Imane Karich – Consultante BELSIF – Islamic Banking & Investing Seminar 29 October 2008 ISLAMIC...

28

Imane Karich – Consultante BELSIF – Islamic Banking & Investing Seminar 29 October 2008 ISLAMIC VISION of BANKING & INVESTING

-

Upload

amber-wilkerson -

Category

Documents

-

view

222 -

download

0

Transcript of Imane Karich – Consultante BELSIF – Islamic Banking & Investing Seminar 29 October 2008 ISLAMIC...

Imane Karich – Consultante

BELSIF – Islamic Banking & Investing Seminar29 October 2008

ISLAMIC VISION of BANKING & INVESTING

Table of Content

Islamic Finance – Theory & Concepts

Description of the main islamic financial instruments

2

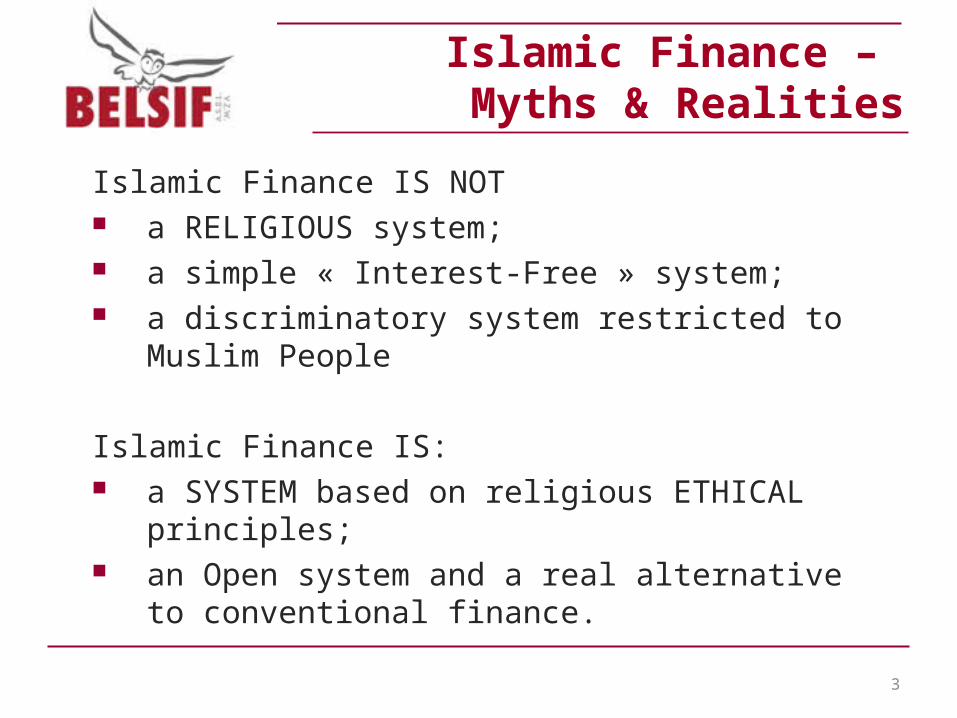

Islamic Finance – Myths & Realities

Islamic Finance IS NOT a RELIGIOUS system; a simple « Interest-Free » system; a discriminatory system restricted to Muslim People

Islamic Finance IS: a SYSTEM based on religious ETHICAL principles; an Open system and a real alternative to conventional

finance.

3

BASIC PRINCIPLES

Islamic Finance is part of the Islamic Economic System, part of the Chari’a System

Islamic Economy is a Normative system supported by moral and ethical values and guidelines of the Islamic Law;

Islamic Finance tends to establish financial equity and preventing injustice in business deals

General Basis Rule of the Economic Islamic System:CORAN - Sourate Al Baqarah - Verse 275 – 1st part:

« God has allowed Trading…. »

Fundamental principle of trading system: exchange of real goods Incentive for Participation and Risk Taking:

Principle of Profit & Loss sharing No transfer of risk with the capital

4

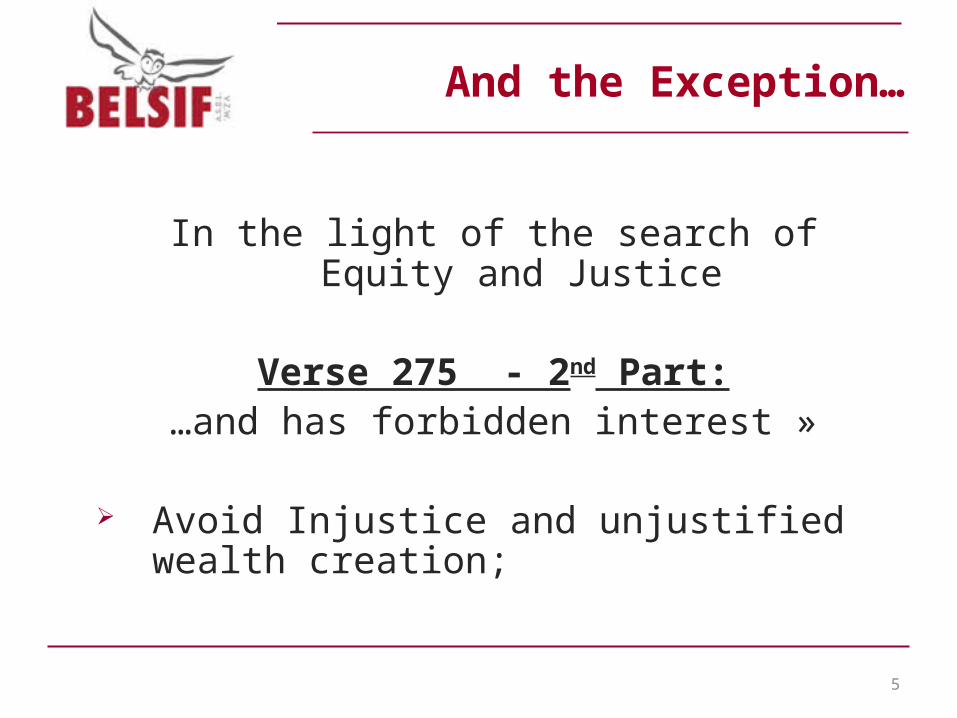

And the Exception…

In the light of the search of Equity and Justice

Verse 275 - 2nd Part:…and has forbidden interest »

Avoid Injustice and unjustified wealth creation;

5

Roles of Money and Definition of Riba

Difference between Usury & Interest ? > Notion and role of Money:

Unity of Measure; Mean of exchange Reserve of Value

Conclusion: no difference between « reasonable » interest and usury

6

Gharar

Fuzziness – Ignorance – Uncertainty in the contractual terms – ex:

Contingency of exchange results, Absence of the good during the exchange, …

≠ Risk taking inherent to trading; Less strict than the interdiction of Riba.

7

Islamic Banking system

Same role as the conventional banking system: Financial intermediary between investors and

entreprenors To improve the efficiency and the liquidity of financial

resources exchange;

The main difference is situated in the risk taking owner : is not transfered with the capital but remains with the property right of the financial resources.

The Bank becomes a privileged partner in Business transactions.

8

Islamic Bank – Basic functioning

Islamic Bank

Contract Mudharaba (or Wakalah)

9

BANQUE

MUDHARIB

RABB

al

MAL

Clients Investissors/depositors

Clients Entrepreneurs/Debitors

Funds mobilisationFunds User

Islamic Vision on Investment

Investment in the sources of Islam: Thesaurisation Zakat Financial Risk Speculation

10

Thesaurisation: Authorised sparing:

Balance and Equilibrium; With a clear objective;

= wealth accumumation without spending or investment objectives on a medium/long term

Zakat: Progressive seizure of the non used wealth;

Islamic Vision on Investment

11

Notion of Financial Risk: Pure Risk vs Financial Risk; Commercial Risk vs Speculative Risk; Profit & Loss Risk; Objective Risk;

Speculation: Bet on a future event on an aleatory and

subjective way; Without rational fundements; Voluntary excessive risk;

Islamic Vision on Investment

12

Investment Universe

Limited investment universe No Alcohol, entertainment, banking, gambling arms…

activities + other specific rules applied to mutual funds (see

later)

13

Description of main Financial Instruments

Based on Islamic Commercial Law and on traditional commercial contracts;

Different categories of contracts:

Participation contracts (PLS based); Musharaka and Mudharab

Financing contracts (debt based) Murabaha and Ijara

14

MUSHARAKA

15

Project Financing

MUDHARABA

16

Project Financing

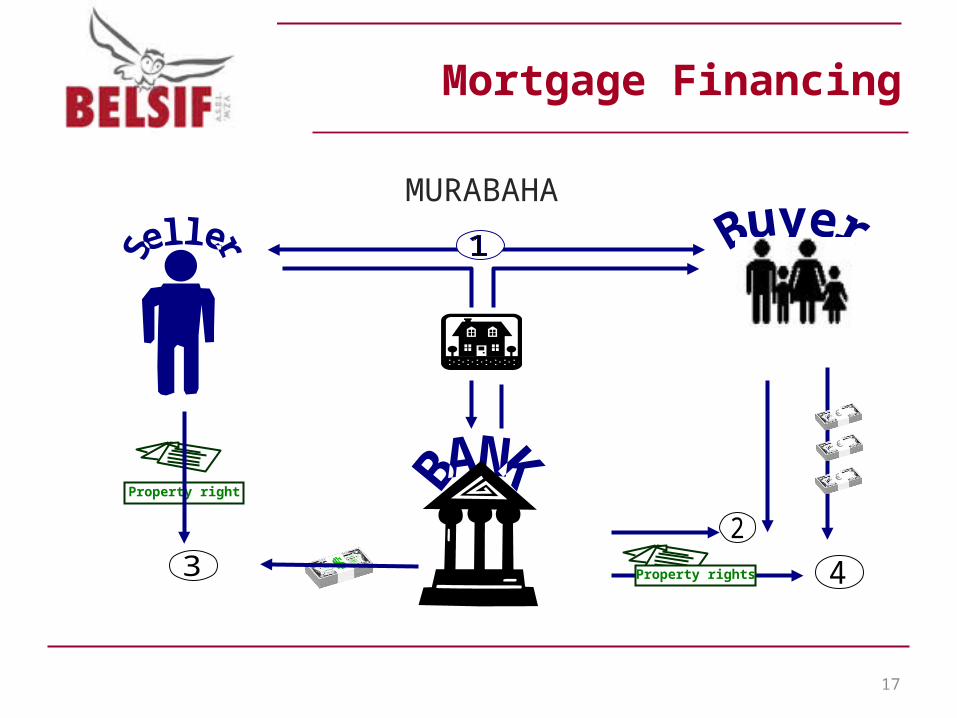

Mortgage Financing

MURABAHA

17

Property right

Property rights

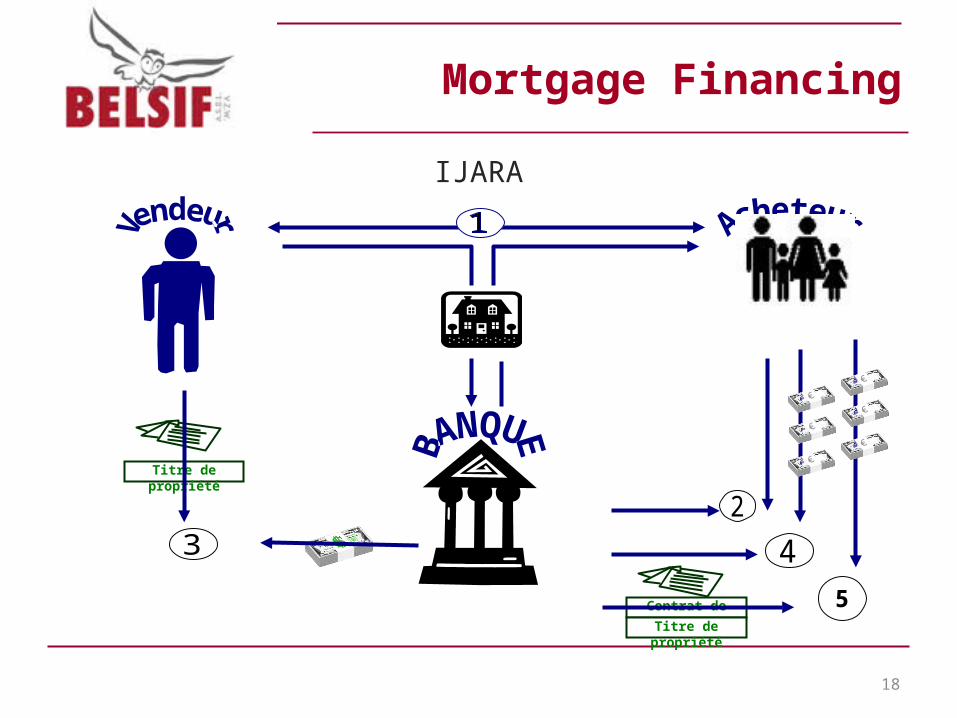

Mortgage Financing

IJARA

18

Titre de propriété

Contrat de vente

Titre de propriété

5

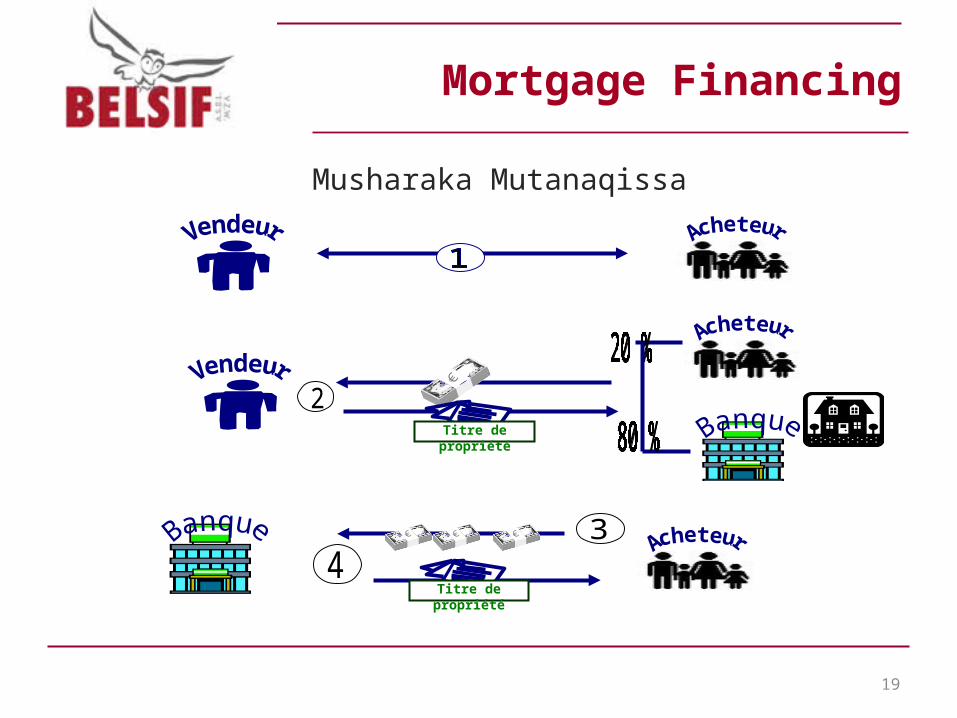

Mortgage Financing

Musharaka Mutanaqissa

19

Titre de propriété

Titre de propriété

Islamic Investment in Practice

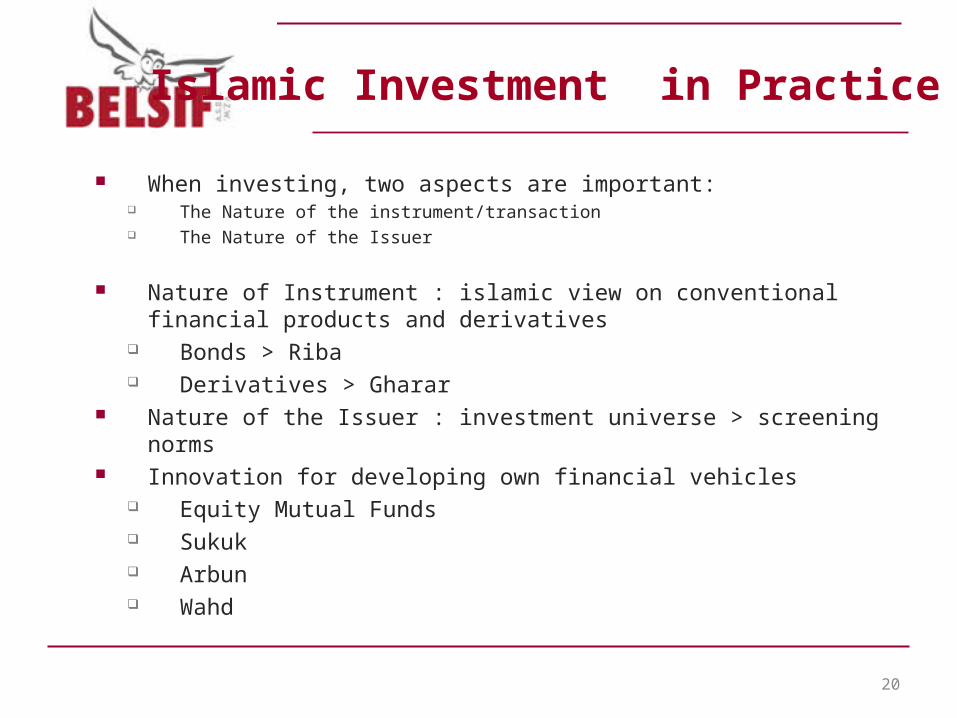

When investing, two aspects are important: The Nature of the instrument/transaction The Nature of the Issuer

Nature of Instrument : islamic view on conventional financial products and derivatives

Bonds > Riba Derivatives > Gharar

Nature of the Issuer : investment universe > screening norms Innovation for developing own financial vehicles

Equity Mutual Funds Sukuk Arbun Wahd

20

Islamic Investment in Practice

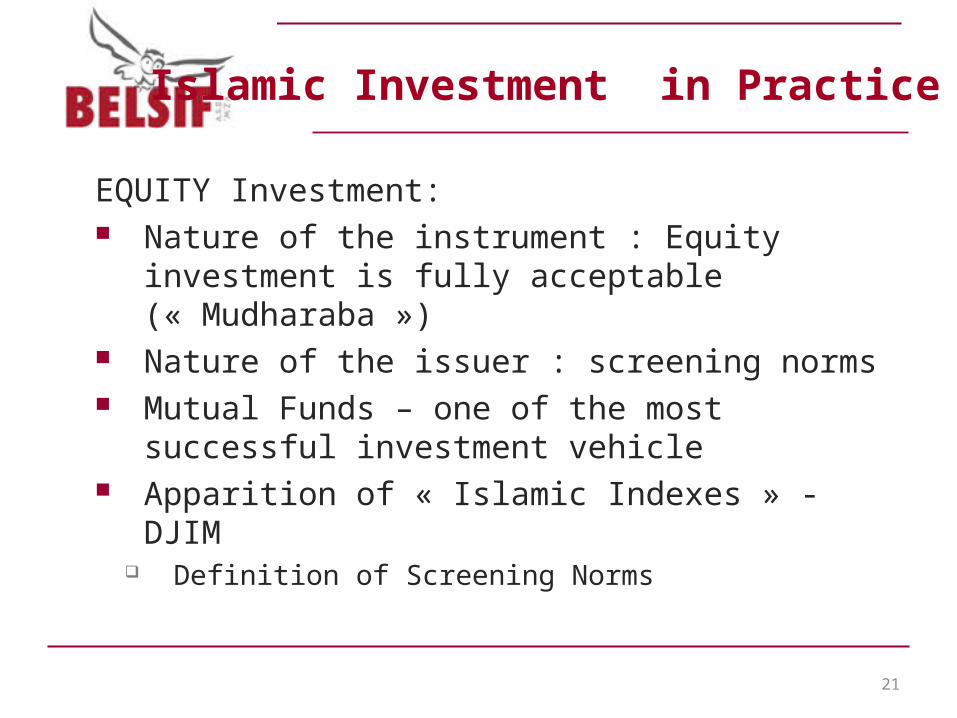

EQUITY Investment: Nature of the instrument : Equity investment

is fully acceptable (« Mudharaba ») Nature of the issuer : screening norms Mutual Funds – one of the most successful

investment vehicle Apparition of « Islamic Indexes » - DJIM

Definition of Screening Norms

21

Islamic Investment in Practice

Screening Norms:1. Business of the Issuer Company (core and secondary activities):

22

Islamic Investment in Practice

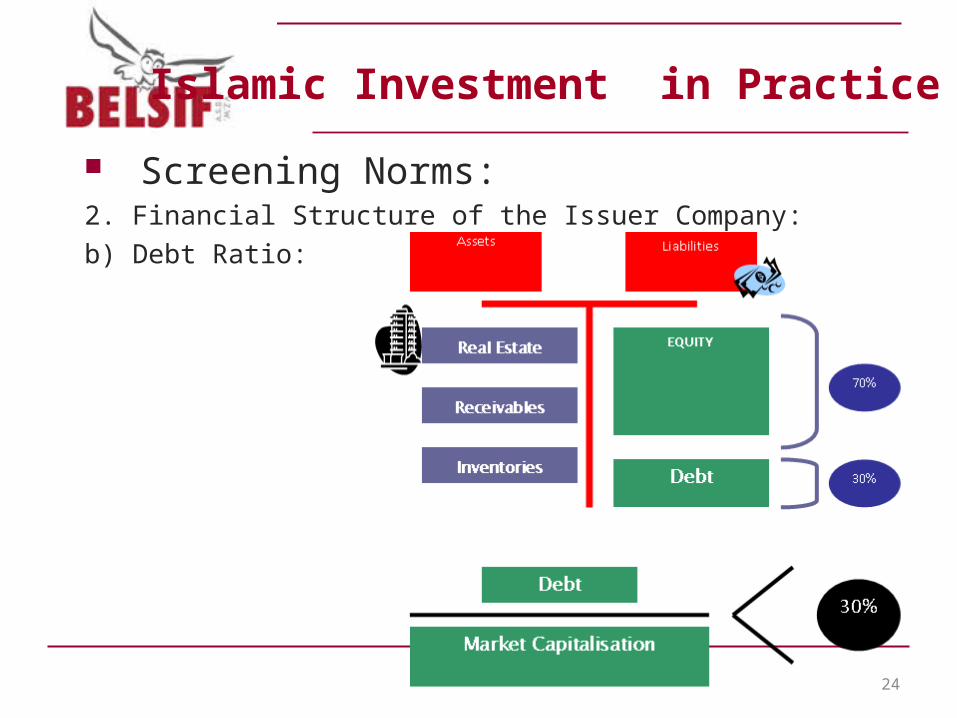

Screening Norms:2. Financial Structure of the Issuer Company:

a) Interest Earnings:

23

Islamic Investment in Practice

Screening Norms:2. Financial Structure of the Issuer Company:

b) Debt Ratio:

24

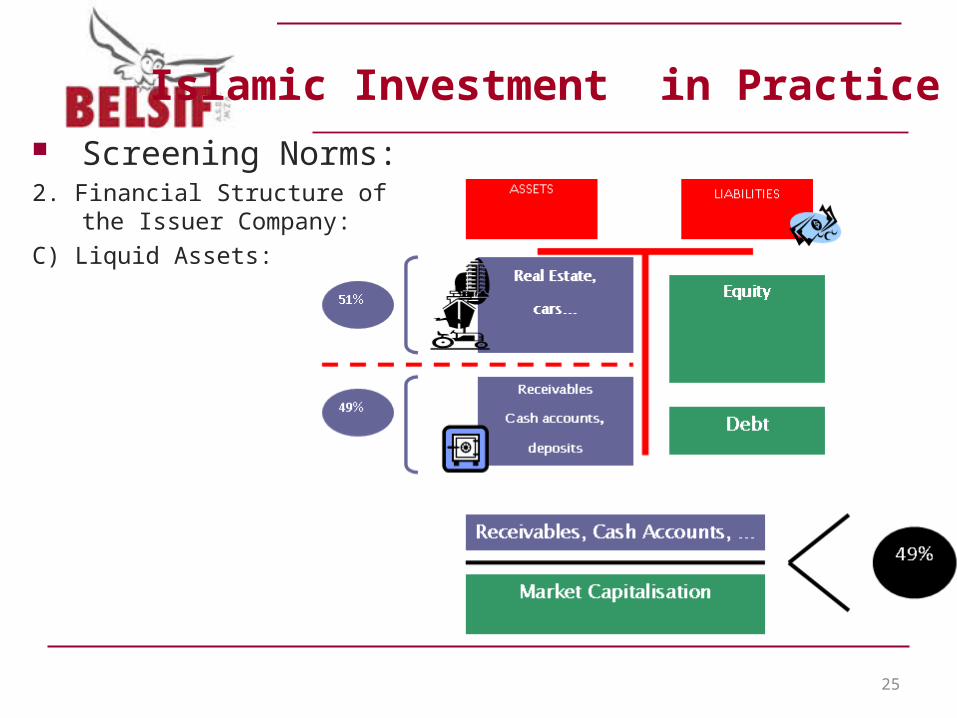

Islamic Investment in Practice Screening Norms:2. Financial Structure of the Issuer

Company:

C) Liquid Assets:

25

Islamic Investment in Practice

Dow Jones Islamic Market Index – DJIM: Introduced in 1999 First benchmarks for sharia-compliant portfolio

management; Performance:

YTD : -27% Since 5 years : +44%

More info : www.djindexes.com

26

Islamic Investment in Practice

Creative engineering – new products: Success of Sukuk investments; Alternative for derivatives products : ‘arbun contracts,

wahd contracts, …

27