IIFM Interbank Unrestricted Master Investment … IIFM Interbank Unrestricted Master Investment...

13

1 IIFM Interbank Unrestricted Master Investment Wakalah Agreement IIFM Industry Seminar on Islamic Capital and Money Market Hosted by Bank Indonesia Tuesday, 6 th May 2014, Jakarta Ijlal Ahmed Alvi Chief Executive Officer IIFM What is the IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement? The IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement is a framework agreement which sets out the terms upon which the Muwakkil (Investor) will transfer certain funds to the Wakil (Agent) as its agent to invest such funds in a Shari’ah compliant manner Entering into the Master Agreement does not of itself give rise to any transactions. After the Parties have entered into the Master Agreement, they may subsequently enter into Wakalah Investment Transactions which will be subject to and governed by the Master Agreement Note that the Governing Law of the Master Agreement may be decided by the Parties, although the Agreement had been prepared on the implicit understanding that English Law will be the Governing Law predominantly used 1 IIFM Industry Seminar on Islamic Capital and Money Market Tuesday, 6 th May 2014, Bank Indonesia, Jakarta

Transcript of IIFM Interbank Unrestricted Master Investment … IIFM Interbank Unrestricted Master Investment...

1

IIFM Interbank Unrestricted Master Investment Wakalah Agreement

IIFM Industry Seminar on Islamic Capital and Money Market Hosted by Bank Indonesia

Tuesday, 6th May 2014, Jakarta

Ijlal Ahmed Alvi

Chief Executive Officer

IIFM

What is the IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement?

The IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement is a framework agreement which sets out the terms upon which the Muwakkil (Investor) will transfer certain funds to the Wakil (Agent) as its agent to invest such funds in a Shari’ah compliant manner

Entering into the Master Agreement does not of itself give rise to any transactions. After the Parties have entered into the Master Agreement, they may subsequently enter into Wakalah Investment Transactions which will be subject to and governed by the Master Agreement

Note that the Governing Law of the Master Agreement may be decided by the Parties, although the Agreement had been prepared on the implicit understanding that English Law will be the Governing Law predominantly used

1 IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

2

What is the purpose of entering into an Unrestricted Inter-Bank Wakalah Agreement?

For many years, IFI’s have relied mainly on commodity Murabahah for their wholesale liquidity management purposes notwithstanding issues and concerns related to commodity Murabahah transactions, such as the cost of commodity brokerage, or the amount of Shari‘ah compliant commodities available at any particular moment in time to cover transaction volumes etc

In order to diversify the range of liquidity management solutions available to the IFI’s, the last few years have witnessed the active use by IFI’s of Wakalah arrangements/transactions particularly Unrestricted Wakalah as an alternative liquidity management tool. The objective of this activity has been to reduce the over reliance by the IFI’s on commodity Murabahah

2 IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

What are the Key Features of the Master Agreement?

The key features of IIFM Inter-Bank Unrestricted Master Investment Wakalah Agreement are:

Clause 1 (Definitions and Construction)

This clause defines terms used in this Wakalah Master Agreement, details the rules of construction which apply to the Master Agreement and explicitly states that only the Parties may enjoy the benefits of this Master Agreement (Clause 1.4). In addition, the purpose of Clause 1.3 (Single Contract) is to clarify that, as the Master Agreement is a framework agreement, when Wakalah Investment Transactions are subsequently entered into, the Master Agreement will apply to such Wakalah Investment Transactions. So, although a Wakalah Investment Transaction will be a separate document, the Wakalah Investment Transaction will be regarded as entered into upon the terms set out in the Master Agreement and covered by the framework created by the Master Agreement.

3 IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

3

Clause 2 (Wakalah Terms and Conditions)

This clause deals with the appointment by the Muwakkil of the Wakil as its agent in relation to each Wakalah Investment Transaction

Clause 3 (Wakalah Investment Transactions)

This clause states that the Master Agreement does not of itself create an obligation on the part of the Wakil or the Muwakkil to enter into any Wakalah Investment Transactions.

Clause 4 (Payments)

This clause deals with the mechanics of how payments are made under this Master Agreement, the currency of payments

4

What are the Key Features of the Master Agreement? (continuation)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Clause 5 (Representations)

This clause contains a set of standard representations which each Party is required to make including that they have the power and authority to enter into Wakalah Investment Transactions and that they do not have any proceedings pending against them.

Clause 6 (Undertakings)

This clause requires each Party to undertake amongst other things that it will comply with all laws and regulations to which it may be subject and that it will notify the other Party of any Default.

Clause 7 (Events of Default)

The occurrence of certain events will result in termination of any Wakalah Investment Transactions then in existence. Such events include the Wakil failing to pay any amounts under the Master Agreement, misrepresentation by a Party and insolvency. The clause also details what happens upon the occurrence of an Event of Default (See Clause 7.7) and the payments due thereunder (See Clause 7.8).

5

What are the Key Features of the Master Agreement? (continuation)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

4

Clause 8 (Early Termination)

This clause deals amongst other things with the right of the Muwakkil to terminate a Wakalah Investment Transaction, the Wakil’s acceptance of an Early Termination Request and the ability of the Wakil to notify the Muwakkil of a Revised Anticipated Profit Rate (See Clause 8.3).

Clause 9 (Late Payment Amount)

This clause obliges a Party to pay a Late Payment Amount where it fails to pay a sum on a Due Date. Clause 9.2 (Calculation of Late Payment Amount) deals with how the Late Payment Amount is calculated and Clause 9.3 (Payment of Late Payment Amount) covers how such amount shall be applied.

6

What are the Key Features of the Master Agreement? (continuation)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Clause 10 (Miscellaneous)

This clause contains miscellaneous agreements of the Parties, including a provision that neither Party may assign its rights under the Master Agreement and when notices are deemed to be served.

Clause 11 (Governing Law and Jurisdiction)

This clause contains the governing law and dispute resolution forum provisions. The governing law is to be selected by the Parties. The forum for dispute resolution will be the courts of the jurisdiction of the governing law unless the Parties choose arbitration.

7

What are the Key Features of the Master Agreement? (continuation)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

5

The Schedules

1. Schedule 1 (Form of Wakil Offer Notice) (Offer)

2. Schedule 2 (Form of Muwakkil Acceptance Notice)

When the Parties wish to enter into a Wakalah Investment Transaction they should do so by completing Schedules 1 and 2 in accordance with the mechanics detailed in Clause 3 (Wakalah Investment Transactions).

8

What are the Key Features of the Master Agreement? (continuation)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Are There Any Other Features of the Master Agreement?

Yes, this agreement is supplemented with a set of items as follows:

1. Operational Guidance Memorandum which covers the operational procedures to be implemented by the Wakil as well as the Wakil and Muwakkil responsibilities

9 IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

6

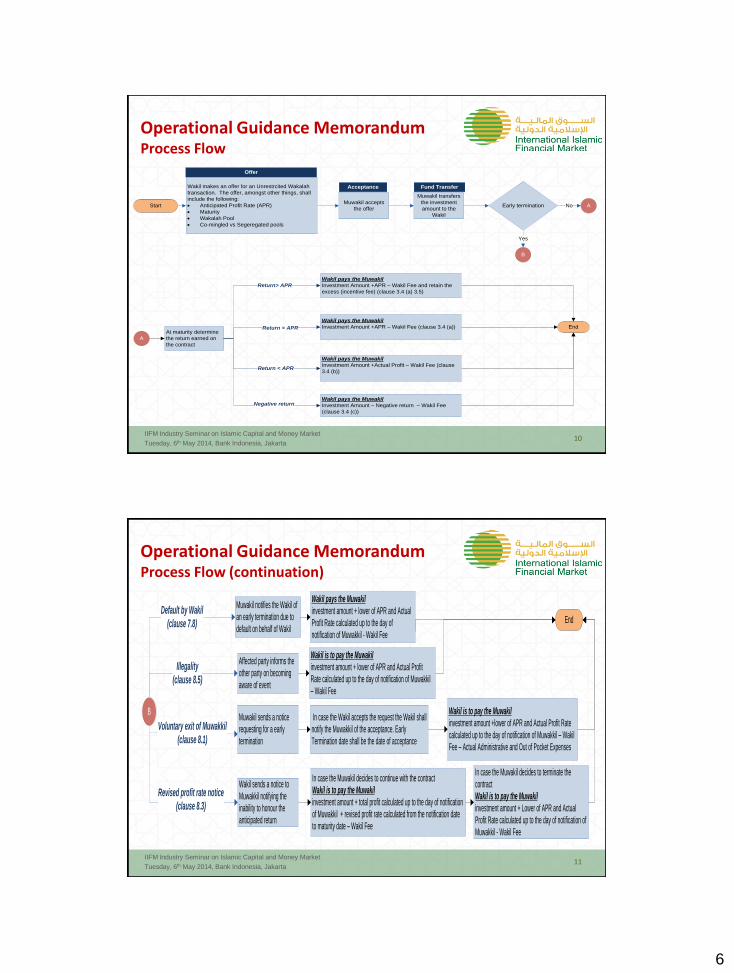

Operational Guidance Memorandum Process Flow

10

Start

Wakil makes an offer for an Unrestrcited Wakalah

transaction. The offer, amongst other things, shall

include the following:

· Anticipated Profit Rate (APR)

· Maturity

· Wakalah Pool

· Co-mingled vs Segeregated pools

Muwakil accepts

the offer

Muwakil transfers

the investment

amount to the

Wakil

Early termination A

B

No

Yes

A

Offer

Acceptance Fund Transfer

At maturity determine

the return earned on

the contract

Wakil pays the Muwakil

Investment Amount +APR – Wakil Fee and retain the

excess (incentive fee) (clause 3.4 (a) 3.5)

Wakil pays the Muwakil

Investment Amount +APR – Wakil Fee (clause 3.4 (a))

Wakil pays the Muwakil

Investment Amount +Actual Profit – Wakil Fee (clause

3.4 (b))

Return> APR

Return = APR

Return < APR

Wakil pays the Muwakil

Investment Amount – Negative return – Wakil Fee

(clause 3.4 (c))

Negative return

End

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

11

Affected party informs the

other party on becoming

aware of event

B

Default by Wakil

(clause 7.8)

Wakil sends a notice to

Muwakkil notifying the

inability to honour the

anticipated return

Muwakil sends a notice

requesting for a early

termination

Voluntary exit of Muwakkil

(clause 8.1)

Revised profit rate notice

(clause 8.3)

Illegality

(clause 8.5)

Wakil is to pay the Muwakil

investment amount + lower of APR and Actual Profit

Rate calculated up to the day of notification of Muwakkil

– Wakil Fee

In case the Wakil accepts the request the Wakil shall

notify the Muwakkil of the acceptance. Early

Termination date shall be the date of acceptance

Muwakil notifies the Wakil of

an early termination due to

default on behalf of Wakil

Wakil pays the Muwakil

investment amount + lower of APR and Actual

Profit Rate calculated up to the day of

notification of Muwakkil - Wakil Fee

Wakil is to pay the Muwakil

investment amount +lower of APR and Actual Profit Rate

calculated up to the day of notification of Muwakkil – Wakil

Fee – Actual Administrative and Out of Pocket Expenses

In case the Muwakil decides to continue with the contract

Wakil is to pay the Muwakil

investment amount + total profit calculated up to the day of notification

of Muwakkil + revised profit rate calculated from the notification date

to maturity date – Wakil Fee

In case the Muwakil decides to terminate the

contract

Wakil is to pay the Muwakil

investment amount + Lower of APR and Actual

Profit Rate calculated up to the day of notification of

Muwakkil - Wakil Fee

End

Operational Guidance Memorandum Process Flow (continuation)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

7

Does the agreement require minimum risk assessment procedures and due diligence to be

carried out by the contracting parties and what are the contracting parties responsibilities?

Muwakkil retains the risk of loss of principal and there is no loss indemnification by the Wakil; (clause 2.4)

Muwakkil’s minimum due diligence (clause 2.1 (e))

Wakil is expected to communicate with the Muwakkil in a transparent manner both before and after the execution of the Wakalah Investment Transaction until maturity. (clauses 2.3 (a), (b) and (d))

12

Operational Guidance Memorandum Risk Management

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

As a commitment to transparent and enhanced disclosures as an agent

in the financial sector, the Wakil should also consider presenting a business plan or a feasibility report to the Muwakkil before the Wakalah Investment Transaction. Such business plan shall include description on the Wakil’s investment plan including the targeted Wakalah Pool (mix, sector, geography, asset class, liquidity features etc.), indicative returns that the Wakil expects the Wakalah Pool to generate and the Wakil’s assessment of ability to liquidate the Wakalah Pool at the time of Investment Maturity.

13

Operational Guidance Memorandum Risk Management (continuation)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

8

Commingled or general treasury pool

Segregated pool

Asset allocation within the Wakalah Pool

Replacement of assets in Wakalah Pool

14

Operational Guidance Memorandum Wakalah Pool

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Actual Profit Rate

Actual Profit Rate different from the Anticipated Profit Rate? What are the consequences

In case the Actual Profit is in excess of the Anticipated Profit Rate, is Wakil required to disclose the incentive fee to the Muwakkil?

15

Operational Guidance Memorandum Anticipated Profit Rate

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

9

Accounting assessment

IIFM Interbank Unrestricted Master Investment Wakalah Agreement

16 IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Background

17

The IIFM Agreement is primarily designed for use in interbank transactions, although its framework may be applicable for other unrestricted Wakalah arrangements. The IIFM Agreement has been developed for use by IFIs to reduce their over reliance on commodity Murabaha. Although both restricted and unrestricted Wakalah were generally being used, the unrestricted Wakalah arrangement has greater potential to emerge as one of the main Islamic inter-bank money market tools. However, comprehensive discussions were needed among Shari’a scholars and market practitioners to develop solutions on the following issues: • Credit risk; • Issue of off-balance sheet and on balance sheet treatment; • Operational handling of asset pool and indicative rate of return; • Regulatory environment and applicability of arrangement; and • Accounting issues and legal interpretation.

IIFM had attempted through the IIFM Agreement to address these issues through a standardised approach that will provide the IFIs direction on the use of inter-bank unrestricted Wakalah. In this analysis, we have assessed the accounting implications of the IIFM Agreement from the perspective of the receiving IFI (Wakil).

For the purpose of our assessment, we have considered the following:

• A comingled pool would imply that the Wakil would identify from its pool of jointly financed assets a reference pool of assets for the Wakalah Investment that would be used to calculate profits and for distributions. However, the Wakil has the ability to change the composition of this reference pool of assets.

• In a segregated pool, an identified pool of assets is allocated/ acquired using the Wakalah Investment and all cash flows from this pool is passed to the investment accountholders after deduction of agreed fees and incentives.

Key IIFM Agreement features relevant for accounting assessment

The unrestricted nature of the product allows the Wakil to invest the proceeds at its discretion

The funds are comingled and invested in a floating pool of assets (i.e. no legal separation and could be a pre-existing asset pool)

The underlying pool is allocated but not legally ring-fenced and can be changed at the Wakil’s discretion

Returns are calculated on a floating reference pool, but cash flows are not fully assigned and passed on to the investors (i.e. incentives accrue to the benefit of the Wakil and allocation of the pool is at the Wakil’s discretion)

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

10

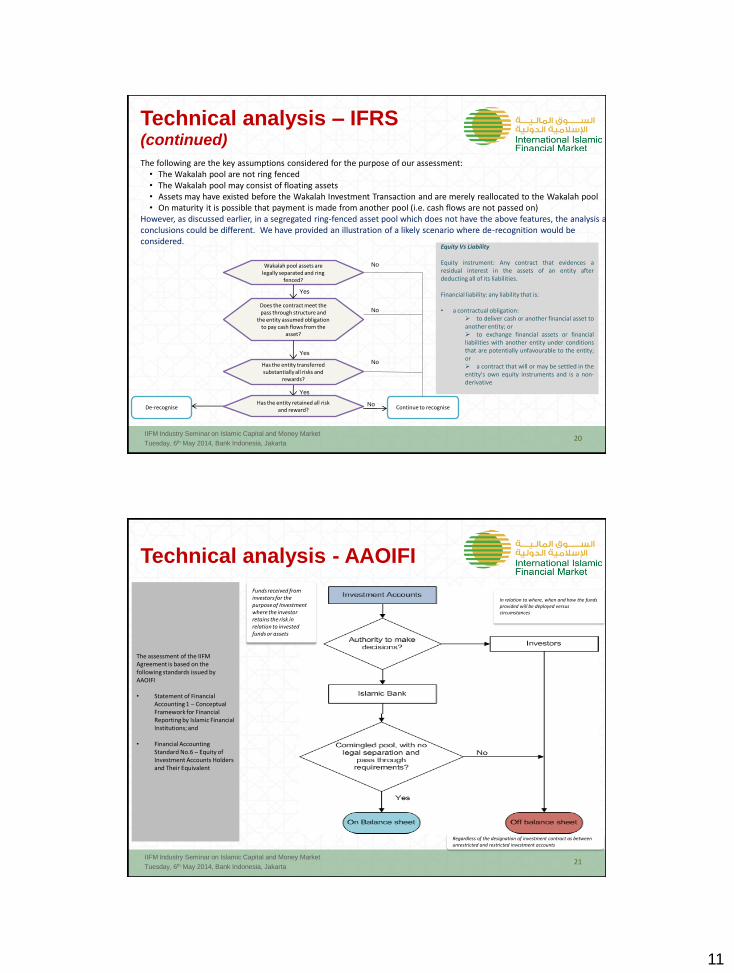

Technical analysis - IFRS

18

De-recognition requirements for financial assets

The below flowchart depicts the de-recognition requirements of

financial assets under IAS 39 in a glance:

Determine whether de-recognition principles below are applied to a part or all of an asset (or group of similar assets)

Have rights to cash flows from the asset expired?

Has the entity transferred the right to receive cash flows

from the asset?

Has the entity assumed obligation to pay cash flows

from the asset?

Has the entity transferred substantially all risks and

rewards?

Has the entity retained all risk and reward?

Has the entity retained control of the asset?

Derecognise

Continue to recognise

Derecognise

Continue to recognise

Derecognise

Continue to recognise

Yes

No

Yes

Yes

Yes

Yes

No

No

No

No

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Technical analysis – IFRS (continued)

19

Condition Assessment Comingled pool

Segregated pool

De-recognition condition to part or a group of financial assets?

Would be applied to the underlying reference pool of assets and not to individual assets - -

Rights to contractual cash flows from the asset expired?

No, the rights to cash flows from the assets would not expire until disposal.

Has the entity transferred the right to receive cash flows from the asset?

Although the Wakalah contract would imply that the cash flows from the underlying pool of assets would be used to repay the investment, there is no contractual transfer of rights as the asset pool remains to be floating (a reference pool only) and is part of a comingled pool. There is no clearly identifiable cash flows that can be identified and allocated for the Wakalah account. This may be possible in a ring fenced segregated pool.

? Has the entity assumed obligation to pay cash flows from the asset?

Same as above. In a comingled pool, the cash flows from the entire group of underlying assets is not contractually assigned towards the obligations. The pool is floating and could be bought and sold during the investment period without transfer of cash flows. The cash flow is assigned/ arranged only at the time of settlement. However, this could be possible in a ring fenced segregated pool structure where pass through criteria under IAS 39 is met.

?

Has the entity transferred substantially all risks and rewards?

This depends on the pool of assets and returns generated and the proportion distributed. To the extent of the investors share in the pool, the risk is transferred. However, the upside of investors may be capped thereby providing more rewards to the Wakil. Hence, whether substantially all benefits get passed would need to be assessed on a case-by-case basis.

Has the entity retained all risk and reward?

No, usually all risk and rewards would not be retained. Example, risk of impairment is not generally retained and fully passed on to the investors.

Has the entity retained control of the asset?

Yes

Criteria for de-recognition met?

As assessed above, the assets in a comingled pool would not meet the de-recognition criteria. In a ring-fenced segregated pool that qualifies a pass through test, de-recognition may be possible. If the asset is recognised on-balance sheet, the funding would also be reflected on-balance sheet.

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

11

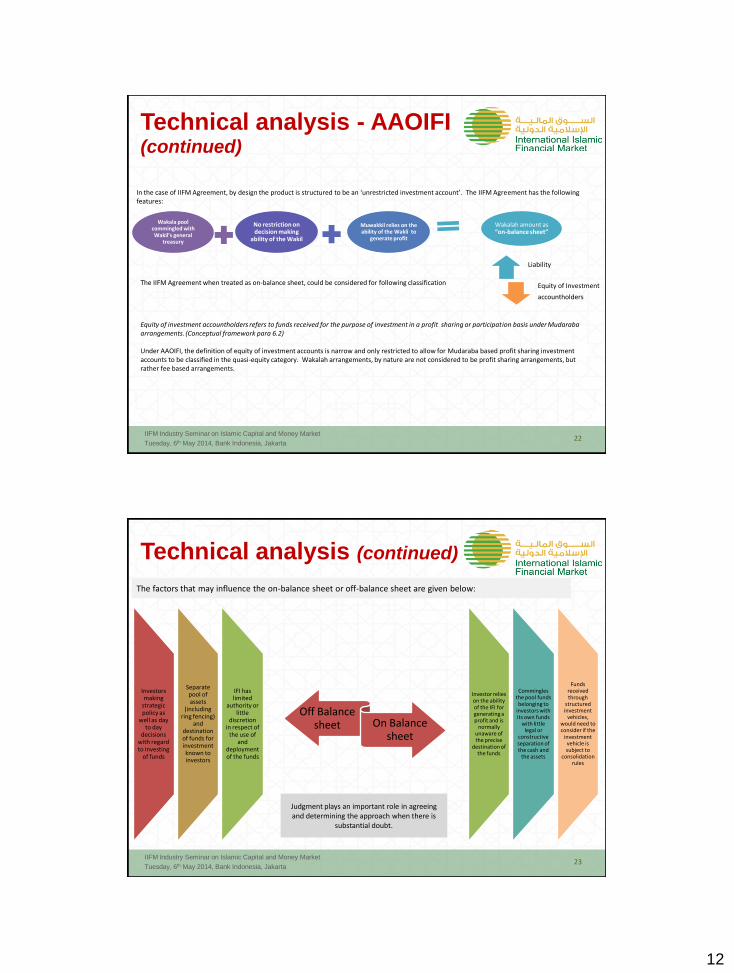

Technical analysis – IFRS (continued)

20

The following are the key assumptions considered for the purpose of our assessment: • The Wakalah pool are not ring fenced • The Wakalah pool may consist of floating assets • Assets may have existed before the Wakalah Investment Transaction and are merely reallocated to the Wakalah pool • On maturity it is possible that payment is made from another pool (i.e. cash flows are not passed on)

However, as discussed earlier, in a segregated ring-fenced asset pool which does not have the above features, the analysis and conclusions could be different. We have provided an illustration of a likely scenario where de-recognition would be considered.

Wakalah pool assets are legally separated and ring

fenced?

Does the contract meet the pass through structure and

the entity assumed obligation to pay cash flows from the

asset?

Has the entity transferred substantially all risks and

rewards?

Has the entity retained all risk and reward? Continue to recognise

No

Yes

Yes

No

Yes

De-recognise

No

No

Equity Vs Liability Equity instrument: Any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Financial liability: any liability that is: • a contractual obligation:

to deliver cash or another financial asset to another entity; or to exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavourable to the entity; or a contract that will or may be settled in the entity's own equity instruments and is a non-derivative

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Technical analysis - AAOIFI

21

Regardless of the designation of investment contract as between unrestricted and restricted investment accounts

The assessment of the IIFM Agreement is based on the following standards issued by AAOIFI • Statement of Financial

Accounting 1 – Conceptual Framework for Financial Reporting by Islamic Financial Institutions; and

• Financial Accounting Standard No.6 – Equity of Investment Accounts Holders and Their Equivalent

In relation to where, when and how the funds provided will be deployed versus circumstances

Funds received from investors for the purpose of Investment where the investor retains the risk in relation to invested funds or assets

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

12

Technical analysis - AAOIFI (continued)

22

Wakala pool commingled with Wakil’s general

treasury

No restriction on decision making

ability of the Wakil

Muwakkil relies on the ability of the Wakli to

generate profit

Wakalah amount as “on-balance sheet”

In the case of IIFM Agreement, by design the product is structured to be an ‘unrestricted investment account’. The IIFM Agreement has the following features:

The IIFM Agreement when treated as on-balance sheet, could be considered for following classification

Liability

Equity of Investment

accountholders

Equity of investment accountholders refers to funds received for the purpose of investment in a profit sharing or participation basis under Mudaraba arrangements. (Conceptual framework para 6.2) Under AAOIFI, the definition of equity of investment accounts is narrow and only restricted to allow for Mudaraba based profit sharing investment accounts to be classified in the quasi-equity category. Wakalah arrangements, by nature are not considered to be profit sharing arrangements, but rather fee based arrangements.

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Technical analysis (continued)

23

The factors that may influence the on-balance sheet or off-balance sheet are given below:

Off Balance sheet On Balance

sheet

Investors making

strategic policy as

well as day to day

decisions with regard to investing

of funds

Separate pool of assets

(including ring fencing)

and destination of funds for investment known to investors

IFI has limited

authority or little

discretion in respect of

the use of and

deployment of the funds

Investor relies on the ability of the IFI for generating a profit and is

normally unaware of the precise

destination of the funds

Commingles the pool funds belonging to

investors with its own funds

with little legal or

constructive separation of the cash and

the assets

Funds received through

structured investment

vehicles, would need to consider if the

investment vehicle is subject to

consolidation rules

Judgment plays an important role in agreeing and determining the approach when there is

substantial doubt.

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

13

General

24

The analysis in this presentation is the view of the speaker and is based on the current form of the IIFM Agreement provided to us. If the IIFM Agreement is modified and the facts, assumptions or circumstances are modified, the analysis may be different. This assessment does not constitute regulatory, legal or Shari’a advice. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation, applicable local laws and regulations. This assessment is given solely in connection with the IIFM Agreement under IFRS and FAS and does not provide any conclusion or opinion on the regulatory treatment for prudential reporting or capital adequacy purposes. Our assessment is on the basis of applicable and effective IFRSs and FAS as of the date of this document, and we are under no obligation to update it in the event of subsequent changes to such standards and practice. This assessment is non-public and confidential in nature and it is for your benefit and information only and that, it shall not be copied, referred to or disclosed, in whole (save for your own internal purposes) or in part, without our prior written consent. The terms and definitions used in this document should be read in conjunction with the IIFM Agreement and Wakala Operational Guidelines issued by IIFM.

IIFM Industry Seminar on Islamic Capital and Money Market

Tuesday, 6th May 2014, Bank Indonesia, Jakarta

Shukaran Wassalamu ‘Alaikum

International Islamic Financial Market (IIFM) Office No. 72, 7th Floor, Zamil Tower (Main Tower), P.O. Box: 11454, Manama, Kingdom of Bahrain Tel: +973 17500161 , Fax: +973 17500171, Email: [email protected], Website: www.iifm.net Disclaimer: The information herein has been obtained from sources believed to be reliable but cannot be guaranteed. The views or opinions expressed are subjected to change at any time. Neither the information nor any opinion expressed can be construed as a solicitation for the purchase or sale of any securities. International Islamic Financial Market disclaims liability in this respect.