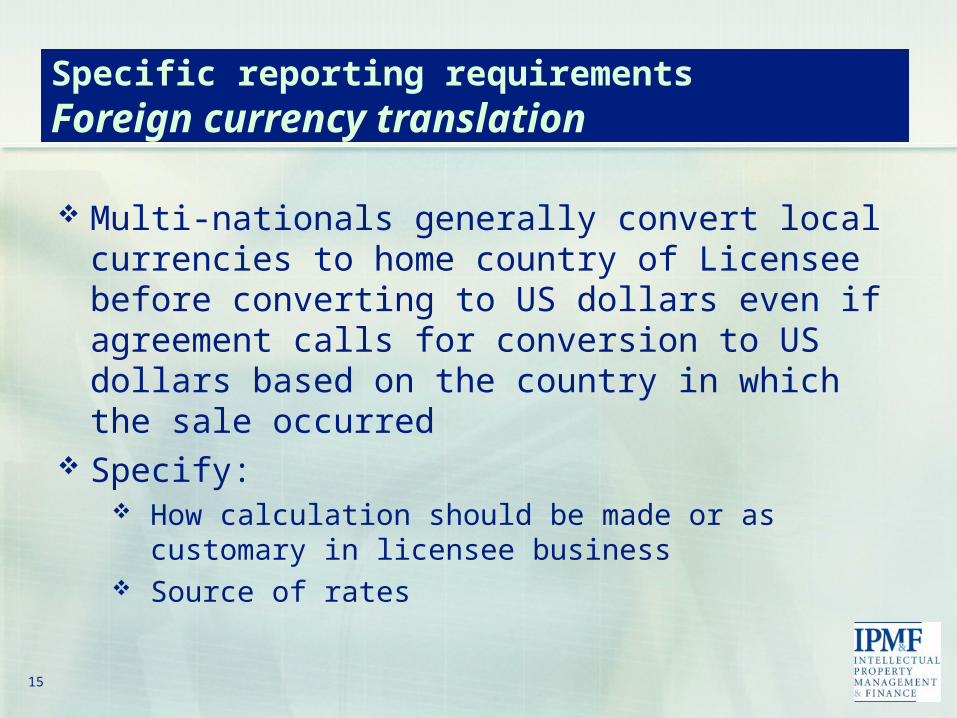

Specific reporting requirementsForeign currency translation

Multi-nationals generally convert local currencies to home country of Licensee before converting to US dollars even if agreement calls for conversion to US dollars based on the country in which the sale occurred

Specify: How calculation should be made or as

customary in licensee business Source of rates

16

Agreed upon reporting policy for the Licensee

Specify period covered by royalty report and when each is due

Detailed procedures

17

Continued communication with a Licensee

Consider yourself their bank; they owe you money Need open lines of communication at various

levels Decision maker Person preparing royalty report

Annually, distribute a Licensee questionnaire Who calculates royalties due? Do they have the agreement? What procedures are performed in calculating royalties? Is a second review performed? Etc.

18

Desk audits

With each payment: Historical payment trend analysis Overall company health analysis Industry trend analysis Math check Follow up on all questions Communicate, communicate, communicate

19

Royalty compliance audit for all Licensees

The confirmation that a license/contract is being complied with, including: Payments Research milestones Advertising, or Any other clause that allows itself to be tested by an

independent party

What is a royalty compliance audit?

20

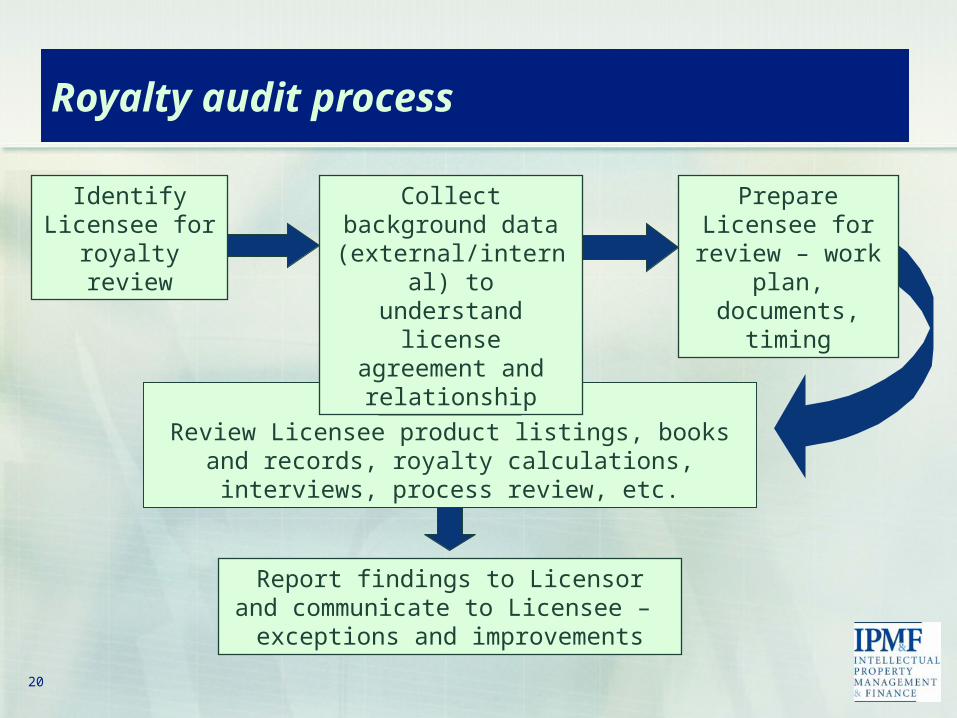

Identify Licensee for

royalty review

Prepare Licensee for

review – work plan,

documents, timing

Field WorkReview Licensee product listings, books and

records, royalty calculations, interviews, process review, etc.

Report findings to Licensor and communicate to Licensee –

exceptions and improvements

Collect background data

(external/internal) to understand

license agreement and relationship

Royalty audit process

21

Royalty reporting red flags

22

Red flags: there may be errors in the royalty report if…

Change in the person preparing royalty report New products launched Selling product in new territories New manufacturing facility Licensee has been acquired or has merged Licensee is having financial difficulty

23

More red flags: there may be errors in the royalty report if…

Accounting systems change Royalty reports are progressively late Licensee’s sales of the covered product are not in

line with the industry Humans are involved in report preparation

24

Common findings

25

Common findingsErrors discovered

Clerical math Conversion rates Omission of new products

developed Transfer pricing to affiliates Controls not in place to ensure data

accuracy Misinterpretation Arbitrary interpretations

Unintentional

Intentional

26

The cost of royalty reporting errors

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

Prior Period 2001 2002 2003 2004

Audit Fees & Expenses

Interest

Unreported Product Line(and license misinterpretation)

Unreported Geographic Region(and license misinterpretation)

Reported

Royalties

27

Why have a royalty compliance program?

To maximize revenue negotiated To maintain a good licensee relationship To ensure compliance To demonstrate intent to protect rights

28

Speakers

Karen H. Wang, CPA, CVASenior Vice President

(410) [email protected]

Judy Ann Byrd, CPA, CIRAVice President(410) [email protected]

Intellectual Property Management & Finance1637 Thames Street

Baltimore, MD 21231www.ipmf.com