Impact of Working Capital Management Policy on Market...

20

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA) An Online International Research Journal (ISSN: 2311-3162) 2015 Vol: 1 Issue 2 354 www.globalbizresearch.org Impact of Working Capital Management Policy on Market Value Addition R.M.S. Bandara, Department of Accountancy, University of Kelaniya, Colombo, Sri Lanka. Email: [email protected] _______________________________________________________________________________________________________ Abstract Working Capital Management (WCM) includes maintaining appropriate levels of current assets and current liabilities required by a firm. Management of short-term assets and liabilities needs a careful investigation since it plays an important role in deciding the firm’s profitability, risk as well as its value. This research study investigated the impact of Working Capital Management Policy (WCMP) on firm value in Sri Lankan Companies. Data were gathered from 74 companies listed in the Colombo Stock Exchange (CSE) covering seven business sectors for the sample period of 2009/10 to 2013/14 which comprises 370 firm year observations. Descriptive statistics, correlation and panel regression analysis were employed as measures of analysis. Firms’ Working Capital Investment Policy (WCIP) and Working Capital Financing Policy (WCFP) were used as independent variables. Firm value was measured in terms of Market Value Addition (MVA) as dependent variable in the study. According to the overall panel regression model, WCIP and WCFP both recorded a negative relationship to MVA proving the individual model results. The results showed significant negative relationship between the firms’ degree of aggressiveness of WCIP and MVA of the companies in Sri Lanka. It provided evidence that the minimum level of investment in current assets leads to have higher MVA of the firms in Sri Lanka. Further results do not provide statistically significant results to prove the negative relationship between WCFP and MVA. ___________________________________________________________________________ Key words: Working Capital Management Policy, Firm Value, Market Value Added, Sri Lanka

Transcript of Impact of Working Capital Management Policy on Market...

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

354 www.globalbizresearch.org

Impact of Working Capital Management Policy on

Market Value Addition

R.M.S. Bandara,

Department of Accountancy,

University of Kelaniya, Colombo, Sri Lanka.

Email: [email protected]

_______________________________________________________________________________________________________

Abstract

Working Capital Management (WCM) includes maintaining appropriate levels of current

assets and current liabilities required by a firm. Management of short-term assets and

liabilities needs a careful investigation since it plays an important role in deciding the firm’s

profitability, risk as well as its value.

This research study investigated the impact of Working Capital Management Policy (WCMP)

on firm value in Sri Lankan Companies. Data were gathered from 74 companies listed in the

Colombo Stock Exchange (CSE) covering seven business sectors for the sample period of

2009/10 to 2013/14 which comprises 370 firm year observations.

Descriptive statistics, correlation and panel regression analysis were employed as measures

of analysis. Firms’ Working Capital Investment Policy (WCIP) and Working Capital

Financing Policy (WCFP) were used as independent variables. Firm value was measured in

terms of Market Value Addition (MVA) as dependent variable in the study.

According to the overall panel regression model, WCIP and WCFP both recorded a negative

relationship to MVA proving the individual model results. The results showed significant

negative relationship between the firms’ degree of aggressiveness of WCIP and MVA of the

companies in Sri Lanka. It provided evidence that the minimum level of investment in current

assets leads to have higher MVA of the firms in Sri Lanka. Further results do not provide

statistically significant results to prove the negative relationship between WCFP and MVA.

___________________________________________________________________________

Key words: Working Capital Management Policy, Firm Value, Market Value Added, Sri

Lanka

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

355 www.globalbizresearch.org

1. Introduction

Corporate financial officers identify Working Capital Management (WCM) as being

important to their firms’ value. Management of short-term assets and liabilities needs a

careful investigation since the WCM plays an important role in the determination of the

profitability, liquidity and risk as well as the ultimate objective of firm’s value (Smith, 1980).

The greater the investment in current assets lead for the lower risk due to ability of settling

short term obligation, but also the lower the profitability obtained, because of the inability to

invest in the profitable long term investments. Efficient management of working capital is a

fundamental part of the overall corporate strategy to create shareholders’ value. Firms try to

keep an optimal level of working capital that maximizes the value of the firms (Howorth and

Westhead, 2003; Deloof, 2003 and Afza and Nazir, 2007 & 2008).

The main objective of WCM is to maintain an optimal balance between each of the

working capital components. Business success heavily depends on the ability of financial

executives to effectively manage the working capital component of receivables, inventory,

and payables (Filbeck and Krueger, 2005). Firms can reduce their financing costs and/or

increase the funds available for expansion projects by minimizing the amount of investment

tied up in current assets while arising a higher level of liquidity risk.

Working Capital Management Policy (WCMP) is the firm’s way of making investment in

their current assets which is known as working capital investment policy and use short-term

liabilities to finance firms’ assets which is known as working capital financing policy.

Theoretically, a firm can adopt different working capital management practices as aggressive

working capital management policy, moderate working capital management policy and

conservative working capital management policy based on its investment and financing

policies. Those different policies and practices are affecting the profitability, liquidity, risk as

well as finally the value of the firm in different ways.

The Firm Value is the present value of the expected future flows discounted at the rate of

return required by investors (Robert, Mark and Rabhi, 2008). Any investment in working

capital larger than this optimum would increase the firm’s assets without a proportionate

increase in its returns and thus lowering the rate of return on investment. Weston and

Copeland (1992) suggested that, given the optimum, increasing the cash holding which is one

of the working capital components of the company, negatively affects the shareholder value.

Peter Drucker (1998) has stated that until a business earns a profit that is greater than its cost

of capital, it operates at a loss, means firm is not operating as a value creator, it destroy the

value. While most of the studies suggest that firms which minimize their investment in net

operating capital leading for an aggressive working capital management policy, will

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

356 www.globalbizresearch.org

maximize their profitability and thereby maximize firm value, this inference does not

necessarily follow.

In the current research work, a deep attention was given to the financial statements of

listed companies in Sri Lanka. Based on the financial figures extracted from the annual

reports, researcher observed that organizations are having different levels of current assets

and liabilities. Further, some organizations adopt aggressive working capital policy while

some are running with conservative and moderate level of policies. Therefore, researcher is

interested to carry out a study, to identify the impact of working capital policy on firm value

of the listed companies in Sri Lanka.

1.1 Problem statement

How does Working Capital Management Policy impact on Firm Value in Sri Lanka?

The problem is to identify the relationship between working capital management policy

and value of the Sri Lankan companies listed in the Colombo Stock Exchange (CSE).

1.2 Research Question

What is the relationship between Working Capital Management Policy (WCMP) and

Firm Value?

It is argued that the failure of WCM is mainly due to inability of reflecting the

characteristics and challenges of contemporary organizational settings that has led to a loss of

relevance and give rise to the need for a conceptual framework explaining current WCMP.

Having identified working capital management Investment Policy (IP) and Financing Policy

(FP) of the firms, backed by the literature and theoretical domain, researcher examined the

relationship to value of the firms which is measured by the Market Value Added (MVA).

With the answer of this research question, researcher elaborates the behaviour of the WCM in

an organization and how it leads to create firm value in Sri Lankan organizations.

1.3 Research objective

The researcher expects to achieve following objective at the completion of the study.

To determine the relationship between Working Capital Management Policy & Firm

Value in Sri Lanka.

1.4 Significance of study

In the today’s dynamic business environment, survival of the organization is more

uncertain even though the companies are earning profit, unless they can’t meet the short term

obligations. Corporate finance basically deals with three decisions such as capital structure

decisions, capital budgeting decisions, and working capital management decisions. Among

these, working capital management is a very important component of corporate finance since

it affects the profitability and liquidity of a company and finally to its value. Efficient WCM

involves planning and controlling current assets and current liabilities in a manner that

eliminates the risk of inability to meet short term obligations on one hand and avoids

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

357 www.globalbizresearch.org

excessive investment (Eljelly, 2004). Therefore, it is deemed that there is a need of studying

the role of working capital management policies on firm value in the Sri Lankan context.

Further, a profitable company may fail, if it does not have adequate cash flow to meet its

liabilities as they fall due. On the other hand, one of the main objectives of a firm is to

maximize its value. Therefore, it is important to study how firms should keep the proper

investments in current assets and maintain proper level of current liabilities in an enterprise

with maximizing its’ value. Moreover Firm value is more important to have sustainable

growth rate for a business leading to attract prospective investors. Because value of the firm is

the form that investors motivate to invest in the business and increase of value will benefit the

firms’ prestige by increasing future growth. Further, firm value is also important since it

affects to achieve the desired performance and long term survival of the enterprises.

Therefore with the current study, researcher attempted to support for the organizations to keep

a healthy WCMP in such a way to maximize firm value.

If the management of working capital policy is satisfactory, there is high performance in

the organization, possibly leading to create its value. Theory explains that the lower degree of

aggressiveness is leading for low level of liquidity, high level risk and high level of

profitability; it does not explain the ultimate impact to the value creation of an organization.

And also it varies according to the Investment policy and the financing policy of the firm. It is

evidenced by the inconclusive results generated by the researchers in the literature as

mentioned earlier paragraphs. Further, Wadsworth and Bryan (1974) pointed out that

sometime managers’ decisions relating to the working capital management will increase

earnings but it destroy value of the firm while some decisions increase the value but no profit

is added to the firm. Therefore, researcher expects to study the behavior of working capital

management policy adopted by the Sri Lankan organizations and how it leads to create value

to the firm. Further, it will contribute to fill the knowledge gap in the existing literature.

According to the literature available, very few researches have been carried out in the area

of WCM in Sri Lanka and less researches have been carried out relating to the WCMP and the

firm value in specific in the Sri Lankan context. Therefore the researcher expected to study

the behavior and stability of working capital management in different business sectors and the

impact of those on the firm value. While the propose study enhances the WCMP ensuring the

maximum utilization of current assets and current liabilities in Sri Lankan enterprises to

achieve ultimate objective of value creation, it will lead to fill the empirical gap exists.

2. Literature Review

A wide-ranging literature review was conducted to identify the direction of this study and to

understand the broader perspectives of Working Capital Management (WCM) and its impact

to the value of the firm.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

358 www.globalbizresearch.org

WCM is important because of its impact on the firm’s profitability and risk, and

consequently its value (Smith, 1980). Excessive levels of current assets may have a negative

effect on the firm’s profitability whereas a low level of current assets may lead to lower level

of liquidity and stock-outs resulting in difficulties in maintaining smooth operations (Van

Horne & Wachowicz, 2004). Accordingly, greater the investment in current assets, the lower

the risk, but also the lower the profitability obtained. Filbeck and Krueger (2005) highlighted

the importance of efficient WCM by analyzing the WCMP of 32 non-financial industries in

USA. According to their findings significant differences exist between industries in working

capital practices over time. WCM literature presents a long debate on the risk/return tradeoff

among different WCMP (Brigham and Ehrhardt, 2004; Gitman, 2005; Moyer et. al., 2005 &

Pinches, 1991). Accordingly, it is worth to notice that more aggressive working capital

policies are associated with higher return and higher risk while conservative working capital

policies are concerned with the lower risk and return (Carpenter and Johnson, 1983; Gardner

et al., 1986 & Weinraub and Visscher, 1998). It further explain, when a company is

continuing with the aggressive working capital management policy will lead to have higher

level of return, lower level of liquidity and higher level of risk which is not healthy every

time. However, effective management of working capital policy has been receiving little

attention and yielding more significant results. More aggressive working capital policies are

associated with higher return and higher risk while conservative working capital policies are

concerned with the lower risk and return (Gardner et al., 1986 & Weinraub & Visscher,

1998).

Salawu R.O. (2006) investigated fifteen diverse industrial groups over an extended period

to establish the relationship between aggressive and conservative working capital practices.

The results strongly explained that the industries had significantly different current asset

management policies. Additionally, the relative industry ranking of the aggressive or

conservative asset policies exhibited remarkable stability over time. It is evident that there is a

significant negative correlation between industry asset and liability policies. Relatively

aggressive working capital asset management seems balanced by relatively conservative

working capital financial management. Furthermore he explains that a firm in deciding its

working capital policies should consider the policies adopted in that particular industry in

which it operates and a firm pursing aggressive working capital investment policy should

match it with a conservative working capital financing policy. This is important to mitigate

the risk being faced under aggressive working capital investment policies by safety involved

under conservative working capital financing policy.

However, Weinraub and Visscher (1998) have discussed the issue of aggressive and

conservative working capital management policies by using quarterly data for a period of

1984 to 1993 of US firms. The researchers have examined ten diverse industry groups to

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

359 www.globalbizresearch.org

study the relative relationship between their aggressive/conservative working capital policies

and they have concluded that the industries had distinctive and significantly different working

capital management policies over the time. Moreover, the relative nature of the working

capital management policies exhibited remarkable stability over the ten-year study period.

The study showed a significant negative correlation between industry asset and liability

policies. It is important to notice that they also generated similar results and additionally they

concluded that relatively aggressive working capital asset policies (working capital

investment policy) are followed and balanced by relatively conservative working capital

financial policies confirming the Salawu’s (2006) similar findings in Nigerian context.

Further, Afza and Nazir (2007) investigated the relationship between the aggressive and

conservative working capital policies for seventeen industrial groups and a large sample of

263 public limited companies listed at Karachi Stock Exchange for a period of 1998-2003.

Using ANOVA and LSD test, the study found significant differences among their working

capital investment and financing policies across different industries. Moreover, rank order

correlation confirmed that these significant differences were remarkably stable over the

period of six years of study. Finally, ordinary least regression analysis found a negative

relationship between the profitability measures of firms and degree of aggressiveness of

working capital investment and financing policies.

Another important study which confirms the results of Afza and Nazir (2007), conducted

by Mian S. and Talaf (2009) have shown that the negative relationship between the

profitability measures of the firm and the degree of aggressiveness of working capital

management policies by analyzing the 204 Pakistan firms listed under sixteen industrial

groups in the Karachchi Stock Exchange (KSE). The data was analyzed for the period of

1998-2005.

Theoretically, greater the investment in current assets, the lower the risk, but also the

lower the profitability obtained. In contradiction, Carpenter & Johnson (1983) provided

empirical evidence that there is no linear relationship between the level of current assets and

revenue systematic risk of US firms; however, some indications of a possible non-linear

relationship were found which were not highly statistically significant. So, the link between

WCM and firm value is not simple as the link between WCM and firm profitability discussed.

Turning to the empirical literature on WCM policy and the firm value, researcher could

not find any published study of the relationship between WCMP and firm value in specific.

Hall, J. (2001); Ruback and Sesia (2000) and Smith (1980) stated that efficient level of

WCM is one of the driver for value creation. Deloof (2003); Garcia-Teruel and Martinez-

Solano (2007); Soenen (1993) and Shin and Soenen (1998) all showed that the profitability

of a firm, measured by either return on assets or return on equity, is improved as the firm

improves its management of its working capital. While most of such studies suggest that firms

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

360 www.globalbizresearch.org

that minimize their investment in net operating capital will maximize their profitability and

thereby maximize firm value, this inference does not necessarily follow (Robert, Mark &

Rabhi, 2008).

The study available relating to the Sri Lankan context is the research done by Pandey and

Perera (1997), providing an empirical evidence of WCMP and practices of the private sector

manufacturing companies in Sri Lanka. The information and data for the study were gathered

through questionnaires and interviews with chief financial officers of a sample of

manufacturing companies listed on the Colombo Stock Exchange. They found that most

companies in Sri Lanka have informal working capital policy and company size has an

influence on the overall working capital policy (formal or informal) and approach

(conservative, moderate or aggressive). And also, company profitability has an influence on

the methods of working capital planning and control. According to the study conducted by S.

Morawakage and Lakshan A.M.I (2009) with the companies registered in Colombo Stock

Exchange, results suggest that managers can increase corporate profitability by reducing the

number of inventory turn over days and increasing the creditor’s payable days in order to

minimize the length of the working capital cycle. Increase in creditor’s payable days would

give opportunities to the company for further investments.

Turning to the literature on firm value, a well designed and implemented working capital

management is expected to contribute positively to the creation of a firm’s value. De Wet

(2005) has studied companies listed on the JSE Securities Exchange South Africa, using

market value added (MVA) as a proxy for shareholder value. The results suggest strong

relationship between MVA and cash flow from operations. The study also found very little

correlation between MVA and EPS, or between MVA and DPS, concluding that the

credibility of share valuations based on earnings or dividends must be questioned. The main

objective of a firm is to increase the market value. Working capital management affects

profitability of the firm, its risk, thus its value (Smith, 1980). In other words, efficient

management of working capital is an important component of the general strategy aiming at

increasing the market value (Afza & Nazir, 2007; Deloof, 2003 and Howorth & Westhead,

2003). Even though there are pros and cons of using MVA to measure the firm value, it has

been proved by the literature that MVA can be used as the better proxy for measuring the

value of the firm.

3. Methodology

Research methodology is mainly focused on discussing the hypotheses and relevant

variables that are considered in the research design to achieve its above mentioned research

problem.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

361 www.globalbizresearch.org

3.1 Hypotheses

The following hypotheses were formulated in the study to examine the impact of WCMP on

firm value.

H1: There is a negative relationship between the degree of aggressiveness of working capital

management investment policy and MVA of the companies in Sri Lanka.

H2: There is a negative relationship between the degree of aggressiveness of working capital

management financing policy and MVA of the companies in Sri Lanka.

3.2 Variables

3.2.1 Independent variables

For the study, independent variable is the working capital management policy and selected

two indicators to measure the degree of aggressiveness of WCMP based on followings two

aspects*.

Investment Policy (IP)

Financing Policy (FP)

With the support of available literature and relevant theories of WCM, the degree of

aggressiveness or conservativeness is measured by; (Afza, Nazir, 2007; Weinraub Visscher,

1998 and Salawu, 2006)

Total Current Assets to Total Assets Ratio (Investment Policy)

Total Current Liabilities to Total Assets Ratio (Financing Policy)

3.2.2 Investment Policy (IP)

It explains the way of firm can invest their funds in the short term or long term assets

resulting in minimal level of investment of the firm’s funds in current assets comparatively to

the fixed assets closes to the more aggressive and if it is vise-versa close to the

conservativeness. In order to measure the degree of aggressiveness or conservativeness,

following ratio will be used: (Afza, Nazir, 2007; Weinraub and Visscher, 1998 and Salawu,

2006)

IP = Total Current Assets (TCA) X 100

Total Assets (TA)

Where a lower ratio means a relatively aggressive policy.

Where a higher ratio means a relatively conservative policy.

3.2.3 Financing Policy (FP)

It discusses the way that a firm finances their permanent or temporary assets by using short

term or long term funds. If a firm utilizes higher levels of current liabilities and less long-term

debt to finance its current assets will be close to the aggressiveness and if a firm uses long

term funds to finance its permanent assets as well as current assets it closes to

conservativeness. The degree of aggressiveness or conservativeness of a financing policy

* See Afza, Nazir, 2007; Weinraub and Visscher, 1998 and Salawu, 2006 for further evidence

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

362 www.globalbizresearch.org

adopted by a firm will be measured by: (Afza, Nazir, 2007; Weinraub and Visscher, 1998;

Salawu, 2006)

FP = Total Current Liabilities (TCL) X 100

Total Assets (TA)

Where a higher ratio means a relatively aggressive policy.

Where a lower ratio means a relatively conservative policy

When the degree of aggressiveness i.e. current assets as a percentage of total asset ratio is

close to zero, it is referred as aggressive working capital management policy while that ratio

is close to hundred, it is named as conservative working capital management policy. On the

other hand degree of aggressiveness i.e. current liabilities as percentage of total asset ratio is

close to zero, it is referred as conservative working capital management policy while that ratio

is close to hundred it named as aggressive working capital management policy.

3.2.4 Market Value Addition (MVA)

Market value is the difference between market value of the firm’s stock and the amounts

of equity capital supplied by investors. It measures the effect on value of management’s

decisions since the firm’s inception. Further it says how much management has added to

shareholder value over the company’s history.

The main distinguishing feature of MVA is that, it is largely a cumulative measure and

therefore communicates the market’s present verdicts on the Net Present Value (NPV) of all

the firms’ past, current and contemplated capital investment projects (O’Byrne, 1996). MVA

measures the effect on value of management’s decisions since the firm’s inception. It is

calculated as follows.

MVA = Market Value of Company – Total Operating Capital Invested

(O’Byrne, 1996)

Based on the above mentioned constructs and concepts following expression can be made;

Firm Value = f (Aggressive Investment Policy, Aggressive Financing Policy, Conservative

Investment Policy, Conservative Financing policy, Moderate Investment

Policy and Moderate Financing Policy )

Where the degree of aggressiveness or conservativeness is measured by

Total Current Assets to Total Assets Ratio (Investment Policy)

Total Current Liabilities to Total Assets Ratio (Financing Policy)

FVit

= β0 + β1 (TCA/TA

it) + β

2 (TCL/TA

it)

Where:

FV it

= Firm Value of firm i for time period t

TCA/TA it = Total Current Assets to Total Assets Ratio of firm i for time period t

TCL/TA it

= Total Current Liabilities to Total Assets Ratio of firm i for time period t

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

363 www.globalbizresearch.org

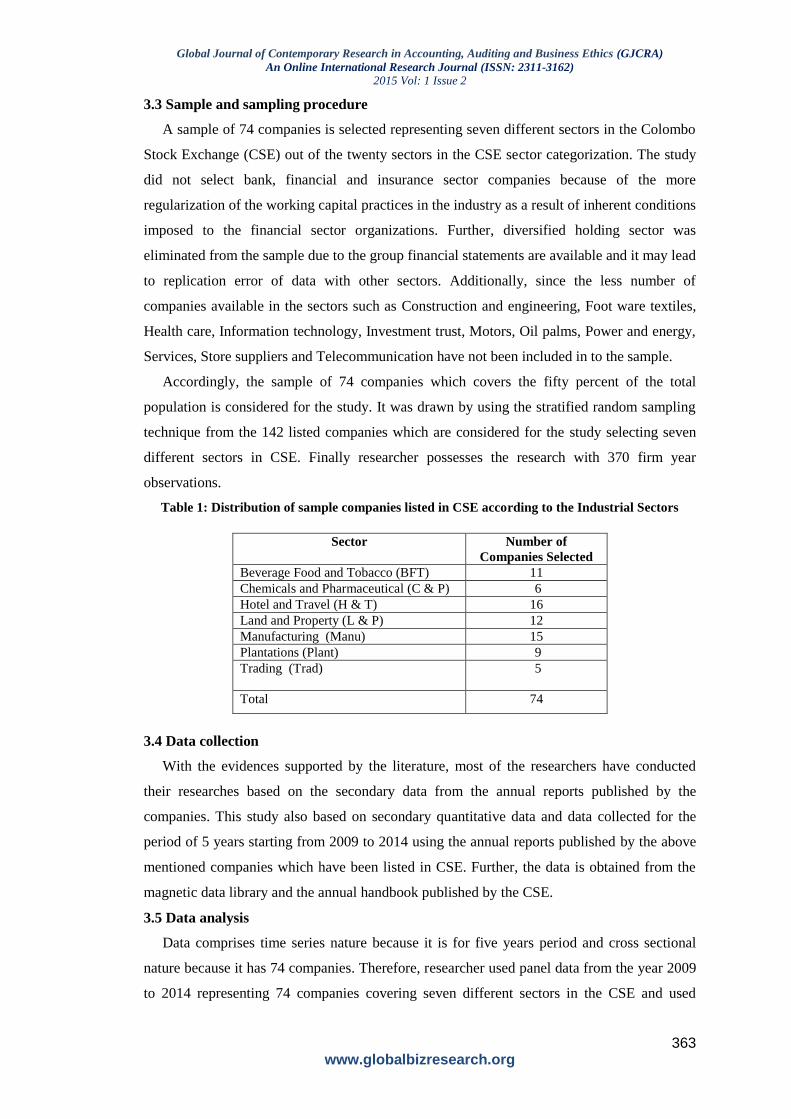

3.3 Sample and sampling procedure

A sample of 74 companies is selected representing seven different sectors in the Colombo

Stock Exchange (CSE) out of the twenty sectors in the CSE sector categorization. The study

did not select bank, financial and insurance sector companies because of the more

regularization of the working capital practices in the industry as a result of inherent conditions

imposed to the financial sector organizations. Further, diversified holding sector was

eliminated from the sample due to the group financial statements are available and it may lead

to replication error of data with other sectors. Additionally, since the less number of

companies available in the sectors such as Construction and engineering, Foot ware textiles,

Health care, Information technology, Investment trust, Motors, Oil palms, Power and energy,

Services, Store suppliers and Telecommunication have not been included in to the sample.

Accordingly, the sample of 74 companies which covers the fifty percent of the total

population is considered for the study. It was drawn by using the stratified random sampling

technique from the 142 listed companies which are considered for the study selecting seven

different sectors in CSE. Finally researcher possesses the research with 370 firm year

observations.

Table 1: Distribution of sample companies listed in CSE according to the Industrial Sectors

Sector Number of

Companies Selected

Beverage Food and Tobacco (BFT) 11

Chemicals and Pharmaceutical (C & P) 6

Hotel and Travel (H & T) 16

Land and Property (L & P) 12

Manufacturing (Manu) 15

Plantations (Plant) 9

Trading (Trad) 5

Total 74

3.4 Data collection

With the evidences supported by the literature, most of the researchers have conducted

their researches based on the secondary data from the annual reports published by the

companies. This study also based on secondary quantitative data and data collected for the

period of 5 years starting from 2009 to 2014 using the annual reports published by the above

mentioned companies which have been listed in CSE. Further, the data is obtained from the

magnetic data library and the annual handbook published by the CSE.

3.5 Data analysis

Data comprises time series nature because it is for five years period and cross sectional

nature because it has 74 companies. Therefore, researcher used panel data from the year 2009

to 2014 representing 74 companies covering seven different sectors in the CSE and used

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

364 www.globalbizresearch.org

SPSS for basic statistical analysis and E-views software package for panel data regressions to

analyse the data. With the secondary data obtained from the annual reports, following data

analysis techniques were used to meet the research objectives.

Measures of descriptive statistics such as mean, maximum, minimum, standard deviation

is used to analyse the variables. Regression analysis was used to examine the impact of

WCMP as IP and FP on Firm Value which is measured and MVA. Pearson’s correlation

coefficient is used to see the relationship between Firm Value and WCMP of the companies.

4. Results and Discussion

4.1 Results

4.1.1 Investment policy, Financing policy and firm value

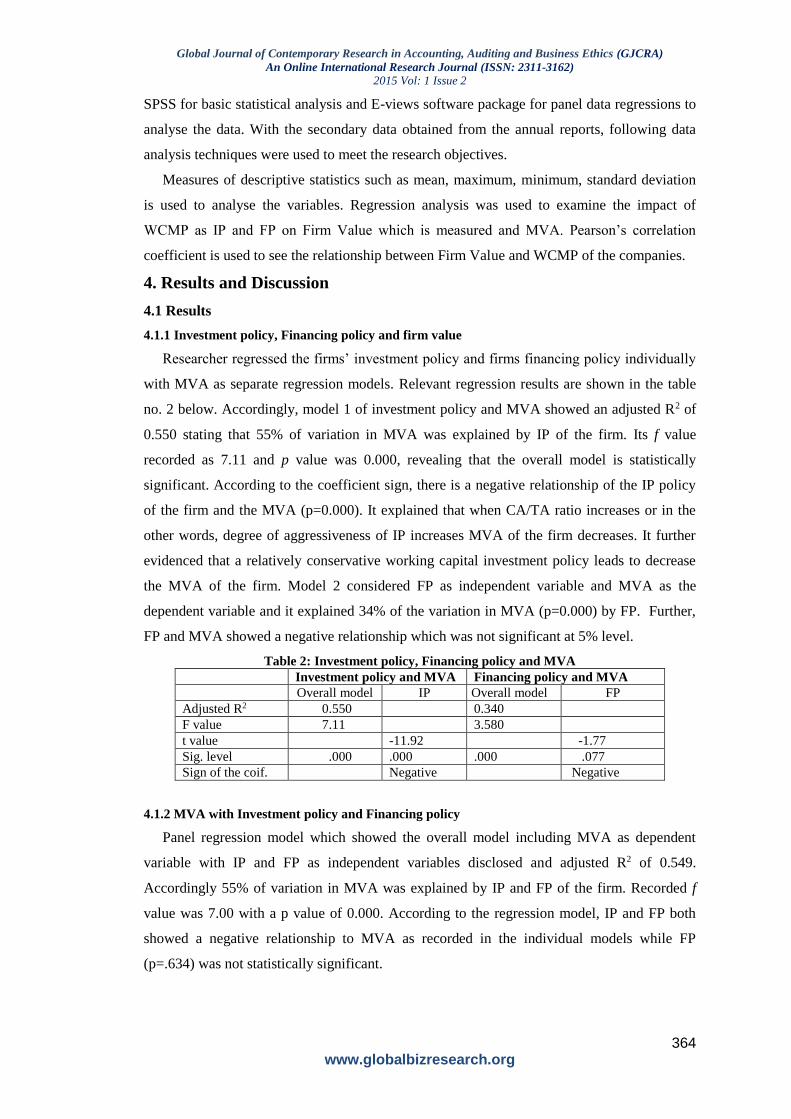

Researcher regressed the firms’ investment policy and firms financing policy individually

with MVA as separate regression models. Relevant regression results are shown in the table

no. 2 below. Accordingly, model 1 of investment policy and MVA showed an adjusted R2 of

0.550 stating that 55% of variation in MVA was explained by IP of the firm. Its f value

recorded as 7.11 and p value was 0.000, revealing that the overall model is statistically

significant. According to the coefficient sign, there is a negative relationship of the IP policy

of the firm and the MVA (p=0.000). It explained that when CA/TA ratio increases or in the

other words, degree of aggressiveness of IP increases MVA of the firm decreases. It further

evidenced that a relatively conservative working capital investment policy leads to decrease

the MVA of the firm. Model 2 considered FP as independent variable and MVA as the

dependent variable and it explained 34% of the variation in MVA (p=0.000) by FP. Further,

FP and MVA showed a negative relationship which was not significant at 5% level.

Table 2: Investment policy, Financing policy and MVA

Investment policy and MVA Financing policy and MVA

Overall model IP Overall model FP

Adjusted R2 0.550 0.340

F value 7.11 3.580

t value -11.92 -1.77

Sig. level .000 .000 .000 .077

Sign of the coif. Negative Negative

4.1.2 MVA with Investment policy and Financing policy

Panel regression model which showed the overall model including MVA as dependent

variable with IP and FP as independent variables disclosed and adjusted R2 of 0.549.

Accordingly 55% of variation in MVA was explained by IP and FP of the firm. Recorded f

value was 7.00 with a p value of 0.000. According to the regression model, IP and FP both

showed a negative relationship to MVA as recorded in the individual models while FP

(p=.634) was not statistically significant.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

365 www.globalbizresearch.org

Table 3: MVA with Investment policy and Financing policy

Overall model IP FP

Adjusted R2 .549

F value 7.00

t value -11.72 -0.47

Sig. level .000 .000 .634

Sign of the coif. Negative Negative

According to the correlation analysis taking all the companies together, it recorded a

negative relationship between IP and MVA. According to the regression analysis, the

relationship between IP and MVA is significant. Also, FP and MVA is not significant.

4.2 Discussion of Findings

4.2.1 Investment Policy (IP) and MVA

The first hypothesis in the study states that there is a negative relationship between the

degree of aggressiveness of working capital management investment policy and MVA of the

companies in Sri Lanka. According to the Pearson’s correlation coefficients, IP indicated a

highly negative correlation to MVA as -.714 (p= .000). It explains that the increase in IP

which is measured in terms of the ratio of CA/TA resulted in decreasing the MVA of the firm.

Complying with the results laid down by the correlation coefficient between IP and MVA, the

regression IP and MVA as independent and dependent variables respectively, showed an

adjusted R2 of .550 (p= .000) and .549. It explains that on an average 55% of variation in

MVA is explained by IP of the firm. Further, both models record a significant negative

relationship between the IP and MVA. This negative relationship between the IP of the firm

and MVA explains that, when CA/TA ratio increases or in the other words, degree of

aggressiveness of IP increases, MVA of the firm decreases.

According to the statistical evidence given by the correlation as well as regression, first

hypothesis was failed to reject. It says that any firm invests more in to the current assets

compared to the total assets leads to have a lower level of MVA of firms. A firm with high

level of CA/TA ratio maintains a relatively conservative working capital management IP

which leads to have relatively lower level MVA. On the other way around, it concludes that,

if any firm has a low level of CA/TA ratio or a relatively aggressive working capital

management IP yields a relatively higher level of MVA.

In the empirical research domain, there are few specific evidences to justify the

relationship between IP and MVA. On the grounds provided by the literature, profitability has

a positive relationship with the value of the firm; this study results in consistent with the

findings of Soenen and Solano (1993). Their research was on the effects of working capital

management on the profitability of a sample of small and medium-sized Spanish firms with

the panel data, covering the period 1996-2002. This results demonstrated that managers can

create value by reducing their firm’s number of day’s accounts receivable and inventories, i.e.

by reducing the level of CA. Moreover, current finding complied with the study conducted by

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

366 www.globalbizresearch.org

Deloof (2003). He analyzed a sample of large Belgian firms during the sample period 1992-

1996 and the results indicated that Belgium firms can improve their profitability by reducing

the number of accounts receivable days and by reducing inventories.

Results of the study can be further validated by examining reasons from the theoretical

aspects. Accordingly, one of the reasons for the negative relationship between WC investment

policy and the value of the firm is that, minimum level of CA decreases the level of

operational capital in the business yielding a high level of operational cash flows in the

business and finally it helps to create value to the firm. On the other hand low level of CA as

a percentage of TA, leads to have high level of FA which increases the future expansion

capacity and revenue generation capacity of the firm as an attractive indicator for the

investors. Therefore, it creates a high demand for the shares of the firm leading to increase the

market value of the firm.

Another reason for the negative relationship is that any firm invests more in the stocks

leads to have an unsold stock which tide up money unnecessarily and stock loss cost etc.

Similarly, keeping more money in the debtors, having more opportunity cost of cash and

possibility for bad debt, and it leads to have cash insufficiency to pay for creditors as a result

of financing alternatives with high borrowing cost. Additionally, any investment in working

capital more than its optimum, would increase the firm’s assets without a proportionate

increase in its returns and thus lowering the rate of return on investment. This low level of

return causes to have a low market demand for the shares and ultimately decrease the MVA.

Weston and Copeland (1992) also suggested that, given the optimum, increasing the cash

holding negatively affects the shareholder value.

Moreover, excessive exposure to have liquid assets generated higher sales revenues, but at

the same time the positive results of increase in the sales volumes have been offset by high

level of generated costs of keeping the high level of liquid assets and finally firm generates a

lower value. All these cause to have negative value for the firm as a result of high level of

investment in CA.

Even though the current findings are supported by the literature and theoretical aspects, as

decreasing level of CA as a percentage of TA yield to have higher MVA, in the

implementation by the firms, they should consider the liquidity as well as risk aspects. When

firms try to minimize the investment in CA, it causes to a lower level of liquidity, insufficient

stocks to run day today operations and lower level of debtors would result to decrease the

revenue. Finally, it leads to have a lower level liquidity and high level of operational risk to

the business. Therefore, it is worth to reduce the level of CA investment in such a way to have

proper balance between liquidity and risk associated with the business.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

367 www.globalbizresearch.org

4.2.2 Financing Policy (FP) and MVA

The second hypothesis of the study states that there is negative relationship between the

degree of aggressiveness of working capital management financing policy and MVA of the

companies in Sri Lanka. The regression model indicated a negative relationship between

working capital FP and MVA of the firm but relationship was not statistically significant at

5% level. Similar result was given by the Pearson’s correlation coefficients as FP has a lower

level negative correlation to MVA as -.129 (p= .013). According to the hypothesis, it explains

that the increase in FP measured by the ratio of CL/TA, leads to decrease the MVA of the

firm. On the other hand, the increase in CL/TA ratio means the degree of aggressiveness

Increases. Therefore, when degree of aggressiveness of the FP increases, the value of the firm

decreases. It further states that the relatively aggressive FP policy yields negative results of

MVA providing evidence that if the firms finance their TA more and more CL, leads to have

a lower level of MVA. Since the FP to MVA did not demonstrate a statistically significant

negative relationship, study rejected the hypothesis no 2 stated as “there is a negative

relationship between the degree of aggressiveness of working capital management financing

policy and MVA of the companies in Sri Lanka”.

According to the empirical studies, it has been concluded that there is no universally

applicable pattern in the FP and value of the firm. The FP is affected by the different

environmental conditions prevailed in different countries in different periods. It was further

confirmed by the present study findings that there was no linear negative relationship between

FP and MVA in Sri Lankan companies. One of the reasons that the negative relationship does

not exist in Sri Lankan market may be insufficiency of information to the investors about the

FP of the companies because of FP is more internally driven methodology while MVA is

more externally driven measurement tool.

5. Conclusion and Recommendation

Working capital management (WCM) is vital and an integral part in the financial

management which affects the profitability, liquidity, risk as well as the value creation.

Empirical research provided evidence that there is negative relationship between the degree of

aggressiveness of working capital investment and financing policies with the firm value,

stating that more aggressive working capital management is associated with higher

profitability leading higher value of the firm.

In the study of Working Capital Management Policy (WCMP) and firm value, Investment

Policy (IP) and Financing Policy (FP) were considered as independent variables. IP explains

the alternative ways in which a firm can invest their funds in assets, either in short term or in

long term. The minimal level of investment of the firm’s funds in current assets

comparatively to the fixed assets leads to the more aggressive IP. FP shows the way in which

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

368 www.globalbizresearch.org

a firm uses temporary funds to finance all of its temporary assets, along with some or even all

of its permanent assets. The minimum level of short term funds to finance temporary and

permanent assets leads to more conservative FP.

Market Value Added (MVA) which, was selected as dependent variable is important tool

to measure the Value of the firm. Market value is the difference between market value of the

firm’s stock and the amounts of equity capital supplied by investors. It measures the effect on

value of management’s decisions from the firm’s inception.

The study identified that the WCMP followed by the firms as IP and FP with the ratios of

Current Assets (CA) as a percentage of Total Assets (TA) and Current liability (CL) as a

percentage of TA respectively, and examined the relationship of those policies with EVA and

MVA. Moreover, researcher identified impact on firm size to the WCMP and firm value as

moderator variable. In addition to the main objectives of the study, based on the IP and FP of

the firms, researcher examined the relationship between the different WCM practices

followed by the firms as aggressive, conservative or moderate with value of the firm.

The study used the sample of 74 listed companies including 370 firm year observations taken

over the last five year period from 2009 to 2014 representing seven different business sectors

in the Colombo Stock Exchange (CSE).

According to the correlation analysis taking all the sample companies together, recorded a

negative relationship between IP and MVA. Similar results were given from the sector-wise

correlation analysis. According to the sector-wise correlations, all the sectors’ IP recorded

significant negative relation to MVA, but provided insignificant negative relationship

between FP and MVA. Similarly, sector-wise correlation between FP and MVA was negative.

Results given by the regression analysis showed that the relationship between IP and MVA

was significant and results between FP and MVA were not significant. Regression results

derived for the different sectors did not deviate from the overall regression results. According

to the examination of sector-wise impact on MVA, study revealed that there is no significant

impact of the different sectors on the overall results.

According to the statistical evidence supported by the correlation and regression analysis,

researcher failed to reject the hypothesis no. 1(H1) which stated that there is a negative

relationship between the degree of aggressiveness of IP with MVA. Accordingly, researcher

concluded that the firms can maximize MVA by investing their minimum level of funds in

current assets compared to non-current assets. It proves the relatively aggressive WCM IP

gives higher MVA. Further, H2 states that there is a negative relationship between the degree

of aggressiveness of IP to MVA. The results do not provided sufficient statistical evidence to

accept the hypotheses no. 2 (H2). Therefore, researcher does not have enough evidence to

declare that the firms can improve their MVA by financing their assets with the short term

funds. Furthermore, there is no sector-wise impact from the overall sample. Sector-wise

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

369 www.globalbizresearch.org

regression and correlation analysis of WCMP and firm value also provided the similar results

to overall sample correlation and regression results. It proved that there were no significant

sector- wise differences in the findings.

The first conclusion derived from the study is, the firms that are running with an

aggressive IP i.e. maintaining lower level CA as a percentage of TA, can improve their MVA.

Finally, the firms which followed MWCMP can improve the MVA of the listed non-financial

companies in Sri Lanka. Further, by analysing the different WCM practices used by the firms,

researcher identified that firms following MWCMP can improve the MVA compared to the

CWCMP.

In view of the above facts, the study reveals that the firms with an aggressive working

capital investment policy lead to improve the MVA. Therefore, firms with minimum level of

investment in CA in such a way to have enough liquidity to run day to day operations, can

improve the MVA.

References

Afza, T & Nazir, M. S., 2007, Working Capital Management Policies of Firms: Empirical Evidence

from Pakistan. Presented at 9th South Asian Management Forum (SAMF) on February 24-25, North

South University, Dhaka, Bangladesh.

Afza, T. & Nazir, M. S., 2008. Is it better to be Aggressive or Conservative in managing working

capital? COMSATS Institute of Information Technology, M.A. Jinnah Campus, Lahore, Pakistan.

Agarwal, N. K., 1977. Management of working capital. Phd. diss., Delhi School of Economics.

Akinwande, G.S., 2009. Working capital management in telecommunication sector. Business Analyst,

37 (2): 24–32.

Ali Uyar, 2009. The Relationship of Cash Conversion Cycle with Firm Size and Profitability: An

Empirical Investigation in Turkey. International Research Journal of Finance and Economic, Issue 24

(2009).

Asogwa, R. C., 2009. Measuring the determinant of value creation for publicly listed banks in Nigeria:

A Random effect profit (REP) model analysis. African review of money, banking and finance, 23(2),

231-268.

Bao, B. H. & Bao, D. H., 1998. Usefulness of Value Added and Abnormal Economic Earnings: An

Empirical Examination. Journal of Business Finance and Accounting, 25, 1- 2: 251-265.

Baum, C.F. Äafer, D. Sch & Talavera, O., 2006, The Effects of Short-Term Liabilities on Profitability.

Department of Economics, Boston College, Research Department of the Deutsche Bundesbank.

Baum, C.F. Äafer, D. Sch & Talavera, O., 2007. The Effects of Short-Term Liabilities on Profitability.

A Comparison of German and US Firms. The effect of short-term Liabilities on Profitability: A

comparison of Garman and US firms; Journal of Financial and Strategic Decision, 14(2): 16-17.,

Biddle, G., Bowen, R., & J. Wallace. , 1997. Does EVA beat earnings? Evidence on the associations

with stock returns and firms values. Journal of Accounting and Economics, 24, 301-306.

Brigham, E. & Daves, P. 2007. Intermediate Financial Management, 9th edition, Mason, OH:

Thomson Learning.

Brigham, E. F. & M.C. Ehrhardt, 2004. Financial Management: Theory and Practice (11th

Edition).

New York: South-Western College Publishers.

Carpenter, M. D. & K. H. Johnson, 1983. The Association between Working Capital Policy and

Operating Risk. The Financial Review, 18(3): 106-106.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

370 www.globalbizresearch.org

Christopher, F. B., Dorothea, S. & Oleksandr, T. (2006). The effect of short-term Liabilities on

Profitability; Journal of Financial and Strategic Decision, 12(4): 14-15.

Damon, W. W., & Schramm, R., 1972. A simultaneous decision model for production, marketing and

finance. Management Science, 19(2), 161-172.

De Wet, 2005. EVA versus traditional accounting measures of performance as drivers of shareholder

value – A comparative analysis, Meditari Accountancy Research, Vol. 13 No. 2 2005: 1-16.

Deloof, M., 2003. Does Working Capital Management Affect Profitability of Belgian Firms? Journal

of Business, Finance and Accounting, 30(3&4): 573-587.

Drucker, P., 1995. “The information executives truly need”. Harvard Business Review, (January-

February), 54-62.

Drucker, P., 1998. The Information Executives Truly Need to Know, in Harvard Business Review on

Measuring Corporate Performance, Boston: Harvard Business School press.

Eljelly, A.M.A. 2004. Liquidity-Profitability Tradeoff: An Empirical Investigation in an Emerging

Market. International Journal of Commerce & Management, 14(2): 48-61.

Emery, D.R. Finnerty, J.D. & Stowe, J., 2004. Corporate financial management. Upper Saddle River,

NJ: Prentice Hall.

Enyi, P. 2007. A Comparative Analysis of the effectiveness of three solvency management models.

AAFM Journal .Volume 7, pp. 122-141.

Evans, H.M. 1998. Discussion on Working Capital Management. Brierly Jones Nigeria Limited, Lagos.

Fazeeria, R., 2002. Working capital policy in India. Business Analysis, May: 15–20.

Filbeck, G. & Krueger, T., 2005. Industry Related Differences in Working Capital Management. Mid-

American Journal of Business, 20(2): 11-18.

Finegan, P.T., 1991. Maximizing shareholder value at the private company. Journal of Applied

Corporate Finance, 23(2): 51-69.

Garcia-Teruel, P. & Martinez-Solano, P, 2007. Effects of working capital management on SME

profitability. International Journal of Managerial Finance, 3,164-177.

Gardner, M. J., Mills, D. L., & Pope, R. A., 1986. Working Capital Policy and Operating Risk: An

Empirical Analysis. The Financial Review, 21(3): 31-31.

Ghosh, A & Ghosh, S (2003). Do Leverage, Dividend Policy and Profitability influence the Future

Value of Firm? Evidence from India. The Management Accountant, 32(4):256-287.

Ghosh, S. K. & Maji, S. G., 2004. Working Capital Management Efficiency: A Study on the Indian

Cement Industry. The Management Accountant, 39(5): 363-372.

Gitman, L. A., 2005. Principles of Managerial Finance (11th

Edition). New York: Addison Wesley

Publishers.

Gombola, M. J. & Ketz, J. E., 1983. Financial Ratio Patterns in Retail and Manufacturing

Organizations. Financial Management, 12 (2): 45-56.

Grant, J.L. 1996. Foundations of EVATM for investment managers. The Journal of Portfolio

Management, 23, Fall: 41-45.

Gregory T. Fraker., 2006, Using Economic Value Added (EVA) to Measure and Improve Bank

Performance; Financial Practice and Education, 10(1): 34–39

Gujarati,D.N. & Sangeetha 2007, Basic Econometric, The Mcgraw-hill companies.

Gupta, M. C. 1969. The Effect of Size, Growth and Industry on the Financial Structure of

Manufacturing Companies. Journal of Finance, 24(3): 517-529.

Haitham Nobanee & Maryam AlHajjar 2005, Model of Working capital management on empirical

grounds’. Department of Banking and Finance, The Hashemite University ,Global Journal of Finance

and Management ,Volume 1, Number 1,(2009), pp. 21–31.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

371 www.globalbizresearch.org

Hall, J.H., 1998. Variables determining shareholder value of industrial companies listed on the

Johannesburg Stock Exchange. Doctoral thesis, University of Pretoria, Pretoria.

Hall, J. H. 2000. Dissecting EVA: The Value Drivers determining the shareholders’ value of Industrial

companies. Department of Financial Management, University of Pretoria, Pretoria.

Hampton, J. J. & Wagner, C. L. 1989. Working capital management. New York, NY: Wiley.

Harris, A. 2005. Working Capital Management: Difficult, but Rewarding. Financial Executive, 21(4):

52-53.

Hill, N. C. & Sartoris, W .L. 1992. Short-term financial management: text and cases (2nd ed.). New

York, NY: Maxwell Macmillan International.

Howorth, C. & Westhead, P. (2003). The Focus of Working Capital Management in UK Small Firms.

Management Accounting Research, 14(2): 94-111.

Igben, R. O. 1999. Financial Accounting Made Simple, (first edition) ROI publisher, Lagos.

Jeng-Ren Chiou et.al. 2006. The Determinants of Working Capital Management. The Journal of

American Academy of Business, Cambridge Vol. 10 Num. 1 September 2006.

Jose, M. L., Lancaster, C. & Stevens, J. L. 1996. Corporate Returns and Cash Conversion Cycle,

Journal of Economics and Finance, 20(1): 33-46.

Kieschnick, 1960.Working Capital Management, Access to Financing, and Firm Value. Sloan

Management Review 27, 15-24.

Lamberson, M. (1995). Changes in Working Capital of Small Firms in Relation to Changes in

Economic Activity. Mid-American Journal of Business, 10(2): 45-50.

Lazaridis, I. & Tryfonidis, D. 2006, Relationship between working capital management and

profitability of listed companies in the Athens Stock Exchange. Journal of Financial Management and

Analysis, 19 (1): 26–35.

Lo, N. 2005. Go with the flow. http://www.cfoasia.com/archives/200503-02.htm.

Long, M. S., Malitz, I. B., & Ravid, S. A. 1993. Trade Credit, Quality Guarantees, and Product

Marketability. Financial Management, 22: 117-127.

Maurice, G. & William R., 1971. A dictionary of Statistical terms, Hafner Publishing Company, New

York, and P.8.

Marshall, A. 1920. Principles of Economics, 8th Edition, 1990 Reprint, London:Macmillan.

Mclnness, J.S. 2000, Accounting for Change, Industry Week, vol. 247, no. 17, pp. 63–65.

Maxwell, C. E., Gitman, L. J. & Smith, S. A. M. (1998). Working Capital Management and Financial-

Service Consumption Preferences of US and Foreign Firms: A Comparison of 1979 and 1996

Preferences. Financial Practice and Education, 8(2): 46-52.

Mian, S. N. & Talat, A. 2009. Impact of Aggressive Working Capital Management Policy on Firms’

Profitability. The IUP Journal of Applied Finance, Vol. 15, No. 8, 2009 12: 112-124.

Milunovich, S. & A. Tsuei (1996). EVA in the Computer Industry. Journal of Applied Corporate

Finance, Vol 9 No. 1

Minton, B., & Schrand, C. 1999. The Impact of Cash Flow Volatility on Discretionary Investment and

the Costs of Debt and Equity Financing, Journal of Financial Economics, 54, 423-460.

Morawakage & Lakshan A.M.I 2009. Determinants of profitability underlining the working capital

management and cost structure of Sri Lankan companies. Department of Accountancy, University of

Kelaniya, Sri Lanka.

Moyer, R. C., McGuigan, J. R. & Kretlow, W. J., 2005. Contemporary Financial Management (10th

Edition). New York: South-Western College Publication.

O’Byrne, S.F., 1996. EVA and Market Value, Journal of Applied Corporate Finance, 9, 1: 116-125.

Olowe, R. A. 1997, Financial Management Concepts. Analysis and Capital Investment.

Omolumo, I. G., 1997. Financial Management and Company Policy. Omolum consult, Lagos.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

372 www.globalbizresearch.org

Osisioma, B. C., 1997. “Sources and Management of Working Capital”, Journal of Management

Sciences, Awka: Vol. 2. January.

Pandey, I. M. & Parera, K. L. W., 1997. Determinants of Effective Working Capital Management - A

Discriminant Analysis Approach. Research and Publication Department Indian Institute of

Management, Ahmedabad India.

Pinches, G.E., 1991. Essentials of Financial Management, 4th

Edition), New York: Harper Collins

College Division.

Ramachandran, A. & Janakiraman, M., 2009. The Relationship between Working Capital

Management Efficiency and EBIT.

Ramana, 2005). Market Value Added and Economic Value Added: Some Empirical Evidences.

International Review of Business Research, 3 2): 275–96.

Rappaport, A., 1998. Corporate Performance Standards and Shareholder Value. The Journal of

Business Strategy, 4, 28-38.

Reason, T., 2008. Preparing your company for recession. Retrieved December, 2010 from

http://ezproxy.lincoln.ac.nz/login?url=http://proquest.umi.com/pqdweb?did=1423329

071&Fmt=7&clientId=18963&RQT=309&VName=PQD.

Rehman, A., 2006. Working Capital Management and Profitability: Case of Pakistani Firms

Unpublished Dissertation). Pakistan: COMSATS Institute of Information Technology Islamabad.

Robert, K., Mark, L. & Rabhi, M., 2008. Working Capital Management, Access to Financing, and Firm

Value. Journal of Applied Corporate Finance, 19, 2: 114-135.

Ruback, R. & Sesia, A., 2000. "Dell's Working Capital." Harvard Business School Case 201-029.

Saddle River, NJ: Prentice Hall.

Sagan, J. 1955). Toward a theory of working capital management. The Journal of Finance, 10 2): 121–

9.

Salawu, R.O., 2006. Industry Practice and Aggressive Conservative Working Capital Policies in

Nigeria. European Journal of Scientific Research, Vol.13 No.3 (2006), pp. 294-304.

Sartoris, W. L., Hill, N. C., & Kallberg, J. G., 1983. A Generalized Cash Flow Approach to Short-Term

Financial Decisions/Discussion. The Journal of Finance, 38(2), 349-360.

Scherr F. C., 1989, Modern Working Capital Management; Text and Cases. Prentice Hall, Englewood

Cliffs.

Schilling, G., 1996, Working capital's role in maintaining corporate liquidity. TMA Journal, 16(5), 4-7.

Sekaran, U., 1984. Research Methods for Business: A skilled building approach, John Wiley, New

York.

Shin, H. & Stulz, L., 2000 “Working Capital Management and Profitability,” Business Analyst, 34 (1):

25–43.

Shin, H. H. & Soenen, L., 1998. Efficiency of Working Capital and Corporate Profitability, Financial

Practice and Education, 8(2): 37–45.

Smith, K., 1980. Profitability versus Liquidity Trade-offs in Working Capital Management, in

Readings on the Management of Working Capital. New York: St. Paul, West Publishing Company.

Smith, M. B. & Begemann, E., 1997. Measuring Association between Working Capital and Return on

Investment. South Africa Journal of Business Management 28(1): 1-5.

Soenen, 1993. Investing excess working capital. Management Accounting, 71(9), 24-27.

Solomons, D., 1965. Divisional Performance: Measurement and Control, Homewood, IL: Irwin.

Soenen & Solano, 1993. Cash conversion cycle & corporate profitability. Journal of Cash Management

13(4): 53-58.

Stewart, G.B. III (1991). The quest for value. New York: Harper-Collins.

Stern, J. (1993). Value and people management. Corporate Finance, July: 35-37.

Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics (GJCRA)

An Online International Research Journal (ISSN: 2311-3162)

2015 Vol: 1 Issue 2

373 www.globalbizresearch.org

Stewart, G.B. (1994). EVA: Fact and fantasy, Journal of Applied Corporate Finance, vol. 7, no. 2, pp.

71–84.

Sushma, V. & Bhupesh, K., 2007. Working capital management policy and profitability in India.

Business Analyst, 29 (2): 17–28.

Teruel, P. J. G. & Solan, P. M., 2005. Effects of Working Capital Management on SME Profitability.

Working Papers Series. Universidad de Murcia, Campus Espinardo, Spain.

Trahan, E. A., & Gitman, L. J., 1995. Bridging the theory-practice gap in corporate finance: a survey of

chief financial officers. Quarterly Review of Economics and Finance, 35(1), 73-87.

Uyemura, D. G., Kanto, C. C., & Petit, J. M., 1996. EVA for Banks: Value Creation, Risk

Management, and Profitability Measurement, Journal of Applied Corporate Finance, 9, 2: 94-111.

Van Horne, J. C., 1969. Risk-return analysis of a firm working capital. The Engineering Economist, 14

(Winter): 71–89.

Van Horne, J. C. (1977). Financial Management Policy, Englewood Cliffs: Prentice Hall International.

Vander Weide, J. H. & Maier, S., 1985. Managing corporate liquidity: an introduction to working

capital management. New York, NY: Wiley.

Van-Horne, J. C. & Wachowicz, J. M. (2004). Fundamentals of Financial Management (12th

Edition).

New York: Prentice Hall Publishers.

Wadsworth, G. & Bryan, J., 1974. Applications of Probability and Random Variables, 2nd edition,

New York: McGraw-Hill.

Weinraub, H. J. & Visscher, S., 1998. Industry Practice Relating To Aggressive Conservative Working

Capital Policies. Journal of Financial and Strategic Decision 11(2): 11-18.

Weston, J.F. & Copeland, T. E. 1992. Managerial Finance. 9th edition. The Dryden Press, New York.

Yang, G., Ronald, R. J., & Chu, P., 2005. Inventory models with variable lead time and present value.

European Journal of Operational Research, 164(2), 358-366.

Young, D., 1999. Some Reflections on Accounting Adjustments and Economic Value- Added. Journal

of Financial Statement Analysis, 4, 2: 7-13.