Impacto del TPP y del TTIP en América Latina -...

13

Impacto del TPP y del TTIP en América Latina Foro de comercio exterior CANIPEC-COMCE Oportunidades para México entre un mercado latinoamericano y el europeo Ciudad de México 30 de junio de 2016 Beatriz Leycegui

Transcript of Impacto del TPP y del TTIP en América Latina -...

Impacto del TPP y del TTIP en América Latina

Foro de comercio exterior CANIPEC-COMCE

Oportunidades para México entre un mercado latinoamericano y el

europeo Ciudad de México

30 de junio de 2016 Beatriz Leycegui

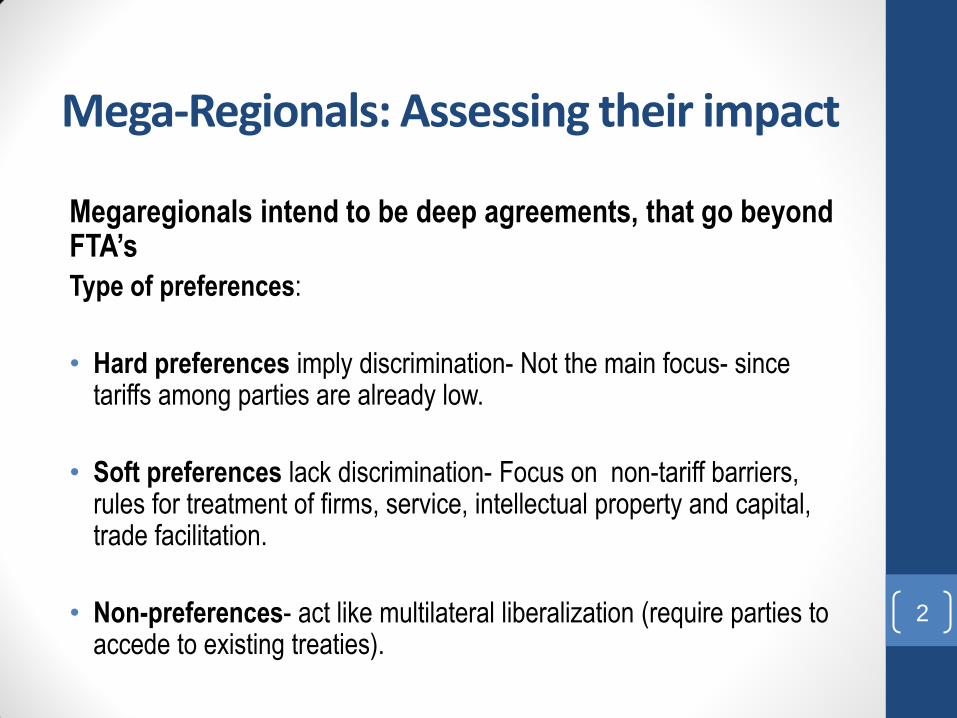

Megaregionals intend to be deep agreements, that go beyond FTA’s

Type of preferences:

• Hard preferences imply discrimination- Not the main focus- since tariffs among parties are already low.

• Soft preferences lack discrimination- Focus on non-tariff barriers, rules for treatment of firms, service, intellectual property and capital, trade facilitation.

• Non-preferences- act like multilateral liberalization (require parties to accede to existing treaties).

2

Mega-Regionals: Assessing their impact

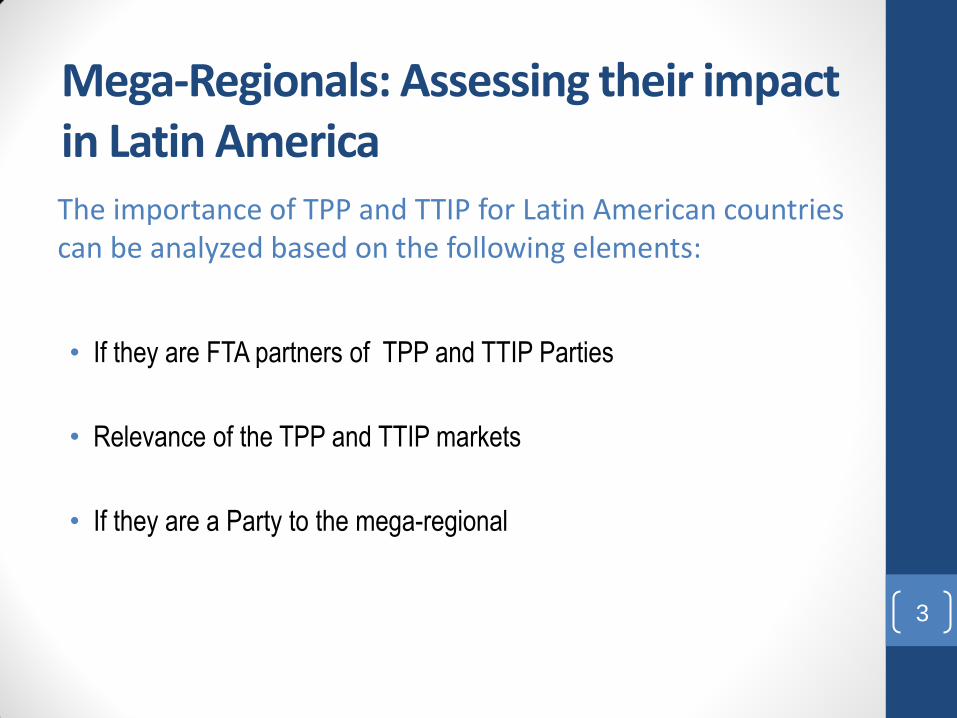

• If they are FTA partners of TPP and TTIP Parties

• Relevance of the TPP and TTIP markets

• If they are a Party to the mega-regional

3

Mega-Regionals: Assessing their impact in Latin America The importance of TPP and TTIP for Latin American countries can be analyzed based on the following elements:

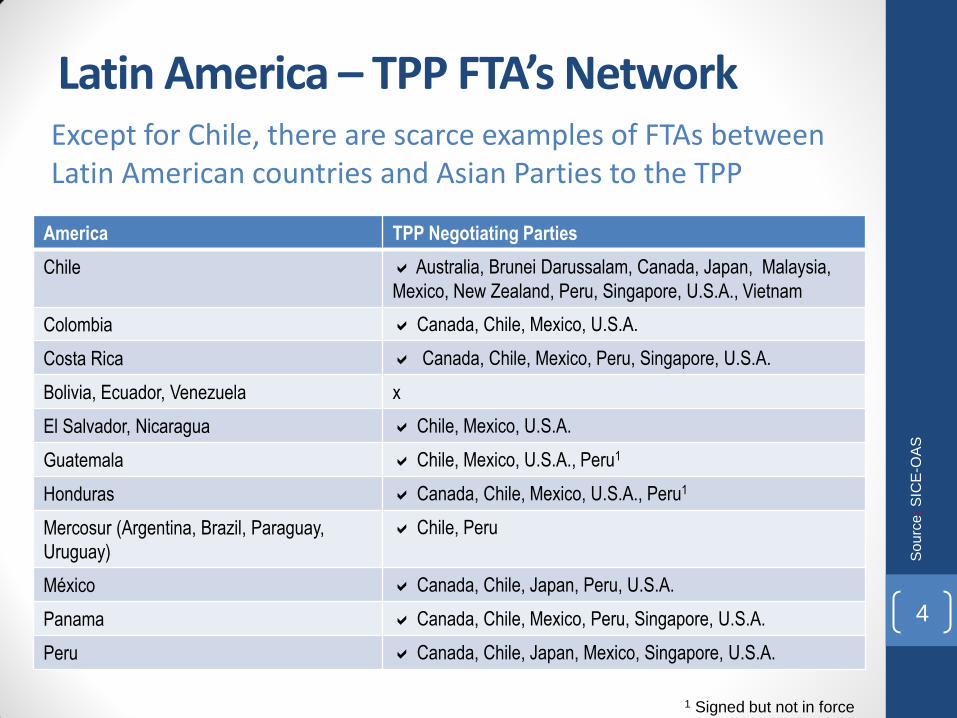

Latin America – TPP FTA’s Network

4

So

urc

e: S

ICE

-OA

S

Except for Chile, there are scarce examples of FTAs between Latin American countries and Asian Parties to the TPP

America TPP Negotiating Parties

Chile a Australia, Brunei Darussalam, Canada, Japan, Malaysia,

Mexico, New Zealand, Peru, Singapore, U.S.A., Vietnam

Colombia a Canada, Chile, Mexico, U.S.A.

Costa Rica a Canada, Chile, Mexico, Peru, Singapore, U.S.A.

Bolivia, Ecuador, Venezuela x

El Salvador, Nicaragua a Chile, Mexico, U.S.A.

Guatemala a Chile, Mexico, U.S.A., Peru1

Honduras a Canada, Chile, Mexico, U.S.A., Peru1

Mercosur (Argentina, Brazil, Paraguay,

Uruguay)

a Chile, Peru

México a Canada, Chile, Japan, Peru, U.S.A.

Panama a Canada, Chile, Mexico, Peru, Singapore, U.S.A.

Peru a Canada, Chile, Japan, Mexico, Singapore, U.S.A.

1 Signed but not in force

5

So

urc

e: S

ICE

-OA

S

Latin America – TTIP FTA’s Network

In contrast, virtually all Latin American countries have a FTA with

the EU, and an increased number of them have a FTA with the USA

Latin America European Union

Mercosur (Argentina, Brazil, Praguay,

Uruguay, Venezuela)

a2

El Salvador, Guatemala, Nicaragua a

Guatemala a

Honduras a

Bolivia x

Ecuador, Venezuela x

Chile a

Colombia a

Costa Rica a

México a

Panama a

Peru a

2 In negotiation

Relevance of Negotiating Countries’ Markets

6

So

urc

e: W

orld

Eco

no

mic

Foru

m

Latin American countries export on average three times more exports to the EU than to TPP Asian countries

4.7 4.8 5.8

13.4

1.8 1.3 2.1 6.2

1

14.4

5.6

20.2

15.4 14.9

5.9

14.6 16.4

11.2

0

10

20

30

40

50

60

70

80

90

Argentina Bolivia Brazil Chile Colombia Mexico Paraguay Peru Uruguay

Non-AmericanTPP countries(1)

American TPPCountries (2)

USA(TPP/TTIP)

EuropeanUnion (TTIP)

(1) Australia, Brunei,

Japan, Malaysia, New

Zealand, Singapore

Viet Nam

(2) Canada, Mexico,

Chile and Peru

Exports from LAC to TPP and TTIP countries (2012)

Figures presented in (%)

LAC to EU: 12.5%

LAC to Non-American TPP

countries: 4.1%

Participation in Negotiations - TPP

• Compensating erosion of tariff preferences with new concessions

• Deepening integration with the U.S.

• Increasing their participation in regional value chains and secure not to

be left out of existent ones

• Strengthening economic ties with Asian TPP counterparts

• Participating in the rewriting of the new generation rule book

7

Chile, Mexico and Peru are the only Latin American countries part of the TPP, focusing their interests in:

Participation in Negotiations - TPP

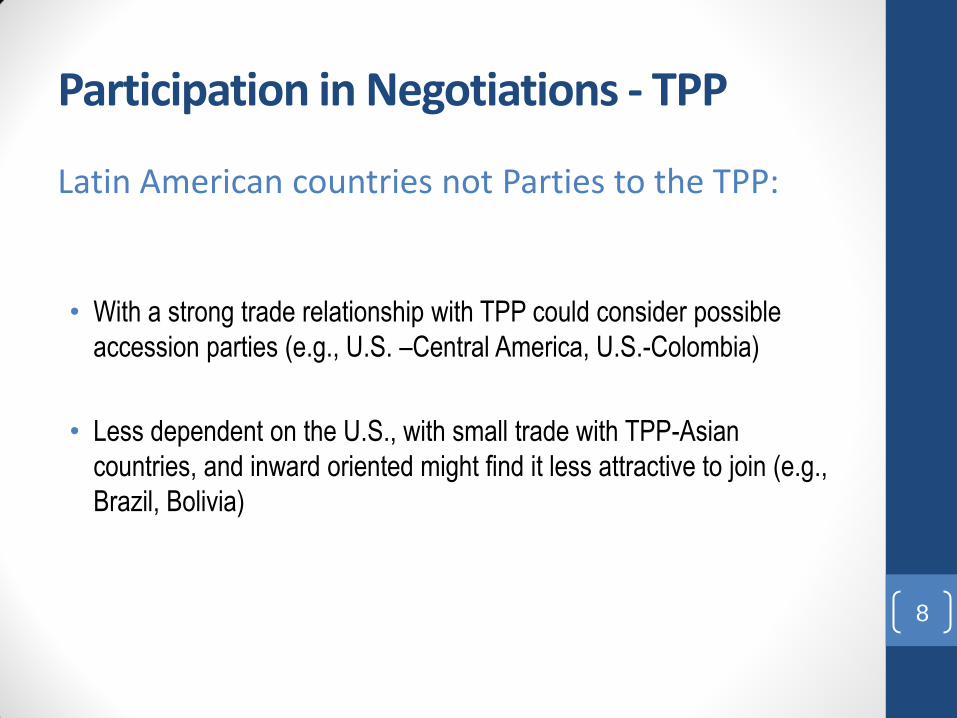

• With a strong trade relationship with TPP could consider possible

accession parties (e.g., U.S. –Central America, U.S.-Colombia)

• Less dependent on the U.S., with small trade with TPP-Asian

countries, and inward oriented might find it less attractive to join (e.g.,

Brazil, Bolivia)

8

Latin American countries not Parties to the TPP:

• Only two negotiating parties – USA and EU, closed negotiation that has

rejected Mexico and Canada

• The TTIP could represent a great opportunity for Latin American

countries, e.g.:

• Cummulation of origin could diminish trade-diversion effects

• TTIP could eventually converge with other FTAs of the region.

• Response from Mexico. Deepen existing FTA with the EU

Risk of certain countries such as Mercosur, given the preferences possibly

granted to the U.S. in the agricultural sector.

9

Degree of Participation in Negotiations - TTIP

Mexico-TPP

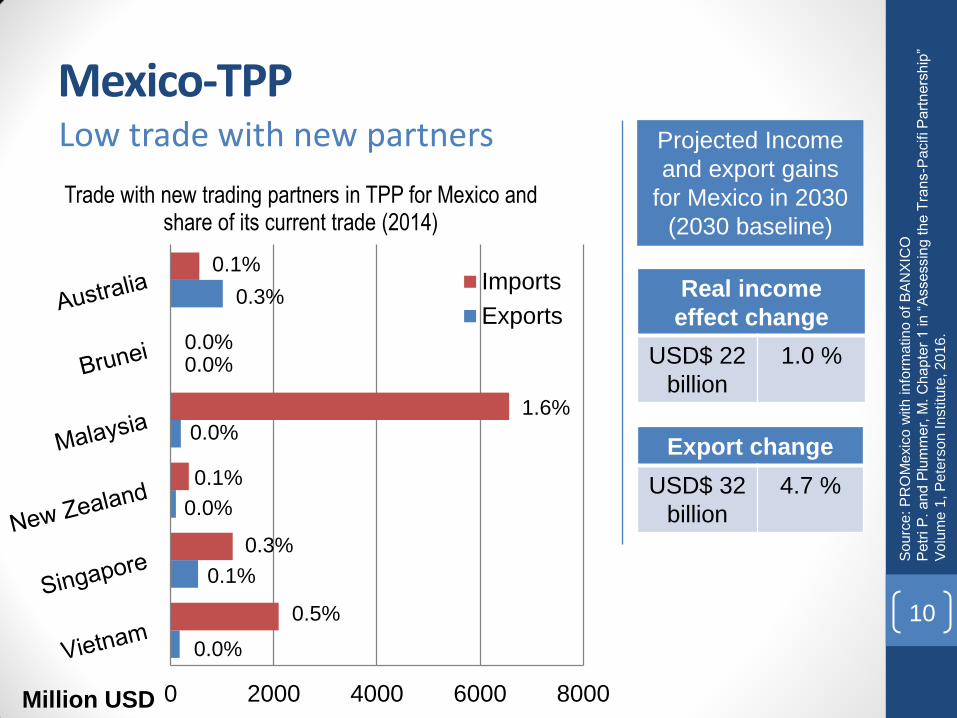

0 2000 4000 6000 8000Million USD

Trade with new trading partners in TPP for Mexico and share of its current trade (2014)

Imports

Exports

10

Low trade with new partners

0.3%

0.1%

0.0%

0.0%

0.0%

0.0%

0.1%

0.3%

1.6%

0.5%

0.1%

0.0%

So

urc

e: P

RO

Me

xic

o w

ith in

form

atin

o o

f B

AN

XIC

O

Pe

tri P

. a

nd

Plu

mm

er,

M. C

hap

ter

1 in

“A

sse

ssin

g th

e T

rans-P

acifi P

art

ners

hip

”

Vo

lum

e 1

, P

ete

rso

n In

stitu

te, 2

01

6.

Real income

effect change

USD$ 22

billion

1.0 %

Projected Income

and export gains

for Mexico in 2030

(2030 baseline)

Export change

USD$ 32

billion

4.7 %

NAFTA-TPP Relevant Issues

11

• Coexistence of TPP with NAFTA and

other FTAs-challenge in identifying

which is more favorable

• Accession clause: could promote

integration in North and South America

• Development of North America’s and

Asia Pacific value chains

• Single set of rules of origin and

accumulation of origin

• NAFTA-the increase in common FTA’s

could facilitate the negotiation of a

customs union

Integration in Latin America will progress if:

• it is based ina common political and economic vision, as opposed to only geographical proximity;

• integration is adopted as a State policy that trascends changes in governments;

• democratization of trade occurs which will help gain support for regional and global integration (more companes, sectors and regions benefitting); and

• pragmatism prevails over dogmatism, populism.

12

Final comments

13

Beatriz Leycegui [email protected]

Edificio Plaza Reforma Prol. Paseo de la Reforma #600-010-B

Santa Fe Peña Blanca, México, D.F. 01210

Tel. (55) 5985 6685 Fax: (55) 5985 6628

www.sai.com.mx