IMIA Conference Rio de Janeiro - September 2012 IMIA WGP ... · PDF fileIMIA Conference Rio de...

26

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 1 IMIA Conference Rio de Janeiro - September 2012 IMIA WGP 77(12) Entrepreneurial Risks Working Group Members: Benedikt Schermutzki (Munich Re), Chairman John Forder (Willis) Thomas Gebert (Zürich) Karl-Christian Hertenberger (HDI-Gerling) Stephan Lämmle (Munich Re) Katia Luz (Odebrecht) Federico Pereira (Hannover Re) Daniela Reia (Odebrecht) Carl-Johan Silfwerbrand (Allianz) Darren Smart (Liberty) Peter Tailby (ACR Retakaful) John Timothy (Infrassure) Francisco Triviño (XL Group) Marina Zyuganova (Renaissance) Dieter Spaar (HDI-Gerling) Max Benz (XL Group), Sponsor of the Executive Committee

Transcript of IMIA Conference Rio de Janeiro - September 2012 IMIA WGP ... · PDF fileIMIA Conference Rio de...

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 1

IMIA Conference Rio de Janeiro - September 2012

IMIA WGP 77(12)

Entrepreneurial Risks

Working Group Members:

Benedikt Schermutzki (Munich Re), Chairman John Forder (Willis) Thomas Gebert (Zürich) Karl-Christian Hertenberger (HDI-Gerling) Stephan Lämmle (Munich Re) Katia Luz (Odebrecht) Federico Pereira (Hannover Re) Daniela Reia (Odebrecht) Carl-Johan Silfwerbrand (Allianz) Darren Smart (Liberty) Peter Tailby (ACR Retakaful) John Timothy (Infrassure) Francisco Triviño (XL Group) Marina Zyuganova (Renaissance) Dieter Spaar (HDI-Gerling) Max Benz (XL Group), Sponsor of the Executive Committee

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 2

IMIA Working Group Paper

Entrepreneurial Risks The topic paper discusses entrepreneurial risks affecting the Engineering industry. To what extent can these be transferred to insurance markets and to which extent are solutions already available?

Table of Contents

1. Purpose of Entrepreneurial Risk Management ............................................................... 4

1.1 Introductory Remarks ...................................................................................................... 4

1.2 Insureds' Business Environment Evolution ................................................................... 4

1.3 Examples of Entrepreneurial Risk Insurance to Date .................................................. 5

2. Types of Entrepreneurial Risks affecting the Engineering Industry ................................. 5

2.1 Operational Risks ............................................................................................................ 7

2.2 Financial Risks ................................................................................................................. 7

2.3 Contractual Risks ............................................................................................................ 7

2.4 Environmental Risks ....................................................................................................... 8

3. Insurability Aspects ........................................................................................................ 8

3.1 Preconditions ................................................................................................................... 9

3.1.1 Insurer as Entrepreneur .......................................................................................... 9

3.1.2 Risk versus Uncertainty........................................................................................... 9

3.1.3 Asymmetric Information......................................................................................... 10

3.1.4 Risk of Change....................................................................................................... 10

3.2 Actual Criteria .............................................................................................................. 11

3.2.1 Independence ........................................................................................................ 11

3.2.2 Randomness .......................................................................................................... 11

3.2.3 Measurability .......................................................................................................... 12

3.2.4 Large number of risks ............................................................................................ 12

3.3 Summary ........................................................................................................................ 13

4. Specific Risks and Insurance ....................................................................................... 13

4.1 Sabotage, Strike and Lockout ...................................................................................... 13

4.1.1 Description of Risk ................................................................................................. 13

4.1.2 Underwriting Considerations ................................................................................. 14

4.1.3 Market and Products ............................................................................................. 14

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 3

4.2 Design errors ................................................................................................................. 15

4.2.1 Description of Risk ................................................................................................. 15

4.2.2 Underwriting Considerations ................................................................................. 15

4.2.3 Market and Products ............................................................................................. 16

4.3 Subcontractor/Supplier Insolvency .............................................................................. 16

4.3.1 Description of Risk ................................................................................................. 16

4.3.2 Underwriting Considerations ................................................................................. 16

4.3.3 Market and Products ............................................................................................. 17

4.4 Volatility of Commodity Prices, Interest Rates, Inflation and Exchange Rates ........ 17

4.4.1 Description.............................................................................................................. 17

4.4.2 Underwriting Considerations ................................................................................. 18

4.4.3 Market and Products ............................................................................................. 18

4.5 Non-Fulfillment of Agreed Specifications .................................................................... 19

4.5.1 Description.............................................................................................................. 19

4.5.2 Underwriting Considerations ................................................................................. 19

4.5.3 Market and Products ............................................................................................. 20

4.6 Cost Overrun .................................................................................................................. 20

4.6.1 Description.............................................................................................................. 20

4.6.2 Underwriting Considerations ................................................................................. 21

4.6.3 Market and Products ............................................................................................. 21

4.7 Unforeseen Ground Conditions .................................................................................... 22

4.7.1 Description.............................................................................................................. 22

4.7.2 Underwriting Considerations ................................................................................. 22

4.7.3 Market and Products ............................................................................................. 22

4.8 Insufficient Supply Chain Management and Transport Delay/Disruption ................. 23

4.8.1 Description of Risk ................................................................................................. 23

4.8.2 Underwriting Considerations ................................................................................. 23

4.8.3 Market and Products ............................................................................................. 24

5. Conclusion and Outlook ............................................................................................... 25

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 4

1. Purpose of Entrepreneurial Risk Management

1.1 Introductory Remarks

In its simplest form entrepreneurial risk is that risk associated with a profit driven venture or enterprise. It usually comprises a financial value but can also involve a value of time, particularly for construction projects. As such the risk can lead to a profit or loss.

The risk which is of a commercial nature is governed to a large extent by the individual or company’s initiative, knowhow and flexibility in the market.

Hence to differentiate between entrepreneurial risk and “conventional” risk the former is the profit driven part. To further differentiate entrepreneurial risk from “conventional” risks is to insist that any conventional loss triggering an engineering line insurance must be damage related.

When one considers insuring entrepreneurial risk one has to determine whether such risk is insurable or not; or, to put it another way, whether the outcome can be determined with a reasonably high probability and profit margins can be predicted. Insurability is determined if the chance of the risk’s occurrence can be reasonably well calculated and if the premium can be priced. Thresholds of risk’s severity and frequency also govern whether the risk is insurable or not.

There can be an element of entrepreneurial risk in all engineering lines, for example design risk, guarantee maintenance and fluctuating commodity prices affecting gross profit to name a few.

Management of entrepreneurial risk by an insurance buyer is carried out by the buyer deciding which element of his risk is economically viable to insure, if at all possible and acceptable to the insurance market. Similarly insurers do likewise, but have to rely heavily on past experience.

There is a constant tension in risk ownership between the insurance buyer and the insurer, and during soft and hard markets the balance is to the buyer’s and insurer’s advantage respectively. The danger the insurance company has to avoid is not to allow their insureds to retain too little of their business and if they do then the insured’s interest in their results would diminish and potentially create a moral hazard. The greater the amount of entrepreneurial risk transferred to insurers, the more competitive the insured is likely to be in their chosen market.

1.2 Insureds' Business Environment Evolution

With the constant evolution of the business environment, the risks that each organization faces have become more complex. For example, sourcing of products or components from newly emerging supply sources brings new contractual risk exposures, less familiar foreign exchange risk, additional transport risk etc. Traditional risks such as a fire in a production facility or liability arising from goods sold or services provided - including those specific to construction/engineering activities - have been the subject of risk management focus for many years. However, in the current environment there is an increasing focus on the various financial risks that companies face, many of which are currently either uninsured or only partially insured. Larger industrial clients have of course adopted an "Enterprise Risk Management (ERM)" approach in order to better identify, map and control this complex risk environment.

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 5

Where an ERM system is in place a more holistic view of risks has been adapted and the identified risks have been analysed in depth and mitigation plans put into place, according to the risk profile and appetite of the company. There will however always remain risks that are much more difficult to quantify - either by the Insured or Insurers - and these perhaps constitute at least one significant facet of entrepreneurial risks.

In modern corporations, Risk Management is today an active tool used to address a very diverse landscape of risk. On the one hand there is of course a desire of shareholders to have stable and predictable earnings - a key objective of ERM for many companies - whilst on the other hand, the acceptance of higher risk can result in opportunistic value creation for the company and therefore shareholders. Active and informed risk acceptance is of course another facet of entrepreneurial risk, whereby the company is then more confident of accepting higher risks, particularly financial ones.

Insurance has traditionally been used to address the so called "known risks" such as fire, natural catastrophe and machinery breakdown. However, there is now a clear trend towards a focus on less obvious risks that can have significant financial impact such as Contingent Business Interruption. The larger corporations have a number of solutions available to mitigate or hedge their risks and these include futures, options and of course insurance. Insurance is of course only a hedge against a "downside" in case of an insurable risk actually occurring, whereas financial hedging instruments generally have both, a downside and upside application.

1.3 Examples of Entrepreneurial Risk Insurance to Date

It should be noted that various forms of consequential loss suffered by the Insured following indemnifiable loss or damage (such as CBI and increased cost of working) are effectively the covering of at least one element of entrepreneurial risk. For contractors and engineers, their entrepreneurial risks are typically those that are "non-damage" related and typically financial in nature such as project cost over-run, delay in completion and failure to perform in accordance with contractual obligations. Over the past 20 years, there have been several insurance products that could be considered as entering in to the world of such entrepreneurial risks and these would include the following:-

• Sponsor (Project Cost Over-run) • Force Majeure (non-damage) • Inefficacy (non-damage/non-performance) • Liquidated damages for delay (damage and non-damage)

2. Types of Entrepreneurial Risks affecting the Engineering Industry

There are several types of entrepreneurial risks affecting the engineering business. These risks are normally divided between the participating parties in such a project. The basis for the risk sharing mechanism is based on the construction contract, for example FIDIC. The intention of this paper is to highlight risks which are not related to physical damage. The topic for physical damage related risks have been already discussed widely and they are placed very much as standard insurance products in the traditional insurance markets.

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 6

Due to the increasing complexity of projects, further developed risk assessment techniques, cost pressure and recent loss experience stakeholders of large projects have to perform state of the art project risk management, including the management of entrepreneurial risks.

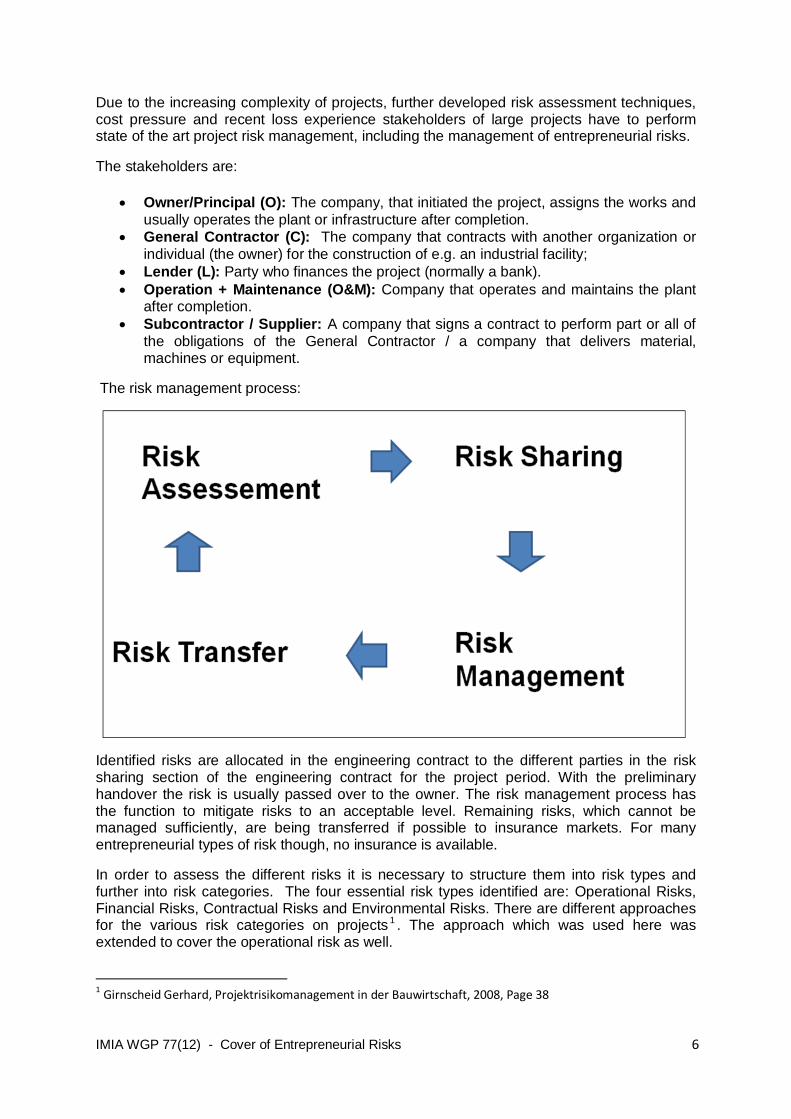

The stakeholders are:

• Owner/Principal (O): The company, that initiated the project, assigns the works and usually operates the plant or infrastructure after completion.

• General Contractor (C): The company that contracts with another organization or individual (the owner) for the construction of e.g. an industrial facility;

• Lender (L): Party who finances the project (normally a bank). • Operation + Maintenance (O&M): Company that operates and maintains the plant

after completion. • Subcontractor / Supplier: A company that signs a contract to perform part or all of

the obligations of the General Contractor / a company that delivers material, machines or equipment.

The risk management process:

Identified risks are allocated in the engineering contract to the different parties in the risk sharing section of the engineering contract for the project period. With the preliminary handover the risk is usually passed over to the owner. The risk management process has the function to mitigate risks to an acceptable level. Remaining risks, which cannot be managed sufficiently, are being transferred if possible to insurance markets. For many entrepreneurial types of risk though, no insurance is available.

In order to assess the different risks it is necessary to structure them into risk types and further into risk categories. The four essential risk types identified are: Operational Risks, Financial Risks, Contractual Risks and Environmental Risks. There are different approaches for the various risk categories on projects 1 . The approach which was used here was extended to cover the operational risk as well.

1 Girnscheid Gerhard, Projektrisikomanagement in der Bauwirtschaft, 2008, Page 38

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 7

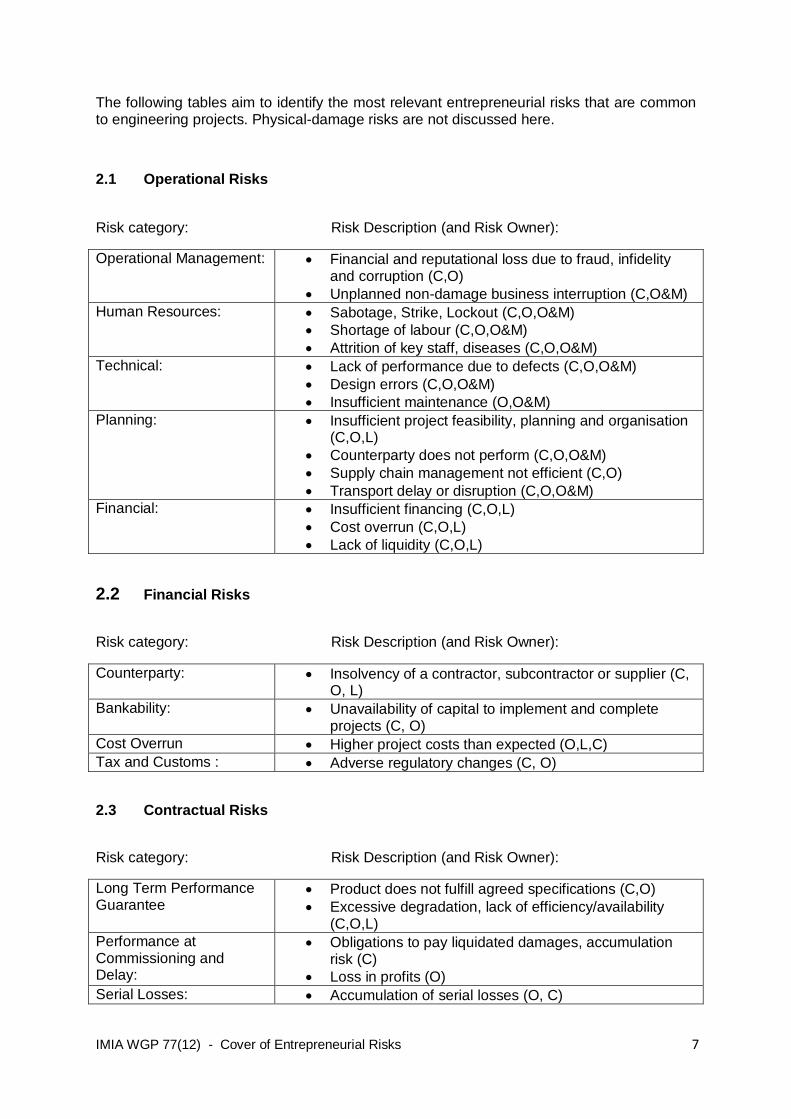

The following tables aim to identify the most relevant entrepreneurial risks that are common to engineering projects. Physical-damage risks are not discussed here.

2.1 Operational Risks

Risk category: Risk Description (and Risk Owner):

Operational Management: • Financial and reputational loss due to fraud, infidelity and corruption (C,O)

• Unplanned non-damage business interruption (C,O&M) Human Resources: • Sabotage, Strike, Lockout (C,O,O&M)

• Shortage of labour (C,O,O&M) • Attrition of key staff, diseases (C,O,O&M)

Technical: • Lack of performance due to defects (C,O,O&M) • Design errors (C,O,O&M) • Insufficient maintenance (O,O&M)

Planning: • Insufficient project feasibility, planning and organisation (C,O,L)

• Counterparty does not perform (C,O,O&M) • Supply chain management not efficient (C,O) • Transport delay or disruption (C,O,O&M)

Financial: • Insufficient financing (C,O,L) • Cost overrun (C,O,L) • Lack of liquidity (C,O,L)

2.2 Financial Risks

Risk category: Risk Description (and Risk Owner):

Counterparty: • Insolvency of a contractor, subcontractor or supplier (C, O, L)

Bankability: • Unavailability of capital to implement and complete projects (C, O)

Cost Overrun • Higher project costs than expected (O,L,C) Tax and Customs : • Adverse regulatory changes (C, O)

2.3 Contractual Risks

Risk category: Risk Description (and Risk Owner):

Long Term Performance Guarantee

• Product does not fulfill agreed specifications (C,O) • Excessive degradation, lack of efficiency/availability

(C,O,L) Performance at Commissioning and Delay:

• Obligations to pay liquidated damages, accumulation risk (C)

• Loss in profits (O) Serial Losses: • Accumulation of serial losses (O, C)

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 8

2.4 Environmental Risks

Risk category: Risk Description (and Risk Owner):

Market: • Risk of brand/trademark damage, negative customer perception (C,O,O&M)

• Volatility of commodity prices, interest rates, inflation and exchange rates. (C,O,L)

Location: • Pandemic/Epidemic (C,O, O&M) • Unforeseen ground conditions (C,O) • Discovery of archaeological site or rare species (C,O) • Polluted soil (C,O) • Exploration risk (O) • Lack of wind, water or sun (O) • Adverse weather conditions (C) • Interruption of utilities (C,O,O&M)

Regulatory: • Failure to obtain licenses, permits, approvals (O, C, L) • Regulatory changes (O, C, L) • Failure to meet deadline for production tax credit or feed

in tariff (O,L) • Failure of carbon credit certificate (O)

Legal: • Denial of access (C,O) • Patent infringement/intellectual property (O) • Legal complaints and law suits (C,O)

Political: • Civil society opposition against projects (O, L) • Confiscation, expropriation, forced buy out, contract

repudiation (O, L) • Insufficient contract certainty and enforceability (O, C, L,

O&M) • Extortion, kidnap, ransom (O, C, L, O&M) • Strike, riot, civil commotion (O, L) • War, Terrorism (O, C, L, O&M)

3. Insurability Aspects

There are a lot of publications discussing this subject. Therefore, in order to derive a meaningful statement more tailored to the main topic of this article one has to get clarity of the main aspects to be considered when designing new products of entrepreneurial insurance in the engineering arena.

For the purpose of this article risk-owners are understood to be the entrepreneurs of various businesses, typically designing, constructing/erecting/building, supplying, owning, operating or funding technical assets of any size and number. These entrepreneurs are dealing with risks of various complexities. The previous chapter has identified clusters of risk types such as operational, financial, contractual, environmental risks.

Risk-takers of entrepreneurial risks can be various market participants, typically insurers, reinsurers but as well capital markets (e. g.: cat bonds) and even the governments (e.g.: terror schemes).

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 9

3.1 Preconditions

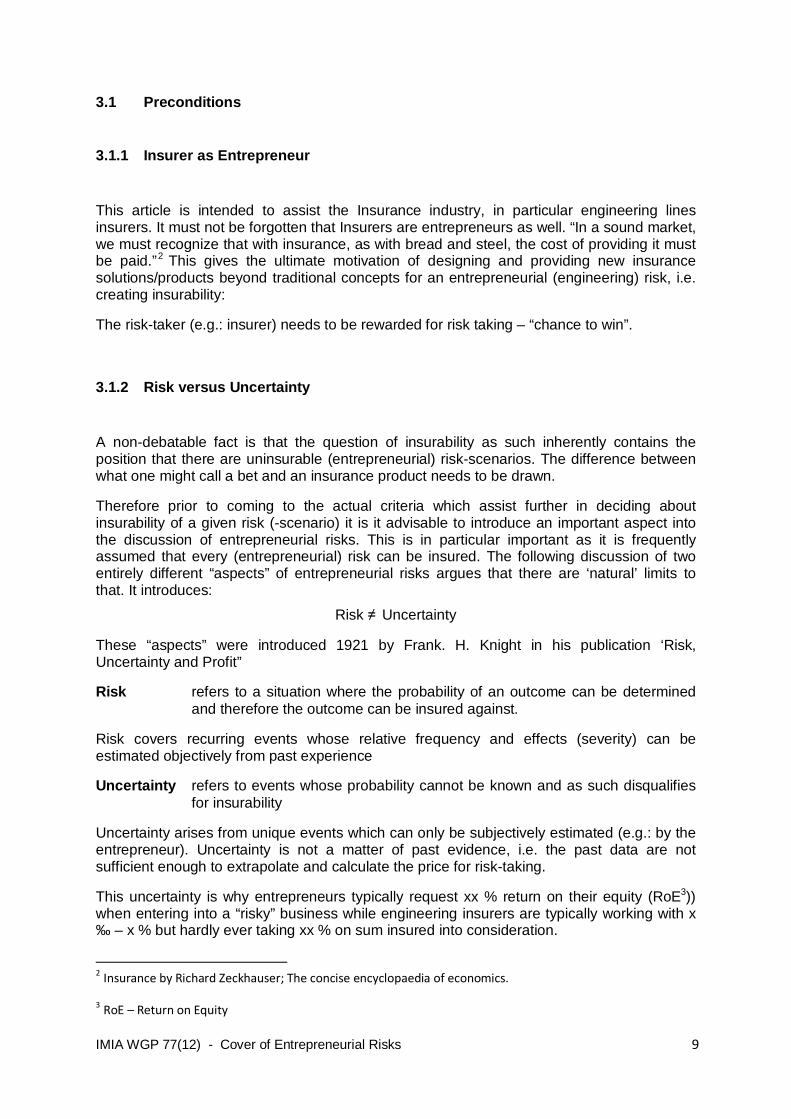

3.1.1 Insurer as Entrepreneur

This article is intended to assist the Insurance industry, in particular engineering lines insurers. It must not be forgotten that Insurers are entrepreneurs as well. “In a sound market, we must recognize that with insurance, as with bread and steel, the cost of providing it must be paid.”2 This gives the ultimate motivation of designing and providing new insurance solutions/products beyond traditional concepts for an entrepreneurial (engineering) risk, i.e. creating insurability:

The risk-taker (e.g.: insurer) needs to be rewarded for risk taking – “chance to win”.

3.1.2 Risk versus Uncertainty

A non-debatable fact is that the question of insurability as such inherently contains the position that there are uninsurable (entrepreneurial) risk-scenarios. The difference between what one might call a bet and an insurance product needs to be drawn.

Therefore prior to coming to the actual criteria which assist further in deciding about insurability of a given risk (-scenario) it is it advisable to introduce an important aspect into the discussion of entrepreneurial risks. This is in particular important as it is frequently assumed that every (entrepreneurial) risk can be insured. The following discussion of two entirely different “aspects” of entrepreneurial risks argues that there are ‘natural’ limits to that. It introduces:

Risk ≠ Uncertainty

These “aspects” were introduced 1921 by Frank. H. Knight in his publication ‘Risk, Uncertainty and Profit”

Risk refers to a situation where the probability of an outcome can be determined and therefore the outcome can be insured against.

Risk covers recurring events whose relative frequency and effects (severity) can be estimated objectively from past experience

Uncertainty refers to events whose probability cannot be known and as such disqualifies for insurability

Uncertainty arises from unique events which can only be subjectively estimated (e.g.: by the entrepreneur). Uncertainty is not a matter of past evidence, i.e. the past data are not sufficient enough to extrapolate and calculate the price for risk-taking.

This uncertainty is why entrepreneurs typically request xx % return on their equity (RoE3)) when entering into a “risky” business while engineering insurers are typically working with x ‰ – x % but hardly ever taking xx % on sum insured into consideration.

2 Insurance by Richard Zeckhauser; The concise encyclopaedia of economics.

3 RoE – Return on Equity

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 10

Summarizing Knight’s argument insurers are well advised to clearly acknowledge and differentiate entrepreneurial risk-scenarios in those containing ‘risk’ only and those characterised by ‘uncertainty’. Providing “design or defects” cover for unproven or prototypical elements can most likely be seen as ‘uncertainty’ already. Having in mind that today’s large industrial equipment is very often subject to continuous evolution (unproven, prototypical?), one recognises how innovative engineering insurers are already - in particular under current soft-market conditions.

3.1.3 Asymmetric Information

This differentiation discussed above leads automatically to another precondition of insurability. Insurability can only be reached by in particular avoiding any situation of asymmetric information.

This is referring to a risk-scenario where a potential risk-seller (entrepreneur) has more information about his risk than the buyer (insurer, who buys risk by receiving a reward/money). The potential seller might have “hidden” information that relates to the particular risk-scenario, and those (risk-owners), whose (own) information is unfavourable, are thus most likely to purchase.4

This leads immediately to adverse risk-selection which will not allow insurers to build up attractive portfolios. Risk-takers cannot be expected to accept any situation where risk-owners seem to be in a more favourable situation in respect to information of actual risk to be transferred. Coming back to the (re-)insurer as entrepreneur one has to acknowledge that risk-scenarios where the “chance to win” for the risk-taker is (purposely?) adversely affected by the risk-owner (supposed to be information-owner) will contribute to an unbalanced business; thus avoiding insurability due to lack of information that is available to the risk-taker only.

3.1.4 Risk of Change

Typically a risk-analysis focuses on information available today. In the context of insurability and evaluating risk information it must not be forgotten that information, i.e. the framework under which a risk has been assumed might change over time. Classic examples are weather related hazards and long-term product-guaranties covering full/partially manufacturers warranties and/or lack of sun/wind/water etc. Severity and frequency of losses can adversely be affected – this calls for a prudent risk-analysis to consider whether the risk (probability of loss) remains the same over time. Can the risk of change be objectively assessed?

Limiting this ‘risk of change’ for the risk-taker during risk-life is one further crucial aspect when designing and underwriting innovative covers.

4 Insurance by Richard Zeckhauser; The concise encyclopaedia of economics

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 11

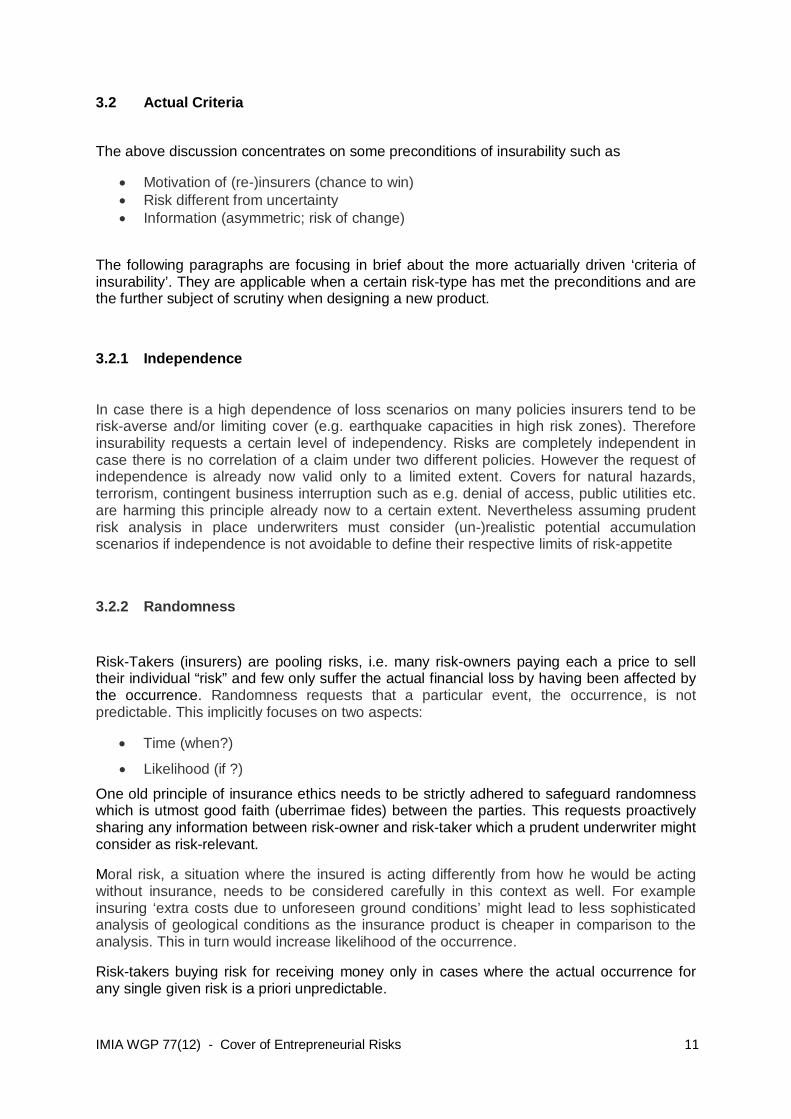

3.2 Actual Criteria

The above discussion concentrates on some preconditions of insurability such as

• Motivation of (re-)insurers (chance to win) • Risk different from uncertainty • Information (asymmetric; risk of change)

The following paragraphs are focusing in brief about the more actuarially driven ‘criteria of insurability’. They are applicable when a certain risk-type has met the preconditions and are the further subject of scrutiny when designing a new product.

3.2.1 Independence

In case there is a high dependence of loss scenarios on many policies insurers tend to be risk-averse and/or limiting cover (e.g. earthquake capacities in high risk zones). Therefore insurability requests a certain level of independency. Risks are completely independent in case there is no correlation of a claim under two different policies. However the request of independence is already now valid only to a limited extent. Covers for natural hazards, terrorism, contingent business interruption such as e.g. denial of access, public utilities etc. are harming this principle already now to a certain extent. Nevertheless assuming prudent risk analysis in place underwriters must consider (un-)realistic potential accumulation scenarios if independence is not avoidable to define their respective limits of risk-appetite

3.2.2 Randomness

Risk-Takers (insurers) are pooling risks, i.e. many risk-owners paying each a price to sell their individual “risk” and few only suffer the actual financial loss by having been affected by the occurrence. Randomness requests that a particular event, the occurrence, is not predictable. This implicitly focuses on two aspects:

• Time (when?)

• Likelihood (if ?)

One old principle of insurance ethics needs to be strictly adhered to safeguard randomness which is utmost good faith (uberrimae fides) between the parties. This requests proactively sharing any information between risk-owner and risk-taker which a prudent underwriter might consider as risk-relevant.

Moral risk, a situation where the insured is acting differently from how he would be acting without insurance, needs to be considered carefully in this context as well. For example insuring ‘extra costs due to unforeseen ground conditions’ might lead to less sophisticated analysis of geological conditions as the insurance product is cheaper in comparison to the analysis. This in turn would increase likelihood of the occurrence.

Risk-takers buying risk for receiving money only in cases where the actual occurrence for any single given risk is a priori unpredictable.

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 12

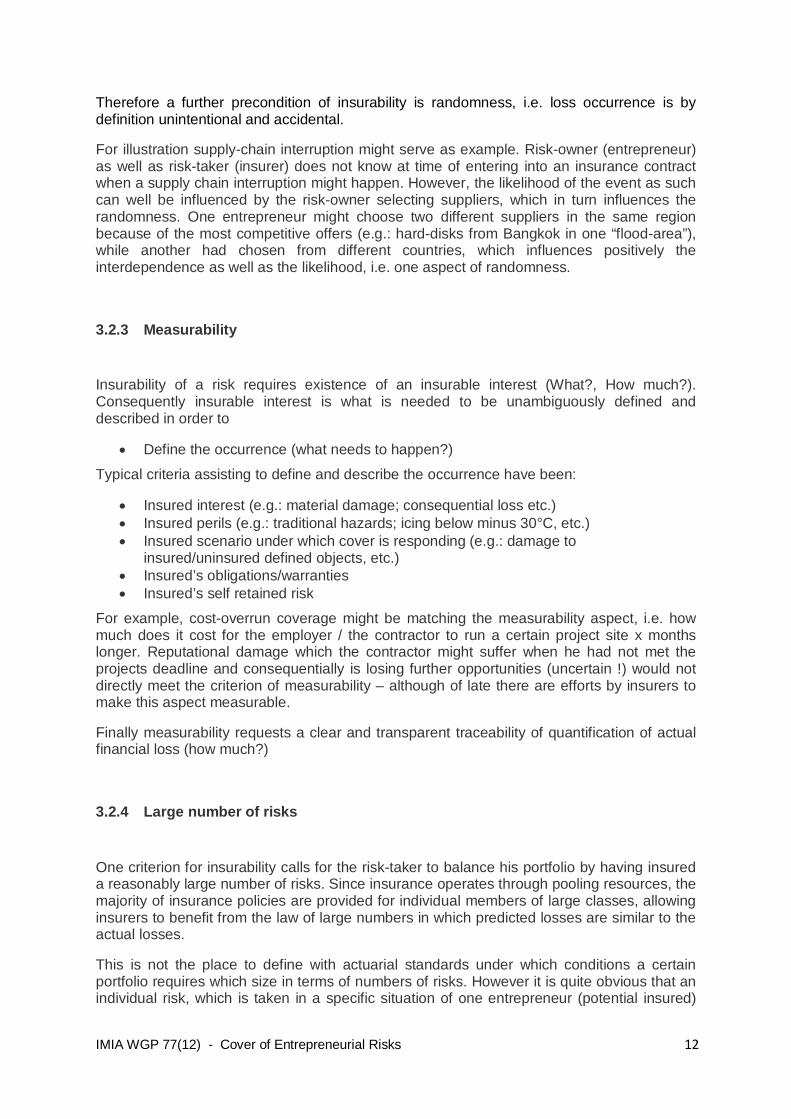

Therefore a further precondition of insurability is randomness, i.e. loss occurrence is by definition unintentional and accidental.

For illustration supply-chain interruption might serve as example. Risk-owner (entrepreneur) as well as risk-taker (insurer) does not know at time of entering into an insurance contract when a supply chain interruption might happen. However, the likelihood of the event as such can well be influenced by the risk-owner selecting suppliers, which in turn influences the randomness. One entrepreneur might choose two different suppliers in the same region because of the most competitive offers (e.g.: hard-disks from Bangkok in one “flood-area”), while another had chosen from different countries, which influences positively the interdependence as well as the likelihood, i.e. one aspect of randomness.

3.2.3 Measurability

Insurability of a risk requires existence of an insurable interest (What?, How much?). Consequently insurable interest is what is needed to be unambiguously defined and described in order to

• Define the occurrence (what needs to happen?)

Typical criteria assisting to define and describe the occurrence have been:

• Insured interest (e.g.: material damage; consequential loss etc.) • Insured perils (e.g.: traditional hazards; icing below minus 30°C, etc.) • Insured scenario under which cover is responding (e.g.: damage to

insured/uninsured defined objects, etc.) • Insured’s obligations/warranties • Insured’s self retained risk

For example, cost-overrun coverage might be matching the measurability aspect, i.e. how much does it cost for the employer / the contractor to run a certain project site x months longer. Reputational damage which the contractor might suffer when he had not met the projects deadline and consequentially is losing further opportunities (uncertain !) would not directly meet the criterion of measurability – although of late there are efforts by insurers to make this aspect measurable.

Finally measurability requests a clear and transparent traceability of quantification of actual financial loss (how much?)

3.2.4 Large number of risks

One criterion for insurability calls for the risk-taker to balance his portfolio by having insured a reasonably large number of risks. Since insurance operates through pooling resources, the majority of insurance policies are provided for individual members of large classes, allowing insurers to benefit from the law of large numbers in which predicted losses are similar to the actual losses.

This is not the place to define with actuarial standards under which conditions a certain portfolio requires which size in terms of numbers of risks. However it is quite obvious that an individual risk, which is taken in a specific situation of one entrepreneur (potential insured)

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 13

only and is not comparable with other similar risks, rather disqualifies for insurability under the aspect of large numbers (e.g. market introduction of a new product). On the other hand, for large insurers such new risks might serve as a good diversification in the sense of the previously discussed independence of risks.

3.3 Summary

The previous chapter was focused on elaborating on some criteria for prudent underwriting, such as

• Preconditions of risk analyses o Chance to win? o Risk or uncertainty? o Full information at time of / during risk taking

• Criteria of insurability o Independence o Randomness o Measurability o Large Number of risks

Entrepreneurial risks are typically individual to a certain extent. Insurability requests uniformity to a certain level. This dilemma could be approached systematically by analysing the criteria discussed.

These criteria could serve for a selection of risk-types where it might be worthwhile to consider further steps of product design.

In total it could be stated that responsibility of correct risk identification as a basis for appropriate “terms & conditions” is transferred from risk-owner to risk-taker.

4. Specific Risks and Insurance

4.1 Sabotage, Strike and Lockout

4.1.1 Description of Risk One of the risks considered in this chapter is loss or damage caused by riots, sabotage, strikes and lockouts. This risk is included in the category of political risks, but it depends on political, economical and sociological factors of the country the risk is situated in. The main peril here is damage to the property in course of construction caused by persons involved in the abovementioned events, including those who are taking part in the protest and those who on behalf of the civil authorities try to suppress a violation of public order. Additionally these risks can cause, even without property damage, a significant loss for the contractor and the investor due to delay to the original time schedule and the corresponding loss of revenue. Usually, contractor and owner are carrying this risk together, as per their contractual obligations.

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 14

4.1.2 Underwriting Considerations Such risks, if covered, require very careful underwriting. The most reliable guide is recent experience in the territory concerned, although the conditions may change rather rapidly. There are several countries where industry-specific or nationwide strikes occur rather often. Of course the underwriting of such a risk in these territories should be carefully considered. The underwriter also should take into account the following political, economical and social events that can occur during the construction period and thus increase the possibility of the insured event:

• Presidential or parliamentary election(s) and similar political events • Major sports events • Major religious events • Long-lasting economical or political instability

The risk is most likely to occur in the capital cities, with a high population density and mostly for civil engineering projects. Sometimes the insured project itself may be the reason for a riot. In this case, if the socio-political situation around the project is unstable before the beginning of construction and we cannot clearly say that this damage caused by violation of public order is unforeseen, it is better not to provide such a coverage. The risk is insurable if:

1. the peril is sudden and unforeseen for the parties who are carrying the risk and, 2. there are certain statistics concerning the number of such events and the scope of

damage for the pertinent period and, 3. insurer and insured have agreed the scope of cover.

Normally, a strike affecting only the insured or only one site should be excluded due to the inherent moral hazard.

4.1.3 Market and Products As Contractor and Owner have little influence on these risks, it is in their interest to find an insurance solution for it. The most wide-known coverage extension is a Strikes, Riots and Civil Commotions Extension of standard Contractor’s (Erection) all risks coverage (SRCC).

• The risk here is clearly defined: Only sudden and unforeseen events are covered, including damage caused by those involved in the violation of public order and damage caused by the prevention or suppression of actions of these persons.

• Only direct material damage is covered, all the consequential losses connected with the deprivation of the insured property and cessation/slowdown /termination of works are excluded.

• There are certain statistics based on the usage of such a coverage and appropriate rating tools.

• Mostly all the insurance markets are ready to provide such a coverage. Market capacity can differ from country to country, but in general such risks are included in the reinsurance treaties with certain limits. There are also the possibilities to insure such risks via insurance/reinsurance pools.

The portion of this risk for which no standard traditional insurance solution is available, is the risk of project delay and associated cost overrun and loss of profits. However, to a limited extent some insurers have developed specialised coverage solutions for this. These however are not sold as extensions of standard covers, but on a stand-alone basis.

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 15

4.2 Design errors

4.2.1 Description of Risk Describing design errors is a very extensive and complex matter. It is very important here firstly to introduce the definitions of “defect” and “damage”, the difference of them and also to differentiate between “defects cover“ for building and civil engineering projects and for mechanical and electrical engineering projects. To cut a long story short: A defect is a condition and damage is an occurrence. Property can be defective (i.e. in defective condition), without being damaged in the usual insurance sense by an occurrence that happened at the insured place and time. And this is the main issue with the defects cover. As an example, the building under construction may have a defect in design, known to the contractor, but it has not collapsed and there is no damage. Or, another example from a mechanical engineering project: It was found during the cold testing that there is a defect in turbine blades. But as there were no load conditions and no testing damage has not occurred yet. Another important part here is consequential loss. A relatively minor defect can result in fire, explosion or collapse with catastrophic consequences. For example, a steel framed building collapses due to defective nuts and bolts in framework construction. In general, defects can be considered as being attributable either to design, specification, material or workmanship. In civil engineering most of the huge losses caused by defects were connected with design errors. However, the insured contractor usually is not responsible for the design, as it is the responsibility of the architect and consulting engineer. In electrical and mechanical engineering projects such losses are connected mainly with the prefabricated main aggregates (turbines, engines, furnaces, boilers etc.) and their parts. Here, the contractor may often not be responsible for the design of these machines and for the materials used. So we can subsume that for CAR policies the main risk is driven by designers’ errors and for EAR by manufacturer’s errors (which include design and material defects).

4.2.2 Underwriting Considerations As defects cover is a complex matter, a number of important aspects need to be considered when granting it. Here again, a distinction between construction and erection risks needs to be made.

For civil construction the main risk factors are the following: 1. Constructor’s and main subcontractors’ experience, loss record 2. Designer’s experience, loss record 3. Complexity of project 4. Degree of innovation (prototype) of the project 5. The existence of an independent technical inspector and the frequency of his site

visits. 6. The existence of wide spans

For the mechanical and electrical engineering projects:

1. Installing constructor’s and main subcontractors’ experience, loss record 2. Manufacturer’s experience, loss record 3. The extent and degree of new technology use, if any 4. Loss experience of items before design change, if any 5. The type of machinery and its location (i.e. the exposure of adjacent property) 6. The value of machinery 7. The existence of an independent technical inspector and the frequency of his site

visits.

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 16

4.2.3 Market and Products Historically, insurers insisted on the total exclusion of all four types of defects, as the costs of remedying such defects is perceived to be a commercial risk. As the insured contractors felt uneasy with this total exclusion and argued that there are certain good reasons to widen the coverage Insurers, following due consideration of the case, may be ready - to a limited extent - to provide coverage as expressed via the following standard exclusions that imply different levels of coverage:

- DE1 - total (outright) exclusion, - DE2 - extended defective condition exclusion, - DE3 - limited defective condition exclusion, - DE4 - defective part exclusion, - DE5 – design improvement exclusion. Or - LEG 1- outright defects exclusion, - LEG 2 - consequences defects exclusion, - LEG 3 – improvements defects exclusion.

In terms of market capacity, it needs to be noted that nowadays in most treaties the full defects coverage is excluded.

4.3 Subcontractor/Supplier Insolvency

4.3.1 Description of Risk

General contractors are usually investing a lot of work in selecting suppliers and subcontractors who can serve best the interests of the project. In turn, principals need to apply the same scrutiny when selecting contractors. However contractors’, subcontractors’ or suppliers’ defaults might occur.

Defaults can be of financial nature, e. g. one of the parties becomes insolvent and therefore incapable of fulfilling its further obligations. Or the party does not fulfil its obligations for other reasons, e. g. mismanagement. This is a risk on every very large project and can cause a lot of negative implications such as:

• Additional costs • Delay • Uncertainty regarding ownership • Quality

4.3.2 Underwriting Considerations

The general contractor as well as the owner has a large interest in mitigating or transferring risks associated to defaults.

The mitigation may involve e.g. a detailed subcontractor prequalification process and quality assurance program.

Part of the underwriting process for any such risks will have to be a careful analysis of the owner’s or constructor’s selection process of contract partners. Further, prior experience

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 17

with contractors and sub-contractors needs to be evaluated. The financial solidity of contract partners plays an important role. Further, to reduce the moral hazard that only very adversely exposed projects of a contractor are insured (anti-selection), ideally all or most projects of the contractor in a year need to be insured (mandatory cession).

4.3.3 Market and Products

Specifically for subcontractors an insurance solution is possible for subcontractor default (SDI).

The scope of coverage of SDI includes the costs of completing any unfulfilled subcontractors’ or suppliers’ obligations, including costs related to subcontractor replacement, job acceleration, extended overhead, liquidated damages and claim preparation expenses.

Additional features include:

• Indemnification for direct and indirect costs resulting from default in performance of any enrolled subcontractor or supplier

• Broad coverage for all enrolled subcontractors and suppliers that qualify under the contractor’s pre-qualification system

4.4 Volatility of Commodity Prices, Interest Rates, Inflation and Exchange Rates

4.4.1 Description

The volatility of commodity prices, interest rates, inflation and exchange rates pose a real threat to the entrepreneur’s success in their business as the volatility is largely out of their control. These risks are largely influenced by a country’s economy as well as that of the global economy. These risks are not only experienced by individual companies but also by governments who, due to the volatility of the aforementioned risks, struggle to manage their budgets and achieve their debt targets. For the last several decades governments have tried to stabilize these factors and still give it their full attention.

Commodity Prices

For the purpose of this paper commodities are physical, like oil, iron ore or wheat. Commodity prices fluctuate depending on the local and global demand for the raw materials. As such companies are exposed to the volatility of commodity price and sales prices of goods. For example if a company cannot pass on increased costs of a commodity to its customer this will directly affect its budget and profits. Similarly if a supplier/exporter experiences a drop in the value of its commodity and inventories his borrowing costs may increase. A commodity which affects most entrepreneurs is energy; not surprisingly as energy represents 50% of the world economy exports.

Interest Rates

The rise and fall of economic activity, changes in investment preferences and credit ratings are the main factors which affect interest rates. These fluctuations can have a direct influence on companies if they have long term debt. For example if a company arranges a

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 18

long term contract in a developing country and receives fixed agreed interim payments, but his long term debt is financed with a variable interest rate, then adverse increases in interest rates will affect its overall profit.

Exchange Rates and Inflation

As much foreign investment pours into developing countries, companies continuously have to deal with the volatility of local country currencies and inflation. If for example international contractors who report in their own currencies get paid in a local currency then any local currency devaluation will adversely affect their profit. Similarly if an infrastructure project, such as a power plant, has foreign investment then as the tariffs are paid in local currency the profit will suffer on any downturn of the local currency. Worse still would be if the power plant were powered by oil (a tradable commodity and hence a world price), then local currency devaluation would only add to the investor’s problems. Often the volatility of exchange rates is addressed in contracts by way of formulas which adjust payments over time, but this is not always the case, and indeed in these cases it is the clients who bear the exchange rate risk. Exchange rates and inflation rates are interrelated, as indeed are interest rates. In countries that have low inflation their currencies tend to strengthen whilst those who have high inflation often see devaluations of their currencies. It is generally agreed that increases in commodity prices or production and labour costs, and an increase in supply of money or increase in demand of supplies can lead to high inflation.

4.4.2 Underwriting Considerations

The volatility of commodity prices, interest rates, inflation and exchange rates are a very well known phenomenon and are common risks to private companies and governments. History has proven that these risks can be successfully insured against by banks and insurance companies.

Insurability of such risks depends on whether one can predict to some degree of probability the trend of such volatility. Market analysts do this on a regular basis where some trends are easier to predict than others. Analysts can use historical data to help determine future trends. Even the new appointment of governments can indicate trends based on their manifestos, assuming that they keep their promises.

Governments and their politics have a huge impact on these risks. By keeping budget deficits low, curbing the amount of money supply and spending, reducing reliance on foreign currency debt are some ways to control interest rates, inflation and exchange rates. Commodity price fluctuations are harder to control as these are determined by global supply and demand.

4.4.3 Market and Products

As mentioned above there are markets and products available to insureds to protect them from the volatility of the aforementioned risks.

The standard product available to those who wish to minimise these risks is called hedging. Hedging comes in many forms and specifically for the risks of commodity prices, interest rates, inflation and exchange rates available products essentially provide a so-called “cap” or “floor” to the upward or downward volatility of the risk. Put simply in exchange for a premium

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 19

if the trend is upward or downward the insured is protected against its risk exceeding predefined upper and/or lower limits.

These hedging products are typically banking products. In insurance solutions typically these risks play an indirect however sometimes very substantial role: E.g. in the case of business interruption or delay a possible loss of income/profits can heavily depend on commodity prices. This can e. g. also influence the indemnifications paid under ALoP/DSU covers.

4.5 Non-Fulfillment of Agreed Specifications

4.5.1 Description

There are many different ways in which a situation can occur where contractually agreed specifications of a product are not met. In the following these are split into three categories:

Type of product: Machinery

There is a large array of specifications which might be required relative to the provision of machinery and equipment. These specifications can be environmental (emissions, energy consumption, efficiency), throughput-related (flow rate, energy generated at peak and mean operating regimens), quality-related (purity of product) or financial (operating cost, maintenance cost), or related to its short or long term availability. Specifically for plants, often certain performance requirements are agreed upon which are measured at the point of commissioning. E.g. for a power plant this would typically be a certain MW output.

Type of product: Structure

If the product is a structure rather than a machine, the specification might dictate that it carries a specific volume of traffic, easing transport problems in a metropolitan area. In the case of a bridge, there might also be requirements for it to remain operational during periods of high winds, and in the case of a tunnel, a need to efficiently expel exhaust fumes rapidly during periods of heavy use.

For a manufacturing plant this could be a certain throughput rate.

Type of product: Fit-out

The products, fixtures and furniture installed at the completion of a construction project, for instance in a hotel project, will by necessity have to withstand regular heavy use without significant signs of deterioration, thus maintaining an acceptable appearance and having a high availability level.

4.5.2 Underwriting Considerations

For products constructed, erected or installed which are not performing as intended or as agreed, the criteria for insurability needs to be established clearly and immediately. In order to establish a possible basis for insurability the details of the specification must be revealed in full, and this specification cannot be random or bespoke, but must have a clear, objective mechanism for assessing the extent to which the specification is being met or missed. Underwriters presented with this mechanism might seek to investigate and model examples

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 20

of a failed specification and acceptable failure rates in order to establish indemnity scenarios.

It is common in the supply of industrial equipment and structures that a guarantee of sorts will be provided. This may be in the form of a service agreement, a financial incentive (or more often a penalty or liquidated damages), or most often both. It would be usual for the guarantee provider to be the buyer of the insurance product

If it is to be in any way insurable, the provision of guarantees of any given specification must be wholesale and cannot allow selection of the most challenging risk exposures.

4.5.3 Market and Products

For material damage product guarantees, there exists already an established insurance solution. Such policies are related to products where the failure modes are specified and their homogeneous nature allows an assessment of the anticipated rates of failure or damage, howsoever defined.

Products which may fail to fulfil their specification for reasons other than material damage may yet be afforded a degree of insurance cover. The Liquidated Damages Insurance product is long established and can be insurable when the amounts levied are a reasonable estimate of the cost of a failure to fulfil an element of a contract. These costs are not insurable if they are considered excessive or if they are intended to penalise the party responsible for the failure.

In exploring modes of contractual failure, the grey area between physical damage and acceptable performance of a product is inhabited by the often highly-subjective nature of what constitutes satisfactory performance. Specific measurable elements such as flow rate, availability percentage and output are contractually simple to adjust with liquidated damages. However into the grey area will fall certain situations which are beyond the control of the product supplier or contractor: Lack of sun or wind for renewable power, low take up rates for a new toll road, or a change in consumer preference.

As far as plant performance at commissioning is concerned, insurance offerings do exist. These would be typically for the contractor and indemnify for liquidated damages payable. Insurers will often be required to insure a contractor’s whole project portfolio (as opposed to individual projects) against liquidated damages payments, in order to avoid anti-selection.

4.6 Cost Overrun

4.6.1 Description

Cost Overrun is fundamentally the risk of exceeding budgeted costs for a specific construction project. Since more and more projects are sold on fixed priced basis “cost overrun” is a significant risk faced by those involved in construction and engineering projects.

Cost overrun can arise from a multitude of directions:

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 21

Owner/ developer risk: Delay in land acquisition or access to land or unforeseen change orders. Both can result out of unforeseen factors such as change in environmental law, local environmental complaints etc.

Contractors Risks: Increased costs of materials or liquidated damage payments for delay in completion.

The allocation of such cost overrun risk varies from project to project. It is of major concern for both owners and contractors and is commonly a hot topic during project execution. A contractor suffering from Cost Overruns or delays (that can result in time liquidated damages at the end of the project) can recover the losses by overcharging or demanding extensive time allocations for the change order placed by the owner during the project execution.

Today this risk is mitigated contractually between owner and contractor through “cost certain” contracts (where the contractor bears the majority of the cost overrun risk), “costs plus” basis i.e. where the contractor does not have the risk of cost escalation above budget but equally its income is restricted to an agreed percentage over and above actually incurred costs. In simple terms, whichever party has the risk has the option to include some form of contingency within their budget. This then allows for an element of protection against cost overrun, but at the same time it is usually restricted in amount in order to maintain competiveness.

The project owner/developer can offset much of his risk of project cost overrun by requiring bids from contractors on a “fixed price” basis and also purchasing DSU type coverage for such financial cost overruns as those involved in re-financing a debt servicing programme due to project delays. Contractors generally have far less ability to in any way transfer the cost overrun risk and their own costs can also be dramatically impacted by a delay in completion, particularly as many fixed price contract are also “date certain” and apply liquidated damages for delayed completion. Some solutions are the profitable change orders or short cuts in the construction works that inherently lead to an end product of lower quality than originally planned for.

4.6.2 Underwriting Considerations

As with all risks, the classical trigger factors , limits, underwriting information and accumulation control have to be considered in the underwriting analysis. Regarding the cover itself – special consideration must be paid to avoid the cover acting as an alternative solution to a bad contractual arrangement between owner and contractor but rather to act as balance sheet in case unforeseeable events occur.

One strong sales argument to implement entrepreneurial covers, such as Cost Overruns, is to have a close relationship between insurer and the insured. Consequentially, it may be a good starting point to have this type of cover on an annual basis.

4.6.3 Market and Products

In terms of the insurance of such risks, perhaps the most innovative coverage was that developed some 20 years or so ago and known as “Sponsor”. This was specifically designed to cover project cost overrun following both damage and non-damage events, but

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 22

gained very little attraction amongst potential buyers at the time and quickly disappeared from the market. It would perhaps be interesting to review this product and the concept behind it with a view to further consideration of its viability as a sustainable and sellable product. Another example would be the various forms of “Force Majeure” insurance, particularly those relating to non-damage events such as change of law and labour disputes.

Specifically for the risk of construction delay insurance options do exist. These are offered in the form of liquidated damages cover for the contractor or non-physical damage delay cover for the owner. In the latter case loss of profits in excess of what the owner can recover from the contractor can be insured.

4.7 Unforeseen Ground Conditions

4.7.1 Description

Project cost overrun can come from a multitude of different events or circumstances but particular examples would be those that arise from Unforeseen Ground Conditions (UGC). This is a very good example of a risk that was in the past largely retained by the owner/developer (particularly when it was a government body) but it is these days very often a risk – including the cost overrun associated with it – that is left with the contractor. Whilst UGC can be a problem on virtually any kind of construction or erection project, it is of course most relevant to tunnelling projects. The direct project overrun risk of such projects of course relates to the increased cost of construction due to for example more grouting, temporary lining or greater areas of more resistant final lining than envisaged at bid stage. Typically a Contractor includes an allowance within its contract price for UGC and if the ground conditions are better than expected then they make a profit. Conversely, if they are worse than expected then the contingency is fully utilised and additional cost above that is for the contractor. Occasionally, the owner/developer decides to retain the risk of UGC provided that the contractor maintains “skin in the game” and they will then reimburse the contractor for costs in excess of what is effectively a “self insured retention” as regards such costs. The risk can of course be dramatically reduced by more detailed geotechnical investigation before commencement of works, but typically the contract price has already been agreed to at a much earlier stage in the process.

4.7.2 Underwriting Considerations

As Unforeseen Ground Conditions is a subclass of the above described Cost Overrun – the same underwriting considerations apply for this cover as well.

4.7.3 Market and Products

We understand that some insurers have previously offered cover for project cost overrun due to UGC, based upon the Contractor first fully utilising a realistic contingency allowance within their contract price and then limiting cover to perhaps the same amount again in excess of that, i.e. a 100% margin of error on the contingency allowance within the contract. However, beyond what is covered within a CAR Policy, the risk of UGC is currently largely

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 23

uninsured and represents a significant entrepreneurial risk, typically for the contractor rather than the owner/developer.

4.8 Insufficient Supply Chain Management and Transport Delay/Disruption

4.8.1 Description of Risk

Recent events like the volcano eruption of the Eyjafjallajökull in Iceland causing the closing of major European airports or the Japanese earthquake and tsunami of 2011 preventing supplies to the global semiconductor or automobile industry, demonstrated once again the vulnerability of supply chains in a globalized world.

In construction projects up to 90% of project cost refers to material or equipment supply or services to the site, often in a fragmented way involving up to hundreds of different parties making the construction industry particularly dependent on supplies.

Supplied material is required to be on-site in–time in order to have a continuous construction process. On the other hand on-site logistics tend to reduce stand-still periods and overcapacities.

With further globalization there is a trend to international suppliers which again rely on sub-suppliers which increases the fragmentation of the supply chain.

Failures in the supply-chain design can cause increased project costs but also project delay, which can imply liquidated damages to the main contractor.

The main contractor has therefore a financial interest in avoiding problems in the supply chain.

Disruption of a supply can have a variety of reasons, apart from natural events, and just to mention some of them, it can be caused by production problems of the supplier, labour unavailability or skills shortage, insolvency of the supplier, accidents or political risks. Not always a problem in the supply chain is attributable to a material damage accident in the supply chain.

4.8.2 Underwriting Considerations

The complexity of an existing supply chain can cause tremendous challenges to the underwriters to assess the various exposures5:

• First- , second- and third-tier suppliers

• Globalization, single sourcing and outsourcing

• Business contingency planning

• High level of dependence of insured on the supply chain

• Willingness of insured to constantly improve the resilience of its supply chain 5 Supply Chain Insurance – Can it be an attractive Product? Insurance Issues 06/2011 Leo Ronken , Gen Re

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 24

• Monitoring of accumulations with other risks in portfolio (also from other business lines)

• Possible concerns of the insured about disclosure of confidential information

• Build up of the sustainable portfolio taking into consideration the one-off character of construction projects

As described previously in this paper the question of insurability has to be assessed for each single entrepreneurial risk, by checking basic principles of insurability.

Some examples of uninsurable risks:

Own errors and omissions of the insured (example: delayed arrival of equipment because the procurement for this equipment was done too late.)

Wilful acts of suppliers (example: withholding the supply due to non-payment or other breaches of contract by the insured)

Important aspects of underwriting:

• Map out critical supply chains and profit dependencies • Assess every named supplier and the most important sub supplier • Consider also industry suppliers exposure from political, economical and structural

perspectives • Define and evaluate risk scenarios • In order to be in the position to monitor accumulations, the suppliers must be namely

known to the insurer. • Who is the insured? The main contractor? The supplier (depending on sub-

suppliers)? • The indemnity structure has to be clearly defined: Compensation for liquidated

damages caused by an interruption of the supply chain? Or for increased costs to find another supplier? Both?

4.8.3 Market and Products

Delay in Start-up or Advanced Loss of Profits covers can include suppliers’ extensions. This extension covers delays in project completion arising from damages to suppliers’ premises. The beneficiary of this cover is the principal and the insured perils are normally limited to material damage which would be compensated under the project policy.

Contingent Business Interruption covers (for operational risks) follow a similar loss trigger, as described above.

In recent years a new insurance product has come up, the so called Supply Chain Insurance. This Product tries to complement the two covers mentioned before by adding also non-material damage triggers. It is predominantly requested for operational risks and with focus on high-tech industry such as semi-conductor and automobile. Although a transfer of this product to the construction industry would be in principle feasible the actual experience on the operational risk side is not that promising as the success of this product in the insurance market is so far rather limited. Due to unresolved challenges such as accumulation control or lack of loss probability data, underwriters tend to protect themselves by offering limited coverage, lower loss limits, only named suppliers, high self retentions, hence offering a product that meets only partially the demands of the insured and certainly not the all-in-one insurance cover for every purpose.

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 25

Another insurance product focussing on transport disruption or delay is the trade disruption insurance. It covers loss of gross earnings and extra expenses caused by political risks such as embargoes, confiscation, terrorism, strikes, political violence or war, blockage of waterways or closing of ports, but also natural perils as well as the insolvency of a dedicated supplier or customer. The extra expenses can be additional transportation costs or costs of alternative sourcing.

5. Conclusion and Outlook

Whilst a number of the risks discussed in the previous chapters are inherent in the day to day business of the construction/engineering industry, other entrepreneurial risk taking is done with the specific purpose of creating additional profit and revenue growth.

Insurance, as addressed in the previous chapter, effectively only provides hedging or protection against the occurrence of a downside risk. Entrepreneurial risks placed in the insurance markets are typically at least to a degree quantifiable using traditional methods, e.g. measurement of probability in terms of both severity and frequency of losses occurring. For Insurers the obvious aim is to gather more premium than they pay out in losses and this fundamental approach cannot be forgotten when searching for the pre-conditions that could enable Insurers to expand the area of coverage for entrepreneurial risks.

Bearing in mind that a significant area of entrepreneurial risk taking has the aim of securing higher profits for the company in question, a possible product development for Insurers could be one that covers the downside but also shares in the upside? This would of course be transformational in terms of insurance product and require a fundamental change of direction for an insurance company. However, this may be a possible future scenario for Insurers, but would at the same time take them into competition with other financial instrument providers, primarily the banking sector. The scope of what that new landscape for Insurers may look like is outside of the realm of this particular IMIA Working Group Paper.

In addition to the examples of insurance products for entrepreneurial risks referred to above, there are of course other more "standard" risks to which Insurers have managed to adapt. An example would be the evolution of the design parameters of gas turbines, where Insurers utilised their knowhow and experience to assess the risks and provide defined coverage solutions that allow a degree of risk transfer of what some might say is an Entrepreneurial Risk associated with research and development. The key in this instance was for Insurers to fully understand the implications of the design changes etc. and to look for a sufficient pricing uplift combined with more restricted coverage than would otherwise be the case for more traditional technology.

It can be appreciated that there are infinitely varied forms of entrepreneurial risks ranging from those that are already on the periphery of traditional insurance - and can be covered and priced for as extensions to more standard policy forms - to those that are currently completely outside of the current underwriting philosophy of Insurers in general. However, by carefully but progressively accepting at least peripheral entrepreneurial risks, with appropriate premium, terms and conditions etc., it is possible to gain more experience on the additional exposures created by such broadening of coverage. The key is clearly the collecting of risk information and its analysis and evaluation both through experiencing losses and of course through proper risk surveying and monitoring. With the evolution of the risks our clients are facing and which are increasingly financial in nature, it is clear that it is

IMIA WGP 77(12) - Cover of Entrepreneurial Risks 26

not enough for Insurers to look only at technically based solutions through employment of engineers etc., but also to employ those that are financially and/or legally trained in order to more fully understand the financial and legal risks that are currently beyond traditional insurance but may eventually become "business as usual" for Insurers of the future.

Last, but not least, insurers should bear in mind that in insurance markets that can be perceived as saturated in terms of capacity, considering new innovative and indeed entrepreneurial types of insurance cover can offer significant opportunities for the insurance industry itself. Not considering this opportunity one might consider an entrepreneurial risk for any insurer concentrating solely on standard coverage solutions. Demand for non-traditional insurance solutions is vast and profitable business opportunities do exist. However, only for a limited number of risks insurance solutions exist, and for some risks only very limited insurance solutions exist. To move the boundaries of insurability significant investments need to be made in product development and new approaches for risk assessment and pricing.

![IMIA Working Group Paper [WGP 114 (19)] IMIA Annual ...€¦ · These can contain material that deteriorates in the presence of water. • The increasing use of partially lined, or](https://static.fdocuments.in/doc/165x107/5f0eff027e708231d441f848/imia-working-group-paper-wgp-114-19-imia-annual-these-can-contain-material.jpg)

![IMIA Working Group Paper [WGP 99 (16)] IMIA Annual Conference … · 2019-10-28 · IMIA – WGP 99 (16) - Natural Catastrophe Modelling for Construction Risks 3 Disclaimer The present](https://static.fdocuments.in/doc/165x107/5e8e3c5361ce6e64462341fd/imia-working-group-paper-wgp-99-16-imia-annual-conference-2019-10-28-imia.jpg)