IMM Quarterly Report: Winter 2016 · 2017-02-07 · Michael Wander Potomac Economics March 22, 2016...

32

MISO Independent Market Monitor Michael Wander Potomac Economics March 22, 2016 IMM Quarterly Report: Winter 2016

Transcript of IMM Quarterly Report: Winter 2016 · 2017-02-07 · Michael Wander Potomac Economics March 22, 2016...

MISO Independent Market Monitor

Michael Wander

Potomac Economics

March 22, 2016

IMM Quarterly Report:

Winter 2016

Quarterly Summary

- 2 -

Value

Prior

Qtr.

Prior

Year Value

Prior

Qtr.

Prior

Year

RT Energy Prices ($/MWh) $21.80 -13% -29% FTR Funding (%) 102% 95% 99%

Fuel Prices ($/MMBtu) Wind Output (MW/hr) 5,731 6% 11%

Natural Gas - Chicago $2.10 -13% -40% Guarantee Payments ($M)4

Natural Gas - Henry Hub $2.04 -13% -34% Real-Time RSG $6.5 -63% -55%

Western Coal $0.55 -7% -16% Day-Ahead RSG $10.0 -17% -60%

Eastern Coal $1.36 -8% -28% Day-Ahead Margin Assurance $6.4 -20% -36%

Load (GW)2 Real-Time Offer Rev. Sufficiency $1.7 -41% -48%

Average Load 74.0 2% -8% Price Convergence5

Peak Load 98.2 -14% -8% Market-wide DA Premium 2.0% 1.0% 1.2%

% Scheduled DA (Peak Hour) 98.9% 98.3% 99.5% Virtual Trading

Transmission Congestion ($M) Cleared Quantity (MW/hr) 11,995 9% 31%

Real-Time Congestion Value $200.7 -36% -41% % Price Insensitive 28% 32% 38%

Day-Ahead Congestion Revenue $138.4 -20% -31% % Screened for Review 1% 1% 1%

Balancing Congestion Revenue3 -$11.1 -$7.4 $1.8 Profitability ($/MW) $0.58 $0.76 $0.74

Ancillary Service Prices ($/MWh) Dispatch of Peaking Units (MW/hr) 535 979 416

Regulation $5.46 -17% -29% Output Gap- Low Thresh. (MW/hr) 42 85 97

Spinning Reserves $1.14 -17% -10% Other:

Supplemental Reserves $0.44 -60% -5%

Key: Expected Notes:

Monitor/Discuss

Concern

4. Includes effects of market power mitigation.

Change1

Change1

1. Values not in italics are the value for the past period rather than the change.

2. Comparisons adjusted for any change in membership.

5. Values include allocation of RSG.

3. Net real-time congestion collection, unadjusted for M2M settlements.

• Overall, the market performed competitively and reliably this winter.

• Winter 2016 was characterized by a continuing decline in energy prices caused by record low natural gas prices and moderate weather and load.

Gas prices were roughly 40 percent lower this winter, driving system-wide energy prices down almost 30 percent from last year to $21.80 per MWh.

Average and peak load were both down 8 percent from last year as winter conditions were significantly milder than normal in most MISO areas.

• Wind output was high and MISO set a new wind generation record in February.

• The record lows in natural gas prices also contributed to reductions in other costs:

Congestion levels similarly fell 30 to 40 percent in the day-ahead and real-time compared to last winter due to the lower gas prices and mild conditions.

Real-time RSG fell more than 50 percent from last winter even though MISO dispatched more peaking units. At current natural gas prices, peaking units are more economic and more frequently dispatched in-merit order.

Price volatility make-whole payments were down more than 40 percent, due in part to low fuel prices and in part to improvements to the state estimator model.

• The elimination of the SRPBC at the beginning of February contributed to a significant increase in economic transfers between the Midwest and South regions, allowing MISO to capture substantial dispatch savings.

Summary of Winter 2016

- 3 -

Decline in Fuel and Energy Prices (Slides 9, 11, 12, 20, 21, 25-27)

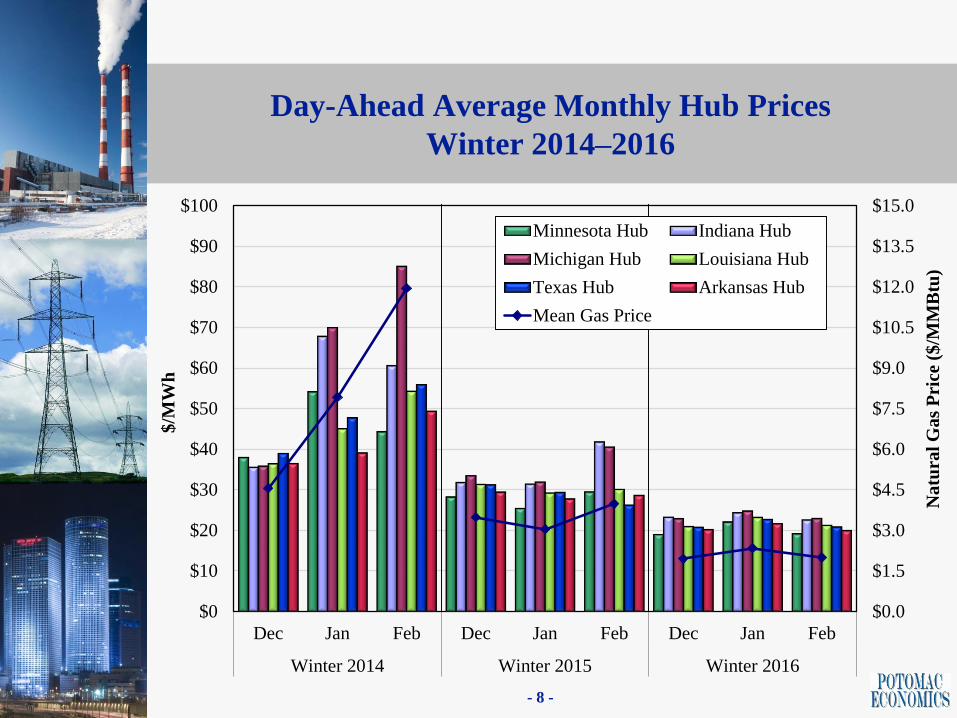

• Mild winter conditions and the shale gas supplies caused the downward trend in gas prices to continue, affecting many aspects of the market this quarter.

The Chicago and Henry Hub natural gas prices both ended February well below $2 and are the lowest since the start of the market.

• Lower gas and coal prices led to broad reductions in prices and costs this quarter.

Energy prices fell almost 30 percent to the lowest levels since the markets began.

RSG and PVMWP fell 40 to 60 percent as energy prices and volatility decreased. These costs also fell as lower gas prices reduced the spread in costs between gas-fired peaking resources and other types of units.

Congestion also fell 30-40 percent as gas-fired units became more economic to re-dispatch to manage network flows.

• Low gas prices increased utilization of gas-fired units, displacing coal-fired units.

Capacity factors of combined-cycle units averaged 45 percent this quarter, compared to 39 and 26 percent over the past two winters, respectively.

Likewise, capacity factors of MISO’s peaking resources averaged 18 percent, up from 14 and 12 percent over the past two winters.

Coal capacity factors averaged roughly 50 percent, down from almost 70 percent two winters ago as they were increasingly displaced by gas and wind.

Highlights from Winter 2015

- 4 -

Regional Transfers (Slide 22)

• The drop in gas prices and the termination of the SRPBC have resulted in

significant changes in both the direction and magnitude of the regional flows.

Since the integration of MISO South, prevailing flows have been North-to-South (58 percent of all intervals).

Regional transfers shifted sharply to the South-to-North direction this winter, flowing in that direction in 81 percent for the quarter.

• Per the recent Settlement Agreement, the SRPBC and ORCA were terminated

at the beginning of February.

The agreement replaces these constraints with the Regional Directional Transfer (RDT) Constraint which limits flows in the North-to-South direction

to 3000 MW and the South-to-North direction to 2500 MW.

As expected, the elimination of the SRPBC has sharply increased economic

transfers between the regions.

In December and January, the average flow from South-to-North was 750

MW. This flow more than doubled in February to 1550 MW.

Highlights for Winter 2016

- 5 -

• We responded to FERC questions related to prior referrals regarding resources

failing to update real-time offers and continued to meet with FERC staff on a weekly and monthly basis to discuss market outcomes.

• We filed comments on the MISO and PJM Coordinated Transaction Scheduling proposal. We supported the CTS filing, but asked FERC to mandate a change.

We presented market results from the CTS provisions implementation between

NYISO and both PJM and ISO-NE. The results show that the CTS is much more

liquid and effective with ISO-NE than with PJM.

We attribute this partly to the charges to CTS transactions, so we recommended

that FERC order PJM to eliminate all charges (MISO proposed no charges).

• We presented our Fall Quarterly Report to stakeholders at the MSC.

• We participated in the FERC technical conference on alternative approaches FTR

funding and allocating FTR shortfalls.

• We provided comments to MISO and stakeholders on the Ramp Product, and will

are working closely with MISO during testing.

• We continued working with MISO and customers to improve transmission ratings

provided by transmission owners in order to more fully utilize the network.

Submittals to External Entities and Other Issues

- 6 -

• In December, FERC issued an Order requiring significant changes to the PRA Auction and Module D Reference Methodology.

We worked with MISO to prepare tariff revisions and its compliance filing.

• We continued to work with MISO and PJM to develop proposals for firm capacity delivery procedures as an alternative to pseudo-tying resources to PJM.

The procedures would guarantee the delivery of energy from external capacity resources that have been exported to PJM.

The proposal would provide benefits to all of the parties and address the economic and reliability concerns raised by large quantities of pseudo-ties.

• We continued to work with MISO, PJM and its customers to evaluate near-term improvements that could be made to improve the RTO’s interface prices.

We conducted a comparative analysis of two alternatives that have been proposed.

We also comments on a collaborative analysis performed by the RTOs.

• We commented on the capacity market alternatives for competitive retail areas and

provided a proposal that would integrate well into MISO’s current market.

We recommended that MISO adopt a sloped demand curve and modified limits

into the area, and not adopt a mandatory forward procurement structure.

Submittals to External Entities and Other Issues

- 7 -

Day-Ahead Average Monthly Hub Prices

Winter 2014–2016

- 8 -

$0.0

$1.5

$3.0

$4.5

$6.0

$7.5

$9.0

$10.5

$12.0

$13.5

$15.0

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Dec Jan Feb Dec Jan Feb Dec Jan Feb

Winter 2014 Winter 2015 Winter 2016

Na

tura

l G

as

Pri

ce (

$/M

MB

tu)

$/M

Wh

Minnesota Hub Indiana Hub

Michigan Hub Louisiana Hub

Texas Hub Arkansas Hub

Mean Gas Price

All-In Price

2014 –2016

- 9 -

$0

$15

$30

$45

$60

$75

$0

$4

$8

$12

$16

$20

14 15 16 J F M A M J J A S O N D J F M A M J J A S O N D J F

Winter 2014 2015 2016

All

in

Pri

ce (

$/W

Mh

)

Na

tura

l G

as

Pri

ce (

$/M

MB

tu)

Capacity

Ancillary Services

Uplift

Energy (Shortage)

Energy (Non-shortage)

Natural Gas Price

Monthly Average Ancillary Service Prices

December 2014 to February 2016

- 10 -

-$2

$0

$2

$4

$6

$8

$10

D J F MAM J J A S O N D J F D J F MAM J J A S O N D J F D J F MAM J J A S O N D J F

14 2015 2016 14 2015 2016 14 2015 2016

Regulation Spinning Reserve Supplemental Reserve

$/M

Wh

Regulation Price (exclude shortages)

MCP Impact from Reg Shortages

Spinning Reserve Price (exclude shortages)

MCP Impact from Spin Shortages

Supp Reserve Price (exclude shortages)

MCP Impact from OR Shortages

Day-Ahead Premium

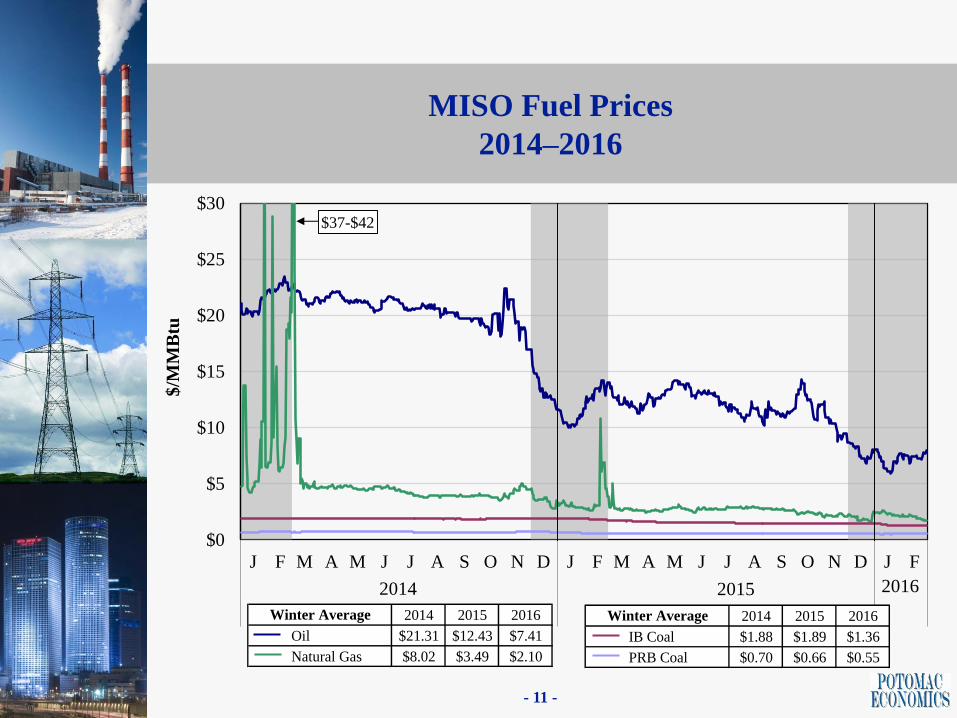

MISO Fuel Prices

2014–2016

- 11 -

$0

$5

$10

$15

$20

$25

$30

J F M A M J J A S O N D J F M A M J J A S O N D J F

2014 2015

$/M

MB

tu

2014 2015

$37-$42

2016

2014 2015 2016

Oil $21.31 $12.43 $7.41

Natural Gas $8.02 $3.49 $2.10

Winter Average 2014 2015 2016

IB Coal $1.88 $1.89 $1.36

PRB Coal $0.70 $0.66 $0.55

Winter Average

Capacity Factors By Fuel Type

Winter 2014–2016

- 12 -

0%

10%

20%

30%

40%

50%

60%

70%

80%

MAM J J A S O N D J F MAM J J A S O N D J F MAM J J A S O N D J F MAM J J A S O N D J F

Coal Steam Combined Cycle Combustion Turbine Wind

Ca

pa

city

Fa

cto

r

2015-2016

2014-2015

2013-2014

Load and Weather Patterns

Winter 2014–2016

- 13 -Note: Midwest degree day calculations include four representative cities in the Midwest: Indianapolis, Detroit, Milwaukee and

Minneapolis. The South region includes Little Rock and New Orleans.

0

25,000

50,000

75,000

100,000

125,000

0

250

500

750

1,000

1,250

14 15 16 13 14 15 14 15 16 14 15 16

Winter Dec Jan Feb

Lo

ad

(M

W)

Ad

just

ed D

egre

e D

ay

s

Average Load

Peak Load

CDD

HDD

Historical Avg.

Day-Ahead and Real-Time Price Convergence

2015–2016

- 14 -

-$10

$0

$10

$20

$30

$40

$50

$60

DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT DA RT

15 16 J F M A M J J A S O N D J F

Win. Avg. 2015 2016

$/M

Wh

Average Price Difference

Absolute Difference

RT RSG Rate DA RSG Rate

Average RT Price Average DA Price

Indiana Hub 1 1 1 1 0 1 2 3 1 2 0 3 2 -2 3 1Michigan Hub 7 2 7 6 -1 2 0 0 0 0 -3 2 3 0 4 3Minnesota Hub 0 4 -1 0 -1 2 3 -1 3 0 -2 14 5 3 4 5WUMS Area 0 2 1 0 2 4 1 3 3 0 1 1 -1 0 4 3Arkansas Hub 0 3 -3 3 -3 4 3 3 -3 0 0 0 6 4 2 2Louisiana Hub 1 3 0 2 -10 -2 0 -10 1 -5 0 0 -1 4 2 3Texas Hub 0 3 -1 1 -5 4 -10 4 0 -7 -2 -12 -15 3 1 6

Average DA-RT Price Difference Including RSG (% of Real-Time Price)

Wind Output in Real-Time and Day-Ahead Markets

Monthly and Daily Average

- 15 -

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

J F M A M J J A S O N D J F 1-7 8-14 15-

21

22-31 1-7 8-14 15-

21

22-30 1-7 8-14 15-

21

22-29

2015 2016 Dec. 2015 Jan. 2016 Feb. 2016

Monthly Average Daily Average

Qu

an

tity

(M

W)

Net Virtual Supply

Day-Ahead Wind

Real-Time Wind

Day-Ahead Peak Hour Load Scheduling

2015–2016

- 16 -

80%

84%

88%

92%

96%

100%

104%

14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016

Sh

are

of

Act

ua

l L

oa

d

Net Virtual Supply Net Virtual Load

Net Real-Time NSI (Negative) Net Real-Time NSI (Positive)

Price Based Load Fixed Load

Share of Actual Load (%)

All Hours

Peak Hours

Midwest

Peak Hours

South

100.7

99.1

98.6

99.9

98.9

98.6

99.3

99.4

98.5

99.4

99.6

98.5

98.2

97.9

98.4

99.0

98.2

100.7

99.1

98.6

99.8

99.3

98.6

99.1

98.6

98.3

97.9

98.2

97.0

98.6

99.2

99.7

99.2

98.8

100.7

99.1

98.6

101.8

98.3

101.3

102.6

101.8

98.1

100.6

101.4

99.9

101.0

96.8

99.5

99.1

98.9

Virtual Load and Supply

2015–2016

- 17 -

24,000

21,000

18,000

15,000

12,000

9,000

6,000

3,000

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

14 15 16 J F M A M J J A S O N D J F 14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016 Winter 2015 2016

Midwest South

Av

era

ge

Ho

url

y V

olu

me

(MW

)

← S

up

ply

Dem

an

d →

Uncleared

Cleared, Price Sensitive

Cleared, Price Insensitive

Cleared, Screened Transactions

Virtual Load and Supply by Participant Type

2015–2016

- 18 -

30,000

27,000

24,000

21,000

18,000

15,000

12,000

9,000

6,000

3,000

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

14 15 16 J F M A M J J A S O N D J F 14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016 Winter 2015 2016

Financial-Only Participants Generators / LSEs

Av

era

ge

Ho

url

y V

olu

me

(MW

)

← S

up

ply

Dem

an

d →

Uncleared

Cleared, Price Sensitive

Cleared, Price Insensitive

Cleared, Screened Transactions

Virtual Profitability

2015–2016

- 19 -

-$2

$0

$2

$4-$15 M

-$10 M

-$5 M

$0 M

$5 M

$10 M

$15 M

$20 M

$25 M

$30 M

14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016

Pro

fits

per

MW

To

tal

Pro

fits Supply

Demand

Gross

Percent Screened

Demand 6.4 1.9 0.8 1.6 3.0 1.7 1.0 1.7 1.6 1.6 1.7 1.0 1.1 1.4 0.6 0.8 1.0

Supply 2.0 0.9 0.4 0.6 1.0 1.0 0.9 1.0 0.4 0.4 0.2 0.5 0.5 0.4 0.2 0.4 0.5

Total 4.7 1.4 0.6 1.1 2.1 1.4 1.0 1.4 0.9 1.0 1.0 0.8 0.8 0.8 0.4 0.6 0.7

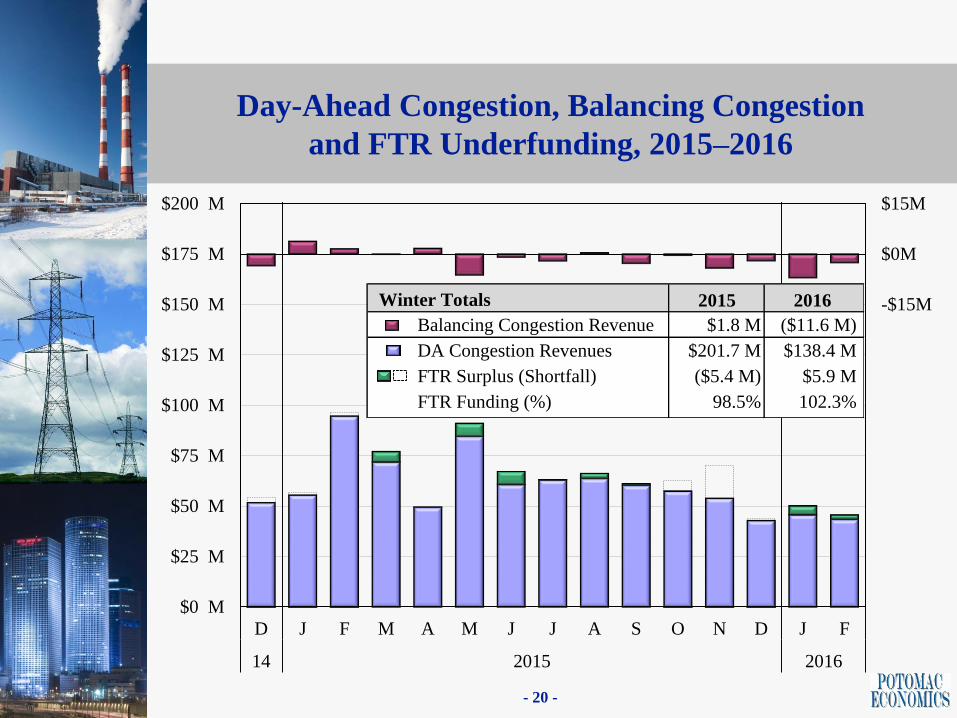

Day-Ahead Congestion, Balancing Congestion

and FTR Underfunding, 2015–2016

- 20 -

-$15M

$0M

$15M

$0 M

$25 M

$50 M

$75 M

$100 M

$125 M

$150 M

$175 M

$200 M

D J F M A M J J A S O N D J F

14 2015 2016

2015 2016

Balancing Congestion Revenue $1.8 M ($11.6 M)

DA Congestion Revenues $201.7 M $138.4 M

FTR Surplus (Shortfall) ($5.4 M) $5.9 M

FTR Funding (%) 98.5% 102.3%

Winter Totals

Value of Real-Time Congestion

2015–2016

- 21 -

$0

$50

$100

$150

$200

$250

$300

14 15 16 J F M A M J J A S O N D J F

Win. Mo. Avg. 2015 2016

Co

ng

esti

on

Va

lue

($ M

illi

on

s)

Win. 15 Fall 15 Win. 16

Midwest 289.6 M 227.2 M 167.0 M

Transfer Constraints 7.8 M 10.0 M 4.5 M

South 43.1 M 78.9 M 29.2 M

Total RT Value 340.5 M 316.1 M 200.7 M

DA Congestion Revenue 201.7 M 172.4 M 138.4 M

Real-Time Hourly Interregional Flows

Nov. 2015 - Feb. 2016

- 22 -

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

OR

CA

/RD

T F

low

No

rth

to

So

uth

(M

W) 3000 MW ORCA/RDT Limit

-3000/-2500 MW ORCA/RDT Limit

Shares of Flow Total Dec.-Feb. Feb.

North to South 58% 19% 13%

South to North 42% 81% 87%

Congestion Costs on SPP Flowgates

2014–2016

- 23 -

0%

10%

20%

30%

-$4

-$2

$0

$2

$4

$6

$8

$10

J F M A M J J A S O N D J F M A M J J A S O N D J F

2014 2015 2016

Sh

are

of

Eff

ect

on

LM

P

Co

ng

esti

on

Va

lue

($ M

illi

on

s)

JOA Payments

Balancing Congestion Cost

Day-Ahead Congestion Cost

Share of Effect on Generation LMP

Peaking Resource Dispatch

2015–2016

- 24 -

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

2,750

14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016

In-M

erit

MW

(%

)

Av

era

ge

Ho

url

y M

W

Real-Time Local Voltage

Real-Time Congestion

Real-Time Capacity

Committed Day-Ahead

Percent In-Merit

Day-Ahead RSG Payments

2015–2016

- 25 -

$0

$10

$20

$30

$40

$50

$60

14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016

RS

G P

ay

men

ts (

$ M

illi

on

s)

Midwest South Total

Fuel-Adjusted RSG: VLR $3.5 M $6.8 M $10.3 M

Fuel-Adjusted RSG: Capacity $2.7 M $3.2 M $5.9 M

VLR RSG not Allocated $0.9 M $0.9 M

Other Capacity RSG $2.7 M $2.4 M $5.1 M

Total Nominal RSG $4.5 M $5.5 M $10.0 M

RSG Mitigation $0.1 M

RSG Distribution: Winter 2016

Real-Time RSG Payments

2015–2016

- 26 -

$0

$10

$20

$30

$40

$50

$60

14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016

RS

G P

ay

men

ts (

$ M

illi

on

s)

RSG Distribution: Winter 2016 Midwest South Total

Fuel-Adjusted RSG: VLR $0.3 M $0.3 M $0.5 M

Fuel-Adjusted RSG: Congestion $3.0 M $2.1 M $5.1 M

Fuel-Adjusted RSG: Capacity $5.7 M $0.8 M $6.5 M

Total Nominal RSG $2.7 M $3.8 M $6.5 M

RSG Mitigation $0.0 M $0.0 M $0.0 M

Price Volatility Make Whole Payments

2015–2016

- 27 -

$0

$3

$6

$9

$12

$15

$0

$3

$6

$9

$12

$15

14 15 16 J F M A M J J A S O N D J F

Win. Avg. 2015 2016

Vo

lati

lity

(Av

era

ge

Inte

rva

l P

rice

Ch

an

ge)

Up

lift

Pa

ym

ents

($

Mil

lio

ns)

DAMAP (Midwest) RTORSGP (Midwest)

DAMAP (South) RTORSGP (South)

SMP Volatility LMP Volatility

Generation Outage Rates

2015–2016

- 28 -

0%

5%

10%

15%

20%

25%

14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016

Sh

are

of

Ca

pa

city

Winter 2014 2015 2016

Short-Term Forced Outages 3.4% 1.9% 1.7%

Long-Term Forced Outages 5.3% 2.5% 3.7%

Planned Outages 9.3% 5.7% 5.4%

Total 17.9% 10.0% 10.7%

Monthly Output Gap

2015–2016

- 29 -

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0

50

100

150

200

250

300

350

400

14 15 16 J F M A M J J A S O N D J F

Winter 2015 2016

Sh

are

of

Act

ua

l L

oa

d

Ou

tpu

t G

ap

(M

W)

Low Threshold

High Threshold

Share of Actual Load

Low Threshold Results by Unit Status (MW)

High Threshold Results by Unit Status (MW)

Offline

Online

Offline

Online

201 12 7 11 17 5 3 11 34 49 58 50 25 0 7 5 10

81 13 5 6 24 16 10 19 24 9 14 16 14 6 8 6 5

235 18 8 12 32 5 4 15 43 54 66 57 32 0 10 6 11

186 46 33 34 71 53 46 90 68 43 56 57 63 45 34 36 31

Day-Ahead And Real-Time Energy Mitigation

2015–2016

- 30 -

0

200

400

600

800

1000

1200

0

400

800

1200

1600

2000

2400

14 15 16 J F M A M J J A S O N D J F 14 15 16 J F M A M J J A S O N D J F

Win.

Tot.

2015 2016 Win.

Tot.

2015 2016

BCA NCA

MW

Mit

iga

ted

Ho

urs

DA Hours Mitigated, NCA

RT Hours Mitigated, NCA

DA Hours Mitigated, BCA

RT Hours Mitigated, BCA

Combined MW Mitigated

Day-Ahead and Real-Time RSG Mitigation

2015–2016

- 31 -

0

30

60

90

120

150

180

210

$0.0 M

$0.5 M

$1.0 M

$1.5 M

$2.0 M

$2.5 M

$3.0 M

$3.5 M

14 15 16 J F M A M J J A S O N D J F

Win. Avg. 2015 2016

Mit

iga

ted

Un

it-D

ay

s

RS

G M

itig

ati

on

Do

lla

rs

DA RSG Mitigated

RT RSG Mitigated

Combined Unit-Days

AMP Automated Mitigation Procedures

BCA Broad Constrained Area

CDD Cooling Degree Days

CMC Constraint Management Charge

DAMAP Day-Ahead Margin Assurance

Payment

DDC Day-Ahead Deviation & Headroom

Charge

DIR Dispatchable Intermittent Resource

HDD Heating Degree Days

JCM Joint and Common Market Initiative

JOA Joint Operating Agreement

LAC Look-Ahead Commitment

LSE Load-Serving Entities

M2M Market-to-Market

MSC MISO Market Subcommittee

NCA Narrow Constrained Area

ORCA Operations Reliability Coordination

Agreement

ORDC Operating Reserve Demand Curve

PITT Pseudo-Tie Issues Task Team

List of Acronyms

- 32 -

PRA Planning Resource Auction

PVMWP Price Volatility Make Whole

Payment

RAC Resource Adequacy Construct

RDT Regional Directional Transfer

RSG Revenue Sufficiency Guarantee

RTORSGP Real-Time Offer Revenue

Sufficiency Guarantee Payment

SMP System Marginal Price

SOM State of the Market

SRPBC Sub-Regional Power Balance

Constraint

TLR Transmission Line Loading

Relief

TCDC Transmission Constraint

Demand Curve

VCA Voluntary Capacity Auction

VLR Voltage and Local Reliability

WPP Weekly Procurement Process

WUMS Wisconsin Upper Michigan

System