Impact of Corporate Brands in Consumer Electronics and …€¦ · Impact of Corporate Brands in...

281

Impact of Corporate Brands in Consumer Electronics and Home Appliances Sector on its Extensions to Diversified Markets with special reference to L.G. Electronics India Thesis submitted to the Padmashree Dr. D.Y.Patil University, Department of Business Management in partial fulfillment of the requirements for the award of the Degree of DOCTOR OF PHILOSOPHY In BUSINESS MANAGEMENT Submitted by Mr. Mangesh Prasad Kasbekar (Enrollment No. DYP-PhD-086100007) Research Guide Prof. Dr. G.S. Monga PADMASHREE DR. D.Y.PATIL UNIVERSITY, DEPARTMENT OF BUSINESS MANAGEMENT, Sector 4, Plot No. 10, CBD Belapur, Navi Mumbai- 400614 August 2011

Transcript of Impact of Corporate Brands in Consumer Electronics and …€¦ · Impact of Corporate Brands in...

Impact of Corporate Brands in Consumer Electronics and Home Appliances Sector on its Extensions to Diversified Markets

with special reference to L.G. Electronics India

Thesis submitted to the Padmashree Dr. D.Y.Patil University, Department of Business Management

in partial fulfillment of the requirements for the award of the Degree of

DOCTOR OF PHILOSOPHY

In

BUSINESS MANAGEMENT

Submitted by

Mr. Mangesh Prasad Kasbekar

(Enrollment No. DYP-PhD-086100007)

Research Guide

Prof. Dr. G.S. Monga

PADMASHREE DR. D.Y.PATIL UNIVERSITY,

DEPARTMENT OF BUSINESS MANAGEMENT,

Sector 4, Plot No. 10,

CBD Belapur, Navi Mumbai- 400614

August 2011

Impact of Corporate Brands in Consumer Electronics and Home Appliances Sector on its Extensions to Diversified Markets with special reference to L.G. Electronics India

DECLARATION

I hereby declare that the thesis entitled, “Impact of Corporate Brands in

Consumer Electronics and Home Appliances Sector on its Extensions to

Diversified Markets with special reference to L.G. Electronics India”

submitted for the Award of Doctor of Philosophy in Business Management at the

Padmashree Dr. D.Y.Patil University Department of Business Management is my

original work and the thesis has not formed the basis for award of any degree,

associate ship, fellowship or any other similar titles

Place: Navi Mumbai

Date:

Signature of the Guide Signature of the Signature of the Student Head of the dept.

CERTIFICATE

This is to certify that the thesis entitled “Impact of Corporate Brands in

Consumer Electronics and Home Appliances Sector on its Extensions to

Diversified Markets with special reference to L.G. Electronics India” and

submitted by Mr. Mangesh Prasad Kasbekar is a bonafide research work for

the award of the Doctor of Philosophy in Business Management at the

Padmashree Dr. D. Y. Patil University Department of Business Management in

partial fulfillment of the requirements for the award of the Degree of Doctor of

Philosophy in Business Management and that the thesis has not formed the

basis for the award previously of any degree, diploma, associate ship, fellowship

or any other similar title of any University or Institution. Also certified that the

thesis represents an independent work on the part of the candidate.

Place: Navi Mumbai

Date:

Signature of the Signature of the GuideHead of the department

ACKNOWLEDGEMENT

I am indebted to the Padmashree Dr. D.Y. Patil University, Department of

Business Management, which has accepted me for the Doctorate program and

provided me with an excellent opportunity to carry out the present research

project.

I would like to express my sincere thanks to my guide Dr. G S Monga for his

assistance, encouragement and for spending necessary hours during this

research study. It was his constant inspiration that kept me together all the time

and work continuously towards achieving a high quality of work.

This thesis wouldn’t have been completed without the support, guidance, and

blessings of Dr. R. Gopal. He has helped me during my tough times even at odd

hours. Dr. Monga and Dr. Gopal, both have shaped me first as a better

researcher, and inducted me into the process of writing a good quality research.

I would specially like to mention Mr. Amol Koparkar from LG India for his

immense contribution. I thank all my faculty colleagues especially to Mrs.

Madhumita Patil, CEO, Chetana Institute of Management for their constant

support and motivation. I would like to take the privilege to thank Dr. Pradeep

Manjrekar for his valuable inputs. Finally I would like to thank my family for their

immense support and love without which this thesis wouldn’t have been

completed.

Place: Navi Mumbai

Date: Signature of the student

This thesis is dedicated to my family

CONTENTS

Chapter No.

Title Page No.

List of Abbreviations

List of Tables

List of Figures

Executive Summary

1 Introduction 1

1.1 Introduction & Background 2

1.2 Brand Architecture 4

1.3 Introduction to Corporate Brands 7

1.3.1 Corporate Brands vis-à-vis Product Brands 8

1.4 Introduction to Brand Extensions 14

1.5

Corporate Brand Extension 17

2 Review of Literature

20

2.1Brand Extension Literature: Definition, Benefits, Drawbacks

21

2.2 Concepts for evaluating Brand Extensions

25

2.3Influence of Brand extension on the Parent brandand vice-versa

29

2.4 Consumer’s Attitude towards Brand Extension 34

2.5Corporate Brand Literature: Definition, Measure,Associations

35

2.6 Perspectives of Brand Equity 39

2.7Leveraging the Corporate Brands & ChallengesInvolved

52

2.8 Dimensions of Corporate Branding 55

2.9 Corporate Brand Extensions 57

2.10 Research Gap 60

3

Purpose, Objectives, Hypotheses of the Study 62

3.1 Purpose of the study 63

3.2 Objectives of the study 65

3.3

Hypotheses 67

4 Research Methodology

70

4.1 Research Design 71

4.2 Primary and Secondary Research 79

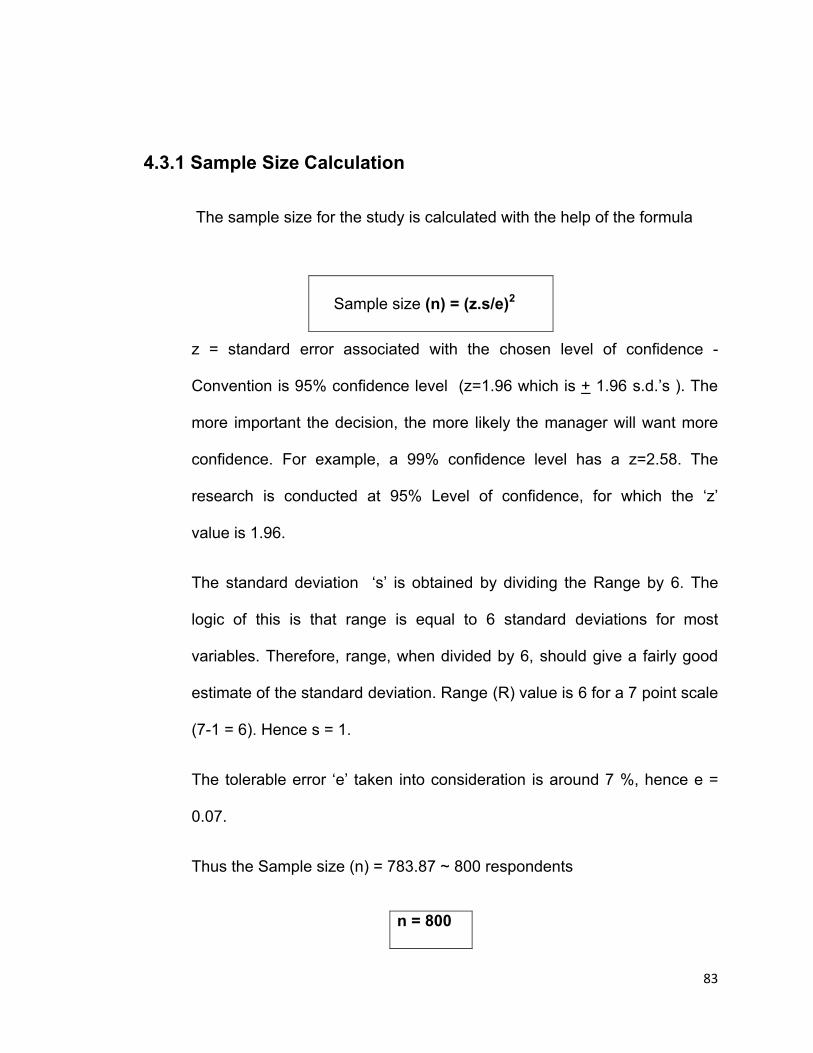

4.3 Sampling Design & Demographics 80

4.4 Data Collection Tool (Focus Group & Questionnaire Design)

84

4.5 Pilot Testing 91

4.6

Survey 95

5Consumer Electronics and Home AppliancesIndustry

96

6 Case Study - LG Electronics India 114

6.1 LG Electronics India as a Case 115

6.2 Overview of LG Electronics India 116

6.3 Hypothetical Extensions for LG 124

6.4 Market Scenario of New Product Categories

125

7

Data Findings & Analysis

130

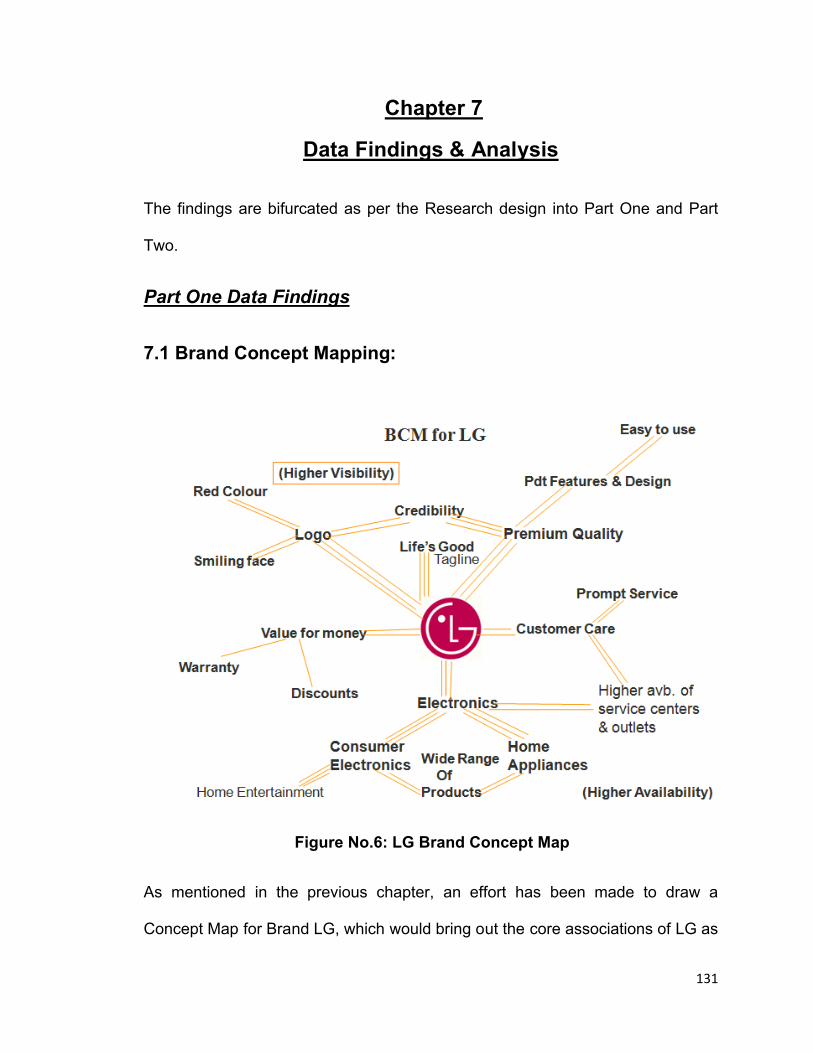

7.1 Brand Concept Mapping 131

7.2 Attribute association matching 133

7.3 Rating of Core Association 133

7.4

Demographics for the survey 134

7.5 Corporate Brand Strength Parameters 136

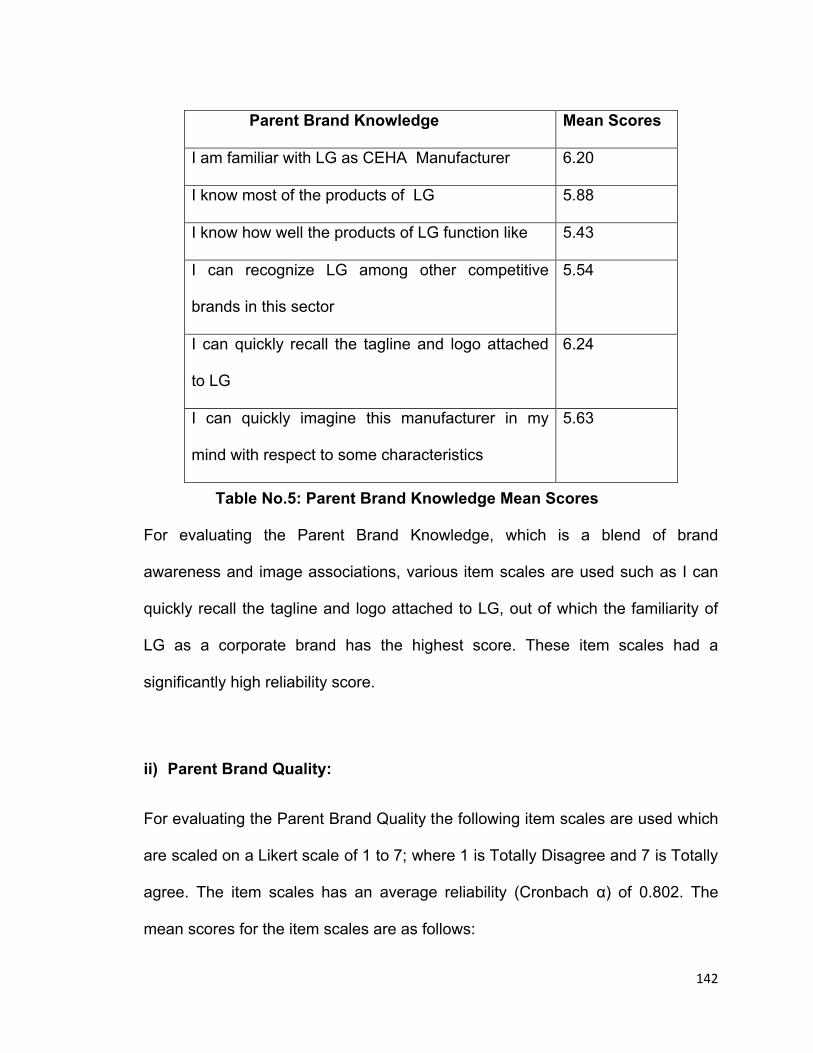

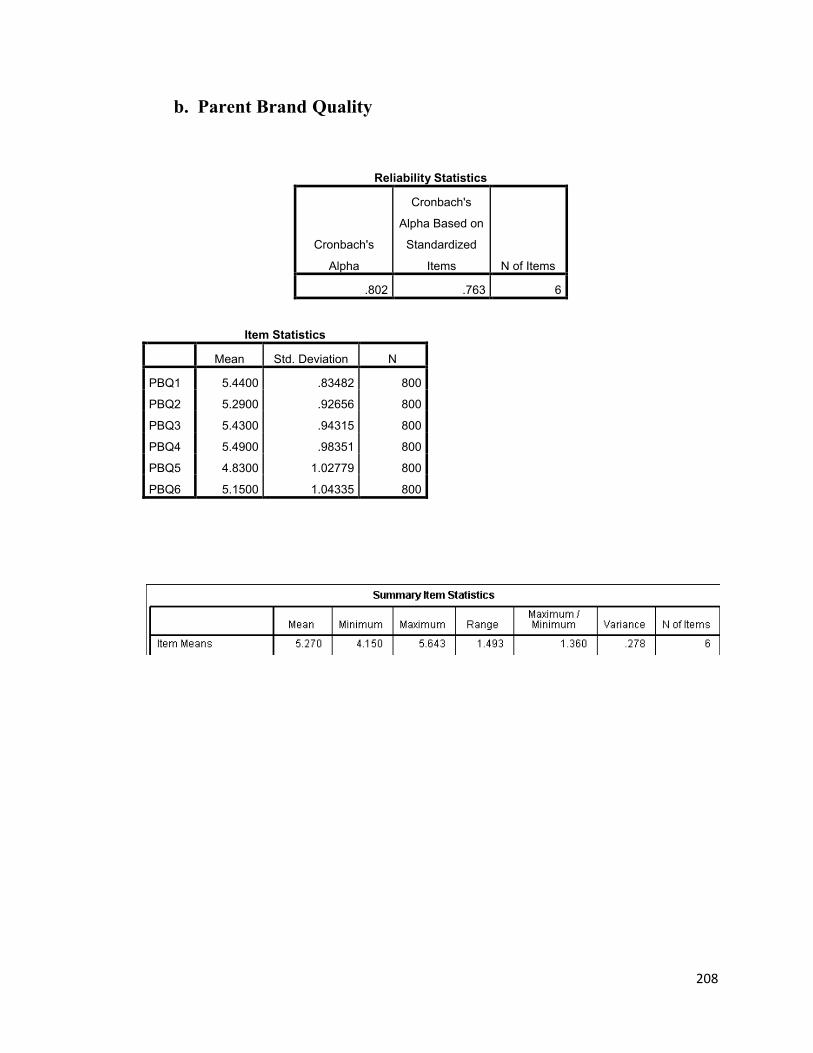

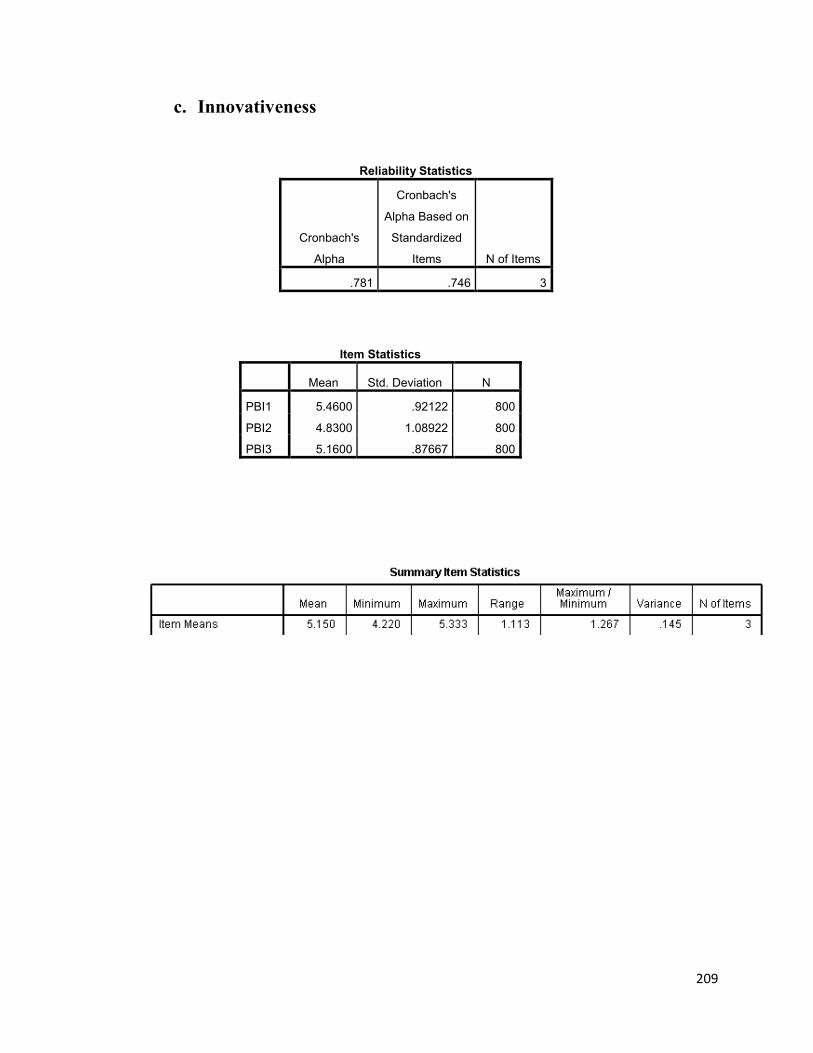

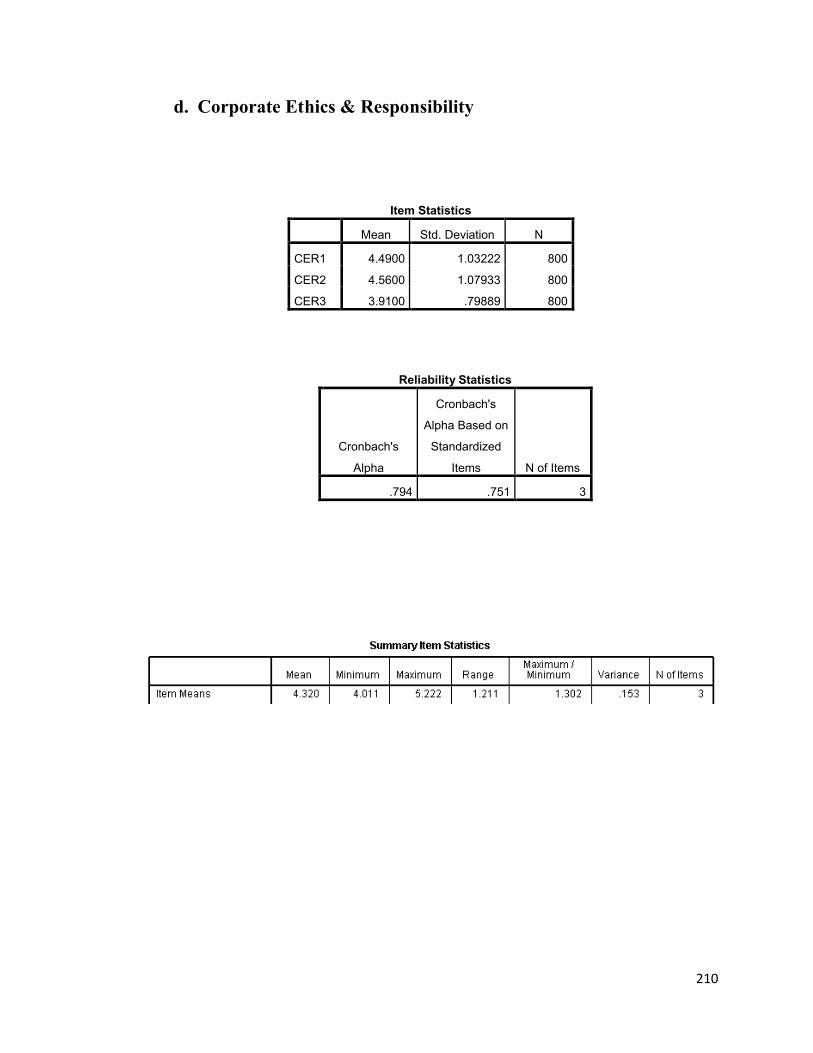

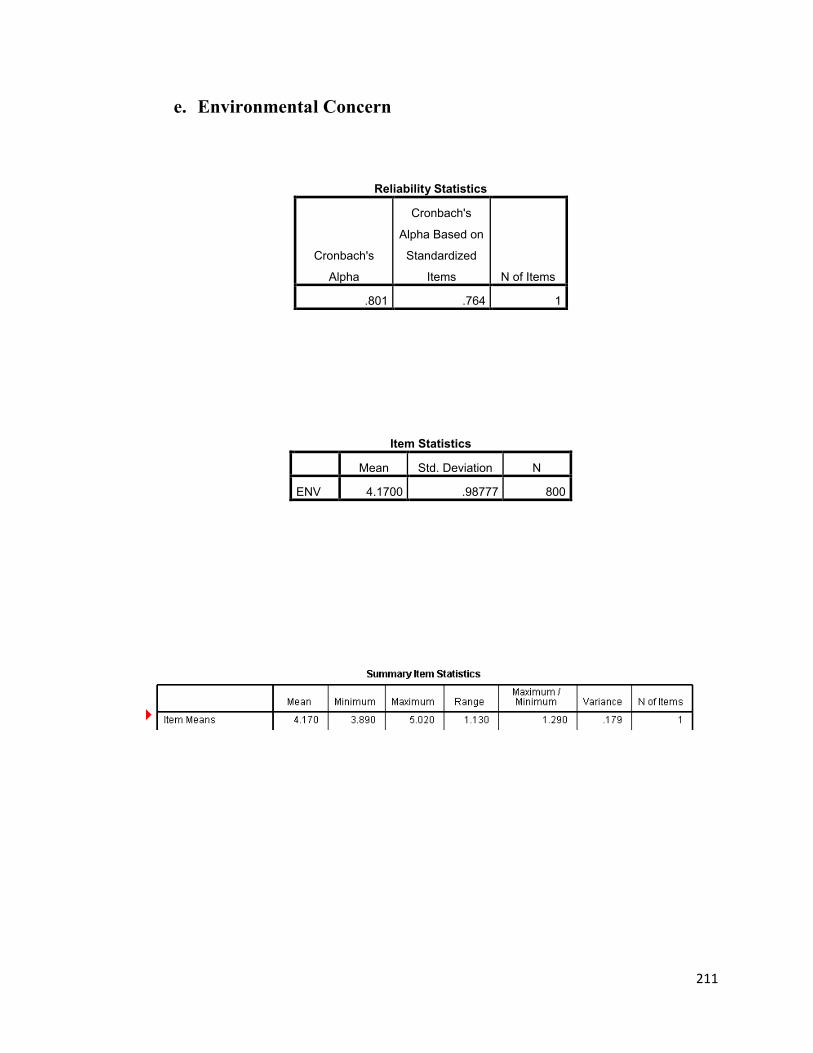

7.6.1 Parent Brand Characteristics Evaluation 141

7.6.2

Extension Characteristics Evaluation of the Parent Brand 146

7.6.3

Parent Brand & Extension Scores 147

7.7Overall Model Summary for ATBE of LG to Hypothetical extensions

148

7.8 Hypothesis Testing Results 151

7.9Attitude Towards Brand Extension Scores for new product categories

154

7.10 Attitude towards the products of LG 155

7.10.1 Range of Attitude Scores of LG 156

7.11 Range of Attitude scores and Hypothetical Extensions

157

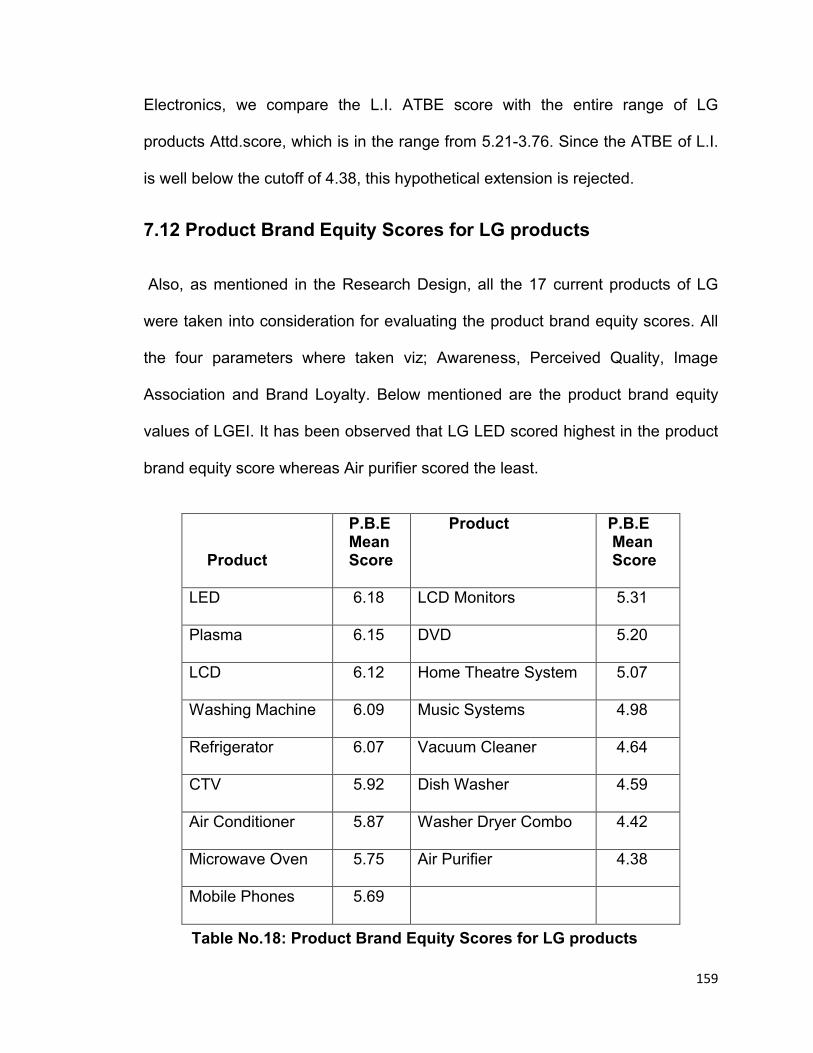

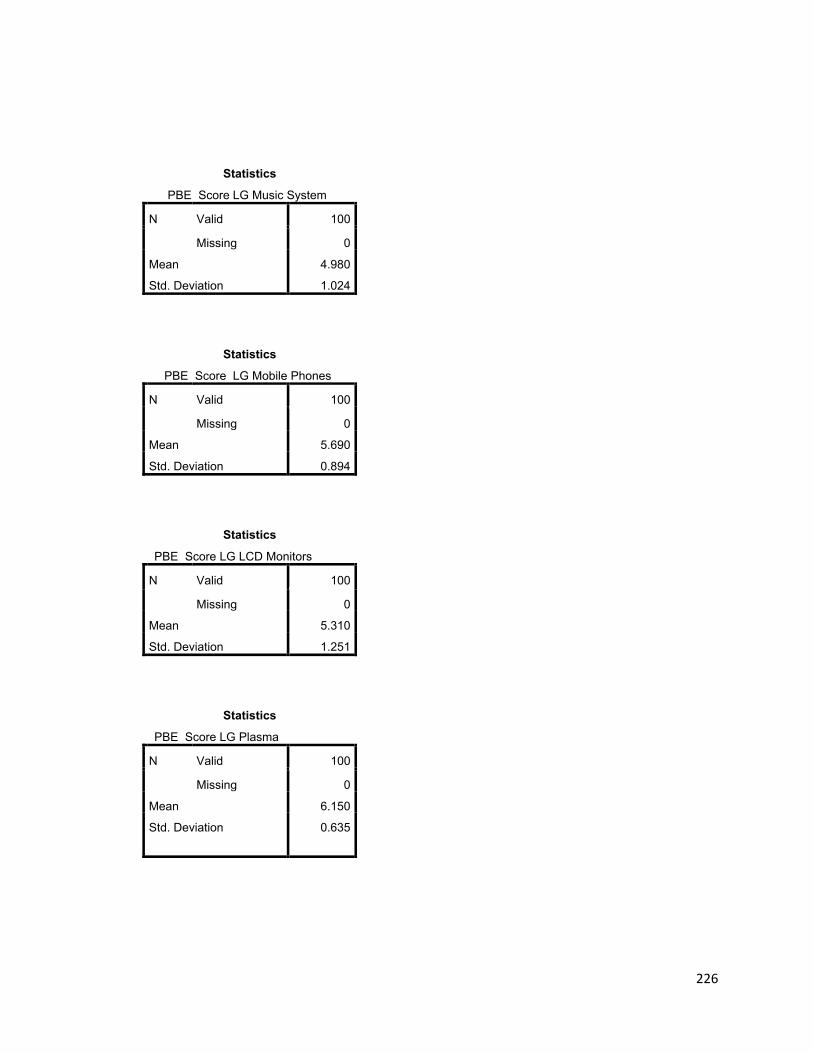

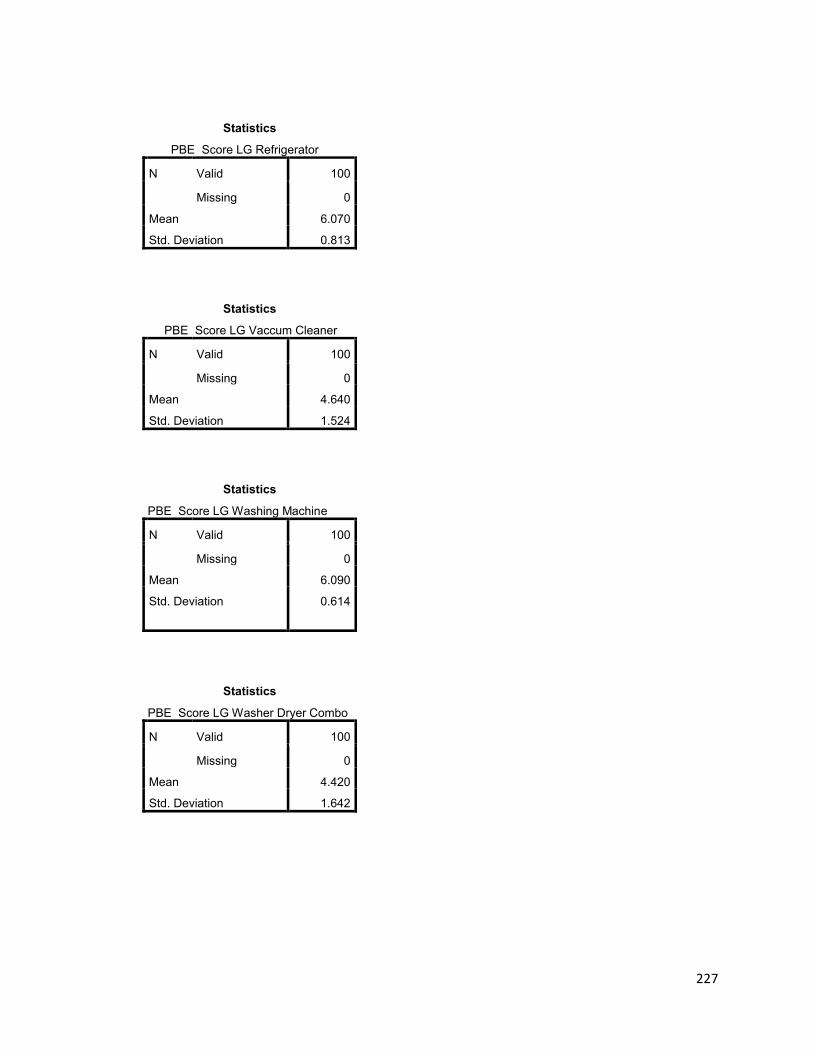

7.12 Product Brand Equity Scores for LG products 159

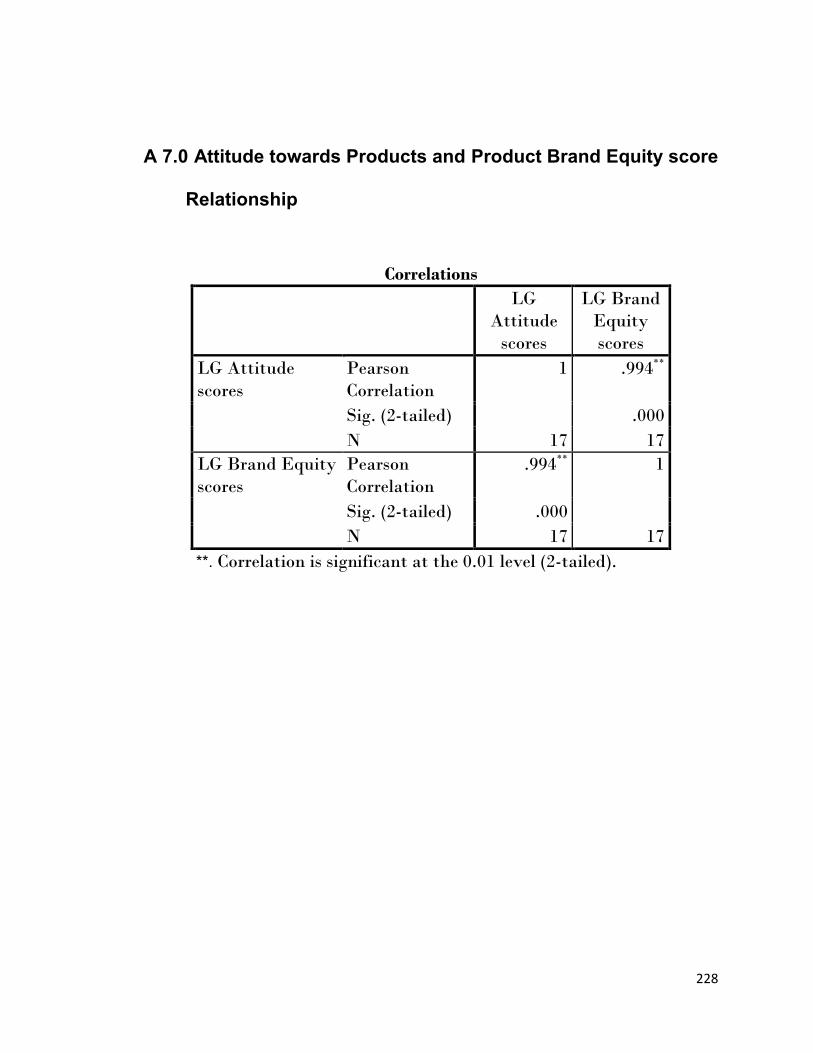

7.13Attitude towards Product and Product Brand Equity Relationship

160

8 Conclusion 161

9 Limitations and Future scope of study 164

10

Suggestions & Recommendations 166

Bibliography 171

Annexure: i) SPSS Output ii) Questionnaires 202- 248

Appendix 249

List of Abbreviations

LGEI LG Electronics India

CEHA Consumer Electronics and Home Appliances

DTH Direct to Home Services

MSP Mobile Service Provider

ISP Internet Service Provider

WP Washing Powder

L.I Life Insurance

ATBE Attitude towards Brand Extension

CBS Corporate Brand Strength

CTV Colour Television

HTS Home Theatre System

LED Light Emitting Diodes

LCD Liquid Crystal Display

List of Tables

Table No.

Content Page No.

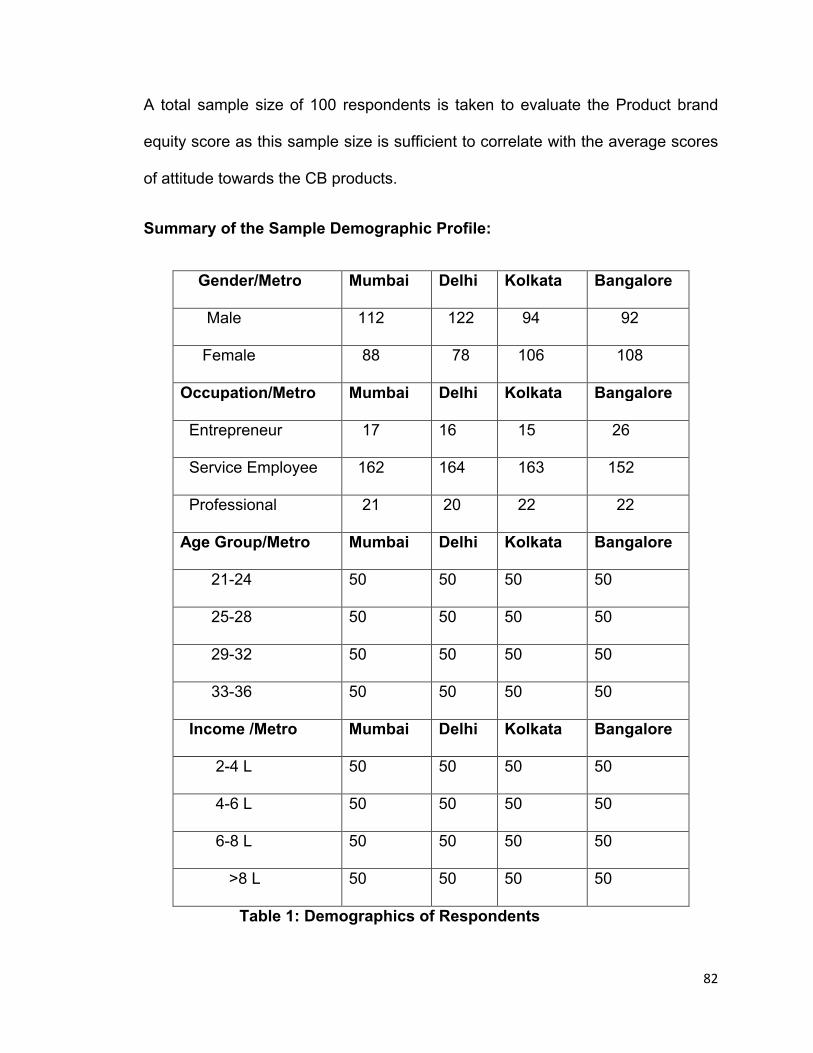

1 Demographics of Respondents 82

2 Corporate Brand Positioning Mean Scores 138

3 Corporate Brand Identity Mean Scores 139

4 Corporate Brand Perceived Quality Mean Scores

140

5 Parent Brand Knowledge Mean Scores 142

6 Parent Brand Quality Mean Scores 143

7 Parent Brand Innovativeness Mean Scores 144

8 Corporate Ethics & Responsibility Mean Scores 145

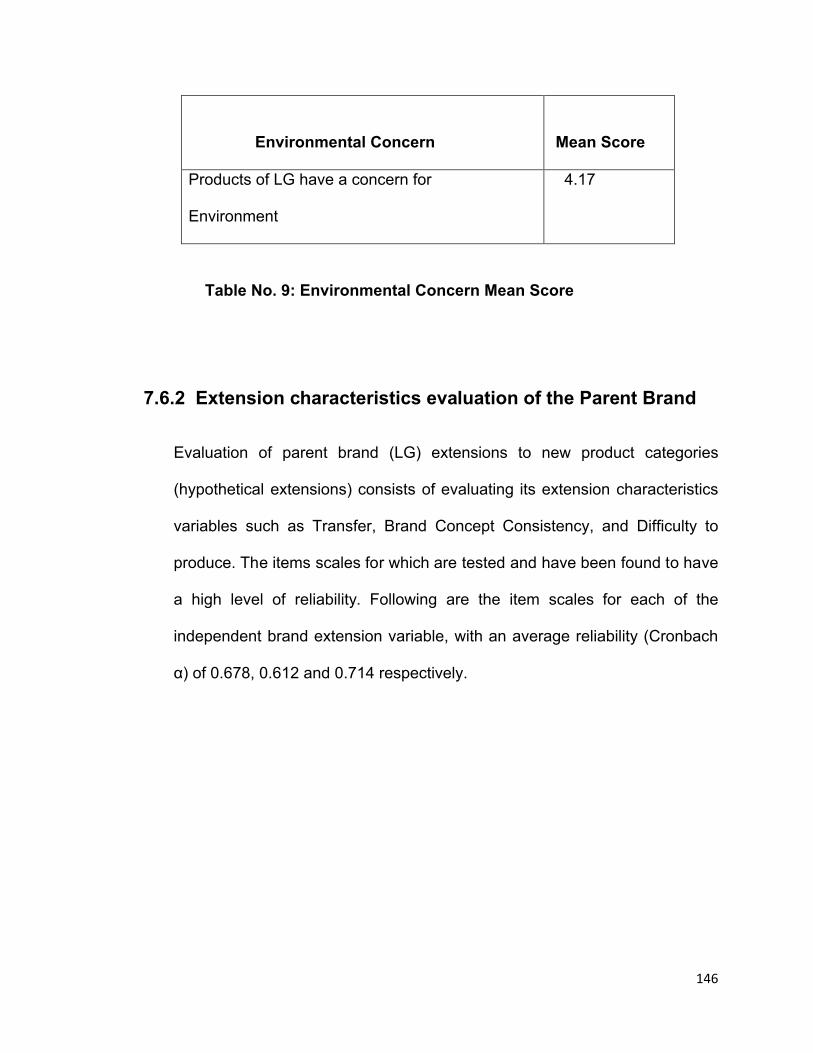

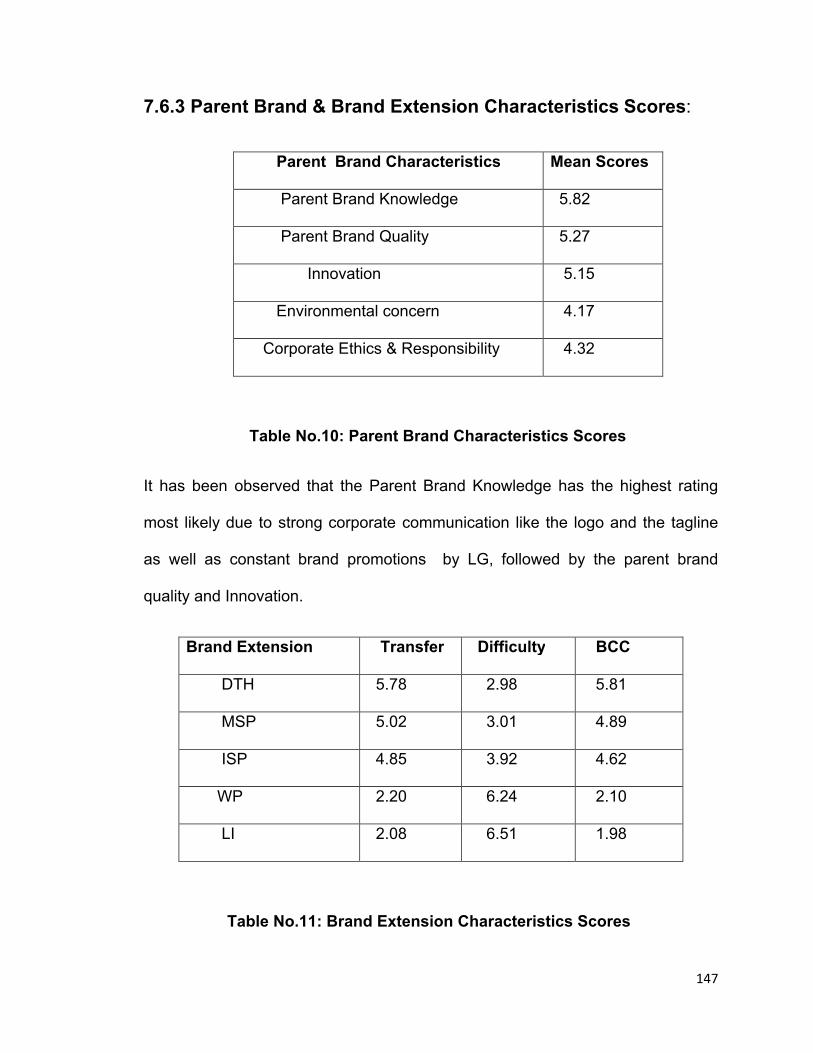

9 Environmental Concern Mean Score 146

10 Parent Brand Parameters Mean Scores 147

11 Brand Extension Parameters Mean Scores 147

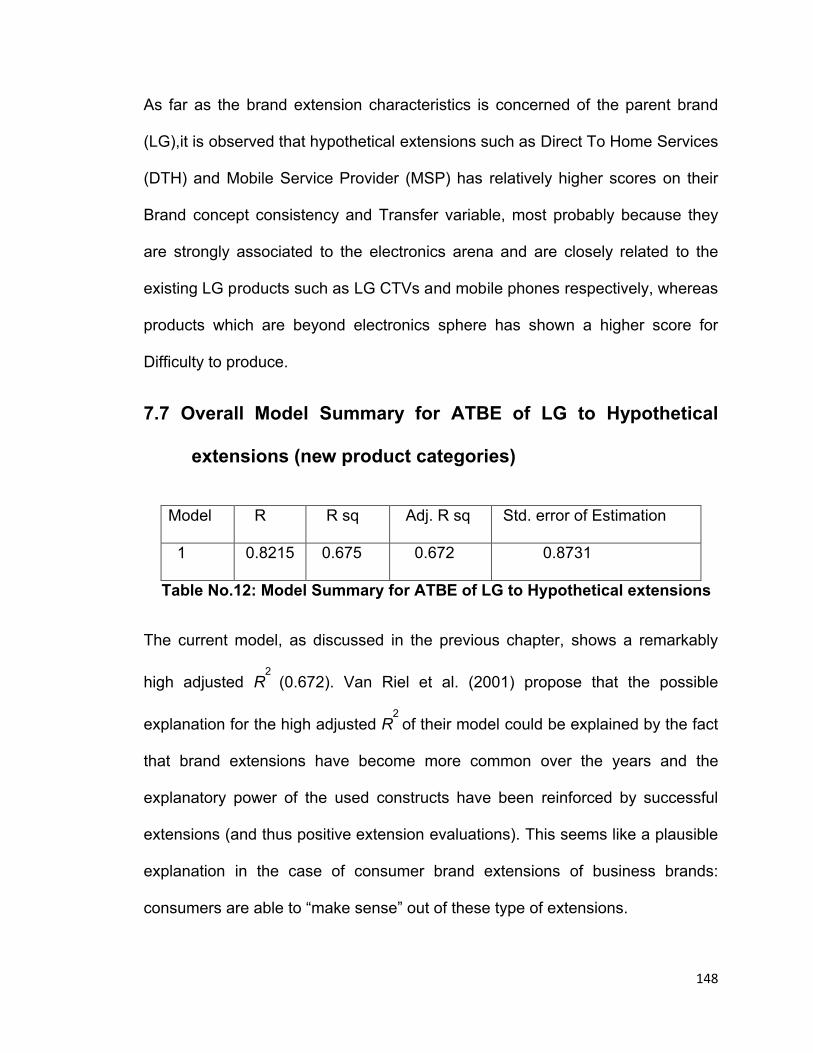

12 Model Summary for ATBE to Hypothetical extensions 148

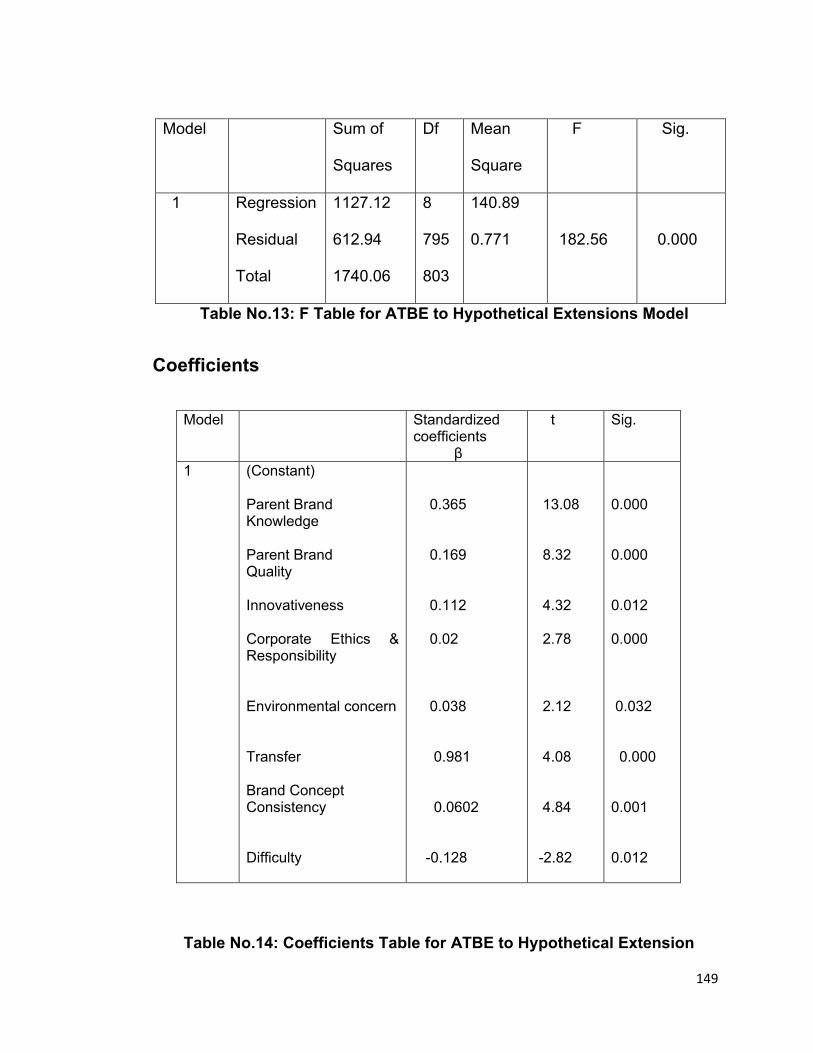

13 F Table for ATBE to Hypothetical Extensions Model 149

14 Coefficients Table for ATBE to Hypothetical Extensions

149

15 Hypothetical Extension Mean Scores 154

16 Attitude Scores of LG products 155

Table No.

Content Page No.

17 Range of Attitude Scores 156

18 Product Brand Equity Scores for LG products 159

19 Attitude and Product Brand Equity Correlation 160

Annexure

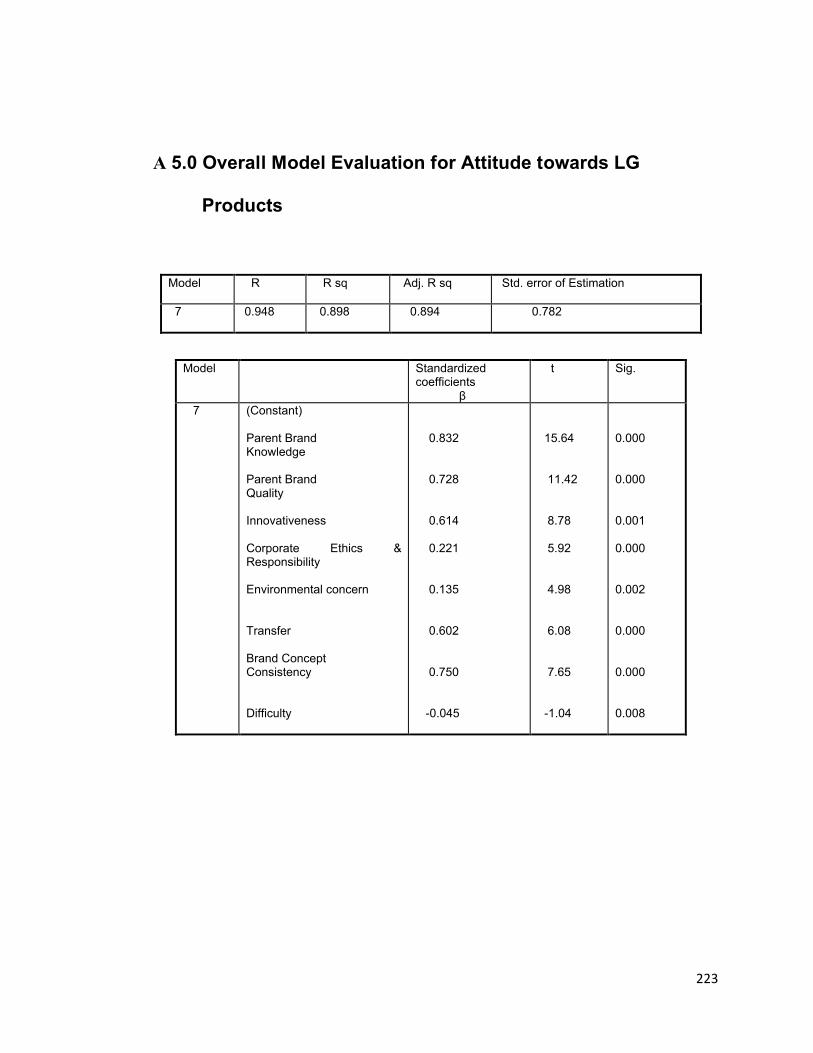

A 4 Model Evaluation for Individual Hypothetical

Extensions

218

A 5 Overall Model Evaluation for Attitude towards LG

Products

223

List of Figures

Figure No.

Content Page No.

1 Brand Equity Evaluation System 44

2 Indian Consumer Durable Industry Segment 98

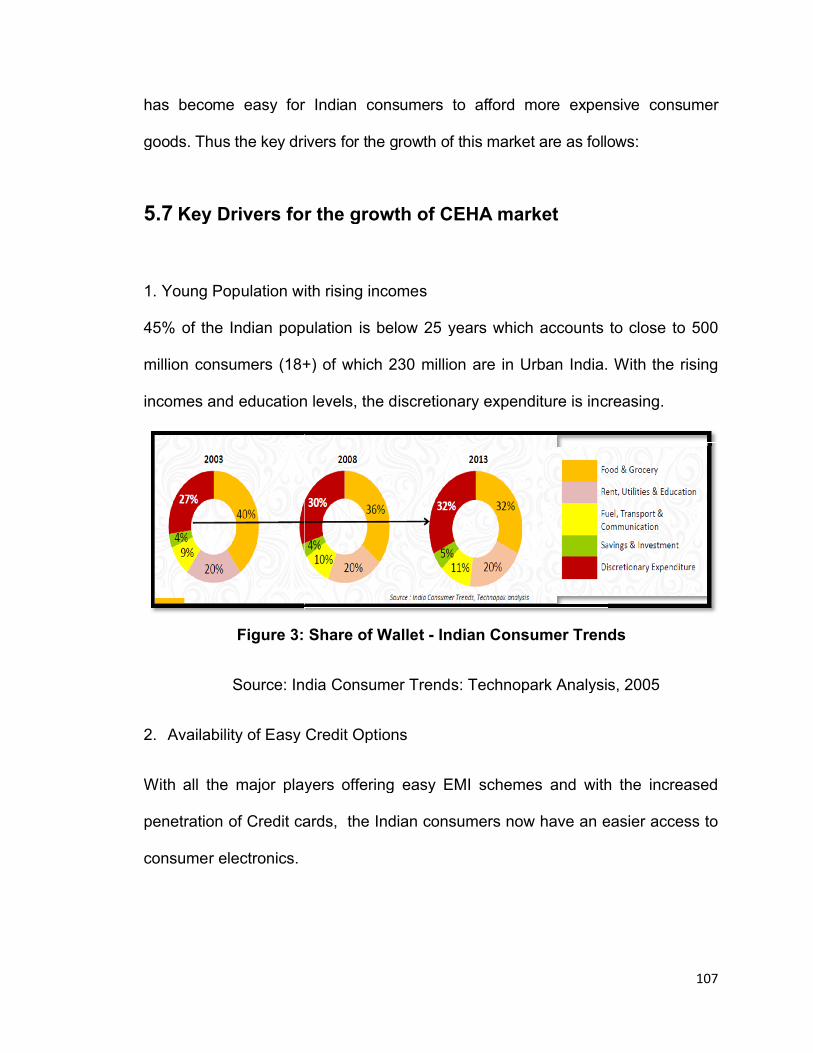

3 Share of Wallet - Indian Consumer Trends 107

4 LG India Financial Performance 118

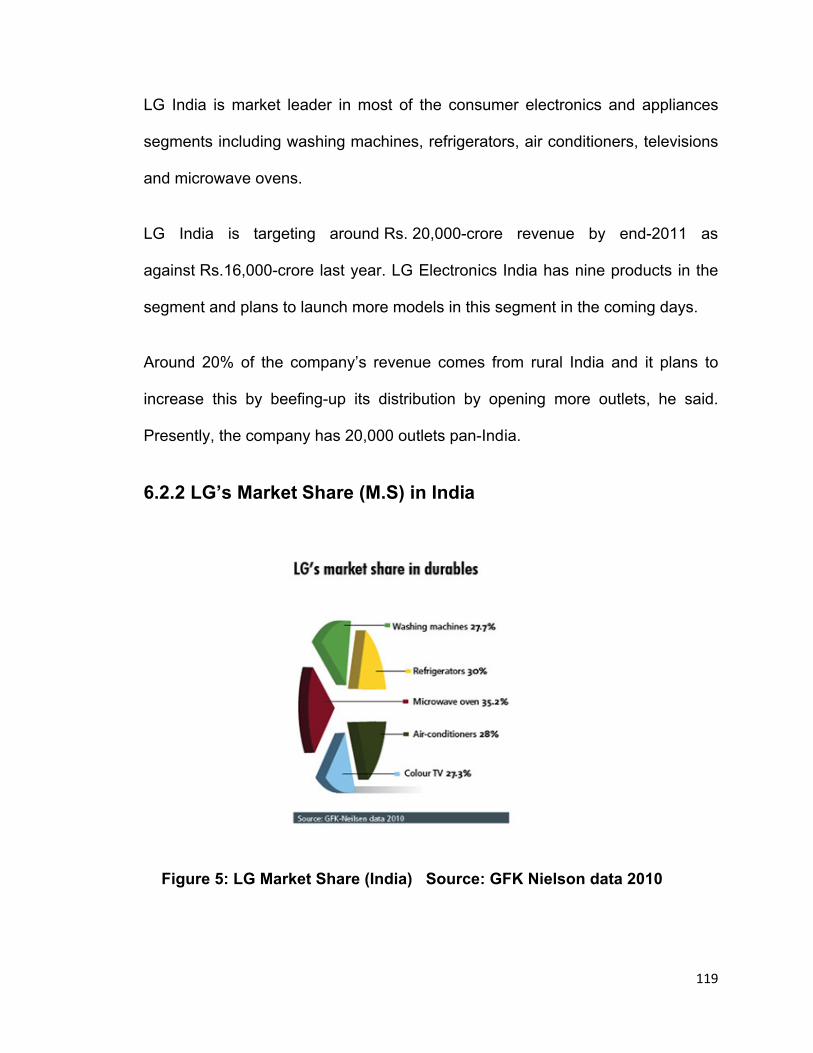

5 LG India Market Share 119

6 LG Brand Concept Map 131

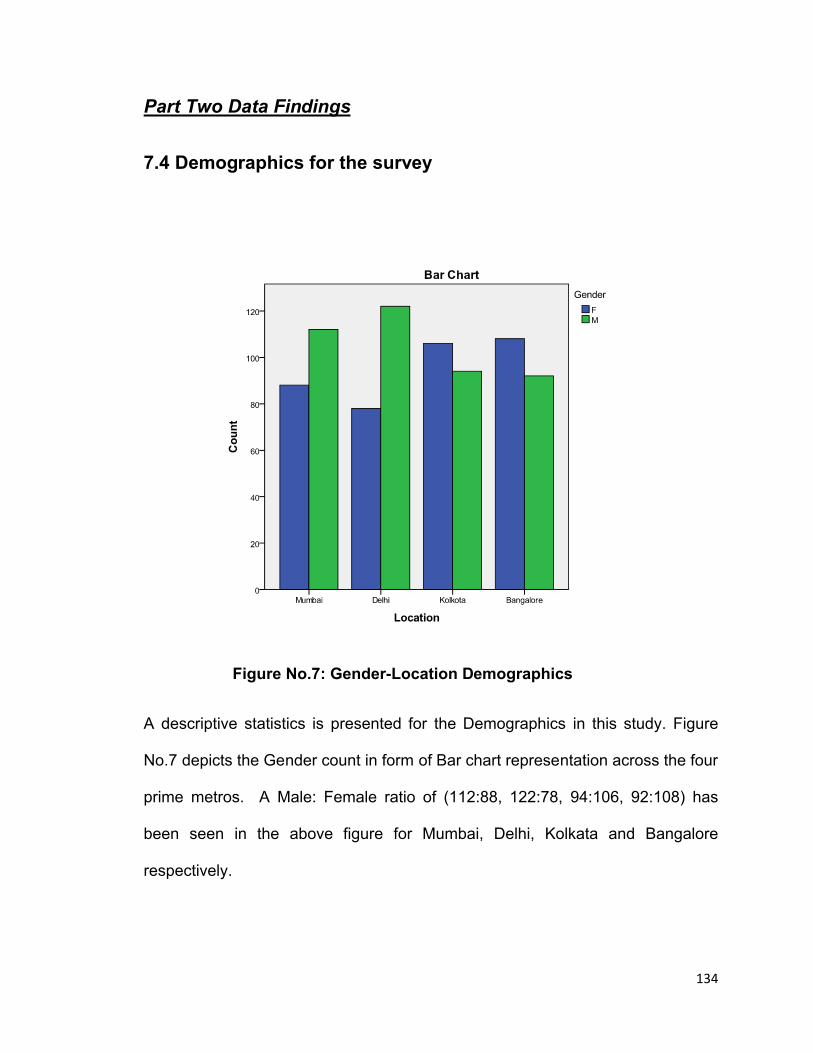

7 Gender-Location Demographics 134

8 Occupation-Location Demographics 135

Executive Summary

Successful organizations all over the world recognize the importance of new

product launches as a means of organic growth and as a means to differentiate

themselves from others. At the same time, in an increasingly competitive

environment, it is not an easy task to create winning products. Considering the

high failure rate of new products, launching a new product is a risky proposition.

Brand marketers seek ways to achieve growth while reducing both the cost of

new product introductions as well as the risk of new product failure. A popular

way of launching new products has therefore been to leverage the equity of an

existing brand into a new sector, market, or product category popularly called as

Brand extension.

According to Aaker when brands are managed separately and independently,

overall resources allocation among brands may be less than optimal (1996).

Therefore, having the corporate brand, or in other words cohesive brand

portfolio, instead of number of individual product brands, is more rational from the

company’s point of view.

Companies are increasingly taking their corporate brand into new and unrelated

business areas in order to capitalize on their brand equity.

Since it’s a matter of establishing an association with the corporate brand, also

observed as a parent brand in branded house strategy or Master brand

architecture, the core association of the corporate brand plays a pivotal role in

deciding the extension with respect to the associations consumers have

regarding the corporate brand. In case of unrelated categories diversifications

usually known as conglomerate diversification, the extent of the core association

of the corporate brand seems to be more difficult.

Thus the purpose of this research lays in identifying the extent of the Corporate

Brand stretch i.e.; to what extent a Corporate Brand can stretch itself.

Simultaneously the extent to which a new product category would leverage on

the core associations of the Corporate Brand. Finally analyzing the extent of it’s

stretch to new product categories on its brand equity.

The objectives of the research are:

1. To study the extent to which a Corporate Brand can stretch itself

2. To study the core association of the Corporate Brand

3. To identify the new product categories and study how far can they leverage

on the core association.

4. To establish a relationship between Attitude towards Brand Extension and

various parameters which affect the same.

5. To measure the Attitude towards Brand Extension score for new product

categories (hypothetical extensions).

6. To measure the attitude towards the Corporate Brand’s products and

formulate a range across various sectors of the Corporate Brand, eventually

establishing cut offs for the respective sectors.

7. To analyze the Attitude towards Brand Extension score for new product

categories (hypothetical extensions) and the Attitudinal ranges established

for the Corporate Brand.

8. To examine the relationship between the attitudes towards the Corporate

Brand’s products scores with product brand equity scores of various

products of the Corporate Brand and thus establish a relationship with their

respective ranges.

9. To establish a relationship among Attitude towards brand extension scores

of the new product categories, attitudinal and product brand equity ranges of

the Corporate Brand and the Corporate Brand Strength (which is an integral

part of the Corporate Brand Equity).

Methodology Adopted

Considering the purpose of the research, an Exploratory as well as an

Experimental approach is taken into consideration. The entire research design is

divided into two parts; Part One which majorly adopts a Qualitative Methodology

and Part Two which purely adopts a Quantitative Methodology.

In Part One of the research design, a Brand Concept Map (BCM) is established

for the Corporate Brand (CB) under study, for which the extension possibilities in

the form of hypothetical extensions are taken into consideration to analyze how

far this corporate brand can stretch itself. This BCM would bring out the core

associations of this CB. The hypothetical extensions or the new product

categories which are to be associated with the CB, to test how far the CB can

associate itself with them, a Qualitative methodology is adopted with the help of

Focus Groups as a Data collection tool and the respondents are advised to write

down all the attributes they would be looking forward while purchasing such

products. These attributes are listed down and are ranked for individual

hypothetical extension or the new product category. With the help of a set of core

associations of the CB, an attribute association matching is done. The

respondents are also instructed to rate the core association of the CB on a scale

of 1 to 10 across the hypothetical extensions. A ranking of these hypothetical

extensions or new product categories is thus established from this exercise.

In Part Two of the research design, a Quantitative methodology is adopted for

evaluating i) Parent Brand characteristics & evaluation of the Parent brand

extensions to new product categories (This research considers the Parent Brand

to be the Corporate Brand.) ii) Attitude towards the CB’s products evaluation as

well as iii) Evaluation of product brand equity scores for the CB’s products. An

effort is also done in analyzing the Corporate Brand Strength, which forms an

integral part of Corporate Brand Equity

As a part of the Research design, a Case study approach has been adopted. LG

Electronics India as a case is taken into consideration, since they are the market

leaders in most of the Consumer electronics and Home appliances products.

Hence, it would be interesting to figure out how far LG can stretch itself.

In this research, hypothetical extensions are chosen for LG considering their

extensions within the arena of Consumer durables particularly consumer

electronics and outside the arena of Consumer durables (conglomerate

diversification). Five hypothetical extensions have been taken into consideration

for LG such as Direct to Home services (DTH), Mobile Service Provider (MSP),

Internet Service Provider (ISP), Washing Powder (W.P), Life Insurance (L.I.).

For evaluating the Attitude towards the Brand extension, the original model of

Attitude towards brand extension of Aaker and Keller has been modified in the

current context. First, the variable Knowledge has been added as an

independent variable. Second, independent variables such as Substitute and

Complement have been omitted and are replaced by a new variable Brand

Concept Consistency. Third, three new independent variables have been be

added to the new model i.e.; Innovativeness of the parent brand, Corporate

Ethics & Responsibility, and Environmental concern. Hence in the current model

of Attitude towards brand extension the independent variables taken into

consideration are Parent Brand Knowledge, Innovativeness, Parent Brand

Quality, Environmental concern, Transfer, Brand Concept Consistency, Difficulty

to produce, and Corporate Ethics and Responsibility.

The Attitude towards brand extension (ATBE) score has been calculated for each

hypothetical extension as well as the Attitude towards the current products of LG

is evaluated with the help of all the current products of LG evaluated on the same

parameters along with Product brand equity scores for all the current products of

LG.

From the above attitude scores of all the LG products, 3 different ranges of

attitudinal (Attitude) scores are established, viz; a. Total Range of Attitude scores

of LG, b. Range of Consumer Electronics Attitude Scores, c. Range of Home

Appliances Attitude Scores. The ATBE scores of the hypothetical extensions has

been compared with these ranges for their respective sectors i.e. the sectors to

which the hypothetical extensions belong for example Consumer Electronics or

Home Appliances sector or beyond. If the ATBE scores has been within the

range and above the cutoff of the respective ranges, the hypothetical extension

has been accepted or else the extension is rejected.

A relationship has been established between the Attitude scores of all the

products of LG and their respective Product brand Equity scores. Thus leading to

relationship between their respective ranges (Attitudinal Range and Product

Brand Equity Range).

A relationship has been finally established among Attitude towards brand

extension scores of the new product categories, attitudinal and product brand

equity ranges of the Corporate Brand and the Corporate Brand Strength (which is

an integral part of the Corporate Brand Equity).

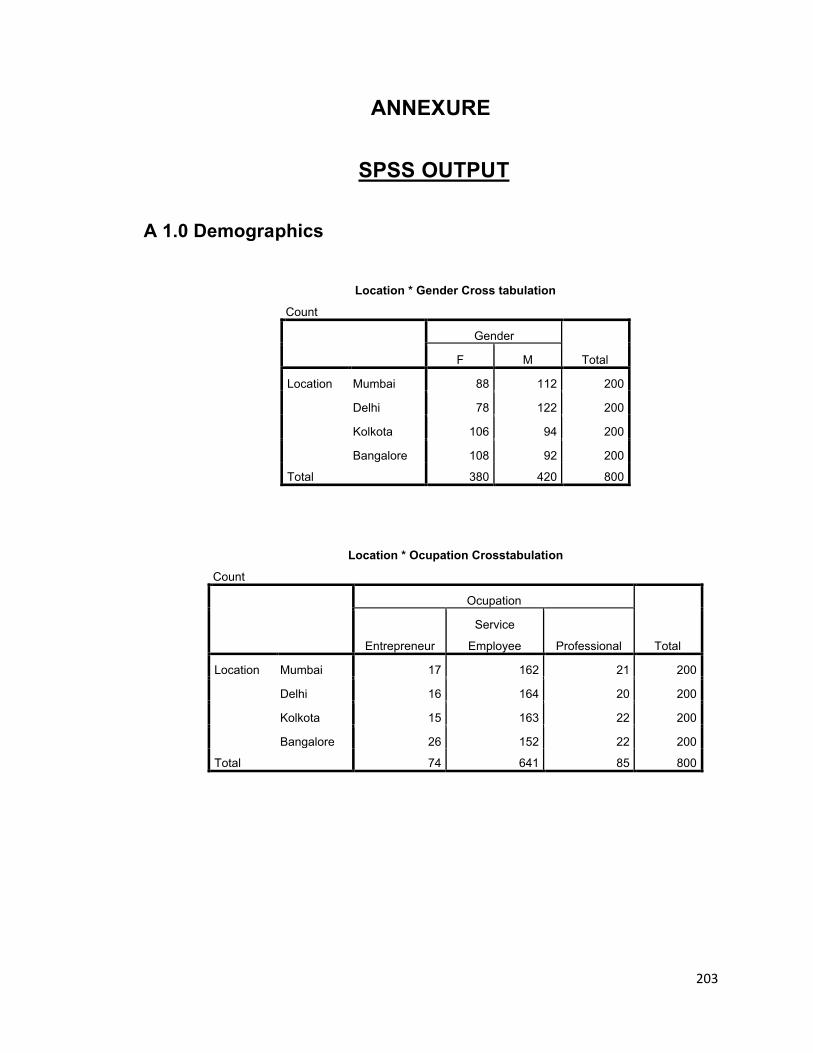

For the evaluation of all the above mention scores a survey has been conducted

at major metropolitan cities viz; Mumbai, Delhi, Kolkata, Bangalore with a sample

size of 200 respondents each. An even distribution of 200 respondents is chosen

from each prime metro. Convenience sampling has been used as the sampling

technique for the survey. The demographic variable studied are Income, Gender

and Occupation. Questionnaire is used as a data collection tool. The entire

Questionnaire design is divided into four parts. The four parts are viz;

Questionnaire for i) Evaluation of Corporate Brand Strength ii) Parent (Corporate)

Brand Evaluation & evaluation of the parent brand extensions to hypothetical

product extensions, iii) Attitude towards all the LG products evaluation as well as

iv) Evaluation of product brand equity scores for all the LG products.

Findings of the Study

1. Amongst the Parent Brand Characteristics of the CB, Parent Brand

Knowledge has the highest rating most likely due to strong corporate

communication like the logo and the tagline as well as constant brand

promotions, followed by the parent brand quality and Innovation.

2. As far as the Parent brand extension characteristics is concerned, it is

observed that for hypothetical extensions such as Direct To Home Services

(DTH) and Mobile Service Provider (MSP) has relatively higher scores on

their Brand concept consistency and Transfer variable, most probably

because they are strongly associated to the electronics arena and are closely

related to the existing LG products such as LG CTVs and mobile phones

respectively, whereas products which are beyond electronics sphere has

shown a higher score for Difficulty to produce.

3. The Attitude Towards Brand Extension Scores is highest for the DTH service

hypothetical extension followed by LG as a Mobile service provider. The

hypothetical extensions such as washing powder and life insurance has the

least attitude towards brand extension score.

4. There has been a confirmation of ranking of the new product categories, both

quantitatively in part two by measuring the Attitude towards the Brand

Extension scores of the new product categories as well as qualitatively by

matching the set of attributes of the hypothetical extensions with the core

associations of LG qualitatively in part one.

5. In the Attitudinal scores of LG products LG LED has the highest score and Air

purifier has the lowest.

6. There exists a positive relationship between attitude towards CB’s products

scores as well as product brand equity scores which further implies that their

respective ranges also have a positive relationship. Which means that as the

range of the product attitude score is higher so is the product brand equity

range.

7. The ATBE of DTH is within the range and above the cutoff of the Range of

Consumer Electronics Attitude Score. Hence DTH as a hypothetical extension

is accepted.

8. The ATBE of MSP as a hypothetical extension of LG is within the range and

above the cutoff of the Range of Consumer Electronics Attitude Score. Hence

MSP as a hypothetical extension is accepted.

9. The ATBE of ISP as a hypothetical extension of LG is within the range and

above the cutoff of the Range of Consumer Electronics Attitude Score. Hence

ISP as a hypothetical extension is accepted.

10.The ATBE of W.P as a hypothetical extension of LG is out off the range and

below the cutoff of the Total range of Attitude Score of LG. Hence W.P as a

hypothetical extension is rejected.

11.The ATBE of L.I as a hypothetical extension of LG is out off the range and

below the cutoff of the Total range of Attitude Score of LG. Hence L.I as a

hypothetical extension is rejected.

Analysis

The ATBE score of the hypothetical extensions, W.P and L.I has been observed

falling well below the range of the attitude towards the products of CB, i.e.; falling

below the cut off score of the attitudinal range of the CB, which would eventually

lead to a higher product attitude range and thus a higher product brand equity

range. Higher product brand equity range in Master brand type of architecture,

which is a kind of umbrella branding, as seen in Corporate branding, would imply

a weaker umbrella brand equity, which eventually implies a weaker Corporate

brand strength, eventually weakening the Corporate Brand Equity. Thus leading

to a logical conclusion that LG should not diversify into these (L.I and W.P)

markets, in particular, other than CEHA market.

On the other hand the ATBE score of the hypothetical extensions, DTH, MSP

and ISP has been observed falling well above the range of the attitude towards

the products of CB, i.e.; falling above the cut off score of the attitudinal range of

the CB, which would eventually lead to a lower product attitude range and thus a

lower product brand equity range. Lower product brand equity range in Master

brand type of architecture, which is a kind of umbrella branding, as seen in

Corporate branding, would imply a stronger umbrella brand equity, which

eventually implies a stronger Corporate brand strength, eventually strengthening

the Corporate Brand Equity. Leading to a logical conclusion that LG should

diversify into these (DTH, MSP and ISP) markets, in particular, the product

categories which fall into the CEHA market.

Benefits

This research would thus benefit the organisations who adopt Corporate

branding strategies, with respect to how far can it stretch its corporate presence

without the corporate brand getting diluted or it’s brand equity getting affected.

This would in turn benefit the organisations in taking Corporate strategic

decisions with respect which product in an unknown category should they invest

and which ones should they not.

Scope & Limitation

As this study is primarily focused on the metros, one can figure out whether there

is a similar level of acceptance in the Tier II and Tier III cities as well as amongst

rural population since LG is spreading itself rapidly in the rural areas as a part of

its expansion strategy.

Suggestions

The research suggests a roadmap for any corporate brand to figure out its

eligibility in venturing into any kind of diversifications, which is as follows

1) Draw a “Brand Concept Map” for the Corporate Brand (CB)- Bring out the

“core associations” of CB. 2) Choose the “new product categories” (hypothetical

extensions). 3) Draw out a set of “attributes” for the “new product categories”

4) Correlate the set of attributes with the core associations of CB and rank the

new product categories. 5) Measure the “Attitude towards the Brand Extension

scores” of the new product categories and rank them. 6) Compare and reconfirm

the ranking with Step 4. (7) Calculate the Attitude scores of all the current

products of the CB and form the ranges and cut offs. 8) Check out the ATBE

score for the respective new product category (hypothetical extension), if it is

below the respective cut offs or beyond the range, reject the Hypothetical

extension or else accept it. 9) Calculate the Product Brand Equity scores of all

the current products of the CB. 10) With the help of Product brand equity scores

formulate a Product brand equity range for the CB. 11) Correlate the attitude

towards the products scores with the product brand equity scores. Find out the

relationship. 12) If there is a positive relationship between the attitude towards

the products scores and product brand equity scores of the CB, then it implies

that Narrower the Attitude towards products range (Range of Attitudinal scores)

=> Narrower the Product Brand Equity range => Stronger the Corporate Brand

Strength => Stronger the CBE. 13) If the ATBE score below the cut off or

beyond the range it may eventually affect the Corporate Brand Equity.

As per the findings and the subsequent analysis, we can recommend for

corporate brands like LG, which has a very strong presence in its electronics and

electronic related sphere that it should try and extend its corporate brand

essence in its own related field. This corporate brand has yet to build up a

greater sphere with respect to its sets of associations, for it to venture into

unrelated product categories.

Thus in general we can predict the success or failure of a corporate brand

extension, within or beyond its related sector, with the help of the above

mentioned roadmap.

1

CHAPTER 1

INTRODUCTION

2

Chapter 1

Introduction

1.1 Introduction & Background

Companies are able to realize in recent times, that leveraging on one of the most

important assets they own, the brand, may help them to achieve their long-term

growth objectives not only more quickly, but also in a more profitable way. These

companies are starting to view their products and services as more than just a

“thing” a customer buys. This makes sense, because brands are not only what a

company sells, they are what a company does and, more importantly, what a

company is.

Many companies, though, are not maximizing their financial returns because they

are not maximizing the power of their brands. For instance, if the company has

sales of $100 million, it means that the companies believe they can increase

revenues by $30 to $50 million with commensurate profits over the next five

years. This will happen if, and only if, companies decide to let the brand help to

drive their growth, and they take advantage of what is the most important

weapon they have at their disposal, i.e. their brand.

Balmer (2001a) views brand as an intangible but critical component of what a

company stands for. While a consumer generally does not have a relationship

with a product or a service, a consumer can have a relationship with a brand.

A brand represents a set of promises. It implies trust, consistency, and a defined

set of expectations. The strongest brands in the world own a positioning in the

3

consumer's mind that is unique to that brand and can universally be articulated

by almost everyone.

Nowadays, the company is witnessing a shift from product branding to corporate

branding (Aaker, 1996; de Chernatony, 1999; Hatch and Schultz, 2001, 2003;

Keller, 2003). Corporate branding goes far beyond the well-established tradition

of product branding: It does not explicitly deal with product features, but rather

transports a well defined set of corporate values (Aaker and Joachimsthaler,

2000; Hatch and Schultz, 2003; Schultz and de Chernatony, 2002). The general

aim of corporate branding is to build a sustainable bond between the branded

company and its customers through a clear value proposition (Schultz and de

Chernatony, 2002).

In an era when the emphasis is moving from line branding to corporate branding

(Balmer, 1995; Mitchell, 1997), there is a need to better appreciate the

management approach for corporate branding as this needs different

management from line branding. One of the key differences between line and

corporate branding is that the latter requires greater focus within the

organization. The size and composition of brand management teams are

changing, requiring greater co-ordination of activities. One of the implications of

this is that corporate marketing necessitates not only a planning perspective

which addresses the matching of external opportunities with core competencies,

but also considers the integration of internal activities to ensure cohesion and

therefore consistency in delivery.

4

The concept of the corporate brand has recently been raised to prominence in

both academic and practitioner fields, with a number of authors pointing to the

potential economic value inherent in managing and developing the brand at the

level of the organization (Fombrun and Van Riel, 1997; Greyser, 1999; Aaker and

Joachimsthaler,1999). Before proceeding into the meaning of Corporate Brands

and Corporate branding, it is imperative to study the architecture of brands,

cooperate branding being one of them.

1.2 Brand Architecture

Currently, there are many different branding architectures and strategies for a

company to pursue. Branding architecture illustrates the structure of the brand

portfolio that specifies brand roles and the relationships among and between

corporate, company and product brands (Aaker & Joachimsthaler, 2000b; Balmer

& Gray, 2003). In recent years, corporations have evolved from simple brand

architectures to complex brand architectures, due to the rising trend towards

industry consolidation through mergers and acquisitions (Muzellec & Lambkin,

2009; Aaker & Joachimsthaler, 2000b). Corporations’ complex branding

architectures make it extremely challenging for managers to manage them.

Therefore, companies should regularly rationalize brand portfolios in order to be

able to better serve customers and maximize profits (Kumar, 2003). After all, a

comprehensive analysis of a company’s brand portfolio can highlight which

brands are suited for possible brand extensions and leveraging brand equity.

5

Most companies do not regularly examine their brand portfolio. However,

managers should discover whether they are focusing on too many brands, and

discontinue less profitable brands (Kumar, 2003). It is important to clarify that

most large companies do not follow one concrete branding architecture, but use

a mixture of different branding strategies (Laforet & Saunders, 2005; Muzellec &

Lambkin, 2009). Aaker and Joachimsthaler (2000b) developed, ‘the brand

relationship spectrum’ which is an influential branding architecture tool that

illustrates four main branding strategies.

First of all, the two most extreme branding architectures will be explained, these

are ‘house of brands’ and ‘branded house’ and will explain ‘endorsed brands’ and

‘subbrands’ in more detail.

Corporate brands like P&G and Unilever are using a so-called house of brands

strategy. This implies that both firms have a wide range of powerful brands in

their brand portfolio. A house of brands strategy allows firms on the one hand to

position brands on functional benefits, and on the other hand to dominate niche

segments (Aaker & Joachimsthaler, 2000b).

The corporate and its product brands avoid being associated with each other and

do not show any clear linkages to the customers (Muzellec & Lambkin, 2009).

Throughout, the corporate brand can penetrate into new and different product

categories without the possibility of diluting its corporate equity (Muzellec &

Lambkin, 2009). If the new brand is unsuccessful this does not hurt the corporate

brand equity, because the corporate and product brand are clearly separated in

the minds of the customers.

6

By contrast, a branded house strategy is when both the corporation and its

products share the same name, which is known as the master brand (Muzellec &

Lambkin, 2009). Pursuing a branded house architecture can enhance clarity,

maximizes synergy and provides brand leverage (Aaker & Joachimsthaler,

2000b). An example of this is Virgin who uses its master brand name as an

umbrella in various different industries such as Virgin Atlantic and Virgin Money.

The advantage is that consumers may have developed favourable associations

towards the master brand and these favourable associations might be easily

transferred to its products. However, if the product is unsuccessful, sharing the

same name can hurt the master brand and have a devastating effect on brand

equity. Additionally, when the master brand weakens this can significantly affects

sales and profit margins (Aaker & Joachimsthaler, 2000b).

Endorsed brand is another branding architecture for a company to pursue. The

endorsed brand is independent, and usually endorsed by an organizational

brand. Corporate brand, Nestlé, uses an endorsed brand strategy on a variety of

its product brands (e.g. Kit Kat by Nestlé, Nesquik by Nestlé and Smarties by

Nestlé). Motivation for using an endorsement is that it provides credibility and

substance, and it also can provide beneficial associations for the endorser (Aaker

& Joachimsthaler, 2000a). However, there is also a downside to using an

endorsement strategy. For example, if Nestlé uses its corporate brand name to

endorse a variety of their product brands, and negative publicity spreads, this can

endanger the entire reputation of the company (Launders & Saunders, 2005).

7

The last brand architecture strategy draw upon is subbrands, which are brands

connected to a master brand and adapt the associations of the master brand

(Aaker & Joachimsthaler, 2000b). The connection between subbrands and

master brand is closer than between endorser and endorsed brand (Aaker &

Joachimsthaler, 2000b). This implies that subbrands can highly influence the

associations of the master brand. For companies to pursue a subbrand strategy

enables the master brand to stretch and enter new markets.

To conclude, there is a vast diversity in the way that corporations manage their

brand portfolios, even within the same industry, corporations pursue different

branding architectures (Laforet & Saunders, 1994). This paper deals with

Branded house strategy i.e.; the Master Brand Architecture, which is a prominent

brand architecture in Corporate Branding. For which it is necessary to

understand a Corporate Brand.

1.3 Introduction to Corporate Brand

Corporate brand is defined at the level of the company. The positive image of a

strong company usually extends to credibility of the products sold under the

company’s brand, both existing ones and those that are new to the market

(Siburian, 2004). According to Aaker when brands are managed separately and

independently, overall resources allocation among brands may be less than

optimal (1996). Therefore, having the corporate brand, or in other words

8

cohesive brand portfolio, instead of number of individual product brands, is more

rational from the company’s point of view.

Corporate brand is defined primarily by organizational associations (Aaker,

2004). It is extremely important to notice that organisational associations are

equally important for both product and corporate brands. Nevertheless, the

power, number and credibility of the organisational associations are larger in

case of corporate associations.

It is reported that a corporate brand can add value to the company’s product

policy and linking corporate and product brands will be beneficial to both the

corporate and its individual products. Several multinationals have become aware

of the importance of their names and are trying to establish and create a strong

link between their corporate brand and product brand (Uehling, 2000). However,

although there are many theories that have been advanced explaining how

customers evaluate and select a particular product (Bettman, 1970; de

Chernatony and Dall’Olmo Riley, 1998; Jamal and Goode, 2001; Kim and Chung,

1997; Lee and Ganesh, 1999; Low and Lamb, 2000; Mitchell and Olson, 1981;

Muthukrishnan and Kardes, 2001; Woodside and Clokey, 1974), most of these

attempts have only partially examined the impact of corporate branding on

consumers’ product evaluation.

1.3.1 Corporate Brands vis-a-vis Product Brands

The main distinction between the product brand and corporate brands is that

once the product brand is established, it begins its life in the eyes of customers

9

independent of the organisation which created it. Corporate brand is permanently

tied to both organisations and other brands of the company: product brands.

According to Aaker (2004), The corporate brand is special because it explicitly

and unambiguously represents an organisation as well as a product. As a driver

or endorser, it will have a host of characteristics and programs that can help build

the brand. It can help differentiate, create branded energizers, provide credibility,

facilitate brand management, support internal brand building, provide a basis for

a relationship to augment that of the product brand, support communication to

broad company constituencies, and provide the ultimate branded house.

First, differentiation in the organizational associations can be potentially found

out by corporate brands. While products and services tend to become similar

over time, organisations are inevitably very different. Wells Fargo is very different

from its competitor Bank of America in terms of style, personality, headquarters,

location, skills, citizen ship programmes and heritage. A person may be more

comfortable with one organisation over another, particularly if the products are

similar. The challenge is to identify those organizational characteristics and make

them relevant to customers.

Second, organizational programs can be drawn by a corporate brand that would

provide energy to product brands. Citizenship programmes and major

sponsorship will usually span the organisation and thus the corporate brand is in

much better position to exploit these than product brands, whose link to hem

10

might be weak. A corporate program is more effective and efficient than one that

reaches only one product class.

Third, credibility can be provided by corporate brand associations. Attitude

research in psychology has shown that believability and persuasive power is

enhanced when a spokesperson is perceived as being trustworthy, well-liked,

and expert. These same characteristics are relevant when evaluating whether a

claim made by an organisation will be given the benefit of the doubt; an

organisation will be liked because of its citizenship activities; and an expert

organisation will be seen as especially competent in making and selling its

products. Trust is a particularly important attribute and it is easier to develop for

an organisation than for a product.

Fourth, brand management is easier and more effective, leveraging on the

corporate brand across products and markets. Off- brand programs and

initiatives become more visible when the corporate brand is leverage across the

organisation.

Fifth, the translation of the corporate brand internally to employees must be

supported by the mission, goals, values, and culture of the organisation, It is

important for employees to buy into organizational values and programs. The

corporate brand identity serves as the link between the organisation and the

customer. Thus, it can play a key role in articulating these elements to

employees, retailers, and others who must buy into the goals and values of the

11

corporate brand and represent them to the customers. In case of product brands,

there is n o such supporting system.

Sixth, message provided by a corporate brand for the customer relationship that

can be very different from that of the product brand. This can be extremely

valuable for large, established brands that are perceived as reliable, high quality,

and respected but are also perceived as boring and dated. A solution is to

employ the organisation brand to represent the heritage and allow the product

brand to inject energy. If the product brand involves, a strong sub-brand, the sub-

brand can be the energy generator. However, if the product brand is the same as

the corporate brand, as it is for Virgin, Mitsubishi and G.E, then only a dual brand

conceptualization can achieve this.

Seventh contrast between product and corporate brand is a difference in who the

brand relates to in terms of both attraction and support. While product brands

mainly target consumers or customers, corporate brands also contribute to the

images formed and held by organisational and community members, investors,

partners, suppliers and other interested parties (i.e. all company stakeholders).

Instead of relating to consumers through a variety of individual products and

services with distinct product brand names, the corporate brand relates all of the

organisation’s multiple stakeholders and its products and services to each other

through their relationship with the corporation.

Eighth difference between product and corporate branding involves defining who

is responsible for the branding effort. Corporate branding requires much more

complicated and sophisticated organisational practices than did product branding

12

(for related arguments see Balmer, 2001a; de Chernatony, 2001; Will et al.,

1999; Harkness, 1999; Van Riel, 1995). Whereas product branding could be

handled within the marketing department of company, corporate branding

requires organisation-wide support.

The corporate brand is realized by the whole organisation from top to bottom and

across functional units, along with the audiences the brand is meant to attract

and engage. As we will argue next, this is because a successful corporate brand

is formed by the interplay between strategic vision, organisational culture and the

corporate images held by its stakeholders. As this range of issues significantly

overextends the expertise of the typical marketing department, we believe that

successful corporate branding involves the integrated efforts of all organizational

departments (e.g. operations, marketing, strategy, communication and human

resources). For example, Balmer (2001a, b) argued that deliberate and

orchestrated communication of corporate brands depends on the total corporate

communication mix because corporate branding requires integration of internal

and external communication, as well as creating coherence of expression across

multiplicity of channels and news media.

Ninth, the time dimension constitutes another difference between product and

corporate brands. Product brands live in the present. They are short term in their

ambitions to attract potential customers and help deliver sales. When product

brands have been around for some time, like Tide or Budweiser, marketers feel a

strong need to “freshen” them with innovative ad campaigns and to update their

13

iconography. Corporate brands, by contrast, live both in the past and the future

for, as Olins (1989) indicated, corporate brands stimulate associations with

heritage and articulate strategic visions of what is to come. As a symbol of the

company’s heritage and the vision of its leaders for the future, the corporate

brand has a much broader temporal base than does a product brand.

Tenth, Because of the greater reach of corporate brands relative to product

brands – in terms not only of relating past and future, but also of the number of

stakeholder groups targeted and the use of the whole company to support the

brand we believe that corporate branding takes on strategic importance relative

to the functional (marketing and sales) importance typically accorded a product

brand. The strategic importance of corporate branding lies not only in its

positioning of the company in its marketplace, but in creating internal

arrangements (e.g. organisational structure, physical design and culture) that

support the meaning of the corporate brand.

Finally, a corporate brand provides the ultimate branded house and captures all

the efficiencies of dialing up a single brand, even more so when descriptors are

employed and the use of sub brands is limited. In this case, the brand will gain

synergy and association reinforcement. Further, and more important, limited

brand building resources will be less diluted when there is a single mother brand.

The branded house is always the preferred strategy when it is feasible.

14

1.4 Brand Extensions

A brand extension is defined as using the current brand name to enter a different

product class, such as Ivory moving from soap to shampoo (Aaker and Keller,

1990), and Billabong entering the snowboard and skateboard categories from

their base in casual surfwear. This strategy is frequently used in mature fast-

moving consumer goods (FMCG) categories such as personal care products

(Ambler and Styles, 1997). Myriad academic studies have appeared exploring

successful approaches in applying brand extensions and investigating

consumers’ responses towards brand extensions (Aaker and Keller, 1990;

Ambler and Styles, 1997; Barone, 2005; Bottomley and Holden, 2001;

Fedorikhin, Park and Thomson, 2008)

Brand extensions have become one of the most heavily-researched topics as

well as one of the most influential areas in branding (Czellar, 2003). Successful

brand extensions depend on consumers’ perceptions of fit or similarity between

the new extension and the parent brand (Aaker and Keller, 1990; Czellar, 2003;

Klink and Smith, 2001; Volckner and Sattler, 2006). Furthermore, studies reveal

an interaction between the parent brand and the extension category: factors

affecting the parent brand will affect the extension as well. Similarly, factors that

influence the extension category will affect the parent brand (Byung Chul,

Jongwon and Robert, 2007; Hem, 2001; Kumar, 2005; Martinez and Pina, 2003;

Martinez, Polo and de Chernatony, 2008; Maureen, 1999; Nan, 2006; Yeung and

Wyer Jr, 2005). Customers evaluating brand extensions may change their core

15

beliefs about parent brands, which may lead to a stronger or weaker brand

positioning (Sheinin,2000).

Importance of Brand Extension is observed with regards to factors such as,

Innovation: which allows the brand to remain up to date and demonstrates and

increasing urge to detect and respond to the profound changes in customer

tastes & expectations. Brands that have stuck to a single state-of-art product,

relying on communication alone to update their image, have not done well.

Cost of advertising: Advertising is very essential to achieve an extended market

share (from local market to national to international market). If one adds to this

the need to be heard as much as the competitors, at least matching their share of

voice, one understands why advertising expenditure is raising so much. The cost

of advertising makes it impossible to support too many brands; efforts have to be

concentrated on a few brands only. It is imperative to decide which brands

should be advertised more. Therefore, brands extensions prove to be much more

economical.

Brand extension is the only way of defending a brand at risk in a basic market.

Brand extension gives access to an accumulated images capital. Brand

awareness surveys are done to find out the existing images of the brand in the

minds of the consumer. This not only makes us aware of the perception of the

brand in the market but also gives adequate information of the extension

potential of the brand.

Extending the brand enables the reinforcement of the image capital of the brand

and fuels it. By coming up with new or rejuvenated product, a brand can prove

16

that it is relevant and up to date. For that reason brand extension, far from

weakening the brand often makes it healthier.

The brand extension strategy is often seen as beneficial because it reduces new

product introduction marketing research and advertising costs, and increases the

chance of success due to higher preference derived from the core brand equity

(Chen & Liu, 2004). All investigations on the determinants of successful brand

extensions initially assume that a brand is an accumulation of associations

(Keller, 1993) and the parent brand associations can influence consumers'

reactions to brand extensions (Aaker & Keller, 1990; Bhat & Reddy, 2001). In

previous studies different authors identified some antecedents of brand

extension attitude of consumers. The antecedents they have identified are

parent brand trust and parent brand affect.

A brand extension strategy can be beneficial because it reduces the new product

introduction costs and also increases the chance of success (Kapferer, 1994).

The rationale behind brand extensions is simple: when a strong brand has been

established, the brand has moved beyond the functional product into a realm of

values. It makes economical sense to try to deliver the same emotional benefits

in a different market (Mortimer, 2003). Since awareness of a certain brand

already exists, costs of launching a new product will, ceteris paribus, be lower

than in the absence of a strong brand. The main objective of brand extensions is

hence to leverage the intangible qualities of a brand since the functional benefits

can generally be imitated (Urde, 1999).

17

1.5 Corporate Brand Extensions

A company makes a corporate brand extension when it relies on its corporate

name to launch a new product. A corporate brand extension clearly identifies an

organization with the product, and so evokes different reactions from consumers

than a product brand extension. A corporate brand may create associations in

consumers' minds that reflect the values, programs, and activities of the firm.

(Aaker & Keller 1998).

Companies are increasingly taking their corporate brand into new and unrelated

business areas in order to capitalize on their brand equity. Wally Olins points to

one of the most essential strategic issues concerning branding strategy: Brand

Extension. With the increasing focus on optimization of brand value, one of the

main strategic brand issues for companies to consider is how the brand equity

can create value across more activities, markets, and product categories (Balmer

& Grey, 2003; Aaker, 2004). Many companies therefore work at stretching or

extending their brand into business areas that are not related to the business in

which the brand originated.

One significant explanation for the success or failure of a corporate brand stretch

is to be found in the role played by the culture and identity of the organisation in

the brand stretch process. Brands and organizational culture and identity are

becoming more closely interlinked. A corporate brand stretch strategy and the

organizational culture and identity will therefore mutually influence each other.

Extensions always carry the risk of diluting what the original brand name means

to consumers, especially in the case of extensions that are inconsistent with the

18

brand’s existing image. The dilution has also been investigated through empirical

research and there are results showing that under certain conditions, a brand

extension can diminish consumer feelings and beliefs about a brand name. The

risk of diluting the parent brand is also a concern (Keller, 2000). The conclusion

in most research on brand extensions is that the brand needs to be a strong

brand with a very precise meaning- a solid brand identity- in order to cover a

broad range of unrelated products. The more a brand covers different categories,

the more it stretches and weakens, losing its force like an elastic band (Kapferer,

1992).

An example of a well known brand that has been stretched too far is the Pringle

brand, known for its colourful high quality knitwear for men and sponsorship of

top golfers. In 1993, the company rolled out a diversification strategy, and

suddenly the Pringle brand appeared on everything from jeans to cotton dresses,

blazers, luggage, belts and silk. Pringle even moved into retailing, launched a

chain of Pringle shops selling their own apparel, and soon discovered the logistic

nightmare which this rapid expansion entailed. All new product lines, apart from

knitwear, were outsourced and were found to be difficult to coordinate. They

became too diversified too fast, in areas their consumers didn’t expect them to

be. For eg; the cotton dresses which seemed to be out of step with the masculine

Pringle brand. From a theoretical perspective it can be argued that Pringle

extended its brand in directions, that in the minds of consumers, did not fit with

the original masculine, high class image closely connected to knitwear. The core

19

identity compromised, and the organisation also seemed to lack the necessary

competencies for the expansion so the launch failed.

The changing market dynamics and heightened competition of the global

economy has amplified the role of Corporate brands to an unsurpassed level.

Marketers seek ways to achieve growth while reducing both the cost of new

product introductions as well as the risk of new product failure. A popular way of

launching new products into a new sector or market has therefore been to

leverage the equity of the corporate brand.

20

CHAPTER 2

REVIEW OF LITERATURE

21

CHAPTER 2

REVIEW OF LITERATURE

2.1.1 Brand Extension Definition

According to Keller (2003), a brand extension is defined as “when a firm uses an

established brand name to introduce a new product”. Brand extensions are made

on an ad hoc basis or according to a strategy to create a range brand (Aaker,

1996).

Sharp (1993) illustrates how important it is that the extensions of a brand share

the features of the original brand, which were an important factor in the

differentiation of the competitors and lead to competitive advantage of the

original brand, in order to be able to use and manage the marketing strategy of

brand extensions wisely. Sustaining brand equity deals with maintaining the bond

with the customer, and proper usage of brand extension appears to be about

regarding the important factors that build the brand in the first place. Therefore,

one has to ensure that any extension of a brand is a quality product release that

will be held up well by the marketing effort.

Davis and Halligan (2001) illustrates how growing the value of a brand includes a

lot more than just extending that brand by adding products and services or

through maximizing delivery channels. In order for a brand extension to be

successful, the underlying association of the brand have to be created,

22

maintained and expanded because those associations imply a promise to the

consumer from the organisation as a whole. They also state that a brand is not

worth anything if it does not have an impact on the customer’s experience with

the company or organisation.

Davis and Halligan (2001) also believe that it is critical for a company to extend

the equity of their brands in order to achieve full growth and out space

competitors. If marketers manage to link brand extensions back to the customer

relationship and how the relationship has been used as a basis for brand

positioning, the extensions are even more dominant. When a brand is extended it

either extends the target market of the company, or it can also extend the

business definition or the point of difference, or extends the entire position of the

brand.

2.1.2 Benefits of Brand Extension

Keller (2003) distinguishes two kinds of benefits:(1) benefits that relate to the

acceptance of the brand extension, and (2) benefits that relate to the parent

brand image.

Kapferer (1997) also makes a distinction between brand extensions and their

benefits from an operational point of view, and proposes that brand extensions

that are intended to boost sales should be distinguished from new products that

carry brand image and exist to fuel the brand.

23

2.1.2 a. Benefits related to brand extension acceptance

As per Keller (2003) Brand extensions allow consumers to draw conclusions and

form expectations about the potential performance of a new product (i.e. the

brand extension) based on their existing knowledge about the brand.

Keller (2003) further claimed that provided a strong brand name is present, the

perceived risk by consumers is substantially reduced when familiarity and

knowledge about the parent brand is present.

Keller, Kapferer (2003) linked benefits derived from introducing new products

with achieving operational efficiencies. A favorable parent brand reduces costs

associated with gaining distribution since retailers are more positive to stock and

promote a brand extension. As per Keller, Kapferer (2003) another benefit relates

to marketing communications: since brand awareness already exists,

promotional activities (including introductory and follow-up advertising and other

marketing programs) of a brand extension can be less intensive and thus less

costly than those of a totally new brand and product. Other efficiencies includes

avoiding costly development of brand names, logos, symbols, packages,

characters, slogans, etc. (Keller, 2003).

2.1.2.b Benefits relating to the parent brand image

Brand extensions also have positive spillover effects on the parent brand. Firstly,

as per Keller (2003), extensions can clarify the brand meaning to consumers and

define the boundaries of the domain in which it competes. Secondly as per , by

24

improving the favorability of an existing brand association, adding a new brand

association, or a combination of these, a brand extension can enhance the

parent brand image.

Morrin (1999), in consistent with the above mentioned views, propose that

consumer exposure to brand extensions will increase parent brand awareness in

terms of recognition and recall.

Similarly, Balachander and Ghose (2003) find evidence of beneficial spillover

effects of advertising of a child brand, for example a brand extension, on choice

of a parent brand.

As per Keller (2003); Kapferer (1997) the third benefit involves brand

revitalization—a new or rejuvenated product can be a mean to renew interest

and improve attitude towards the parent brand.

2.1.3 Drawbacks associated with Brand Extension

Keller (2003) mentions several drawbacks of brand extensions. First, the image

of the parent brand can be hurt irrespective of the success or failure of the

extension. This happens when the attributes of the extension are seen as

inconsistent or conflicting with the corresponding attributes of the parent brand.

Second, brand extensions may obscure the identification of the brand with its

original categories, reducing brand awareness and/or diluting the brand meaning.

Third, brand extensions can lead to problems of practical nature, for example a

25

large number of extensions might confuse or frustrate customers, and there

might be problems with retailers being unwilling to shelf/store all the different

extensions.

Similarly, Loken and John (1993) suggest that “unsuccessful brand extensions

can dilute brand names by diminishing the favorable attitudes that consumers

have learned to associate with the family brand name”.

2.2 Concepts for Evaluating Brand Extensions

2.2.1 Extension reaction

Aaker and Keller’s (1990) study on how consumers evaluate brand extensions is

principle study in the field of brand extensions. The authors hypothesize that

“evaluations of brand extensions are based on the quality of the original brand,

the fit between the parent and extension categories and the interaction between

the two” (Bottomley & H olden, 2001, p. 494).

Despite the fact that this study by Aaker & Keller (1990) per se provides no

evidence that a direct relationship between the quality of the parent brand and

the consumer evaluation of the brand extension exist, the empirical

generalizability of Aaker and Keller’s (1990) model is well supported in Bottomley

and Holden’s (2001) secondary analysis, which examines seven replication

studies.

26

Bottomley and Holden (2001) draw three general conclusions:(1) The quality of

the parent brand and the fit between the parent brand and the brand extension

are key determinants of consumer evaluations of brand extensions; (2)

Consumer’s brand extension evaluations are also determined by (a) the

dimensions of fit (i.e. the complementarity and transferability of assets and skills)

between the parent brand and the brand extension, and (b) to what extent

consumers perceive the brand extension is difficult to produce; (3) Cultural

differences influence how brand extensions are evaluated with respect to relative

measurement factors.

2.2.2 Spillover and substitution effects

While Aaker and Keller (1990) and consequent replication studies provide a

rationale for leveraging parent brand equity through brand extensions, from

which economic profits can be extruded, Balachander and G hose (2003)

examine the reciprocal effect of brand extensions on the parent brand.

As per Balachander and Ghose (2003) the reciprocal effect of brand extensions

on the parent brand is measured by “brand-choice elasticities”, which measure

the increase in choice probability that results from increase in exposure. The

findings of Balachander and Ghose (2003) provide strong support to positive

spillover effects from advertising of a brand extension on choice of a parent

brand. This reciprocal spillover effect does, however, not seem to be

symmetrical—that is, forward spillover effects from advertising of a parent brand

on choice of a brand extension are limited.

27

2.2.3 Categorical and piecemeal evaluation processes

Kapferer (1997) states that to understand how consumers evaluate new brand

extensions, categorization theory is a useful concept. It aims at identifying the

processes by which consumers form categories, and assigns certain objects to

one category rather than another.

Mervis and Rosch (1981) propose that “a category exists whenever two or more

distinguishable objects are treated equivalently”. As per (Loken & John, 1993)

when a new brand extension is launched, a set of attributes or beliefs in addition

to the already existing family or parent brand image is introduced. If these

attributes or beliefs are consistent with the parent brand image, an extension is

considered to be acceptable (Kapferer, 1997) or perceived to “fit” the category

(Boush & Loken, 1991).

Fiske, Cohen (1982) and Brooks (1978) set up another concept for attitude

formation towards brand extensions so-called; “piecemeal”, “analytical” or

“computational” processing, where attitude is “computed” from specific brand

extension attributes. This type of model does not aim to describe conscious

evaluation processes (Boush & Loken, 1991).

Fiske and Pavelchak (1986) propose a two-step process of evaluation. In the first

step, the consumer attempts to match a brand extension (or some other new

object) with the current category. If categorization is successful, in other words, if

28

there is a match, the affect that is associated with the category type is applied to

the brand extension and so the evaluation process is complete. If there on the

other hand is a poor match between the category and the brand extension,

piecemeal processes are initiated. Affect is then evaluated through a weighted

combination of attributes.

As per Loken & John (1993), even if inconsistency implies that the extension is

not “integrated” in the parent category, an inconsistent brand extension can have

a negative impact on the parent brand by “diluting” specific attribute beliefs that

consumers have come to hold about an established brand name, rather than

“diluting” the global affect associated with the established brand name. The

negative impact of an inconsistent extension depends on the typicality of the

brand attribute at stake. Hence, brand dilution is an important issue when

launching new brand or category extensions.

2.2.4 Brand-specific associations

MacInnis & Nakamoto (1990) defines brand-specific association as an attribute

or benefit that differentiates a brand from competing brands. This means that a

brand can be associated with a salient attribute, but this association is per se not

strongly associated with competing brands or the product class as a whole

(Broniarczyk & Alba, 1994).

29

Since the brand association varies depending on the benefits that are sought

within a particular product category, a consumer’s evaluation of a brand

extension need not correspond to evaluation of that brand in its original category.

Thus Broniarczyk and Alba’s (1994) research comes up with three conclusions:

(1) A perceived lack of fit between the product category of the parent brand and

the proposed extension category can be overcome if key parent brand

associations are salient and relevant in the extension category; (2) brand-specific

associations allow for brand extensions to unrelated product categories. Brand-

specific associations moderate the role of product category similarity in brand

extension judgments; a brand extension is more preferred in an unrelated

category that valued its association than in a similar category that does not value

its associations; and (3) the boundaries for the appropriateness of a certain

brand extension were determined by knowledge about the incumbent brand.

2.3.1 Influence of Brand extension on the Parent brand

Three studies that investigated the influence of brand extensions on the parent

brands particularly influenced this research.

1. Martinez & Pina (2003) examined the negative impact of brand extensions on

parent brand image. 2. Pina, Martinez, De Chernatony, and Drury (2006)

developed an empirical model which explains the effects of service brand

extensions on corporate image. 3. Martinez, Polo, & de Chernatony (2008)

investigated the effect of brand extension strategies on brand image in a

30

comparative study of the UK and Spanish markets, particularly the industry of

sport products. These three studies suggest brand extensions have a significant

effect on the parent brand image.

Sheinin (2000) explored how brand extensions influence knowledge about parent

brands. The major finding is that brand extensions influence knowledge of

unfamiliar parent brands more than familiar parent brands. However brand image

and brand knowledge are only two dimensions of branding. Other aspects such

as the consumer-brand relationship, brand experience, brand personality, and

brand architecture still need to be examined.

2.3.2 Influence of the Parent Brand Characteristics on Brand

Extension

Keller (2003) states that there has to exist a brand node in the consumer’s

memory with a variety of associations linked to it–this is conceptualized as brand

knowledge. Information stored in the memory network can be verbal, visual,

abstract, or contextual in nature. Brand knowledge can be characterized in terms

of two components: brand awareness and brand image.

Whereas Broniarczyk & Alba (1994) claims that if consumers are to appreciate

the appropriateness of the brand extension, knowledge of the brand-specific

association is required.

Aaker and Keller (1990) propose a relation between perceived quality of parent

brand and consumers’ attitude toward the extensions in unrelated product

31

categories. As the perceived quality (termed QUALITY) of the parent brand is

higher, the transfer of positive attitudes toward the extension is also higher.

Zeithaml (1988) defines perceived quality as a global assessment of a

consumer’s judgment about the superiority or excellence of a product, and also

concludes that perceived quality is a construct that is on a higher level of

abstraction compared to a specific product attribute.

Keller and Aaker (1997) mention that corporate brand equity lies in the

association of consistent delivery of superior functionality and performance that

customers or suppliers have with a firm’s offering.

Keller and Aaker (1997) propose that marketing efforts that emphasize

innovation leads to favorable perceptions of corporate expertise and thus has a

positive impact on corporate brand extension evaluation. For the purposes of the

current study, it is then reasonable to assume that a parent brand that is

perceived to be innovative will lead to a more favorable brand extension

evaluation compared to a brand which is not perceived as innovative.

Aaker and Keller (1990) also states that the transfer of positive attitudes is also

influenced by the similarity between the corporate brand and the extension. This

follows the categorization theory and category-based processing, where

consumers evaluate a new brand extension as to how well this “fits” with the

parent brand.

32

Similarly, Boush and Loken (1991) propose that affect associated with the

original brand is transferred to the extension when similarity between the two

products is high. Following this, if consumers perceive a “fit” between a business-

to-business brand and a consumer product class, they will transfer perceptions of

quality to the new brand extension.

Aaker and Keller (1990) identify two additional dimensions of fit: the first one is

Complement, which is related to the product; the second one is Substitute, which

is related to the producer.

As per Henderson & Quandt (1980), when the product of the parent brand and

the brand extension can be consumed jointly to satisfy some need, it is said that

they complement each other. On the other hand, when the brand extension can

be used instead of the parent brand product, they are substitutes.

As per Bottomley & Holden (2001), substitutability is generally weak predictor,

since relatively few brand extensions represent true substitutes. In the case of an

extra-sectoral movement, the brand extension can by definition not substitute for

the product of the parent brand. The Substitute dimension will hence be omitted

from further analyses. The original microeconomic definition of complementarity

is limited for current purposes, as according to above given definition it involves

joint consumption of two product classes. In the case of an extra-sectoral

movement, it is not possible for a brand extension to complement the original

brand, since the customers for the original brand and brand extension

33

respectively are different.

Broniarczyk & Alba (1994) proposes a useful alternative measure for

complementarity that is the concept of brand associations, which proposes that

consumer do not only evaluate the brand extension based on the perceived

product category fit, but that their assessment are driven primarily by the

associations of the brand. In other words, if a person considers a brand

extension to be relevant with the original brand concept, the attitude towards the

extension will be positive.

Aaker and Keller (1990) also introduced a Difficulty as a variable, This denotes

the perceived difficulty in designing or producing the brand extension product. If

the extension is perceived to be difficult to make, consumers’ attitude towards the

extension will be negative. This is because a parent brand manufacturing a new

product class which is difficult to manufacture would challenge the competency of

the parent (corporate) brand resulting a costly or an incompetent end product

which may also take into consideration the cost of outsourcing if required to build

the unit or the product class, which would thereby lead to exploitive pricing.

Henderson and Quandt (1980) states that when the product of the parent brand

and the brand extension can be consumed jointly to satisfy some need, it is said

that they complement each other. On the other hand, when the brand extension

can be used instead of the parent brand product, they are substitutes.

34

2.4 Consumer’s Attitude towards Brand Extension

Aaker and Keller (1990) hypothesized that “the consumer’s attitude towards the

brand extension is a positive function of the quality of parent brand, the fit

between the parent’s brand category and the extension category (measured in

terms of the transferability of skills and expertise from one category to the other

and the complementarity and substitutability of one category and the other), the

interactions of quality with three fit variables, and the degree of difficulty in

designing and making a product in the extension category” (Bottomley & Holden,

2001, p. 495).

Loken and John (1993) stated that Inconsistent brand extension can have a

negative impact on the parent brand by “diluting” specific attribute beliefs that

consumers have come to hold about an established brand name, rather than

diluting the global effect associated with the established brand name. When a

new brand extension is launched, a set of attributes or beliefs in addition to the

already existing family or parent brand image is introduced.

Broniarczyk and Alba (1994) proposed that, If consumers are to appreciate the