IIFL Sector Report: Weaving a digital story

42

Transcript of IIFL Sector Report: Weaving a digital story

1 | P a g e

Premia Research

Table of Contents

NSE

Table of Contents Page No.

Sectoral Outlook 2

Key Global markets trends 3-7

India’s growth on global trends 8-11

Favorable factors for sector 12-14

Digitization to drive mid-term growth 15-16

OTT platforms in India and its Impact 17-18

Zee Entertainment Enterprises Ltd 19-24

Sun TV Network Ltd 25-30

Shemaroo Entertainment Ltd 31-35

TV Today Network Ltd 36-40

Disclaimer 41

2 | P a g e

Premia Research

Weaving a digital story

Zee Entertainment Enterprises– BUY

CMP Target Upside

539 691 28%

Sun TV Network – BUY

CMP Target Upside

782 984 26%

Shemaroo Entertainment – BUY

CMP Target Upside

481 580 21%

TV Today Network – BUY

CMP Target Upside

412 517 25%

Prices as on 02/07/2018

Financials (`cr) ZEE Enter. FY19E FY20E

Rev. 7,868 9,190

EBITDA Mar (%) 31.4 32.1

PAT 1,738 2,076

P/E x 29.8 24.9

Sun TV FY19E FY20E

Rev. 3,515 4,062

EBITDA Mar (%) 68.1 67.4

PAT 1,401 1,649

P/E x 22.0 18.7

Shemaroo FY19E FY20E

Rev. 566 635

EBITDA Mar (%) 29.9 30.4

PAT 99 113

P/E x 13.2 11.6

TV Today Net. FY19E FY20E

Rev. 786 871

EBITDA Mar (%) 29.1 30.1

PAT 154 183

P/E x 16.0 13.4 Source: IIFL Research

The ‘Digital’ wave in India (as a medium of entertainment) on the back

of higher internet penetration will drive the next leg of growth for the

Media and Entertainment (M&E) industry. The launch of Jio has made

mobile data accessible and affordable for masses (avg. mobile data

price has dipped from ~`200/GB two years back to `3.2/GB currently).

Further, rising internet subscribers (from ~45cr in December, 2017 to

~83cr in FY21E) coupled with declining internet costs is leading the

consumption pattern towards digital. Moreover, with advent of Over

the Top (OTT) platforms, content has become an ‘Anytime, Anywhere’

service, benefiting broadcasters and content aggregators/producers.

Robust internet consumption to propel digital growth

Given the favorable infrastructure, the total Indian mobile data

traffic/month is expected to increase to 14 Exabyte (EB) by CY23E

(2.4EB in December, 2017). Moreover, rising affordability of devices

and falling data cost would result in ~3x growth of the digital platform

subscribers over CY17-20E. Hence, digital subscription revenue would

register CAGR of 72.7% over CY17-20E.

Advertisement spends to shift towards digital

The rising online video viewing audience in India is expected to

increase at CAGR of ~26% over CY17-20E to ~500mn, resulting in

higher time spent on internet. The trend of rising online video

consumption would lead to higher advertisement spends in the digital

space. Hence, digital advertising revenue would grow at CAGR of 21%

over CY17-20E and is projected to contribute ~22% of total advertising

revenues of M&E sector in CY20E (~17% in CY17).

We prefer (1) Zee Entertainment Enterprises, owing to launch of ZEE5

(OTT platform) with strong content inventory (1,00,000+ hours) and

portfolio of channels; (2) Sun TV Network, a similar player in south

region with digital platform SunNXT (4,000+ movies) and stable

financial position aiding its expansion plan; (3) TV Today Network,

given leadership of its flagship brand AajTak and acquisition of digital

business from parent; and (4) Shemaroo Entertainment, considering

its huge content inventory (3,400+ titles) driving robust growth of its

digital segment.

Analyst – Tushar Jain [email protected]

July 03, 2018

3 | P a g e

Premia Research

Key Global markets trends

Global internet users reached 3.6bn in CY17 Favorable infrastructure combined with rising affordability of devices

is driving overall internet consumption globally. Further, overall cost of

internet is also declining and global internet penetration has reached

~49% in CY17 from ~24% in CY09.

Exhibit 1: Rising global internet users

Source: Internet Trends 2018, IIFL Research

Rising digital media usage in developed countries

The hours spent (daily basis) on digital media grew at CAGR of ~9% to ~6hours over CY08-17 in US. This growth is led by time spent on mobile, which grew at CAGR of ~31% over the same period. The advertisement spends have followed the consumption pattern and mobile internet advertising revenue stood at $49.9bn in CY17 in US compared to negligible in CY08.

Exhibit 2: Daily time spent on digital media in US (hours)

Considered adult users only Source: Internet Trends 2018, eMarketer, IIFL Research

0

2

4

6

8

10

12

14

16

0

100

200

300

400

CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17

Global Internet Users (cr) LHS yoy growth (%) RHS

0

1

2

3

4

5

6

7

CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17

Other Connected devices Desktop/Laptop Mobile

4 | P a g e

Premia Research

Key Global markets trends

Exhibit 3: Internet advertising growth in US (US$ bn)

Source: IAB internet advertising revenue report 2017, IIFL Research

Investment in content leading to subscriber addition

Leading Global digital M&E company, Netflix’s content cost has

increased at CAGR of 23.9% over CY12-17 and subscribers have grown

from 33mn to 117mn over the same period. However, same has helped

the company in attaining a revenue CAGR of 26.5% over CY12-17.

Hence, adaptability and ability of a company to produce relevant

content and predict customer behavior is of vital importance for the

digital industry.

Exhibit 4: Netflix subscribers (mn)

Source: Netflix, Valuewalk.com, IIFL research

Geographical expansion

In CY10, Netflix launched its services in Canada, while in CY12, it became available in Europe (including UK, Ireland and Nordic countries). Further, in CY15, it was launched in Australia and New Zealand and since CY16 onwards, Netflix is available worldwide.

0

10

20

30

40

50

60

70

80

90

100

CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17

Non Mobile Mobile

0

20

40

60

80

100

120

140

CY12 CY13 CY14 CY15 CY16 CY17

US users Rest of the world

Continuous focus on relevant content

has led to rapid geographical

expansion

Facebook’s annualized revenue per

daily user reached to US$34 in Q1CY18

from US$ 16 in Q1CY15

5 | P a g e

Premia Research

Key Global markets trends

Exhibit 5: Netflix’s financial highlights (US$ mn)

Source: Netflix, Bloomberg, IIFL Research

Staying relevant is the key

This FAANG (Facebook, Apple, Amazon, Netflix, Google) stock with

Market Cap of ~US$170bn has managed to grow by staying relevant to

the market and transforming its products according to consumer

preferences. M&E sector, one of the highest dynamic sectors,

demands huge degree of prediction of consumer behavior and their

responses to technological changes.

Netflix Timeline

Year Event/Initiative

1997 Reed Hastings and Marc Randolph co-found Netflix to offer online movie rentals

1998 Launches the first DVD rental and sales site, netflix.com

1999 Debuts a subscription service, offering unlimited DVD rentals for one low monthly price

2000 Introduces a personalized movie recommendation system, which uses Netflix members’ ratings to accurately predict choices for all Netflix members

2002 Makes its IPO on Nasdaq under the ticker “NFLX” with 600,000 members in the US

2007 Introduces streaming, which allows members to instantly watch television shows and movies on their PCs

2008 Partners with consumer electronics companies to stream on the Xbox 360, Blu-ray disc players and TV set-top boxes

2009 Partners with consumer electronics companies to stream on PS3, internet connected TVs and other internet connected devices

2010 Netflix is available on the Apple devices, the Nintendo Wii, and other internet connected devices

2013 Launches its first original content “House of Cards”

2016 Netflix is available worldwide

Source: Netflix, IIFL Research

0

2,000

4,000

6,000

8,000

10,000

12,000

CY12 CY13 CY14 CY15 CY16 CY17

Total revenue Content cost Operating income

From a DVD rental company to FAANG

stock, Netflix has managed to become

world’s biggest entertainment

company by staying relevant

6 | P a g e

Premia Research

Key Global markets trends

Better quality of content leads to higher paid subscribers

Globally, subscribers are moving towards paid content. This can be

witnessed by the rise in the revenues of key players like Netflix, Spotify,

etc. Further, Global Music/Audio giant Spotify’s paid subscribers stood

at ~45% of monthly active users (MAU) in CY17 vs. ~26% in CY14.

Exhibit 6: Spotify subscribers (mn)

Source: Spotify, Internet Trends 2018, IIFL Research

Ad-spends to shift towards digital

In CY17, proportion of daily time spent on digital media by an individual

in US stood at ~49% of total time spent on media. While proportion of

advertising spends on digital media in US stood at ~41% of total media

advertising spends. Going forward, the advertisement spends would

move towards digital from traditional media given the popularity and

rising customer base of digital media.

Exhibit 7: Time spent on media vs. advertising spending (US)

Source: IAB internet advertising revenue report 2017, emarketer, Statista, IIFL Research

-

20

40

60

0

25

50

75

CY14 CY15 CY16 CY17

Subscribers(LHS) % of MAU (RHS)

-

10

20

30

40

50

60

70

Traditional media Mobile Other digital platforms

% of time spent % of advertisement spent

This conversion to paid subscribers is

dependent on user experiences

7 | P a g e

Premia Research

Key Global markets trends

China’s online video subscribers to increase 1.6x in 3 years

China’s subscription Video-on-demand (SVOD) viewers are expected to

reach ~234mn by CY20E (~144mn in CY17) aided by favorable internet

infrastructure. China’s online video subscribers are closing the gap

with the no. of Cable TV subscribers.

Exhibit 8: China’s SVOD viewers

Source: emarketer, IIFL Research

0

20

40

60

80

100

0

50

100

150

200

250

CY14 CY16 CY18E CY20E

SVOD viewes (mn, LHS) % of digital video viewers (RHS)

% of cable TV subscribers (RHS) % of broadband subscription (RHS)

8 | P a g e

Premia Research

India’s growth on global trends

Multifold increase in the average data usage

The last four years have seen boost in the data consumption owing to

decline in the data cost, better network availability and rising

smartphone penetration. According to Nokia MbIT report, 2018, in

CY17, India’s average 4G data consumption stood at record level of

~11GB/user/month.

Exhibit 9: Average data usage/user/month (MB)

Source: Nokia MbIT report, 2018, Analysys Mason, IIFL research

Subscriber base is expected to reach ~83cr by FY21E

India’s internet subscribers are expected to grow from ~446mn in

December, 2017 to ~829mn in FY21 owing to increasing affordability

of smartphone devices and falling data cost. As per the EY-FICCI report,

India is the second largest smart phone market in the world after

China.

Exhibit 10: Internet subscribers in India (mn)

Source: IBEF, TRAI, IIFL research

216 220 259 320680 753 849

2,970

11,04810,604

CY14 CY15 CY16 CY17

2G 3G 4G

0

100

200

300

400

500

600

700

800

900

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY21

As per Ericsson’s prediction, data

traffic is expected to reach

18GB/month/smartphone in CY23

As per Nokia MbiT report, installed

base of 3G and 4G capable devices

grew by 1.4x and 4.6x respectively

from CY15 to CY17

9 | P a g e

Premia Research

India’s growth on global trends

India’s exponential data consumption growth

4G continues to drive India’s overall data consumption. In December, 2017, 4G traffic consisted of ~82% of the total data traffic. Falling data prices, affordability of devices, development of indigenous video content and network expansion are the factors behind the spike in the data consumption. Further, with the advent of 5G, which India is aspiring to launch at par with developed countries, this data consumption trend is expected to continue on the same track.

Exhibit 11: India’s mobile data usage – per month

Source: Nokia MbIT report, 2018, Analysys Mason, Ericsson mobility report, IIFL research,

from CY13 to CY17, monthly data of December is taken; EB- Exabyte, PB- Petabyte

Indian online video audience to double by CY20E

Online video viewing audience in India is expected to grow at CAGR of

~26% over CY17-20E. The growth will be faster than the developed

countries like China and US, which are expected to grow at CAGR of

~6% and ~2% respectively over the same period.

Exhibit 12: Online video audience (mn)

Source: EY-FICCI March-18 report, IIFL Research

49PB 85PB 128PB1EB

2.4EB

14EB

CY13 CY14 CY15 CY16 CY17 CY23E

0

100

200

300

400

500

600

700

Brazil US India China

CY17 CY20E

In December, 2017, India consumed

~2,360 petabytes data, which is 48x of

December, 2013 consumption

10 | P a g e

Premia Research

India’s growth on global trends

The impact on the media sector is clearly visible, as telecom giant

Reliance is investing heavily in content and OTT companies.

In July, 2017 it had invested `413cr in the content producer Balaji Telefilms, which gave it the access to content generated by Balaji Telefilms to be used by its platform Jio Cinema.

Further, in February, 2018, it has also announced Joint Partnership with Eros India to set up a `1,000cr fund to co-produce and consolidate content.

In March, 2018, It also executed definitive agreement for the combination of Saavn, a leading global music OTT platform with JioMusic.

Indian broadcasters have also launched their own OTT platforms like

Star launched Hotstar, TV18 launched VOOT and ZEE launched ZEE5.

Further, distributor TATA Sky has launched its mobile app for

competing against Mobile TV platforms launched by Telecom players

like Airtel TV, Jio TV, etc.

11 | P a g e

Premia Research

India’s growth on global trends

Indian channels leading on YouTube

Indian YouTube channels are clearly leading in terms of cumulative

views compared to international channels in the same category. As on

June 29, 2018, SET India and Zee TV channels have crossed 19.7bn and

17.1bn total views on YouTube respectively, which is higher than

some of the leading international channels like ABS-CBN, ChuChu TV,

etc.

Exhibit 13: YouTube stats (TV channels)

Channels Subscribers (mn) Views* (bn) Base Country

SET India 26.2 19.7 India

Zee TV 15.2 17.1 India

ABS-CBN Entertainment

10.6 15.3 Philippines

ChuChu TV (Kids Songs)

18.1 14.4 Global

SAB TV 9.4 8.6 India

Ch3Thailand 9.8 8.4 Thailand

Colors TV 10.8 7.3 India

one31 9.1 6.5 Thailand

GMA Network 5.2 6.3 Philippines

Disney Junior UK 4.3 5.1 United Kingdom

Source: socialbakers.com, YouTube, IIFL Research

*Total uploaded video views

Further, in film industry channels category also, the Indian channels

like YRF, Rajshri and Shemaroo are amongst the top viewed YouTube

channels with total views of 6.7bn, 4.1bn and 3.9bn respectively.

Exhibit 14: YouTube stats (Film Industry)

Channels Subscribers (mn) Views* (bn) Base Country

DisneyChannelLA 8.9 7.1 Global

YRF 11.9 6.8 India

Teremok TV 4.0 5.1 Russia

Rajshri 7.5 4.2 India

Shemaroo 9.0 4.0 India

Warner Bros. Pictures

5.5 3.3 Global

DreamWorks TV 4.4 3.0 Global

Walt Disney Animation Studios

3.0 2.1 Global

Telugu Filmnagar 4.0 2.0 India

Sony Pictures Entertainment

2.4 2.0 US

Source: socialbakers.com, YouTube, IIFL Research

*Total uploaded video views

12 | P a g e

Premia Research

Favorable factors for sector

Gaming and Digital will be the fastest growing segments: Digital media and Online Gaming are the driving factors for the growth of the Indian M&E sector going ahead. The M&E sector is expected to reach `2 lakh cr by CY20E from `1.5 lakh cr in CY17, a CAGR of 11.3%. The Digital Media segment is expected to register CAGR of 23.5% over the same period, and would overtake Filmed Entertainment by CY20E.

Exhibit 15: Segment wise growth of Indian M&E sector

Segment (`Cr) CY16 CY17 CY18E CY20E CAGR (%)

(CY17-20E)

Television 59,400 66,000 73,400 86,200 9.3

Print 29,600 30,300 33,100 36,900 6.8

Filmed Ent. 12,200 15,600 16,600 19,200 7.2

Digital media 9,200 11,900 15,100 22,400 23.5

Animation and VFX 5,400 6,700 8,000 11,400 19.2

Live events 5,600 6,500 7,700 10,900 18.8

Online gaming 2,600 3,000 4,000 6,800 31.6

Out Of Home media 3,200 3,400 3,700 4,300 8.1

Radio 2,400 2,600 2,800 3,400 9.4

Music 1,200 1,300 1,400 1,800 11.5

Total 1,30,800 1,47,300 1,66,000 2,03,200 11.3 All Figures are gross of taxes Source: EY-FICCI March-18 report, IIFL Research

Digital subscription revenues to outperform advertising revenues Indian OTT players are projected to reflect the growth pattern of Netflix and Spotify in increasing the number of subscribers. Rapid growth of device base and better connectivity will drive faster digital subscription revenue vs. advertising revenue. Subscription revenues stood at ~3% of total digital revenues in CY17, which is expected to grow to ~10% in CY20E.

Exhibit 16: Digital subscription and advertising revenues (`Cr)

Source: EY-FICCI March-18 report, IIFL research

-

500

1,000

1,500

2,000

2,500

5,000

10,000

15,000

20,000

25,000

30,000

CY16 CY17 CY18E CY20E

Advertising (LHS) Subscription (RHS)

Digital media is expected to overtake

Filmed entertainment by CY20E

The digital subscription and

advertising revenues are expected to

grow at a CAGR of 72.7% and 21% over

CY17-20E respectively

13 | P a g e

Premia Research

Favorable factors for sector

Rising income level to drive demand

The rising proportion of high income group in overall population will drive future growth for internet consumption and smartphones. The proportion of aspirers in overall households will increase from 15% in CY17 to 20% by CY25E.

Exhibit 17: Indian households’ income groups (%)

Source: IBEF, IIFL research

Further, as per EY-FICCI report, the shift in the consumption pattern will be more on the basis of ability to pay rather than on geographic, gender and age criteria. Hence, by CY20E, tactical digital consumers (using Pay TV and Pay OTT) are expected to grow 3.3x from CY17, faster than mass consumers (TV+ Free OTT), which are expected to grow 2.5x over the same period.

Exhibit 18: Customer segment in India

Segment CY17 CY20E

Digital only (No TV) 1-1.5mn subscribers 4mn subscribers

Tactical digital consumers (Pay TV + Pay OTT)

6mn subscribers 20mn subscribers

Mass consumers (Pay TV or Free TV + Free OTT)

200+ mn subscribers 500+ mn subscribers

Source: EY-FICCI March-18 report, IIFL Research

0

20

40

60

80

100

CY05 CY16 CY17 CY25E

Elite (>US$30,800) Affluent (US$15,400-30,800)

Aspirers (US$7,700-15,400) Next billion (US$2,300-7,700)

Strugglers (US$2,300)

Large working population with lower

expenses on M&E activities presents a

potential opportunity for the M&E

industry in India

By CY20E, tactical digital consumers are

expected to grow ~3.3x from CY17,

while mass consumers are expected to

grow 2.5x

14 | P a g e

Premia Research

Favorable factors for sector

M&E sectors’ growth is parallel to the economy

In past, the growth patterns of advertising revenue of M&E sector have always been faster but in the same direction of the real GDP growth of the country. Further, World Bank is forecasting India’s growth rate at 7.5% both in CY19E and CY20E (aided by reforms like implementation of GST, Insolvency and Bankruptcy Code, etc.). Going forward, we expect the advertising revenue to grow parallel to economy at CAGR of 11.4% over CY17-20E.

Exhibit 19: Advertisement revenue growth vs. Real GDP (%)

Source: EY-FICCI March-18 report, IIFL Research

2

4

6

8

10

12

14

16

CY12 CY13 CY14 CY15 CY16 CY17

Advertising revenue growth in M&E Industry (%) Real GDP growth (%)

15 | P a g e

Premia Research

Digitization to drive mid-term growth

The cable TV Digitization amendment bill was passed in 2011, which has transformed the Indian TV distribution industry. Digitization bill mandated all analog cable distributors to digital addressable system. It was implemented in four phases. Digitization is providing significant advantages to entire TV Value Chain in terms of transparency and reduction in the revenue leakages, which would result in an ARPU increase across value chain and higher taxes for the government.

As a result of forced digitization, the digital cable subscribers are expected to reach 82mn by CY20E.

Exhibit 20: Indian TV subscriber split by distribution platform (mn)

Source: FICCI-KPMG 2017 report, IIFL research

Higher revenue collection from end use customers has resulted in higher share for Multi System Operators (MSOs) and broadcasters.

Prior to digitization, Local Cable Operators (LCOs) used to under report the actual number of subscribers and availed ~70% of the customer ARPU (Average Revenue Per User). Post digitization, due to higher transparency, it has come down to ~50%. This has resulted in increase in the Broadcasters’ share from ~15% to ~25% of the total customer ARPUs.

Exhibit 21: Customer ARPU share for various players in India

Stakeholders Before Digitisation (%) After Digitisation (%)

Consumer ARPU 100 100

LCOs 65-80 45-55

MSOs 10-20 15-25

Broadcasters 10-20 20-30

Source: EY-FICCI March-18 report, IIFL Research

69 7047

1 1

19 2945

76 82

3440 54 78 84910

2231

31

0

50

100

150

200

250

CY12 CY14 CY16 CY18E CY20E

Analog Cable Digital Cable Pay DTH Free Dish

Currently, ~83% of the total TV

households are paying subscribers

16 | P a g e

Premia Research

Digitization to drive mid-term growth

Increase in the ARPU shares for broadcasters will help them gain subscription revenue CAGR of 8.1% over CY17-20E. TV penetration in India has reached 64% taking the total number of TV viewing households to 183mn in CY17. This accounts for ~780mn viewers. TV viewing households are expected to reach to 198mn in CY20E.

Exhibit 22: Indian Broadcaster’s revenue mix (`Cr)

Source: EY-FICCI March-18 report, IIFL research

Digitization phases

Phases Implementation

Phase I Covered four metros (Mumbai, Delhi, Kolkata and Chennai) to be digitised

Phase II Focused on the 38 top cities with population more than 1mn

Phase III Rest of the urban area

Phase IV Rest of India

Digitization has resulted in significant capital requirements for cable

and DTH platforms, as set top boxes were made mandatory for all the

households. This can be witnessed by recent consolidations and

investments.

In July, 2017, GTPL Hathway got listed and raised ~`485cr, out of which `240cr was fresh issue. Dish TV and Videocon D2H also amalgamated their businesses to gain synergy benefits.

In November, 2017, Reliance Communication Ltd sold its DTH business, Reliance Big TV Ltd to Pantel Technologies, an Information Technology and Communication devices hardware company.

9,000 9,900 10,900 11,700 12,500

24,300 26,700

30,400 33,500

36,800

-

10,000

20,000

30,000

40,000

50,000

60,000

CY16 CY17 CY18E CY19E CY20E

Subscription Advertising

Increased transparency due to

digitization will lead to reduction in

revenue leakages for broadcasters

17 | P a g e

Premia Research

OTT platforms in India and its impact

Indian platforms are still cheaper than Netflix

With the advent of Netflix all the broadcasters have launched own OTT platforms. Netflix has gained huge popularity in developed countries owing to its huge content inventory. However, Indian OTT platforms are way cheaper than Netflix. Leading Indian platforms like Hotstar, Zee5, SunNXT and Sonyliv have monthly subscription fees ranging from ~`40 to ~`83. While Netflix’s subscription fee is ~`800/month.

Exhibit 23: Various OTT platforms in India

OTT Platform Revenue model Monthly price (`) Global entrants

Netlfix SVOD ~800

Amazon prime SVOD ~83

Broadcasters

Hotstar Freemium ~83

VOOT AVOD -

Sony liv Freemium ~42

Zee5 Freemium ~83

SunNXT SVOD ~40

New entrants

TVF AVOD -

Producers

ALT Freemium ~25

EROS Freemium ~79

Audio

Saavn Freemium ~83

Gaana Freemium ~33

Telcos

Jio Cinema Free -

Source: IIFL Research; AVOD- Advertising Video-on-demand, SVOD- Subscription Video-on-demand

In freemium model, companies offer

free subscription for some episodes,

while some content is provided on paid

basis.

18 | P a g e

Premia Research

OTT platforms in India and its impact

Segment wise impact of OTT platforms

Players Impact Reasons

Broadcasters Neutral Launched own OTT platforms. All channels are available on Telecom platforms like Jio TV, Airtel TV, etc.

Content Producers/Aggregators

Positive Competition intensity of OTT players and Telecom operators will drive overall content demand.

Exhibitors Moderate

Film producers may sell rights of small budget movies directly to OTT platforms. Big budget movies with special effects are bound to go for theatrical releases in order to realize higher costs.

DTH/Cable operators Negative

Declining internet costs will take away the lower cost advantage of distributors in medium term. However, for small cities and rural markets, the threat is limited in medium term due to lower internet penetration.

Radio/Print Media Neutral

No impact expected on Print Media/Radio from OTT players, as both these serve different purposes to the consumers.

19 | P a g e

Premia Research

Zee Entertainment Enterprises Ltd CMP: ` 539; 1-year target: ` 691

Sector M&E

Recommendation BUY

Upside 28%

Stock Data

Sensex 35,264

52 Week h/l (`) 619/477

Market cap (` Cr) 51,768

BSE Code 505537

NSE Code ZEEL

FV (`) 1

Div yield (%) 0.51

Shareholding Pattern

Sep-17 Dec-17 Mar-18

Promoters 43.07 43.07 41.62

DII+FII 50.52 50.65 52.18

Individuals 6.41 6.27 6.20

Source: ACE Equity, IIFL Research

Share Price Trend

Prices as on 02/07/2018

Zee Entertainment Enterprises Ltd (ZEEL), one of the largest

broadcasting houses in India is set to benefit from its newly launched

digital platform ZEE5 and its collaboration with telcos. Further, it is

also considering to enter into new Malayalam market in FY19E.

Hence, we forecast revenue and PAT CAGR of 17.2% and 24.3%

respectively over FY18-20E. Further, ZEEL is debt free at net debt level

We recommend BUY with a target price of `691 (32x FY20E EPS).

Digital offerings to drive growth: In February, 2018, ZEEL had

launched its OTT platform ZEE5 with 100,000+ hours of video content,

which has received favorable initial response. ZEE5 has already crossed

10mn+ installs on PlayStore, which is further expected to reach 60mn+

by FY20E. Further, ZEEL has guided to host 90+ original shows on its

platform by March 2019 from ~20 in April, 2018. Hence, we expect

ZEEL to generate ~`150cr from ZEE5 platform in FY20E.

Increasing viewership to lead to higher ad revenue: ZEEL’s network

market share improved from 16% in FY17 to 18% in FY18. This

combined with improved films content will drive viewership gains.

Further, we expect consumption boost owing to positive macros like

higher disposable and per capita income, which will drive higher ad

spends. Thus, we expect 19.8% ad revenue CAGR over FY18-20E.

Outlook & Valuation: Management has guided faster than industry

growth of 10% in FY19E. We have a very positive outlook on ZEEL owing

to its plan to expand in new genres, growth of subscription revenues

supported by digitization and movies in pipeline. The company is

currently trading at a valuation of 24.9x FY20E EPS (~47% discount

from its 5 years’ average valuation).

Financial Summary

Consolidated `Cr FY16 FY17 FY18 FY19E FY20E

Revenue 5,813 6,434 6,686 7,868 9,190

YoY Growth (%) 19.0 10.7 3.9 17.7 16.8

EBITDA Margin (%) 26.0 29.9 31.1 31.4 32.1

PAT 857 997 1,343 1,738 2,076

PAT Growth (%) -12.3 16.4 34.7 29.4 19.4

RoE 16.6 17.4 18.8 21.1 21.2

P/E x 60.4 51.9 38.5 29.8 24.9

EV/EBITDA x 33.1 25.2 24.4 20.3 16.7

Source: Company, IIFL Research

30000

35000

450

550

650

Jun-17 Oct-17 Feb-18 Jun-18

Zee Entertainment Enterprises Ltd.Sensex

20 | P a g e

Premia Research

Zee Entertainment Enterprises Ltd

Company Overview

ZEEL is present across broadcasting, movies, music, live entertainment and digital businesses, both within India and overseas. It has more than 240,000 hours of television content, offered through 32 domestic and 39 international channels.

ZEEL houses the world’s largest Hindi film library and has rights to more than 4,200 movie titles across various languages. ZEEL has also produced several movies for theatrical release and is the fastest growing music label in India. It has recently launched digital platform, ZEE5, with 100,000 hours of multilingual content.

Exhibit 1: ZEEL (Revenue segments, FY18)

Exhibit 2: Leading in FTA* GEC**

Weekly/mn impressions; Source: BARC, IIFL Research; *FTA – free to air; GEC General entertainment channel

ZEEL has been maintaining its leadership position in Hindi FTA GEC space. Its Kumkum Bhagya and Kundali Bhagya are two of the most popular shows in India.

0

200

400

600

800

1,000

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

Dec

-17

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

Sony Pal Zee Anmol Star Utsav Rishtey

21 | P a g e

Premia Research

Zee Entertainment Enterprises Ltd

Exhibit 3: Clear winner in Marathi

Weekly/mn impressions, Source: BARC, IIFL Research

Exhibit 4: Stiff competition in Telugu space

Weekly/mn impressions, Source: BARC, IIFL Research

Exhibit 5: Hindi GEC pay channel: Competing with Colors

Weekly/mn impressions, Source: BARC, IIFL Research

0

50

100

150

200

250

300

350

May

-17

Jun

-17

Jul-

17

Jul-

17

Au

g-1

7

Sep

-17

Sep

-17

Oct

-17

No

v-1

7

No

v-1

7

Dec

-17

Jan

-18

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

Ap

r-1

8

May

-18

Zee Marathi Colors Marathi Zee Talkies Star Pravah

200

250

300

350

400

450

500

550

600

650

May

-17

Jun

-17

Jul-

17

Jul-

17

Au

g-1

7

Sep

-17

Sep

-17

Oct

-17

No

v-1

7

No

v-1

7

Dec

-17

Jan

-18

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

Ap

r-1

8

May

-18

ETV Telugu Maa TV Zee Telugu Gemini TV

100

200

300

400

500

600

700

800

May

-17

Jun

-17

Jul-

17

Jul-

17

Au

g-1

7

Sep

-17

Sep

-17

Oct

-17

No

v-1

7

No

v-1

7

Dec

-17

Jan

-18

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

Ap

r-1

8

May

-18

Star Plus Colors Zee TV Sony

In Marathi space, Zee Marathi got ~270mn weekly average impressions in last one year vs. ~93mn and ~90mn of Colors Marathi and Star Pravah

In Hindi Primary GEC space, Zee TV got ~594mn weekly average impressions in last one year vs. ~546mn of Colors

22 | P a g e

Premia Research

Zee Entertainment Enterprises Ltd

Exhibit 6: Growth of subscription revenues

Source: Company, IIFL Research

We expect ZEEL’s subscription revenue CAGR of ~12.4% over FY18-20E driven by digitization and increase in ARPU. Consolidation of distribution platform operators (DPOs) will give them greater pricing power, which ultimately bodes well for the company. Further, its partnership with telcos will also drive subscription revenues.

Margin expansion to improve return ratios: The company’s EBITDA margin is estimated to expand from 31.1% in FY18 to 32.1% in FY20E owing to expected viewership gains, higher advertisement revenues, sell of loss making sports business and partnership with telcos. The higher margin will drive growth of return ratios going forward. We expect ROE and ROCE to expand by ~230bps and ~340bps to 21.2% and 24.8% by FY20E.

Exhibit 7: EBITDA margins and return ratios

Source: Company, IIFL Research

-15

-10

-5

-

5

10

15

20

-

500

1,000

1,500

2,000

2,500

3,000

FY16 FY17 FY18 FY19E FY20E

Subscription revenue (Rs cr) LHS Growth (%) RHS

20

22

24

26

28

30

32

34

15

17

19

21

23

25

27

29

31

FY16 FY17 FY18 FY19E FY20E

EBITDA margins (%) RHS ROE (%) LHS ROCE (%) LHS

ROCE and ROE would increase on account of improving margin profile and low debt

Digitization has increased transparency, which is leading to lesser leakages of revenues for Broadcasters

23 | P a g e

Premia Research

Zee Entertainment Enterprises Ltd

Exhibit 8: Balance sheet summary and key ratios

Consolidated ~ ` Cr FY16 FY17 FY18 FY19E FY20E

Cash & Cash equivalent 1,722 3,800 2,981 2,844 3,438

Inventories 1,318 1,696 2,628 3,092 3,637

Receivable 1,348 1,242 1,537 1,787 2,062

Other Current Assets 1,035 1,389 1,444 1,651 1,691

Creditors 477 834 1,150 1,353 1,580

Other Current Liabilities 382 272 621 273 307

Net Current Assets 4,565 7,021 6,820 7,748 8,940

Fixed Assets 1,443 956 1,413 1,262 1,312

Investments 389 271 315 326 326

Other Long-term assets 711 902 812 885 964

Total net assets 7,107 9,151 9,359 10,221 11,542

Borrowings 2,271 2,460 1,783 1,257 857

Other long-term liabilities 30 - - - -

Shareholders' equity 4,806 6,691 7,576 8,964 10,685

Total liabilities 7,107 9,151 9,359 10,221 11,542

Key Ratios Valuation ratios EV/sales 8.6 7.5 7.6 6.4 5.4

EV/EBITDA 33.1 25.2 24.4 20.3 16.7

P/E 60.4 51.9 38.5 29.8 24.9

P/B 10.8 7.7 6.8 5.8 4.9

Working capital days

Inventory days 83 96 143 143 144

Debtor days 85 70 84 83 82

Creditors days 30 47 63 63 63 Source: Company, IIFL Research

24 | P a g e

Premia Research

Zee Entertainment Enterprises Ltd

Rationale for PE multiple: We have assigned target multiple of 32x

FY20E EPS, which is at ~16% discount to its 5 years’ average valuation

considering its expected increase in the content cost. However,

considering its high return ratios, debt free position at net debt level

and launch of its OTT platform, ZEE5, it deserves such valuation. The

stock is currently trading at a valuation of 24.9x FY20E EPS.

Exhibit 9: 1-Year forward PE band

Source: ACE Equity, IIFL Research

Key Risks

Rising content cost may affect its margins.

Pricing pressure due to competition intensity may affect advertisement revenues.

15

20

25

30

35

40

45

50

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

Mar

-18

Jun

-18

25 | P a g e

Premia Research

Sun TV Network Ltd

CMP: ` 782; 1-year target: ` 984

Sector M&E

Recommendation BUY

Upside 26%

Stock Data

Sensex 35,264

52 Week h/l (`) 1097/652

Market cap (` Cr) 30,799

BSE code 532733

NSE code SUNTV

FV (`) 5

Div yield (%) 1.08

Shareholding Pattern

Sep-17 Dec-17 Mar-18

Promoters 75.00 75.00 75.00

DII+FII 16.82 16.99 16.86

Individuals 8.18 8.01 8.14

Source: ACE Equity, IIFL Research

Share Price Trend

Prices as on 02/07/2018

Sun TV Network Ltd (STV) is a part of one of the largest Indian media

conglomerates – the Sun Group. STV is set to benefit from TRAI’s

pricing order for ala carte offerings post which ARPUs are expected

to grow. To ride on the OTT wave, it has already launched its digital

platform SunNXT with 4,000+ movies, originals and live TV. It already

has 5mn+ installs on PlayStore, which we expect to cross 20mn by

FY20E. Hence, we project revenue CAGR of ~17% and PAT CAGR of

~21% over FY18-20E. STV is debt free with RoE and RoCE of ~26% and

~37% (FY18) respectively. We recommend BUY with target price of

`984 (23.5x FY20E EPS).

Digitization to drive subscription revenues: Currently, 4.5mn

households have been digitized in Tamil Nadu and ~9mn more

households are expected to be digitized by FY19E. STV has also

concluded an agreement with Tamil Nadu’s Arasu Cable TV

Corporation. ARPU for Arasu has increased from ~`70 to ~`90, out of

this ~`40 ARPU share is expected for STV, driving domestic

subscription revenue CAGR of ~19% over FY18-20E.

STV’s share in Tamil GEC and movie market to improve: STV

continues to hold more than 50% market share in Tamil GEC and movie

market and which is expected to improve further. We expect STV to

launch second Tamil GEC channel and enter a new regional market in

FY19E driving advertising revenue CAGR of ~12% over FY18-20E.

Outlook & Valuation: We have a very positive outlook on STV given

optimization in movie capex, IPL franchisee turning profitable, fading

political headwinds and strong ad revenue growth. The company is

currently trading at a valuation of 18.7x FY20E EPS. (~26% discount

from its 2 years’ average valuation).

Financial Summary

Consolidated `Cr FY16 FY17 FY18 FY19E FY20E

Revenue 2,474 2,646 2,963 3,515 4,062

YoY Growth (%) 3.3 7.0 12.0 18.6 15.6

EBITDA Margin (%) 70.0 66.9 67.6 68.1 67.4

PAT 904 1,030 1,135 1,401 1,649

PAT Growth(%) 15.6 14.0 10.2 23.4 17.7

RoE 26.1 27.5 26.0 27.2 26.6

P/E x 33.4 29.9 27.1 22.0 18.7

EV/EBITDA x 17.1 16.7 14.4 11.9 10.0 Source: Company, IIFL Research

30000

32000

34000

36000

38000

650

850

1050

Jun-17 Oct-17 Feb-18 Jun-18

Sun TV Network Ltd. Sensex

26 | P a g e

Premia Research

Sun TV Network Ltd

Company Overview

Sun TV Network is part of India’s largest media conglomerate – the Sun Group, run by Kalanithi Maran. The network has a power packed 33 TV channels in four south Indian languages. These channels are present in general entertainment, news, movies and kids’ entertainment genres with the reach of more than 95mn households in India.

Primarily, it caters to the south Indian markets. Moreover, its channels can be viewed in 27 foreign countries. Further, it has huge movie library with perpetual rights. In CY12, the company had acquired Hyderabad franchise of Indian Premier League (IPL). Its production studio, Sun Pictures has also produced movies like Enthiran and Siragugal starring Rajinikanth and Vikram respectively.

Exhibit 1: STV (Revenue segments, FY18)

Subscription revenues include international subscription as well

Caters to strongest TV market of the country: As per EY-FICCI

report, daily time spent by south Indian individuals on TV is higher by

~38mm than that of other Hindi speaking markets (HSM; Week 40-52,

2017). Further, daily and weekly tune-ins are also higher for south

Indian market.

Exhibit 2: Individual tune-ins on TV and daily time spent in India

Geographies Weekly Tune-

ins (%) Daily

Tune-ins (%) Daily Time spent on TV

(HH:MM:SS)

HSM 91.80 68.40 03:31:36

South 94.80 78.30 04:09:25

India 92.70 71.50 03:44:28 Source: EY-FICCI, All India/Individual/Week 40-52, 2017, IIFL Research

27 | P a g e

Premia Research

Sun TV Network Ltd

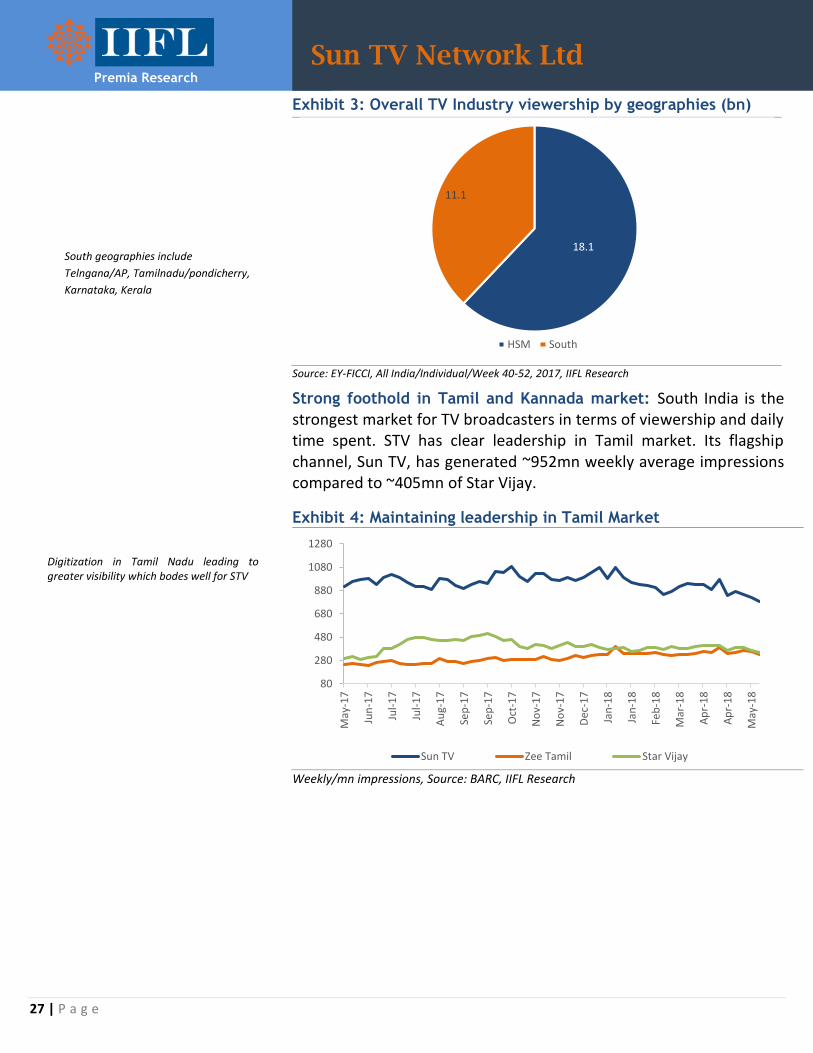

Exhibit 3: Overall TV Industry viewership by geographies (bn)

Source: EY-FICCI, All India/Individual/Week 40-52, 2017, IIFL Research

Strong foothold in Tamil and Kannada market: South India is the strongest market for TV broadcasters in terms of viewership and daily time spent. STV has clear leadership in Tamil market. Its flagship channel, Sun TV, has generated ~952mn weekly average impressions compared to ~405mn of Star Vijay.

Exhibit 4: Maintaining leadership in Tamil Market

Weekly/mn impressions, Source: BARC, IIFL Research

18.1

11.1

HSM South

80

280

480

680

880

1080

1280

May

-17

Jun

-17

Jul-

17

Jul-

17

Au

g-1

7

Sep

-17

Sep

-17

Oct

-17

No

v-1

7

No

v-1

7

Dec

-17

Jan

-18

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

Ap

r-1

8

May

-18

Sun TV Zee Tamil Star Vijay

Digitization in Tamil Nadu leading to greater visibility which bodes well for STV

South geographies include

Telngana/AP, Tamilnadu/pondicherry,

Karnataka, Kerala

28 | P a g e

Premia Research

Sun TV Network Ltd

STV’s another channel Udaya TV has been gaining viewership continuously over last one year (refer Exhibit 5). As per BARC data, its average weekly impressions for first four weeks of May, 2018 stood at ~214mn compared to ~147mn in June, 17.

Exhibit 5: Udaya gaining viewership in Kannada

Weekly/mn impressions, Source: BARC, IIFL Research

However, there is no clear winner in Telugu market. Its channel Gemini TV faces tough competition from Maa TV and Zee Telugu (refer Exhibit 6).

Exhibit 6: Stiff competition in Telugu market for Gemini

Weekly/mn impressions, Source: BARC, IIFL Research

Robust revenue growth ahead: Digitization, ARPU increase and IPL

franchisee’s increasing popularity will aid STV to clock ~12% and ~19%

advertising and domestic subscription revenue CAGR over FY18-20E

respectively. Further, consumption boost, entry into new regional

markets and higher internet penetration bodes well for the company.

050

100150200250300350400450500

May

-17

Jun

-17

Jul-

17

Jul-

17

Au

g-1

7

Sep

-17

Sep

-17

Oct

-17

No

v-1

7

No

v-1

7

Dec

-17

Jan

-18

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

Ap

r-1

8

May

-18

Colors Kannada Udaya TV Suvarna Zee Kannada

100

200

300

400

500

600

700

May

-17

Jun

-17

Jul-

17

Jul-

17

Au

g-1

7

Sep

-17

Sep

-17

Oct

-17

No

v-1

7

No

v-1

7

Dec

-17

Jan

-18

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

Ap

r-1

8

May

-18

ETV Telugu Maa TV Zee Telugu Gemini TV

29 | P a g e

Premia Research

Sun TV Network Ltd

Exhibit 7: Advertising and domestic subscription revenues

Source: Company, IIFL Research

IPL franchisee turning profitable: We expect the company’s IPL franchisee to turn profitable in FY19E, as IPL franchisee cost is decided at ~20% revenue share vs. `85.5cr fee earlier. STV’s Hyderabad franchisee won its maiden IPL title in 2016, while stood second in 2018.

Rationale for PE multiple: In our opinion, a company like STV

deserves premium valuation considering its high return ratios, debt

free position and strong foothold in South market. Further, political

headwinds are also fading, as the ruling party in Tamil Nadu is in its

second term and is no longer as powerful as it was during Jayalalitha’s

Era. The stock is currently trading at 18.7x FY20E EPS. We have valued

the stock at its last 2 years’ average valuation of 23.5x.

Exhibit 8: 1 Year Forward PE band

Source: Ace Equity, IIFL Research

-5

0

5

10

15

20

25

0

500

1000

1500

2000

2500

FY16 FY17 FY18E FY19E FY20E

Advertising revenues Subscription revenues

Advertising revenue growth yoy (%) Subscription revenue growth yoy (%)

0

5

10

15

20

25

30

35

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

Dec

-17

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

As per EY-FICCI report, overall industry

subscription and advertising revenues

are expected to grow at a CAGR of 8.3%

and 11.4% over CY17-20E

Strong balance sheet with debt free

position will help company to fund for

expansion plans in newer geographies

with internal accruals

30 | P a g e

Premia Research

Sun TV Network Ltd

Exhibit 9: Balance Sheet summary and key ratios

Consolidated ~ ` Cr FY16 FY17 FY18 FY19E FY20E

Cash & Cash equivalent 1,149 1,334 1,888 2,428 3,444

Inventories 1 1 0 1 2

Receivable 776 773 1,064 1,252 1,436

Other Current Assets 396 156 149 217 262

Creditors 56 72 84 96 111

Other Current Liabilities 192 208 409 278 321

Net Current Assets 2,075 1,982 2,608 3,525 4,713

Fixed Assets 846 1,213 1,189 1,138 1,108

Investments 392 615 636 680 680

Other Long-term assets 200 287 350 364 380

Total net assets 3,512 4,098 4,782 5,707 6,881

Borrowings - - - - -

Other long-term liabilities 35 65 90 92 94

Shareholders' equity 3,477 4,032 4,692 5,615 6,786

Total liabilities 3,512 4,098 4,782 5,707 6,881

Key Ratios Valuation ratios

EV/sales 12.0 11.1 9.8 8.1 6.7

EV/EBITDA 17.1 16.7 14.4 11.9 10.0

P/E 33.4 29.9 27.1 22.0 18.7

P/B 8.9 7.6 6.6 5.5 4.5

Working capital days Inventory days 0 0 0 0 0

Debtor days 115 107 131 130 129

Creditors days 8 10 10 10 10 Source: Company, IIFL Research

Key Risks

Competitive intensity in south Indian market may put pricing pressure on the company.

Rise in the content cost may affect its margins.

Political instability might put regulatory risk on the company in the Tamil market.

31 | P a g e

Premia Research

Shemaroo Entertainment Ltd

CMP: ` 481; 1-year target: ` 580

Sector M&E

Recommendation BUY

Upside 21%

Stock Data

Sensex 35,264

52 Week h/l (`) 595/325

Market cap (` Cr) 1,310

BSE code 538685

NSE code SHEMAROO

FV (`) 10

Div yield (%) 0.31

Shareholding Pattern

Sep-17 Dec-17 Mar-18

Promoters 65.82 65.82 65.82

DII+FII 18.24 18.12 16.59

Individuals 15.94 16.06 17.59

Source: ACE Equity, IIFL Research

Share Price Trend

Prices as on 02/07/2018

Shemaroo Entertainment Ltd (Shemaroo), one of the largest content

aggregators of India is set to benefit from rising internet usage

leading to robust growth of its digital business. We forecast revenue

CAGR of ~14% over FY18-20E. Further, Reduction in debt leading to

reduction in finance cost will drive PAT CAGR of 26% over FY18-20E.

Considering its strengthening balance sheet with ROE and ROCE of

17.5% and 23.7% (FY18) respectively, we recommend BUY with a

target price of `580 (14x FY20E EPS).

Robust growth of Digital segment: The average price for mobile data

has fallen from ~`200/GB two years back to `3.2/GB currently.

Currently, Shemaroo’s content gets ~700mn monthly views on

YouTube compared to ~300mn two years back. This bodes well for the

company’s digital segment. Hence, we expect digital revenue CAGR of

~23% over FY18-20E.

Investment phase is over: Company’s inventory grew by ~`72cr p.a.

over FY13-18 due to heavy investment in movie titles. However, going

forward we expect it to grow by only ~`40cr p.a. in both FY19E/20E, as

company now has sufficient inventory (+3,400 titles) to monetize from.

Hence, we expect the net debt to equity to come down from ~0.4x in

FY18 to ~0.2x in FY20E.

Outlook & Valuation: We are positive on Shemaroo owing to its

strong movie inventory, launch of new spiritual applications and higher

content expenditure guidance by the broadcasters (customers of

Shemaroo). Company is reasonably priced at 11.3x FY20E EPS (trading

at a discount to Balaji Telefilms, 33.8x FY20E EPS).

Financial Summary

Consolidated `Cr FY16 FY17 FY18 FY19E FY20E

Revenue 375 426 489 566 635

YoY Growth (%) 16.0 13.5 14.8 15.9 12.1

EBITDA Margin (%) 28.7 30.0 29.1 29.9 30.4

PAT 52 61 71 99 113

PAT Growth (%) 27.5 17.9 15.7 38.9 14.3

RoE 15.3 15.5 15.4 18.2 17.5

P/E x 25.1 21.3 18.4 13.2 11.6

EV/EBITDA x 14.1 12.6 10.6 8.7 7.4

Source: Company, IIFL Research

30000

32000

34000

36000

38000

330

430

530

Jun-17 Oct-17 Feb-18 Jun-18

Shemaroo Entertainment Ltd.

Sensex

32 | P a g e

Premia Research

Shemaroo Entertainment Ltd

Company Overview

Shemaroo is an established Filmed Entertainment “content house” with activities across content aggregation & ownership, value addition to content and content distribution with a library of over 3,400 titles. Shemaroo is engaged in the distribution of content for satellite channels, physical formats and emerging digital technologies like mobile, internet, broadband and DTH among others.

Shemaroo purchases titles of movies from TIPS, Sohail Khan Productions, Viacom 18, etc. Its customers include OTT players like Netflix, Broadcasters like Star Gold, Set Max, Zee Cinema, etc. It also sells it content to other media like overseas and in flight.

Company typically participates in the second and subsequent cycles of film monetization, which is after 5-7 years of release of the movies. These subsequent cycles contribute 5-10% of the producers’ revenue. There is a lower risk in these cycles due to visibility of performance of movies during first cycle of launch.

The company has agreements with major telecom operators namely Airtel, Vodafone, Idea, etc. It also distributes its contents to other media platforms like In-flight entertainment, Overseas, International Film festivals, etc., with presence in US, UK, Canada, UAE, Australia, Singapore, etc. Exhibit 1: Mobile internet consumption in India

Source: FICCI-KPMG 2017 report, IIFL Research

Video content is dominating mobile internet usage and going forward the same trend is expected to continue further. The contribution from videos in overall internet consumption is expected to grow to ~75% in CY21E from ~49% in CY16.

CY16

File sharing Video

CY21E

Streaming Audio Other

Installed base of 3G and 4G capable

device base grew by 1.4x and 4.6x

respectively from CY15 to CY17

India is second largest smart phone

market in the world after China

33 | P a g e

Premia Research

Shemaroo Entertainment Ltd

Exhibit 2: Shemaroo’s content views on YouTube (lakhs per day)

Source: Company, IIFL Research

Shemaroo is amongst the most viewed channel partners for YouTube in India. It has more than 40 channels of its own on YouTube. Till now, its two flagship channels Shemaroo and FilmiGaane have already crossed 4bn and 3bn cumulative views respectively.

Shemaroo’s digital segment to outperform traditional business

Rising internet penetration will drive faster digital revenue growth at a CAGR of 23% over FY18-20E compared to 10.5% of traditional over the same period. Digital revenue contribution is expected to reach to ~31% by FY20E in overall revenue from ~27% in FY18.

Exhibit 3: Traditional and Digital segment revenues

Source: Company, IIFL Research

0

10

20

30

40

50

60

70

80

-

100

200

300

400

500

FY16 FY17 FY18 FY19E FY20ETraditional Media (Cr) Digital Media (Cr)

Traditional Media growth (%) Digital Media growth (%)

Overall industry’s digital media is

expected to grow at a CAGR of 23.5%

over CY17-20E

Shemaroo’s content on YouTube gets over

7,000lakhs views a month or more than

200lakhs hits per day

34 | P a g e

Premia Research

Shemaroo Entertainment Ltd

Exhibit 4: Return ratios to improve with margin expansion

Source: Company, IIFL Research

We expect ROE and ROCE to expand by ~210bps and ~440bps to 17.5% and 23.7% respectively owing to margin expansion. Increase in the monetization opportunities going forward will help company to expand its PAT margin by ~320bps over the same period. Rationale for PE multiple and peer comparision: Current scenario of rising internet penetration with higher per capita disposable income bodes well for content players. We prefer Shemaroo over EROS and Balaji Telefilms considering its consistency in the profitability and higher return ratios. Hence, we assign it a target multiple of 14x FY20E EPS. Stock is currently trading at 11.3x FY20E EPS, which is at a huge discount from its peer Balaji Telefilms’ multiple of 33.8x FY20E EPS.

Exhibit 5: 1 Year forward PE

Source: ACE Equity, IIFL Research

0

5

10

15

20

25

5

10

15

20

25

30

35

FY16 FY17 FY18 FY19E FY20E

EBITDA margin (%) LHS PAT margin (%) LHS

ROE (%) RHS ROCE (%) RHS

4

6

8

10

12

14

16

18

Oct

-14

Dec

-14

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

Dec

-15

Feb

-16

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

Dec

-16

Feb

-17

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

Dec

-17

Feb

-18

Ap

r-1

8

Jun

-18

35 | P a g e

Premia Research

Shemaroo Entertainment Ltd

Exhibit 6: Peer comparison P/E EV/EBITDA ROE FY19E FY20E FY19E FY20E FY19E FY20E

Balaji Telefilms 38.2 33.8 16.3 13.4 3.1 3.3

Shemaroo Enter 13.2 11.6 8.7 7.4 18.2 17.5 Source: Bloomberg, IIFL Research

Exhibit 7: Balance Sheet summary and key ratios

Consolidated ~ ` Cr FY16 FY17 FY18E FY19E FY20E

Cash & Cash equivalent 2 2 1 2 3

Inventories 388 500 530 565 615

Receivable 107 191 141 157 174

Other Current Assets 68 36 16 34 38

Creditors 11 19 18 21 24

Other Current Liab. 18 34 17 19 22

Net Current Assets 535 677 653 717 784

Fixed Assets 31 35 33 33 33

Investments 8 7 10 11 11

Other Long-term assets 9 9 3 3 4

Total net assets 584 728 700 765 831

Borrowings 212 296 202 171 131

Other long-term liab. 7 8 5 5 6

Shareholders' equity 364 423 493 589 695

Total liabilities 584 728 700 765 831

Key Ratios

Valuation ratios

EV/sales 4.0 3.8 3.1 2.6 2.3

EV/EBITDA 14.1 12.6 10.6 8.7 7.4

P/E 25.1 21.3 18.4 13.2 11.6

P/B 3.6 3.1 2.6 2.2 1.9

Working capital days

Inventory days 377 429 396 366 354

Debtor days 104 164 105 101 100

Creditors days 10 16 14 14 14 Source: Company, IIFL Research

Key Risks:

Competition intensity may negatively affect realizations for its

content.

Content library management is always a challenge; any

irrelevant content acquisition can lead to cash burns.

36 | P a g e

Premia Research

TV Today Network Ltd

CMP: ` 412; 1-year target: ` 517

Sector M&E

Recommendation BUY

Upside 25%

Stock Data

Sensex 35,264

52 Week h/l (`) 558/211

Market cap (` Cr) 2,462

BSE code 532515

NSE code TVTODAY

FV (`) 5

Div yield (%) 0.43

Shareholding Pattern

Sep-17 Dec-17 Mar-18

Promoters 57.42 57.42 57.42

DII+FII 20.78 21.96 22.81

Individuals

21.18 20.62 19.76

Source: ACE Equity

Share Price Trend

Prices as on 29/06/2018

TV Today Networks Ltd (TTNL) is one of the leading media companies

with flagship channel Aaj Tak in Hindi new genre. TTNL is set to

benefit from strong TV broadcasting revenue growth owing to

digitization and acquisition of digital segment from parent. Hence,

we expect revenue CAGR of ~10% over FY18-20E. Further, the sale of

loss making radio business will drive PAT CAGR of ~17% over the

same period. Currently, it is debt free with RoE and RoCE of 21.7%

and 26.9% (FY18) respectively. We recommend BUY with target price

of `517. (16x FY20E EPS).

Acquisition of digital business from parent: In Q3FY18, it had

acquired digital business from its parent at a reasonable valuation of

0.33x price/sales. Rising time spend on the internet is driving

advertisement shift towards digital. Hence, we expect the company to

post digital revenue CAGR of ~22% over FY18-20E.

Margin expansion owing to sale of radio business: Company has

recently announced its exit from radio business. Its radio segment

reported losses of ~14cr in FY18. It is selling all 3 radio stations to

Entertainment Network for which it is awaiting Ministry of Information

and Broadcasting’s approval. With this sale, we expect expansion of

company’s EBITDA margin by ~130bps to 30.1% over FY18-20E.

Outlook & Valuation: We have a positive outlook on TTNL given

expected breakeven in its print segment by FY20E and cash rich

balance sheet providing opportunities of expansion/acquisition.

Further, going forward, the election years will aid company to clock

broadcasting revenue CAGR of ~11% over FY18-20E. The stock is

currently trading at a valuation of 13.4x FY20E EPS (trading at a

discount to Zee Media, ~21x FY20E EPS).

Financial Summary

Consolidated `Cr FY16 FY17 FY18 FY19E FY20E

Revenue 582 652 721 786 871

YoY Growth (%) 22.0 12.1 10.5 9.1 10.8

EBITDA Margin (%) 27.8 24.9 28.8 29.1 30.1

PAT 92 92 133 154 183

PAT Growth (%) 13.6 -0.2 44.5 15.6 19.0

RoE 20.0 17.4 21.4 21.4 21.7

P/E x 26.7 26.8 18.5 16.0 13.4

EV/EBITDA x 14.3 13.6 10.9 9.4 7.8 Source: Company, IIFL Research

30000

35000

200

400

Jun-17 Oct-17 Feb-18 Jun-18

TV Today Network Ltd. Sensex

37 | P a g e

Premia Research

TV Today Network Ltd

Company Overview

TV Today Network (TTNL), is one of the leading Indian news television networks. Company’s segments include TV broadcasting, radio broadcasting, newspaper publishing and digital. Its flagship channel Aajtak is leader in Hindi news genre, while other channels include India Today, Tez and Dilli Aaj Tak. The company also operates three radio stations under brand ISHQ 104.8 FM in Delhi, Mumbai and Kolkata.

Its newspaper publication business publishes Mail Today newspaper in Delhi covering stories like politics, entertainment, automobiles, fashion, etc. Its digital business includes e-newspaper, websites and mobile applications.

Exhibit 1: TV Today Network (Revenue segments, FY18)

Aaj Tak amongst leaders on YouTube: Aaj Tak is clearly a leader in terms of subscribers on YouTube amongst its peer channels. As on June 29, 2018, Aaj Tak has 7.4mn subscribers while India TV and ABP News have 5.2mn and 4.9mn subscribers respectively. In terms of total views, it has 2.3bn views, which is just behind India TV’s views (2.5bn views).

Exhibit 2: YouTube stats (TV channels)

Channels Subscribers (mn) Views* (bn)

India TV 5.2 2.5

Aaj Tak 7.4 2.3

ABP News 4.9 1.9

News 18 India 1.5 0.3 Source: socialbakers.com, YouTube, IIFL Research *Total uploaded video views

38 | P a g e

Premia Research

TV Today Network Ltd

TV Broadcasting revenues to benefit from digitization

Digitization has led to reduction in the revenue leakages for broadcasters. This will be very positive for the company, as Aaj Tak is leader in both rural and urban areas. Hence, we expect TV broadcasting revenues to grow at CAGR of ~11% over FY18-20E.

Exhibit 3: TV Broadcasting revenues (`Cr)

Source: Company, IIFL Research

We expect company to attain breakeven in its Print business by FY20E. Further, with the sale of radio business, EBITDA margins are expected to expand by ~130bps over FY18-20E. This will aid the company to improve its return ratios.

Exhibit 4: Strong EBITDA margin and return ratios

Source: Company, IIFL Research

0

2

4

6

8

10

12

14

16

18

0

100

200

300

400

500

600

700

800

FY16 FY17 FY18 FY19E FY20E

TV Broadcasting revenues Growth (%) yoy

10

15

20

25

30

35

10

12

14

16

18

20

22

24

26

28

30

FY16 FY17 FY18 FY19E FY20E

ROE (%) LHS ROCE (%) LHS EBITDA margin (%) RHS

As per EY-FICCI, overall industry broadcasters’ revenue is expected to grow at a CAGR of 10.4% over CY17-20E

39 | P a g e

Premia Research

TV Today Network Ltd

Strong balance sheet with cash surplus: Company has a debt free balance sheet with disciplined working capital cycle. This will lead to continuous increase in the cash surplus for the company. We expect company to have cash surplus of ~`410cr by FY20E from ̀ 200cr in FY18 given its disciplined working capital cycle. This gives the company ability to acquire/expand for continues market share gains and growth.

Exhibit 5: Cash rich balance sheet (`Cr)

Source: Company, IIFL Research

Rationale for PE multiple: Company is currently trading at a valuation of 13.4x FY20E EPS, which is at cheaper valuation than its peer Zee Media (~21x FY20E EPS) despite better return ratios. Further, considering its debt free position of the company, strong foothold in Hindi news genre, acquisition of digital business and upcoming elections we assign it a multiple of 16x FY20E EPS.

Exhibit 6: 1 Year forward PE band (x)

Source: Ace Equity, IIFL Research

0

100

200

300

400

500

600

700

800

900

1000

FY16 FY17 FY18 FY19E FY20E

Equity Cash and Cash Equivalents Total Debt

0

5

10

15

20

25

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

Mar

-18

Jun

-18

40 | P a g e

Premia Research

TV Today Network Ltd

Exhibit 7: Peer comparison

Company P/E EV/EBITDA ROE

FY19E FY20E FY19E FY20E FY19E FY20E

Zee Media 27.3 21 11.6 9.9 6.8 7.8

TV Today 16.0 13.4 9.4 7.8 21.4 21.7 Source: Bloomberg, IIFL Research

Exhibit 8: Balance Sheet summary and key ratios

Consolidated ~ ` Cr FY16 FY17 FY18 FY19E FY20E

Cash & Cash equivalent 170 263 199 298 420

Inventories 1 2 2 2 4

Receivable 151 179 185 200 219

Other Current Assets 57 63 71 77 85

Creditors 70 91 87 95 105

Other Current Liabilities 47 49 73 80 88

Net Current Assets 263 366 297 402 535

Fixed Assets 219 204 255 259 264

Investments 7 6 5 6 6

Other Long-term assets 41 50 117 120 122

Total net assets 531 627 674 786 926

Borrowings 49 35 - - -

Other long-term liabilities

9 11 13 13 14

Shareholders' equity 472 581 662 773 912

Total liabilities 531 627 674 786 926

Key Ratios

Valuation ratios

EV/sales 4.0 3.4 3.1 2.7 2.3

EV/EBITDA 14.3 13.6 10.9 9.4 7.8

P/E 26.7 26.8 18.5 16.0 13.4

P/B 5.2 4.2 3.7 3.2 2.7

Working capital days

Inventory days 1 1 1 1 2

Debtor days 95 100 94 93 92

Creditors days 44 51 44 44 44

Source: Company, IIFL Research

Key Risks:

Too much dependency on Aaj Tak. Launch of new Hindi news channels, increasing competitive

intensity, aggressive pricing strategy by competitors.

Poaching of Anchors by other news channels

41 | P a g e

Premia Research

Disclaimer

Recommendation Parameters for Fundamental/Technical Reports: Buy – Absolute return of over +10% Accumulate – Absolute return between 0% to +10% Reduce – Absolute return between 0% to -10% Sell – Absolute return below -10% Please refer to http://www.indiainfoline.com/research/disclaimer for recommendation parameter, analyst disclaimer and other disclosures. IIFL Securities Limited (Formerly ‘India Infoline Limited’), CIN No.: U99999MH1996PLC132983, Corporate Office – IIFL Centre, Kamala City, Senapati Bapat Marg, Lower Parel, Mumbai – 400013 Tel: (91-22) 4249 9000. Fax: (91-22) 40609049, Regd. Office – IIFL House, Sun Infotech Park, Road No. 16V, Plot No. B-23, MIDC, Thane Industrial Area, Wagle Estate, Thane – 400604 Tel: (91-22) 25806650. Fax: (91-22) 25806654 E-mail: [email protected] Website: www.indiainfoline.com, Refer www.indiainfoline.com for detail of Associates. Stock Broker SEBI Regn.: INZ000164132, PMS SEBI Regn. No. INP000002213, IA SEBI Regn. No. INA000000623, SEBI RA Regn.:- INH000000248 For Research related queries, write at [email protected] For Sales and Account related information, write to customer care: [email protected] or call on 91-22 4007 1000