III Ipdf.usaid.gov/pdf_docs/pnaca759.pdf · ... Phase III (AP AP III) USAID Contract No. LAG ......

127

I I I I I I I I I I I I I I I LIKELY IMPACTS OF THE GATT AGRICULTURAL AGREEMENT ON AFRICAN AGRICULTURAL TRADE AND DEVELOPMENT May 1997 APAP III Research Report No. 1024 Prepared for Agricultural Policy Analysis Project, Phase III (APAP III) USAID Contract No. LAG-4201-C-00-30S2-00 Authors: Lawrence Kent David Wilcock Cheryl Gwynn Development Alternatives Inc. )

Transcript of III Ipdf.usaid.gov/pdf_docs/pnaca759.pdf · ... Phase III (AP AP III) USAID Contract No. LAG ......

I I I I I I I I I I I I I I I

LIKELY IMPACTS OF THE GATT AGRICULTURAL AGREEMENT ON AFRICAN AGRICULTURAL TRADE AND DEVELOPMENT

May 1997

APAP III Research Report No. 1024

Prepared for

Agricultural Policy Analysis Project, Phase III (AP AP III)

USAID Contract No. LAG-4201-C-00-30S2-00

Authors: Lawrence Kent David Wilcock Cheryl Gwynn Development Alternatives Inc. )

jmenustik

Rectangle

jmenustik

Rectangle

jmenustik

Rectangle

I I I I I I I I I I I I I I I I

TABLE OF CONTENTS

IN'TRODUCTION ..................................... . . . . . . . . . . . . . . . . . . . . . . . iii

PART 1: IMPACTS OF THE AGRICULTURAL AGREEMENT ON AFRICA ........ 1

Summary of Agricultural Agreement ................................... I What Are the Probable Impacts on African Agricultural Exports? ............ I How Serious Is the Preference Erosion Problem for Africa? ................ 5

PARTTI: COUNTRY CASE STUDIES: METHODOLOGY AND SUMMARY-OBSERVATIONS ................................................ 31

Case Study Methodology ........................................... 31 Importance of Looking at Trade Impacts at the National Level ............. 33 Summary of the Degree and Importance of Preference Erosion ............. 34

PARTITI: CONCLUSIONS AND IMPLICATIONS ............................. 37

Conclusions on the Impacts of the AA ................................ 37 Conclusions on Future Directions .................................... 39 Implications for USAID ............................................ 41

BffiLIOGRAPHY ............................................................ 45

ANNEX A. KENYA CASE STUDY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. A-I

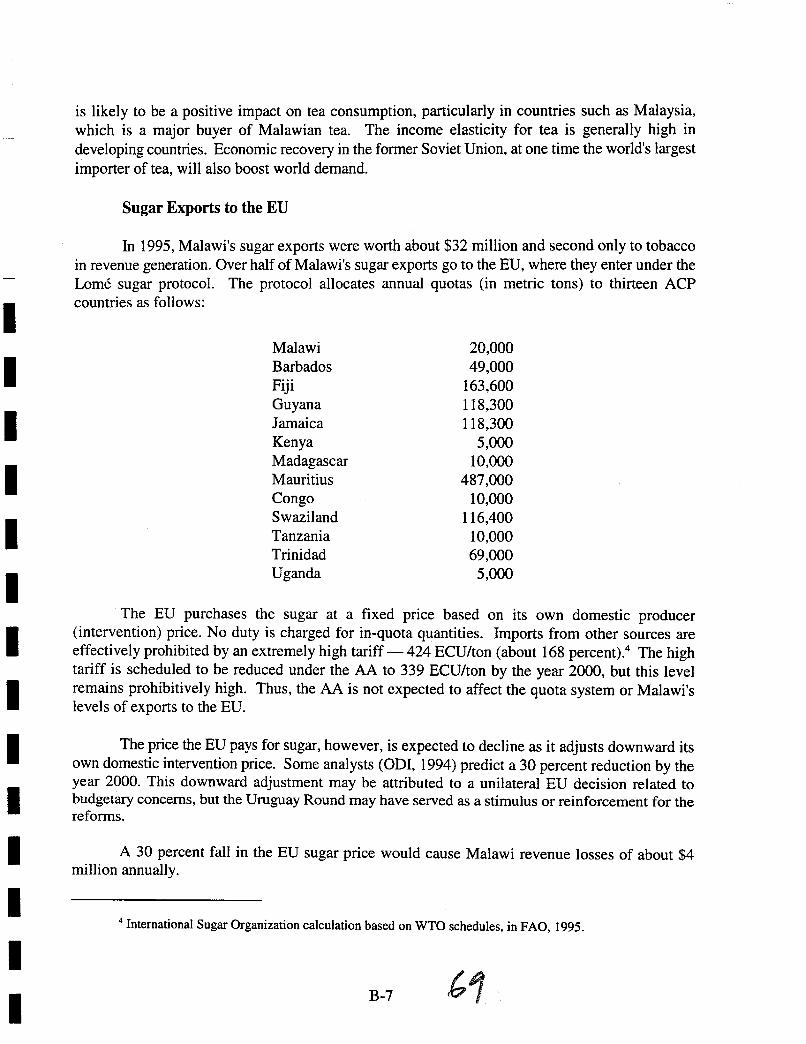

ANNEX B. MALAWI CASE STUDY ........................................... B-1

ANNEX C. MOROCCO CASE STUDY ......................................... C-l

ANNEX D. SOUTH AFRICA CASE STUDY ................................... D-I

ANNEX E. COTE D'NOIRE CASE STUDY ..................................... E-l

ANNEX F. SENEGAL CASE STUDY .......................................... F-l

L

I I I I I I I I I I I I I I

I I

LIST OF TABLES

1 Incidence of OECD Tariffs on Sub-Saharan Countries' Non-Oil Exports (%) ........ 10

2 ACP Export Losses to the EU, Relative to Total Revenue from Exports to the EU and to the World .................................................... 12

3 FAD-Predicted Change in World Food Prices by the Year 2000 Relative to 1987-90 I..evels ......................................................... 16

4 Agricultural Commitments in the UR by Sub-Saharan African Countries ........... 21

5 Predicted Effects of the AA on Sub-Saharan Africa Trade in Temperate Crops (TCs, in millions of SUS) ................................................ 24

6 Examples of the Erosion of Preference Margins in the Access of African Agricultural Exports into Important Markets .................................. 35

A-I Kenya's Major Agricultural Exports by Destination, 1992 (thousands of SUS) ..... A-I

A-2 Major Exporters of Cut Flowers to the EU, 1994 ............................ A-6

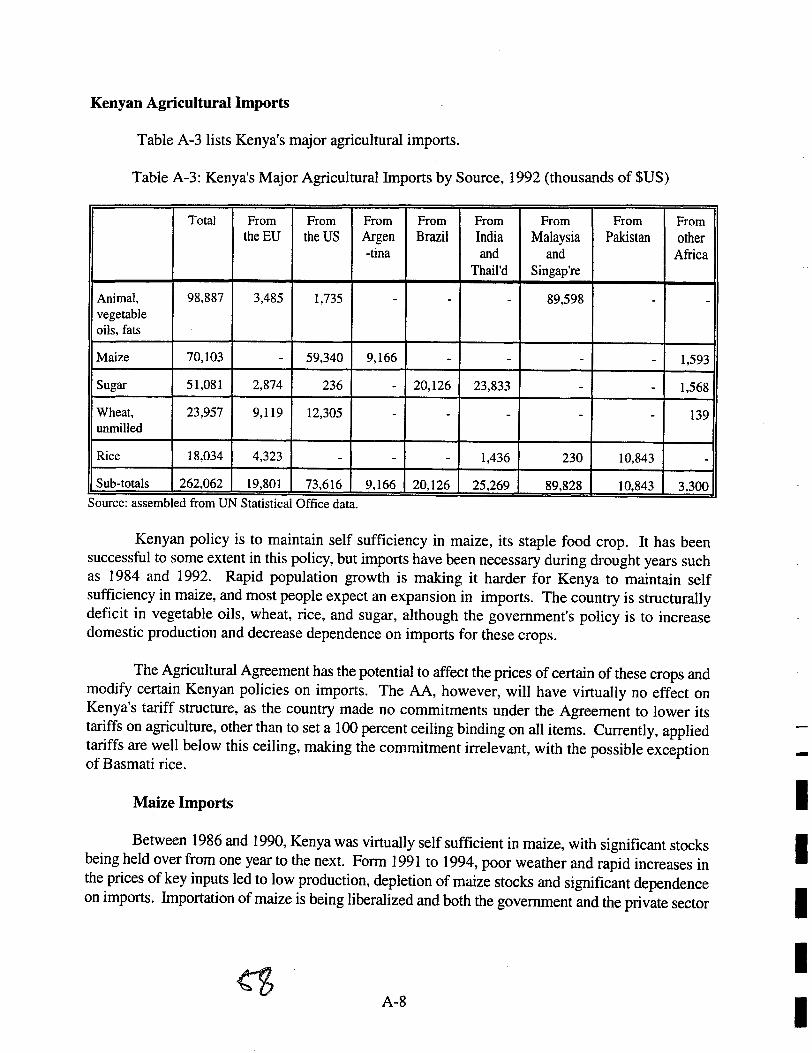

A-3 Kenya's Major Agricultural Imports by Source, 1992 (thousands of SUS) ......... A-8

B-1 Malawi's Major Agricultural Exports by Destination, 1991 (thousands of SUS) ..... B-1

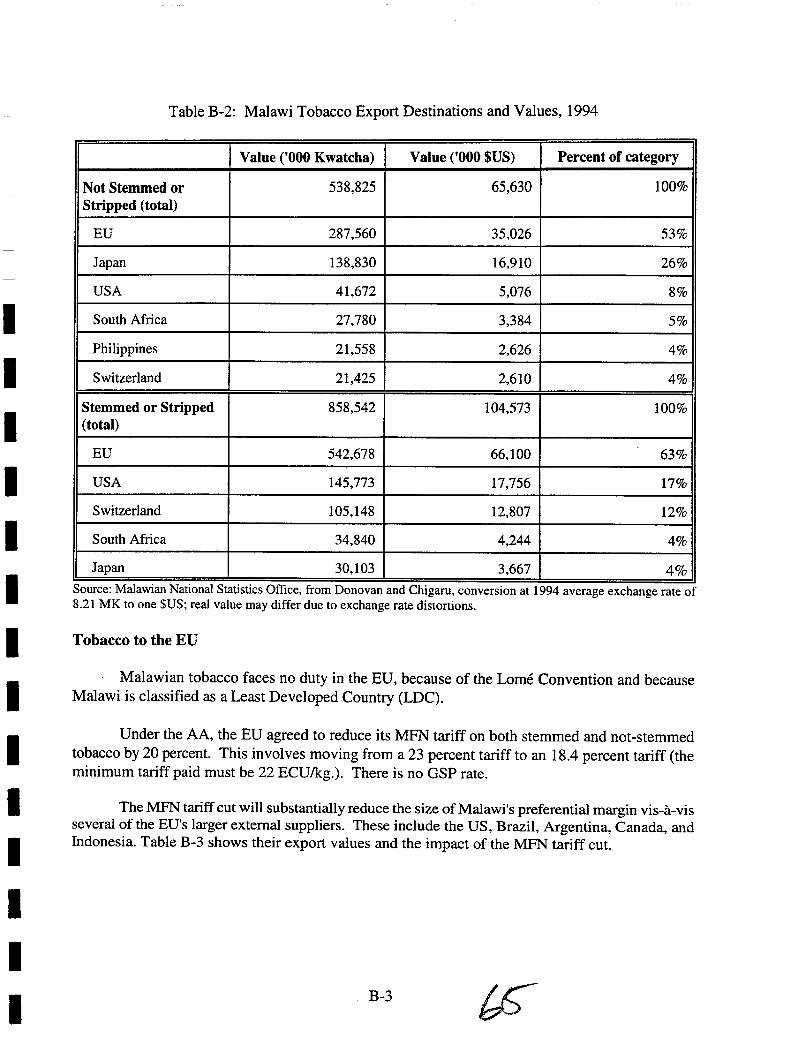

B-2 Malawi Tobacco Export Destinations and Values, 1994 ....................... B-3

B-3 Major External Tobacco Suppliers to the EU and Effects of the AA .............. B-4

B-4 Malawi's Major Agricultural Imports by Source, 1992 (thousands of SUS) ........ B-9

B-5 Maize Production and Requirement Estimates (in tons) ....................... B-I0

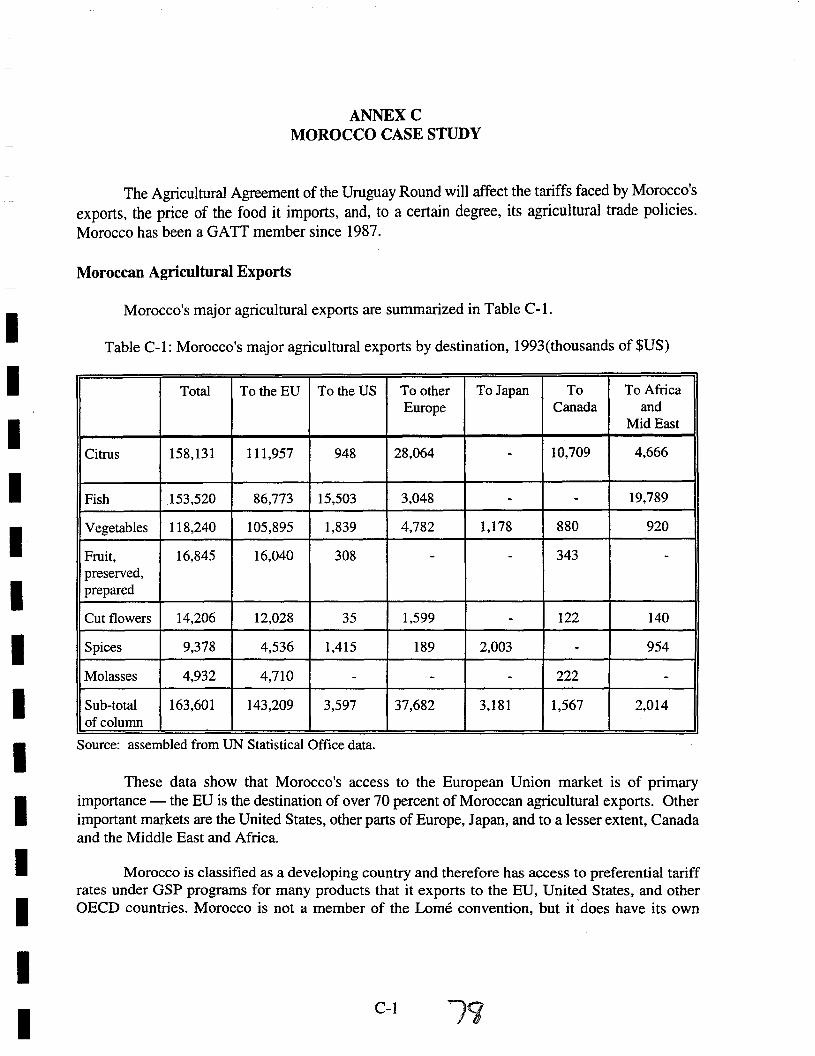

C-l Morocco's Major Agricultural Exports by Destination, 1993 (thousands of SUS) .... C-l

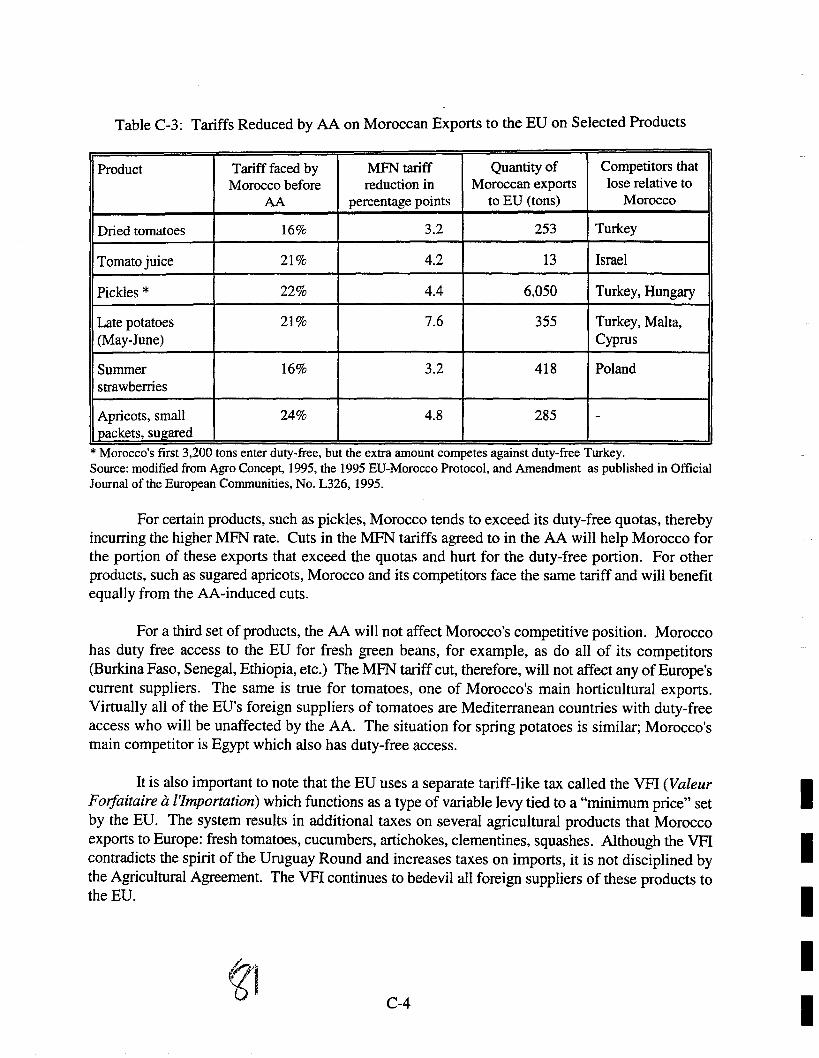

C-2 Preference Erosion Caused by AA on Moroccan Exports to the EU on Selected Products ..................................................... C-3

C-3 Tariffs Reduced by AA on Moroccan Exports to the EU on Selected Products ...... C-4

C-4 Anticipated Effects of AA on Moroccan Exports to the United States of Certain Products ...................................................... C-6

3

C-5 Major Exporters of Oranges, Mandarins, and Clementines to the EU, 1994 ........ C-9

C-6 Morocco's Major Agricultural Imports by Source, 1993 (thousands of $US) ...... C-12

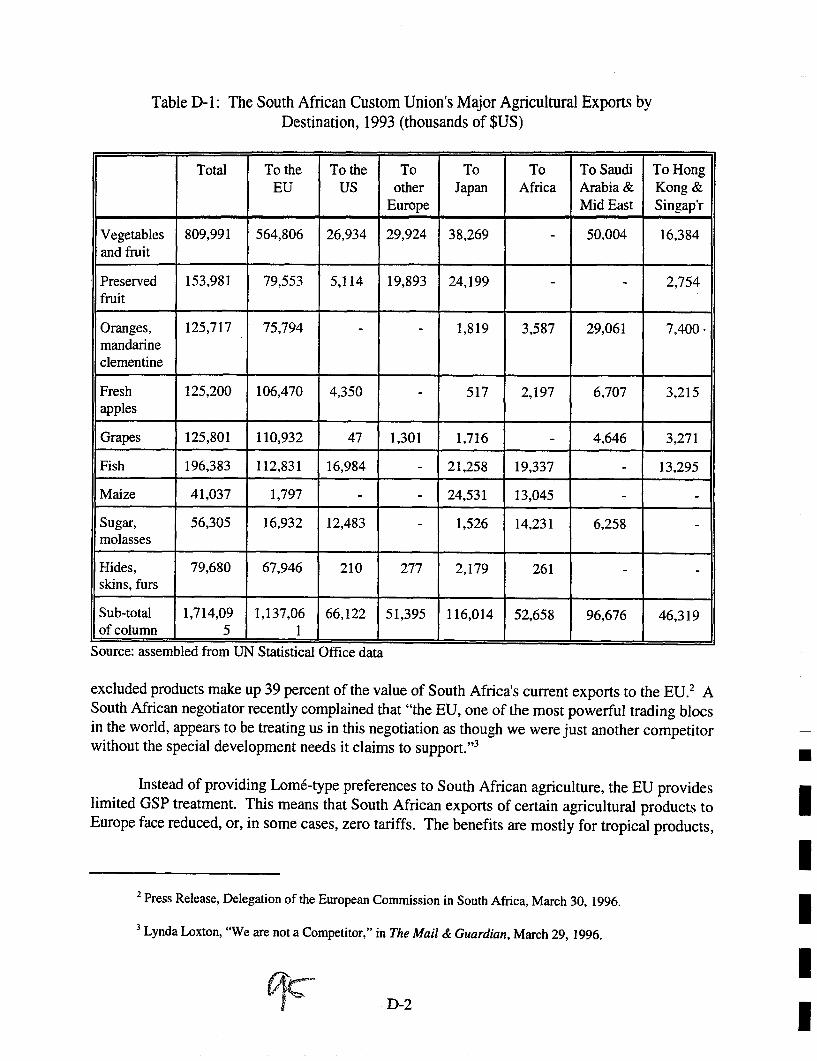

D-l The South African Custom Union's Major Agricultural Exports by Destination, 1993 (thousands of SUS) .............................................. D-2

D-2 South African Maize Exports by Major Trading Partners (in tons) .............. D-7

D-3 Change in Tariff Escalation in Hides and Skins ............................. D-8

D-4 South Africa Custom Union's Major Agricultural Imports by Source, 1993 (thousands of SUS) ................................................... D-9

D-5 South African Tariff Reduction Commitments and Actual Tariffs Applied, Selected Agricultural Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. D-ll

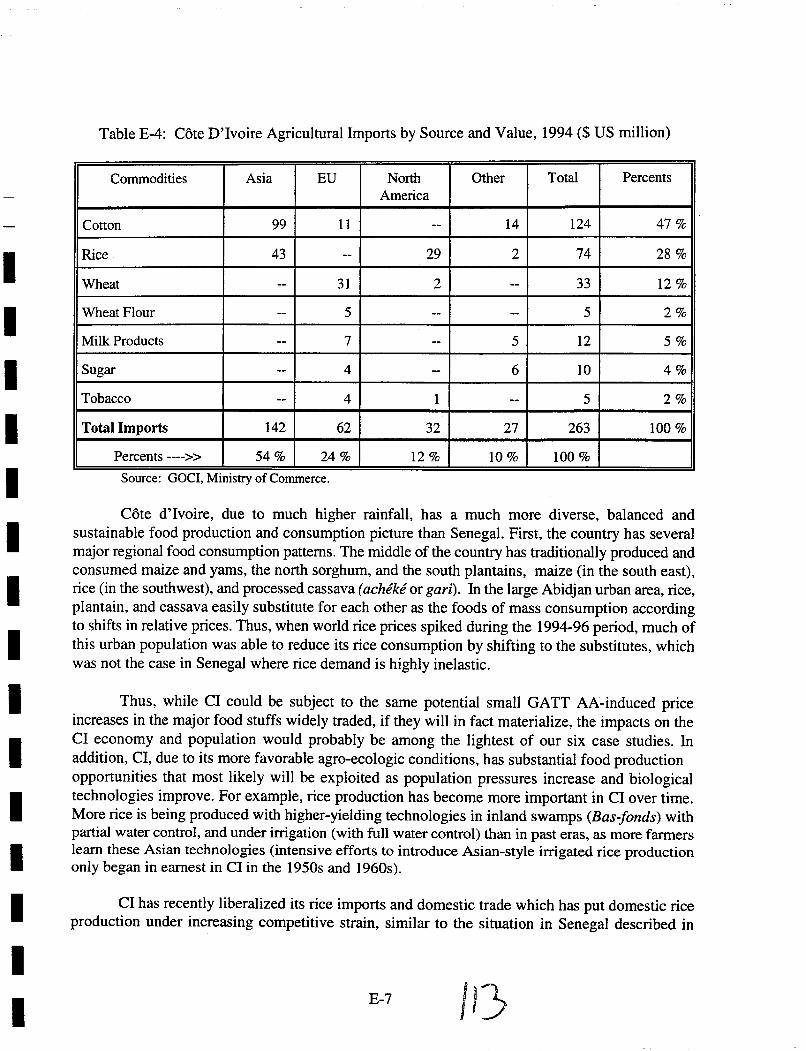

E-I Value of Cote d'Ivoire Agricultural Exports, by Destination, 1994 ($US mill) ...... E-1

E-2 Cote d'Ivoire Exports oflnstant Coffee, 1992-94 ($US millions) ................. E-5

E-3 Cote d'Ivoire Exports of Pineapple, Banana, and Rubber, 1989-94 (in SUS millions) ...................................................... E-5

E-4 Cote d'Ivoire Agricultural Imports by Source and Value, 1994 ($ US million) ...... E-7

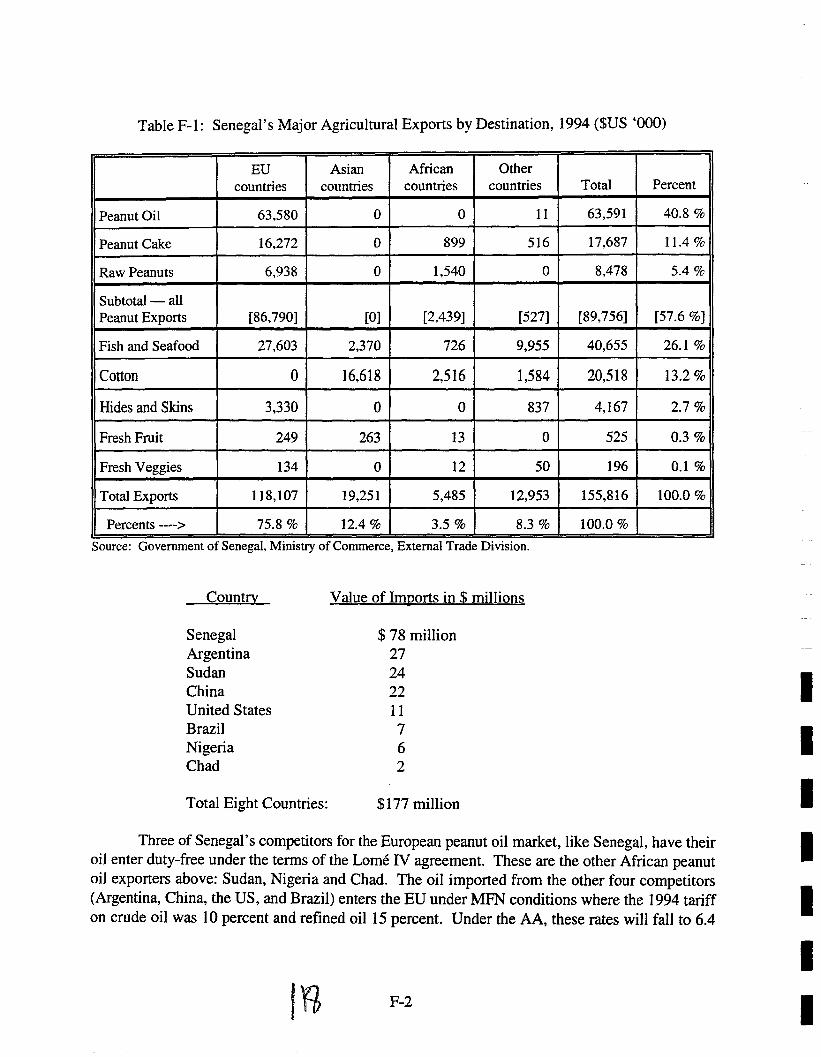

F-I Senegal's Major Agricultural Exports by Destination, 1994 ($US '000) ........... F-2

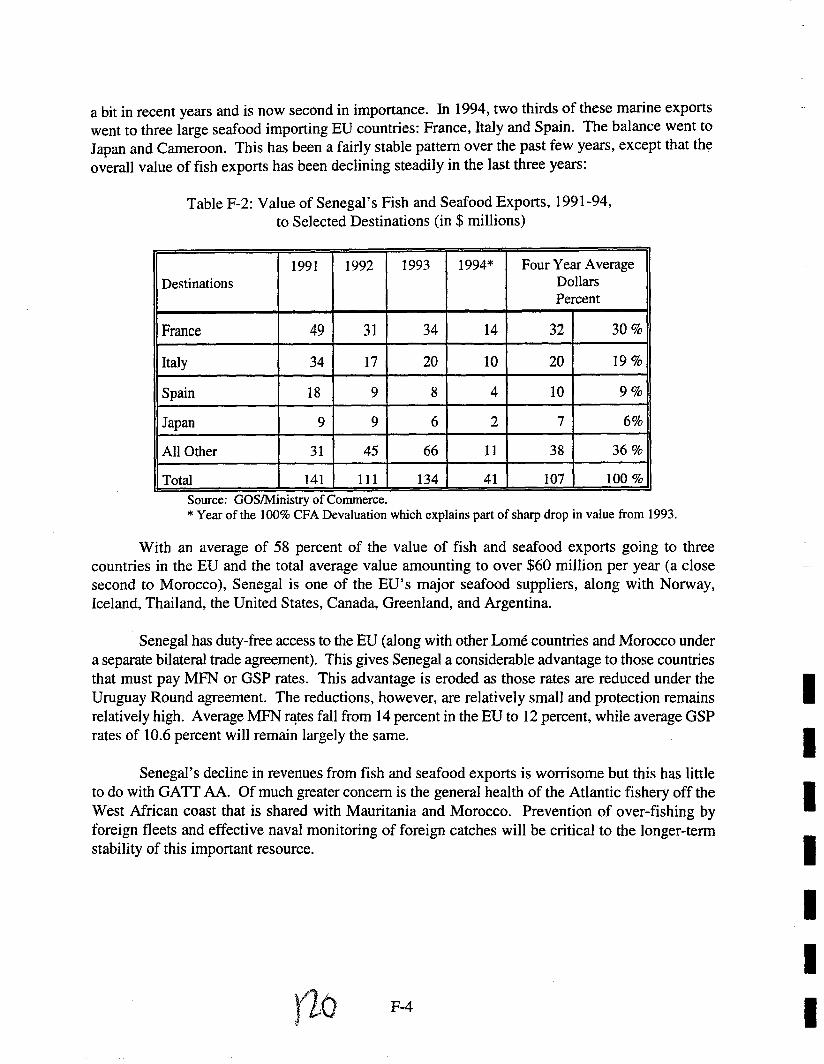

F-2 Value of Senegal's Fish and Seafood Exports, 1991-94, to Selected Destinations (in $ millions) ......................................................... F-4

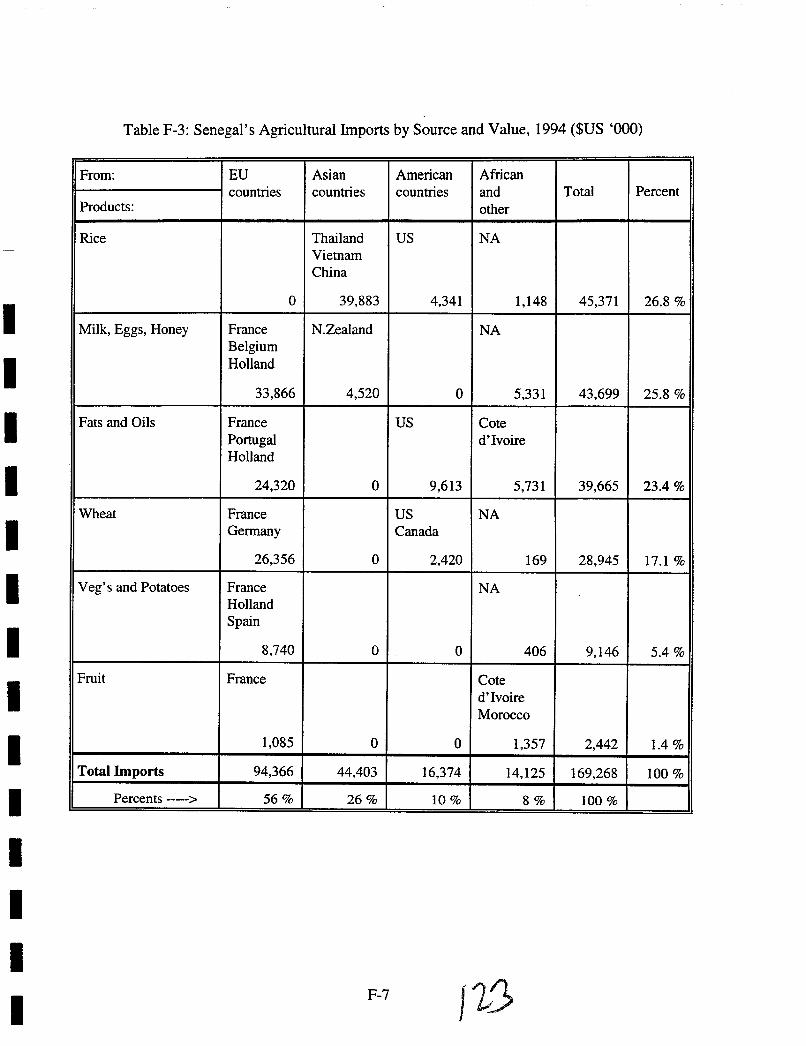

F-3 Senegal's Agricultural Imports by Source and Value, 1994 ($US '000) ............ F-7

I I I

I I I I I I I I I I I I I I I

INTRODUCTION

This report analyzes the expected impacts on Africa of the Agricultural Agreement (AA) negotiated as part of the GATT Uruguay Round. The topic is important because agriculture is important for Africa, and the Uruguay Round is expected to have significant impacts on many dimensions of Africa's agricultural trade. Agriculture accounts for about 30 percent of African GDP, 75 percent of employment, and two thirds of all exports. The signing of the Agricultural Agreement has raised hopes about new market openings for African agriculture at the same time that it has raised concerns about the Agreement's impact on food security and domestic policy formulation. This report aims to help USAID develop a fuller understanding of these issues so that it can take them into account during its programming and policy dialogue with African countries.

The first part of this report synthesizes the existing literature on the probable impacts of the Uruguay Round (UR) and the Agricultural Agreement (AA) on developing countries, with particular attention on Africa. A large amount of ink has been used in speculating about these impacts over the past six years, including analyses conducted before and after the 1994 signing of the Agreement. Part I of this report draws on this literature to address key questions about the AA's expected impact on African agricultural exports and food imports.

The second part of this report moves away from the generalizations available in the existing literature to look at the expected impact of the GATT/AA at the micro level, that is, on the agricultural trade of six specific African countries: Morocco, Senegal, Cote d'Ivoire, Kenya, Malawi, and South Africa This section explains the methodological approach we used in doing these case studies and presents some summary observations. The detailed country case studies are included as annexes. They include our own analyses of agricultural trade data for each country, looking at: (a) which products each country exports and how the URI AA affects access to each of the destination markets, and (b) which agricultural products each country imports and how the URI AA may affect availability, price, and food security. The case studies also draw on information gathered by local consultants hired in each country to provide a local perspective.

The third part of this report draws summary conclusions about the impacts of the AA on African countries and what countries might do to improve their overall competitiveness in world markets. What are the implications of the AA for domestic policy reform, export promotion, food security policy, and future trade negotiations? How can African governments seize the opportunities offered by a liberalizing international trade environment and prepare their economies for increasing competition? Finally, Part ill suggests types of project interventions USAID might wish to consider to pursue a trade-led development strategy in African countries where it has maintained its assistance programs.

/

I I I I I I I I I I I I I I I

PART I

IMPACTS OF THE AGRICULTURAL AGREEMENT ON AFRICA

Summary of the Agricultural Agreement

The agricultural sector was dealt with in a serious way for the first time by the GAIT during the Uruguay Round (UR). To help open world agricultural markets and increase the volume of world trade, it was agreed that tariff levels would be lowered and non-tariff barriers would be converted into tariffs (tariffication). In addition, levels of domestic support to agriculture would be reduced, and made more transparent, to reduce distortions of domestic and world market signals, thus improving sectoral efficiency.

The UR Agricultural Agreement (AA) is expected to achieve reform in world agricultural trade through provisions designed to:

• Expand market access (and thus promote expanded trade in agricultural products) through tariffication and lowering of tariff levels;

• Reduce export subsidies (provisions which affect North America and the EU most directly);

• Reduce internal or domestic support to agriculture through reductions in aggregate measures of support (AMS); and

• Unify sanitary and phytosanitary measures and reduce their use as "non-scientific" barriers to trade.

The potential impact of the Agricultural Agreement on developing countries has been a topic of considerable study and analysis over the past six years, including the four years prior to the signing of the agreement and the two years since. These studies estimate the Agricultural Agreement's probable impact on the developing world and on Africa in particular. We draw on these studies to address key questions below.

What Are the Probable Impacts on African Agricultural Exports?

The degree to which the Agricultural Agreement will affect African agricultural exports depends on several factors:

• The degree to which the AA actually reduces tariffs and non-tariff barriers on African exports, thereby improving access to markets;

• The degree to which the AA reduces the tariffs and non-tariff barriers on Africa's competitors, thereby eroding the value of the special tariff preferences that African countries have traditionally been accorded in many developed markets, especially the European Union;

• The degree to which the Agricultural Agreement and the entire Uruguay Round agreement lead to increases in global income and thereby increased demand for African products;

• The degree to which reduced domestic support for agriculture and reduced export subsidies in developed countries affect the prices of products which Africa exports; and

• The degree to which the AA requires African countries to modify their own support program for crops which they export.

Thirty-four African countries are WTO members, including all of the larger economic powers. Applications are pending for the Seychelles, Sudan, and Algeria. Several of the smallest countries (Cape Verde, Equatorial Guinea, Comoros, Sao Tome and Principe) are not official members but apply the agreements under the status of former colonies.

To what degree does the AA actually reduce tariffs and non-tariff barriers on African exports, thereby improving access to markets?

The AA calls for developed countries to reduce the average level of their Most Favored Nation (MFN) agricultural tariffs by 36 percent with a minimum reduction of 15 percent for each product. Developing countries are required to reduce average tariffs by 24 percent with a minimum of 13 percent for each product. All tariffs are to be bound; that is, the agreed upon rates cannot be exceeded. Developed countries are to phase in their reductions over a six -year period from 1994 to 2000, while developing countries have 10 years to phase in their reductions. The poorest countries are exempt from reduction commitments.

All signatories are required to convert non-tariff barriers (NTBs) on agricultural products into tariffs, through a process called tariffication. Once converted, these new tariffs must be reduced along the same lines as other tariffs.

Minimum market access provisions require a country whose NTBs effectively kept all foreign supply of a good out of its markets prior to the AA to guarantee that three to 5 percent of its market will be supplied by foreign countries under the new regime. The United States, for example, excluded foreign suppliers from its peanut market prior to the AA, but now is committed to allowing annual imports of 56,283 tons by the year 2000. The allowed quantities enter at a favorable tariff rate, but quantities beyond the "tariff quota" would generally face prohibitively high tariffs.

Sanitary and phytosanitary provisions call for member countries to employ scientific standards to determine all health-related measures that affect trade. The goal is to stop the use of

1 /

-I I

I I I I I I I I I I I I I I

arbitrary measures as a tool to restrict trade. Members are encouraged, but not required, to use international standards, such as those set by the F AO's Codex Alimentarius Commission, the International Office of Epizootics, and the International Plant Protection Convention. Members can use their own stricter standards, if they choose to, as long as the standards are "science-based."

At first glance these changes appear promising for African exporters. Upon closer examination, however, the results are less dramatic. There are several reasons for this.

First, the 36 percent average reductions to which the developed countries committed themselves are simple averages rather than weighted averages. Developed countries were allowed to chose which cuts to make on which products to achieve the simple 36 percent average reduction, and they tended to make smaller cuts on those commodities that were most heavily traded and most directly in competition with their own domestic production. To check what level of cuts were made on each agricultural product, one must check carefully each country's "schedule" of tariff commitments annexed to the overall Uruguay Round Agreement.

Second, the tariff cuts are to be made on the basis of average tariff levels in the 1986-1988 period. This was a period of particularly low commodity prices and therefore a period of particularly high tariff levels. Thirty-six percent reductions from these high levels result in much less actual tariff reduction than they would if they were applied to more recent tariff levels. In a few cases current tariff levels are already 36 percent below the 1986-88 levels.

Third, the process of tariffication did not improve market access in most cases. Under tariffication, the EU and United States transformed their existing agricultural import quotas into a system of Tariff Rate Quotas (TRQs) which allow imports of a commodity at a low tariff up to a certain quota but charge prohibitively high tariffs on any amounts beyond the quota limit. In most cases the effect is essentially the same as the original quota system. According to research conducted by Hathaway and Ingco (paper presented at World Bank Conference 1995), the EU, the United States, and many other countries tended to set over-quota tariff levels at exaggerated levels in a process the authors label "dirty tariffication." Because of these exaggerated levels, promised reductions of 15 to 36 percent will still result in tariffs that are too high to allow expanded trade in these products (e.g., the U.S. peanut tariff will fall from 155 percent to 131.8 percent).

Fourth, the minimum market access commitments made by developed countries, while significant, do not favor Africa's major export crops. The most significant minimum market access commitments were made by Japan and Korea to allow imports of foreign rice, a crop which Africa does not export.

Fifth, the AA includes "special safeguard provisions" that will allow, for those commodities subject to tariffication, the upward adjustment of tariffs to protect domestic production if:

• The volume of imports exceeds the average of the previous three years' imports by a certain "trigger amount," with the trigger level based on that commodity's proportion of consumption in the importing country; or

/

• The price of the imported product drops 10 percent below the average 1986-88 world reference price.

Sixth, and most importantly, most African agricultural exports already receive preferential tariff treatment in developed country markets, through mechanisms such as the Generalized System of Preferences, which provides duty-free or reduced-tariff access for some commodities originating in developing countries, and the Lome Agreement, which allows duty-free access to the EU for many commodities originating in developing countries with historical, colonial relationships with Europe. Boxes I and 2 explain how these systems work. Almost all African countries receive such preferential treatment for most of their agricultural exports. The cuts in the MFN rates agreed to in the URI AA do not, therefore, help Africa in most cases. Instead, the cuts erode these countries' margins of preference and cause their competitive position to deteriorate vis-a.-vis other suppliers. Trade losses will occur as some preference-receiving goods are displaced (diverted) by exports from other (non-preference receiving) countries.!

The UR did not cut GSP or Lome rates, which are very low or zero for most products (and cannot be cut below zero). Preferential treatment is considered a bilateral issue and strictly outside the multilateral trade negotiations.

For developing countries which hold a tariff preference over their competitors because of Lome or GSP, cuts in MFN rates reduce the level of their competitive advantage - a process called preference erosion. In this sense, the MFN tariff cuts agreed to in the AA represent a threat to Africa's market share in many commodities in developed countries. Morocco, for example, can export asparagus duty free to Europe, while the United States and Chili must pay a 16 percent tariff on their exports. Under the AA, this 16 percent MFN tariff will be reduced to 10 percent, cutting the advantage that Morocco enjoys by 6 percentage points.2

! Alexander Yeats, "What are OEeD Trade Preferences Worth to Sub-Saharan Africa?," African Studies Review, Volume 38, April 1995.

2 Oddly, several documents reviewed for this research seem to forget about preference erosion when hailing the achievements of the DR in reducing tariff rates. Blackhurst, Enders, and Francois (1995) present a table showing the 29 percent tariff reduction on coffee and cocoa as a benefit to 23 African countries, without so much as an asterisk to explain that all of these countries have duty free access to the EU and therefore wi1l be hurt, not helped, by the tariff reduction. The misleading table also appears in the WTO's own publication, International Trade Forum (111995).

q 4

I I I I

-I I I I I I I I I I I I I

I I

Box 1: The Generalized System of Preferences (GSP)

The principle of GSP - granting tariff reductions to developing countries - was first internationally accepted at an UNCT AD conference in 1968 where support was voiced for a "generalized, nonreciprocal, nondiscriminatory system in favor of developing countries." Under the GSP principle, industrialized countries make unilateral decisions to grant lower tariffs to developing countries, and each industrialized country decides how large these reductions will be and which countries are eligible.

Tariff reductions are helpful to developing countries; however, far from being generalized, nearly all schemes are subject to restrictions affecting country coverage, product coverage, depths of tariff cuts, safeguards, and rules of origin. Often times these require complex paperwork and are temporary in nature in the sense that they could be withdrawn at anytime. "Sensitive" products are usually excluded. About 30 percent of exports from the least developed countries that qualify for GSP tariff reductions fail to receive those reductions because of difficulties meeting administrative requirements (Lal, 1994).

The United States excludes Nigeria and Gabon from its GSP program because they are OPEC members, and India, Argentina, South Africa and many other countries are excluded on certain products. The U.S. GSP rate is usually zero, but citrus, grapes, tomatoes, roses, many types of fish, rice, and hundreds of other line items are totally excluded. Japanese GSP rates range from a 10 percent discount off the MFN rate to full duty-free. Product coverage is limited and ceilings apply for countries that exceed certain volumes.

The GSP of the EU excludes more line items than it includes, and the list of qualifying countries varies over time. GSP rates are less than MFN rates but usually more than zero. Currently, the EU is considering modifying its GSP to vary the tariff reduction depending on the beneficiary country's level of development and compliance with "social policies" such as environmental protection and child labor laws.

GSP rates were not negotiated in the Uruguay Round, and some say such preferences "are beginning to smack of a bygone era" (Page, Davenport, and Hewitt, 1992). The importance of GSP has shrunk as MFN rates have fallen and regional, more preferable preference schemes, such as Lome, have expanded.

How Serious Is the Preference Erosion Problem for Africa?

To answer this question one must first understand the pennissible complicated systems of tariff preference that currently exist. These are reviewed below:

• Most Favored Nation (MFN). These rates are the standard tariffs offered to all countries that are signatories of the GAIT (now known as members of the WTO). MFN tariffs are not preferential rates but rather the rates to which preferential rates should be compared.

• Generalized System of Preferences (GSP). These rates are the preferential tariffs accorded to developing countries and some transitional countries for certain commodity groups. They are intended to help developing countries develop exports. GSP rates are either zero or a percentage of the regular MFN rates. Each developed country decides

5 )!Q

for itself which products it will offer asp rates and how big the reduction will be. From mid-1995 until August 1996 the GSP program in the United States was suspended. The August 1996 legislation only extended the program to the end of May, 1997, so things are still in flux. The asp system in the EU is also under revision.

• Least Developed Countries (LDC). Under this sub-system of the GSP, OECD countries allow duty-free entry of certain commodities from the poorest developing nations. The ED's list includes 41 countries, most of which are in Africa, but excludes more developed countries such as Nigeria and Cote d'Ivoire. Most of these countries already benefit from the Lome Convention. The EU offers similar tariff terms to countries affected by drug trafficking in the Andean Pact and Central America. The U.S. list includes 35 countries, mostly African, that receive duty-free access for commodities designated as GSP goods, without any quantity limitations. The WC program will be suspended in the United States for as long as the GSP program is suspended.

• Bi-Iateral Trade Accords. Reduced rates or zero tariffs have been negotiated in trade agreements between the United States and its neighbors. These include: the North American Free Trade Agreement (NAFT A), the Andean Trade Preference Act, the Caribbean Basin Act, and the US-Israel Free Trade agreement. The European Union has similar agreements with its neighbors in Europe and the Mediterranean, including Turkey, Morocco, Algeria, Tunisia, Egypt, Cyprus, Malta, the non-EU Western European countries (EFT A), the countries of Eastern Europe, and Israel. These agreements offer generous tariff discounts or zero tariffs on many agricultural goods, but not on all. Preferences are often limited to fixed quantities of each commodity.

• The Lome Convention. Tariff rates are zero for the members of the convention on practically all agricultural exports to the EU. Lome convention countries are also known as ACP countries (Africa, Caribbean, and the Pacific). Virtually all African countries are members, with South Africa and the North African countries being the only exceptions. ACP exports of tropical products to the EU are not limited, but exports of sugar, beef, rum and a few other temperate crops are subject to quotas, which are defined in the convention and subsequent regulations.3

3 It is common practice to divide agricultural products into two groups: tropical products and temperate zone products. Although there are no agreed-upon definitions of these terms, in practice, tropical products applies to beverages like tea, coffee and cocoa; cotton and hard fibers like jute and sisal; and fruits like mangoes and guavas. Temperate zone products are those that are grown, and often subsidized, in DECO countries, such as wheat, other grains, meat, temperate fruit and vegetables, and dairy.

I I 6

I I I I

I I I I I I I I I I I I I I

Box 2: The Lome Convention

The Convention is a treaty of cooperation between the European Union and 70 of the world's poorest countries in Africa, the Caribbean, and Pacific (ACP). Most are ex-European colonies, and all of Sub-Saharan Africa is included, except South Africa. The first convention was signed in 1975, and the latest (Lome N) was signed in 1990, with a scheduled validity of 10 years.

Under Lome, the EU grants duty-free access to the ACP countries for almost all of their exports - a substantial and cherished preference. Quantity restrictions are applied only to tuna and a few vegetables and fruits (currently under revision), and special quotas apply to four "sensitive" crops: sugar, beef, rum, and bananas. These quotas are assigned to individual countries which use them to sell in the lucrative EU market, where prices are well above world levels. In Africa, beef quotas are assigned to Botswana, Kenya, Madagascar, Swaziland, Zimbabwe, and Namibia. Sugar quotas are assigned to Swaziland, Mauritius, Malawi, Madagascar, Kenya, Uganda, and Tanzania.

Doubts exist about whether the Lome scheme meets the GA'IT criteria for permissible preferential arrangements, but a waiver was obtained for the life of the existing convention, which expires in the year 2000.

Analysts agree that African countries will suffer the most serious preference erosion under the UR because they have the most to lose, particularly in the EU, where over half of their exports are destined (Harrold, 1995). Preferences result in at least 97 percent of each African country's exports entering the Community free of duty (Yeats, 1995).

Preference erosion will occur on some of Africa's most important agricultural exports: coffee, cocoa, other tropical products, and fish. Before the Agreement, GSP and MFN countries faced a 5 percent tariff on coffee beans in the EU while Lome convention countries faced no tariff. The 5 percent tariff is to be reduced to zero under the AA, thereby eliminating the Lome tariff preference. Before the AA, GSP and MFN countries faced a 3 percent tariff on cocoa beans while Lome countries faced no tariff. The 3 percent tariff will be eliminated under the AA.

On other tropical products, Lome countries faced no tariffs while MFN competitors faced an average of 7.6 percent and GSP countries faced 6 percent. Under the AA, the MFN rate is scheduled to fall to 4.2 percent and presumably the GSP rate will fall to the same level (ODI, 1994). The size of the Lome preference margin will thereby be reduced by 3.4 percentage points or 48 percent.

In the case of fish, MFN rates are scheduled to drop from 14 percent to 12 percent, while GSP rates of 10.6 percent remain the same. The size of the Lome preference margin for fish will fall by 2 percentage points but will still remain substantial.

Lome convention countries have better preferential tariff entry than other developing countries in some important sectors, including processed and unprocessed cocoa, in which Africa

7

competes with Brazil, Malaysia and Indonesia; processed and unprocessed coffee, in which Africa competes with Colombia and Brazil; pineapples, in which Africa competes with the Philippines; tobacco, in which Zimbabwe and Malawi compete with Brazil, India and the Republic of Korea; palm oil, in which West Africa competes with Malaysia; and beef, in which Africa competes with Argentina. In so far as these competitors enjoy tariff cuts under the AA, the Agreement hurts African exports.

North African countries generally have bi-Iateral trade agreements with the EU that give their products duty-free access to the EU up to certain quantity limits. The value of these preferential arrangements will be reduced as the AA cuts the MFN rates of their competitors.

In markets outside the EU, African countries generally face the same tariffs as other developing countries, i.e., the GSP or MFN rates (depending on whether or not the destination country offers the preferred rates for the particular product). In those cases where the GSP rate is below the MFN rate, cuts in MFN rates will erode the African preference margin. This is the case, for example, for pyrethrum flowers imported into Japan. African exporters of pyrethrum, such as Kenya, face no duty while developed countries, such as Australia, faced a 20 percent duty prior to the AA, an amount scheduled to drop to 12 percent under the Agreement.

For many agricultural commodities, there are no GSP rates and therefore African countries must pay full MFN tariffs. In these cases, AA tariff cuts will be beneficial to Africa. In the United States, for example, African countries face the full MFN tariff on bulk pineapples ($O.64lkg) while competitors with special trade arrangements with the United States face no tariffs (such as Mexico, and the Caribbean and Andean countries). Under the AA, the MFN rate will fall to $0.51Ikg, thereby providing a small improvement in Africa's competitive positi0n vis-a.-vis the Latin Americans.

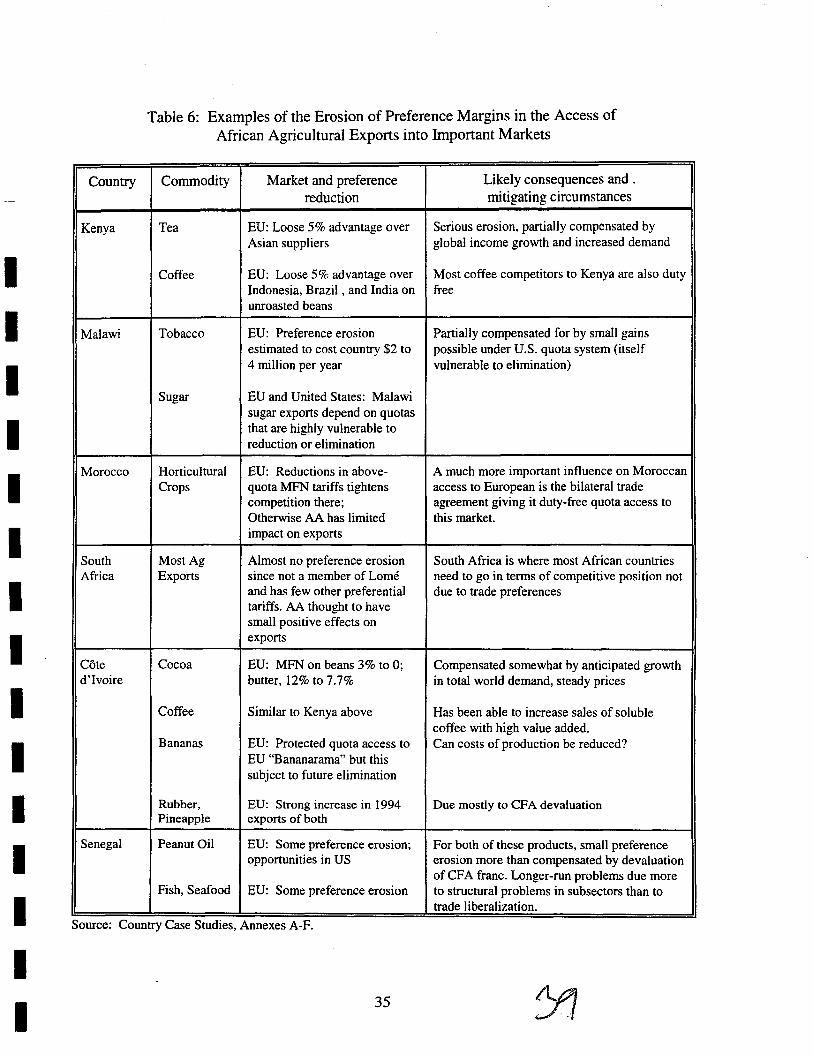

As the above examples demonstrate, preference erosion is a real issue, but calculating the degree of erosion is complicated because of the complex maze of tariff levels that exist for different products, for different destinations, and for different preference schemes (which vary by product, season, and frequent legislative changes in destination countries). AA-induced tariff reductions will erode African preferences in many cases, but they will help African exporters and erode their competitors' preferences in other cases. Accurate assessments of impacts are probably best made on an individual country basis, allowing analysis of competitive positions for the products that each country exports. We attempt to carry out such assessments for six African countries in Part IT of this report.

In his article on DECD trade preferences, Yeats' figures are based on complete elimination of MFN duties. His analysis was conducted before the DR was finalized, which in the end cut MFN rates by about 36 percent. His projections, therefore, need to be adjusted downward by 64 percent, to a new estimate of $63 million in annual losses.

Lal of the World Bank (1994) updates Yeats' analysis, using actual DR results, but focuses only on the Least Developed Countries. He concludes that preference erosion will cause Africa's poorest countries to lose export revenues of $5.5 million in the EU, $6.5 million in Japan, and gain

8

-I I

I I I I I I I I I I I I I I I I

$4.2 million in the United States - resulting in an overall loss of $7.7 million - 0.1 percent of their total exports. Unfortunately, Lal's analysis does not separate the effects of the Agricultural Agreement from other aspects of the Round.

Harrold, in a draft paper for the 1995 World Bank Conference on the Uruguay Round, argues that the importance of preferences, and concerns about their erosion, are exaggerated. Harrold presents data showing that African exports to the EU typically enjoy preferences in the range of 2.1 to 4 percentage points (on average), while exports to the United States typically receive preferences of under 2 percentage points.4

Despite the difficulties of generalizing, several analysts have attempted to assess the degree of preference erosion caused by the Uruguay Round and the AA on Africa and developing countries on the whole.

Yeats (1995) analyzes African exports in detail and finds that Sub-Saharan African countries generally face low tariffs on their exports. The average tariff faced by African countries in OECD countries is only 0.66 percent which is 2.4 percentage points less than the average tariff faced by non-African exporters of the same goods (Table 1). Yeats calculates the trade losses that would occur if African preference margins disappeared due to liberalization of MFN rates. He finds that a complete liberalization of MFN duties would produce annual African trade losses of about $250 million in the EU and $14 million in Japan. In the US, the cuts would actually increase African exports by $89 million, because of the helpful effects of MFN cuts on textiles and clothing, mostly produced in Mauritius. Overall, the net losses from preference erosion would be $175 million annually.

According to Harrold, these preferences are quite low and therefore their erosion is not alarming. Harrold draws on a partial equilibrium trade projection model developed by the World Bank and UNCT AD to stimulate the impact of the actual Uruguay Round tariff cuts and predict the costs of preference erosion on African Least Developed Countries (LDCs). The results predict net trade losses of about $7.5 million in the OECD markets with a loss of $5.4 million occurring in the European Union. Harrold points out that this represents only a tenth of 1 percent loss in total African LDCs' exports to these destinations. Losses in the EU are somewhat offset by positive trade gains in the United States market due to reductions in the MFN tariffs that Africa faces on textiles and clothing exports to that market. Harrold concludes that "the impact of preference erosion on African exports will only have a very small impact on trade," and the effects "would be so small as to be unnoticeable in comparison with other factors influencing exports and development in Africa."

4 The averages presented by Harrold are based on all aspects of the Uruguay Round and not just the Agricultural Agreement. The inclusion of clothing trade may explain the higher preferences in the EU, which allows duty-free entry for ACP countries, and the lower preferences in the United States, which excludes clothing and textiles from preferences.

9 )~

Table 1: Incidence of OECD Tariffs on Sub-Saharan Countries' Non-Oil Exports (%)

OECD Average European Community Japan United States

Exporting African Preference African Preference African Preference African Preference

country tariff margin * tariff margin tariff Margin tariff margin

Angola 0.2 -1.5 0.3 -3.2 1.8 0.0 0.1 -0.4

Botswana 0.3 -2.8 0.1 -2.9 0.0 -2.1 3.5 -1.1

Cameroon 0.4 -2.5 0.1 -2.8 0.0 0.0 2.1 -1.1

C.A.R. 0.2 -2.2 0.2 -2.3 0.0 0.0 0.0 -1.1

Chad 0.4 -2.7 0.2 -2.9 2.5 0.0 1.6 0.0

Congo 0.1 -1.4 0.0 -2.2 0.0 0.0 0.3 -0.6

Cote D'Iv. 0.7 -3.1 0.3 -3.3 1.2 -0.5 3.3 -2.0

Ethiopia 0.7 -1.3 0.1 -1.9 1.5 -1.3 2.0 0.4

Gabon 0.6 -2.0 0.0 -2.7 0.0 0.0 2.9 0.7

Ghana 1.0 -2.2 0.1 -3.1 2.3 0.0 2.6 -0.9

Guinea 0.6 -2.3 0.0 -2.9 1.8 -1.9 1.9 -1.0

Kenya 0.5 -3.3 0.2 -3.5 2.4 -1.1 3.1 -2.3

Liberia 0.6 -1.7 0.3 -1.9 0.0 -0.3 2.5 -1.1

Madagascar 0.5 -2.0 0.4 -2.7 0.8 -0.2 0.8 -1.0

Malawi 1.1 -2.4 0.1 -3.5 0.0 -0.1 5.4 -0.6

Mali 0.4 -3.4 0.2 -3.5 0.0 -1.6 3.1 -2.2

Mauritania 1.7 -2.3 0.2 -3.9 3.6 -0.4 1.2 -1.6

Mauritius 1.3 -3.1 0.2 -3.4 4.8 -1.1 6.4 -1.8

Niger 0.1 -3.0 0.0 -3.0 0.0 0.0 3.3 -1.6

Nigeria 2.7 -0.9 0.1 -2.6 3.7 -0.8 5.2 0.7

Senegal 0.5 -3.3 0.3 -3.5 3.6 0.1 4.9 -1.2

Sierra 0.5 -3.1 0.0 -4.0 2.6 -0.7 2.3 -0.2

Sudan 0.1 -1.5 0.1 -1.9 0.0 0.0 0.7 -1.0

Swaziland 0.8 -4.4 0.5 -4.9 6.7 -3.0 3.5 -1.9

Tanzania 0.1 -2.3 0.0 -2.5 1.4 -1.0 0.0 -2.4

Togo 0.3 -2.8 0.2 -2.8 9.8 -0.8 0.2 -2.8

Uganda 0.9 -2.4 0.6 -3.0 0.0 0.0 2.1 -0.3

Zaire 0.3 -2.1 0.1 -2.4 0.0 -0.5 1.3 -1.1 Zambia 0.3 -1.7 0.5 -2.9 0.0 -0.6 1.4 -1.4

Zimbabwe 0.9 -2.5 0.2 -3.3 1.2 -1.0 4.0 -1.0

*Negatlve values show the average preferential tariff margins (in points) that the African Exporter has over all other exporters of the same goods. Positive values indicate that the exporter faces a higher than average tariff due to preferences other countries receive. All tariffs shown above are the simple average (unweighted) of duties faced on the country's exports. Source: Yeats, 1995.

10

I I I

I I I I I I I I I I I I I I I I

Evaluation of the accuracy of Harrold's conclusion is difficult for several reasons. First, his partial equilibrium estimates are based only on the Least Developed Countries, leaving out some of Africa's biggest traders such as Cote d'Ivoire, Kenya, South Africa, Nigeria, Cameroon, and the Maghreb countries. Losses could be much greater if these countries were included in the analysis. Second, his analysis is based on the entire UR and not just the AA, which is our focus in this paper. If the analysis were restricted to the AA, net losses might be smaller or greater, because both total losses and total gains would be smaller. Overall, our impression is that Harrold is overly eager to downplay the importance of preference erosion. The evidence suggests that preference erosion on tropical exports will not be devastating, but it will be significant, particularly in Europe where most African exports are directed, and the impact will be substantial for many other agricultural products for many African countries.

Three analysts at the Overseas Development Institute (ODI) also address the issue of preference erosion in a 1994 report called "The Impact of the GATT-Uruguay Round on ACP States" (Davenport, Hewitt, and Koning). Based on partial equilibrium modeling, the report estimates that African ACP States will lose $175 million of their export revenue due to preference erosion, an amount equal to 0.7 percent of their total export earnings on the EU market. Most of this loss is due to preference erosion for coffee and cocoa beans, basic wood exports, and metals and minerals. The authors stress that this estimate only suggests the static loss in current African exports, and that dynamic losses will be greater through lost investment.

According to ODI, African ACP countries were hurt most by preference erosion in the area of tropical products exports, with coffee beans and cocoa beans being the most important products, but with cut flowers and plants, nuts and tropical fruits, spices, and tobacco also responsible for significant losses. For ACP exporters of coffee and cocoa beans, the earlier preferences of 5 and 3 percentage points are eroded 100 percent under the AA. For the other tropical products, the ACP countries lose 48 percent of their advantage vis-a.-vis MFN exporters and 30 percent vis-a.-vis GSP exporters. Overall, ACP countries are expected to lose export revenues of $45 million in the area of tropical products. Ghana and Cote d'lvoire are hard hit by preference erosion in cocoa, while Uganda, Kenya, Cote d'Ivoire and Cameroon loose the most in coffee.

Fish exports to the EU is another area of concern for the African ACP countries. Luckily, from their point of view, average MFN tariffs in this sector did not drop dramatically - only from 14 percent to 12 percent - thereby leaving a substantial level of preference for the duty free ACP countries. The 001 report estimates that losses from this small preference erosion will be limited to $31 m annually, with Senegal losing about $2.3 m and Cote d'lvoire about $1.9 m.

The 001 report analyzes separately the negative effects of the Uruguay Round on the earnings of ACP countries from exports of beef and sugar to the EU. Under the Lome Convention, certain ACP countries are allocated quotas of allowable exports of these products into the EU for sale at internal EU prices - prices that are substantially higher than world prices. These quotas, therefore, are highly prized. The ODI model assumes that EU import prices fall by 30 percent for sugar and beef as the result of EU reductions in farm support induced by the Uruguay Round. The revenue generated by the ACP preferences for these products therefore falls by 30 percent in the

11 JL

model. According to the authors, losses will be significant for these African beef exporters: Botswana, Kenya, Madagascar, Swaziland, Zimbabwe, and Namibia, and these African sugar exporters: Swaziland and Mauritius. The ODI report does not report on the value of these losses separately; instead, it combines them with other preference losses and trade losses to estimate an overall commodity trade loss of $230 million per year for African ACP countries, which represents 1.3 percent of its export revenues to the EU.

The authors acknowledge that this overall estimate seems small. They explain that only

about half of ACP exports to the EU will suffer trade diversion since the other half consists of products which already enter the EU market free of tariffs for all suppliers. Even where MFN tariffs are non-zero, in many cases the main competitors to the ACP are other developing countries which enjoy comparable preferential treatment. The reported losses, however, are only static estimatesdynamic effects on investment and future export earnings are difficult to quantify but they may double the loss figures.

The authors point out that aggregate losses are small in percentage terms, but losses are likely to be much higher in certain countries. The biggest losers in Africa are shown in Table 2 below:

Table 2: ACP Export Losses to the EU, Relative to Total Revenue from Exports to the EU and to the World

Total export Loss as % Loss as % loss ($ millions) of total exports of total exports

to the EO to world

Ethiopia -13.6 -10.62 -3.97

Mauritius -44.6 -4.96 -3.52

Senegal -17.2 -4.58 -2.39

Tanzania -6.4 -3.40 -1.37

Malawi -5.6 -3.07 -1.35

Source: OD!, Davenport et. aI., 1994. Note: these losses are due to lost preferences in agriculture, fish, wood, and manufactures (clothing and textiles losses are excluded).

The ODI authors conclude that continent-wide estimates are likely to overlook many of the complex ways that AA-induced tariff and policy shifts can affect trade patterns. They recommend a more detailed study, looking into all products exported by the ACP states individually, and taking into account changes in MFN and asp tariffs plus non-tariff barriers for each product, to get a better picture of the effects of the opening of the EU market.

Another study that addresses the preference erosion question is Blackhurst, Enders, and Francois (1995). Without looking at the issue in as much detail as the aDI report, they find that Africa will suffer from preference erosion in Europe, but that conditions of market access may

1\ 12

I I I I

I I I I I I I I I I I I I I I I

improve in Japan and the United States. The improvements in the United States and Japan, however, are unsure because price advantages to African exporters granted under GSP in these markets will be eroded and because there is an absence of comprehensive data on the benefits offered under these programs. The authors conclude that the overall significance of GSP preference erosion is likely to be negligible since most donor countries circumscribe the benefits available by quota limitations, excluded products and eligibility conditions.

A recent paper prepared by the WTO and UNCT AD Secretariat (April 1996) recognizes that preference erosion may lead to significant losses in some specific products exported by specific countries; however, the paper emphasizes that overall losses will be slight and the new MFN tariffs are legally bound, in contrast to the preferential rates which are not. Emphasizing the positive, the WTO and UNCT AD argue that "the margin of preference may be lower, but the security of market access is unambiguously greater."

To what degree will the Agricultural Agreement and the entire Uruguay Round lead to increases in global income and thereby increased demand for African products?

While preference erosion will hurt Africa, increases in global income resulting from trade liberalization caused by the DR Agreement will help Africa by increasing demand for its products. The effects on global income have been estimated by a number of economic modelers:

Study Estimates of increase in global income

GATT (1994) $235 billion annually by 2005 from the full market access package (1992 dollars)

World Bank/OECD (1993) $213 billion annually by 2002 from liberalization on industrial tariffs and agriculture (1992 dollars)

OECD (1993) $274 billion annually by 2002 from liberalization of industrial tariffs and agriculture (1992 dollars)

Nguyen, Perroni, and Wigle (1993) $212 billion annually from the full market access package

Source: GAIT 1994 In am 1994

These four studies predict (on average) an annual increase in world income of about 1 percent by 2002. According to the OD! report, the increased demand triggered by this growth would increase Mrican export revenues by $481 million dollars, assuming an income elasticity of one for Mrican products, or by $1.4 billion dollars, assuming an income elasticity of three. These expected gains are $251 million larger than the expected losses due to preference erosion, resulting in an expected net gain in African export revenues of 0.6 percent (using the lower elasticity estimate) or 2.7 percent (using the higher elasticity estimate). Such gains are not uniform, however, and about 25 African countries will still show losses, even after the income effect (using the lower elasticity estimate).

13

A second set of analysts that have considered this issue (Goldin, Knudsen, and van der Mensbrugghe, 1993) agree that GAIT -induced growth in OECD countries will help expand demand for African exports and thereby increase African revenues. They calculate that if OECD real income increases by 18 percent between 1993 and 2002, this effect alone will result in a real income gain of about 2 percent in Africa. Higher gains will accrue to those countries with the highest level of penetration in the economies of the DECD countries.5

More recent work on this question by Goldin and van der Mensbrugghe (1995) greatly scales back the predictions for global income gains. Based on an analysis of the actual agreement, with less liberalization than was originally hoped for, these analysts now predict gains of $25-48 billion in global income, roughly a quarter of what was originally expected. These more modest gains will mean more modest growth in demand for African exports.

To what degree will reduced domestic support for agriculture and reductions in export subsidies in developed countries affect African exports?

These measures, as required by the Agricultural Agreement, would be expected to lead to less production of temperate crops in developed countries and therefore higher prices on world markets. Higher prices for wheat, coarse grains, rice, beef, and other such commodities will improve earnings for African exporters, but will hurt African importers, particularly countries that are heavy food importers. In this section, we consider impacts on exports only, leaving questions of import bills for later.

Analysts that have looked at this issue predict that the reduced domestic support levels for agriCUlture agreed in the UR will have a limited impact on world prices, but reductions in export subsidies will have a more substantial impact.

Domestic Support: Hathaway and Ingco (1995) show in their paper how Agricultural Agreement provisions requiring reductions in domestic subsidies were watered down during the final months of the negotiations, minimizing their probable impact. The final Agreement requires developed countries to cut their aggregate level of subsidization for agriculture (as measured by the Aggregate Measure of Support - AMS) by 20 percent over the six-year implementation period, but it does not make reference to any specific commodities. According to Hathaway and Ingco, this leaves the door open for maintaining high subsidy levels for sensitive crops and achieving the required aggregate cuts through creative accounting or through cuts that have already occurred for independent domestic reasons. They also point out that the Agreement exempts major subsidy programs in the United States and EU (e.g., U.S. deficiency payments) as well as a variety of other subsidies considered "non-distorting" (so called "green box" policies). As a result, in their assessment, there are likely to be few policy changes that will reduce the incentives to produce in DECD countries, and thus the hoped-for cut backs in subsidized outputs are unlikely to be realized.

SPAO (1995) stresses that global income growth, induced by the UR, will have a particularly strong effect on demand in particular commodities. Rising world incomes are predicted to expand sugar demand by 5 percent over baseline projections by the year 2000. In addition, smaller increases in coffee and cocoa exports are predicted.

/0, 14

I I I I

I I I I I I I I I I I I I I I

In another paper, Ingco (1995) concludes that the "new. commitments may not involve any further real reductions in current levels of domestic support" (p. 12).

This conclusion is accepted by other analysts, such as Francois, McDonald, and Nordstrom (1995) who state that the committed reduction in domestic support involves no cuts beyond those already undertaken in recent years. According to these analysts, the calculation of the base Aggregate Measure of Support, to which the cuts apply, is based on outlays during the period 1986 to 1988, which was characterized by relatively low world market prices for agricultural goods and therefore high outlays of domestic support to farmers. Because of a combination of higher world market prices and domestic reforms, the new commitments may not, at least in the short to medium run, entail any further cuts in domestic support. Believing the commitments to be impotent, these analysts drop them from any consideration in their economic modeling of the UR.

Export Subsidies: The impacts of reductions in export subsidies are expected to be more important. The agreement defines the permissible upper limit in the use of export subsidies by country and commodity and defines these limits in the individual country schedules. Where countries had no export subsidies in the base period, they are prohibited from using them in the future, and countries which use them cannot use them on products where they were not used in the base period. Developed countries are required to reduce the volume (quantity subsidized) of their subsidies to a level 21 percent below the volume in the base period 1986-90. They are required to reduce their budget outlays on subsidies to 36 percent of the average amount spent during the base period. These reductions should be made over the six-year implementing period. Developing countries are also required to reduce export subsidies, but by a lesser amount, over 10 years. The EU, United States, Canada, Turkey, Hungary, and Brazil are the most important subsidizers.

The reports by Hathaway and Ingco (1995) and Ingco (1995) analyze the reduction commitments of the major export subsidizers to assess the probable impact of these reductions on world markets for the relevant commodities, i.e., wheat, rice, sugar, dairy products, vegetable oil, coarse grains, beef and veal, pork, and pOUltry. They find that during the base period of 1986-90:

• Subsidized wheat accounted for nearly half of world trade in wheat;

• Subsidized dairy products accounted for over half of world trade in dairy products;

• Subsidized beef accounted for about one third of world trade in beef;

•

•

Subsidized coarse grains accounted for about a quarter of world trade in coarse grains; and

But subsidized exports in rice, sugar, and vegetable oil accounted for only about 5 percent of world trade in these commodities.

They conclude, therefore, that the export subsidy reductions will have significant impacts on world markets for wheat, beef, dairy products, and (to a lesser extent) coarse grains markets, but that they

15

will not significantly impact rice, vegetable oil, or other markets where subsidies have been less dominant. Price increases can be expected on wheat, dairy products, beef, and coarse grains, but the authors decline to speculate about the size of these increases, saying too much uncertainty surrounds how domestic policy shifts in the United States and EU may affect their use of export subsidies.

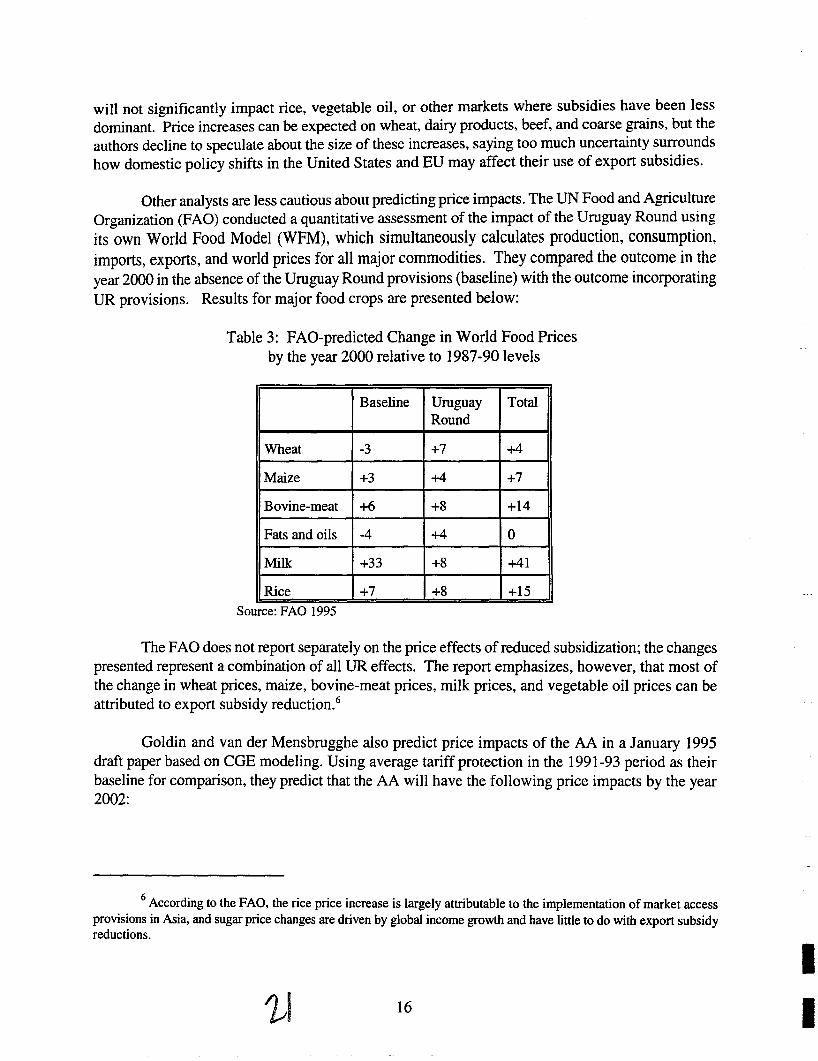

Other analysts are less cautious about predicting price impacts. The UN Food and Agriculture Organization (FAO) conducted a quantitative assessment ofthe impact of the Uruguay Round using its own World Food Model (WFM), which simultaneously calculates production, consumption, imports, exports, and world prices for all major commodities. They compared the outcome in the year 2000 in the absence of the Uruguay Round provisions (baseline) with the outcome incorporating UR provisions. Results for major food crops are presented below:

Table 3: FAD-predicted Change in World Food Prices by the year 2000 relative to 1987-90 levels

Baseline Uruguay Total Round

Wheat -3 +7 +4

Maize +3 +4 +7

Bovine-meat +6 +8 +14

Fats and oils -4 +4 0

Milk +33 +8 +41

Rice +7 +8 +15 Source: FAO 1995

The FAD does not report separately on the price effects of reduced subsidization; the changes presented represent a combination of all UR effects. The report emphasizes, however, that most of the change in wheat prices, maize, bovine-meat prices, milk prices, and vegetable oil prices can be attributed to export subsidy reduction.6

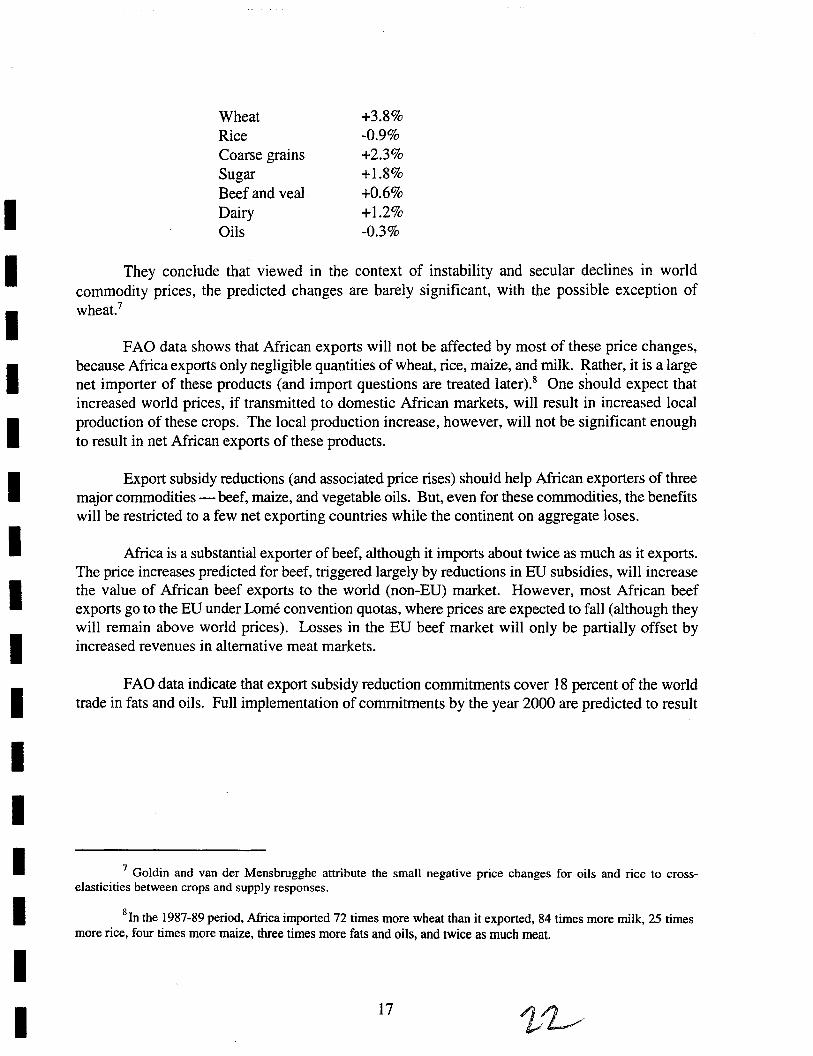

Goldin and van der Mensbrugghe also predict price impacts of the AA in a January 1995 draft paper based on CGE modeling. Using average tariff protection in the 1991-93 period as their baseline for comparison, they predict that the AA will have the following price impacts by the year 2002:

6 According to the FAO, the rice price increase is largely attributable to the implementation of market access provis~ons in Asia, and sugar price changes are driven by global income growth and have little to do with export subsidy reductIOns.

16

I I

I I I I I I I I I I I I I I

I I

Wheat +3.8% Rice -0.9% Coarse grains +2.3% Sugar +1.8% Beef and veal +0.6% Dairy +1.2% Oils -0.3%

They conclude that viewed in the context of instability and secular declines in world commodity prices, the predicted changes are barely significant, with the possible exception of wheat. 7

FAD data shows that African exports will not be affected by most of these price changes, because Africa exports only negligible quantities of wheat, rice, maize, and milk. Rather, it is a large net importer of these products (and import questions are treated later).8 One should expect that increased world prices, if transmitted to domestic Mrican markets, will result in increased local production of these crops. The local production increase, however, will not be significant enough to result in net African exports of these products.

Export subsidy reductions (and associated price rises) should help Mrican exporters of three major commodities - beef, maize, and vegetable oils. But, even for these commodities, the benefits will be restricted to a few net exporting countries while the continent on aggregate loses.

Africa is a substantial exporter of beef, although it imports about twice as much as it exports. The price increases predicted for beef, triggered largely by reductions in EU subsidies, will increase the value of African beef exports to the world (non-EU) market. However, most African beef exports go to the EU under Lome convention quotas, where prices are expected to fall (although they will remain above world prices). Losses in the EU beef market will only be partially offset by increased revenues in alternative meat markets.

FAD data indicate that export subsidy reduction commitments cover 18 percent of the world trade in fats and oils. Full implementation of commitments by the year 2000 are predicted to result

7 Goldin and van der Mensbrugghe attribute the small negative price changes for oils and rice to crosselasticities between crops and supply responses.

8In the 1987-89 period, Africa imported 72 times more wheat than it exported, 84 times more milk, 25 times more rice, four times more maize, three times more fats and oils, and twice as much meat.

17

in prices 4 percent higher for vegetable oils than without the UR. Although Africa as a whole is a net importer of vegetable oils, certain countries, such as Cote d'Ivoire, are net exporters that will benefit from the price increases.9

For maize, the FAD predicts that the reduction in subsidized exports under the DR is likely to cause higher international maize prices. A few Southern African countries that are normally net exporters will benefit from this increase, although in recent years drought conditions have made most of these countries net importers, like the rest of Africa. Interestingly, South Africa has been a subsidizer of maize exports in the past, and is required to reduce those subsidies in the Agricultural Agreement.

Will the AA require African countries to modify their own support program for crops that they export?

According to Harrold (1995) the negotiations in the Uruguay Round were essentially a conversation between developed countries. As a consequence, very little is asked of developing countries, particularly those in Africa.

In theory, developing countries are to reduce their domestic subsidization of agriculture (AMS) by 13 percent over 10 years, but in practice this measure will have no affect on agricultural support programs in Africa. This is because of the many exceptions given to all countries for "green box" policies and the special exceptions given to developing countries. Thus, virtually all government support measures for agriculture can be justified in Africa, including services such as agricultural research and extension, marketing and promotion, targeted credit provision, public stock holding for food security reasons, domestic food aid, regional assistance programs, investment subsidies, and agricultural input subsidies to low-income or resource-poor producers. For developing countries, subsidies that do not exceed 10 percent of the value of a country's agricultural production are exempt from discipline.

DR commitments on export subsidy reduction are also unlikely to impact African agricultural policy in any way, with the exception of South Africa. Least developed countries are exempt from reduction requirements, and African countries generally cannot afford and do not use export subsidies anyway. Indeed, their tradition has been one of taxing exports, a practice that is not disciplined by the GATT. The Agricultural Agreement disallows introduction of new export subsidies, thereby forbidding African countries from introducing export subsidies in the future, but this is probably not something they could afford or planned to do anyway. The door is left open for developing countries that want to subsidize marketing or internal transport of agricultural products. South Africa is the only African country that uses export subsidies on a regular basis. It has committed to reduce its subsidies on coarse grains from a base of 24 million metric tons to 19.5 million tons by the year 2000.

9 Ingco (1995) disagrees with the FAO assessment on vegetable oils, saying that the volume of subsidized exports is a small share of world trade and reductions are unlikely to have a significant impact on world prices (p. II).

18

• I I

I I I I I I I I I I I I I I I I

committed to reduce its subsidies on coarse grains from a base of 24 million metric tons to 19.5 million tons by the year 2000.

In sum, the AA will have little effect on Mrican export policies, with the exception of South Africa. According to the FAO (1994),

[I]t is apparent that the agricultural component of the UR agreement is primarily designed to affect the behavior of policy makers in developed countries, where agricultural producers generally benefit from substantial subsidies. In contrast, in many developing countries the main thrust of policy has been to tax agricultural producers, particularly those producing export crops. The extent to which agricultural producers and exporters are taxed is not likely to form a requirement of any international agreement, even though it is likely to form part of domestic reform policies.

The domestic support and export subsidy reduction measures in the AA thus will have virtually no affect on African export policies. The agreement, however, will have a greater effect on agricultural import policies, which are addressed separately below.

What are the probable impacts of the AA on agricultural imports and food security in Africa?

The AA can affect imports and food security in Africa in three ways:

• By requiring liberalization in the tariffs that African countries charge on food imports;

• By causing increases in world food prices, making iinports more expensive; and

• By influencing the availability of food aid.

Will the AA require African countries to lower tariffs and allow more imports?

Detractors of the Agricultural Agreement have asserted that it will require poor developing countries to throw their markets open to uncontrolled imports from developed countries that have large-scale farms, pushing peasants from their small farms into urban slums. A careful reading of the agreement, especially the associated country schedules, reveals that these assertions are groundless. In truth, very little is asked of developing countries under the AA and it requires very little actual tariff reduction in Africa.

Unlike industrial countries, developing countries were not required by the AA to bind their tariffs at a level based on their 1986-88 tariff levels. mstead, they were permitted to declare simple "ceiling bindings," without relation to existing tariffs, at levels they chose arbitrarily - at high levels in most cases. Developing countries are required to reduce these bound levels by 24 percent over

19

a 10-year period, but least developed countries are exempted from these reductions. Most African countries, therefore, made no tariff reduction commitments. 10

Harrold shows the extent of African commitments in Table 4 (which contains only the agricultural portion of the original table). The table shows that African bindings are very high, generally over 100 percent. Average applied rates in these commodities are usually well under 50 percent. Thus the ceiling bindings have no practical impact. Senegal, for example has bound itself to a ceiling of 180 percent compared with average applied tariffs of 44 percent. Sub-Saharan African countries make no commitments to reduce internal support or export subsidies, with the exception of South Africa. From these data, Harrold concludes that the rationalization of protection In

agriculture in Africa will have to rely on unilateral actions and not the WTO.

Ingco also shows how little the Agricultural Agreement asks of Sub-Saharan African countries. While all were required to bind their agricultural tariffs, most chose to do so at prohibitive levels (100-300 percent) set way above pre-DR levels of protection. And very few Sub-Saharan African countries offered reductions in their ceiling bindings, with only Cote d'Ivoire, Ghana, and Zimbabwe offering minimum reductions on several commodities. The South African Customs Dnion (South Africa, Swaziland, and Namibia) is the exception, as it committed to reduce its duties from more than 70 percent to 40 percent over six years.

In North Africa, the DR commitments indicate no or very little liberalization in most commodities. In Morocco, for example, import licenses have been maintained for many commodities and state trading enterprises continue to monopolize imports of most grains, vegetable oils, and sugar. In the DR, Morocco established tariff equivalents which provide potentially higher rates of protection for most agricultural products. The bound tariffs submitted by Morocco were substantially higher than the actual tariff equivalent rates during the base period. Although these tariffs are to be reduced by 24 percent, most commodities will still receive higher protection rates at the end of the DR implementation period relative to the pre-DR period. In the case of wheat, for instance, the bound tariff was set at 190 percent for durum wheat in 1995, declining to 144 percent in 2004, which is still higher than the estimated tariff equivalent at 130 percent in 1986-88.

Aside from tariffs, there are three other areas where African policy makers have expressed concerns about the AA's impact on food import policies.

10 According to Hathaway and Ingco (1995), "it was not until the country schedules were tabled in the final days of 1993 and early 1994 that it was generally recognized that developing countries could choose to escape the disciplines and that many had chosen to do so."

20

• I I I I

I I I I I I I I I I I I I I I

Country

Benin

Burkina Faso

Cameroon

Congo

Cote d'Ivoire

Gabon

Ghana

Kenya

Madagascar

Mali

Mauritania

Mauritius

Namibia

Niger

Nigeria

Senegal

South Africa

Swaziland

Tanzania

Uganda

Zambia

Zimbabwe

Table 4: Agricultural commitments in the DR by Sub-Saharan African Countries

GAIT Status Average rate of tariff Average applied binding (%) rates (%)

LD 80

LD 150 .

D 310

D 30

D 215

D 260

D 98 22*

D 100 44*

LD 280

LD 110

LD 54

D 135

D 40

LD 132

D 230 47*

D 180 44*

IND 40 7*

D 40

LD 240

LD 80

LD 124

D 161 24* LD=least developed, D=developmg, IND=mdustnahzed *from GAIT Trade Policy Reviews, latest available • provided list of permitted programs but no subsidy reduction commitments source: Harrold (1995)

21

Domestic Export support subsidies

- -

- -

- -

- -

• -

- -

- -

- -

- -

• -- -

- -

- -

- -

- -

• -

by 2000 by 2000

- -

- -

- -- -

- -

The first has to do with state trading enterprises and their monopoly on imports of various food commodities in many African countries. Such monopolies are not prohibited by the AA. Their "mark-ups," however, are constrained, in theory, by countries' tariff bindings. As Ingco explains, "if a tariff is bound, at say 40 percent, any duty at the border greater than 40 percent is prohibited whether it is a tax levied by the government or a "mark u" charged by a state trading enterprise (STE) ... Under the agreement, STEs or any import monopoly cannot provide domestic protection in excess of the tariff bindings" (p. 7). However, as shown earlier, bindings were set so high in most African countries that this constraint on "mark ups" will not be relevant for the foreseeable future. Ingco (1995) argues that the AA failed to bring any discipline to STEs, thereby leaving room for significant trade distortions, and she is skeptical about the ability of the WTD to control STE actions or discipline resale prices.

Variable levies are another policy issue affected by the AA. In the last few years, a few African countries have been considering establishing variable levies on commodity imports as a means to insulate their markets from world price instability. Under the GATT and the UR, these types of variable levies are formally forbidden. Ingco points out, however, that the door is not closed on variable levies. Under the AA, countries can charge tariffs at varying levels within the margin of the binding, which could be linked to an internal price. The duty can be set as the difference of the given domestic price and the world price as long as the tariff charged does not exceed the binding. In practice, this could work like a variable levy. The permissibility of such a policy remains ambiguous at this time.

A third import policy that may be affected by UR rules is the use of minimum prices in customs valuation. In West Africa, customs offices routinely use minimum price lists (prix mercuriales) to assess the value of imported goods. The technique is designed to reduce customs fraud and under-invoicing for tax evasion. Under the UR, an agreement on customs valuation prohibits the use of minimum prices, requiring their phase-out in five years; however, it is unclear how rigorously this will be enforced in the case of Africa.

How will the AA affect food import expenses?

Until very recently, most analysts predicted that the AA would cause a substantial rise in international food prices, thereby causing sizable increases in the food import bills of developing countries. The international price increases would be driven by subsidy reductions in the DEeD countries and therefore reduced production and tighter supplies. According to the FAD (1995), developing countries in Africa can expect their food import bill to increase from $6 billion in 1989 to $10.5 billion in the year 2000, with about $0.5 billion of the increase (11 percent) attributable to the effects of the Uruguay Round. The FAD predicts that the UR will lead to increases in wheat prices by 7 percent, rice prices by 8 percent, and maize prices by 4 percent.

There have been widespread concerns about these projected increases and their impact on the poorest food importing countries. According to the FAD, there will be cases where low-income developing countries that are frequent recipients of targeted export subsidies will see the availability

t1 22

I I I I

I I I I I I I I I I I I I I I I

of these subsidies reduced and as a result will have to pay world market prices for more of their food at a time when world prices are expected to increase.

In response to these concerns, the UR issued a "Decision on Measures Concerning the Possible Negative Effects of the Reform Programme on Least-developed and Net Food Importing Countries." This decision recognizes the concerns of developing countries and suggests that some compensation be provided in the form of food aid and technical assistance for agricultural development. The Decision also refers to the possibility of assistance from the International Monetary Fund and the World Bank with respect to the short-term financing of food imports. The Decision is not very specific or operational, but its implementation is the responsibility of the WTO's Committee of Agriculture.

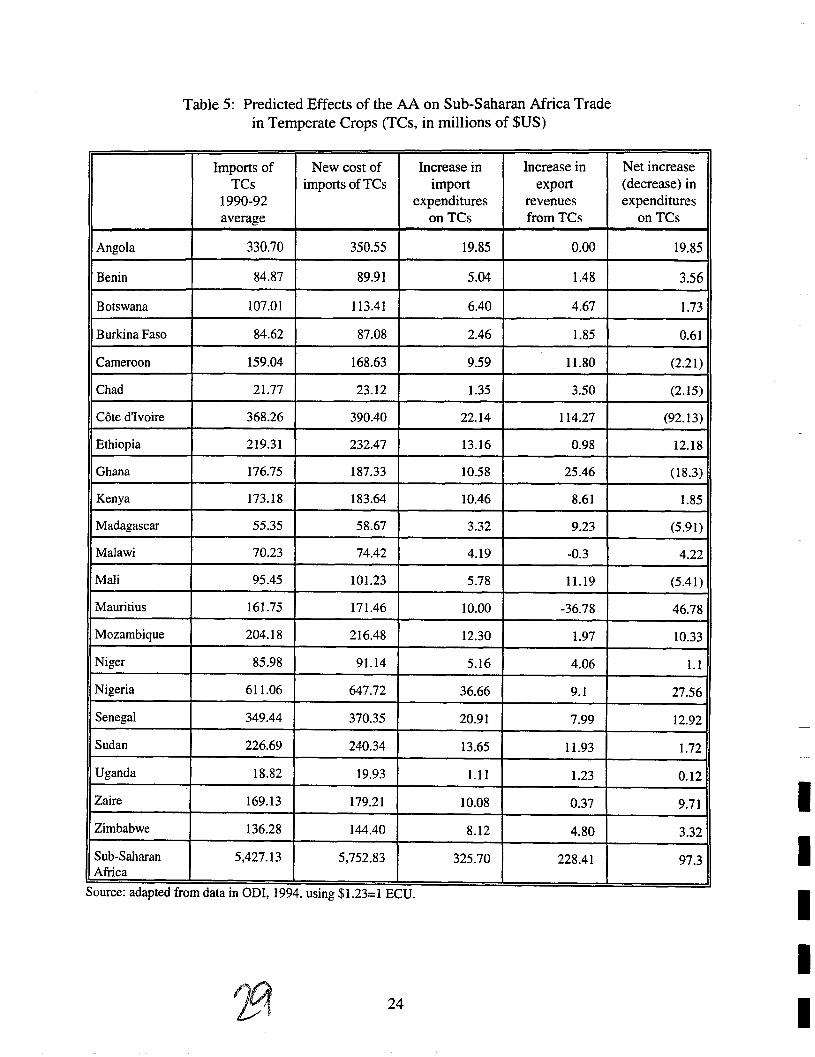

ODI examines the question of food import bills in its 1994 report on the ACP States. ODI assumes that the AA will cause a 5 percent increase in the prices of temperate crops such as wheat and an 8 percent increase in sugar prices. As a result of these price increases, Sub-Saharan Africa's annual food import bill is projected to increase from $5.43 billion to $5.75 billion because of the AA (assuming import volumes are constant). This $320 million increase is offset to some degree by improved earnings from African exports of temperate crops, so that the net food expenditure increase for Africa is estimated at $97 million. Table 5, adapted from the OD! report, shows the effects on selected SSA countries.

Harrold, commenting on the ODI study, concludes that price increases caused by the AA will raise the net food deficit in Sub-Saharan Africa by "about $100 million only, or perhaps close to $200 million if the gainsfor Cote d'Ivoire and Ghana (the only major winners) were excluded." Harrold concludes that "Clearly, therefore, we are discussing a change that might affect import bills by a fraction of 1 percent, and an effect that will therefore be de minimis."

Harrold also questions ODI's assumptions about food price rises, suggesting that 5 percent is likely to be an overestimate. This questioning is supported by the modeling results of Goldin and van der Mensbrugghe (1995) which predict wheat price rises caused by the UR of only 1.2 to 3.8 percent and coarse grain price rises of only 0.1 to 2.3 percent. Goldin and van der Mensbrugghe conclude that viewed in the context of instability in world commodity prices, and given that UR changes will be phased in gradually, the predicted changes are "barely significant."

Nonetheless, they recognize that even small food price increases can have negative consequences for the most food insecure countries, particularly in Africa. ODI predicts that Ethiopia, for example, will see its annual imported food bill increase by $13 million because of the AA. If OEeD agricultural subsidies are cut more deeply in future negotiating rounds, these effects can be expected to become more severe. Goldin and van der Mensbrugghe predict that Africa would suffer a $2.5 billion income loss if, someday, OECD countries made genuine 36 percent cuts in their overall subsidization of agriculture.

Much of this discussion became moot in 1995-96 because of rises in world markets for temperate crops. Droughts in Australia and the United States and expanded imports by China led

23

Angola

Benin

Botswana

Burkina Faso

Cameroon

Chad

Cote d'Ivoire

Ethiopia

Ghana

Kenya

Madagascar

Malawi

Mali

Mauritius

Mozambique

Niger

Nigeria

Senegal

Sudan

Uganda

Zaire

Zimbabwe

Sub-Saharan Africa

Table 5: Predicted Effects of the AA on Sub-Saharan Africa Trade in Temperate Crops (TCs, in millions of $US)

Imports of New cost of Increase in Increase in TCs imports of TCs import export

1990-92 expenditures revenues average on TCs from TCs

330.70 350.55 19.85 0.00

84.87 89.91 5.04 1.48

107.01 113.41 6.40 4.67

84.62 87.08 2.46 1.85

159.04 168.63 9.59 11.80

21.77 23.12 1.35 3.50

368.26 390.40 22.14 114.27

219.31 232.47 13.16 0.98

176.75 187.33 10.58 25.46

173.18 183.64 10.46 8.61

55.35 58.67 3.32 9.23

70.23 74.42 4.19 -0.3

95.45 101.23 5.78 11.19

161.75 171.46 10.00 -36.78

204.18 216.48 12.30 1.97

85.98 91.14 5.16 4.06

611.06 647.72 36.66 9.1

349.44 370.35 20.91 7.99

226.69 240.34 13.65 11.93

18.82 19.93 1.11 1.23

169.13 179.21 10.08 0.37

136.28 144.40 8.12 4.80

5.427.13 5.752.83 325.70 228.41

Source: adapted from data mODI. 1994. usmg $1.23=1 ECU.

24

Net increase (decrease) in expenditures

on TCs

19.85

3.56

1.73

0.61

(2.21)

(2.15)

(92.13)

12.18

(18.3)

1.85

(5.91 )

4.22

(5.41)

46.78

10.33

1.1

27.56

12.92

1.72

0.12

9.71

3.32

97.3

I I I I I

I I I I I I I I I I I I I

I I

to unusually high world prices. Analysts agreed that these high prices had little to do with the Uruguay Round.

Because of the high prices, the United States and the EU suspended their subsidization of agricultural exports for almost all temperate crops. The programs were suspended not because of the AA but because world prices were so high that farmers could make profits without export subsidies. The EU, in fact, switched from subsidizing wheat exports to actually taxing them.

in this context, AA commitments to reduce export subsidies are irrelevant. There are no grain subsidies to reduce at this time. Therefore, one cannot say that the AA commitments to reduce export subsidies are causing food price increases.

Since world markets are predicted to remain relatively tight and food prices high, the AA commitments to reduce export subsidies will remain irrelevant. Eventually, this situation changed - prices have fallen, but OECD countries have not expanded their export subsidization again.

How will the AA affect food aid and government stockholding of food commodities?

The Agricultural Agreement states that members that are donors of international food aid shall ensure:

(a) That the provision of international food aid is not tied directly or indirectly to commercial exports of agricultural products to recipient countries;

(b)

(c)